Abstract

The deregulatory perspective on labor market institutions argues that such institutions push up wage and employment costs while discouraging hiring and job seeking. In contrast, an institutionalist perspective argues that labor market institutions support deeper skill formation and better job searches. Building on this literature, the authors focus on temporal variation, emphasizing that some labor market institutions are likely countercyclical: they can potentially limit job losses in economic downturns. For 21 countries from 1985 to 2012, the authors examine the association of labor market institutions with overall employment outcomes as well as how these associations vary during financial crises. They find limited first-order associations of institutions with employment outcomes, procyclical associations for union density, and countercyclical associations for unemployment insurance and employment protection legislation. These findings suggest that labor market institutions could be a useful countercyclical tool in an era of recurrent financial crises.

From the 1980s to 2000s, an extensive, highly cited, cross-disciplinary literature debated the effects of labor market institutions on employment outcomes in comparative perspective. One group, composed mostly of labor economists, argued that labor market institutions were harmful “rigidities” that had distortionary effects on labor markets, which in turn pushed up unemployment levels (Elmeskov, Martin, and Scarpetta 1998; Nickell 1997; Siebert 1997). For these scholars, labor market institutions increased employers’ costs of hiring and employing workers while at the same time discouraging unemployed workers from seeking new work. Overall, labor market institutions raised wages and employment costs above market clearing levels, thereby increasing overall levels of unemployment. Later works from this perspective considered the interaction between macroeconomic change and institutions and further argued that labor market institutions may make economic shocks persist (Blanchard 2006; Blanchard and Wolfers 2000).

Another perspective, coming mostly from scholars in sociology and political science, saw labor market institutions as part of a broader set of complementary, coordinating institutions (Baker et al. 2005; Bassanini and Duval 2006, 2009; Bradley and Stephens 2007; Estevez-Abe, Iversen, and Soskice 2001; Hall and Soskice 2001; Hicks and Kenworthy 1998; Kenworthy 2002, 2004, 2008). From this perspective, labor market institutions such as encompassing trade unions, coordinated wage bargaining, unemployment insurance, and employment protection encourage deeper firm-specific skill formation and are part of corporatist bargaining structures in which labor moderated wage demands and employers made long-term employment commitments. The net effect of labor market institutions on employment performance, therefore, is argued to be neutral or favorable (Avdagic and Salardi 2013; Baccaro and Rei 2007; Bradley and Stephens 2007).

In the 1980s and 1990s, the superior employment performance of economically liberal countries with weaker labor market institutions vis-à-vis several coordinated continental European countries seemed to validate the deregulatory perspective favoring labor market deregulation. Yet the most coordinated countries—Nordic countries—achieved the highest levels of employment, challenging the deregulatory account. Furthermore, European countries experienced less favorable macroeconomic conditions during this period. German reunification, higher real interest rates, and the Nordic banking crisis each pushed up unemployment. And in the past 15 years, most countries have deregulated their labor markets to some extent, yet unemployment has persisted, only coming down after a decade-long economic expansion. These patterns question whether employment problems can be attributed to labor market institutions. Indeed, labor economists and economic policy organizations have softened their stance on labor market institutions in recent years, moderating the deregulatory perspective in some respects and conceding that some labor market institutions may support income and job security and reduce inequality (Jaumotte and Buitron 2015; OECD 2019).

The employment record of rich countries over the past 15 years suggests another complexity to this debate. Anglophone countries, especially the United States, had large cyclical employment losses in the wake of the 2008 financial crisis. In contrast, countries of continental Europe with “rigid” labor markets had smaller employment losses. For example, German employment increased during the 2008 crisis, which observers have attributed largely to coordinating institutions such as high union density and expanded unemployment insurance for short-time workers (Burda and Hunt 2011; Dustmann et al. 2014; Thelen 2014; see also Abraham and Houseman 1993). Appelbaum (2011) and Schmitt (2011) argue that labor market institutions have important countercyclical effects that lessen employment losses and stabilize demand in financial downturns. However, this countercyclical perspective has not been evaluated empirically against the deregulatory and institutionalist perspectives in the comparative employment performance literature.

In this article, we examine how labor market institutions attenuate or magnify the effects of financial crises on unemployment, revisiting the deregulatory versus institutionalist debates of the 1990s and 2000s. Although existing works have argued that labor market institutions can make shocks such as financial crises persist (Blanchard and Wolfers 2000), we point out that some of these institutions are archetypal examples of automatic stabilizers or institutional stabilizers (Keiser 1956). Such institutions were designed in part to lessen employment losses and support consumer demand in economic downturns. Consistent with earlier institutionalist research (Avdagic and Salardi 2013; Baker et al. 2005; Baccaro and Rei 2007; Bradley and Stephens 2007), we find limited first-order correlations of labor market institutions on employment performance. However, we find that unemployment insurance and employment protection legislation have robust, countercyclical associations with employment outcomes.

The findings in this article suggest a role for labor market institutions, not only for labor markets and social welfare but perhaps also for economic policy. Stock and real estate markets are greatly inflated around the world, with many exceeding the heights of the mid-2000s. A crash may be on the horizon. The main response of rich countries to past crashes has been to substantially cut interest rates, but interest rates are now around zero (Summers 2018). Central banks will not be able to address high unemployment in future economic downturns with interest rate cuts. Labor market institutions, specifically unemployment insurance and employment protection, may have an important function for the stabilization of economies, as states have few other countercyclical policy options.

Labor Market Institutions: Liberal and Coordinated, Procyclical and Countercyclical

Labor Market Institutions as Harmful Rigidities

Observing high unemployment in European countries and low unemployment in the United States and many other Anglophone countries, a number of prominent works attributed differences in employment outcomes to differences in labor market institutions (Bassanini and Duval 2006, 2009; Bean 1994; Daveri et al. 2000; Elmeskov et al. 1998; Nickell 1997). Siebert (1997) declared that labor market rigidities were “at the root of unemployment in Europe.” Broadly, labor market institutions are argued to increase the costs to employers of hiring and firing and discourage work and job seeking by the unemployed. Many contributions to this literature argued that for Western European countries to solve their unemployment problems, they had to deregulate their labor markets. In the policy domain, the influential 1994 Organisation for Economic Co-operation and Development (OECD) Jobs Study reflected and promoted this perspective.

Across these works, most attention fell on four labor market institutions: unions, payroll and social security taxes, unemployment insurance, and employment protection legislation. Unions are argued to push wages above market clearing levels and impede the flexibility to adapt to changing economic conditions, thereby discouraging hiring in anticipation of these conditions. Income, payroll, and social security taxes (such as mandatory contributions to social insurance programs) are argued to impose additional costs on employers while also decreasing the net wages of workers. This drives a wedge between what employers pay and what workers receive, which can push employment below market clearing levels. Unemployment insurance provides income support for the unemployed, discouraging job seeking. Relatedly, unemployment insurance can also increase reservation wages, thereby making unemployed workers choosier and discouraging them from accepting new employment. Employment protection mandates notification periods or severance pay for displaced workers, with varying levels for permanent and temporary workers. Employment protection is argued to lower employment levels because it impedes flexibly hiring and firing. Employers cannot lay off workers in an economic downturn, and anticipating these downturns, employers limit hiring.

Although presenting compelling arguments with some face validity, the labor market rigidities explanation for comparative employment performance was limited by at least two empirical patterns. First, it was inconsistent with the superior performance of Nordic countries. For much of the 1980s and 1990s, the Nordic countries achieved the highest levels of employment and the lowest levels of unemployment, despite extensive union coverage, generous unemployment benefits, high payroll taxes, and, apart from Denmark, regulations on dismissals. Some accounts focusing on Nordic institutions saw that high-level wage coordination could offset the effects of these other institutions (Calmfors and Driffill 1988), though other observers were skeptical that any labor market regulations could improve employment outcomes (Siebert 1997). Second, strong labor market institutions were compatible with full employment in earlier periods (Bradley and Stephens 2007). In the 1960s, many European countries’ heavily regulated labor markets had sustained unemployment levels of just 1 percent to 2 percent, while the liberal United States achieved levels of 4 percent to 5 percent only in the best of times. This questioned whether labor market rigidities were at the root of unemployment, or if other structural factors were playing a larger role.

Since the emergence of the deregulatory perspective in the 1980s and 1990s, some labor economists and economic policy organizations associated with the deregulatory perspective have softened their stance on labor market institutions. In the 2000s, some advanced a set of policies comprising a “flexicurity” model that aimed to combine labor market flexibility with income support for the unemployed, usually with many job seeking requirements and other activation conditions attached (Blanchard, Jaumotte, and Loungani 2013; Wilthagen and Tros 2004). The most common form, inspired by Denmark, combines unemployment insurance contingent on retraining and work requirements, high levels of coordination with unions, and weak employment protection. The deregulatory perspective also continued to evolve in the post-2008 financial crisis era. In a context of growing inequality, stagnant wage growth, and increasing precarity of employment, a uniform approach to labor market liberalization, single-mindedly focused on unemployment, has become increasingly unpopular. There is growing recognition of the inequality-reducing functions of labor market institutions (Jaumotte and Buitron 2015; OECD 2019), consistent with earlier works by sociologists (Brady 2009; Kenworthy 2004, 2008).

Coordinating Institutions and Varieties of Capitalism

Responding to the deregulatory perspective, institutionalists argue that labor market institutions such as unions, unemployment insurance, and employment protection legislation are part of a broader set of coordinating institutions that constitute an institutional model qualitatively different than the liberal Anglophone model. The most prominent perspective in this literature, the varieties of capitalism perspective (Hall and Soskice 2001), argues that industrial and employment relations are pursued cooperatively in several Western European countries, emphasizing relational contracting and strategic interaction. This contrasts with the more competitive relations characteristic of North America. Labor market institutions are key supports for cooperative arrangements that may help generate positive outcomes for both employers and workers. Union organization and employment protection facilitate deeper skill formation among workers, long-term capital investment by firms, improved cooperation between firms and workers, and long-term employment. Together, these institutions and their effects on industrial relations and industrial strategy can lead to employment performance that is equal or superior to the liberal, flexible, model, and the varieties of capitalism perspective emphasizes that cooperative arrangements may have benefits beyond employment.

A number of comparative works reassessing the deregulatory perspective have found that labor market institutions have little effect on employment outcomes, challenging the deregulatory account and providing support for the institutionalist counterargument (Avdagic and Salardi 2013; Baccaro and Rei 2007; Baker et al. 2005; Bradley and Stephens 2007). Early works from the deregulatory perspective looked at change over two periods, but when annual data are used, as well as advances in time-series cross-sectional methodology such as panel-corrected standard errors (Beck and Katz 1995, 2011), labor market institutions have limited effects. Individual or multilevel analyses show that liberalization of employment protection has not improved employment outcomes for youth or low-skilled workers (Gebel and Giesecke 2011, 2016), and more generous unemployment insurance leads to improved worker-employer matching, lower earnings losses, and longer duration of subsequent employment (Gangl 2004, 2006).

Do Labor Market Institutions Make Shocks Persist?

Blanchard and Wolfers (2000) address some of the limitations of the deregulatory perspective by bringing in the role of economic shocks and how these shocks interact with labor market institutions. In doing so, they give more attention to underlying changes in economic conditions. Blanchard and Wolfers focused on four shocks: interest rate changes, declining productivity growth, a novel measure of labor demand, and “common shocks” proxied by year dummy variables. They argue that labor market institutions create wage rigidities, impeding the downward adjustment of wages in economic downturns. Furthermore, generous unemployment insurance can prolong unemployment spells following economic downturns, and such long unemployment spells make workers less likely to later reenter the labor force. Their findings suggest that labor market institutions can worsen the effects of macroeconomic shocks. However, later works challenge these conclusions, instead finding that the interactions of these shocks and institutions have negligible results (Avdagic and Salardi 2013; Baccaro and Rei 2007; Nickell, Nunziata, and Ochel 2005).

Are Labor Market Institutions Countercyclical?

The recent trends in employment performance in rich countries suggest a countercyclical role for labor market institutions. In the wake of the 2001 and 2008 downturns, employment levels fell substantially in the United States (Freeman 2013). Only after a decade have U.S. employment levels recovered. Most European countries experienced a smaller contraction of employment despite a similar fall of output and financial indicators (Schmitt 2011). This pattern holds despite the additional stresses of the Eurozone debt crisis. Yet few works have considered the potentially countercyclical effects of labor market institutions. Nunziata (2003) finds that stronger employment protection and looser working time regulations reduced the elasticity of unemployment and output. Gnocchi, Lagerborg, and Pappa (2015) examine episodes of labor market liberalization and found that employment volatility increases after liberalization, further suggesting that stronger labor market institutions are countercyclical.

Unemployment insurance and taxation are classical examples of automatic stabilizers, a term that refers to policies and institutions, usually fiscal, which exert a downward pull on economic output and employment during economic expansions and an upward push in economic downturns (Keiser 1956). Automatic stabilizers are countercyclical. They are automatic in the sense that they are institutionalized in advance of when they are needed and are not a legislated response to a downturn. They can be contrasted with fiscal stimulus policies, which usually are enacted after the onset of a downturn. Automatic stabilizers can respond faster than stimulus policies because the latter have a time lag involving political debate and policy implementation, either or both of which can be quite slow.

Unemployment insurance is countercyclical by design. Employed workers or employers pay into unemployment insurance schemes, so contributions are highest in periods where employment is highest. In economic downturns, unemployment insurance funds are paid to unemployed workers. These funds stabilize displaced workers’ incomes and aggregate consumer demand, supporting basic consumption and attenuating the demand shortfall in an economic contraction. Labor market taxation can play a similar countercyclical role. Assuming progressive taxation, when incomes increase in an economic expansion, tax revenue increases disproportionately. In an economic contraction, both the effective rate and revenue fall.

Employment protection legislation (EPL) is likewise designed to be countercyclical (Bentolila and Bertola 1990; Nunziata 2003). EPL requires that dismissals have notification periods and often compensation, which together can make dismissals long and costly. Thus EPL discourages employers from firing or laying off workers in an economic downturn, running against the normal tendency of economic downturns to result in shedding of jobs. However, employers may anticipate these downturns and the essentially fixed costs of employing additional workers, so they may be hesitant to hire even in a period of economic growth and favorable business expectations.

Unions, coordinating institutions, and employment protection legislation are not fiscal policy institutions but potentially have countercyclical functions similar to automatic stabilizers. Although the deregulatory perspective argues that unions impede labor market flexibility, the varieties of capitalism literature argues that unions and broader coordinating structures promote internal flexibility, whereby employment reductions can be achieved through production reorganization, work time reductions, and furloughs rather than layoffs (Thelen 2001). Dustmann et al. (2014) argue that the superior employment performance of Germany in the wake of the 2008 crisis can be attributed to employer-union coordination. Consistent with these works is Gnocchi et al. (2015)’s finding that, after episodes of wage bargaining liberalization, employment volatility increases.

In summary, labor market institutions may discourage job loss and support consumer demand in economic downturns. Our analysis reassesses the labor market institutions literature by asking, like existing works, whether labor market institutions are positively or negatively associated with employment performance. But we build on these works, which focus on first-order correlations, by asking whether labor market institutions are procyclically or countercyclically associated with employment performance in the wake of financial crises.

Labor Market Institutions in Financial Crises: Procyclical or Countercyclical?

Our analysis focuses on financial crises, which we operationalize as stock selloffs of 25 percent or more in a given year. With the increased prominence of financial markets and financial motives in the post–Golden Age period (Epstein 2005; Hyde, Vachon, and Wallace 2018; Krippner 2005, 2011), financial boom-bust cycles are a key determinant of broader macroeconomic conditions and expectations. Financial booms and busts now mark the business cycle. The United States experienced three such stock selloffs in the period under examination, and other rich countries have been similarly affected, albeit with somewhat different timing.

We expect that financial crises affect employment similarly to the economic shocks examined by Blanchard and Wolfers (2000), except at a much larger magnitude. Asset price crashes affect employment outcomes severely. They involve reversals of investor and lender confidence and attendant credit crunches. In turn these lead to a chain of pathological outcomes: weak investment, contraction of business demand, job loss, and contraction of consumer demand.

The “common shocks” proxied by year dummy variables by Blanchard and Wolfers (2000) are perhaps intended to reflect financial crises to some extent. However, financial crises are geographically and temporally uneven. The 1990s Nordic and East Asian banking crises had little effect on North America, which experienced a sustained economic boom through the 1990s. As the U.S. asset bubble linked to this boom deflated, Australia and New Zealand were well into the rise of a commodity boom linked to rapid growth in East Asia, which largely spared the broader Asia-Pacific region from the upheavals of the early 2000s. The 2008 global financial crisis is the single instance of a financial crisis being a common shock. Thus, a focus on common economic shocks misses the heterogeneous patterning of financial crises.

Data and Model

Our analysis examines the unemployment rate, which is the number of unemployed workers divided by the labor force size. Importantly, unemployed workers are counted only if they are immediately available for work and have recently searched for a job. A well-known limitation of the unemployment rate is that it omits discouraged workers. In periods of high labor market slack and low labor demand, unemployed workers may suspend active job searches, and surveys exclude these workers from the official count of the unemployed. This lowers the headline unemployment rate and makes the employment situation appear more favorable. Given this limitation, we supplement the analysis and demonstrate the robustness of our findings by examining another measure of employment performance, the employment-to-population ratio. This quantity refers to the proportion of a country’s population aged 15 to 64 years that is currently employed. A limitation of this measure is that over time it has been largely influenced by the entry of women into the labor force, and because of this, it shows an upward trend in many countries despite growing levels of labor market slack.

We measure financial boom-bust cycles using Reinhart and Rogoff’s (2011) indicator of a stock market crisis (see also Hyde et al. 2018). This variable is coded 1 in years when a country’s total stock market capitalization drops by 25 percent or more, indicating a major selloff, and coded 0 otherwise. 1 We considered two alternative financial crisis measures, also from Reinhart and Rogoff. One measure is whether a major financial institution has failed. We investigated this measure and found that it is highly correlated with country size, as larger countries have more major financial institutions. Unfortunately, there is no straightforward way to normalize this dummy variable measure by the size of a country’s economy or population. Second, we examined Reinhart and Rogoff’s external debt crisis variable but found too few instances to investigate in a regression framework. In most cases, an external debt crisis was followed by a stock market selloff, so our analysis accounts for but does not distinguish between these two crises.

We use a set of labor market institution measures common to the comparative employment literature. To measure distortions associated with collective bargaining, we use union density data from the OECD (2018) and Visser’s (2016) measure of wage coordination. The “tax wedge” is measured as the sum of income, payroll, and social security taxes, expressed as a share of gross domestic product. These data are from the OECD’s (2017) revenue statistics. We use Bradley and Stephens’ (2007) measure of the strictness of employment protection legislation, which is the unweighted average of the OECD’s six-point employment protection measures for permanent and temporary workers. These data are from Brady, Huber, and Stephens’s (2014) Comparative Welfare States Data Set. Finally, we measure the generosity of unemployment benefits using Scruggs, Jahn, and Kuitto’s (2014) unemployment insurance replacement rates. We use the average of single and family rates. Scruggs et al.’s measures are net of taxation of benefits, which reflects that increasing taxation of benefits has reduced the net amount available to displaced workers.

In addition to the stock market crisis variable, we include several economic variables capturing broader economic conditions. First, we include trade openness to control for the increasing exposure of states to the global market. This measure is the sum of imports and exports expressed as a share of gross domestic product, and the data are from Brady et al. (2014). Second, we include Blanchard and Wolfers’s (2000) measure of real interest rate levels. This measure is the nominal long-term interest rate, representing the cost of borrowing for businesses, from which we subtract the five-year moving average of the inflation rate. Third, we include a control for labor productivity growth, controlling for that portion of economic growth not driven by changes in employment, our outcome of interest. These data are from Feenstra, Inklaar, and Timmer (2015). Finally, we include a dummy variable for Germany after 1991 to capture the unique effect of reunification.

Our data form a time-series cross-section data set of 21 rich countries (Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Japan, the Netherlands, Norway, New Zealand, Portugal, Spain, Sweden, Switzerland, the United Kingdom, and the United States) over the period from 1985 to 2012. Our analysis starts in 1985 because the employment protection data begin there, and it ends in 2012 because coverage for several institutional variables ends there. Missing data make the data set unbalanced. The unit of analysis is the country-year. The Appendix contains descriptive statistics and a correlation matrix for all variables.

We use a dynamic model specification common to the comparative literature on labor market institutions (Avdagic and Salardi 2013). The equation for our model is

where yi, t is the unemployment rate or employment-to-population ratio, yi,t−1 is the lagged dependent variable, xi,t−1 is the lagged independent variable, and ai is a fixed-effect dummy variable for each country.

Our analysis addresses issues common to time-series cross-section regression models. Partial adjustment models lag independent variables one year. We use panel-corrected standard errors to address unit correlation of errors and unequal variances across countries. We include country fixed effects to specify a different intercept for each country and, in doing so, control for unmeasured time-invariant, country-specific factors influencing employment performance (Halaby 2004). The simultaneous use of fixed effects and a lagged dependent variable raises the potential of “Nickell bias” (Nickell 1981), but this issue is mitigated when T is large (Beck and Katz 2011), as in our analysis. Finally, an important caveat to note is that our analysis is based on observational data and is subject to the limitations of observational data. Our analysis should not be taken as formally causal.

We performed many robustness checks. We repeat our analysis using the employment-to-population ratio as the dependent variable, which we present in the main results. We also replaced the union density variable with collective bargaining coverage, because some countries have high coverage but lower union density, most notably France. A limitation of the collective bargaining coverage variable is that some countries had gaps in the data or data at only five-year intervals, so we performed a linear interpolation. Because collective bargaining decline is usually a slow institutional change, the interpolation should be valid. With this alternative measure, we do not find statistically or substantively significant associations for the first-order terms or interactions. We also examined models that omit unit fixed effects. The variation for some labor market institutions is larger across than within countries, motivating some existing works to omit unit fixed effects (Bradley and Stephens 2007; Kenworthy 2002). Omitting unit fixed effects, we might observe larger effect sizes for these variables. We report these results in the appendix and briefly discuss them in the next section. Finally, we reestimated our models in first differences, finding similar results. However, a key limitation of differenced models is that they discard any information about variables’ levels (Beck and Katz 2011), instead focusing on year-to-year change. As a result, these models investigate somewhat different relationships than those discussed in this article. Therefore we omit these results, but they are available upon request.

Results

Table 1 shows the results of our analysis. Models 1 and 2 are baseline models that only include first-order terms. Models 3 through 10 separately interact the institutional variables with the financial crisis variable. Given the relatively small n of our time-series cross-section data set, multicollinearity is a problem with multiple interaction terms that have common parts, so we limit our analysis to single interaction terms. In Table 2, we combine the first-order term and interaction term and consider their statistical significance.

Regression of Employment Outcomes on Selected Independent Variables and Country Fixed Effects, 1985 to 2012.

Note: Values in parentheses are standard errors. Emp. = employment; EPL = employment protection legislation; UI = unemployment insurance; unemp. = unemployment.

p < .05. **p < .01. ***p < 0.001.

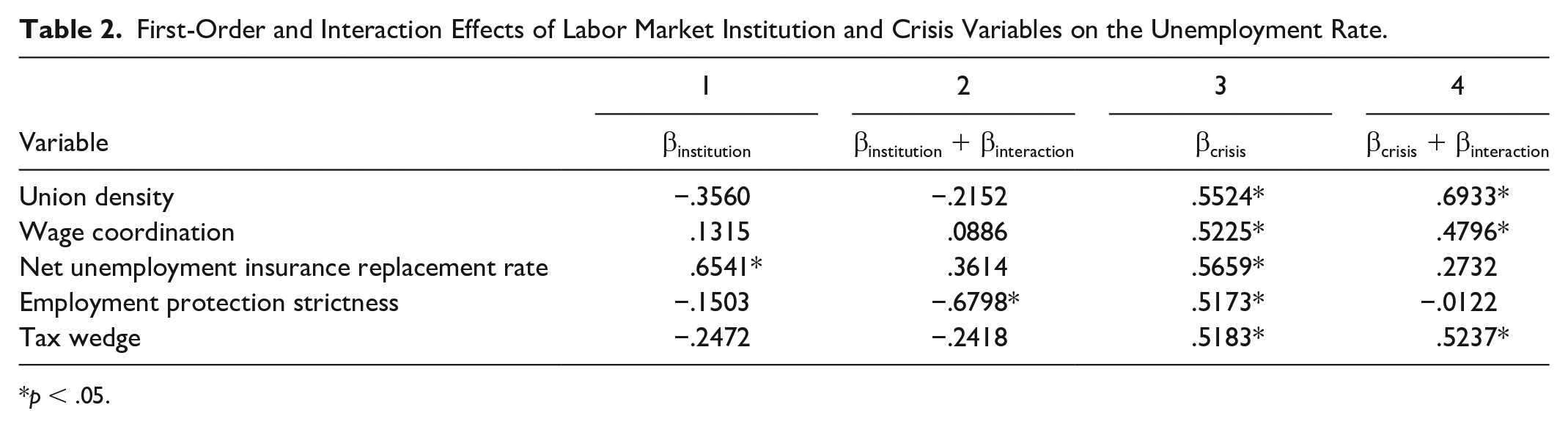

First-Order and Interaction Effects of Labor Market Institution and Crisis Variables on the Unemployment Rate.

p < .05.

Models 1 and 2 are our baseline models looking at only first-order terms for the two dependent variables. Focusing on the institutional variables, we see limited evidence in support of the deregulatory argument that labor market institutions are to blame for poor employment performance. Only the coefficient for unemployment insurance replacement rates in the unemployment rate models reaches statistical significance. None of the other first-order institutional variables has a statistically significant association with employment outcomes. These results are consistent with a number of institutionalist works that have shown that labor market institutions have limited first-order correlations with employment (Avdagic and Salardi 2013; Baccaro and Rei 2007; Bradley and Stephens 2007). The results in the analysis at hand support the institutionalist argument that labor market institutions together may constitute a different capitalist institutionalist model than the liberal American variant but are not associated with worsened employment outcomes. At the same time, these results do not suggest that more regulated labor markets are associated with improved employment performance. The baseline models suggest that macroeconomic conditions, specifically labor productivity growth and financial crises, are stronger correlates of employment performance over this period than labor market institutions.

The direction, magnitude, and significance of the interaction terms in later models are of primary importance and necessitate some comments on interpretation. To facilitate comparison, the macroeconomic and institutional variables are standardized, so the coefficients show how a 1 standard deviation increase of the institutional variable is associated with the dependent variable. The crisis dummy variables are coded 0 or 1 and not standardized. The coefficients for the first-order institutional variables can be interpreted as the association of that institution with employment outcomes in the absence of a financial crisis (where the financial crisis dummy variable equals zero). The sum of the first-order and interaction coefficients describes the association of the labor market institution with employment outcomes in a crisis. The coefficient for the interaction term is the difference of the association of the institutional variable and the outcome between crisis and noncrisis years. We note that the standardized version of the institutional variable is used for constructing the interaction term. 2 We first consider individual coefficients, and later in Table 2, we look at the marginal associations.

Models 3 and 4 interact the financial crisis indicator variable with union density, assessing the how the association of union density with employment outcomes varies cyclically. We see that the interaction term is negatively associated with the employment-to-population ratio and positively associated with unemployment, though the coefficient for unemployment is not statistically significant. These results are consistent with the argument of Blanchard and Wolfers (2000), perhaps suggesting that high levels of union density can increase job losses in downturns. As with the other statistical findings, we examined the robustness of this result. Interestingly, we find that it is driven by Denmark and Sweden. When either of these countries is omitted from the analysis, the interaction term is roughly halved and does not approach any standard level of statistical significance. Substantively, both Denmark and Sweden are Ghent-system countries with exceptionally high levels of union density. Denmark in particular is the archetype of the “flexicurity” model, which aims to combines institutional interventions in the labor market with high levels of flexibility. Although we are hesitant to draw definitive conclusions from results that are not robust to alternative specifications, these findings may suggest that exceptionally high levels of union density are perhaps not a source of labor market rigidity and may actually facilitate employment adjustments in downturns.

Models 5 and 6 examine the financial crisis-wage coordination interaction term, which does not show a statistically significant association with either outcome. Wage coordination is a key dimension of the broader systems of coordination underlying the liberal versus coordinated market economy distinction, which is hypothesized to influence employment outcomes in expansions and downturns. Yet the nonsignificant association of the first-order term and interaction with employment outcomes do not provide evidence that wage coordination shapes employment in either macroeconomic context. Nonetheless, methodological limitations of wage coordination measures deserve comment, as the validity and reliability of wage coordination scales have been debated (Kenworthy 2001). Wage coordination is a difficult concept to operationalize and measure, and it may not map well onto an ordinal scale. Moreover, much of the variation in the wage coordination scale is across countries rather than over time (Kenworthy 2002). The country fixed effects may absorb some of this variation, though we found similar results in models without country dummies, which we describe later in this section.

The next two sets of models provide evidence of a countercyclical relationship of labor market institutions, specifically unemployment insurance and employment protection legislation, with employment outcomes. Models 7 and 8 test the interaction term for the financial crisis indicator and the net unemployment insurance replacement rate. The coefficient for the first-order term for unemployment insurance replacement rates becomes statistically significant for both outcomes, whereas in earlier models, the first-order term is significant only for the unemployment rate. The interaction term is statistically significant, and for both dependent variables, greater unemployment insurance generosity in financial crises is associated with improved employment outcomes. In models 9 and 10, the financial crisis indicator is interacted with the employment protection measure, which is the average of the OECD’s permanent and temporary employment protection legislation scales. As expected, the interaction term is statistically significant in a countercyclical direction, showing that in financial crises, greater employment protection is negatively associated with unemployment rates and positively associated with the employment-to-population ratio. Interestingly, the first-order term remains nonsignificant, suggesting limited employment costs to employment protection legislation, even in economic expansions. Bentolila and Bertola (1990) argued that employment protection limits dismissals more than hiring, and these results are consistent with their argument.

Models 11 and 12 interact the tax wedge with the financial crisis variable. Taxation is the most common example of an automatic stabilizer because revenues increase during economic expansions and decrease during economic contractions. Assuming progressive taxation, effective tax rates increase as incomes increase (Keiser 1956). Yet the regression results do not show a significant cyclical association of the tax wedge with employment outcomes. One possible explanation is that despite the common assumption of progressive taxation, taxation is generally regressive in rich countries (Prasad and Deng 2009). Payroll and social security taxes are often flat up to a cap, after which further income is exempt, making them overall somewhat regressive. The progressivity of labor income taxation has decreased in rich countries, too. Effective tax rates do not increase much or may decline with growing incomes, meaning that taxation could have less of a countercyclical effect on employment.

Before moving onto interpreting the marginal associations of the interaction terms, one of our robustness checks deserves comment. We replicated the models in Table 1 while omitting country fixed effects. We report these results in Appendix Tables A3 and A4. In these models, we find results that are generally similar to those that include country intercepts. The main difference is that we find a negative coefficient for the first order tax wedge term in models of the unemployment rate but not the employment ratio. We also find somewhat more robust evidence of a procyclical association of union density with employment outcomes, though again this is sensitive to the inclusion of Denmark and Sweden. The estimates are otherwise similar to the models that include country fixed effects.

In Table 2, we show the marginal associations taking the first-order and interaction coefficients together. In this table, we consider the combined magnitude of the first order and interaction coefficients. This is similar to a marginal effects plot for two continuous variables (Brambor et al. 2006). For the sake of brevity, and because the stock market crisis variable is binary, we report results in tables instead of marginal effects plots. Standard errors and confidence intervals, as well as the variances and covariances that we calculate them from, are in the Appendix.

Interaction terms are symmetric (Berry, Golder, and Milton 2012; Franzese and Kam 2007), and the interpretation of what is moderating what is guided by theory. Here, both interpretations of the interaction terms are theoretically useful. We have argued that some labor market institutions have different effects in economic expansions and contractions, and conversely, labor market institutions offset the tendency of financial crises to generate job losses.

In Table 2, column 1 shows the first-order association of the institutional variables with the unemployment rate. These quantities are simply the first-order coefficients for each variable in Table 1. Column 2 sums the first-order coefficients and the interaction terms. For the both first-order term and the two terms added together, union density, wage coordination, and the tax wedge are do not have statistically significant associations with the unemployment rate, consistent with earlier results. The unemployment insurance replacement rate has a statistically significant first-order coefficient, showing that a 1 standard deviation increase in the replacement rate is associated with a .65 increase of the employment rate, a modest effect size. In financial crises, the interaction term attenuates this relationship, nearly halving it, so the net association in a financial crisis is not statistically different from zero. Although the results should not be taken as causal, they suggest that if unemployment insurance is associated with lower levels of unemployment, this relationship is mitigated during financial crises.

A different pattern emerges for employment protection. The first-order coefficient shown in column 1 is not statistically significant, but the sum of the first-order coefficient and the interaction term (column 2) is statistically significant. A 1 standard deviation increase of the strictness of employment protection is associated with a .68 increase of the unemployment rate, but only during a financial crisis. Outside of these periods, employment protection is not meaningfully correlated with unemployment.

The interaction terms are symmetrical, so it is worth considering the opposite interpretation: that the association of financial crises with unemployment is attenuated by labor market institutions. In Table 2, columns 3 and 4 present first-order and combined coefficients for financial crises. Column 3 is the association of a financial crisis with unemployment at the average level of that institutional variable, while column 4 is the association of a financial crisis with unemployment where the institutional variable is one standard deviation greater. For the union density, wage coordination, and tax wedge variables, the positive association of financial crises with unemployment persists, which is consistent with the interpretation of the regression results in Table 1. When the first-order and interaction terms are combined, the resultant coefficients for union density, wage coordination, and the tax wedge are similar, suggesting no cyclical relationship. For unemployment insurance and employment protection, we see that the combined coefficient in column 4 is considerably smaller than the first order coefficient in column 3, showing that these institutions attenuate the positive association between financial crises and unemployment.

In sum, the results provide mixed support for the various first-order and cyclical arguments outlined in the first half of the paper. Across all models and dependent variables, the common measures of labor market institutions have limited first-order associations with employment outcomes. Union density is procyclically associated with the employment ratio but not the unemployment rate, while the unemployment insurance replacement rate and strictness of employment protection legislation are countercyclically associated with the unemployment rate and employment to population ratio.

Discussion

In this article we have revisited a prominent debate on labor market institutions and comparative employment performance. Scholarship working from the deregulatory perspective in the 1990s and 2000s argued that labor market institutions discourage hiring and job seeking while also pushing wages above market clearing levels (examples include Elmeskov et al. 1998; Nickell 1997; Siebert 1997). Another perspective argues that labor market institutions are part of a broader set of cooperative, coordinating institutions that constitute a qualitatively different capitalist institutional model than the liberal, Anglophone model (Baker et al, 2005; Bassanini and Duval 2006, 2009; Bradley and Stephens 2007; Estevez-Abe et al. 2001; Hall and Soskice 2001; Hicks and Kenworthy 1998; Kenworthy 2002, 2004, 2008). From this perspective, labor market institutions may be associated with overall similar or improved employment outcomes. In our analysis of 21 countries from 1985 to 2012, we do not find much support for the argument that labor market institutions are at the root of unemployment. We find limited first-order correlations of most institutional indicators with overall employment performance.

Another aspect of employment performance that has received less attention is the procyclical or countercyclical effects of labor market institutions. Blanchard and Wolfers (2000) argued that these institutions can make economic shocks persist, prolonging their effects on unemployment. Varied works on automatic stabilizers and institutional perspectives on labor markets suggest that labor market institutions may have countercyclical effects. Case studies of the 2008 crisis offer some empirical support for this perspective (Appelbaum 2011; Freeman 2013; Schmitt 2011). Extending these works to the quantitative, comparative literature on employment outcomes, our analysis demonstrates that some labor market institutions are procyclically or countercyclically associated with employment outcomes. Union density shows procyclical associations (though this result is sensitive to what outcome is examined and what countries are included), while unemployment insurance and employment protection legislation strictness are countercyclically associated with both employment outcomes.

The countercyclical association of unemployment insurance and employment protection with employment outcomes suggests that these institutions could be increasingly important for macroeconomic policy in a context where interest rates at or below zero. Over the past few decades, rich countries have been jolted by economic turbulence from financial crises. Central banks have responded to these deep downturns by successively cutting interest rates and maintaining these low rates for extended periods. These cuts are aimed at spurring investment and economic growth and helping employment recover. But at present, interest rates are near or below zero, as they have been for nearly a decade. At the same time, asset prices are surging. Stock indexes have surpassed records, and real estate markets are likely overvalued (UBS 2018). These markets may be due for a major correction soon, which would put the economies of rich countries into a potentially deep recession. Central banks have responded to such recessions in the recent past by cutting interest rates, but now that rates are around zero, interest rates cannot be effectively cut any further. The main countercyclical response to financial crises that countries have used in recent decades is now unviable.

Unemployment insurance and employment protection could be tools to address this problem. Unemployment insurance is an automatic stabilizer that supports demand immediately in response to an economic downturn, and it does not have the lag from policy debate and implementation that other fiscal policies such as government stimulus programs have. Generous unemployment insurance can potentially stabilize consumer demand and encourage effective job searches, while employment protection decreases the cyclical aspect of employment, discouraging the shedding of workers in economic downturns and increasing commitments among employers.

It is important to note a caveat that comes with these policy suggestions. Our analysis is based on observational data, not a controlled experiment, which is not feasible at a country level. Our analysis could be affected by issues common to analyses of observational data, including unobserved confounders and multicollinearity. In this article, we aim to make a first pass at this research question, and perhaps more rigorous causal methods could be used in future research where exogenous variation can clearly be identified. Beyond quantitative methods, country case studies and comparative-historical research may also help establish causal relationships and provide richer evidence of how these relationships play out in individual countries.

This article suggests areas for future research. One issue to consider is whether there are trade-offs to dampening cyclical employment variation with stronger labor market institutions. Employers may offset the “quasi-fixed” character of employment in other ways. One way is work time reduction. If employers cannot lay off workers, they may reduce their hours. Case studies of Germany show that working hours were reduced in the Great Recession. achieved by flexible working time accounts, union cooperation, and extending unemployment insurance payments to workers working short-time (Burda and Hunt 2011;Dustmann et al 2014; Thelen 2014). However, the observed reduction of working hours in Germany was still much lower than the United States, suggesting that employment rigidity was not wholly offset by working time reduction.

Another potential trade-off relates to wages. We do not see much evidence of widespread, downward wage movements in the wake of the Great Recession, but the costs of adjustment may have been pushed onto workers in subsequent wage negotiations. The weak wage growth across advanced economies may be evidence of this, though wage growth trends do not appear to be correlated with the extent of labor market regulation. A final way that adjustment may have been absorbed is by employers. Interestingly, in countries with the most regulated labor markets, the profit share of national income decreased during the Great Recession. This suggests that employers absorbed adjustment costs to a greater extent in countries with more rigid labor markets. However, employers may build these anticipated hits to profits into their wage and hiring plans in the wake of financial crises, which makes the net distributional result ambiguous.

Although our analysis has focused on employment outcomes, the broader effects of institutions on other social outcomes should also be kept in mind. Protective labor market institutions support lower levels of income inequality and poverty (Brady 2009; Jaumotte and Buitron 2015; Kenworthy 2004, 2008). Labor market institutions can improve job quality, especially in low-skill jobs, and the deregulation of labor markets has been implicated in the growth of low-paying, low-productivity, insecure jobs (Wulfgramm and Fervers 2015). The varieties of capitalism perspective emphasizes that labor market protections encourage workers to invest more deeply in firm-specific technical skills, potentially raising overall levels of human capital (Hall and Soskice 2001). Looking beyond labor markets, employment and income security is associated with improved health and wellbeing (Sjöberg 2010). And considering broader macroeconomic outcomes, the hypothesized wage rigidities of labor market institutions may be stemming deflation. In the absence of these institutions, prices may fall, making consumers put off purchases and spurring further economic contraction.

Footnotes

Appendix

Regression of Employment Outcomes on Selected Independent Variables and Country Fixed Effects, 1985 to 2012.

| 1 |

2 |

|

|---|---|---|

| Variables | Unemployment | Employment Ratio |

| Lagged dependent variable | .898*** (.0608) | .905*** (.0312) |

| Labor productivity growth | −.263** (.0806) | .223** (.0779) |

| Real interest rates | .410** (.150) | −.240 (.139) |

| Trade openness | −.211 (.302) | .541 (.303) |

| Tax wedge | −.169 (.266) | .00738 (.286) |

| Union density | −.586 (.420) | .426 (.376) |

| Unemployment insurance replacement rate | .376 (.312) | −.355 (.268) |

| Wage coordination | .272 (.190) | −.250 (.180) |

| Employment protection legislation strictness | −.198 (.259) | .126 (.239) |

| Collective bargaining coverage | .265 (.227) | −.195 (.177) |

| Stock market crisis | .515** (.172) | −.622*** (.167) |

| Financial Crisis × Collective Bargaining Coverage | −.129 (.0750) | .108 (.0620) |

| Constant | .00648 (.731) | 7.374*** (2.185) |

| Countries | 21 | 21 |

| Observations | 494 | 480 |

| R 2 | .885 | .980 |

Note: Values in parentheses are standard errors.

p < .01. ***p < 0.001.

Acknowledgements

For helpful comments on this article, we thank Ho-fung Hung, Lindsay Monte, and Roshan Pandian. An earlier version of this paper was presented at the 2018 Annual Meeting of the American Sociological Association.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by National Science Foundation Doctoral Dissertation Research Improvement Grant 1637129.

1

These data end in 2010. We extended them to 2011 with market capitalization data from the U.S. Federal Reserve, noting that none of the countries under examination experienced a large stock selloff in 2011.

2

We distinguish this from standardizing or centering the variables constituting the interaction term but leaving the first order term unstandardized or uncentered. This common approach is purported to reduce multicollinearity, which has been shown to be false by Brambor, Clark, and Golder (2006) and ![]() .

.