Abstract

Information disclosure policies influence nearly every consumer domain. Disclosure research across various sectors, particularly finance and nutrition, demonstrates how policymakers can enhance consumer decision-making and promote a fair marketplace. In particular, five key considerations make policies more effective: understanding existing consumer preferences, capturing and maintaining consumer attention, providing actionable knowledge, anticipating firm responses, and recognizing potential perverse effects of information provision. An overarching “theory of change” organizes these considerations and other steps to reveal how disclosure policy can promote consumer well-being. Implementing disclosure policies using these psychological and behavioral insights will maximize their effectiveness.

Social Media

Effectively providing information empowers consumers to make better decisions. For maximum impact, information policies should consider consumer attentional capacity, consumers’ high-level goals, consumers’ beliefs prior to seeing information, and robustness to changing contexts.

Key Points

Providing information is a popular tool for consumer protection; five considerations help implement it well.

Given consumers’ limited attention, lengthy disclosures hinder information-gathering and subsequent behavior change.

Effectively formatting information makes high-level goals salient and then allows consumers to drill down into the details and optimize goal achievement.

Sometimes, providing information can reduce consumer well-being; capturing consumers’ beliefs prior to seeing information will help identify these domains.

Policies that mandate information occur in a dynamic environment, where firms and organizations will respond to new requirements by changing their product assortments and advertising. Robust policies account for these likely responses from firms.

Information provision is a popular policy tool intended to facilitate consumer choice in practically every imaginable domain, including health care, finance, nutrition, and education. Mandatory disclosure policies ideally clarify choices that consumers make and alert them to otherwise hidden information, while also providing some assurance of an even competitive playing field. By providing communication standards, information provision policies partly determine how firms position themselves against competitors and market themselves to their target audiences. In a marketplace where many products are more accessible than ever before, information provision policies have an outsized influence in determining whether and how consumers and firms connect.

Most instances of information provision are relatively low-cost interventions, at least compared to alternative solutions commonly proposed by policymakers, such as increasing the number of choices available or incentivizing certain preferred options. Policies intended to encourage home ownership offer one example. Although policymakers could facilitate home ownership by increasing the stock of single-family units available in a given area or by providing tax benefits for first-time home buyers, both of those interventions require substantial financial resources. By contrast, providing information about existing tax benefits available to homeowners, available financing options, or a side-by-side comparison of the costs of renting versus owning a home may all seem considerably more tractable in the face of limited budgets. However, these information interventions may fall on deaf ears if not properly calibrated to their intended audiences and the problems at hand.

Information provision is worthwhile; disclosure is an essential tool in the policymaker's toolkit. Though many of the considerations highlighted below suggest flaws or concerns with information provision, these considerations aim to take information provision seriously and implement it well, not to argue against information provision as a policy intervention.

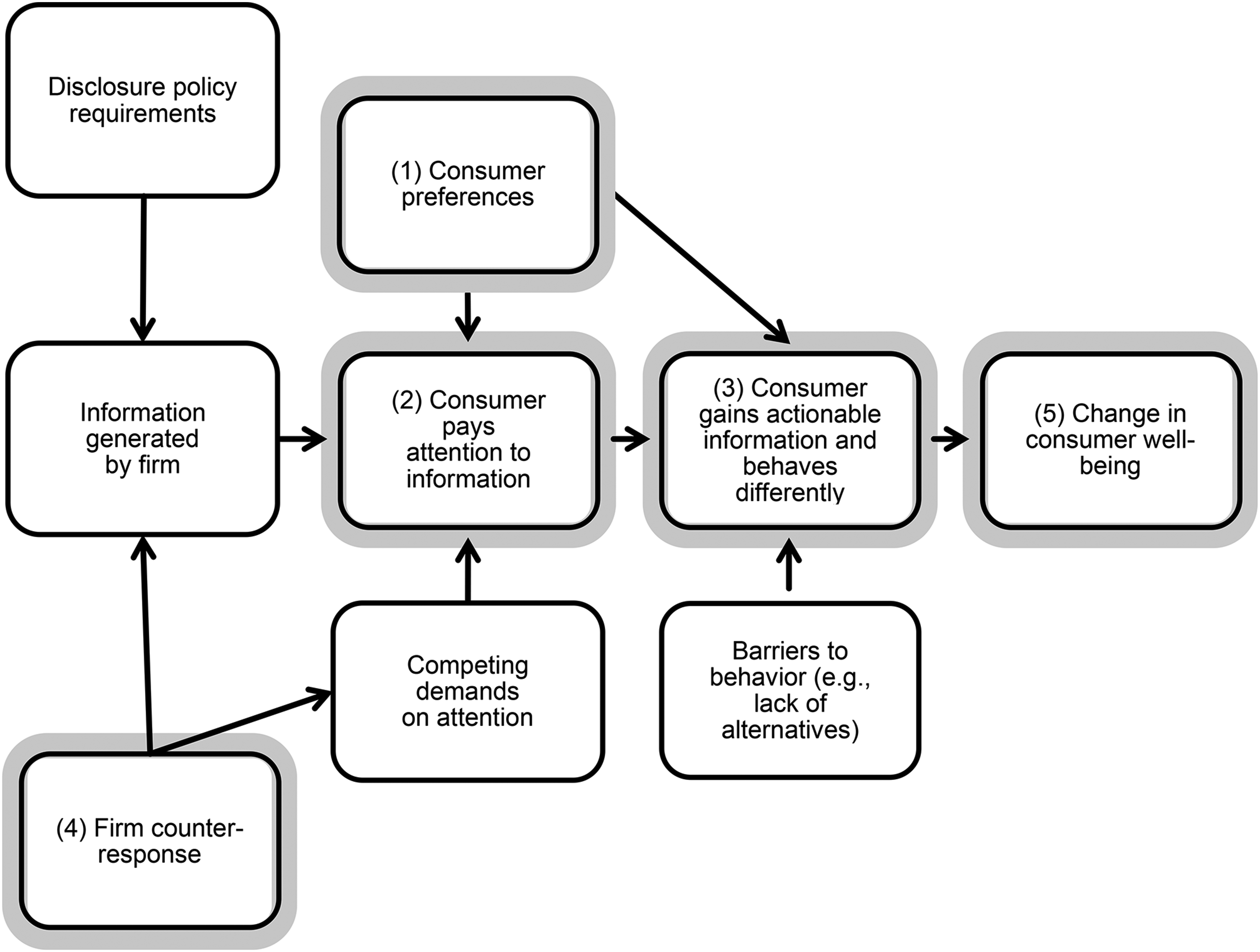

A “theory of change” conceptual framework (see Figure 1) organizes the discussion, aiming to help readers think about the criteria necessary for a given disclosure policy to succeed. That is, a policymaker who is interested in improving consumer welfare (at the far right of the diagram) and is considering using disclosure policy to do so (at the upper left) may find it useful to consider the sequence of intervening steps necessary for the disclosure policy to work. The top left shows policymaker behavior; the bottom left shows firm counter-responses to disclosure policies; and the remaining boxes show the interactions among consumers, the information they receive, and the situation.

Theory of change for information provision policies.

Theory of Change

Information disclosure requirements are typically imposed on firms, including financial service providers and food manufacturers. Consumers then receive firm-generated information in a variety of ways, including receiving a mailing from an existing investment (as in the case of mutual fund shareholder reports) or seeing food package labeling in a grocery store aisle (as in the case of nutrition facts).

To be directly effective, consumers must pay attention to the information. This could occur because they are actively seeking out information, are attracted to information by some attention-grabbing display, or by coincidence – perhaps because a family member mentions the retirement program at their new job, or because calorie labels are now posted in their favorite restaurant. After attending to the disclosure, consumers may gain actionable information and change their behavior. Ideally, this change is in a beneficial direction, and a resulting increase in consumer well-being occurs.

Notably, moderating effects occur for multiple reasons. In this review, these include competing demands on attention, which limit the chances that a consumer will pay attention to a disclosure, as well as preferences and constraints on behavior that affect the likelihood of a change in consumer well-being.

The following sections highlight five essential and often overlooked considerations of effective information provision policies (numbered 1 through 5 in Figure 1). To clarify how these considerations affect consumer decision-making, we apply them to both financial and food-related decisions, reviewing relevant work in behavioral science as support

Consideration 1

Some issues are about consumers’ preferences, not about a lack of information.

An initial question for information policies is whether consumer well-being is hindered by a lack of information. In addition to limitations that lie beyond a person's control (e.g., financial constraints that limit one's ability to invest; food allergies that dictate meal choices), information may fail to change behavior when the ultimate determinant of behavior is an existing preference. In this theory of change, preferences can affect both information acquisition and behavior in response to acquired information.

Starting with effects on information acquisition, in some instances, consumers might have a preference about the information to which they are exposed. Recent work has demonstrated instances of “deliberate ignorance” (Hertwig & Engel, 2016; see also Golman et al., 2017; Golman et al., 2022; Loewenstein et al., 2014) whereby people choose to avoid potentially useful information as a means of accomplishing a wide variety of goals, such as regulating their emotions (e.g., avoiding feelings of regret), preserving fairness in decision-making (e.g., preempting bias by using gender-blind auditions for symphony orchestras [Goldin & Rouse, 2000]), and gaining strategic advantages (e.g., avoiding social or legal liability). If preferences lead consumers to avoid information altogether, policies providing information are unlikely to yield downstream benefits.

Effects of preferences on attention appear in our two example domains of nutrition and finance. For example, one paper showed that restaurant menus that group low-calorie items together may undo some of the calorie reductions achieved by posting calorie labels on menus in the first place (Parker & Lehmann, 2014). If consumers rule out low-calorie options early in the consideration process (a decision made easier by grouping low-calorie items together), then they may make their final decision with little consideration for calorie information. In another paper, 58% of consumers who had the opportunity to learn calorie information as they selected a meal actively avoided calorie information (Thunström et al., 2016; for similar results, see Woolley & Risen, 2018). In financial contexts, past research has shown an “ostrich effect” where investors monitor their accounts less frequently when the overall stock market is down (Karlsson et al., 2009), presumably to avoid learning that they have lost money. Consumers also avoid learning about financial benefits of decisions that involve the suffering of others (e.g., that a destructive hurricane might hit another country and generate returns for those holding a “catastrophe bond” [Woolley & Risen, 2018]). These decisions to avoid information tend to increase when “cover” is available–that is, when an alternative attribute provides a reasonable justification for a decision maker to avoid information (Woolley & Risen, 2021).

Preferences may also directly affect behavior, thereby limiting the effect of an information policy. For instance, most people know that French fries are unhealthier than side salads, so labeling these items does not provide new information about relative nutrition. People who prefer French fries may simply have a strong preference that will be unaffected by information provision. Similarly, the investment domain demonstrates that preferences can make information less effective. In particular, 48% of American families have no stock holdings (including indirect holdings like investment funds [Federal Reserve Board, 2023]). In surveys of non-investors, 37% say that a dislike for “think[ing] about my finances” is very or extremely important in driving their noninvestment decisions (Choi & Robertson, 2020). Furthermore, 19% of these non-investors have more than $100,000 available to invest, suggesting that a lack of wealth is unlikely to be the main barrier to investing. To encourage investing, it may be more effective to rely on direct methods of behavior change, such as automatic enrollment into a retirement plan, rather than information that educates about the financial benefits of investing (for a review of automatic enrollment into savings, see Chin et al., 2024).

In general, the goal of information provision is not to subvert people's preferences, but to facilitate their acting on preferences with full information. Accordingly, thinking about preferences may help policymakers calibrate the expected impact of a disclosure policy. Just because people will continue eating ice cream after calorie labels are posted does not mean that the information should not be posted—it may even motivate some customers to try a new flavor—but effects will be moderated by existing preferences. Lesson from Consideration 1: Before formulating an information policy, consider the receptivity of the audience.

Consideration 2

Disclosures must capture consumers’ attention—both initial and sustained.

Consumers have a multitude of sources they can use to inform product decisions, including product reviews, word-of-mouth recommendations, and mandatory disclosures (e.g., on packaging). Because of this rich information environment, no particular disclosure is guaranteed to attract attention; for instance, clickstream data show that very few website visitors view the terms of a software purchase (Bakos et al., 2014), and lab experiments show that people can be distracted from viewing disclosures by factors as simple as having another person present (Chin & Beckett, 2018). Similarly, despite the fact that almost all Americans consume foods labeled with nutrition facts panels, estimates suggest that fewer than one-third of young adults frequently use these labels when buying a product for the first time (Christoph et al., 2018).

Due to the limits on consumer attention, a potentially counter-intuitive, welfare-improving intervention would be to design disclosures that help people optimally disengage when information is unnecessary, saving their time and attention for other matters. Chin et al. (2022) examined information at the top of an overdraft disclosure that asks, “Is overdraft right for you?”, thereby communicating information about the product class before delving into specific product details (e.g., the actual overdraft fee, or how overdraft coverage varies across payment methods). This work found that such headers can affect engagement and improve consumers’ confidence about their ultimate overdraft decisions. Although the role of headers should be examined in other contexts, this research suggests that signals of where not to direct one's attention would give consumers reassurance that they are not overlooking something important, potentially saving them time.

Even when consumers do engage with disclosed information, there remains the possibility that the sheer volume (Persson, 2018), underlying complexity (Schwarcz, 2004), and jargon (Bonsall IV et al., 2017; Donovan-Kicken et al., 2013; Loughran & McDonald, 2014) used to communicate information may prevent individuals from maintaining their attention through an entire disclosure. Rather, they likely satisfice, making the best decision that they can under the circumstances–here, their own limited processing capacity and the amount of information available (Grether et al., 1985). Importantly, the notion of satisficing suggests that disclosures frequently fail to fully inform consumers. The best disclosures should recognize realistic constraints of consumer attention and limit the amount of information consumers are expected to consider.

To make sure that consumers’ attention is not wasted, a significant body of research has concentrated on making financial information understandable. A promising set of interventions centers on providing consumers with contextual information. One way to do so is by displaying information in useful, familiar units. When considering mutual fund fees, for instance, disclosing fees in dollars (rather than percentages or basis points) makes the charges that accompany those funds more salient (Parida, 2024). When fees are clearer, consumer demand shifts away from higher-fee funds, and expensive mutual fund companies are driven to reduce their fees.

An alternative way to provide context is to display comparisons to alternative product options. For instance, although it may be difficult to know whether paying a 0.5% expense ratio on a mutual fund is “too high,” that task becomes easier when investors see that comparable products’ fees range from 0.05% to 0.55%. Indeed, communicating the range of available fees on comparable products can significantly reduce unnecessary fees paid (Scholl et al., 2023). This kind of range-based contextual information helps ensure that consumers do not rely merely on local comparisons (e.g., “Is this product better than a salient alternative?”), which could otherwise leave consumers vulnerable to decoy or dominance effects (Fridman et al., 2024; Heath & Chatterjee, 1995; Huber et al., 1982). With greater context, consumers can make better decisions and potentially learn about underlying attributes. Lesson from Consideration 2: Consumers have limited attention and information-processing capacity. Contextual information and judicious use of disclosures are essential to cut through the noise and truly inform consumers.

Consideration 3

Consumers should gain actionable knowledge from information disclosures to encourage behavior change.

The next step in ensuring the effectiveness of a disclosure is for consumers to gain actionable information and change their behavior accordingly. The link between information and behavior change highlights two key factors: the goals that individuals have and the environmental or situational constraints that may be present.

Different consumers have different goals. In the case of nutrition, some need to restrict sodium intake, others want to maximize protein intake, and others have no idea what they need. To address these varying situations, the temptation is to disclose everything. Yet, given limitations on consumer attention, discussed under Consideration 2, forcing consumers to read excessive information introduces a barrier to gathering actionable information and subsequent behavior change. Instead, people should receive information formatted to make salient the high-level goals that policymakers prioritize (e.g., moderate- to low-calorie meals, moderate- to low-fee investments), accompanied by detailed, full information only if consumers want to drill down into the details and optimize their decision-making process. More succinctly: first make the goal salient, then allow for optimization.

A policymaker's objective should include recognizing what consumers need to know to achieve long-term goals. In finance, low-cost investments can help people achieve long-term financial security. In nutrition, many consumers need information to help them identify their superordinate goal of eating reasonably healthy meals, and they may also need more detailed information to choose the appropriate items to meet that goal. For example, calorie labeling that provides dynamic color-coded prescriptive guidance for the total calorie content of a meal (where “green” signals that a meal meets a calorie goal, “yellow” signals that the goal is at risk of being unmet, and “red” signals that a meal has too many calories) can be paired with precise numeric calorie labels for individual items. Such labeling both motivates and enables comparisons across items, leading to healthier substitutions (VanEpps et al., 2021).

Beyond goals, a crucial consideration for encouraging behavior change is the set of barriers that are present when a consumer interacts with a disclosure. Barriers can take the form of structural factors, such as a marketplace that lacks multiple products; if there is only one internet service provider available for your home or one healthcare provider in your region, cost information will not make you switch. Barriers can also take the form of transient situational or personal factors. For instance, online information may help consumers make comparisons more easily on their phone or computer than when in a store, restaurant, or other physical location. Meaningful reductions in calories occur when calorie labels are applied in online ordering settings (VanEpps et al., 2016a), potentially because shifting the timing of the ordering decision reduces the impact of present bias, hunger, or other contextual cues (VanEpps et al., 2016b). By contrast, calorie labeling at the point of purchase on restaurant menus has yielded more mixed results (Bleich et al., 2017). Recognizing that consumers need the time, motivation, and cognitive resources to consider and act on calorie information may help explain why fast-food environments—where consumers are rushed, focused on familiar items at little expense, and influenced by potential distractions—have generally experienced smaller changes in consumer behavior in the presence of calorie labeling, relative to table-service restaurants (Zlatevska et al., 2018).

Whenever possible, disclosures should be timed to align with the consumer's motivation to act on information; if disclosures are aimed to guide purchasing decisions, they should be salient and easily accessible at the time when consumers evaluate alternatives (e.g., in the store). If, instead, the goal of a disclosure is to help people to use a product properly, then disclosures should be readily available at the point of consumption (e.g., at the kitchen table).

Both policymakers and researchers often neglect the feasible set of actions that consumers have available when viewing disclosures, as well as whether these actions are clear to consumers from the disclosures themselves. In the investment context, for example, shareholders receive semi-annual reports from mutual fund companies about the products they own. However, whether it is useful to read these disclosures is debatable. Should investors who made an informed decision about an investment product be required to refresh this knowledge every six months? If not, perhaps material changes in investment strategy, fees, or other decision-relevant criteria should be highlighted outside of these regular reports. More broadly, if improving consumers’ well-being is a policymaker's ultimate goal, the actions necessary to improve that well-being must be clear and accessible so that consumers can engage in them. Such considerations may mean that disclosures need to be paired with newly created opportunities for action; someone who receives a semi-annual report might benefit most from also receiving a form that can be completed to shift investment allocations, rather than being told to visit a website or call a phone number to change their investments. Lesson from Consideration 3: Disclosures should encourage actionable improvements by focusing on consumer goals and ways to facilitate consumer action. If consumers cannot take immediate action based on the information provided, they are unlikely to remember or use that information later.

Consideration 4

Firms and retailers will react to information provision requirements in ways that may change the effectiveness of disclosures.

Greater transparency concerning important attributes for consumer decision-making should, in principle, not only shift consumer choices among static options, but also dynamically change the types of products offered by firms to consumers. Often, these firm responses are positive, in that retailers adjust their offerings to improve the disclosed attribute. For instance, a meta-analysis of 41 studies of menu offerings in response to mandated calorie disclosures found that the average item had 15 fewer calories after disclosures relative to before disclosures were required (Zlatevska et al., 2018). Indirect effects have also been posited in theoretical models of the mortgage market, in which companies change prices in response to well-informed consumers (Alexandrov & Koulayev, 2018).

Before firms make such changes to their products, however, they may also engage in substantial lobbying efforts to avoid mandatory disclosures. With regard to calorie labeling, many food retailers—such as bakeries, convenience stores, and grocery stores—lobbied to be exempt from calorie labeling laws, even as restaurant groups lobbied that those same food retailers should be subject to calorie labeling laws (VanEpps et al., 2016c). Such lobbying efforts probably delayed implementation of calorie labeling on restaurant menus—whereas requirements for calorie labeling were included in the Patient Protection and Affordable Care Act of 2010, the implementation of these requirements did not go into effect until May 2018. Indeed, the food industry has fought against labeling laws for both restaurant menus and packaged foods at the local (Farley et al., 2009), national (VanEpps et al., 2016c), and international (Kurzer & Cooper, 2013; Lyn et al., 2019; Mialon et al., 2021) levels.

After disclosures go into effect, firms may respond depending on how well their products align with the newly disclosed product attribute. To the extent that a company is selling a product high in calories, expensive in fees, or risky as an investment, the company will likely attempt to skirt requirements to reduce the impact of a relevant disclosure requirement. Sometimes, this action takes the form of providing information in a less useful way. Consumers have less accurate (and often overly optimistic) estimates of the calories in a meal at Chipotle when menu boards are labeled with ranges (e.g., a burrito labeled as having 350 to 970 calories [Liu et al., 2015]), and may struggle to calculate total calories ordered when information is presented in a piecemeal fashion, such as calories per slice of pizza (VanEpps et al., 2016c, 2021). Mutual fund managers may intentionally create complex disclosures of their high fees to confuse investors (deHaan et al., 2021) and may concentrate more of their fees in the types of fees that consumers struggle to understand or notice (Anagol & Kim, 2012).

In short, companies can juke the statistics and respond to labeling laws strategically, attempting to emphasize their strengths while obscuring areas of weakness. To combat these attempts, policymakers should consider specificity in disclosure rules to prevent attempts to circumvent the goals of disclosure, or push for “all-in” disclosures, such as a “total cost” metric that makes individual-level fees less important. The same “all-in” disclosure logic would recommend a comprehensive nutrition labeling system that includes a weighted average of different nutrients (Chantal et al., 2017; Sutherland et al., 2010), rather than allowing companies’ products to appear healthy by emphasizing a single attribute while being unhealthy on other attributes (e.g., being “low fat” but high in sugar). Alternatively, policymakers may consider dynamic rules to preempt firm attempts at “gaming,” such as requiring firms to make certain fees particularly salient to consumers when they generate high revenues. This strategy has been adopted for prepaid card fees (12 CFR Part 1005),

1

where the physical size of prepaid cards constrains the amount of information displayed. Furthermore, policymakers may wish to evaluate the impact of potential rules in extensive pre-implementation testing via a mix of qualitative and quantitative research. Lesson from Consideration 4: To predict the likely net effects of an information policy, consider how market players may respond by changing available products or obscuring detrimental information.

Consideration 5

A lack of information might not necessarily be harmful. More information (or higher-quality information) could have perverse effects.

Consumers operating in a marketplace naturally form beliefs about product attributes, such as price or calories. For example, most consumers believe that fast food is unhealthy; on the other hand, they may have more weakly held beliefs about the relative healthfulness of a full-service restaurant, where typical meals are higher in calories than many fast-food meals. Variation in preexisting beliefs means that information policies may have counterintuitive effects.

Imagine a consumer who is considering ordering food from McDonald's. In all likelihood, their expectation is that many items on the McDonald's menu are unhealthy, especially a prominent item like the Big Mac. However, perhaps as a function of remaining largely unchanged over the decades, the Big Mac has a relatively modest calorie content of 590 calories (McDonald's, 2024). Relative to expectations that the Big Mac could have 800 or more calories, truthfully disclosing the actual calorie content may motivate more consumers to purchase the Big Mac and perhaps add a side dish they would have omitted had their expectations not been corrected. Such backfiring effects, whereby disclosure leads to unhealthier behavior, have been shown for calories-per-serving labels (Tangari et al., 2019) and could explain why calorie labels have generally not reduced average calorie consumption in fast-food environments (Bleich et al., 2017; Long et al., 2015).

In the investment domain, information may also have counterintuitive effects, particularly when the information is irrelevant to the actual decision at hand. Perhaps the most glaring example is the fact that past investment performance does not predict future performance, and yet consumers act as though it does (Johnson et al., 2022). Providing information on past investment performance might feel like a worthwhile intervention to facilitate comparisons across different investments, but it can lead people to anchor their evaluations on irrelevant information. The type of information shown must be carefully chosen to avoid this kind of misleading updating of beliefs.

There is significant policy concern about consumers paying too much for investment products, but care must be taken when deciding whether and how to communicate the costs of these products to increase awareness. Survey research shows that 41% of 401(k) plan participants believe they pay no fees on their plan, and another 23% are not sure; in reality, however, they all pay fees (GAO, 2021). One might worry that educating consumers about investment-related costs would have the perverse effect of deterring investment behavior; perhaps a lack of information about these fees is the optimal policy for many consumers. Similarly, as the investment industry starts allowing investors to make zero-cost trades (a move that may appear to be good for consumers), it may simultaneously recoup the lost revenue in other ways (like selling data on investors’ transactions). Accordingly, it is not clear whether emphasizing costs may motivate firms to adjust business practices in ways that have other negative effects for consumers.

Before implementing information provision as an intervention to change behavior, policymakers should more regularly first capture beliefs in the absence of information. When a priori beliefs drive people toward behaviors that improve their well-being, the provision of corrected, accurate information may backfire. But when people's expectations can be disconfirmed in a way that fosters healthier decisions, information provision can be quite useful (Burton et al., 2015). To be sure, this last consideration is paternalistic, because it invites the policymaker to consider whether it is better for consumers to be ignorant or otherwise ill-informed about some phenomena. When comparing the costs and benefits of different interventions, however, include the possibility that even well-intentioned interventions can backfire. Lesson from Consideration 5: To predict the efficacy of a disclosure policy, first capture consumers’ beliefs in the absence of information, with the goal of identifying potential backfiring effects.

Conclusion

The disclosure of information to consumers is a useful and popular intervention to influence consumer behavior, but these policies are not without challenges. Five considerations, placed within a broader theory-of-change framework, should guide policymakers as they attempt to design optimal disclosure policies. Drawing from research regarding nutrition and finance, this paper illustrates the importance of audience receptivity, consumer attention, immediate action steps, firm responses, and potential unintended consequences. The two domains are simply illustrative; the same principles and framework can and should be applied to disclosure policies for other important consumer decisions.

The framework may serve multiple audiences, including policymakers and consumer advocates considering which information policies to pursue and how to make these policies most effective. When policy proposals are made public (e.g., through the federal government's notice-and-comment process), companies may also use this framework to suggest improvements to disclosure policies. For instance, companies may be well-equipped to understand limited attention to disclosures using data on clickthrough rates or may recognize avenues for changing a customer's experience to strengthen the link between information and action. Indeed, the strongest collective evidence in the present review concerns limited attention and the link between actionable information and behavior change (Considerations 2 and 3). There is relatively less work on how firms might leverage disclosure changes to advertise their superior position within a marketplace, how to encourage consumers to optimally disengage attention, or how consumers and firms respond to each other's behavior in the wake of new disclosure policies. Future studies should pursue these important avenues, as well as continue to build nuanced insights around specific consumer decisions and disclosure interventions.

Because this research concerns consumers, firms, and policymakers, essentially everyone has a stake in getting information disclosure policy right. We hope that the considerations provided here can encourage researchers and practitioners to reengage in work that raises consumers’ overall well-being.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.