Abstract

Firms’ success depends on their ability to deal with formal institutional quality. Specifically, firms exposed to a diversified set of institutional profiles can achieve institutional competitive advantage that provides firms with diverse knowledge and broader learning opportunities. While prior studies argued that being exposed to a diversified set of institutional profiles negatively influences firms because institutional knowledge can only be replicated in similar institutional profiles, they missed the point of learning from diversity. The purpose of this study is to further understand how firms’ institutional experience moderates the relationship between formal institutional quality and firms’ performance. We argue that firms with higher and more diverse institutional experience will adapt more efficiently to formal institutional quality, thus improving firms’ performance. We test the hypotheses on 4,011 publicly traded firms from the European Union between 2010 and 2021, and our results show that firms that develop higher institutional experience are better able to efficiently adapt to and leverage formal institutional quality and achieve higher firm performance. We contribute to the ongoing discussion on how formal institutions influence firms’ performance by acknowledging the importance of developing a diversified institutional experience.

Keywords

Introduction

Firms’ success depends on their ability to adapt to the quality of the institutional environment (Cuervo-Cazurra, Mudambi, & Pederson, 2019; Jackson & Deeg, 2008). If institutions are the rules of the game (North, 1991), then how firms adapt to the rules of the game remains an important question (Dau et al., 2020; Kostova & Hult, 2016; Peng et al., 2008). The general idea is that if firms adapt to the quality of institutions, following transaction costs theory prescriptions, firms will perform well over the long run (Argyres & Zenger, 2022; Williamson, 1991). Since institutions influence transaction costs, institutional quality can greatly affect how firms conduct their activities and organize for economic success (Hennart & Verbeke, 2022). Thus, firms should focus on how to efficiently adapt to the circumstances at hand by addressing the institutional opportunities and challenges to improve their performance (Argyres & Zenger, 2012, 2022).

However, Williamson’s “efficiency-as-strategy” logic does not fully and satisfactorily explain persistent performance differences between firms (Argyres & Zenger, 2012, 2022; Barney et al., 2023). Firms may develop resources and capabilities that improve firms’ adaptation to formal institutional quality, which may create persistent performance differences among firms (Grøgaard & Verbeke, 2012; Hennart & Verbeke, 2022; Narula & Verbeke, 2015). Specifically, by being exposed to a diversified set of institutional profiles, firms benefit from diverse knowledge and broader learning opportunities that can translate into institutional competitive advantages (Fuentelsaz et al., 2022; Lundan & Li, 2019). Nonetheless, prior research arguably missed the point of learning from diversity (Lumineau et al., 2021; Lundan & Li, 2019; Pattnaik et al., 2021) by positing that institutional knowledge can only be replicated if obtained from similar institutional profiles (Perkins, 2014; Trąpczyński & Banalieva, 2016). Despite acknowledging that the institutional experience, which is a multidimensional concept to account for the similarity, breadth, and depth of involvement in institutional environments (Perkins, 2014), is an important source of institutional competitive advantages (e.g., Domínguez et al., 2023; Fuentelsaz et al., 2022; Lundan & Li, 2019; Trąpczyński & Banalieva, 2016), there is still limited knowledge on how firms gain an advantage by learning from a diversified set of institutional profiles and benefit from institutional experience (Lumineau et al., 2021; Pattnaik et al., 2021).

The purpose of this study is to further understand how firms’ institutional experience moderates the relationship between formal institutional quality and firms’ performance. We build upon the theoretical approach that firms learn from being exposed to diversified set of institutional profiles (Lumineau et al., 2021; Pattnaik et al., 2021; Perkins, 2014). More importantly, firms’ institutional experience can evolve into a firm-specific resource (Perkins, 2014), such as diversified knowledge, adaptative firm processes, and more arbitrage opportunities (Lundan & Li, 2019), thus granting firms institutional competitive advantages capable of generating persistent performance advantages (Fuentelsaz et al., 2022). We argue that firms with higher levels of institutional experience will adapt more efficiently to the level of formal institutional quality of the host country by overcoming institutional inefficiencies, while benefiting from the institutional opportunities, thus improving firms’ performance. We test the hypotheses on an unbalanced panel of 4,011 publicly traded firms from the European Union (EU) between 2010 and 2021. Our results show that formal institutional quality has a positive effect on firms’ performance through the minimization of transaction costs. Also, we confirm that firms that have a higher level of institutional experience are better able to efficiently adapt to formal institutional quality and thus achieve higher firm performance.

We contribute to the International Business (IB) literature by adding to the ongoing discussion on the effect of formal institutional quality on firms’ performance in two ways. First, we contribute to further understand why previous research on this relationship yielded mixed results (e.g., Banalieva et al., 2018; Chari & Banalieva, 2015; Cuervo-Cazurra & Dau, 2009) by adding to the argument that firms differ in their ability to benefit from the formal institutional quality (Cuervo-Cazurra, Mudambi, & Pederson, 2019; Dau et al., 2020; Kafouros & Aliyev, 2016a, 2016b; Kafouros et al., 2022, 2024). We follow a call from Dau et al. (2020) to further delve into the starting position of the firm that allows firms to efficiently adapt to the formal institutional quality, by combining the institutional approach with firms’ resources that are developed as a consequence of firms’ transactions (Argyres & Zenger, 2012, 2022; Barney et al., 2023). We argue that firms that develop superior resources (Grøgaard & Verbeke, 2012; Narula & Verbeke, 2015), such as higher institutional experience, are better able to adapt to the formal institutional quality and achieve performance advantages (Hennart & Verbeke, 2022).

Second, we contribute to shed light on the ongoing debate regarding the importance of developing a diversified institutional experience. We follow a call from Trąpczyński and Banalieva (2016) to further address the mixed findings on the influence of institutional experience on firms’ performance. Learning from similar environments provides increased synergies from similar routines, while learning from dissimilar environments may cause penalty effects from unrelated learning (Perkins, 2014; Trąpczyński & Banalieva, 2016). We contribute to the theoretical view of learning from diversity (Lumineau et al., 2021; Lundan & Li, 2019; Pattnaik et al., 2021), by arguing and confirming that firms exposed to a diversified set of institutional profiles are able to achieve institutional competitive advantage that provides firms with diverse knowledge and broader learning opportunities (Fuentelsaz et al., 2022; Lundan & Li, 2019). Empirically, we propose a multidimensional measure of institutional experience that combines the depth and breadth of firms’ institutional experience, by accounting for the intensity, diversity, and distance of institutional experience, that overcomes shortcomings of previous measurements of institutional experience (see the review by Trąpczyński & Banalieva, 2016).

Literature review

Institutional economics considers institutions as constraints guiding economic actions and behaviors (Cuervo-Cazurra, Mudambi, & Pederson, 2019). Formal institutions are defined as a set of explicit and codified rules of the game (North, 1991). As market transactions are deemed imperfect due to bounded rationality, opportunism, and information asymmetries, market transactions require guidance to be efficient (North, 1990, 1991; Williamson, 1975, 2000). Consequently, institutions have been devised to create order and reduce uncertainty in exchange (North, 1990, 1991). Together with the standard constraints of economics, institutions determine the transaction costs (North, 1991). Therefore, institutional economics focuses on the transaction costs associated with either using markets or firms as alternative instruments for completing a related set of transactions (Williamson, 1975).

A country is considered to have higher formal institutional quality when the laws and regulations facilitate market relationships among economic actors (Cuervo-Cazurra, Mudambi, & Pederson, 2019). Formal institutional quality is defined as the overall effectiveness and efficiency in helping firms engage and gain from market transactions (Kafouros et al., 2022). Thus, formal institutional quality is reflected in the quality of the written rules of the game, and the effectiveness of enforcing mechanisms during economic transactions (Williamson, 2000). For example, formal institutional quality includes efficient written laws, the quality of government regulation, the existence of property rights, judicial independence and effectiveness, the efficacy of the legal system, and execution of undue influence by government officials (Kafouros et al., 2022; North, 1991).

Formal institutional quality is broadly acknowledged to influence firms’ performance (Banalieva et al., 2018; Dau et al., 2020; Kafouros et al., 2024). On the one hand, market transactions under higher formal institutional quality occur in the form of more efficient written rules of the game, with more efficient enforcement mechanisms, thereby providing firms with reduced opportunistic behavior and less information asymmetries (Banalieva et al., 2018; Kafouros & Aliyev, 2016a, 2016b; Kafouros et al., 2022). Thus, higher formal institutional quality influences positively firms’ performance, as more efficient market mechanisms reduce transaction costs (Cuervo-Cazurra & Dau, 2009; Kafouros & Aliyev, 2016a; Kafouros et al., 2022). On the other hand, higher formal institutional quality may also negatively influence firms’ performance (Chari & Banalieva, 2015; Chari & David, 2012), as efficient market mechanisms increase firms’ competition, thus leading to the redistribution of income rather than increased income (Chari & Banalieva, 2015; North, 1991). Therefore, the relationship between formal institutional quality and firms’ performance yields mixed and inconclusive results (Chan & Du, 2021; Cuervo-Cazurra, Mudambi, & Pederson, 2019; Fuentelsaz et al., 2022).

Several theoretical insights advance possible explanations for the extant mixed and conflicting results regarding formal institutional quality. Motives such as the conceptualization and measurement of institutions (Aguilera & Grøgaard, 2019; Cuervo-Cazurra, Mudambi, & Pederson, 2019), the dynamics of institutional theory (e.g., institutional change, synchronization, predictability, and fragility; Banalieva et al., 2018; Cuervo-Cazurra, Gaur, & Singh, 2019; Fuentelsaz et al., 2022; Shi et al., 2017), and, arguably more importantly, the firms’ characteristics define firms’ ability to deal with formal institutional quality (Dau et al., 2020). Thus, previous mixed findings suggest that not all firms benefit the same way from formal institutional quality (Cuervo-Cazurra, Mudambi, & Pederson, 2019; Dau et al., 2020; Kafouros et al., 2022). As transaction costs theory does not fully explain why some firms might operate more efficiently than others (Argyres & Zenger, 2012, 2022; Barney et al., 2023), IB scholars have been shifting focus to the development of firm resources and capabilities, as competitive advantages to efficiently adapt to formal institutional quality (Argyres & Zenger, 2012, 2022; Barney et al., 2023; Hennart & Verbeke, 2022) to explain firms’ performance.

The strategic theory of the firm offers a novel view of the combination between institutional approaches and firms’ resources and capabilities as the direct outgrowth of firms’ transactions, capable of creating persistent performance differences among firms (Argyres & Zenger, 2022; Barney et al., 2023). It complements prior studies that found that specific firms’ characteristics distinguish more successful firms from less successful ones depending on the level of formal institutional quality (Kafouros & Aliyev, 2016a, 2016b; Kafouros et al., 2022). For example, larger firms that internalize market functions that are not efficiently acquired through market mechanisms obtain a competitive advantage over rivals in lower quality institutional environments (Kafouros et al., 2022). Also, subsidiaries’ capabilities were found to be a useful mechanism in lower institutional quality, since subsidiaries’ intangible assets were found to enhance firms’ growth in higher institutional quality (Kafouros & Aliyev, 2016b). And firms that operated internationally were found to adapt more efficiently to the institutional quality because firms that acquired market knowledge and capabilities abroad were able to use the knowledge in home country (Dau, 2013; Fuentelsaz et al., 2022).

However, the organizational learning literature has also provided mixed findings regarding how institutional experience affects firms’ performance (Trąpczyński & Banalieva, 2016). The potential benefits are related to the learning synergies from similar memorized routine from similar institutional profiles, while the potential hindrances are related to the penalty effect from unrelated learning (Perkins, 2014; Trąpczyński & Banalieva, 2016). Thus, it is not clear how firms can learn from institutional diversity (see Lumineau et al., 2021; Pattnaik et al., 2021), specifically considering the diversified knowledge, adaptative firm processes, and more arbitrage opportunities (Lundan & Li, 2019) that grant firms with institutional competitive advantages capable of generating persistent performance advantages (Fuentelsaz et al., 2022). Although recent studies distinguished between the depth and breadth of institutional experience, and between similar and dissimilar institutional experience, there is a misconception that the degree of firms’ internationalization equals to institutional experience. There is a need to acknowledge that two firms with the same number of foreign subsidiaries and operating in the same number of foreign countries can be exposed to different levels of institutional diversity (Lundan & Li, 2019; Wu et al., 2015). Therefore, the role of firms’ institutional experience in the relationship between formal institutional quality and firms’ performance requires additional attention.

Conceptual model

Formal institutional quality and firms’ performance

Significant differences in the quality of formal institutions can notably affect how firms operate and organize for economic success (Hennart & Verbeke, 2022). However, how one firm adapts more efficiently than another to the environment depends on the given circumstances at hand. Therefore, we first need to define the circumstances at hand based on the level of formal institutional quality (the effectiveness of laws and regulations combined with the formal enforcement) that consequently define the level of institutional hazards (e.g., opportunism and information asymmetry) that firms must cope with. Hence, as formal institutions attain higher quality, we expect all firms to minimize transaction costs under more effective formal institutions, thereby increasing firms’ performance.

In the context of lower formal institutional quality, the written rules of the game are inefficient and unclear, accompanied by ineffective enforcing mechanisms, thus decreasing the overall effectiveness of engaging and gaining from market transactions. According to wealth-maximizing behavior and asymmetric information, practically every individual has some advantage over all others by possessing unique information (Williamson, 1975). As a result, not only do contractual relations run under greater levels of information asymmetry but also contractual relations face higher risks of opportunistic behavior (North, 1991; Williamson, 2000), thus making contractual relations increasingly costly, incomplete, and without any contract enforcement mechanism. Moreover, lower formal institutional quality presents limited opportunities to generate income, since inefficient institutions—such as poor protection of property rights—prevent appropriation of value and deter investments. Therefore, in the context of lower formal institutional quality, we expect transaction costs to increase due to higher levels of opportunism and information asymmetries, thus diminishing the firm’s performance.

In the context of higher formal institutional quality, the written rules of the game are efficient and clearer, accompanied by effective enforcing mechanisms, thus increasing the overall effectiveness and quality of engaging and gaining from market transactions. Efficient formal institutions will decrease information asymmetries and uncertainties, while also diminishing the potential for opportunistic behavior. For example, firms are no longer expected to face additional costs for obtaining information and enforcing contracts, since more efficient transparency requirements and efficient court systems reduce the costs involved in contracts. Moreover, higher formal institutional quality also creates opportunities for more income—even if efficient market mechanisms increase firms’ competition (Chari & Banalieva, 2015; Chari & David, 2012). The institutional opportunities include the public investments in infrastructure such as education that facilitates the development of human capital and knowledge transfer (Kafouros et al., 2022). For example, effective protection of property rights, such as patents and copyrights, will help firms appropriate value from their innovations (Kafouros et al., 2022), by using efficient market mechanisms to sell or license their innovations. Consequently, higher formal institutional quality allows firms to employ their competitive advantages in market transactions. Therefore, we argue that in the context of higher formal institutional quality, firms will be more capable of benefiting from the market opportunities, with lower transaction costs, thus enhancing firms’ performance (Figure 1). Hence, we hypothesize the following:

Baseline hypothesis 1 (H1). Formal institutional quality has a positive effect on firms’ performance.

Conceptual model.

Formal institutional quality and firms’ institutional experience

The strategic theory of the firm (Argyres & Zenger, 2012, 2022; Hennart & Verbeke, 2022) offers an explanation as to how firms, by developing firms’ resources (e.g., institutional experience), can efficiently adapt to formal institutional quality and create persistent performance differences (Lundan & Li, 2019; Perkins, 2014). We define institutional experience as the experiential learning derived from knowledge acquired by being exposed to host country’s institutional profile (Perkins, 2014). Our theoretical approach emphasizes learning from institutional diversity (Lumineau et al., 2021; Pattnaik et al., 2021), meaning being exposed to a diversified set of institutional profiles that allow firms to adapt more efficiently to formal institutional quality (Dau, 2013; Fuentelsaz et al., 2022; Perkins, 2014). Thus, institutional competitive advantages are the distinctive knowledge and rationality, obtained from the interaction with a diversified set of institutional profiles, capable of generating future economic value (Fuentelsaz et al., 2022). We expect firms with higher institutional experience to better adapt to formal institutional quality and increase firms’ performance.

In the context of lower formal institutional quality, the written rules of the game are inefficient and unclear, accompanied by ineffective enforcing mechanisms, thus decreasing the overall effectiveness of engaging and gaining from market transactions. We argue that firms with higher institutional experience will be better able to protect against the increased risks and uncertainty, and the market failures provided by lower formal institutional quality. Since lower formal institutional quality increases the risk and uncertainty associated with the lack of contract enforcement, information asymmetry, and the potential for opportunistic behavior, taking efficient strategic decisions becomes a challenging task (Fuentelsaz et al., 2022). Thus, firms may need to protect themselves against the risk of incurring additional transaction costs. Firms with lower institutional experience will not be able to avoid the existing transaction costs, since they fail to put in place additional contract enforcement mechanisms, to access additional information, or even to identify market transactions that are about to be made under opportunistic behavior. Hence, we argue that the performance-consequences disadvantages of lower formal institutional quality will be stronger for firms with lower institutional experience than for firms with higher institutional experience.

In the context of higher formal institutional quality, the written rules of the game are effective and clearer, accompanied by effective enforcing mechanisms, thus increasing the overall effectiveness and quality of engaging and gaining from market transactions. As it depends on the firm’s ability to benefit from the institutional opportunities, firms with higher institutional experience will be better able to capitalize on the opportunities and maximize value creation. For instance, higher formal institutional quality increases the effectiveness of laws and regulations, which provide opportunities for firms to engage in market transactions with lower transaction costs. The reduced transaction costs provide firms with additional resources that can be further augmented in the favorable institutional opportunities identified by the firms with higher institutional experience. Thus, the improved knowledge and learning will further benefit firms from the performance-enhancing mechanisms that the cooperative solutions in the market provide. We argue that the positive effect of formal institutional quality on firms’ performance will be stronger for firms with higher institutional experience than for firms with lower institutional experience.

In sum, we hypothesize that a higher level of firms’ institutional experience positively moderates the relationship between formal institutional quality and firms’ performance, such as firms with higher institutional experience will benefit from greater maximization of value creation while minimizing transaction costs in both lower and higher formal institutional quality when compared to firms with lower institutional experience. Hence, we hypothesize the following:

Hypothesis 2 (H2). The firms’ institutional experience positively moderates the relationship between the formal institutional quality and firms’ performance, such as the higher the level of firm institutional experience, the stronger the positive effect of formal institutional quality on firms’ performance.

Method

Research on the topic of institutional quality and firms’ performance has largely assumed that developed economies are not prominent in setting the field for theoretical developments (Dau et al., 2020; Miroshnychenko et al., 2023), thus most research focused on emerging (Banalieva et al., 2018; Chari & Banalieva, 2015; Kafouros et al., 2022, 2024), developing economies (Cuervo-Cazurra & Dau, 2009; Dau, 2013), and transition economies (Kafouros & Aliyev, 2016a, 2016b). However, this assumption led to specific characteristics of the countries not properly accounted for. Especially in the EU, where the recent major expansions (e.g., CEE countries) led to the application of convergent mechanisms (Blevins et al., 2016) imposed by other governments or supranational entities, with limited ability to refuse or adopt another institutional model (Cuervo-Cazurra, Gaur, & Singh, 2019). Nonetheless, the emergence of a convergent institutional environment appears to be illusive as the institutional divergence between EU members remains significant (Blevins et al., 2016; Jaklič et al., 2020; Meyer & Peng, 2016), thus making the EU a still promising research area for providing research outputs beyond the EU (Jaklič et al., 2020).

Data collection and sample

We constructed a dataset of publicly traded firms from the EU. The countries that are EU members are Austria, Belgium, Bulgaria, Croatia, 1 Republic of Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, and the United Kingdom. 2 We identified a total of 13,356 publicly active available firms in the EU between 2010 and 2021. We selected firms’ unconsolidated accounts to exclude the financial effect of firms’ subsidiaries. Furthermore, we excluded observations with missing information and financial type firms. The final valid N listwise consisted of 48,132 total observations, from a total of 28 countries from the EU and 4,011 total companies, for a time window of 12 years, between 2010 and 2021. The data were obtained from the Orbis Europe Database, which is compiled by Bureau van Dijk (BvD) and includes comparable financial data for EU firms.

Dependent variable

The dependent variable was the firm’s performance, defined as the firm’s profitability each year. We used single accounting-based measures because the single accounting-based measures were found to be significant in the relationship between institutions and firms’ performance (see Kostova et al., 2020). Thus, we used return on equity (ROE), which is the ratio between yearly net income and shareholders’ equity, in percentage, with data collected in the Orbis Europe database.

Independent variables

The independent variable formal institutional quality refers to the overall effectiveness and efficiency of the country’s formal institutions guiding economic transactions (Kafouros et al., 2022). While both the Economic Freedom Index (EFI) and Worldwide Governance Indicators (WGI) are commonly used to measure institutional quality (see Kostova et al., 2020), we argue that the WGI is better suited for our research question as it captures the perceptions of country’s formal institutional quality regarding the quality of laws and regulations and the effectiveness of enforcement mechanisms. The WGI comprises six pillars: (1) Voice and accountability, (2) Regulatory quality, (3) Political stability and absence of violence/terrorism, (4) Rule of law, (5) Government effectiveness, and (6) Control of corruption (World Bank). Each of the six pillars of WGI is graded on a scale from −2.5 to 2.5, such that a higher value means a higher formal institutional quality. To aggregate the data of the six pillars, we ran a confirmatory factor analysis, which retained a single factor with 86.35% total variance explained (KMO = 0.92, p-value = .00).

Moderating variable

The moderating variable institutional experience refers to the experiential learning derived from knowledge acquired from being exposed to host country’s institutional profile (Perkins, 2014). Our theoretical approach emphasizes learning from contextual heterogeneity while being exposed to a diversified set of institutional profiles (Lumineau et al., 2021; Pattnaik et al., 2021) that allow firms to adapt more efficiently to formal institutional quality (Dau, 2013; Fuentelsaz et al., 2022; Perkins, 2014). We build upon the ideas of Perkins (2014) and Trąpczyński and Banalieva (2016) to define a multidimensional measure that considers both the breadth and depth of firms’ institutional experience. To do so, we adapted the approach of Miller et al. (2016) to propose the three facets of firm’s institutional experience, namely institutional intensity, institutional diversity, and institutional distance.

Institutional intensity captures the depth of firms’ institutional experience defined as the degree of firms’ foreign operations, measured by the total number of foreign subsidiaries (Trąpczyński & Banalieva, 2016). Institutional diversity captures the breadth of firms’ institutional experience defined as the degree of variance between the host countries’ formal institutional profiles (Zhao et al., 2020). We measured institutional diversity by the standard deviation of the set of host countries’ formal institutional profiles that firms have been exposed to (Wu et al., 2015; Zhao et al., 2020). Institutional distance captures the degree of cross-national differences of formal institutional quality between the firm’s home country and the set of host countries of its foreign subsidiaries (Miller et al., 2016). We measured institutional distance by calculating the distance between the home country and each host country WGI indicator, which produced a single factor with a total variance explained of 89.25% (KMO = 0.92, p-value = .00) when using a principal component factor analysis with varimax rotation. Finally, we constructed a multidimensional measure of institutional experience consisting of the three facets, that by using principal component factor analysis with varimax rotation, produced a single factor with a total variance explained of 65.90% (KMO = 0.58, p-value = .00; see Supplemental Appendix A1 for additional information).

Control variables

The control variables capture variations at the country level and firm level. At the country level, we included the country size (measured using the natural logarithm of the country’s GDP in constant dollars) and country growth (as a percentage of total GDP growth year over year) to account for the domestic markets’ opportunities, in constant USD, to isolate the effects of price changes. Larger markets may provide firms with greater opportunities, thus influencing firms’ performance (Banalieva et al., 2018; Fuentelsaz et al., 2022; Shi et al., 2017). We also included the country FDI defined as the foreign direct investment received by the home country, measured as a percentage of net FDI inflows over total GDP. Higher inward FDI may bring about greater competition, thus hindering firms’ ability to perform (Banalieva et al., 2018; Shi et al., 2017). The data were obtained from the World Bank Database. Finally, we included countries’ dummies (28 country dummies).

At the firm level, firm size captures the scale of resources, measured using the natural logarithm of the firm’s total assets in thousands of dollars. We expect larger firms to have greater levels of resources, thus benefiting from internalization advantages (Kafouros & Aliyev, 2016b; Kafouros et al., 2022). We included firm age, which relates to the firm’s experience in the country, measured using the natural logarithm of the number of years since foundation plus one (Banalieva et al., 2018; Shi et al., 2017). Older firms may be more profitable because they are more established in the market (Banalieva et al., 2018; Fuentelsaz et al., 2022). We included firm liquidity, which is the firm’s ability to pay its short-term debt. Firms with greater debt may be more prone to pursue more short-term strategies with certain payoffs to cover their liabilities (Banalieva et al., 2018). We included foreign firm defined as the majority of a firm’s capital being foreign capital. To identify whether a firm is foreign, we used the information on the Global Ultimate Owner (GUO). We created a binary variable where we classified with foreign firm = 1 when the country of the GUO was different than the firm’s home country, and zero otherwise. Finally, we included industry dummies using the NACE rev. 2 main categories for the firms’ industry (category A to U, a total of 21 industry dummies were included; Shi et al., 2017). The data were obtained from the Orbis Europe database.

Finally, we included the year dummies (12 years) to control for year-fixed effects in all our models (Fuentelsaz et al., 2022; Shi et al., 2017).

Procedure of analysis

Our dependent variable firms’ performance may present inertia over time, as current values may be affected by the performance of prior periods. For this reason, we use dynamic panel data analysis to control possible endogeneity by including the lag of the dependent variable (e.g., Fuentelsaz et al., 2022). The Generalized Method of Moments (GMM) estimator produces dynamic estimates that are consistent in the presence of endogeneity problems (Arellano & Bond, 1991). We followed the validation of GMM estimators used in Fuentelsaz et al. (2022) and it requires three tests: (1) the Hansen test, (2) the test for AR(2), and (3) the Wald-Chi tests. First, the Hansen statistic of excessive identification restrictions is used to prove the absence of correlation between the instruments and the error term. The result of the test is statistically nonsignificant, with levels of significance between 0.15 and 0.16, therefore there is no overidentification (the instruments are valid). Second, to prove that error terms are uncorrelated, the model’s error terms are required to not be second-order correlated (as evidenced by the lack of significance for the AR(2) test). Third, the Wald-Chi tests are presented to measure the joint significance of the variables in the models, thus all the Wald tests support the joint importance of the coefficients.

Results

Table 1 provides the descriptive statistics—means and standard deviations—and the correlations matrix. We provide additional unstandardized descriptive statistics for the variables that were mean centered in Table 1. Related to firms’ performance, we note that firms have on average 1.87% (SD, 48.93) on ROE. We note that formal institutional quality has a mean value of 1.03, with a standard deviation of 0.53. Related to the firm’s institutional experience, we note that firms have on average 20.12 (SD, 82.86) total foreign subsidiaries, with an average institutional diversity of 0.25 (SD, 0.35), and an average institutional distance of each formal institutional dimension between 0.30 and 0.47. We note that firms have an average firm size of 433.67 million dollars of total assets (SD, 161.18 million dollars of total assets) and an average firm age of 33.24 years old (SD, 33.87). Finally, we did not identify any high correlations in our data (Table 1), suggesting that our results are absent of multicollinearity.

Descriptive statistics and correlations.

The independent variables formal institutional quality and institutional experience were centered (M =0 and SD = 1) in the future analyses.

p < .05.

Hypotheses testing

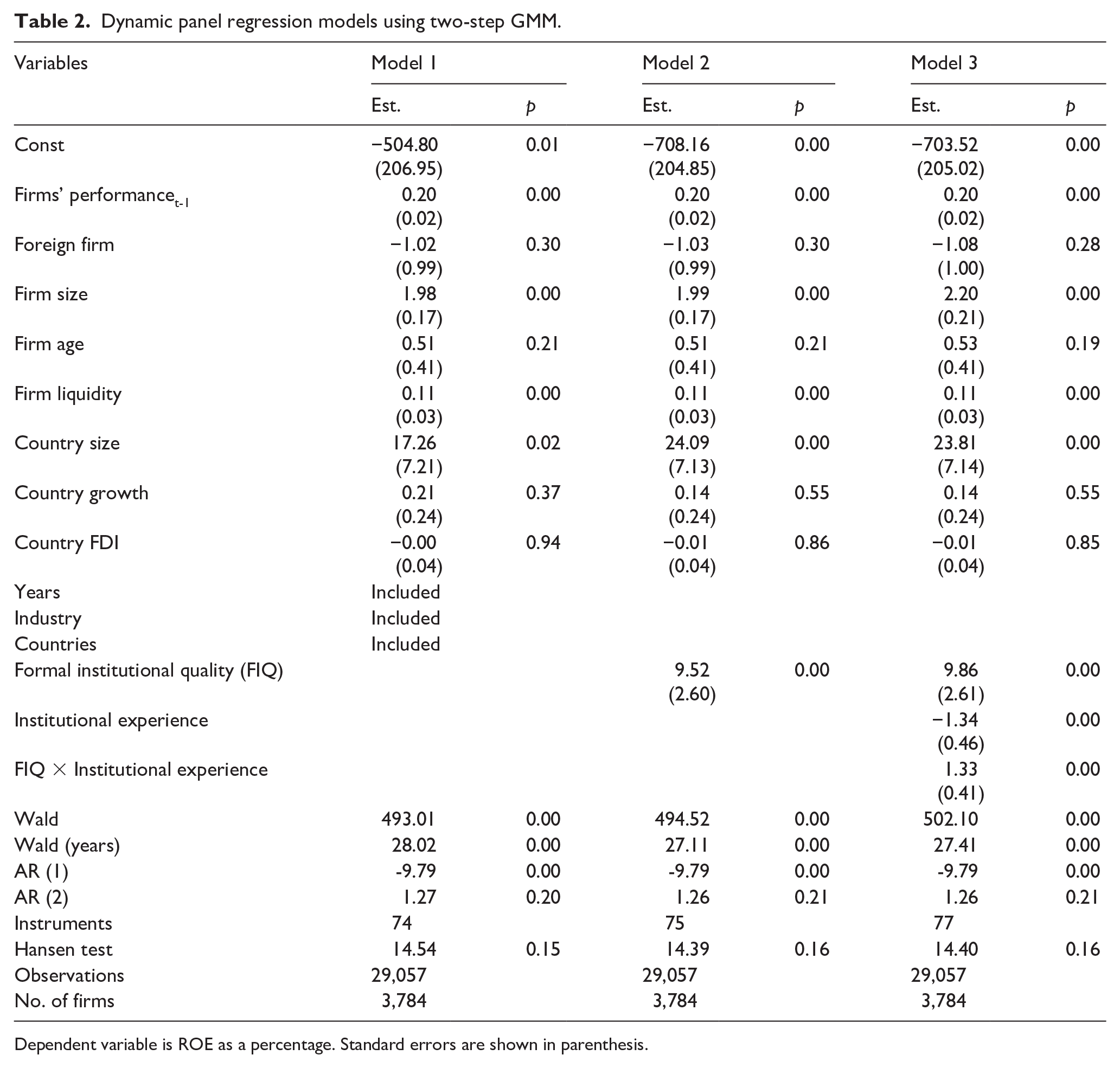

We start our analysis by estimating a dynamic regression model of the predictive variable firms’ performance. Thus, Table 2 reports the obtained results. In model 1, we include only the control variables. In model 2, we include the independent variable formal institutional quality. In model 3, we include the moderating variable institutional experience, and we provide the full model with all the variables and interactions included in the conceptual model, where we test H1 and H2.

Dynamic panel regression models using two-step GMM.

Dependent variable is ROE as a percentage. Standard errors are shown in parenthesis.

In model 3 of Table 2, we tested the H1. We argued that formal institutional quality has a positive effect on firms’ performance. A positive and significant coefficient in model 3 (β = 9.86, p-value = .00) confirms that formal institutional quality has a positive effect on firms’ performance, and we find support for H1.

In model 3 of Table 2, we tested H2. We argued that the firm’s institutional experience positively moderates the relationship between the formal institutional quality and firms’ performance, such that the positive effect is stronger for firms with greater institutional experience. A positive and significant coefficient of the interaction variable between formal institutional quality and institutional experience in model 3 (β = 1.33, p-value = .00) confirms that firm size positively moderates the relationship between formal institutional quality and firms’ performance, and we find support for H2. Also, by following Kingsley et al. (2017) recommendations, we provide visual clarification of the marginal effect of formal institutional quality on firms’ performance depending on the level of firm’ institutional experience, with confidence bands at 95% confidence level (Figure 2). Critically, since the confidence interval bands do not cross zero for values of institutional experience greater than or equal to 0, we can conclude that the marginal effects are statistically different from zero (at the 95% level) over the range of institutional experience between 0 and 12.

Marginal effect of formal institutional quality on firms’ performance based on firms’ institutional experience.

Robustness tests

One possible alternative explanation for the results is due to the method of analysis used. We thus ran the analyses using the random effects generalized linear models. Also, in both methods of analysis, we tested whether the results were due to the data not being lagged by at least 1 year. To address this issue, we ran the analyses with 1-year lag times for the independent variables of interest and without lagging the control variables. This is important to test whether the effect is consistent over time once the effect of other factors has been controlled for. The results of these analyses were once again consistent with those presented and provide further support for the robustness of the findings (full results in the Supplemental Appendix Tables A2.1., A2.2., and A2.3.).

Another possible alternative explanation is that the results are due to measures used in the main analysis. Therefore, we ran the analyses using alternative measures for the main variables of interest. First, instead of using the WGI pillars to measure formal institutional quality, we used the Economic Freedom Index (Supplemental Appendix Table A3) and we note that the coefficient although positive did not yield significant effect with respect to the main hypothesis (H1). Second, in place of using the ROE, we used the return on assets (ROA) before and after taxes, and ROE before taxes (Supplemental Appendix Table A4). Third, instead of using the multidimensional measurement of firms’ institutional experience, we ran robustness tests by considering disaggregated effects of institutional intensity, institutional diversity, and institutional distance (Supplemental Appendix Tables A5.1. and A5.2.). Fourth, we ran the analyses by using alternative measures for the control variables (e.g., GDP per capita instead of total GDP; Supplemental Appendix Table A6). Our additional analyses were broadly consistent with those provided in the main models and provided equivalent support for the hypotheses (full results in the Supplemental Appendix).

Additional analyses

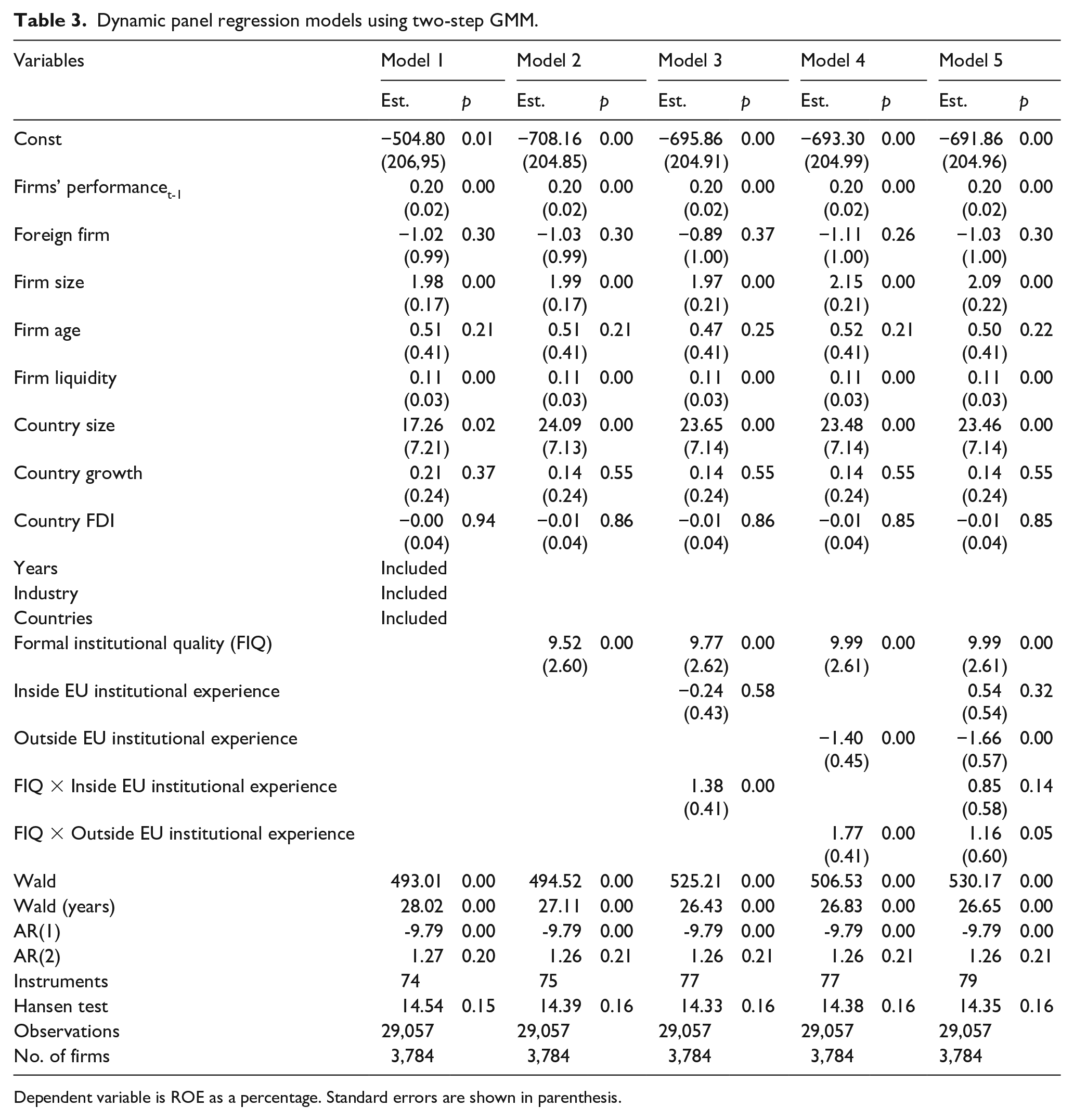

As an additional analysis for H2, we compare the moderating effect of the firm’s institutional experience obtained through being exposed to countries inside the EU and outside the EU on the relationship between formal institutional quality and firms’ performance. Although the results of the main analyses provide support for the notion that firms with higher institutional experience are better able to deal with formal institutional quality, thus enhancing firms’ performance, it is important to further understand whether this effect is contingent on the location that the institutional experience was obtained. Here, we test this assertion (Table 3).

Dynamic panel regression models using two-step GMM.

Dependent variable is ROE as a percentage. Standard errors are shown in parenthesis.

We developed the measure of firm’s institutional experience acquired inside the EU by applying the formula presented in section “Moderating variable” but considering only being exposed to the set of institutional profiles inside the EU. We ran a confirmatory factor analysis between the three dimensions of institutional intensity, institutional diversity, and institutional distance and retained a single factor with a total variance explained of 64.49% (KMO = 0.58, p-value = .00). On the other hand, we measured the firm’s institutional experience acquired outside the EU by applying the formula presented in section “Moderating variable” but considering only being exposed to the set of institutional profiles outside the EU. We ran confirmatory factor analysis between the three dimensions of institutional intensity, institutional diversity, and institutional distance and retained a single factor with a total variance explained of 64.74% (KMO = 0.59, p-value = .00).

The results of these analyses are presented in Table 3. A positive and not significant coefficient of the interaction variable between formal institutional quality and inside EU institutional experience in model 5 (β = 0.85, p-value = .14) does not confirm that firm’s institutional experience acquired inside the EU positively moderates the relationship between formal institutional quality and firms’ performance. On the other hand, a positive and mild significant coefficient of the interaction variable between formal institutional quality and outside EU institutional experience in model 5 (β = 1.16, p-value = .054) does mild confirm (at 10% confidence level) that firm’s institutional experience acquired outside the EU positively moderates the relationship between formal institutional quality and firms’ performance. We find mild support for the assertion that the benefits of being exposed to the heterogeneity of institutional profiles are contingent on the location where the institutional experience was acquired. Nonetheless, we ran robustness tests by considering disaggregated effects of institutional intensity, institutional diversity, and institutional distance (Supplemental Appendix Tables A7.1., A7.2., A7.3., and A7.4.).

Discussion and concluding remarks

Our study offers novel insights on how firms adapt to the formal institutional quality to organize for economic success by using firm’s institutional experience to generate and capture performance advantages. While most previous research focused on arguing that firms will perform well over the long run if they minimize transaction costs (Williamson, 1975), it did not take into account that the performance differences between firms may be further explained by their ability to develop resources and capabilities to benefit from the formal institutional quality (Argyres & Zenger, 2012, 2022; Barney et al., 2023; Hennart & Verbeke, 2022). Our findings corroborate a strong reminder that scholarly attention is in great need to dive deep into firms’ ability to learn from a diversified set of institutional profiles to obtain firms’ institutional experience, thus developing institutional competitive advantages that generate economic advantages. Research on formal institutional quality and firms’ performance that does not account for the combination of institutional perspectives and firm’s resources is thus likely to be incomplete.

We contribute to the IB literature by adding to the ongoing discussion on the effect of institutions on firms’ performance in two ways. First, we contribute to further understand why previous research on this relationship yielded mixed results (e.g., Banalieva et al., 2018; Chari & Banalieva, 2015; Cuervo-Cazurra & Dau, 2009) by adding to the argument that firms differ in their ability to benefit from the formal institutional quality (Cuervo-Cazurra, Mudambi, & Pederson, 2019; Dau et al., 2020; Kafouros & Aliyev, 2016a, 2016b; Kafouros et al., 2022, 2024). We theorize and conclude that the relationship between formal institutional quality and firms’ performance is contingent on firms’ resources such as the level of institutional experience. This evidence is in agreement with the studies that shed additional light on the different abilities of firms to deal with the institutional quality (Dau et al., 2020), such as that larger firms may have a greater ability to internalize inefficient market functions and reduce the economic disadvantages of low-quality formal institutions (Kafouros et al., 2022) and that subsidiary’s intangible assets enhance firms’ growth in high-quality institutions (Kafouros & Aliyev, 2016b). These findings support our theoretical perspective that firms with greater resources benefit from performance-enhancing mechanisms in both low- and high-quality formal institutions.

Second, we contribute to the ongoing debate regarding the importance of developing firm’s institutional experience. We follow a call from Trąpczyński and Banalieva (2016) to further address the debate in the organizational learning literature regarding the mixed findings on how institutional experience affects firm performance. We conclude that firms that develop higher institutional experience are better able to adapt to formal institutional quality and achieve higher firms’ performance. Our findings suggest that firms’ institutional experience can evolve into a firm-specific resource (Perkins, 2014), such as a diversified knowledge, adaptative firm processes, and more arbitrage opportunities (Lundan & Li, 2019), thus granting firms with institutional competitive advantages capable of generating persistent performance advantages (Fuentelsaz et al., 2022). This evidence is in line with studies that show that Multinational Enterprises (MNEs) may learn from prior institutional environments and transfer this knowledge to the home country to better deal with quality of institutions (Fuentelsaz et al., 2022), and that firms that operate internationally acquire market knowledge to respond to institutional reforms at home (Dau, 2013).

In contrast, institutional experience was found to have negative consequences on firms’ performance due to the possible penalty effect from unrelated learning (Perkins, 2014; Trąpczyński & Banalieva, 2016). However, we argue that firms can gain an advantage by exploring a diversified set of institutional profiles, thus achieving institutional competitive advantages by transforming their institutional experience into a firm-specific resource. We argue that firms develop their institutional experience by being exposed to a set of diversified institutional profiles, adapt more efficiently to formal institutional quality and achieve persistent performance advantages over competitors. Our findings confirm that, contrary to previous findings (e.g., Perkins, 2014; Trąpczyński & Banalieva, 2016), learning from being exposed to a diversified set of institutional profiles is beneficial for improving firms’ performance. Also, we move beyond assuming that firms’ internationalization is representative of firms’ institutional experience, by proposing a novel multidimensional approach that reflects both the depth and breadth of firms’ institutional experience (including institutional intensity, institutional diversity, and institutional distance). This is a step forward from the oversimplification of assuming that two firms that have the same number of foreign subsidiaries and operations in the same number of host countries have levels of institutional experience (Lundan & Li, 2019; Wu et al., 2015).

Moreover, our additional findings suggest that the benefits of the firm’s institutional experience are contingent on the location where the firms had subsidiaries. In the case of firms that have their foreign subsidiaries in countries outside the EU, we find mild support for the benefit of institutional experience in the relation between formal institutional quality and firms’ performance, whereas the effect is not significant for institutional experience developed by being exposed to countries inside the EU. Our results do not fully corroborate the idea that institutional divergence is significant across EU countries (Blevins et al., 2016; Jaklič et al., 2020), and that EU firms can benefit from institutional experience obtained by being exposed to EU institutional environments. Nonetheless, the mild support appears to be related to the multidimensional nature of firms’ institutional experience. Our robustness checks suggest that when the moderating variable institutional experience is disaggregated, the institutional diversity outside the EU provides significant support for the moderating effect of firms’ institutional experience, while both institutional intensity and distance show no significant effect (Supplemental Appendix A7.1., A7.2., A7.3., and A7.4.). These findings suggest the need to further understand the complexity of developing firm’s institutional experience, as it is not the question of whether institutional experience matters, but how it matters.

Management and policy implications

For firms’ managers in the EU, we show how firms may adapt to the formal institutional quality to achieve economic success. First, we suggest the firms’ managers to conduct their economic activities in markets with higher formal institutional quality to benefit from reduced transaction costs. Second, we suggest the firms’ managers to further develop their institutional experience by being exposed to diversified set of institutional profiles, particularly by expanding their subsidiaries abroad to countries outside the EU. Therefore, we provide firms’ managers in the EU with additional evidence on how to adapt to the formal institutional quality in the EU.

For the policymakers, we provide additional evidence that higher formal institutional quality has a positive effect on firms’ performance. Thus, we suggest policymakers to develop formal institutional quality by increasing the effectiveness and efficiency of written laws and regulations, together with the formal mechanisms of enforcement. We reinforce the idea that efficient laws and regulations require effective enforcement mechanisms to properly guide economic activity. Therefore, we provide policymakers in the EU with additional evidence on how to efficiently increase the quality of country’s institutional environment to provide effective economic transactions.

Limitations and future research

Future research can build upon the ideas presented here while addressing some limitations of the research. First, our access to the Orbis Europe Database information was limited, thus we could not match the firm’s performance with the formal institutional quality for a longer period of analysis. Thus, future research may find it useful to extend the time window to further capture the institutional transition in the CEE-EU countries. On the other hand, our study provides a static view of the institutional environment, meaning the formal institutional quality that is set in place in each period of analysis. However, recent studies have acknowledged that the institutional change, in terms of pro-market reforms and reversals, and the speed of change, matters for firms’ strategies and performance (Banalieva et al., 2018; Cuervo-Cazurra, Gaur, & Singh, 2019; Fuentelsaz et al., 2022). Therefore, future research may further enhance our knowledge by applying a dynamic view of institutional change in the EU. Also, the existing indicators of formal institutional quality are not always consistent, which prevents more robust conclusions.

Second, our sample only includes publicly traded firms from the EU. Thus, we acknowledge that countries must have, to some extent, effective formal institutions to join the EU. Although EU countries may share similarities in formal institutional quality, the institutional divergence has been found to be significant across EU members (Blevins et al., 2016; Jaklič et al., 2020). We also compared the EU country with the lowest formal institutional quality in 2021 (Greece = 60.9), with emerging economies, such as Russia (61.5), South Africa (59.7), China (58.4), India (56.5), and Brazil (53.4). Thus, we argue that our research sample provides outputs that improve our knowledge on the institutional complexities in the EU. Nonetheless, future research may find it interesting to explore other research settings, such as Emerging Economies, Latin America, and Africa.

Third, we had no information regarding the date of incorporation of each firm’s subsidiaries, thus we did not differentiate between the date of obtaining each institutional experience. It is possible that our results show a slight mismatch between the date of obtaining each institutional experience and the level of formal institutional quality that is set in place. However, we argue that the values of firms’ institutional experience in 2021 are representative because each firm’s internationalization strategy is not likely to significantly change in a time span of 12 years, thus being a significant proxy to measure firms’ ability to develop firms’ institutional experience through being exposed to different sets of institutional profiles. Nevertheless, future research may find it useful to further understand whether the benefit of the firm’s institutional experience on adapting to the formal institutional quality is contingent on the date of obtaining the institutional experience.

Also, we provide future research avenues that do not result from the limitations of this study. It is also important to assess how particular formal institutional dimensions influence and shape global firms (Aguilera & Grøgaard, 2019). Thus, a thicker approach involves looking at the interaction between different formal institutional dimensions (Jackson & Deeg, 2019), meaning the recognition that the impact of one dimension may depend on other institutional dimensions (Aguilera & Grøgaard, 2019; Jackson & Deeg, 2019). This is particularly important as the misalignment and unsynchronized formal institutional dimensions create cognitive complexity (Chan & Du, 2021; Shi et al., 2017), thereby leading to ambiguous and conflicting expectations about future prospects (Shi et al., 2017). In the CEE-EU, the severe institutional development conducted in the absence of sufficiently supporting overall institutional infrastructure (Dau et al., 2020) may have created additional institutional turbulence, thus rendering the institutional environment fragile (Shi et al., 2017). Therefore, future research may further understand the relationship between different formal institutional dimensions and firms’ strategy and performance (Cuervo-Cazurra, Gaur, & Singh, 2019).

We acknowledge the recent discussion on the importance of including informal institutions, as IB research may be missing a large part of the equation and can lead to incomplete and inaccurate findings (Dau, Chacar, et al., 2022; Dau, Li, et al., 2022). The main reason is that formal and informal institutions can vary in how harmonious they are relative to each other, and in the degree of formal institutional quality and the subsequent role that informal institutions take (Dau, Chacar, et al., 2022; Dau, Li, et al., 2022). This is particularly relevant in the CEE-EU where countries share informal connections with prior Soviet Bloc. Therefore, the institutional configuration of a given environment is contingent of its formal institutional quality, informal institutional quality, and the alignment between formal and informal institutions (Dau, Chacar, et al., 2022; Dau, Li, et al., 2022). Hence, future research may further understand how informal institutional quality is defined and what is the subsequent role of informal institutions in the EU.

Supplemental Material

sj-docx-1-brq-10.1177_23409444241301067 – Supplemental material for Institutional experience, formal institutional quality, and firm performance: An analysis of firms from the European Union

Supplemental material, sj-docx-1-brq-10.1177_23409444241301067 for Institutional experience, formal institutional quality, and firm performance: An analysis of firms from the European Union by Alexandre Oliveira, Fernando Carvalho and Nuno Rosa Reis in BRQ Business Research Quarterly

Footnotes

Acknowledgements

We thank the Associate Editor, Elisabet Garrido, for her insightful comments and suggestions that helped us improve the manuscript. We also thank the participants of European International Business Academy (EIBA) and Iberian International Business Conference (IIBC) for their valuable comments and suggestions in the earlier versions of this article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work has been funded by national funds through FCT—Fundação para a Ciência e a Tecnologia, I.P., Project UIDB/05037/2020, Project UIDB/04928/2020, and Project UI/BD/151279/2021 (![]() ).

).

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.