Abstract

Founders of family firms differ from descendants, particularly in terms of affective attachment, cognitive identification, and social concern. This study examines how these generational differences between founder-led and descendant-led family firms affect corporate social responsibility (CSR) decoupling, which is the gap between stated CSR policies on paper and their actual implementation in practice. While decoupling may yield economic benefits by saving on implementation costs if concealed, it can damage socioemotional wealth if revealed. The findings, based on a sample of 3,576 firm-year observations from large firms in the United States, demonstrate that the relationship between family ownership and CSR decoupling is contingent upon family generation. Family ownership decreases CSR decoupling in founder family firms, while it increases CSR decoupling in descendant family firms. It indicates that family firms perceive the benefits and risks of CSR decoupling differently based on the generation of family leaders.

Keywords

Introduction

Research interest in the causes of corporate social responsibility (CSR) decoupling—defined as the gap between avowed CSR policies and actual CSR practices or outcomes—is on the rise (Bothello et al., 2023; Gull et al., 2023; Tashman et al., 2019). Recent studies have identified corporate governance as a crucial aspect for understanding why CSR decoupling occurs (Talpur et al., 2024; Velte, 2023), and have explained CSR decoupling by examining top managers, such as the chief executive officer (CEO), considering factors like CEO overconfidence (Sauerwald & Su, 2019) and CEO power (Shahab et al., 2022). However, the roles of family owners and family managers, who are crucial to corporate governance, remain largely unexplored in the literature (Parra-Domínguez et al., 2021). Although Parra-Domínguez et al. (2021) addressed the differences in CSR decoupling between family firms and nonfamily firms, to our knowledge, no study has yet addressed family firm heterogeneity and the impact of family leadership—defined as strategic control exercised through the involvement of the controlling family in top management (Miller et al., 2013)—on CSR decoupling.

Prior research defines family firms as those “in which the founder or a member of his family by blood or marriage is an officer, director, or blockholder, either individually or as a group” (Anderson & Reeb, 2003; Feldman et al., 2016, p. 434). Family firms are characterized by “significant ownership by a single family and more than one family member (founder or descendants of founders) involved in the firm as officers and/or directors” (Cannella et al., 2015, p. 438). Family firms have unique characteristics, such as a focus on family values and other family centered utilities, that may influence their approach to CSR (Berrone et al., 2010; Hsueh et al., 2023). These traits could influence not only the extent to which family firms engage in CSR activities (Cennamo et al., 2012) but also the degree to which they may decouple their CSR policies from their actual practices (Parra-Domínguez et al., 2021). Decoupling can be a managerial response of corporate leaders to institutional pressures (Westphal & Zajac, 2001; Xu et al., 2024). However, the motivations of family leaders are largely unknown in the literature on CSR decoupling (Talpur et al., 2024), even though they are key decision-makers in a considerable number of firms (Burkart et al., 2003; La Porta et al., 1999).

In this study, we examine the impact of family firm heterogeneity on CSR decoupling through the lens of the socioemotional wealth perspective, thereby elucidating the diverse motivations of family leaders (Gomez-Mejia et al., 2007). Socioemotional wealth refers to “non-financial aspects of the firm that meet the family’s affective needs, such as identity, the ability to exercise family influence, and the perpetuation of the family dynasty” (Gomez-Mejia et al., 2007, p. 106). We use this theory to argue that family leaders may have different affective, cognitive, and social concerns between founder and descendant family members, and that such heterogeneity within family firms affects CSR decoupling. Using a sample of 3,576 firm-year observations from U.S. large firms listed on the Standard & Poor’s 500 (S&P 500) index, we explore the link between family ownership and CSR decoupling and how family leadership affects this relationship differently depending on the generation of family leaders. We specifically address the following research question: How does the relationship between family ownership and CSR decoupling vary with the generation of family leadership? To do this, we categorize family firms into two types: founder-led and descendant-led, based on the generation of family leaders. Then, we investigate how the generational differences in family leadership determine the conditions under which family ownership either alleviates or aggravates CSR decoupling. As a result, we find that family ownership decreases CSR decoupling in founder-led family firms, but increases it in descendant-led family firms. This difference is attributed to the distinct affective attachment, cognitive identification, and social concerns of founders compared with descendants.

This study makes several important contributions to the literature on antecedents of CSR decoupling, in which family firms have been largely overlooked (Talpur et al., 2024). First, it contributes to CSR research by offering new insights into how generational differences within family firms affect CSR decoupling. By highlighting the contrasting dynamics between founder-led and descendant-led family firms, the study emphasizes the critical role of family leadership in shaping CSR decoupling. Second, the study advances family business literature by applying the socioemotional wealth perspective to explain how varying levels of affective attachment, cognitive identification, and social concern among family leaders influence CSR practices. This provides fresh evidence that generational differences in family leadership are key to understanding family firm heterogeneity (Chua et al., 2012; Daspit et al., 2018). Finally, the study offers practical implications for managers of family firms. Our findings suggest that descendant-led family firms need to address the risks of CSR decoupling more proactively to protect their legitimacy, while founder-led firms can leverage their socioemotional wealth to enhance CSR implementation and avoid the superficial adoption of CSR policies.

Theoretical framework and hypotheses

This study focuses on how CSR decoupling may vary among family firms, specifically those where members of the founding family are involved in top management, based on the generation of their family leaders. For this purpose, we distinguish between founder-led family firms, which are those where the CEO is the founder of the firm, and descendant-led family firms, which refer to those where the CEO is a descendant of the founder. Our distinction between founder-led and descendant-led family firms is consistent with previous studies that have differentiated types of family CEO firms according to whether the CEO is a founder or a descendant (Anderson & Reeb, 2003; Feldman et al., 2016; Villalonga & Amit, 2006).

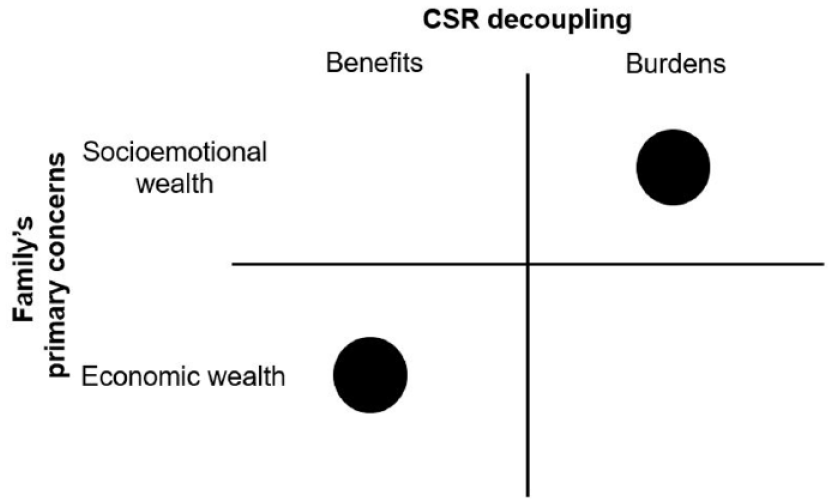

We first propose that the controlling family’s interpretation of the returns and risks from CSR decoupling varies with the family governance of the family firm. Family governance consists of two distinct dimensions: family ownership and family management (Block & Wagner, 2014; Miller et al., 2013; Villalonga & Amit, 2006). We emphasize that these two dimensions have different implications on the benefits and burdens that firms may find from CSR decoupling. Family ownership inherently represents the financial interests of the controlling family. However, in addition to this financial concern, family management demonstrates nonfinancial concerns such as “the ability to exercise authority” and “the perpetuation of family values” (Gomez-Mejia et al., 2007, p. 108). When the financial concern is prioritized over nonfinancial concerns, firms are likely to opportunistically perceive more returns than risks from CSR decoupling, which can save the costs of substantive CSR implementation while seeking legitimacy from symbolic CSR adoption. In contrast, when the nonfinancial concerns are valued over the financial concern, firms become more vulnerable to the risks of CSR decoupling due to potential damage to the family’s socioemotional wealth. Figure 1 depicts our basic theoretical framework.

Theoretical framework.

Family ownership

As a baseline, we posit that family ownership per se increases firms’ CSR decoupling. This is consistent with agency theory (Eisenhardt, 1989; Fama, 1980; Jensen & Meckling, 1976; Mitnick, 1973, 1975; Ross, 1973), which “assumes that owners are atomistic and homogeneous with a single preference—(economic) wealth maximization” (Cannella et al., 2015, p. 436, parentheses added). Although family owners are more heterogeneous than others in their preferences, they may prioritize financial interests over socioemotional interests as they acquire more stock ownership, which forms the basis of their economic wealth (Shi et al., 2022; Souder et al., 2017).

Previous research in the socioemotional wealth perspective suggests that the perception of decoupling risk to socioemotional wealth and the prioritization of financial interests and socioemotional interests may vary depending on the type of family involvement (Alessandri et al., 2018). We extend this idea to contend that family involvement in ownership and managerial leadership has a contrasting effect on CSR decoupling. When the controlling family is involved in ownership only, financial interests may take precedence over socioemotional concerns. In contrast, when family members engage in both ownership and leadership, socioemotional concerns are likely to overshadow financial interests (Park, 2019; Park & Kim, 2019). Family members take part in top management to establish and maintain the socioemotional wealth of the controlling family (Liang et al., 2014, p. 129).

Family ownership per se increases the economic wealth consideration of controlling family, thus heightening the tensions between socioemotional goals and economic goals of the family firm (El Ghoul et al., 2016). Even if CSR activities can benefit the controlling family’s socioemotional wealth through a good reputation, CSR activities might not look attractive to family owners if the costs of implementing CSR outweigh the expected socioemotional benefits (Block & Wagner, 2014; Labelle et al., 2018). Rather, family principals can be inclined to choose CSR decoupling as a risky but less costly option because the symbolic adoption of CSR activities can duplicate such benefits while it can save the costs of substantive implementation. Due to similar reasons, Park and Kim (2020) found that large family firms in South Korea with high levels of family ownership tend to exhibit greater levels of CSR decoupling. Therefore, we propose that family ownership has a positive impact on CSR decoupling:

Founder-led family firms

Drawing upon the socioemotional wealth perspective (Gomez-Mejia et al., 2007, 2011), we assume that family firms use corporate social practices as “a means of enhancing the family’s noneconomic utilities and/or preventing losses of socioemotional wealth” and this tendency is particularly salient “when the family controls large stakes in the firm and (when) the (family) CEO has employment security” (Berrone et al., 2010, p. 91, parentheses added). Prior research indicates that firms led by family CEOs are more likely to prioritize the preferences of the controlling family in responding to institutional pressures on CSR (Berrone et al., 2010). However, the influence of coercive, mimetic, and normative isomorphic pressures on firms can vary depending on how family leaders perceive the importance of responding to these pressures (Arregle et al., 2007). In this study, we argue that there is an important distinction between founder-led family firms and descendant-led family firms in a way that the former is more likely to attenuate the positive effect of family ownership on CSR decoupling, while the latter is likely to amplify it. We posit that founders and descendants frame costs (losses) and benefits (gains) of CSR decoupling differently according to their affective, cognitive, and social stakes. Founders of the family business are unique and distinctive from other and descendant family members (Block, 2012; Miller et al., 2007). We have identified three distinct factors that differ between founder and descendant family CEOs: affective attachment, cognitive identification, and social concern.

First, founder CEOs vary from other family members in terms of affective attachment based on both physical and psychological commitment to their business (Fang et al., 2018; Mariotti et al., 2021). Founders invest all their efforts into their firms, and these inputs entail not only economic or physical attachment but also emotional or psychological attachment. Thus, founder family CEOs are more likely to exhibit affective commitment, while descendant family CEOs are more likely to display normative or continuance commitments (Allen & Meyer, 1990; Sharma & Irving, 2005). Affective commitment is characterized by a strong emotional desire to do something, while continuance and normative commitments are driven by needs and obligations, respectively (Allen & Meyer, 1990). Palmer and Barber (2001) further note that founder family CEOs exhibit distinctive affective attachment compared with later generation owner-CEOs. As a result, founders are less likely to engage in CSR decoupling, even if the family has a high ownership stake, due to their deep devotion to their own business. This strong attachment may amplify the perceived risk of CSR decoupling, which could potentially harm their reputation when disclosed.

Second, founders are unique in the cognitive identification with their founding firms. The identity of a founder often overlaps significantly with that of his or her founding firm. Family members identify themselves with their family firms, and such identification is most salient for founders. This is consistent with the literature, which states that “the founder’s identity is tightly linked to that of the organization” (Dobrev & Barnett, 2005, p. 435) and “founder view the firm as an extension of themselves” (Cannella et al., 2015, p. 439). Bingham et al. (2011) also note that “founders—and particularly those of family firms—see their firms as extensions of themselves and their families” (Bingham et al., 2011, p. 571). Founders often act as stewards and pursue intrinsic rewards (Wasserman, 2006). For this reason, it has been argued in previous studies that founders tend to prevent their firms from becoming involved in socially irresponsible events (Dyer & Whetten, 2006). This is evident in social identity theory (Ashforth & Mael, 1989; Tajfel, 1981) and the theories of organizational identity and identification (Albert et al., 2000; Albert & Whetten, 1985; Dutton & Dukerich, 1991; Dutton et al., 1994). These theories indicate that people are more likely to identify themselves with their affiliated organizations when the perceptions of in-group members stem from distinct and prestigious self-concepts and those organizations are salient in the awareness of out-groups. In both aspects, founder family CEOs are most likely to identify themselves with their founding firms because founders tend to equate themselves with their firms, and others surrounding founders also perceive them in the same way. Thus, we predict that such strong identification of founder family CEOs weakens the positive effect of family ownership on CSR decoupling.

Third, founder family CEOs differ from other CEOs, including descendants, in terms of social concern and prioritization of business goals (Meier & Schier, 2022). It is also conceivable that founders are relatively more prudent in social commitment than other family members. The primary focus of founders on firm growth and maintaining control may lead them to view CSR as a secondary concern (Dick et al., 2021). As a result, the likelihood of CSR decoupling may decrease in founder-led family firms, even if family ownership is high, as CSR decoupling is more likely to occur when there is a combination of high CSR adoption and low CSR implementation (Roulet & Touboul, 2015).

In summary, founders of family firms differ from other family members in terms of affective attachment, cognitive identification, and social concern. These distinctive characteristics of family firm founders suggest that the positive effect of family ownership on CSR decoupling is weaker in founder-led family firms:

Descendant-led family firms

In the previous section, we argued that founder family CEOs could mitigate the positive effects of family ownership on CSR decoupling, based on three factors: affective attachment, cognitive identification, and social concern. In this section, we will discuss how these three factors may differ in descendant family firms and how such differences may affect CSR decoupling in the opposite direction. We have two reasons for this argument.

First, descendant CEOs have significantly lower affective and identity stakes in their inherited firms compared with the founder CEOs, who have “significant psychic income” based on a strong identification with their firms (Cannella et al., 2015, p. 438). This fundamental difference is why we expect that the influence of descendant leadership on family firms in terms of CSR decoupling would differ from that of founder leadership. In fact, as the firm progresses through successive generations, the socioemotional wealth of the family often changes between the founder stage and the succession stage (Martin & Gomez-Mejia, 2016). Many societies also hold a similar belief that the wealth created by founders does not sustain beyond three generations (e.g., “clogs to clogs”). One reason for this phenomenon is explained by Fiss and Zajac (2004) as follows: “Later generations may be less motivated or able to run the family business, and larger families in succeeding generations are often marked by conflict due to different interests and values” (Fiss & Zajac, 2004, p. 510). They also point out that “[i]n those later generations, the family may be held together by nothing more than their common financial interests” (Gersick et al., 1997, p. 219; as cited in Fiss & Zajac, 2004, p. 510). Similarly, Bertrand and colleagues also argue that descendants facilitate the decay of family controlled business groups in Thailand (Bertrand et al., 2008). Thus, we expect that the positive effect of family ownership on CSR decoupling is likely to be more prominent in descendant-led family firms.

Second, succeeding generations of family CEOs have different social concerns compared with the founders. As mentioned earlier, founder family CEOs are more likely to focus on building a reputation based on business goals (Dick et al., 2021; Villalonga & Amit, 2006). On the contrary, descendant family CEOs are often faced with a legitimacy deficiency and may be more inclined to prioritize overcoming this deficiency (Jeong et al., 2021). From a stakeholder perspective, heirs of family firms may be perceived as less competent and less professional (Jaskiewicz et al., 2015). To overcome this liability, descendants need to establish more legitimacy than their founders (Block & Wagner, 2014). As a result, it is highly likely that descendant family CEOs may exaggerate their firms’ CSR efforts to gain legitimacy and support from stakeholders. This inference can be drawn from the fact that firm managers often strive to narrow the legitimacy gap between their firms and peer firms in the same industry, particularly when the legitimacy deficiency is more severe (Berrone et al., 2013). However, due to the potential lack of charismatic leadership qualities among descendants, they may face greater challenges in pursuing their social goals compared with their ancestors. This inconsistency between the willingness and ability of descendant family leaders may further enhance the positive effect of family ownership on CSR decoupling:

Method

Sample and data

Our baseline sample was composed of the S&P 500 firms as of 31 December 2001 with an observation period from 2002 to 2017. The Wharton Research Data Services (WRDS) provided Compustat Capital IQ, which we obtained S&P 500 firms’ balance sheets and income statements for measuring control variables. Based on this database, we merged the family data of S&P 500 firms (hereafter, family data), which was initially hand-collected for Anderson and Reeb (2003) and updated thereafter to 2017 by Ronald C. Anderson. We collected the information necessary to construct CSR decoupling from Thomson Reuters ESG (environmental, social, governance) data (hereafter, ESG data), formerly known as ASSET4 and currently labeled as LSEG ESG data, also recognized as Refinitiv ESG data. Thomson Reuters is widely recognized as one of “the most reliable CSR data providers,” with its highly specialized researchers (Timbate, 2023, p. 333). It delivers “one of the most comprehensive ESG databases in the industry and covers over 80% of the global market cap” (Hou et al., 2023, p. 5). We integrated this ESG data into the merged dataset comprising Compustat data and family data. We then removed observations with a missing value, reducing the final sample size to 3,576 firm-year observations (282 firms). In our sample, family led firms are 380 observations, comprising 10.6% of the total sample. Specifically, of the family led firms, 197 (5.5%) were led by the firm’s founders, while 183 (5.1%) were led by descendants of the founding family. The number of family led firms varies from year to year. On average, there were 13.3 founder-led family firms and 12.2 descendant-led family firms each year. We chose the period from 2002 to 2017 because Thomson Reuters started providing ESG data in 2002, and this dataset ended in 2018 when Refinitiv acquired the data, ceasing the provision of raw data for measuring CSR decoupling.

Variables and measures

CSR decoupling

Following Roulet and Touboul (2015), we measured CSR decoupling as the ratio of adopted CSR policies to implemented CSR policies. We calculated CSR decoupling as the inconsistency between CSR adoption and CSR implementation, which were derived from 30 sub-ratings. These sub-ratings consisted of 15 sub-ratings related to CSR adoption and 15 sub-ratings related to CSR implementation; 15 sub-ratings were drawn from the environmental category (3), social category (7), and corporate governance category (5), respectively. To be specific, we used 15 items from ESG data to investigate the adoption of CSR policies (Table 1), and another 15 items to assess the implementation of the adopted CSR policies (Table 2).

Items for CSR adoption.

Items for CSR implementation.

Family ownership

Following Anderson and Reeb (2003) and other family business research (e.g., Kim et al., 2008; Luo & Chung, 2013), we measured family ownership as fractional equity holdings of the founding family (Anderson and Reeb, 2003). In line with Anderson et al. (2009), we did not rely on a minimum ownership threshold and used a continuous measure of founder or heir ownership. In our sample, the average family ownership among founder-led family firms was 0.1445 (14.45%), while the average family ownership among descendant-led family firms was 0.1469 (14.69%).

Moderating variables

Founder-led family firms were measured as 1 if a founder family CEO controls the firm, and 0 otherwise. Descendant-led family firms were coded as 1 if a descendant family CEO manages the firm at the helm, and 0 otherwise.

Control variables

We controlled for several factors that can affect CSR decoupling. Due to the paucity of the past research on CSR decoupling, we included firm-level factors that have found in the previous studies to have an impact on CSR. First, we included firms’ CSR strengths and CSR concerns in our models because of their potential strong influences on the following year’s CSR decoupling. We measured CSR strengths and CSR concerns as Thomson Reuters ESG Score and the reversed values of ESG Controversies Score, respectively (Park, 2018). We controlled for firm age because younger firms are more dependent on external resources, thereby suggesting a negative relationship between firm age and CSR adoption (Höllerer, 2013). We measured firm age as years since the founding year. Firm size was also included as a natural logarithm of sales because of its positive effect on CSR decoupling in the previous research (Tashman et al., 2019). For the same reason, we controlled for research and development (R&D) intensity and organizational slack, which has been reported as having statistically significant negative and positive effects, respectively, on CSR decoupling (Tashman et al., 2019). We measured R&D intensity as the ratio of R&D expenditures to sales (Kim et al., 2008). As an organizational slack measure, we used inverse values of the ratio of total liabilities to total shareholder equities (Patel & Chrisman, 2014). We also considered other types of organizational slack such as absorbed slack—the ratio of selling, general, and administrative expenses to sales—and unabsorbed slack—the ratio of current assets to current liabilities. Among three types of slack, we included potential slack only because, after testing hypotheses, we found that including three slack measures were redundant for a parsimonious model. We choose potential slack because it had the fewest missing values. Instead, we included debt ratio, measured as the ratio of total liabilities to total assets. We controlled for advertising intensity—the ratio of advertising expenditure to sales—and return on assets (ROA)—as the ratio of net income to total assets—because of their close relationship to firms’ CSR engagement (McWilliams & Siegel, 2000). In addition to accounting performance (ROA), we also controlled for Tobin’s Q, an indicator of financial market performance. We measured Tobin’s Q as “the ratio of the market value of assets to the book value of assets,” defined by Gompers et al. (2003, p. 127). Finally, we included CSR decoupling as an independent regressor with a 1-year lag from the dependent variable (CSRD t+1) to control for autocorrelation in panel data. Using a lagged dependent variable has also an advantage that it can account for the path dependence in CSR decoupling (see Dokko & Gaba, 2012: 573). Year fixed effects were included in all models to control for annual trends that could influence the level of CSR decoupling (Berrone et al., 2013). By using fixed effects models, we also controlled for unobserved heterogeneity among industries. The dependent variable was measured at t+1 and other all other variables, including explanatory variables and moderators, were measured at t so that a reverse causality concern was addressed.

Results

Table 3 summarizes our variables and correlations. To test for multicollinearity, we ran variance inflation factors (VIF). The mean (1.34) and the maximum VIF (1.88, firm size) were much lower than the cutoff (10) (Greene, 2003), indicating that multicollinearity is not a problem.

Descriptive statistics and correlations.

N = 282 firms (3,576 obs.). All correlations above or equal to| 0.03| are significant. p < .05 for two-tailed test.

A Hausman test rejected the random effects specification (χ2 = 620.72, p < .01), rendering fixed effects models appropriate (

Results of fixed effects panel data regression models for CSR decoupling t+1.

Unstandardized coefficients are reported with standard errors in parentheses.

p < .001, **p < .01, *p < .05, †p < .10. Two-tailed tests.

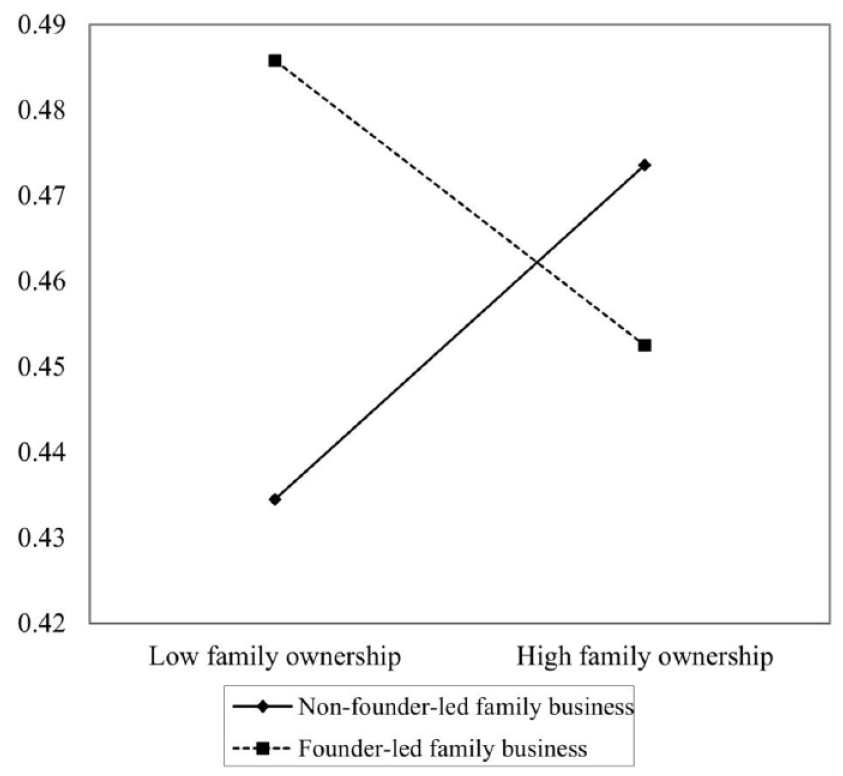

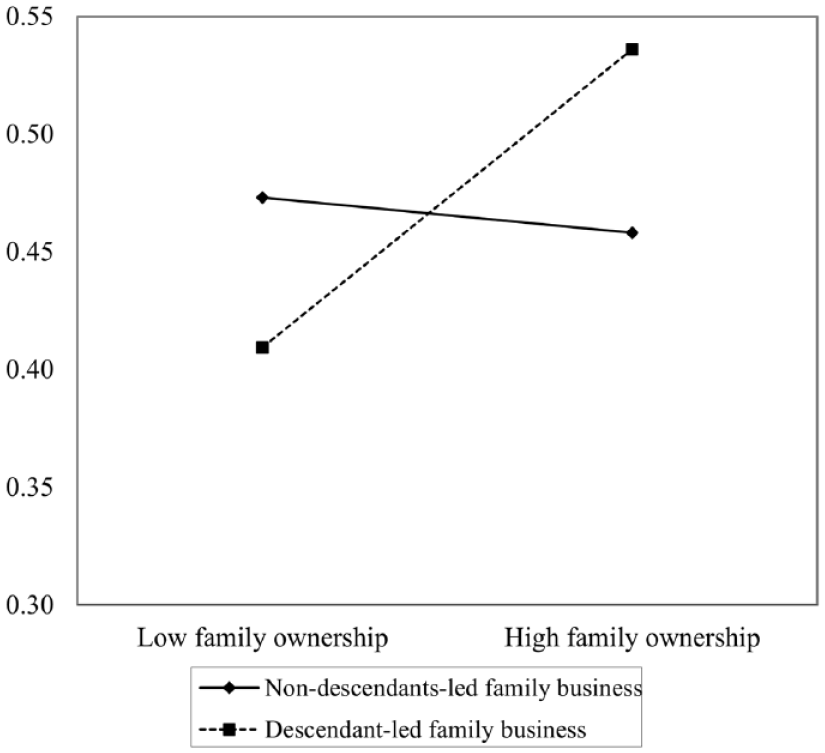

The first hypothesis predicts that family ownership has a positive relationship with CSR decoupling. The result of Model 2 shows a positive and insignificant coefficient on family ownership (b = 0.13, p = .50). Thus, Hypothesis 1 is unsupported. In our second hypothesis, we expect that this positive relationship is weaker in founder-led family firms. Model 4 indicates a negative and significant effect of an interaction term between the family ownership and the founder family CEO (b = 0.20, p = .00). Therefore, we find a strong support for Hypothesis 2. Our third hypothesis posits that the positive effect of family ownership on CSR decoupling is more salient in descendant-led family firms. As shown in Model 5, the coefficient of the interaction term between family ownership and descendant family CEO is positive and significant at p < .1 (b = 0.39, p = .08), indicating marginal support for Hypothesis 3. Model 6 is the full model with all main variables and interaction terms. The above results remain stable and significant. Figures 2 and 3 represent the graphical representations of the results of testing Hypothesis 2 and 3, respectively. In both figures, we use two standard deviations above and below mean (Dawson, 2014), lending credence to both hypotheses.

Moderation effect of founder-led family business.

Moderation effect of descendant-led family business.

Discussion

This study investigates the impact of generational differences between founder-led and descendant-led family firms on CSR decoupling, which refers to the disparity between a company’s CSR policies on paper and their actual implementation in practice. The study analyzes data from a sample of large U.S. companies and finds that the relationship between family ownership and CSR decoupling is contingent on family generation. Specifically, family ownership has a diminishing effect on CSR decoupling in founder-led family firms, whereas it has an amplifying effect in descendant-led family firms. We argue that this contrasting effect of family ownership on CSR decoupling between founder-led and descendant-led family firms is due to the distinctive affective, cognitive, and social aspects of founder-led family firms.

Discussion of results

We propose that family ownership increases CSR decoupling overall (Hypothesis 1). While the results indicate a positive but insignificant relationship between family ownership and CSR decoupling, this suggests that family ownership alone may not be a primary driver of decoupling. This finding is consistent with prior literature, which has suggested that family firms tend to prioritize socioemotional goals, such as maintaining the family’s legacy, over short-term financial gains (Gomez-Mejia et al., 2007).

Founder-led family firms, we hypothesize, weaken the positive impact of family ownership on CSR decoupling (Hypothesis 2). Our results strongly support this, showing a significant negative interaction between family ownership and founder leadership. Founders, who often see their firm as an extension of themselves, are more likely to implement CSR policies substantively to protect their personal and family reputation. Their higher affective attachment to the firm also aligns with past research, which emphasizes the importance of personal identification with the business in reducing decoupling tendencies (Bingham et al., 2011).

We also predict that descendant-led family firms strengthen the positive relationship between family ownership and CSR decoupling (Hypothesis 3). The results provide marginal support for this expectation, revealing that descendants, who may lack the same emotional attachment and face greater legitimacy pressures, are more prone to symbolic CSR adoption. This aligns with research suggesting that descendants may exaggerate CSR efforts to enhance their legitimacy (Block & Wagner, 2014).

This variation in CSR decoupling between founder-led and descendant-led family firms reflects the broader challenge of balancing family interests with business objectives. Family firms often seek to “balance the needs of the family with the ‘strategic’ needs of the business” (O’Gorman, 2012, p. 387), which presents unique challenges for family leaders (Gomez-Mejia et al., 2018). For instance, they may prioritize preserving the family’s reputation or legacy over profit maximization, influencing the extent to which they decouple CSR policies from daily activities (Combs et al., 2023). Despite this, most research on CSR decoupling has focused on nonfamily firms. An exception is Parra-Domínguez et al. (2021), who found lower CSR decoupling in family firms but did not address generational differences in leadership (Fernández Méndez et al., 2024). Thus, the literature has yet to fully consider family firm heterogeneity, leaving it unclear how CSR decoupling varies across family firms. This study finds that family ownership’s effect on CSR decoupling differs between founder-led and descendant-led firms, offering insights into family firm heterogeneity.

Theoretical implications

Our findings make an important contribution by challenging previous research on CSR decoupling that has treated family firms as a homogeneous group, having uniformly lower levels of CSR decoupling (Parra-Domínguez et al., 2021). Tackling this unrealistic assumption, this study demonstrates that the impact of family business on CSR decoupling varies depending on the degree of family involvement in ownership and the generational heterogeneity of family leadership. This highlights the importance of adopting a more nuanced perspective on family firms when examining their CSR practices (Mariani et al., 2021; Marques et al., 2014). Given this point, this study contributes to understanding how family firms can effectively engage in CSR. In addition, studying CSR decoupling in family firms can help shed light on the unique characteristics and challenges these firms face in implementing CSR. Specifically, our contribution is threefold.

First, our study contributes to the literature on CSR decoupling, which refers to “a symbolic strategy whereby firms overstate their CSR performance in their disclosures to strengthen their legitimacy” (Tashman et al., 2019, p. 154). Although such inflated or exaggerated CSR prevails in many firms (Siano et al., 2017), little has been known about why some firms decouple declared CSR policies from daily practices, while others integrate CSR policies into the actual implementation. Furthermore, previous studies have not adequately addressed the heterogeneity across family businesses in relation to the factors that contribute to CSR decoupling. In previous studies on CSR decoupling, family governance has been solely considered as a dummy variable—specifically, categorized into family business and nonfamily business (Parra-Domínguez et al., 2021). Parra-Domínguez and colleagues (2021) found that family firms exhibit lower CSR decoupling compared with nonfamily firms. They attributed this result to the fact that family firms engage less in decoupling due to “the risks that it may entail for their image and legacy, opting instead for a stronger connection between what they do and what they say” (Parra-Domínguez et al., 2021, p. 40). Notably, recent review papers have pointed out the significant absence of discussion around family leadership in the literature on CSR decoupling (Talpur et al., 2024; Velte, 2023). We fill this research gap by focusing on family firms and their generational diversity. Our research makes a unique theoretical contribution by employing the socioemotional wealth perspective (Gomez-Mejia et al., 2007, 2011) to reveal the underlying psychological, economic, and social factors that contribute to the varying degrees of CSR decoupling observed in different companies. Previous research has only explored the differences in CSR decoupling between family firms and nonfamily firms, thereby providing a limited understanding of the heterogeneity within family firms in terms of CSR decoupling (Diéguez-Soto et al., 2024; Mariani et al., 2021; Parra-Domínguez et al., 2021). Previous studies discuss certain dimensions of socioemotional wealth such as family control, family identity, and the renewal of family bonds to the firm through dynastic succession as key characteristics that distinguish between family firms and nonfamily firms (Firfiray & Gomez-Mejia, 2021). Our results provide a unique insight into the socioemotional wealth perspective by suggesting that socioemotional wealth may not only vary across family firms but also within the same family firm, depending on the generation of family leadership.

Second, we contribute to the literature on family business and CSR (Diéguez-Soto et al., 2024; Hsueh et al., 2023; Mariani et al., 2021; Preslmayer et al., 2018) by explaining how the socioemotional wealth of family, which differs between founder and later generations, influences CSR decoupling. This study challenges the traditional assumption that family ownership unilaterally drives socioemotional wealth in family businesses (Souder et al., 2017). Our findings reveal that family ownership is not always positively related to CSR, as commonly assumed in prior research (Berrone et al., 2010). Rather, family leadership can significantly moderate the relationship between family ownership and CSR decoupling, indicating the importance of considering both family ownership and leadership in understanding socioemotional wealth and its influence on CSR. A firm is often treated as a separate entity from the family, which can be defined as “two or more people related by birth, marriage, or adoption residing in the same unit” (Welsh, 2012, p. 557; Smith & Hamon, 2017, p. 7). In reality, however, many firms are owned or/and managed by a controlling family as “an intergenerational social group organized and governed by social norms regarding descent and affinity, reproduction, and the nurturant socialization of the young” (Smith & Hamon, 2017, p. 80; White, 1991). In this sense, many firms are embedded in familial contingencies (Aldrich & Cliff, 2003; Steier et al., 2009). However, previous studies in the literature on family business and CSR largely assume that family firms are homogeneous in terms of socioemotional wealth (Diéguez-Soto et al., 2024). This literature remains silent about whether and how the socioemotional wealth of controlling families differs across the generation of family leaders, and how this generational difference in family leadership can bring about different results in the firm’s CSR activities. This is surprising given that “[n]ot only do SEW priorities vary among firms and even family members within a firm, they also may vary across the life cycle (and generation) of a family in its firm (leadership)” (Miller & Le Breton-Miller, 2014, p. 714, parentheses added). This study addresses this gap by providing theoretical reasons for the generational differences across family firms with regard to CSR. In this way, we offer a nuanced understanding of family business, which is one of the most complex organizational forms (Craig & Moores, 2006; Neubauer & Lank, 1998). The complexity of family business has been long acknowledged since the emergence of family business research. The first article of Family Business Review, an academic journal dedicated to family research, pointed out this issue in its first sentence: “[p]eople seem to understand what is meant by the term family business, yet when they try to articulate a precise definition they quickly discover that it is a very complicated phenomenon” (Lansberg et al., 1988, p. 1). This study sheds new light on the complex nature of family businesses and their implications for CSR.

Third, our study contributes to a deeper understanding of the heterogeneity within family businesses (Chua et al., 2012; Daspit et al., 2018; Marques et al., 2014). While previous studies have primarily focused on differences between founder- and descendant-CEO family firms in terms of firm performance (Anderson & Reeb, 2003; Villalonga & Amit, 2006) or international business strategies (Fang et al., 2018; Mariotti et al., 2021), as far as we are aware, there has been no research dedicated to exploring potential differences in CSR decoupling between founder- and descendant-led family firms. The differences between family firms and nonfamily firms have gained increasing scholarly attention in the literature on family business and CSR (Dick et al., 2021), and socioemotional wealth has been argued as the main source of family firm distinctiveness (Diéguez-Soto et al., 2024). Although the literature documents the heterogeneity in socioemotional wealth across family firms, little is studied about the generational differences between founder-led family firms and descendant-led family firms in terms of CSR. Extending the socioemotional wealth perspective (Gomez-Mejia et al., 2007, 2011), we provide an explanation of why founder-led family firms differ from descendant-led family firms in terms of CSR decoupling. We also distinguish between family ownership and family management (Sciascia & Mazzola, 2008; Villalonga & Amit, 2006). In doing so, we explicate the heterogeneity among family firms and its effects on CSR decoupling.

Managerial implications

Family business is ubiquitous and the most prevalent organizational form across the world. It is approximately “95 percent of all U.S. companies (that) are either family-owned or family-controlled” (Lansberg, 1983, p. 29, parentheses added). The literature further states that “approximately 14.4 million of the 15 million businesses in the United States are family-controlled” (Beckhard & Dyer, 1983, p. 5) and that “[m]ost firms in the United States are family businesses—organizations where two or more extended family members influence the direction of the business through the exercise of kinship ties, management roles, or ownership rights” (Tagiuri & Davis, 1996, p. 199). Despite this, empirical studies on family leaders still remain scarce and scattered. As a result, firm managers have limited knowledge about the roles of different family leadership, particularly in the strategy implementation regarding CSR. In response, our study provides an important practical implication to understand how family leadership and its generational differences matter for symbolic or substantive processing of the stakeholder demands. In this way, this study helps advance our understanding of the complex relationship between family ownership, leadership, and social responsibility and provides insights for practitioners. By considering the different motivations and priorities of different generations within the family, practitioners can better understand the factors that influence CSR decoupling in family businesses and develop strategies to encourage more consistent and effective CSR practices.

Potential limitations and future research

Despite the aforementioned contributions, this study has some limitations that can be addressed in future research. First, we did not incorporate the effect of founder imprints into our arguments (Hollander & Elman, 1988; Schein, 1983; see also Adams et al., 1996, pp. 159–160). However, it is reasonable to consider that certain family firms may be influenced by founder imprints, leading to relative stability in terms of socioemotional wealth across multiple generations. In fact, several scholars noted “the impact that an organization’s founders have on firm values” (Bingham et al., 2011, p. 571), suggesting a possible avenue for future research to explore which descendant-led family firms are more similar to founder family firms.

Second, this study focuses on the policy-practice CSR decoupling, which arises from the gap between adopted CSR policies and actual CSR implementations (Crilly et al., 2012; Meyer & Rowan, 1977). While our concept and measure of CSR decoupling is well suited to this purpose (Meyer, personal correspondence, April 4, 2021), we encourage future researchers to address means-ends CSR decoupling that occurs in the gap between implemented CSR practices and intended outcomes (Bromley & Powell, 2012). Firms often fail to internalize CSR policies even though they intend to do so (Boiral, 2007; Wijen, 2014). One problem may be attributed to compartmentalization or endemic reform (Bromley & Powell, 2012). While CSR policies are mainly initiated by top managers (e.g., CEO or chief sustainability officer) (Kanashiro & Rivera, 2019) or the CSR department (Crilly et al., 2012), middle managers have considerable agency in their actual implementation. While the oversight capacity of CSR initiators is limited to control over subunits (Wickert et al., 2016), CSR implementers in subunits are more motivated by personal motives—for example, salary, promotion—or interests of their units than those of an entire organization (see Simon, 1947/1997, p. 287). Managers often identify themselves with their sub-goals rather than organizational goals. The problem is that “despite corporation-wide policy in each firm, implementation is often left to the discretion of business unit and line managers” (Crilly et al., 2012, p. 1441). Even if middle managers and rank-and-file employees conform to top–down CSR policies, their faint CSR efforts may result in unintentional decoupling (Gondo & Amis, 2013) or, at best, instrumentalism if they lack cooperation and conscious reflection during CSR implementation (Gondo & Amis, 2013). Although “[c]ommitment to the tools of action is indispensable,” “the pursuit of the goals which initiated action demands continuous effort to control the instrument it has generated” (Selznick, 1949/1966, p. 258). Thus, firms need to develop an aligned and well-coordinated strategy for substantive CSR implementation. Delmas and Burbano (2011, p. 84) also point out that “the adjustment and alignment of employee incentives is an important means to reducing the likelihood of greenwashing.”

Last, we note that this study examines the generational differences of family firms within a single country, the United States. Future studies can test and improve the generalizability of our findings in the different contexts. Thus, we encourage future studies to utilize a multi-country sample and to explore the boundary conditions of our findings.

Conclusion

In this study, we examine the effects of family ownership and leadership on the gap between a firm’s CSR rhetoric and reality. By exploring generational differences, we develop and test hypotheses on how family ownership influences CSR decoupling in founder-led versus descendant-led firms. Specifically, we propose that these generational differences moderate the relationship between family ownership and CSR decoupling, challenging the assumption that all family firms are less likely to decouple than nonfamily firms. Our findings reveal a contrasting effect of family ownership between founder-led and descendant-led family firms, attributed to differences in affective attachment, cognitive identification, and social concern. This suggests that socioemotional wealth varies across family firms and generations, offering insight into how the controlling family shapes CSR decoupling based on the generation of family leaders.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.