Abstract

Despite the importance of Corporate Social Responsibility (CSR) firm controversies, little is known about their effect on institutional investors. We study the most important institutional investors worldwide: pension funds and mutual funds. The separation between fund management and ownership raises the need to examine how fund managers and fund participants react to investee-firms’ CSR controversies. Considering the conventional/Socially Responsible Investment (SRI-fund nature, we find that investee-firms’ controversies diversely affect fund performance, depending on the controversy type. Furthermore, participants and managers of SRI pension and SRI mutual funds display a passive behavior toward controversies. These attitudes are consistent with enduring behavior and continuity investment policies, such as amending/controlling CSR-firm controversies. In contrast, conventional pension-fund and conventional mutual-fund participants seem guided by traditional investment rules to deal with unsatisfactory situations and respond to controversies after managerial decisions regarding these events with negative reactions. Finally, firms developing CSR-engagement strategies may soften market and managerial reactions toward controversies. Nonetheless, symbolic CSR-engagement practices arouse participants’ responses.

Introduction

The growth of Socially Responsible Investment (SRI) among institutional investors has increased the demand for investee-firms’ Corporate Social Responsibility (CSR) information, including CSR controversial events (Vollero et al., 2019).

CSR controversies are actions or incidents experienced by firms that can negatively impact stakeholders and the environment (Sustainalytics, 2014). Controversies are usually classified as environmental, social, or governance (ESG) events due to their diversity; for example, toxic waste spills are environmental controversies, human-rights abuses are social controversies, and accounting frauds or corrupt CEOs are governance controversies, among many others (Nugent et al., 2021). Various CSR-firm controversies have drawn media attention in recent decades (Enron, HealthSouth, Parmalat, Shell, Siemens AG, Tyco, or WorldCom controversies, among others) due to their large and diverse consequences on multiple stakeholders. The following press release on Enron’s controversy exemplifies an accounting controversy: The Securities and Exchange Commission today initiated civil charges against Kenneth L. Lay, former Chairman and Chief Executive Officer of Enron Corp., for his role in a wide-ranging scheme to defraud by falsifying Enron’s publicly reported financial results and making false and misleading public representations about Enron’s business performance and financial condition. (SEC, Washington, DC, 8July 2004)

1

The demand for investee-firms’ CSR controversial information by institutional investors reveals an increasing active shareholding in investee firms, amending less active past behavior (Jansson, 2013). Thus, the increasing concern and commitment of institutional investors toward these issues make it necessary to examine the repercussions of CSR-firm controversies on these investors. Although previous literature analyzes the effect of CSR-firm strategies on institutional investors (Chen et al., 2020; Erhemjamts & Huang, 2019), the specific impact of CSR controversies on institutional investors has not been analyzed, as far as we are aware, since it is accepted that controversies affect shareholders via prices (Flammer et al., 2021). Moreover, little is known about the reactions of institutional investors as major market players toward CSR-firm controversies. As a result, this article contributes to fill these gaps and first studies the influence of CSR controversies on institutional investors and the attitude of fund participants (i.e., fund shareholders or fund investors) and fund managers toward these events.

Institutional investors comprise the largest share of investment activity globally (Erhemjamts & Huang, 2019), highlighting the institutional ownership of mutual and pension funds with more than €61.6 trillion and €34 trillion of global assets under management in 2021, respectively (INVERCO, 2022). Thus, pension and mutual funds are the most important institutional investors worldwide. Mutual and pension funds present similarities in several aspects: both invest on behalf of and for the best interest of fund beneficiaries, are professionally managed, are able to invest in a broad range of assets, share investment-asset universes, portfolio-management principles are similar, and managers’ remuneration is based on management fees charged as a percentage of assets under management (Del Guercio & Tkac, 2002; Sandberg, 2013). However, their nature, purposes, and clientele are different (Del Guercio & Tkac, 2002). On the one hand, pension funds are not part of investment funds (as mutual funds) because pension-fund liabilities are long-term and present rigid conditions for the encashment (International Monetary Fund [IMF], 2004). Specifically, pension-fund participants cannot collect pension savings until they reach certain (retirement) age (IMF, 2004; Organisation for Economic Co-operation and Development [OECD], 2005). Hence, pension funds are characterized by the management of large retirement savings with long-term orientation, a social nature, and fund savings cannot be recovered until retirement 2 (Himick & Audousset-Coulier, 2016; Sandberg, 2013). In addition, pension funds are more norm-constrained due to larger scrutiny exposure by the general public (Cox et al., 2004). On the other hand, mutual funds are the main channel for retail investors to participate in capital markets with a short-term vision (Goyal & Wahal, 2008).

Accordingly, institutional investors cannot be treated as a homogeneous group and diverse categories can be distinguished according to the investment horizon (Hoskisson et al., 2002). Unlike previous works, we separately analyze pension and mutual funds and study whether pension-fund characteristics (long-term investment horizon, social nature, and larger investment constraints) originate differential institutional-shareholding behavior regarding CSR-firm controversies, leading pension funds to larger activism and engagement in investee firms with controversies.

Furthermore, the importance of studying pension and mutual funds considering CSR investee-firms’ controversies is multiple. First, institutional investors are “universal owners” that represent the whole capital market, that is, their interests differ from those of other shareholders, especially those concentrated in a firm (Chen et al., 2020). Chen et al. (2020) argue that institutional funds are exposed to various controversy risks due to the investment in multiple stocks (based on portfolio-diversification principles); hence, institutional funds are concerned with the effects of potential controversies in multiple investee firms. Second, as fund management is separate from fund ownership, agency problems may arise when managerial actions with regard to CSR-firm controversies are not aligned with the values of fund-participants. Previous studies find that pension-fund participants present more enduring behavior and higher loyalty to the selected funds than mutual-fund participants, mainly due to persisting preferences over time and some prioritization of non-financial aspects (Sialm et al., 2015). Therefore, CSR-firm controversies might originate lower reactions among pension-fund participants. Despite this, the fund loyalty may be due to no skills to condemn firm misconducts, limited attention associated with the long-term nature, or disinvestment restrictions (Barnett, 2014). Finally, the limited evidence on this topic for mutual funds and especially pension funds lends support to our analysis.

On the other hand, the inclusion of ESG criteria among pension and mutual funds reaches conventional-fund and SRI-fund segments, making it is necessary to analyze both segments. We may expect that the strategic-fund priorities may set the response to CSR controversies. SRI funds might avoid controversial firms to a greater extent (Jin & Han, 2018). Nevertheless, the SRI evolution from an SRI niche to a mainstream SRI has generated diverse ESG criteria among conventional and SRI funds (Revelli, 2017). Conventional funds are increasingly considering ESG criteria and some SRI funds have diminished the ESG standards to provide similar performance to conventional funds, resulting in low ESG-scored SRI funds (Barnett & Salomon, 2006; Revelli, 2017). The ESG-standard variety may produce SRI ambiguities and diverse ESG-fund scores among SRI and conventional funds (Nath, 2021). Hence, the effect of and reaction to investee-firms’ controversies may be diverse between conventional and SRI funds in pension-fund and mutual-fund industries.

This study focuses on UK mutual and pension funds because these UK industries present distinctive features that make them relevant for our analysis, providing new evidence outside the US market. First, the United Kingdom is the second worldwide and the largest European market in assets under management (GBP 9.4 trillion assets in 2020), the management-industry size is almost five times the United Kingdom’s economy (almost 500% of UK gross domestic product [GDP] in 2020), and institutional investors managed 80% of these assets in 2020 (The Investment Association, 2021). Specifically, the UK pension-fund industry is the second global pension-fund market with more than €2.6 trillion under management and 118.5% of the UK GDP in 2020 (INVERCO, 2022; OECD, 2021). On the other hand, the UK mutual-fund market managed around 25% of the European funds, reaching GBP 1.4 trillion assets in 2020 (The Investment Association, 2021). Second, the UK pension system belongs to the Anglo-Saxon welfare model, characterized by non-large public pensions, which significantly enhanced the growth of private pension funds. As a result, pension funds are the main savings vehicle of UK households (56.5% of UK household savings are invested in pension funds and insurances—INVERCO, 2021). Besides, mutual funds are the second institutional investment vehicle of UK household assets (5.8% in 2020—INVERCO, 2021).

Furthermore, the United Kingdom is the leading European country in SRI with GBP 72 billion in responsible investment funds (Global Sustainable Investment Alliance [GSIA], 2021). The United Kingdom is a pioneer in developing regulation on sustainable and responsible investment in Europe, including the disclosure of ESG issues by pension funds (UKSIF, 2018; UK Statutory Instruments No. 988 Pensions, 2018), and the Pensions Schemes Act 2021 was modified to consider Paris Goals in the fund investment strategy (GSIA, 2021). In addition, the United Kingdom sets extra stewardship codes for asset management. The UK Stewardship Code 2020 introduces higher standards than those established by the EU Shareholder Rights Directive (European Union, 2017), demanding description of engagement policy as well as outcome-based reporting of the voting and engagement actions (GSIA, 2021). The importance of these UK fund industries and the larger concern about ESG issues provide us an opportunity to explore the consequences and reactions of UK mutual and pension funds toward CSR-firm controversies.

Among the profuse literature on CSR controversial events, this article is part of the literature that relates CSR controversies and shareholders (Beatty et al., 2013; Sane, 2019; Xu et al., 2016; among others). Specifically, this study relates to the limited works examining the relation between institutional investors and investee-firms’ CSR (Chen et al., 2020; Erhemjamts & Huang, 2019; among others). Unlike previous institutional-investor studies focusing on firm’s side, we examine institutional-investors’ side. We then analyze this relation from a new perspective, contributing to disentangle the consequences of investee-firms’ controversial incidents for institutional investors and their conducts toward these events. Thus, the aim of this article is threefold. First, we study the impact of multiple investee-firms’ CSR controversies on the performance of UK domestic-equity pension and mutual funds (conventional and SRI). Our study incorporates controversies in the three ESG dimensions (environmental, social, and governance) to fill the literature gap of considering isolated ESG dimensions. Second, although institutional investors are increasingly considering non-financial matters in the fund investment, the attitudes of fund managers and fund participants toward investee-firm controversies have not been previously analyzed, as far as we know. We then separately analyze fund-managers’ and fund-participants’ reactions toward investee-firm controversies. In addition, we examine whether the existence of controversies in investee firms that develop CSR-engagement strategies can mitigate and prevent negative effects of controversies on fund performance, managerial decisions, and participants’ reactions (Li et al., 2019). These analyses contribute to the literature about institutional-investor preferences regarding CSR issues and complete the partial view about the effect of investee-firm controversies on institutional investors.

The rest of the article is organized as follows. Section “Reactions toward CSR-firm controversies” contains the literature review and research hypotheses. Section “Data, sample construction, and variables” describes the data, sample construction, and variables. Section “Results” contains the results. The last section concludes.

Literature review and hypotheses

The impact of CSR-firm controversies on fund performance

In line with agency theory, fund managers should handle resources in the best interest of beneficiaries (Sandberg, 2013). However, little is known about the effect of CSR controversies on fund participants and their financial interests. This situation may be due to a late inclusion of CSR controversies in CSR policies, considering them by the Global Reporting Initiative (GRI) since 2002 and the United Nations Global Compact (UNGC) principles since 2004 (Blanc et al., 2019).

Accordingly, the financial impact of CSR controversies is still unclear (Aouadi & Marsat, 2018; Nirino et al., 2021). Some studies find that CSR controversies negatively affect performance (Capelle-Blancard & Petit, 2019; Krüger, 2015; Nirino et al., 2021). Cui and Docherty (2020) find negative financial outcomes with controversial ESG news and, particularly, with transient institutional investors. However, Aouadi and Marsat (2018) find positive effect of some ESG controversies (executive-board compensation, insider-dealing, labor-diversity, and product-quality) on the performance of high-attention firms. Agle et al. (1999) find that events related to primary firm stakeholders (employees and customers) are more salient than those related to more distant stakeholders, such as the environment or local communities. The lack of clear empirical evidence suggests that the effect of CSR investee-firm controversies on fund performance may depend on the type of controversy. Considering these premises, we hypothesize the following:

H1. CSR controversies have diverse impact on fund performance, depending on the controversy type.

Reactions toward CSR-firm controversies

The management and the ownership of pension and mutual funds are separated; therefore, the responses of fund managers and fund participants to CSR-firm controversies may differ.

On the one hand, the reaction of fund participants may be based on the fact that institutional participants use ESG information to a greater extent than other investors (Cui & Docherty, 2020). The main mechanism to assess the reaction of fund participants toward investee-firm controversies is to analyze fund flows (Cui & Docherty, 2020). Previous evidence shows mixed reactions. Krüger (2015) and Capelle-Blancard and Petit (2019) indicate that investors react negatively to controversial ESG news, especially toward concerns related to employees, the environment, and communities. Hartzmark and Sussman (2019) report outflows/inflows in funds with poor/good ESG ratings. However, Beatty et al. (2013) find greater investment during scandal periods due to distorted signals. Barnett (2014) indicates limited ability to condemn firm controversies. In addition, fund-participants may not react to controversies when controversies are minor, there is information overload, controversies are unnoticed or disregarded by society, or these events fall outside their diligence (Aouadi & Marsat, 2018). That is, the impact on flows may also depend on factors such as the time period or the sample. Taking into account these considerations, we hypothesize the following:

H2. CSR-firm controversies affect fund flows diversely depending on the controversy type.

On the other hand, fund managers can modify the fund shareholding in investee firms to deal with unsatisfactory situations (McCahery et al., 2016). Hirschman (1970) highlights that unpleased institutional investors with a portfolio firm can leave the firm (i.e., exit decision), but they can also engage with the firm management to intervene directly through shareholding activism. Nofsinger et al. (2019) find lower institutional ownership with ESG concerns. In contrast, McCahery et al. (2016) find that institutional investors use shareholding activism rather than exit decisions with non-satisfactory events in investee firms, especially by long-term institutional investors such as pension funds. Consequently, we may expect that pension funds decrease fund shareholding after controversies to a lower extent. In line with this evidence, we propose the following:

H3. Mutual-fund managers decrease the fund shareholding in investee firms with controversies to a greater extent than pension-fund managers.

Managerial reactions to controversies may also influence fund participants, that is, fund participants can react to managerial decisions. Fund participants know managerial actions with some delay (Janney & Gove, 2011); hence, whether fund participants support managerial decisions, we may expect stable fund flows some time later. Tamayo-Torres et al. (2019) conclude that supply-chain controversies increase firm-sustainability practices 2 years later, mainly due to reactive behavior of institutional investors (Aouadi & Marsat, 2018). Accordingly, the fourth hypothesis considers potential late reactions of fund participants (via fund flows) toward managerial decisions made regarding controversies:

H4. Fund participants react after managerial decisions with regard to investee-firm controversies, affecting fund flows with some delay.

Substantive and symbolic engagement

Some authors argue that the effects of CSR-firm controversies may be alleviated when investee firms have extended history of ESG practices, such as CSR-engagement, reducing market over-reactions, and massive stock sales (Nirino et al., 2021). Specifically, CSR-engagement practices are voluntary CSR-firm actions taken beyond regulation that may help to re-establish the firm situation and reputation with the stakeholders and the environment to the pre-controversy level, mitigating performance deterioration (Park et al., 2014).

CSR-firm engagement strategies are divided into “symbolic” (non-real) and “substantive” (real) CSR-engagement (Perez-Batres et al., 2012). Symbolic CSR-engagement displays ceremonial conformity and willingness to develop CSR issues, without necessarily developing meaningful changes, for example, signing the United Nation Principles for Responsible Investment (UNPRI) or the UNGC principles (Pérez-Batres et al., 2012). In contrast, substantive CSR-engagement refers to real CSR-firm actions that entail changes in business processes and long-term commitment to CSR, requiring higher expenses (Li et al., 2019; Perez-Batres et al., 2012). Actions displayed on CSR reports published according to GRI guidelines are examples of CSR-substantive engagement (Perez-Batres et al., 2012).

Symbolic and substantive CSR-engagement practices try to reduce negative CSR impacts; however, the limited studies on this topic show a gap about their influence on financial performance (Li et al., 2019). Flammer (2013) shows that long-term investors obtain better performance due to CSR activities of investee firms. Flammer (2013) also finds that substantive CSR-engagement may improve funds’ stability when the market considers firm controversies as non-usual conducts. Eccles et al. (2014) find higher performance with substantive CSR-engagement policies. Nevertheless, CSR-engagement actions cannot moderate the negative relationship between controversies and performance when investors do not update their beliefs after ESG news (Nirino et al., 2021). Furthermore, ESG events may have no implications on performance when investors prioritize non-financial aspects (Werther & Chandler, 2005). Therefore, investee-firm controversies experienced after CSR-engagement practices may continue to have a diverse impact on fund performance, depending on the controversy type as well as the investor financial preferences.

On the other hand, symbolic and substantive CSR-engagement actions can moderate the reactions of fund participants to controversies (Tamayo-Torres et al., 2019). Li et al. (2019) argue that shareholders better distinguish between symbolic and substantive CSR-engagement than other stakeholders. Shareholders usually respond positively to symbolic CSR-engagement with minor controversies because of its short-lived character (Li et al., 2019). Ammann et al. (2019) demonstrate that funds with good records on sustainability attract flows. However, Hawn et al. (2018) find limited reaction to sustainability changes. Considering the previous evidence, we may expect lower fund outflows after controversies in investee firms with symbolic and substantive CSR-engagement. In addition, symbolic and substantive CSR-engagement practices may influence managerial decisions. Krüger (2015) argues that ESG efforts enhance managers’ reputation. Flammer et al. (2021) find that institutional-fund managers value voluntary climate-risk disclosures and consider engagement rather than divestment in firms disclosing negative climate-risk information.

This prior evidence indicates that the impact of controversies on fund performance, fund participants’ reactions, and fund managers’ decisions may be modified due to CSR-engagement practices of investee firms. We then pose our last hypotheses:

H5. Investee-firm controversies experienced after CSR-engagement (symbolic and substantive) diversely affect fund performance according to the controversy type.

H6. CSR-engagement (symbolic and substantive) practices of investee firms moderate fund outflows after investee-firm controversies.

H7. Fund managers do not react negatively to controversies in firms with CSR-engagement (symbolic and substantive) practices.

Data, sample construction, and variables

Our sample is drawn from several sources. The pension-fund and mutual-fund data of all UK domestic-equity funds are obtained from Morningstar Direct database. We exclude index funds for robustness and include both live and dead funds to avoid survivorship bias. Moreover, funds have at least 75% of their holdings invested in stocks. The samples are formed of 359 pension funds and 1,008 mutual funds. Morningstar database distinguishes between SRI and conventional funds with the “Socially-conscious” variable, 3 which indicates Yes/No when a fund is a SRI/conventional fund. We transform the socially conscious variable into an SRI dummy by designating 1/0 when the socially conscious variable of Morningstar labels Yes/No to identify funds as SRI/conventional funds. As a result, our pension-fund sample is divided into 28 SRI and 331 conventional pension funds. The mutual-fund sample is divided into 42 SRI and 966 conventional mutual funds.

The fund data include, from January 1999 to November 2019, quarterly portfolio holdings (i.e., fund-shareholding weights on investee firms); quarterly, monthly, and daily returns; quarterly Total Net Assets (TNA); inception date; annual turnover ratios; and annual expense ratios. From the inception date, we obtain the fund age each quarter (expressed in years). We also calculate the quarterly percentage fund flows. 4 Following previous ESG and CSR controversy studies (Cui & Docherty, 2020; Flammer et al., 2021; Hawn et al., 2018; among others), we calculate the traditional performance measure of the four-factor alpha of Carhart (1997). We obtain the quarterly four-factor alpha with 36-month return rolling windows from the European risk-factors available on French’s data library 5 (see Online Appendix 1 for further details). Thus, our analyses are restricted from January 2002 to November 2019.

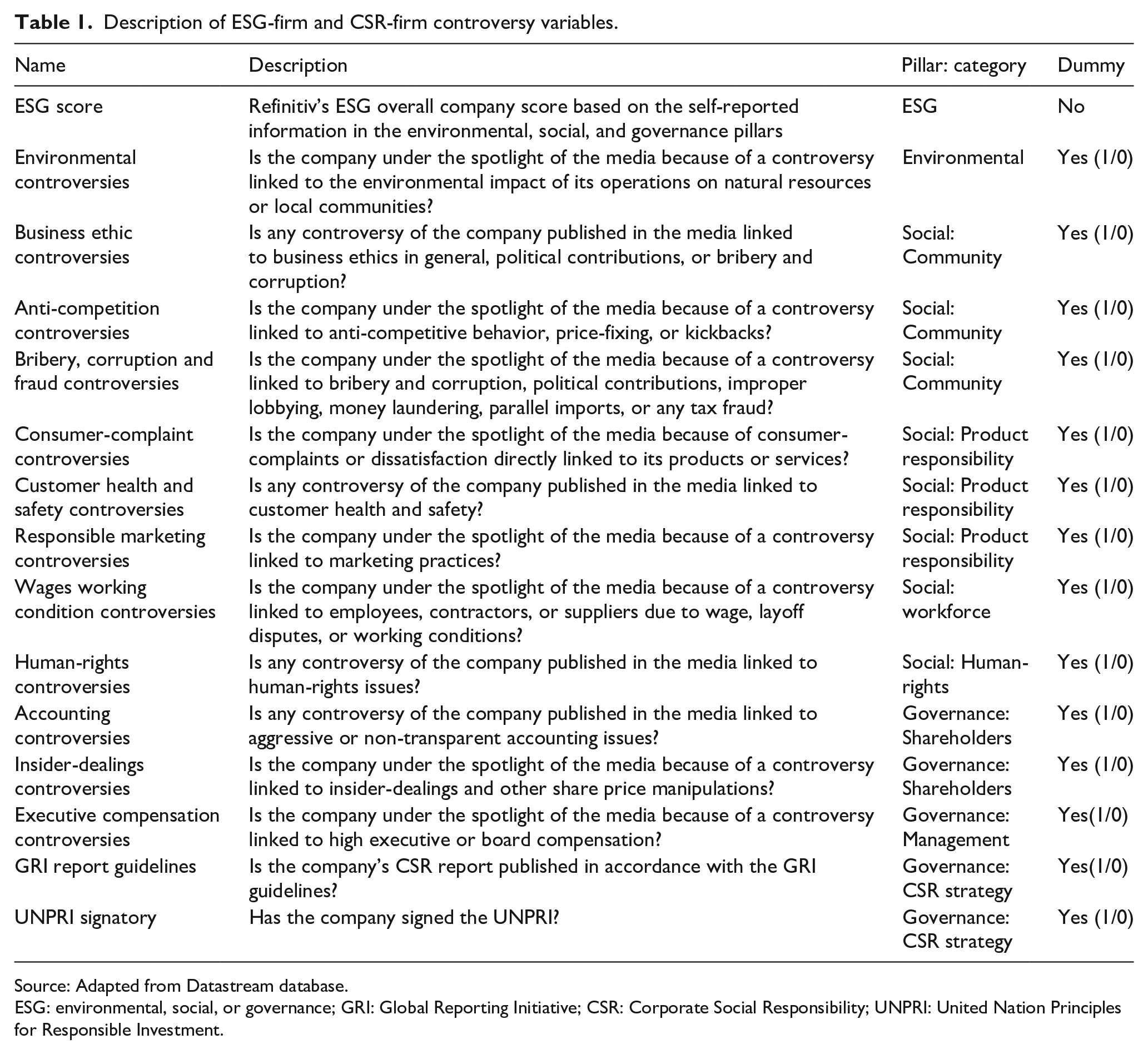

We collect data of the portfolio holdings from the pension and mutual funds analyzed and obtain that these funds invest in 6,991 distinct stocks. Considering the 6,991 investee firms, we obtain 15 quarterly ESG-firm variables from Datastream database (in the ESG-Asset4 category) from 2002 to 2019 (November). These variables include the ESG-firm score (ranging from 0—lowest to 1—highest), 12 CSR-firm controversies covering the main categories of the ESG pillars, according to Refinitiv, 6 a substantive CSR-engagement variable (GRI), and a symbolic (UNPRI) CSR-engagement variable (see Table 1 for a full description). To select these variables, among those available in the ESG-Asset4 category, we exclude variables with numerous missing data, 7 non-available data, and inactive variables. The controversy variables (except three variables) are quarterly dummy variables that equal 1 when a firm experiences a controversy at that quarter and 0 otherwise. The three non-dummy controversy variables (business-ethics, human-rights, and accounting controversies) show the number of controversies experienced by a firm quarterly. Thus, we transform these variables into dummies 8 to provide homogeneity between variables (i.e., these variables equal 1 if a firm suffers a controversy and 0 otherwise; see Table 1 for further detail).

Description of ESG-firm and CSR-firm controversy variables.

Source: Adapted from Datastream database.

ESG: environmental, social, or governance; GRI: Global Reporting Initiative; CSR: Corporate Social Responsibility; UNPRI: United Nation Principles for Responsible Investment.

We match the quarterly portfolio holdings of the 359 pension funds and the 1,008 mutual funds (obtained from Morningstar) with the quarterly ESG-firm variables of the 6,991 firms (from Datastream) from January 2002 to November 2019. First, we use the holding data to calculate ESG-fund scores from ESG-firm scores. We calculate the ESG-fund score to control the ESG standards of SRI and conventional funds, given that the mainstream SRI has generated diverse ESG criteria among conventional and SRI funds (Barnett & Salomon, 2006; Revelli, 2017). We calculate quarterly ESG-fund scores as the quarterly weighted sum of ESG-firm scores of all investee firms held by a fund and the fund portfolio-holding weights of all investee firms held by a fund each quarter. Second, we calculate quarterly fund controversies in each controversy type studied as the addition of all controversies experienced by all investee firms held by a fund each quarter.

Finally, we obtain the OECD-based recession indicator for the United Kingdom from the Federal Reserve Economic Data 9 to detect recession and expansion periods (the indicator equals 1 in recessions and 0 otherwise).

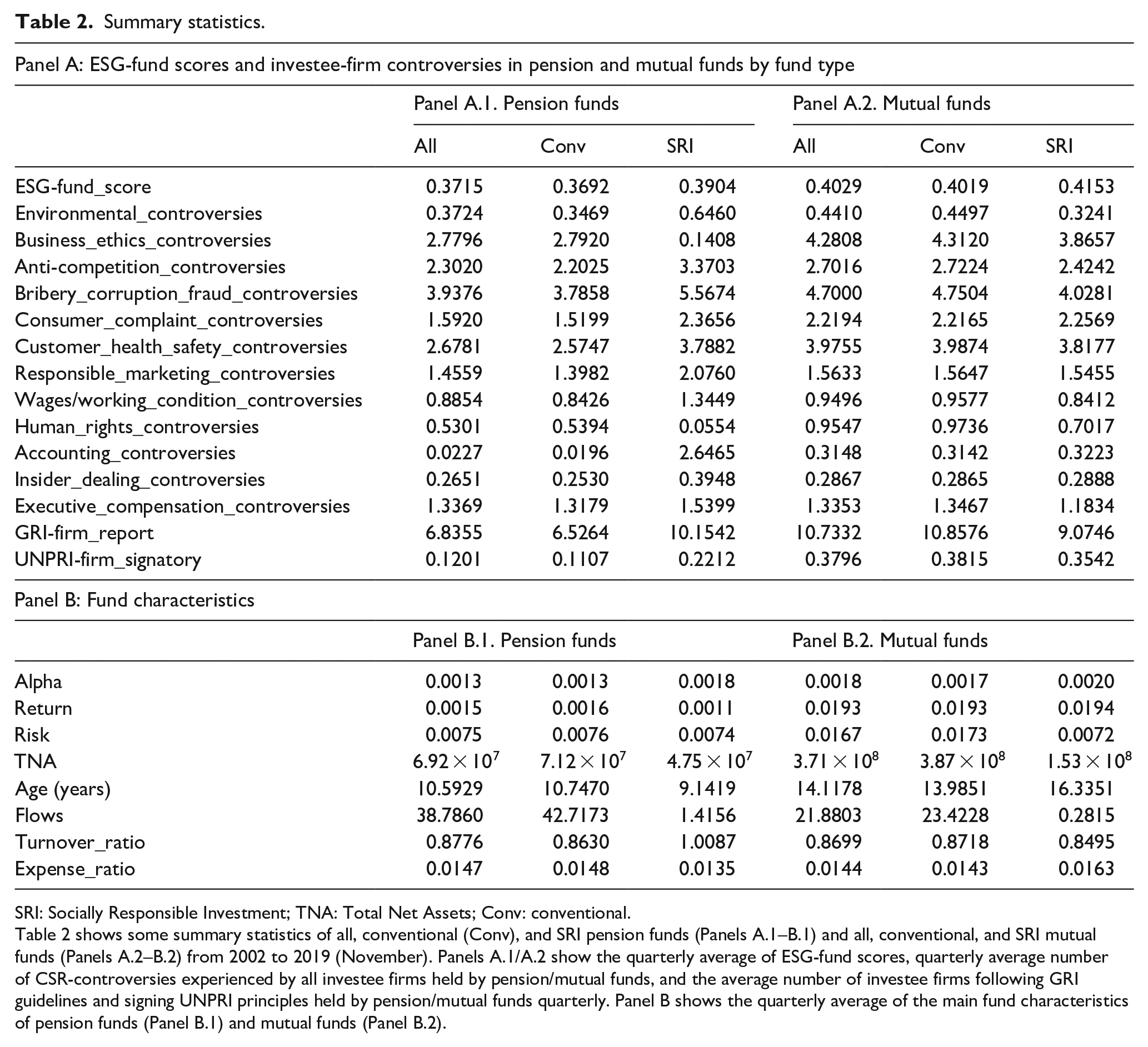

Table 2 shows some summary statistics of pension funds (conventional and SRI) in Panels A.1–B.1 and mutual funds (conventional and SRI) in Panels A.2–B.2. Panels A.1–A.2 show that the ESG-fund scores of pension and mutual funds are 37.15% and 40.29%, on average, respectively. The moderate scores indicate that pension and mutual funds invest in firms with controversies. Furthermore, the ESG score is higher in SRI funds than in conventional funds (39.04% vs 36.92% in pension funds and 41.53% vs 40.19% in mutual funds). With regard to controversies, the three most relevant controversies of the firms held by pension and mutual funds are business ethics, bribery/corruption/fraud, and customer health/safety controversies. In contrast, the least common controversies are accounting, insider-dealing, and environmental controversies. In general, SRI pension (SRI mutual) funds hold higher (lower) firm controversies than conventional pension (mutual) funds. This shows that SRI pension funds may be engaged in active shareholding to amend and control firms with controversies, consistent with the social nature of pension funds (Himick & Audousset-Coulier, 2016; Sandberg, 2013); however, SRI mutual funds follow higher ESG standards. On the other hand, SRI pension (mutual) funds hold firms with higher (lower) transparency, publishing more (fewer) CSR reports with GRI guidelines and signing UNPRI principles to a greater (lower) extent than investee firms of conventional pension (mutual) funds. These results show the increasing inclusion of ESG criteria among conventional funds and the diverse ESG standards among funds.

Summary statistics.

SRI: Socially Responsible Investment; TNA: Total Net Assets; Conv: conventional.

Table 2 shows some summary statistics of all, conventional (Conv), and SRI pension funds (Panels A.1–B.1) and all, conventional, and SRI mutual funds (Panels A.2–B.2) from 2002 to 2019 (November). Panels A.1/A.2 show the quarterly average of ESG-fund scores, quarterly average number of CSR-controversies experienced by all investee firms held by pension/mutual funds, and the average number of investee firms following GRI guidelines and signing UNPRI principles held by pension/mutual funds quarterly. Panel B shows the quarterly average of the main fund characteristics of pension funds (Panel B.1) and mutual funds (Panel B.2).

Results

This section shows the empirical results to test the hypotheses proposed. Online Appendix 2 shows the models applied in the analyses.

The effect of investee-firm controversies on fund performance and flows

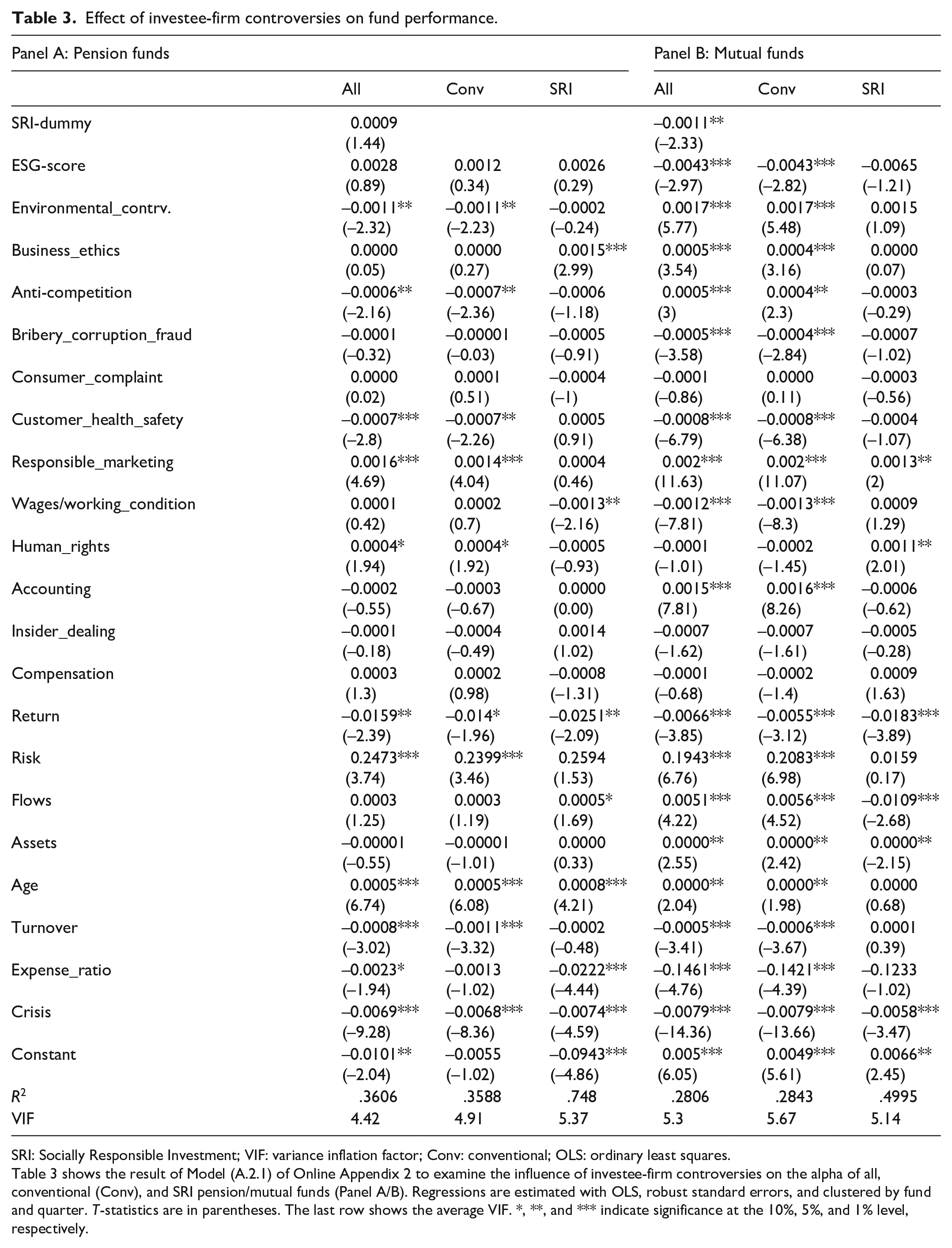

We study the effect of firm controversies on the four-factor alpha (Table 3) and flows (Table 4) of pension funds (Panel A) and mutual funds (Panel B). The models are described in Online Appendix 2 (Models A.2.1 and A.2.2). Models (A.2.1) and (A.2.2) include lagged independent variables to avoid endogeneity problems. All models are estimated with robust and clustered standard errors by fund and quarter to address heteroskedasticity problems and correlated errors (conditional on independent variables) within the fund and time dimensions. The last row of Tables 3 and 4 shows the average variance inflation factor (VIF) of the estimated coefficients to assess multicollinearity. 10

Effect of investee-firm controversies on fund performance.

SRI: Socially Responsible Investment; VIF: variance inflation factor; Conv: conventional; OLS: ordinary least squares.

Table 3 shows the result of Model (A.2.1) of Online Appendix 2 to examine the influence of investee-firm controversies on the alpha of all, conventional (Conv), and SRI pension/mutual funds (Panel A/B). Regressions are estimated with OLS, robust standard errors, and clustered by fund and quarter. T-statistics are in parentheses. The last row shows the average VIF. *, **, and *** indicate significance at the 10%, 5%, and 1% level, respectively.

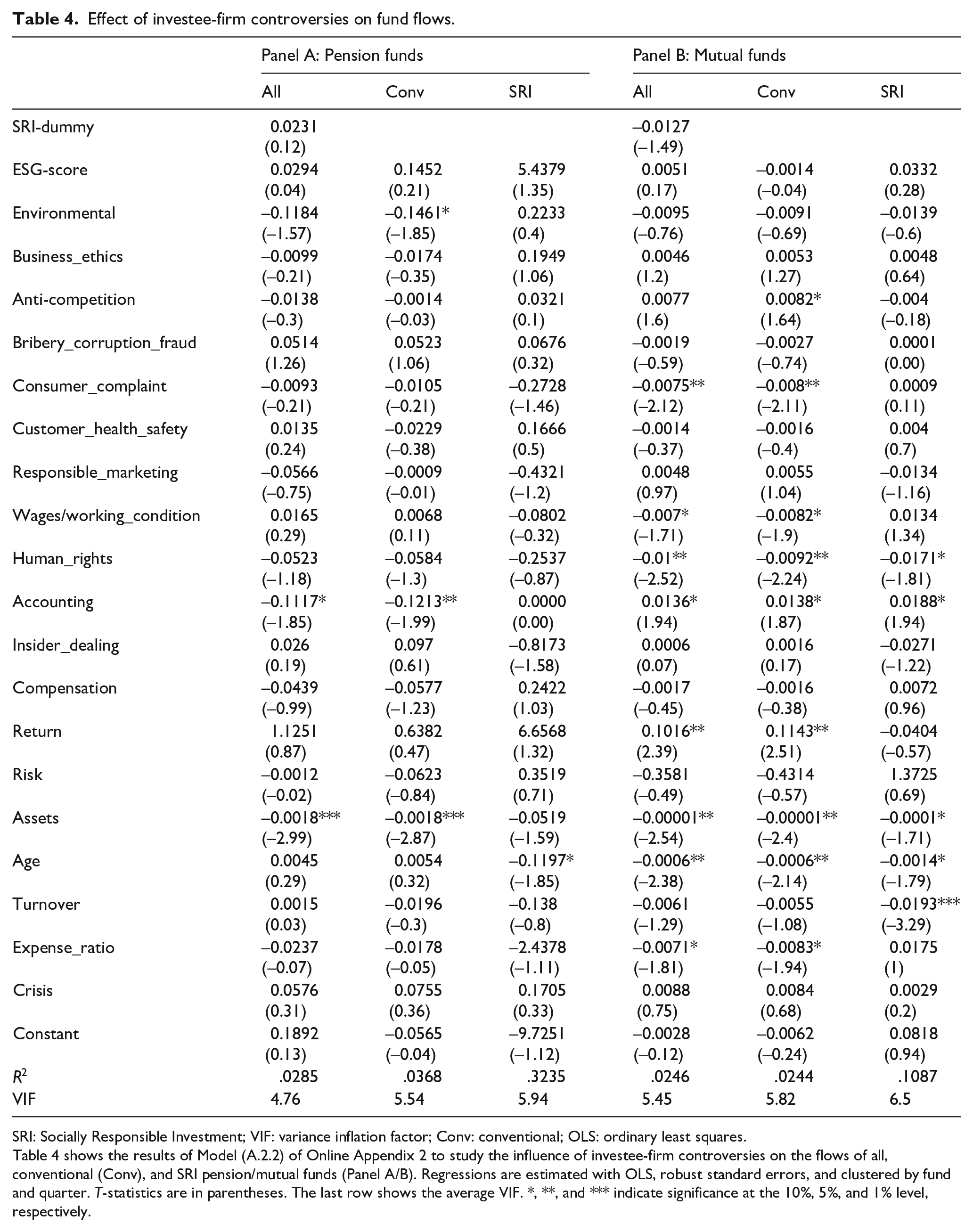

Effect of investee-firm controversies on fund flows.

SRI: Socially Responsible Investment; VIF: variance inflation factor; Conv: conventional; OLS: ordinary least squares.

Table 4 shows the results of Model (A.2.2) of Online Appendix 2 to study the influence of investee-firm controversies on the flows of all, conventional (Conv), and SRI pension/mutual funds (Panel A/B). Regressions are estimated with OLS, robust standard errors, and clustered by fund and quarter. T-statistics are in parentheses. The last row shows the average VIF. *, **, and *** indicate significance at the 10%, 5%, and 1% level, respectively.

Panel A of Table 3 shows that the SRI-fund nature and the ESG-fund score do not affect the fund performance of pension funds (non-significant SRI-dummy and ESG-score coefficients). In addition, controversies differently affect performance, in line with our first hypothesis (H1). The conventional-fund performance is negatively (positively) affected by environmental, anti-competition, and customer-health-safety (responsible-marketing and human-rights) controversies. On the other hand, wages/working-conditions (business-ethics) controversies affect negatively (positively) SRI-fund performance. The positive coefficients are consistent with the frequent overlook of social misconducts in areas such as business ethics or human-rights, mainly due to information overload in these areas (Aouadi & Marsat, 2018). Furthermore, the market receives news with some delay, and initially, some misconducts seem profitable, reporting higher performance (Beatty et al., 2013). That is, the market only penalizes certain controversies.

Panel B shows mutual-fund results. In accordance with previous SRI mutual-fund studies (Barnett & Salomon, 2006; Jin & Han, 2018; among others), the SRI-fund nature negatively affects performance (significantly negative SRI-dummy). Previous studies find that the ESG standards of SRI funds limit their investment universe, produce management constraints, and restrict performance (Barnett & Salomon, 2006; Jin & Han, 2018). Furthermore, higher ESG-fund scores decrease the performance of conventional funds. A higher ESG score means more restrictive ESG criteria, which may cause under-diversification, investment-opportunity losses, and underperformance (Barnett & Salomon, 2006; Jin & Han, 2018; Revelli, 2017). Then, conventional mutual funds are not able to fully integrate extra ESG criteria; however, the ESG score does not affect SRI-funds’ performance With regard to controversies, these events diversely affect mutual-fund performance, consistent with H1 and our pension-fund results (Panel A). The conventional-fund performance is positively (negatively) affected by environmental, business-ethics, anti-competition, responsible-marketing, and accounting (bribery-corruption-fraud, customer-health-safety, and wages/working-condition) controversies. On the other hand, higher controversies in responsible-marketing and human-rights areas increase the SRI mutual-fund performance. The positive coefficients are found again in areas with information overload and frequent overlook of these conducts, providing distorted and delayed signal about these controversial events (Aouadi & Marsat, 2018; Beatty et al., 2013).

Our results support the diverse financial impact of CSR controversies found in previous studies (Aouadi & Marsat, 2018; Capelle-Blancard & Petit, 2019; Krüger, 2015; Nirino et al., 2021). Furthermore, regarding H1, we notice that the influence of CSR controversies on performance depends on the controversy type. Specifically, controversies in areas characterized by information overload (business ethics, responsible-marketing, and human-rights) positively affect the performance of pension and mutual funds, which might mislead long-term consequences (Aouadi & Marsat, 2018). In contrast, customer-health-safety and wages/working-condition controversies negatively affect performance in pension and mutual funds. That is, the market is concerned about controversies related to the wellbeing of primary stakeholders (customers and employees). Agle et al. (1999) also find larger impact of events related to primary stakeholders. Furthermore, unlike Agle et al. (1999), we find that controversies of more distant stakeholders (environmental and social-community categories: business-ethics, anti-competition, and bribery/corruption/fraud) also affect performance, except in SRI mutual funds. As a result, environmental and social issues of investee firms are significant for pension and mutual funds. Nevertheless, it is noticeable that controversies related to governance issues (shareholders: accounting and insider-dealing, and management: compensation) seem to be practically unnoticed by the market, possibly because these are perceived as internal-firm affairs. In conclusion, our evidence does not allow us to reject H1.

Table 4 shows the influence of controversies on fund flows. Panel A barely displays significant impact of controversies on pension-fund flows, contrary to our H2 (CSR-firm controversies affect fund flows diversely depending on the controversy type). Flows of conventional pension funds decrease with more environmental and accounting controversies (significant coefficients at 10% and 5% levels, respectively). This shows a penalty of fund participants for holding firms with these controversies. However, SRI-fund flows are not significantly affected by controversies. In general, the results of Panel A are in line with the “sticky behavior” found in pension funds (Sialm et al., 2015). Sialm et al. (2015) find that pension-fund participants develop an enduring behavior due to scarcer reallocation and preferences for non-financial issues, aligned with the social nature of pension funds. This passive behavior indicates loyalty and persistent preferences over time, as well as lack of attention and/or limited ability to condemn firm controversies by pension-fund participants (Barnett, 2014).

Panel B shows that controversies influence conventional mutual-fund flows to a greater extent, and mutual-fund participants penalize some controversies and support others. Specifically, more controversies in anti-competition and accounting (consumer-complaint, wages/working-conditions, and human-rights) areas increase (decrease) conventional mutual-fund flows. Furthermore, more controversies in accounting (human-rights) controversies increase (decrease) SRI mutual-fund flows. The positive coefficients indicate that mutual-fund investors are attracted by undervalued controversies, replicating a return-chasing behavior observed in past undervalued controversies (Blocher, 2016). Nevertheless, coefficients are significant at 5% and 10% levels, showing scarce influence on flows, especially by SRI mutual-fund participants.

The results of Table 4 display different investment preferences among fund participants, which do not allow us to accept H2. Pension-fund (conventional and SRI) and SRI mutual-fund participants demonstrate a passive behavior and scarce reaction toward controversies, contrary to H2. However, the mixed reactions of conventional mutual-fund participants show dissimilar conducts by controversy type (consistent with H2). In line with the results of Table 3, controversies related to primary stakeholders (consumers and employees) produce negative reactions of participants (lower flows with consumer-complaint, wages/working-conditions, and human-rights controversies), indicating the concern of fund participants about these stakeholders. Krüger (2015) and Capelle-Blancard and Petit (2019) also find negative reactions to controversial events related to employees and communities. On the other hand, the greater flows with anti-competition and accounting controversies may be due to distorted signals. Beatty et al. (2013) find that distorted accounting information may lead peers to invest with accounting misreporting.

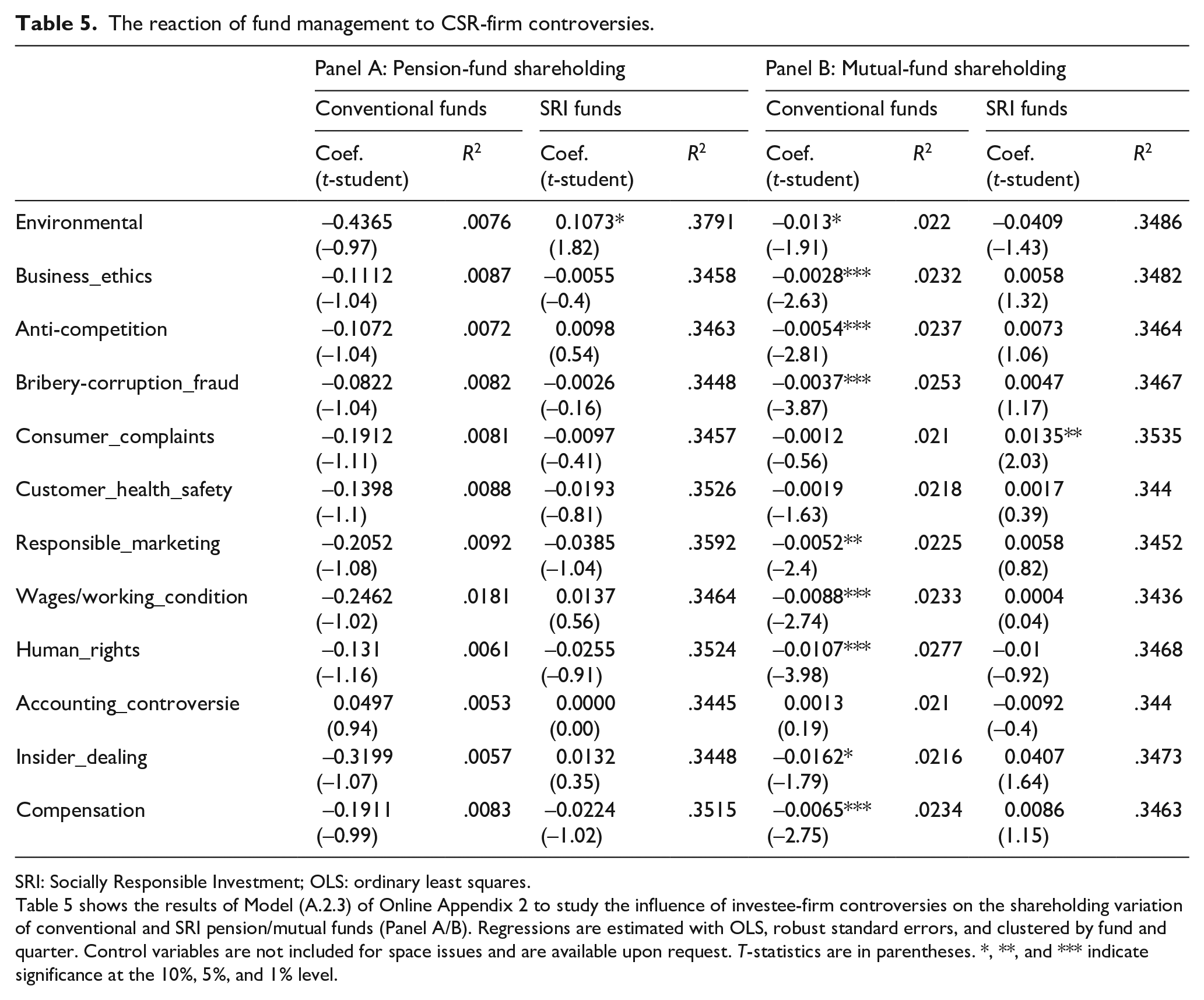

Reaction of fund managers to CSR-firm controversies

In this section, we analyze whether fund managers react to firm controversies by modifying the fund shareholding in these firms. To develop this analysis, first, we calculate the quarterly portfolio-holding variation in each firm experiencing a controversy at that time. Second, we obtain the total quarterly controversial portfolio-holding variation by considering all shareholding variations in all controversial firms held by a fund quarterly. 11

Table 5 shows the results of Model (A.2.3), described in Online Appendix 2. Panel A shows that pension-fund managers do not vary the fund shareholding in firms after controversies. Consistent with the enduring behavior found in pension-fund participants (Table 4), pension-fund managers do not adjust portfolios with investee-firm controversies. That is, pension-fund managers do not react to controversies because pension-fund participants do not respond to these events. Nonetheless, this lack of reaction might be also related to the increasing monitoring of these funds in investee firm (Erhemjamts & Huang, 2019; McCahery et al., 2016; Pucheta-Martínez & Chiva-Ortells, 2020). Pension funds may continue investing in firms with controversies to monitor, support, and help them to overcome CSR controversies through active shareholding (Erhemjamts & Huang, 2019; McCahery et al., 2016; Sonza & Granzotto, 2018).

The reaction of fund management to CSR-firm controversies.

SRI: Socially Responsible Investment; OLS: ordinary least squares.

Table 5 shows the results of Model (A.2.3) of Online Appendix 2 to study the influence of investee-firm controversies on the shareholding variation of conventional and SRI pension/mutual funds (Panel A/B). Regressions are estimated with OLS, robust standard errors, and clustered by fund and quarter. Control variables are not included for space issues and are available upon request. T-statistics are in parentheses. *, **, and *** indicate significance at the 10%, 5%, and 1% level.

Panel B shows that, in general, higher controversies reduce the conventional mutual-fund shareholding in controversy investee firms. As we pose in H3 (mutual-fund managers decrease the fund shareholding in investee firms with controversies to a greater extent than pension-fund managers), conventional mutual-fund managers withdraw their support from controversy investee firms. This conduct is coherent with the findings of Nofsinger et al. (2019) and some negative reactions of conventional mutual-fund participants, found in Panel B of Table 4. Nevertheless, SRI mutual-fund managers show no reaction to controversies, except for the positive relation between fund-shareholding and consumer-complaint controversies. The lack of managerial reaction is consistent with the scarce response of SRI mutual-fund participants (Panel B of Table 4). This evidence also suggests that SRI mutual funds continue investing in firms with controversies to monitor, support, and help with CSR investee-firm issues (Erhemjamts & Huang, 2019; Lim et al., 2007; Sonza & Granzotto, 2018).

Overall, Table 5 displays two managerial reactions to deal with investee-firm controversies. On the one hand, conventional mutual funds mostly sell controversial stocks. On the other hand, pension funds (conventional and SRI) and SRI mutual funds barely react to controversies (in line with the passive behavior of fund participants). Therefore, managerial decisions regarding controversies seem to be related to investors’ behavior rather than the investment vehicle (pension/mutual fund). The similar patterns in managerial decisions in pension funds and SRI mutual funds may be based on the social nature of pension funds, approaching SRI values by both conventional and SRI pension funds (Himick & Audousset-Coulier, 2016; Sandberg, 2013). In conclusion, we reject H3 because only conventional mutual funds (and not SRI mutual-fund managers) strongly react to CSR-firm controversies by decreasing portfolio shareholdings.

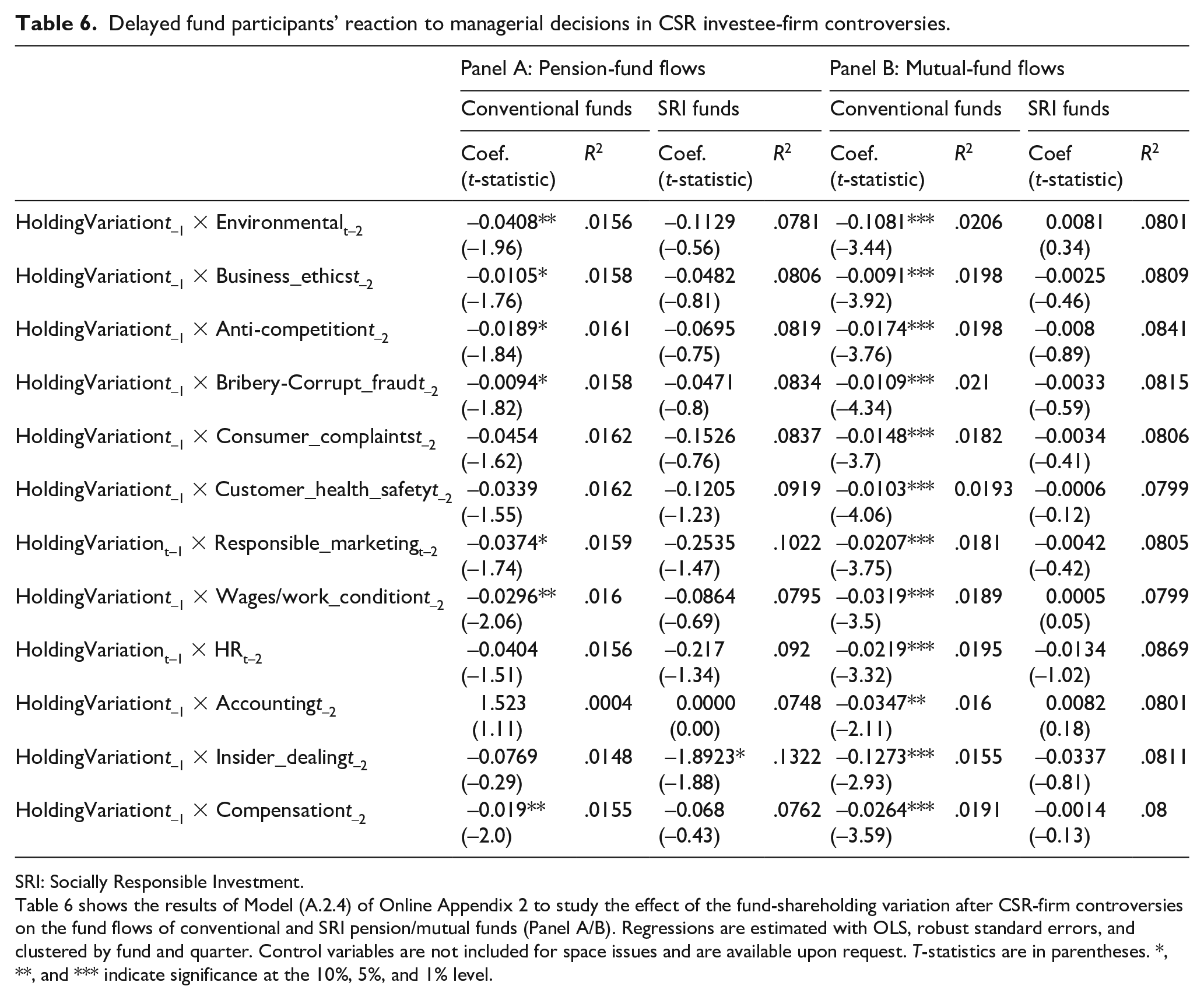

Delayed reactions of fund participants

Fund participants may also react to managerial decisions regarding controversies. Since managerial decisions are disclosed with some delay, fund-participants would modify their investments after observing managers’ decisions. We build Model (A.2.4) of Online Appendix 2 with interactive shareholding_variation-controversy variables to analyze this reaction. The interactive variables of Model (A.2.4) consider that managers react after controversies and participants react after managerial decisions, that is, the interactive variables are obtained by multiplying the two-period lagged controversies and the one-period lagged controversial fund-shareholding variation

Table 6 shows the results of Model (A.2.4) for pension funds (Panel A) and mutual funds (Panel B). Panel A discloses a negative relation between conventional pension-fund flows and fund-shareholding variations after 7 of the 12 controversies studied (coefficients are significant at 10% and 5% levels). Alternatively, SRI pension-fund participants do not react to managerial decisions, preserving the enduring behavior found in Table 4. On the other hand, Panel B also shows a negative relation between conventional mutual-fund flows and shareholding changes after controversies (negative coefficients). Furthermore, we confirm the enduring behavior of SRI mutual-fund participants (no significant coefficients).

Delayed fund participants’ reaction to managerial decisions in CSR investee-firm controversies.

SRI: Socially Responsible Investment.

Table 6 shows the results of Model (A.2.4) of Online Appendix 2 to study the effect of the fund-shareholding variation after CSR-firm controversies on the fund flows of conventional and SRI pension/mutual funds (Panel A/B). Regressions are estimated with OLS, robust standard errors, and clustered by fund and quarter. Control variables are not included for space issues and are available upon request. T-statistics are in parentheses. *, **, and *** indicate significance at the 10%, 5%, and 1% level.

Our results indicate distinct attitudes of conventional-fund and SRI-fund participants for both pension and mutual funds. Hence, our fourth hypothesis (fund participants react after managerial decisions with regard to investee-firm controversies, affecting fund flows with some delay) holds for conventional-fund participants, rejecting it for SRI-fund participants. Conventional-fund participants are more active after managerial decisions and flows decrease/increase with higher/lower fund-shareholding in controversy firms. To be precise, conventional-fund participants do not want to continue investing in funds with more holdings in controversial firms and support the disinvestment managerial decision. This pattern indicates that conventional participants are still guided by financial principles and avoid events that might damage the investment. In contrast, SRI-fund participants present a passive behavior with regard to managerial decisions after controversies. This behavior may be explained by several causes. First, SRI-fund participants accept managerial decisions, including no reaction after controversies (evidence found in Table 5). Second, participants may overlook controversial-firm events because of the long-term vision of SRI funds, displaying loyalty and persisting preferences over time (Sialm et al., 2015). And, on the contrary, the long-term vision can encourage participants to provide fund managers with the opportunity to engage in controversy firms’ management, act as active institutional shareholders, and help firms to achieve long-term sustainability (Aouadi & Marsat, 2018; McCahery et al., 2016; Tamayo-Torres et al., 2019).

Robustness tests

In this section, we develop some robustness tests. 12 First, we control for the relative importance of each controversy over all controversies on performance and flows. We weight each controversy type with regard to the total number of controversies experienced by a fund’s investee-firm’s quarterly and replace the controversy-type variables by these weighted-controversy variables in Models (A.2.1) and (A.2.2). Table A.3.1 of Online Appendix 3 shows the results. Panel A shows diverse effect of controversies on alpha, and Panel B displays no reaction of flows toward controversies. Although these results are in line with our previous analyses, panel A shows that the effect of most controversies on performance is non-significant and significantly negative. Moreover, several positive coefficients found in Table 3 turn to non-significance in this panel. These results indicate that the fund performance is also influenced by the relative importance of each controversy with regard to all controversies in the fund holdings. The relative importance of controversies in each fund can eliminate the effect of some controversies and the possibility of exploiting undervalued controversies in pension and SRI mutual funds. On the other hand, a higher importance of the controversies (except environmental and responsible-marketing) among conventional mutual-fund holdings damages performance. Cui and Docherty (2020) find negative financial outcomes with ESG controversies in transient institutional investors because these investors overweight the probability that these events occur again, mainly due to their shorter investment horizon (such as that of conventional mutual funds).

Panel B confirms the scarce reaction of pension-fund and SRI mutual-fund participants. In addition, the influence of controversies on conventional mutual-fund flows disappears with weighted controversies (comparing Panel B2 of Table A.3.1 and Panel B of Table 4). This indicates that mutual-fund participants guide their investment/de-investment decisions based on specific controversies (Panel B of Table 4) rather than on the importance of each controversy with regard to the total controversies suffered by funds’ investee firms.

The second robustness analysis examines the joint effect of all controversies. We aggregate all investee-firm controversies by fund and quarter and create the variable Total_controversies. Table A.3.2 of Online Appendix 3 shows the results of Models (A.2.5)–(A.2.8), described in Online Appendix 2. Panel A shows that the total number of controversies does not affect (positively affects) pension-fund (mutual-fund) performance. These findings indicate that the diverse effects (positive and negative) of controversies found on the performance of pension funds (Panel A of Table 3) offset each other considering their joint impact. Furthermore, the positive joint effect of controversies on mutual-fund performance is in line with the greater positive influence found by controversy type in Panel B of Table 3.

Panel B of Table A.3.2 shows that controversies barely influence flows (significant coefficients at 10%), sustaining the enduring and passive behavior of fund participants (found in Table 4). Panel C shows that portfolio holdings are not affected by controversies in pension and SRI mutual funds. However, conventional mutual-fund managers decrease the fund shareholding with a higher number of controversies in investee firms. These findings are in line with the conclusions reached in Section “Reaction of fund managers to CSR-firm controversies” (Table 5). Panel D shows an inverse relation between flows and the fund shareholding after controversies in conventional pension and conventional mutual funds. We confirm that conventional-fund participants are more active than SRI-fund participants and make investment decisions after receiving market and managerial information. Moreover, conventional funds are based on traditional investment guidelines and reducing flows may be related to the perception that more controversies erode performance over time. In summary, analyses with individual and total controversies led us to reach similar conclusions.

Third, we study how controversies affect funds considering the ESG-score level of investee firms. We estimate Models (A.2.1)–(A.2.2) of Online Appendix 2 by ESG-fund score terciles. Tables A.3.3 and A.3.4 of Online Appendix 3 show these results. Table A.3.3 shows the effect of controversies on alpha by ESG-score terciles. The results support our findings in Table 3, regardless of the ESG-fund level, that is, controversies diversely affect performance and controversies in high-attention areas are able to positively influence performance, linked to information overload and/or return-chasing behavior of past profits in similar controversial events (Aouadi & Marsat, 2018; Blocher, 2016). In addition, controversies related to primary stakeholders (customers and employees) erode performance (Agle et al., 1999). Nonetheless, the performance of pension funds and SRI mutual funds in the top ESG-score terciles is affected by controversies to a lower extent than the performance of these funds in the bottom terciles. Funds with higher ESG scores hold investee firms with lower ESG concerns, and therefore, lower controversies affect performance to a lower extent. Despite this, it is noticeable that the performance of conventional mutual funds in the top ESG-score tercile is largely affected by controversies (vs bottom-tercile fund performance). Dorfleitner et al. (2020) argue that this evidence is driven by the outstanding effect of a few low-rated firms among a majority of non-controversial investee firms.

Table A.3.4 shows the effect on flows by ESG-fund score terciles. The limited reaction of fund participants remains by ESG-score level. This inertia is higher among participants of top ESG-scored pension and SRI mutual funds (Tercile 1). The latter participants may rely on the professional fund management because higher ESG-fund levels might indicate superior ESG skills. In fact, participants of bottom ESG-scored funds (Tercile 3) respond to controversies to a greater extent. The lower ESG-fund standards activate the supervision of fund participants. However, participants only respond to certain controversies, probably because of lax supervision, maintaining the generalized passive conduct. Thus, the passive behavior may also indicate ignorance of investee firms’ controversies.

In our fourth analysis, we take into account that the positive controversy-performance relation found in some controversies may lead fund managers to consider that the market undervalues controversies. Hence, fund managers may choose firms with higher risk of suffering controversies (i.e., greater ESG-firm concern score). In this case, controversies would not be unexpected events. Nevertheless, we previously argue that institutional investors may engage in firms with active shareholding and control CSR issues of investee firms; as a result, past ESG-controversy scores would not be predictive of future controversies. Then, we study whether past ESG concerns of investee firms influence the likelihood of suffering subsequent controversies among fund firms. To develop this analysis, we obtain the quarterly ESG-controversy score of all investee firms studied from 2002 to 2019 (November) from Datastream. This score ranges between 0 (no controversies) and 1 (maximum level of controversies) and measures a firm’s exposure to ESG controversies and negative events reflected in global media. 13 Next, we calculate the quarterly ESG-fund controversy score as the quarterly weighted sum of the ESG-controversy scores of all investee firms held by a fund and the fund-holding weights of all investee firms held by a fund quarterly.

We estimate Logit Model (A.2.9) of Online Appendix 2 to develop this analysis. The logit model allows us to analyze the influence of the ESG-controversy score on the likelihood of suffering controversies by investee firms. Table A.3.5 of Online Appendix 3 shows the results for the 12 controversies studied. Panels A and B shows that, in general, the probability of suffering controversies by investee firms of conventional and SRI pension funds decreases with higher ESG-controversy scores (negative ESG_cont coefficients). In contrast, the probability of suffering controversies by investee firms increases with higher ESG-controversy scores in conventional and SRI mutual funds (Panels C and D). Our findings show that pension funds investing in firms with more ESG concerns are able to monitor, support, and help firms to reduce the probability of future controversial CSR events with active shareholding (Erhemjamts & Huang, 2019; López-Iturriaga et al., 2015; Pucheta-Martínez & Chiva-Ortells, 2020). However, the shorter investment horizon of mutual funds does not allow mutual funds to control CSR controversies when investee firms have a history on controversial events.

Finally, size differences between fund samples may prevent us from making adequate comparisons. To handle this potential concern, previous literature treats larger samples with a matching procedure in which the smaller subset is matched with similar funds in the larger fund subset, reducing linear-regression problems and asymptotic biases due to self-selection (Hartzmark & Sussman, 2019; Sane, 2019). Following previous literature, we apply the nearest-neighbor matching process to achieve higher balance between samples and avoid biases (Ammann et al., 2019; Bilbao-Terol et al., 2017). This method matches the control individuals to the treated group with the smallest distance on fund characteristics (size, age, turnover ratio, expense ratio, managing company, and investment area 14 ), discarding non-matched control individuals (Bilbao-Terol et al., 2017; Kreander et al., 2005). The similarity measure between funds is the propensity score estimated with logistic regression on the fund characteristics mentioned (Bilbao-Terol et al., 2017). Furthermore, control funds are only matched once (cannot be matched multiple times) to build balanced matched samples.

We develop the matching process in two stages. In the first stage, we match mutual funds and pension funds (considering the conventional/SRI nature). In the second stage, we match conventional pension funds with SRI pension funds and conventional mutual funds with SRI mutual funds. The first matching stage provides a more balanced mutual-fund sample; specifically, 359 mutual funds matched with the pension-fund sample, divided into 331 conventional and 28 SRI mutual funds. The second-stage process provides 28 matched conventional pension funds for the 28 SRI pension funds and 28 matched conventional mutual funds for the 28 SRI mutual funds. Consistent with previous studies, our matched samples improve parametric statistical models, showing reduced standardized bias across covariates (Ammann et al., 2019; Bilbao-Terol et al., 2017). We repeat the analyses of sections “The effect of investee-firm controversies on fund performance and flows,” “Reaction of fund managers to CSR-firm controversies,” and “Delayed reactions of fund participants,” and our main conclusions sustain, showing no concerns about sample-size differences (these results are not included for the sake of brevity and are available upon request).

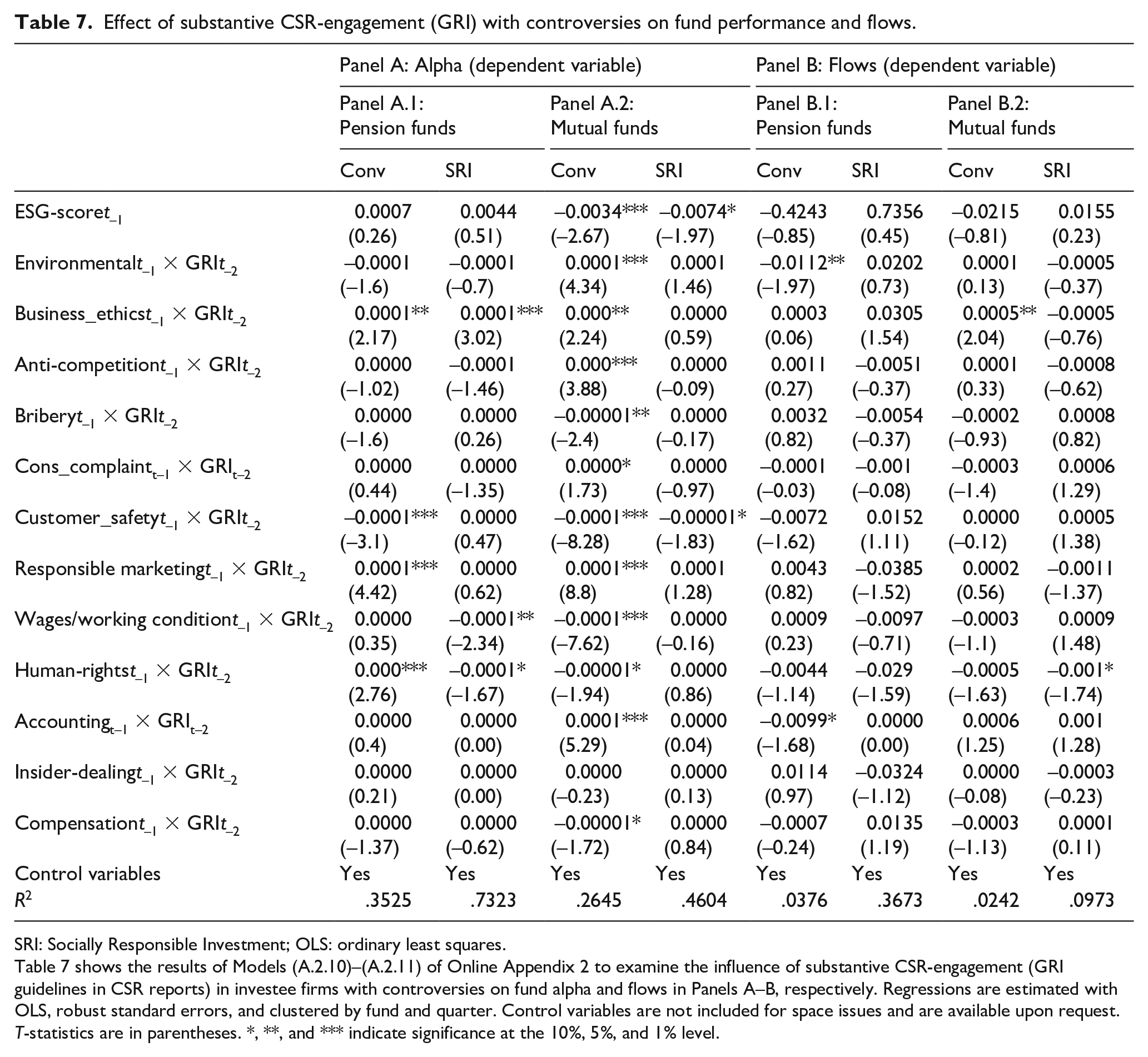

The influence of substantive and symbolic CSR-firm engagement on funds with investee-firm controversies

In this section, we study whether CSR-engagement practices alleviate negative effects of controversies (Nirino et al., 2021) and/or whether markets, participants, and managers penalize firms experiencing controversies after CSR-engagement practices due to insincere behavior. We estimate Models (A.2.10)–(A.2.15) of Online Appendix 2 to analyze the effect of controversies on funds when investee firms have developed substantive and symbolic engagement before suffering controversies.

Table 7 shows the influence of controversies with substantive CSR-engagement (i.e., development of CSR-firm reports following GRI guidelines) on alpha (Panel A) and flows (Panel B). Consistent with H5, Panel A shows diverse impact of controversies after substantive CSR-engagement on alpha. This indicates that the conclusions reached with the results of Table 3 sustain. Specifically, despite substantive CSR-engagement practices, most controversies with negative/positive impact on fund performance follow affecting performance in the same manner. Nonetheless, significant coefficients are lower in Table 7 than in Table 3, that is, substantive CSR strategies soften market reactions (Tamayo-Torres et al., 2019).

Effect of substantive CSR-engagement (GRI) with controversies on fund performance and flows.

SRI: Socially Responsible Investment; OLS: ordinary least squares.

Table 7 shows the results of Models (A.2.10)–(A.2.11) of Online Appendix 2 to examine the influence of substantive CSR-engagement (GRI guidelines in CSR reports) in investee firms with controversies on fund alpha and flows in Panels A–B, respectively. Regressions are estimated with OLS, robust standard errors, and clustered by fund and quarter. Control variables are not included for space issues and are available upon request. T-statistics are in parentheses. *, **, and *** indicate significance at the 10%, 5%, and 1% level.

Panel B shows the influence of controversies after substantive CSR-engagement on flows. The sparse reaction of fund participants confirms the passive behavior of pension-fund and mutual-fund participants, as we find in Table 4. Nevertheless, the negative reactions of conventional mutual-fund participants after controversies disappear with substantive CSR-engagement (Panel B2 of Table 7 vs Panel B of Table 4). Subsequently, conventional mutual-fund participants rely on the accountability of CSR actions developed and published in CSR-firm reports following GRI guidelines. This evidence is consistent with our H6. In addition, we cannot reject H6 because substantive CSR-engagement moderates fund outflows after investee-firm controversies (negative coefficients are lower in Panel B of Table 7 than in Table 4).

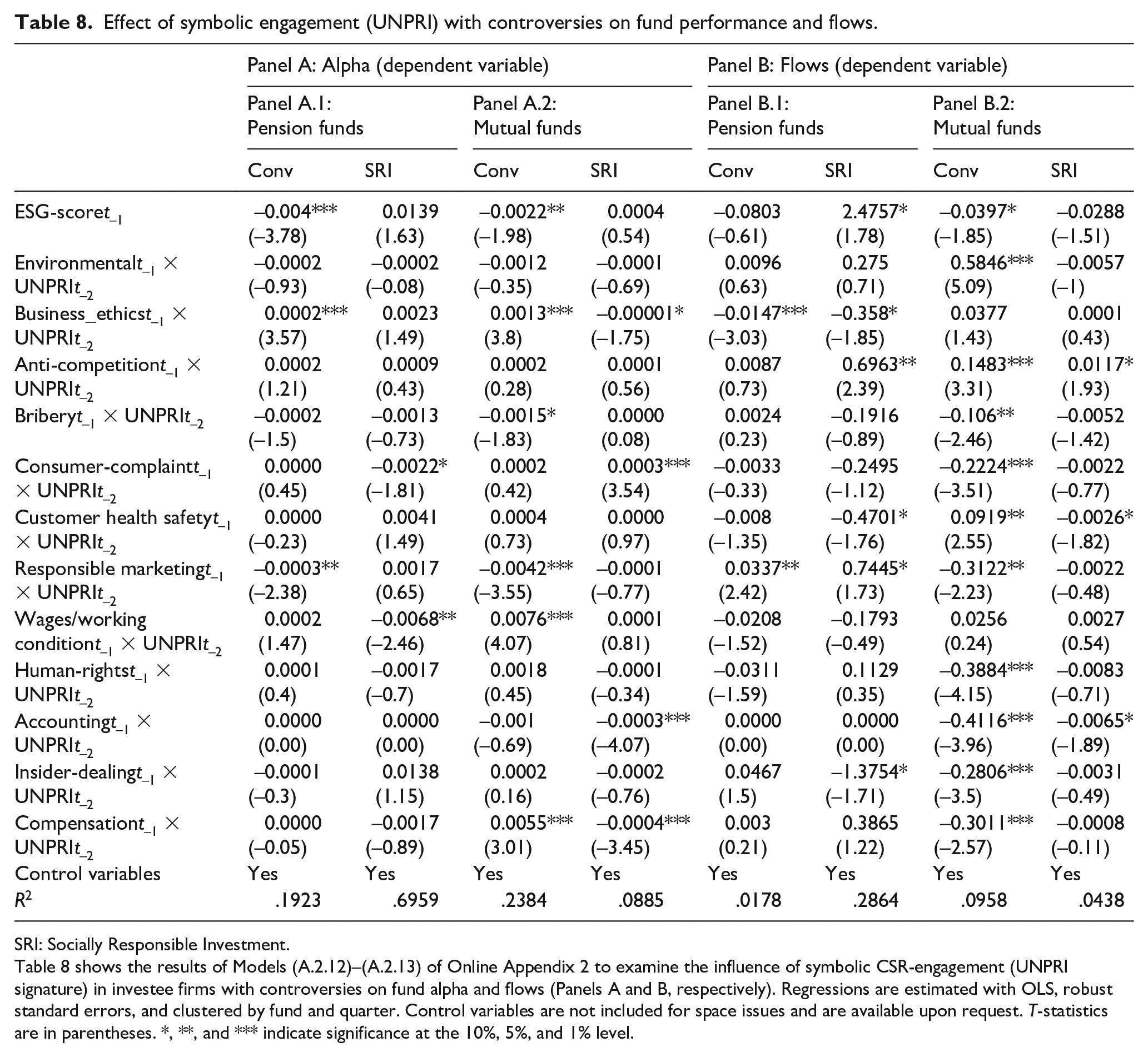

Table 8 shows the effect of controversies after symbolic engagement (i.e., investee firms signing UNPRI principles) on performance (Panel A) and flows (Panel B). Panels A1–A2 corroborate the diverse effect of controversies on performance—evidence that does not allow us to reject H5. Nonetheless, Panel A2 displays that controversies experienced after symbolic strategies have less (more) significant impact on the performance of conventional (SRI) mutual funds than substantive CSR-engagement (Panel A2 of Table 7). The lower cost of symbolic strategies is positively perceived by the conventional niche, softening the impact of controversies on performance. This is particularly observed in controversies with commonly greater economic penalties, such as environmental, customer-safety, or wage controversies (non-significant or significantly positive coefficients in Panel A2 of Table 8 vs significantly negative coefficients in Panel A2 of Table 7 and Panel B of Table 3). In contrast, the SRI mutual-fund performance is negatively affected by controversies after symbolic engagement to a greater extent. The SRI niche possesses more experience in ESG issues and perceives symbolic engagement as hypocrite promises rather than real changes.

Effect of symbolic engagement (UNPRI) with controversies on fund performance and flows.

SRI: Socially Responsible Investment.

Table 8 shows the results of Models (A.2.12)–(A.2.13) of Online Appendix 2 to examine the influence of symbolic CSR-engagement (UNPRI signature) in investee firms with controversies on fund alpha and flows (Panels A and B, respectively). Regressions are estimated with OLS, robust standard errors, and clustered by fund and quarter. Control variables are not included for space issues and are available upon request. T-statistics are in parentheses. *, **, and *** indicate significance at the 10%, 5%, and 1% level.

Panel B of Table 8 displays higher reaction of fund participants toward controversies after symbolic engagement than after substantive engagement (Panel B of Table 7). This result may be explained because firms publicize more the symbolic engagement to draw attention on green-washing strategies (Walker & Wan, 2011). Participants may better identify symbolic strategies advertised because knowing and analyzing substantive initiatives collected in CSR reports following GRI guidelines may take more time. Nevertheless, the greater awareness of symbolic strategies produces diverse effects, showing more flow penalties, especially in conventional mutual funds (Panel B2). Conventional mutual-fund participants do not identify the UNPRI signature as a real commitment to change if firms suffer controversies afterward. We then reject H6 with symbolic engagement; to be precise, symbolic engagement does not moderate outflows with controversies. Panels B1 and B2 also show that fund flows increase with certain controversies after UNPRI signing, displaying the distorting signal of the symbolic CSR commitment and/or higher engagement of institutional investors to repair and amend controversial events with active shareholding. In conclusion, symbolic engagement strategies are able to draw the attention of fund participants and reduce their passive behavior.

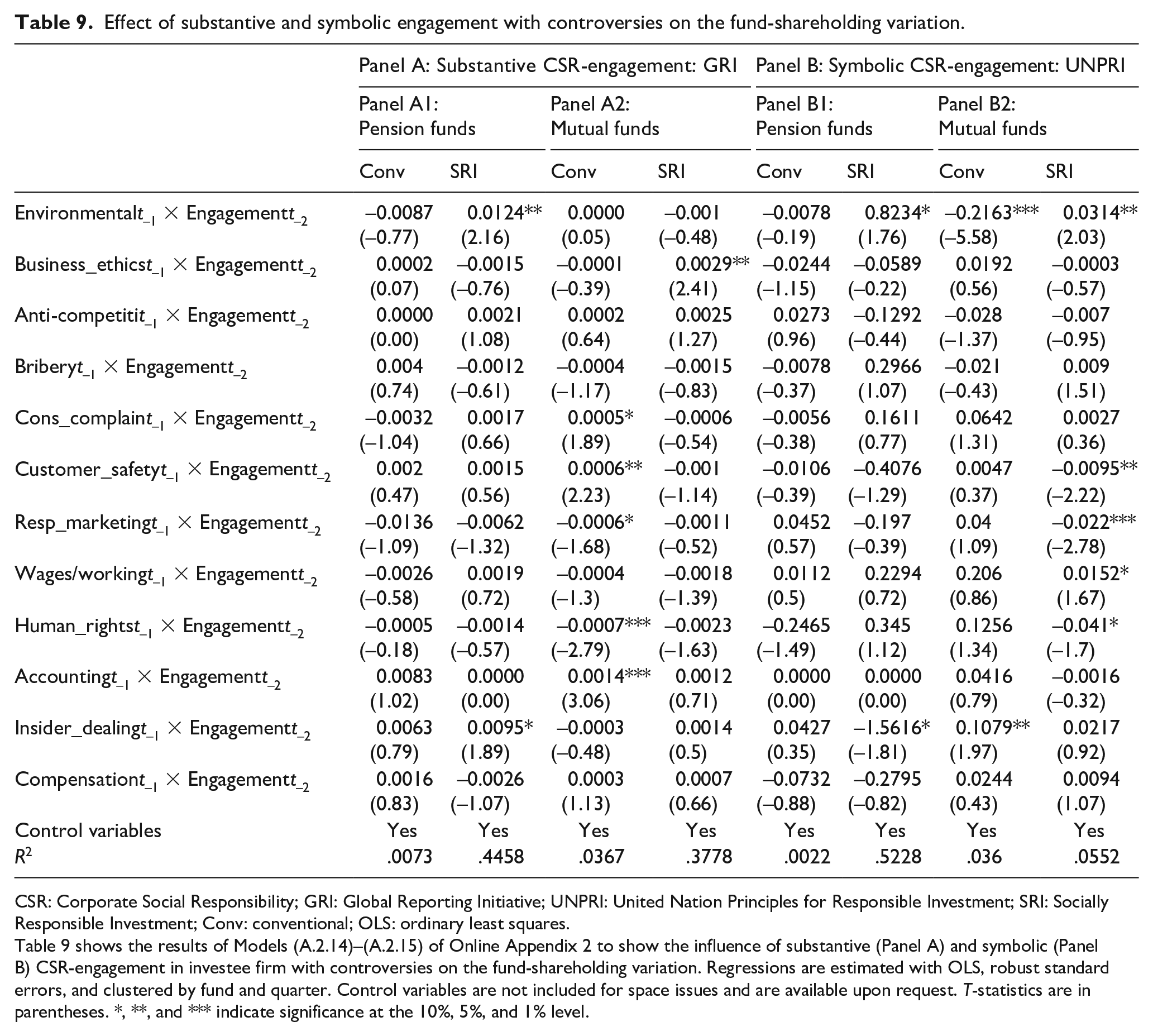

We examine the reaction of managers toward controversies after CSR-engagement strategies in Table 9. Comparing the results of Tables 9 and 5, the inactivity of pension-fund managers remains with substantive and symbolic engagement (Panels A1 and B1 of Table 9). In addition, SRI mutual-fund managers maintain the scant reaction toward controversies with substantive CSR-engagement (Panel A2). This evidence is aligned with the enduring behavior of pension-fund and SRI-mutual-fund participants found with substantive engagement in Panel B of Table 7. Moreover, conventional mutual-fund managers diminish the disinvestment behavior with controversies after substantive and symbolic engagement (Panels A2 and B2 of Table 9 vs Panel B of Table 5). This indicates that managers positively assess CSR-engagement practices since these practices also reduce the market reaction on performance. The latter evidence is consistent with H7 (fund managers do not react negatively to controversies in firms with CSR-engagement practices). However, SRI mutual-fund managers increase the reaction after symbolic engagement (positive and negative coefficients). Thus, our mixed evidence does not allow us to accept H7.

Effect of substantive and symbolic engagement with controversies on the fund-shareholding variation.

CSR: Corporate Social Responsibility; GRI: Global Reporting Initiative; UNPRI: United Nation Principles for Responsible Investment; SRI: Socially Responsible Investment; Conv: conventional; OLS: ordinary least squares.

Table 9 shows the results of Models (A.2.14)–(A.2.15) of Online Appendix 2 to show the influence of substantive (Panel A) and symbolic (Panel B) CSR-engagement in investee firm with controversies on the fund-shareholding variation. Regressions are estimated with OLS, robust standard errors, and clustered by fund and quarter. Control variables are not included for space issues and are available upon request. T-statistics are in parentheses. *, **, and *** indicate significance at the 10%, 5%, and 1% level.

Finally, we apply the robustness tests described in section “Robustness tests” for the CSR-engagement analyses. Our conclusions sustain, showing reliable results (these analyses are not included for the sake of brevity and are available upon request).

Conclusion

Our research provides new insights into the non-explored influence of CSR investee-firm controversies on the two main global institutional investors (pension and mutual funds). We consider CSR controversies in the core environmental, social, and governance areas of the investee firms held by UK conventional and SRI domestic-equity pension and mutual funds.

Our results show that CSR-firm controversies diversely affect fund performance. A positive influence is observed in areas with common information overload and distorted signals (such as business ethics). Controversies related to primary stakeholders (customers and employees) negatively influence pension-fund and mutual-fund performance. Controversies related to more distant stakeholders (environmental and social categories) also affect performance. However, governance issues (shareholders and management) are practically unnoticed by the market, possibly due to their internal character. On the other hand, we study the behavior of fund managers toward controversies. Managers of pension funds and SRI mutual funds do not reallocate portfolios after controversies. This attitude is consistent with the social nature of pension funds and the SRI principles of SRI funds, which incentivize fund managers to engage in active shareholding and improve firms’ long-term sustainability. In contrast, conventional mutual-fund managers decrease the fund shareholdings in investee firms after CSR controversies, guided by the traditional financial principles of conventional investments.

We also examine the conducts of participants toward controversies and managerial decisions regarding controversies. Fund participants display a passive conduct toward controversies (fund flows are barely influenced by controversies). Nevertheless, conventional mutual-fund participants decrease their investment after controversies, guided by the traditional investment principle of disinvestment to deal with unpleased events. In addition, we find distinct attitudes between SRI and conventional participants regarding managerial decisions toward controversies. SRI pension-fund and SRI mutual-fund participants barely react to managerial decisions regarding controversies, revealing persistent preferences and acceptance of managerial decisions. In contrast, conventional pension-fund and conventional mutual-fund participants penalize the managerial decision of supporting firms with controversies.

Finally, we analyze the effect of controversies when investee firms have implemented substantive and symbolic CSR-engagement practices. Developing CSR-engagement strategies before suffering controversies softens market and managerial reactions toward controversies. Nevertheless, fund participants seem to be aware of symbolic CSR-engagement practices to a greater extent and reduces their passive behavior by increasing negative reactions after investee-firm controversies (due to non-real firm transformations with symbolic CSR-engagement practices). Furthermore, we carry out several robustness analyses and our previous conclusions sustain.

Our findings provide a better understanding of participants’ preferences, helping fund managers to know participants’ concerns and guide their conduct in the event of CSR-firm controversies (disinvestment vs engagement). Our results also present interesting information for regulators, identifying the effects of CSR-firm controversial events on these institutional investors and noticing their reactions as leading capital-market members. The generalized scarce reaction of fund participants shows that fund participants should be more aware about their capital allocation and, similarly, fund managers should ensure proper communication about their management regarding controversies to avoid agency problems.

Although our results display new evidence on this topic, further research on other institutional investors and markets may offer a complete picture about priorities and reactions of multiple agents toward CSR-firm controversies. The study of other European markets can complement our findings. The diverse development of mutual-fund and pension-fund industries among Europe may produce uneven responses to CSR-firm controversial events. Differences might be especially relevant among European pension-fund industries because European welfare models (Anglo-Saxon, Continental, Mediterranean, and Nordic) have established various pension systems, causing dissimilar growth among pension-fund industries (Sapir, 2006). Furthermore, the late and scarce European regulation about SRI and ESG for financial markets may produce lower reactions toward CSR controversies (relative to the more advanced UK markets). However, this situation may be changing with the European Commission’s Sustainable Finance Action Plan (European Union, 2019), which introduces the Sustainable Finance Regulation Disclosure. The main provisions of this regulation are applicable from March 2021, requiring sustainability-related disclosures on financial-market participants and financial products (funds). Nonetheless, the European Commission delayed the application of the regulatory technical standards to January 2023 (European Commission, 2022). Despite this, examining the consequences of this regulation on funds’ investment decisions toward CSR investee-firm controversies will be an interesting study. Table A.4.1 of Online Appendix 4 includes a summary of possible expected results for European fund markets regarding the hypotheses studied. Moreover, this article assesses several controversies in the main ESG areas; however, the inclusion of other controversies could provide a comprehensive study. An additional extension may be the analysis of institutional investors as important governance mechanisms in the CSR strategy of investee firms. All these analyses will complete our results.

Supplemental Material

sj-docx-1-brq-10.1177_23409444221110588 – Supplemental material for The reaction to CSR controversies by institutional investors

Supplemental material, sj-docx-1-brq-10.1177_23409444221110588 for The reaction to CSR controversies by institutional investors by Mercedes Alda in Business Research Quarterly

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Ibercaja and University of Zaragoza (Grant JIUZ-2020-SOC-02), Spanish Ministry of Science and Innovation funded by MCIN /10.13039/50110001103, and by ERDF (Grant RTI2018-093483-B-I00) and Government of Aragon (Grant S38_20R).

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.