Abstract

Using arguments from the behavioral theory of the firm, agency theory, and the literature on internal capital markets, this article investigates the relationship between financial slack and firms’ profitability in standalone versus business group–affiliated firms. Using a large sample of French privately held firms, we show that there is a quadratic, inverse U-shape relationship between financial slack and profitability for privately held firms. We observe that the relation is steeper for business group affiliated firms than for standalone firms, which is consistent with the idea that firms in business groups are in competition for the business groups resources. Moreover, we explore whether business groups characteristics and position and weight of a given affiliated firm in the business group organization influence the impact of financial slack on profitability. Our results show that for firms that are closest to the business group head firm and that have a higher weight in the business groups, the quadratic, inverse U-shaped relationship is steeper. These findings suggest that the bargaining power that firms have in business groups plays an important role in explaining the relation between financial slack and profitability.

Introduction

A fundamental idea in strategic management research is that firms need resources and an adequate management of these resources to grow and survive (Barney, 1991; McKelvie & Wiklund, 2010; Nason & Wiklund, 2018; Penrose, 1959; Sirmon & Hitt, 2003). However, what role “excess,” or slack resources play in explaining firms’ performance is less straightforward (Daniel et al., 2004; Mishina et al., 2004; Tan & Peng, 2003). Slack resources represent an amount of assets (financial or human resources) that are not explicitly required for day-to-day operations (George, 2005). In that sense, slack resources are available for other purposes that include the exploration of new business opportunities, the adaptation to new operating conditions or changes in strategy (Bourgeois, 1981). At first look, slack resources bring more flexibility (adaptative function) and represent a buffer against risks that should enhance performance (stabilizing function; Cyert & March, 1963). However, large amounts of slack resources may also cause inefficiencies as a result of agency conflicts (Jensen, 1986) and lower entrepreneurial management attitude (Bradley, Shepherd, & Wiklund, 2011) that negatively affect performance. Accordingly, most of the empirical studies on the topic conclude that there is a curvilinear, quadratic relationship (inverted-U shape) between slack resources and performance (Bradley, Wiklund, & Shepherd, 2011; Tan & Peng, 2003; Vanacker et al., 2013). A substantial body of research has also examined the moderating factors of this relationship ranging from institutional level characteristics (Lee, 2015; Vanacker et al., 2017) to ownership structure (Vanacker et al., 2013), financing conditions (Mousa & Reed, 2013), and entrepreneurial context (Bradley, Shepherd, & Wiklund, 2011; Bradley, Wiklund, & Shepherd, 2011).

Despite these efforts, the slack literature has somehow overlooked the various organizational forms businesses can have. It has indeed been widely acknowledged that firms are not isolated organizations but often belong to business networks, strategic alliances, and business groups (BGs) that provide access to resources outside the boundaries of the firm itself (Lavie, 2006; McKelvie & Wiklund, 2010). Articles in the slack literature either exclude firms that are affiliated to a larger business entity (Bradley, Shepherd, & Wiklund, 2011; Bradley, Wiklund, & Shepherd, 2011) or do not mention whether or not their sample firms are part of a larger business organization, thus assuming some degree of homogeneity among the organizational forms (George, 2005; Vanacker et al., 2017). Focusing on the role of ownership structures, only studies by Kim et al. (2008) and Vanacker et al. (2013) explicitly take into consideration the role played by actors external to strict boundaries of the firm. From a theoretical perspective, the possibility that a given firm belongs to a larger business entity challenges the classical view on the stabilizing and adapting functions of slack. Indeed, if transfers of resources are possible between a given firm and the rest of the business entity in larger, more complex organizations, the accumulation of slack resources at the firm level is less necessary. In other words, if firms that belong to a more sophisticated business structure have access to this structure’s resources, the need to hold slack within the boundaries of the firm is intuitively lower because slack is simply located somewhere else in the business structure and accessible.

Several questions arise from this observation. Are more “complex” business organizations efficient in the resource allocation process? In other words, is the presence of slack at the firm level less important for the performance of a firm that belongs to a more complex business organization? Does the slack–performance relationship at the firm level depend on the larger organization’s characteristics, for instance, because larger organizations have more and manage slack more efficiently? Is there competition between firms belonging to the same business entity to attract resources? Our goal in this article is to propose to answers these questions, which have important managerial implications. Indeed, if the allocation of financial slack is inadequate, because some business entities hold too much or too few slack, both these entities and the overall business structure’s performance is likely negatively affected.

Among the various forms of possible business organizations, one seems especially interesting from the slack resources perspective, namely BGs. BGs are sets of legally standalone firms that are held together by controlling interests, like equity ties (Khanna & Yafeh, 2005). In most countries, BGs represent the most common form of business organization (Carney et al., 2011; Holmes et al., 2018; Khanna & Yafeh, 2007). In Western Europe, more than half of firms are affiliated to a BG and one out of three small firms are affiliated to a BG (Belenzon et al., 2013; Hamelin, 2011). The main characteristic of BGs is the presence of an internal market that allows for resource-sharing activities that mitigate financial constraints (Almeida et al., 2015; Boutin et al., 2013). More specifically, firms affiliated to a BG can share financial resources through intra-group loans, internal trade credit, and equity investment (Chang & Hong, 2000). As a result, firms affiliated to BGs hold less cash (financial slack) because they can raise money fast through the internal market when they detect business opportunities (Locorotondo et al., 2014).

Given the ubiquitous nature of BGs around the world and the unique channel through which firms affiliated to BGs can share resources, it seems important to investigate the relationship between slack resources and performance in BG-affiliated firms. We propose to study this relationship in the context of a developed economy, France, where BG affiliation is more a standard than an exception (Belenzon et al., 2013; Hamelin, 2011) and focus on one dimension of performance, profitability, which is commonly used in the slack literature (George, 2005; Vanacker et al., 2017). French BGs are typically made of one mother firm that creates and retains equity control over multiple subsidiaries, giving rise to pyramidal structures (Colpan & Hikino, 2018; Masulis et al., 2011). Through a diversification process, BGs gradually grow as new subsidiaries are formed or acquired. The BG organizational form is reported to be particularly suited to manage growth in France (Lechner & Leyronas, 2009). Our results show that for standalone firms, the relation between cash holdings and profitability has an inverted-U shape, and this relation is steeper for BG-affiliated firms. In other words, inadequate slack allocation in BG firms is more harmful for profitability than in the case of standalone firms. Having a closer look at BG-affiliated firms, we observe that these results are more salient for smaller BGs. Interestingly, firms that occupy a central position in the BG and those that have a great weight in the BG activities are those that concentrate the “excessive” levels of financial slack. For firms that lie at the periphery of the BG or that have a modest weight in the BG, the relation between financial slack and profitability is linear and positive. In other words, the inefficiencies previously mentioned arise because BG head firms retain too much and do not allocate it to those subsidiaries that most need it. Overall, this study contributes to the stream of research that focuses on the role played by ownership structure on the use of slack resources (Kim et al., 2008; Vanacker et al., 2013).

Theoretical framework

Slack resources and performance

The literature on the role of slack resources is strongly divided into two main theoretical frameworks. On one hand, the behavioral theory of the firm (BTF) posits that slack resources are vital within an organization because they perform several functions (Bourgeois, 1981). First, slack resources represent a buffer against external shocks. During industrial downturns, slack allows firms with high investment opportunities to invest and avoid financial distress costs (Bates et al., 2009). Second, slack resources bring flexibility in the firm’s strategy because it increases the ability to experiment and take risks. Third, slack resources help resolve conflicts within an organization’s top management team (Bourgeois & Singh, 1983). Fourth, the presence of slack resources is an additional motivation for the organization’s members to remain in the organization. For these reasons, the general view of BTF is that slack resources provide the required discretional room to support a firm’s performance and ability to survive (George, 2005).

A fundamentally different approach on the role of slack is found in the agency theory that distinguishes the motivations of shareholders and managers within a firm (Jensen & Meckling, 1976). According to agency theory, managers use some of the firm’s resources in their own interest unless strict governance and monitoring efforts discipline their actions. For example, firms with high cash flows and low investment opportunities do not return cash to their shareholders because managers use cash to pursue their own personal goals (Jensen, 1986). As a result, managers of firms with high slack resources have a large discretional space and they utilize this space to increase their own profit and reputation. Conversely, managers of firms with low levels of slack need to acquire externally resources (bankers in the case of financial resources) and their actions are monitored by these external stakeholders. This results in a disciplinary power of resource constraint (Jensen, 1986).

The extensive empirical literature on the role of slack resources reports that the benefits slack resources provide outweigh the costs and possible inefficiencies of holding them (Bradley, Shepherd, & Wiklund, 2011; George, 2005; Tan & Peng, 2003). In other words, all firms need to hold slack resources to some extent. This, of course, does not mean that it suffices to hold more and more slack to improve performance. Holding resources is one thing, utilizing them and converting them to exploit opportunities is another one (Sirmon et al., 2007; Sirmon & Hitt, 2003). Intuitively, there is a level above which it becomes impossible to exploit an additional opportunity even if there are sufficient slack resources to do so because managers are not able to explore these opportunities (Vanacker et al., 2013; Wang et al., 2016). Once this critical level of slack resources is reached, inefficiencies arise and increase the likelihood of agency issues. Thus, the relationship between slack resources and performance is not supposed to be linear but quadratic (inverse U-shape) indicating that both low and high levels of slack resources are related to lower performance. This view has received empirical support (Bradley, Wiklund, & Shepherd, 2011; Kim et al., 2008; Wang et al., 2016). Consistent with the literature, we, therefore, propose that:

Hypothesis 1. The relationship between financial slack and profitability is quadratic for privately held firms, with a positive linear term and a quadratic negative term.

The role of slack resources for standalone firms and BG-affiliated firms

BGs are sets of legally independent firms tied together by controlling interests and they represent a very common form of business organization in most countries (Khanna & Yafeh, 2007). Although there are various forms of BGs, they all have in common the existence of an internal market that allows the affiliates to share resources (Khanna & Palepu, 1997; Khanna & Yafeh, 2007). In France, the country of our study, BGs are pyramidal organizations with holding firm at the top of the pyramid that centralizes equity control (Almeida & Wolfenzon, 2006; Belenzon et al., 2013). Through the internal market channel, BG affiliates can acquire financial, human, and managerial resources at a lower cost because there is a lower degree of informational opacity between BG affiliates than between an affiliate and an external firm. This internal market is, therefore, likely efficient and allocates resources to affiliates with promising growth opportunities (Gopalan et al., 2007; Khanna & Palepu, 1997; Manikandan & Ramachandran, 2015). Because of this argument, BG affiliation is supposed to be positively related to performance. Whether the effect of BG affiliation is, on average, positive or negative has been extensively studied in the empirical literature. However, no consensus has been reached so far (Carney et al., 2011; Holmes et al., 2018). It appears that BG affiliation might be beneficial in specific contexts, for example, during industrial downturns (Bamiatzi et al., 2014) or in countries with low developments of financial and labor market institutions (Carney et al., 2011) where they fill institutional voids (Leff, 1978).

If a BG internal capital market is efficient, BG-affiliated firms should exhibit the minimum level of financial slack that is required to deal with day-to-day operations (Khanna & Palepu, 1997; Locorotondo et al., 2014). There is indeed no need for them to maintain a high level of slack as any funding required to explore a new opportunity can be provided easily through the internal capital market. Conversely, should a BG-affiliated firm face an unexpected shock, the BG would immediately act to prevent the affiliated firm bankruptcy. Bankruptcies of BG firms are indeed highly detrimental for the entire BG, depending on the role the BG firm plays in the organization (Beaver et al., 2019; Dewaelheyns & Van Hulle, 2006). Due to the imbrication of BG firms and the reciprocal ties they share, a single firm’ bankruptcy can destabilize the whole BG. It is important to acknowledge that institutional differences condition the extent to which a BG can be considered as liable for its subsidiaries’ losses (Belenzon et al., 2018). France is a context where the likelihood that a BG is held liable by a court for its affiliates’ losses is one of the highest in the world. 1 As suggested by the propping literature, BGs would do whatever necessary to avoid such situations, and thus, rescue their distressed subsidiaries through intra-group loans. It follows that BG-affiliated firms need less slack than standalone firms that cannot rely on the internal capital market mechanism to raise money fast when needed. An important implication of this lower need for slack is that the profitability of BG-affiliated depends less on the level of slack held at the firm level.

On the contrary, high levels of slack are less detrimental for the performance of BG-affiliated than for standalone firms since slack in BG firms can be redeployed fast in other BG entities. If a standalone firm has a high level of slack, it can only mobilize its slack for available growth opportunities. In that sense, redeployment of strategic resources is easier in BGs because of their multi-entity form that greatly increases the scope of their operations (Lieberman et al., 2017; Manikandan & Ramachandran, 2015).

In other words, the relationship between financial slack (at the firm level) and profitability (at the firm level) depends on the existence of financial slack at the group level and ability of the BG to allocate slack to affiliated firms when necessary. To be clear, we assume that the existence of a BG organization to which a firm is affiliated increases the overall amount of financial slack that is accessible. Because of this greater pool of financial slack in BGs, the profitability of a BG-affiliated firm depends less on the financial slack held at the firm level. Thus, we hypothesize that the impact of financial slack on profitability is weaker for BG firms than for standalone firms. In other words, the relationship between financial slack and performance is “flatter” for BG firms than for standalone firms:

Hypothesis 2a. There is a lower negative impact of both high and low levels of financial slack on the profitability of BG-affiliated firms when compared to standalone firms.

The previous hypothesis is built on the idea that the internal capital markets of BGs are “efficient” in the sense that firms affiliated to a BG need less to hold financial slack. Having access to the internal market means that the benefits (or costs) on profitability of having (not having) slack is lower than for standalone firms. But what if the internal capital market is not efficient? To be clear, we do not focus on market efficiency in the sense of this term in the finance literature. However, a radically different theoretical approach can be built with the BTF. A key idea in the BTF is that firms are coalitions of individuals that have (at least sometimes) different goals (Cyert & March, 1963). One can think about BGs as coalitions of firms that also have sometimes different goals. For instance, managers of BG-affiliated firms have a motivation to maximize the performance of the firm they manage, even if doing so implies to corner BG resources that could be better used elsewhere in the BG at this very moment. 2 This raises two questions. Can BG-affiliated firms’ managers assess where the BG resources will be best employed? Do these managers want to share the BG resources with other managers? To the first question, the intuitive answer is “most likely not,” and it is the role of the BG head firm to allocate resources where they will be best used. The second question is more interesting and easier to investigate empirically. It suggests that there is competition for the BG resources between the affiliated firms. By comparison, for standalone firms, there is less risk of competition for slack resources because there is only one legal entity. The BG resources, even when they are very large, are limited. This is obviously true for financial slack. In the BTF, slack is considered beneficial for profitability because with enough slack, everyone is “happy” in the coalition in the sense that slack plays a stabilizing role in the organization and reduces internal tensions. However, financial slack is a scarce resource and members of the coalition (BG firms) will compete to access these resources. This competition is a source of inefficiencies in the allocation of slack if some coalition members have a strong bargaining power and a willingness to attract financial slack that exceeds their current needs for slack. Note that the inefficiencies we refer to not only affect the BG overall performance (which is not our focus) but the BG-affiliated firms themselves. If a very powerful subsidiary in a BG keeps the majority of slack while other subsidiaries have growth opportunities, opportunity costs arise. First, the slack–rich subsidiary could gain financial profits by lending financial slack to the subsidiary that have growth opportunities. Second, slack–poor subsidiaries could only benefit from these additional slack resources to explore new business opportunities. By comparison, standalone firms are less affected by such opportunity costs.

Building on agency theory, Scharfstein and Stein (2000) propose a model of internal capital markets in conglomerates in which division managers compete to attract financial resources in their own divisions, because doing so increases their own discretional space. These authors propose that division managers that have a strong bargaining power vis-à-vis the conglomerate’s CEO obtain more financial resources than what they really need, which results in inefficiencies in the internal capital market. If one extends the Scharfstein and Stein (2000) proposition to BGs, firms in a BG can have difficulties in obtaining financial slack from the BG when they need it because other firms with more bargaining power corner financial slack. In such a case, having financial slack at the firm level is at least as important for profitability as it is for standalone firms. In fact, it can be even more important because firms in a BG operate with less cash holdings because of the existence of the internal capital market (Locorotondo et al., 2014). Conversely, firms that corner financial slack because of their greater bargaining power experience opportunity costs, because it would have been more profitable to lend money to other members of the coalition via intra-group loans than to stockpile cash. These opportunity costs negatively affect profitability. These arguments provide a radically different picture of the role of financial slack in BG firms because it suggests that the relation between financial slack and profitability is steeper and not flatter for BG-affiliated firms than for standalone firms:

Hypothesis 2b. There is a higher negative impact of both high and low levels of financial slack on the profitability of BG-affiliated firms when compared to standalone frms.

BG characteristics and place of affiliated firms in the BGs as moderators of the financial slack–performance relationship

It is now important to question if and to what extent factors internal to the BG organization influence the resource-allocation mechanism. A priori, two sets of factors likely play a role in the ability and efficiency with which the internal capital market allocates financial slack across affiliated firms. First, there are important differences between BGs. Second, affiliated firms do not have the same position and weight within the BG organization, and thus not the same bargaining power.

Indeed, BGs are not homogeneous entities, even in a given country, an idea that has been somehow neglected by previous research on BG (Holmes et al., 2018). Some BGs are very large, complex organizations made of hundreds of subsidiaries that generate billions of sales turnover while others are small organizations made of a few subsidiaries. The formation and expansion of BG through the foundations of subsidiaries and acquisitions of other companies is a particular form of growth that is common in Western Europe (Lechner & Leyronas, 2009). BG expansion is the result of a diversification process both at the geographical and industrial levels (Iacobucci & Rosa, 2005, 2010; Hernández-Trasobares & Galve-Górriz, 2016). In other words, firms grow as BGs because this organizational form facilitates the management of multiple and sometimes unrelated activities. For example, the BG structure facilitates the incorporation of new top managers that receive shares of the BG affiliate they manage, which increases their motivation (Iacobucci & Rosa, 2010).

A simple but important factor that distinguishes BG is their respective size. Larger BGs provide access to a larger and more diversified set of resources (Colli & Colpan, 2016; Manikandan & Ramachandran, 2015). Larger BGs have, for example, larger, and potentially more efficient, internal capital markets, and they have, everything else being held equal, a greater capacity to allocate financial slack (Locorotondo et al., 2014). On the contrary, small BGs are not very different from standalone companies in terms of diversification of activities, market power, and access to resources (Lechner & Leyronas, 2009). In Western Europe, small BGs are “patient” firms that promote growth and performance for their affiliated firms in the long term (Hamelin, 2011). At the same time, small BGs may lack financial skills and overall access to financial resources to efficiently allocate slack resources (Belenzon et al., 2013). We, therefore, propose that larger BGs are both more powerful (they have more financial slack) and efficient in the allocation of slack resources across affiliated firms. It follows that the impact of financial slack on the profitability of affiliated firms should be lower, both for high and low levels of financial slack for firms affiliated to larger BGs. Indeed, if larger BGs have more efficient internal markets, the current level of financial slack that an entity has is not important because the internal market will react fast to any need for or accumulation of financial slack should an external shock occur or a business opportunity be available. We, therefore, propose that the relation between financial and profitability flattens in larger BGs:

Hypothesis 3. The negative impact of both high and low levels of financial slack on profitability is lower for firms affiliated to larger BGs when compared to smaller BGs.

The previous hypothesis focuses on an important characteristic of BGs. However, it is also likely that the role of a given affiliated firm within the BG organization affects the relationship between financial slack and profitability. We previously argued that the allocation of slack in BG-affiliated firms is the result of a competition between these firms, assuming that BG firms’ managers have an intrinsic motivation to corner resources at their own benefit. Managerial pressure to seek performance can lead some subsidiaries to accumulate more slack than what is required (Diwei Lv et al., 2020). Following this idea, it seems reasonable to identify factors that could measure the ability of some BG firms to attract resources. For instance, Ayyagari et al. (2015) and Gubbi et al. (2015) provide evidence that the centrality of the position of a firm in the BG structure contributes to explain not only the ability of a firm to attract BG resources but also the reactivity with which these resources are mobilized into new business opportunities. We thus focus on two factors that measure the strength of bargaining power of a BG firm in the organization, namely the distance of a given firm to the BG head firm (Gubbi et al., 2015) and the weight of a given firm within the BG (Scharfstein & Stein, 2000).

Our argument here is that further an affiliated firm is from the BG head firm, more difficult it is for information, and thus for slack resources to circulate freely. It is indeed more difficult for BG head firms to identify needs for financial slack or excess levels of financial slack in affiliated firms that stand at the periphery of the BG than for affiliated firms that are very close to them. Centralization of control, which is higher when direct equity ties exist between the BG head and its affiliates, is a fundamental aspect of the benefits BG affiliation provides (Mahmood et al., 2017; Masulis et al., 2011). Ayyagari et al. (2015) show that affiliated firms that stand at the center of a BG have a higher degree of reactivity to answer market entry from rival firms that benefit from foreign investments. Indirectly, their results suggest that firms occupying a central position in a BG have more direct access to the BG resources and a greater capacity to attract the BG resources. Assuming a pyramidal organization within the BG (which is standard in Western Europe, the context of this study), we propose that firms that stand closer to the top of the pyramid (the “core” of the BG) are more likely to have inadequate level of financial slack. Indeed, such firms are in privileged position to obtain financial slack from the BG because they are closer to the BG head firm. Their bargaining power is thus higher. Indeed, because BGs are pyramids, firms closer to the BG head firm are also the older ones and those that have activities very close to the head firm core business (Iacobucci & Rosa, 2005; Lechner & Leyronas, 2009). Because firms close to the BG head firm have a greater bargaining power, their capacity to accumulate and retain excessive levels of financial slack is also higher. It follows that these firms experience opportunity costs if other firms in the BG could have made a better use of financial slack since lending money from one BG firm to another generates financial profits. Overall, the relationship between financial slack and profitability is expected to be steeper for affiliated firms that are closer to the BG head firm:

Hypothesis 4. The negative impact of both low and high levels of financial slack on profitability is higher for firms standing at the center of the BG than for firms standing at the periphery of the BG head firm.

Finally, we propose that the weight of a given firm in the BG organization influences the relation between financial slack and profitability. Not all BG-affiliated firms contribute in the same way and to the same extent to the overall performance of the organization. Typically, as BGs grow, they use their newly founded subsidiaries as “experience labs” for innovation and internalization (Iacobucci & Rosa, 2010; Lechner & Leyronas, 2009). New subsidiaries are created in BGs when previous activities in other subsidiaries reach maturity (Iacobucci & Rosa, 2005). However, the extent to which BGs expand through the creation of additional subsidiaries also depends on institutional context. In the case of France, the strictness of enterprise liability tends to constrain the growth of BG, which also implies that BG growth in France may be slower than in other countries (Belenzon et al., 2018).

It follows that the direct contribution to the performance of BGs is different between BG-affiliated firms. Resource-allocation decisions should be motivated by the importance subsidiaries play in the organization, meaning that affiliated firms that contribute most to the overall performance of the BG should receive more slack than less important entities, holding everything else equal. It is also important to acknowledge that some affiliated firms may attract more resources than what they need. As proposed by Scharfstein and Stein (2000), influential managers of an organization’s entity can pressure CEOs to obtain more from the organization’s resources than what their entity really needs. These authors point out the risk that such “rent-seeking” intermediate managers benefit from generous capital-budgeting decisions that are, overall, detrimental for the entire BG and, thus, for other entities within the BG. The work of Scharfstein and Stein (2000) does not consider BGs, however, for US conglomerates in which divisions’ managers try to attract as much resources as possible from the organization, their arguments make sense for managers of firms affiliated to a BG. Gubbi et al. (2015) provide results that echo the model of Scharfstein and Stein (2000) as they show that firms that have a prominent position in a BG have a greater bargaining power and ability to attract BG resources. Because our focus is on the relationship between financial slack and profitability for affiliated firms and not at the global BG level, we propose that the risk of inefficient financial slack allocation is higher for affiliated firms, which play a greater role in the BG. Indeed, these firms are those that have the highest bargaining power in the BG organization. Specifically, we propose that the relationship between financial slack and profitability steepens for affiliated firms, which have a higher weight in the BG performance:

Hypothesis 5. The negative impact of both low and high levels of financial slack on profitability is higher for firms that have a greater weight in the BG structure than for firms that have a smaller weight in the BG structure.

Methods

Sample

Our source of information is the Amadeus database provided by Bureau Van Dijk. Amadeus offers access to accounting and financial data for public and private European firms of various sizes. This database has been successfully used by prior research on slack resources (Vanacker et al., 2017) and BG affiliation (Belenzon et al., 2013) and is considered as one of the best available in terms of coverage and reliability. Although Amadeus grants access to firms operating in many European countries, we restrict ourselves to only one country, France. Our motivation to do so is threefold. First, cross-country studies on the role of BG typically suffer from the lack of comparability between the institutional settings that explain the existence of BG (Holmes et al., 2018). As a result, BGs are heterogeneous in their internal organization, ability to allocate resources, and more crucially in the nature of the ties between the affiliates depending on the considered country (equity based, family based, business networks, see the study by Khanna & Yafeh (2007) for a review). Focusing on only one country helps us alleviate the concerns that the forms BGs take influence our results and that other factors (like fiscal policy and income tax rates) influence our results. Second, BGs are numerous in France, making it an interesting field of study (Belenzon et al., 2013; Hamelin, 2011). Indeed, more than two-thirds of our sample firms are affiliated to a BG. The presence of so many BGs in France is largely related to the relative low developments of public equity markets when compared to North America (Belenzon et al., 2013). Third, French BGs are typically organized as pyramidal structures of multiple independent firms controlled by a holding company that centralizes equity ties. This organizational design facilitates the transmission of BG from one generation to another in family firms (Masulis et al., 2011). Thus, the identification of the BG boundaries is easier because they are based on equity ties and not on more informal ties, which is the case in other countries (Khanna & Yafeh, 2005). These arguments make France an interesting field of study for our research.

We collect data over the 2009–2018 period as Amadeus has a 10-year extraction limit. We exclude firms that operate in the financial industry from our sample as the role of slack resources for banks and investment funds is out of the scope of this article. We also exclude firms listed on stock markets because financing decisions are rather different between publicly listed firms and privately held firms. For instance, Brav (2009) shows that the sensitivity of capital structure decisions to performance is stronger in privately held firms. Furthermore, because the low development of financial markets in France explains the presence of BGs, it seems cautious to restrict the sample to privately held firms (Belenzon et al., 2013). The sample after excluding missing information represents 87,847 privately held French firms. Of that, 61,119 firms are affiliated to a BG and 26,728 are standalone small firms. They represent 402,891 firm-year observations for the first part of the analysis and 99,600 (19,820 individual firms affiliated to BGs) for the second part of the analysis. We identify firms affiliated to a BG as follows. Amadeus provides for each firm the number of firms within the BG to which the firm is affiliated, this number being zero for standalone firms. Firms are considered affiliated to a BG if the BG head firm has, directly or indirectly, at least 50% of the control rights. Importantly, this means that BG head firms do have the power to allocate resources across their affiliates. We winsorize all our observations at the first and 99th percentiles to mitigate the influence of extreme values.

Dependent variable

We consider one dimension of performance, namely profitability. We measure profitability as return on assets (ROA) and make it our dependent variable. ROA is the ratio of operating income to total assets and has been commonly used in research both on slack resources (Bradley, Shepherd, & Wiklund, 2011) and on the role BG affiliation (Hamelin, 2011; Khanna & Palepu, 2000). There are, of course, alternative measures of performance and profitability like gross profit, defined as sales turnover less cost of goods sold divided by total assets (George, 2005; Vanacker et al., 2017). Still, to ensure comparability across studies, we use alternative definitions of profitability with similar results. Concretely, we use both EBITDA (earnings before interest and taxes) and net income over total assets as alternative profitability measures and obtain comparable results. We use a 1-year lag between ROA (t + 1) and all our independent and control variables (t) to partially limit the risk of endogeneity between profitability and financial slack. One year is indeed considered by the literature as a sufficient time for firms to redeploy slack resources (Vanacker et al., 2017).

Independent variable

There are several forms of slack resources that have been found to drive firms’ performance, like human resources slack (Kiss et al., 2018) and research and development slack (Mousa & Reed, 2013). However, our focus is on the role of financial slack, which is the most commonly explored form of slack (Bradley, Shepherd, & Wiklund, 2011; Bradley, Wiklund, & Shepherd, 2011; Kiss et al., 2018; Mousa & Reed, 2013; Vanacker et al., 2017). A fundamental advantage of financial slack is the speed at which it can be redeployed whenever necessary. Other forms of slack are sticky and their use in empirical analysis requires longer time horizons (Bradley, Wiklund, & Shepherd, 2011). The literature distinguishes between different forms of financial slack that are based on their availability and the degree of discretion with which they can be used (Bradley, Wiklund, & Shepherd, 2011; Bromiley, 1991). Cash is considered as a high-discretion financial slack resource because it can be allocated fast and in many different ways (George, 2005).

We create our financial slack measure following the article of Wang et al. (2016). Specifically, we measure slack as the residuals of a first-step regression in which we regress a firm’s cash ratio, calculated as cash and equivalents divided by total assets, on a set of variables known to influence the amount of cash that firms hold (Bates et al., 2009; Locorotondo et al., 2014). We regress the cash ratio on a firm’s size (natural logarithm of number of total assets), age (natural logarithm of number of years since firm creation), leverage (short-term debt and long-term debt over total assets), net operating working capital (inventories plus accounts receivable less accounts payable over sales), and a dummy variable that takes the value 1 if a firm is affiliated to a BG and 0 otherwise. Because the industry in which a firm operates and macroeconomic conditions influence a firm’s cash holdings, we run separate regressions for each industry, using four-digit standard industrial classification codes (SIC), and year. The rationale behind our approach is that the variables we use as regressors determine the “normal” level of cash that firms should hold and that the residuals of the regressions thus represent slack or excess levels of cash. The use of a regression-based financial slack is the standard approach in the study by Wang et al. (2016) and has been used as a robustness test by other studies (Vanacker et al., 2017). Crucially, our approach ensures that we capture the fact that standalone firms and BG firms can operate efficiently at different levels of financial slack and that the level of slack depends on BG affiliation. Still, we present the results with the standard cash ratio as an alternative independent variable with comparable results (see Model 3, Table 3).

Moderating variables

In the first part of the empirical analysis, we compare standalone firms and BG-affiliated firms. To identify BG-affiliated firms, we use a dummy variable BG affiliation, which takes the value 1 if a firm is affiliated to a BG and 0 otherwise. BG affiliation is identified in Amadeus as the number of firms within the BG to which a firm is affiliated, providing the BG head firm has at least 50% of direct or indirect control rights over the considered firm. It is important to notice that this variable is static because Amadeus only provides this variable for the most recent year available and we acknowledge this as a limitation of our study. However, two arguments mitigate this issue. First, most French BGs are “small” and made of less than five subsidiaries, so changes in the composition and structure of BGs are rare (Deroyon, 2016; Hamelin, 2011). Second, the growth process of BG is slow. It takes dozens of years for BG to emerge, and even very old BG incorporate only a few firms (Iacobucci & Rosa, 2005; Lechner & Leyronas, 2009). These arguments suggest that over a 10-year period, it is unlikely that important changes in the structure of BG affect our result.

In the second part of the empirical analysis, we consider only the subsample made of firms affiliated to a BG. Following our hypotheses, we create a variable that measures the size of a BG. BG size is measured as the natural logarithm of total assets. We also create two variables to capture the distance of a given affiliated firm from the BG head and the weight of a firm in the BG. Distance from head firm is calculated as the position in the BG which is the ratio of a given firm’s number of subsidiaries divided by the total number of affiliated firms in the BG. Thus, firms at the periphery of the BG have a low value of position (0 if they don’t have subsidiaries themselves) and firms close to the BG head firm have a position that is close to one. We acknowledge that this measure is not perfect. For instance, if a firm is directly controlled by the head firm but has no subsidiaries, our position variable takes the value zero. However, given the pyramidal structure of French BG, we believe that this measure can still provide useful empirical insights. Last, we calculate the weight in the BG as a given firm’s sales divided by the BG total sales. It is important to notice that we use BG total assets to measure the BG size and a different variable (sales) to measure the weight within the BG. Indeed, using the same size variable as the one used as the denominator of a ratio leads to biased results (see George, 2005 and Vanacker et al., 2017 for a comment of this issue). BG total assets are directly taken from the Amadeus database because for each firm an identification number of its BG head firm is available and makes it possible to extract consolidated BG accounting information in a second time. Alternatively, we use the number of firms in the BG as a measure of size and obtained comparable results.

Control variables

Following previous articles on the relationship between financial slack and profitability, we include a number of control variables that can simultaneously impact financial slack and profitability. These control variables are created at the firm level, at the BG level (for the second part of the analysis), at the industry level, and at the regional level.

First, we include firm’s size and age because larger and older firms have been reported to hold different levels of slack resources. Size is calculated as the natural logarithm of the number of total assets and age as the natural logarithm of the number of years since firm’s creation. Second, the extent to which a firm’s assets are tangible is the measure of operating risks and fixed costs, which influence profitability (Grau & Reig, 2021). We calculate asset tangibility as the ratio of tangible assets (properties, plant, and equipment) over total assets. Third, income tax rate influences the cost of raising external debt when compared to the opportunity of having slack resources (Serrasqueiro & Maças Nunes, 2012). It is also possible that BG smooth their affiliated firms’ revenues for taxing considerations (Gramlich et al., 2004; Klassen et al., 1993). We calculate income tax rate as income tax divided by earnings before tax. Fourth, there are other forms of slack that should be controlled for. The amount of current assets firms hold also represents a form of financial slack sometimes referred to as recoverable slack (Bradley, Shepherd, & Wiklund, 2011). However, not all the current assets can be converted into cash because a fraction of them is required to cover the needs of current liabilities. Thus, we use a firm’s working capital, calculated as inventories and accounts receivable less accounts payable scaled by total assets (Mousa & Reed, 2013). Because working capital and cash are substitutes, the inclusion of working capital as a measure of recoverable slack is important (Baños-Caballero et al., 2012; Bates et al., 2009). Following Vanacker et al. (2017), we subtract to a firm’s working capital the annual industry mean working capital. Potential slack is another form of financial slack that is related to a firm’s remaining capacity to raise money from external sources. The common measure of potential slack is the ratio between total financial debt (short term plus long-term debt) over total assets. Controlling for potential slack is important because firms may hold different levels of cash depending on their ability to externally raise money fast. Again, we subtract to a firm’s ratio between financial debt and total assets the annual mean industry financial debt to total assets ratio. Vanacker et al. (2017) indicate that human resources (HR) slack also represent an important form of slack resources that affects profitability. Therefore, we calculate HR slack as the ratio of the number of full-time equivalent employees divided by sales less the annual industry mean ratio of full-time equivalent employees divided by total sales (Vanacker et al., 2017). We include the squared terms of the three slack control variables (recoverable, potential, and HR slack) in the regressions to take into account the nonlinear relationship between slack and profitability.

We also include BG-level controls in the second part of the empirical analysis. We control for the location of the BG head. Indeed, BGs are very common in France, but not all BGs are controlled by French firms. French BGs may be more “patient” regarding the value-creation process while foreign-based BGs may require higher profitability. Furthermore, international differences in taxing systems probably need to leave financial slack in affiliated firms rather than bringing cash back for foreign-based firms. We, therefore, use a dummy BG Head French, which takes the value 1 if the BG head firm is located in France and 0 otherwise. We also include the natural logarithm of the number of shareholders as a control variable to account for tunneling. Indeed, if the BG head firm is the single shareholder, tunneling is ruled out. On the contrary, the probability of tunneling increases with the number of other shareholders, which are in our case minority shareholders since the BG head holds at least 50% of total control.

We also include three industry-level controls as in the study by Vanacker et al. (2017). First, we account for industry complexity as measured by the sum of the squared market shares of each firm within a given industry (Hirschmann–Herfindahl index). Market share is the ratio of sales over the industry total sales. Second, we measure competitors market power as the average size of competitors within an industry. Third, we include the mean annual industry ROA (Jung et al., 2019). We classify firms into different industry categories by using four-digit SIC codes.

Last, we include a set of dummy variables to account for the impact of geographic location using the French administrative classification into 104 regions called “départements.” Indeed, it is well known that firms agglomerate in well-delineated regions to benefit from externalities related to the resources offered by a given geographical context (McCann & Folta, 2008). France is a highly centralized country and there are great differences between rural contexts and urban contexts that we can capture with these dummy variables.

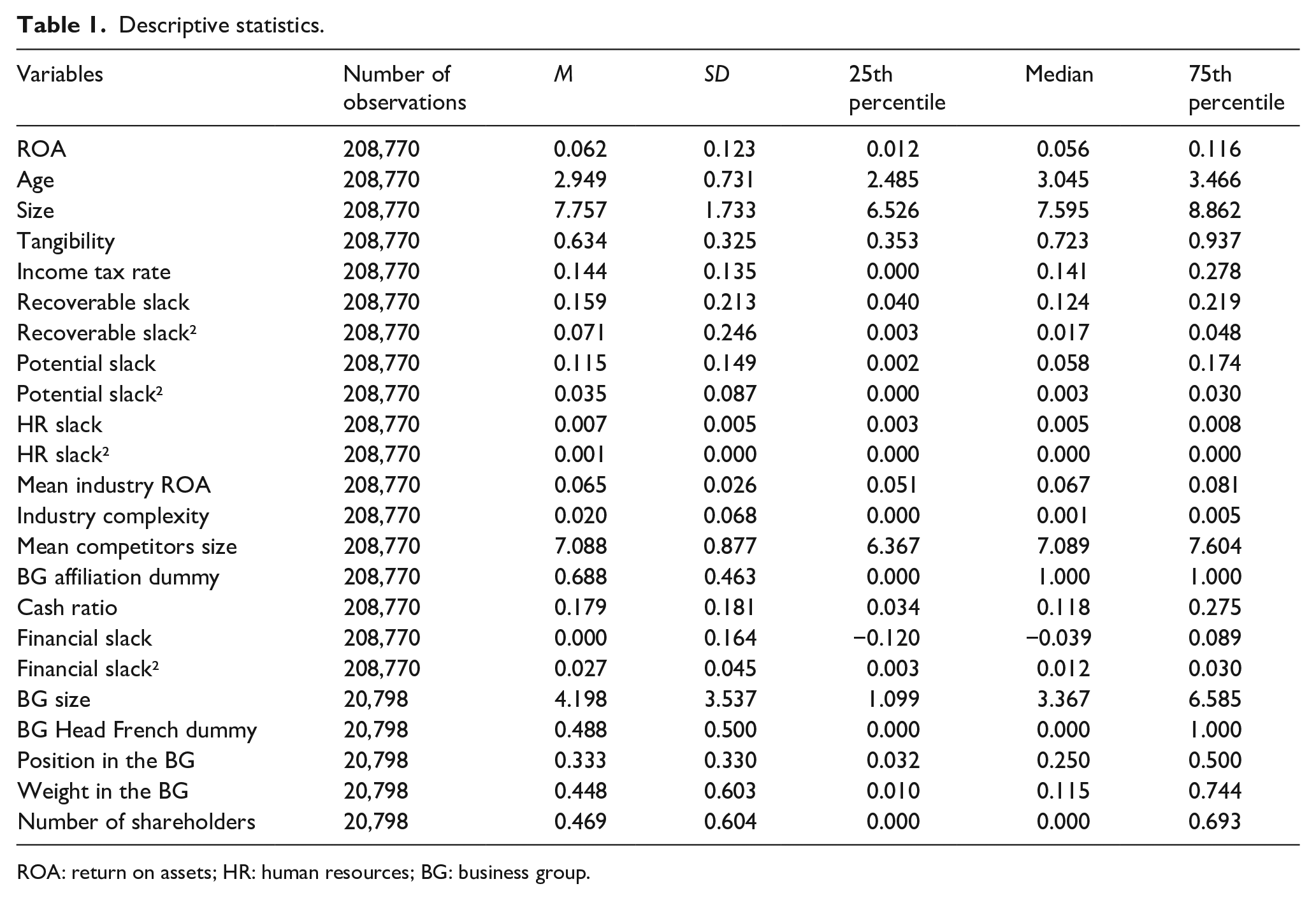

Descriptive statistics

We present the summary descriptive statistics in Table 1 below. The average firm is 19.1 years old and hold 2.34m euros of total assets. The mean ROA is 6.2% (median is 5.6%) and 68.8% of our sample firms are affiliated to a BG, a figure that highlights the ubiquitous nature of BGs in France but is in line with previous studies (Belenzon et al., 2013). The average cash ratio is 17.9% (median is 11.8%) and the mean of our financial slack measure is 0.0% (median is −0.38%). The average BG holds 66.6m euros total assets indicating that many BGs are rather small. We do not report a full table with descriptive statistics for standalone firms and BG firms for brevity. Still, there are important differences between these two categories of firms. Standalone firms are more profitable (mean ROA is 7.3% versus 5.7%), younger, smaller, and more leveraged than BG firms. More importantly, standalone firms hold much more cash than BG firms (mean is 24.3% of total assets versus 15.6%). The mean financial slack is 0.002 for standalone firms and −0.002 for BG-affiliated firms, and the difference is statistically significant (p = .000).

Descriptive statistics.

ROA: return on assets; HR: human resources; BG: business group.

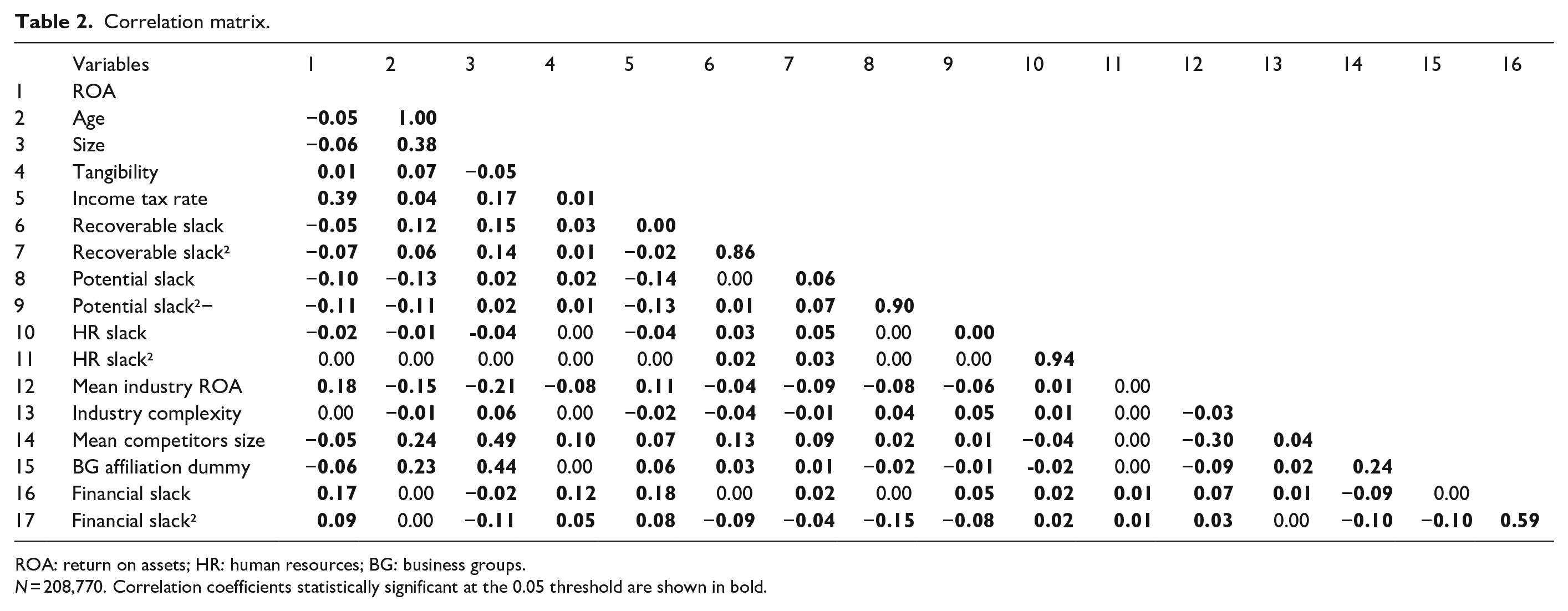

Table 2 provides a correlation matrix for the variable used in the first part of the empirical analysis where we compare standalone and BG-affiliated firms. A correlation matrix for all the variables used in the second part of the analysis where we consider only BG-affiliated firms is available upon request to the author. We ensure that multicollinearity is not an issue by calculating the variance inflation factors (VIFs). The highest VIF is 1.78 and the mean VIF is 1.18, which is well below the commonly accepted level of 5, so multicollinearity does not severely affect our data.

Correlation matrix.

ROA: return on assets; HR: human resources; BG: business groups.

N = 208,770. Correlation coefficients statistically significant at the 0.05 threshold are shown in bold.

Analysis and results

Comparing BG-affiliated firms and standalone firms

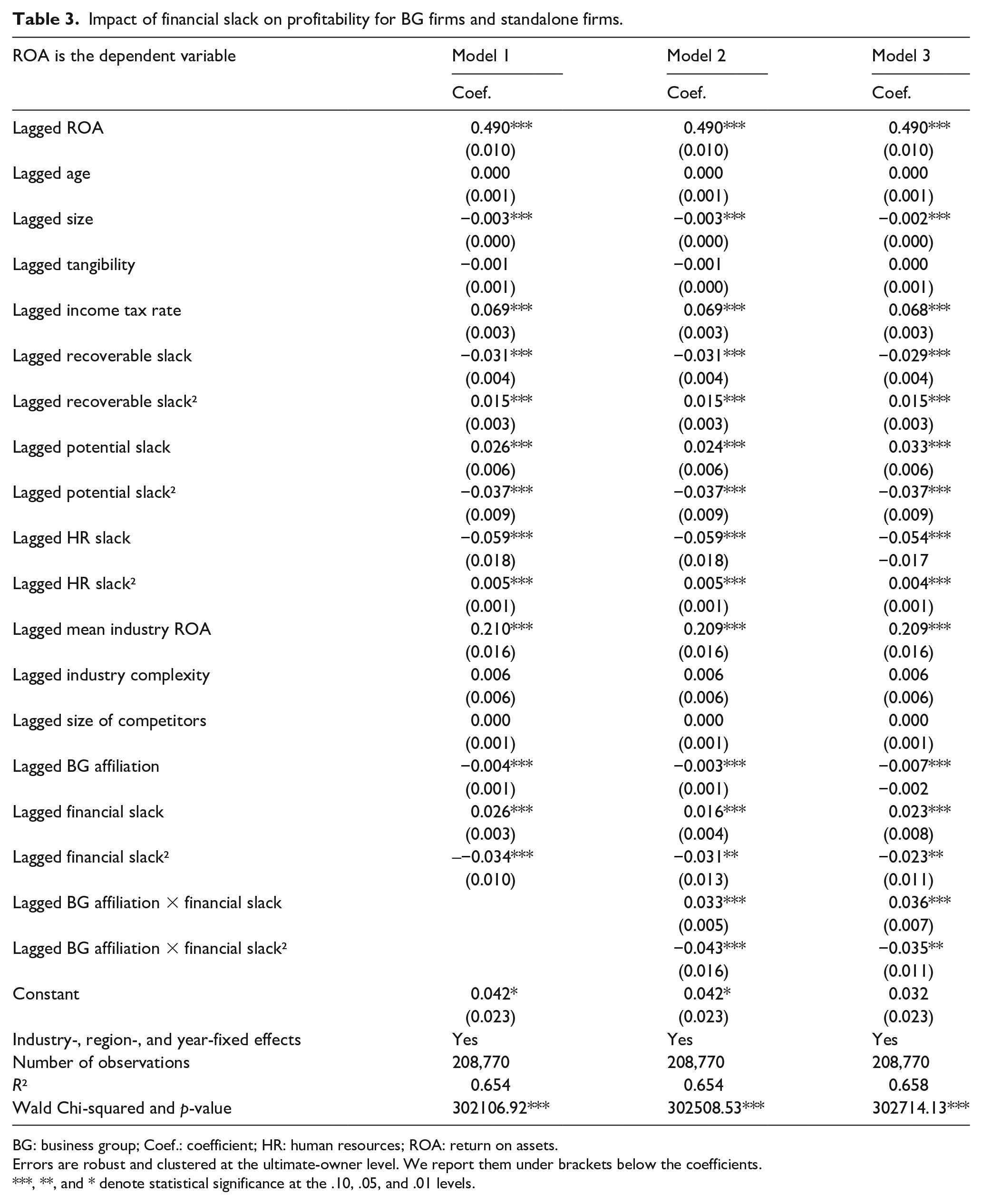

We begin our multivariate analysis by comparing the relation between financial slack and profitability for BG-affiliated firms and standalone firms. Our econometric approach is a firm random-effects with industry and year-fixed effects model to account for heterogeneity across firms and industries as well as macroeconomic shocks, which could affect the benefits of holding financial slack. 3 The standard errors are robust and clustered at the ultimate-owner level, meaning the BG for BG-affiliated firms. We alternatively use generalized estimated equations and obtained similar results (results unreported but available upon request). We report the results of regressions where the dependent variable is a firm’s profitability (ROA) and the independent variable is the amount of financial slack (and its squared term) lagged by 1 year in Table 3. We lag our independent and control variables by 1 year to ensure the direction and causality. One year is generally considered as a sufficient period of time to redeploy slack resources but we also use a longer time-lag in the robustness tests (Vanacker et al., 2017). We also include the lagged value of ROA as a control variable because profitability is largely persistent over time. However, in unreported regressions, we observed identical results when we did not include lagged ROA as an additional control. Including the lagged value of ROA provides conservative results regarding the magnitude of the coefficients of our independent variables. Squared terms for three other forms of slack resources (recoverable, potential, and HR slack) are included following recommendations by previous works (Bradley, Shepherd, & Wiklund, 2011).

Impact of financial slack on profitability for BG firms and standalone firms.

BG: business group; Coef.: coefficient; HR: human resources; ROA: return on assets.

Errors are robust and clustered at the ultimate-owner level. We report them under brackets below the coefficients.

, **, and * denote statistical significance at the .10, .05, and .01 levels.

In Table 3, Model 1 includes the BG affiliation dummy and the linear and squared terms of financial slack. According to Hypothesis 1, we expect a quadratic relation between financial slack and profitability with a positive linear term and a negative squared term for financial slack. The linear term for financial slack is positive and statistically significant (p = .00) and the squared term is negative and statistically significant (p = .00) in Model 1. These results are necessary but not sufficient conditions to the existence of a quadratic, inverse U-shaped relationship between financial slack and performance, because the turning point could lie outside the data range (Haans et al., 2016). Following the recommendation of Haans et al. (2016), we apply the three-step methodology of Lind and Mehlum (2010) using the “utest” command available for Stata 16. The first step is to ensure that the squared term is negative and statistically significant. The second step is a Sasabuchi’s (1980) test to reject the joint null hypotheses that the effect of financial slack on performance does not increase (decrease) at high (low) values of financial slack. The t-value for Sasabuchi’s test is 3.05 (p =

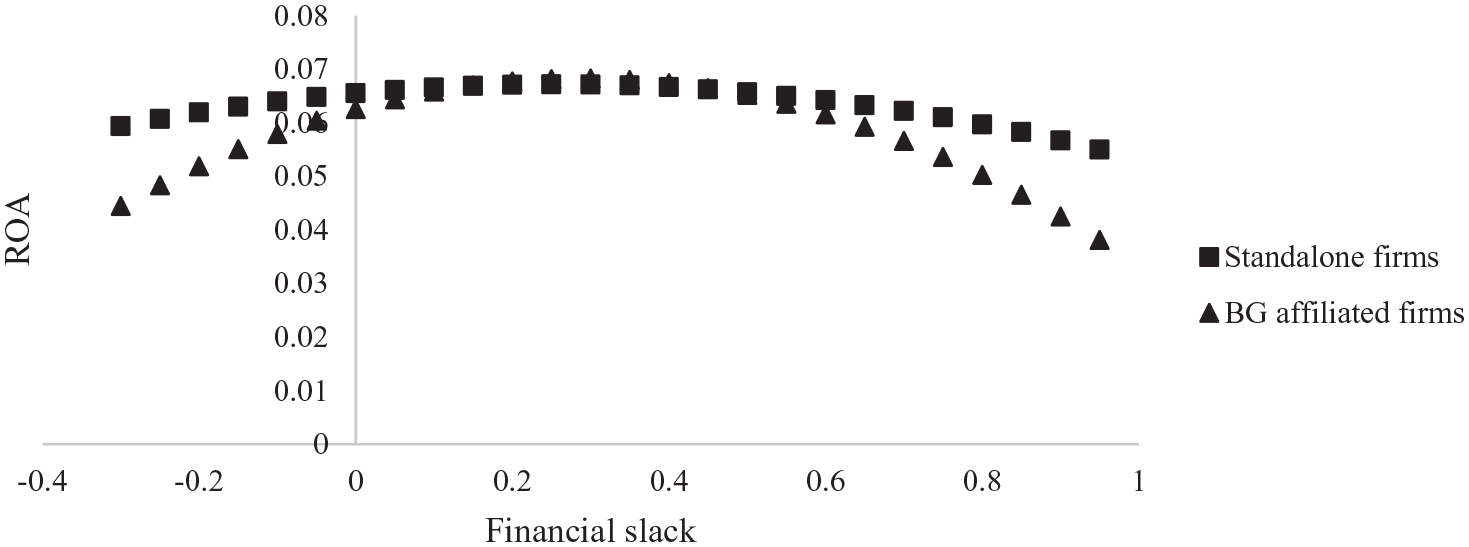

We now turn to Hypothesis 2 in which we predict that the relationship between financial slack and profitability flattens for BG-affiliated firms as a result of their access to the BG internal capital market. This means that we hypothesize that the interaction between the BG affiliation dummy and the squared financial slack term is positive. Model 2 is the fully specified model in which we include the interactions between the BG affiliation dummy and both the financial slack and squared financial slack terms. The results are as follows. First, for standalone firms the linear term is still positive and statistically significant (p = .00) and the squared term is negative and statistically significant (p = .02). The three-step Lind and Mehlum (2010) procedure confirms the existence of quadratic, inverse U-shaped relationship between financial slack and profitability for standalone firms as the t-value for Sasabuchi’s test is 1.97 (p = .02) and the turning point is 0.26, which is well within the data range. Second, for BG-affiliated firms, as the squared term is negative and statistically significant (p = .00), we observe that relationship between financial slack and profitability is steeper and not flatter. It means that low and high levels of financial are more detrimental for the profitability of BG-affiliated firms than for the profitability of standalone firms. The Figure 1 below illustrates the relationship between financial slack and profitability when all the other variables equal to their means (the full data range for financial slack is used). We show in Model 3 of Table 3 the results obtained with the cash holdings variable instead of the regression-based measure of financial slack, and they are comparable.

Relation between financial slack and profitability (ROA).

Financial slack and profitability for BG-affiliated firms

In the second part of the multivariate analysis, we consider only BG-affiliated firms and include in our specifications additional variables to investigate the impact of BG size, position of a firm in the BG, and weight of a firm in the BG. We also include two other control variables, namely a dummy variable to identify whether the BG head firm is located in France or not and the number of shareholders of the considered firm to account for the risk of tunneling. These variables have been defined in the “variables” section of the article. Missing values for some variables reduce the size of the sample and we only have 20,798 firm-year observations in this part of the analysis. We now cluster the robust standard errors at the BG level.

The results are presented in Table 4 below. Several preliminary points are worth noting (Model 1, Table 4). The coefficient for BG size is negative and statistically significant (p = .00) indicating that there is a negative relation between BG size and the profitability of affiliated firms. The coefficient for position in the BG is negative and not statistically significant (p = .44). There is a negative and statistically significant relation between the weight of a given firm in the BG and profitability (p = .00). Last, there is a negative relation between the number of shareholders and profitability (p = .01). This observation suggests that it is possible that tunneling affects our results. The presence of multiple minority shareholders increases the risk that the BG head firm siphons resources away from minority shareholders.

Moderating effects of BG size and BG affiliates’ position and weight in the BG on the relation between financial slack and profitability.

BG: business group; ROA: return on assets; Coef.: coefficient; HR: human resources.

Errors are robust and clustered at the BG level. We report them under brackets below the coefficients.

, **, and * denote statistical significance at the .10, .05, and .01 levels.

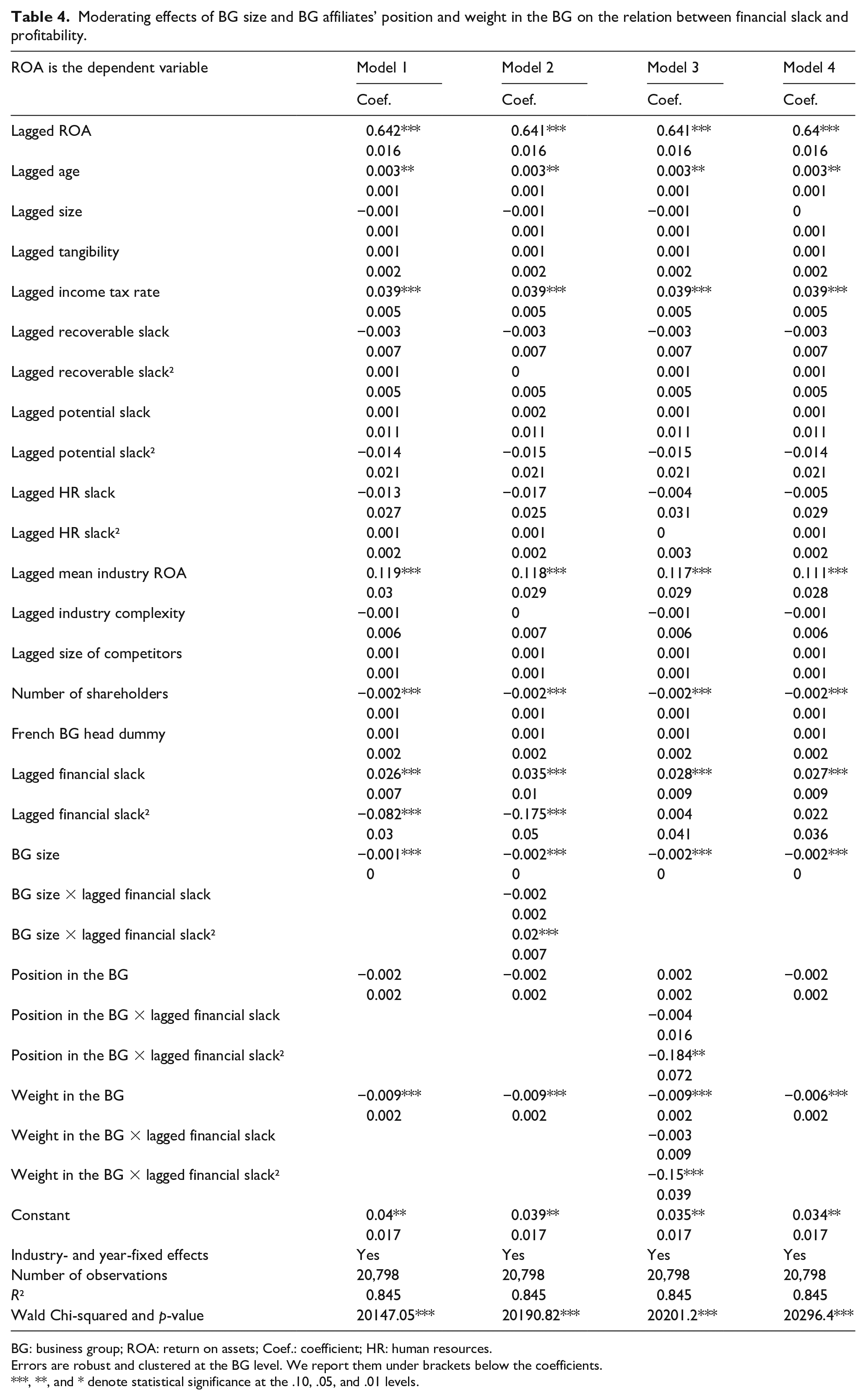

In Model 2 of Table 4, we focus on the role of BG size. We observe that the linear term of financial slack is positive and statistically significant (p = .00) and the squared term is negative and statistically significant (p = .00). The two other steps of the study by Lind and Mehlum (2010) are passed since Sasabuchi’s (1980) test statistics is 3.33 (p = .00) and the turning point is 0.10 (Fieller 95% confidence interval is [0.05;0.19]). We observe that the relation between financial slack and profitability has an inverted-U shape for this subsample. The linear term of financial slack interacted with BG size is negative and not statistically significant (p = .29) and the squared term interacted with BG size is positive and statistically significant (p = .01). In other words, the relation is flatter for firms affiliated to larger BG, which provides support to Hypothesis 3. Figure 2 helps visualize the results.

Role of BG size in the relation between financial slack and profitability (ROA).

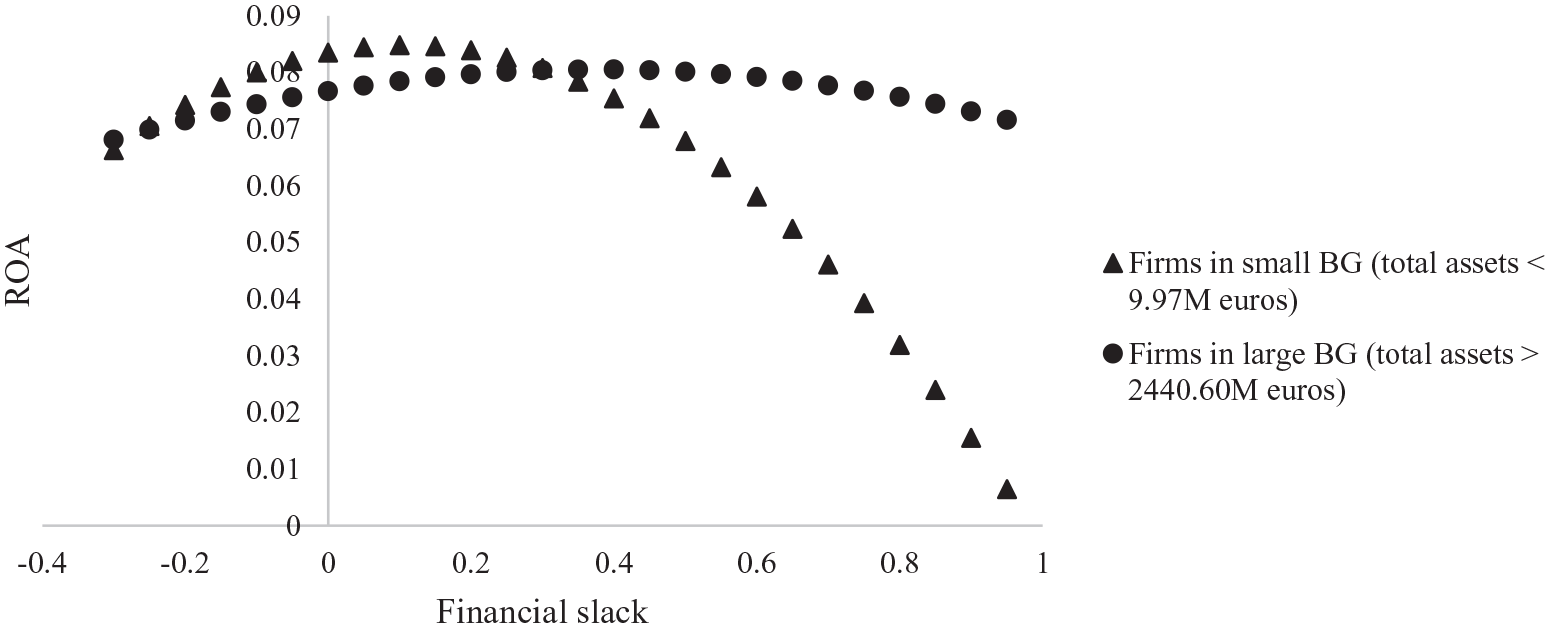

In Model 3 of Table 4, we observe that the linear financial slack term is positive and statistically significant (p = .00) and the squared term is positive and not statistically significant (p = .997). For firms at the periphery of the BG, the relation between financial slack and profitability is linear and positive. For firms that stand at the “core” of the BG (like BG head firms), the relation has an inverted-U shape because the interaction term between position and the squared financial slack term is negative and statistically significant (p = .01). Firms that occupy a central position in the BG can hold financial slack in an inefficient way. Figure 3 helps visualize the results.

Role of the position in the BG structure in the relation between financial slack and profitability (ROA).

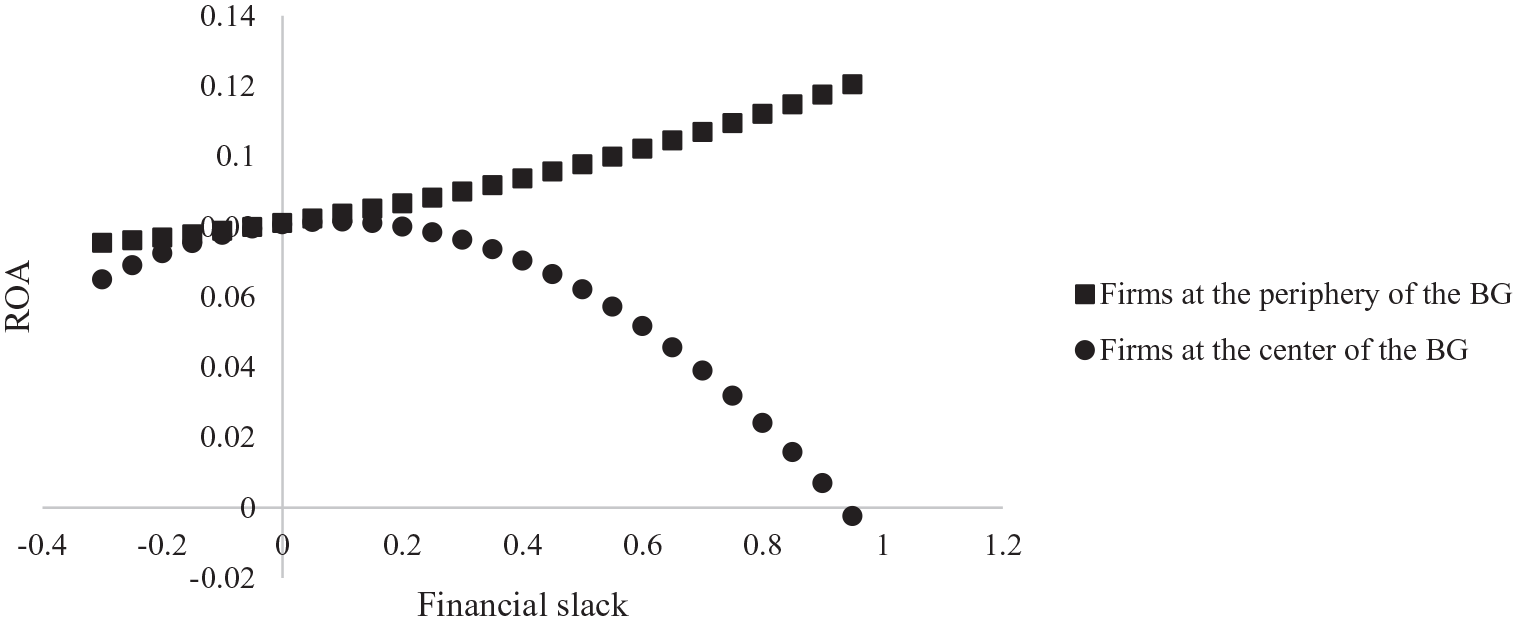

In Model 4 of Table 4, we make a very similar observation. We observe that the linear term of the financial slack variable is positive and statistically significant (p = .00) and the squared term is negative and not statistically significant (p = .54). The interaction term between the weight of a given firm in the BG and the squared term of financial slack is negative and statistically significant (p = .00). We observe here that for firms that have a modest weight in BG, the relation between financial slack and profitability is linear and positive. This relation has an inverse U-shape for firms that have a more important weight in the BG. This observation can be interpreted as follows. Firms that have a larger weight in the BG structure accumulate financial slack in an inefficient way and smaller firms, because of their lower bargaining power in the BG, never have “too much” slack. Figure 4 helps visualize the results.

Role of the weight a firm has in the BG in the relation between financial slack and profitability (ROA).

In all these regressions, the number of firm-year observations that lie at the right-hand side of the turning point (those that have “too much” financial slack) represents approximately 10% of the subsample size.

Robustness tests

We decide to run two robustness tests to assess whether the results can be considered as valid. Following Vanacker et al. (2017), we first extend the time-lag between our financial slack measure and profitability as it is possible that firms need more than a year to redeploy financial slack. The results, unreported but available upon request, are comparable when we extend the time lag to 2 and 3 years. The relation between financial slack and profitability has an inverted-U shape. This relation is steeper for firms affiliated to a BG. In the BG-affiliated firms’ subsamples, the inverted-U-shaped relation is flatter for firms affiliated to large BGs. For firms that have a high weight or a central position in the BG, the relationship between financial slack and profitability has an inverted-U shape. For firms that have a small weight, the relation is positive. The statistically significant and positive squared term indicates that the strength of relation is increasing but not that the relation becomes U-shaped because all the observations are located at the right-hand side of the turning point. For firms that lie at the periphery of the BG, the relation is not significant. This robustness test also contributes to alleviate an important endogeneity issue about the existence of a “reverse causality” mechanism, since one could argue that firms that have a higher profitability are also more likely to accumulate financial slack. The fact the results hold even with a 2- and a 3-year lag brings more support to our hypotheses.

Second, we decide to use other profitability measures. We run the regressions with three alternative measures of profitability: return on investment (net income divided by total assets), return on equity (net income divided by equity), and gross margin (sales less cost of goods sold divided by total assets). We observe once again comparable results (full results are available upon request).

Conclusion

Discussion of the results

The discussion on the impact of slack resources on firm performance is long-standing in management and deeply rooted in the BTF (Cyert & March, 1963). In this literature, relatively little attention has been devoted to the role of interorganizational ties that allow transfers of resources. This article contributes to slack literature by investigating the relationship between financial slack and profitability in BG-affiliated firms that have access to an internal capital market that allows transfers of slack. From a theoretical perspective, we built the literature on internal capital markets, according to which the impact of financial slack at the firm level on profitability is limited because the BG slack is accessible, and the BTF according to which BG firms compete for the BG resources. Our main findings are as follows. We confirm the existence of an “optimal” level of financial slack that maximizes profitability on a sample of French privately held firms. There has been conflicting findings about this result in past studies as many studies predicted and observed an inverted-U-shaped relation (Vanacker et al., 2013; Wang et al., 2016), but others failed to confirm it empirically, except in specific environments (Bradley, Shepherd, & Wiklund, 2011). Recent articles support the idea that the relation is in fact positive (La Rocca et al., 2019; Vanacker et al., 2017). Our results show that it is possible for firms to hold “too much” cash, even if only approximately 10% of our sample firms are in this situation.

The inverted-U-shaped relationship is steeper for firms affiliated to a BG than for standalone firms. This result is in line with our theoretical prediction that firms affiliated to a BG compete for the financial slack pool of the BG and that some firms corner the BG financial slack in an inadequate way. In larger BG, the relation between financial slack and profitability is flatter because larger BG have more financial slack and a greater capacity to allocate slack adequately. When looking at the characteristics of the firms in the BG organization, we observe that for firms that have a greater capacity to attract resources (firms that occupy a central position and have a higher weight in the BG), the relation between financial slack and profitability is steeper. Interestingly, our results echo the attention-based view according to which the allocation of resource to and performance of affiliated firms depend on their position in the BG structure. As highlighted by Belenzon et al. (2019), further the firms stand from the BG head firm, lower is the attention they receive, because organizational distance increases autonomy in the typical pyramidal structure of French BG. BG head firm cannot dedicate the same attention to all their subsidiaries, because attention is a limited resource. Firms that stand at the periphery of the BG structure represent diversified activities (Iacobucci & Rosa, 2005) and are thus less monitored by the BG head firms (Belenzon et al., 2019). It follows that the relation between financial slack and profitability is relatively similar between standalone firms and BG-affiliated firms that stand at the periphery of BG. It should be noted, however, that “attention” of BG head firms is not related to “efficient” resource-allocation decisions, because firms that have a greater weight or that stand close to the BG head firm are also those for which inefficiencies are observed.

Our results have interesting implications both for management research and practitioners. The study of the relation between slack resources and performance becomes complex when one acknowledges the existence of various interorganizational ties, networks, and alliances that allow transfers and flows of resources. Members of these coalitions have sometimes competing interests and try to corner the coalition’s resources, leading to a poor allocation of resources. Active resource-allocation decisions and monitoring appear essential to ensure the best possible repartition of slack in an organization and avoid “inertia” (Lovallo et al., 2020). The article also contributes to the literature on BG. A highly debated question in the BG literature is whether BG affiliation is overall beneficial or detrimental to firm performance (Carney et al., 2011; Holmes et al., 2018). Our results show that the allocation of financial slack is an important aspect of affiliated firms’ profitability, because it directly reflects the efficiency of the internal capital markets. The fact that BGs are not homogeneous, and that the benefits they provide are also heterogeneous is relatively well acknowledged in the literature (Belenzon et al., 2013; Holmes et al., 2018). However, there exists only limited evidence about the fact that the characteristics of the firms in a BG influence the allocation of resources (Ayyagari et al., 2015; Gubbi et al., 2015; Locorotondo et al., 2014). Our focus on the bargaining power of affiliated firms broadens our understanding of the way BG internal markets operate. For BG managers, an important implication of this study is the need to actively monitor the needs for financial slack of affiliated firms. We provide practical guidance to identify where BG managers should look to identify inadequate cash allocation: in the largest and most central firms in the BG organization. Typically, our results suggest that BG head firms themselves hold too much financial slack and that a more dynamic allocation of this key resource would be beneficial.

Limitations and directions for future research

This article has limitations, which also offer new avenues for future research. Investigating the relation between financial slack and performance in BG is challenging because of the resource-allocation mechanisms that characterizes BG. By exploring the relation between financial slack and profitability in BG-affiliated firms, this article offers a first contribution. However, we did not investigate how the global level of financial slack at the BG level, and not in affiliated firms, influences the global performance of the BG. The fact that the level of slack of a given firm is inadequate for a given firm does not mean that the global allocation of slack is detrimental for the performance of the BG seen as a firm. It would, therefore, be interesting to measure the amount of financial slack a BG has globally speaking and assess what the impact on the BG performance is. For example, it is possible to calculate the distance to the optimal level of financial slack for each firm affiliated to a BG and to add these distances for each firm within a BG to estimate the amount of financial slack at the BG level. Such an approach would bring a new level of analysis to the literature on financial slack in organizations. We were not able to implement this approach because our database does not provide a sufficient coverage of all the firms affiliated to a BG, as some of these firms are not based in Europe. Another limitation comes from the identification of BG firms. It is well known that identifying the boundaries of BG is highly challenging (Khanna & Yafeh, 2005, 2007). In fact, it is always difficult to identify the ultimate shareholder in a complex organizational structure; and in large BGs, capturing all the ties between firms is not easily achieved. An important issue is, for instance, whether one should consider an organizational structure as a BG in which an individual (and not a firm) is the ultimate shareholder of multiple firms (Cainelli & Iacobucci, 2011). In this article, we adopt a definition of BG that is slightly different from that of other studies to ensure that cash transfers are legally possible between firms and require that a firm is controlled by another firm to be considered as affiliated to a BG. Indeed, if firms are controlled by an individual and not by a firm, French laws severely constrain inter-firm loans and cash transfers 4 (Organisation for Economic Co-operation and Development, 2020). Recently, several authors considered the existence of a common ultimate owner to identify BG boundaries using various controlling interests thresholds (Belenzon et al., 2013; Belenzon & Tsolmon, 2016; Faccio & O’Brien, 2020). Specifically, Belenzon et al. (2013) consider organizations as BGs in which a single individual has direct control over several firms. Since cash transfers and loans are not possible in France in such organizations, we excluded such BGs from the analysis. Future research could investigate cash transfers and cash allocations in BGs by using alternative identification strategies that could better capture the complexity and variety of ties in BGs in other institutional contexts.

Another interesting question is whether other forms of slack affect the performance of BG and BG-affiliated firms. BGs have internal labor markets that facilitates the transfer and training of employees, and intuitively reduce the need to hold HR slack (Holmes et al., 2018). Belenzon and Tsolmon (2016) show that in countries with high labor rights protection, internal labor markets of BG provide a competitive advantage by facilitating the transfer of employees across firms affiliated to a BG. It would be interesting to cross the work of Belenzon and Tsolmon (2016) with the Vanacker et al. (2017) study on HR slack to examine potential differences in the relation between HR slack and performance for standalone and BG-affiliated firms.

Understanding the relation between resources and performance is at the core of strategic management. We hope that this article will stimulate research on the role of interorganizational structures in the process of resource allocation, since this study is only a first step to take into account the complexity of organizations.

Footnotes

Acknowledgements

The author thanks two anonymous reviewers for their comments and suggestions.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Réseau de Recherche et d’Expertise en Entrepreneuriat. Funding by the European Regional Development Fund and Région Grand Est is gratefully acknowledged.