Abstract

Although the resource-based view (RBV) of the firm is one of the most accepted theories of strategic management, it has been criticized for its limited empirical support. The RBV basically predicts the relationship between the firm’s resources and its performance. This study argues that it is more appropriate to measure firm performance using profit efficiency than traditional financial or accounting measures and that frontier models have great potential in empirical research on the RBV. To test this idea empirically, we used a stochastic frontier model with random coefficients to evaluate the impact of corporate reputation on profit efficiency. Finally, implications of the aforementioned focal points are discussed.

JEL classification: C11, L25, M10, M20

Keywords

Introduction

One of the basic questions that occupies both researchers and professionals in strategic management is to understand and explain why firms in the same industry generate differing performance. The answer to this question lies in determining the sources of competitive advantage, identifying where these advantages are based and specifying how they can be sustained. Therefore, one controversial aspect of empirical studies on management research is the measurement of firm performance as a reflection of its competitive advantage. Most of the research on strategic management uses accounting or financial indicators to measure firm performance, such as return on assets (ROA) or return on equity (ROE), among others (e.g., Bierly & Chakrabarati, 1996; De Carolis, 2003; Deephouse, 2000; Fernández, Iglesias-Antelo, López-López, Rodriguez-Rey & Fernández-Jardon, 2019; Hull & Rothenberg, 2008; Lin & Wu, 2014; Markides & Williamson, 1996; Wu, Yeniyurt, Kim & Cavusgil, 2006). However, the use of an aggregate measure such as these accounting or financial indicators as a dependent variable has serious drawbacks. In this sense, Coff (1999) argues that it is possible that not all rent generated by a competitive advantage will be reflected in traditional financial measures of performance. For example, “a resource-based advantage may result in relatively little rent observable in measures of firm performance. . . . most performance measures capture only the rent that is not appropriated by the most powerful stakeholders” (Coff, 1999: 131).

In addition, assessing only the financial dimension of performance ignores other relevant dimensions. A purely financial measure does not take into account, for example, that the efficiency with which a firm uses its resources can be the main source of its competitive advantage (Chen, Delmas & Lieberman, 2015). Furthermore, simple financial metrics are not relative measures of performance, as they cannot reveal the gap between actual and optimal performance.

Given the importance that a firm’s performance has for research on strategic management, the measurement of such performance requires greater consideration in the literature. As noted by Richard, Devinney, Yip and Johnson (2009), examination of a firm’s performance requires addressing both its dimensionality and the nature of its measurement. To overcome the drawbacks of traditional measures of a firm’s performance, we propose an innovative concept of performance measurement: profit efficiency. Profit efficiency refers to a firm’s ability to manage its resources and produce outputs with greater economic value. This concept encompasses errors on the input side as well as on the output side. In addition, unlike the performance measures used by previous studies in the RBV-related literature, profit efficiency is an indicator that assesses both the efficiency of a firm and the potential profit that this firm could earn if it were completely efficient. Consequently, profit efficiency is a better predictor for evaluating the overall performance of a firm than accounting and financial indicators.

It is expected that this novel performance measure will provide different results than previous empirical work on RBV. Financial and accounting indicators usually have different scores than profit efficiency and cannot be correlated due to intrinsic differences (Han, Kim, & Kim, 2012). For example, a firm with a high ROA may be inefficient when other economic and environmental dimensions are taken into account. Therefore, using profit efficiency as a performance measure can provide more empirical support to RBV research than has been achieved so far.

Profit efficiency measures the distance between the current profit of a firm and the efficient profit frontier (Berger & Mester, 1997). As indicated by Chen et al. (2015), it is rare for a firm to be top on the list of all possible measures of performance. Therefore, “identifying the firms that define the best performance frontier across the relevant measures is an important task that is seldom performed” (Chen et al., 2015: 20). The frontier methodology allows us to estimate the efficient frontier (in this case of profits) and to understand performance beyond a mere comparison with profitability or financial performance, since it evaluates the performance of a firm in relation to the efficiency frontier.

To investigate our proposal, we will apply one of the most important theories of strategic management: the resource-based view (RBV) of the firm (Barney, 1991; Wernerfelt, 1984). As Peteraf and Barney (2003: 311) argue, the RBV is “an efficiency-based explanation of performance differences, rather than one relying purely on market power, collusion, or ‘strategic’ behaviours”. In the RBV, firms obtain a sustained competitive advantage by developing resources and capabilities that are valuable, rare, inimitable, and non-substitutable. This theory highlights the importance of the resources and capabilities of the firm to achieving performance above the industry average. From an analytical perspective, the RBV assumes that the competitive position of a firm depends on how specialized its assets and skills are and focuses its attention on the optimal use of these to create competitive advantage. For this, the RBV is based on two main assumptions (Barney, 1991): (1) the firms in an industry are heterogeneous with respect to the resources they possess and (2) these resources are not perfectly mobile and, therefore, the heterogeneity will persist over time.

The utilization of resources is an important issue in the RBV (Majumdar, 1998; Miller & Ross, 2003), since as Winter (1995) argues, the mere possession of an exclusive resource does not guarantee that a firm achieves a competitive advantage. In this sense, Mahoney and Pandain (1992) argue that firms can achieve a greater profit not because they have superior resources but because their distinctive competences allow them to use those resources more efficiently. That is, a firm may have the skills to accumulate resources, but these resources would not be sufficient to achieve a competitive advantage; in addition, these resources must be used efficiently (Majumdar, 1998; Peteraf, 1993). In summary, firms that do not use their resources efficiently in production processes cannot expect to obtain a potential competitive advantage from them (Ray, Barney & Muhanna, 2004).

There are numerous theoretical and empirical works in the literature on RBV. Newbert (2007) has reviewed this literature to assess how the RBV has been empirically tested, as well as the level of support the RBV has received. Armstrong and Shimizu (2007) have also reviewed the empirical research on the RBV but focus more on methodological issues. Although the RBV has provided important knowledge for strategic management, Hoskisson, Wan, Hitt, and Yiu (1999) argue that the empirical research supporting the RBV is limited. In this same sense, Newbert (2007: 134), concludes that “. . ., it seems that while the RBV has received considerable attention in the empirical literature, it has only received marginal support”. This author found that only 53% of the studies analysed support the RBV. However, it is not clear if this lack of empirical support is “attributable to the RBV or to methodological problems” (Armstrong & Shimizu, 2007: 960) 1 .

The objective of this paper is to argue, in the framework of the RBV, that it is more appropriate to measure a firm’s performance using profit efficiency than using traditional financial or accounting measures. To test this idea empirically, we used a stochastic frontier model with random coefficients to evaluate the impact of corporate reputation on profit efficiency. This methodology has great potential for empirical research on the RBV, since it allows researchers to assess efficiency in the use of resources and capabilities from a firm-specific point of view (Chen et al., 2015; Lieberman & Dhawan, 2005). Furthermore, a central factor in the RBV is that firms in an industry are heterogeneous in terms of the resources that they possess. Therefore, one must assume that firms, even in the same industry, face possibilities of different productions. However, although most prior studies on the RBV theoretically recognize the heterogeneity of firms with respect to strategically relevant resources, in practice, such studies use methodologies that do not assume this heterogeneity (Mackey, Barney & Dotson, 2017). Tsionas (2002) proposes a stochastic frontier model with random coefficients in which it is assumed that firms do not operate under a common frontier, assuming that firms are heterogeneous.

Reputation is a resource whose determinants are complex, intrinsic to the firm and possessing a high degree of ambiguity, all of which make it a difficult resource to imitate 2 . Flanagan and O’Shaughnessy (2005) point out that reputation is likely one of the most important strategic resources, and, as suggested by Barney (1991) and Hall (1992), a positive corporate reputation can be a source of sustained competitive advantage. There have been various studies investigating the relationship between reputation and firm performance (e.g., Black, Carnes, & Richardson, 2000; Boyd, Bergh, & Ketchen, 2010; Deephouse, 2000; Roberts & Dowling, 2002; Vergin & Qoronfleh, 1998) confirming a positive relationship between reputation and performance. However, many of these studies use financial performance as a dependent variable and cross-sectional methods. In contrast, this investigation uses a measure of performance and a methodology that are novel to empirical research on RBV.

This paper contributes to extending the existing literature on empirical tests on the RBV, providing two important contributions: (1) it uses the concept of profit efficiency as a measure of firm performance, and (2) it uses a stochastic frontier model with random coefficients to estimate profit efficiency while assuming the heterogeneity of resources. The rest of the study is organized as follows. In the next section, we discuss the concept of profit efficiency as a measure of performance. Next, we analyse the stochastic frontier methodology. Then, we use a sample of firms to empirically test the relationship between reputation and profit efficiency. Finally, we present the results and conclusions.

Profit Efficiency as A Measure of Performance

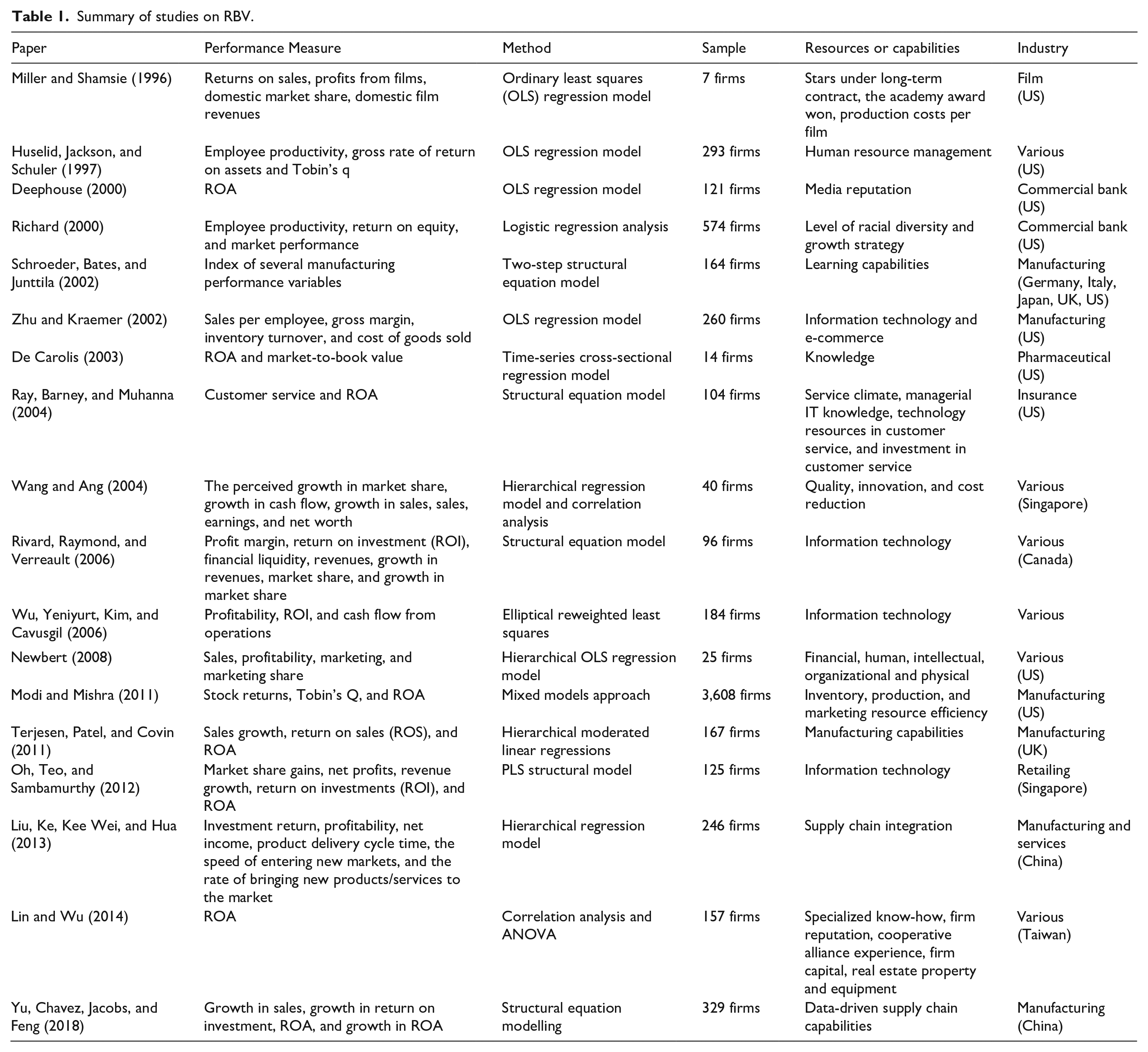

The measurement of firm performance is a core issue in strategic management. The measurement of firm performance is essential for researchers and managers because it enables them to evaluate the effectiveness of the strategies they have implemented. Table 1 summarizes previous RBV studies and the methods they used to evaluate firm performance. As shown in Table 1, most of the empirical research on the RBV uses a financial measure of performance such as ROA. However, measuring performance using accounting and financial indicators has considerable shortcomings. Financial and accounting measures only reflect the economic interests of managers and shareholders but not the interests of other important stakeholders such as employees, suppliers and customers (Richard, et al., 2009). As indicated previously, Coff (1999) points out that stakeholders can appropriate part of the rent generated by a competitive advantage, and therefore, it will be not reflected in the firm’s financial performance. In this context, the choice of accounting and financial indicators may bias the measurement of performance by ignoring the distribution of created value across stakeholder groups.

Summary of studies on RBV.

Simple financial metrics also ignore other relevant dimensions. These metrics do not consider the gap between actual and potential performance because they are not relative performance measures, nor do they consider how managers use resources. To address these shortcomings, we propose an innovative concept of performance measurement: profit efficiency. This concept reflects the ability of firms to exploit their exclusive resources and capabilities in a way that enables them to reduce costs and/or increase revenues by responding optimally to changing market conditions.

Resource heterogeneity is also a fundamental issue in RBV. As shown in Table 1, most research uses methodologies to evaluate the impact of different resources or capabilities on the performance but that do not adequately capture the heterogeneity of resources across firms. These methodologies only examine the average relationship between resources or capabilities and firm performance. This constraint leads to a mismatch between theoretical RBV assumptions and empirical RBV studies. To adequately incorporate resource heterogeneity, we propose an alternative methodology for empirical RBV research: stochastic frontier model with random coefficients. Finally, as shown in Table 1, the resources and capabilities analysed are diverse, and the samples used are relatively small and focused on different industries in different countries.

Additionally, most of the studies on RBV also consider the concepts of “competitive advantage” and “performance” as interchangeable, accepting the hypothesis that a competitive advantage produces superior performance (Newbert, 2007; Powell, 2001). However, according to Newbert (2008), the fact that a firm possesses exclusive resources/capabilities does not necessarily imply any performance improvement. Therefore, it should not be assumed that there is a direct relationship between competitive advantage and improved performance. In other words, access to exclusive resources is irrelevant if these resources are not used efficiently (Majumdar, 1998).

To improve performance, firms must be able to efficiently use their exclusive resources/capabilities in a way that allows them to reduce costs, exploit market opportunities and/or neutralize competitive threats (Newbert, 2008). Consequently, as previously indicated, we consider profit efficiency as a measure of performance since it is superior to the traditional measures of performance used in empirical research on the RBV. The concept of profit efficiency refers to the firm’s ability to reduce costs and to create greater economic value from its output.

Peteraf and Barney (2003) emphasize the role of a firm’s strategic resources in the creation of value. For these authors, the economic value of a good or service is the difference between its selling price and the economic cost of producing it. This definition of economic value is less associated with price or cost than with the commercial margin of a product. For a firm to generate a higher margin or greater value, it must not only combine and use its resources efficiently (cost efficiency) but also choose an efficient product-market combination (revenue efficiency). In this manner, a firm could create more value than its competitors by being capable of generating more revenue at the same cost and/or by incurring lower costs while producing the same revenue.

The economic literature considers the two most important concepts of efficiency to be cost efficiency and profit efficiency, since they are based more on economic optimization in reaction to prices and competition in the market and less on the use of a certain technology (Berger and Mester, 1997). In other words, these two concepts of efficiency respond to two important economic objectives: the minimization of costs and the maximization of profits. Cost efficiency is defined as the ratio between the minimum cost that can be achieved for a given volume of production and the current production cost. This concept tells us how much higher the costs of a firm are in relation to the costs of the most efficient firm that produces the same combination of outputs given the same prices for inputs, considering that the difference cannot be explained by a random error. For Leibenstein (1966), most of these inefficiencies have their origin in management and/or organizational errors. Consequently, we can affirm that cost inefficiencies are due, first, to a bad choice of production plan (allocative inefficiency) and, second, to poor implementation of the production plan (technical inefficiency). Cost efficiency thus refers to the ability of a firm to minimize its costs for a given amount of output.

A recent research study by Chen et al. (2015) describes in detail the few studies in the literature on strategy that use efficiency as a performance measure 3 . For each of these studies, the authors analyse the estimation methods used, sample size, input and output variables selected, industry type, and average cost efficiency obtained. All these studies represent a major step forward in the literature on strategy since (1) the capacity of firms to minimize their costs is part of the RBV and (2) the efficient use of resources is crucial to achieving competitive advantage (Majumdar, 1998). However, despite the importance of cost efficiency as a potential source of cost reductions, this concept suffers from two significant weaknesses (Berger & Mester, 1997):

Cost efficiency evaluates efficiency for a given level of output, which normally does not have to correspond to the optimal level of production. Thus, even if a firm is cost-efficient for its current scale of output, it is very likely that it is not for its optimum level of output.

Cost efficiency does not include possible differences in the quality of outputs. If these quality differences are not taken into account, given that higher quality implies a higher cost, we could make the mistake of considering this higher cost as inefficiency when in fact it is due to unmeasured differences in the quality of outputs.

These shortcomings, together with the fact that the objective of a firm is not only to minimize its costs but also to choose a combination of outputs that maximizes its revenue, have given rise to the concept of profit efficiency. Profit efficiency is defined as the proportion of the maximum profit 4 that a firm obtains (Berger & Mester, 1997), and it incorporates both cost efficiency and revenue efficiency. Revenue inefficiencies have their origin in an erroneous choice of market and/or competitive strategy and reflect the failure to produce a higher output value. Alternatively, a firm can also have revenue inefficiencies if the response to the relative prices of the outputs is poor and it produces few of the high margin outputs and many of the low margin ones. In this way, revenue inefficiencies are analogous to cost inefficiencies, since in both cases they cause a net loss of real value, whether the loss is in terms of a lower value of the output produced or a higher value of the consumed inputs. As such, for a firm to create value, it must increase its efficiency, and the efficiency concept that best measures this value creation is the profit efficiency.

This concept also takes into account possible differences in the quality of outputs, since the additional revenue from generating higher quality output is included, which can more than compensate for the extra cost of this higher quality. That is, if a firm spends an additional one euro to increase the quality of its output such that income is increased by two euros, ceteris paribus, this would be correctly evaluated as improving the profit efficiency, but it would be incorrectly evaluated as lowering cost efficiency.

Thus, profit efficiency is a concept that connects not only with the reduction of costs but also with the creation of a higher value output, in line with the concept of efficiency proposed by Peteraf (1993) and Peteraf and Barney (2003) in the framework of the RBV. Defined in this manner, profit efficiency is the most appropriate concept of efficiency for evaluating overall performance because it accounts for the impact of a firm’s activity in terms of both costs and revenues, as well as their interaction, thereby better reflecting the goal of profit maximization. Therefore, considering profit efficiency as a measure of performance will allow us to know not only the differences in the use of resources among firms (cost efficiency) but also the differences in the response to the relative prices of the outputs (revenue efficiencies). In addition, profit efficiency, unlike other financial or accounting measures of performance, is an economic indicator that not only reveals how efficient a firm is but also indicates how much more profit that firm could achieve if it were completely efficient (Han, et al., 2012).

The literature distinguishes between standard profit efficiency and alternative profit efficiency depending on whether the hypothesis of perfect competition in the markets of inputs and outputs is assumed or not (Humphrey & Pulley, 1997). Standard profit efficiency measures how close a firm is operating to its maximum profit given a price level for inputs and a price level for outputs, assuming perfect competition in these markets. This means that a firm takes as given the prices of inputs and outputs and maximizes its profit by adjusting their quantities. Therefore, the standard profit function can be expressed as

where π is the profit variable, p is the price vector of the variable outputs, w is the price vector of the variable inputs, uπ represents the inefficiencies found that reduce profit, and vπ represents random error.

However, in practice, the assumption of perfect competition is not applicable in many industries, as firms can exercise some market power in setting the price of outputs. In this case, the estimation of standard profit efficiency is not advisable, since alternative profit efficiency is more appropriate. Alternative profit efficiency measures how close a firm is operating to its maximum profit given its level of output. That is, in estimating the alternative profit efficiency, the quantity of output is taken as given and the price of the outputs is allowed to vary freely and affect the profit of the firm (Berger & Mester, 1997). In this way, we define the alternative profit function as

where the variables are defined as in (1) and y is the vector of quantities of the variable outputs. Based on equation (2), the alternative profit efficiency of a firm b (

Profit efficiency thus defined is simply the proportion of the maximum profit obtained by a firm; thus, the closer the value of Eπ is to one, the greater the profit efficiency is. For example, a profit efficiency ratio of 0.80 would indicate that, due to excessive costs and/or inadequate revenue, a firm is losing approximately 20% of its maximum potential profit.

Stochastic Frontier Methodology

The frontier method has been the most often used methodology for estimating efficiency. According to this methodology, a firm is labelled efficient if it operates in the efficient frontier of the industry. There have been numerous studies on strategic management 5 that use the frontier method (Chen et al., 2015; Delmas & Montes-Sancho, 2010; Knott, Posen & Wu, 2009; Majumdar, 1998; Majumdar & Marcus, 2001;). Among these methods, data envelopment analysis (DEA) and the stochastic frontier approach (SFA) are the most used. The DEA was introduced by Charnes, Cooper and Rhodes (1978) and uses linear programming techniques to estimate efficiency. However, the DEA is a nonparametric method that ignores prices and, therefore, can only measure technical efficiency. A second drawback of this method is that it considers the entire distance between a firm and the efficient frontier as inefficiency, not taking into account the possible existence of random errors.

The SFA is a methodology that uses econometric methods to estimate efficiency; it was introduced simultaneously by Aigner, Lovell and Schmidt (1977) and Meeusen and Van den Broeck (1977). Unlike DEA, SFA is a parametric technique that is better suited to the concept of profit efficiency discussed above. In the SFA, it is said that a firm is inefficient in profit if its profit is less than the best-practice profit after eliminating the random error. That is, the performance of a specific firm is evaluated with respect to the efficient frontier, and any deviation from this efficient frontier is due to random errors and inefficiency. In the SFA, this deviation is represented by a compound error term.

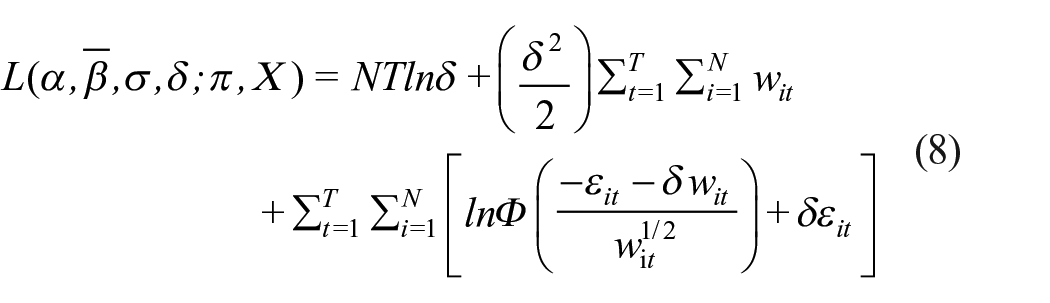

The possibility of having panel data allows more reliable estimates of efficiency to be obtained, since it provides a level of efficiency for each firm throughout the study period. Normally, panel data models assume that efficiency is invariant over time. However, Battese and Coelli (1995) propose a model that relaxes this assumption and suggest that the determinants of inefficiency can be expressed as a linear function of a set of explanatory variables that reflect the inherent characteristics of a firm. Therefore, the model of Battese and Coelli (1995) enables estimation of the efficiency for each firm and of the factors that explain the efficiency differences between firms in a single stage estimation procedure 6 . This paper uses the Battese and Coelli model (1995) to estimate the alternative profit frontier function and the effects function of inefficiency. The alternative profit function can also be expressed as

i = 1. . ., N firms, t = 1. . ., T periods

where π

it

is the profit of firm i at time t, α is an intercept,

The traditional frontier models consider that all the firms in an industry share the same technology; that is to say, there is no heterogeneity between them and, therefore, it is assumed that the efficient frontier is common for all firms. However, a basic assumption of the RBV is the heterogeneity of resources between firms (Barney, 1991; Peteraf, 1993). If firms are heterogeneous from the point of view of resources, in the sense that some firms have resources that generate more value than others (Peteraf, 1993), then the assumption that all firms face the same efficiency frontier is incorrect. That is, each firm will have its own efficiency frontier and, therefore, inefficiency will be given by the deviation of each firm from its frontier of possibilities. Tsionas (2002) proposes a new model where it is possible to relax the assumption that all firms in an industry are homogeneous and face the same efficient frontier. This model is called the random stochastic frontier model and can be expressed as

i = 1. . ., N firms, t = 1. . ., T periods

where β i is the vector of random parameters to be estimated. That is, it is assumed that the coefficients of the explanatory variables vary between firms, and therefore, each one has its own optimal possibilities frontier 8 . This approach takes into account the differences in the allocation of resources between firms. The other variables have the same interpretation as in equation (4).

The stochastic frontier can be estimated using maximum likelihood techniques or Bayesian techniques. The use of Bayesian techniques is gaining prominence due to their greater flexibility and benefits with respect to the maximum likelihood method. The Bayesian approach easily incorporates non-sample information in the analysis, the results are presented in terms of probability density functions (pdfs) and it allows the estimation of more complicated and robust models (Assaf, Oh, & Tsionas, 2016). In addition, the estimation is unbiased with respect to the sample size (Chen, Barros, & Hou, 2016). Therefore, we estimate model (5) using Bayesian techniques, and the parameters β i are considered to follow a multivariate normal distribution such that

where

It is also assumed that β i is independently distributed, and therefore, both v it and u it are independent of x it . This model is considered a hierarchical model with two levels of latent variables, β i and u it . Each firm in the sample has its own profit function with parameters β i capturing the heterogeneity between the firms.

If we substitute expression (6) into (5), we obtain

where ε

it

is are independently distributed as

The Bayesian estimation of model (5) requires prior information about the parameters. A common practice is to specify non-informative priors. Following Tsionas (2002), we consider the following:

α is a normal distribution with mean α0 and variance

β

i

is distributed as

σ2 follows a gamma distribution, such that σ−2~ (a,b), with mean a/b and variance a/b2, where a= 10−3 and b=10−3.

In the Bayesian approach, it is usually assumed that the inefficiency term u it follows an exponential distribution with parameter λ it (Assaf, 2009; 2011; Chen, Barros, & Borges, 2015), such that u it ~ (λ it ). It is assumed that profit inefficiency (u it ) depends on covariates with λ it = exp(z it δ), where z it represents the determinant factors of u it and δ represents the parameters to estimate. The prior of parameter λ it is defined as λ it ~ (−logr*), where r* is the mean prior efficiency of the different firms in the sample. Given that there is little evidence of what this mean profit efficiency would be, we consider that r* ~ (0.5,0.8), that is, efficiency varies within a range from 50% to 80%.

In turn, the likelihood function of the model (7) can be expressed as

where

Once the priors and the likelihood function are specified, the posterior distributions of each of the parameters of the model can be estimated 9 . Finally, the estimation of the stochastic frontier with random coefficients is carried out using the Markov chain Monte Carlo (MCMC) method. In particular, the Gibbs algorithm is used, introduced by Koop, Steel, and Osiewalski (1995).

Data and Model Specification

Data and variables

The RBV explains in essence the relationship between resources (independent variables) and the performance of a firm (dependent variable) (Armstrong & Shimizu, 2007). To test our proposal on the measurement of a firm’s performance and the potential of frontier models in empirical research on the RBV, we will empirically analyse the relationship between the resource “corporate reputation” and profit efficiency. Reputation is probably one of the most important strategic resources for achieving a competitive advantage in practically any industry (Boyd, Bergh & Ketchen, 2010).

When the resource to be investigated is a valuable resource across many industries, it is advisable to include firms from different industries in the sample (Armstrong & Shimizu, 2007). According to Dess, Ireland and Hitt (1990), empirical research in a multi-industry context, independently of increasing the size of the sample, has the following advantages: (1) its results are more accurate, since they probably will not be contaminated by the characteristics of each industry and (2) its results allow greater generalization. However, when the research includes firms from different industries, these authors highlight the importance of controlling the possible effects that the industry environment can have on firm performance. To do this, control variables that reflect this effect must be introduced in the analysis. In our case, these control variables are not necessary, since the frontier model with random coefficients used in the empirical analysis assumed that they do not operate under a common frontier. That is, it is assumed that firms are heterogeneous, not only within firms in different industries but even within firms in the same industry 10 .

This study uses balanced data from 49 Spanish firms belonging to different industries during the period 2010-2016 (343 observations) 11 . Employing panel data in empirical research on RBV is necessary if we want to analyse the impact of resources on sustained competitive advantage, since it seems evident that the use of longitudinal data allows us to more adequately capture the concept of sustainability than cross-sectional analysis (Armstrong & Shimizu, 2007).

The financial data were extracted from the Iberian Balance Sheet Analysis System, eliminating the firms for which there was missing information. To measure corporate reputation, the Corporate Reputation Business Monitor (MERCO) was used 12 . MERCO is a reputation evaluation instrument based on a multi-stakeholder methodology and composed of diverse evaluations and multiple sources of information; it is one of the reference tools to measure the extent of the corporate reputation of Spanish firms. In this way, the research design integrates a qualitative and quantitative methodology that is “likely to be a fruitful course, especially because of the reemphasis on issues inside the firm through the RBV” (Hoskisson et al., 1999: 447).

The selection of the variables was made according to the literature and available information. Regarding the profit frontier function, we specify two outputs, operating revenue and other operating revenues, and four inputs (resources necessary to obtain the revenue of the firms). These inputs include the number of full-time equivalent employees, total spending on materials, other operating expenses and physical capital. The prices of the inputs cannot be identified directly, therefore, it must be approached from the available information. Last, the dependent variable of the profit frontier function is the EBIT. All of these variables are listed below 13 :

Output variables

x1 = Operating revenues

x2 = Other operating revenues (includes other revenue not earned from the firm’s principal activity: rental of premises, laundry services, beauty and hairdressing salons, casinos, tours, sports venues, conferences, swimming pools, etc.).

Input variables

x3 = Price of labour (estimated as total cost of salaries, including social security costs, divided by the number of equivalent full-time employees)

x4 = Price of materials (estimated as total spending on materials divided by operating revenues)

x5 = Price of other operating expenses (estimated as other operating expenses divided by operating revenues)

x6 = Price of physical capital (estimated as the depreciation of fixed assets divided by the fixed assets)

Dependent variable

π = EBIT (earnings before interest and taxes)

Variables for the effects of inefficiency function:

z1 = reputation

z2 = time trend (this variable equals 1 in 2010, 2 in 2011, . . ., and 7 in 2016)

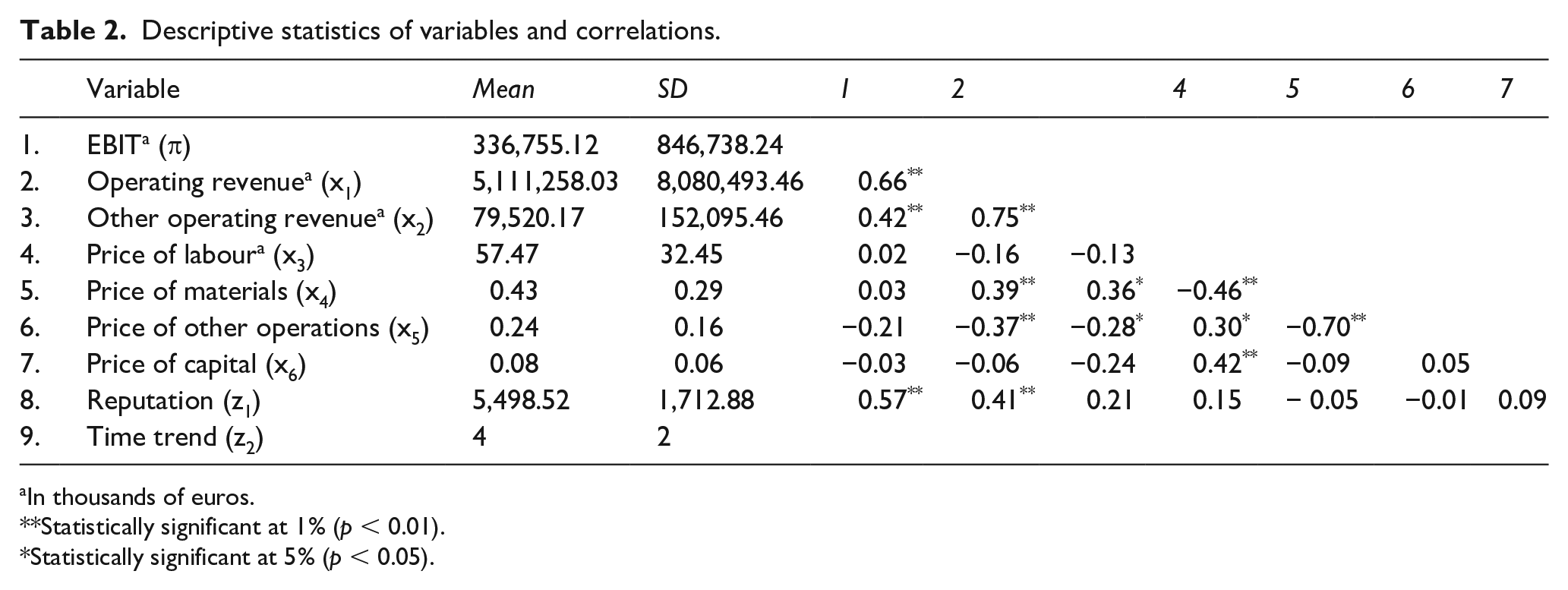

Table 2 shows the descriptive statistics of the variables between 2010 and 2016. The average reputation is 5,498, and its standard deviation is 1,712, showing that reputation differs among the firms in the sample, a necessary condition for a resource to be rare.

Descriptive statistics of variables and correlations.

In thousands of euros.

Statistically significant at 1% (p < 0.01).

Statistically significant at 5% (p < 0.05).

Model specification

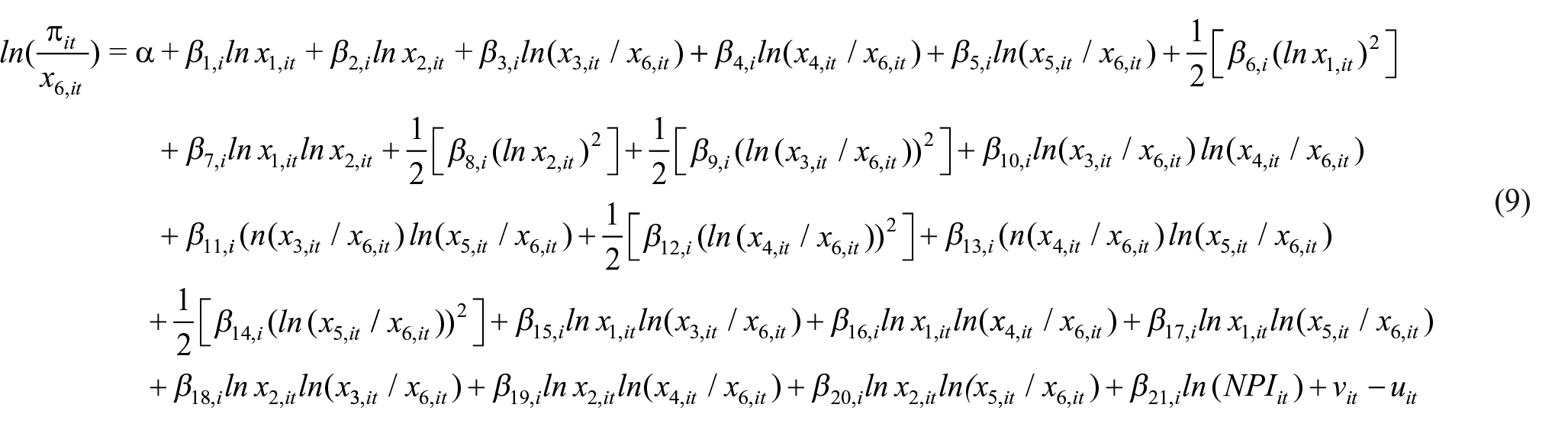

One of the requirements for estimating the stochastic frontier is to specify its functional form. Most studies have chosen between two functional forms: Cobb-Douglas and translog. To choose the most appropriate, we will use the deviance information criterion 14 (DIC) (Spiegelhalter, Best, Carlin, & Van der Linde, 2002). The functional form that best fits the sample of this study is the translog, since it has a DIC = −671.74, which is lower than the Cobb-Douglas functional form (DIC = −361.3).

An important issue to take into account with the translog functional form is that the dependent variable, π it , takes negative values when the firm obtains losses, causing a problem in the estimation of the stochastic frontier, since the logarithm of a negative number is not defined. Therefore, the standard approach to calculating the optimal frontier is to rescale the variable π it , such that the profits of each firm are added to the absolute value of the highest observed loss in the sample plus 1 (π+|πmin|+1). However, this manipulation of the data can cause non-controllable effects on the structure of the error term, which is particularly problematic when we are interested in estimating inefficiency (Bos & Koetter, 2011).

Bos and Koetter (2011) propose an alternative approach, which is to create a new independent variable called the negative profit indicator (NPI). When the firm obtains positive results, this variable is equal to one, since all the available information is already collected in the dependent variable. However, when the firm incurs losses, the NPI variable is equal to the absolute value of those losses. In this case, the dependent variable, π it , takes the value of one. Bos and Koetter (2011) compare both methodologies and show that this new approach improves the accuracy of the levels of profit efficiencies obtained, the discriminatory power of the model, and the rank stability. For this reason, this study will apply the approach proposed by these authors.

According to the above, the specification of the stochastic profit frontier translog with random coefficients for the case of two outputs and four inputs and imposing the restrictions of homogeneity and symmetry can be expressed as

where u it ~ Exp (λ it ) and λ it =exp (γ1Z1,it + γ2Z2,it). The variable Z1, represents the corporate reputation of each company i in year t, and the variable Z2,it represents the trend.

Empirical Results

The implementation of the MCMC for the estimation of the stochastic profit frontier is carried out using the WinBugs package. The Gibbs algorithm involves a total of 50,000 iterations, discarding the first 5,000 to avoid the sensitivity of the initial values and thus guaranteeing convergence.

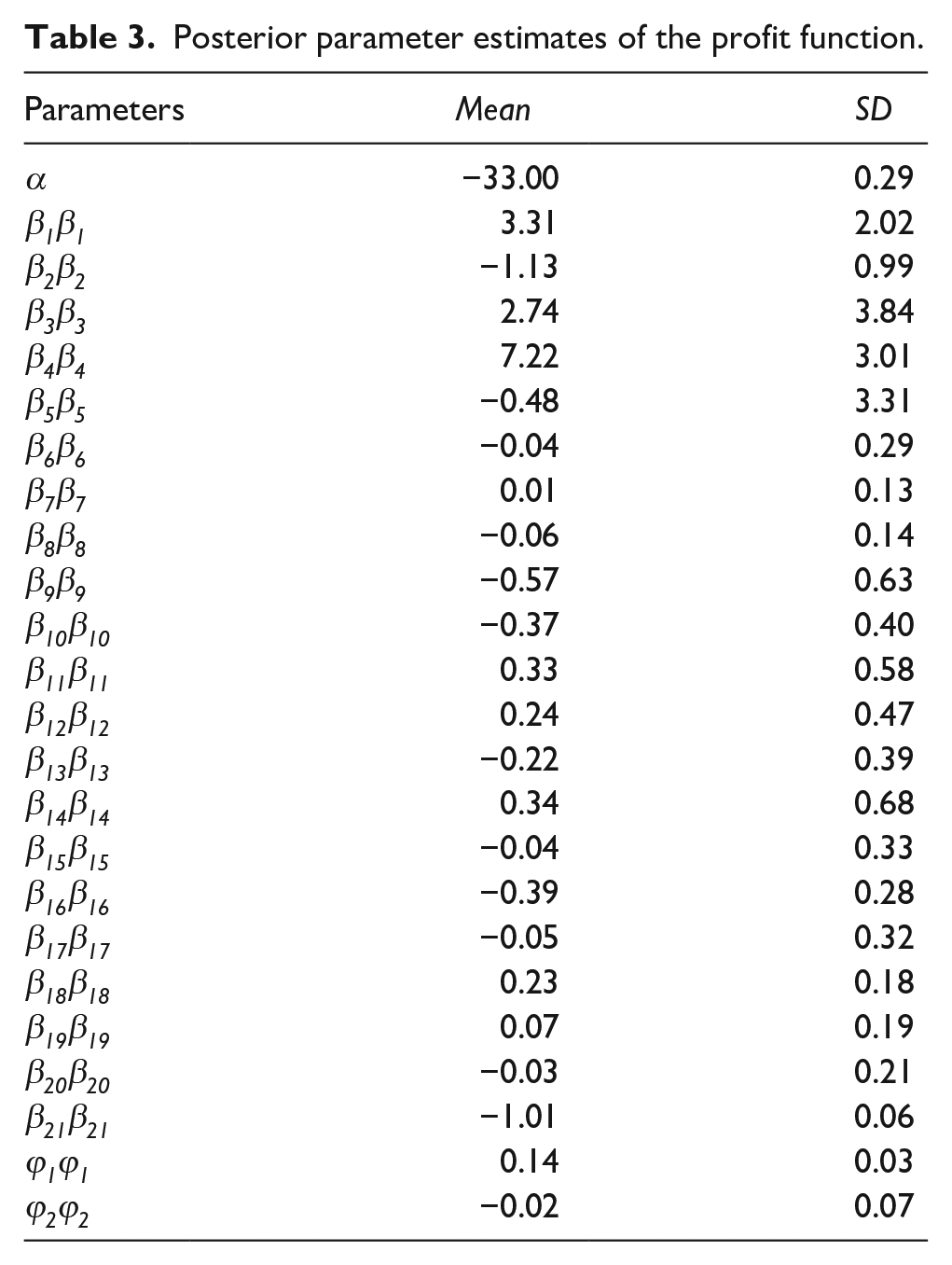

Table 3 shows the posterior mean and posterior standard deviations of the parameters estimated from the profit frontier with random coefficients. The number of coefficients generated by the model is very large to be reported in this table. However, the coefficients reveal some variability, which confirms that the firms in the sample have different profit frontiers.

Posterior parameter estimates of the profit function.

To reaffirm the suitability of the random stochastic profit frontier model compared to the fixed stochastic profit frontier model, we again use the DIC test. The random coefficient model has a DIC = −671.74, lower than the DIC of the model with fixed coefficients (DIC=753.3). This result confirms the assumptions of heterogeneity among the firms in the sample and of how this heterogeneity is affecting their performance.

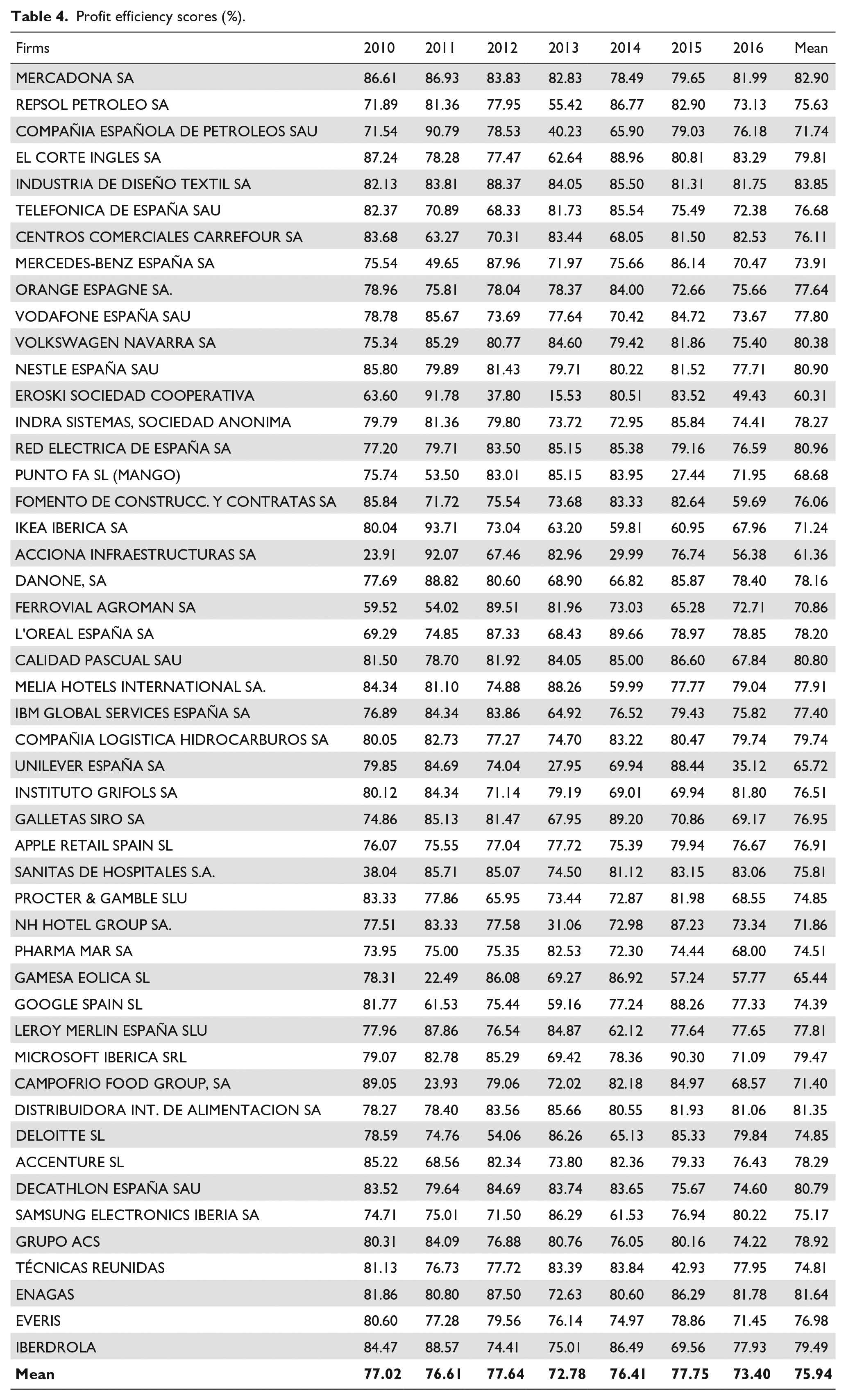

Once the parameters of the proposed model have been estimated, it is possible to calculate the profit efficiency for each firm. The efficiencies obtained throughout the period of study (2010-2016) are presented in Table 4. The average efficiency of the profit frontier with random coefficients is 75.94%, which implies that these firms are wasting, on average, 24.06% of their maximum potential profit. However, the average profit efficiency level decreases significantly (57.40%) if we use a fixed coefficient frontier model 15 to estimate these efficiencies. This difference between the estimated efficiencies exists because, unlike the random coefficient frontier model, the fixed coefficient frontier model does not take into account the heterogeneity between firms, leading to erroneous efficiency estimates when overestimating inefficiencies. That is, the fixed coefficient model assumes homogeneity among the firms when estimating a common efficient frontier for the whole sample and measures the efficiency by the distance of each firm from this common frontier. However, the random coefficient model considers firms to have different resources, and therefore, each firm will have its own efficient frontier. In this case, efficiency is measured by the distance of each firm from its efficient frontier.

Profit efficiency scores (%).

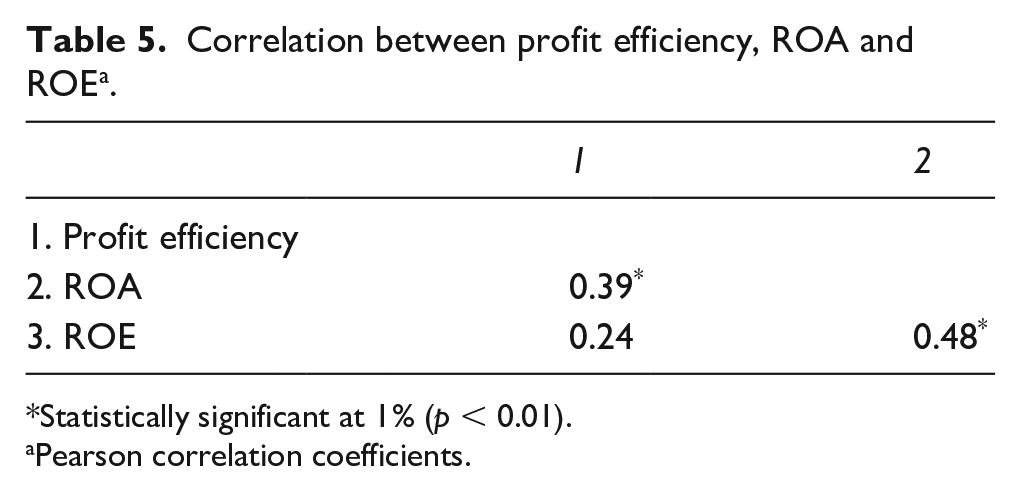

As indicated previously, profit efficiency is a measure of firm performance that is different from traditional accounting or financial measures, and they are not necessarily correlated. In this case, the correlation between profit efficiency and ROA is significant, although low (0.39, p <0.01), while profit efficiency is not correlated with ROE (Table 5). This result confirms the idea that a firm can have high efficiency, and yet this greater efficiency may not be reflected in ROA or ROE.

Correlation between profit efficiency, ROA and ROE a .

Statistically significant at 1% (p < 0.01).

Pearson correlation coefficients.

By specifying the inefficiency effects function, frontier models also allow us to incorporate, in a single stage estimation procedure, a hypothesis test about the sources of competitive advantage. The coefficient of the variable reputation (z1) in the profit inefficiency effects function is positive (0.14) and significant (p < 0.01), indicating that it is a determinant factor in profit efficiency and, therefore, a greater corporate reputation means an increase in performance. This result supports the hypothesis that reputation is a strategic resource that allows firms to improve their performance as measured by profit efficiency. The coefficient of the variable trend (z2) was also included in the inefficiency effects function to assess whether profit efficiency remains constant over time or varies during the study period. The estimation of this parameter was not significant, so we can affirm that profit efficiency has remained unchanged during the study period.

Discussion and Conclusions

Since the first works of Wernerfelt (1984) and Barney (1991), there have been numerous studies on the RBV. However, this theory has often been criticized for its lack of empirical support. Two of the most controversial issues surrounding the empirical tests on the RBV have been the measure of the firm’s performance and the applied methodology. Most RBV research employs accounting and financial indicators to measure a firm’s performance. However, these indicators have serious shortcomings. Furthermore, the methodologies used so far do not adequately address a key issue for RBV – the heterogeneity of resources across firms.

This paper introduces two important innovations to the existing literature. First, we argue that using profit efficiency as a dependent variable in the empirical tests on the RBV is more appropriate than using the traditional financial or accounting measures of firm performance. Second, our study proposes an appropriate methodology for measuring firm performance based on the efficient use of its resources: the frontier model with random coefficients. This methodology allows, on the one hand, to separate the inefficiencies in the transformation of resources from differences in the allocation of resources across firms and, on the other, specification of a hypothesis test with respect to the sources of competitive advantages in a single stage estimation procedure. Thus, using a stochastic frontier model with random coefficients enables an appropriate consideration of resource heterogeneity. Both the measurement of performance and the methodology are, to our knowledge, being used for first time in empirical research on the RBV.

Using profit efficiency as a measure of the firm’s performance does not present the drawbacks of traditional financial measures. As Coff (1999: 131) states, traditional measures of performance usually only include a small portion of the rent generated in the firm, since most of this rent is appropriated by the most powerful stakeholders. In contrast, the concept of profit efficiency reveals how much more profit a firm could achieve if it were fully efficient in the use of its resources, both in costs and in revenues. In addition, efficiency allows a firm to monitor its effectiveness in achieving its goals and objectives, and “it is closely linked to efforts to make strategic plans, clarify organizational goals and objectives, characterize decision-making needs, and analyse managers’ needs for information” (Assaf & Magnini, 2012: 642). Therefore, we believe that profit efficiency is a better predictor of performance because it measures a firm’s ability to manage its resources and produce outputs with greater economic value.

The results of the study show that the mean profit efficiency of the firms in the sample is 75.94%, indicating that there is significant margin to increase performance by improving the efficiency of costs and/or revenue. Likewise, the marked difference between the average efficiency level of the random coefficient model and that obtained by the fixed coefficients model (57.40%), clearly shows the heterogeneity in the allocation of resources among firms and the importance of incorporating this heterogeneity into the empirical analysis. If heterogeneity is not conveniently captured in the empirical methodology, it can lead to an erroneous measurement of the efficiency and, therefore, of firm performance. As a result, we highlight the importance of using the stochastic frontier model with random coefficients in the empirical test on the RBV to adequately capture the differences in the allocation of resources across firms.

In addition, the stochastic frontier models have the advantage of allowing the sources of competitive advantage to be tested. The results reveal that reputation is a strategic resource that provides the firm with a sustainable source of competitive advantage and, consequently, helps it to achieve higher performance, thus providing solid empirical support for the RBV approach. Although other previous works have reached similar conclusions (e.g., Deephouse, 2000; Roberts & Dowling, 1997, 2002; Shamsie, 2003; Vergin & Qoronfleh, 1998), the results of this paper complement these studies on the relationship between corporate reputation and performance using a novel measure of performance and a novel methodology.

This study also incorporates certain topics discussed by Armstrong and Shimizu (2007) regarding empirical research on the RBV:

Sustainability of the dependent variable. This research uses a sample of firms from 2010-2016 (longitudinal analysis) to incorporate the performance “sustainability” test. According to Barney (1991), if a firm persistently achieves superior performance over a long period of time, then we can state that the company has a sustained competitive advantage.

Multi-industry sample. This study uses data from 11 industries, since within the RBV framework, the value of a resource depends on the specific environment in which a firm operates (Barney, 2001). In addition, this type of sample allows for broader generalization of the results. However, when using a multi-industry sample, it is necessary to control for effects on the performance of each industry. Control for these effects is not necessary when using the stochastic frontier model with random coefficients since this methodology assumes that each firm has its own possibility frontier.

Heterogeneity. The heterogeneity of resources is a central element in the RBV. As such, a methodology that does not consider firms to be homogeneous should be used in empirical studies. As we have noted, the stochastic frontier model with random coefficients considers firms in the sample to be heterogeneous, and it estimates a possibility frontier for each firm.

In conclusion, profit efficiency is a more appropriate indicator than the traditional outcome measures used to date in the empirical tests on RBV. Likewise, the methodology used must adequately capture a central condition of the RBV, that is, the heterogeneity between firms. The frontier model with random coefficients used in this study conveniently reflect this heterogeneity, and it therefore has great potential for empirical research on the RBV.

Although this research does provide empirical support to the RBV literature, it has certain limitations. The sample used is relatively small given the inherent difficulties in measuring intangible resources such as reputation. In addition, due to the unavailability of data, the sample is basically composed of large firms. We also believe that estimating input prices using proxy variables is another limitation of this study. Lastly, it would be beneficial to consider resources/capabilities other than reputation, which would enable their joint impact on performance to be studied.

Footnotes

Acknowledgements

The authors wish to thanks the comments of the Editor and the two anonymous referees.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.