Abstract

Using generalized difference-in-difference and synthetic control modeling, this study estimates the influence of the community-college baccalaureate (CCB) on institutional finance over time and by intensity. Leveraging data spanning 19 years (1999–2017), I find no impact on overall revenue but suggestive evidence of upfront costs and slight increases in total spending post-adoption. Coupled with increased enrollment, per-full-time-equivalent (FTE) revenue and spending decrease, on average, by approximately 12% and 6%, respectively. Adoption of an additional CCB is associated with a 3% decrease in revenue and a suggestive 2% reduction in spending per FTE. Additional robustness checks suggest that these impacts may vary by state. These results suggest that institutions should consider the trade-offs in broadening access to baccalaureate-level education with the associated strain on resources. Policymakers should consider how best to financially support adoptive institutions as they work to meet student and workforce needs. Implications for policy, practice, and research are discussed.

Half of the states in the United States have authorized at least one of their community colleges to offer bachelor’s degree programs (Meza & Love, 2022). Community-college baccalaureates (CCBs) are often applied degrees directly tied to local- or state-level economic needs; are cheaper than comparable programs at traditional 4-year institutions; and are typically implemented in areas with less access to baccalaureate education, with some exceptions (Bragg & Soler, 2017; Walker & Pendleton, 2013). As such, advocates for CCB proliferation point toward their utility in increasing access to baccalaureate-level education, geographically and financially, while simultaneously supporting workforce development (Bragg, 2019; Floyd & Skolnik, 2019). Our extant understanding of the impacts of CCB adoption point to mixed success in helping achieve these goals (Love, 2020; Meza & Bragg, 2020; Park et al., 2018; Wright-Kim, 2022).

The success of these programs as well as of the CCB-granting institutions themselves requires attention to their financial contexts. Institutions are adopting CCBs from increasingly financially constrained positions due to declining enrollment and volatile funding from public sources (Artis & Bartel, 2021; Myran, 2013; Price et al., 2016; Romano & Palmer, 2016). Compared to their public 4-year counterparts, community colleges generate just two-fifths of the revenue (Yuen, 2020) and spend approximately 66% less per full-time equivalent (FTE) (author’s calculations; NCES, 2021). This chronic under-resourcing has long raised concerns regarding the sector’s ability to adequately fulfill the needs of its students (Hillman, 2020; Kahlenberg et al., 2018) and begs the question of how expansion toward 4-year programming influences the issue (Romano, 2012; Thor & Bustamante, 2013).

Although some scholars describe CCB adoption as a potential boon to greater financial security (e.g., Skolnik, 2008), others have noted it as a potential source of “resource stress,” as community colleges attempt to accommodate 4-year programming alongside their laundry list of 2-year functions (Levin, 2004, p. 19). Available research regarding the fiscal ramifications of CCB adoption remains limited (McKee, 2005). Although ostensibly offering avenues to increased funding (Bemmel et al., 2008; Martinez, 2018; Plecha, 2007), recent analyses find no significant impact on total revenue post–CCB adoption (Ortagus & Hu, 2020). Simultaneously, CCB-granting institutions may have to significantly increase spending to cover the costs associated with baccalaureate-level education, including new faculty, student programming, and investments in instructional and academic resources (Makela et al., 2015; McKinney & Morris, 2010). However, more research is needed to further highlight the financial implications of CCB adoption, including how revenue and spending may vary over time and by the number of CCBs adopted (e.g., Ortagus & Hu, 2020).

Financial benefits and resource stress brought on by CCB adoption depend on, among other things, the number of students that adoptive institutions must serve. Evidence suggests that adding baccalaureate-level education to academic offerings leads to increasing enrollment (Neuhard, 2013; Vidal-Rodriguez, 2019). A significant influx of students may bring increases in enrollment-based revenue, but if enrollment growth outpaces incoming resources, adoptive institutions may end up having fewer resources per student overall; institutional spending may be similarly affected. As such, examination of financial measures that account for these variations in enrollment may be particularly useful (Romano, 2012).

As policymakers introduce more CCB legislation (Love et al., 2021) and institutional leaders consider baccalaureate-degree adoption, the need to more fully understand the financial implications becomes apparent. Such an examination contributes to the discussion of potential resource stress and yields insight into how CCB adoption may affect the resource constraints and fiscal sustainability of the community-college sector, including whether adoptive institutions end up doing “more with less” (Kahlenberg et al., 2018) as they attempt to support more students through dual 2-year and 4-year missions. Moreover, it provides potential CCB adopters and institutions considering expansion an indication of the fiscal realities of baccalaureate-degree growth, which may be crucial to successful CCB adoption and implementation (Essink, 2013; Floyd & St. Arnauld, 2007; Loglisci, 2018).

This study contributes to this understanding by leveraging a national sample and utilizing quasi-experimental approaches to estimate the average and dynamic impacts of CCB adoption on institutional finance. In doing so, it directly builds upon prior research by estimating shifts in revenue and spending over time, while accounting for shifts in enrollment and exploring how finances may shift at adoptive institutions as the number of CCBs changes.

Specifically, I explore these questions:

What is the impact of CCB adoption on institutional revenue and revenue per FTE over time and by level of adoption?

What is the impact of CCB adoption on education and general (E&G) expenditures and E&G spending per FTE over time and by level of adoption?

Literature Review

To contextualize this exploration, I first outline the general nature of CCB adoption. Then, I explore the extant literature regarding potential catalysts for revenue shifts post-adoption before outlining what is known regarding CCBs and institutional spending.

The Nature of CCBs

Although they have been in existence since the 1970s, CCBs began proliferating in earnest in the early 2000s, and their numbers continue to increase (Floyd & Skolnik, 2019; Love et al., 2021). Authorization to offer CCBs typically comes from state-level legislation. Approval processes vary by state but often require institutions interested in developing bachelor’s programs to show evidence of student demand, documented economic need for the degree, and proof of no competition with 4-year programs (Fulton, 2020). CCBs are often applied degrees with an occupational focus; sample programs include bachelor of applied science in distribution management and bachelor of applied technology in building technology, although some institutions also offer more typical 4-year degrees, such as a bachelor of arts (Bragg & Soler, 2017; Floyd et al., 2005).

The intensity of CCB adoption varies across states and institutions. Initial adoption is typically limited to select institutions and a specific number of programs, and some institutions have maintained limited levels of adoption (Floyd & Skolnik, 2019; Fulton, 2020). However, others have experienced exponential growth over time. For example, beginning with a single institution approved to offer a bachelor’s degree in 2001, virtually all of Florida’s community colleges now offer CCBs, resulting in almost 200 distinct programs (Love & Palmer, 2020). Scholars note the potential impacts of CCB adoption, including influences on institutional finance, are likely to change along with the number of CCBs adopted (Daun-Barnett & Escalante, 2014; Ortagus & Hu, 2020).

The most consistently cited motivations for CCB adoption include broadening educational access and addressing unmet community needs, including issues of workforce development (Floyd & Walker, 2008; Walker & Pendleton, 2013), although some studies suggest that the potential benefits for institutional finances may also play a role in the adoption of baccalaureate programs (Loglisci, 2018; McKinney et al., 2013; Plecha, 2007). At a minimum, scholars and practitioners have emphasized the importance of resource considerations in successful CCB adoption and implementation (e.g., Bemmel et al., 2008; Essink, 2013). Given the potential for implementers to have “significantly underestimated” the resources necessary for certain aspects of the CCB process, examination of the range of financial implications for adoptive institutions may be particularly informative for future policy and practice (McKinney & Morris, 2010, p. 198).

CCBs and Revenue

CCBs present an opportunity for institutions to broaden their target market (Phelan, 2016) by appealing to students’ preferences via lower-cost degrees connected to employment opportunities (e.g., Reyes et al., 2019). Recent analysis shows a .05% increase in total FTE enrollment at the state level post–CCB adoption (Vidal-Rodriguez, 2019). Recent institution-level analyses at CCB-granting institutions suggest an approximate 8% increase, on average, in FTE post-adoption (Wright-Kim, in press). As institutions predominately reliant on enrollment-based revenues (Romano & Palmer, 2016), such increases have the potential to significantly benefit community colleges’ financial landscapes.

Institutions may also garner additional funds by adopting CCBs from changes in state appropriations (Bemmel et al., 2008) or state-sponsored pilot funds for baccalaureate-programming development. For example, for every student enrolled in upper-division baccalaureate courses in the Florida College System, the community college receives 85% of the direct cost of the state-university funding for similar upper-division programs (Bemmel et al., 2008; Furlong, 2003, 2005). In 2005, the state of Washington allocated $100,000 to help four selected community colleges pilot the development of applied baccalaureate programming and provided $6,300 per FTE to support the equivalent of 40 full-time enrollees. Expansion into baccalaureate-level education may also help traditional 2-year institutions attract other sources of funds, including external grant funding or research dollars (Furlong, 2005; Martinez, 2019; Plecha, 2007).

However, CCBs may not be as revenue-generating as previously thought. In his mixed-methods study, Essink (2013) surveys 27 stakeholders and interviews 10 faculty and administrators representing different CCB-granting institutions regarding their baccalaureate programming. Almost half (48%) of respondents rank “additional financial resources” as the most important necessity to transition to baccalaureate degree–granting status. Half of the interviewees describe fiscal strain post–CCB adoption, wherein the costs of investing in staff and programming have outpaced increases in revenue. As one respondent notes, they have not “seen the ability to add resources” (Essink, 2013, p. 79).

In their national quasi-experimental analysis, Ortagus and Hu (2020) estimate the fiscal impact of CCB adoption on total institutional revenue as well as institutional dependence on certain sources of funding. The authors find no significant impact on total revenue. However, compared to non-adopting institutions, CCB-granting institutions have decreased their reliance on public appropriations by as much as 3% and have increased their reliance on tuition revenue as a proportion of total revenue (approximately 1.7%). This shift is due, in part, to increased tuition and fee rates at adoptive institutions (Ortagus & Hu, 2019).

This foundational research (e.g., Essink, 2013; Ortagus & Hu, 2020) sets an important baseline understanding but also points to further necessary inquiry for a holistic comprehension of the revenue-related impacts of CCB adoption. For example, impacts on revenue may vary over time; after initial start-up funding, Washington made cuts to the higher-education budget, leaving community colleges to rely on diminished public support or “other fund sources” to implement CCBs (England-Siegerdt & Andreas, 2012, p. 31). The wide variation in funding approaches that states take toward CCB programming suggests that impacts may also vary by state (Floyd & Skolnik, 2019; Love & Palmer, 2020). Finally, revenue shifts likely vary by the number of CCBs implemented (e.g., Ortagus & Hu, 2020), as more programs likely attract more students. Given these potential shifts in enrollment (Vidal-Rodriguez, 2019), attention to shifts in revenue per FTE post–CCB adoption may be particularly useful in accurately assessing the level of resources that institutions have to serve their students and fulfill their expanded missions.

CCBs and Spending

CCB adoption may also increase institutional spending. Increased spending may come from hiring more doctorate-holding faculty or investing in library resources and learning, academic, and student-support services that can come from offering bachelor’s degrees (e.g., Wheelan & Benberg, 2013). In the case of one CCB-granting institution, interviewees identified investing in advising, first-year experience programming, and support staff post-adoption (Martinez, 2018). Case-study research and web-based inventories of select CCB-granting institutions also suggest that adoptive institutions may direct additional resources toward financial-aid expenditures (Elue & Martinez, 2019; Makela et al., 2015).

Similar to revenue, the costs associated with CCB adoption may vary over time and intensity of adoption. For example, extant descriptive literature suggests that CCB adoption incurs substantial upfront costs. College leaders from the Florida College System noted start-up costs of “about $125 to $165 thousand” per CCB (McKinney & Morris, 2010, p. 201). Although these figures may be limited in generalizability, given Florida’s broad authorization for and high levels of CCB adoption (Floyd & Skolnik, 2019), they provide an illustration of the type of spending needed to enter into baccalaureate-level education. Initial costs may stem from compliance with changes in accreditation associated with moving from a 2- to 4-year institution or implementing specific accredited programs (e.g., Floyd & St. Arnauld, 2007), which require institutions to “have sufficient resources to fulfill their mission,” although the level of resources deemed “sufficient” by such accreditation agencies is unclear (Wheelan & Benberg, 2013, p. 66). For example, the Southern Association of Colleges and Schools Commission on Colleges (2018), an accreditation agency, requires an “adequate number of academic and student support services staff . . . to accomplish the mission of the institution” and that institutions must provide “appropriate” services and activities “consistent with their mission” (pp. 114–116).

Some research suggests that institutions may need to invest more resources than allocated by the state to implement CCBs (e.g., Essink, 2013). Between 2001 and 2010, CCB-granting institutions in Florida invested almost $47,000,000 more in their baccalaureate programs than was allocated by the state to support the baccalaureate initiatives (in 2010 dollars; Bottorff, 2011). In such occasions, resources may need to be diverted from other programming (McKinney & Morris, 2010). If spending outpaces increases in revenue, coupled with potential increases in enrollment, then CCB-granting institutions may have to spread continually strained resources across a wider array of functions and students (Romano, 2012).

The need to build upon this prior research and examine potential shifts in spending is twofold. First, a nuanced understanding of the spending required to adopt and expand baccalaureate programs is key to the success of the initiatives (Bemmel et al., 2008; Essink, 2013; Floyd & Skolnik, 2019; McKinney & Morris, 2010). More broadly, this examination contributes to the discussion surrounding resource stress (e.g., Levin, 2004) amid CCB expansion and the extent to which CCB-granting institutions are spreading finite resources across additional functions and students, thereby continuing to “educate the students with the greatest needs, using the least funds” (Century Foundation Task Force, 2013, p. 4). These financial impacts may also have broader implications for the institutions themselves. For example, although the evidence connecting community-college spending and student outcomes remains somewhat mixed (Calcagno et al., 2008; Ishitani & Kamer, 2020; Stange, 2012), a recent exploration of student outcomes and institutional characteristics across community colleges notes some significant associations between institutional spending per FTE and 3-year graduation rates (Ishitani & Kamer, 2020). As such, shifts in spending per FTE in either direction may have impacts for student success overall.

Conceptual Framework

Community colleges are navigating an ever-shifting environment of volatile public funding (Ma et al., 2020), declining enrollments (Romano & Palmer, 2016), increasing need for baccalaureate-level education, and workforce demands (Floyd & Skolnik, 2019; Hanson, 2009). Neo-institutional theories (DiMaggio & Powell, 1983; Meyer & Rowan, 1977), including resource-dependence theory (Pfeffer & Salancik, 1978), suggest that these factors may induce community colleges to shift their behavior as a means of “organizational responsiveness to external demands and expectations” (Drees & Heugens, 2013, p. 1673). Moreover, such behavioral shifts may be influenced by institutions’ need to shore up institutional stability and acquire the resources needed for survival (Davis & Cobb, 2010). Through this lens, CCB adoption can be cast as a rational response to external pressures. Indeed, research suggests that CCB adoptions are tied to combatting issues of educational attainment and labor shortages (Henderson, 2014), while also recognizing the potential influences on community-college resources (e.g., enrollment, revenue; Loglisci, 2018; McKinney & Morris, 2010; Plecha, 2007).

Although resource dependence offers a lens through which shifts in community-college behavior could be viewed in terms of resource generation, it also points to the potential impacts that such pursuits have on overall institutional performance (Zona et al., 2018). This focus is also salient in the CCB context. As Skolnik (2008) notes, in addition to increasing access to the baccalaureate and meeting community needs, although CCB-granting institutions may very well be motivated by “increased stature” or “more resources,” they do so to increase their performance and abilities “in fulfilling [their] mission” (p. 148). One potential measure of performance likely affected by CCB adoption is institutional spending. Institutional expenditures are directly connected to shifting patterns of revenue (Chakrabarti et al., 2020; Fowles, 2014; Leslie et al., 2012). A growing body of work confirms that policy adoption that alters community colleges’ resource environments also significantly alters their spending patterns (e.g., Delaney & Hemenway, 2020; Odle & Monday, 2021). This suggests that the shifts in sources of funding amid baccalaureate expansion (Ortagus & Hu, 2019, 2020) also influence institutional spending. Moreover, CCB adoption further alters the dynamics surrounding institutional spending itself, including the number of students needing to be served (Vidal-Rodriguez, 2019), the types of programming required to support baccalaureate-level education (Martinez, 2019; McKinney & Morris, 2010), and the altered expectations regarding investments in academic and other resources that accrediting bodies set before adoptive community colleges as newly authorized 4-year degree-granting institutions (Floyd & St. Arnauld, 2007)—all of which suggest the potential for significant impacts on institutional expenditures.

Overall, adoption of the CCB—whether motivated by a desire to address communal needs, a need to address persistent resource constraints, or both—sets the stage to significantly alter institutions’ financial landscapes. These potential impacts on revenue and spending stem from a range of changes in institutional environments, including those catalyzed via the adoption process (i.e., funding regulations outlined in state-level CCB authorization or standards set by accreditation agencies) as well as other by-products of CCB adoption (e.g., increases in FTE).

As state legislatures and institutional leaders continue to debate whether or not to adopt and/or expand CCBs (Love & Palmer, 2020), the need to more fully understand the financial implications becomes more apparent. An accurate understanding of the resources needed to adopt and expand CCBs is vital to the success of these programs (e.g., Floyd & St. Arnauld, 2007), but it also contributes to the broader discussion of resource stress at adoptive institutions, as they add another function to their already-expansive missions (Cohen et al., 2014). Specifically, this study seeks to build on the growing body of CCB-related literature and contribute to this understanding by rigorously examining the dynamic impacts of CCB adoption on revenue and spending and providing novel estimated impacts over time and the number of programs implemented.

Data

To answer my research questions, I constructed a data set spanning academic years 1999–2000 to 2017–2018 of all public 2- and 4-year U.S. institutions (n = 1,673). I cross-referenced prior research (e.g., Ortagus & Hu, 2019, 2020), state legislation, academic catalogs, and Community College Baccalaureate Association’s (CCBA, n.d.) inventory of CCB programs to identify treatment. Identification of CCB institutions often varies across scholarship (Floyd & Skolnik, 2019); Appendix A outlines the treated institutions used in this study as well as commonly identified CCB-granting institutions that were removed due to data limitations.

After identifying treated institutions, I limited the sample to 2-year institutions with associate degrees as their highest offering to remove the non-CCB-granting 4-year institutions (n = 906). I then limited the data set to those institutions present across the entire panel. To help maintain sample size, I employed within-campus linear interpolation to impute missing outcome or covariate values for observations in this remaining sample. 1 The resulting analytic sample consists of 783 institutions across 19 years, including 85 CCB-granting institutions.

To assess the effects of CCB adoption on institutional finances, I explored four outcome variables. Like prior researchers (Ortagus & Hu, 2020), I first explored total operating and nonoperating revenue before estimating the impact on revenue per FTE. Then, I explored shifts in spending, operationalized as total E&G expenditures. I used total and per-FTE 2 E&G expenditures to account for shifts in institutional enrollments. I defined E&G expenditures as the current year’s total expenditures in instruction, research, student services, public services, academic and institutional support, operations and maintenance, and net grant aid. 3 All outcome variables were compiled from the Urban Institute’s (n.d.) Education Data Explorer, which cleans data from the Integrated Postsecondary Data System (IPEDS) for longitudinal analyses across institutions. 4 All financial variables were adjusted to 2017 dollars via the consumer price index for all urban consumers.

To help reduce the bias of my estimates, I included a series of state-, county-, and institution-level covariates also known to affect institutional finances (see Table 1 for descriptive statistics). Time-varying control variables included state-level political and spending characteristics (e.g., Kelchen & Stedrak, 2016; Tandberg et al., 2017) as well as population size (Dowd & Shieh, 2014). I included a series of demographic and economic county-level characteristics to account for the influence of local service-area characteristics on community-college enrollments and revenues (Hillman & Orians, 2013). Finally, I included a vector of institutional characteristics, including tuition rates and enrollment demographics, that may influence institutional revenue and spending (e.g., Dowd & Grant, 2006; Ortagus & Hu, 2019, 2020). To account for economies of scale (Toutkoushian & Paulsen, 2016), I also included a measure of institutional size in the models, with outcomes not scaled by FTE enrollment. Given the identified correlation between institutional revenues and expenditures (Leslie et al., 2012), I included measures of total revenue and total spending when modeling the impact on their counterpart. See Appendix B for a full list.

Average descriptive statistics, final year of panel

Note. Standard deviations are in parentheses. All finance variables are adjusted to 2017 dollars. CCB = community-college baccalaureate; E&G = education and general; FTE = full-time equivalent; URM = underrepresented minorities.

Empirical Strategy

I employed a difference-in-differences (DID) approach with staggered treatment to estimate the average treatment effect (ATT) of CCB adoption. Scholars have commonly used a two-way fixed-effects (TWFE) regression in the event of staggered treatment and often include an event study specification to assess changes over time. However, recent work has noted key limitations to these approaches, including the introduction of bias in the event of heterogeneous treatment effects over time (Borusyak et al., 2021; Callaway & Sant’Anna, 2020; Goodman-Bacon, 2021; Sun & Abraham, 2021). To address these issues, I employed the alternative DID estimator described by de Chaisemartin and D’Haultfoeuille (2020a, 2020b), which, unlike TWFE regression, is robust to these issues; the approach was implemented through the did_multipleGT Stata package (de Chaisemartin et al., 2021). The general specification is represented as

where

This approach yields instantaneous treatment effects for the year of CCB adoption as well as cumulative effects for

However, CCB adoption expands beyond a simple binary treatment. Intensity of adoption ranges from one program to more than 20 in the last year of the panel. Equation 1 also accommodates continuous treatments, wherein treated institutions experiencing a change in the number of CCBs adopted in a given year are compared to institutions with the same level of treatment. For example, when Gulf Coast State College goes from offering two CCBs at time t to three CCBs at t + 1, the “control” units it will be compared to are institutions that maintained their number of CCBs at two across both time periods. As with binary treatment, this approach yields instantaneous and dynamic treatment effects over time and, when aggregated, provides a weighted sum of the ATT and suggests the average effect produced by a one-unit increase in CCB programs (de Chaisemartin & D’Haultfoeuille, 2020a, 2020b).

To account for this variation, I estimated a second set of models by using a continuous treatment—the number of CCBs implemented in a given year—constructed primarily by using institutional academic catalogs and cross-referencing with state legislation, resources provided by CCBA, and prior research. Programs were counted as distinct CCBs if they resulted in different degrees (bachelor of arts vs. bachelor of applied science) or were housed in different disciplines (bachelor of arts in mathematics versus bachelor of arts in criminal justice) and were counted as being an additional program starting the year of their implementation. As a check on the sensitivity of the results based on this classification, I also estimated models by using two alternative constructions: a categorical treatment based on quartiles of the number of CCBs adopted and a categorical treatment based on the distribution of the number of CCBs adopted to represent the range of adoption.

Similar to standard DID (Angrist & Pischke, 2009), both estimators described above rely on the common-trends assumption for causal inference. I took multiple steps to assess its plausibility. First, I constructed multiple control groups to help ensure the identification of a compelling counterfactual: all non-treated public 2-year community colleges in the continental U.S. (the primary control group), all non-adopters in states with CCB authorization, and all public 2-year institutions in non-adoptive states (Furquim et al., 2020). Finally, I extended Equation 1 to include the placebo estimators,

Limitations

Although it provides important implications for practitioners, policymakers, and other stakeholders regarding CCB adoption, this study has several limitations. First, by design, a DID approach treats CCB adoption as an exogeneous shock to institutional finance. CCB approval typically comes from external authorities (Fulton, 2020), but CCB adoption may be endogenous to institutions, as they play a role in seeking approval and may systematically differ from non-adoptive institutions (Floyd & Skolnik, 2019). I attempted to address this issue by controlling for various institution-, county-, and state-level characteristics and using multiple control groups as sensitivity checks. However, in the absence of random assignment, care should be taken when interpreting these results as causal. Potential violations of the common-trends assumption when exploring shifts in spending further warrant cautioned interpretation.

There are also inherent issues when using IPEDS expenditure data, including inconsistent reporting standards over time and institutional discretion in how it categorizes its spending (Kolbe & Kelchen, 2017). Using aligned Urban Institute (n.d.) data and an aggregated measure, such as E&G expenditures, reduces these concerns. I conducted additional analyses using total expenditures not subject to institutional categorization as a sensitivity check. Yet by using aggregated financial measures, I was unable to explore the specific sources of revenue and allocations of expenditures that may be directly affected by CCB adoption (e.g., instructional expenditures). Future research using system- and institution-provided administrative data is needed to further explore these nuances.

Additionally, although this study attempts to build on prior research (Ortagus & Hu, 2019) by capturing the variation in the number of CCBs adopted in a year, these results rely on my definition of distinct CCBs. I attempted to address this issue by including alternative categorical constructions of the continuous treatment variable and cross referencing with external data sets. 5 However, using publicly available institution-level finance data limits the ability to explore potential heterogeneity in the impact of CCB adoption by program type or function. For example, I was unable to ascertain which types of CCB programs at a given institution may have a differential effect on revenue and expenditures.

Additional Robustness Checks

Finally, although the primary empirical approach accounts for instantaneous and dynamic effects of CCB adoption, it aggregates impacts across institutions and obscures potentially useful information regarding the varied impacts of CCB adoption across policy contexts (e.g., CCB legislation, states’ approach toward proliferation; Fulton, 2020). Moreover, prior research suggests that differing state-level approaches to CCBs may uniquely drive the results of CCB-impact studies (i.e., Florida; Park et al., 2018). I conducted two additional robustness checks to better explore these potential nuances. Following prior research (Park et al., 2018), I estimated Equation 1 again but removed Florida institutions from the analyses to explore the impact of CCB adoption without the influence of the state’s unique level of CCBs. Second, given its ability to estimate treatment effects on a sample size as small as a single institution (Xu, 2017), I leveraged the generalized synthetic control (GSC) approach as a way to examine this variation, even in states with low CCB adoption. Using a nested interactive fixed-effects and factor analysis (Bai, 2009), GSC constructs a synthetic control group by weighting observations from a pool of non-CCB granting institutions, such that its trends in pretreatment outcome are comparable to those of CCB-granting institutions (Xu & Liu, 2018). The functional form of the GSC model is

where

Findings

To assess the impact of developing and implementing baccalaureate-level education on community-college finances, this study explores the effect of CCB adoption on institutional revenue and spending, overall and per FTE student. I first present findings from the specification, using the binary treatment. I then explore the results by using the number of CCBs adopted as the treatment before discussing findings from select robustness checks. In all cases, outcomes are logged and may be interpreted as changes in percentages.

Effects of Overall CCB Adoption

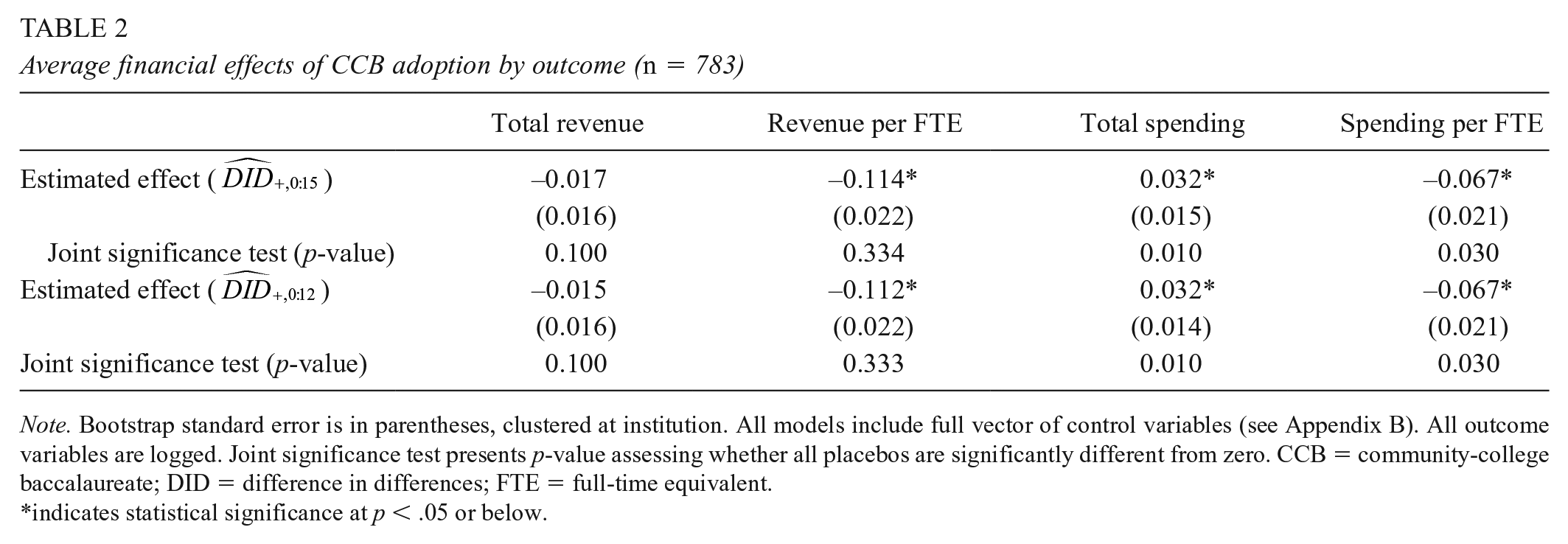

Table 2 presents the aggregated cumulative treatment effects of CCB adoption 15 years (

Average financial effects of CCB adoption by outcome (n = 783)

Note. Bootstrap standard error is in parentheses, clustered at institution. All models include full vector of control variables (see Appendix B). All outcome variables are logged. Joint significance test presents p-value assessing whether all placebos are significantly different from zero. CCB = community-college baccalaureate; DID = difference in differences; FTE = full-time equivalent.

indicates statistical significance at p < .05 or below.

Insignificant F-tests of joint significance across revenue-related outcomes suggest plausible adherence to the common-trends assumption. These results are also generally robust to alternative comparison groups (Appendix D), specifications (Appendices E and F), and aggregation at year 12 (Table 2;

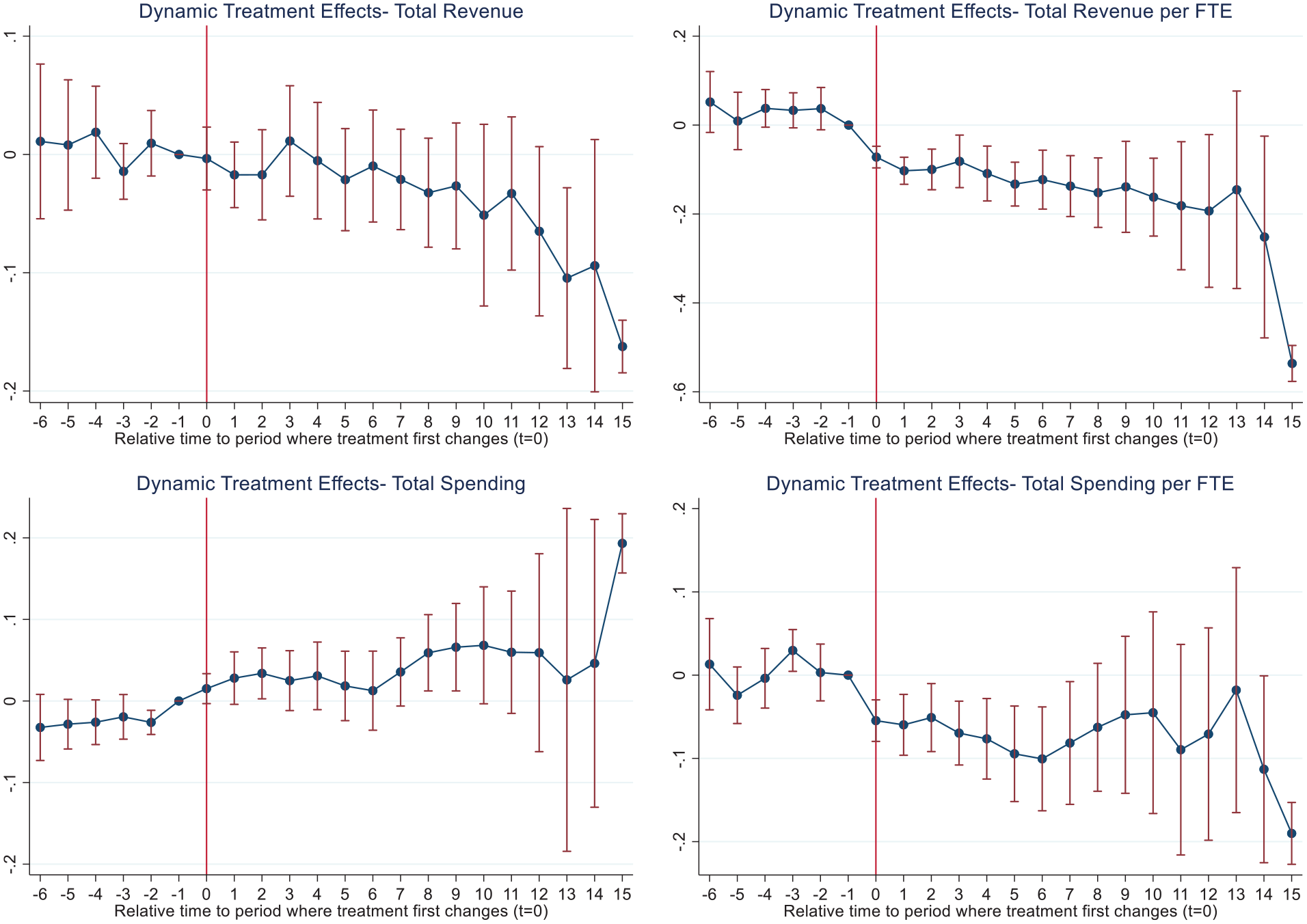

Figure 1 presents the

Dynamic financial effects of CCB adoption over time.

Regarding spending, the results show potential evidence of upfront costs associated with CCB adoption. On average, CCB-granting institutions spent approximately 1.5% more than non-adopters in their first year of implementation (

Effects of CCB Adoption by Intensity

Table 3 presents the estimated ATTs at 15 (

Average financial effects of CCB adoption by outcome, using continuous treatment variable (n = 783)

Note. Bootstrap standard error is in parentheses, clustered at institution. All models include the full vector of control variables (see Appendix B). All outcome variables are logged. Joint significance test presents p-value assessing whether all placebos are significantly different from zero. CCB = community-college baccalaureate; DID = difference in differences; FTE = full-time equivalent.

indicates statistical significance at p < .05 or below.

Dynamic financial effects of CCB adoption over time—continuous treatment.

Similar to the primary estimates, I find no significant average impacts on total revenue, yet I note an approximate 1% increase in spending (

Figure 2 shows the dynamic treatment effects using the continuous treatment, which follow the same trends as the primary dynamic estimates. Aside from a slight peak at period 3, estimated impacts on total revenue show insignificant decreases over time. Alternatively, a one-unit increase in CCBs is associated with a significant decrease of approximately 7% (

Figure 2 shows significant increases in spending, on average, in the initial years post-adoption. A one-unit shift in the number of CCBs adopted is associated with an approximate 1.5% (

GSC modeling—counterfactual plots by state and outcome.

Robustness Checks

Estimates Without Florida

Although the aggregated impact of CCB adoption is robust to its removal (

Average financial effects of CCB adoption by outcome, without Florida institutions (n = 758)

Note. Bootstrap standard error is in parentheses, clustered at the institution. All models include a full vector of control variables (see Appendix B). All outcome variables are logged. Joint significance test presents p-value assessing whether all placebos are significantly different from zero. Due to data limitations, ATT is inclusive of only 12 years post-adoption. ATT = average treatment effect; CCB = community-college baccalaureate; DID = difference in differences; FTE = full-time equivalent.

indicates statistical significance at p < .05 or below.

The results show consistent null impacts on total revenue. Significant decreases in revenue per FTE of approximately 9.5% (

GSC

The overall average impacts of CCB adoption across revenue and spending measures estimated via GSC modeling (see Appendix K) generally support the primary estimates of an approximate 7% increase in spending, on average, with decreases in revenue and spending per FTE, although levels of significance differ. To further explore the potential for heterogeneous effects across CCB adopters indicated by Table 4, Figure 3 presents the counterfactual plots constructed via the GSC approach by outcome and state. The blue dotted line shows observed trends in each outcome for the constructed counterfactual, while the black shows the trends for the treated institutions within a state. Alignment between counterfactual and observed trends before treatment (i.e., prior to the gray line) suggests adherence to the common-trends assumption; any divergence in trends after treatment (i.e., to the right of the gray line) could be interpreted as the potential impact of adoption.

In general, when disaggregated by state, the estimated ATTs are rendered statistically insignificant; 7 however, the plots below are illustrative of some potential for varied impacts of CCB adoption by state. In line with the primary estimates, most states show negligible shifts in overall revenue; however, descriptive trends across North Dakota’s and Hawaii’s few CCB-granting institutions suggest an increase in revenue post-adoption when compared to their counterfactuals. Most states exhibit decreases in revenue per FTE post-adoption; however, contrary to the trends in Table 2, plots of North Dakota and Georgia suggest comparative increases, although wide fluctuations in Georgia pretreatment make a clear relationship less discernable.

Descriptive evidence of shifts in total and per-FTE spending is more varied. Such states as Washington and Colorado show suggestive evidence of increases in overall spending, while comparisons between observed and synthetic control in Florida show virtually no deviation. Some states, such as California and Michigan, show no discernable trends in spending per FTE, while the remaining states generally align with the primary DID estimates and suggest decreases in spending per student over time. Such potentially heterogeneous shifts by state across total and per-FTE spending may be driving the somewhat-inconsistent estimates across Tables 2 and 4 and other alternative comparisons (e.g., Appendix D).

Discussion

CCBs have the potential to increase access to baccalaureate education by offering lower-cost alternatives to traditional programs, particularly for geographically bound students (Floyd & Skolnik, 2019). They can help address pressing economic needs by offering workforce-oriented credentials (Bragg, 2019; Walker & Pendleton, 2013). CCBs may also benefit adoptive institutions by broadening their markets and increasing revenue streams, both of which may bolster a sector of higher education that is particularly affected by volatile public support (Cohen et al., 2014).

Despite these potential benefits, concerns remain that the addition of baccalaureate-level programming may cause resource strain at community colleges (Levin, 2004), further compounding the preexisting gaps in resources between 2- and 4-year institutions (Kahlenberg et al., 2018). This potential unintended consequence has given rise to some stakeholders worrying about the ability of adoptive institutions to support dual 2- and 4-year missions (Thor & Bustamante, 2013; Wattenbarger, 2000). Others note the need to understand the fiscal implications of CCB adoption to help ensure programmatic success (e.g., Loglisci, 2018).

This study contributes to this discussion and the growing CCB literature methodologically and substantively. First, it extends prior research (Ortagus & Hu, 2020) by examining the dynamic and cumulative impacts of CCB adoption over time rather than looking solely at single average estimates; the results presented here also add to the scant primarily descriptive examinations of institutional spending among CCB proliferation. Second, it presents novel estimates regarding the institution-level fiscal impacts of an additional CCB program. Finally, although largely descriptive in nature, it takes initial steps toward offering a fuller understanding of how the impacts of CCB adoption may vary across state contexts.

Although prior research disabused the notion of CCBs as financial boons overall (Ortagus & Hu, 2020), the results presented here further suggest that baccalaureate adoption may not even be effective in attracting resources in the early years of implementation, contrary to some accounts (e.g., Floyd et al., 2005; Loglisci, 2018). Alternatively, due to estimated increases in enrollment ranging from 0.5% to approximately 8% (Vidal-Rodriguez, 2019; Wright-Kim, in press), adoptive institutions have significantly fewer resources to support the influx of students, as measured by revenue per FTE. Moreover, although the estimates are somewhat inconsistent, the evidence presented here suggests that institutions weather stagnant revenues and increasing demand while footing the bill to grow baccalaureate programs. Significant increases in spending, particularly in the initial years post-adoption, identified here align with prior descriptive accounts (e.g., McKinney & Morris, 2010) and suggest that the expansion into baccalaureate-level education comes with marked upfront costs. Yet when viewed on a per-FTE basis, decreases in spending that grow over time suggest that adoptive institutions are having to spread increasingly strained resources across their broadening student populations. However, as suggested in the robustness analyses, these aggregating findings may obscure insightful variation in the impacts of CCB adoption across the country.

These findings provide multiple insights to help inform the future research, practice, and policy surrounding baccalaureate-level education in the community-college sector. First, although CCB adoption may be a useful tool to offset declining enrollments, stagnant levels of revenue suggest that institutions should not view expansion toward baccalaureate education as an expansion toward financial stability. Multiple mechanisms could lead to this effect. Despite perspectives suggesting otherwise, adding bachelor’s degree programs to institutions’ offerings may not open as many opportunities for new or increased funding as hoped (Loglisci, 2018; Martinez, 2018; McKinney et al., 2013; Plecha, 2007). Alternatively, CCB adoption may allow institutions to increase certain revenue streams (i.e., tuition; Ortagus & Hu, 2020), but divestments from other sources result in neutral net effects on revenue.

Although it is outside the purview of this study, future research should explore this phenomenon and ascertain whether, if not a lever to increase overall revenue, CCB adoption could be used to increase specific sources of revenue (e.g., philanthropy). More nuanced examinations of overall expenditures may prove similarly useful, particularly in helping potential CCB adopters in identifying what it costs to adequately support such programs (Loglisci, 2018; Romano, 2012). Given the suggestive evidence for varied impacts by level of CCB adoption and state, these future analyses should take these contexts into account when further examining the impacts of CCB adoption.

Still, extant analyses point to the need for institutional stakeholders to consider the potential financial implications of CCB adoption. Significant overall declines in revenue and spending per FTE suggest that concerns regarding resource stress may be warranted (Levin, 2004; Russell, 2010; Wattenbarger, 2000). As institutions consider expanding their baccalaureate offerings or developing 4-year degrees for the first time, they may need to consider direct examinations of their “financial health” via such measures as the Composite Financial Index to further assess their financial stability (Hearn & Burns, 2021, p. 331). Such examinations may be useful as CCB adopters consider the start-up and expansion costs. Although these costs may fluctuate over time, underestimating the upfront costs related to baccalaureate adoption may cause tension as community colleges navigate their new roles as 4-year degree providers (e.g., McKinney & Morris, 2010).

General declines in per-FTE spending suggest that CCB adoption may exacerbate preexisting resource inequities within the community-college sector (Kahlenberg et al., 2018). Although the connections between institutional spending and measures of institutional outcomes are not fully clear for community colleges (Ishitani & Kamer, 2020; Stange, 2012), practitioners and institutional leaders should consider how the additional strain on resources brought on by CCB adoption may influence student success at the institutions overall. For example, higher-education research is only beginning to explore the idea of “adequacy” in funding (Kahlenberg, 2015), but stakeholders on behalf of the California Community College Chancellor’s office estimated that, based on the demographics and needs of their students, community colleges would need to spend approximately $9,200 per FTE to ensure a quality education (Chancellor’s Office, 2003), far exceeding current spending levels.

Relatedly, stakeholders should consider how CCB adoption influences resource allocation across institutions’ various functions. Most CCB-granting institutions are maintaining their commitments to their historic functions (e.g., developmental education, associate degrees) in addition to baccalaureate education (Floyd & Skolnik, 2019). Emergent research of the Florida College System suggests that CCB-granting institutions are able to sustain their associate degree–granting focus, as measured by the number of degrees conferred (Ortagus et al., 2020), but it is unclear how CCB adoption may influence institutional emphasis in other areas. Given that the cost of educating students from disadvantaged backgrounds is higher than for their more privileged peers (the Century Foundation Task Force, 2013; Cohen et al., 2014), it is important for stakeholders to identify whether institutions may be shifting resources from these high-need areas to accommodate the costs associated with bachelor’s degrees.

Citing baccalaureate programming as an example, Romano (2012) warns that community colleges should be wary of taking on “roles that spread resources too thin,” particularly if those roles fall outside the “core” mission and do not bring in enough revenue to cover their costs (p. 183). The evidence presented here suggests that institutions should consider whether CCB adoption is a financially feasible, and responsible, role to pursue. However, some suggest that baccalaureate education is a “core” mission of community-college work, as it represents an extension of the community college’s commitment to meeting the needs of its students and community (Skolnik, 2008). In many respects, bachelor’s degrees have become the “standard postsecondary credential” (Hanson, 2009, p. 992). By function of most approval processes, CCBs are also meeting community needs by providing academic programs directly tied to economic needs that go unmet by 4-year institutions (Fulton, 2020). Data suggest that CCBs by and large serve students from populations historically underserved by the traditional 4-year sector (e.g., Love, 2020). Studies also suggest that the educational experiences of CCB enrollees (e.g., Shah, 2010) and the job-market prospects of graduates (Meza & Bragg, 2020) are positive.

Given these important benefits of CCB adoption, rather than characterizing the decreases in revenue and spending per FTE presented here as evidence that community colleges are unable to support dual 2- and 4-year missions, stakeholders should consider how to better support these institutions as they broaden access to baccalaureate education and fulfill community needs. Recent data show concern among community-college presidents that states are not providing enough financial support to institutions to ensure quality 4-year programming (Love & Palmer, 2020). For policymakers, this means that rather than divesting from appropriations for adoptive community colleges (Ortagus & Hu, 2020), they should incorporate funding mechanisms that resource CCB-granting institutions at higher levels than are currently done. Increased support from state funds may be particularly important to help community colleges maintain affordable tuition rates for baccalaureate programs (Ortagus & Hu, 2019).

The trends in the interest in and growth of CCBs show no signs of stopping (Love et al., 2021). But to help ensure the sustainability and success of CCB programs and the institutions that adopt them, stakeholders should remain cognizant of the intentional, and perhaps unintentional, impacts of CCB adoption. The fiscal implications of expansion into the baccalaureate will likely remain forefront in the discussions surrounding this proliferating phenomenon. As such, I hope that the findings presented here help inform policymakers, institutional leaders, and other stakeholders as they continue to debate CCB-related policies and shed light on the need to structure institutional and programmatic funding and resource allocation to ensure that CCB-granting institutions can meet the changing baccalaureate and workforce needs of their communities while maintaining robust support for the other facets of their mission.

Supplemental Material

sj-docx-1-ero-10.1177_23328584221126473 – Supplemental material for The Dynamic Financial Implications of the Community College Baccalaureate: An Institutional Exploration

Supplemental material, sj-docx-1-ero-10.1177_23328584221126473 for The Dynamic Financial Implications of the Community College Baccalaureate: An Institutional Exploration by Jeremy Wright-Kim in AERA Open

Footnotes

Author Note

This research was supported by a grant from the American Educational Research Association, which receives funds for its AERA-NSF Grants Program from the National Science Foundation under NSF award NSF-DRL #1749275. Opinions reflect those of the author and do not necessarily reflect those of AERA or the NSF. An earlier version of this paper was presented at the 2022 annual meetings of the American Educational Research Association (virtual) and the Council for the Study of Community Colleges (virtual). The author would like to thank the editors and three anonymous reviewers at AERA Open for vital feedback that greatly strengthened the manuscript.

Supplemental material

Supplemental material for this article is available online.

Notes

Author

JEREMY WRIGHT-KIM is an assistant professor in the Center for the Study of Higher and Postsecondary Education (CSHPE) at the University of Michigan. He studies the intersection of finance, public policy, and institutional and student equity and success, particularly in the community college sector.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.