Abstract

Social finance, an arena of international finance comprising social banking, impact investing, and microfinance, offers a powerful conceptual lens through which to interrogate the interface of finance and labor in financial capitalism. This article investigates social finance’s development at the crossroad of two processes. Social finance emerged in the context of a process of laboring finance, an often-coercive inclusion of workers and households into financial circuits of accumulation and expansion made possible by labor market changes that began in the 1970s. The global financial crisis occasioned the growth of social finance, which, by means of financing labor, placed the reproductive needs of labor—the needs of society’s most disadvantaged agents, the poor, the homeless, the marginal, and unemployed workers—at the center of financial accumulation. By informing an oscillatory movement between laboring finance and financing labor, and, affectively, between trust and distrust, social finance primes and cultivates financial market participants’ belief in purported solutions to the social problems financial capitalism has contributed to create. As a critical investigation of the complex interface between finance and labor that animates social finance’s operations, this article aims to provide conceptual resources that can contribute to releasing labor’s social cooperation from finance’s hegemony.

With its ancient Islamic roots, medieval forebearers and precedents in eighteenth century cooperative, in its present form, social finance is a relatively new arena of international finance. Social finance combines market, financial, and neoliberal processes to address social needs, such as housing, employment, and health, in exchange for an expected return. It consists of a set of institutions, social environments, and financial instruments that aim to support positive social outcomes through the deployment of private capital, often in combination with government funding. This article approaches social finance as a conceptual lens through which to interrogate the interface between finance and labor in financialization processes. The debate on financialization has shown how the trajectories of accumulation and expansion of financialized capitalism impact and disrupt labor’s production and social reproduction dimensions. However, this debate has often conceived labor as a “collateral damage” of financialized capitalism rather than a feature of its dynamism (Adkins 2020; Cooper, 2015; Montgomerie 2020; Thompston and Cushen 2020). I argue that social finance illustrates how labor, as work power in the world of production and as “pure life” or bios, is central to the stability and expansion of financialised capitalism.

Social finance is for many an expression of the need for finance to act as a “servant” to the economy (Dembinski 2009). Although it has precedents that predate the global financial crisis (GFC), its expansion is often related to this tumultuous economic event, which marks the tipping point of a long process of subjugation of society to the rule of finance. The rise of social finance thus accompanies a more general economic transformation in which finance moves beyond its classic role of converting savings into investments to instead become “a coherent pattern of techniques, institutions and behaviors” (p. 2).

I identify two reciprocal processes to conceptually explain how social finance relates to labor, and to orient empirical investigations of how this relation plays out in different national and regional contexts. The first process is laboring finance, which involves the often-coercive inclusion of workers, pensioners, households, and other subjects into financial circuits of accumulation. The second is financing labor, which describes a proliferation of practices, products, and strategies that deliver financial resources to address situations of social and economic disadvantage that are otherwise difficult to tackle under social conditions characterized by the retreat of welfare states and wage repression. I suggest that the reciprocal relation of laboring finance and financing labor gives rise to an oscillatory movement that is vital to explain the workings of social finance. However, such a movement cannot account for the extraordinary growth of this set of socially oriented financial practices. Doing so means adding an additional conceptual frame, centered on the notion of trust. I argue that a loss of trust in the financial system due to the GFC and the material violence and social dislocation occasioned by the GFC is central to understanding the post-2008 boom in social finance. A handshake between governments and finance secures the trust that allows social finance to become a favored means of addressing social reproductive needs, including subsidized housing, education, employment, training, low-income healthcare, and anti-recidivism programs.

My theoretical argument centers around the identification of an oscillatory movement between laboring finance and financing labor, and, affectively, between trust and distrust. Social finance primes and cultivates the potential for financial market participation and growth. A central contribution of this article is to clarify the ideological function of social finance. By enticing subjects traditionally skeptical about finance’s capacity to address social issues to doubt their own distrust, social finance operates as a pivot that regulates an oscillatory movement between trust and distrust. Importantly, the swinging motion that social finance initiates between finance and labor, laboring finance-financing labor, establishes the inter-dependence of these two processes. Rather than conceiving social finance in the context of a sought-after equilibrium between demand for and supply of financial resources devoted to socially relevant needs, social finance promotes and justifies further market expansion, the retreat of governments, and financialization of labor.

By investigating the interface between finance and labor that animates social finance’s operations, I hope to contribute to the literature on the sociology of finance. Drawing on classical sociology (Simmel 1978; Weber, 1981) first, and on the new economic sociology of the 1980s (Granovetter 1985; White 1981), the new economic sociology has approached markets as socially embedded institutions grounded in trust relationships. The study of social finance, particularly its ideological function and its response to recent crises of trust in capitalism, belongs to this long tradition. In the 1980s and 1990s financial markets have been conceived as self-referential systems, the study of which has often been conducted separately from their relationships with labor and labor markets (Knorr Cetina 2007). Social finance represents an opportunity to resist the decoupling between the sphere of production and the financial sphere. While the current iteration of social finance is usually understood in the context of financialized modes of accumulation (Fine 2012), I agree with those who have emphasized the need to further investigate the social and cultural transformation of the bios often conceived as subsumed in the processes of financialization (Langley 2008; Martin 2002). Social finance contributes to studies of financialization by illustrating labor’s ongoing centrality to capitalist dynamics rather than treating it as “collateral damage” within processes of financialization (Adkins 2020; Cooper, 2015; Montgomerie 2020; Thompston and Cushen 2020).

The article is organized in six sections. In the first section, I explore key empirical coordinates of social finance and its modes of operation. In the second section, I argue that social finance emerges from the redeployment, initially in the UK and the US, of the first instances of microfinance implemented in the global South. This redeployment allows social finance to develop and expand in the global North in the 1970s and 1980s. Furthermore, this expansion occurs at the crossroads of three intertwined developments, namely, financialization, the structural changes that shaped labor markets, and the transformation of modes and cultures of governance in Western liberal welfare states. The third section illustrates the saliency of the post-2008 years, both in terms of breaks and continuity with respect to the pre-GFC period, to understanding the exorbitant growth of social finance. In the fourth section, I illustrate the ideological function of social finance in the face of the crisis of trust in the financial system that emerged in the post-2008 period. Section five further develops this theoretical argument, centered on the post-2008 shift of affects toward finance and its institutions. In the last section I discuss the contested future of social finance and the constraints that spaces and actors of resistance and contestation place on its further development.

The Empirical Coordinates of Social Finance

With a complex history that arguably has Islamic roots, social finance has medieval forebearers (Rexhepi 2016). It also has precedents in eighteenth century cooperative and saving banks as well as financial practices associated with the social and environmental movements of the 1970s (Tischer and Remer 2016). The current iteration of social finance is a relatively new arena of international finance that has taken significant strides forward after the GFC and promises to play a central role in the post-pandemic effort to make social development “investible” (Gabor 2021).

In many present instances, social finance is an umbrella term in which the word social refers to the impact of the object of financial investment (Rosenman 2019:142). In this sense, social finance brings together diverse activities consisting of social and ethical investing, social impact bonds, and microfinance, among others. In other instances, social finance includes activities based on the process-related impact of investments (for example, the impact on decent work of employees) (Hilbrich 2021:1). Other definitions refer to the purpose of social finance. Conceived as a set of initiatives and mechanisms to “allocate capital for social as well as economic value creation” (Nicholls, Paton, and Emerson 2015:1), it purports to offer finance and financiers a way to “do good, while doing well” (Fetherston 2014:28). In fact, most agents involved in social finance (individuals, institutional investors, banks, and investment companies) operate with aims that range within a spectrum of social and financial returns (Brandstetter and Lehner 2015).

When defined in terms of impact and purpose, not surprisingly, social finance involves a plurality of actors that sources the finances involved in social finance. Investors such as Deutsche Bank, Goldman Sachs, and the European Investment Fund, mix with corporations such as Google, Netflix, Paypal, and Starbucks, financial institutions such as JPMorgan Chase and Prudential Financial, and not-for-profit foundations such as the Kellogg Foundation (Lamy, Leijonhufvud, and O’Donohoe 2021) in complex private–public social finance institutions operating under the auspices of powerful institutional actors such as the European Union, the Catholic Church, the World Economic Forum, among others (Chiapello and Knoll 2020:8).

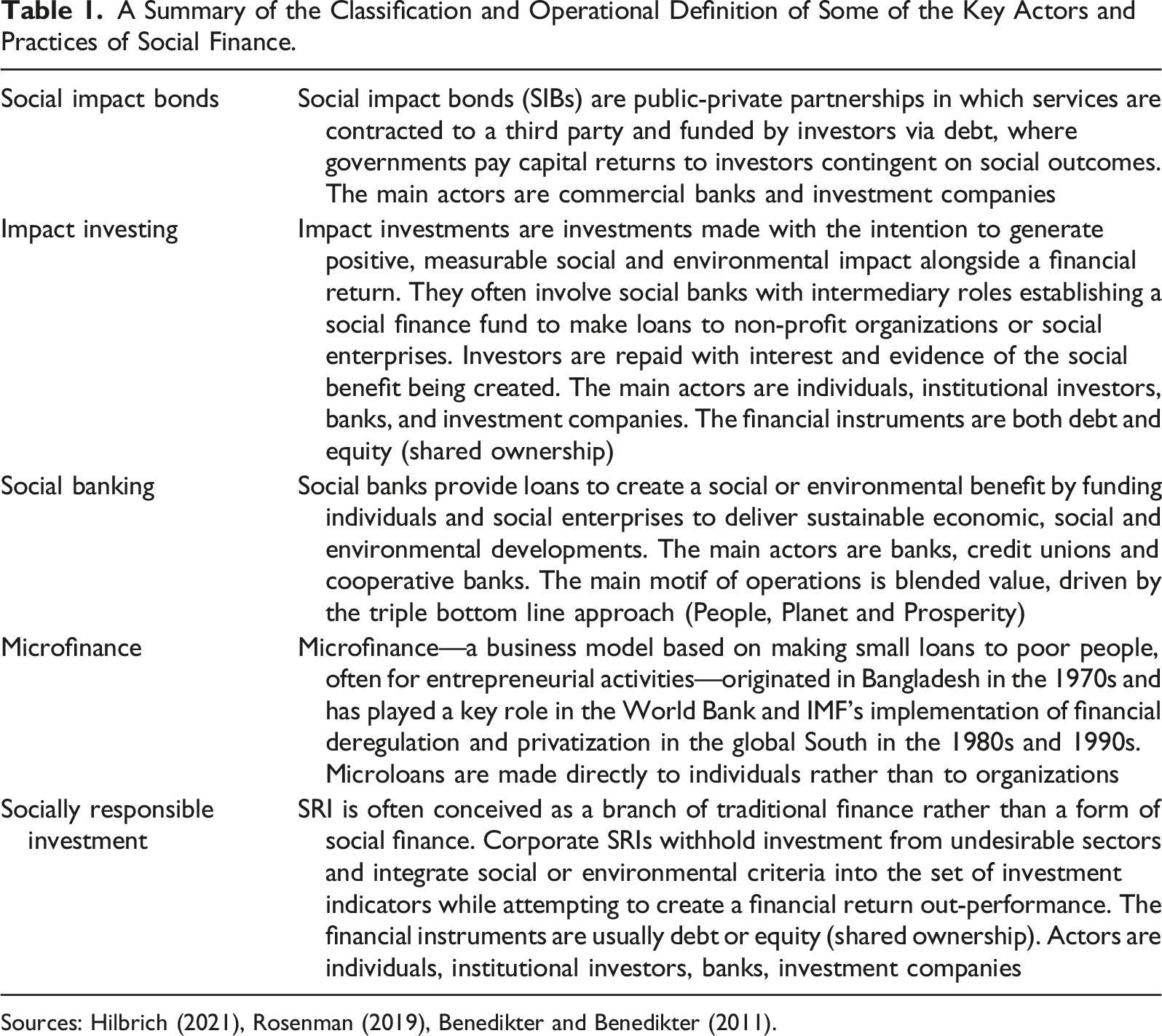

A Summary of the Classification and Operational Definition of Some of the Key Actors and Practices of Social Finance.

Doubtless the question of definition is vexed. Many studies skirt this problem by focusing on one or two different types of social finance, exploring their different contexts of application, and even venturing comparisons. Those interested in the further development of the social finance market often acknowledge that the “opaque conceptual underpinnings” of the term constitute a challenge (Hilbrich 2021:3). My approach is less interested in strict definitions, and adopts an open attitude toward the issue of what might comprise social finance to further explore its anchoring term, namely social, within the context of the deep labor market transformations of the late 1970s and 1980s, and, later, of the GFC. By reaching across different examples, I am interested in locating social finance’s different modalities with respect to processes of subjectification and objectification that shift the very notion of what constitutes the social in social finance. I will argue that labor and the workings of labor markets are central to the emergence and expansion of social finance. Labor, in this regard, is not just the subjective face of work or an objective social force active in the production of value but rather extends to the field of the bios and the inscription of life itself into capitalist regimes of accumulation and valuation. Many social studies of finance have rightly made the point that financial operations bypass labor in the making of value, allowing money to beget money (e.g., Adkins 2018). I suggest that a labor-focused study of social finance enables us to understand something about finance more generally—that is, its dependence on patterns of sociality and social cooperation that are not of its own making.

The modalities of social finance are always relevant to how its dynamics play out. Take the examples of social impact bonds and microfinance. Social impact bonds have mostly been deployed in liberal democracies located in the global North, such as the United Kingdom, the United States, and the Netherlands. They involve public-private partnerships in which governments pay capital returns to investors based on the results of social programs, for instance in family welfare, environmental protection, or incarceration prevention. Microfinance, by contrast, finds its contexts of application primarily in the global South, where, since the 1970s, it has been a favored form of social finance to deal with issues of poverty and uneven development, particularly at the margins of the global financial system (Bernards 2022; Rosenman 2019). It addresses poverty conceived as a by-product of financial exclusion by providing small loans directly to those traditionally excluded from financial markets. Conceptually, the differences among these two modalities of social finance can be specified in terms of the processes of laboring finance and financing labor that provide the theoretical coordinates of my argument.

In both these instances of social finance, labor and finance intertwine and engage with the processes of laboring finance and financing labor in complex ways. This is best illustrated through concrete examples. Begun in 2013, Rotterdam Employment South is a social impact bond that relies on a public–private partnership to facilitate the employment of young unemployed individuals. Laboring finance, in this context, takes the form of enticing private socially conscious investors into buying these bonds. Financing labor consists in channeling these financial resources to fund the delivery of training programs to support unemployed youth. Effectively, the social in this instance is a heterogeneous mix comprising low-income and young unemployed workers but also the care labor of the contractors, and the professional labor of financial managers.

Let’s contrast this social impact bond to Kiva, a microfinance institution located in San Francisco and operating in the US and globally since 2005. Kiva establishes innovative ways to raise funds to finance the living needs of the poor. In this instance, laboring finance involves the collection of funds from private actors through crowdfunding and peer-to-peer lending. These funds are used for financing labor, where labor is not only the work performed by poor-turnedentrepreneurs in micro-enterprises, but also the sustenance of the bios, which in this case encompasses the needs of the living, including housing, education, health services, and access to clean water.

As these examples illustrate, the processes of laboring finance and financing labor take on different forms depending on social context and the kinds of financial instruments used in different settings. I contend that these concepts might be used similarly, or better analogously, to specify the differences among any of the various modalities of social finance listed in Table 1. The contexts, actors, and practices will change, but the gambit of this article is to argue that laboring finance and financing labor name empirical processes that are at stake in social finance’s operations. Beyond this claim, I suggest that these categories provide a kind of conceptual grid within which to understand social finance’s history and origins. This is the work I will initiate in the next section.

Laboring Finance: Entangling Labor Into the Architecture of Finance

Social finance is usually understood to involve the application of financial logic to areas in which they were not previously dominant—for example, welfare and development aid. In this respect, social finance is positioned as part of a wider movement of financialization and the financialization of social protection (Fine 2012). The debate on financialization has been expansive, pointing to features such as new patterns of capital accumulation (Krippner 2005), changing models of corporate governance (Friedman 2007; Lazonick and O’Sullivan 2000), rising household debt (Fernandez and Aalbers 2016), and shifting parameters of income distribution (Pariboni and Tridico 2019; Tomaskovic-Devey and Lin 2011). Importantly, the concept of financialization has been extended beyond the economic sphere and applied to the social and cultural transformation of the bios itself—a financialization of life (Langley 2020a; Martin 2002). However, the extent to which financialization discourses have integrated consideration of labor issues is limited (Adkins 2020; Cooper, 2015; Thompston and Cushen 2020). Rather than conceiving disruptions to the productive and reproductive dimensions of labor as a side-effect of financialized capitalism, I argue that the deep labor market transformations of the late 1970s and 1980s establish the necessary conditions for the emergence of social finance.

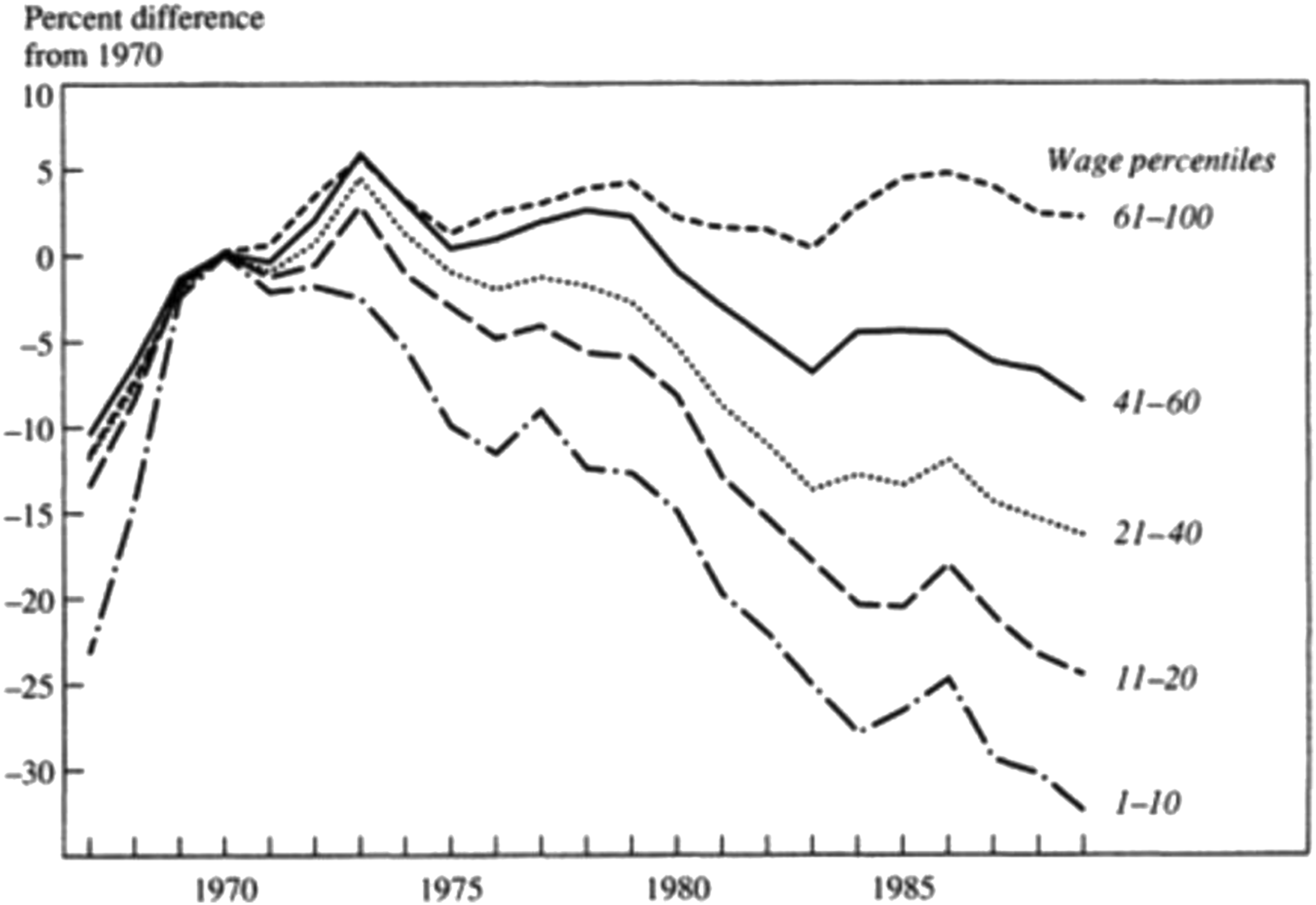

Labor market deregulation in the advanced capitalist economies of USA and Western Europe in the 1970s and 1980s (e.g., Gosling and Lemieux 2001) has offered enormous opportunities for value extractions from labor, primarily through the loss of the social wage, widespread welfare reforms, and the consequent indebtedness of workers. Changes in technology and trade drove down the demand and wages for unskilled workers in the 1980s (Autor, Katz, and Kearney 2006; Machin 2001). Transformations to the international division of labor and deindustrialization processes in most liberal economies in the global North made unskilled workers unnecessary for the running of postindustrial capitalism, leading to a crisis of social reproduction. The wages of common workers were driven down not only relative to the cost of living but also with respect to the social insurance benefits that Western governments were still providing. Declining real wages for the bottom decile of wage recipients as in Figure 1 below marked the rapid growth of the working poor (e.g., Juhn et al. 1991) and equally rapid declining labor force participation rates among poorly educated workers (Krause and Sawhill 2017). Real hourly wages (in logs) relative to 1970 by percentiles of the US Wage Distribution, 1967-1989, reproduced with permission by Juhn et al. 1991.

Wage incentives became the preferred tool to manipulate increasingly conflictual capital-labor relationships and boost workers’ performance. With the exorbitant growth of the average compensation for top executives, the income share of the top one percent of income recipients in both the UK and the US in the late 1970s reached unprecedented levels (Atkinson 2015). Policy responses were grounded in neoliberal governance philosophies that approached inequality as a “natural” by-product of the competition prevailing among agents “construed and constructed as human capital” (Brown 2015:37). In reformed labor markets, “inequality, not equality” became “the medium and relation of competing capital” (p. 38).

With skyrocketing profits directed to shareholders and an increasing gap between wages and labor productivity, governance strategies based on shareholder primacy led the transformation of productive capital into finance capital in the 1980s (Stockhammer 2004). Corporate finance was not the only aspect of finance that was redefining its relationship with labor. As Atkinson (2015) illustrates, this period witnessed a dramatic decline in social insurance in all major OECD countries. With a retreat of the welfare state in all major liberal economies and wages unable to satisfy basic needs such as housing, health, and education, “entrepreneurial forms of citizenship which condition how individuals participate (...) in a financialized economy” (Montgomerie 2020:383). Wage repression fueled household debt, the “wages of the future” to which creditors lay claim in the present (Montgomerie 2009; Ross 2014). Cynamon and Fazzari (2016) document how in the US, starting from 1980, habit persistence and conspicuous consumption drove increased levels of household debt.

In the US, the mortgage industry responded to increasing demand for access to debt by facilitating credit to low-income households. Starting from the mid-1990s but accelerating after 2002, the lobbying activities of the mortgage industry mounted for Congress to pass legislation that led to higher subprime borrowing capacity (Mian, Sufi, and Trebbi 2013). Meanwhile, attitudes toward risk were subject to potent social engineering. Regulatory changes, such as those involving the Employee Retirement Income Security Act (1974), its 1978 amendment, and the Garn-St. Germain Act of 1982 permitted pension funds and insurance companies to invest substantial proportions of their portfolios in corporate equities and other risky securities (e.g., “junk bonds”). In the 1990s, with the shift of pension systems in countries such as the US and the UK from “defined benefit” to “defined contribution,” pensioners, a group previously sheltered from financial manoeuvres, were forced to approach their pensions as financial investments. 1

These trends marked a significant turn in the relationship between production and finance. According to Magdoff and Sweezy (1983), the co-presence of a financial explosion with a counteracting stagnation represented a qualitatively new historical development and posed danger for the economic and social stability of financial capitalism. Conceived as a culturally embedded social relationship within financialized capitalism rather than simply as a financial contract (Montgomerie 2020), debt operated as a “powerful mechanism of the enrolment of labour into the architecture of finance” (Adkins 2020:335).

By 2005, a significant increase in the global supply of savings relative to the desire to invest, a global “savings glut,” had emerged, with its potential to destabilize financial markets, neutralize monetary policies, and undermine the foundation of the world’s major capitalist economies (Bernanke 2005). Addressing the problem at its root would have involved recognizing that savings were driven by a rich minority and the decline in consumption was led by most households becoming poorer (Mah-Hui and Ee 2011). Resetting a crisis prone capitalism would have involved balancing the power between finance and labor and focusing “on the primary social aims, putting the most essential needs of people and the environment before profits, (…) to provide jobs…for the unemployed, food for the hungry, houses for homeless, adequate health care and income security and a decent environment for all of us” (Magdoff and Sweezy 1987:88–90). Instead, by drawing agents of production and reproduction of labor into the power of financial operations broadly conceived (Hyde, Vachon, and Michael 2018), the broad changes in the labor markets of the 1970 and 1980s combined with governments and corporations to make financial subjectivities part of the core of financial accumulation (Langley 2020a), a process that I call laboring finance.

Financing Labor: The Global Financial Crisis and the Growth of Social Finance

Before the recession induced by the SARS-CoV-2 pandemic in 2020, the global financial crisis was the most severe economic crisis since the Great Depression (Gopinath 2020). Globally, during the GFC, hundreds of millions of jobs were lost, which exacerbated the collapse of the US financial sector following the collapse of Lehman Brothers. From 2008 to 2010, US government anti-poverty programs had grown to assist one in six Americans, victims of the GFC. In 2010, close to 10 million received unemployment insurance, more than 40 million were receiving food stamps, more than 4.4 million people were on welfare, and more than 50 million Americans were on Medicaid, the federal-state program aimed principally at the poor. Wolf’s (2010) account of the effect of GFC on public finance is staggering: the financial outlets of Medicaid had jumped 36% in 2 years, the cost of jobless benefits had soared by almost 400%, and the food stamps program has risen by 80%. More than 180 banks in the United States and dozens in Europe were bankrupted between January 2009 and March 2010. The total public debt in leading OECD economics, such as the US and Germany, soared. The overlapping dependence on debt by households, a trend that started long before 2008, and by national governments, central banks and financial institutions, particularly after 2008, marked the call to austerity that underwrote the continued financialization of the economy and society after the GFC.

The central argument developed in this section is that the GFC represents a significant point of discontinuity in the intensity and reach of social discontent with traditional finance and more broadly with modes of accumulation in financialized capitalism. I argue that social finance emerges as a response to what at the societal level financial capitalism had both helped to constitute and imagined itself to resolve. This response was realized by means of financing labor, a social process that converts impoverished and vulnerable workers, the poor, and other marginalized subjects into objects of new financial instruments. In practice, this process of financing labor pairs with the emergence of the financial inclusion movement, which advocates and promotes financial literacy, to fashion an institutional response to systemic distrust by performing a finance that returns society to its master role.

Although, as detailed in Table 1, social finance has precedents in the microfinance initiatives that extended through the global South from the 1970s, public and governmental endorsements supported the expansion of social finance in the few years prior the GFC or immediately after. For instance, in early 2005, the responsible investment industry was firmly established by a joint venture headed by the United Nations and involving twenty of the world’s largest institutional investors to incorporate environmental, social and governance (ESG) issues into investment practices. The responsible investment industry has grown steadily since then, particularly in the post-GFC period, to reach over 5000 signatories in 2022 and over US$121 trillion of assets under management globally.

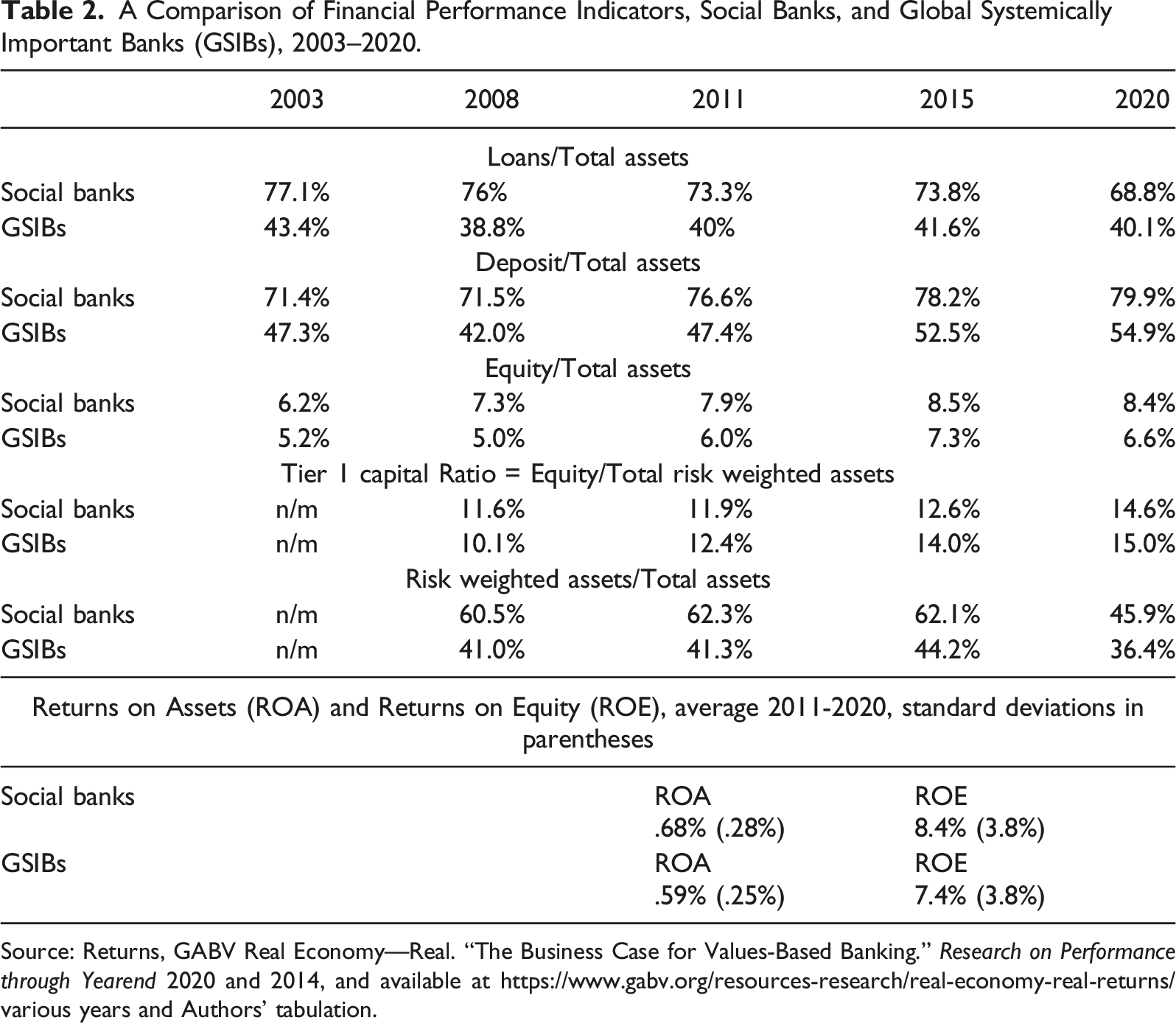

A Comparison of Financial Performance Indicators, Social Banks, and Global Systemically Important Banks (GSIBs), 2003–2020.

Source: Returns, GABV Real Economy—Real. “The Business Case for Values-Based Banking.” Research on Performance through Yearend 2020 and 2014, and available at https://www.gabv.org/resources-research/real-economy-real-returns/various years and Authors’ tabulation.

According to GABV, the higher reliance on deposits by social banks, which Table 2 illustrates, signals their strong commitment to service the real economy. The high share of customers’ deposits in the social banks’ liabilities reduces their risk of illiquidity. Importantly, particularly in the post-GFC period, social banks appear to out-perform traditional banks in terms of returns and thus appear to have provided reliable rewards to investors. Social impact bonds are another modality of social finance that have experience rapid growth, particularly in recent years. According to the Asian Development Bank (ADB 2021:14), the global issuance of social impact bonds rose by 27% from 2017 to 2018, by 44% from 2018 to 2019 and by an extraordinary 720% from 2019 to 2020, a fact that indicates how tightly the success of social finance is linked to humanitarian disasters such as the SARS-CoV-2 pandemic.

In short, in the post-2008 period, the poor economic performance of traditional financial assets was balanced by the solid performance of social finance products. By proposing a way to reimagine social policy in the face of the profound social challenges emerging from the GFC, social finance further extended the boundaries of mainstream finance. Through its applications to welfare, social finance operated by breaking down complex societal issues into depoliticized (fictitious) commodities subjected to measurable metrics to which simple economic principles could be applied for outcome-based solutions (Sinclair, McHugh, and Roy 2021:13). The result was a conversion of social problems into small-scale objects amenable to “technical interventions” (p. 12). With its reframing of welfare policy, away from any attempt to tackle the actual causes of problems and focused instead on win-win solutions to their most obvious manifestations, social finance revealed its true value. It is in the process of financing labor, the unrelenting entanglement of the bios, the wide field of lived social relations and experience that contributes to the making of value, in the sphere of finance that we see social finance’s success. Outside of the narrow sphere of financial markets, social finance was called upon to play a major ideological role.

Social Finance and the Crisis of Trust

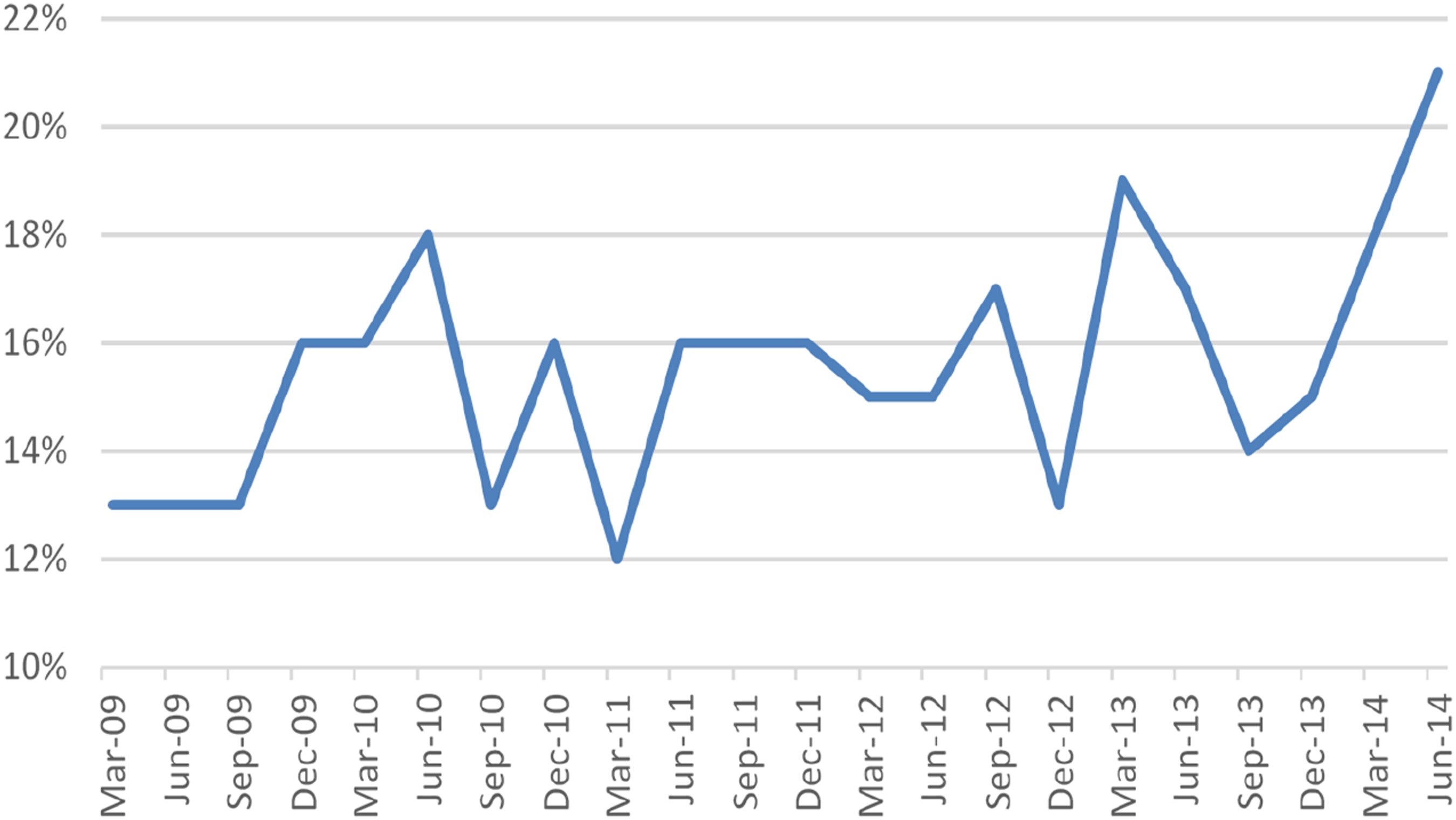

The GFC was a catastrophic collapse in confidence (Reich 2008; Stiglitz 2008). Information extracted from the Financial Trust Index survey in December 2008, just 3 months after the collapse of Lehman Brothers, and in the following years, reveals the extent of the devastation wrought by the crisis on people’s trust in the market economy, banks, and corporations. As represented in Figure 2 below, the percentage of US people trusting the stock markets, at 13% in March 2009, hit a bottom low and fluctuated from 12% to 19% for several years following the GFC before stabilizing in 2014. Percentage of US citizens who trust the stock markets, 2009, 2014.

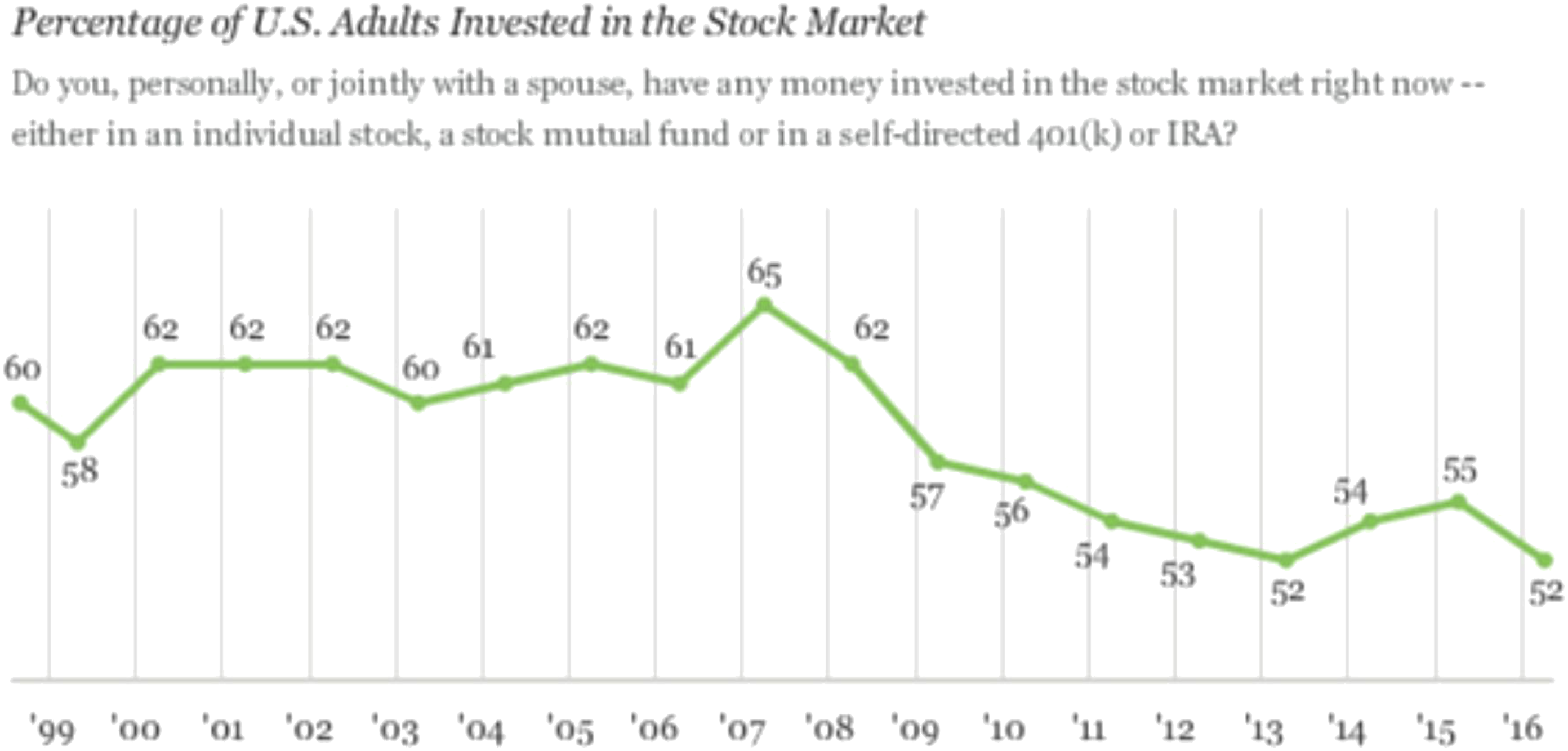

As expected, the post-2008 crush of trust and its slow recovery heavily impacted participation in financial markets (Guiso, Sapienza, and Zingales 2008). For instance, the percentage of Americans reported investing (directly or indirectly) in the stock market declined steadily from 65% in 2007 to 52% in 2013, as Figure 3 illustrates. Percentage of US adults who have invested in the stock market, either individually, through mutual funds or through pension funds, 1999-2016.

As a key to understanding the dynamics of social relationships, trust has occupied a central stage position in sociological investigations (Durkheim 2008; Weber, 2012). Defined as the willingness of an entity (i.e., the trustor) to become vulnerable to another entity (i.e., the trustee), trust may not be fully rational (Schilke, Reimann, and Cook 2021), because people use affect to make decisions about trust using simple, evaluative rules without deliberate rationalization, particularly in situations involving risk. Trust, affect, and shared values and intentions shape social interactions in settings where complex knowledge systems are involved, and where information asymmetries among agents contribute to establishing relationships of power between trustor and trustee. Empirical research on social trust emphasizes the primacy of affect for the success of communication strategies that institutions adopt in the face of crises (Siegrist, Gutscher, and Keller 2007).

Social trust is central to several social processes, including those related to cooperation and economic performance (Fukuyama 1995; Putnam, Leonardi, and Nanetti 1992). Niklas Luhmann understands trust as central to meaning-generating communications among systems in complex societies (Luhmann 1982). For Anthony Giddens (2008), trust has ontological properties, which are evident in its link to “ontological security,” the confidence that most people have in continuity of their identity and in the steadiness of the social and material environments in globalized social settings. Affective approaches to trust resonate with theories of finance that emphasize the tendency of financial markets to function according to the mass behavior of investors (Orléan 1989).

The global wave of protests that followed the GFC focused on anti-austerity and pro-democracy claims, which were aimed toward specific targets, particularly financial systems. These social struggles were framed around the legitimacy of representative democracy and its socioeconomic governance. An important instance is the Occupy Wall Street (OWS) movement of 2011, which multiplied beyond New York to other cities around the globe and linked to freedom movements in the Arab world (Calhoun 2013). In voicing distrust in the social legitimacy of finance, OWS demanded purposeful wealth management and distribution to better the condition of the “99%” and echoed the general discontent with corporate power and banks. In this sense, the movement reacted to the direct material dislocation occasioned by the crisis, including such phenomena as eviction, poverty, and unemployment. However, OWS also forged ways of understanding the crisis in relation to processes of neoliberalization, globalization, and financialization rooted in the capitalist world system (Hardt and Negri 2011). This meant that its expression of distrust extended beyond the immediate material forms of the crisis to give voice to wider concerns regarding subjectivity and society (Appel 2014).

In contrast to OWS, a mainstream narrative emerged about the need to educate financially illiterate participants in the financial markets that had failed them. Economic and sociological approaches to trust converged in acknowledging that some factors, for example, understanding the “rules of the game,” matter for trust to lie alongside the market (Greenspan 2002). Financial education and literacy programs have been usually designed with one of two general approaches, either comprehensive financial literacy campaigns or ad hoc and targeted intervention programs. An early example of financial education campaigns, the comprehensive financial literacy program “There’s a Lot to Learn About Money” was launched by the US Federal Reserve in 2003. More specifically targeting low-income pensioners, the Irish Pension Board, the Irish regulator for occupation pensions, has sponsored annual national pension awareness campaigns since 2004 (Smith 2006).

Although cries for financial literacy had been audible for decades (Lazarus 2020), they were amplified in the wake of the GFC and framed globally as necessary for financial inclusion of people at the bottom quartile of income distribution. Government-sponsored national strategies for financial education, a set of nationally coordinated activities to foster financial literacy in relation to identified national needs and gaps, multiplied in the immediate post-2008 period. By 2012, fifteen countries had already implemented a national strategy (Mundial 2014). For example, the Brazilian national strategy for financial literacy was implemented as a privatepublic partnership in 2010. It targeted high school students before implementing a wider national program, which explicitly aimed to achieve financial market growth, investor inclusion and protection, and broadened use of financial institutions, primarily those involved in home lending and households’ credit. Financial literacy campaigns emerged from the understanding that “the ultimate protection against financial excess was a more sophisticated population of consumers and investors” (Lo 2009). More analytically, they became important instruments for the creation of the financial subject (Langley 2008). Their effectiveness hinged on “changing people’s thought processes, feelings, motivations, and ultimately their values (Willis 2011:432). In this aspect, financial literacy became an important ideological accompaniment to what I call the priming function of social finance—that is, its ability to prepare subjects for market participation.

The Oscillation of Trust in the System

Social finance is premised on the idea that changing preferences for financial participation requires changing people’s emotional responses to money. Social finance encourages market participation through its priming role. The term priming refers to the activation and manipulations of preferences, judgments, and behaviors through the mobilization of mental concepts (Lodder et al. 2019). Following the GFC, the debate on financial literacy and the related policy interventions turned to an interesting question. How can financially illiterate agents trust themselves and the system? Luhmann (1982:75) proposes: “You actually shift forward the threshold of effective distrust.”

Massumi (2015:8) offers an interesting interpretation of this phrase from Luhmann: “you foster distrust as a starting condition … not as the opposite of trust: as its ‘functional equivalent.’” Part of his wider reflections on power as a mode of pre-emption, Massumi has in mind an interlocking or resonance of trust and distrust, such that “the resulting affective state of the individual oscillates between them” (p. 8). At stake is the making of a subject open to inherently risky activities such as financial investing not because they have come to trust the system but because, moving from a base of distrust, they can easily “tip towards the other at the slightest agitation” (p. 8). The concept of oscillation here captures the sense in which the priming of the financial subject, its pre-emption toward market participation, requires an almost imperceptible movement between trust and distrust. Social finance works as a means of rebuilding trust in the financial system not because its modes of directing finance to social ends are distant from finance as traditionally practiced, but rather because they are so close to them, indeed in some cases imperceptibly so.

This is why social finance and financial literacy pose such effective responses to the crisis of distrust that follows the GFC. One does not need to move the subject much, especially when they are already enrolled into financial systems by the processes I have described as laboring finance. Consider the following scenario. A worker is automatically signed up to a defined-contribution pension scheme when they take up employment. They worry when a financial turn runs their benefits down, experiencing mounting distrust in the financial system. Social finance manages this distrust by offering alternative paths of investment, which adhere to the processes I have called financing labor and are seemingly at odds with rapacious market trends that have induced the crisis. When small returns result, the affective line is crossed, distrust modulates into trust, and the subject is ready to invest again, perhaps in more traditional financial products, because, in the meantime, a financial literacy campaign run by the pension fund has explained the benefits of portfolio diversification. The example is somewhat simplified because it involves an individual worker and doesn’t capture how these affects are easily transmitted, but it makes the point. Through a pendulum-like oscillation between trust and distrust at the affective level, and between laboring finance and financing labor at the technical level, social finance produces a “readiness potential” to financial market participation.

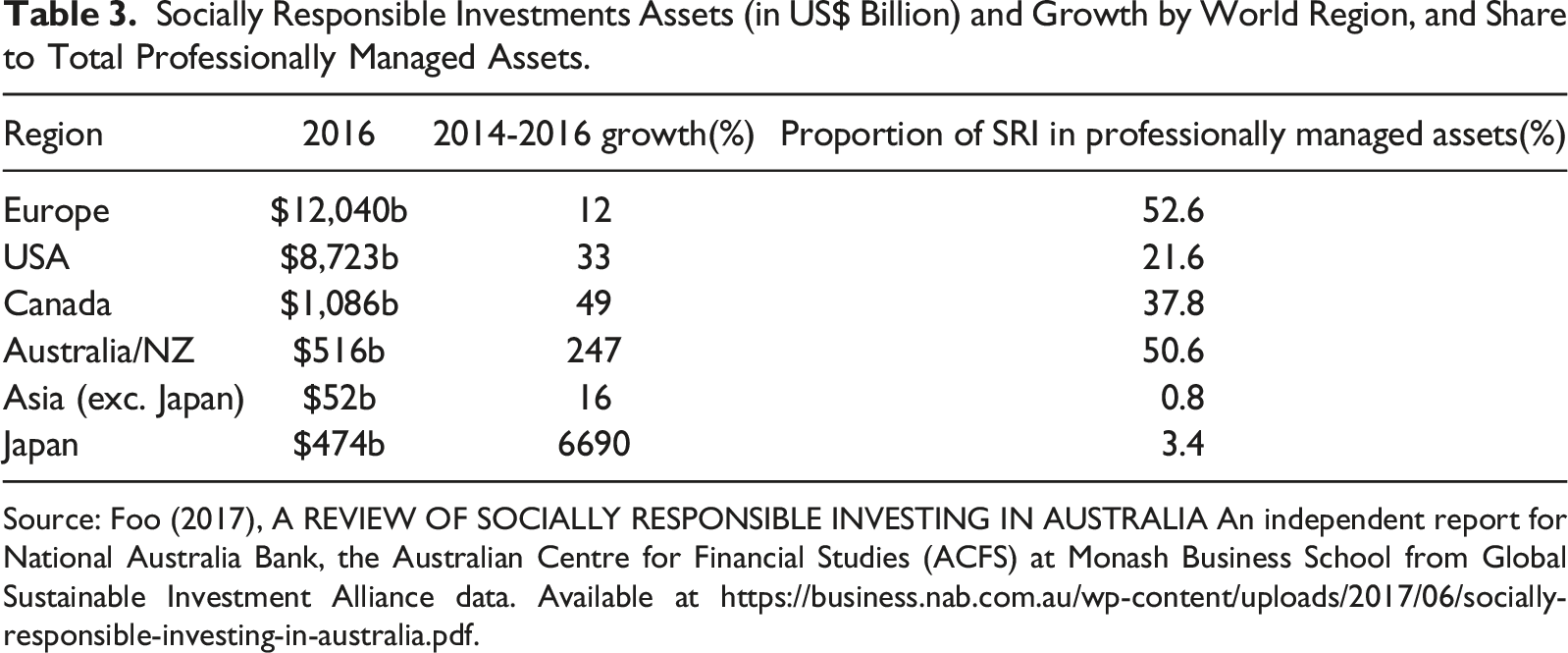

Socially Responsible Investments Assets (in US$ Billion) and Growth by World Region, and Share to Total Professionally Managed Assets.

Source: Foo (2017), A REVIEW OF SOCIALLY RESPONSIBLE INVESTING IN AUSTRALIA An independent report for National Australia Bank, the Australian Centre for Financial Studies (ACFS) at Monash Business School from Global Sustainable Investment Alliance data. Available at https://business.nab.com.au/wp-content/uploads/2017/06/socially-responsible-investing-in-australia.pdf.

The Global Impact Investing Network (GIIN) reports a similarly hyperbolic growth trend for the impact investing market. Its size currently stands at USD 1.164 trillion in assets under management (AUM), of which 63% are with larger institutional investors, who use social finance products to decrease short-term high volatility at the portfolio level (GIIN 2020).

Despite the emphasis of social finance being on social/environmental return rather than monetary value, professionally managed “blended finance” combines the various financial assets in an array of possible financial configurations diversified by degrees of risk, financial and non-financial returns. With its triple bottom line mission encompassing diverse objectives of prosperity, people and planet, social finance promises to continue the process I call laboring finance by flexibly reaching a new generation of investors with their individualized social values in a continuum of possible bundles of risk and commitment to “doing well while doing good.” 2 In the context of blended finance, the emphasis is no longer on the social/environmental value of social finance products, but rather the overall performance of the blended portfolio. Grounded on partnerships with market-based models of economic development and poverty alleviation programs and efficiently integrated into modern financial portfolio diversification strategies (Cooper et al. 2016), social finance’s current trends illustrate that the bios is more and more central to global capital (Bernards 2022; Ono 2016).

Not only has social finance provided legitimacy to financial systems that have rapidly lost their credibility after the GFC. It should now be clear how social finance brings together the two essential elements of hegemonic power, namely coercion and consent. Social finance reshapes the grounds of finance and labor, and the discourses that frame finance and labor, by drawing upon the coercive modeling of markets, government solutions, and the desires and actions of subjects (as subjects willing, albeit unable to participate in those market solutions), to support the primacy of finance. Through the oscillatory movement it establishes between finance and labor (laboring finance - financing labor), social finance establishes the commonality of these grounds. By concealing the coercion of an endogenously created demand for social impact, and by organizing consensus around finance’s ability to fund the needs of the bios, social finance masks an underlying inequality of power between finance and labor. This process, which social finance enacts, grounds the hegemony of finance.

Uncontested Social Finance?

The consensus social finance builds for financing labor, the tackling of the very same social, economic and ecological problems that the primacy of finance has contributed to create, raises the question: is social finance uncontested? And what are the parameters and implications of this contestation? Rather than conceiving social finance as an implacable force somehow unconstrained or “too big to fail,” a critical investigation of the interface between finance and labor opens the door to further interrogation of areas of inconsistencies, contestation or resistance to social finance. For instance, the “hybridity” of social finance (Langley 2020b), its blurred boundaries to traditional finance, potentially magnifies the risk of a multiplication of false or exaggerated claims about the impact of social finance on the social and environmental problems it claims to address. GABV Senior Manager, Adriana Kocornik-Mina (2023), in the face of risk of extinctions of humanity, whether caused by climate change or by the next pandemic, cries “what about (social finance’s) credibility, integrity and transparency? What about actual progress?” The risk of “social washing” potentially undermines social finance’s role in pivoting the pendulum of trust/distrust in capitalism and threatens social finance’s capacity of laboring finance. Furthermore, the individualization of the social issues that social finance addresses, their reshaping as technical in nature and the selection that social finance carries out away from the complex social problems that would require more radical transformational action, will further define its impact and potentially reform the contours of the process of financing labor. Finally, the fierce protests against microfinance carried out by Sri Lankan women collectives in March 2021 and by farmers in Kathmandu in March 2023 illustrate the contestation of social finance’s ways of seeing and addressing social issues by the very financial subjects social finance assumes as its objects. These protests contribute to expose the resistance to social finance’s legitimizing ideological function in the context of exploitative conditions of production and social reproduction faced by the indebted.

To further critical investigation of labor’s centrality to financialized modes of capitalist accumulation, this article offers a theoretical reflection that rejects the distinction between finance and labor as separate forms of profit extractions, and privileges considerations of finance and labor’s mutual interdependence (laboring finance - financing labor). Fruitful future research will need to further investigate the relationship between finance and labor that emerges from the material instances of operation of differentiated systems of communications, such as global health and the global financial system, in the face of contingent events such as the SARS-CoV-2 pandemic, which, like the GFC in 2008, has disrupted the livelihoods of billions, cost trillions of dollars, and has contributed to elevate social finance to the center of the public health policies in many parts of the world. One area where systemic clashes between finance and labor may intensify are in social entrepreneurial ventures where “the labor of exploiting and the exploited labor both appear identical as labor” (Marx 1981:382–383).

Footnotes

Acknowledgments

I thank all participants at the Crossroads in Cultural Studies Conference, Sydney, the Sociology Colloquia, Macquarie University, Sydney, the EMES-Polanyi International Seminar in Copenhagen, the World Association for Political Economy conference, and the Cambridge Journal of Economics conference for their comments to previous versions of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Australian Research Council (ARC DP160101914) is gratefully acknowledged.