Abstract

We analyze Donald J. Trump’s Twitter activity over the last months of the 2016 presidential campaign, his period as President Elect, and his Presidential term until Fall 2019, shortly before the outbreak of the pandemic. Trump weaponized social networks as a communication tool to build influence on the financial market and the public opinion. We relate Trump’s communication on Twitter to the dynamics of the NASDAQ100 trend over the whole period of study as well as two subperiods, pre-presidential versus presidential. We find that Trump’s hyperactivity on Twitter is followed by a negative market trend, and that tweets covering politically, and economically sensitive topics seem to negatively impact the market, except for real economy-related tweets. Some topics positively received by the market in the pre-presidential phase (e.g., China) become anticipators of negative trading days during the presidential one. We also consider the emotional tone of Trump’s tweets and find an unexpected reversal of the communicative valence of the tweets as to their expected impact on the stock market. Positive sentiment tweets seem to be followed by negative market performance and, maybe more surprisingly, vice versa. It seems that, during the period of observation, the market has learnt to interpret the emotional tone of Trump’s tweets as instrumental to Trump’s political strategy. In particular, the market seems to have realized that negative sentiment in Trump’s communication was entirely functional to political consensus building and not meant to convey market-relevant information. This is at odds with the idea that presidential communication should reflect the public interest, and especially so when it has major implications for the economy. Trump’s use of social media during both his presidential campaign and term questions the principle that institutional responsibility in the digital realm implies treating the infosphere as a commons. We discuss the implications for the functioning of the stock market and the emerging public interest ethical issues related to the breakdown of such principle.

Introduction

In his influential book on narrative economics, Shiller (2019) argues that economic behaviors, and especially stock market behaviors, are influenced by “contagious popular stories that spread through word of mouth, the news media, and social media” (p. 3). The success and viral diffusion of narratives, in Shiller’s view, depends on repetition of content (Irvin, 2019) and on attachment, that is, on the reference to people’s core values and social orientations (Sacco et al., 2021). Despite that word-of-mouth diffusion of information and stories is as old as humankind, and despite the news media’s key role in the construction of today’s knowledge society, it is undeniable that social media have provided the ideal platform for an unprecedented escalation of narratives as a driver of rapid socio-economic change (van Dijck, 2013). They seem to be ideally designed to exploit at best the two principles highlighted by Shiller: an endless repetition and reverberation of contents that “go viral” (Pressgrove et al., 2018), and a tendency to polarize users in terms of their values and social orientations (Bail et al., 2018).

Viralization is fueled by the emotional arousal and valence of content (Berger & Milkman, 2012; Botha & Reyneke, 2013). What elicits a visceral emotional response is more likely to spread and capture attention (Brady et al., 2017). Negative and positive affect may both be powerful drivers of diffusion, although for different reasons (E. L. Cohen, 2014).

As anticipated, stock markets are a particularly fertile terrain, where irrational exuberance phenomena have been observed long before the advent of social media (Shiller, 2016). Social media content has amplified such phenomena even more (Piñeiro-Chousa et al., 2017). The socio-cognitive effects of social media are often counter-intuitive (Van Erkel & Van Aelst, 2021). Moreover, social media sentiment also tends to spill over to mass media, doubling down on their influence upon financial markets (Ren et al., 2021). Regulating social media communication with major business implications is therefore becoming an urgent issue (Karppi & Crawford, 2016). Social media-savvy billionaires such as Elon Musk heavily influence stock and cryptocurrency markets. Their sophisticated communication strategies skillfully play with content tone and sentiment (Huynh, 2022; Strauss & Smith, 2019) while being often presented as impulsive, un-filtered emotional outbursts. The case of the (in)famous Twitter poll asking users whether he should sell 10% of his Tesla shares (Krisher, 2021) is a clear example. The issue is even bigger for institutional public figures, such as the President of the United States (Brans & Scholtens, 2020). Here, a major ethical issue arises: should public figures with a key institutional role be bound by criteria of protection of public interest in their use of social media?

Among social media platforms, Twitter is especially important for stock markets, due to its design features: instant interaction via brief messages where single word choice makes a big difference in terms of content meaning and impact (Dann, 2010). This makes Twitter especially suited for timely communication, for example, during disasters calling for rapid, targeted messaging to improve effectiveness of response (Martínez-Rojas et al., 2018), as a tool for rapid-response corporate publics cultivation in the context of a global crisis (Huang et al., 2022) or for countering reactance during crisis communication (Xu & Wu, 2020). Likewise, it fits well with the high-frequency, complex interactions of market trading (Sprenger et al., 2014). Twitter is also a data mining source for financial prediction, which is mainly based on the extraction of wisdom-of-crowds sentiment for expectations formation, driven by the distillation of emotionally charged communication (Sul et al., 2017) and by uncommon spikes of online debate concerning specific stocks (Tafti et al., 2016).

Another field where Twitter has become the default social media and where content is heavily laden emotionally is political communication. The speed and immediacy of tweets caters to a public perception of frankness and authenticity that is especially functional to the populist discourse (Casero-Ripollés et al., 2017). Even politicians’ online blunders may win appreciation by the public (Lee et al., 2020), reinforcing the political value of visceral reaction and emotionally charged online content.

An unprecedented confluence between Twitter-based political and stock market-targeted communication is found in the Twitter activity of Donald J. Trump (Stolee & Caton, 2018). Trump’s use of Twitter has overturned the social media institutional etiquette, including that of former USA Presidents, in favor of “simple, impulsive, and uncivil” discourse (Ott, 2017). Trump’s Twitter feed has become a primary source of key pronouncements on political (Kreis, 2017), foreign (Boucher & Thies, 2019), and economic (Tillmann, 2020) policy issues, with relevant implications for stock markets (Cervantes & Rambaud, 2020). Such online activity mostly consisted of an apparently un-filtered, impulsive response to news and events by the President himself, bypassing the advice of communication experts and political staff (Surowiec & Miles, 2021).

There have been already many studies on the impact of Trump’s Twitter activity on stock markets, which we will review below. However, a less researched issue has been how Trump’s emotional communication has influenced the social dynamics of stock market sentiment. The emotional arousal and valence of messages plays a crucial role in the informational and behavioral implications of the related narratives (Nummenmaa et al., 2014). Trump’s communication is set to embed all its social media output within a powerful, polarizing narrative (Mollan & Geesin, 2020) which, as argued by Shiller, is another element that amplifies its social impact. The effects of Trump’s Twitter activity on stock market sentiment are a key benchmark to study the relationship between new forms of populist political communication and stock market dynamics. Many other political leaders have taken Trump’s communication strategy and style as a model (Cornut et al., 2022).

We have studied the relationship between Trump’s Twitter activity and the trend followed by the NASDAQ100 US market index between September 2016 and October 2019. Our choice to consider all the tweets in the selected time range and to categorize them according to their emotional content has led us to record and analyze the market dynamics in the first market day in which traders could exploit the information contained in the tweet. Although our analysis does not allow to establish a direct causal link between Trump’s tweets and financial market reactions, it nevertheless provides a first basis to discuss the ethical implications of social media communication by major public figures. We consider, therefore, all of Trump’s tweets during this period (more than 3,000), categorizing them in terms of their emotional content (positive, negative, or neutral sentiment), and the stock market dynamics in the first market day in which the information carried by any given tweet was available to traders.

Our results seem to suggest that Trump’s tweets tend to be associated to a prevalence of negative sentiment in the market. We find that the more Trump tweeted during a given day, the more negative the subsequent stock market performance. Secondly, we classify Trump’s tweets according to their topic to verify a possible correspondence between the subject of the tweets and the stock index trend in the short-term. We find that certain topics appear to be associated with a relatively stable influence on the stock market, whereas others are only relevant in certain periods, following the evolution of Trump’s political agenda as perceived by the public opinion. Finally, we find that the market seems anti-correlated to the emotional valence of Trump’s tweets. Positive sentiment ones are linked to a negative effect on the stock market, whereas negative sentiment ones to a (much weaker) increase. The size of the negative effect associated to the positive sentiment tweets is about four times bigger than that of the positive effect associated to the negative sentiment tweets. Such paradoxical effect emerges after Trump is sworn in and solidifies along his term. This suggests that the markets do not interpret the valence of the emotional content as a reliable signal, and especially they tend to associate some concern to positive sentiment messages as if they were anticipating future instability. Conversely, negative sentiment messages are interpreted as more reliable and bring about some modest positive effect on the market dynamics.

The general picture seems to suggest that the market has gradually learnt to regard Trump’s messages as a source of uncertainty, and to consider oscillations in the associated sentiment as potentially threatening, taking negative sentiment as the default mode. The size of the effects is however relatively small, which also seems to suggest that the market essentially immunizes itself against the informational shocks related to Trump’s social media activity, apart from a small number of very sensitive topics. Despite that this is a preliminary result related to a specific case study, it will be interesting to check more generally whether permanent exposure to emotionally laden communication by populist political leaders causes stock markets to progressively desensitize themselves with respect to the information content of such communication and learn to filter only the most relevant bits of communication related to critical topics. Such an effect seems to resonate with the emotional desensitization bias which tends to emerge as a consequence of excessive experience in emotional perspective taking (Campbell et al., 2014).

Despite that a causal influence in the strict sense cannot be determined, these results point out that the social media activity of prominent institutional figures poses as-yet not fully recognized ethical issues, best framed in terms of the infosphere as a commons. Although such social media activity cannot be thoroughly regulated, the emergence of compelling social norms that limit its use in the public interest seems to be necessary.

The remainder of the paper is organized as follows. Section 2 presents a literature review and introduces the main hypotheses of our study. Section 3 presents the data. Section 4 presents our results. Section 5 discusses the ethical implications. Section 6 concludes.

Literature Review

To analyze the relationship between social media communication and financial markets, we need to consider at least four strands of research:

The theory of market efficiency and the relationship between information and noise;

The relevance of heuristics and some related biases;

The role of mainstream media in information diffusion, and their ability to impact or relate with the financial world;

Social networks and financial markets with a special focus on Twitter.

Irrational exuberance of the stock market represents a clear departure from the efficient market hypothesis (Malkiel & Fama, 1970), both in terms of rationality of the economic agents as commonly defined, and of the treatment and correct interpretation of the potentially relevant information. Information is the basis for efficiency, and the separation of information from noise has been debated for decades (Kahneman & Tversky, 1984), linking noise trading to forms of bounded rationality or to specific biases (Barber et al., 2009). Whether efficiency and bounded rationality in the financial markets may be compatible remains an open question (Mousavi & Gigerenzer, 2017). Biases provide important insights into the impact of media on financial choices. For instance, the psychological necessity of a comfort zone in filtering information while building a portfolio of assets translates into a preference for a domestic portfolio of securities offered in the native language (Grinblatt & Keloharju, 2001), as investors are more able to capture the emotional nuances of their mother tongue than second language speakers (Caldwell-Harris, 2015).

It would be improper, though, to conclude that sensitivity toward emotional nuances such as those that can only be captured by one’s own mother tongue is evidence of irrationality. The widely held view that emotional response is an impulsive, un-reflexive reaction to be controlled by rational deliberation is increasingly questioned (Lindquist et al., 2012). Such response may instead be a resource with distinctive cognitive value to navigate, and to give meaning to, complex social phenomena (Hoemann et al., 2019). Some studies emphasize the role of emotional attitudes such as pessimism as a driver of savings behavior and stock market participation (Grevenbrock, 2020) and of optimism as predictor of the share of wealth held in stocks (Angelini & Cavapozzi, 2017).

As observed above, all the media play a relevant role in the dissemination of financially relevant information, and the separation of information from noise is a long-standing problem (Engelberg & Parsons, 2011). Markets can react to news even when unrelated to actual, genuine information (Fang & Peress, 2009) and momentary salience tends to prevail upon later fact-checking (Birz, 2017). As Tetlock (2007) shows, the emotional content of news matters for markets, that react to pessimism with bearish price drops to later revert to fundamentals, whereas unusually high or low pessimism predicts high market trading volume. Language is key in the construction of emotion concepts (Lindquist & Gendron, 2013), and but investors are sensitive to language mood (Whitehouse et al., 2018) as a powerful tool to spread fundamentals-related information that can be appreciated only through mastery of expressive nuances (Tetlock et al., 2008).

An effect of media coverage upon trading decisions and not vice versa is found by Engelberg and Parsons (2011) and Tetlock (2007). The opinion that media coverage causes market anomalies, preventing convergence of opinion while providing information on market fundamentals (Fang and Peress (2009) is corroborated by other studies. They show for instance that an increase in capital flows to a fund and a spillover effect upon other funds of the same company is favored by its mention in the Category King section of the Wall Street Journal (Kaniel and Parham (2017). As a rule, choice of communication strategies for conveying given content has an impact on market choices even in contexts where such communication is intentionally as neutral and un-emotionally charged as possible, such as in the case of analyst reports (Klimczak & Dynel, 2018). This confirms the difficulty in filtering signals from noise in financial markets.

The advent of social media amplifies these aspects: back in 2013, Ritholz (2013) in the Washington Post warned that Twitter was becoming the premier source of investment news, with the aggravation that the high decentralization and the style of communication do not favor the distinction of information from noise. Nevertheless, a relevant effect in terms of traded volume and price is attributable to the information posted by critical stakeholders, such as trade unions and consumer associations (Gomez-Carrasco & Michelon, 2017). Social media, then, may also function as an effective channel to report financial results (Meyer Alexander & Gentry, 2014) that influence financial decisions.

Another covered topic (Bollen et al., 2011) is the emotional tone of online communication, emphasizing how only calm, low-arousal messages, can predict changes in the Dow Jones with a lag of 3 to 4 days, although a causal relationship cannot be established. Such studies make a case for including public mood measures in financial analysis forecasts to improve prediction accuracy. The intuition that sentiment dynamics matters in understanding Dow Jones performance and returns of the financial markets informs other studies. Zhang et al. (2011) find a correlation between emotional outbursts in Twitter posts and next-day Dow Jones performance. The mood of sentiment dynamics significantly impacts the returns of major financial market indices (Yang et al., 2015) showing its salience in the small-world financial community. The role of bias in an opportunistic use of Twitter financial reporting to profit from the hype effect emerges from a few studies such as Xiong et al. (2019). A positive impact on US tech stock prices from positively toned tweets and vice versa with negatively toned ones has also been found (Teti et al., 2019). However, the sentiment cue mostly works for short-term decisions as a way to capture information that is not transmitted by prices, but its relevance quickly fades. But still, only the sentiment associated to key influencers shows predictive power on market performance while an excessive volume of economy-themed content can be read as a signal of uncertainty on the future that depresses the market, encouraging disinvestment (Reed, 2016).

These streams of research create a useful context for the specific study of the relationship between Trump’s online activity and stock markets. Here, the evidence escapes simple interpretation. If Trump’s online lack of appreciation for a company may cause a depreciation of the company’s stocks, appreciative tweets are not followed by an appreciation of the stock (Brans & Scholtens, 2020). Moreover, only unexpected pieces of news mentioned in Trump’s tweets have impact on the market (Ge et al., 2018). This suggests that Trump’s online comments of already known aspects are not deemed relevant.

A typically negative impact of Trump’s tweets on stock markets, associated with an increase in uncertainty and trading volume, is found by Gjerstad et al. (2021). Details also matter. Choice of topic, sentiment, and political context influence Trump’s impact on markets. The announcement of the trade war with China depresses the market and impacts the price of gold (Gjerstad et al., 2021). According to Benton and Philips (2020) the tweets associated with an increase in volatility are the most emotionally charged posted after the Republican Party nomination, as well as those in the period between his electoral success and the inauguration day. This suggests that Donald Trump’s relevance is unrelated to content but related to contextual political factors and emotional tone. Russia is a sensitive issue, and the ruble depreciates in the short term due to messages with a negative emotional tone, while nothing happens if the tweets concern possible sanctions (Afanasyev et al., 2021). Deciphering the effects of Trump’s online activity on stock markets is not just of interest to researchers. After the enigmatic “Covfefe” tweet, in September 2019, J.P. Morgan created a new index significantly named “Volfefe” that quantified the effect of Trump’s Twitter activity on treasuries, and which seems to account for a large part of the USA bond’s volatility.

Volfefe data and updates are for J.P. Morgan’s internal use. However, Klaus and Koser (2021) show that the Index is quite effective in predicting concurrent European stock market returns. The negative market reaction to Trump’s activity is confirmed by Liu (2019): when Trump posts more, the S&P 500 and the Dow Jones show negative trends.

This brief review of some of the most relevant contributions suggests that Trump’s Twitter activity has an impact on the financial markets, which tend to perceive Trump more as a source of uncertainty driven by emotional volatility and contextual factors than as a source of information. This brings about in turn a generally negative impact on the stock markets dynamics. Such findings from the literature lead us to formulate some research questions related to Trump’s Twitter activity and to the relevance of the emotional tone of his tweets.

To this purpose, we analyze the link between Trump’s tweets and the subsequent performance of the US financial market, on a relatively long time span, ranging from a couple months before the 2016 election day, to the period immediately before the start of the global pandemic (Fall 2019). Such period essentially spans Trump’s presidential cycle until the occurrence of a major structural shock such as the COVID-19 crisis, where the focus of communication suddenly changes, calling for a specific analysis. We then cover the following: the last phase of the electoral campaign, the Election Day and its immediate aftermath, the Inauguration Day and most of Trump’s term of Presidency. Moreover, we study the relationship between Trump’s tweets and the whole US stock market, as proxied by the NASDAQ100, including companies from various industries but not financial ones, like commercial and investment banks. Also in this sense, our study takes a broader perspective with respect to previous work.

The first research question we want to test is whether, as already found by Liu (2019), Trump’s tweets could be perceived by the market as a source of intrinsic uncertainty also in a large time window and for the whole US market:

R1: Is a relatively high number of Trump’s tweets in a given day followed by a negative performance of the NASDAQ100 the next trading day?

A second important question is whether, independently of the emotional mood, there are specific topics which resonate particularly with the stock market when they are covered by Trump’s tweets. With respect to previous studies covering this aspect, we consider a longer time span and a very representative stock market not analyzed so far, as well as a relatively wide spectrum of topics. Does topic content make any difference in Trump’s tweets as far as the stock market is concerned? Even if Trump is not recognized as a reliable source of information, it remains undisputable that his discretionary power may have a considerable impact on many issues of primary relevance for stock markets. His tweets could then be considered a potentially reliable source of information about his own future moves. Therefore:

R2: Are Trump’s tweets differently received by the stock market depending on their topic? Is there is a group of sensitive topics that has a particularly tight link with the market when covered in Trump’s tweets?

Finally, we consider the relationship between the emotional content of Trump’s tweets and the short-term market trend. As Trump is not perceived as a reliable source of information and has a reputation of an emotionally unstable public figure, we can conjecture that the emotional tone of his messages will be read as information about the evolution of his own mood states. It would be intuitive to speculate that a positive emotional tone is associated to positive market performance and accordingly for negative emotional tone. However, if the emotional tone of Trump’s messages is mostly a predictor of his own future mood states, and in view of the fact that his rhetorical political strategy is strongly centered on negativity (Ross & Caldwell, 2020), one may expect that messages with a positive tone pave the way to future messages with a negative tone. By the same token, messages with a negative tone will likely bring more negative ones. That is, positive sentiment in Trump’s tweets can be considered as a signal of instability and uncertainty more than negative sentiment, which is on the contrary a signal of relative expected stability:

R3: Is the emotional tone of Trump’s tweets readable in different ways by the stock market according to whether it is positive or negative? May the uncertainty associated to Trump’s tweets cause positive sentiment tweets to be read as signals of future negative sentiment and thus cause negative short-term market performance? In contrast, might negative sentiment be read as an implicit signal of (mood) stability and linked with relatively positive short-term market performance?

Notice how the paradoxical character of R3 strictly depends on Trump’s peculiar communication style on Twitter and on the underlying political strategy. However, such peculiarity does not entail an excessive limitation of the interest of our analysis, as Trump’s communication style is now being increasingly adopted by populist political leaders across the world. If R3 is corroborated, it means that Trump’s Twitter activity can be considered as an endogenous source of noise rather than as a source of information. On the other hand, the sensitivity of the stock market to the emotional content of Trump’s tweets is not necessarily evidence of irrational exuberance. It might rather reflect a well-motivated attribution of salience to a signal which has an objective information value in signaling possible future choices and behaviors of the nation’s main executive authority. This awareness of the peculiarity of Trump’s communication strategy on Twitter, and of style of government more generally, should become clearer the longer Trump stays in office. So we expect that the evidence for R3 is especially robust as we get close to the end of the period of observation, and specifically after Trump is sworn in as President.

Data

In this section we introduce the data used for our analysis.

Sample

We created two different datasets: one for Trump’s tweets and the other for NASDAQ100 data. Our collection period ranges from September 6th, 2016, to October 25th, 2019. It spans the last 2 months of the Presidential Election campaign in 2016, Trump’s period as President Elect (November 9, 2016–January 19, 2017), and his presidential term from inauguration to the beginning of the pandemic. We have chosen to leave out the pandemic period where new uncertainty and volatility factors come into play, likely causing a major structural shock.

Tweets Dataset

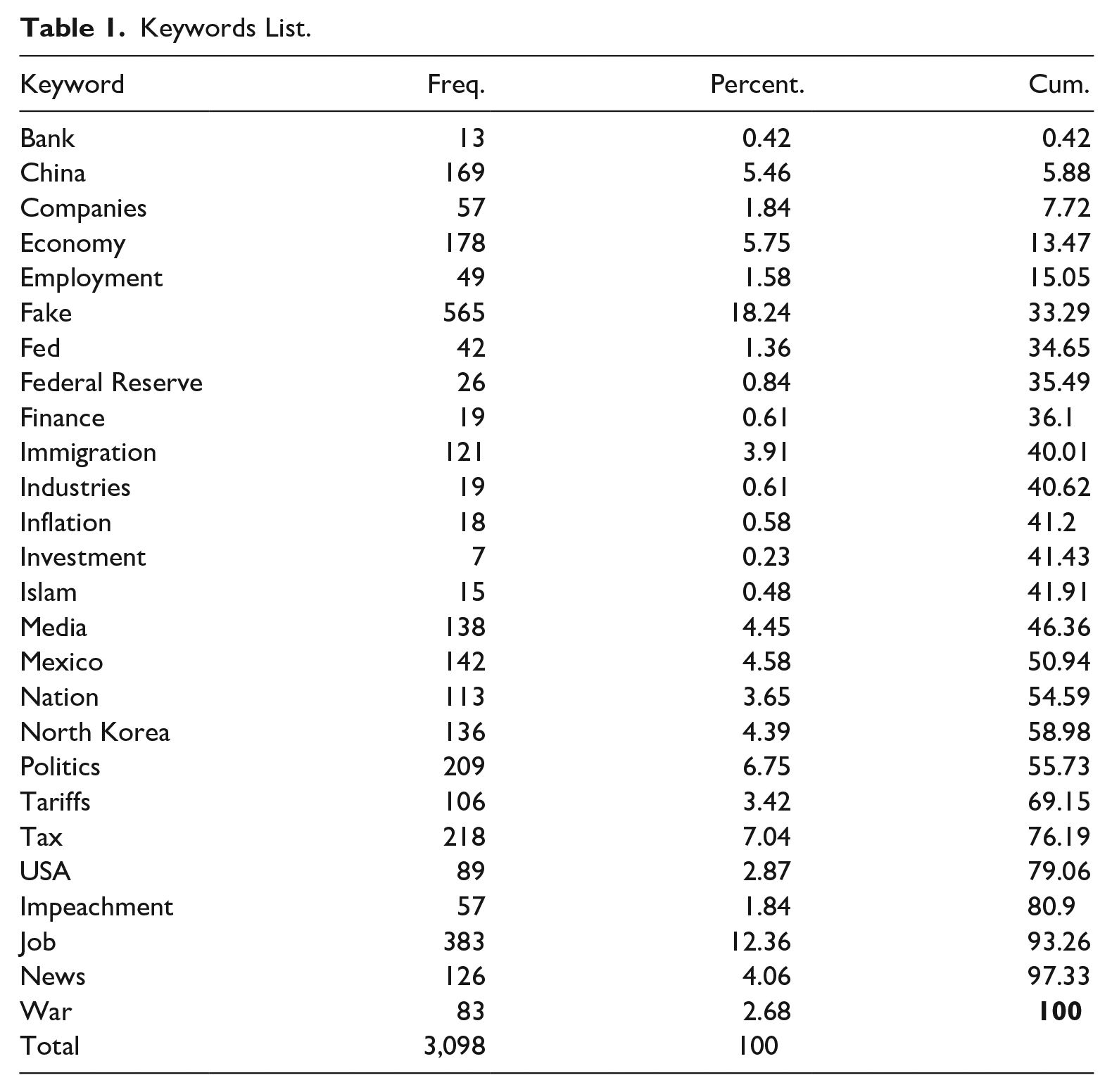

To create the first dataset, we collected Donald Trump’s tweets as stored in the website http://www.trumptwitterarchive.com. We collected the text of every tweet, day and time of publication, and number of likes received, excluding retweets. We then proceeded to classify each tweet in terms of topic and sentiment. As to topics, we have built a list of keywords that reflects two criteria: politically salient issues with significant potential stock market impacts, and/or recurrent issues in Trump’s rhetoric. We have some very frequently touched topics, and less frequent but highly salient ones for the stock market such as finance, investment, and inflation. The list of keywords we use is reported in Table 1. We parsed each tweet to determine whether they would cover a topic in our list and selected only those that matched one of our keywords, for a total of 3,098 tweets over the period of observation.

Keywords List.

We then proceeded to parse the selected tweets according to their sentiment, following Ajjoub et al. (2021), who built a lexicon of characteristic terms in Trump’s tweets that typically determine their sentiment. The formulaic linguistic patterns in Trump’s communication style (Dunning, 2018) create an unusually strong association between use of certain words and the general emotional tone of the tweet.

By checking for characteristic Trump emotional word markers, we assigned an emotional tone to each message. When a tweet contains one of the negative-sentiment words, we labeled it as NEG. When it contains one of the positive-sentiment words, we labeled it as POS. In case the post does not include neither kind of words, we considered the sentiment to be neutral and label it as NEUTR. Sometimes, the post contains both positive and negative words: this happens in 511 tweets from our selection. In this case, we manually parsed each of the ambiguous tweets to assign them a sentiment based on personal judgment.

Another important aspect for the sake of our analysis is the timing of the tweets: it makes a difference whether they are posted while the stock exchange is open or in the off hours. Trump has a habit of posting comments late in the afternoon or at night, and then typically after the closure of the Stock Exchange, or early in the morning, before the Stock Exchange opens. For our purposes, the possible impact of the tweet on the stock market has to be assessed with reference to the next trading day. The impact day is therefore the date used to match daily stock prices and tweets. Obviously, when Trump tweets while the market is open, the resulting impact day is the current one. When the tweets are posted after 4 p.m. of the working day, we identify the market impact day as the next one (publication day + 1). If the tweets are posted on Saturday or Sunday, the impact day is next Monday (publication day + 2 or publication day + 1, according to cases).

The resulting dataset has a structure that is easily exemplified by a random couple of (partial) records, as reported below.

To track the potential impact of choice of topic in Trump’s tweets, we add a variable for each listed keyword, whose daily value is the count of the number of daily tweets which include the given keyword. For example, on 14/05/2019, Trump posted seven messages with “China” as a keyword; hence, the variable “China” has a value 7 on 14/05/2019, and so on. To track the amount of emotionally positive and negative tweets per day, we add three more variables: POS, NEG, NEUTR, which count the daily number of positive, negative, or neutral tweets, respectively. We also include one last variable: TOT_TWEET, which counts the total number of tweets posted on a given day.

We thus obtain the final form of our dataset, which includes the tweets’ text, day and time of posting, number of likes, emotional tone, and impact day. A partial representation of a couple of random records is provided below for convenience.

Nasdaq Dataset

As anticipated, we have chosen NASDAQ100 as our target stock market index, in view of its diversification and representativeness of the economy as a whole, as it includes the 100 largest domestic and international non-financial companies listed on the NASDAQ Stock Market by capitalization. Our dataset includes the following prices: open, close, adjusted close, high, low. Besides, we added the traded volume per day. We gathered the same information not only for the NASDAQ100 index, but also for each of its companies, to test the link between Trump’s communication and specific companies. Moreover, we classified each company by industry, according to the Bureau Van Dijk classification system, to assess whether the effect changes from one industry to another.

An analysis of the most volatile periods that characterize the NASDAQ100 in our time window is necessary to choose the best control variables for our study: micro and macro events that occurred in the period of observation affect our choice, as explained below.

We moreover included additional variables to capture the volatility of both the index and the stock prices: overnight, during the day, over the weekend, to mention the most relevant ones. Table 2 presents the complete list of the variables that we considered in our expanded NASDAQ100 dataset.

List of Stock Market Variables.

We then collected all the data needed to fill the above table for NASDAQ100, for each company included in the index, and each control variable.

Analysis and Results

To test our hypotheses, we choose the multiple linear regression model, with ordinary least squares (OLS):

which requires a careful choice of control variables to yield reliable results.

Analysis

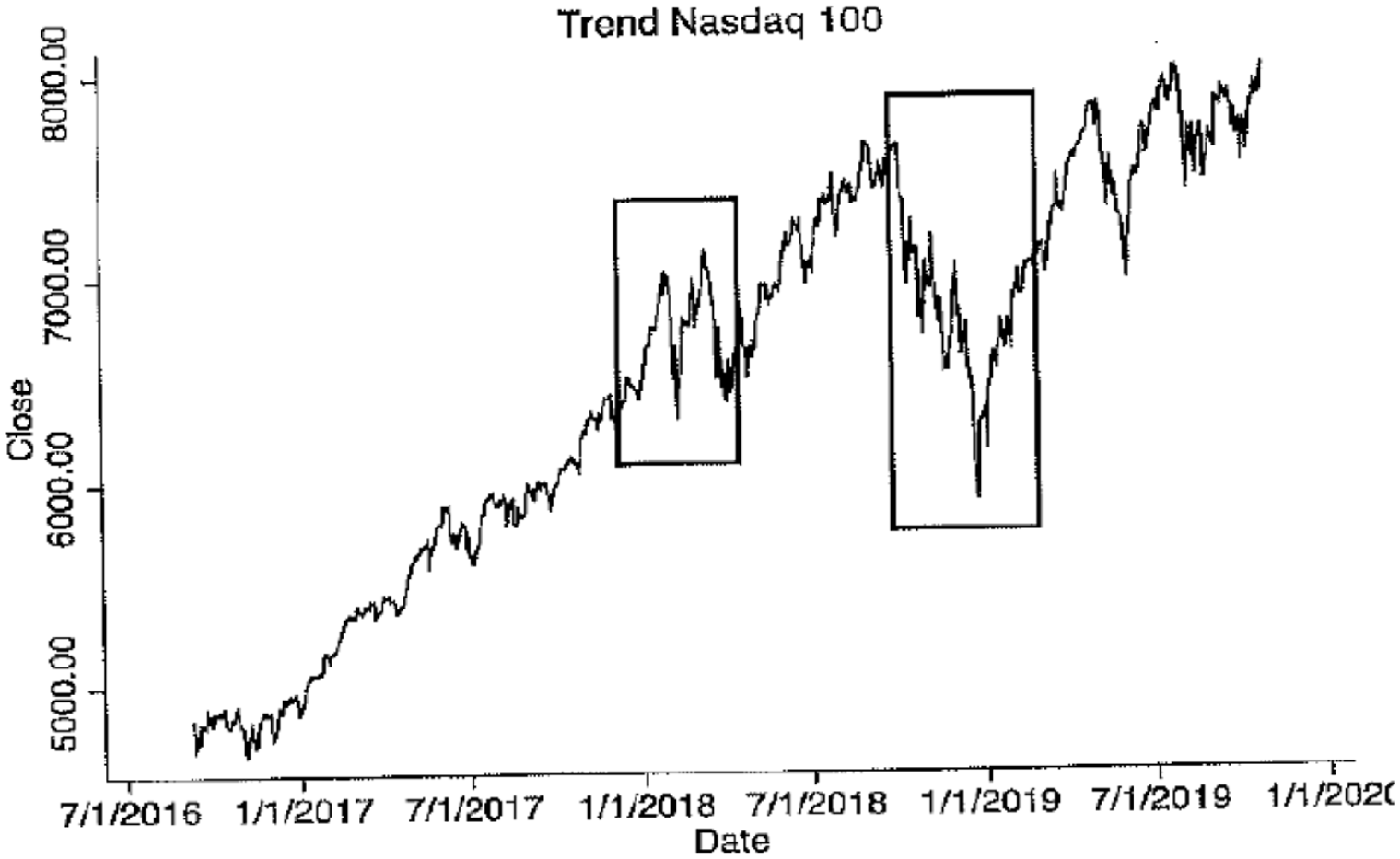

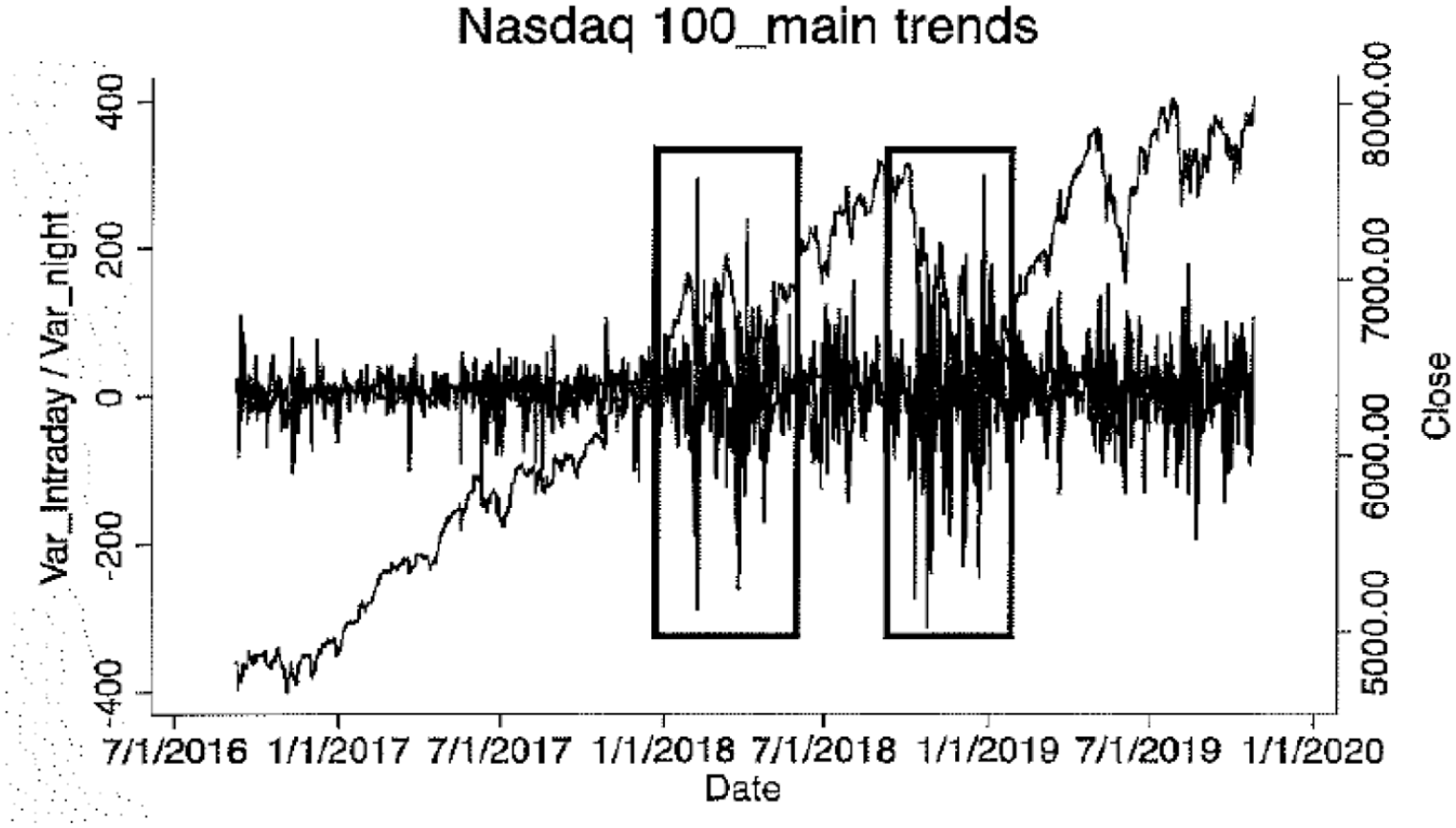

To this purpose, we need to figure out the financial market environment in the period under study, and we start by considering its volatility patterns. Tracking the closure prices of NASDAQ100 over the period of observation, we get the information presented in Figure 1.

NASDAQ100 Close trend.

Figure 1 highlights some periods characterized by high volatility: Q1 2018, Q4 2018, and Q1 2019. To better understand the reasons behind these volatility peaks, we plot NASDAQ100 closure prices together with the variables Var_Intraday and Var_night defined above, as depicted in Figure 2.

NASDAQ100 Close trend versus Var_intraday and Var_night.

To determine high volatility phases, we set two cutting thresholds of 150 and 200 for the difference between open and close, to classify a trading day as a high variability one when intraday variation is above 150 or below −150, or above 200 or below −200, respectively. We consider two possible thresholds to inquire whether our results are influenced by how high variability is defined. The choice of these threshold values is justified by the fact that 150 or 200 points are typical volatility benchmarks in intraday trading. The output is summarized in the Supplemental Material to the paper (Tables A_1: A and B). Table (A_1A) lists the intraday variations that cut the threshold value of 150, whereas Table (A_1B) lists the variations that cut the 200-threshold value. From the comparison, we see that the identification of high variability phases is not critically dependent on the choice of the cutting threshold. The most volatile months turn out to be February, October, November, December 2018, and January 2019.

Let’s consider the instability in February 2018. A consultation of newspapers, media archives, and official communications from the Federal Reserve, shows that the instability affected all major US market indexes. In that month, the Dow Jones Industrial recorded the worst intraday fall in market history, with a drop of more than 1,500 points. S&P 500 also reported a significant loss, and Stock Exchanges in other countries appeared unstable as well.

The main driver of such instability does not seem to be linked to fundamentals: no negative news about the US economy or alarming forecasts were released in that period. The most likely explanation for this volatility is negative expectations about future inflation (Irwin, 2018). On February 2nd, 2018, a very positive report about the US job market was released, recording an increase in both jobs and hourly wages. This fact, combined with a statement from the White House about the intention to further strengthen the economy in the long-term, raised the fear among investors of a more aggressive monetary policy, with a possible inflationary push and a consequent likely move by the FED to raise interest rates. Another cause for concern for traders was the bond market: its yields were rising, making debt more attractive for investors than riskier stocks. According to the NASDAQ website, the losses suffered by the index followed the down in technology companies like Apple and Amazon. The worries about inflationary tensions were not groundless: the Federal Reserve increased interest rates four times during that period.

The second period of US market turbulence occurred in the Fall of 2018 and was the consequence of several factors. One of them was the “trade war” proclaimed by Trump against China, which led to diplomatic strife and fluctuations of import-export tariffs, as well as to a slowdown of the Chinese economy. This topic is also widely covered in Trump’s tweets, and it is intuitive to expect that such tweets have been correlated with the NASDAQ100. Other relevant factors, in addition to the rise in the interest rates that made bonds relatively more attractive than stocks, were the uncertainty induced by a slowdown in global growth, the disappointing performance of Apple, Google, and Snap (which led to a drop in the NASDAQ index), and the trend of oil prices. This latter source of instability was related to rumors about sanctions against Saudi Arabia in response to the murder of Jamal Khashoggi: the ensuing concerns about a drop in oil production led some to fear a rise in oil prices (Krauss & Gladstone, 2018). As high oil prices tend to slow down economic growth, particularly where the economy heavily relies on oil imports, this crisis raised concerns, causing market instability.

We consequently chose a set of control variables that cover the main macroeconomic effects behind the periods of high volatility. Specifically:

Brent oil prices

Futures on gold prices

Exchange rates EUR/USD

Yield of treasury 10 years

Results

We are now ready to test our research hypotheses, starting with R1.

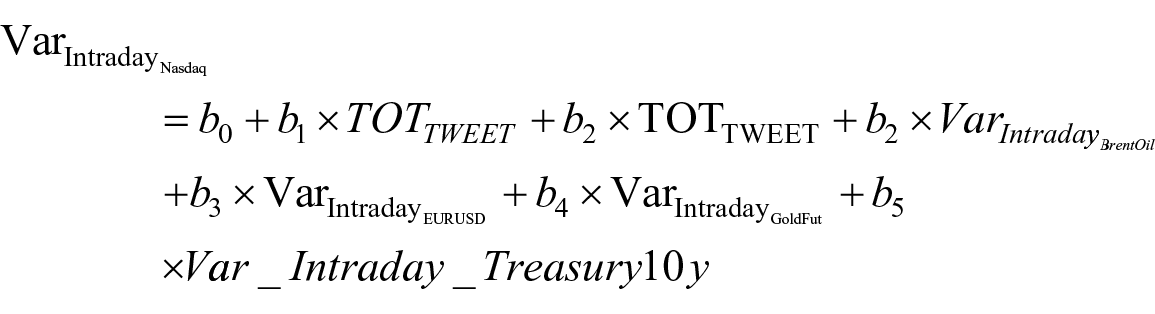

To this purpose, we take Var_Intraday, that is, the overall intraday variation of the stock prices, as the dependent variable, and the total daily number of Trump tweets and the control variables as the independent variables.

Our model is the following:

Over the whole period of observation, we find a mildly significant negative correlation (p < .1) for the total number of tweets, the intraday variation of the Brent Oil price, the intraday variation of the exchange rate between Euro and Dollar and, not surprisingly, the variation in the yield of Treasury Bonds with 10 years maturity.

A more detailed disaggregated analysis, that considers the impact on the stocks of the single companies included in the NASDAQ100, increases the level of significance of the independent variables (the number of tweets specifically reaches a level of significance close to 1%). 1 The result is not surprising considering that several companies in the index have similar fundamentals, and their stock market trends tend to be highly correlated.

The increase in the significance of TOT_TWEET from the aggregate to the more disaggregate model could also be due to the weighting method employed to compute the NASDAQ100, based on the market capitalization of the included companies, which does not allow the fluctuations of single firms’ stocks to be fully reflected into the daily NASDAQ100 performance.

It is also worth observing that the R-squared in our regressions is generally low, but this is expected, in that additional variables are necessary to fully explain the intraday variation in the index and in the share prices. However, since our goal is not to explain whole intraday variation but to assess whether Trump’s tweets are related to the stock market dynamics, this is not a critical issue.

Our results seem therefore to support R1: Trump’s tweeting activity is negatively related to NASDAQ100, the more so the more intense such activity on a daily basis. This result agrees with those from previous studies such as Liu (2019) and Reed (2016). Given the evidence from our own study and from the literature, we conclude that an intense daily tweeting activity by Trump creates uncertainty that affects the stock market.

We now ask whether our results change once we distinguish two subperiods: before and after Trump is sworn in. We re-estimate our model for the two subperiods separately (see Supplemental Materials, Annex A2). A relevant additional result that emerges from the comparison is the statistical significance of the future gold price control variable. The variable was not significant for the whole period of observation. However, it becomes significant once we separate the two phases, with their different implications for market expectations. In the pre-presidential phase, the daily number of tweets has a positive relationship with the stock market, and only when Trump is sworn in the association becomes negative (see Supplemental Materials)—that is, it seems to be specifically associated to the fact that certain tweets are posted by a public figure in his presidential role. In other words, Trump’s tweeting style comes to be associated with instability only after he has taken service. Whereas it can be expected that a presidential candidate posts highly emotional and controversial tweets during the campaign to mobilize his electoral basis, once he is sworn in the market seemed to expect that the tone and content of his tweets would adapt to his new role. This unexpected continuity in style of communication, and the consequent lack of customary institutional composure (Cilizza, 2018) seem to be associated to the market’s gradual shift in its perception of Trump’s tweets. Also here, the R-squared remains very low.

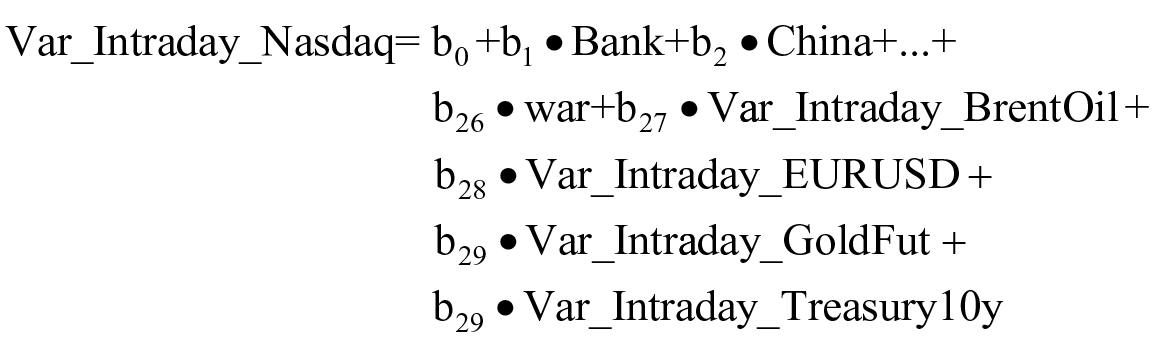

We can now test R2: are there specific topics that resonate with the stock market among those more systematically covered in Trump’s tweets? And if so, which is the sign of the effect, its size, and its statistical significance?

Our model now needs to include the variables for each of the keywords in our lexicon presented in Table 1 above:

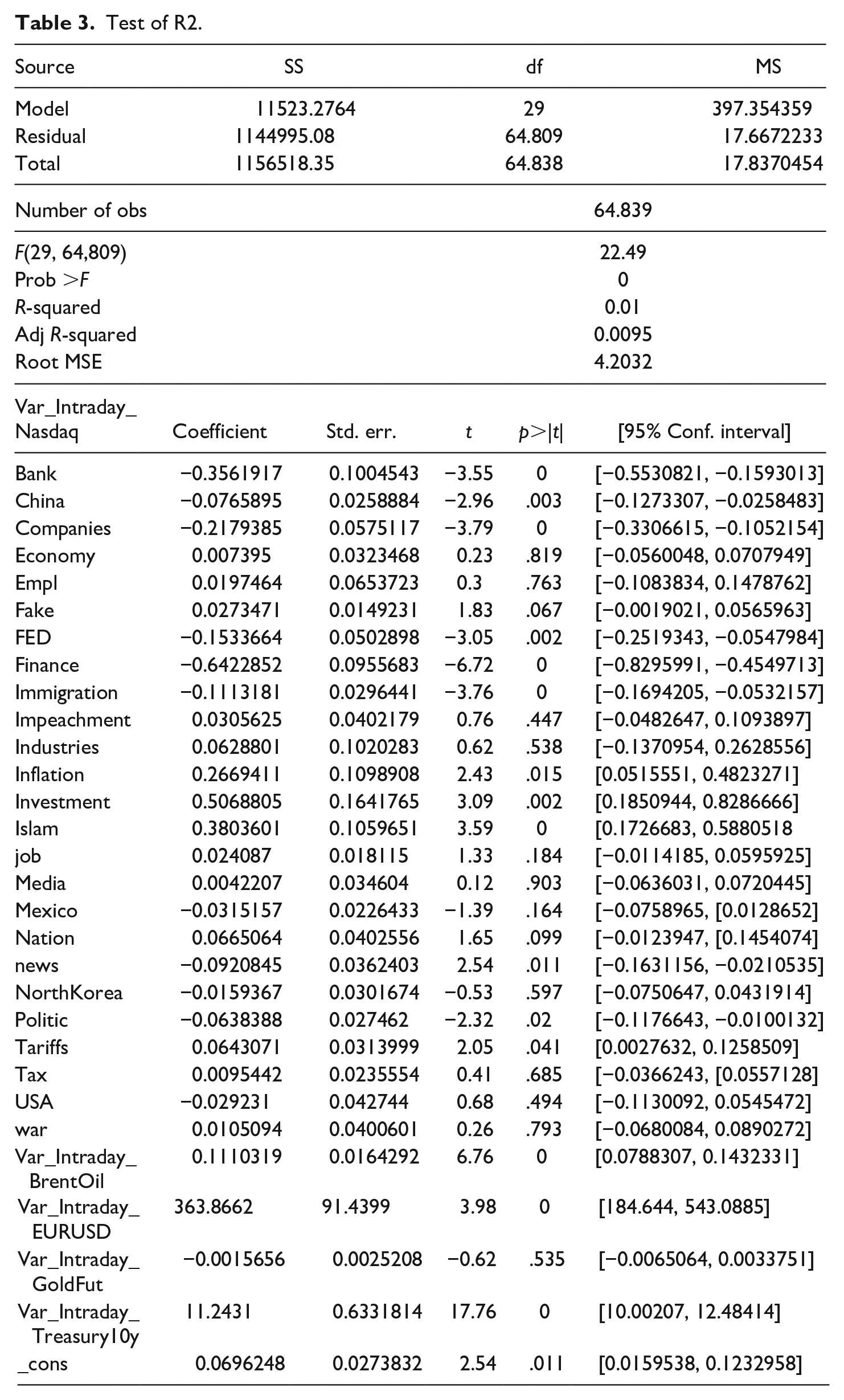

Our results are listed in Table 3.

Test of R2.

What we find is that the role of certain keywords remains substantial across the whole period, whereas for others it varies over time, as it can be checked by splitting again the sample in two subsamples, one for the pre-presidential period and the other for the presidential one (see Supplemental Materials, Annex A3). Keywords that remain significant over the whole period are, for instance, China, Immigration, Islam, Job—topics that have remained central in Trump’s narrative, both during the electoral campaign and throughout his presidency. Other topics which have been relevant during the electoral campaign, such as Mexico, gradually lost importance during the presidential term. Other keywords such as Fake that are substantially meaningless during the electoral campaign, become significant at p < .1 when the whole period of observation is considered. As it could be expected, the weight of topics is closely related to their political relevance in the moment.

Despite many keywords are significant in the 1% to 10% p-value range, sign and size of the effects differ. For instance, a tweet about banks is associated to an average drop of −0.356$ in the value of stocks, whereas one about inflation is linked to an average rise of +0.267$. However, in some cases, the sign of the relationship changes across the two periods, pre-presidential and presidential, while remaining statistically significant. For instance, China has a positive coefficient of +0.30 during the electoral campaign but flips to −0.086 in the presidential period—which again seems to capture the market’s growing concern, as the Trump presidency unfolds, that his mentions of sensitive topics on Twitter may have a destabilizing effect.

Therefore, the relevance of certain topics for the stock market is significant, and the sign and size of the effect depend on contextual factors, which seem to be closely related to the evolution of market perceptions about Trump’s political and communication strategy, as it unfolds during the presidency. It is interesting to compare the topics that are statistically significant over the whole period of observation in terms of their signs. The keywords that have a positive sign are Inflation, Investment, and Tariffs. Those with negative sign are Banks, Companies, FED, and Finance. It seems that when Trump focuses on the financial economy, the market is concerned, whereas when he focuses on the real economy, the market is positively stimulated. This might depend on the fact that, before the pandemic, Trump’s best approval ratings concerned the economy (P. Cohen, 2020). However, as Trump is being increasingly perceived as a source of destabilization, the market tends to assume defensive positions as to finance-oriented topics, where the role of emotionally charged tweets on critical issues may be immediate and substantial. Moreover, the Trump presidency has largely contributed to the American public opinion’s increased distrust in institutions (Edgecliff-Johnson & Bond, 2018), and therefore it is not surprising that any mention of critical regulatory agencies such as the FED is received with alarm by the markets.

R2 is therefore confirmed by the data, but with a few interesting twists: the difference in sign of the relationship between Trump’s tweets and the financial and the real spheres of the economy, respectively, and the different relevance and/or sign of the effect of certain topics in the pre-presidential versus presidential periods, as the market gradually familiarizes with Trump’s political strategy and communication style along the presidency. Other relationships are as expected, and especially for politically sensitive topics that are central to Trump’s narrative and related rhetoric.

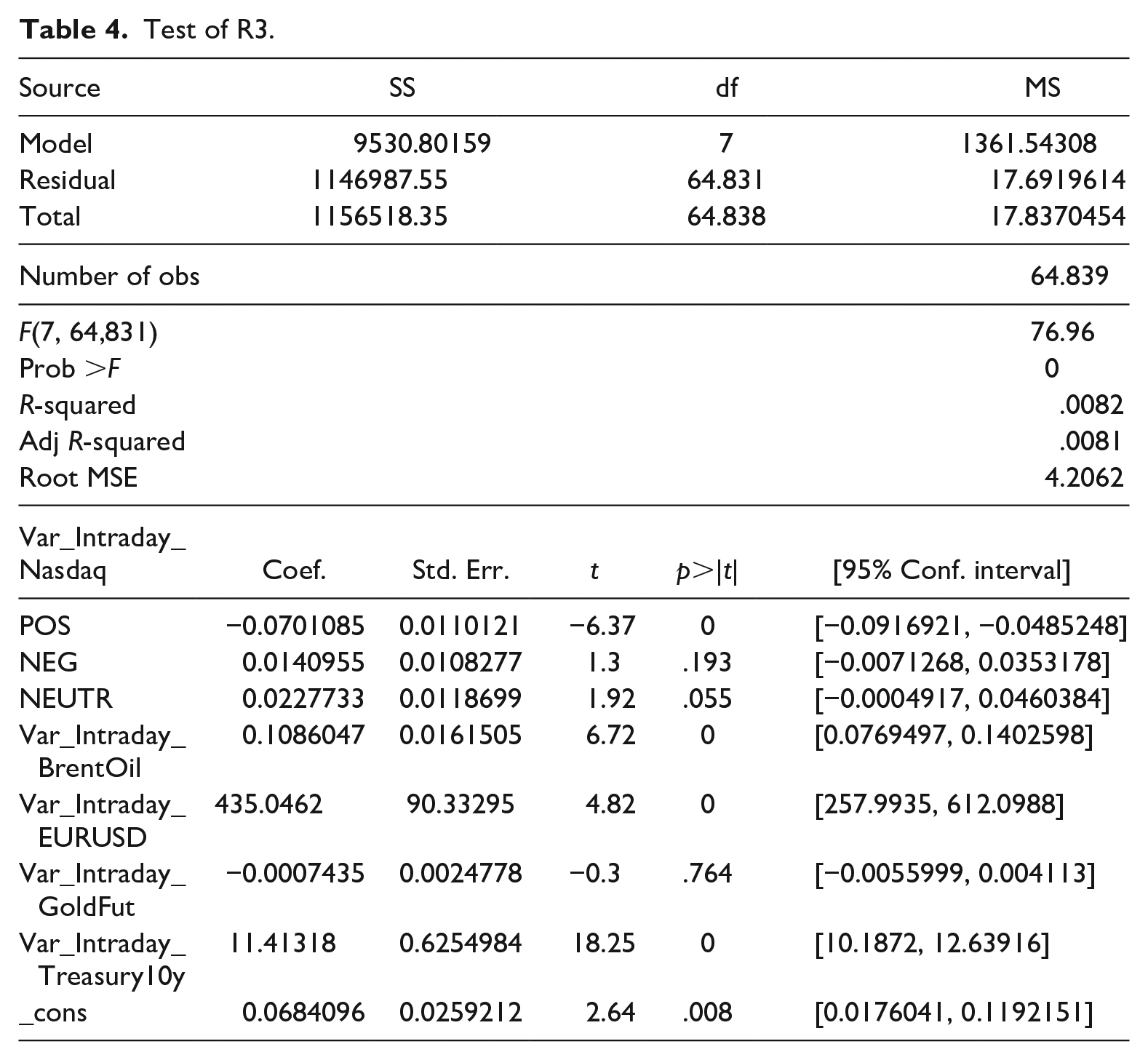

We can now test R3, where the role of the emotional content of Trump’s communication is being considered.

We use the following model:

whose results are reported in Table 4.

Test of R3.

Over the whole period, only positively toned and emotionally neutral tweets are significant in terms of impact, whereas negatively toned ones are not significant at p < .1. As expected, positive sentiment tweets are associated to negative stock market performance (an average drop of −0.07$), confirming that negative sentiment is perceived as Trump’s default mood state, with occasional, short-lived positive sentiment parentheses. Despite lack of significance, negatively toned tweets have a small positive effect, and the same holds for emotionally neutral tweets whose effect is however statistically significant.

When we consider the two sub-periods, pre-presidency and presidency, the negative effect of positively toned tweets becomes more significant. The more the market familiarizes with Trump’s political and communication strategy, the more it tends to regard positively toned communication as a sign of forthcoming emotional reversal (see Supplemental Materials, Annex A4). The lack of significance of negatively toned messages corroborates this interpretation: once negative sentiment is established as Trump’s default emotional mode, the market becomes less sensitive to it, considering it as “background informational noise.”

R3 is therefore partially confirmed, with the additional twist that negatively toned tweets do not have a statistically significant effect on the stock market.

It is however useful to test the statistical robustness of our results a little deeper. To control for possible bias, we run all the regressions using robust standard errors, and we verify that neither the p-values change their level of significance, nor the coefficients change their sign. In particular, when the coefficients change, such change is negligible.

Moreover, we control for multicollinearity among variables for all models. Results for the R1–R3 models are reported in the Supplemental Materials, Annex A5. We find no evidence of multicollinearity across our variables in any of the three models.

Twitter Communication, Public Responsibility and the Infosphere as Commons

With his hubristic leadership style (Akstinaite et al., 2020), Donald Trump has set a new standard in the relationship between the presidential role and the political responsibility that goes with it, and the pursuit of his own political goals and private interests (Scheuerman, 2019). In the context of a wider shift from “fair play” to “power play” in American political culture (Wolfensberger, 2018), he has explicitly and repeatedly refused to abide by deep-seeded, unwritten rules of institutional responsibility. This includes the unwillingness to concede the presidential race against Joe Biden (Arcenaux & Truex, 2022), and the alleged attempt to rebel against the electoral outcome, as culminated in the January 6, 2021 Capitol Hill incident (Taylor, 2021). Trump has legitimized a new playbook for institutional leadership that is relatively rare in mature democracies: a decision-making and communication style founded upon emotional unpredictability and visceral reaction (Drezner, 2020).

The power of social media in accelerating this complex socio-political transition may hardly be overestimated. Harton et al. (2022) argue how social media discussion may upscale the group dynamics leading to social intolerance and violence. Without a responsible use by major institutional and political figures, social media may fuel extreme polarization, and undermine the viability of non-partisan consensus around basic principles and facts (Flew & Iosifidis, 2020).

As shown in our study, Trump’s use of Twitter had important implications not only in the political sphere, but also, inevitably, in the economic one. Despite that a strict causal imputation cannot be made in our study, there is a clear pattern in the market dynamics on the first trading day after Trump’s tweets were posted. During his presidential term, the market appears to have progressively given up treating his tweets as a source of information about the economy, considering them as a predictor of his own future mood states. Given Trump’s presidential role, such mood states had nevertheless some effect on the stock market, but as an exogenous source of noise. Moreover, Trump has stood out among past presidents as one of the most economic statecraft-oriented (Drezner, 2019), and therefore his mood instability provides real motives for attention and concern for the stock market and for the economy more generally.

These results raise serious ethical problems about the responsibility of public personalities in key institutional positions. It is true that, after all, the market has learnt to cope with the rhetorical tactics of institutional communication (Brühl & Kury, 2019) and thus also to “sterilize” Trump’s tweets as carriers of information about anything else than his own mood state. However, making markets insensitive to the information content of statements from primary institutional figures is a serious blow to the scope and operation of public policy. Such statements may have a crucial importance to stabilize the economy in critical moments, and political credibility is a crucial precondition for sustained growth (Borner et al., 1995). Filtering information from noise is intrinsically difficult in financial markets, due to the growing number and variety of potentially relevant sources (Buscema et al., 2022). It is therefore in the public interest to ensure that all possible sources of noise are filtered off to promote market stability and growth. If one such source comes from an institutional role whose task is also ensuring economic stability and fighting uncertainty, this is not only paradoxical, but also a serious breach of the ethics of political responsibility.

Trump’s online activity is a systematic overturn of such responsibility. Public communication customarily plays with ambiguity (Johansson & Nord, 2018), but generally within reasonable boundaries. By transforming public communication on major public policy issues into exogenous noise as far as economic fundamentals are concerned, not only a new source of uncertainty and potential instability is introduced, but also a dangerous precedent is set. In particular, markets cannot anymore take for granted that public presidential statements should be considered by default a reliable source of information. Moreover, if public announcements with relevant potential economic consequences may be essentially driven by the logic of polarizing political discourse, post-truth politics may easily morph into post-truth economics, with all the implied risks of excess volatility and destabilization.

Should this lead to a massive regulation of social media use by public figures and politicians? This would be a rocky path. In the case of Trump, Twitter has eventually suspended his account, 2 although for reasons that are unrelated with the effect of his tweets on the economy. This may be seen as an extreme solution, which cannot be generalized as it potentially undermines basic principles of freedom of expression in democratic societies. Such a concern applies not only to public authorities, but also to private entrepreneurs that use social media in a similarly unrestrained way (Markham, 2019). However, a feasible approach to an effective governance of social media communication is that of regulating the infosphere as a commons: a public, unrestrained resource ruled by social norms of fair access and use (Floridi, 2021). This implies that clear violations of the basic principles of fair resource access and use should be sanctioned, as this is the only possible option that preserves the commons in the short term. However, since the control of social media platforms is in the hands of private businesses, the principle that private parties can decide who has voice on matters of public interest, and under what conditions, is critical and raises once more strong ethical concerns (Du, 2022).

Such top-down, private regulation is not only questionable in principle, but also counterproductive in the long-run, as typically an optimal management of a commons is reached with the gradual bottom-up emergence of effective sanctioning systems (Casari & Plott, 2003). The functioning of such systems is deeply related to the commitment to social norms relying upon basic behavioral mechanisms such as forms of reciprocity or inequality aversion. But our understanding of their operation, and our capacity to effectively intervene on them, is still partial and fragmented (Bolton et al., 2021). To what extent such mechanisms can work in digital contexts, and under what conditions, is a still open issue that needs to be urgently addressed by future business communication research.

The misuse of social media by key public figures reflects our lack of understanding of the functioning of social media and of digital content ecosystems more generally. Developing a digital platform and enabling its use by millions or even billions of users simultaneously need not imply an understanding of what kinds of collective behaviors will emerge, even when we set the rules ourselves. This is due to the ecosystemic nature of the infosphere where different platforms and media are connected in complex ways (Bennett et al., 2018; Neu et al., 2022). In this perspective, the dysfunctional relationship between Trump’s Twitter communication and the stock market has not been fully perceived in its both short- and long-term implications. As of today, little research has appeared on the public ethics of social media communication and its implications for public affairs (see e.g., Rauf, 2021). The ethical and policy implications for financial markets are still largely unexplored. Our results make a sobering call for more such research.

Conclusions

Our paper belongs to an emerging line of research that studies the role of social media communication in financial markets. Here, Twitter is the social media of choice, due to both its high affordance for rapid, timely and targeted communication and the availability of data. Such literature sits within the broader framework of the impact of media on stock market behaviors, and of the role played by narratives in shaping market reactions (Laskin, 2018). The activity of Donald J. Trump on Twitter is of particular interest in this regard, due to his highly unusual mode and style of communication through social media, and especially so during his term of presidency. Trump’s highly emotionally charged communication was initially surprising in view of the pre-existing social expectations of institutional communication by a US President. However, it has rapidly led to a complex adjustment by the markets, that is reflected in our results.

As markets have become more familiar with Trump’s political strategy and communication style, their sensitivity to the emotional tone of Trump’s tweets has evolved. The markets have increasingly discounted the negative sentiment prevalent in Trump’s tweets as the default mode of his communication strategy. They have accordingly interpreted his positively toned tweets as negative anticipatory signals of likely future emotional downturns, with a consequent negative relationship with market performance. In the pre-presidential period, positively toned tweets still had a generally positive, mildly significant association with the stock market, as it could be expected. However, Trump’s mere activity on Twitter has gradually come to be perceived as a source of instability with negative effects on market performance, and the same is true in particular for most politically sensitive topics, including key foreign policy ones and those related to the financial economy and to policy regulation. We then observe a flip in the sign of the relation for certain crucial topics as Trump’s presidential term unfolds. This is the case of China, where the association was initially positive but turns negative once Trump proclaims an explicit trade war. However, when the topic concerns the real economy where Trump’s performance has been generally appreciated by the public opinion, the stock market performance is generally positive.

This emotional desensitization process applies to the general public opinion, and more specifically to stock markets, but for Trump’s supporters, on the contrary, emotional hyping has succeeded in turning political support into something closer to a personality cult (Reyes, 2020). Unsurprisingly, Twitter has emerged as a powerful political marketing tool for emotionally focused communication which is best exploited by neo-populist movements, which make use of a prevalently negative emotional tone (Calderón-Monge, 2017). Positive emotions may instead be particularly effective in social media mobilization of the electorate in building trust toward institutions (Marquart et al., 2022). What is interesting for our study is that, in his political strategy, Trump seems to have prioritized use of negatively emotionally charged communication to galvanize his electorate even at the cost of losing emotional connection and credibility with major national stakeholders such as the financial environment. This has serious ethical implications in that it sets a dangerous precedent that could have long-term consequences on the use of public statements from key institutional figures as a primary public policy resource, with considerable impact on the public interest.

The relevance of our study rests upon the width of the period of observation and the specific target variable we consider, the NASDAQ100 Index, providing a valid proxy for major non-financial companies across a variety of sectors. Our results are consistent with previous studies that addressed the same issues with different data and partially different methodologies. But we also explore the role of the emotional tone of Trump’s tweets jointly with stock market performance. We find a new, interesting result, that could be synthetically labeled as “emotional desensitization” in view of its intriguing parallel with well-studied effects in social and personality psychology, which may be related to exposure to emotionally abusive content (Krahé et al., 2011). An emotionally charged communication where tone and arousal are systematically manipulated to capture attention and hijack the public debate, as in the case of Trump (Wiemer & Scacco, 2018), gradually led to a lack of perceived significance of tone as a channel of social cognition regarding future market dynamics. The main social cognition content of the emotional tone of Trump’s tweets seems to be self-referential: it is primarily a useful signal to predict Trump’s own mood dynamics and carries an interest as to market prediction mostly in these terms. With his use of social media, Trump has therefore entirely appropriated the value of social media communication in the public interest for the pursuit of his own political and private goals, turning it into an extension of his private conversational space.

Our results provide only a preliminary analysis of these relevant issues for both theory and policy design. Trump’s communicational legacy has inspired many other populist political leaders worldwide (Serhan, 2020), as well as many political communication strategists and advisors (Hollinger, 2018). An enhanced understanding of the role of emotional content in eliciting certain kinds of market (and more generally socio-behavioral) responses to the social media communication of public figures of major importance ranks high in the future research agenda. A full-fledged understanding of these mechanisms calls for a more systematic consideration of the overarching narratives. In the case of Trump, the constant counterpoint of his narrative has been a strongly negative emotional tone underlining the “doomsday” consequences of presumed errors and misdeeds of previous political leaders, often accompanied by open displays of frustration and anger (Bucy et al., 2020). We find that this seems to have led the market to develop a new coping strategy. One might expect that new waves of populist communication would play in a more nuanced way with positive and negative sentiment, and develop less polarizing and intimidating narratives, but the current momentum seems to be headed in the opposite direction.

Our study has limitations. However representative, we have focused upon a single market index, NASDAQ100, and have exclusively assessed the next market day effect of Trump’s tweets. Working with a more composite set of stock market indicators and tracking longer-term impacts, and in particular the persistence of effects over time also depending on the topic and on the emotional tone, is certainly an important next step in the analysis, also in view of literature results that suggest that such effect is likely to decay quickly. Moreover, we have worked with a given lexicon of keywords which capture the most frequently touched topics in Trump’s tweets and/or the most relevant policy issues. Testing the whole corpus of Trump’s tweets via more sophisticated content analysis methodology is another important step forward. Furthermore, more conclusive interpretations could derive from the inclusion of instrumental variables that help define the direction and strength of the causal relationship. Different simultaneous directions of causality should also be explored. In addition to the possible causal effect of Trump’s tweets on the market, which has been at least partly corroborated by the available literature, this additional step of the analysis would help us understand the effect of previous short-term stock market performance on Trump’s tweets.

Finally, we have considered a very simple technique for sentiment analysis, based upon a selected list of emotional tone markers, but again working with a more sophisticated sentiment analysis methodology could help to further refine our results and capture more, so far unnoticed nuances.

Supplemental Material

sj-docx-1-job-10.1177_23294884231156903 – Supplemental material for Commentary—Much ado About Something Else. Donald Trump, the US Stock Market, and the Public Interest Ethics of Social Media Communication

Supplemental material, sj-docx-1-job-10.1177_23294884231156903 for Commentary—Much ado About Something Else. Donald Trump, the US Stock Market, and the Public Interest Ethics of Social Media Communication by Leonella Gori, Pier Luigi Sacco, Emanuele Teti and Francesca Triveri in International Journal of Business Communication

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability

Data are available from the authors upon request.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.