Abstract

Farmers regularly make intertemporal decisions under risk or uncertainty. To improve how farmers behave when faced with decisions that have financial consequences, there is a need for a deeper understanding of farmers’ risk and time preferences. While the relationship between individual components of affect and risk preferences is well documented, the same cannot be said for holistic measures of affect on one hand, and for affect and time preferences on the other hand. The data analysed in this paper is the 2014–2015 Indonesian Family Life Survey Wave 5. The survey included experimental measures designed to elicit both risk and time preferences from the same subjects. We analysed the data using limited dependent variable regression models. Our findings strengthen what is known about the affect infusion model. With increased pleasant affect, farmers’ willingness to take risks increases significantly. The results also suggest that pleasant affect is associated with increased odds that farmers will choose future rewards in the long horizon but had no statistically significant effect on the short horizon. The practical implications are that an experience of pleasant affect before decision-making may cause the decision-maker (DM) to perceive a prospect as having high benefits and low risks. Pleasant affect may also induce lower sensitivity towards losses and play the role of a buffer which reduces the immediate negative impact of information that otherwise would prevent the DM from focusing on the long-term.

Introduction

It is well documented in the literature that the behaviour of individuals differs depending on their mood or state of emotion. Some studies (e.g., Kliger & Levy, 2003; Lepori, 2010) have also shown that statistically significant relationships exist between affect and risk attitudes in both laboratory and field conditions. However, these findings are not unanimous in the direction of the effect or have favoured contradicting theories. Hence, there remains considerable debate in the decision-making literature regarding the role that affect plays in decisions making. Further, the economics literature is lacking in accommodating psychological insights related to affect (Drichoutis et al., 2014).

We identify gaps in the literature. First, most studies focused on examining the interaction between a few selected positive affect 1 such as happiness or enthusiasm and risk preferences (e.g., Guven & Hoxha, 2015; Ifcher & Zarghamee, 2011). Second, many of the previous studies have focused on examining the influence of affect on risk preferences with only a few such as Lukoseviciute (2011) examining the link between affect and time preferences. Third, several studies have artificially induced moods (e.g., with music or movies in Chung et al., 2016; Lepori, 2010) with only a handful relying on induced mood arising from real-world circumstances. To address these gaps, this paper investigates whether a statistically significant relationship exists between affect and risk and time preferences after controlling for the effect of selected phenomena. We achieve these objectives by estimating data from a cross-sectional survey using appropriate regression models.

Why the Focus on Farmers?

Risk attitudes and attitudes towards future events impact the economic lives of farmers by playing a crucial role in agricultural decisions. These decisions range from adoption decisions (Duquette et al., 2012; Meijer et al., 2015), input use (Qiao & Huang, 2021), insurance payment (Elabed & Carter, 2015), response to climate change (Jianjun et al., 2015) among others. Considering that farmers have to make an enormous number of decisions under uncertainty and risk, measuring the impact of affect on risk and time preferences is crucial. Affect not only plays the role of a motivator of behaviour and information processing but also influences how individuals perceive and evaluate risks and the subsequent problem-solving strategy (Blanchette & Richards, 2010; Isen, 2001). This investigation will result in a better understanding of farmers’ decisions when they are faced with different situations and guide the approaches extension services or policymakers employ to communicate with farmers. It will also help in improving the design of future interventions. Another important reason for focusing on farmers is that compared to other groups, less is known about the risk and time preferences of farmers as many studies use convenience sampling, for example, with students. Considering that across many low-and-middle-income countries, farmers make up one of the largest occupational groups and the evidence that risk and time preferences vary with groups, there is the need to extend such investigation to actual farmer-subject if the goal is to fully understand the behaviour of farmers.

Theoretical Backgrounds

The use of the term ‘mood’ and ‘emotion’ in the literature is fuzzy. However, some authors (see Beedie et al., 2005) have argued that there exist fundamental differences in the constructs they represent despite their close relation. From the perspective of duration, it is postulated that emotions have the propensity to be extremely brief. Typically, it lasts for a few seconds compared to moods which last much longer (Drichoutis & Nayga, 2013). Michl et al. (2011) argue that the distinctions between mood and emotion are more theoretical than empirical. However, both mood and emotions can be categorized as affect—a facet of subjective well-being. The context in which we use the term ‘affect’ in this paper is similar to van Knippenberg et al. (2008) which is more broadly defined to accommodate both discrete emotions and diffuse mood states (e.g., feeling good or being in a bad mood) as well as a proclivity towards certain ‘feeling’ states.

For brevity, this paper defines risk preference as the attitude respondents’ hold towards risks. Farmers are categorized as being risk-avoiding if they prefer sure gains over the equivalent uncertain gains. A similar definition has been employed in Guo and Spina (2016). On the other hand, the context in which time preference is used in this paper is similar to Frederick et al. (2002) which implies a preference for present over future utility. We discuss this further in the third section.

Affect as Determinant of Risk Preferences

In the current literature, the controversy lingers as to the extent to which positive and negative affects are phenomenologically separable. However, without entering into this contested literature, it has been observed that positive and negative affects do not necessarily have the opposite effect on risk attitude. For instance, there is empirical evidence that happiness and anger may have a similar effect on risk attitude (Lerner & Keltner, 2001). Several findings provide evidence that suggests that an individual in a positive emotional state is more likely to perceive a prospect as having high benefits and low risks. Kliger and Levy (2003) observed that a good mood prompts investors to be less willing to tolerate risk and vice versa while Grable and Roszkowski (2008) found that participants’ happy mood was positively associated with greater financial risk.

The results from Meier (2019) suggest that within-individual changes in selected positive and negative affects correlate with changes in risk attitudes and patience. Meier (2019) found that conditional on the other emotions, however, the direction of the relationship varied. Happiness and anger increased willingness to take risks while fear reduced the willingness to take risks. Meier (2019) observed that happiness tends to increase patience while fear and anger encourage less patience. This finding has been investigated further at domain-specific levels. Campos-Vazquez and Cuilty (2014) found a statistically significant relationship between risk aversion and emotional state but observed that sad decision-makers (DMs) were more risk-averse in the gain domain, angry DMs were less loss averse, and anger had a stronger impact on the loss domain compared to sadness.

Many studies have induced moods of respondents and observed the effect on various decisions. For example, Capra et al. (2010) induced respondents’ mood then examined their behaviour in a price auction. They found that under positive mood, respondents submitted bids that were significantly higher than their values. Similarly, Lahav and Meer (2012) found that although subjects induced with positive mood tend to bid on fewer units of the share, they are willing to pay higher amounts for the shares.

There are arguments over the consistency and reliability of measures of both risk and affect. However, the widely adopted measure of affect is via self-report (Diener, 2020). This is mostly through ratings on semantic differential scales or observational and computational methods such as coding facial expressions. Two predominantly used tools for measuring individual differences in risk preference are the psychology-based self-reported method and the economics-based experimental method. Questions in the self-reported questionnaire typically take the form of psychometric measurement similar to ‘close associates say I am a risk taker’ or ‘taking risks in most aspects of my life is something I enjoy’. It also takes the form of propensity to take risks across situations measured using Likert type scales. On the other hand, experimental approaches involve participants being presented with pairs of lotteries with different outcomes in which the variance of the payoff increases with an increase in the expected payoff.

Affect as Determinant of Time Preferences

There are studies that have provided evidence on the influence affect has on time preferences. Drichoutis and Nayga (2013) induced subjects into the positive or negative moods and observed that both negative and positive mood states increase patience but in different magnitudes. Ifcher and Zarghamee (2011) elicited time preference through a matching procedure where participants reported the present value of a future payment. They found that positive affect had a significant effect on time preference with mild positive affect significantly reducing participants’ time preference compared to neutral affect.

Meier (2019) reported that happiness increases patience, anger reduces patience and fear leads to less patience conditional on the other emotions. However, Lerner et al. (2013) documented different results from their experiments. Lerner et al. (2013) found that sadness significantly increases impatience and made people more present biased although not globally more impatient. Lukoseviciute (2011) observed that while mood and pre-existing risks do not affect risk preferences, it, however, has a significant effect on time preferences. Overall, these arguments together suggest that positive affect appears to increase patience. Further, it highlights the fact that not much is known about the nature of the effect negative moods have on patience.

The methods used for measuring time preference are mainly through experiments, for example, measured using a standard matching procedure, in which subjects report the present value of a future payment. However, few studies have used self-reported indicators of patience.

Leading Hypotheses Linking Affect with Risk and Time Preferences

Findings have largely favoured the tenets of two main theories, the affect infusion model (AIM) and the mood-maintenance hypothesis (MMH) (Kramer & Weber, 2012). The AIM rationalizes mood congruent effect in social cognition. Affect infusion materializes when moods or emotions have an invasive and subconscious impact on the way individuals think, form judgments and behave in social situations. According to findings of the AIM, a person in happy moods tends to take more risk arising from lower sensitivity towards losses (Chou et al., 2007; Grable & Roszkowski, 2008). On the other hand, the MMH (Isen & Patrick, 1983) postulates that a good mood stifles risky behaviour particularly in situations where the possibility for losses is salient. This reason being the individual intends to maintain the good mood being experienced (Juergensen et al., 2018).

Several other hypotheses have also been tested in the literature. For example, the mood repair hypothesis suggests that risky choices in decision-making function as a medium to repair a DM’s negative affect. The argument is that negative affect prompts the objective of mood repair which the DM may achieve through risk taking (Tice et al., 2001). This behaviour has been observed with previous findings that reported that when a DM is in a negative affective state, the DM disposition to take risks in order to secure an outcome that would trigger happiness becomes higher (Isen & Geva, 1987). According to Mittal and Ross (1998), negative mood motivates willingness to take higher risks for the sake of obtaining higher potential rewards that will repair their current negative mood state.

The basis of the depletion hypothesis is that risky choices are the mere ramifications of a state of depletion ensuring from engagement in active mood regulation attempts. This implies that following an experience of negative affect a DMs actively endeavour to regulate their mood with the attended effect of consuming scarce self-control resources in the process. The state of depletion that ensues then drives a greater desire for risk taking (Bruyneel et al., 2006; Vohs & Faber, 2007). The results in Bruyneel et al. (2009) show support for the depletion due to active mood regulation attempts in explaining the link between risky choices and negative affect.

The risk-as-feelings hypothesis (Loewenstein et al., 2001) suggests that DMs construct risk preferences from a combination of analytical and emotional inputs. It draws attention to the role of affect experienced at the point of decision-making (Grable et al., 2020). The risk-as-feelings hypothesis incorporates emotions as an anticipatory factor, which suggests that the effect of feelings on behavioural choices is direct and posits a reciprocal relation between cognitive evaluations and feelings (Kobbeltved et al., 2005).

The affect-as-information on the other hand assumes that a DM relies on his/her feelings as a source of information, with distinct feelings supplying different types of information (Schwarz, 1990). The pathway through which feelings interact with thought processes is through judgments made about external situations relying on one’s feeling about it rather than being based on objective facts. The mood-as-resource hypothesis suggests that a positive mood provides people with the resources to handle short-term negative consequences of a message (Raghunathan & Trope, 2002). As such, a positive mood plays the role of a buffer which reduces the immediate negative impact of information that otherwise would prevent an individual from focusing on the long-term benefits.

The self-control framework which is mainly applied to link affect with time preference entails the ability to control emotions particularly when faced with competing options, for example, one available immediately versus one delayed into the future. It argues that any act requiring self-control (e.g., mood suppression) may have important effects on impulsivity. From this perspective, choosing outcomes that are smaller but immediate (i.e., a high rate of discounting) is categorized as an impulsive choice compared to the larger but future outcomes considered as reflecting self-control. This paper investigates which one of the hypotheses and theories explains the effect of mood on risk and time preferences. The AIM, MMH, mood repair hypothesis and the depletion hypothesis have been tested using similar experiments as what is employed in this paper (e.g., Bruyneel et al., 2009; Drichoutis & Nayga, 2013; Kassas et al., 2020; Michl et al., 2011).

Methodology

Data

The results in this paper are from the analyses of the 2014–2015 Indonesian Family Life Survey (IFLS) Wave 5 (Strauss et al., 2016). The suitability of the IFLS dataset in examining the relationship between affect and risk and time preferences is credited to the data consisting of a nationally representative sample of the Indonesian population. The data cover 16,204 households and 50,148 individuals across 13 of the 27 provinces. After excluding non-farmers and individuals with missing information, the analysis was conducted using 3,626 farmers. The data we use in this paper include measures of self-report to elicit affect and revealed preference measures 2 to elicit risk attitudes and time preferences.

Determining Risk Attitudes

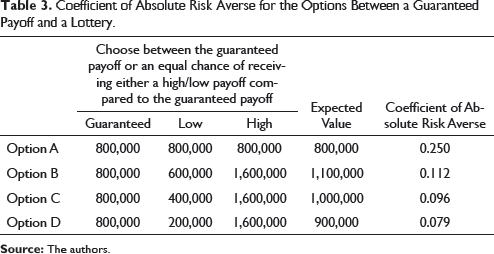

Participants were asked which options they preferred between a hypothetical guaranteed payoff and a lottery in which the lower payoff is smaller (and the higher payoff is larger) than the guaranteed payoff. In the 1st instance, participants were asked to choose between two options.3, 4

Option 1 guaranteed participants an income of Rp 800,000 per month. While for Option 2 participants had an equal chance of receiving either Rp 1.6 million per month or Rp 400,000 per month.

If the participant chooses the guaranteed payoff over the lottery, then the participant is asked:

Option 1 guaranteed participants an income of Rp 800,000 per month. While for Option 2 participants had an equal chance of receiving Rp 1.6 million per month or Rp 600,000 per month.

On the other hand, if the participant chooses the lottery over the guaranteed payoff, then the participant is asked to choose between:

Option 1 which guaranteed participants an income of Rp 800,000 per month. While Option 2 participants had an equal chance of receiving Rp 1.6 million per month or Rp 200,000 per month.

In summary, while all three lotteries have a 50/50 chance of doubling the sure payoff on the higher end, Lotteries 1, 2 and 3 have a 50/50 chance of obtaining 50%, 25% and 75% respectively lower than the guaranteed payoff. We follow the methods used in previous studies (such as Barsky et al., 1997; Sohn, 2017) in categorizing participants based on their risk preferences without the assumption of any specific functional form for the utility function. We obtained two main categories of risk preference from the responses. Any participant that rejected both equal chances of receiving Rp 1.6 million or Rp 400,000 and Rp 1.6 million or Rp 600,000 and chose instead the guaranteed income of Rp 800,000 is risk-avoiding. Otherwise, we classify participants as risk taking. A similar method of classification is used for the short and long-time horizon preferences.

Determining Time Preferences

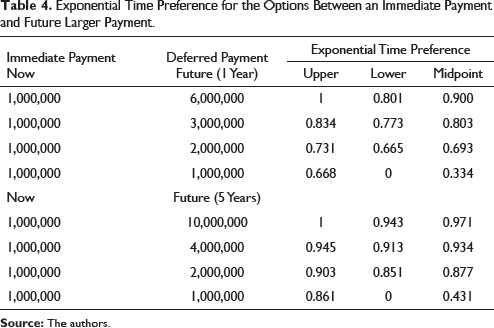

The time preference was obtained for what we categorize as short (1 year) and long (5 years) time horizons. For the short time horizon, participants were told to imagine they had won some money but had to choose between two options.

Option 1 offered immediate payment of Rp 1 million. For Option 2, the payment of Rp 3 million will be deferred to one year time.

If the participant chooses the immediate payment over the future larger payment, then the participant is asked what their choice will be when:

Option 1 offered immediate payment of Rp 1 million. For Option 2, the payment of Rp 6 million will be deferred to one year time

On the other hand, if the participant chooses the lottery over the guaranteed payoff, then the participant is asked:

Option 1 offered immediate payment of Rp 1 million. For Option 2, the payment of Rp 2 million will be deferred to one year time.

A similar format is repeated for the long-time horizon but with payments of Rp 4 million, Rp 10 million and Rp 2 million in 5 years each compared to an immediate payment of Rp 1 million. From the responses, the two categories of time preference obtained for each time horizon are impatient and patient.

Measures of Affect

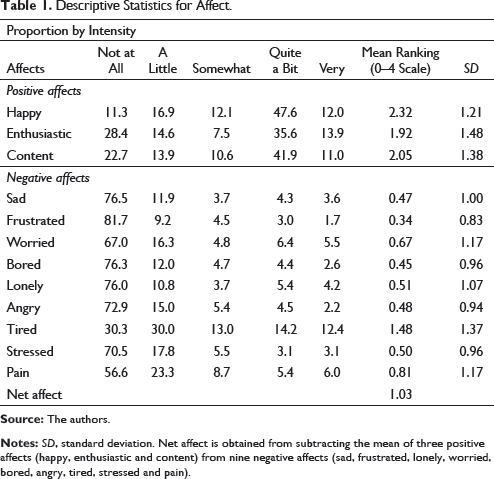

In a slightly different approach from Hirt et al. (2016) and Egan et al. (2015) where the mood was manipulated through an autobiographical memory task, subjects were required to recall their activities and experiences of the day prior to the interview (albeit as a general part of the survey). This was asked prior to the questions on risk and time preferences. Subjects were then to rank the intensity of the 12 different components of affect experienced (namely happy, enthusiastic, content, frustrated, sad, lonely, worried, bored, angry, tired, stressed and pain). The ranking was on a scale of 0–4, which represented ‘Not at all, A little, Somewhat, Quite a bit and Very’, respectively. Previous studies (e.g., Callen et al., 2014) have shown that experimentally recalled affect influences attitudes and decision-making.

In order to calculate net affect, this paper classifies affect into unpleasant and pleasant from the dimensions of positive affect (happy, enthusiastic and content) and negative affect (frustrated, sad, lonely, worried, bored, angry, tired, stressed and pain). Composite measures of negative and positive affect were calculated by averaging respondents’ responses for happy, enthusiastic and content and frustrated, sad, lonely, worried, bored, angry, tired, stressed, pain. Net affect (a widely employed measure of mood in the psychology literature) is calculated by subtracting the mean of the positive affect from the mean of the negative affect elicited on a 5-point scale. Similar to Kahneman and Krueger (2006) and Connolly (2013), in any case where the maximum scores of the negative descriptors of affect are larger (smaller) than the maximum scores of the positive descriptors we categorized as an unpleasant (pleasant) affective state. The hypothesis in this paper is that respondents risk attitudes and time preferences will be determined by the most dominant affect (i.e., either pleasant or unpleasant).

Estimation Method

We employ probit regression to estimate the relationship between affect and risk attitudes and affect and time preference due to its suitability to empirically test the predictive strength of the explanatory variables (Greene, 2000). We consider risk taking (or patience in the case of time) as a binary outcome y (1 = risk taking (or patience), 0 otherwise),

Results

The demographic features of respondents were examined, and the results are discussed. The mean age of farmers was 38 years. The proportion without any sort of formal education was 3%. The majority (51%) were female. About 57% avoided risk compared to 43% that chose the risky lottery over the guaranteed payment. In the short horizon, 67% of farmers were impatient while 76% displayed impatience in the long horizon, that is, by rejecting in all cases the future payment in favour of the immediate payment.

Descriptive Statistics for Affect.

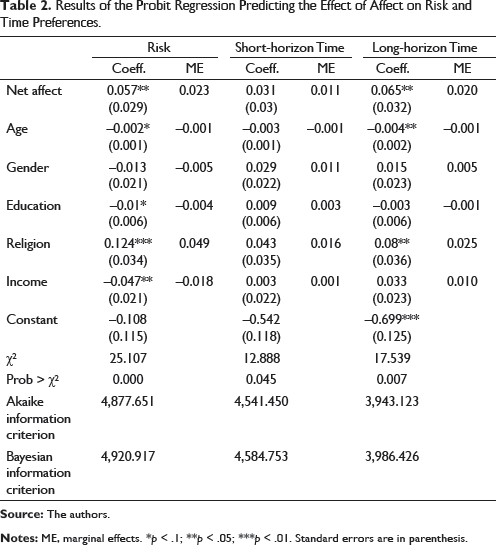

Given concerns of potential endogeneity arising from simultaneity between net affect and risk preferences on one hand and net affect and time preferences, on the other hand, we estimated an instrumental variable regression. We use neighbourhood safety as the instrument. The safety referred to in this paper is not one related to conflict and violence as those can affect behaviour including risk preferences. It relates to trust among those in the neighbourhood in terms of the willingness of others to help when needed, whether or not people will take advantage of others, and the safety of one’s property. To measure neighbourhood safety, subjects were asked how they consider their neighbourhood. The responses were measured on a scale of 1–4 with 1 scored as very safe and 4 being very unsafe. This measure is highly correlated with the suspected endogenous variable, that is, net affect (a Spearman correlation coefficient of 0.62). The tests of exogeneity (Wald: χ 2 = 0.71, p = .40) for the risk model (Wald: χ 2 = 0.35, p = .55) the short horizon model and the long horizon model endogeneities (Wald: χ 2 = 0.26, p = .61) show that there is not sufficient information in the sample to reject the null hypothesis of no endogeneity suggesting that a regular probit regression is appropriate.

Results of the Probit Regression Predicting the Effect of Affect on Risk and Time Preferences.

Effect of Net Affect on Risk Preference

As shown in Table 2, the probit model predicting risk preferences suggest that affect is a significant predictor of risk preference when age, gender, education, religion and income are controlled for. Thus, the more pleasant the net affect, the more likely the farmers will choose to take a risk. This result is in accord with those obtained by Tesfu (2017) that reports that happier people are more likely to take risks. However, the finding contradicts Guven and Hoxha (2015) who reported that happy individuals appear to be more risk-averse in financial decisions.

Effect of Net Affect on Time Preference

For the long horizon (5 years), farmers that experienced net pleasant affect are more likely to be patient holding age, gender, education, religion and income at a fixed value. However, in the short horizon (1 year), affect was not a statistically significant determinant of patience in financial decisions. These results coincide with those obtained by Ifcher and Zarghamee (2011) results that showed mild positive affect significantly reduces time preference over money.

Coefficient of Absolute Risk Averse for the Options Between a Guaranteed Payoff and a Lottery.

Exponential Time Preference for the Options Between an Immediate Payment and Future Larger Payment.

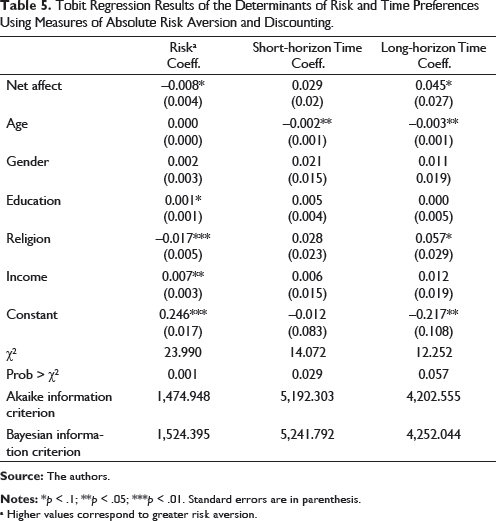

Tobit Regression Results of the Determinants of Risk and Time Preferences Using Measures of Absolute Risk Aversion and Discounting.

a Higher values correspond to greater risk aversion.

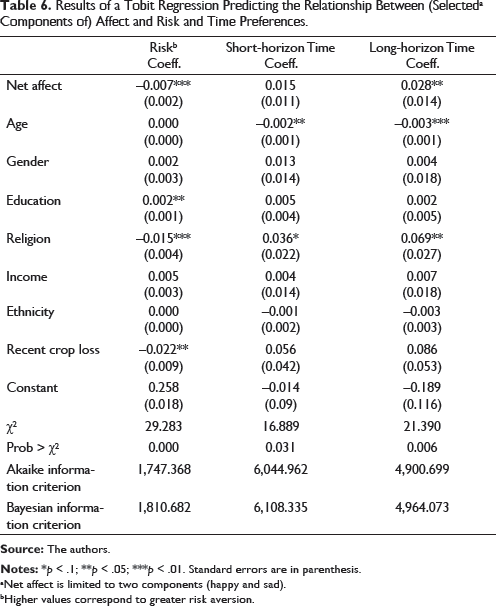

Results of a Tobit Regression Predicting the Relationship Between (Selecteda Components of) Affect and Risk and Time Preferences.

aNet affect is limited to two components (happy and sad).

bHigher values correspond to greater risk aversion.

Discussion

The study investigated whether affect shapes farmers’ risk and time preferences. We hypothesized that an overall pleasant state, that is, when net affect is positive, the likelihood of risk-taking increases. Our findings strengthen what is known about the affect-infusion model—that a person in happy mood tends to take more risks. The current research finding is complementary to research by Chou et al. (2007) and Grable and Roszkowski (2008). Notably, economic utility theory postulates that people act rationally when faced with trade-offs on risk and return, thus the response to a questionnaire or experiment should not be subject to the mood of respondents. However, the results in this paper suggest that this hypothesis may not be true in its entirety. We show that risk-taking is determined in part by a short-term affective state.

Regarding our findings on time preferences, the effect of positive affect on time preference has previously been reported in Ifcher and Zarghamee (2011) where they also find that positive affect significantly reduces preference for present over the future utility of money. This finding that pleasant net affect has the potential to induce patience fits within the self-control framework and lends support for the mood-as-a-resource hypothesis which suggests that positive affect enhances DM’s ability to act according to their long-term goals in lieu of short-term outcomes. In other words, this could be further evidence that DMs use positive affect as a resource in the pursuit of long-term goals.

Given the evidence that affect is instrumental to influencing risk and time preferences, we highlight the possible manner how this effect occurs. Several possibilities are discussed. One pathway in which affect influences risk attitude is more likely to be that—the recall which induces the short-term affect—may differentially make more salient various options for responding to the lottery tasks. This could also be via a passive effect in which case the attractiveness of different potential future courses of action is governed by recent short-term affect. There is the possibility that being in a net pleasant state enhances future levels of utility which makes people think more about the future. On the other hand, the possible pathways in which affect drives time preference may be that being in a pleasant state of affect acts as a substitute for receiving money immediately. This result in farmers experiencing pleasant affect being more willing to delay seeking financial rewards to a time when they may be experiencing unpleasant affect. Perhaps overall, pleasant affect increases optimism and confidence, thus making farmers more patient. A practical implication directly related to respondents in this study is that regarding innovation and technology adoption, farmers may be confident about the future in spite of the up-front investments that are involved before future returns can be obtained. However, we note that while the conclusions from the results of this study are based on aggregated affect, it is possible that differences could be observed should the consideration be on specific positive or negative affect.

Crucially, our findings demonstrate that affect is an important variable that should be considered in models of decision-making. Its understanding could help shed light on implementing solutions to important agricultural issues, for example, in the case of encouraging risky technology adoption, interventions that integrate positive mood-gaining elements to reinforce or encourage positive affect could get more favourable acceptance.

There are some limitations to our study. The data do not permit investigating the effect of long-term affect on risk and time preferences. Also, given that respondents reported affect on a scale, there is no guarantee that the response of one individual regarding the intensity of a particular feeling is equivalent to that of the other respondents. Further, although the questions on the risk and time preferences are preceded by those measuring affect, subjects were asked to recall their activities and experiences of the day prior to the interview as a general part of the survey. 5 A direct ‘manipulation’ to prime subject’s affect may yield more reliable results. In the literature, there are concerns regarding the adequacy of using self-reports in the assessment of positive and negative affects. We used a higher number of negative affects compared to positive affects. In the case where subjects treat all negative and positive affects as part of two groups and are subject to partitioning effect, it results in the reported average value for positive affect being higher than otherwise. Finally, our adoption of a single score for net affect is arguably likely to over-simplify the phenomenon and makes a limited contribution to empirical evidence whether positive affect is the direct opposite of or is independent of negative affect.

Conclusion

In decision-making research, there are existing gaps in our understanding of the role affect plays at the time of decision-making. Specifically, the nature of the aggregate effect of affect on risk and time preferences has not gained as much attention. In this paper, we examine the influence of affect on risk and time preferences. Our results showed it is likely that with increased pleasant affect, willingness to take risk will increase significantly. The results also suggest that pleasant net affect is associated with increased odds that farmers will choose future rewards in the long horizon. This paper provides useful evidence that examining this previously overlooked relationship could shed light on our understanding of the contribution of affect to real-world economic decision-making. Although the results are obtained from estimating data of farmers in Indonesia, the methods employed could be easily applied to other subjects worldwide and still retain relevance. In concluding, we highlight some potential aspects for future research that will deepen understanding of the relationship between affect and real-world decisions making. Future studies could investigate affect by expanding the list of affective items from the few positive or negative affects predominantly examined. There is also scope for future studies to consider simultaneously the frequencies of affect alongside the intensities of affect.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.