Abstract

Heavy share buyback years after the global finance crisis 2008–2009 drew criticism from scholars and financial press that share repurchases were being used by firms to manipulate their stock prices. This paper examines whether a greater firm’s repurchase intensity distorts stock prices reflecting to information. We analyse 2 sets of unbalanced panel data that contain a sample of 337 US and another sample of 167 Malaysian repurchasing firms between 2012 and 2016. Contrary to the criticism, we find that a greater firms’ share buyback intensity in the USA stimulates faster incorporation of information in price and results in more efficient stock prices. The main findings hold true and are robust when an alternative measure of share repurchase intensity was used. The findings of US sample support the notion that share repurchase serves as a signalling tool and price support to promote more efficient stock prices. We also find no strong evidence supporting the notion that shares repurchased by Malaysian firms distort stock prices.

Keywords

Introduction

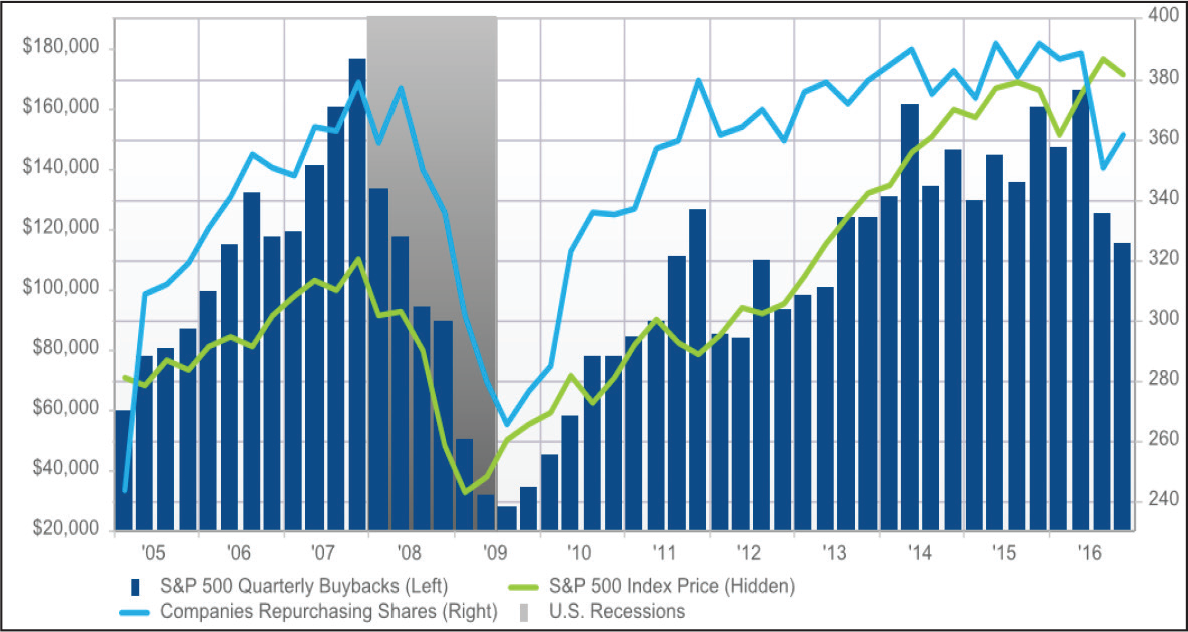

Since the US subprime mortgage crisis and the European financial crisis, stock buyback has hit a new high record, and this buyback frenzy has drawn market attention. A zero interest rate policy implemented by the US Federal Reserve aftermath of the US financial crisis till the end of 2015 to stimulate economic growth. The interest rate hovered at or close to zero between 2012 and 2016. In a zero or low interest environment where cost of debt is a cheaper source of financing, firms tend to restructure their capital structure via share repurchases and share repurchases continue to flourish. The dollar amount of share repurchases could increase by 20% reaching US$700 billion in 2016, as estimated by Goldman Sachs analyst David Kostin (Derousseau, 2017). There was a continuing surge in dollar spent and number of shares repurchased by S&P 500 companies quarter-over-quarter since 2012, as shown in Figure 1. In fact, the total dollars spent in share repurchases in the post-crisis period were substantially more than that in the pre-crisis period. Hundreds of billions of dollar spent in share repurchases were commonly viewed by some practitioners and scholars as distributing some part of firm earnings to shareholders. This motive is criticized by some scholars, and business and financial press. The concern was addressed by Professor Lazonick in The Harvard Business Review during the buyback frenzy that financial capital could have been invested in innovation and job creation, and he also argued that firms have incentives to manipulate their share prices (Lazonick, 2014). Following criticism made in other business and financial press that is an expensive tool used by managers to manipulate the stock price and secure their equity based compensation

Managers use share repurchases to signal or convey information (Babenko et al., 2012; Lee & Mauck, 2018; Leng & Noronha, 2013). These studies documented the signalling effect and information content of share repurchases that promote more incorporation of information into share prices. Their findings suggest that the subsequent actual share repurchases will facilitate markets to reveal the information managers intend to convey; as such, it leads to a greater incorporation of information into share prices and share prices will adjust over times. A recent study documented that share repurchases may give false signal to mislead investors (Li et al., 2019). Busch and Obernberger (2017) investigate whether intensity of share repurchases causes price delay for US repurchasing firms, and its sample period covers the period from 2004 to 2010. Under the environment of zero interest rate where firms’ share repurchases were rampant in the USA, it is intriguing to investigate whether share repurchase distort share price between 2012 and 2016.

This paper uses two sets of research samples, a sample of 337 US repurchasing firms and another sample of 167 Malaysian (MY) repurchasing firms; they are public listed firms selected from their respective stock exchanges. These two countries are selected due to their distinctive differences in terms of market size, level of market efficiency, and repurchase rule and regulation. The US stock market is larger and more efficient than MY stock market. In addition to that, both nations are subject to different rules and regulations in share buyback; for instance, under the US Securities Exchange Commission (SEC) Rule 10b-18, firms can buy back their shares not more than 25% of daily trading volumes, while MY firms are permitted to buy back a maximum of 10% of the number of shares outstanding. Such context will potentially contribute more insight as to how share repurchases affect stock price efficiency in different contexts. Unbalanced quarterly data are used to examine whether firm’s share repurchases distort stock price. We use actual repurchased shares to compute share repurchase intensity (REP) by taking actual repurchased shares divided by number of shares outstanding. We also use an alternative measure of share repurchase intensity, that is, (RTVOL), a ratio of actual repurchased shares divided by trading volume, for robustness test. We compute price delay after firm’s share repurchase, which is an inverse measure for stock price efficiency. Two measures of price delay (DELAY) and coefficient-based delay (C.DELAY) are adopted from past studies (Busch & Obernberger, 2017; Hou & Moskowitz, 2005) to inversely measure stock price efficiency.

This research found that greater repurchase intensity has a negative effect on price delay post-actual repurchase (in order words, greater share repurchase intensity promotes more efficient stock price), which is consistent with past research findings. Particularly, effect of share repurchases on price efficiency found in the US repurchasing firms. This finding provides evidence to the fact that share repurchases promote and facilitate more efficient stock price for the US repurchasing firms. In conjunction to documented literature, the empirical evidence supports the notion that share repurchase could be used by managers: (a) to signal new information and incorporate new information in stock prices and (b) to provide price support at fundamental price. Thus, the finding rejects the notion that stock price manipulation is caused by share repurchases.

This work contributes to the literature in three ways. First, it contributes to the debate around the price manipulation via share repurchases, since criticisms made by some scholars and financial press on massive dollar amount spent in firm’s share repurchases and market participants are sceptical on claim. Second, this study helps us to understand whether the extent of firm’s share repurchases has an impact on stock price efficiency. We find that in case of US firms with greater repurchase intensity, their share prices tend to experience less delay in later period. Hence, the findings provide evidence that share price is more efficient post-share repurchases and yet rejects price manipulation. Third, this study uses a sample period of 2012-216, which is a period of buyback frenzy in a zero interest rate environment in the US, and also provide comparison in findings between the US and the Malaysia.

The remainder of this paper is organized as follows: in the second section, we discuss the association between share repurchases and price efficiency. We describe our sample and data and define our models and variables in the third section. Our results are presented in the fourth section. We conclude in the sixth section.

Theoretical Review

Stock Price Manipulation

Equity compensation received by managers such as equity ownership and employee stock option spur managers to use share repurchases to deliberately increase the stock price above its fundamental value. Numerous articles in the business and financial press criticized share buybacks for being used by managers as a costly tool to manipulate the stock price which boosts stock price in the short-term; however, they destroy shareholders value (Alsin, 2017; Ausick, 2017; Byrne, 2017; Dohmen, 2017; Gandel, 2017). Past empirical findings support the argument that managers deliberately try to alter the stock price to increase their compensation (Babenko, 2009; Bonaime & Ryngaert, 2013; Fenn & Liang, 2001).

Nevertheless, rules and regulations adopted by government and stock exchange curb price manipulation; for example, SEC Rule 10b-18 (U.S. Securities and Exchange Commission, 2004) safe harbour provision allows repurchasing firms to repurchase their shares provided the firms conduct repurchases in accordance with the rule’s ‘manner, timing, price, and volume’ conditions. Furthermore, SEC Rule 10b-5 (U.S. Securities and Exchange Commission, n.d.) in the USA prohibits firms and insiders from trading in the firm’s shares while in possession of non-public information which has material effect on the price or value of stock. Fried (2005) addressed false signalling that mislead investors and propose new regulations to govern firm’s open market repurchases. Chan et al.'s (2010) empirical result finds that only a limited number of managers potentially use repurchase announcements to mislead investors. Hence, the argument of price manipulation against the use of stock repurchases deserves research attention.

Market Inefficiency and Imperfection

Under the efficient-market hypothesis (EMH) developed by Fama (1970), a market is efficient when stock prices reflect all available information. However, the relationship between the information diffusion speed and market frictions discussed in literature conform with market imperfection theories such as (a) limited participation in stock market (Basak & Cuoco, 1998; Shapiro, 2002) and (b) neglected firms or small firms (Ellouz, 2011; Hou, 2007). They argue that lack of institutional holding, higher transactions costs, and higher cost in information set-up can diminish the process of information incorporation for less visible, segmented firms. Peng (2005) showed that constraints on the amount of information investors possess can interrupt asset price responsive to news and firm announcements.

Reasons for markets’ possible inefficiency or delayed prices’ responses to event announcements are stocks with lack of liquidity (Hou & Moskowitz, 2005) and inattentive investors (Titan, 2015), which possibly cause a delay in stock price reaction or under-reaction. Hence, price inefficiency could be attributed to illiquid stock trading in stock market. Shares of a larger firm with a higher stock liquidity are more efficient in pricing, while shares with greater bid-ask spreads tend to have less efficient price (Saffi & Sigurdsson, 2011). Stocks with small firm size and high volatility respond to good news much more slowly than to bad news (Mcqueen et al., 1996). Stock prices react slowly to common factors yet overreact to firm-specific information and the sluggish reactions to common factors drive increase to the lead-lag effect in stock returns (Jegadeesh & Titman, 1995). Since inefficient price is caused by market imperfection, it is intriguing to look at whether share repurchases would promote more efficient price. This would imply that managerial share repurchase could contribute to more efficient price.

Share Repurchase Intensity and Stock Price Efficiency

An increase in share repurchases could attract institutional investors (Jain, 2007). Busch and Obernberger (2017) further claimed that share repurchases can attract the investors’ attention towards neglected stock. More public and stock analysts’ attention can promote stock price efficiency. The placement of a market order by the firm directly incorporate the positive market information (Busch & Obernberger, 2017). Fu and Huang (2015) found that disappearance of long-run abnormal returns in post event of repurchase is a reflection of stock price efficiency. Past researches find that share repurchases will improve the speed of incorporating new positive information into the stock price (Busch & Obernberger, 2017; Hou & Moskowitz, 2005) and improve the accuracy of the stock price by providing price support at fundamental values (Brav et al., 2005; Busch & Obernberger, 2017; Dittmar, 2000). The existing literature acknowledges signalling effect and price support of share repurchases, but the question of whether share repurchases rejuvenate price reflection to information, requires more empirical evidence.

Signalling Effect of Share Repurchase

Share repurchases can serve as a means for communicating and conveying information to shareholders, as clarified in literature (Huang, 2015; McNally, 1999; Vermaelen, 1981). They suggested that investors perceive share repurchases as signals of stock undervaluation and management’s assessment of a company’s performance and prospects. Findings of past empirical research confirmed signalling effect of stock repurchase by relating to informed trading, thereby providing the researchers some clues on how firm’s stock repurchase contributes to stock price efficiency. As such, Barclay and Smith (1988) and Franz et al. (1995) found that the decline in bid-ask spread is due to a decrease in informed trading risk related with the announcements of open market repurchase. In most cases, insider trading and firm stock repurchases are due to stock undervaluation, although insider trading behavior prior to stock repurchases announcement is useful to confirm undervaluation signal, particularly for unvalued firm. (Chan et al., 2012).

The share repurchase may also engender an influence on the information content of shares, as determined by positive price reaction. In some prominent studies, their research findings showed positive market reaction to repurchase programme announcements, and they often associate their findings consistent to information signalling (Babenko et al., 2012; Ikenberry et al., 1995; Zhang, 2005). The initial repurchase announcement was likely to significantly reduce any information asymmetries, signal higher information content and higher market reaction than subsequent repurchase announcements (Andriosopoulos & Lasfer, 2015). In a similar vein, abnormal returns were found to be larger when the repurchase programme was initiated by firms for the first or the second time, thus, indicating that the information content in these announcements is perceived to be more valuable than that in a regular use of repurchase programmes (Högholm & Högholm, 2017). Some research findings suggest that stock market may not fully discover all information that managers intend to convey via share repurchase; the market will further interpret the information and incorporate the information in stock price in subsequent actual share repurchases (Babenko et al., 2012; Lee & Mauck, 2018; Leng & Noronha, 2013). Therefore, if firms are genuinely using share repurchase to signal information, it would promote greater efficiency in price discovery.

Price Support

Another possible reason for repurchase effect on stock price efficiency is that firms buyback their shares to provide price support. Recent empirical research find that share repurchase enhances the accuracy of the stock price by providing price support at fundamental values (Busch & Obernberger, 2017; Dittmar & Field, 2015; Liu & Swanson, 2016). Even though firms do not commit to purchase their shares after announcement of open market repurchases, it attracts scrutiny from speculators, and the presence of abnormal returns surrounding the announcement documented in existing literature (Bhattacharya & Jacobsen, 2015) indicates the amount of mispricing being corrected by speculators to subsequently discover the true value of the firm.

Methodology

Data and Sample

This study analyses two research samples which comprise a sample of 337 US and another sample of 167 MY repurchasing firms. They are public listed firms which bought back their shares from open market. Those firms announcing repurchase but do not have actual share buyback are excluded from the samples. In line with most repurchase research, financial and utility companies, foreign companies, exchange traded funds, closed-end funds, and real estate investment trusts (REITs) are excluded from the sample due to volatility of data variables, different fundamental and capital structure from that of other firms, and regulatory factors that affect financial and utilities firms (Bonaime et al., 2014; Huang, 2015; Mietzner, 2017). Firms that experience stock split, reverse splits, stock dividends, spin-offs, and right issue are excluded. Number of shares repurchased from open market are collected from the Bloomberg financial database. Lastly, complications related to thinly traded, illiquid stocks and tiny buyback volume are excluded from the research sample. A 5-year unbalance panel data in quarterly from 2012 to 2016 is used.

Econometric Model

Following past research, appropriate lag length for repurchase intensity is applied, and the relationship between delay measure and lagged share repurchase is expected to be negative (Busch & Obernberger, 2017; Hou & Moskowitz, 2005).

where

F denotes price efficiency and it is inversely measured by price delay;

REP denotes share repurchase intensity;

SIZE refers to firm size measured by its market capitalization;

PB represents price–book ratio;

INSTI denotes institutional holding;

ANALYST represents number of analysts covering the stock;

TVOL refers to trading volume;

VOL denotes volatility of stock return;

PSR denotes positive stock return; and

NSR refers to negative stock return.

Share Repurchase Intensity

REP measures the extent to which firms repurchase their shares from open market, using a ratio of number of repurchased shares to number of shares outstanding. We also use an alternative of repurchase intensity measure, that is, a ratio of number of repurchased shares to trading volume (RTVOL), to test for robustness of finding. Since number of shares repurchased from the open market is a fraction of trading volume, the rationale of using this measure is to gauge intensity by taking the amount of share repurchased against the trading volume. Using REP and RTVOL to measure REP is in line with past research (Busch & Obernberger, 2017).

Measure of Stock Price Efficiency

Delay Measure

The delay measure quantifies speed and accuracy of new information incorporated into prices by assessing whether lagged returns in an extended market model (Equation 3) have higher explanatory power than a simple market model (Equation 2). Both Equations (2) and (3) are estimated using 60 daily returns, in line with past researches (Boubaker et al., 2014; Busch & Obernberger, 2017; Vo, 2017). Therefore, the following models for each firm and each month are estimated:

where r i,t represents return of firm i on day t; r m,t represents market return on day t; and r m,t-n denotes market return n days prior to day t.

If all new information instantly incorporated into a firm’s stock price, that price incorporation is accounted for by the coefficients of contemporary market returns, and the coefficients of the lagged market returns equals to 0 since there is no price delay. Nevertheless, if there is a delay in incorporation of new information into price, the coefficient for the lagged market returns (βin) is different from zero, and consequently, the extended market model will have more explanatory power than the base model.

Delay and coefficient-based delay adopted from Busch and Obernberger (2017) and Hou and Moskowitz (2005) are inverse measures of stock price efficiency. The 1st delay measure is the ratio of the R-squared estimates of the two models:

where R2base denotes R-square for the baseline regression, and R2extended represents R-square for the extended regression. The greater degree of stock price efficiency indicates quicker new information incorporated into stock prices and the smaller the discrepancy in explanatory power between the base model and the extended market model. Hence, the 1st delay measure will decrease when stock price efficiency increases and vice versa.

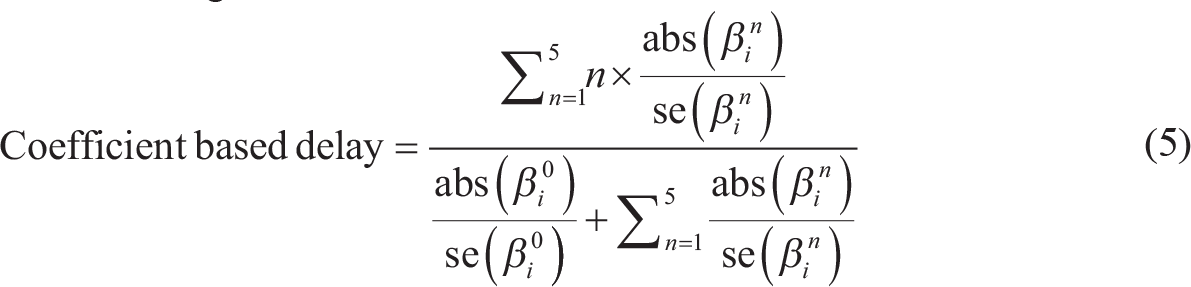

Coefficient-based Delay

The 2nd delay measure is constructed based on the coefficients of the two regressions from Equations (2) and (3). The coefficient-based delay measure is computed as per the Equation (5), the ratio of the lag-weighted sum of the absolute coefficients of the lagged market returns (numerator) relative to the sum of all coefficients (denominator), scaled by the standard errors of the coefficients, as shown in the following:

Where abs (βin) denotes the absolute (abs) coefficients; se (βin) represents standard error coefficients. Likewise, coefficient-based delay also shows reduction with greater efficiency of stock price and indicates faster information incorporation, as the lagged market returns deteriorate its explanatory power towards stock return.

Control Variables

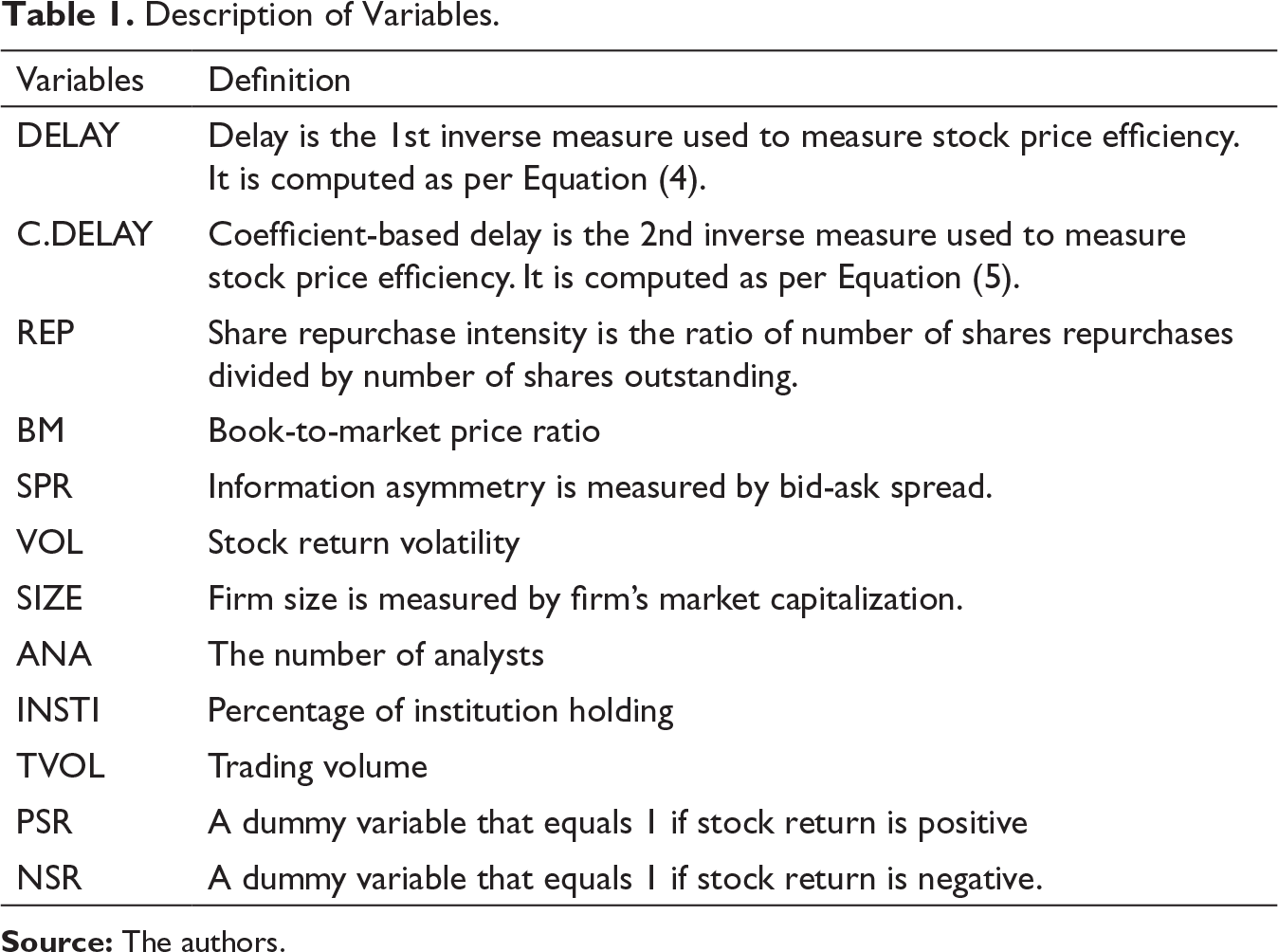

Description of Variables.

Finding and Discussion

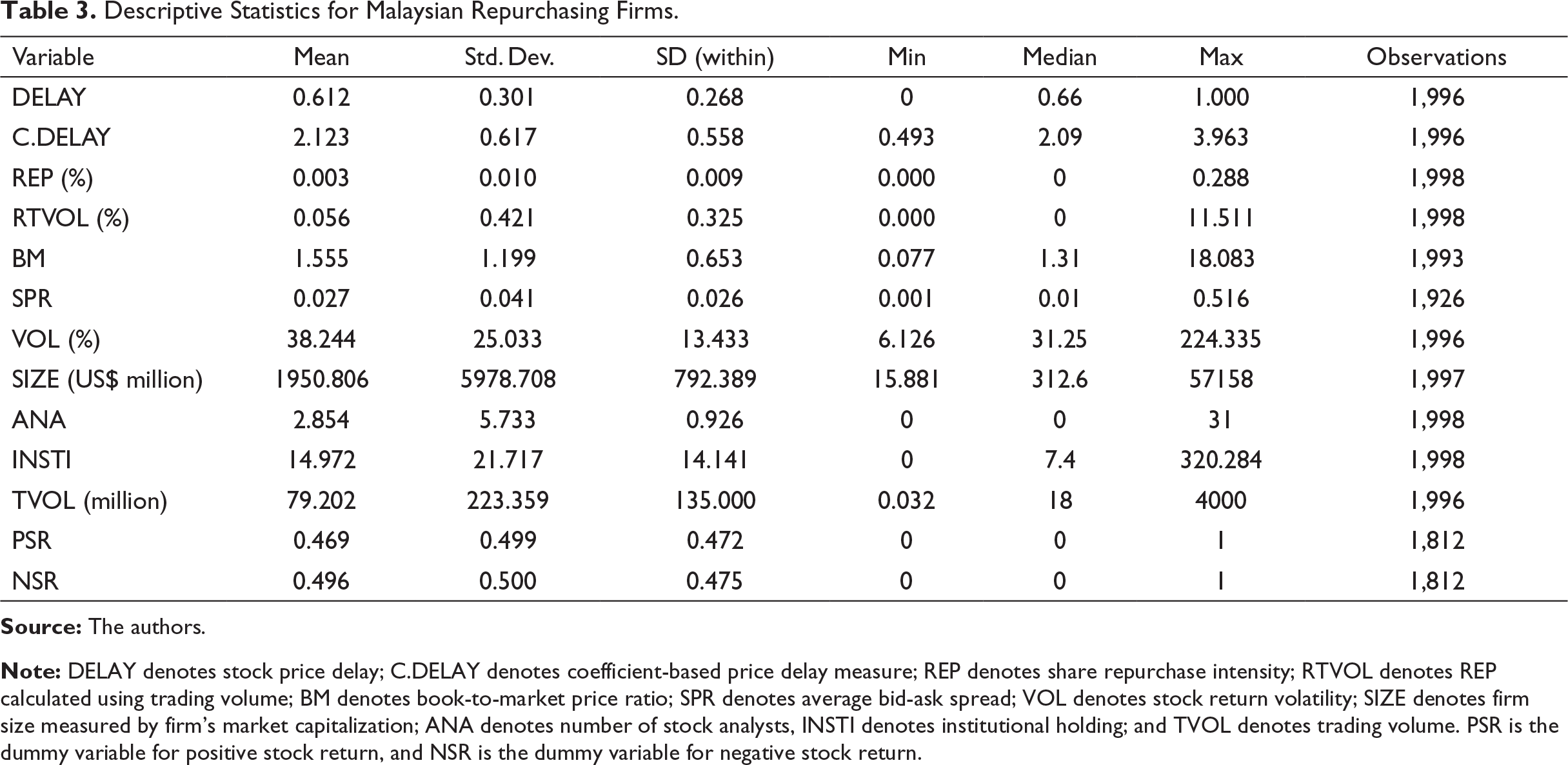

Descriptive Statistic and Mean Comparison Analysis

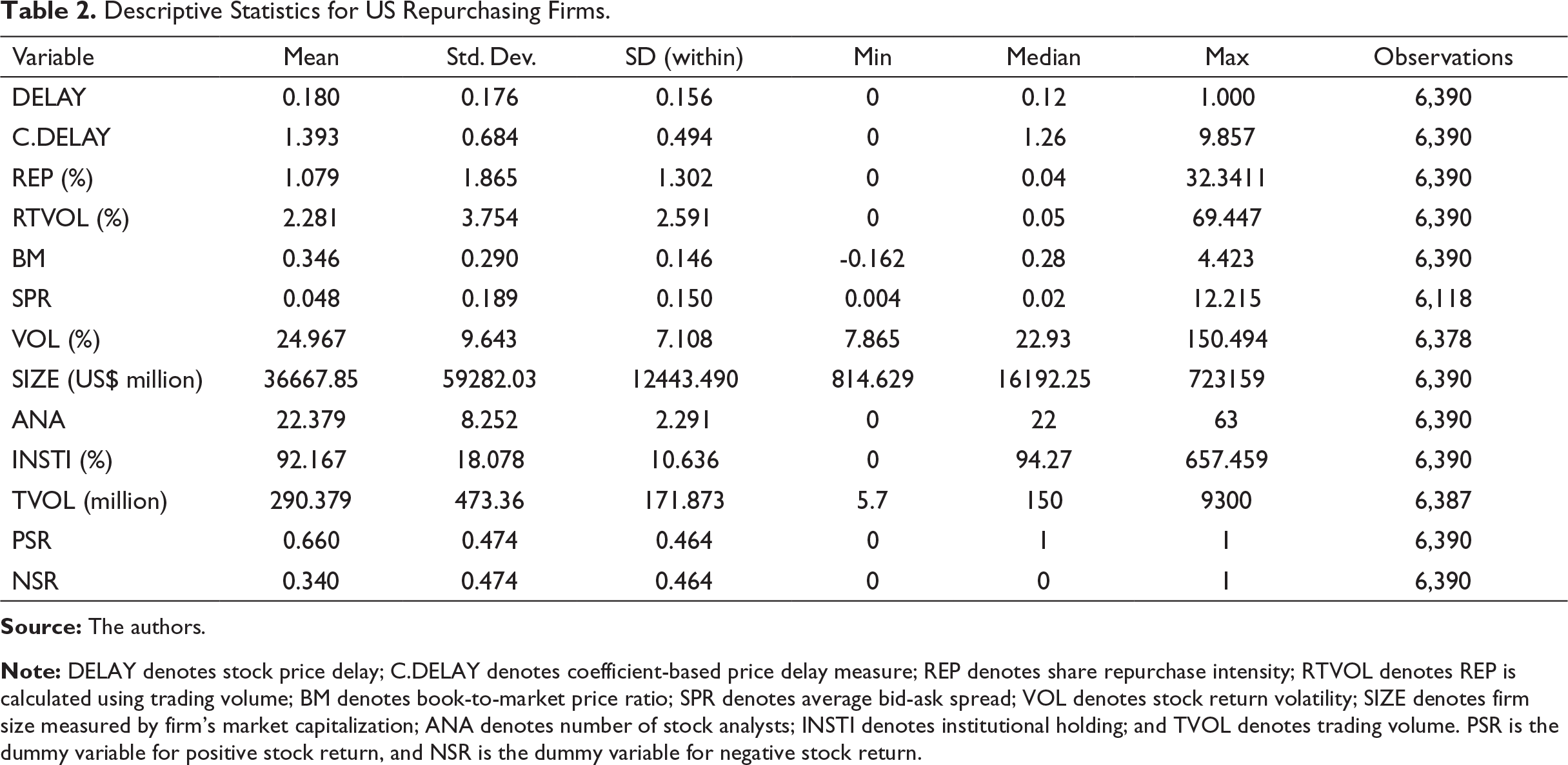

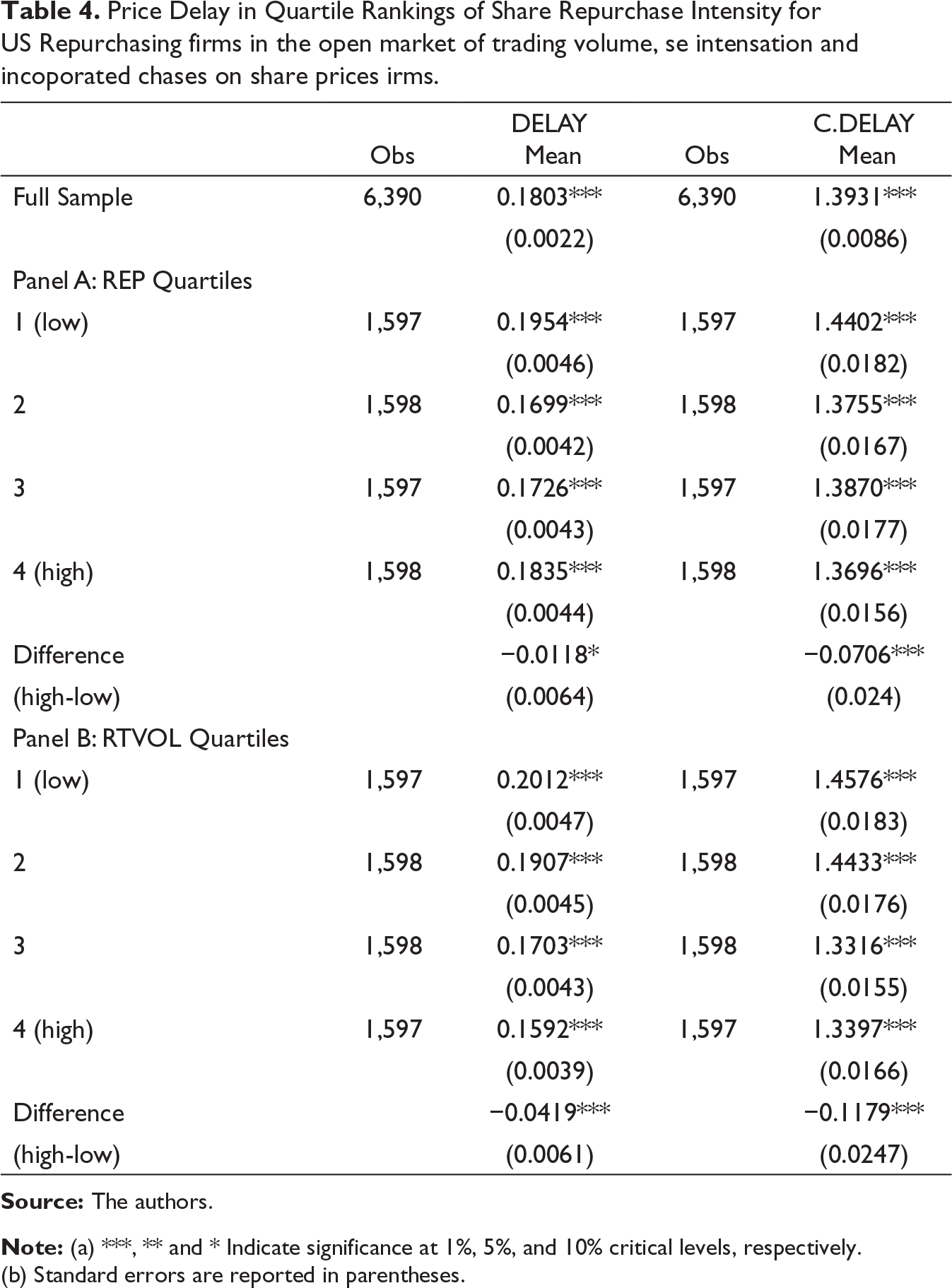

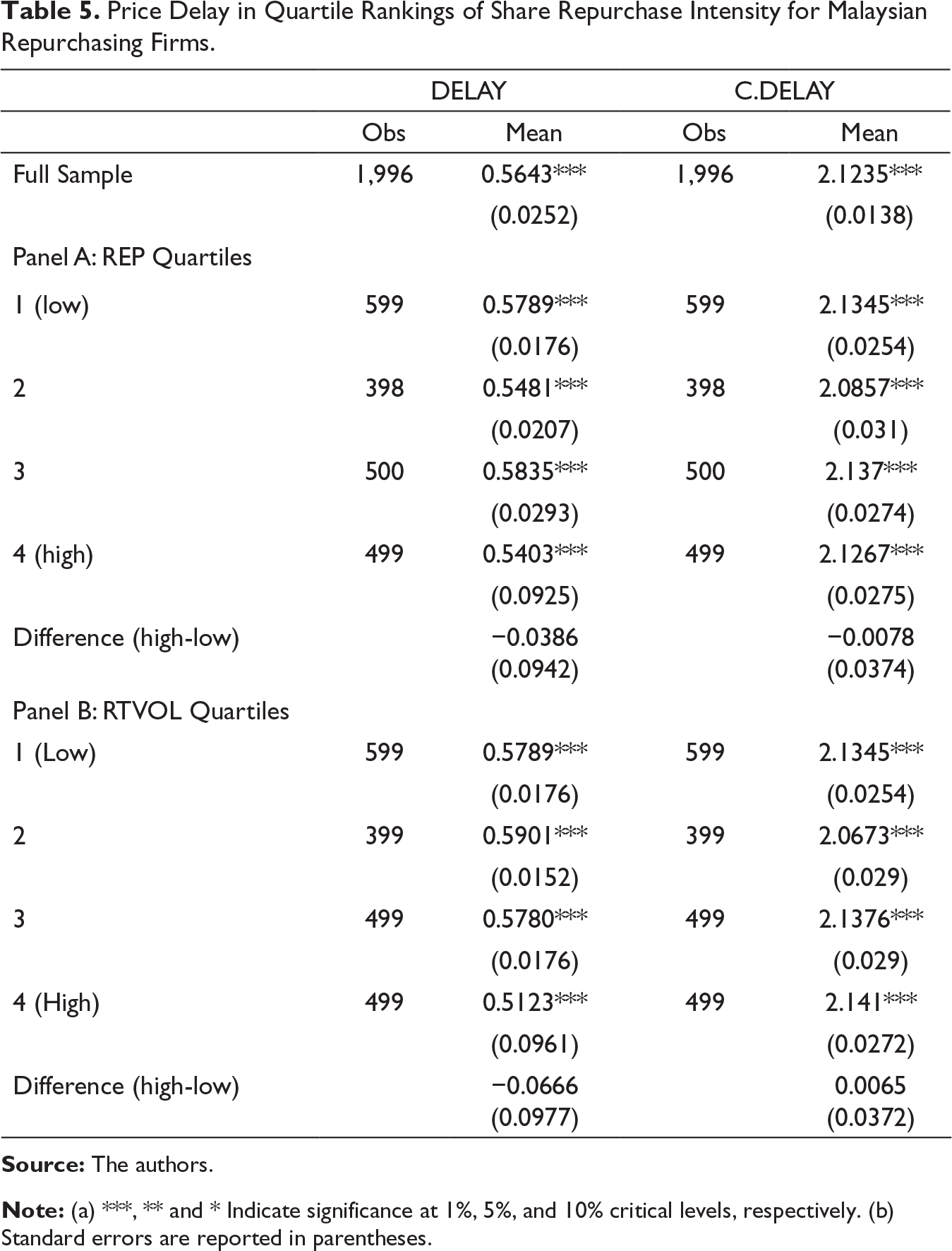

Descriptive statistics are presented in Tables 2 and 3. In Table 4, US repurchasing firms experienced price delay after their share repurchases on an average of about 0.18 for DELAY and 1.39 for C.DELAY. In panels A and B, the US repurchasing firms which were ranked the highest quartile of REP experienced significant lower price delay than those that were ranked the lowest quartile. Furthermore, a significant mean difference in price delay between the highest and the lowest quartiles was found in Table 4. Similar results were found by employing the second measure of price delay (C.DELAY) in Table 5.

Descriptive Statistics for US Repurchasing Firms.

Note: DELAY denotes stock price delay; C.DELAY denotes coefficient-based price delay measure; REP denotes share repurchase intensity; RTVOL denotes REP is calculated using trading volume; BM denotes book-to-market price ratio; SPR denotes average bid-ask spread; VOL denotes stock return volatility; SIZE denotes firm size measured by firm’s market capitalization; ANA denotes number of stock analysts; INSTI denotes institutional holding; and TVOL denotes trading volume. PSR is the dummy variable for positive stock return, and NSR is the dummy variable for negative stock return.

Descriptive Statistics for Malaysian Repurchasing Firms.

Note: DELAY denotes stock price delay; C.DELAY denotes coefficient-based price delay measure; REP denotes share repurchase intensity; RTVOL denotes REP calculated using trading volume; BM denotes book-to-market price ratio; SPR denotes average bid-ask spread; VOL denotes stock return volatility; SIZE denotes firm size measured by firm’s market capitalization; ANA denotes number of stock analysts, INSTI denotes institutional holding; and TVOL denotes trading volume. PSR is the dummy variable for positive stock return, and NSR is the dummy variable for negative stock return.

Price Delay in Quartile Rankings of Share Repurchase Intensity for US Repurchasing firms in the open market of trading volume, se intensation and incoporated chases on share prices irms.

Note: (a) ***, ** and * Indicate significance at 1%, 5%, and 10% critical levels, respectively. (b) Standard errors are reported in parentheses.

Price Delay in Quartile Rankings of Share Repurchase Intensity for Malaysian Repurchasing Firms.

Note: (a) ***, ** and * Indicate significance at 1%, 5%, and 10% critical levels, respectively. (b) Standard errors are reported in parentheses.

Panel Regression Analysis

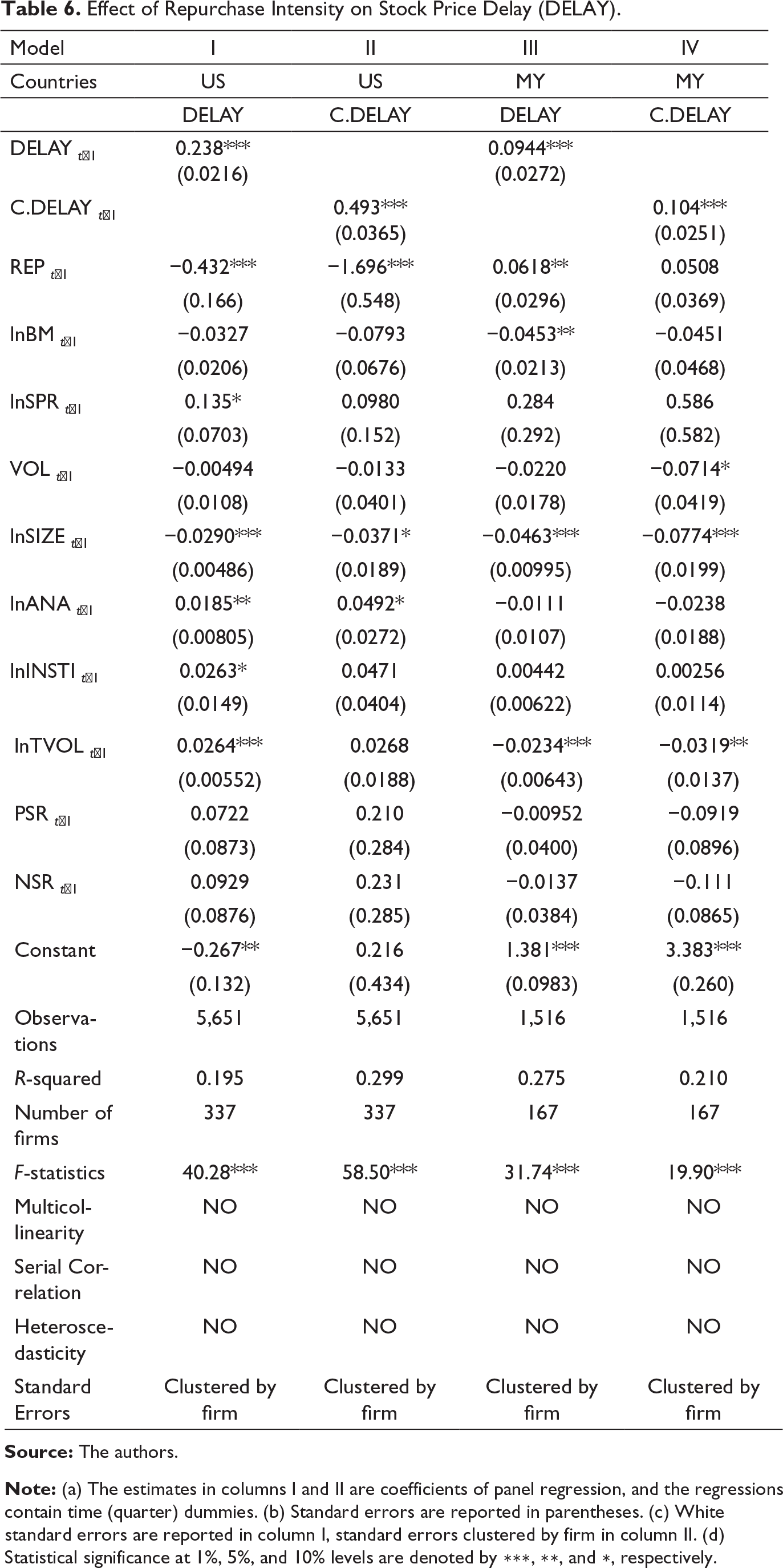

Validated by both Breusch Pagan Lagrange Multiplier test and Hausman test, there is a presence of fixed effect in the panel data. Time dummies and standard errors clustered by firms are applied in fixed effect models to accommodate heterogeneity across time and firms. Repurchase intensity has a significant negative effect on price efficiency found in US firms for both measures of price efficiency, as presented in Table 6. A one-within-standard-deviation (0.01302) increase in repurchase intensity (REP) caused a decrease in the price delay by 0.56% (0.01302 × −0.432 = −0.0056 where −0.432 is the coefficient of REP from Model I of Table 6), which corresponds to 4.67% of median DELAY (−0.0056/0.12 = −0.0467 where 0.12 is the median of DELAY obtained from Table 2). A similar effect of REP on coefficient-based delay (C.DELAY) is found in Model II of Table 6 which reports a decrease of C.DELAY by 2.21% due to an increase of one-within-firm standard deviation in REP. 1 For MY repurchasing firms, the share price (DELAY) was delayed by 0.0006% due to a one-within-standard-deviation (0.00009) increase in repurchase intensity, which corresponds to 0.0009% of DELAY median. 2 The positive impact of REP on DELAY is rather marginal, merely caused by slight price distortion. This result was not further confirmed with coefficient-based delay (C.Delay), as presented in Model IV.

Robustness Test

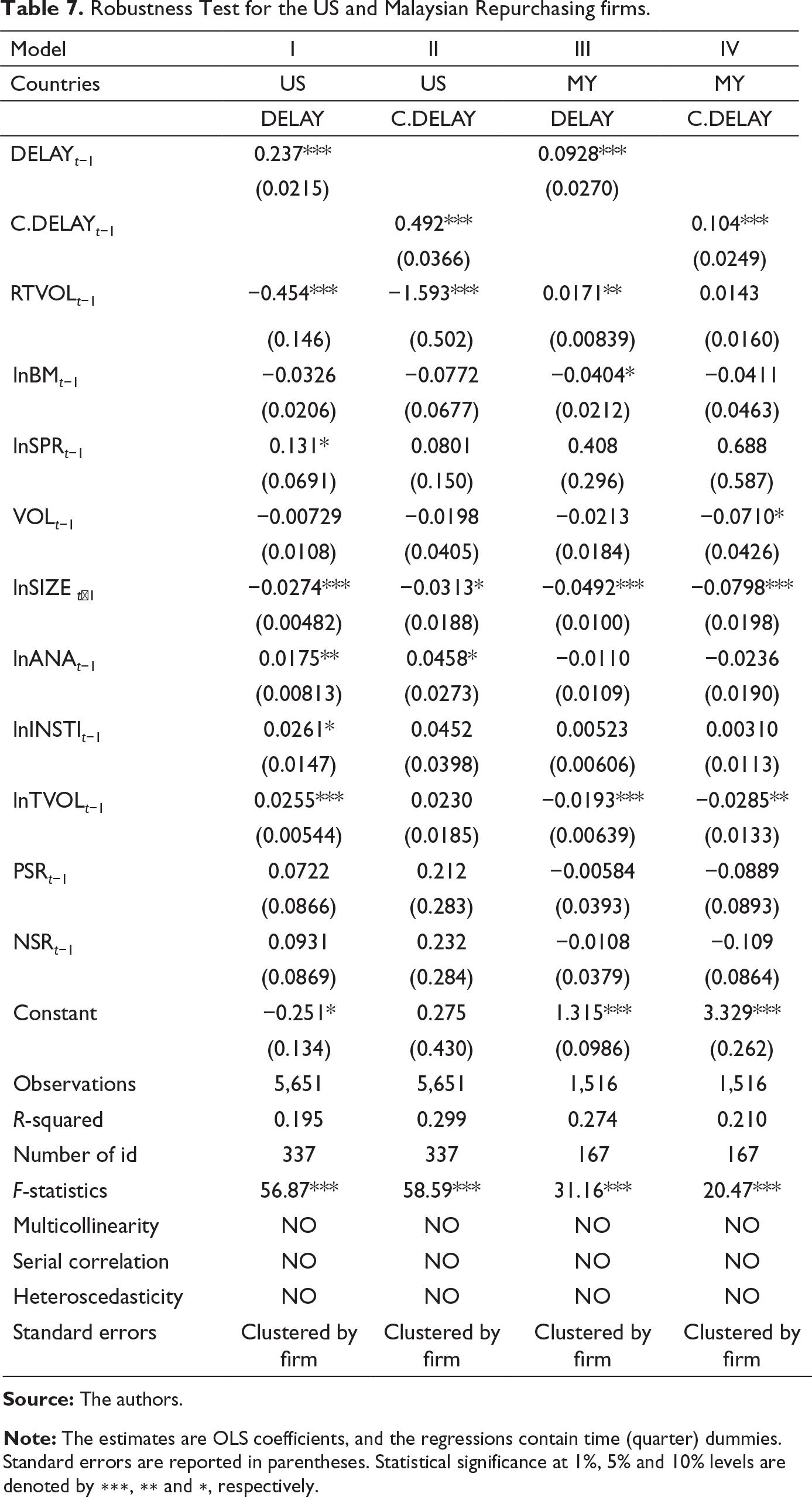

RTVOL, which is the ratio of number of shares repurchased to trading volume, is an alternative measure of REP adopted to examine its impact on stock price efficiency to ensure robustness of the main findings found in the earlier section. Negative effect of share repurchase on price delay in the US repurchasing firms is more pronounced and further confirmed. In Table 7, Model I shows that a one-within-standard-deviation (0.0259) increase in RTVOL is associated with a 1.17% decline in price delay (DELAY). 3 In addition, Model II reports a reduction of C.DELAY by 4.12% due to a one-within-firm-standard-deviation increase in RTVOL. 4

In line with the main results, both findings conclude that firm’s share repurchases cause less price distortion and, thus, promote more efficient stock price.

Since both delay and coefficient-based delay are inverse measures to stock price efficiency, the negative relationship found in US repurchasing firms indicates that more repurchase intensity causes less price delay (or more efficient stock price). Consistent to the past research findings (Busch & Obernberger, 2017; Hou & Moskowitz, 2005), a greater firm buyback intensity will result in more efficient stock price post-actual repurchase quarter. This finding rejects the notion that firm or manager manipulates stock price. Private information signaling via open market stock repurchase could influence stock trading among investors. Consequently, the signalling power will translate to more informed trading among traders. As such, the results support empirical evidence of informed trading documented in literature that informed trading: facilitates stock prices to converge to true values (Bloomfield et al., 2007); causes greater market efficiency (Sung et al., 2016); reduces the deviations from the fundamentals (Blasco & Corredor, 2017). This findings holds the view that stock repurchases improve new information incorporated in stock price via its signalling effect and provide price support at the fundamental value, that is consistent to the arguments from the literature.

A slight price distortion (DELAY) post-actual repurchase was found in MY repurchasing firms, as reported in Model III of Table 7. An increase of DELAY by 0.0056% was observed due to a one-within-standard-deviation increase in RTVOL. 5 Nevertheless, that result is not confirmed with the coefficient-based delay. By combining results from the main estimation and the robustness test, we were unable to draw a concrete conclusion that firm’s share repurchases caused price distortion for MY repurchasing firms. A possible explanation to this finding is that a low repurchase intensity does not seem to contribute efficiency in price discovery. The average repurchase intensity of the MY repurchasing firms is lower than that of the US repurchasing firms, as indicated in descriptive statistic provided in Tables 2 and 3.

Regarding the impact of control variables on price delay, we find that large firm (lnSIZE) experienced a reduction in price delay for both US and MY repurchasing firms, as reported in Table 6. That finding indicates that stock prices of large firms tend to be more responsive to current information than that of small firms. Share prices of large firms reflect faster to new information than do the share prices of small firms, as found in Hou’s (2007) study. Stock price of large firm tends to be more efficient, partly due to the fact that small firms display the highest degree of information asymmetry in their risk compared to large firms (Perez-quiros & Timmermann, 2000).

Apart from that, stock prices of US repurchasing firms with larger trading volume (lnTVOL) and severe information asymmetry (lnSPR) tend to experience an increase in price delay (DELAY) of 13.5% and 2.64%, respectively. Trading volume is closely related to informational differences (information asymmetry) as higher trading volume could be a result of differential prior disclosure information or differential interpretation on information (Bamber & Barron, 2011; Chae, 2005). This could possibly explain why prices of heavy traded stocks and stocks experiencing greater bid-ask spread do not tend to efficiently reflect information. For MY repurchasing firms, higher trading volume tends to reduce price delay.

Effect of Repurchase Intensity on Stock Price Delay (DELAY).

Note: (a) The estimates in columns I and II are coefficients of panel regression, and the regressions contain time (quarter) dummies. (b) Standard errors are reported in parentheses. (c) White standard errors are reported in column I, standard errors clustered by firm in column II. (d) Statistical significance at 1%, 5%, and 10% levels are denoted by ∗∗∗, ∗∗, and ∗, respectively.

Robustness Test for the US and Malaysian Repurchasing firms.

Note: The estimates are OLS coefficients, and the regressions contain time (quarter) dummies. Standard errors are reported in parentheses. Statistical significance at 1%, 5% and 10% levels are denoted by ∗∗∗, ∗∗ and ∗, respectively.

Conclusion and Implication

Massive dollar spent by US firms in their share repurchases has drawn criticism from some scholars and financial press that firms manipulate stock price via their share repurchases. This motivates the researchers to investigate whether a greater intensity in firm’s share repurchases has an impact on price delay. For the data analysis, we analyse 2 samples, which are 337 US and 167 MY repurchasing firms, for a data period from year 2012 to 2016. Two inverse measures of stock price efficiency are adopted, which are price delay (DELAY) and coefficient-based delay (C.DELAY). We find that negative effect of share repurchases on both DELAY and C.DELAY are found in US repurchasing firms. However, we do not find concrete evidence that shares repurchased by MY firms distort their share prices

We use a ratio of number of repurchased shares to number of shares traded (RTVOL) as an alternative measure of REP to assess the robustness of the main finding. The same result, that is, negative effect of REP, is found on both price delay measures. The findings indicate that greater intensity of firm’s share repurchases caused less delay or distortion in a process of reflecting stock price to information. Thus, firm’s share repurchases promote better price efficiency.

The main contribution of this research is to provide additional insights and empirical evidence to existing literature that share repurchases promote efficiency in price discovery. The research findings of the US repurchasing firms are consistent with the notion that share repurchases promote incorporating new information via signalling effect and increase price accuracy by providing price support. However, the research findings do not support the argument that firms tend to manipulate their share prices using share repurchases.

Our findings have three important practical implications on how share repurchases can be used by managers: first, to ease panic selling and deep selling pressure during the downtime; second, to enhance informed trading, which is a result of information signalled by managerial share repurchases; and third, to attract investors’ attention on neglected and undervalued stock. Hence, share repurchases allow managers to take proactive measures to mitigate inefficient stock price caused by market imperfection. As regards research limitation, this study is unable to accommodate price adjustment and reaction to short-lived information post-actual share repurchases. Hence, future research can study the impact of share repurchase on high-frequency price adjustment.