Abstract

The main purpose of this research is to empirically examine the antecedents of household savings behaviour in the Metekele, Beneshangu Guzu state of Ethiopia. In this study, three broader factors (household characteristics, socio-economic variables and institutional variables) influencing savings decisions of households have been identified and examined. This study followed mixed method research design with questionnaire and in-depth interviews as the main instruments. Binary logistic regression has been mainly utilized to analyse the quantitative data. The findings revealed age, educational level, family size, number of livestock unit, income, irrigation utilization, production season, participation in non-farm activities, use of credit, training and education significantly impact savings behaviour. However, sex, religion, marital status, land ownership and expenditure were found insignificant contributors to the model. The government and concerned parties should support more for the decision to save by facilitating and undertaking training on saving options, conducting regular review and monitoring to develop a clear policy on the importance of savings specifically for households on habit of regular savings.

Keywords

Introduction

As one of the factors affecting growth, savings have been well thought out to lead developing countries on the path of development. It is a vital factor of households’ welfare in developing countries (Wieliczko et al., 2020). Saving is one of the important tools for successful well-being, compensating for times of shocks, and providing precautions to help people cope with disasters (Ansah et al., 2021). National savings are frequently viewed as a source of economic growth (Larissa et al., 2020; Lea, 2021). The higher a country’s savings rate, the more opportunities for high investments which lead to employment, industrial growth and economic development (Ribaj & Mexhuani, 2021; Zwane et al., 2016). Low-household savings have been a defining feature of the South African economy since the 1990s (Nduku, 2017; Precious & Asrat, 2014). Low savings, according to Nduku (2017), act as a roadblock to economic growth and development, putting strain on the country’s current account. The Old Mutual Investment Group’s 2017 report is based on a survey of 1,000 working South Africans in metropolitan areas about their attitude toward savings and investments. According to the findings of the survey, 15% of the income is saved, which has remained consistent since 2015. As a result, the low-savings rate combined with low-investment returns is deemed insufficient for retirement (Engelbrecht et al., 2018). Domestic savings, particularly household savings, are therefore critical to economic development. Despite the fact that South Africa’s GDP has increased over the last two decades, the country still trails emerging markets in terms of savings. It does, however, show that South Africa’s standard of living is improving, though not at the same rate as other emerging economies such as Mexico, Indonesia, Nigeria, Turkey, Brazil and China (Kempen, 2016).

Savings provide a basis for a country’s capital formation, investment and growth (Topcu et al., 2020). On the other hand, households have few other tools to smooth out unexpected variations in their income without savings (Abebe, 2017). It establishes the base for capital accumulation and promotes development of any nation. In order to move forward towards development, developing countries must improve their savings habit among people. The individual household savings play a decisive role for the national savings and economic development as the private savings eventually increase the growth of national economy. The main basis for the rise or failure of economic development in any economy is the household-savings rate.

Developing countries’ savings philosophy is also influenced by many different factors, such as insufficient financial service, inaccessibility of financial institutions, low interest rates and no or little incentive to save and insufficient income to save (Obayelu, 2012). The majority of the population has no knowledge of existing savings as they still keep most of their savings in cattle, store in grains and goods, jewellery and the highest portion of African households’ asset is stored in non-financial type of which 80% of their assets are in non-financial form. Many developing countries face a critical challenge in obtaining finance, and as a result, a number of community-based financial intermediation models, like village savings and lending associations, have been implemented to improve access to finance (Khan et al., 2020; Maliti & Mwewa, 2015). Poor households access finance mainly through informal systems in Africa, mainly in Ethiopia, such as local money lenders, traders, friends or relatives, Edirs and Ekubs (informal, group-based savings and loan associations). There is almost no access to formal financial institutions for poor households (Omar & Inaba, 2020), but nowadays government is working on extension of savings and credit cooperatives and other semi-formal micro enterprises that work to increase the public involvement into savings for transformation (Karki & Risal, 2021; Tariq et al., 2020). However, the purpose of savings for transformation is to strengthen the human, social and financial assets of the most vulnerable communities. A savings group improves the economic safety and cash-flow management of members, thereby improving flexibility to economic shocks (World Vision International, 2018). It promotes the capability for savings, cash-flow management and income smooth out. Savings group make a local pool of capital to enable households to survive during emergencies and develop income-generating activities, which contribute towards economic growth in other direction. Savings are important for preparing households for unexpected events. Accessing formal credit, safe shelter and asset generation would be impossible without savings. Undersaving has a number of important welfare consequences, according to Karlan et al. (2014), including variable consumption, low-shock resilience and foregone-profitable investments. Cronjé and Roux (2010) emphasize the importance of a country’s gross national savings in reducing its reliance on and exposure to the volatile global capital market. Cronjé and Roux (2010) report that South Africa’s savings levels are very low compared to other similar developing economies like China and India, forcing the country to rely on foreign investment to fund its future growth. Personal savings, according to the same authors, are necessary for maintaining and improving quality of life while also relieving the state of the burden of providing. Individuals with the ability to save can develop an entrepreneurial spirit.

Several factors that have been identified as important antecedents of savings behaviour in previous studies are highlighted in the discussion above. However, exogenous factors that are contextual do not always cut across the board in the same way. There is a scarcity of information on how to save in order to improve household livelihoods through increased income and asset accumulation. This study looks at the issue of savings in an attempt to address that gap. For policymakers as well as other major stakeholders and institutions, a thorough investigation of the various aspects of factors influencing household-savings behaviour is critical. It indicates that the important variables should be given due policy considerations in order to improve household savings in the area of study. The present study focuses on the antecedents of savings behaviour in Benishangul Gumuz of Ethopia. According to research, household savings play a significant role in promoting sustainable growth in both developed and developing countries due to their direct influence on the economic model. The study identifies group of factors that may have an impact on the savings patterns of low-income households in the country.

Review of Literature and Hypotheses Development

The majority of the population in developing countries, particularly in Sub-Saharan Africa, continues to live in poverty and is excluded from the development process (Kates & Dasgupta, 2007; Modi, 2019; Thurlow et al., 2019). In African households, saving is a tradition (albeit a modest one given the level of wealth) and is often done through informal channels. They frequently use informal financial mechanisms like the ‘tontine’ (pooling of funds in a sum which is redistributed alternately to the members of the group). In terms of number of applicants, Sub-Saharan Africa is still the second largest regional market. Savings mechanisms are evolving in English-speaking Africa toward more formalized village banking models with formal structures, which will improve governance and management of these groups. This has paved the way for more formal financial institutions to participate in savings collection. According to Lafourcade et al. (2005), contrary to global trends, more than 70% of reporting African Micro-finance Institutions (MFIs) offer savings as a basic financial service to clients and use it as an important source of funds for loans (Bhat & Tariq, 2020). According to Goldstein et al. (1999), contrary to popular belief, the microfinance sector in West Africa has a high level of dynamism in terms of mobilizing savings that are used not only for family or social purposes, but also to meet economic needs (Tariq & Sangmi, 2018). Anang et al. (2015) targeted the clients of the Bonzali Rural Bank in the Tolon-Kumbungu district of Northern Ghana. They identified the respondent’s age, gender and marital status as factors influencing their decision to save. Income level and educational status were not found to be significant factors in determining savings behaviour in their study. In the Ho Municipality of Ghana’s Volta Region, Mensahkla et al. (2017) investigated the determinants of savings behaviour among employees and management, customers, market, men and women of some selected financial intermediaries. They discovered that majority of the people in the Ho municipality save with a financial institution, and that the determinants of saving behaviour differ from person to person because people save and consume money for different reasons. Interest rates influence many people’s decisions about which financial institution to use. Zwane et al. (2016) use panel data estimation models to investigate the determinants of household savings in South Africa between 2008 and 2012. The findings show that household savings are heavily influenced by factors such as income, age structure, educational attainment and employment status. Household size has a negative impact, which means that larger families have a lower chance of executing savings behaviour. Economic development and business savings are inextricably linked. As a result, the economic importance of savings cannot be overstated. Savings, for example, can allow farmers to invest in their farms and increase production, resulting in higher-profit margins. Savings ensure the survival of a business by providing new funds to expand it and acting as a safety net in the event of an emergency (Frank et al., 2015). Savings also improve farmers’ eligibility for credit from credit providers like banks and microfinance providers. Zwane et al. (2016), D’Orazio and Giulioni (2017), Baranov and Kohler (2018) show that maintaining household savings increases the likelihood of potential investment at both the macro and micro levels of the economy. Furthermore, household savings have been described as a path to economic development that extends from the household to the country as a whole. Because of its role in the circular flow of income in the economy, this assertion has been empirically established in both developing and developed countries (Blanchard & Giavazzi, 2016; Chamon et al., 2013; Lin & Peter, 2018). Odoemenem et al. (2013) found that a farmer’s sex and income had a significant impact on savings based on their findings in Nigeria. Other authors, like Frączek (2011), argue that the amount of money saved is determined by a variety of factors, including income, interest rates, fiscal factors, demographics, psychological, cultural and social factors. Kibet et al. (2009) found that household income and education have a significant impact on savings behaviour among rural farmers, entrepreneurs and teachers in Kenya. According to Sebatta et al. (2014), once a smallholder farmer decides to borrow from the agricultural finance market, the level of education of the household head, household size and the farmer’s voluntary savings, all play a significant role in determining the intensity of participation as measured by the size of the loan taken. Furthermore, the findings show that a farmer’s personal savings have a significant and positive impact on the amount of credit he or she can obtain once a loan decision has been made. Income, age bracket, educational attainment and employment status have all been linked to household savings in South Africa.

Impact of Demographic Factors on Savings Decisions

There are several demographic/household characteristics, such as age, sex, marital status, religion, education and family size, that act as antecedents to savings behaviour of individuals as evident from the results in existing studies. Researchers mainly in Ethiopian context though have recognized several demographic factors such as type of occupation, household income, age, gender of the head of household, level of education, dependency ratio, service charges, transport costs, child support and wealth which strongly determine savings (Addis et al., 2019; Mirach & Hailu, 2014; Teshome et al., 2013). However, some have claimed age of head of household as one of the effective determinants of savings. For instance, Zeleke and Endris (2019) claim that households’ head’s age has a significant impact on household savings status and the odds for non-saving households’ head’s aged 26–35 and 46 and above were 6.22 and 2.78 times higher than those aged 18–25, respectively. On the other hand, in case of female-headed households, Saliya (2018) found total-household income and savings experience has a positive and significant impact on household savings. The age of the head of household, the additional household earner and the household dependency ratio also has an impact on household savings. Moreover, with reference to rural areas of Ethiopia, level of education, the size of landholdings and the involvement in small-business activities, education, gender (being female) and accessibility of financial institutions like banks and microfinance institutions were found positively and significantly impacting household savings. While, early age, household heads’ location (households residing in rural areas) and household size have a negative effect on household savings (Talent et al., 2016). Among the demographic variables, religion was also found as a positive determinant of savings decisions, for instance, by using survey data generated from 384 religious sample households, Yayeh (2014) investigated the impact of religion on household-savings behaviour in western Amhara national regional state. The findings of this study revealed that 240 (62.5%) of the entire sample, of which 162 (67.5%) were orthodox Christian, 74 (30.8%) Muslim and 4 (1.7%) Protestant households had saved. Time during the survey and thus religious affiliation impacts savings behaviour on the choice to save money or not. The findings further show that Christians are more likely to save and save more than non-Christian believers by comparing religiosity in the form of Christians to non-Christian believers. On the contrary, negative effect of some demographic variables on saving decisions have also been reported. According to the study conducted by Ayenew (2014), on the determinants of saving behaviour of women’s in Ethiopia, in which variables of interest related to women include education level of respondent, employment status, income from various sources, credit accessibility, age of the respondent, family size and agriculture. The results revealed, education and age have a negative influence on savings whereas, ownership of agriculture and income level have a positive effect on savings behaviour. While, women’s access to credit and family size has a significant negative influence on savings. Markos (2015) gathered data from 150 respondents who were drawn by field survey in 2012/2013 and the study results show that household head, sex, household landholding, marital status, livestock size, education of households decrease household savings levels.

Impact of Socio-economic Factors on Savings Decisions

Research claims the socio-economic variables, such as size of land ownership, number of livestock, total value of crops produced, participation in non-farm activities, income, expenditure and use of irrigation, also determine savings behaviour to a large extent (Aseyehegn et al., 2012; Patel, 2015; Talent et al., 2016). In east Hararghe zone, Oromia regional state, Teshome et al. (2013) discovered using the survey data on study variables such as the level of household heads’ education, livestock holdings, access to credit service, income, investment, participation in training, contact with extension, forms of savings and saving motives. The results of the study indicate that rural households save money regardless of their low income, mainly in informal saving institutions with a high demand for formal saving accessibility potential. However, Saqib et al. (2016) in the context of Pakistan found mixed results that income and employment in both urban and rural areas has a significant and positive association with household savings. Whereas, education has an important but a negative association with household savings. Van Rijckeghem and Üçer (2009) considered disposable income as the main factor in individual savings that could not be saved by people with a low income. Individual utilities are generally assumed to be a consumption function, and savings are often handled by residual resources that remain after consumption. By modelling the savings behaviour of households in Ethiopia with the two-part model, Asare et al.’s (2018) study contributes to the understanding of household-savings behaviour in Africa. The study findings show that the number of contacts for extension and access to market information has a significant and positive impact on the probability of savings of a household. In addition, land holdings and production season have a substantially positive impact on household’s expected amount of money to save. However, Hone and Marisennayya (2019) found that consumption expenditure incurred by households has a negative impact on savings. Abebe (2017) argued that human capital variables like health and training for non-farm activities have a positive impact on the decision-making of male-farm household members to participate off-farm for savings. Also, Zahonogo (2011) claimed, irrespective of the area considered, the contribution of non-farm activities to household income and savings in the rural area was important and households combined several strategies to diversify household-income sources.

Impact of Institutional Factors on Savings Decisions

Some of the prominent institutional variables that include credit service and training and education have been found as important antecedents of savings behaviour. For instance, Mirach and Hailu (2014) explained that credit can increase the access of consumers to essential resources and fuel economic growth. It also allows risk, costs and financial reserves to be allocated efficiently. Furthermore, farmers can acquire inputs and equipment that make them more productive and improve overall agricultural productivity, such as fertilizers, tractors, farming equipment and livestock. It is also widely recognized that access to credit is critical for cultivators especially in money scarce seasons at rural level that compel the farmers to borrow money from merchants for their raw materials with a lower price or in auction to face the challenge at a time. Menza and Tsegaw Kebede (2016) conducted a study on the impact of microfinance on household savings and the study output showed that financial and non-financial savings were practiced by 70% of sampled households, while the remaining 30% did not practice any form of savings. Surprisingly, 73.27% were from the treatment group, while only 26.73% were from the control group, which shows that savings and credit associations have a positive impact on household savings in the study area. Credit plays a crucial role in bridging the gap between individual consumption, low income and poor savings mobilization. Previous research (NyatichiMauti et al., 2017; Peprah & Ayayi, 2016; Ravi, 2014) has shown that access to credit improves one’s savings mobilization. These researchers believe that once credit is obtained and used effectively, revenue generated from usage will rise, affecting people’s willingness to save. According to Asante-Addo et al. (2017), the most important factors influencing farm households’ decisions to participate in credit programs are the process of obtaining credit and increased savings for farming. It also revealed that important variables such as the gender of the household head, formal education level and farm size have an impact on farmers’ willingness to participate in credit programs.

Analytical Framework

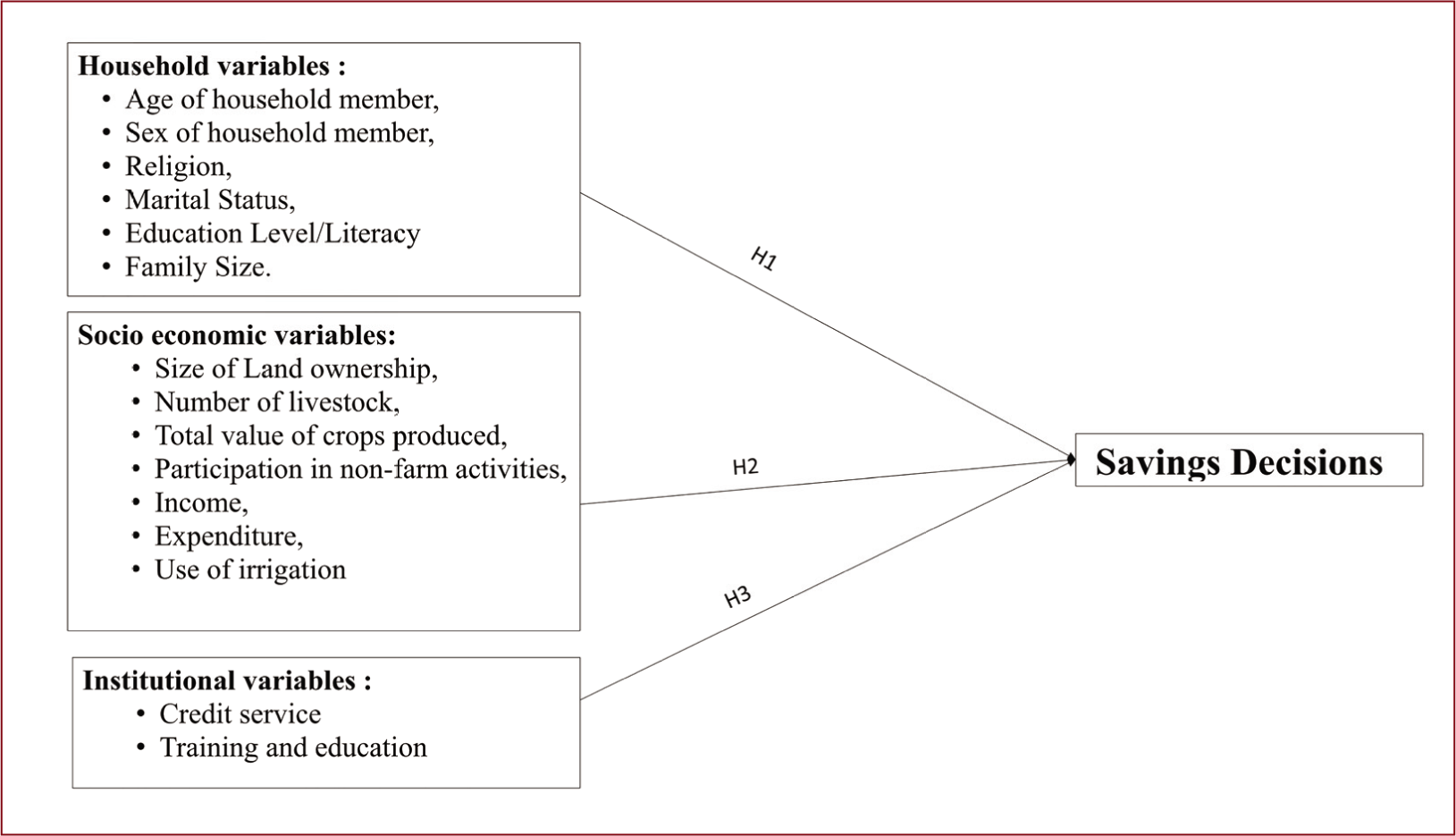

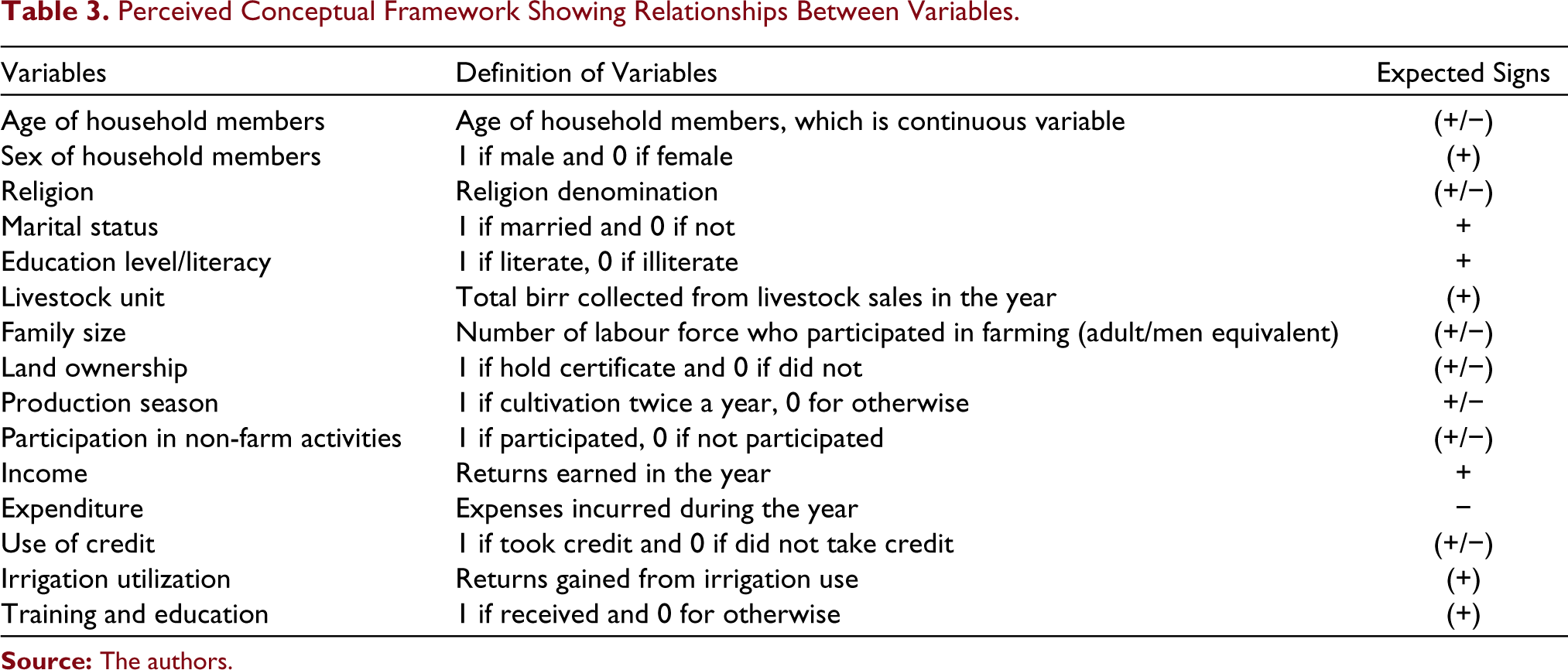

The framework is adapted from previous studies and serves as the foundation of this study. The framework (Figure 1) is formulated to explain the relationship of the dependent variable (savings decisions) with several predictors (household, socio-economic and institutional factors). As discussed below, the two categories of variables include explanatory and descriptive variables. The participation of household in savings as well as change in evaluation should be considered. The need and interest towards savings also vary depending on economic conditions, beliefs, marital status, educational levels, expenditures, accessibility to financial institutions and infrastructures, their personal background and so on.

Research Methodology

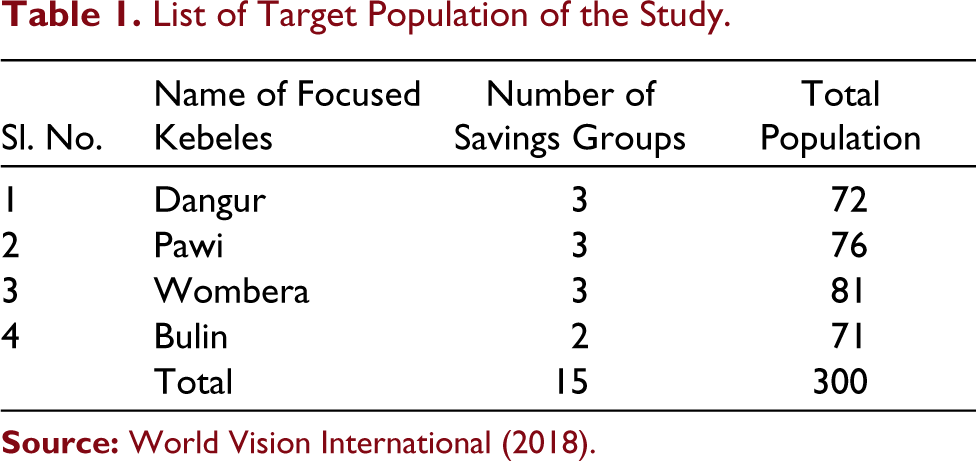

For this study, mixed method research design has been utilized that efficiently assesses antecedents of savings behaviour at Metekele zone, Benishangul Gumuz regional state (Saunders et al., 2012). The researchers utilize both quantitative and qualitative research approaches to achieve the objectives effectively. The study is conducted in Metekele zone by focusing on the rural parts of Woredas in which the savings groups are organized and functional. The Metekele zone, Benishangul Gumuz regional state is targeted as the decline in poverty slowed down between 2010–2011 and 2015–2016 in this region. In contrast to monetary poverty, the percentage of people living below the food-poverty line continued a steep decline from 55% in 1999–2000 to 24% in 2015–2016, about the same as the national average of 25%. Around 25% of rural people in Benishangul-Gumuz are poor compared to only 18% of urban people. However, due to the difficulty of covering all the total Woredas, and due to population’s similar characteristics who were organized, use of simple random sampling is more suitable (Kothari, 2004).

In addition to quantitative approach, qualitative approach has also been employed in the present study with the purpose to get more clear insights and understanding regarding savings determinants. Several qualitative research tools such as focus group discussions, in-depth interviews, field notes, observation and case stories have been well-utilized in good number of studies (Ganle et al., 2015; Kato & Kratzer, 2013; Khan et al., 2020; Kim et al., 2007). However, for the present study in-depth interviews were found apt and conducted with the 50 respondents individually.

The researchers are obliged to minimize study area by focusing on four randomly selected Woredas (Table 1). Accordingly, a total sample of 300 members has been selected for the determination of the expected sample size to be used as a representative of other Woredas in the zone, which have greater effect to influence the household-savings behaviour and the Woredas overall social and economic issues. Hence, the Woredas selected consist of Wombera, Bulin, Pawi and Dangur for the present study.

List of Target Population of the Study

In order to determine the sample of the study, the following formula given by Yamane (1967) is followed. This procedure is appropriate when there is finite and homogenous population. The socio-economic activities, institutional factors and demographic factors that determine the savings decisions are similar along with the characteristics of the population and the majority of population of the Woredas are engaged in similar socio-economic activities. The following formula is applied for sample-size determination.

where

n = sample size required,

N = number of people in the population and

e = estimated variance in population, as a decimal 0.5.

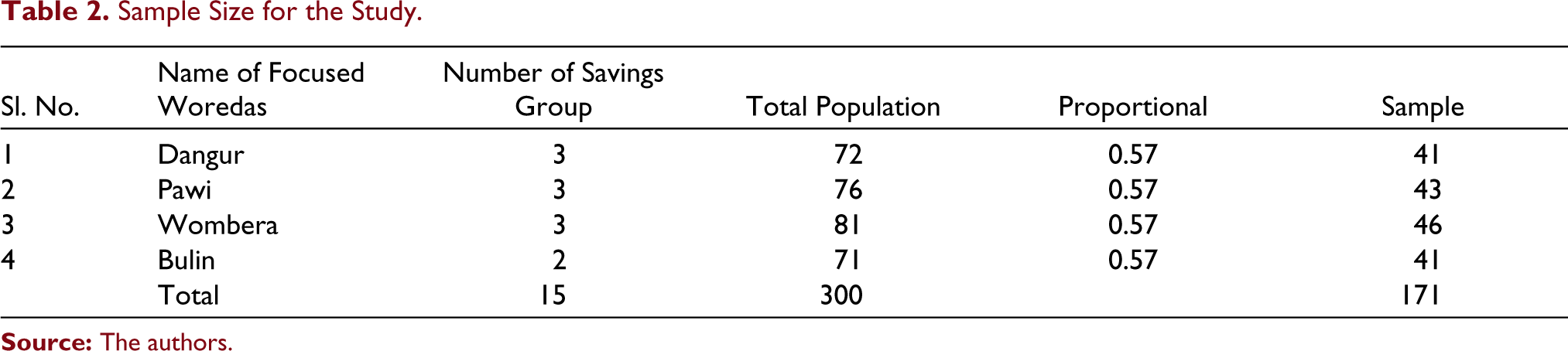

Questionnaires were distributed to 171 households by simple random sampling method (Table 2). The format of the questionnaire has been adopted from the prior authors and prepared in accordance with rationale and objectives of the study. The instrument used for data collection is based on the research questions and objectives under investigation, the research design and the information to be gathered focusing the questionnaire prepared about the variables under consideration. Since, in any survey where the questionnaires can be completed by the respondents, the appearance and layout of the questionnaire is of greater importance (John et al., 2012). The questionnaire layout was kept very simple and prepared in two different versions (English and Amharic) that helped to improve the understanding of respondents’ meaningful participation. The questionnaire had three sections, that is, demographic information of respondents, socio-economic status of the respondents and institutional factors that determine savings behaviour. Using the Statistical Package for Social Sciences (SPSS Version 20), data is coded and entered into the computer. Data is analysed for each of the independent and dependent variables in terms of mean, standard deviation and frequency distribution. Savings decisions variable is regressed using the binary logistic regression model against the 17 independent variables.

Sample Size for the Study

Determinants of Outcome Variable (savings decisions)

The factors determining savings decisions have been categorized into three groups:

Model Specification for the Study

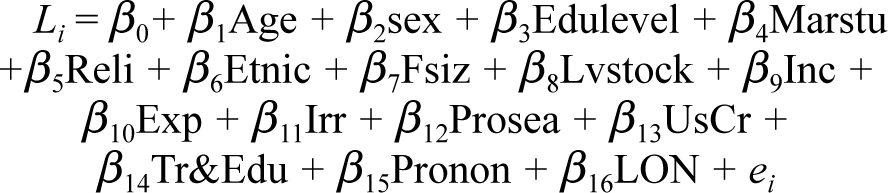

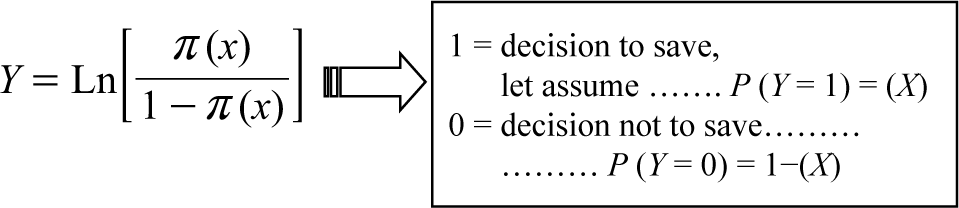

One of the statistical tools used to calculate the probability of two possible results is binary logistic regression (Bagley et al., 2001). Logistic regression requires a large sample size, but if a small sample is used for the study, as suggested by researchers, bootstraping methods should be used (Fitrianto & Cing, 2014). Logistic regression can also deal with non-linear relationships between dependent and independent variables, as a non-linear transformation of the linear regression log is applied. In this research, the two possible outcomes are either household decide to save or not to save. Thus, the dependent variable (Y) is coded as 1(decision to save) and 0 (decision not to save). The equation for binary logistic regression is formulated as follows. Gujarati and Porter (2003) gave the general expression for logistic model as,

From this general logit model, the following are derived and applied for this specific study.

where Li = log of the odd ratio of savings decisions.

Li = logs of odds ratio/logit

Ln = natural logarithm

βi = coefficient for each independent variable

β0 = intercept of the regression or constant

β1, β2, …, β16 are slope coefficients of explanatory

Xi = each independent variable and ui = error term

Inc = income (continuous variable)

UsCr = use credit (dummy variable)

Edulevel = educational qualification

Age = age of household member (continuous variable)

Lvstoc = livestock unit (dummy variable)

Sex = sex of the household member

Marstu = marital status

Etnic = ethnic group of households

LON = land ownership (dummy variable)

Fsize = family size (continuous variable)

Exp = expenditure (discrete variable)

Tr&Edu = training and education (discrete variable)

ProSea = production season (dummy variable)

Irr = irrigation use

Pronon = participation in non-farm activities

The dependent variable is the degree of savings decisions by households at Metekele zone, Benishangul Gumuz regional state which is undertaken to identify the factors that determine it. Logistic regression is helpful when one intends to predict categorical variables from a set of predictor variables (Pallant, 2005; Tariq & Sangmi, 2019). Thus, logistic regression is conducted to examine whether the three broad categories of variables (Table 3), that is, household variables (age, sex, ethnic group, religion, education level, marital status and family size); socio-economic variables (numbers of livestock units, income, expenditure, production season, participation in non-farm activities, land ownership, distance from microfinance institution and irrigation utilization); institutional variables (use of credit and training and education) significantly predict savings behaviour of households in an Ethiopian context.

Perceived Conceptual Framework Showing Relationships Between Variables

Data Analysis and Interpretation

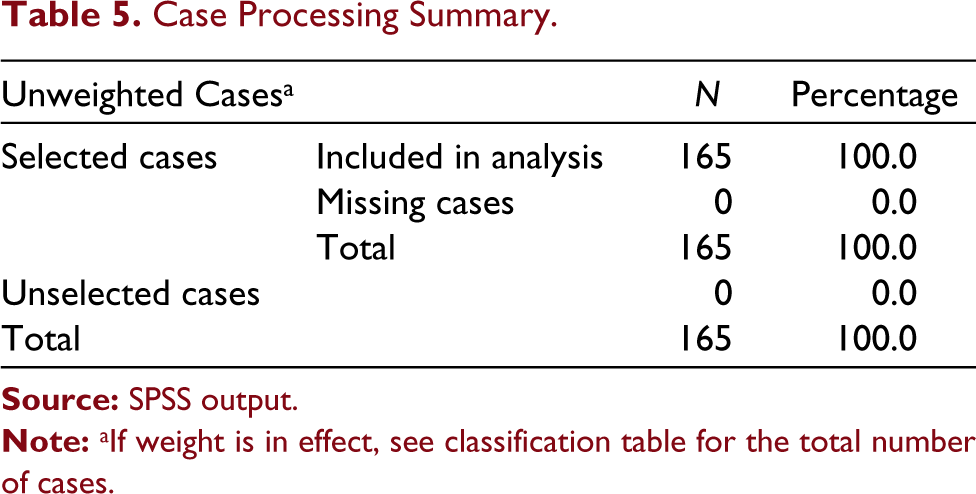

The questionnaires were distributed to 171 randomly selected respondents out of which 165 were completed and returned, resulting in a response rate of 96%. The collection procedures involved personal administration, follow up after distribution of questionnaires through mobile phone calls for validation of data, when they would be equipped for collection and personal collection whenever possible. The response rate was found to be sufficiently satisfactory for analysis of the data. The six unreturned questionnaires (4%) could be credited to delay on the part of the respondents and hence being unable to return back. Therefore, data collected from 165 (96%) respondents is considered for the present analysis.

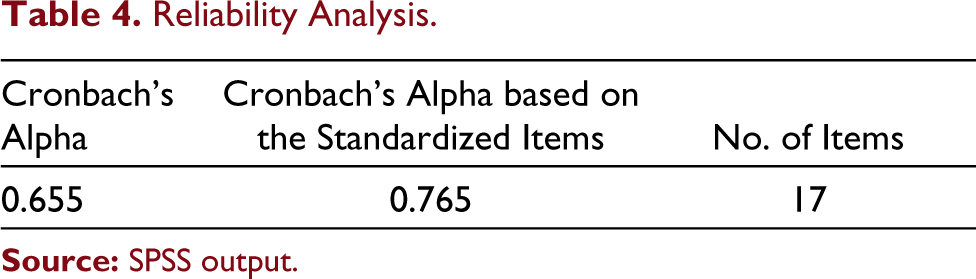

Validity and Reliability Analysis

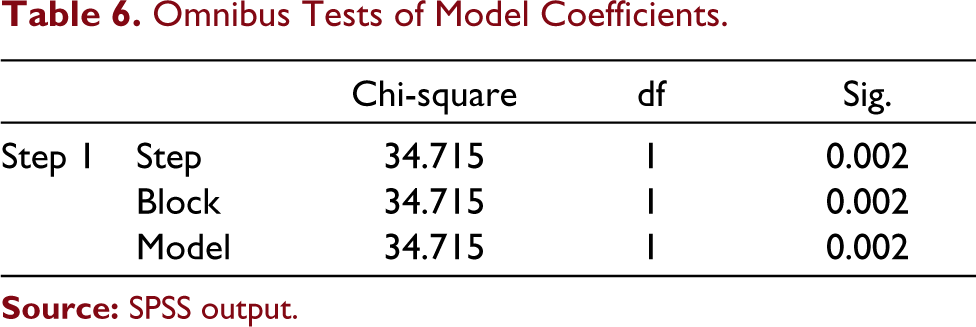

Validity refers to the extent to which reliable and adequate evidence can be shown by the researchers for the statement (Grix, 2004). Since questions are tested for their clarity and comprehensibility and important conclusions are drawn using these questions, the validity of the collected data is ensured (Table 4). The reliability analysis is then necessary to measure the consistency of the questionnaire to reflect the overall reliability of the constructs it is measuring. The most common measure of scale reliability is Cronbach’s Alpha (α) to perform the reliability analysis, and a value greater than 0.700 is very acceptable (Cohen & Sayag, 2010; Field, 2009) and a reliability value (α) greater than 0.600 is also acceptable according to Cronbach (1951). Chi-square test, (Hosmer & Lemeshow, 2000), Omnibus tests (χ2 = 34.715) are also used in this study to discover the significant determinants and the relationship of several predictors with the outcome variable.

Reliability Analysis

Binary Logistic Regression Analysis

In the present analysis, it is important to carry out a statistical analysis, which would incorporate more than one predictor variable at a time. The regression analysis method adopted in this study is binary logistic regression, which would allow the identification of the effect of each of the selected predictor variables on savings behaviour (decision to save or not to save) (Table 5).

Case Processing Summary

Table 6 above shows that when all the three category of predictor variables are considered together, they significantly predict the savings decisions variable at χ2 = 34.715, df = 17, N = 165, p < 0.05. The table labelled variables not in the equation implies that the residual chi-square statistic is 34.715 which is significant at p = 0.000 (<0.05). In other words, its predictive power will be significantly affected by the addition of one or more variables to the model (Table 7). If the residual chi-square probability was greater than 0.05, it would indicate that it would not have made a significant contribution to its predictive power to force all the variables excluded from the model.

Omnibus Tests of Model Coefficients

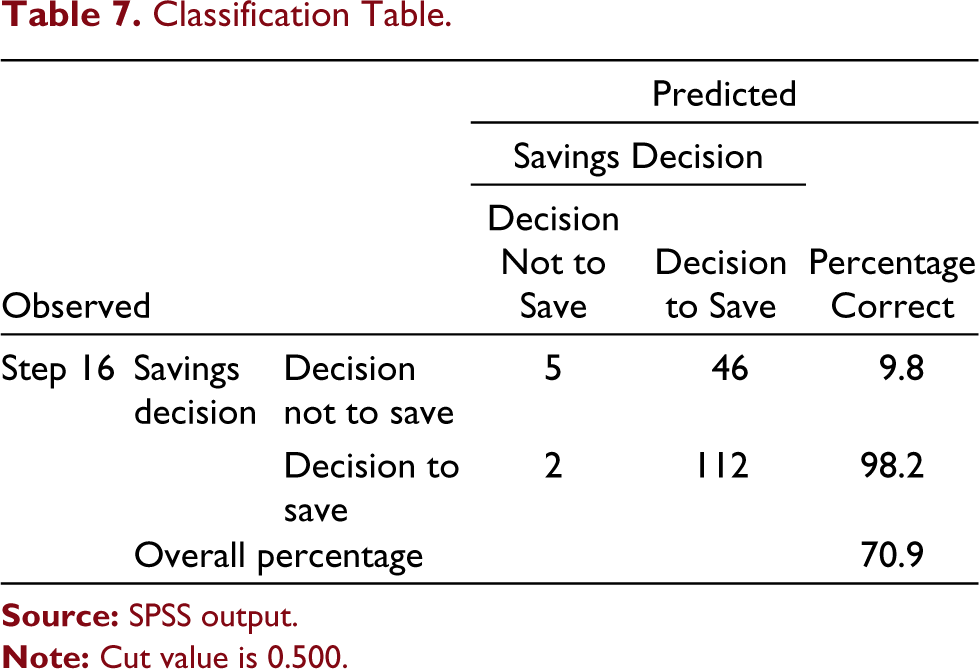

Classification Table

Evaluation of Prediction Power of Models with all the Predictors

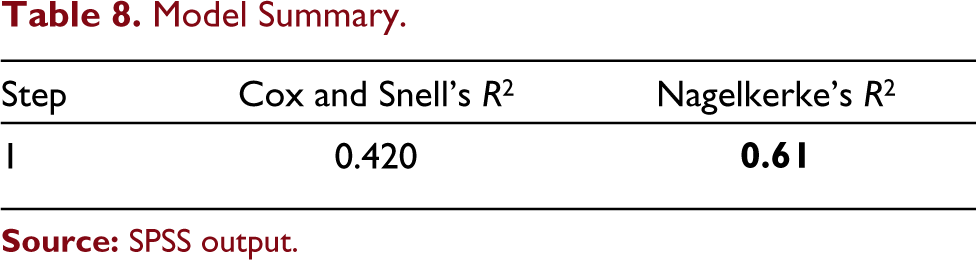

Further analysis of the prediction power of models with all the predictors and percentage-dependent variable explained by independent variables is explained in this section. Table 8, therefore, provides an indication of the amount of variation in the dependent variable with Cox & Snell’s R2 and Nagelkerke’s R2. However, the R2 modification of the Nagelkerke that varies from 0 to 1 is more reliable measure of the relationship with a better model that shows a value closer to 1 and provides an indication of the fitting information of the model. Therefore, at 61%, there is a good connection between the predictors and the response variable. And also with all the predictors, 70.9% is accurate in determining the dependent variable, as per Table 8.

Model Summary

Goodness of Fit of the Model

Table 9 shows the Hosmer–Lemeshow test, which divides subjects into 10 ordered subject groups and then compares the actual number (observed) in each group with the predicted probability of occurrence in the model population subgroups. On the basis of the actual observed outcome variable (decision to save and decision not to save), each of these categories is further divided into two groups. Under the linear model, a probability (p) value is calculated (comparing the frequencies observed with those expected) from the chi-square distribution with eight (number of groups 2) degrees of freedom to test the logistic model’s fit. Small values indicate a good fit for the data (with a large p-value closer to 1), that is, an insignificant chi-square indicates a good fit for the data and therefore a good overall model fit. As the p-value is 0.548, which is negligible, our fitted logistic regression model is therefore a good fit (see Table 9). On this basis, the Hosmer–Lemeshow test indicates that the model fits well with the statistics χ2 = 6.899 & p value of 0.548, which is (>0.05), which means that the data fits the model properly (Hosmer & Lemeshow, 2000).

Hosmer–Lemeshow Test

A lower difference in the observed and predicted classification indicates the better model fit. The Hosmer–Lemeshow goodness-of-fit test actually tests the assumptions.

Results of Binary Logistic Regression Model

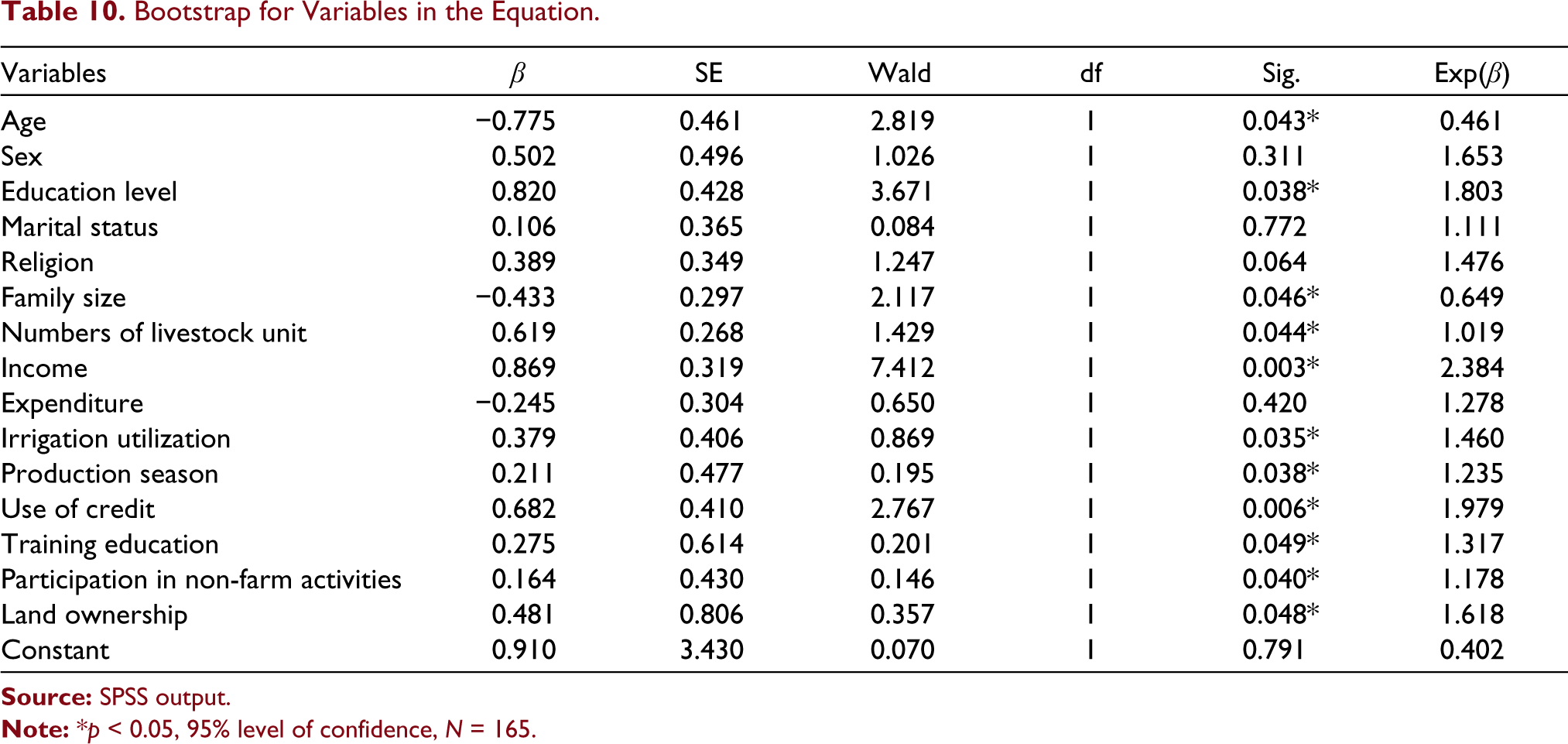

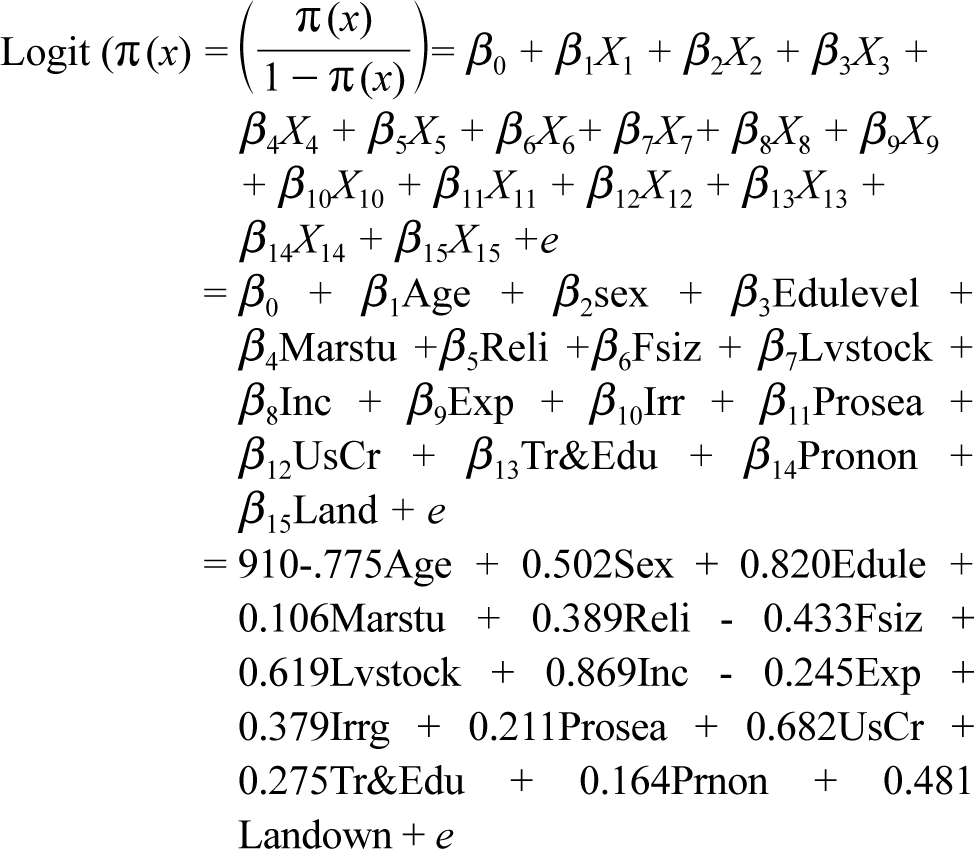

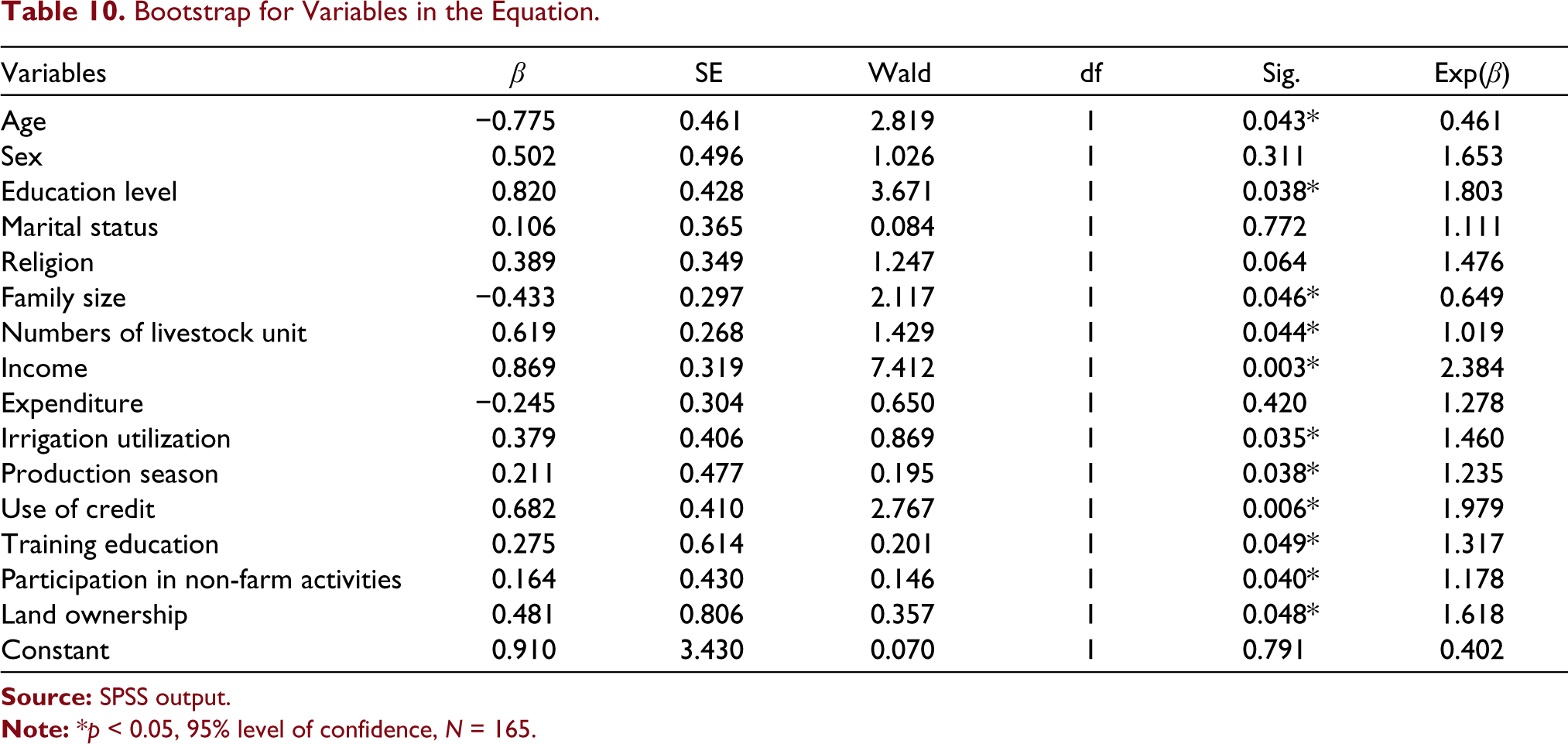

The logistic coefficients that can be used to create a predictive equation (similar to the beta values in linear regression) are the β values based as can be seen in Table 10. The researchers formulated the following expected complete model by applying all coefficients to the logistic regression model:

Bootstrap for Variables in the Equation

The chi-square distribution of the Wald statistics provides an index of the effect of the predictors on the dependent variable in the equation that is used to test whether all coefficients of predictors differ from zero to demonstrate and to understand that at least one predictor has an impact on results (Bewick et al., 2005). In addition, the p-value is the simplest way of evaluating each predictor’s significance. In this case, if the p-value of the predictors is less than 0.05 (p < 0.05), then each predictor has a significant effect on the dependent variable. In addition, EXP(β) is referred to as the odds ratio, that is, the exponential of the logistic coefficients reveal the type of relationship between the predictors and the results and also presents the extent or influence level to which the odds ratio is influenced by raising the corresponding measure by one unit. Consequently, if the EXP(β) value is just below 1 indicating that the event is less likely to occur compared to the base group, indicating that there is no effect of that variable on the outcome at which the Wald statistical outcome is close and becomes null and the p-value outcome is not significant. If the EXP(β) value is just above 1 to infinity, compared to the base group, it indicates that the event is more likely to happen (Park, 2013). The EXP(β) value associated with income, for example, is 2.384. Holding another factor constant, the odds ratio is 2.384 times as large when income is increased by one unit, and therefore, savings decisions are 2.384 times likely and significant.

Moreover, in this study as revealed in Table 10 all explanatory variable coefficients of Wald statistics are different from zero (2.819, 1.026, 3.671, 0.084, 1.247, 0.889, 2.117, 1.429, 7.412, 0.650, 0.869, 0.195, 2.767, 0.201, 0.146 and 0.357) that confirm that explanatory variables effect outcome variable. The p values of predictors are less than 0.05 (i.e., 0.043, 0.038, 0.046, 0.044, 0.003, 0.035, 0.038, 0.006 and 0.048) which confirm that the above ten explanatory variables (age, education level, family size, number of livestock unit, income of households, irrigation utilization, use of credit, training and education, participation in non-farm activities, land ownership) are significant in influencing the outcome. However, the odds ratio of each predictor as stated in Table 10—age, ethnic group and family size—for which odds ratio are less than one, revealing that there is a positive relationship between predictors and the outcome variable (savings decisions).

Statistical Test of Hypotheses

The logistic regression statistics computed in Table 10 were considered and demonstrated by the Wald test, the significance level (p-value) and the odds ratio achieved by each of the independent variables, in order to achieve the objectives of the study and test the related hypotheses. The hypotheses sought to test for a significant influence of household characteristics (age, sex, education level, marital status, religion, family size), socio-economic variables (land ownership, numbers of livestock unit, income of households, expenditure, irrigation utilization, production season, participation in non-farm activities) and institutional factors (use of credit, training and education) on savings behaviour.

Household Characteristics and Savings Decisions

The results of logistic regression are shown in Table 10. The individual test figures of age of households (Wald test = 2.819, p = 0.043, Exp(β) = 0.461) indicate age of household determines savings decision as revealed by Wald test of 2.819 and the p-value is also less than significance level 0.05. The results clearly show that the age of households has a significant effect in determining the outcome. The individual test figures of sex of the households (Wald test = 1.026, p = 0.311, Exp(β) = 1.653) suggest, sex of the household member has an insignificant effect on the savings decision. In this research study, the education level of households is also expected to determine savings. This hypothesis is supported by the logistic regression outcome at 5% (p < 0.05) level of significance and indicated by Wald test = 3.671, p = 0.038, Exp(β) = 1.803. Therefore, the education levels of households determine well-savings decisions in the Woredas. Moreover, holding other factors constant, when the education level of household members increases by one unit, saving decision in the Metekele zone is expected to present by 1.803 and the relationship is statistically significant at 5% level.

As shown in logistic output above, family size in household contributes towards savings decisions but it negatively determines savings as supported by coefficient (β = −0.433). Thus, it can be concluded, as the family size by household increases the decision to save does not happen. The results (Wald test = 0.084, p = 0.772, Exp(β) = 1.111) show that it has no effect on the savings decisions as shown by the Wald test of 0.084 near to zero or less than 1, and the p value is also greater than the significance level of 0.05 with regard to the marital status of households. On the other hand, the individual household religion test figures indicated by Wald test = 1.247, p = 0.064, Exp(β) = 1.476 show that household religion has no effect on savings decisions as the p value is greater than the significance level 0.05. But, as shown by the Wald test of 1.247 and an odds ratio greater than one, that contributes positively to outcome variable. Current findings have been linked with Zwane et al. (2016) and Markos (2015) who also found age and education positively impact savings decision, however family size negatively determines savings decision.

Socio-economic Characteristics of Households and Savings Decisions

Among the socio-economic variables, the result of logistic regression is shown in Table 10, reflecting household income, which determines the savings as shown by the Wald test of 7,412 and the odds ratio of 2,384. In determining the outcome variable, household income is, therefore, important as the p-value (0.003) is lower than the significance level of 0.05. Another feature of household land is also expected to determine savings decision in this study. The logistic regression results (Wald test = 0.357, p = 0.048, Exp(β) = 1.618) support that land possessed by households contribute towards savings decision in the zone. Moreover, holding other factors constant, when the land belonging to household increase by one unit, savings decision in the Metekele zone is expected to present by 1.618 and the relationship is statistically significant at 5% level, as shown by the Wald test of 1.429 and the odds ratio of 1.019, respectively. Another variable viz. number of livestock units belonging to household determine savings. In addition, the household livestock unit is important in determining the outcome as the p-value (0.044) is lower than the 0.05 significance level. This has clearly shown that the livestock unit significantly determines the savings decision. The individual test figures of crop production season of households indicated by Wald test = 0.195, p = 0.038, Exp(β) = 1.235 suggests that the production season of household affects savings decisions as the p-value is also less than significance level of 0.05. But, as revealed by Wald test of 0.195 near to 0 and odds ratio greater than 1 which positively contribute towards savings decisions. However, expenditure incurred by household does not contribute towards savings decisions as the p-value (p = 0.420) greater than significance level with negative coefficient (β = −0.245) indicating negative effect on savings decisions. It is revealed that as the consumption or expenditure by household increases, the decision to save declines.

The utilization of irrigation by households is also supposed to determine savings decisions of the respondents. The logistic regression results (Wald test = 0.869, p = 0.035, Exp(β) = 1.460) support significant effect of utilization of irrigation on savings decisions. Therefore, the utilization of irrigation by individual households has contribution towards savings decision in Woredas. The individual test figures of participation in non-farm activities of households indicated by Wald test = 0.146, p = 0.040, Exp(β) = 1.178 indicate that the participation in non-farm activities by household impacts savings as the p value is also less than significance level of 0.05. Brown and Taylor (2014) and Mosca and McCrory (2016) have also found socio-economic variables understudy strongly influence an individual’s propensity to save which impacts savings behaviour.

Institutional Factors and Savings Decisions

In addition, institutional factors are supposed to determine household-savings decisions, and the use of household credit significantly determines savings decisions, as shown by the Wald test of 2,767 and the odds ratio of 1,979, respectively. Thus, use of credit by household is significant in determining the outcome variable as the p-value (0.006) is less than significance level 0.05. The results show that the training and education taken by household members determines savings decisions as revealed by the odds ratio of 1.317 which is greater than one. Training and education is also important in determining the outcome variable as indicated by the p-value (0.049) that is lower than the level of significance. Menza and Tsegaw Kebede (2016), Fernandes et al. (2014) and Linardi and Tanaka (2013) also found credit access and financial education and training significantly determine savings decision of households.

In-depth Interviews: Results

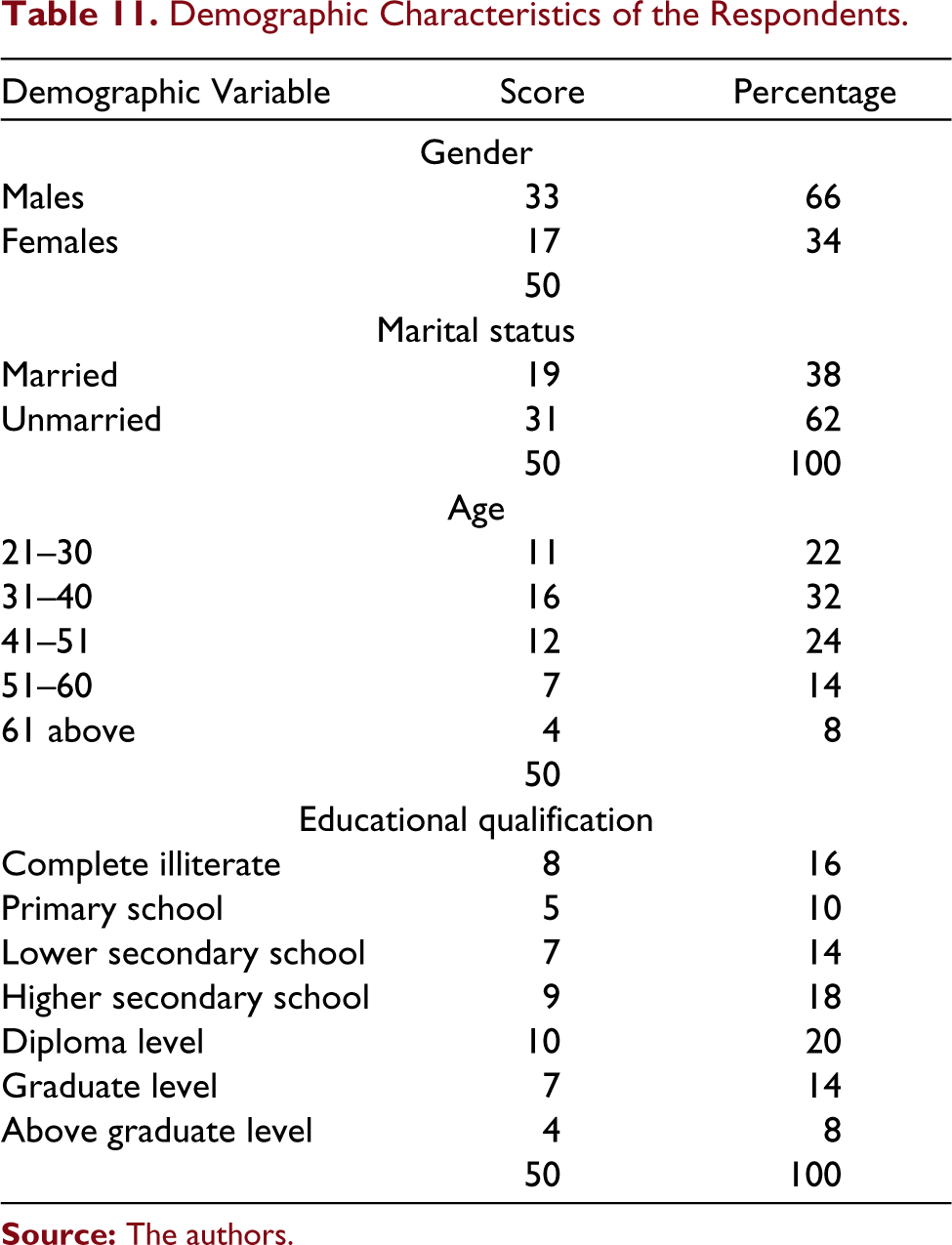

Analysing qualitative data in NVIVO gathered through in-depth interviews of 50 respondents, the findings of the study were further enriched and confirmed. For demographic data, respondents were given brief questionnaire at the end of the interviews. In these interviews, majority (33) of the participants were males and only 17 were females. Majority (31) of the respondents were unmarried and 19 were married. Most of the respondents were of middle-age group (21–40). However, the respondents greatly vary in terms of educational qualifications as shown in Table 11.

Demographic Characteristics of the Respondents

Each of the interviews lasted for around 30 minutes and was audio recorded with the approval of the respondents. Subsequently, recorded interviews were transcribed into quoted statements of the respondents. Using theoretical analytical procedures, transcripts were coded with an aim to identify thematic categories (Warren & Karner, 2005). The two major themes viz. socio-economic characteristics and institutional factors were identified on which in-depth discussion was conducted with each of the respondents. In relation to socio-economic characteristics, respondents talked about their income, expenses, participation in non-farm activities, use of irrigation facility, size of their land ownership, number of livestock possessed by them, total value of crops produced during crop season and how these contributed to their saving decisions. On the other, regarding institutional factors, respondents were persuaded to talk about the role of credit service they avail and training and educational programs in their saving decisions.

It is clear from the narrations of the respondents, majority of the factors viz. household characteristics, socio-economic factors as well as institutional factors contribute towards households’ decision to save and transform their lives. In households, where heads of the family are of higher age, well educated, are more likely to save. The sex is not determining savings decisions, as both men and women are likely to make savings decisions in this study. Respondents who were whether married or unmarried reported about saving decisions likewise. These findings related to household characteristics can be corroborated with Zwane et al. (2016) and Markos (2015). With reference to socio-economic factors, only sufficient income certainly determines households’ savings decisions positively. As one of the respondents reports, ‘the decision to save dependents on my income level, the more I earn the more I can think about savings. At times when income is low, just expenses are covered from it and at that time I don’t think of savings’. Those households who participate in non-farm activities and possess more number of livestock units are much more likely to save. As the respondent reports, ‘since we are engaged in non-farm income generating activities, we earn more compared to earlier and thus can think of savings now’. Moreover, crop season as well as using irrigation facility further determines households’ decision to save. However, those household members who reported of huge daily expenditures are not able to make any saving decisions, for lack of money in their hands. As the respondent narrates, ‘all the income that I earn goes to my daily household expenditures such as food, clothing, school fees and other expenses of my children, so I hardly think of savings, as generally I go short of cash’. These results are in line with Brown and Taylor (2014), and Mosca and McCrory (2016) who found socio-economic variables influence an individual’s propensity to save which influence savings behaviour. Of the institutional factors, it is revealed that households, which mostly rely on credit facility by Microfinance institutions along with the proper training and education about this facility are able to take better saving decisions. As one of instance of respondents’ narration is,

my participation in microfinance schemes has changed my life. It has developed not only my savings habit but granted credit amount in my favour that helped me much to meet the needs and ultimately enabled me to think about savings. Another participant reports, due to attending several training programs of MFIs and other government institutions, awareness about the importance as well as ways of savings has been increased to some extent. Though the number of trainings offered has been limited in our area.

These findings are akin to the findings of Menza and Tsegaw Kebede (2016) Fernandes et al. (2014) and Linardi and Tanaka (2013). Moreover, the findings from in-depth interviews with regard to all the predictors under study of savings decisions are mostly found consistent with the results obtained from quantitative analysis leading to reliability of the objectives achieved.

Conclusion and Discussion

The most important value of this research is that the questionnaires followed by in-depth interviews can be useful to understand household-savings decisions in Metekele zone. In addition, it was operable to determine socio-economic and institutional factors of saving decisions relevant for each household to enhance savings for transformation process. In conclusion, the inferential analysis shows that savings are carried out by 69.09% of sample households and low income and family size, social affairs and expenditure are the common reasons for households not to save. In addition, demographic economic analysis shows that income, age, gender, marital status, forms of saving institutions and the frequency of receiving money are important determinants of the study area’s household savings. Based on the findings, the following conclusions can be drawn. The targeted households are appropriate to this research due to their know-how regarding savings and institutions as they have received training and education. The analysis of logistic regression reveal a very strong contribution of these variables to the savings behaviour. Therefore, overall effect of age, level of education, family size, number of livestock units, income, use of irrigation, production season, participation in non-farm activities, use of credit, training and education contribute significantly and positively to savings decisions. Brown and Taylor (2014) and Mosca and McCrory (2016) also claimed that socio-economic variables influence an individual’s propensity to save, which further influence their savings behaviour. According to Lusardi (2008), high illiteracy rates jeopardize people’s ability to make well-informed financial decisions. Members’ human capital is thus enhanced through trainings that improve their knowledge and skills in financial management and overall financial control. Most of the demographic determinants have effect on savings decisions of households as shown in logistic regression output, as age and education level of households advanced the decision to save. These findings are in line with Zwane et al. (2016) and Markos (2015).

A surge in the number of financial institutions like banks and microfinance institutions, on the other hand, provide households with credit opportunities that boost savings decisions (Tariq & Sangmi, 2020). Therefore, households’ use of credit provides an opportunity to save. Menza and Tsegaw Kebede (2016) also found access to credit from Microfinance institutions influence individuals’ decision to save positively. Most of the households are engaged in agriculture, non-farm activities, and have their own land that, during any emergency, forms an asset for them that leads to savings decisions. The socio-economic status of the households (income, participation in non-farm activities and producing crops twice a year) contributes towards savings of households. Van Rijckeghem and Üçer (2009) also found disposable income as the main factor in individual savings that does not lead to saving decisions by people with a low income. Whereas, Asare et al. found (2018) production season of last year had a substantially positive impact on a household’s expected amount of money to save. The studies conducted by Abebe (2017) and Zahonogo (2011) also indicate that participation in non-farm activities has a positive impact on the savings decisions of the male-household members.

Practical Implications

Based on the findings, the following are specific areas that need due emphasis to improve the savings for transformation of households. There should be coordination with the concerned stakeholders and some organs so that more factors that determine the savings of households would be traced, for instance, extension of employees in rural areas of the Metekele zone. Thus, the government and concerned parties should support more for the decision to save by facilitating and undertaking training on saving options, conducting regular review and monitoring to develop a clear policy on the importance of savings specifically for households on habit of regular savings. Further, in order to improve the importance of savings, government should impart training and education to the poor households regarding financial matters by organizing financial literacy campaigns.

Moreover, to encourage savings among village savings and loan association (VSLA) members, VSLA leaders and stakeholders should enact prudent financial management programmes with the married women with the desire to take loans for home assets and donations at various cultural and religious programmes as prime targets. This approach will assist in reducing the probability of depleting savings of these targeted women and that of the association. Additionally, programmes by the Government and other NGOs to promote the participation of VSLA should consider targeting the matured women who are mostly married and located in rural areas. This is because they are likely to be receptive to such a course.

Research Implications

The study uniquely contributes through the analysis of credit access factor determining savings decision in the financial market. Moreover, examining training and education as an institutional factor influencing savings is another important contribution. Previous studies have not considered these factors for studying the causal relationship between them, which the present study does. Though ample care was taken to minimize the limitations of the study, yet certain loopholes remained there. First, sample size was not sufficient; hence, future studies can take large sample to draw more accurate inferences. Second, the study is focused on rural areas only so lacks comparison. It is suggested to conduct comparative studies while focusing both the rural as well as urban areas. Third, limited institutional variables have been considered and examined in this study. The future researchers can consider other factors. In addition, inclusion of cultural factors to address the Barnard et al.’s query (2017) is another opportunity to consider. Agyapong (2021) claims digitalization can also affect savings. Hence, all these factors should be considered and examined.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.