Abstract

Goal:

Cost estimations in healthcare are crucial to make sound and adequate economic evaluations and assessments. The concept of indirect costs’ estimation seems to be still not very well developed and systematized. This article is dedicated to the problem of indirect costs estimation of different types of cancer. The main aim of the article is to analyse the frequency of usage of different methods used for estimating indirect costs in economic analysis.

Methods:

There are discussed various methods used for indirect costs’ estimations. Among them, in details, there are described: human capital approach (HCA), friction cost method (FCM) and health state valuation (HSV). There is included a systematic review of the articles dedicated to the problem of cancer costs’estimation.

Principal findings:

Analysing the results of our analysis it turns out that the most frequently used method of estimating indirect costs is the human capital approach (HCA). It makes more than 53% of the analysed studies. The second most frequently used method is the health state valuation (HSV) which constitutes less than 17%.

Practical applications:

Calculating indirect costs in the proper way is of a great importance to adequate overall costs’ evaluation of disease. It is very important to be aware of different attitudes towards estimating indirect costs of diseases as it may allow for much more accurate assessments which will be beneficial for healthcare systems and proper allocation of limited resources. The deliberations presented in this paper might be very useful for the health technology assessment institutions.

Keywords

Introduction

Development of healthcare systems needs to be based on sound and reliable economic evaluations and assessments. That is why adequate cost estimations are crucial to make such analyses. It is necessary to run many economic evaluations aimed, first, at calculating real costs of the diseases to societies and then to carefully analyse how these costs may be reduced. Each disease is associated with both direct as well as indirect costs. The reduction of indirect costs is of great importance due to the linkage between disease and the condition of each country’s economy presented in Abegunde and Stanciole’s 1 research (see Figure 1).

Linkages between diseases and the economy.

The most common groups of diseases worldwide include heart disease, lung disease and cancer. Different types of cancer make one of the most important causes of death all over the world and are a very important burden to the worldwide healthcare systems. Quite often authors analysing costs of many diseases, including cancer, use in their calculations only direct costs. However, for societies, so-called indirect costs of diseases, seem to be equally important (see Figure 1). Indirect costs may have a significant influence on efficiency ratios. 2

The deliberations in this article are dedicated to the problems and costs that different types of cancers might cause to societies. The main aim of this article is to analyse the frequency of usage of different methods of estimating indirect costs of cancer in economic analysis. On the one hand, literature review suggests that the most frequently used method to estimate indirect costs is so-called human capital approach3,4 but on the other hand so-called health state valuation method is widely recommended as a method of estimating indirect costs.5–7 What is more, due to the fact that higher level of education in the area of indirect costs can significantly reduce many doubts about the use of this relatively new tool in healthcare analyses. 8 The term ‘indirect costs’ itself is sometimes quite ambiguous. It can be interpreted in different ways, both more broadly (like change in the use of time caused by illness or injury, both for the sufferer and the affective environment including leisure time value, informal care cost, etc.) and more narrowly (like loss of work productivity). Hence, it is necessary to present some theoretical background in the matter and the different methods that are used to estimate indirect costs of disease. In our article there are discussed different methods of calculating indirect costs and some advantages and disadvantages of each of them.

The importance of indirect costs in economic analysis in healthcare can be observed by analysing searches of the phrase ‘indirect costs’ in PubMed database (see Figure 2).

Items of ‘indirect costs’ in PubMed database in years 2010–2022.

As it is presented in Figure 2 the number of articles including the phrase ‘indirect costs’ is generally on growth, which is probably mainly due to the tips for conducting Health Technology Assessment (HTA) analyses suggesting incorporating into such analyses not only direct costs but also indirect ones. 10 It is very important as HTA analyses are more and more often being linked to the serious decision-making processes. 11

To conclude, after an initial analysis of the literature, we noted that there is a research gap in analyses focussing on literature reviews of the prevalence of methods used to estimate the social costs of diseases in the last 5 years in Europe. The added value of our study will be to conduct such an analysis and extend it to the type of cancer analysed and the country in which the study was conducted.

Indirect costs – General idea

In terms of economic evaluations the problem of indirect costs estimation is still under discussion and quite often indirect costs are understood and defined in many different ways. 12 Władysiuk 8 emphasize, that the costs of medical technology can be divided into: direct (expenditure related to illness and treatment), indirect (generally speaking – resources lost due to illness and its consequences) and intangible costs (non-financial and hardly measurable consequences of illness such as e.g. pain and suffering). Indirect costs are a broad and multidimensional term. They can be analysed in terms of accounting and medical technology. They express the value of all burdens resulting from illness and its treatment. According to Krol et al., 13 these are ‘costs associated with loss of production and replacement costs due to illness, incapacity (temporary or permanent) and premature death’. Different attitudes towards indirect costs understanding were presented by Calhoun et al., 14 Severens et al., 15 Koopmanschap et al., 16 Hartmann et al. 17 or Gutierrez-Delgado. 18 In terms of indirect costs of cancer Doran et al., 19 Lidgren et al., 20 Kim et al. 21 and Gutierrez-Delgado 18 presented their general understanding. Knowing that there are different methods of literature review, such as systematic review, umbrella review or others, in this article we apply the method of systematic review.

Methods of indirect costs measurement

According to latest research of Hubens et al. 22 there are many different method and instruments that could be used for indirect costs estimation (productivity loss estimation). However, according to authors, most were not suitable for capturing productivity changes for economic evaluations from a societal perspective. 22 In the literature, though, three main different methods of indirect cost measurement are pointed out: human capital approach (HCA), friction cost approach (FCA) and health state valuation (HSV). Hermanowski 23 also pointed out some methods designed only for evaluation of indirect costs in terms of presentism connected with a single company or professional groups for example, a firm or introspective method (FIM), Murphy’s model (MM), team production method (TPM) but they will not be widely described and used in our study due to the fact they are not very prevalent in the subject literature. Instead we focus on the first three methods that is, HCA, FCM and HSV.

Human capital approach (abbr. HCA)

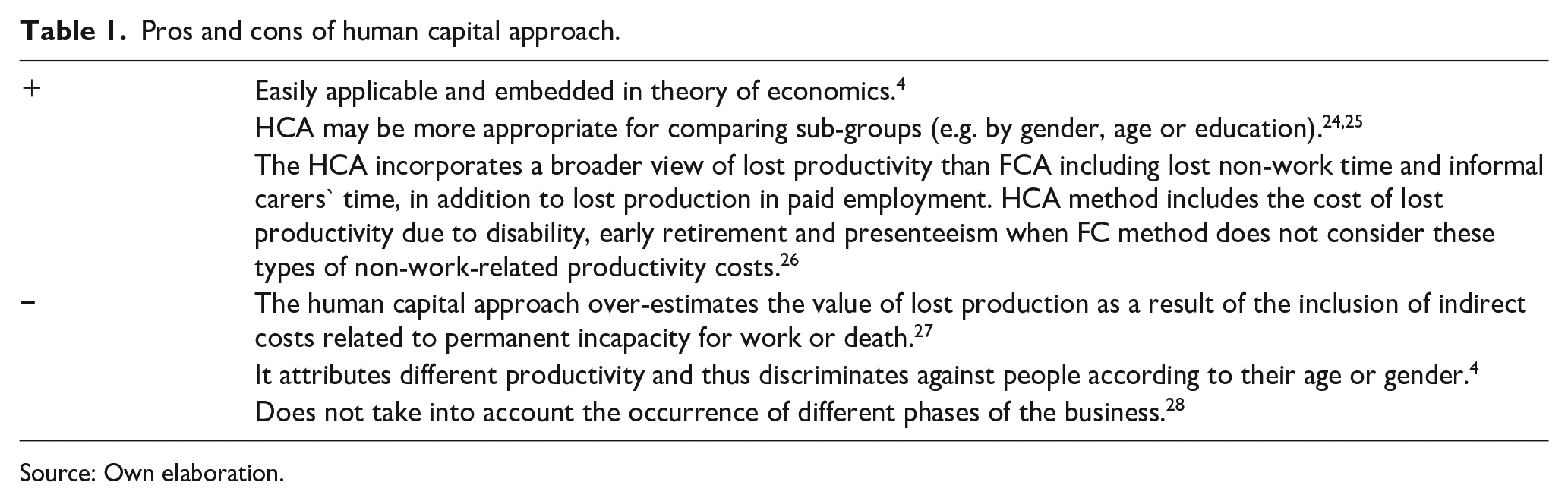

Literature analysis indicates that the human capital approach is the most widely used and the most commonly used method of estimating indirect costs. 3 According to Koopmanschap, Rutten 3 the human capital approach estimates the value of potentially lost production (or the potentially lost income) as a consequence of disease. According to the authors the word potentially is used because in case of permanent disablement or premature death at a specific age, the total productive value from that age until the age of retirement is counted as indirect costs. In other words, the indirect cost calculated on the basis of HCA includes the loss of productivity associated with reduced employee’s productivity (presenteeism), absenteeism, permanent incapacity or death.

The HCA method has both advantages and disadvantages, which are pointed out by many authors (see Table 1).

Pros and cons of human capital approach.

Source: Own elaboration.

It is worth to point out that most of the attributes concerning the disadvantages of human capital approach are not focussed on the criticism of the HCA method itself but rather on some imperfections of measures of lost productivity. It seems that using possibly objective data and taking care of due diligence while making estimations will allow repelling the criticism to some extent and to obtain reliable results of the analysis. 4

Friction cost approach (abbr. FCA)

This approach was introduced by Koopmanschap et al. 27 as a response to the shortcomings of the human capital approach. In contrast to the human capital approach, the friction cost method takes into account more economic factors which reduce the estimated production losses substantially as compared with those based on HCA.

In the friction cost method, the indirect cost of the disease is analysed from an enterprise perspective. According to Koopmanschap et al. 27 in the case of short-term absences, some of the duties of the ill worker may be taken over by the others, while less urgent duties may be fulfilled by the employee after their healing, or sometimes they may be abandoned altogether. Therefore the friction cost method accepts the following assumption: in the situation of incomplete use of workforce in economy, the indirect costs will constitute this part of the capital, which will not be worked out by the co-worker or ill person after his/her return to full recovery. Adopting an enterprise perspective means that in the case of long-term absenteeism or death, the indirect costs are incurred only for the time necessary to replace the lost employee by a new one, that is, until the company returns to the initial production level – so-called fricative period. 4

The use of the friction cost method meets with some criticism of its implementation. However, it also has its followers (see Table 2).

Pros and cons of friction cost method.

Source: Own elaboration.

Health state valuation (abbr. HSV)

The health state valuation, based on questionnaires, 8 assumes that the productivity loss can be classified as a health effect. Drummond and McGuire 33 outlines that in this method quality of life already takes into an account indirect costs and their independent analysis results in an error of their double counting. Bebrysz et al. 34 conclude, that the cost of job loss is already included in the quality of life of the patient along with non-measurable costs. These costs are estimated, for example, by the willingness to pay (WTP) method – mainly used to measure goods and services that do not have their market price. Authors of Ernst & Young 4 report assume that the production loss, in case of this method, is expressed by the monetary value that a person would be able to pay for lowering the probability of illness or premature death. According to the report this value can be estimated by stated or revealed preferences methods.

The health state valuation method has both, supporters and opponents of its use (see Table 3).

Pros and cons of health state valuation.

Source: Own elaboration.

It is worth to emphasize that the method by which productivity costs should be measured also differs between countries. Lensberg et al. 26 note that in Sweden more recommended is the traditional human capital method which values lost productivity in terms of gross earnings. In Canada, Netherlands and Australia authorities recommend the friction cost method where the FC approach is focussed on the time required to restore the lost productivity due to the absent worker.

General assessment of different methods used for indirect costs analyses

The human capital method is above all a well-understood method by the public, commonly used in practice, well embedded in economic theory and relatively easy to apply. The main complaint regarding the use of the HCA method is the overestimation of the value of lost production as a result of the inclusion of indirect costs related to permanent incapacity or death. This objection can be repelled by applying in the calculations the occupational activity ratios, lifetime tables as well as making the corrections in terms of decreasing productivity. As we have mentioned, the vast majority of reservations do not refer to the concept of the method itself, but to the imperfection of applied measures of lost production which can be eliminated or mitigated by using as objective data as possible and due diligence in the process of estimation.

Methods

Study design

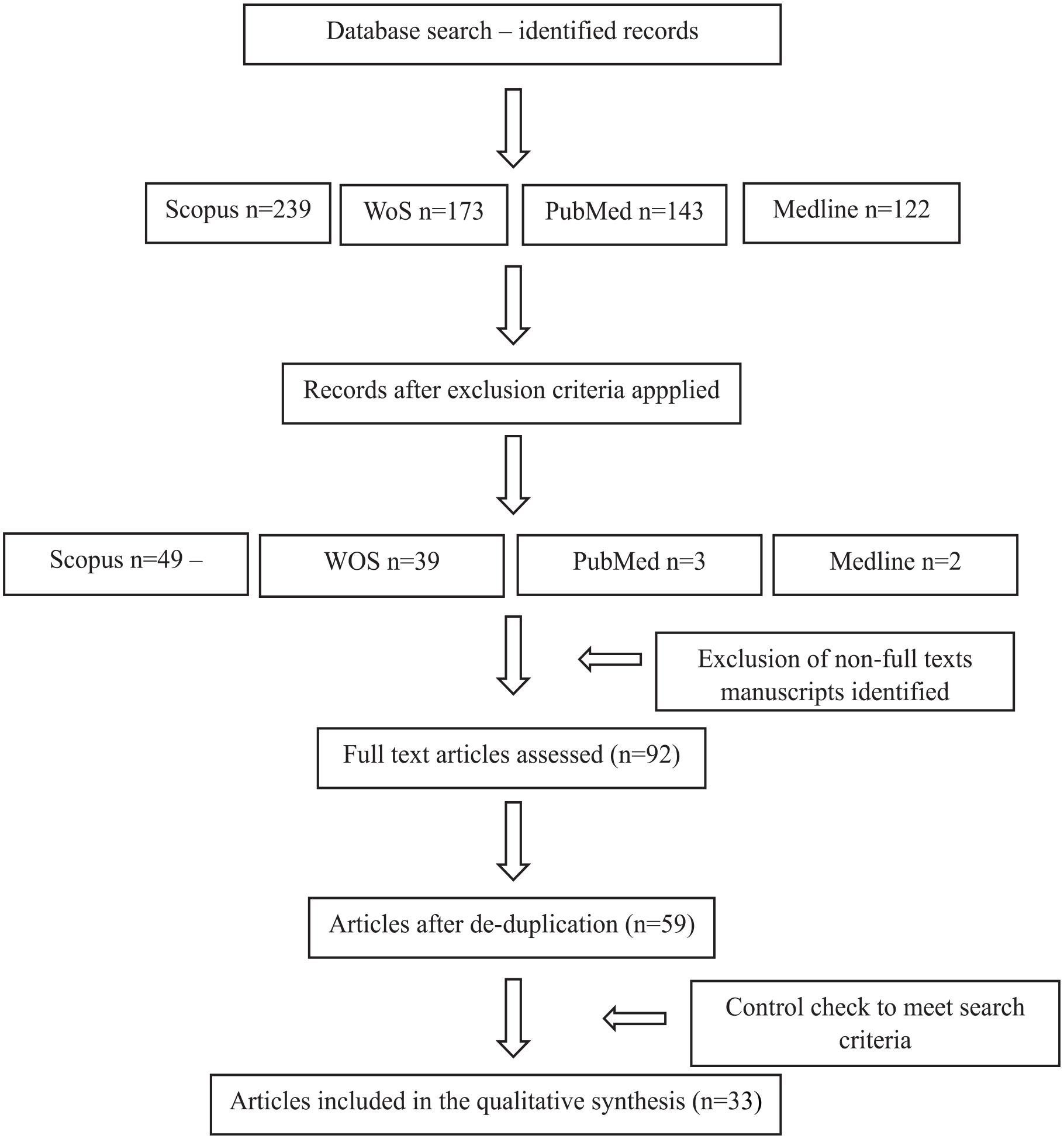

To analyse the frequency of various methods of indirect costs estimations in economic analyses of different types of cancer a systematic literature review was conducted. The literature review was conducted based on three databases: Web of Science, Scopus and PubMed.

The literature search was performed on 19 February 2024, on the following databases: SCOPUS, Web of Science, PubMed and MEDLINE (Medical Literature Analysis and Retrieval System Online; via PubMed). The search was conducted based on an analysis of abstracts, titles and keywords. The systematic literature review was conducted based on selected Prisma guidelines, however the review was not registered. The search term was constructed as a combination of domains related to ‘indirect cost’ and ‘cancer’ and ‘indirect costs estimation methods (such as: HCA, FCA, WTP and HSV)’ (see Tables 1–3). The study design is presented in Figure 3.

Study design.

As an example the search strategy for PubMed is presented below:

(‘Indirect cost’ [TIAB] OR ‘Productivity loss’ [TIAB] OR ‘Lost Productivity’ [TIAB] OR ‘Cost of Absenteeism’ [TIAB] OR ‘Presenteeism cost’ [TIAB] OR ‘Cost of Presenteeism’ [TIAB] OR ‘Cost of illness’ [TIAB] OR ‘Sickness Cost’ [TIAB] OR ‘Cost of Sickness’ [TIAB] OR ‘Burden of Disease’ [TIAB] OR ‘Economic Burden of Disease’ [TIAB] OR ‘Illness Burden’ [TIAB] OR ‘Cost of Disease’ [TIAB] OR ‘Disease Cost’ [TIAB] OR ‘Disease costs’ [TIAB] OR ‘Costs of Disease’ [TIAB] OR ‘Productivity costs’ [TIAB] OR ‘Human capital’ [TIAB] OR ‘Economic burden’ [TIAB]) AND (‘Cancer’ [TIAB]) AND (‘human capital approach’ [TIAB] OR ‘human capital method’ [TIAB] OR ‘friction cost method’ [TIAB] OR ‘friction cost approach’ [TIAB] OR ‘willingness to pay’ [TIAB] OR ‘health state valuation’ [TIAB]).

After the first step (databases search) the amount of articles were limited on the basis of the exclusion criteria. Articles that met the following criteria were taken for further analysis:

Language: English

Years: 2019–2024

Document type: article

Publication stage: final

Source type: journal

Country/territory: Europe

The literature was limited to English language articles published after 2019. We have decided to concentrate on up-to-date articles in accordance with guidelines presented in Fasseeh et al. 36 study. According to which articles selected in the process should be up-to date in order to balance between the requirements of HTA and sufficient information to draw a conclusion. 36 In our sample, we included only original articles removing literature and systematic reviews, medical trials etc. All the documents that did not meet all criteria were excluded from further analysis. Due to the overlap of the databases the process of de-duplication was conducted with a help of Mendeley embedded feature. After the de-duplication procedure control check of the selected articles was made. The step-by-step procedure is shown in the figure below. Thus, of the initial 675 articles searched (in four databases), 36 were finally analysed.

Results and discussion

In accordance with the proposed study design we analysed 34 articles fulfilling the assumed criteria. The results of our analysis are presented in Table 4.

Different methods used for estimating indirect costs of cancer.

Source: Own elaboration.

Analysing the results of our analysis it turns out that the most frequently used method of estimating indirect costs is the human capital approach (HCA). It makes more than 53% of the analysed studies. The exact percentage values are presented at Figure 4.

The proportion of HCA, FCM and HSV methods in estimating indirect costs of cancer.

The second most frequently used method is the health state valuation (HSV) which constitutes less than 17%. The least popular method of estimating indirect costs according to our analysis is the friction cost method (FCA). It was used just in two studies incorporated into our analysis together with the human capital approach method.

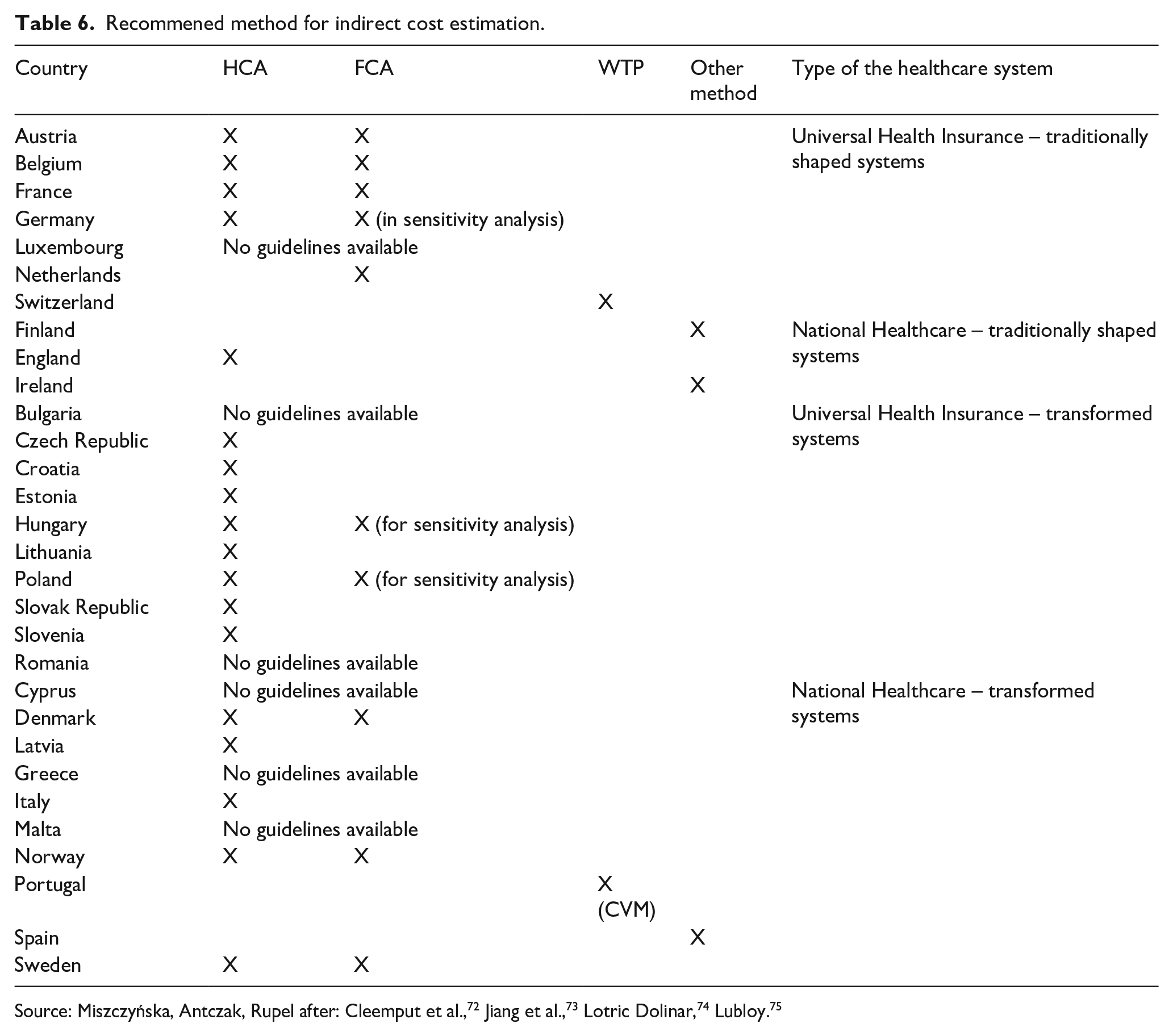

The results for the countries in which the surveys were conducted are also interesting. In addition to surveys based on EU countries, more frequent surveys have been carried out in Spain and Sweden in the last just over 5 years (see Table 5).

Different scopes of analysed studies.

Source: Own elaboration.

From the perspective of health policy making, the analysis of productivity losses (indirect costs) due to illness plays a very important role. 71 The choice as to the method used is dedicated by government recommendations. These recommendations relate not only to the method itself, but also to the perspective applied to their calculation. 71 As the study conducted by SBU stated, most countries recommend societal perspective in costs calculation. However, our analysis brought the results that in general indirect costs estimation process in case of cancer is still not very well developed. Only less than half of the articles from our initial sample included such costs’ estimation. On the other hand, the systematic review presented by Hubens et al. 22 pointed out the existence of many other productivity loss estimation, that unfortunately are not applicable in indirect costs estimation.

According to our analysis the HCA method of estimating indirect costs is the most frequent one. It is consistent with the earlier literature studies concerning indirect costs estimation,3,4 however, stays somehow opposite to the recommendations towards the usage of health state valuation method for estimating indirect costs in economic analyses.5–7 The reasons for HCA frequency probably results from the fact that it is soundly embedded in the theory of economics and is also easily applicable. The frequency of occurrence of this method over the others is evident. According to the authors’ assessment the HCA method, despite some drawbacks (which can be mitigated at least to some extent), can be portrayed as the best method to estimate indirect costs in economic evaluations. This practice is also in line with country-specific HTA guidelines.

In the analysed countries, the most frequently chosen method for estimating indirect costs is the HCA method. An interesting phenomenon of the use of indirect cost estimation methods occurs in the system - Universal Health Insurance - traditionally shaped systems - where in countries such as Austria, Belgium, France, Germany, both cost estimation methods, namely HCA and FCA, are used. In other systems, dual methods, that is, HCA and FCA, are still used only in Denmark, Norway, Sweden, Poland and Hungary. Details of the application of the guidelines in each country are shown in Table 6.

Recommened method for indirect cost estimation.

Despite the fact that HSV was suggested as the most approved method to incorporate indirect costs into economic evaluations of diseases, its frequency of usage is rather poor. It is probably due to its subjectivity and high costs necessary to conduct the estimation of indirect costs using the health state valuation. The friction cost approach is also quite rare probably due to the problems of its implementation and the fact that it has no sound background in the theory of economics. Hence, the authors would probably prefer to apply the method which rather overestimates the costs of health technologies like HCA because of prudent inference to be inconsistent with the economic theory and to avoid excessive costs of studies. It should be underlined that Hanly et al. 53 made lately an attempt to generate two alternative estimates of the friction period for European countries and to apply the FCA to illustrate the impact on cancer-related lost productivity costs. The author stated that the newly presented approaches will enable researchers to apply the FCA to estimate the productivity cost of diseases across Europe from an employer’s perspective. 53

It could also be observed that in many articles the methods that were used for estimating indirect costs are directly presented. Very often there is no clear information if the FCA, HCA or HSV method was applied. Instead, there are presented some assumptions describing just the way the indirect costs were calculated whereas there exists a sound theory explaining how to calculate indirect costs. Therefore, in most cases we were forced to make assignments of particular methods of indirect costs calculation on our own. This sort of subjective judgement may constitute a sort of limitation to this study. Though, it also shows that the topic of indirect costs’ estimation, which may have significant meaning for overall costs of diseases calculations, is not well structured and systemized.

Moreover, it is worth to point out that some analyses also include into indirect costs such elements as travel expenses, extra costs of treatment or the costs related to sending invitations or reminders to patients which should be rather classified as direct non-medical costs.10,76 It shows the vagueness concerning the analysed matter and also supports the thesis that the problem of indirect costs estimation should be explored, popularized and described in a more precise way.

In the article, we tried to systematize and describe in details indirect costs estimation methods and make their assessment. What is more, we also tried to rank the methods according to their frequency of usage. As a proxy we restricted our deliberations just to different types of cancers which is obviously a sort of limitation of our study. The other limitation might be the number of studies included into our sample. However, we believe that the distribution of different methods according to their frequency of usage among other diseases as well as conducted on a bigger sample would be probably similar. Moreover, we have confidence that cancer is one of the most serious and wide-spread diseases of current times. Hence, it needs careful and in-depth attention.

Conclusions

Analysing the problem of different methods used for estimating indirect costs in case of different types of cancers it is clearly visible that the problem is evolving. Due to the fact that each of the methods used for estimating indirect costs is not free of drawbacks, it seems quite reasonable to incorporate into such economic evaluations of costs of cancers as well as other diseases more than one method of indirect costs’ estimation, describing in details research assumptions. Then the readers would have definitely a greater chance to figure out a more accurate point of view after reading such a study.

As it was mentioned earlier in the article the problem of indirect costs estimation in economic evaluations is still under many debates and the higher level of discussion in the area of indirect costs can significantly reduce many doubts about the use of this relatively new tool in healthcare analyses. Calculating indirect costs in the proper way is of a great importance to adequate overall costs’ evaluation of disease. Moreover, thanks to incurring indirect costs into HTA analysis it is possible to choose between two medical technologies with identical health effects and identical costs of treatment. In such a case the use of indirect costs might be crucial to absorbing the technology featured by the lower costs from the societal perspective, which is particularly important for limited medical resources. However, the ongoing debate about the appropriateness of the two main methods suggested in HTA recommendations - HCA and FCA - has continued unabated for several decades. Thus, it is difficult to disagree with the view put forward by Pike and Grosse that the lack of standardization of the HCA and FCA methods makes productivity cost estimates difficult to compare across studies. And, crucially, the demand for the use of indirect costs in healthcare analysis is particularly evident in developed countries.

What is more, the discussion about different methods in the matter might be also beneficial for improving them or even creating the new methods of which potential drawbacks might be mitigated at the very first start.

High level of awareness among researchers in the area of indirect costs’ estimations in health and medicine will allow definitely for much more accurate assessments which will be beneficial for healthcare systems’ financing and proper allocation of limited resources.

In the nearest future it seems necessary to fully systemize the subject of indirect costs’ estimation and highly promote associated theory among researchers incorporating this kind of costs into their analyses.

Footnotes

Acknowledgements

We would like to thank Radosław Pastusiak for his help in initiating the study.

Author contributions

Katarzyna Miszczyńska: Conceptualization; Formal Analysis; Methodology; Investigation; Writing; Original Draft Preparation; Writing; Review & Editing. Bartłomiej Krzeczewski: Conceptualization; Methodology; Investigation; Writing; Original Draft Preparation; Writing; Review & Editing. Joanna Stawska: Conceptualization; Investigation; Writing; Original Draft Preparation; Writing; Review & Editing.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.