Abstract

This article examines the extent of web utilization as a tool for the disclosure of corporate information on the website and exhibits the association between bank-specific attributes such as size, age, profitability, market discipline, listing status, leverage, foreign ownership, and type of sector in relation to the web disclosures of 87 public, private, and foreign sector Indian commercial banks. To achieve the objective, a checklist index of 143 items of information was developed. To examine the hypotheses of the study, a panel regression model was estimated on the data of 87 Indian commercial banks. Panel regression results indicate that size, market discipline (CAR), profitability, listing status, type of ownership, and type of sector have a significant relationship with the level of web disclosure, and banks are more likely to use the websites to disclose information. On the contrary, age, leverage, and market discipline (NPA) have insignificant relationship with the web-based disclosure level, and Indian banks have not shown any relationship with the disclosure score. The study will help the managers to meet the actual and potential informational needs of the investors; for the investor, it will help to assess investment decisions in a better way.

Keywords

Introduction

Web is nowadays considered one of the better mediums of the disclosure of financial and non-financial information of companies, the major benefit being its competence to provide a direct link between the management and stakeholders without involving intermediaries like the publication media or financial analysts (Singh & Malhotra, 2004). Internet has become the common practice of the corporate sector as it enables relatively cheap and speedy delivery of useful information in different formats to the mass public, who use the internet every day, at a very low cost (Lymer, 1999). Today, users with a computer and internet connectivity can get the required information that was previously available only to the company’s top officers, professional financial analysts, and the publication media (Sharma, 2013). Web-based disclosure, therefore, has the advantage of providing information about the company on a website to anyone, anywhere, and at any time (Verma, 2010). Web disclosure states the use of the World Wide Web (WWW) by companies to disseminate and release insider financial and non-financial information of the organization into public domain (Lymer, 1999). Nowadays, the communication of information through the web is of particular attention. However, companies are liberal to disclose information on the web as per their needs due to the absence of standardized protocols for web-based reporting (Henchiri, 2011). Web-based disclosure is still a voluntary exercise in all other countries except the United States of America and Canada. In the United States of America, the US Securities and Exchange Commission (SEC) has adopted the Electronic Data Gathering, Analysis, and Retrieval (EDGAR) filing system and made it compulsory for larger organizations to provide their financial information on the web. In Canada, Ontario Securities Commission has used the System for Electronic Document Analysis and Retrieval (SEDAR) to disclose information on web.

In order to measure the level of web disclosures (financial and non-financial) made by the banks, it was necessary to quantify the results of 87 banks. The scores have been calculated in the form of a disclosure index. There are in all 143 disclosure items in the index, divided into ten categories. Disclosure score is presented as a percentage calculated by dividing the total number of items disclosed by a particular bank by 143 and then multiplying it by 100. The identification of the items and scoring method have been done on the basis of

information included under the indices prepared and used in previous studies, annual reports of banks, provisions of the Reserve Bank of India Act, 1934 and Banking Regulation Act, 1949, websites of different banks, and opinion and advice of experts in the field on what factors are to be considered and which information items are to be analyzed.

Unraveling the attributes that have an association with web disclosure is important. It would be helpful to understand the significance of various attributes of web-based disclosures in a bank-based economy like India. In this article, an attempt has been made to examine the relationship between various corporate attributes and web-based disclosures of banks.

The objective of this article is to examine internet web reporting practices and attributes in Indian public, private, and foreign sector banks. The rest of this article is structured as follows. A review of relevant literature is provided in the next section. The research methodology is discussed in the third section. The fourth section provides analyses and discussions on the relationship between different attributes and web disclosure. Summary and conclusion are presented in the final section.

Review of Literature

Increasing evidence of awareness of web-based disclosures has witnessed heightened interest in the practices of web reporting, particularly by large corporations worldwide. Agency theory explains that managers do not always work in the interest of shareholders (Singh, 2013). As a result, conflicts can be aroused between them due to asymmetrical information, and communicating proper information can bring the interest of the entrepreneur in line with stakeholders’ interest (Jensen & Meckling, 1976; Shehata, 2014). Signaling theory propounded to reduce the information asymmetry in the labor market (Spence, 1973), and it asserts that providing more information to the stakeholders generates a good signal in the market about the image of the company that helps in achieving the ultimate goal of the organization (Siala et al., 2014). Most of the previous disclosure studies found a connection between the level of disclosure practices and various company-specific characteristics applied in the developed countries—China (Liu & Eddie, 2007); Japan (Marston, 2003); the UK (Craven & Marston, 1999); the US (Kaya, 2014); Spain (Álvarez et al., 2008); and France (Boubaker et al., 2011). The disclosure practices of developing countries were studied by other groups such as Ghana (Bokpin, 2013); Indonesia (Pertiwi, 2013); India (Bhatia & Tuli, 2017; Hossain et al., 2009; Verma, 2010); Malaysia (Arussi et al., 2009; Sharma, 2013); and Bangladesh (Khan, 2006). Recent research has suggested that the majority of the international companies are publishing web-based reports. Major studies in this section are reviewed below: Khan (2006) surveyed the top 60 companies that were listed on the Chittagong Stock Exchange to study the availability of web-based corporate disclosure. The results of the study specified that 24 out of 60 companies in Bangladesh had websites, and these websites were active in promoting the company’s business. These websites provided information in relation to the company’s profile, product, and service information, and much other promotional information about company’s activities. Momany and Al-Shorman (2006) analyzed the extent of web-based financial reporting by the Jordanian companies listed on the Amman Stock Exchange. The researchers reported that 45% of the companies had websites, and 70% of the companies reported financial information on their websites. A total of 31.5% of the sample companies stated a set of financial statements, 15.8% of the sample companies reported partial financial statements, and 52% of the sample companies stated financial highlights. Hossain and Reaz (2007) examined Indian banking companies regarding the determinants of voluntary disclosure and revealed that banks disclose very less voluntary information. The lowest and highest ranges of disclosure vary from 20 to 55. And public sector banks disclose more of the voluntary disclosure than private banks. Multivariate regression analysis was done to study the relationship between voluntary disclosure and companies’ characteristics (size, age, multiple listing, complexity of business, board composition, and an asset in place), and the results revealed that size and asset-in-place had a significant impact on voluntary disclosure. Hossain et al. (2009) examined the voluntary and mandatory disclosure of Indian-listed banks and revealed that Indian banks don’t do not disclose voluntary (requirements) items. They are far behind in disclosing. Disclosure index of 184 items was created to study 38 annual reports. The impact of age, profitability, size, complexity of business, board composition, asset-in-place, market discipline, the size of assets, and profitability were statistically examined through multivariate analysis, and all these variables had a significant impact on the disclosure level. Kelton and Yang (2008) in their research paper concluded that the use of hyperlinks by companies to present financial information to existing and potential investors. The study reported that approximately 98.00% of sample companies provided hyperlinks as a navigational tool within their corporate website. Arussin et al. (2009) examined the effect of company size, profitability, financial leverage, and industrial classification on the extent of web disclosure by the leading 97 companies traded under the Kuala Lumpur Composite Index (KLCI) on Bursa Malaysia. Company size and financial leverage were found to influence the extent of Internet disclosure of some items of financial information. There was no significant association between profitability, industry classification, and the extent of internet disclosure. Chander (2011) studied the disclosure practices of public and private sector banks in India through annual reports. The results of the study showed that highly disclosed items were generally those that were mandatory under one or another law, like the bank’s financial position, board meetings, internal control system, and so on. The voluntary items of disclosure like the history of bank, organization structure chart, risk-weighted assets, disaster recovery management, and so on, had zero or very low disclosure. Sharma (2013) examined the corporate governance disclosure practices of public and private sector banks in India during the years 2008 and 2012. The results of t-test indicated that there had not been any significant difference in the corporate governance disclosure practices of public and private sector banks for both years. It had also been found from the study that both sectors of banks were following the guidelines as prescribed by the Reserve Bank of India (RBI) and Securities and Exchange Board of India (SEBI) regarding corporate governance disclosure.

Hypothesis Development

In order to find the relationship between various corporate attributes and web-based disclosures, various hypotheses were developed and formulated. Previous empirical research that checked the relationship between the extent of web disclosure and various attributes had shown that there were many company characteristics that influenced the level of extent of web disclosure, like size of bank, age of bank, profitability of bank, market discipline, ownership structure, listing status, and so on. Based on the theoretical and empirical studies available, hypotheses have been framed to incorporate bank-specific variables that affect web disclosures in Indian commercial banks. These hypotheses are mentioned in the form of alternative hypotheses.

Size of a Bank

The size of a bank is in fact the most common and significant factor that explains the variation in the relationship between various corporate attributes and web-based disclosures. There are a number of measures available for gauze size, as per the existing literature. It can be measured in different ways: total assets, total deposits, total loans, market capitalization, number of employees, number of branches, number of customers, net income, and number of shareholders. Cooke (1991) mentioned that size can be measured in a number of different ways, and there is no particular method to select one over another. In this study, total assets and total deposits were utilized as measure of a commercial bank’s size. In the present study, size is taken as natural logarithm of total assets and as natural logarithm of total deposits. RBI glossary defined the size of bank in terms of total assets as the combined amount of the bank’s fixed assets and current assets as recorded in the balance sheet of a particular bank. This shows all the assets used by the bank, regardless of how they are financed. This asset position of a bank’s capital includes cash, government securities, and interest-earning loans, for example, mortgages, letters of credit, and inter-bank loans. Total deposits, as defined by the RBI glossary, are equal to the total money placed into the banking institutions for safekeeping accounts.

Most of the previous disclosure studies have empirically agreed that corporate size has a positive relationship with the level of disclosure practices (Abdullah, 2006; AbuGhazaleh et al., 2012; Al-Htaybat et al., 2011; Buzby, 1974; Cooke, 1989; Cooke, 1991; Haniffa & Hudaib, 2004; Hossain & Reaz, 2007; Hossain & Taylor, 2007; Hossain, 1994; Hossain et al., 1995; Sharma 2013; Singhvi & Desai, 1971; Uyar, 2012). These studies revealed that there was a positive relation between size and web disclosure by firms because larger firms usually enjoy ingrained technology and information system infrastructure as well as the required financial resources. Larger-sized banks have good access to website disclosure as more access by a more number of users (Chander & Singh, 2009). The use of websites for the disclosure of financial and non-financial information helps in proper dissemination and communication of information by the banks. Also, large banks tend to take more advantage of the digital and innovative technology of communication and have a greater ability to attract potential customers (Chander & Singh, 2009). This enables them to strengthen the relationships with current as well as potential users. Web-based reporting provides many and better options for making financial reporting vibrant, and it creates a friendly and close relationship by helping users to make better decisions (Khan, 2006). Also, larger firms have the ability to bear the cost of collecting and disseminating the information and large firms have the resources and expertise to produce more in their banks at little extra cost (Hossain & Adams, 1994; Lang & Lundholm, 1993). The other possible benefits of better web-based disclosures are easier marketability of securities, greater ease in financing, and greater public confidence, which smaller enterprises usually can not realize the possible benefits of better disclosure. Finally, large organizations are more visible in the eyes of public and government agencies. Thus, greater external interest results in better disclosure as compared to smaller corporations (Debreceny et al., 2002).

However, a contrary opinion also prevails, which states its validity only up to a certain level of size influenced this relationship (Hossain & Reaz, 2007). In the case of public sector banks, size does not find a statistically significant relationship with the extent of web disclosure. From the preceding discussion, the following hypothesis was developed:

H1: The size of a bank as measured by total assets has a significant impact on the average web disclosure score. H2: The size of a bank as measured by total deposits has a significant impact on the average web disclosure score.

Age of a Bank

The age of a company is a critical determinant in determining the effect of web disclosure. Aged banks are more likely to report more information due to their experience and their willingness to maintain goodwill and image in the market than that of less-aged banks. As a result, there is expected to have a positive association between the age of the bank and the extent and level of their disclosure. This variable has been selected with a consideration that older banks might have higher web disclosure scores with the passage of time (Mahajan, 2014). It may be due to the fact that young banks have to face complex competitive disadvantages in initial stage of establishment, while older banks are enjoying the benefits of accumulated experience, goodwill, and top positions in the list of RBI. Older banks have been in the banking business for many years, and with better knowledge and experience, they have stronger customer relationship management as well and are more secure (Sharma, 2013). These factors help in achieving a better web disclosure score. The other factors are the cost of processing and communicating the required information. Also, at the initial stage of incorporation, younger companies are likely to be more burdensome (Mahajan, 2014).

However, on the other hand, Mahajan (2014) and Hossain and Reaz (2007) found a negative relationship between age and web disclosure score. They argued that new and young firms are disclosing more on their websites as compared to older firms. The reason revealed by the studies is that young firms are more flexible and adaptable to changing environments as compared to older firms. This makes them ready to implement advanced technology at a fast stride and makes them competitive. In this study, the age of a bank has been computed from the year of incorporation till March 2016 (the year of starting to search websites in the study). Therefore, the above argument leads to the formulation of the following alternative hypothesis:

H3: The age of a bank has a significant impact on the average web disclosure score.

Profitability

Profitability-based measurement can serve as a more robust and inclusive means to measure performance by gauging the extent of operational efficiency as well as capturing the nuances of a bank’s diversifying earnings through non-interest income activities and management of their costs. The profitability of a bank can be measured in a number of ways, such as return on assets, risk-adjusted return on capital employed, return on net worth, economic value added, profitability ratios, and more. The study used return on assets as a measure of profitability to test the significance of the relationship between the profitability and the extent of web-based disclosure by banks. The ROA is determined by the amount of fees that it earns on its services and its net interest income. It can be symbolized as

Net interest income depends partly on the interest rate spread, which is the average interest rate earned on its assets minus the average interest rate paid on its liabilities. It depicts how well the bank is earning income on its assets. High net interest income and margin indicate a well-managed bank and also indicate future profitability.

Signaling theory specifies that profitability is considered a good signal for the quality of information. More profitable companies try to distinguish themselves from less profitable companies through enhanced financial reporting. Also, the most profitable companies are always in the limelight, so they are under more pressured to reveal information. Laswad et al. (2005) and Xiao et al. (2004) suggest that “firm profitability attract capital from the security market and in turn it increases the need for disclosure to reduce asymmetries between firm and investors.”

Prior empirical disclosure studies have provided mixed results on the relationship between profitability and the level of disclosure practices. Pervan and Bartulović (2017) mentioned that the financial position of a bank also affects the web-based disclosure score. Generally, more profitable companies have more detailed information to be disclosed in order to prove their efficiency and strength of their company, while less profitable concerns may disclose less on their websites being less competitive (Garg & Gakhar, 2010; Mahajan 2014).

A contrary view states that profitability may be dubious at times. When companies accumulate more profits than required, they need not disclose more information about their goodwill in the market Singhvi and Desai (1971), Chander (1992), and Mahajan (2014). That is how Oyelere et al. (2003), Marston (2003), Aly et al. (2010), Elsayed (2010), and AbuGhazaleh et al. (2012) found an insignificant relationship between profitability and web disclosure score. Profitable companies might seek to avoid public intervention costs, such as litigation, and prefer to reduce their levels of disclosure if their competitive position is likely to be affected (Al-Hajaya, 2014). Moreover, AbuGhazaleh et al. (2012) state “highly profitable firms tend to disclose less information to avoid political attention in the form of pressure for the exercise of social responsibility and greater regulations such as price control and higher corporate taxes.” Thus, the following hypothesis has been established:

H4: The profitability of a bank as measured by ROA has a significant impact on the average web disclosure score.

Market Discipline

Market discipline refers to the obligation of banks and financial institutions to manage their stakeholders’ risks in the course of their day-to-day operations. As per Basel II recommendations, market discipline in banks seeks to achieve increased transparency through expanded disclosure requirements of banks under regulatory system (RBI glossary). The regulatory system of banks based on the Basel pillars specifies that any investor, whether any depositor or professional investor providing funds to a financial institution, must be able to access and monitor its risk profile as well as its financial soundness.

In recent times, market discipline has got more attention in banking sector. Not much research has been conducted in finding the relationship between web disclosure score and market discipline. Still, it has been anticipated that the banks that disclose the market discipline norms like CAMEL (capital adequacy, asset quality, management competence, earnings, and liquidity) ratings are more likely to disclose other information also ( H5: The market discipline of a bank as measured by CAR has a significant impact on the average web disclosure score. H6: The market discipline of a bank as measured by NPA has a significant impact on the average web disclosure score.

Listing Status

The listing status of banks has a great effect on the level and extent of web disclosure scores. A bank that wants to get itself listed on a recognized stock exchange has to abide by the listing agreement, and investors are interested in those banks whose shares are actively traded in the national and international stock markets. Listed banks are expected to report more information in order to reduce agency, political, and monitoring costs. Listing status has been measured by the number of stock exchanges on which banks are listed in India and abroad. Banks that are listed on national or international stock exchanges have to provide detailed information and need to follow the standards and provisions of stock exchanges (Marston & Polei, 2004; Xiao et al., 2004). Also, banks have to follow international standards along with national standards in their financial statements if they have overseas business operations. In order to prove their creditworthiness and procure more funds from national and international sources, more detailed information is required to be disseminated to the stakeholders. In addition, foreign-listed banks have to disclose more information in order to reduce information asymmetries between domestic and international investors. Therefore, web-based disclosure can be used to reduce information asymmetry by mass media communication and wide reach (Debreceny et al., 2002).

However, Al-Hajaya (2014) argued that the listing status of the bank only affects the level of web disclosure score at the adoption stage. The banks that are listed use their websites in undertaking web disclosure to boost disclosure and transparency (Sharma, 2013). It does not mention what type and how the information regarding web disclosure is to be made. The following hypothesis was formulated to check the relationship between listing status and the level of web disclosure:

H7: The listing status of a bank as measured by the total number of national and international listings has a significant impact on the average web disclosure score.

Leverage

The leverage of the banks also affects the level of web disclosure scores. It indicates the proportion of debt and equity in the capital of the banks. In the case of banks, the RBI set a leverage ratio of 3%, and the concept of the leverage ratio is taken from the Basel III guideline, which is 3%. However, the Indian regulator has set the leverage ratio for banks at 4.5%. Previous studies were heavily dependent on the agency theory, which explained that highly leveraged firms would be keen to enlarge the scope and quantity of web disclosure as it may reduce the costs of debt in their capital structure (Ahmed, 1996; Arussi et al., 2009; Ismail, 2002; Oyelere et al. 2003). It is argued that banks with a high ratio of debt to equity have a high level of financial risk, and thus, they disclose more to reduce the risk. Detailed information has to be disclosed in order to convince about the creditworthiness of the banks. Mixed evidence has been revealed by previous literature to explain the relationship between leverage and the extent of web-based disclosure.

However, studies of Kelly (1994), Wallace et al. (1994), and Al-Hajaya (2014) reveal a contradictory finding, where they found a negatively significant association between the debt ratio and levels of disclosure. Low-leveraged firms have a small number of creditors, where information can be communicated directly Bollon et al. (2006). The leverage of a bank can be measured in a number of different ways, such as the ratio of total debts to total equity, the ratio of total debts to total assets, the ratio of total assets to equity share value, and more. In the present study, the ratio of total debt to total equity has been used to measure leverage to check the relationship between leverage and the level and extent of web-based disclosure. The following hypothesis was formulated to check the relationship between leverage and the level of web disclosure:

H8: The leverage of a bank as measured by debt-to-equity ratio has a significant impact on the average web disclosure score.

Foreign Ownership

Another variable that was considered in order to evaluate the web disclosure score is the ownership, which usually comprises domestic or foreign ownership. Banks extending their operations multi-nationally are required to report more detailed information on the websites and follow higher standards of reporting for a number of reasons. First, banks need to increase disclosures relating to websites, as it proves their transparency and competitive strength. Second, the banks have to fulfill the regulatory guidelines of both the host country and the parent country (Ahmed, 1996). Third, foreign banks are usually equipped with superior ICT software tools, efficient management, and the capacity to disclose more information without incurring increased costs of processing. Lastly, foreign banks have to face in-depth inspection of political and economic groups in the host country, and they have good reason to report more information to avoid the pressure of these groups.

A large number of banks that operate in India are in foreign ownership, and these foreign owners are mainly from developed nations with developed capital markets. Foreign shareholders may be more aware of the importance of web-based disclosure than domestic owners, and it can be said that foreign shareholders have a positive impact on the level and extent of web-based disclosure. Due to geographical division, foreign shareholders often suffer from information asymmetry problems more than domestic shareholders, as they usually experience difficulty in gaining access to paper-based corporate disclosure (Henchiri, 2011; Xiao et al., 2004). Also, in order to attract potential customers, banks may undertake website disclosures to satisfy their diversified needs (Al-Htaybat et al., 2011). Studies such as Al-Htaybat et al. (2011) and Henchiri (2011) found a positive relationship between ownership and the extent of web-based disclosures.

However, the findings of AbuGhazaleh et al. (2012), Bollon et al. (2006), and Xiao et al. (2004) did not find any evidence supporting the association between foreign ownership and web-based disclosures. These studies show that foreign shareholders are holding larger amounts of shares and are capable of getting the required information directly from the banks as part of top management. Foreign shareholding has been measured by the number of foreign shareholders in the ownership structure of a bank. The following hypothesis was formulated to check the relationship between ownership and the level of web disclosure:

H9: The ownership of a bank as measured by foreign shareholding has a significant impact on the average web disclosure score.

Type of Sector

The type of sector also influenced the level of web-based disclosure. Different sectors possess divergent characteristics being owned by different stakeholders (Xiao et al., 2004). Public sector banks are owned by the government, while private sector banks are in private hands. Foreign sector banks are mostly owned by the state as well as by private domestic shareholders. Due to competition and internationalization in the banking system, different practices are being followed by public, private, and foreign sector banks. Signaling theory also suggests that the owners and managers are keen to improve web disclosure practices, in order to increase the firm’s stock prices in the capital markets (Healy & Palepu, 2001; Mangena & Pike, 2005). The following hypothesis was formulated to check the relationship between categories of banks on the level of web disclosure:

H10: The type of sector as measured by bank category has a significant impact on the average web disclosure score.

Research Methodology

A number of statistical techniques can be applied to analyze data and test the research hypotheses. Regression analysis techniques have been widely used by researchers in previous studies to test the relationship between the extent of disclosure (dependent variable) and the company-specific attributes (independent variables) (AbuGhazaleh et al., 2012; Al-Htaybat et al., 2011; Cooke, 1989; Hossain et al., 2009; Hossain & Reaz, 2007; Hossain, 1994; Sharma, 2013). In this study, panel data statistical analysis has been performed to investigate the correlation between the extent of web-based disclosure and commercial bank attributes. The following subsections outline these statistical techniques.

Panel data refer to multi-dimensional data frequently involving measurement over time. It contains observations of multiple phenomena observed over multiple periods for the same banks. It is also called longitudinal data or cross-sectional time series data. Panel data model pools the observations over time as well as cross-sectional. It provides more information about data with a higher degree of freedom, higher efficiency, less collinearity among variables, and more variability (Gujarati, 2008). Therefore, it is more beneficial than cross-sectional data or time-series data. Panel data analysis has been used when the data are both cross- sectional and time series in nature. In this study, data from public, private, and foreign banks for 4 years has been collected, which indicates the need to apply panel data regression analysis. In order to identify the association between attributes of web disclosure practices, panel data regression model has been applied to test the developed hypotheses. It is vital to assess the validity of this model before analysis.

In the present study, balanced panel has been used for panel analysis. To see the relationship between various attributes on the web disclosures of Indian commercial banks, the following model was employed to examine the relationship between various attributes and web disclosures by banks:

Where

Y it = Dependent Variable (Web Disclosure Score) for bank i in period t

α0 = Constant

X1 = Size of Bank (Log of Total Assets), and (Log of Total Deposits)

X2 = Age of Bank

X3 = Profitability of Bank

X4 = Market Discipline (CAR), and Market Discipline (NPA)

X5 = Listing Status of Bank

X6 = Leverage Ratio of Bank

X7 = Foreign Ownership

X8 = Type of Sector

ε it = Error Term

i = indicating bank

t = time

This study develops hypotheses concerning the association between the web-based disclosure of banks and different characteristics of banks such as bank size, market discipline (CAR), profitability, listing status, type of ownership, and type of sector. These variables have been discussed in the following sections.

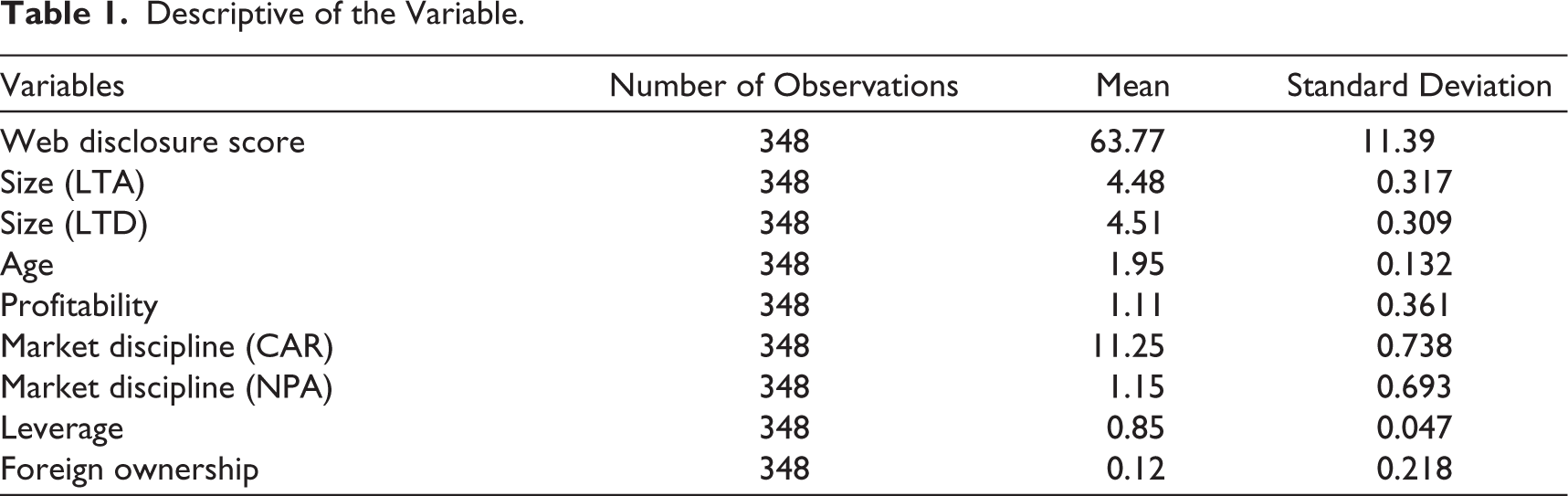

Table 1 presents the descriptive statistics for the given data set. The sample of the study for this objective was 87 banks for the time period of 4 years (2016–2019). The result of Table 1 indicated that the average web disclosure score of Indian commercial banks was 63.77% with a standard deviation of 11.39. In the case of the size, it showed a mean of 4.48% and 4.51% and a standard deviation of 0.3179 and 0.3097, respectively. The age of the banks has shown an average of 1.95% and a standard deviation of 0.132. Moreover, profitability is showing an average of 1.11% and a standard deviation of 0.361. Further, market discipline based on CAR turns out to be mean of 11.25%, and market discipline based on NPA turns out to be mean of 1.15% and a standard deviation of 0.738 and 0.693, respectively. Leverage measured as a debt-to-equity ratio has shown an average of 0.85% and a standard deviation of 0.0472. Foreign ownership has shown a mean of 0.12% and a standard deviation of 0.218.

Descriptive of the Variable.

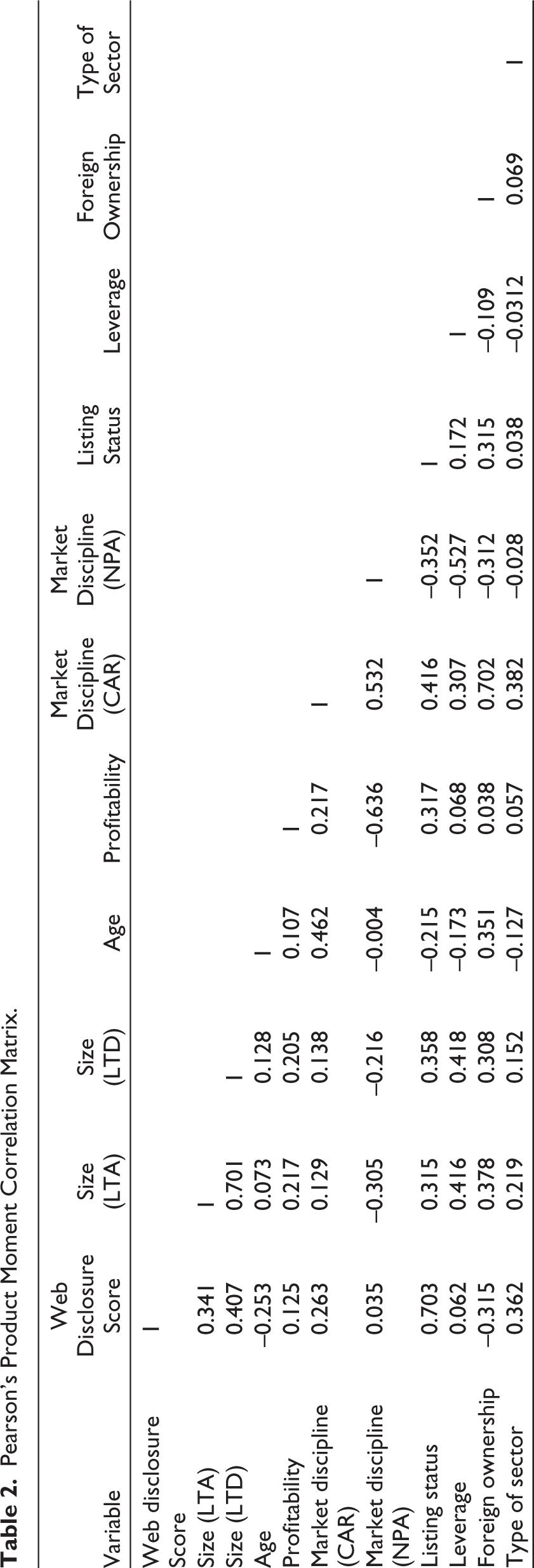

Further, the nature of the relationship among various attributes affecting web disclosure has been obtained through correlation. These coefficients of correlation helped in the identification of different variables moving in the same or different directions. It was also helpful to check the presence of multicollinearity among the explanatory variables. If the pair-wise correlation coefficient between two regressors is more than 0.8, then there is a problem of multicollinearity as per the rule of thumb (Gujarati, 2008). This has been computed through the Pearson Product Moment Correlation method. A correlation matrix of all the values of r for the dependent variable along with explanatory variables is shown in Table 2.

Pearson’s Product Moment Correlation Matrix.

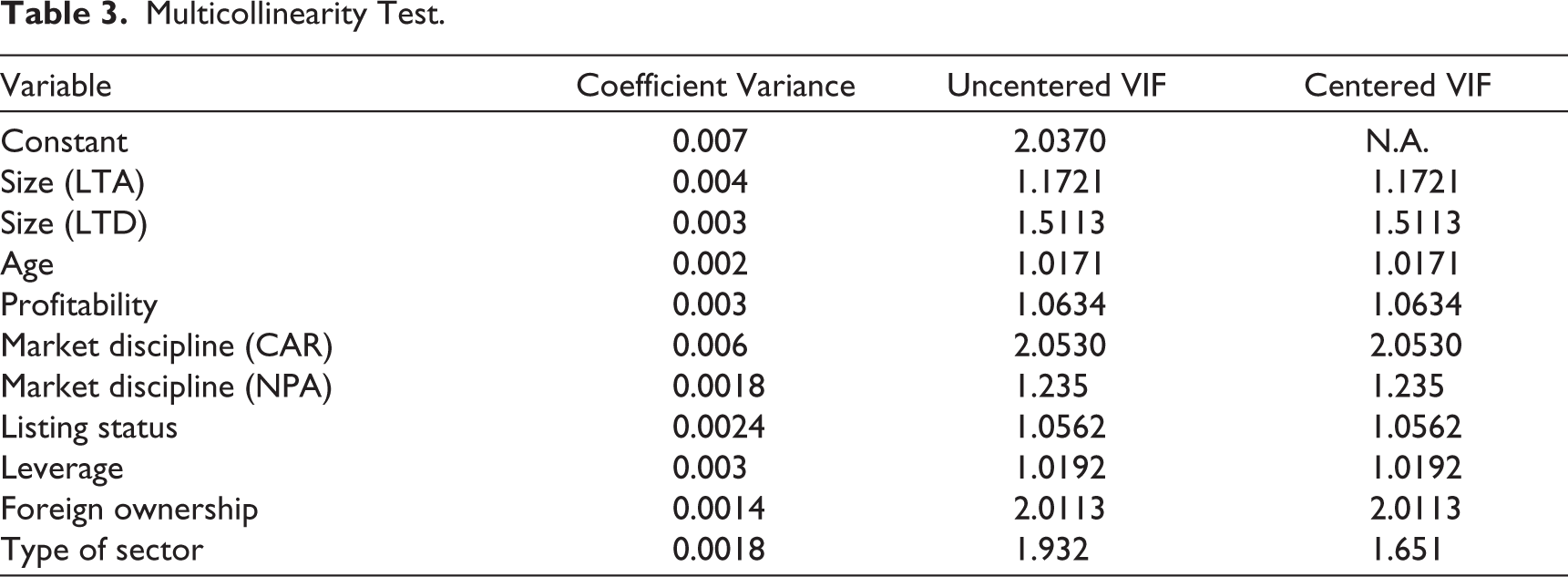

The result of Table 2 indicated that there was no coefficient of the correlation matrix which was greater than 0.8. Thus, there was no severe problem of multicollinearity among the explanatory variables. Multicollinearity was a matter that can be judged from a correlation matrix. Otherwise, the variance inflation factor (VIF) can be calculated to check it. It is presented in Table 3. VIF helps in diagnosing the data for possible levels of multicollinearity. None of the VIF values in the table are above 5, so there was no problem with multicollinearity in the panel dataset, as indicated in Table 3.

Multicollinearity Test.

Hausman Test for Fixed Effect Model or Random Effect Model

Hausman test has been used to check the applicability of fixed effect model (FEM) or random effect model (REM). The null hypothesis under Hausman test is that the coefficients estimated by the FEM are the same as the coefficients estimated by REM. When p value indicates insignificant value and the probability is more than chi-square (Prob. > chi-square higher than 0.05), then REM is used; otherwise, FEM is a better option. The results of the Hausman test are given in Table 4.

Hausman Test Results for FEM or REM.

The results in Table 4 showed that in the case of the independent variable of web disclosure, REM is a better choice than FEM because the probability was higher than chi-square (Prob. > chi-square higher than 0.05). Since in the panel data regression model, a set of attributes affecting web disclosure, the type of industry was also taken as dummy variables, therefore the REM can be relied upon to evaluate the regression results. REM is also referred as a variance component model or an error component model.

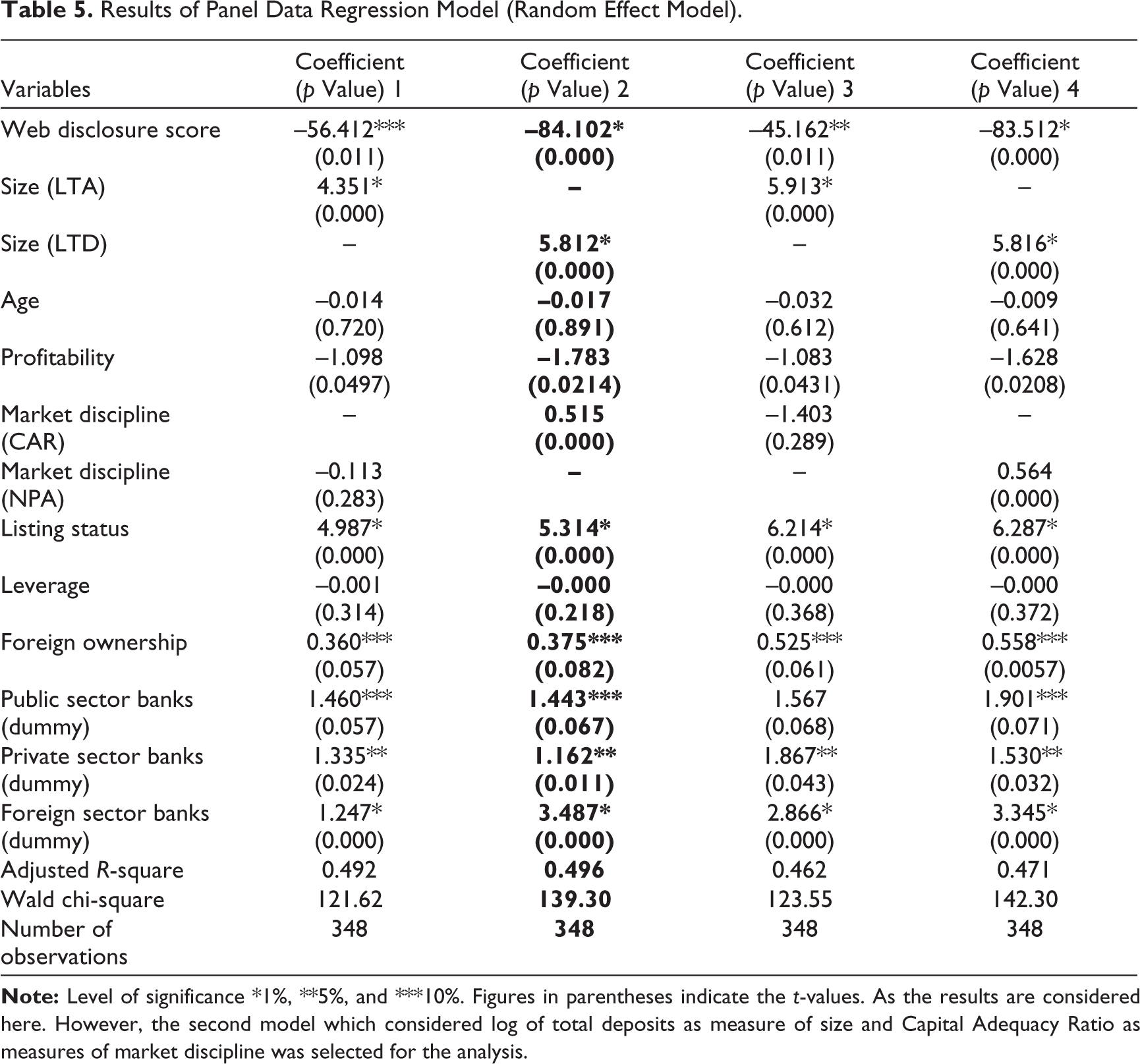

Results of Panel Data Regression Model

Table 5 shows the results of panel data regression model where the web disclosure score was the independent variable.

Table 5 shows the results of hypotheses developed as attributes affecting web disclosure scores in Indian commercial banks. It consisted of 348 observations for the period 2016–2019 with 87 banks as the sample of the study. The table presents the results of panel data regression analysis of the Indian commercial banks that highlighted the relationship between various attributes on the extent of web-based disclosure practices. The four models of regression equation were formed, which considered the measures of size as total assets and size as total deposits, measures of market discipline as CAR, and market discipline as a ratio of NPA to net advances one by one. The results of all the models were almost similar with some variations.

However, the second model, which considered the log of total deposits as a measure of size and CAR as a measure of market discipline, was selected for the analysis. The panel data regression model second gave an adjusted R2 of 0.496 with Wald chi-square value of 139.30, which signifies that 49.6% variation has been explained by all the independent attributes collectively. This model was the best-fit model with the highest adjusted R2. The other three models were also giving almost the same results.

Testing the Hypotheses

H1: The size of a bank as calculated by total assets has a significant impact on the average web disclosure score.

H2: The size of a bank as calculated by total deposits has a significant impact on average web disclosure score.

The results of panel data regression supported the significant and positive impact of the size of a bank in terms of total assets and total deposits on the average web disclosure score. It can be seen from Table 5 that size as measured by total assets and total deposits has a positive and statistically significant (at 1% level of significance) relationship with the web-based disclosure of information of Indian banks. It depicted that large banks are disclosing more information than small banks. Results were similar to the assumptions of agency theory, which states that larger companies have greater agent costs and greater disclosures can reduce such costs (Pervan & Bartulović, 2017). Our results were in line with the previous researchers like Al-Motrafi (2008), Hossain et al. (2009), Aly et al. (2010), Ezat and El-Masry (2008), Kelton and Yang (2008), Arussi et al. (2009), Elsayed (2010), Al-Htaybat et al. (2011), AbuGhazaleh et al. (2012), Sharma (2013), Mahajan (2014), and Pervan and Bartulović (2017), who found a positive relationship between the size of a bank and the average web-based disclosure score. There can be many reasons for significant and positive impact of size of a bank with the extent of web-based disclosure. First, larger banks generally have a more diverse product range and wider customer networks than smaller banks. As a result, larger and more diverse management information systems were required for management and control. Second, larger banks can procure capital more easily and cheaply from the capital market through extensive disclosure of information on their websites (Bonson & Escobar, 2002). Third, it was also argued that there can be information asymmetry among investors and management because of the greater number of stakeholders in the case of larger banks, so more website disclosures might be used in order to reduce the problem of information asymmetry (Debreceny et al., 2002). Lastly, large-sized banks were in a position to easily adapt to advanced digital technology. These banks can meet the growing demands of present as well as potential users (Mahajan, 2014). The presentation and content features of information disclosed on the websites are supposed to be increased in the case of bigger firms because the costs of managing and maintaining the websites will be reduced due to the large scale of economies (Al-Hajaya, 2014). Pervan and Bartulović (2017) state, “Large firm disclosed more extensive information than do small firms.”

Results of Panel Data Regression Model (Random Effect Model).

However, contrary to this, Allam and Lymer (2003), Hossain and Reaz (2007), Aly et al. (2010), and Henchiri (2011) found an inverse relationship between a company’s size and the extent of website disclosure.

The value of coefficient of this variable was 3.812, which is statistically significant at 1% level of significance. It seemed to be a good predictor of web-based disclosure level of public, private, and foreign banks. Thus, H2 has been accepted.

H3: The age of a bank has a significant impact on the average web disclosure score.

The results of panel data regression exhibited that the age of a bank has an insignificant relationship with average web disclosure. It can be seen from Table 5 that age as measured from its incorporation date has an insignificant relationship with the web-based disclosure of information of Indian banks. It depicted that young banks are disclosing more information than old banks. The results of the present study were in consonance with those of the past research conducted by Chander (1992), Hossain et al. (2009), and Mahajan (2014), which found insignificant and negative relations between age and disclosure score. It was argued that old banks are more rigid and unlikely to implement the adjustments required by the changed circumstances. Mahajan (2014) mentioned that age is not a predictor of disclosure score of banks, as “New generation banks were disclosing more as compared to older banks. The reasons being young banks are more flexible and adaptable to changing environment as compared to older banks.” Cooke (1991) argued that young companies would have an incentive to disclose more information on the websites in order to raise the confidence of stakeholders.

However, contrary to this, Hossain et al. (2009) found a positive relationship between the company’s age and the extent of website disclosure. Old companies have a long track record, and they were likely to disclose more information on their websites. These companies have good reporting systems at lower costs. Older companies have more experience and were likely to include more information in order to make a good image in the market (Choi & Sohn, 2005).

The value of coefficient of this variable is –0.017. It does not seem to be a good predictor of the extent of web disclosure. Thus, H3 has been rejected.

H4: The profitability of a bank as measured by ROA has a significant impact on the average web disclosure score.

Table 6 indicates that profitability has a positive and significant impact on web disclosure scores at 10% level of significance. The results of this variable were akin to the results of Craven and Marston (1999), Akhtaruddin et al. (2009), Hossain et al. (2009), Aly et al. (2010), Al-Htaybat et al. (2011), and Henchiri (2011), who found a significant relation with web disclosure. When companies use digital media for dissemination of information, it results in a high level of mass communication with various users, which lead to higher user satisfaction. Signaling theory stated that profitable companies disclosed more detailed information in order to signal their quality to investors, which in turn increases the company’s share price in the market (Marston & Polei, 2004). Agency theory also suggested that highly profitable companies get advantages to disclose more information as managers can adopt website disclosures in order to reduce information asymmetry; improve and maintain the reputation of company (Singhvi & Desai, 1971). It may also be argued that profitable companies have extra financial resources for the voluntary disclosure of information.

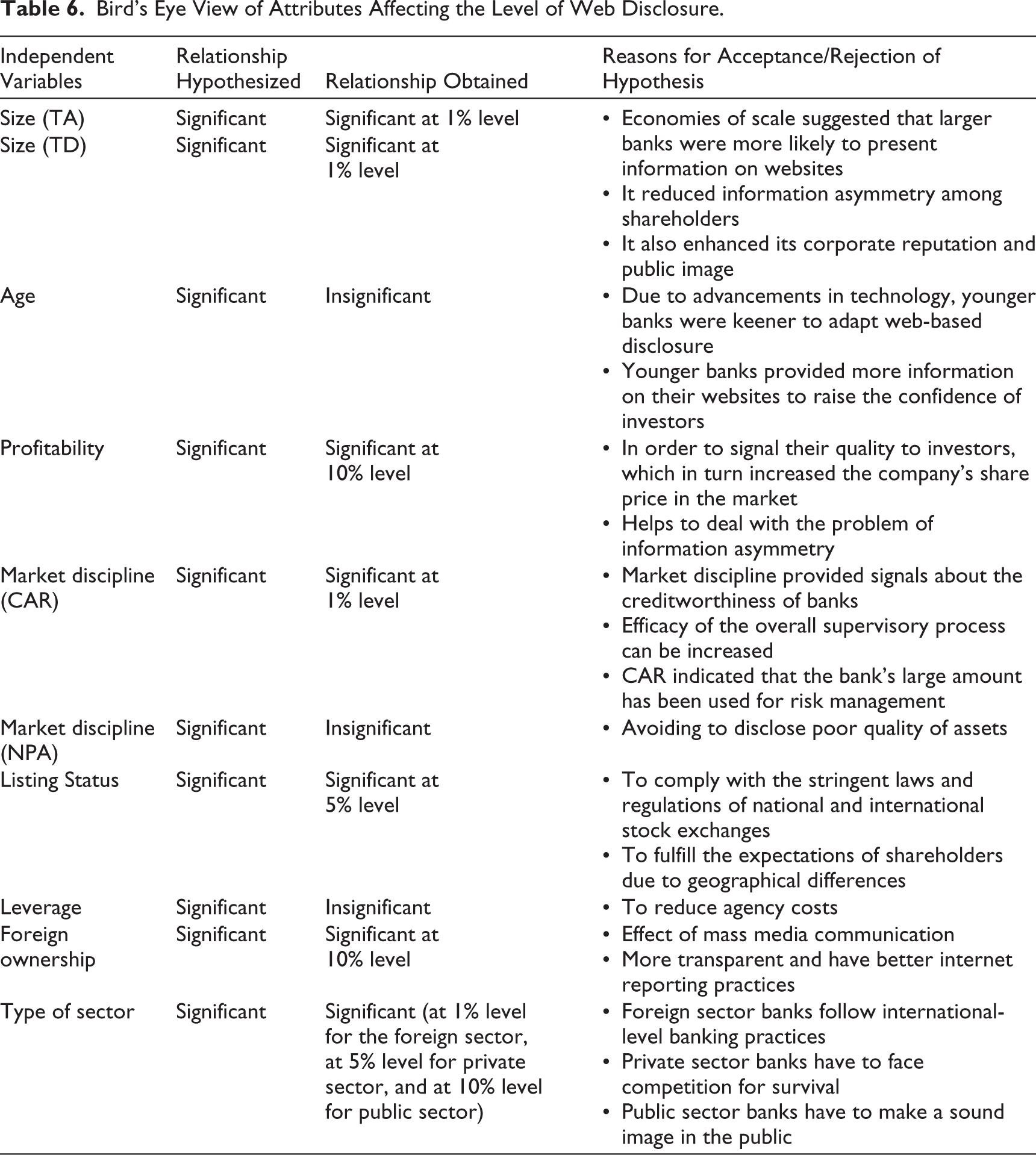

Bird’s Eye View of Attributes Affecting the Level of Web Disclosure.

But it was not corroborated with the studies of Ettredge et al. (2001), Oyelere et al. (2003), Marston (2003), Xiao et al. (2004), Al-Motrafi (2008), Ojah and Mokoaleli-Mokoteli (2012), and Mahajan (2014), who claimed that highly profitable companies might seek to avoid public intervention costs such as litigation as per the political cost theory (Oyelere et al., 2003). These companies preferred to lessen the level of disclosure as it has an effect on the competitive situation (Elsayed, 2010). On the other hand, “Less profitable banks try to explain the reasons for poor financial performance and mitigate negative consequences and loss of reputation” (Pervan & Bartulović, 2017).

The value of coefficient for profitability was 1.783 and is significant at a 10% level of significance. It seemed to be a predictor of web-based disclosure level of public, private, and foreign banks. Thus, H4 has been accepted.

H5: The market discipline of a bank as measured by the CAR has a significant impact on the average web disclosure score.

H6: The market discipline of a bank as measured by NPA has a significant impact on the average web disclosure score.

The results of panel data regression model specify positive and significant relation with the CAR and the extent of web disclosure of Indian commercial banks. It indicated that the banks with high CARs have been disseminating more information as compared to other banks. The results corroborated the past research done by Hossain et al. (2009) and Mahajan (2014), who found a significant relationship between CAR and web disclosure. The objective behind this high level of disclosure is to get the strong position in the eyes of users because the disclosure of CAR has become obligatory in the annual reports as per guidelines of SEBI and Pillar III of Basel II norms. On the other hand, banks with a high NPA ratio to net advances disclose generally less, as it indicated the poor quality of assets in the balance sheet. However, the results were not in consonance with Pervan and Bartulović (2017), who found that the CAR does not have any impact on the bank’s online disclosure practices. It is argued that larger banks have better risk management practices.

Market discipline based on CAR was found significant at 1% level of significance. The value of coefficient for this variable was 0.515, which was positive and statistically significant. So, it proved to be a good predictor of the web disclosure score of Indian commercial banks in this study. Thus, H5 has been accepted.

H7: The listing status of a bank, as calculated by the total number of national and international listings, has a significant impact on the average web disclosure score.

The result of panel data regression showed a positive and significant relation between listing status and web disclosure of Indian commercial banks at 1% level of significance. The results of this factor were in line with the literature of Oyelere et al. (2003), Xiao et al. (2004), and Hossain and Taylor (2007). Listed companies have to provide detailed information if they are listed on foreign stock exchanges in addition to the national stock exchange. First, foreign-listed companies have to comply with the stringent laws and regulations of not only the host country but also the parent company, and higher standards of accounting and reporting are maintained as per the rules. These have to follow the stringent laws of stock exchanges to meet the requirements of SEBI and also of the investors because of more publicly visible. Second, the information asymmetry problem was expected from foreign stakeholders due to the geographical separation between management and owners (Creswell, 2003). Third, foreign-listed companies were under closer supervision from various political and pressure groups within the host country that view them as sources of economic exploitation and agents of imperialist power. Finally, separation of ownership has been empirically found to be an important variable in explaining the reason for the disclosure of information on the website (Creswell, 2003; Hossain, 1994; Leftwich et al., 1981), and the demand for information is expected to be greater when foreign investors hold a high proportion of shares.

However, it does not corroborate with the empirical findings of Hossain and Reaz (2007), which stated that mandatory disclosures were given priority over voluntary information in Indian commercial banks.

The value of coefficient for this variable was 5.314, which was positive and statistically significant. So, it proved a good predictor of web disclosure score of Indian commercial banks in this study. Thus, H7 has been accepted.

H8: The leverage of a bank as calculated by debt-to-equity ratio has a significant impact on the average web disclosure score.

The result of panel data regression model specified negative and insignificant relations with leverage and the extent of web disclosure. It means the leverage of banks does not have any effect on the web disclosure level. The results corroborated the past research done by Leftwich et al. (1981), Wallace (1994), Brennan and Hourigan (2000), Debreceny et al. (2002), Joshi and Al-Modhahki (2003), Oyelere et al. (2003), Bollen et al. (2006), Arussi et al. (2009), Singh (2013), Sharma (2013), and Mahajan (2014). Agency Theory suggested that proportionately higher costs will be there if more debt was present in the capital structure which adds extra costs associated with dissemination. Oyelere et al. (2003) explained that these extra costs may be due to the differences between online reporting and print-based reporting environment.

However, the results were not in consonance with Hossain et al. (1995), Brennan and Hourigan (2000), and Mahajan (2014), who found a significant relation between leverage and the extent of web disclosure score of companies. It was argued that highly leveraged companies would be keen to have detailed disclosures to enable creditors to assess the financial strength of the companies (Arussi et al., 2009). Moreover, due to the financial nature of the business of banks, these companies were required to disclose more depth detail of their assets and liabilities. Empirical evidence reveals that voluntary disclosure can reduce agency costs by facilitating the assessment of a firm’s ability to meet its debts. Leftwich et al. (1981) stated that there was an agency relationship between external creditors and internal creditors. Agency theory suggested that proportionately higher costs were there if more debt was present in the capital structure, which would add extra costs associated with dissemination, but this dissemination would provide more reliable information to debt providers and would in turn reduce agency costs.

The value of coefficient for leverage as a variable was very low and statistically insignificant. Thus, H8 has been rejected.

H9: The ownership of a bank as measured by foreign shareholding has a significant impact on the average web disclosure score.

Table 5 indicates that foreign shareholding has a positive and significant impact on the web disclosure score at 10% level of significance. Banks with foreign shareholdings were using the web as an additional medium to disseminate information to shareholders and have a high web disclosure score. The result of this variable was akin to the result of Bollon et al. (2006), Al-Htaybat et al. (2011), and Henchiri (2011). It was being stated that foreign shareholders’ demand for disclosure of information was expected to be higher due to geographical differences between ownership and management (Bollon et al., 2006). Also, companies with foreign ownership were more transparent and had better Internet financial reporting practices than those with domestic ownership (Pervan & Bartulović, 2017).

But it does not corroborate the studies of Xiao et al. (2004), Bollon et al. (2006), and AbuGhazaleh et al. (2012), who claimed that there is no significant relationship between types of owners and information disclosure. The reason may be that shareholders are the owners of the company, and they are capable of getting the required information directly from the company because of their direct involvement in the company’s top management.

The value of coefficient for this variable was 0.375 which is positive and statistically significant at 10% level of significance. So, it proved a good predictor of the web disclosure score of Indian commercial banks in this study. Thus, H9 has been accepted.

H10: The type of sector as measured by bank category has a significant impact on the average web disclosure score.

Table 5 depicts the type of sector that has a significant impact on the extent of web disclosure score in the case of foreign sector banks at 1%, private sector banks at 5%, and public sector banks at 10% level of significance. Verma (2010) found a significant positive association between the type of sector and the level and extent of web-based reporting. Foreign sector banks incorporated changes in their websites as per international banking practices as well as national practices, so they provided more updates. Private sector banks also followed these banks to expand their business and to serve national and international users. Private sector banks provide innovative services to customers at a much faster pace than public sector banks. Private sector banks have grown by leaps and bounds in the last few years. These banks were spreading their wings at a much faster rate than public sector banks. Public sector banks were lagging behind private and foreign sector banks, but even at 10% level they are giving significant results.

Studies of Wallace (1994); Craven and Marston (1999); Brennan and Hourigan (2000); found negative or no association with the level of disclosure. This may be due to the fact that different types of industry categorizations were used in previous research. Differences in disclosure levels between different sectors could also be attributed to the high level of voluntary disclosure by a particular company from the whole sector, which leads to a bandwagon effect (Cooke, 1989). Signaling theory provides that companies within the same sector tend to adopt the same level of disclosure. If a company within a sector fails to follow the same disclosure practices, including internet disclosures, as others in the same sector, then it may be interpreted as a signal that the company is hiding bad news (Craven & Marston, 1999).

The value of coefficient for foreign sector banks was 3.487, which is significant at 1% level of significance. Private sector banks were significant at 5% level of significance with 1.162 value of coefficient. The value of coefficient was 1.443 for public sector banks, which was significant at 10% level.

These attributes affecting the level of web disclosure score along with their significance levels are shown in capsule form in Table 6 as follows:

Six variables (size, market discipline [CAR], profitability, listing status, type of ownership, and type of sector) moved in the predicted direction. These have a significant relation with the level of web disclosure. But the other three variables (age, leverage, and market discipline [NPA]) have an insignificant relation with the web-based disclosure level as compared to the predicted direction.

“The importance of good regression equation lies in the fact that the model is correctly specified; that the regressors have the correct (i.e., theoretically expected) signs, and that (hopefully) the regression coefficients are statistically significant at the lowest possible level (1% or 5%) of significance” (Gujarati, 2008). In the present study, four variables out of nine have been found significant (at 1% or 5%) namely, size, market discipline (CAR), profitability, and listing status. The variation explained by independent variables was modest but significantly influenced the disclosure score. The value of the Wald chi-square was also significant at 1% level, which shows the fitness of all the models.

Conclusion

The present study is a comprehensive one that has taken into consideration a comparatively larger number of attributes that affect the web-based disclosure practices of Indian banks. But it was found that the extent of website disclosure, being voluntary, lower than the disclosure of information at the mandatory disclosure level. Most information disclosed on the internet is concerned with general and marketing-related information. The results also identified that the private and foreign sector banks disclosed the highest level of information, while the public sector disclosed the lowest level of information on the internet. Thus, it can be concluded that the banks with a larger size, higher profitability, high CAR, listed on multiple stock exchanges, foreign ownership, and type of sector were disclosing more information on the website of banks. The study also provides evidence for factors related to the disclosure of information on the websites. This information would be useful to investors for making various investment decisions. The study has undertaken a checklist index to examine the extent of information actually disclosed by the banks. Banks can evaluate their organizations on the basis of that index and find out the reasons for the non-disclosure of that element used in the index.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.