Abstract

The present study contributes to our understanding regarding private-sector inflation expectations and how central bank communications influence them in an emerging economy like India. This study uses the Autoregressive Distributed Lag (ARDL) regression function to estimate the influence of the determinants on the survey of professional forecasters for a period ranging from Q1 2014–2015 to Q4 2021–2022. Our results demonstrate the significant positive influence of the lagged period inflation forecasted by the professionals and central bank communications in the form of inflation projections on the inflation forecasted by the professionals in the current period. Macroeconomic variables like repo rate, lagged realized inflation, GDP, merchandise exports and imports, and crude oil rates turned out to be non-significant in influencing the inflation forecasted by the professionals, at least in the short run. The literature highlights the importance of anchoring private-sector expectations by the central bank in an economy, and our results provide empirical evidence for the same, along with its implications on policy making.

Keywords

Introduction

Inflation expectations and inflation perceptions have not been studied much in the Indian context. Whether these expectations and the consequent decisions about spending are consciously made by taking into account all the available information or are merely naïve statements is still a matter of concern. In India, the central bank, the Reserve Bank of India (RBI), tracks the inflation expectations of households and professionals through the Inflation Expectations Survey of Household (IESH) and the Survey of Professional Forecasters (SPF), respectively. Moreover, the RBI forecasts (projections) inflation as a part of the flexible inflation targeting (FIT) policy regime. The expectations made by the private sector get influenced positively by central bank communications and monetary policymaking, which in turn influence the various macroeconomic aggregates (Hubert, 2015b).

Survey data on expectations and perceptions of households, professionals, and agents regarding inflation has increasingly become a vital part of central banks across the globe. The survey data on inflation expectations and perceptions significantly impact the effectiveness of the monetary policy at a macro level (Woodford, 2005). As inflation targeting is the main objective of monetary policy, how households and professionals expect and perceive inflation and incorporate them in their decision-making is pertinent for the efficacy of central banks.

As mentioned above professional forecast is also very necessary. Concerning this, many RBI reports have been published that took the professionals’ forecast on many macroeconomic indicators but here we focus mainly on the forecasts related to inflation. Some of the reports are as follows: the results pertaining to the survey conducted in March 2019 in which 25 panelists participated, using the measures of central tendency, results showed that the median forecast of headline Consumer Price Index-Combined (CPI-C) in Q4 of 2018–2019 was expected to be 2.4% and was expected to increase up to 4.2% in Q4 of 2019–2020. The CPI-C inflation excluding food and beverages, pan, tobacco and intoxicants, and fuel and light was expected to be 5.3% in Q4 of 2018–2019 and to 4.9% in Q4 of 2019–2020. In contrast, the Wholesale Price Index (WPI) for all commodities and WPI non-food manufactured products, the inflation was expected to be 2.9% to 3.6% and 2.7% to 3% from Q4 of 2018–2019 to Q4 of 2019–2020, respectively (RBI, 2019a). RBI (2019b) showed the survey results conducted in May 2019, in which 26 panelists participated. Again, using measures of central tendency, the report showed that the median forecast of headline CPI-C in Q1 of 2019–2020 was expected to be 3.1% and was expected to increase to 4.2% in Q4 of 2019–2020. The CPI-C inflation excluding food and beverages, pan, tobacco and intoxicants, and fuel and light was expected to be 4.5% to 4.8% from Q1 of 2019–2020 to Q4 of 2019–2020, whereas the WPI all commodities and WPI non-food manufactured products was expected to be 3% to 3.8% and 2% to 2.7% from Q1 of 2019–2020 to Q4 of 2019–2020 respectively. The latest report of RBI (2022) showed the results of the survey conducted in March 2022 in which 33, a larger number of professionals as compared to other reports, panelists participated. The median forecast of headline CPI-C in Q4 of 2021–2022 was expected to be 6.1% and was expected to decrease to 5.2% in Q4 of 2022–2023. CPI-C inflation excluding food and beverages, pan, tobacco and intoxicants, and fuel and light, was expected to be 6.2% to 5.6% from Q4 of 2021–2022 to Q4 of 2022–2023. For WPI all commodities and WPI non-food manufactured products, the inflation was expected to decrease from 12.7% to 5.1% and 9.6% to 4.4% from Q4 of 2021–2022 to Q4 of 2022–2023, respectively.

Inflation forecasts’ role in an inflation-targeting framework is vital as they act as an intermediate target (Raj et al., 2019). Croushore (1993) also emphasized the importance of forecasts by experts for the smooth running of an economy and hence suggested relying on the SPF. However, studies on inflation expectations in India are still at their nascent stage. Particularly, studies on inflation forecasts made by experts or professionals in emerging economies like India are scarce; hence, with this objective, the present study examines the effect of RBI communication on the survey-based inflation expectations of professional forecasters (SPF). This article studies the determinants of professional forecasters’ inflation expectations and how the central bank communications and other macroeconomic variables impact them. Lagged period inflation forecast by the professionals and RBI communication or the RBI inflation projections emerges as significant drivers of inflation forecasted by professionals for the current period. However, realized inflation, lagged period realized inflation, crude oil price rate, merchandise exports and imports growth rate, repo rate, and gross domestic product (GDP) do not significantly influence the SPF, at least in the short run.

This study contributes to the scarce literature on inflation expectations in the Indian context. This research will help the central bank and the policymakers understand the importance of central bank communications in anchoring inflation expectations of the professionals and their further role in the monetary policy transmission.

The rest of the article has been organized as follows: the second section presents a brief review of the literature. The third section discusses the objectives and hypotheses of the study. The fourth section includes a description of the data and the methodology adopted. The fifth section presents the results and discusses the findings. Finally, the sixth section concludes the article.

Review of Literature

Ehrmann et al. (2012) highlighted the lower dispersion among professional forecasters in key economic variables as a result of announcing a quantified inflation objective. The study used a large set of proxies for the data set of central bank transparency in advanced economies and employed simple ordinary least squares (OLS) to estimate the models. Hubert (2015a) analyzed the data of a set of central banks’ real-time inflation forecasts via OLS and found their positive influence on five countries’ private inflation forecasts. Hubert (2015b) found a positive influence of central bank communications on private inflation expectations, enabling them to interpret and predict future policy decisions correctly. Hubert (2017) found a positive influence of the interactive effects of both qualitative and quantitative communications of the central bank, European Central Bank on private-sector inflation expectations.

Goyal and Parab (2021) analyzed the impact of qualitative and quantitative communications of the RBI till November 2019 on professional forecasters by estimating the Carroll-type epidemiological models of expectation formation and got a large speed of adjustment of professional forecasts. They used the dictionary method constructed by Apel and Blix-Grimaldi (2012) and highlighted the impact of the choice of words in the RBI monetary policy after October 2016. Studies modeling qualitative communications also found the positive influence of transparent central bank communications on the formation of inflation expectations by professionals (Arango-Thomas et al., 2020; Ullrich, 2008). While focusing on the qualitative communication by the central banks in the form of speeches and statements, the study surveyed the literature and suggested the powerful role of central bank communication in moving financial markets to achieve the economy’s macroeconomic objectives (Blinder et al., 2008). Gertler and Horvath (2018) examined the impact of intermeeting communication among the European Central Bank’s Governing Council members. This study employed least squares and quantile regressions and found key members’ communication influence on the financial market with no significant influence on the exchange rates.

Gelain et al. (2019) reexamined the model with hybrid expectations developed by Smets and Wouters (2007) by using a dynamic stochastic general equilibrium (DSGE) model approach. In this survey, professional forecasters’ expectations were analyzed. The authors found that this model was a better overall fit than the models in which agents had fully rational expectations. The model with hybrid expectations was found to be closely linked with the inflation expected by the professionals in the survey.

A study of 25 countries by Capistrán and Ramos-Francia (2010) showed that there was smaller dispersion in inflation forecasts by the professionals among inflation-targeting countries compared to the countries that did not follow an inflation-targeting framework. The authors used fixed-effects estimator to test their macroeconomic model, which defined the anchoring of inflation expectations. Also, among developed and developing countries, developing countries had smaller dispersion in inflation forecasts after the implementation of inflation targeting. Dovern et al. (2012) researched various determinants of disagreements among the G7 countries, such as cross-sectional dispersion of individual forecasts and disagreements on economic activity, mainly GDP growth, inflation, and interest rates. The findings of fixed-event and fixed-horizon forecasts pointed out that the disagreements regarding GDP growth intensified during recessions. However, the price level, its sensitivity to macroeconomic variables, and its disagreement were higher in the countries in which the central banks became independent in the mid-1990s. Moreover, the findings established the importance of a credible monetary policy in anchoring inflation and interest rate expectations.

A study by Vránková (2012) highlighted the advantage of inflation targeting by the central banks and how the central bank tries to achieve its target by influencing the inflation expectations of individuals. Hayo and Mazhar (2014) studied the transparency of the monetary policy committee of 75 central banks by using an index to measure the educational and professional background of monetary policy committee members published on their respective websites. The study by employing the regression technique on the cross-sectional data of these central banks found the key components of monetary policy committee transparency (MPCT): past inflation, institutional indicators, and monetary policy strategy. MPCT exerted a significant effect on inflation variability and expectations. In addition, MPCT played the role of a compliment and a substitute for the institutional transparency of the central bank. Countries with an inflation-targeting regime had higher transparency than countries with monetary targets.

By using the New Keynesian Phillips Curve (NKPC) as an extensive case study, Coibion et al. (2018) suggested making inflation expectations a monetary policy tool for stabilization. Policymakers should alter the inflation expectations of the people so that perceived real interest rates would be changed, leading to changes in consumption, savings and investment. Berge (2018) examined how household-level and professional forecasters’ inflation expectations behave in the United States through boosting algorithms and found a relationship between household-level expectations and many macroeconomic variables like ongoing prices, food, and energy prices. Professional forecasters did not forecast rationally and made many deviations from rationality but correlated majorly with interest rates.

Patra and Ray (2010) and Pattanaik et al. (2020) found the vital role of inflation expectations in conducting monetary policy and their reflection on the credibility of the central banks. While the former used an autoregressive moving average (ARMA) framework for the analysis of the data on inflation expectations, the latter used hybrid versions of NKPC to examine the usefulness of survey-based inflation expectations to predict inflation. Pattanaik et al. (2020) also used ARDL and a vector error correction model for gauging the influence of household inflation expectations on wage-setting behavior in India. They both highlighted the role of anchored inflation expectations by the central banks in the effectiveness of the monetary policy. Woodford (2005) emphasized the role of communication from the central bank and the inflation expectations in the monetary policy effectiveness.

Bicchal and Raja Sethu Durai (2019) investigated the real-time inflation expectations from Google Trends. They used the Johansen co-integration and error correction model to complete the empirical analysis. They found that these had policy implications for the better conduct of monetary policy as they fulfilled the rationality properties, including efficiency and unbiasedness. Geraats (2014) drew out the importance of transparent monetary policy in reducing the private sector uncertainty and anchoring their expectations by making it more predictable. The study reviewed the theoretical literature and also studied the conceptual framework for central banks’ transparency and empirical evidence of the abovementioned findings.

A review of the extant literature presented above suggests that studies across many countries, primarily the developed ones, have highlighted the role of central bank communications, that is, quantified inflation objective and inflation targeting, in anchoring professional forecasters’ inflation expectations in the effective monetary policy of the countries. However, in developing economies, particularly in the Indian context, research on these issues is at a nascent stage. While some studies analyzed the different aspects of central bank communications and households’ inflation expectations in India, only a few addressed the relationship between central bank communication and professional forecasters’ inflation expectations. Hence, the present study attempts to contribute to the existing research using a different methodology and in-depth data analyses for a different time period characterized by adding a range of macroeconomic variables.

Objectives and Hypotheses

Objectives

The study by Goyal and Parab (2021) particularly motivated us to analyze further the survey-based inflation expectations of the professional forecasters with respect to central bank communications along with the inflation forecasted by professional forecasters at a previous time period and realized inflation of the past and present period. The objectives to be addressed in this study are as follows:

Objective 1: To examine the effects of RBI communication on the SPF. Objective 2: To examine the effects of inflation forecasted by professional forecasters at time Objective 3: To examine the effects of realized inflation at time

Hypotheses

On the basis of the abovementioned objectives, we formulate four hypotheses. Regarding the relationship between the central bank communication and survey-based inflation expectations of the professional forecasters, we conjecture that the RBI communication regarding inflation is likely to impact SPF positively since professional forecasters take into account the RBI communications, actions, and speeches directly. So, with the increase in the inflation projected by RBI, the inflation forecast by the professionals is also likely to increase and vice-versa. Based on the above argument, Hypotheses 1 is formed as follows:

H1: RBI communication has a positive impact on SPF.

Next, for Objective 2 on the impact of inflation forecasted by professional forecasters at time t −1 on the SPF, we surmise that professional forecasters take into account the lagged period forecasts made by them as they track all inflation information published by the RBI, so tracking back to their own expectations is likely to have a positive impact on their subsequent forecasts of inflation. Therefore, Hypothesis 2 is formed as follows:

H2: Inflation forecasted by professional forecasters at time

Furthermore, any dispersion between the professional forecasts and the realized inflation of the current and lagged period can be traced back. So, it is likely for professional forecasters to consider the realized inflation of both periods while forecasting. Hence, the low realized inflation of both periods is likely to have a low inflation forecast from the professionals and vice-versa. Hypothesis 3 and 4 are formulated as follows:

H3: Realized inflation at time H4: Realized inflation at time

Data and Methodology

The article is primarily based on pooled data from the SPF conducted by the RBI. The RBI conducts SPF, and the data has been available bimonthly since April 2014 after the adoption of FIT regime. The SPF is conducted across various institutions like commercial banks, stock exchanges, investment banks, credit rating agencies, and investment banks, etc. At least 25 professional forecasters respond to the survey each time, owing to the clause of anonymity. Professionals’ responses are only in the aggregate median forecast value of the inflation, that is, CPI-C in the survey. The responses in the SPF are the summarized results of the median forecast by the professionals on many key variables along with inflation, such as GDP, crude oil, exchange rate, and repo rate.

However, this study mainly focuses on inflation forecasts by professional forecasters. Since these surveys are conducted bimonthly and the forecasts are given for every quarter-end, we have taken the average of the median forecast for each quarter. 1 Moreover, the article includes data on macroeconomic aggregates, namely, GDP rate, repo rate, percentage growth in crude oil price, that is, crude oil price rate, export growth rate, import growth rate, and inflation rate as measured by CPI-C. The data includes quarterly observations of all the variables mentioned above for the period ranging from Q1 2014–2015 to Q4 2021–2022.

To study how the central bank communications and other macroeconomic variables impact the professional forecasts of inflation, we have developed a model and estimated it using the autoregressive distributed lag (ARDL) regression function. Since we are estimating the influence on the dependent variable by its lag value and the lag value of the other independent macroeconomic variables, we use the ARDL regression function, the general ARDL function is as follows:

where

For the model mentioned above, the ARDL equation function is

where

We use the one month lagged realized

2

inflation (Easaw et al., 2013; Ehrmann, 2015; Goyal & Parab, 2021) as one of the variables that can influence the professional inflation forecasts along with the crude oil price and merchandise export and import quarterly growth rate, repo rate, and GDP rate. For the variable

RBI states its inflation projections in the monetary policy statements as follows:

“... relative to the projections of the second bi-monthly statement, inflation projections in this bi-monthly statement are elevated by the higher than expected June observation but reduced by prospects of softer crude prices and a near-normal monsoon thus far. This implies that inflation projections for January–March 2016 are lower by about 0.2 percent, with risks broadly balanced around the target of 6.0 percent for January 2016...” (RBI, 2015)

Monetary policy statements also provide a wide analysis of the current and economic situation of the country across different sectors, as well as an outlook for the future economy. Apart from this, we have considered the lagged value of the inflation forecast by the professionals to see whether their own previous period forecast influences their current forecasts.

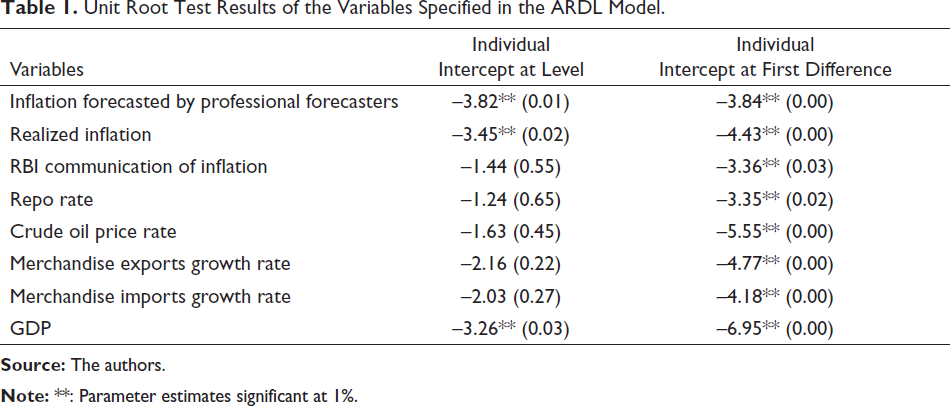

While conducting the ARDL test, the stationarity of the variables plays a vital role. The unit root test is done by using the augmented Dickey–Fuller test. All the variables in Equation (2) are found to be stationary at either I(0) or I(1); hence, the prerequisite for conducting the test is attained.

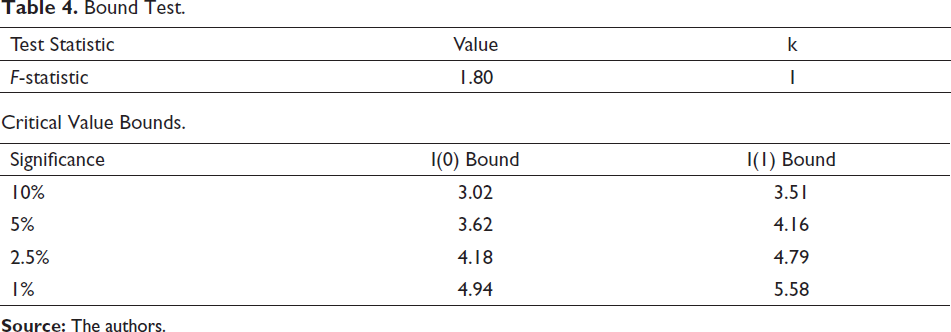

Furthermore, the absence of serial correlation or autocorrelation displayed in Table 3 by using the Breusch–Godfrey test confirms our equation specification. 3 The lag structure has been selected using Akaike’s information criterion. Furthermore, we have estimated the short-run ARDL test since no long-term relationship is found in our variables. This is verified by conducting the coefficient diagnostic long run and bound tests presented in Table 4. The series of variables are found not to be cointegrated with the help of the bound test.

Results and Discussion

Table 1 displays the results of the Augmented Dickey-Fuller test conducted to examine the stationarity of the variables of the model. Inflation forecasted by professional forecasters, realized inflation, and GDP have been found stationary at level, that is, I(0). The remaining variables, RBI communication of inflation, repo rate, crude oil price rate, and merchandise export and import growth rate, have been found stationary at the first level, that is, I(1). Hence, we got the mix of stationarity levels, I(0) and I(1), for all the variables, and the ARDL regression test can be conducted.

Unit Root Test Results of the Variables Specified in the ARDL Model.

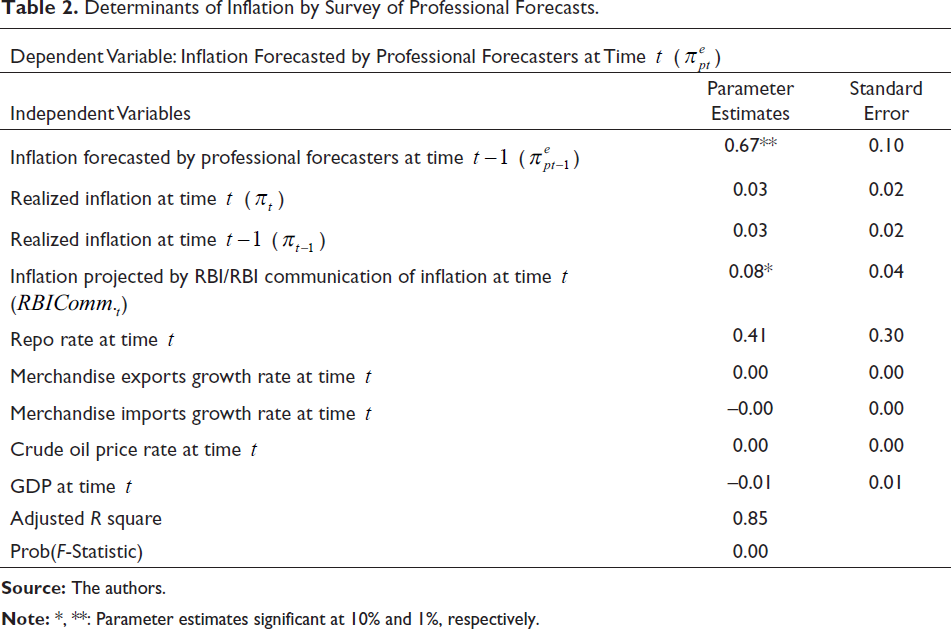

The estimates of Equation (2) are shown in Table 2. Table 2 shows the various determinants of inflation forecasted by the professional forecasters via the ARDL regression method in the short run. Here, we observe that the lagged period inflation forecasted by the professional forecasters has a significant positive influence on current period inflation forecasts by the professionals. Alternatively, we can say that a 1% increase in the lagged period inflation forecasts by the professional forecasters increases the current period inflation forecasts by the professionals by 0.67% in the short run, ceteris paribus. Hence, we accept hypothesis H2.

The influence of RBI’s projected inflation in the current period is again positive and significant. Similarly, keeping other factors constant, 1% increase in the inflation projected by the RBI for the current period increases the inflation expected by the survey professionals by 0.08% in the short run. Hence, we accept hypothesis H1. The rest of the variables, that is, realized inflation, lagged period realized inflation, crude oil price rate, merchandise exports and imports growth rate, repo rate, and GDP, fail to influence the inflation expected by the survey professionals significantly. They do not drive professional inflation forecasts in the short run.

Specifically, the realized inflation at time

Determinants of Inflation by Survey of Professional Forecasts.

Now, to test for the presence of serial correlation, we employ the Breusch–Godfrey test. We conducted this test since the ARDL equation considers the lag form of the dependent and independent variables on the right-hand side of the equation and there are chances that the residuals are serially correlated. The null hypothesis of this test states that there is no serial correlation in the residuals. Table 3 shows that the Prob(F-Statistic) is 0.67, greater than 0.05, hence failing to reject the null hypothesis. Alternatively, there is no serial correlation present among the ARDL model’s residuals and the equation specified for the model of ARDL is free from any biasness.

Breusch–Godfrey Serial Correlation LM Test of the Determinants of Inflation by Survey of Professional Forecasts.

In the next step, Table 4 shows the ARDL bound test conducted to know whether any cointegration exists among the series of variables in the model. The F-statistic value lies between critical bond values, that is, I(0) and I(1), accepting the null hypothesis of having no long-run relationship among the variables. The F-tests confirms the absence of cointegration and hence the presence of only short-run relationship among the variables.

Bound Test.

Therefore, our analysis indicates that RBI communication and the lagged period forecast by the professional forecasters anchor the expectations of inflation of the survey professionals in the current period. Our results showed the original evidence concerning India in support of the literature. The literature emphasizes the importance of inflation forecast by the private sector and how these inflation expectations get influenced by the central bank communication and the monetary policy transmission process and vice versa (Ehrmann et al., 2012; Goyal & Parab, 2021; Hubert, 2015a, 2015b, 2017). The results also show the credibility and transparency of the central bank while anchoring the inflation expectations of the professionals. RBI partly sets the future inflation targets and thus influences the inflation forecasts by the SPF, which comes out as the main determinant of future inflation (Goyal & Parab, 2021).

Conclusion

The present study contributes to the literature on inflation expectations, particularly in the Indian context. The study examines the determinants and their effects on the SPF conducted by the RBI during April 2014–2015 to March 2021–2022. The data set has been collected from the RBI database. We first analyze the data for its stationarity using the augmented Dickey–Fuller test. The results showed a mix of stationarity levels at I(0) and I(1). This fulfils the prerequisite for conducting the ARDL test. Second, we employed an ARDL model to fulfil our objectives. The results showed the positive influence of the RBI communication and the lagged period inflation forecast by the professionals, that is, at time

Furthermore, a host of other macroeconomic control variables turned out to be non-significant as a determinant for the inflation forecasted by professionals or SPFs. Moreover, to check the validity of the ARDL equation specification, we employ the Breusch–Godfrey test that confirms the absence of serial correlation among the residuals of the equation. Lastly, the ARDL bound test reveals the absence of cointegration and long-run relationship among the variables. Hence, the complete analysis has been in terms of the short-run period.

The present study’s findings have important implications for the economy’s monetary policy. This study shows how RBI can anchor the inflation expectations of the private sector via its communication in the form of an announced quantified inflation objective and inflation targeting. These anchored expectations play a pivotal role in successfully conducting an economy’s monetary policy. The shaping of private agents’ expectations by policymakers can make the implementation of monetary policy more effective, and private agents can predict policy decisions correctly (Hubert, 2015a, 2015b). Hence, this spiral of RBI inflation projections impacting inflation expectations and the resulting policy making can be used to conduct successful monetary policy and increase monetary policy credibility in the country.

This study provides empirical evidence supporting literature on the role of central bank communication while highlighting the importance of anchoring the private sector expectations by the central bank in an economy and their role in monetary policy transmission. However, this study has some limitations that should be addressed. Since the data on SPF is available on a bimonthly basis from April 2014 only, that is, after the adoption of the FIT regime, the time period considered in the study is relatively less. Also, the impact of other macroeconomic variables, apart from the ones mentioned in this study, can be seen on the SPF in terms of having relevant policy implications as the research on this subject is in a budding stage. Future research may consider similar surveys further published by the RBI for assessing improvement in them in terms of more data on the survey of professional forecast and other macroeconomic variables.

Footnotes

Availability of Data and Material

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.