Abstract

Technology impacts human life in multiple ways, and the internet offers the facility to perform traditional money transactions instantly. However, technology adoption is risky, and numerous risks hinder the intention formation from using e-money services. The current work investigates four types of associated risks (financial, service, time, and psychological risk) impacting the use intention for e-money services among Saudi Arabian and estimating the effect of e-money services knowledge on the use intention. For the existing cross-sectional study, quantitative data were collected in Saudi Arabia on social media. Analysis was executed with 328 valid sample data with the partial least square structural equation modeling software SmartPLS 3.3. Results revealed that e-money services’ financial, time, and service risks insignificantly influence the e-money usage intention. However, psychological risk and knowledge about e-money services significantly influence the use intention for e-money services. E-money services firms reduce financial, time, and service risk perceptions. Improving knowledge of e-money services and reducing the psychological risk build a favorable usage intention. The results help develop appropriate management and policy guidelines to facilitate Saudi Arabia to become a cashless society by 2030. The study’s limitations and future research options are stated at the end.

Introduction

The turn of the century brings the novel technologies that revolutionize our lifestyle, and the internet, mobile phones, and social media facilitate the infiltration of mobile personal use for everyday life activities (Karialuoto et al., 2020). The improved reliability and advances in mobile services empower mobile users to use mobile services consistently, enjoy the internet, and perform multiple activities for shopping, money transfer, and entertainment purposes (Karim et al., 2020). Smart mobile devices are now affordable, and mobile technologies (4G and 5G) facilitate mobile users to enjoy internet-enabled services (Seetharaman et al., 2017). The mobile phone also became a medium to send and receive money. The advent of smart mobile phones having the 4G and 5G connectivity facilitates the users to perform all the major banking and money related activities on go (Karim et al., 2020).

Electric money (e-money) services permit users to execute money transactions readily and swiftly in a protected style (Karialuoto et al., 2020). Users increasingly accept e-money to execute transactions online or perform everyday money transactions. E-money imitates a physical wallet and offers to perform different money transactions without using or keeping cash (Seetharaman et al., 2017). E-money empowers the users to complete the money transaction with efficacy and securely (Karim et al., 2020). E-money use enriches the users’ experiences with comfort and ease to secularly transfer the payment or execute daily purchases (Yuan et al., 2016).

The wide-ranging infiltration of mobile-run services allows the underprivileged, non-banking users to perform the money transaction expediently (Yaseen & El Qirem, 2018). Mobile devices have increasingly become a key to personal identity, and smartphone-based applications empower mobile users to instantly make and receive payments during COVID-19 (Singh et al., 2020). Reliable mobile connectivity eases the e-payment structures around the globe. The e-payment system facilitates USD 2 billion in transactions and serves 1 billion consumers globally (GSMA, 2021). Around 300 mobile payment service providers work in 95 nations, and the everyday traction can touch the USD 5 billion mark by 2025 (GSMA, 2021). At the same time, KSA is working to become a cashless society in pursuance of Saudi Vision 2030. The overall number of cash transactions significantly reduced recently, but 60% of the money transaction was made in cash (Fintech Saudi, 2021). The currently available facts depict that the acceptance of e-money increases in the KSA but still lacks to achieve the goals set in Vision 2030. It necessitates exploring the e-money factors influencing the user’s acceptance and adoption of e-money among Saudi Arabian respondents.

Cashless or e-payment already gained acceptance before the COVID-19 outbreak in the earlier part of 2020 (Senyo & Osabutey, 2020). The COVID-19-driven lockdown and strict travel conditions disturbed life across the globe. Going with cash also carries the risk of carrying the COVID-19 virus, and using mobile or electronic money (e-money) remains the only option to perform daily shopping activities (Verkijika, 2020). E-money is not widespread as the risk associated with e-money as technology (Singh & Srivastava, 2018). The Saudi Central Bank (SAMA) encourages the acceptance and adoption of e-money in the KSA. Three significant players are working in the e-money business in the KSA, and the market players are STC Pay, Hala, and Bayan Pay (Fintech Saudi, 2021). The Saudi financial technology sector needs to reconnoiter and recognize the fintech consumer risks experiences, improve the fintech consumer experiences, and build the acceptance and adoption of e-money services. The facts mentioned above direct us to explore the factors hindering e-money use. Therefore, the current research intends to discover the risk features that hamper the adoption of e-money services among the KSA residents and how the knowledge about e-money services can reduce the different types of associated risks to build the use intention for e-money services in KSA. The study results facilitate the KSA’s becoming a cashless society by 2030, as envisioned in the KSA vision 2030.

The following section briefly describes the pertinent literature to frame the study’s conceptual background and hypotheses development. Next, we present the discussion of the method espoused for the current study. Later the results of the study were offered in a discussion of the results. Then the current manuscript concludes with a debate on the study’s contribution to the limitation of the study.

Literature Review

Theoretical Foundation

Innovative services and technologies are permanently viewed as chancy to use, and users are unaware about using the technology-based services to achieve the maximum advantage from the technology or novel services (Suki & Suki, 2017). The higher risk perception deters the consumers from using the e-services (Arrifin et al., 2018). E-money services facilitate users, and for many users, e-money services are associated with the issues of secrecy and security to accomplish money-related transactions (Lwoga & Lwoga, 2017). Many consumers are still concerned about the fraud and lack of security for the users and feel that using e-services is the riskiest and avoid using e-money services (Yaseen & El Qirem, 2018).

The perception of risk for online shopping reduces the use intention for online shopping services; the financial, delivery security, and product risk negatively impact the use intention for the online shopping services (Verkijika, 2020; Verma & Sinha, 2018). Primarily e-money users are not satisfied with the security features and misuse of user identity in electronic transactions (Humbani & Wiese, 2019). Compatibility is also necessary to instigate the adoption of innovative technology, and compatibility facilitates the users to think positively about the novel technology that resembles the existing technology in use (Gumussoy et al., 2018).

Use Intention for E-money Services

The individual level of behavioral intention represents the possibility that the potential users participate in a specific behavior, like adopting new technology or services (Aji et al., 2020). Individual attitude formed with the availability of multiple technology-related attributes harnesses the exhibition of intention to use technology like e-commerce or e-money services (Pandey & Chawla, 2019). The intention is the proxy of the performance of actual behavioral adoption (Nawi et al., 2022).

Factors Affecting Intention to Use E-money

Financial Risk

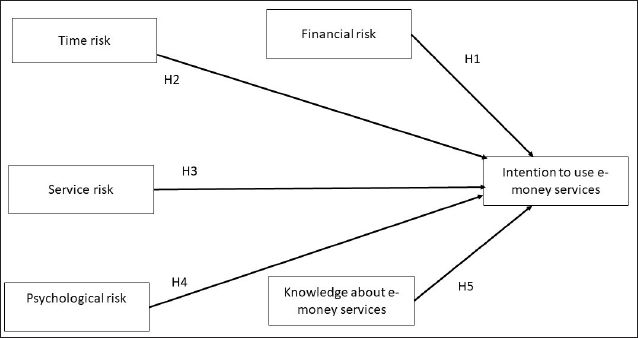

The technology use may bring financial risk, and users find it challenging to have a positive inclination toward using the technology (Yang et al., 2016). The financial risk depicts the probability of the money not being transferred accurately and may risk losing money transferred to the wrong person or destination (Nguyen & Huyuh, 2018). The money transferred online is credited to another account and cannot be returned to the sender without hassle (Aji et al., 2020). The higher awareness of financial risk curtailed the user’s intention to use the online platforms (Jeon et al., 2019). Financial risk entails building the form of vulnerability, and perspective users think twice before using digital money (Aji et al., 2020). The perception of elevated financial risk restricts prospective users from using technology services (Nguyen & Huynh, 2018). The sense of insecurity reduces the users’ intention to use the credit card or relevant technology to transfer money online (Farah et al., 2018). Ariffin et al. (2018) postulated that financial risk undesirably but significantly influences online purchase intention. We, therefore, propose the following for the study.

H1: Financial risk negatively and significantly affects the use intention for e-money among the KSA residents.

Time Risk

Technology offers the facility to the users and reduces the time to make a transaction (Dai et al., 2014). The online technology empowers the users to reduce the waiting time and complete the desired money or non-money activities (Gupta & Arora, 2019). Time-related risk is demarcated as trouble, waiting, and loss of time that occurs while using online technology to transfer money (Ariffin et al., 2018). Dai et al. (2014) postulated that the lack of efficiency in digital services initiates anxiety and distress for the technology users buying items from online platforms. Service delivery through technology requires a higher level of sync between all partners of the technology service providers to deliver the services as promised (Gupta & Arora, 2019). The inconvenience and difficulty in using technology instigate the perception of not using e-money transfer services (Han & Kim, 2017). In terms of online purchases, consumers find it is time-consuming to search, browse, buy and interval for the delivery of produce or service (Chopdar et al., 2018). The higher perception of time risk instigates the attitude to evade the use of technology (Dai et al., 2014). In a topical work, Ariffin et al. (2018) documented that the time risk adversely impacts the use of online technologies. We offer the subsequent hypothesis.

H2: Time risk negatively and significantly affects the use intention for e-money among the KSA residents.

Service Risk

Services are always associated with risk as the services are not delivered physically, and delivery entirely rests on the vendor or service provider’s capacity and willingness to please the consumers (Lai, 2018). The service risk contains the probability that the service may deliver all the attributes promised by the service provider and may not meet the consumer’s expectations (Nguyen & Huynh, 2018). The lack of information or change in service delivery instigates an adverse attitude toward using web services (Dai et al., 2014). The lack of consistency and quality services makes the e-services risky, and consumers face use the e-services is complicated (Senyo & Osabutey, 2020). Han and Kim (2017) postulated that the service risk significantly reduces users’ use intention for online services. Nguyen and Huynh (2018) documented that the risk of product and services negatively influence the intention to use online services for purchase. Therefore, we like to offer the subsequent for the study.

H3: Service risk negatively and significantly affects the use intention for e-money among the KSA residents.

Psychological Risk

The psychological risk represents the loss of self-respect, leading to frustration due to not delivering the right services (Yang et al., 2016). The state of regret and deterrent builds the mental pressure that reusing the technology may not yield the right and desired results (Ariffin et al., 2018). Psychological risk unfavorably instigates the online purchase intention (Hong & Cha, 2013). The perceived psychological risks adversely influence the consumers’ intention to use online technologies for purchase purposes (Chawla & Joshi, 2019). The remorse and frustration build the logical burden as the anticipated expectation is not realized and may affect future action. Ariffin et al. (2018) claimed that the perceived psychological risk adversely prompts the online shopping platforms use intention among Malaysians. We, therefore, suggest the next for the study.

H4: Psychological risk negatively and significantly affects the use intention for e-money among the KSA residents.

Knowledge About E-money Services

The knowledge helps facilitate better understanding and reduce the confusion about using technology (Karim et al., 2020). The consumers’ knowledge facilitates the users to find the product easy to use and builds confidence to use the technology like e-money services (Lwoga & Lwoga, 2017). The adequacy of knowledge nurtures the skills and favorable consideration toward e-money services (Senyo & Osabutey, 2020). The knowledgeable consumer starts feeling competent to use the e-money services and manage the privacy issue to transfer the money accurately (Verkijika, 2020). Lack of knowledge builds the frustration of using novel technology that restricts constructive opinion toward technology use (Senyo & Osabutey, 2020). Building consumer knowledge can facilitate positive attention toward technology use (Karim et al., 2020). Lwoga and Lwoga (2017) claimed that e-money knowledge raisings the users to positive inclination toward using e-payment among consumers from Tanzania. Consequently, we propose the following for the study.

H5: Knowledge about e-money services significantly and positively influences the use intention for e-money among the KSA residents.

Research Methodology

Sample Selection and Data Gathering

For the existing study, we assumed a cross-sectional empirical research design. The sample size estimation was executed in the G-power 3.1 with the model power = 0.95; effect size = 0.15 with the five exogenous constructs. The test result envisages having a minimum of 138 sample size to achieve the required power in the analysis (Faul et al., 2007). However, Hair et al. (2019) suggested having a minimum of 200 valid sample sizes to use the PLS-SEM. The data collection was performed using social media to have a sufficient response and less time and cost. The current study assumed a cross-sectional, quantitative, and survey-based design. The data collection was completed by online survey from December 2021 to January 2022; the snowballing effect helped to reach the study samples. The survey has a qualifying question to validate the respondents, and the respondents’ consent was obtained.

Measurement Scales

The questionnaire items for the present work were assumed from the formerly corroborated scales. The financial risk was assessed with the five items engaged from Hong and Cha (2013) and Ariffin et al. (2018). Time risk for the e-services was gauged with the four items assumed from Ariffin et al. (2018). Four items were employed to estimate the service risks and the items borrowed from Dai et al. (2014). The psychological risk was appraised with the four question items borrowed from Hong and Cha (2013) and Yang et al. (2016). The knowledge about e-money services was judged with the four question items assumed from Lwoga and Lwoga (2017). Lastly, use intention for e-money services was gauged with the five question items, the items adopted from the work of Karjaluoto et al. (2020). The Figure 1 offers the study model. The input variables were estimated with five-point Likert scales, while the outcome variable was measured with the seven-point Likert scale. The study scale was reviewed and permitted by the institutional research review board of Prince Sattam Bin Abdulaziz University, Alkharj, Saudi Arabia.

Study Model.

Calculation of Common Method Variance

Harman’s (1976) one-factor assessment was applied to appraise the subject of common method variance (CMV) (Podsakoff et al., 2003). Single-factor Harman’s test proves that CMV is not a severe subject in the current work as the single factor accounts for about 34.70% change and is under the suggested bound of 40% (Podsakoff et al., 2003).

Assessment of Multivariate Normality

Data set multivariate normality is not a critical issue for using SEM-PLS, as the SEM-PLS is a non-parametric investigation device (Hair et al., 2019). Though multivariate data normality was established on the endorsement of Peng and Lai (2012), web Power (

Data Analysis Method

Partial least squares structural equation modeling (PLS-SEM) was exploited by using the Smart-PLS software 3.3. to analyze. SmartPLS is a multivariate investigation software that gauges the constructs’ path model (Hair et al., 2019). SmartPLS authorizes the scholar to analyse the small data set with the issue of non-normality. Besides, the casual-predictive flora of the PLS-SEM facilitates using multifaceted models with composites, and it has no hypothesis of goodness-of-fit assessment like in the covariance-based SEM (Chin, 2010). A two-phase examination scheme is recommended to conduct the data investigation using the SmartPLS. In the first step, an assessment was achieved of the model to assess its reliability and validity of the model (Hair et al., 2019). The subsequent step accomplishes the structural model relations and examines study propositions with significance levels (Chin, 2010). The current model level assessment achieved with r2 and Q2; effect size (f2) defines the path consequence from the input variables for the outcome variable (Hair et al., 2019).

The importance-performance map analysis (IPMA) describes the input variables as comparatively low to high by conforming to the importance and performance of the outcome variable (Ringle & Sarstedt, 2016). IPMA helps uncover the conceivable areas that need decision makers’ attention to achieve higher performance. IPMA profiles in total consequence of the rescaled variable scores with the unstandardized technique (Ringle & Sarstedt, 2016). Rescaling distributes the latent variables into scores of 0 and 100. The mean score of the variable value indicates the performance of the input variable; here, 0 signifies the least, and 100 signifies the maximum noteworthy for the performance of the outcome variable (Hair et al., 2019).

PLSpredict is endorsed by Shmueli et al. (2019) to confirm the model’s critical outcome construct and scrutinize prediction errors. Predictive performance was assessed with the mean of Q2predict measurement for the authentication with the naïve measure premeditated by the PLSpredict technique (Shmueli et al., 2019). PLSpredict evaluates the naïve yardstick in the linear regression model (LM). Comparing RMSE or MAE scores for LM and PLS models can settle the two approaches’ explanatory supremacy. Shmueli et al. (2016) recommended that the PLS-SEM model has lower predictive power when the PLS-SEM model yields higher prediction faults than the LM standard. If the maximum PLS-SEM analysis brings greater prediction faults than the LM benchmark, it represents the PLS-SEM model’s low predictive power (Shmueli et al., 2016). If only a few paths of the PLS-SEM analysis produce higher prediction errors than the LM model, it specifies that the PLS-SEM model achieves the medium power. However, when no item in the PLS-SEM model produces more faults than the LM standard, the PLS-SEM model has superior predictive power (Shmueli et al., 2019).

Analysis of Data

Sample Demographic

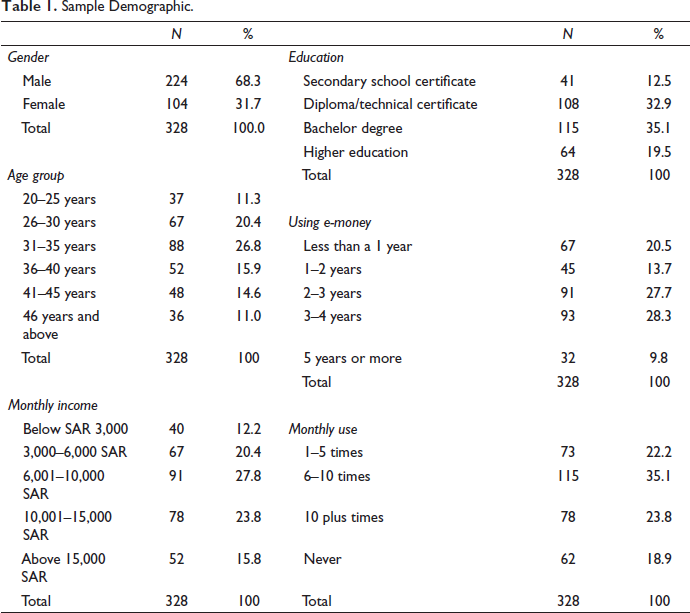

For the current work, data were gathered from young and educated Saudi residents, and 68.3% of the respondent were male. 26.8% of the study respondents were between 31 and 35 years, and 20.4% of the total respondents were aged between 26 and 30. 15.9% of the respondents were between 36 and 40 years of age, 14.6% were between 41 and 45 years, 11.3% were between 20 and 25 years, and the last was above 46 years of age. 35.1% of the samples had a bachelor-level education, 32.9% of the respondents had a diploma or technical level education, 19.5% of the subjects attained a higher-level education, and the remaining had a secondary school certificate-level education. Among the respondents, 27.8% of the respondents had a monthly income of 6,001–10,000 SAR, 23.8% of the subjects had a monthly income of 10,001–15,000 SAR, 20.4% of the respondents had a monthly income of 3,000–6,000 SAR, 15.8% of the respondents had the monthly income over SAR 15,000, and last had the income less than SAR 3,000. The majority of respondents (28.3%) used the e-money services for 3–4 years, 27.7% of the respondents used e-money services for 2–3 years, 20.5% of the respondents used e-money services for less than 1 year, 13.7% of the respondents using the e-money services for 1–2 years and remaining using the e-money services for more than 5 years. The respondents using the e-money monthly for 1–5 times were 22.2%, using 6–10 times monthly were 35.1%, respondents using the e-money more than 10 times in a month were 23.8%, and the remaining were not using the e-moneys monthly. Table 1 presents the respondents’ profile.

Sample Demographic.

Validity and Reliability

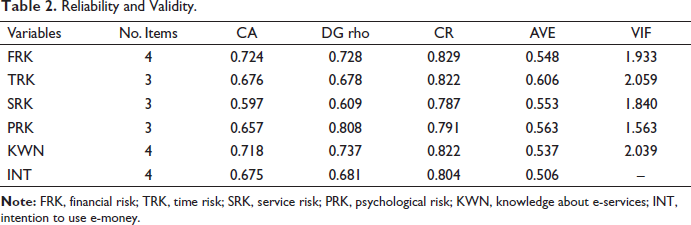

Employing the ratification from Hair et al. (2019), we accomplished and documented the SmartPLS outcomes. For each construct, the model variables’ reliabilities were evaluated by Cronbach’s Alpha (CA), Composite reliability (CR), and rho-A. Outcomes show that all the study constructs have a suitable level of reliability values and the lowermost values are 0.760, 0.751, and 0.849, respectively. For all the constructs, CA, CR, and rho-A are more than the benchmark of 0.70 (Hair et al., 2019). The score for reliabilities is presented in Table 2.

Reliability and Validity.

The average value extracted (AVE) for all items for every variable is necessary to be more than the 0.50 value to justify the convergent validity as a signal of the unidimensionality of every variable (Hair et al., 2019). Variance inflation factor (VIF) for every variable is offered in Table 2, and all VIF scores are below 3.3. It suggests that no issue of multi-collinearity found in the study variables. The question items exhibit those constructs have satisfactory convergent validity.

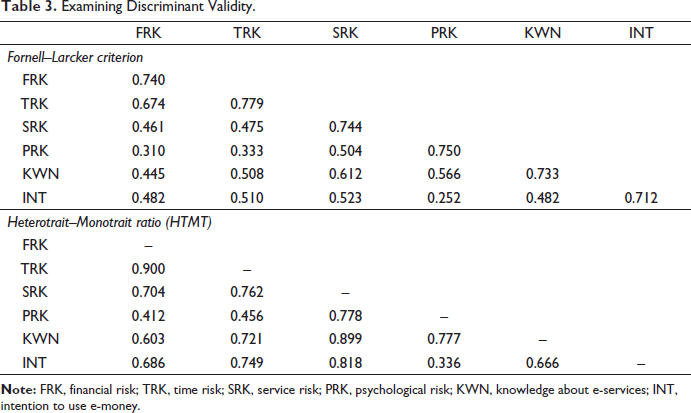

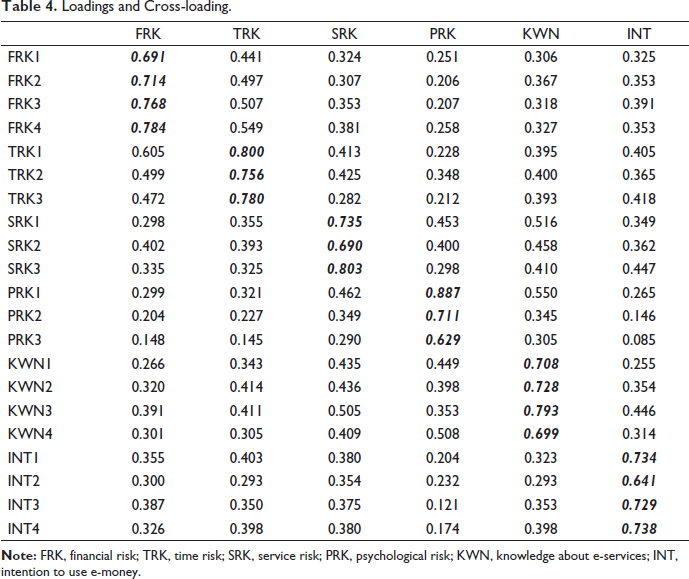

Furthermore, the Fornell–Larcker (1981) criterion, Hetro-trait and mono-trait, and HTMT ratio test were employed to approve the study constructs’ discriminant validities. Outcomes of the Fornell–Larcker criterion are essential to be less than 0.70 to form discriminant validity for every variable (Hair et al., 2019). The question items loading and cross-loading were conveyed for the justification of variables’ discriminant validity. The model variables achieved suitable discriminant validity (Table 3).

Examining Discriminant Validity.

The values shown in italics in the matrix above are the item loadings, and others are cross-loadings.

The HTMT ratio must be under 0.900 to offer the signal for discriminant validity for study variables (Henseler et al, 2015). The Fornell–Larcker measure and HTMT ratio depict the discriminant validity achieved for the current model. Lastly, the loading and cross-loading of the model items show that the model achieves the discriminant validity, and the result is shown in Table 4.

Loadings and Cross-loading.

Path Investigation

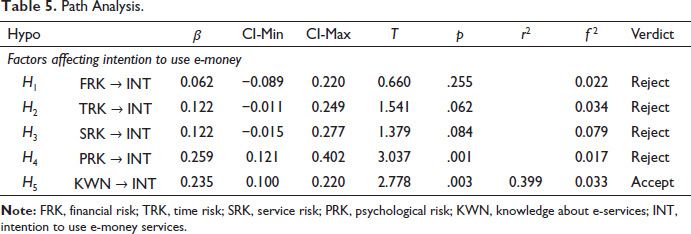

Subsequently, the study model assessment was estimated after appreciating the study’s model validity and reliabilities. At this stage, the effect of the financial, time, service, psychological, and knowledge about e-wallet services on the intention to use e-money was assessed. The adjusted r2 score for the five exogenous constructs (i.e., financial risk, time risk, service risk, psychological risk, and knowledge about e-money services) on the individual use intention for e-money explains the 39% change in individual intention to use e-money.

Table 4 shows the standardized path score and t-values, with the significance levels. The path score between financial risk and intention to use e-money (β = 0.062, t = 0.660, p = .225) signifies an insignificant but positive effect of the financial risk toward e-money on the intention to use e-money. The outcome provides statistical provision not to admit the H1. The beta value for the time risk for the e-money on the intention to use e-money (β = 0.122, t = 1.541, p = .062) result suggests an insignificant but positive effect of the time risk toward using the e-money. Accordingly, it offers statistical provision not to admit the H2. The path value for the service risk and intention to use e-money (β = 0.122, t = 1.379, p = .084) offers insignificant support that the service risk positively influences the intention to use e-money and forms no support to accept the H3. The influence of the psychological risk on the use intention for e-money (β = 0.259, t = 3.037, p = .001) displays the effect of the psychological risk on the individual’s intention to use e-money comes significant as well as positive, thus affords statistically reject the H4. The knowledge about e-money on the intention to use e-money (β = 0.235, t = 2.778, p = .003) expounds on the consequence of the knowledge about e-money on the intention to use e-money as positive and significant; it delivers the statistical indication to accept the H5. The study’s path coefficients are presented in Table 5.

Path Analysis.

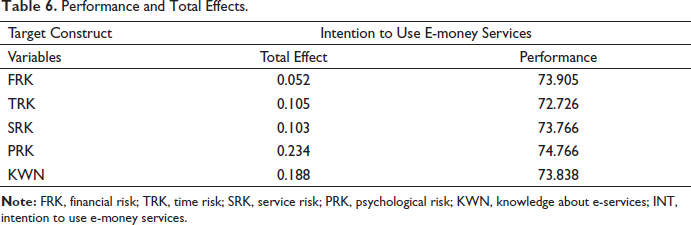

Importance Performance Matrix

The intention to use the e-money services was most suggestively impacted by the psychological risk (0.234; 74.766). The second most vital aspect for the intention to use e-money services, with a score of (0.188; 73.383), is the knowledge about e-money services. The third most vital factor in the performance of intention to use e-money services is the time risk, with a score of (0.105, 72.726). The fourth noteworthy factor for the performance of the intention to use e-money services is the service risk, with a score of (0.103; 73.766). Lastly, financial risk is the minimum important factor instigating the use intention for e-money services. The result is offered in Table 6.

Performance and Total Effects.

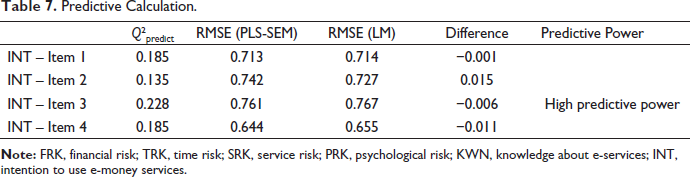

Predictive Calculation

Predictive valuation for the current research reveals that the study model has moderate predictive authority for using e-money services. The Q2 predicted values are more than 0. The Q2 predictive score above 0 recommends that the naïve PLS-SEM model executes better than the LM Model (Shmueli et al., 2019). LM yardstick produces more errors than the PLS-SEM model. The outcomes bring a thoughtful signal that the PLS-SEM model achieves fine for the prediction purposes for out-of-sample results to predict use intention for e-money services (Shmueli et al., 2016). The spread of errors settles that the use intention for e-money services has high predictive power (see Table 7).

Predictive Calculation.

Discussion

Mobile use has been seen in the last decade, and mobile has become a personal device to perform numerous activities and execute financial transactions. Mobile-based e-money gets popular among users and consistently replaces the traditional use of currency notes to perform daily monetary transactions (Gupta & Arora, 2019). The usage of e-money allows users to accomplish financial transactions expediently (Liebana-Cabanillas et al., 2015). The current study result shows that the financial risk negatively but trivially influences the use intention for e-money services. The loss of money is a significant risk that negatively effects the intention to use e-services; the fee charged not according to the promise made by the service provider also forms the financial risk that curtails the intention to accept the e-money services. Our outcome approves with the conclusion postulated by Ariffin et al. (2018) perceived financial risk restricts the prospective user from using e-money services.

The study finding confirms that the time risk stills exist among the users and the positive but insignificant impact of time risk exists on the use intention for e-money services. The e-money service users are not confident that the e-money services are risk-free in terms of time, which still leads to waiting or losing time when they use the e-money services (Gupta & Arora, 2019). The users still engage in avoiding using e-money services. Our result contradicts the finding that Arifin et al. (2018) postulated that the time risk negatively impacts the use of online technologies. For our study, the users build confidence and improve technology, reducing the time risk for the e-money users. Subsequently, the study outcome advocates that the service risk for e-money services insignificantly influences the use intention for e-money services. The e-money users find that the service risk exists and the consistency and quality of e-money services are questionable; it builds doubts in the mind of users and reduces the positive intention to use the e-money services (Chawla & Joshi, 2019). Our finding overlaps with the work of Han and Kim (2017) in that the service risk diminishes the intention to use online services.

Furthermore, the consequence of the current study offers evidence that the psychological risk associated with e-money services positively influences the intention to use e-money services. The finding suggests that e-money services perform well and build no mental pressure on the users. Our study results match the outcome posit by Karim et al. (2020). The respondent feels that e-services technologies can meet consumer expectations and build a positive inclination to use e-money services. Finally, the study outcome suggests that knowledge about e-money services significantly promotes the intention to use e-money services. The service-relevant knowledge nurtures the users’ confidence and harnesses the right skills to use e-money services. Most of the points that our study discovered are in accordance with the results reported by Lwoga and Lwoga (2017), especially that the provision of mobile service-related knowledge positively instigates the predisposition toward mobile payments.

Conclusion

The existing research intends to reconnoiter the formation of an intention to use e-money services among Saudi Arabian adults with associated risks (financial, time, service risk, and psychological risk) and knowledge about e-money services. The penetration of technology-based e-money services enables the KSA to become a cashless society and realize the dreams of vision 2030.

Implications

The study affords to bid on the current scholarship relating to consumer e-money adoption in three manners. The current study augments the principal scholarship about forming an intention to use e-money facilities by curtailing the financial, time, service, and psychological risks. The current work offers an alternative scenario to promote the resolved use of e-money services to conceptualize the risk that may curtail the acquiring of e-money services. The financial, time, and service risks still promote the users’ non-use behavior. The management of the e-money services firm needs to reduce the financial risk as it is, most importantly, curtailing the intention to use the e-money services.

Additionally, most of the studies explored the intention to use e-money among progressive and developed western states (Karjaluoto et al., 2020). The current study backs the prevailing efforts to study the intention to use e-money in an emerging economy such as Saudi Arabia. Presently, the perception of risk undesirably impacts the embracement of e-money services. Knowledge can play a favorable part in forming the intention to use e-money services in developing countries. Users from emerging economies are continuously looking for Government help or inducements to advance the intention to adopt e-money or technology-based payment services (Karim et al., 2020).

The existing study complements consumers’ insights on the acceptance of e-money services in two ways. The study result suggests that e-money is considered risky based on financial, time, and service risks. The proper promotion and service level improvement can help build the right attitude and curtail the negative perception of e-money services. Promoting awareness and knowledge of e-money services can nurture a positive attitude toward e-money services. The knowledge empowers trust and reduces risk perception, harnessing the positive attitude to uptake e-money services (Dai et al., 2014).

Study Limitations

The present study intended to evaluate users’ intention toward using e-money. The current study had its strengths but was associated with three prevalent limitations. Government policies and incentives facilitate the users to adopt novel technologies. It would be exciting to discover the role of Government policies in adopting e-money technologies like an e-wallet. The current study assumed the quantitative design and limited factors utilized to explore the adoption of e-wallets, offering inadequate comprehension of the adoption of e-money. Researchers may adapt the mix-method or qualitative research design to fully explore and expose the phenomenon of e-money adoption. Moreover, it would motivate to assume the mental-societal factors that may instigate the predisposition to use e-money in a diverse personal context such as income, gender and education. Furthermore, personal technology adoption readiness helps explore and moderate the intention formation and adoption of e-wallets.

Footnotes

Acknowledgements

The researchers acknowledge and wishe to thank the Deanship of Scientific Research, Prince Sattam Bin Abdulaziz University, Alkharj, Saudi Arabia, for funding the current project.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Deanship of Scientific Research, Prince Sattam Bin Abdulaziz University, Alkharj, Saudi Arabia funded the current project (Project No: 2021/02/19013).