Abstract

The purpose of the present study was to empirically examine the efficacy of statutory disclosures in the Indian mutual fund industry. Whether the disclaimers aid investors in their decision-making process was investigated. The study made a distinction between type of investors (novice and seasoned investors) as disclaimers affect differently on investor’s belief, attitude and ability to take informed decision. Survey was conducted using a structured questionnaire to evaluate the responses of 388 investors, consisting of 243 novice and 145 seasoned investors. Data was analyzed using mean comparison, independent t-test, and logistic regression model. Results revealed that statutory disclaimers were less effective on seasoned investors compared to novice investors. This suggests seasoned investors process the disclaimer information differently. Novice investors systematically process the disclaimers of mutual fund advertising, and their investment decision was meaningfully affected by the disclaimers. The study offers specific suggestions for stakeholders working in the area of behavioral finance, highlighting the importance of considering the dual process theory of information processing. To the best of authors knowledge, this study is the first of its kind to evaluate the efficacy of mandatory disclaimers in the Indian mutual fund industry, providing unique insights for future research in the field.

Keywords

Introduction

Mutual fund advertisements disclaimers (‘Mutual Fund investments are subject to market risk. Please read the offer document carefully before investing’ and ‘the past performance of the mutual funds is not necessarily indicative of future performance of the schemes’) are purely rhetorical. Dual-modality disclaimers (e.g., visible text plus auditory voice-over) are now a common pattern in mutual fund advertisements. Do these disclaimers create caution for investors and help them make informed decisions?

Statutory disclaimers are assumed to assist investors in processing information that enables judgments and inferences about a product (Johar & Simmons, 2000). Regulators in mutual fund recognize the importance of statutory disclaimers. It requires widespread use of disclaimers in all types of marketing communication. Although the use of such disclaimers has increased in recent years (Hoy & Andrews, 2004), but it is not confirmed whether these disclaimers elicit the intended benefit (Lee et al., 2012).

Another aspect of these disclaimers shows that an increased frequency of disclaimers in advertising coincided with poor attention from the viewers (Hoy & Andrews, 2004). The ultimate effect of these disclaimers depends on factors like how their content is effectively communicated and interpreted. The content of disclaimers may be well attended by investors. But they may purposely overlook data that they consider superfluous, unimaginable, or requiring substantial mind exertion. This condition of investor negligence may be a consequence of investor characteristics, for example, lack of information processing and inability to read and comprehend financial message characteristics. Behavioral factors like overconfidence, which results from investment experience, also affect investor decisions (Quaicoe & Eleke-Aboagye, 2021). Overconfidence among investors overestimates their abilities, knowledge, and information, which has a bearing on decision-making (Manazir et al., 2016). Overconfidence among mutual fund investors increases with investment experience and education (Mishra & Metilda, 2015).

These studies show evidence of the poor efficacy of disclaimers. Different investors get impacted differently (Wilkie, 1982); there is increased frequency and associated ignorance (Hoy & Andrews, 2004) and selection neglect in the advertised mutual funds (Koehler & Mercer, 2009). Investment decision, financial knowledge of investor, and disclosure messages are closely related (Lee et al., 2012).

Investment decisions in financial instruments require investors’ understanding of company financials, industry performance, and economic conditions. Initial years in the market are generally used to gather knowledge and understand investment nuances. Mishra and Metilda (2015) classified investors with less than 2 years of investment experience as less experienced (novice) investors. Those above 2 years’ investment experience was considered as experienced. We interviewed four mutual fund advisors to understand their approach to investor classification. On the basis of our interview, we classified investors with less than 5 years of investment experience as ‘novice’. Investors with more than 5 years of investment experience are considered ‘seasoned’ investors. In the present study, ‘knowledge of investors’ (which is an outcome of time spent by investors in the market) is the differentiator used to categorize investors as seasoned or novice.

Expert and novice investors differ in processing the advertisement content, which may result in likely mutual fund investments (Jordan & Kaas, 2002). Individual investors do not always act rationally. Financial literacy has association with overconfidence and other behavioral biases (Baker et al., 2019). Expert investors are immune due to likeliness affected by behavioral biases (Ahmad, 2021). Lay investors may take suboptimal investment decisions by using material that is wrongly presented to them (Johnson et al., 2022). Compared to experts, novice investors give more importance to advertisements (Alba & Hutchinson, 1987).

Is the use of disclaimers by companies merely a matter of compliance, or does it truly affect investors’ decisions? Disclosures are deemed effective if they change investors’ return expectations about the future (Mercer et al., 2010). The motivation of the present study is to assess the efficacy of statutory disclaimers on Indian investors. Do novice and seasoned investors behave similarly or differently? This study attempts to categorize investors as seasoned or novice to appraise their response to mutual fund statutory disclosures and investment decisions.

Theoretical Linkage, Literature Review and Hypotheses Development

Investing experience of an investor makes them more knowledgeable, which assists them make informed investment decisions. Mercer et al. (2010) opine that the efficacy of mutual fund disclaimers is questionable and endorse them as worthless and ineffective. Ineffectiveness may be due to a variety of factors. For example, increased frequency of disclaimers and associated ignorance (Hoy & Andrews, 2004).

Dual Process Theory of Information Processing and Type of Investor

Dual-process theories of information processing express the idea that all decisions are driven by two processes: (a) Intuitive and (b) Cognitive (Evans, 2008). Dual-process theories of information processing like the Heuristic—Systematic Model (Chaiken, 1980; Chaiken & Trope, 1999; Chaiken et al., 1989) and the Elaboration Likelihood Model (Petty & Cacioppo, 1986) distinguish between heuristic (peripheral) and systematic (central) methods of information processing. System 1 processes can be regarded as quick, heuristic-based, and mainly tied to intuition. Whereas system 2 processes are regarded as deliberate, measured, and conscious (Stanovich & West, 2000). They are responsible for rational thinking and cognitive judgments, which are prerequisites for consistently financially literate investment strategies (Glaser & Walther, 2013). Judgment of an investor is heuristic in nature (Jordan & Kaas, 2002). Cognitive judgments are effortful systematic processing and associated with high involvement, ability, and motivation. In contrast, cognitively less effortful heuristic processing is related to less involvement, ability, motivation, and intuition (Stamos et al., 2018). Ability to process information has capacity limitations, which in turn arises from a time factor or previous knowledge (Ratneshwar & Chaiken, 1991).

Subject knowledge is a crucial part of cognitive capacity, which influences information processing. Experienced people (with attitude-relevant beliefs and prior investing experience), compared with less experienced people, have strong opinion, and do not tend to change even though the message is counter-attitudinal (Wood, 1982). Knowledgeable (seasoned) investors are confident and willing to process the disclaimers that require cognitive effort. They also integrate such information into judgment (Andrews et al., 1998; Zuckerman & Chaiken, 1998) while evaluating any new information. As seasoned investors have more knowledge and experience, they are capable of independently scrutinizing the disclaimer content. Systematic processing of messages is normally an attribute of knowledgeable (seasoned) investors (Biek et al., 1996).

Mutual Fund Disclaimers and Investors

Prominent statutory disclaimers (irrespective of modality type) are anticipated to create caution about the risks associated with investment. Perusing and hearing disclaimers (especially, Mutual funds are subject to market risks…) has become a normal practice for investors. These warnings were a deterrent factor for new investors and responsible for the poor positioning of the mutual fund industry in comparison with other financial products (Kulkarni et al., 2020). Disclaimer in advertising is considered to be a symmetrical tool (helpful for marketers and consumers) that constructs cognitions, attitudes, and affects behavior in the financial marketplace (Franke et al., 2004). Financial knowledge of investors varies with their investing experience. Investors’ familiarity with the market and experience results in higher financial knowledge. Financial knowledge of investors also weighs in understanding and using disclaimers to make investment decisions. Effectiveness differs among investors due to their cognizance of market risks.

Hypotheses of the Study

Efficacy in Communicating Disclaimers

Attention is perceived as a significant decision-making component of a consumer. In the case of financial products that require high level of investor involvement, attention remains an important variable (Hirshleifer et al., 2011; Li & Yu, 2012; Peng et al., 2007). Mutual funds are high-involvement products. Mutual fund buying behavior is driven by prominent and striking information made available by way of advertising. Effectiveness of disclosures and warnings depends on the attentiveness that they are able to create (Stewart & Martin, 2004). For disclaimers to grab attention, it depends on how effectively they are communicated and interpreted by investors. Based on the extant literature, the first hypothesis is proposed:

Investor Belief and Disclaimers

Generally, people form attitudes based on their beliefs (Fishbein & Ajzen, 1975). Literature shows that investors interpret the disclaimers with their own bias, which comes from prior beliefs. Disclaimers are considered effective if they impact the belief system of an investor. It is necessary to understand investor beliefs and their relevance to disclosure information (France & Bone, 2005). Attention is not sufficient for bringing about a change in beliefs, attitudes, and behaviors of investors, as argued by Graham et al. (2012). Mercer et al. (2010) opine that a mandatory disclaimer has no bearing on investor belief. Based on the extant literature, we propose the second hypothesis:

Investor Attitude and Disclaimer

Disclaimers are expected to create informed investors and improve the quality of investment decisions. Attitude-relevant beliefs have an important role in decision making (Wood, 1982). Experienced people with strong attitude-relevant beliefs participate in defense-motivated systematic message processing (Biek et al., 1996). Kim and Hunter (1993) demonstrate a strong relationship between attitude and behavior. The study reveals that advertisements can be a source to create favorable attitudes, which can be regarded as predictor of buying behavior. From a managerial perspective, disclaimers are used to improvise and change perceptions, beliefs, attitudes, and buying propensities (Karrh et al., 2003). Disclaimers are considered effective if they help create the right attitude among investors. Based on previous studies, the third hypothesis is poised as:

Informed Investor and Decision-Making

Forming an attitude toward the content of the message is a significant variable in deciding effectiveness (Vakratsas & Ambler, 1999). Centered on the attitude, people form judgments about the product. Framed judgments can be a predictor of buying behavior (Mowen, 1995). Consumer judgment about product risk and hazards declines after exposure to the warnings (Kaskutas, 1993). Similarly, an investor’s judgment (decision-making) has an impact on disclaimers of mutual funds. Disclaimers are considered effective if they make investors informed about the possible risks associated with investment decisions. Previous research demonstrates a weak impact of disclaimers on the judgment of investors. On the basis of the extant literature, we propose the next hypothesis:

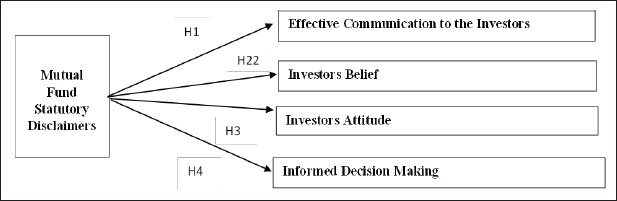

This study proposes the conceptual model as provided in Figure 1.

Research Design

Sample

This study was administered to people residing in urban areas of India. Individuals who continue being mutual fund investors were respondents to the survey. Respondents from western India, that is, the states of Maharashtra, Telangana, and Gujarat were considered. Major cities covered in this study are Mumbai, Pune, Hyderabad, Warangal, Ahmedabad, and Rajkot. Population of the study being infinite, Cochran’s formula was used to derive the sample size. As per this formula, the minimum sample size to be considered was 384. For this study, we received 968 responses from 6 urban cities. Using the randomization technique, we selected 484 responses. The number of responses considered complete and usable for the analysis was 388. Final sample size was within the limit proposed by Cochran.

Questionnaire

Data were collected through a structured, anonymous questionnaire. There were a total of 23 questions, divided into two sections—I and II. The first section captured demographic details with four questions. The second section consisted of 19 questions regarding the efficacy of communicating the statutory disclaimers and investor’s belief, attitude, and ability to take informed decisions as an effect of mutual fund disclaimers. 14 questions in the second section were on a 5-point Likert scale, from strongly disagree to strongly agree. These questions were drawn up based on a review of the literature. Data on efficacy in communicating disclaimers was captured through legibility, caution, indicating risk, and deterrence. Investors’ beliefs and statutory disclaimers had questions on the clarity of objectives, market risks, education, and caution. Investor attitude toward investments captured information on propensity, expectations, and revaluation. Investors and disclaimers covered the statutory disclaimer, raising concerns about ability, other risks, and time horizon. Five questions were in binary form, which captured responses on ‘frequency of attention given to the disclaimers’ and ‘effect of the same on investment decision’.

Data Collection

The present study is descriptive in nature and used simple random technique for data collection. Simple random technique was adopted as it removed biases from the selection procedure and each populace had an equal probability of insertion in the sample (Ghauri & Gronhaug, 2005). Online social media platforms, namely WhatsApp, Telegram, LinkedIn, and email were used for data collection. The online questionnaire link had custom setting to limit responses to one per user. Also, the urban cities chosen for the study were to be picked from the drop-down list. In case a respondent clicked on the questionnaire who did not belong to the chosen study area, they were directed to a thank you page.

Data Preparation and Analysis

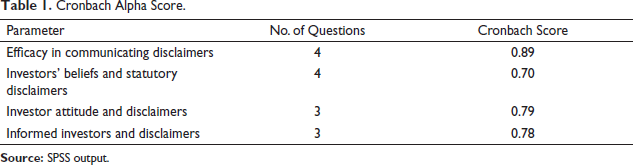

Cronbach Alpha Score.

As evident from Table 1, in all cases, Cronbach’s alpha is greater than the threshold limit of 0.7. This proves the internal consistency of all items on the scale.

Using IBM SPSS 25, a mean comparison, independent t-test, and logistic regression model have been applied for data analysis.

Analysis and Discussion

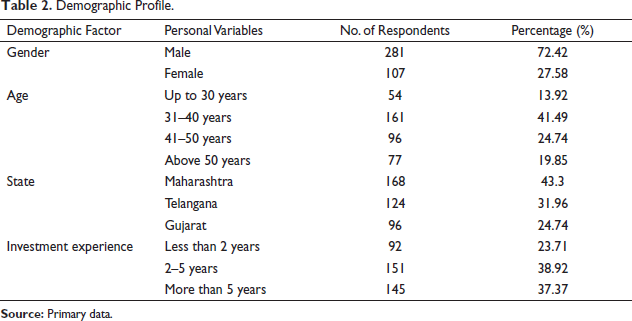

Demographic Profile.

Table 2 shows that, out of 388 responses received, 281 (72.42%) respondents were male and 107 (27.58%) were female. Maximum respondents (41.49%) were in the age group of 31–40 years, followed by 24.74% in the age group of 41–50 years. Respondents from Maharashtra state (43.30%) dominated the sample, followed by 31.96% from Telangana state and 24.74% Gujarat state. Interestingly, 62.63% considered themselves novices, while 37.37% respondents were seasoned investors.

Efficacy in Communicating Disclaimers

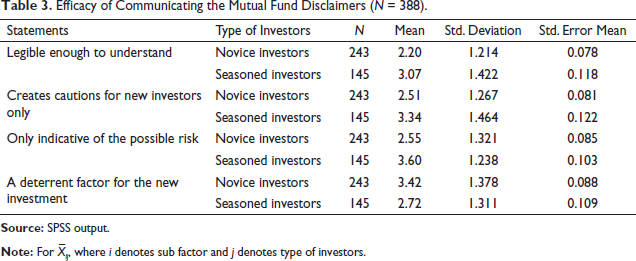

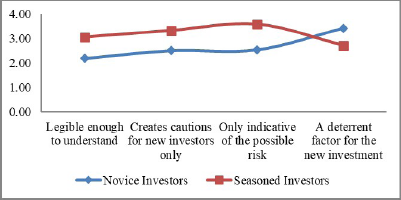

Table 3 gives the results of group statistics efficacy of communicating the statutory disclaimers. It shows the difference between novice and seasoned investors. For the subfactor “legibility to understand,” X̄11 = 2.20 (σ11 = 1.214) and X̄12 = 3.07 (σ12 = 1.422), with respect to the efficacy of communication, as X̄12 > X̄11. Group statistics revealed that X̄12 converged toward an agreeable level of acceptance. It indicates that mutual fund disclaimers are highly legible enough to be understood by seasoned investors. Whereas X̄11 converged toward a disagreeable level, which indicates mutual fund disclaimers are less legible to be understood by novice investors. With respect to the subfactor “creates caution for new investor,” X̄21 = 2.51 (σ21 = 1.267) and X̄22 = 3.34 (σ22 = 1.464). Comparison revealed that X̄22 > X̄21 and X̄22 converged toward an agreeable level of acceptance. It revealed that mutual fund disclaimers are highly significant to create caution for new investors only. For the subfactor “indicative of the possible risk,” X̄31 = 2.55 (σ31 = 1.321) and X̄32 = 3.60 (σ32 = 1.238). As X̄32 > X̄31, it revealed that, for seasoned investors, mutual fund disclaimers are only indicative of possible risk.

Efficacy of Communicating the Mutual Fund Disclaimers (N = 388).

In Figure 2, disordinal interactions between efficacy of communicating the statutory disclaimers and level of acceptance are depicted, with respect to then deterrent factor for the new investment X̄41 = 3.42 (σ41 = 1.378) and X̄42 = 2.72 (σ42 = 1.311). Comparison revealed that X̄41 > X̄42. Also, X̄41 converged toward an agreeable level of acceptance. It shows that mutual fund disclaimers are one of the deterrent factors for novice investors at the time of making new investment decisions. Disclaimers create caution among novices. Hence, novices hesitate whether to invest in mutual funds or not. Mutual fund disclaimers also affect seasoned investors. Comparatively, the impact of mutual fund disclaimers on seasoned investors’ decisions regarding new investments is less.

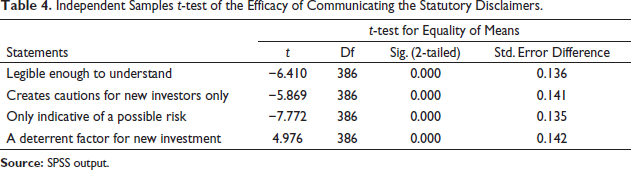

Test of Hypothesis 1

Independent sample t-test was performed to test H1.

Table 4 reveals that all the p-values tend to 0, which is less than the significance value of 0.05. It means that statutory disclaimers of mutual funds are effectively communicated to all investors.

Independent Samples t-test of the Efficacy of Communicating the Statutory Disclaimers.

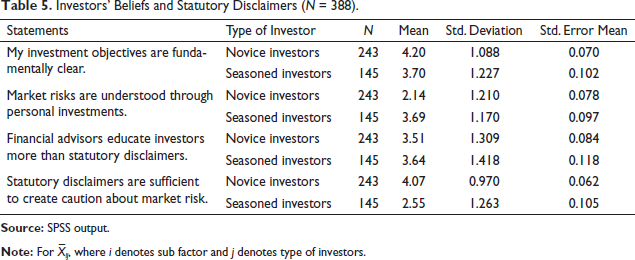

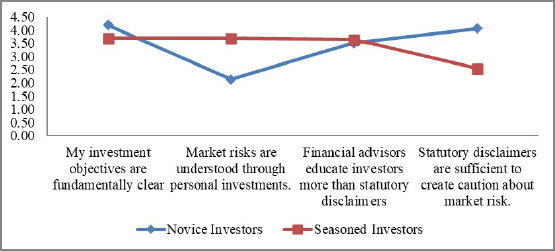

Investors’ Belief and Statutory Disclaimers

Investors’ beliefs and statutory disclaimers were checked by calculating the mean X̄ and standard deviation (σ).

Investors’ Beliefs and Statutory Disclaimers (N = 388).

In Figure 3, disordinal interaction between investors’ beliefs about statutory disclaimers and their level of acceptance is depicted, with respect to the subfactor “market risk,” X̄21 = 2.14 (σ21 = 1.210) and X̄22 = 3.69 (σ22 = 1.170). Comparison revealed that X̄22 > X̄21 and X̄22 converged toward an agreeable level of acceptance, whereas X̄21 converged toward a neutral level. It indicates that seasoned investors have a stronger belief that market risks are understood through personal investments, whereas novice investors are neutral. For the statement “Statutory disclaimers are sufficient to create caution about market risk," X̄41 = 4.07 (σ41 = 0.970) and X̄42 = 2.55 (σ42 = 1.263). Comparison revealed that X̄41 > X̄42. X̄41 converged toward an agreeable level, whereas X̄42 converged toward a neutral level of acceptance. It revealed that statutory disclaimers are sufficient to create the required caution about market risks for novice investors.

Test of Hypothesis 2

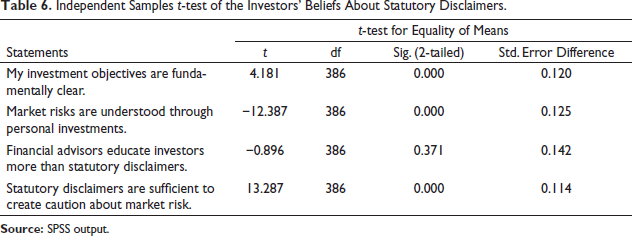

Independent Samples t-test of the Investors’ Beliefs About Statutory Disclaimers.

Table 6 indicates that all the significance values tend to ‘0’, that is, less than 0.05 significance level, except for one significance value on the statement “financial advisors educate investors more about market risks than statutory disclaimers,” that is, 0.371. We can conclude that statutory disclaimers of mutual funds affect investors’ beliefs.

Investor Attitudes and Disclaimers

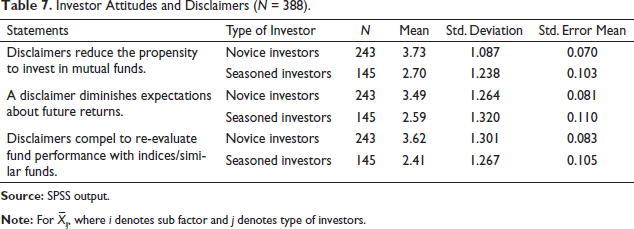

Table 7 gives the result of group statistics of investors’ attitudes toward investments in mutual funds. Both investor groups were associated with three subfactors of attitude. For the subfactor “disclaimers reduce the propensity to invest,” X̄11 = 3.73 (σ11 = 1.087) and X̄12 = 2.70 (σ12 = 1.238), with respect to the investors’ attitude toward investments, as X̄11 > X̄12 also converged toward an agreeable level of acceptance. It revealed that, mutual fund disclaimers reduce the propensity to invest in mutual funds for novice investors, whereas seasoned investors’ attitudes are less affected by mutual fund disclaimers. For the subfactor “expectations about future returns,” X̄21 = 3.49 (σ21 = 1.264) and X̄22 = 2.59 (σ22 = 1.320), as X̄21 converged toward an agreeable level of acceptance. It revealed that disclaimers diminish novice investors’ expectations about future returns, whereas X̄22 converged toward a neutral level of acceptance. It revealed that seasoned investors’ attitudes toward future returns are unaffected by mutual fund disclaimers. For the subfactor “do mutual fund disclaimers compel to re-evaluate fund performance,” X̄31 = 3.62 (σ31 = 1.301) and X̄32 = 2.41 (σ32 = 1.267), as X̄31 converged toward an agreeable level of acceptance, it revealed that disclaimers compel novice investors to reevaluate their fund performance with indices/similar funds. Whereas X̄22 converged toward a neutral level of acceptance, it indicates that disclaimers had no impact on seasoned investors’ attitudes toward fund performance. It does not compel seasoned investors to reevaluate fund performance with indices/similar funds available in the market.

Investor Attitudes and Disclaimers (N = 388).

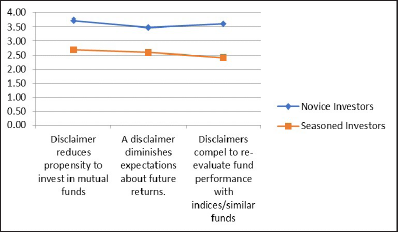

In Figure 4, ordinal interaction between investors’ attitudes toward investment is depicted, where novice investors mean (X̄) converged toward an agreeable level of acceptance. It indicates that novice investors’ attitudes are more vulnerable toward investment in mutual funds due to disclaimers. In contrast, seasoned investors mean (X̄) converged toward a neutral level of acceptance. It reveals that seasoned investors’ attitudes are neutral, and mutual fund disclaimers do not reduce their propensity to invest in mutual funds. Neither do disclaimers diminish seasoned investors’ expectations about future return nor compel them to reevaluate fund performance with indices/similar funds.

Test of Hypothesis 3

Independent sample t-test was used for testing H3.

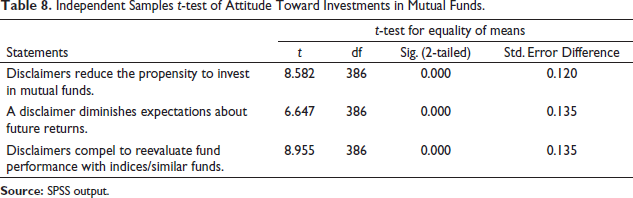

Table 8 shows that all significance values tend to 0, as the significance values are less than the 0.05 significance level. Therefore, t-test analysis led to conclude that statutory disclaimers of mutual funds affect investors’ attitudes.

Independent Samples t-test of Attitude Toward Investments in Mutual Funds.

Informed Investors and Disclaimers

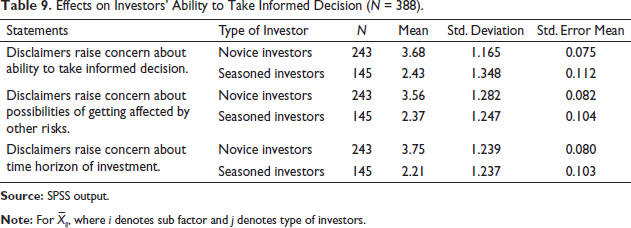

The results of group statistics of effects on investors’ ability to take informed decisions are summarized in Table 9. For the subfactor “disclaimers raise concern to take informed decision,” X̄11 = 3.68 (σ11 = 1.165) and X̄12 = 2.43 (σ12 = 1.348). With respect to investors’ concern, X̄11 > X̄12, and X̄11 converged toward an agreeable level of acceptance. It revealed that mutual fund disclaimers raise concern among novice investors about their ability to make informed decisions. Whereas seasoned investors X̄12 converged toward a disagreeable level. It indicates that disclaimers had no impact on seasoned investors’ ability to make informed decisions. For the subfactor concern about “possibilities of getting affected by other risks,” the mean values are X̄21 = 3.56 (σ21 = 1.282) and X̄22 = 2.37 (σ22 = 1.247). X̄21 converged toward an agreeable level of acceptance. It revealed that disclaimers raise novice investors’ concerns about the possibility of getting affected by other risks, whereas X̄22 converged toward a disagreeable level of acceptance. It indicates that seasoned investors’ concerns about the possibility of getting affected by other risks are unaffected by mutual fund disclaimers. Mean values of concern about the time horizon of investment are X̄31 = 3.75 (σ31 = 1.239) and X̄32 = 2.21 (σ32 = 1.237). Novice investors X̄31 converged toward an agreeable level of acceptance. It revealed that disclaimers raise novice investors’ concerns about time horizon of investment, whereas X̄32 converged toward a disagreeable level of acceptance, which indicates that disclaimers have no impact on seasoned investors’ concerns about time horizon of investment.

Effects on Investors’ Ability to Take Informed Decision (N = 388).

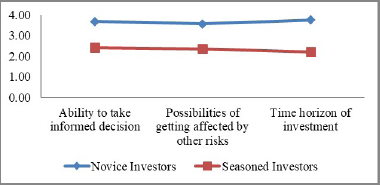

In Figure 5, ordinal interaction between statutory disclaimers of mutual funds affects on investors ability to take informed decisions is depicted, where novice investors’ mean (X̄) of subfactors converged toward an agreeable level of acceptance and seasoned investors’ mean (X̄) of subfactors converged toward a disagree level of acceptance.

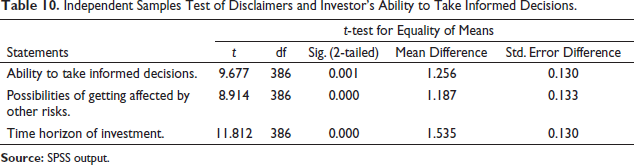

Test of Hypothesis 4

Table 10 depicts significance values tend to 0. All the significance values are less than 0.05. Hence, we conclude that statutory disclaimers of mutual funds affect investor’s ability to make informed decisions.

Independent Samples Test of Disclaimers and Investor’s Ability to Take Informed Decisions.

Primary findings of the study support the existence of a dual process theory of information processing. The factors that differentiate investors as novices and seasoned has a relation with how the disclaimers are understood and processed for taking investment decisions. The tests of hypotheses also regard novices as system 1 and seasoned as system 2. Ability to process information is broadly dependent on previous knowledge about investment (Ratneshwar & Chaiken, 1991). This study regards novices as system 1 due to their less systematic ability for information (disclaimer) processing, low involvement, and high use of intuition. Contrarily, seasoned investors are knowledgeable, have belief in their decisions, and market experience. These factors regard them as system 2. They critically scrutinize the validity of disclaimers. Cognitive ability for information processing is high for seasoned investors.

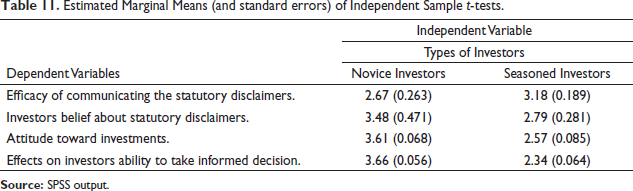

Alba and Hutchinson (1987) demonstrate a strong relationship between consumer knowledge, product expertise, and familiarity. Investment expertise is gained from the experience of the investor; it is plausible to differentiate the effectiveness of investors on the grounds of experience (seasoned and novice investors). Investing experiences have a strong relationship with the efficacy of disclaimers. Literature reveals a negative correlation between the effectiveness of warnings and product familiarity. Familiarity causes people to feel they already know the content of the disclaimer (Rogers et al., 2000). Hence, seasoned investors are more inclined toward the ineffectiveness of disclaimers than novices, who may judge them properly. To test this, independent sample t-tests are applied to the dependent variables (Refer Table 11).

Estimated Marginal Means (and standard errors) of Independent Sample t-tests.

Efficacy of communicating the disclaimers is higher for seasoned investors (MNovice = 2.67, SE = 0.263 vs. MSeasoned = 3.18, SE = 0.189). It is possibly due to the greater familiarity of disclaimers among seasoned investors. Statutory disclaimers affect more on novice investor’s beliefs than seasoned investors (MNovice = 3.48, SE = 0.47 vs. MSeasoned = 2.79, SE = 0.281). It indicates that seasoned investors have rigidity in their investment beliefs. Likewise, seasoned investors are stubborn in comparison to novices in case of investment attitudes (MNovice = 3.61, SE = 0.068 vs. MSeasoned = 2.57, SE = 0.085). Seasoned investors are more informed than novices, which reflects on their ability to take decisions too (MNovice = 3.66, SE = 0.056 vs. MSeasoned = 2.34, SE = 0.064). Efficacy differs for seasoned and novice investors. Novice investors have more efficacy with statutory disclaimers than seasoned investors.

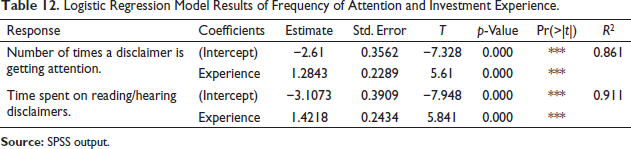

We have further done logistic regression analysis. Logistic regression is used to predict the relationships between attention given by the investors to mutual fund disclaimers and effects of such disclaimers on investment decision with investment experience. The model of Binary Logistic regression analysis is as under.

Logit (Y) = intercept + slope*X,

where, Y = Logit response for disclaimers,

X = Investment experience of investor.

Table 12 furnishes the result of a logistic regression model to predict the relationship between “frequency of attention,” “time spent on reading/hearing disclaimers,” and “investment experience.” Differences in the outcomes of the t-test for each group of investors (novices and seasoned) permit researchers to apply logistic regression for both factors. The significance of the model is evident from p-values that are less than 0.05. R2 indicated goodness of fit measure for logistic regression. It specified the percentage of variance in dependent variables (“frequency of attention” and “time spent on reading/hearing disclaimers”) that occurred as a result of the independent variable, that is, the type of investor. Strength of the relationship is explained by R2 on a convenient scale of 0–100%. In Table 12, the coefficient of determination R2 is 0.861 and 0.911 (R2 > 0.80), which indicates a strong relationship (86.1% and 91.1%) between type of investor and “frequency of attention” and “time spent on reading/hearing disclaimers.”

Logistic Regression Model Results of Frequency of Attention and Investment Experience.

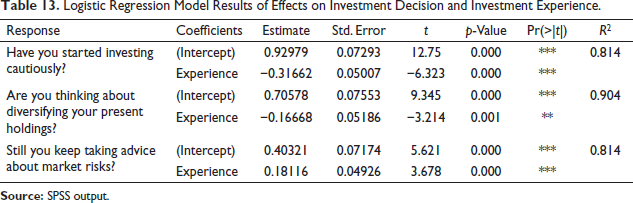

The results of the logistic regression model to predict the relationship between “effects on investment decision” and investment experience are reported in Table 13. In line with the results of the previous regression model, t-test outcomes for each group of investors also differ, making it possible to apply logistic regression to factors such as caution, diversification, and market risk advice taken by investors. For the above factors, the model is significant since all p-values are less than 0.05. Goodness of fit measure (R2) for the model indicates a strong relationship between “effects on investment decision” and investment experience. Coefficient of determination R2 is 0.814, 0.904, and 0.814 (R2 > 0.80), which indicates a strong relationship (81.4%, 90.4%, and 81.4%) between investor type and investment decisions pertaining to caution, diversification, and market risk advice taken by them.

Logistic Regression Model Results of Effects on Investment Decision and Investment Experience.

Conclusion

Our study examined the efficacy of statutory disclaimers of mutual fund on investors. We distinguished between two types of investors (seasoned and novice investors) to assess the efficacy as disclaimers affect differently due to investors’ beliefs and attitudes associated with the ability to take informed decisions. Results suggest that statutory disclaimers are less effective on seasoned investors in comparison with novice investors.

Experience and knowledge of an investor has a bearing on how mutual fund disclaimers are perceived by them. Investors with low financial knowledge systematically process mutual fund advertising claims and generate more attribute-related thoughts. It has a significant impact on investment decisions. Whereas investors with high financial knowledge are less affected due to advertisement disclosures. It highlights that information processed by investors with high or low financial knowledge is different.

Disclaimers are less effective on seasoned investors’ beliefs, attitudes, and abilities to take investment decisions. Although they effectively communicate the risks associated with investments to investors, these disclaimers are incapable of creating caution for seasoned investors. On the contrary, statutory disclaimers are effective on novice investors as they create caution. So, seasoned investors are more inclined toward the ineffectiveness of disclaimers, whereas novices may judge them properly. This can be attributed to the increased familiarity of seasoned investors with market conditions. Seasoned investors are rich in experience, which makes their investment beliefs and attitudes firm. They do not get affected due to statutory disclaimers. The study contributes to behavioral finance literature and helps understand the efficacy of statutory disclaimers mandated by regulators in the Indian Mutual Fund market.

Contribution

This study tests how mutual fund advertisement disclosures affect investors in the Indian market. Our findings contribute to public policy literature, advertisement strategies, and behavioral finance. The study demonstrates how statutory disclaimers affect novice and seasoned investors separately. Mutual fund advertisement disclaimers are viewed and understood by all but processed differently by novice and seasoned investors. Second, SEBI-stipulated mutual fund disclosures have meager impact on seasoned investors. Finally, the study adds to existing literature on behavioral finance. It assists marketers understand the effectiveness of statutory disclaimers in mutual funds. Theoretical anchoring with systems 1 and 2 highlights the casual response given by seasoned investors as opposed to novice investors.

Implications

The outcome of the study has implications for marketers of financial services and regulators. First, marketers of financial services should be aware of the efficacy of the statutory disclaimers, especially in mutual fund markets. It highlights the importance of segmenting the investors as seasoned and novices, as the mandated disclosures affect each of them separately. Segmentation of investors is crucial in the targeting of different investment disclosures and marketing communications. This will possibly help investors make informed investment decisions. Second, statutory disclaimer indicates the strong presence of the regulator (i.e., SEBI) in the Indian mutual fund industry for investor protection. Primary objective of these disclaimers is to inform investors about possible risks associated with investments and create caution. However, the present study shows that statutory disclaimers are less effective on seasoned investors in contrast to novices. With growth in Indian mutual fund industry, the number of novice investors will increase, and existing novice investors will transition to seasoned investors in the future. Seasoned investors gradually get resistant to statutory disclaimers. This may lead to inappropriate investment decisions. SEBI needs to pronounce influential mandatory disclaimers for seasoned investors. Third, this study has implications for the Association of Mutual Funds in India (AMFI). It was established in 1995 to develop and promote interests of Asset Management Companies and their unit holders. Our study shows that mandated disclosures are ineffective on seasoned investors and a deterrent factor for novices. AMFI, as a socially responsible body, should address this mental investment bias through regular, strong messages in social and print media.

Limitations and Future Scope

This study has certain limitations that future research may address. The efficacy of other information disseminated by mutual fund advertisements can be extended by subsequent research. It may include inquiries about new categories of products, celebrity endorsements, content of the advertisements, claims and promises given in the advertisements, etc.

Concentrated geographical pockets are another limitation. Further study can be conducted to broaden the geographical scope by including more states to represent the Indian mutual fund industry. Longitudinal study can be conducted to understand the disclosure efficacy when novice investors shift to seasoned investors. Moderating role of demographic variables (gender, income, level of education, etc.) on perception of statutory disclaimers may also be studied.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.