Abstract

Small and medium-sized enterprises (SMEs) are the driving force for the robust socioeconomic growth of a country. The study primarily aims to empirically evaluate the impact of certain firm-specific factors on the financing preferences of the listed SMEs with specific reference to India. It attempts to examine their financing practices and also investigates if they follow the order explained under various theories of finance. The sample consists of 134 listed SMEs on NSE as well as BSE SME exchange. They have been studied for the period from 2014 to 2019. The sample and the time period of the study differentiates it from the existing studies in the domain. It concludes that though majority of the variables included in the model are statistically significant, there is a possibility of influence of other micro-level variables or macro-level economic factors on the financing decisions of the listed SMEs. It is also revealed that for their financial needs, SMEs prefer short-term spontaneous sources, that is, payables and provisions, then accumulated profits followed by short-term borrowings and in last opt for the long-term debt. The study also found that there is no single theory that can completely explain the financing behavior of the listed SMEs. Moreover, it is also observed that no additional benefit is available for SMEs out of listing in India.

Keywords

Introduction

Small and medium-sized enterprises (SMEs) 1 have become very relevant due to their strategic significance for inclusive economic development (Srinivas, 2013). They are commonly referred to as the growth driver of any country (Boocock & Shariff, 2005). SMEs’ role in poverty reduction through their ability to generate employment is widely acknowledged (Green et al., 2006; Harvie & Charoenrat, 2015). They are widely dispersed and are located in urban. Rural, national, international locations (Ikpor et al., 2017). Out of the total business units in Asia, SMEs along with the micro units constitute approximately 96% of it (Pinho et al., 2018). India has approximately 63 million SMEs providing employment to around 120 million people. In India, SMEs contribute to roughly 45% of total production in the manufacturing sector and contribute 30.5% to the service sector. At present, SMEs in India contribute approximately 29% of country’s total GDP. 2

Similar to any large organization, SMEs also need access to finance on appropriate terms from various sources. Extant literature have identified that SMEs globally are facing financing challenges, which is a major growth constraint (Allen et al., 2012; Beck et al., 2011; De, 2009; Yoshino & Taghizadeh-Hesary, 2016). As per OECD report (2016) despite observed improvement in SME lending, SMEs still experience credit crunch. Banks are observed to be unwilling and cautious in SME lending. Reason for this might be lack of audited financial statement and poor record keeping (Liu & Yu, 2008). As per the latest statistics in India, bank credit to SMEs is approximately 16% of total credit extended leading to a credit gap of ₹16.66 trillion. 3

In lines with the scope identified for governmental interventions globally to deal with financing challenges (Bouri et al., 2011), Indian Government has taken several initiatives to increase the flow of credit to SME sector such as setting up of separate SME exchanges, promoting venture capital fund, and making it available through the channel of public sector bank and various developmental financial institutions (DFIs). 4 Government authorities have displayed a strong intent to significantly improve the flow of funds to this sector.

Debt is considered to be a lesser expensive source of fund as compared to equity for many reasons, but for SMEs either it is unavailable or available only on unfavorable terms. Reason cited for this in academic literature is information asymmetry arising out of poor record keeping and unaudited financial statements (Storey, 1994). SEBI guidelines (2010) provide for establishing separate SME exchanges. The listing requirements for exchanges ensure the availability of financial statements for a certain number of years leading to a better assessment of its track record of companies. This should logically bring down the information asymmetry of listed SMEs and provide them with comparatively easier access to debt in comparison to the non-listed counterparts. This might lead to a significant shift in their financing choices.

In this context, this article attempts to explore the financing choices of Indian listed SMEs. It also aims to explore the various firm-specific factors influencing the financing choices of these SMEs. Considering the aim, following are the research objectives: (a) to identify the firm-specific factors and examine their effect on financing choice of listed SMEs, (b) to evaluate the financing pattern of listed SMEs, and (c) to know if the financing choices of the listed SMEs are in accordance with the established theories of corporate finance.

The study differs from the extant literature in terms of its sample and time period of the study. Remaining article is organized as mentioned: The second section discusses the review of the literature related to the study domain, the third section explains the research scheme followed, whereas in the fourth section, results are presented. The fifth section shows the hypotheses validation and the sixth section contains concluding remarks followed by limitations and identification of future scope.

Review of Literature

This section while summarizing the main theories of capital structure provides review of the extant literature pertaining to the study domain. This is done with the purpose of discovering the research gap and identifying the dependent as well as independent variables.

By the year 1950, capital structure had become a productive and controversial topic within the domain of corporate finance. It all began with the seminal work of Modigliani and Miller (1958) known as “Irrelevance Theory,” which proposed that in a perfect market, financing decisions are irrelevant for company’s valuation. However, after considering tax benefits in a realistic setting, this theory was modified in the year 1963 concluding that capital structure has a bearing on the value of the firm. This pioneering work led to some of the other prominent theories in the field, that is, trade-off theory (TOT) followed by pecking order theory (POT) among several others. Kraus and Litzenberger proposed TOT in the year 1973, which pioneered the term optimal capital structure as the combination of debt and equity with just the right proportion of debt. Contrary to this, Myers (1984) proposed POT, which refuted the idea of optimum capital structure. As per POT, due to information asymmetry firms prefer a particular financing order. They prefer internally generated funds, then debt followed by equity as a last choice (Myers & Majluf, 1984). These theoretical developments have led to vast and diverse research in this field.

Titman and Wessels (1988) in a seminal work concluded that singularity, growth, size, profitability, and non-debt tax shield (NDTS) are some of the prominent factors influencing the financing choices of US enterprises. Fauzi et al. (2013) on the basis of the study of 79 firms registered in New Zealand concluded that size of firm influence the financing choices and stated that large firms prefer debt. Odit and Gobardhun (2011) also observed a significant variation in the financing preferences of large enterprises and SMEs. Gaud et al. (2005) observed that listed firms attempt to adjust leverage ratio toward a value maximizing target following trade-off approach.

Several studies have highlighted the financing challenges of small businesses (Jagoda & Herath, 2010; Yoshino & Taghizadeh-Hesary, 2016). Earlier studies have also tried to understand the preferred financing choices of SMEs. Kremp et al. (1999) on the basis of comparative analysis of 15,000 French and 9,000 SMEs from Germany observed that SMEs follow pecking order theory. Benito (2003) concluded the same on the basis of his studies on SMEs located in Spain and the UK. A similar observation was made by Daskalakis and Psillaki (2008) from their study on French and Greek SMEs. Several studies have indicated the opposite phenomenon. Yartey (2011) found external debt to be more significant for SMEs than internal financing. Odit and Gobardhun (2011) observed that SMEs borrow for a longer duration to finance long-term assets and current assets are financed using shorter duration borrowings. Their study was based on the SMEs in Mauritius. Xiang et al. (2015) with reference to Australian SMEs investigated the impact of various firm-specific factors on their finance seeking behavior. They found that SMEs seek more equity as compared to debt. Mc Namara et al. (2017) analyzed the impact of lending infrastructure on the financing choice in terms of debt and equity of European SMEs belonging to the hotel sector. Study results were supportive of POT and TOT. Adonia et al. (2018), based on his study of micro units in Malaysia, demonstrated that majority of microunits rely on their own funds. External debt financing is opted only in case of shortage of internal funds and when no collateral is required.

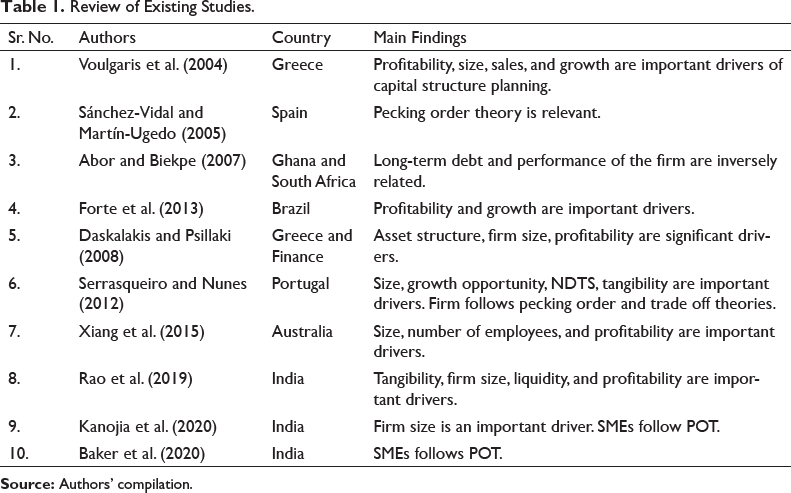

In Indian context also, several studies have been conducted. Love and Peria (2005) compared the financing preferences of SMEs with those of large enterprises between 1994 and 2003. Srinivas (2013) observed that SMEs in India prefer owned funds than debt. As per Kulkarni and Chirputkar (2014), SME listing may increase the flow of funds for long-term growth, expansion, etc. Kumar and Rao (2016) found that SMEs rely more on short-term borrowings. They found that tangibility, firm size, liquidity, and profitability influence the financing decision of SMEs. Hussain et al. (2020) studied the financing preference of tourism SMEs in Punjab, India using post positivist research approach. They concluded that these SMEs follow pecking order trajectory. Baker et al. (2020) examined the financing practices of 309 SMEs belonging to the north western region of India. Their study revealed that SMEs prefer internal funds followed by bank financing. External equity is found to be the last option of financing. Trade credit is the preferred most among informal source. Table 1 presents the selected studies pertaining to the study domain.

Review of Existing Studies.

It is evident from the above discussion that although there are numerous studies discussing the financing decisions, but the studies on SMEs financing especially from the perspective of developing countries are limited. In Indian context, though there is a growing scholarly attention on SMEs, very little evidence is available regarding the consequences of listing. The reason for the same is that in India, SME listing is relatively a new phenomenon with the establishment of Emerge platform in NSE and BSE SME platform in 2012.

The present study with reference to India endeavors to identify various firm-specific internal factors driving the financing preference of the Indian listed SMEs. It adds to the scarce extant literature on SME financing. The study period is 2014–2019 as most of the studies on SMEs are conducted before 2014. It will help SMEs to understand if listing offers any benefits in raising funds from various sources.

Methodology

The methodology followed in the study is explained in this section.

Research Design

The study sample comprises of 149 SMEs from NSE Emerge Platform and 33 SMEs listed on BSE SME exchange as on August 9, 2019. The standard practice of excluding financial companies was followed in this study. This is done as financial statements of the two are different and investor schemes dominate the leverage of financial firms (Noulas & Genimakis, 2014). Thereafter, all those nonfinancial companies have been excluded, where the complete data was not available for all the variables for the chosen period. This resulted in a sample of total 134 firms comprising of 108 manufacturing companies and 26 service firms. Present study uses balanced panel data wherein SMEs represents cross sectional part with time duration of 6 years.

In this study, various firm specific variables have been chosen from the existing literature. Thereafter the impact of these factors has been evaluated on the financing choice of the sample firms. The financial data of the companies has been retrieved from the database ACE equity. Total 134 firms have been analyzed over a time period of 6 years resulted in total 804 firm-year observations. Panel data regression has been employed applying random and fixed effect models.

Data Description and Hypotheses Development

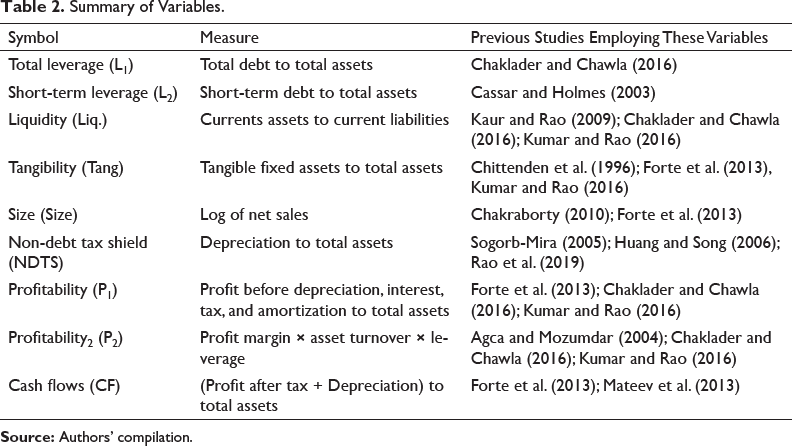

In the present study, leverage is the dependent variable. There are short-term as well as long-term sources of raising debt. Evidence regarding financing preference of SMEs with reference to short-term debt and long-term debt have been mixed. In the present study, leverage is measured in the following two ways:

Total leverage (L1) measuring the proportion of total debt to the total assets of the firm. Short-term leverage (L2) measures the relationship between short-term debt and total assets.

Measuring leverage in multiple ways also ensures the robustness of the results.

Description of Independent Variables

Liquidity: Current ratio is the measure of liquidity. Higher liquidity indicates less dependence on external finance. This leads to the first hypothesis: H1: Liquidity and leverage are inversely related. Tangibility: Tangible assets serves collateral and guarantee in case default occurs (Gaud et al., 2005). Hence, the proportion of tangible assets to total assets should matter for capital structure decisions. This leads to the second hypothesis: H2: Tangibility and leverage are positively related. Size: The size can be stated either in terms of volume of sales, value of assets, or market capitalization of the firm. In the present study, it is expressed in terms of log of sales as it reduces the impact of outliers. Hence, it is easier for the bigger firms to borrow. Moreover, transaction cost is relatively higher for smaller firms, which increases further during financial distress (Wald, 1999). Thus, the third hypothesis is as follows: H3: Size of the firm and leverage are positively related. Non-debt tax shield (NDTS): It considers tax deductions for depreciation and also investment tax credits. NDTS is expected to have negative correlation with leverage as it serves as a substitute for the tax shield from debt financing. Thus, the next hypothesis would be the following: H4: NDTS and leverage are inversely related. Profitability: It can be measured in terms of operating income and return of equity. Small firms rely more on internally generated funds from business operations as compared to external financing. This leads to the following hypothesis: H5: Operating income and leverage are inversely related. Though, return on equity is comparatively less examined variable in SME financing but leverages are known to influence return on equity. This leads to the next hypothesis: H6: Return on equity and leverage are inversely related. Cash flows: Excess cash flows are logically expected to reduce the funding requirement of SMEs forming the basis of the next hypothesis: H7: Cash flows and leverage are inversely related.

Table 2 provides the list of identified variables after extensive survey of the extant studies along with their symbols and measures.

Summary of Variables.

Research Models

The following mentioned models are formulated for further analysis from the variables selected:

Model A

Model B

where

Lit = leverage of ith firm at time t, α0 is an intercept and εit is the error term.

Statistical Methods and Tools

The method used for empirical analysis of data is a panel least square using SPSS and STATA. The widely used methods are ordinary least square (OLS), fixed effect (FE), and random effect (RE).

Analysis and Discussion

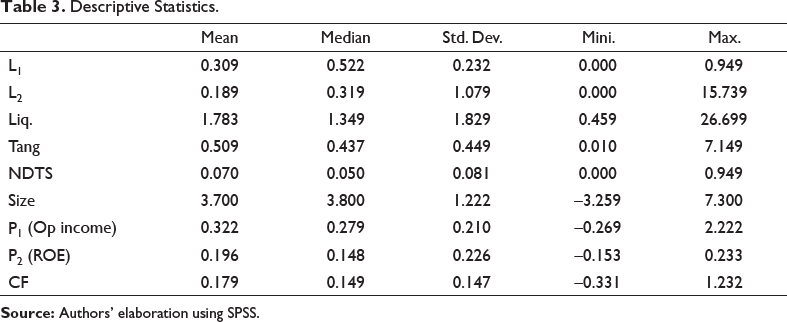

Descriptive Statistics.

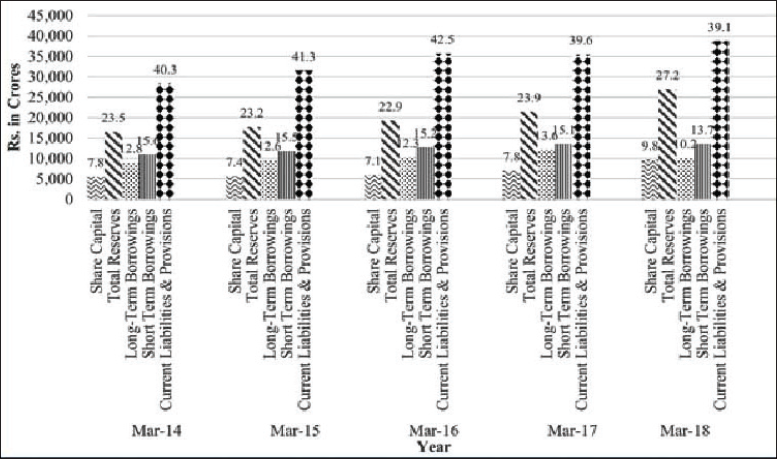

It can be concluded from both the mean values that the SMEs prefer short-term borrowings. This conclusion is in accordance with that of Kumar and Rao (2016) (Table 3).

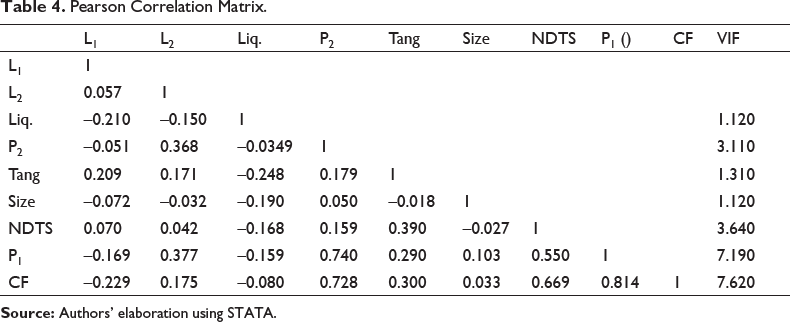

Pearson Correlation Matrix.

Further, for multicollinearity issue, the variance inflation factor (VIF) has been estimated. As shown in Table 4, the variables like operating income, ROE, and cash flows have VIF values less than 10; hence, they can be considered together line extension: they can be considered together for analysis (Neter et al., 1996).

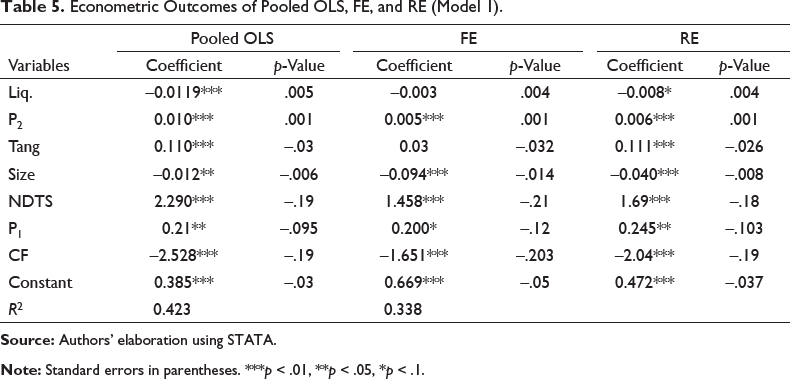

Model 1 Analysis

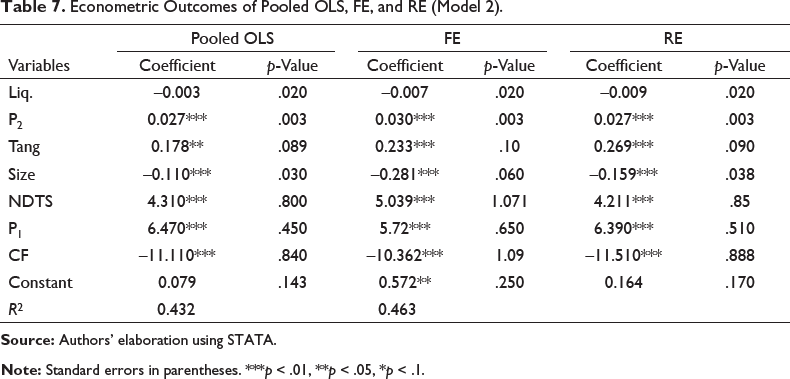

The Durbin–Watson test was conducted to rule out the possibility of autocorrelation among the residuals (Wansbeek, 1992) The test statistic obtained for Model 1 and 2 was 1.69 and 1.52, respectively. These values are considered to be normal. 5

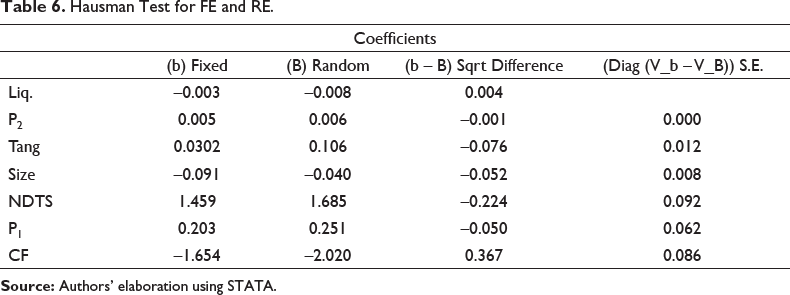

Next, the outcomes of the models were analyzed. The result of the Redundant Fixed Effects Tests rejects pooled OLS. Further, the Hausman test was done to find out the best estimate between the fixed or random effect models.

Econometric Outcomes of Pooled OLS, FE, and RE (Model 1).

Hausman Test for FE and RE.

The results of the Hausman test presented in Table 6 shows that the null hypothesis is rejected. Thus, the fixed-effect model is most suitable for the present study.

Model 2 Analysis

Econometric Outcomes of Pooled OLS, FE, and RE (Model 2).

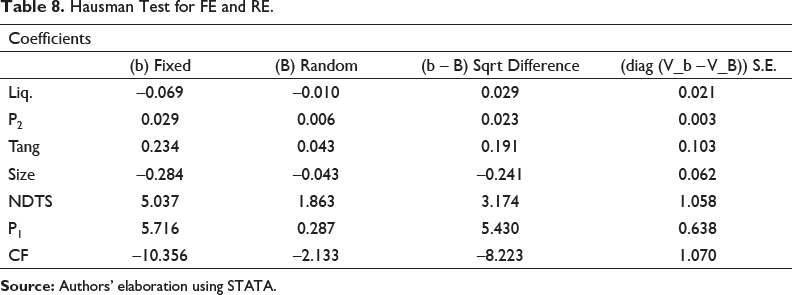

Hausman Test for FE and RE.

Looking at the larger picture, it is observed that the values of the R-square (33.8% in Model 1 and 46.3% in Model 2) in both the models are low. It indicates existence of the following two possibilities: either firm’s financing is affected by some external factors or there are some other firm-based factors influencing it which may not have been identified from the literature.

Mean Values of Leverage Ratios.

Based on their financing choices, it can be concluded that listed SMEs rely much on spontaneous liabilities as it is easy and quick. After that, they prefer to use retained earnings accumulated under the various heads of reserves. Then, if needed, they go for short-term loans. Generally, companies do not choose equity finance as it is a time consuming and costly affair. Hence, it can be observed from the figure that the levels of share capital have been almost the same throughout the period. It was increased a little in the last year that may be due to rise in number of SME listing during that time. Besides, long-term borrowings are preferred due to its tax advantage and in case of expansion plans.

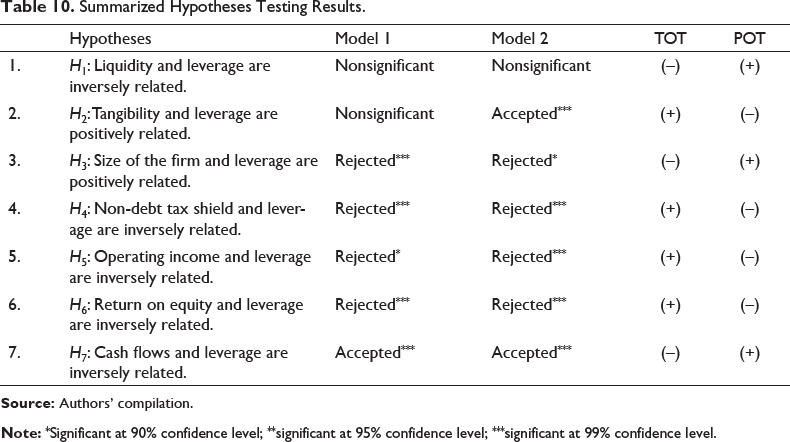

Hypotheses Validation

In this section the postulates made in the study were validated. The outcome of the empirical analysis suggests that the financing choice of SMEs is not affected by the size of the business in both the models. It may be because for the SMEs, investment revolves around their minimum criteria. Hence, size does not matter here.

Summarized Hypotheses Testing Results.

The hypothesis related to return on equity has also been rejected for Model 2. It means that the profitable firms have easier access to bank borrowings.

Concluding Remarks

The study aims to ascertain the key internal factors influencing the financing choices of listed SMEs in India. It evaluates the financing pattern of the Indian listed SMEs and observed if they follow the order explained under chosen theories of finance. The study covers the period from 2014 to 2019. Leverage is chosen as the dependent variable in the study. The outcomes of the empirical analysis suggested that tangibility and NDTS are positively related to financial leverage as per the TOT. Further, cash flows and profitability are negatively related to financial leverage, in accordance with the POT. Thus, the study identifies the factors influencing financing preferences significantly and also concludes that no single theory completely dominates the financing choices since the overall results are mixed.

Observing the financial preferences of SMEs closely, it is noted that first preferable source of finance for SMEs is current liabilities followed by accumulated profits and then short-term borrowings. Long-term borrowings and equity capital are the last choices. This conclusion is in line with Srinivas (2013) while it is in contrast with the study conducted by Kumar and Rao (2016), though their study was conducted for all SMEs and not only listed ones. This finding requires further investigation. The existing literature states that SMEs find it difficult to raise external funds. The major reasons stated by the researchers are lack of proper financial statements. However, this study has considered only listed SMEs that produce audited financial reports on periodic basis. They are considered to have higher creditworthiness, but still their debt–equity ratio show a declining trend. This needs to be studied in detail to examine if lending to any SMEs whether listed or non-listed is considered to be equally risky.

This issue of debt financing for listed SMEs is an area of concern in India. Listed SMEs are part of organized sector and if they are not financed appropriately, the matter may be all the more worse for the unorganized SMEs. It also raises a question on creation of SME exchanges. Additionally, the initiatives launched by the government post-2014 are expected to create a boost for Indian SMEs. It can also be inferred that the listing does not lift the financial strength of SMEs.

Though this is a comprehensive study, certain limitations are there that needs to be acknowledged. The data is entirely obtained from the secondary sources. For those SMEs that got listed recently, data is available for shorter duration while those listed since the inception of the exchange have data for the longer duration. Therefore, the outcomes are not generalizable. This leads to the following points about the scope of the future research that are discussed here: (a) the sample size can be larger, (b) some more firm-specific variables should be explored since the overall model shows lower R-square value, (c) Further, the impact of macroeconomic factors like government initiatives for SMEs, interest, and inflation rate to name a few on financial leverage can also be considered for empirical evaluation. Future studies can also focus on identifying the impact of force majeure event such as COVID-19 on financing pattern of SMEs.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.