Abstract

From antiquity to the present day, the contribution of small businesses to the economic development of a country is overwhelming. Nowadays, COVID-19 lockdown restrictions have exerted an outrageous impact on small businesses survival. In developing countries where government-supporting capacity is low, the severity is substantial. The present study predicts the impact of COVID-19 lockdown restriction and government supporting schemes on small business survival. To meet this purpose, the study primarily used PLS-SEM and binary logit models. The results confirmed that over 44% of small businesses would fail in the first month of lockdown restriction. Moreover, only 6% have cash reserve to survive twelve months. In this regard, the present study suggested that the government should have to abstain from total lockdown measures, without government-supporting schemes. As such, the study has examined the relative importance of COVID-19 based special loan, suspension of payments, withdrawal of restricted funds, and exemption of tax and penalty payments. Among these supporting schemes, COVID-19 based special loan is the most important government-supporting scheme followed by the suspension of interest and principal payments. However, the exemption of tax payments and withdrawal of restricted funds were not significant.

Introduction

There have been many significant pandemic outbreaks recorded in human history. The outbreaks affected the health and economy of society (Qiu et al., 2017). The COVID-19 outbreak was first known in Wuhan, China, in December 2019, and then the World Health Organization declared the outbreak as a pandemic on March 11. Europe, USA and Brazil are countries that suffered more from the pandemic. Egypt, Nigeria and South Africa have recorded the highest numbers of cases of COVID-19 in Africa.

In the COVID’s aftermath, countries put many restrictions around the world such as social distancing, the closing of schools, malls and recreation centers. When these restrictions were believed to be ineffective, most countries declared a state of emergency that led to the partial or total lockdown of people at their homes (Korsgaard et al., 2020). Ethiopia is among the African countries affected by COVID-19. The government announced a state of emergency on April 10, 2020, that put restrictions on public movement and business activities. Deciding based on the trade-off between economic costs of lockdown and the unrestrained spread of the pandemic is the major problem, especially in developing countries like Ethiopia (Qiu et al., 2017)

IIASA (2020) noted that after the economic downturn because of the lockdown restriction, the recovery of business to the usual tread might take three years. Above all, small businesses have less resilience and flexibility of handling the costs these pandemic entail than larger firms (Assefa & Yadavilli, 2020; Fabeil & Pazim, 2020).

As of WTO (2016) report, 95% of companies across the globe are small businesses accounting for 60% of the world’s total employment, 35% of GDP in developing countries, and around 50% in developed countries. However, past literature of COVID-19 focused on the context of economic, political and health arenas (Chetty et al., 2020; Dekker, 2020; IIASA, 2020; Yoshino et al., 2020). But the impact of COVID-19 in the context of small business survival is highly disregarded. To fill this gap, the present study opts to focus on the effect of COVID-19 lockdown restriction on small business survival.

Currently, government lockdown decision is the most controversial issue of controlling the spread of COVID-19. Because lockdown decisions entail an economic cost. Information about the economic cost of lockdown can assists decision-makers in the tradeoff between the economic costs of lockdown and the cost of uncontrolled spread of the pandemic. However, the existing few studies of COVID-19 in the context of small business simply narrates the lockdown effect on employees and owners (Beland et al., 2020; Fabeil & Pazim, 2020; Fairlie, 2020; Korsgaard et al., 2020; Nummela et al., 2020). Differently, this study used a model that predicts the probability of small business survival (economic cost) when 12 hypothetical lockdown periods are imposed. This study finding helps decision-makers to understand the cost and impact of their lockdown decision on small businesses’ survival.

Studies noted that the severity of COVID-19 negative effect on businesses varies depends on the amount of cash reserve (Bartik et al., 2020; Fabeil & Pazim, 2020; Liguori & Pittz, 2020; Morgan et al., 2020). But small businesses have less cash reserve and risk management capacity than large businesses (Arthur, 2007; Assefa & Yadavilli, 2020). For example, Bartik et al. (2020) conducted a survey of 5,800 small businesses in USA. They found that the average business with more than $10,000 in monthly expenses had only about two weeks of cash on hand. As such, small businesses are more vulnerable to COVID-19 lockdown restriction impacts (Korsgaard et al., 2020). Noticeably, the impact would be very serious where lockdown restrictions are imposed without any government financial incentive. Accordingly, many governments around the world have introduced small businesses’ supporting schemes, specifically liquidity supports. WTO (2020) disclosed the list of governments supporting schemes such as provision of COVID-19 based special loan, relaxation of financial requirements, payments suspension and exemptions.

The supporting schemes of developed countries might not be equally important for developing countries. Because, the government supporting capacity, marketing policy, types of financial markets and other institutional factors are different between developing and developed countries. This necessitates designing of supporting model based on the countries-specific circumstances. Despite existing studies describe the type of government-supporting schemes for small business (Brown et al., 2020; Riding & Haines, 2001; Shrimali, 2020; Viney et al., 2020), there is a dearth of literature that statistically predict the effect of government supporting schemes on small businesses survival, especially in the context of developing countries like Ethiopia. In this regard, the present study is exceptional by predicting the effect of Ethiopian government supporting schemes on small business survival.

Literature Review and Hypotheses

According to WTO data, 44 WTO members had announced urgent incentive and backstop actions for businesses by April 2020 1 . These measures essentially comprise state loans and credit guarantees, suspensions of interest and principal payments of outstanding loans, exemption of tax and rent, and loosening of financial regulation (releasing of security deposit or restricted cash). Viney et al. (2020), also survey the New York City small business owners and experts on how policymakers can help small businesses to survive the effect of COVID-19. They reported more than 50 supporting schemes such as helping businesses to retain staff with low or no interest loans, provide grants of up to $100,000 for directly affected businesses, provide a grant program for property owners to keep commercial tenants, lower the cost of debt servicing for small businesses, suspend fines, taxes, penalties, utility bills and insurance premiums.

The financial support of UK small business showed that when small business is facing cash flow issues because of COIVD-19, a new business interruption loan is delivered by the British Business Bank. The government has provided lenders with a partial guarantee of 80% on each loan to give lenders more assurance in continuing to provide finance to SMEs. The government will not burden businesses or banks for this guarantee, and the scheme will fund loans of up to £5 million in value. The first six months of these loans will be interest free. Besides, France announced post payment of direct tax and loans without guarantee, without real collateral on the assets of the company or its manager. General tax authority (GTA) has proclaimed a 2-month postponement for the filing of tax returns for the tax year wind-up December 2019, the new deadline date June 2020.

Middle East countries such as the United Arab Emirates (UAE) and Qatar took various financial supporting measures. In March 2020, the United Arab Emirates (UAE) announced the extension for the filing of tax returns, delay of rent payments by six months, facilitating installments for payments, refunding security deposits and guarantees, termination of fines. Qatar also announced on March 15 for a temporary exemption from payment of water and electricity, fees six months grace period for payment of outstanding loan installments and interest.

Factually, the government of Ethiopia supports SMEs in various aspects such as access to markets and finance. At macro level, the role of SMEs and their performance in the economy is not clearly known. Nevertheless, the government claims that SMEs’ contribution to the GDP is less than 20%.

Recently, to reduce the impact of COVID-19 on employees and to stimulate the economy, the government of Ethiopia announced to cancel payment of fines and interest on deferred tax for the past ten years. According to the ministry of revenue, payment of the principal amount within one month is the major criteria to be eligible for this supporting scheme. Accordingly, on August 22, 2020, Fana broadcasting corporation (FBC), the government affiliated media, reported that tax fines and interest payments were cancelled for 2,411 businesses from deferred tax of the 2015/2016 fiscal year. Besides, from deferred tax of 2015/2016 up to 2019/2020 fiscal years, interest and fines of 5.9 billion Birr has been cancelled for 1,267 businesses that operate in the federal jurisdiction. Nevertheless, the scheme does not explicitly state any special supporting program in the context of small business.

Theory of Business Survival and Survival Strategies

The literature on small business growth and survival has seen a significant expansion in recent years. Most of these studies used business survival theory. Business survival theory assumed that small firm would survive as long as net profit is greater than zero. Normal business operation and determinants of profit are also the founding concept of this theory. Past studies estimated small business survival by analyzing the determinants of profit at the normal business operation. Reid (1993), confirmed that market, financial and life cycle variables are the key determinants of profit in the analysis of small firm survival.

Many countries closed markets and businesses areas to control the spread of COVID-19. As a result, small businesses are paying fixed costs such as salary and rents, while sale is zero or profit is negative. In this regard, the survival theory assumption ‘net profit should not fall below zero’ cannot be sustained. Thereby, survival theory has a limitation to measure small business survival during crisis such as COVID-19 lockdown restriction where profit is negative and businesses are closed.

Assefa and Yadavilli (2020) introduced a new small firm survival theory of lockdown restriction where profit is negative. They stated that cash reserve, fixed cost and lockdown durations are the determinants of small business survival. The theory assumed cash fund should not be less than the product of monthly fixed cost and the number of lockdown months imposed by government. In short, as long as the ratio of cash reserve and fixed cost is greater than one, the business will survive and vice versa. They posit that when cash reserve is less than fixed cost, cost cut measures such as dropping employee can harm the economy and livelihood of the employees at large. They finally suggested that government support is more important than cost-cut survival strategy of the business. Accordingly, to predict the effect of COVID-19 lockdown restrictions and government supporting actions on the survival of small business, the present study opts to use the theory of small business survival strategy when profit is negative.

Hypotheses

The Impact of COVID-19 Lockdown Restrictions on Small Business Survival

Many studies of small businesses in the context of COVID-19 confirmed that small businesses have less resilience and flexibility to survive the crisis than larger firms do (AMTC, 2020; Fabeil & Pazim, 2020; Fairlie, 2020; Lindsay et al., 2020; OECD, 2020; Riding & Haines, 2001; Shrimali, 2020; Viney et al., 2020).

For example, as Liguori and Pittz, (2020) reported the 2020 Goldman Sachs survey of 10,000 small business owners, 96% are already impacted by the COVID-19 and 51% cannot survive 3 months of a lockdown restrictions. Exacerbating the problem, 67% report difficulty accessing emergency funding. Likewise, a survey by Tsinghua and Peking University, of 995 SMEs in China found that 85% could not survive lockdown restrictions for more than three months (OECD, 2020). This implies, less than a year of lockdown restriction can throw 85% of small businesses to failure. According to Lindsay et al. (2020), 50% of small businesses in the United States have already shut down and 27% indicated that they would be obliged to take such actions soon.

Despite their importance, most of these studies used descriptive statistic method that merely narrates the effect of lockdown on small business. As a result, the statistical relation between lockdown period and small business survival is not clearly known yet. To address this problem, the present study used inferential statistical model that predicts the impact of COVID-19 lockdown restriction by manipulating 12 hypothetical lockdown months.

Financial Supporting Schemes (FSS)

Most previous studies of small business in the context of government supporting focused at the normal state of business operation (Bruce et al., 2015; Riding & Haines, 2001). Moreover, they focused on the startup financial and technical supports (Hansen et al., 2009). Despite much has been learned, the government intervention and support during crisis time like COVID-19 lockdown restrictions remain to be explored.

During the lockdown restrictions, cash reserve and cost-cut measures are internal strategies that used to prevent small businesses from failure. However, many small businesses lack sufficient amount of cash reserve (Assefa & Yadavilli, 2020). For example, the Asia-Pacific Trade Coalition reported that almost 50% of small businesses in the region have less than a month or just a month of cash reserves (AMTC, 2020). On the other hand, the cost cut measures such as the dropping of employee might harm the economy and livelihood of employees. Thus, to protect small businesses and the employees they support, governments are obligated to introduce various supporting schemes as the only viable means to de-escalate the negative effects that emanates from COVID-19 lockdown restrictions.

Though studies examined the role of different supporting schemes for small business to coup with lockdown restriction, it is still unknown the aggregate quantitative effect of government supports on the probability of small business survival. As such, this study predicts the effect of government financial supporting schemes on small business survival.

Noticeably, most of the above supports are financial schemes, specifically liquidity measures that intended to increase the cash inflows or decrease cash outflows. Providing COVID-19 based special loan and releasing of restricted fund are intended to increase cash inflows. On the other hand, allowing tax exemption, suspension of loans and other payments are proposed to decrease cash outflows. However, there is a scanty of literatures that consider the entire supporting scheme and gage their relative importance. Thereby, in the context of small businesses survival, this study predicts the importance of special loan, suspension of payment, relaxation of financial requirements and exemption of payments.

In the aftermath of COVID-19, governments have intervened in the capital market as a direct provider or guarantor of loans that financial institutions advance to small businesses has more attention. Studies also recommended a different type of loan that put less burden on small business (Bartik et al., 2020; Viney et al., 2020; Yoshino et al., 2020). Despite government high intervention into the credit market, the demand for special loan is rising steeply. For example, as Liguori and Pittz (2020) reported in the 2020 Goldman Sachs survey of 10,000 small business, economic lockdown effect on small businesses is exacerbated by which 67% are unable to access emergency funding.

Credit market analysis is not the purpose of this study; rather it seeks to estimate how special loan is important for small business survival. Because, relative to other government supporting schemes, the effect of special loan provision on small business survival is not clearly known yet. The present study is important because the results can be used to understand the significance of special loan provision for small business to coup with the social and economic lockdown.

According to WTO (2020), the nature of COVID-19 based special loan is it puts a low burden on borrowers, low-interest rates, long-term maturity, less financial requirements, partially guaranteed by the government. The loan is provided to cover payments for salary, rent and other fixed expenses (insurance and payroll tax). For this study, a special loan is operationalized to consider all the specified characteristics of special loan.

Though time deposits allow withdrawal before the stated maturity, it has penalty equal to some percentage of face value (Gilkeson et al., 1999). Likewise, an early withdrawal from retirement accounts may have less economic benefit when withdrawals significantly reduce retirement resources (Argento et al., 2013)

Literatures of tax policy, particularly tax and penalty exemption reveals a contradicting finding. Hansen et al. (2009) and Gurley-calvez et al. (2008) argued that tax exemption has impact on the performance and location decision of small business. Whereas Bruce et al. (2015) state that relative to property crime rate, tax exemption may not affect small businesses survival.

The theory of small business survival strategy when profit is negative, assumed that variable costs (utility expenses) are zero (Assefa & Yadavilli, 2020). Thus, excluding utility expenses, this study posits that exemption of tax payments and penalties are the suitable supporting scheme.

Methodology

The research used both primary and secondary sources of data. The primary data were collected from eight major cities: Addis Ababa, Adama, Dire Dawa, Jigjiga, Bahir Dar, Gondar, Dessie and Hawassa. Whereas secondary data were collected from related literature, reports, media and magazines. Five-point Likert scale questionnaires were employed for primary data collection. The sample size was determined based on the research model. For the structural equation model, 10 times the maximum number of arrows pointing to a construct rule was applied (Hair et al., 2012). In this study, the maximum numbers of arrows are 3. They are pointing to special loan constructs. Accordingly, the sample size would be 30. But the study used 46 samples that boosted up into 5,000 samples using bootstrapping procedure. On the other hand, to estimate the effect of lockdown on business survival, a standardized table was used. It takes into account the population size, standard of accuracy and acceptable confidence level (Kothari, 2004). The population size of registered small businesses in the study areas is 72,000. According to the standardized sample table, when the population size is less than 75,000 the sample size shall be 372. Thereby, 372 observations were analyzed to predict the probability of small businesses’ failure at lockdown. Since business survival is binominal that is grouped under survival or failure categories, binary logit is used to predict the probability of small business survival.

Descriptive and inferential statistics were used to analyze data. The descriptive statistics employed to summarize, classified and represent results on graphs and tables. To identify the types of relevant financial supporting schemes and to predict the financial supporting schemes’ effect on small business failure prevention, a partial list square-structural equation model (PLS-SEM) was used 2 . Because PLS-SEM is appropriate, where the research model is complex, necessitates both confirmatory factor and cause-effect analysis, weak theoretical support and sample size is small (Fornell & Larcker, 1981; Josephb et al., 2014).

Finally, importance-performance map analysis (IPMA) was used in extending the findings of the basic PLS-SEM outcomes using the latent variable scores. The extension builds on the PLS-SEM estimates of the path model relationships and adds dimension to the analysis that considers the latent variables’ average values. More specifically, the results permit the identification of indicators with relatively high importance and relatively low performance (Lohmoller, 1989).

Research Model Description

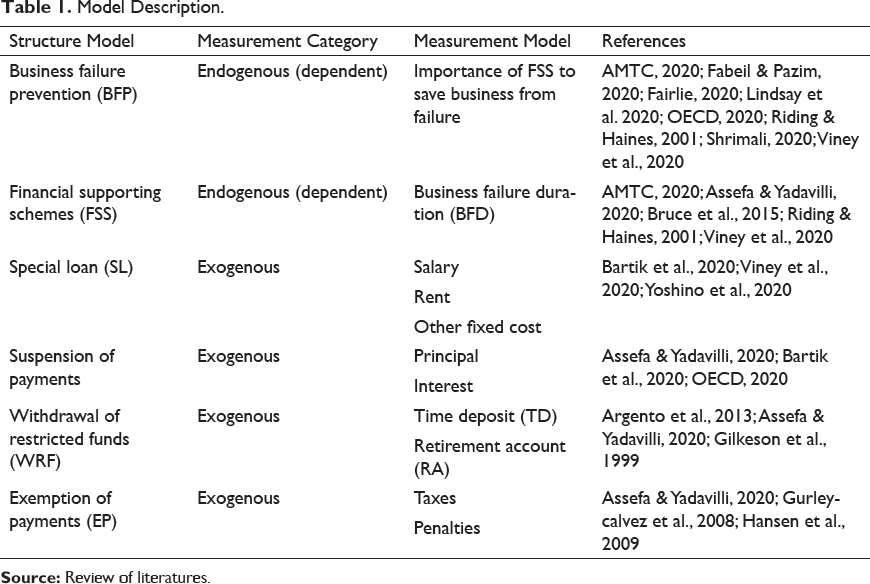

As stated in Table 1, the study model has eleven reflexive indicators and six constructs that are classified under measurement and structural models. The measurement model shows the relationships between indicators and constructs. The structural model explains the connections among constructs that are primarily used to test hypotheses. Furthermore, the structural model is classified under exogenous and endogenous constructs. The exogenous constructs are independent. Whereas the endogenous constructs are dependent on the value of exogenous constructs.

Model Description.

Measurement of Variables

Financial Supporting Schemes

Previous experience shows that one up to three months of lockdown was commonly imposed to control the spread of pandemic disease (Fabeil & Pazim, 2020). The lockdown period is measured by the number of lockdown months imposed by government. The effect of pandemics disease and the number of lockdown months are directly related (Assefa & Yadavilli, 2020). The longer the lockdown months, the larger the business failure will be.

For this study, a maximum of 12 possible lockdown months are assumed. Arithmetically, the value of business failure assumed within the interval (0, 12). On the other hand, the larger the business failure, the higher the financial support required (Assefa et al., 2020). The amount of financial supporting is the product of fixed cost and business failure duration (FC×12).

Business failure duration is measured by the complement of business survival within a year. If there are ‘n’ months of business survival during the lockdown period per year, there will be (12–n) months of business failure duration. Business survival theory of negative profit posits that the longer business failure duration, the larger supporting schemes required and vice versa. Thus, the present study used business failure duration as the indicators of financial supporting scheme construct.

Managers’ responses to five Likert scaled questions were used to measure the relevancy of each financial supporting schemes (SL, SP, EP and WRF). Therefore, as stated in eq. 1, special loan facility (SL), suspension of interest and principal payments of loan (SP), exemption of tax and penalty payments (EP), and withdrawal of restricted fund (WRF) are designed as exogenous constructs that explain the relevancy of financial support scheme (FSS).

Business Survival

Business survival is operationalized as the ability of the business to cover its fixed cost during the lockdown period. In this case, the study assumed that sales and purchases are zero (Assefa et al., 2020). Thereby, it is difficult to measure business survival based on profit. As such, to measure business survival, the study opts to use the ratio of cash reserve and fixed cost.

The business is assumed to have a given risk tolerance, characterized by cash reserve ‘R’. Losing of more than ‘R’ dollars within a given lockdown period represents the business failure. Assuming the cash reserve (R) and fixed expense per month (FC), business survival is computed as follows:

If R/n * FC < 1, the business will face a serious problem to pay salary, rent, debt, interest, insurance and other fixed bills. This condition is the beginning of business failure. On the other hand, if R/n * FC ≥ 1, the business can survive the lockdown without any financial support. When survival equation ratio reaches one, government financial support is mandatory to prevent business from failure and continue for the remaining lockdown period (failure duration; 12–n).

Lockdown duration has a positive relationship with business failure (Assefa & Yadavilli, 2020). The longer the lockdown duration, the larger the business failure will be and vice versa. Thus, the following equation is used to predict the effect of possible lockdown durations on business survival.

In this equation, the predicted values of business survival fail out of (0, 1). To control this limitation, the probability of business failure was computed by:

Then business failure prevention estimated using the following condensed equation:

Evaluation of the Measurement Model

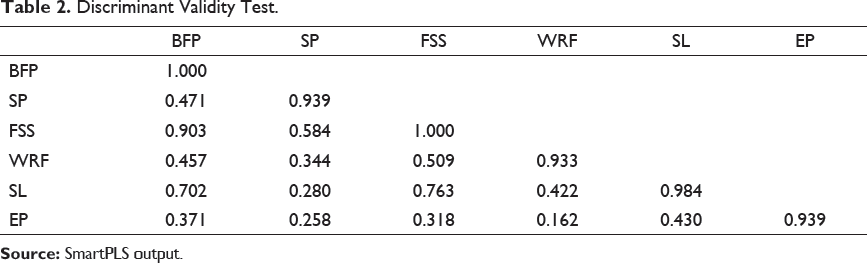

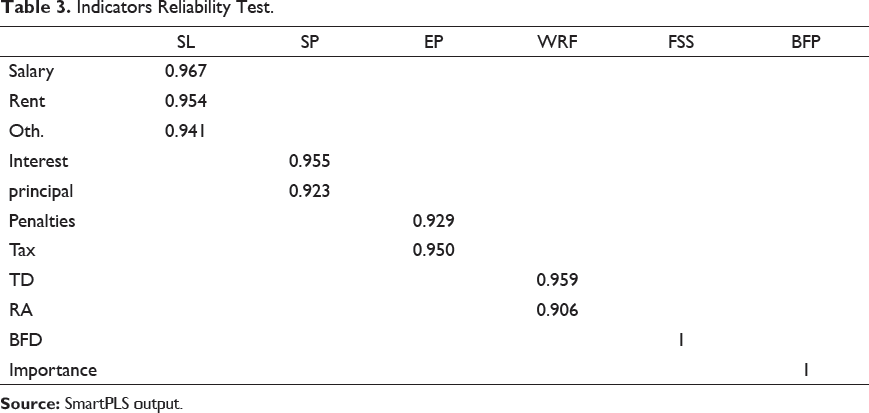

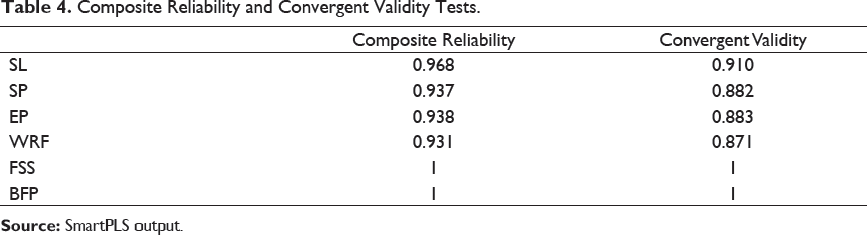

Evaluation of the measurement models delivers empirical measures of the relationships between the indicators and the constructs. In this study, all constructs are framed as a reflexive model. The goal of reflective measurement model evaluation is to confirm the reliability and validity of the construct measures and provide support for the suitability of their inclusion in the path model. The key criteria are indicator reliability, composite reliability, convergent validity and discriminant validity (Hair et al., 2012).

Discriminant Validity Test.

Indicators Reliability Test.

Composite Reliability and Convergent Validity Tests.

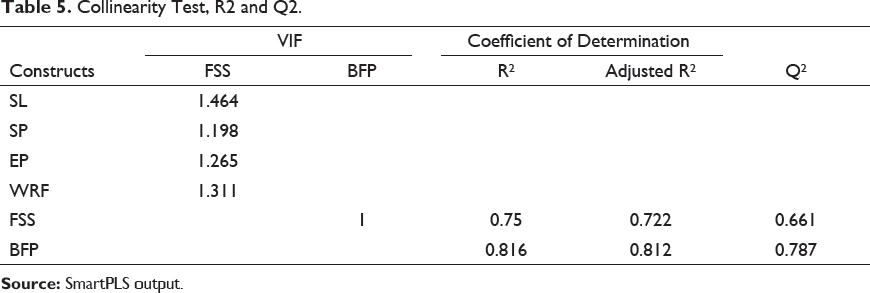

Evaluation of Structural Model

The second part of the test focused on the model’s predictive capabilities. Most importantly, evaluation of structural model used to test the research hypotheses. Collinearity, R2 and Q2 criteria must be achieved before hypotheses testing (Hair et al., 2012). Thereby, the first section presets the structural model test results. Once the model predictive capabilities assured, the second section assess the research hypotheses.

Collinearity: According to collinearity diagnostics rule, each predictor construct’s tolerance value (VIF) must be higher than 0.20 but lower than 5. In Table 5, the maximum and minimum VIF values of the predictive constructs are 1.464 and 1, respectively. Therefore, collinearity issue is not the problem for the structure model.

Collinearity Test, R2 and Q2.

Predictive relevance (Q2): The blindfolding procedure was used to test the predictive relevance of endogenous constructs. As long as q-square is above zero, the path model has a predictive relevance. Table 6 shows that the q-square values of FSS and BFP are 0.661 and 0.787, respectively. This result successfully confirmed the relevancy of BFP and FSS predictive values.

Findings

The Impact of Lockdown Restrictions on Business Survival

The binary logit employed to predict the effect of COVID-19 lockdown restriction on small business survival. As stated in Table 6, the constant and coefficient of business survival equations are 0.487 and –0.267, respectively. However, from this equation, direct probability computation is difficult. To control this limitation, using the constant and coefficient values, the following probability equation has been derived.

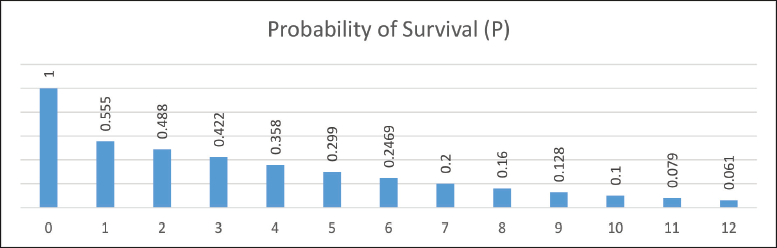

The coefficient (b = –0.267) in Table 6 and the pattern of Figure 2 confirmed that lockdown period has a negative impact on business survival. When the lockdown period increased, the probability of business survival is continuously decreased.

When twelve months of lockdown period assumed, the survival probability is only 0.06. This means, the probability of business failure for twelve months lockdown period is 0.94 (1–0.06). Moreover, business failure probability for the first month restriction is 0.445 (= 1 – 0.555). This is much greater than the cumulative probability of eleven months (0.414 = (0.555–0.061)). This implies, 44.5% of the businesses have less than a month of cash reserve.

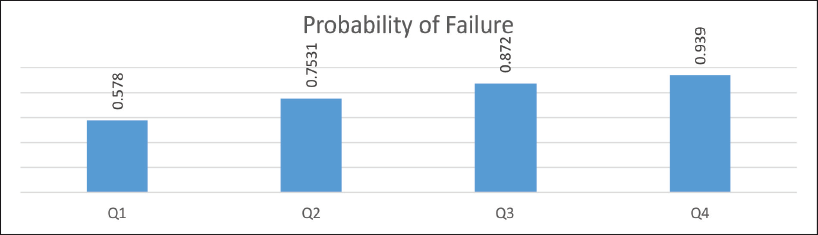

Figure 3 represents the quarterly cumulative probability of business failure. If government imposed three months of lockdown, more than 55% of small business will fail. When the lockdown period extended to six months, the impact will be more than 75% (Q2).

Binary Logit Result.

As stated in Table 6, the path coefficient of the binary logit result was –0.627. This result is statistically significant (p < 1, t = 40.641). Thereby, the first hypothesis ‘the lockdown duration has a significant negative effect on small business survival’ is accepted.

Important Components of FSS in Small Business Failure Prevention

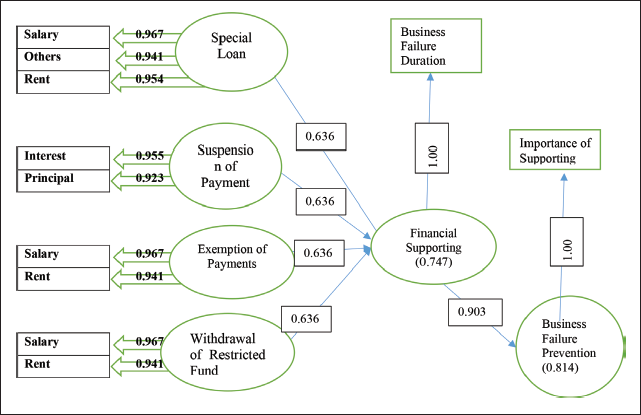

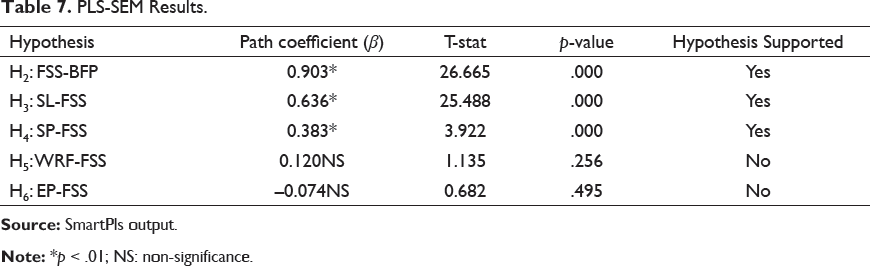

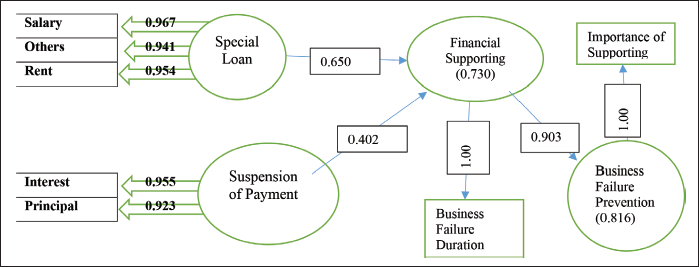

The research model designed special loan (SL), suspension of payments (SP), withdrawal of restricted fund (WRF) and exemption of payments (EP) as the important component of financial supporting schemes (FSS). As presented in Table 7, the special loan has the largest path coefficient (0.636) followed by suspension of payments (0.383). This result confirmed the hypotheses that special loan is an important component of FSS in business failure prevention (t = 25.488; p < 1%) and suspension of payment is an important component of FSS in business failure prevention (t = 3.922; p < 1%).

PLS-SEM Results.

In Table 7, the statistical result revealed that the exemption of payments is not statistically significant to prevent the business from failure (t = 0.682; p = .495). In this regard, the research hypothesis ‘exemption of payments is an important component of FSS to prevent business failure’ is rejected.

Likewise, the path coefficient of WRF (b = 0.12) is not statistically significant (t = 1.135; p = .256). Thus, the research hypothesis ‘withdrawal of restricted fund is an important component of FSS in business failure prevention’ is rejected too.

Finally, the path coefficient of FSS, in Table 6, is statistically significant (b = 0.903; t = 20.665; p < 1%). Therefore, the analysis supported the study hypothesis: ‘FSS has a significant effect on small business failure prevention’. To this end, as depicted in Figure 4, the final research model is developed by dropping exemption of payments and withdrawal of restricted constructs from the original model.

Importance-Performance Map Analysis

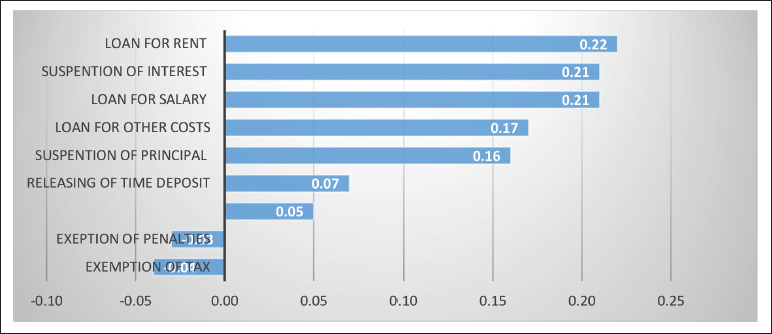

As discussed above, special loans and suspension of payments are the most important predicting constructs of FSS in small business failure prevention. However, the test did not specifically gage the importance of these constructs’ indicators. The importance-performance map analysis (IPMA) is used to rank all predicting indicators of BFP construct. Figure 5 has depicted the relative importance of nine indicators in business failure prevention. The result shows that providing COVID-19 based loan for payment of rent (0.22) is the first important indicator. The suspension of interest payment (0.21) and granting of COVID-19 based special loan for payment of salary (0.21) are the second most important indicators (the ranks are tight).

The third and fourth important indicators are loan for payment of other fixed costs and suspension of loan principal payment, respectively. However, the indicators of exemption of payments and withdrawal of restricted funds—time deposit (0.07) cancelation of penalties (0.05), exemption of tax (0.07), and withdrawal of retirement accounts (0.04)) are not statistically important to save small business from failure.

Discussion and Implication

Most studies of COVID-19 have concentrated on the health, political and macroeconomic impacts. In spite of the small businesses’ substantial economic contribution and their high vulnerability for economic shocks, few studies of COVID-19 focused on small businesses survival. The existing few studies of COVID-19, in the context of small business, primarily narrates the impact of COVID-19 using surveys. The present study is different because it predicts the impact of lockdown restriction on small business survival using 12 hypothetical lockdown periods. The result helps policymakers to trade-off the economic costs of lockdown and the uncontrolled spread of the pandemic.

In view of that, the result confirmed a one-month total lockdown restriction could lead 44% of small business into failure. This means, 44% of small businesses have no cash reserve that can just cover a month of fixed cost. This result is in line with the Asia-Pacific Trade Coalition that reported 50% of small businesses in the region have less than a month or just a month of cash reserves (AMTC, 2020). Furthermore, the model predicted that only 4% of the small businesses have cash reserve to cover 12 months of fixed cost. Being more conservative, if 12 months lockdown assumed, the probability of small business survival is 0.06. When the result closely examined, the first month probability of business failure (0.44>) is greater than the cumulative probability of eleven months (0.414). The quarterly cumulative probability of business failure is 55%. This result is in line with Liguori and Pittz (2020) and OECD (2020) who reported 51% of 10,000 small businesses in USA and 85% of 995 small businesses in China could not survive lockdown restrictions for more than three months, respectively.

As anticipated in H1 , the binary logit path coefficient is negative (b = –0.267). This implies a unit change in lockdown period will reduce the survival probability by the rate of 0.267. Therefore, the study result confirmed the significant negative effect of lockdown duration on small businesses survival (p < 1; t = 40.641).

Predicting the impact of government financial supporting schemes on small business survival was the second objective of this study. The study found that many governments have introduced liquidity support intended to strengthen cash on hand. Though studies and experts recommended the liquidity support, its quantitative effect on the probability of small business survival is unknown.

To fill this gap, the present study predicts the government financial supporting schemes on small business survival. Accordingly, the result confirmed a significant positive effect on small business failure prevention with a large predictive accuracy (R square = 0.816). This means, taking the correlation coefficient of financial supporting schemes and small business failure prevention constructs into account, a unit change in financial supporting schemes can reduce the probability of small businesses failure by 81.6%. For example, as shown in Figure 2, the probability of small business failure for a month lockdown is 0.44. The government supports can reduce this failure probability by 36% (0.44 × 0.816). However, to reduce the small business failure probability into zero, other supporting schemes are required.

Literature reveals that any COVID-19 based financial support has to improve the liquidity level (Liguori & Pittz, 2020). Thereby, providing COVID-19 based special loan and withdrawal of restricted funds increase cash inflows. Whereas the exemption and suspension of payments decrease cash outflow.

There are studies in the context of government supporting schemes. However, there is scanty of literatures that gage the relative importance of each supporting schemes. As such, among many supporting schemes introduced by governments, it is difficult to identify the most or the least important scheme. This study is important because it tests the relative importance of special loan, suspension of payment, withdrawal of restricted funds and exemption of payments using a monologue model.

The model result confirmed that special loan plays the most important role followed by the suspension of payments. Specifically, providing loan for rent and salary expenses payments are the crucial component of COVID-19 based special loans. Among payment suspension indicators, extending the interest payment date is more important than the suspension of the principal due date. The logical reason behind this finding is that interest is usually paid on a monthly or quarterly basis. However, the due date of principal payment is longer than interest payment date, at most a year. Thus, small businesses usually prefer the suspension of interest payment dates.

During the lockdown period, businesses are not obligated to pay tax while sales and purchases are zero. Accordingly, the exemption of tax payment is more convenient at the juncture of normal business operations. The study results confirmed that the exemption of payments and withdrawal of restricted funds are not statistically significant. Moreover, the path coefficient of tax and penalties payments exemption is negative. The negative sign indicates its inverse relation with financial supporting schemes. This implies the importance of tax payment exemption decreases when a lockdown period or business failure increases. Regardless of their significance, during the lockdown restriction period, withdrawal of restricted fund is more important than the exemption of tax and penalties. Based on this result, the exemption of differed tax and payment of liability that was enacted in Ethiopia could not save businesses from failure. The measurement was simply a strategy used to encourage early collection of outstanding tax for more than ten years. Moreover, the schemes exclude the majority of prompt taxpayers and lacks specific consideration of small business. Besides, it excluded those businesses operating in regional jurisdictions.

Conclusion

The study confirmed that lockdown restriction has a devastating impact on the survival of small businesses. As such, the government should have to abstain from total lockdown measures. However, if the government chose lockdown as the only viable option, the government must initiate financial supporting schemes, specifically special loan, and suspension of interest and principal payments.

Since the exemption of payment is not statistically significant, penalties and interests’ payment exemption for the deferred taxes that enacted in Ethiopia could not prevent the small business from failure. Instead, it encourages the prompt collection of outstanding tax. Consequently, the support is more beneficial for government than small businesses.

Recommendation for Long Term Actions

The world is now undergoing in the fourth industrial revolution that can transform the economy in to digital world. This digital transformation mostly helps small business to be efficient in production and marketing. Specifically, at the difficult time like the eruption of COVID-19, digital economy helps small business to survive from the devastating impact of lockdown restrictions.

However Ethiopia is yet unleashed its potential in the digital world that can easily create efficiency in the production and marketing system. Therefore a coordinate actions from government and entrepreneurs are necessary to transform small business’ market into digital space.

Limitation and Future Scope of the Study

Since pandemic like COVID-19 is a rare phenomenon, there is a dearth of empirical literatures and theories about small business survival at lockdown. In this regard, the study lacks sufficient supporting theories and published literatures.

The scope of this study is limited to the short-term financial supporting schemes, specifically liquidity expansion. Future studies can develop a more inclusive supporting model by adding long-term supporting schemes such as trade facilitation, market linkage and the concept of e-market.