Abstract

This article examines the macroeconomic implications of central bank digital currencies (CBDCs) and private cryptocurrencies using a simple real business cycle model. The analysis explores how agents allocate their portfolios among fiat money, CBDCs and private cryptocurrencies in response to inflation shocks and technological advancements in cryptocurrency production. The model predicts that rising consumer confidence can gen-erate inflationary pressures, prompting a shift towards private cryptocurrencies, which are insulated from inflation tax. Additionally, positive shocks in cryptocurrency production can lead to capital reallocation, reducing final goods production and causing a brief spell of recession. A central bank can remarkably counteract this recessionary effect of a crypto boom by lowering the policy rate. These findings highlight the complex interplay between digital currencies and monetary policy, emphasizing the need for strategic interventions using policy rate as a tool to balance economic stability and crypto innovation.

Introduction

In recent years, central banks (CBs) in many countries have considered introducing digital currency. In India, in the Union Budget of 2022-23, the Finance Minister Smt. Nirmala Sitharaman proposed the introduction of central bank digital currency (CBDC) that is known as e-rupee. As of today, e-rupee is still at a pilot phase and not widely available in the public domain. To the best of my knowledge, as of January 2025, nine coun-tries and the Eastern Caribbean Currency Union have adopted CBDC. China is also pondering over such an experiment. UK, US and European CBs are still exploring the possibility of launching CBDC.

The CBDC is not well understood. It is a form of digital token issued by the CB. In contrast, privately issued digital currencies, such as Bitcoin, operate on blockchain technology and circulate without regulatory oversight. These bitcoins are unregulated assets created by the private sector using a sophisticated blockchain technology. The return from this asset emanates from its scarcity value like gold. Such a bitcoin can thus be an income generating asset as well as a means of payment. The blockchain system on which the bitcoins are traded has some degree of anonymity due to its highly decentralized feature. Such an anonymity breeds risk of money laundering, cheating and default in private bitcoin transactions. The introduction of CBDC means that the CB is competing with privately issued bitcoins by offering a digital currency which is free from such risk because CBDC is a legal tender. On the other hand, the expected return from holding CBDC as a store of value may be less than private bitcoins. The private citizens then face a portfolio choice problem of holding riskless CBDC, cash and high-risk–high-return privately issued digital currencies.

In this article, I lay out a simple real business cycle (RBC) model to understand the effect of simultaneous operation of CBDC and bitcoins on the aggregate economy. The model builds on the framework outlined in Basu (2024). Private agents make a dynamic portfolio decision of holding four assets, namely cash, bond, CBDC and bitcoins. Bitcoin production is costly because it diverts physical capital from the production of final goods. Return to bitcoin is risky and so is the production of final goods due to technological uncertainty. Households solve an optimal capital allocation problem every period based on the relative return of bitcoin production vis-à-vis final goods. The CB effectively targets inflation using the policy rate as the instrument. Inflation is also driven by a negative total factor productivity (TFP) shock. An adverse TFP shock in the form of a supply chain bottleneck elevates inflation reminiscent of Covid days.

The model illustrates the complex interactions between the final goods sector and Bitcoin mining in response to various economic shocks. In a scenario where the CB targets inflation using its policy rate while an interest-bearing CBDC is available, a positive consumer confidence shock can stimulate Bitcoin mining and GDP growth through an investment surge. However, the resulting inflationary pressures reduce real balances, CBDC holdings and overall consumption. Similarly, a positive innovation in the cryptocurrency sector can boost Bitcoin mining, drawing physical capital away from final goods production. This decline in final goods output may lead to a spell of recession. The CB can counteract this downturn by lowering the policy rate, which stimulates investment and GDP growth. Conversely, a negative TFP shock, such as one caused by supply chain bottlenecks, can also trigger a recession. However, if Bitcoin offers higher relative returns, investors may shift their portfolios from cash and CBDCs to Bitcoin. In response, the CB may raise policy rates to combat inflation, inadvertently discouraging aggregate investment. The study highlights the important role of the CB’s policy rate as an effective tool to stabilize the economy in response to crypto innovation.

What Are CBDC and Bitcoins?

A CBDC is a sovereign digital currency issued and regulated by a CB. It is designed to retain the essential characteristics of physical currency. The Reserve Bank of India’s (RBI’s) concept note outlines how CBDC will function in India, stating that all private citizens will have access to them. CBDC can be either token based or account based. Token-based CBDC functions like a bearer instrument, meaning its ownership is determined by possession. In this system, the RBI would be solely responsible for issuing digital tokens, similar to physical cash and coins. Account-based CBDC requires an intermediary to verify the identity of the account holder, akin to the Know Your Customer (KYC) process used in banking.

Unlike cash, CBDC transactions will not be anonymous, as the RBI will have the ability to monitor and trace transactions. However, due to the high cost of monitoring, smaller transactions may be subject to lower scrutiny. The exact degree of anonymity has yet to be disclosed by the RBI. Given the digital nature of CBDC, a robust technological infrastructure will be crucial. The RBI may use either a conventional database system or a distributed ledger technology, though it has not yet specified its preferred approach. CBDC will be denominated similarly to physical cash, serving as both a medium of exchange and a unit of account, with legal tender status. Additionally, if CBDCs are designed to bear interest, they could function as a store of value, making them a potential substitute for bank deposits.

Unlike CBDC, Bitcoin is a privately issued and unregulated digital currency that allows transactions without an intermediary, such as a bank. Its creator, Satoshi Nakamoto, described Bitcoin as ‘an electronic payment system based on crypto-graphic proof instead of trust.’ This system requires participants to invest computa-tional resources in mining bitcoins, using blockchain technology to establish proof of ownership. Bitcoin’s value is highly volatile. Since its introduction in 2009, its price has surged dramatically. Due to its limited supply, many investors treat Bitcoin as digital gold, using it as a hedge against inflation and currency fluctuations. Bitcoin holders can convert their assets into cash, which can then be transferred to bank accounts. This conversion is typically facilitated by third-party exchange brokers, including Bitcoin ATMs and debit card services that exchange Bitcoin for cash at a specified rate. Alternatively, Bitcoin can be sold via peer-to-peer transactions. The conversion process usually takes 4–6 days, and transaction fees can be high.

Despite its advantages, Bitcoin faces several challenges. Its unregulated nature makes it susceptible to fraud, though counterfeiting is nearly impossible due to blockchain security mechanisms. Nonetheless, the lack of oversight raises concerns regarding its use in illicit activities endangering financial stability. This article is among the few in the literature that examines the simultaneous operation of CBDCs and Bitcoins. The production of Bitcoin is highly costly, divert-ing resources from the production of final goods and potentially leading to resource misallocation by reducing present consumption. In contrast, while CBDC produc-tion is also costly, its expenses are covered through lump-sum taxes on households, preventing allocative distortions. Since this article focuses on the allocative effects of Bitcoin minting, I deliberately avoid incorporating nominal rigidity and financial frictions, opting instead for a simple RBC model to analyse these issues.

Literature

Although research on CBDC is expanding rapidly, it remains in its early stages. Infante et al. (2022) provide an excellent survey of the existing literature on CBDC. A major concern regarding the intro-duction of CBDC is their potential disintermediation effect on the banking sector. Interest-bearing CBDC could intensify competition with banks for funding. Carapella and Flemming (2020) suggest that while CBDC may serve as an alternative to bank deposits, they also offer potential benefits, such as improved monetary policy transmission. Andolfatto (2021) uses an overlapping generations model to demon-strate that an interest-bearing CBDC could enhance competition in an otherwise imperfectly competitive banking sector. Keister and Sanches (2022) argue that bank disintermediation is inevitable if CBDC competes directly with bank deposits. The extent of this effect depends on whether CBDC provides additional efficiency in facili-tating transactions. A cash-like CBDC may have little to no direct impact on banks, whereas a deposit-like CBDC is more likely to serve as a substitute for traditional bank deposits. Despite the possibility of disintermediation, their findings suggest that CBDC could contribute to a more efficient exchange system.

In this article, I do not focus on the disintermediation effects of CBDCs on banks. Instead, my primary interest lies in exploring the potential substitution between CBDC and Bitcoin in response to macroeconomic shocks, along with the general equilibrium macroeconomic consequences. To investigate this, I employ a simple RBC model. There are few studies that incorporate CBDC within a dynamic sto-chastic general equilibrium (DSGE) framework. Minesso et al. (2022) analyse the implications of CBDC for monetary policy in an open economy using a DSGE model. Another branch of literature examines the role of CBDC in economies with a signif-icant informal sector. Oh and Zhang (2022) develop a DSGE model showing that while CBDC can reduce transaction costs, their benefits may be limited in cash-intensive informal economies. Agur et al. (2022) explore the factors that may hinder CBDC adoption when multiple forms of money coexist. Drawing on the Modigliani–Miller theorem, Brunnermeier and Niepelt (2019) identify conditions under which private and public money can be considered equivalent. Asimakopoulos et al. (2023) models cryptocurrencies in a DSGE setting, but they do not have CBDC in their model.

In the light of this growing literature, my article aims to examine the macroeconomic consequences of a positive innovation in the Bitcoin sector, as well as a negative TFP shock, in an environment where the CB has an additional policy instrument, the CBDC interest rate. The present article is both timely and instructive, particularly in the post-COVID era, as CBs are increasingly considering the appropriate implementation of CBDC. Their task is further complicated by the challenges posed by unregulated Bitcoin payment tech-nologies.

The Model

The model builds on a standard ‘money in the utility function model’ following Brock (1978). I introduce CBDC as an alternative means of exchange, enhancing the representative consumer’s ease of transaction, and thus, it is utility enhancing. The representative agent derives utility from consumption and real balance, which consist of both cash and CBDC. Specifically, the household receives utility from consumption (ct), real balances from the holding cash (mt) and CBDC (mtCBDC) both of which serve as a medium of exchange and as a store of value. The household has an access to a short-term bond market to smooth consumption. A nominal discount bond (bt) pays the interest rate itn which is a policy rate of the CB to target inflation. In addition, the household invests in physical capital (kt). At date t, a fraction ηt of capital stock is allocated to final goods production, and the remainder is used for bitcoin (mtp) mining. Unlike CBDC, bitcoins function only as a store of value.

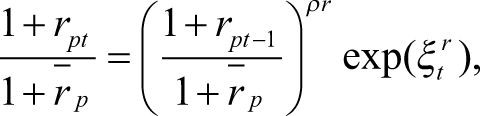

The net return on it (rtp ) is risky and follows a log-linear AR(1) process around the steady state (r̄p) as follows:

with 0 ρr 1 being the AR coefficient, and ξtr is an idiosyncratic shock to the bitcoin technology, which captures the risk of default due to the anonymity of transactions. The CB fixes the CBDC rate at iCBDC.

The optimization facing the representative agent who runs the operation of both production of final goods and bitcoins is as follows:

subject to

where remaining notations are as follows. ct is consumption, ξtd is an independent and identically distributed preference shock which we will call consumer sentiment hereafter or confidence shock with unit mean, kt is the capital stock, itk is the physical investment, At is the TFP shock, δk is the fractional rate of capital depreciation and trt is the net lump-sum transfer.

The right-hand side of the flow budget constraint (2) comprises income from final goods production (yt), real interest income from bond, private bitcoin and CBDC. Notably, all these sources of interest income except for private Bitcoin-are subject to an inflation tax. We assume that Bitcoin mining is immune to both inflation risk and exchange rate risk due to the inherently digital and private nature of its transactions. However, it remains exposed to default risk arising from the anonymity of transactions.

The CB sets the inflation target at the steady state Π- and responds to inflation with a one period lag based on the following Taylor rule:

where ρn is the interest rate smoothing coefficient, ϕπ is the inflation sensitivity coefficient and ξtCB is the idiosyncratic monetary policy shock.

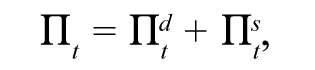

The gross rate of inflation, Π

t

, is characterized as

where

where Π- d is the steady-state demand inflation rate, 0 < ρπ < 1 is the AR coefficient, ξtd is a demand shock, ξtCB is a CB policy rate shock to calm inflation, and λd and λCB are positive inflation sensitivities with respect to these two shocks.

The supply-side component of inflation responds negatively to the TFP shock (At), with λa being a positive parameter reflecting the TFP sensitivity of inflation. In other words,

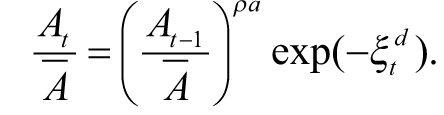

where At follows the process

In other words, a negative TFP shock ξta drives the inflation up. A negative TFP shock mirrors the supply chain bottlenecks during the COVID period. The steady-state inflation is Π- = Π- d + Π- s – λaĀ.

The government prints cash and mints CBDC tokens to meet the transaction demand of the household. The cost of minting CBDC tokens is financed by a lump-sum tax, while cash is given to the household as a lump-sum transfer. The real transfer net of taxes is trt. The government budget constraint is thus simply

Denoting uit as the partial derivative of u(.) with respect to its ith argument, the Euler equations for cash, CBDC, bitcoin and bond are given as follows:

The Euler Equations (10) and (11) have straightforward interpretations. Holding any of these medium of exchange means a utility loss from consumption sacrifice, which is compensated by the direct marginal utility of transaction convenience and the discounted utility benefits of the store of value return from such a medium of exchange. Since cash and CBDC have different transaction conveniences, people may demand both as mediums of exchange. The bond Euler Equation (12) is standard, which shows the marginal equivalence of investing a currency unit in bonds.

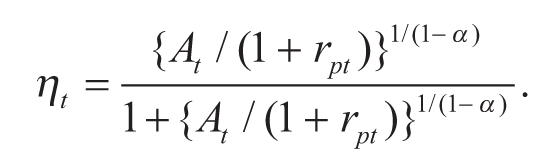

At date t, facing the predetermined capital stock kt – 1, and return to bitcoin rtp, the representative household solves a simple capital allocation problem of choosing ηt such that yt + mtp is maximized. It is straightforward to verify that the optimal ηt is given by

Evidently a higher At or a lower rpt warrants a higher allocation of capital to final goods production.

Once the capital allocation decision is made, the household decides how much to invest (itk ) in physical capital, which is an intertemporal decision problem. The Euler equation for physical investment is given by

Given that the market is complete, comparison of (12) with (14), one obtains a standard arbitrage condition that the bond return in each state must equal the corresponding physical investment return. In other words,

Equilibrium

The equilibrium is characterized by the following conditions:

The household’s Euler equations for cash balance, CBDC and bond holding, namely (10), (11) and (12) hold. The optimal capital allocation condition (13) holds. The bond market clears which means bt = 0. The government budget constraint (9) holds. By the Walras law, the goods market stays in equilibrium, which means

The CB adheres to the interest rate rule (6).

Stochastic Simulation

In this section, I report the short-run analysis and policy simulation of this model based on a stochastic simulation. We specialize to a log utility function: u (ct, mt, mtcbdc) = ξtdlnc

t

+ μmln

mt

+ μmdln mtcbdc, where µm and µmd are positive preference parameters representing household’s demand intensity of cash and CBDC. The parameter values are fixed as follows: β = 0.99, α = 0.3, δ = 0.025, ρα = 0.9, ρrp = 0.9, ρib = 0.9, µm = 0.1, µmd = 0.1, λd = 1, λCB = 1 and λα = 1. In the policy rule (6), the inflation sensitivity parameter

We first compute the recursive steady states of the model. All the structural equa-tions are then loglinearized around the steady-state values. The loglinearized system of equations are then written as a state-space form. Impulse responses and variance decompositions are computed with respect to all four structural shocks that are ξtd, ξta, ξtrp and ξtib . All impulse responses are normalized by the standard deviation of respective shocks. The standard errors of each of these are set at 0.01.

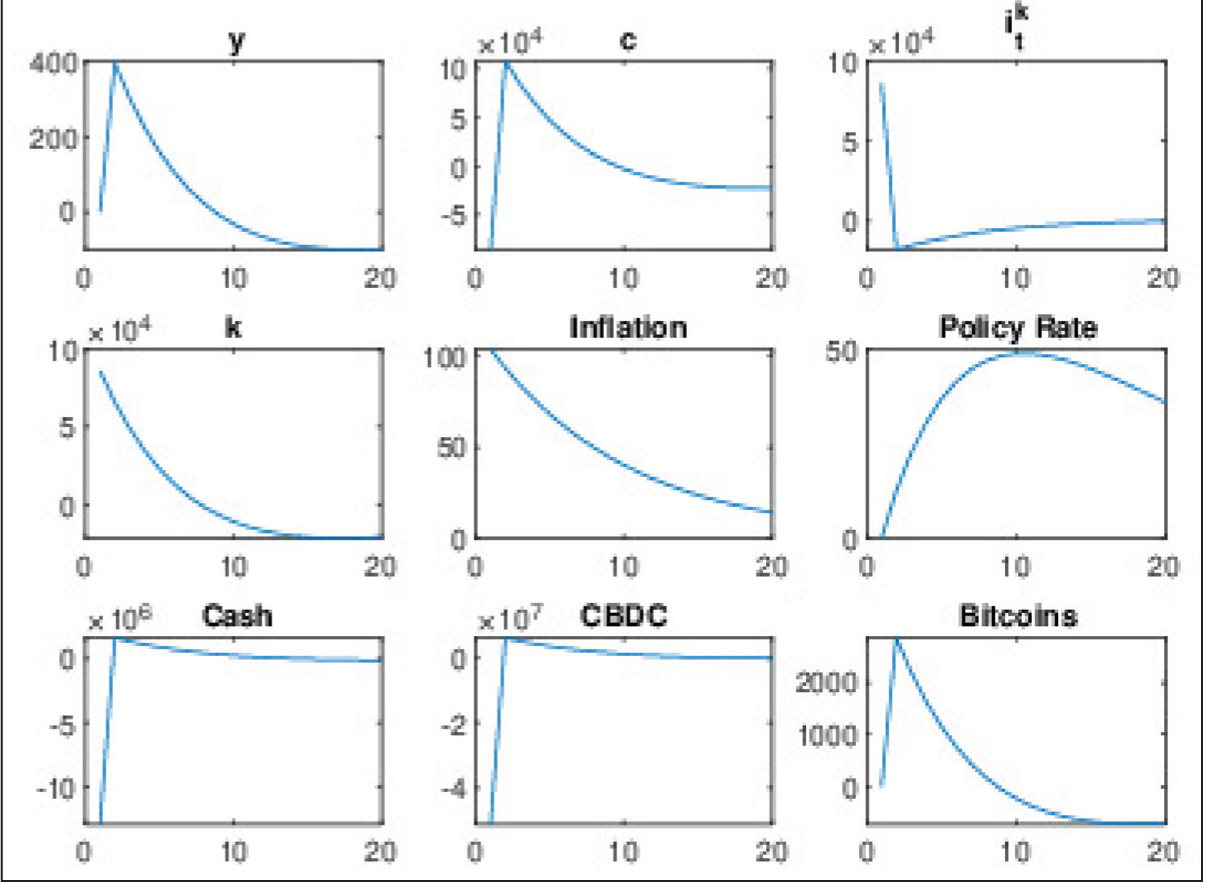

Figure 1 demonstrates the effect of a positive confidence shock on the aggregate economy. Starting from the steady state at date 0, such a shock at date 1 causes a sharp rise in inflation from the steady state. Consumption initially falls due to the inflation tax. Because of the inflation tax, household switches from cash and CBDC to capital accumulation. A positive Tobin-type effect is at work, which stimulates investment and capital stock, and thus the GDP rises. The CB responds to inflation by raising the policy rate. A greater capital stock also boosts bitcoin production, which is immune to the inflation tax. Overall, a positive demand inflation shock has a stimulative effect on the aggregate economy, and it makes households mint more bitcoins.

Response to a Positive Confidence Shock.

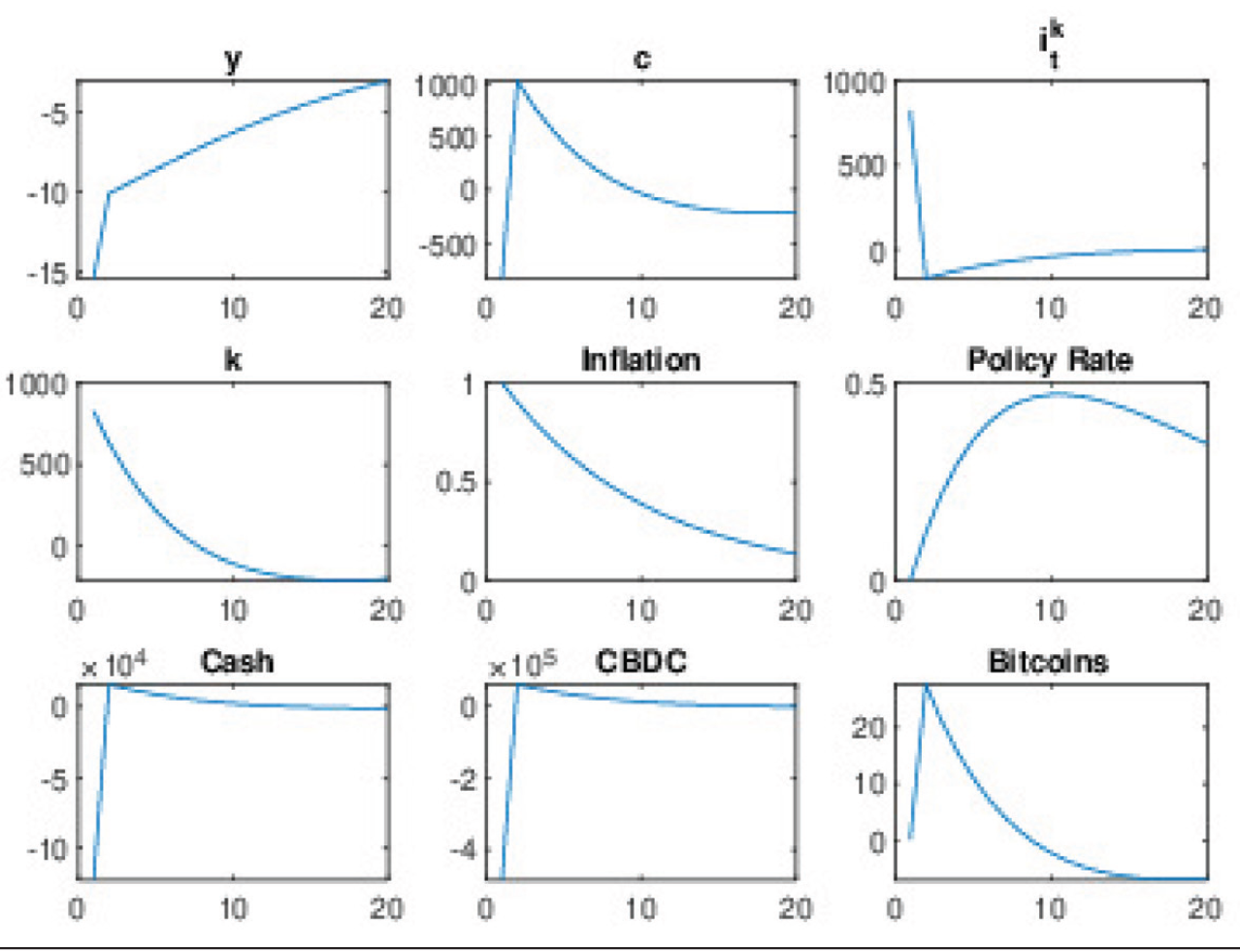

Figure 2 presents the impulse responses of relevant macroeconomic variables with respect to a negative TFP shock, which is indicative of an adverse supply chain shock. GDP declines on impact and the inflation rises. The resulting inflation tax depresses consumption. Since the relative return to bitcoin rises, households switch to bitcoins production which is more lucrative. The increase in bitcoin income results in a positive wealth effect that stimulates overall investment in physical capital. As a result, the GDP subsequently starts recovering. Since the CB aggressively responds to inflation, the policy rate rises

Response to a Negative TFP Shock.

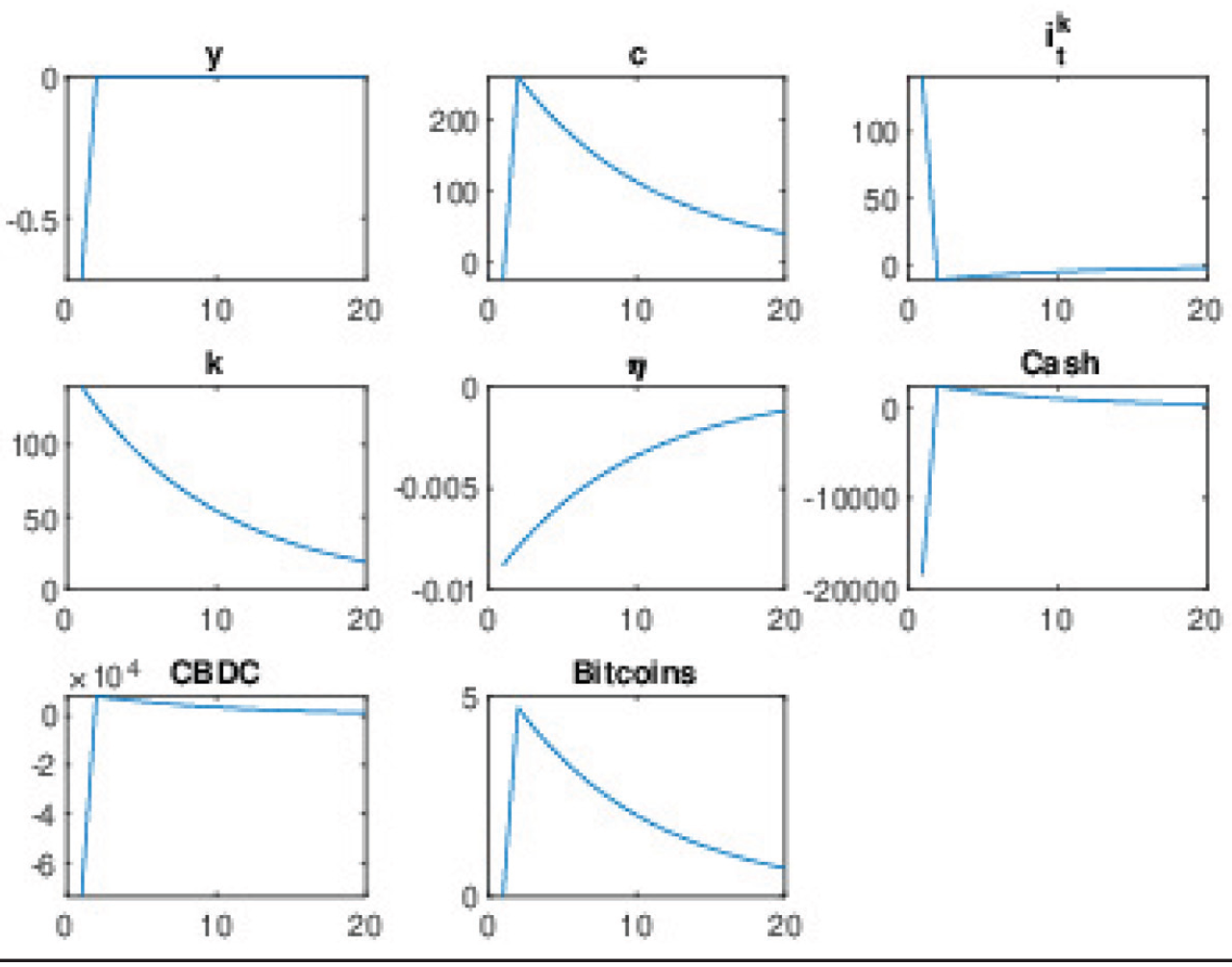

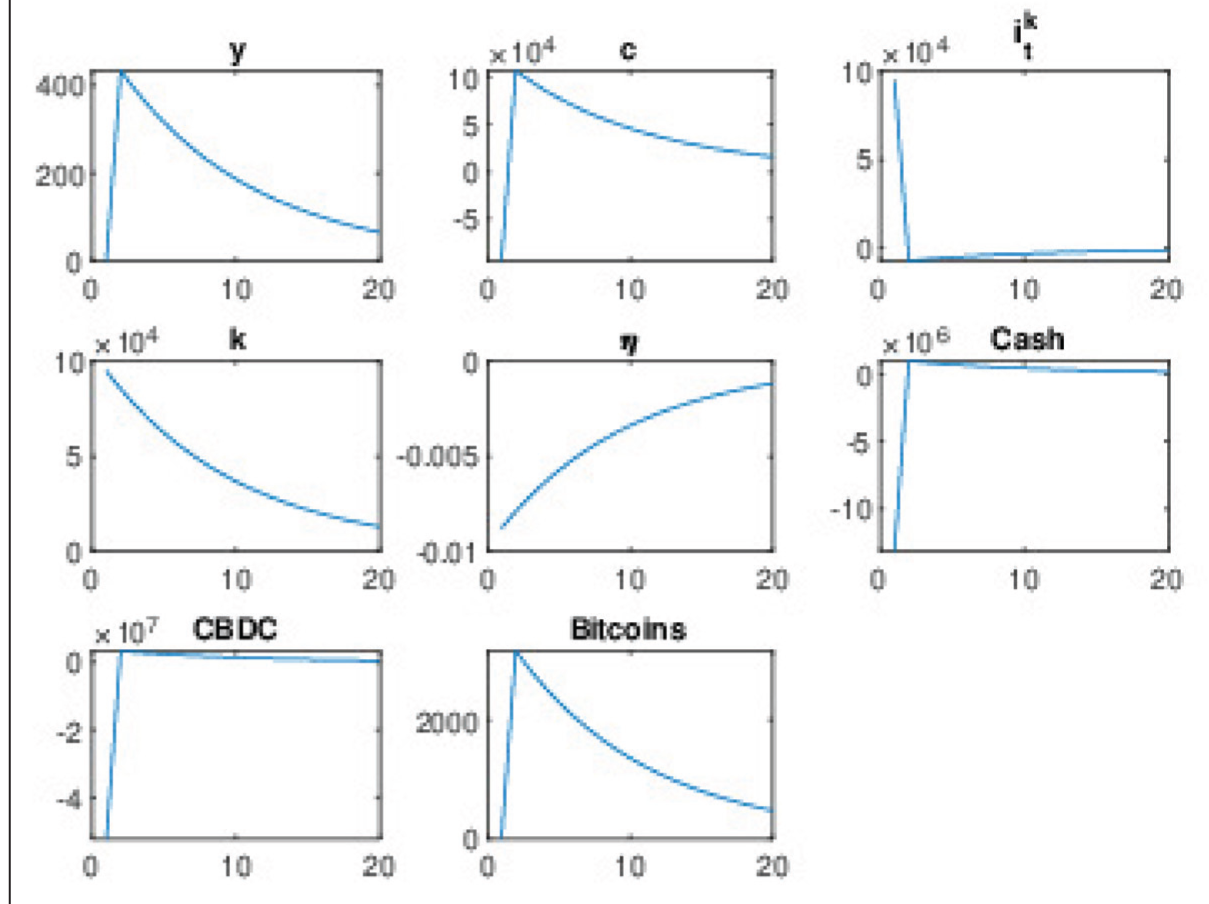

Figure 3 illustrates the effect of a positive shock (ξtr) to bitcoin production tech-nology on the aggregate economy. Not surprisingly, bitcoin minting increases, which raises income from bitcoins. The resulting positive wealth effect boosts consumption. Since capital is diverted from final goods production, GDP falls on impact, but the subsequent investment boom makes GDP recover. Cash and CBDC demands fall as household switches portfolio to bitcoins. The bottomline is that a boom in crypto technology has an initial recessionary effect on the economy.

Response to Bitcoin Innovation.

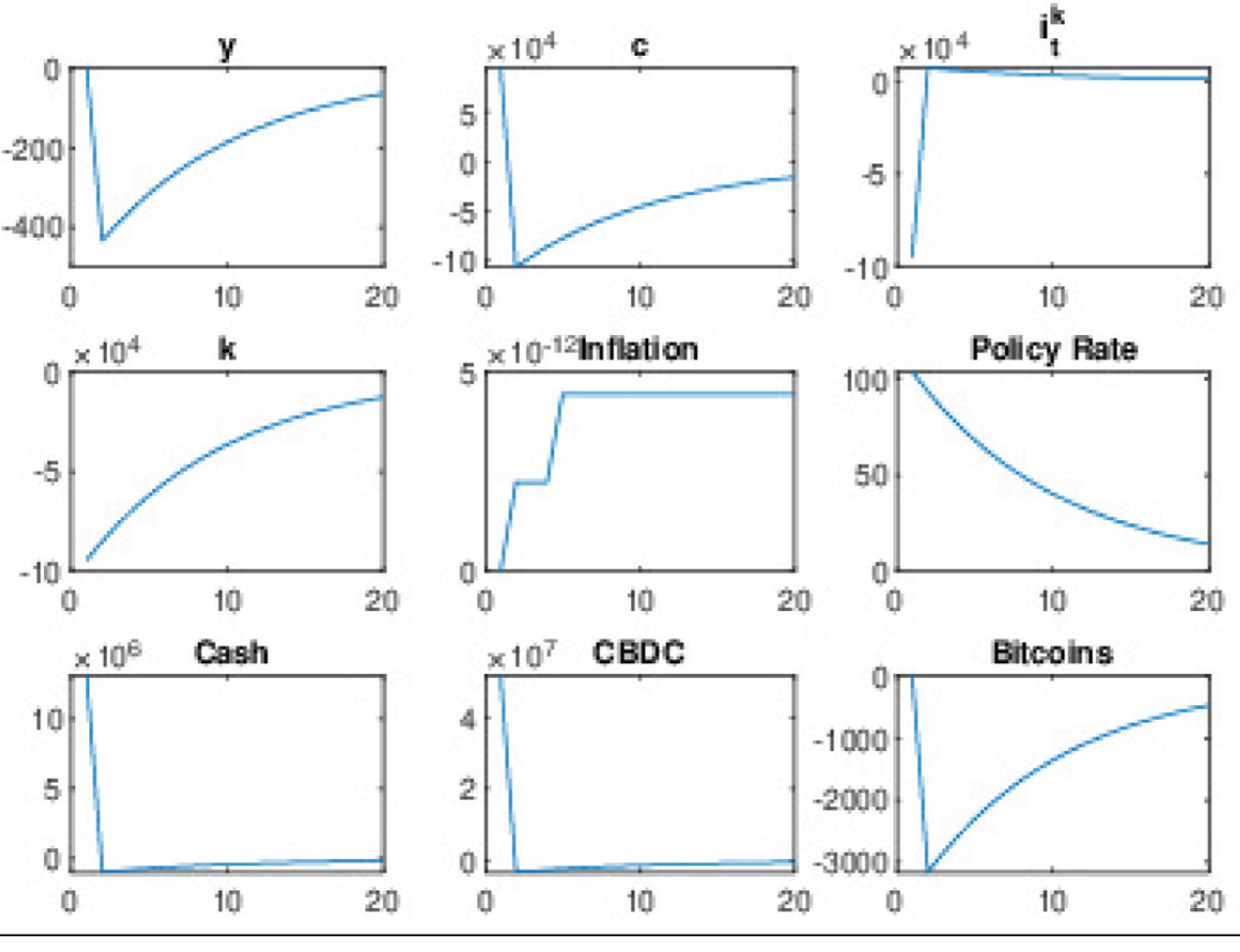

What can the CB do to mitigate the recessionary impact of a crypto boom? The CB can lower the policy rate simultaneously when a positive crypto boom hits the economy. Let the Taylor rule (6) be modified as

Figure 4 shows the effect of a positive bitcoin shock when the CB proactively responds by lowering the rate. The recession is reversed as seen by a lower policy rate. There is also an investment boom due to a lower policy rate based on the arbitrage condition (15). A momentary drop in consumption, cash and CBDC demand happens to accommodate the rise in investment.

Response to Bitcoin Innovation when CB Is Proactive.

Figure 5 demonstrates the impulse response analysis with respect to a rise on the policy rate shock. In response, the capital stock and investment fall on impact due to the arbitrage condition (15). As a result, GDP falls. There is near zero response of inflation to this policy rate shock because lagged inflation is targeted. Fall in the cap-ital stock lowers bitcoin production because the capital allocation (ηt) is invariant to the policy rate shock. Given the resource constraint, consumption, transaction and CBDC money demands initially rise to accommodate the fall in investment. Basi-cally, arise in the policy rate discourages bitcoin production. Thus, if the CB wishes to curtail bitcoin production, raising policy rate is an effective policy tool. 1

Response to Positive Policy Rate Shock.

Conclusion

This article explores the implications of Central Bank Digital Currencies (CBDCs) and private cryptocurrencies on macroeconomic stability using a simple real business cycle model. The analysis reveals that consumer confidence shocks lead agents to shift from fiat money and CBDCs to private cryptocurrencies, which, while insulated from inflation-ary pressures, carry default risks due to transaction anonymity. Additionally, positive technological shocks in the private cryptocurrency sector can trigger a reallocation of capital, reducing final goods production and lowering overall consumption.

The findings underscore the complex interplay between different forms of money and their macroeconomic consequences. The central bank’s policy rate emerges as a crucial tool for mitigating adverse effects, such as inflationary pressures and economic downturns caused by capital shifts towards cryptocurrency production. Simulation results suggest that a proactive monetary policy can counteract recessionary impacts associated with cryptocurrency booms.

This research contributes to the ongoing debate on digital currencies by pro-viding insights into their potential benefits and risks within the evolving financial landscape. While CBDCs offer a safer alternative to private digital currencies by reducing default risks, they do not fully address the broader economic instability posed by cryptocurrency innovations. Policymakers must carefully navigate these challenges, balancing financial innovation with macroeconomic stability through ap-propriate monetary interventions.

Future research can extend this study in several directions. One potential avenue is exploring the optimal monetary policy for issuing the right proportion of CBDC and cash. Another is explicitly incorporating government debt financing into the model to assess its implications for optimal monetary policy. Additionally, the model does not address the inequality dimension of the crypto boom, where only a handful of digitally literate individuals have access to bitcoin technology. This issue could be effectively examined in a framework with heterogeneous agents.

Footnotes

Acknowledgements

Without implicating, the author wishes to acknowledge Shesadri Banerjee for useful comments.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.