Abstract

This research study investigates the impact of cryptocurrency on economic growth in 10 countries across Asia during past period 2013–2020. For this purpose, the sample included a range of economies with the highest number of Bitcoin usages or transactions. For this purpose, the sample included a range of economies with the highest number of Bitcoin usages or transactions, according to recent international rankings. With specific empirical means on panel data modelling, we attempted to show that economic growth, was influenced negatively by the cryptocurrency ‘Bitcoin’, and we concluded that this instrument leads to an increase in the inflation rate in a country according to the quantity theory of money and leads to a disorder in the monetary policy of a country. Our framework shows that the economic growth proxy was substantially influenced positively by economic indicators such as technology, investment and education but negatively by the high rate of participation, which caused an increase in unemployment. Our empirical results offer insights and insist on the importance of the intervention of the authorities to oversee and control the use of the cryptocurrency Bitcoin to avoid its negative effects and implement a strategy that overcomes these effects from a macroeconomic perspective.

Introduction

The cryptocurrency world is a bustling ecosystem filled with unique ideas, exciting opportunities and the potential for considerable financial gains. However, it is vital to understand the connection between economic growth and the financial stability of cryptocurrencies, such as Bitcoin, in order to take advantage of this environment and build a profitable portfolio.

Bitcoin was introduced to the public via a white paper titled ‘Bitcoin: A peer-to-peer electronic cash system’. In this document, Satoshi Nakamoto describes a peer-to-peer system for making direct transactions without the intervention of financial intermediaries. Digital currencies, such as Bitcoin, have come a long way since their inception in 2009. Currently, cryptocurrencies are used by millions of people for trade and investment, whereas they were previously used to facilitate drug deals and other illegal operations. It is challenging to envision today’s economy without considering the impact that cryptocurrencies, such as Bitcoin, have had on our lives. Indeed, the influence has been so significant that the economy and cryptocurrencies have become hot topics of discussion among economists. While Bitcoin has garnered substantial interest not only from investors but also from academics and policymakers, existing theoretical and empirical attempts have not reached a consensus regarding its influence. Recently, the COVID-19 pandemic has once again raised important questions regarding the nature of Bitcoin (Choi & Shin, 2021).

Despite limited literature on Bitcoin as a cryptocurrency, people’s understanding of its economic effects is relatively divided. Consequently, a pivotal question emerges: Does a cryptocurrency like ‘Bitcoin’ engender economic benefits? No final conclusion has been reached so far. Exploring the mechanisms underlying economic effects and developing a robust theoretical framework require further and deeper exploration (Yue et al., 2021). This study aims to investigate whether cryptocurrencies, in general, and Bitcoin, in particular, have a noticeable impact on the economy or mainly function as speculative instruments. We focus on understanding the real impact of Bitcoin as a technological innovation within the financial sector on the country’s economic growth and determining whether this impact is negative or positive.

Besides, we will explore the following research questions from a macroeconomic perspective:

Does Bitcoin serve as a hedge against inflation pressure caused by government stimulus measures? Does Bitcoin function as a safe haven for investors? Can Bitcoin contribute to an increase in the inflation rate due to the significant rise in the money supply resulting from the increased demand for money generated by Bitcoin’s successful transactions?

Interestingly, recent studies have partly answered these questions (Conlon & McGee, 2020; Dutta et al., 2020; Dwita Mariana et al., 2020; Vroman, 2014). However, they did not approach this matter as a macroeconomic phenomenon.

Therefore, to analyse the aforementioned issue, this article will examine the Bitcoin cryptocurrency in 10 Asian countries. These countries will be selected based on the ranking of the highest trading volumes of Bitcoin as well as the availability of data from 2013 through 2020.

The Literature Review

Finextra’s latest research on cryptocurrency has shown that it can significantly impact social and economic growth, especially in developing countries. According to Finextra, the positive economic impacts of cryptocurrency include the expansion and growth of businesses for entrepreneurs, low transaction fees—a significant advantage for unbanked adults—job creation through mining (Okeke et al., 2022) and the promotion of authenticity and transparency between parties. These advantages offer developing countries an opportunity to conduct transactions both locally and abroad and to further engage in international trade and investment.

In addition, other research has revealed additional strengths associated with the use of cryptocurrencies. Cryptocurrency bridges the gaps left by financial institutions by leveraging peer-to-peer technology to address the issue of a rising number of unbanked adults, particularly in developing nations such as those in Africa (Agu, 2020). An earlier study supporting this idea was conducted by McKenzie (2019), who wrote, ‘reportedly, two-thirds of Sub-Saharan Africans do not have a bank account’ (p. 1).

Other studies, such as those by Yue et al. (2021), have classified the economic effects of cryptocurrency into two categories. The initial effect is mainly characterized as the technological aspect of cryptocurrency. The second category encompasses the direct impact of crypto on the economy. Regarding the ‘technology effect’, it has been identified as having ‘innovative technological features with a low transaction fee’. Concerning the direct economic effects, Yue et al. (2021) deduced three major impacts: (a) the impact of speculative transactions on cryptocurrencies varies across research, but cryptocurrency price volatility will affect macroeconomic policy to some degree; (b) over different study periods, the hedging and safe haven features of cryptocurrencies change; and (c) external factors, such as the COVID-19 pandemic and geopolitical threats, may cause price changes and boost the effectiveness of cryptocurrency hedging.

However, it is indisputable that cryptocurrencies have several weaknesses, as highlighted by many authors. In their studies, these authors recommend giving more attention to these weaknesses due to their negative impact on the economy. According to Bearman (2015), some of these weaknesses include the fact that cryptocurrencies can be used for money laundering due to the lack of government involvement. Consequently, other concerns subsequently raised about cryptocurrencies are related to security risks, such as hacks targeting individuals who own large amounts of cryptocurrency. Furthermore, Agu (2020) indicated in her study another major fear related to investors’ primary concern regarding the security of their assets. One weakness of cryptocurrencies is that they might be traded like commodities due to their fluctuations. Investors become fearful due to this fluctuation, especially since most countries do not have laws protecting cryptocurrencies.

In 2018, the number of cryptocurrencies circulating worldwide exceeded 1,800 types (Kethineni & Cao, 2019). Two years later, on 13 August 2020, ‘CoinmarketCap.com’ announced that there were over 6,442 cryptocurrencies in circulation globally. The qualities of each cryptocurrency impact its value, stability and interdependence. Economic uncertainty dynamics and market volatility, along with investor expectations, are factors that may lead to substantial instabilities. Bitcoin, as a currency corresponding to all the foregoing analysis, will be the focal point of our study.

Bitcoin, a virtual currency that facilitates peer-to-peer transactions, was inspired by Satoshi Nakamoto’s blockchain vision (Nakamoto, 2008). Launched in 2008 by a group of anonymous developers, Bitcoin led to the creation of other digital currencies known as altcoins. Bitcoin became a demonstration of a feasible hypothesis when cryptocurrency was explored in 1998. The number of Bitcoin users has massively increased during the last couple of years (Agu, 2020). According to Mazikana (2018), ‘since the start of 2017, Bitcoin has increased by more than 1500 percent’ (p. 21). For instance, while Bitcoin was worth $7,000 in April 2018, it reached around $18.353 in November 2020. It is evident that Bitcoins have skyrocketed in value since their inception. Bitcoin transactions are quick and safe (Kelly, 2014).

From a macroeconomic perspective, there are controversies not only regarding the true nature of Bitcoin but also about its functions. Thus, we observe that some economists regard Bitcoin as a medium of exchange, while others perceive it as a speculative investment, a hedge against inflation or even a booster of it (Badea & Mungiu-Pupăzan, 2021).

If we assume Bitcoin to be a currency, we must first consider the commonly acknowledged roles of money. The history of economic theory reveals a lack of agreement among economists regarding the number of tasks money fulfils over time. For instance, in his 1875 book Money and the Mechanism of Exchange, Jevons classifies the functions of money into four principal roles: an exchange medium, a common measure of value, a standard of value, and finally, a store of value (Jevons, 1975). In contrast, Graham (1940) classifies money functions differently, perceiving only two primary roles: ‘the unit of accounting’ and ‘the bearer of options’, asserting that all other functions derive from these two. However, economic theories have adapted to the evolution of modern times, leading to an upgrade of money’s functions. For example, Kubát (2015) introduced informational and investment functions alongside the classical roles. Given these developments, we align with Kubát’s findings, asserting that Bitcoin does not fit into the definition of money and, therefore, cannot be considered an official currency.

Various economists, including Bal (2015) and Vlasov (2017), suggest that Bitcoin is a speculative investment. They perceive Bitcoin as the next step in the evolution of money, considering it a digital currency detached from the physical world. However, these perspectives on Bitcoin’s function in the modern economy lack widespread support among many other economists. They disagree with the notion that Bitcoin ‘has been turned into an element of speculation rather than functioning as money’ (Cheah & Fry, 2015). Another type of investment identified in studies on Bitcoin’s functions and other economic relationships is mentioned by Demir et al. (2018). Their research explores the correlation between Bitcoin and the uncertainty index of economic policy, highlighting its potential use as a tool for reducing the risk of uncertainty.

Several authors disagree with the preceding deduction, among them Glaser et al. (2020), who argue that speculative bubbles and the poor intrinsic value of cryptocurrencies, such as Bitcoin, create uncertainty and undermine price stability. They draw attention to the role of the media in explaining their findings. Regarding price instability, some authors highlight the major reasons behind it. They state that the inability of a central bank to oversee the supply of Bitcoin is a significant disadvantage that deprives the cryptocurrency of stability (Ammous, 2018). Therefore, they align with Selgin (2015), who asserts that the volatility of the Bitcoin exchange poses a challenge, along with several other issues related to Bitcoin. These include the deficiency of liquidity and the operation of an unregulated market with extremely high-security risks due to two major factors: the absence of market regulation and government oversight.

Accordingly, the creation, growth, and development of cryptocurrencies, such as Bitcoin, and their core technologies, like Blockchain, have made it possible to establish a monetary alternative, as highlighted by authors like Marthinsen and Gordon (2022). They suggest that this solution can aid any country seeking to overcome hyperinflation and transition to a more stable monetary environment. The feasibility of such a transition is evident.

Nevertheless, in the aftermath of the COVID-19 crisis, several nations have implemented what some economists describe as aggressive or hostile fiscal and monetary regulatory policies to support their economies. Additionally, a major issue that emerged during the same period was the supply shortages in critical areas. These circumstances have contributed to the rise of ‘heightened inflation expectations’, as noted by Conlon et al. (2021). These expectations have been worsened by stagnating and declining wages due to significant pandemic-driven changes in worldwide working environments. The uncertainty surrounding the increasing supply of money resulting from unconventional monetary policy operations has also led to highly volatile expectations (Conlon et al., 2021).

Based on the aforementioned assessments, several authors have suggested that investors should strive for what they refer to as ‘safe haven assets’ to diversify and safeguard their portfolios against the anticipated effects of inflation on purchasing power. Consequently, this assertion led Blau et al. (2021) to argue that the increase in expected inflation could be connected to the appreciation of cryptocurrency prices, such as the ‘Bitcoin price’. Urquhart (2018) provided additional critical information, stating that cryptocurrencies, specifically Bitcoin in our case, are subject to the same economic factors as any other asset. They are influenced by the law of supply and demand. Thus, cryptocurrencies, like ‘Bitcoin’, derive price-relevant information from various sources that may be less transparent, many of which are unrelated to predicted inflation. This diversity in information sources provides diversification advantages when aggregate demand surpasses aggregate supply. Therefore, the author supports the idea that inflation and cryptocurrencies (Bitcoin, in our case) are interconnected, emphasizing the need to comprehend and analyse this relationship and its impacts. The question that arises is whether this connection serves as a hedge or a booster for inflation.

Given the contradictory theoretical connections between the Bitcoin cryptocurrency and inflation, we rely on empirical findings to address our research question. Subsequently, we aim to clarify the nature of the relationship between the two factors by identifying any potential ‘hedging’. An empirical framework that validates the aforementioned theoretical assertions can be found in the study conducted by Narayan et al. (2019). In their empirical findings, they suggest that most of the fluctuations in Bitcoin are directly linked to the inflation rate in Indonesia. Consistent with the previous findings, the studies conducted by Blau et al. (2021) represent some of the latest works supporting the positive relationship between Bitcoin and inflation. We believe that the conclusions drawn from these studies carry critical implications for both investors and policymakers. First, their findings suggest that Bitcoin can serve as a ‘hedge against expected inflation’. This result is so crucial for investors seeking protection from inflation risks. Second, the framework of their results indicates that any change in the value of Bitcoin results in a simultaneous change in the expected inflation value. Accordingly, this deduction suggests that Bitcoin operates similarly to a commodity that can be used as an instrument of exchange. This observation holds significance for governments, policymakers, and businesses considering the adoption of a digital currency. For the same purpose, Conlon et al. (2021) relied on empirical evidence in their research to identify this hedging capacity over the period 2010–2021. They not only confirmed the result conducted by Blau et al. (2021) but also found that any relationships are mostly associated with a specific and single point in time. Also, at the onset of the COVID-19 epidemic, the authors confirmed the presence of a noticeable positive correlation, which coincided with a rapid and coordinated decrease in both forward inflation forecasts and the price of cryptocurrencies. However, the authors made other important observations. Apart from the sudden return of forward inflation expectations to pre-crisis levels following the onset of COVID-19, they did not find evidence of any beneficial linkages between inflation and either Bitcoin or Ethereum during periods of heightened forward inflation expectations. These considerations and results have raised serious doubts about cryptocurrencies, such as ‘Bitcoin’, and their ability to hedge against projected inflation in the short term or overall. The results were initially discovered by Conlon and McGee (2020); they established a connection between Bitcoin and the outcome of forward inflation expectations. However, they found that the hedging ability is extremely limited outside the period of crisis.

However, it is evident that forward inflation expectations fell rapidly, not due to the influence of Bitcoin cryptocurrency but because they were affected by a shift in attitude caused by the constraints of the lockdown. Instead, these initial announcements about unconventional monetary and fiscal policies to support the economy led to a subsequent sharp concurrent recovery in both cryptocurrencies and forward inflation expectations. This recovery prompts us to reconsider the perceived positive relationship and impact between these factors and delve deeper into the matter.

These assertions are supported by several renowned economists in their research works, such as Krugman (2013). Krugman contends that Bitcoin is merely a speculative investment that bears no resemblance to a traditional monetary instrument, in contrast to the hedging arguments and definition implied by Reilly et al. (1970) and Cagan (1974). Furthermore, sharing the argument formulated by Krugman (2013), Baur et al. (2018) presented empirical evidence that Bitcoin is not correlated to any traditional assets, such as stocks, bonds or commodities, indicating that it is generally used as a speculative investment. Likewise, Peetz and Mall (2017) claimed that they did not agree that Bitcoin is a transaction currency for several reasons, such as its difficulties in valuation, the lack of intersecting worth and the restricted transaction capacity.

The economic nature of Bitcoin remains a subject of contention, necessitating further clarification within scholarly and legal communities (Badea & Mungiu-Pupăzan, 2021). Some authors, such as Quah (2003), have suggested that an alternative perspective is needed to comprehend Bitcoin’s behaviour and its impact on the economy. For instance, due to its monetary worth, it might be termed a ‘digital asset’, with its processing power determining its rarity and market value (Quah, 2003). However, given the conflicting opinions regarding Bitcoin as a potential inflation hedge, a structural analysis of both Bitcoin and expected inflation seems warranted (Blau et al., 2021). Based on these conclusions, we can assert that several interdisciplinary fields are interested in the economic phenomenon caused by Bitcoin. Some analysts view it as a developed technology, while prior research in economic fields has focused more on its economic outcomes. Nevertheless, research on the economic effects of cryptocurrencies remains insufficient and requires deeper analysis.

Research Method, Data and Model

Research Method and Hypothesis Conceptualization

To address our research question, ‘What is the influence of using cryptocurrency on the economic growth of countries?’, we have formulated the following hypotheses: The null and alternative hypotheses aim to help us investigate whether Bitcoin affects the economic growth of the 10 Asian countries selected for our study. In other words, is there a significant relationship between the two variables? This constitutes our first step. In the second step, we will proceed to understand the effect of accepting the alternative hypothesis. If Hypothesis 1.1 is true, we will support economists who assert that this instrument contributes to increasing inflation by raising the demand for money in the economy. This, in turn, leads to an increase in the money supply and, consequently, the risk of printing money to satisfy the demand, ultimately resulting in hyperinflation. However, if Hypothesis 1.2 proves to be true, we will support the literature’s claim that cryptocurrencies hedge against inflation pressure and that Bitcoin can serve as a safe haven for investors. This led us, in our study, to conduct a panel data analysis using a tool that can assist in deducing and explaining the relationships in statistical panel regression.

Data

The data used for this research comprises a panel covering the period 2013–2020. The Asian countries included in our study, which have adopted Bitcoin, are Japan, China, India, Singapore, Indonesia, Hong Kong, South Korea, the Philippines, Thailand and Turkey. We selected these countries because they have the highest number of Bitcoin users, despite some governments, like China, starting to ban its use.

To conduct the research, we collected the GDP growth rate (GDP_Growth) of 10 countries and data on the average Bitcoin transaction volume. For the Bitcoin variable, we considered the average annual transaction volume in these 10 Asian countries, taking into account their use of Bitcoin since 2013. These data are sourced from the trading volume of Bitcoin by country, available on ‘Cryptocompare’ and ‘Coin.dance’, two websites providing Bitcoin transaction volume data. The selection of these 10 countries was based on rank, such as in 2017, when South Korea became one of the countries with the largest Bitcoin holders. In this case, we can observe the actual transaction value in USD price of Bitcoin (‘BTC’) at a yearly average:

Since the main priority in this research is to determine whether the cryptocurrency ‘Bitcoin’ could influence economic growth, a proper research process cannot be conducted using econometric data if the only variable is a Bitcoin regression towards GDP. As indicated in the literature review, this approach is likely to introduce bias into the results.

Therefore, to maintain consistency with previous research, we will use Solow’s (1956) classical economic theory, which posits that capital and labour contribute to economic growth. In the 1970s, social capital was considered a key contributor to achieving economic growth (Helliwell, 1996; Akçomak & ter Weel, 2009). Whiteley (2000) examined 34 countries over the period spanning 1970–1992, and his findings suggested a strong relationship between social capital and economic growth. Benhabib and Spiegel (1994) also argued that human capital influences economic growth. Consequently, we added some control variables such as labour (L), capital (K), human capital (H) and technology (A). Additionally, we will use the Dummy variable, which in our case is the country ID ‘code’, to adjust our model and absorb some errors. According to Table 1, the data for these variables were retrieved from various sources, such as the World Bank and the IMF databases, which we analysed using the statistical software Stata 17.

Variables, Their Source and Definition.

Data Analyses

This section will report the various analyses conducted on the variables of interest to examine our sample and derive meaningful results.

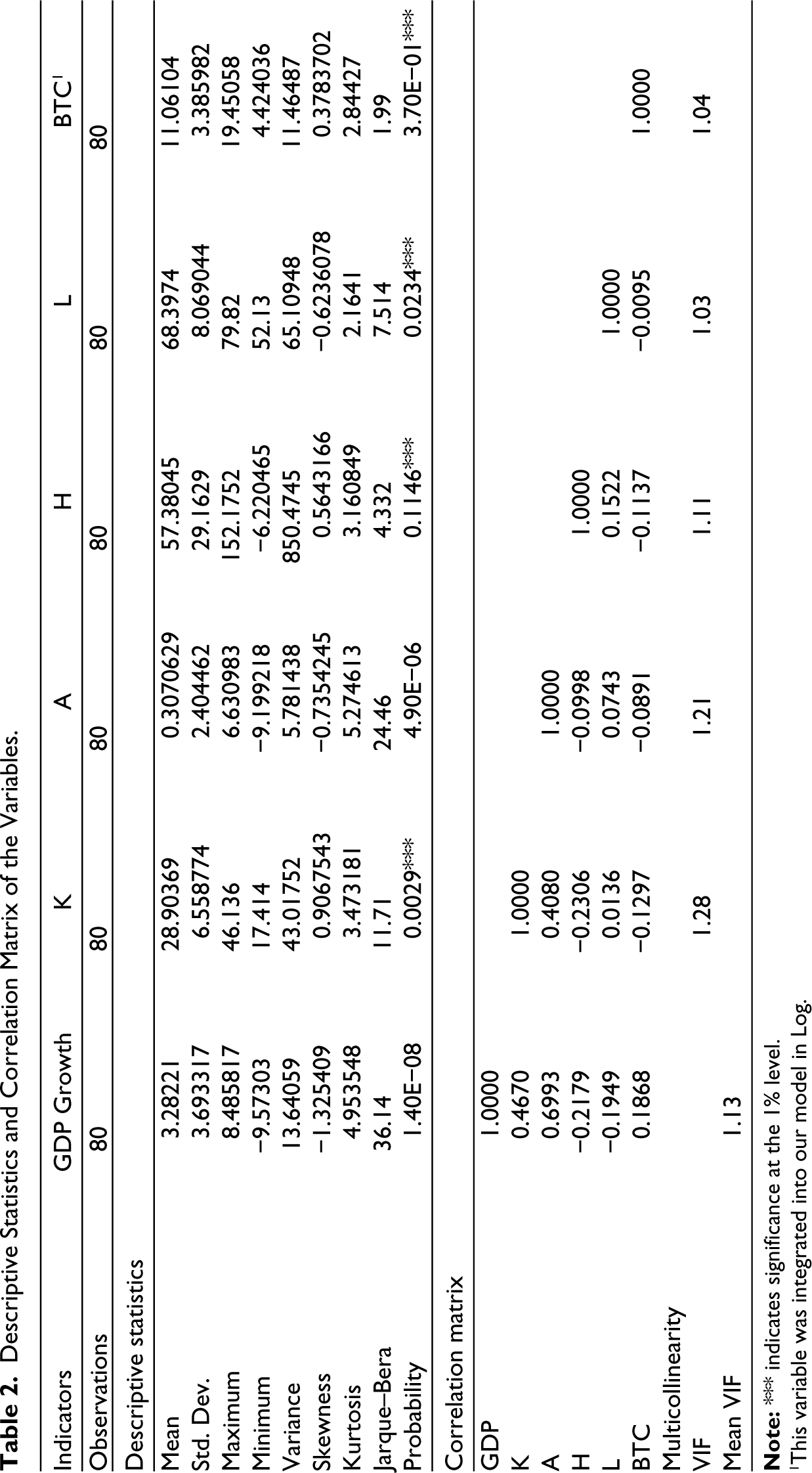

The first round of analyses we conducted included descriptive statistics. Table 2 presents the descriptive statistics for all variables related to GDP_Growth, capital, labour, human capital, technology and Bitcoin. In the second round of analyses, our focus was on testing the correlations between the predictors to identify any correlation issues using Pearson correlation coefficients. The results are presented in Table 2. The third round of analyses aims to detect multicollinearity in a regression analysis using the variance inflation factor (VIF) test. This test estimates the extent to which the variance of a regression coefficient is inflated due to multicollinearity in the model.

Thus, we present the average values of the variables considered in the study: 328.22% for GDP, 289.03% for capital, 30.70% for technology (total factor productivity), 573.80% for human capital, 680.97% for labour (participation rate) and lastly, 110.61% for Bitcoin.

The standard deviation values provide a more accurate and detailed estimate of dispersion, indicating the fluctuation of the time series. In this context, the variable ‘human capital’ exhibited the highest volatility, followed by ‘labour’ and ‘capital’, while ‘technology’ had the smallest volatility.

In terms of skewness, the positive skewness values for capital, human capital and Bitcoin indicated a rightward skew. However, the others exhibited a leftward skewness due to their negative values—specifically, GDP, technology and the labour force. The kurtosis values of our sample were both less than seven and higher than minus seven (Kline, 2013; Murtala Aminu & Noor Mohd Shariff, 2015). Using the Jarque–Bera test, we assessed the normal distribution of the data. The test results revealed that the GDP and technology proxy deviated from normal distribution. However, the remaining variables adhered to the null hypothesis of the normality test at a 1% significance level (Batrancea et al., 2021).

As shown in Table 2, nearly all recorded correlations are at low to moderate levels. Therefore, we concluded that these correlations would not pose issues for the econometric estimations and their conclusions. Additionally, the mean VIF is close to 1, indicating a low risk of multicollinearity. Consequently, we concluded that multicollinearity would not be problematic for the econometric estimations and their derived conclusions.

Descriptive Statistics and Correlation Matrix of the Variables.

1 This variable was integrated into our model in Log.

Model Modulization, Results and Its Validation Tests

Econometric Model and Model Choice

The fourth round of analyses focuses, on the one hand, on the post-estimation test. and, on the other, on the results of the econometric estimations. For these estimations, we specified the following econometric models:

where

• α0 indicates the intercept

• αi indicates individual effect = i. code

• αt indicates temporally effect: i. year

• β1, β2, β3, β4 and β5 indicate the coefficients of the predictors

• EG indicates the dependent variable• K, A, H, L, BTC indicate independent variables

• ‘i. code’ indicates the dummy variable

• i indicates the country

• t indicates the period analysed

• εit indicates the error term

The second equation is referred to as the ‘main module’, in which we will attempt to observe the simultaneous effect of all independent variables on economic growth. The remaining equations—3rd, 4th, and 5th—are called ‘nested modules’—1st, 2nd, and 3rd, respectively. They aim to isolate the impact of independent variables or groups of variables to confirm our deductions.

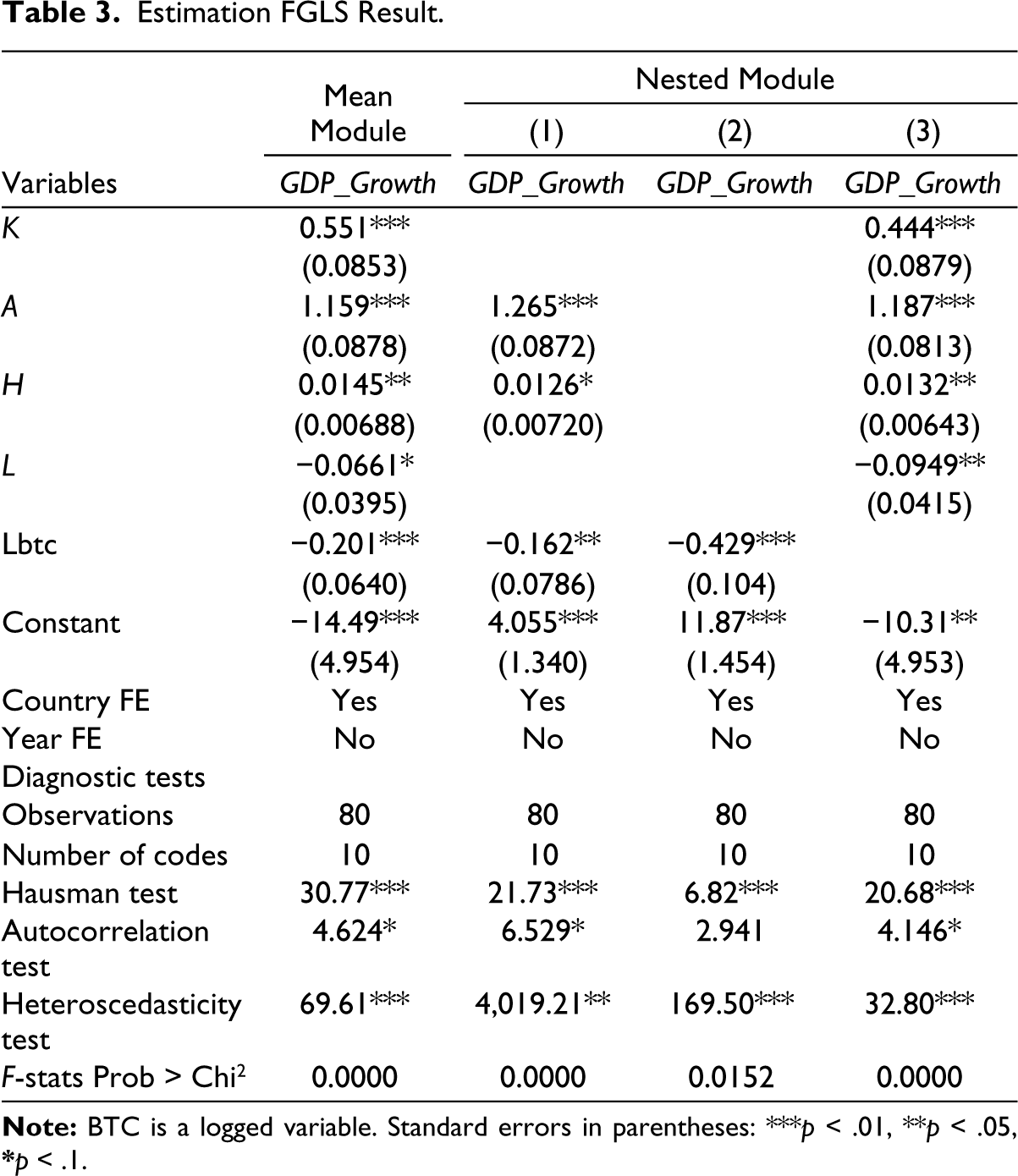

Thus, at this stage of the analysis, as mentioned by Baltagi (2021), any empirical analysis should commence with the decision of estimating results using either a panel regression or a simple regression. To make this decision, one should conduct a specific test that supports the chosen approach. Several tests are available to investigate the presence of specific effects in a model of the panel. We opted for Fisher’s test, which involves choosing between a pooled model and a specific effects model. The test is automatically conducted after estimating the fixed-effect model using Stata 17. The principle of the test is as follows: the null hypothesis suggests that the test results lean towards using the pooled model. According to the decision rule, if the p value associated with the test statistic is higher than α = (1%, 5% and 10%), then the null hypothesis cannot be rejected, indicating a homogeneous panel. Our results, presented in Table 3, using Stata 17, suggest rejecting the null hypothesis for all estimations—main or nested modules. The p values of the F-statistic are less than 1.5% and 10%; hence, the OLS estimator is deemed unfit and inconsistent.

Estimation FGLS Result.

Estimation Results and Diagnostic Tests

Before delving into the analysis of the empirical results, it is imperative to determine the appropriate panel regression based on the Hausman test. Subsequently, it is advisable—often mandatory in some cases—to conduct additional post-estimation tests, such as tests for heteroscedasticity and autocorrelation. This step is crucial for verifying the robustness of the model and, if necessary, resolving any issues to attain more efficient results.

As mentioned earlier, our initial step involves selecting between the fixed-effect model and the random-effect model, determined through the Hausman test. The null hypothesis in this case posits no significant differences between the estimates of the fixed-effect model and the random-effect model. If the null hypothesis is rejected, indicating significant differences, we opt for the fixed-effect model. The output of Hausman’s test is presented in Table 3. The p value, as observed, is below 1%, 5% and 10%. Therefore, rejecting the null hypothesis, we conclude that the fixed-effect model is more suitable for our study across all specifications.

Now, let us proceed to robustness checking, starting with Heteroscedasticity. This test aims to determine whether the variance in the variable is consistent within a regression model. If the variance is uniform, there is no heteroscedasticity problem; in other words, the data item is homoscedastic, and we, therefore, accept the null hypothesis. To examine our model, we employed the Wald test for groupwise heteroscedasticity in a fixed-effect regression model (Greene, 1999, p. 598). The results in Table 3 indicate that across all specifications, including both mean and nested modules, the probability value is less than 1%, 5% and 10%. This implies that we reject the null hypothesis if the data item conflicts with the issue of heteroscedasticity in all specifications.

The second post-estimation test is the autocorrelation test, which is necessary to ensure that the model is free from errors that could bias the results. Autocorrelation arises when the residuals lack independence from one observation to another, often due to errors in certain individuals persisting into the next period. The Wooldridge test can be employed to detect autocorrelation in panel data. The null hypothesis of this test posits the absence of first-order autocorrelation, indicating an absence of the autocorrelation issue. Table 3 shows that, across all specifications, whether mean or nested modules, we accept the null hypothesis as the p value is higher than 5% and 10%. This implies that our models—the main model and 2 Nested models (1st and 3rd)—are in conflict with the autocorrelation issue, except for the 2nd nested module, which suggests the acceptance of the null hypothesis.

Finally, after conducting all the robustness tests on the data, which indicate the absence of multicollinearity and correlation, we still encounter issues related to autocorrelation and heteroscedasticity. To address the latter problem and attain the least biased results, we will employ the feasible generalized least squares estimation for the fixed-effect model, well-known as ‘Xtgls’, 1 with consideration for heteroscedasticity and autocorrelation. Additionally, we introduced a dummy variable, ‘i. code’, into our estimation to further refine the model and mitigate potential errors.

Accordingly, it is advisable to confirm that all specifications provide a better fit to the data than a model that contains no independent variables. Therefore, it is imperative to assess how well the F-test of overall significance aligns with the data. According to the estimation results in Table 3, the p values of F-stats are <1%, 5% and 10%. This implies that the null hypothesis, which suggests that the independent variables simultaneously explain GDP perfectly, is acceptable in all specifications. Now, we can proceed to analyse the significance and impact of each variable on GDP growth.

Thus, building on the analysis above, we have now arrived at the final step where we will analyse and discuss our ultimate estimation results. These results are summarized in Table 3.

Referring to Table 3, the result of the ‘mean module’ estimation yields a p value

2

that is less than α = 1%, 5% or 10%. This finding indicates that:

Bitcoin (BTC) significantly influences GDP_Growth; as each unit of Bitcoin changes, GDP_Growth will undergo a significant alteration of 0.201. The relationship is negative. Labour (L) significantly affects GDP_Growth; as each unit of labour changes, GDP_Growth will either decrease or increase by 0.0661. The relationship is negative. Capital (K) significantly affects GDP_Growth; as each unit of Bitcoin changes, GDP_Growth will undergo a significant alteration of 0.551. The relationship is positive. Technology (A) significantly affects GDP_Growth; as each unit of Bitcoin changes, GDP_Growth will either decrease or increase by 1.159. The relationship is positive. Human capital (H) significantly affects GDP_Growth; as each unit of Bitcoin changes, GDP_Growth will undergo a significant alteration of 0.0145. The relationship is positive.

Consequently, the Nested Module shows the same results in terms of significant impact and its type. Therefore, this allows us to adopt the reached result as the final decision.

Discussion

This study was conducted to investigate, from a macroeconomic perspective, the impact of Bitcoin cryptocurrency variables on sustainable economic growth in the Asian region. To our knowledge, this study represents one of the initial investigations into this topic from this particular perspective. The country sampling included Japan, China, India, Singapore, Indonesia, Hong Kong, South Korea, the Philippines, Thailand and Turkey, each of which is a member of an important regional or global organization. We chose the 2013–2020 timeframe for our analyses, as it represents the period during which Bitcoin witnessed its most significant growth, according to financial experts. Additionally, before that period, some of these countries opted to either ban or implement restrictive policies or even exert other forms of control over the circulation and usage of Bitcoin. Moreover, it is important to highlight that Bitcoin is still relatively new; its usage began in 2009, gaining recognition in Asia in 2011. According to Marr (2017), ‘As it [Bitcoin] had never been traded, only mined, it was impossible to assign a monetary value to the units of the emerging cryptocurrency’. Furthermore, over the past two years, it has been worthwhile to analyse the impact of the spike in the COVID-19 pandemic on the behaviour of this instrument in these economies. Regarding methodology, we opted for panel data analysis conducted using Stata statistical package version 17.

The findings demonstrate that the independent variables, including the Bitcoin variable, exert a significant influence on the dependent variable, ‘GDP’. This implies the acceptance of the alternative hypothesis, indicating that cryptocurrency has a notable effect on economic growth in the 10 Asian countries. Furthermore, the findings reveal a negative correlation between GDP and Bitcoin. Therefore, any unit of Bitcoin price change will negatively impact the economy by decreasing the value of the GDP. Consequently, we accept Hypothesis 1.1.

After conducting a thorough analysis, we successfully addressed our research question, ‘What is the impact of using cryptocurrency such as Bitcoin on the economic growth of countries?’ Our findings aligned with the existing literature on sustainable economic growth, highlighting a significant relationship between the two variables. Furthermore, we assert that this relationship carries a subtle negative impact from a macroeconomic standpoint. In particular, we align ourselves with economists who state that Bitcoin functions as an instrument contributing to increased inflation by raising the demand for money in the economy. This, in turn, leads to an expansion of the money supply, elevating the risk of resorting to printing money to meet demand, thereby leading to hyperinflation. This aligns with the quantity theory of money, which asserts that any increase in the money supply can lead to hyperinflation. Similarly, our results resonate with the existing literature, supporting the idea that cryptocurrencies, such as Bitcoin, exert numerous negative influences on economics, particularly on the finance-macroeconomic aspect. This is notably manifested in their adverse effects on financial and monetary terms.

According to MarketWatch, 3 cryptocurrencies, like traditional currencies, lack intrinsic value. However, unlike authoritative money, they do not have a corresponding liability. This implies that no institution, such as a central bank, has a vested interest in maintaining its value. The implications for central banking and financial stability will be profound, whether this is a bubble that will burst or a sign of a more radical shift in the concept of money. For instance, instead of keeping the cash in the bank and saving it legally, individuals who are concerned about high taxation on assets, government regulations or social and financial insecurity may choose to put their resources at risk. Consequently, an increasing number of people are turning to cryptocurrencies. While cryptocurrencies operate without servers, traditional banks may inevitably run out of cash reserves, leading to a shortage of funds available for loans to individuals. This shortage can diminish investments and capital, posing a potential threat to the economy and causing undesirable effects. Inspired by the above analyses, according to Singh (2023), in an interview with Singapore’s new president, Tharman Shanmugaratnam—formerly the country’s finance minister and central bank chairman—the intended purpose behind the creation of cryptocurrency is no longer to serve as ‘digital money’. Instead, people are currently using cryptocurrencies as speculative instruments, leading to economic challenges, especially in terms of growth. Speculative instruments like cryptocurrency and forex have the potential to increase inflation. This increase results in a reduction in investment volume, causing the economic growth of countries to shrink. These consequences, in turn, can lead to negative externalities, ultimately resulting in a recession.

Finally, in his study, El-Arian (2023) pointed out that, since the government will have no role in monitoring cryptocurrencies, it will undoubtedly be responsible for cleaning up whatever mess is left by a ‘burst bubble’. Regarding where and when the bubble bursts, the ensuing devastation could be significant. For instance, central banks in advanced economies with sound monetary standards may be able to diminish the damage, but the same cannot be applied to emerging economies.

On the other hand, our findings align with Solow’s growth model, as all the variables are suitable to serve as control variables. This is evident from the significant results, as each of them exhibits probability values under 1%, 5% and 10%, proving their effectiveness in explaining the dependent variable ‘GDP growth’ as a proxy for economic growth, albeit with varying effects.

First, capital, as explained in Robert Solow’s theory, has a significant positive impact on economic growth, as demonstrated by the estimation results. These results indicate that in our sample of 10 Asian countries, both capital inflow and outflow are necessary to stimulate production and foster growth. The same principle applies to labour, which Solow identified as one of the production factors. However, our findings reveal a negative impact of this variable on the economic growth of our sample. This implies that a larger labour force is associated with lower economic growth. In other words, these results can be explained by the fact that a large population creates the problem of unemployment, thereby negatively affecting the economic growth of the nation. This is consistent with the characteristics observed in our sample countries. Therefore, we align with economists such as Easterlin (1967) who suggest that ‘it is possible that the effect of population growth on economic development has been exaggerated’ (p. 98).

As for human capital, a variable we employed to illustrate the selected societies’ comprehension and mastery of Bitcoin, it constitutes one of our essential contributions to the existing literature. Bitcoin can be considered a significant economic factor if society understands how to inject it effectively. Therefore, this factor, identified in our study as a key to achieving sustained growth across all sectors, contributes to the proliferation of cryptocurrency. According to our findings, this variable significantly and positively affects the economy: the higher the level of education within the population, the better their understanding of the advantages and disadvantages of using Bitcoin, leading to potentially greater economic growth. This result has been confirmed by Maneejuk and Yamaka (2021), who state,

The regional analysis reveals that higher education impacts become twice as strong when the enrollment rates are greater than a certain level. Therefore, we may conclude that secondary enrollment rates positively affect economic growth; however, higher education is the key to future growth and sustainability. (p. 1)

Finally, Solow’s model underscores the significance of technology in generating long-term growth without experiencing diminishing returns. When the level of technology remains constant, growth either decelerates or, worse, comes to a halt. Technology has created such disparities among countries that are classified as developed and developing. Our empirical results in these 10 Asian countries confirm that technology has a positive influence on their growth. This implies that as these nations gain more technological access and use more sophisticated technologies, their growth rate will increase. These findings align with existing literature.

Conclusions and Policy Implications

According to the scientific literature reports and numerous studies on economic growth, including the work conducted by Leitão (2010), factors like banks, imports and exports, and productivity exert significant influence on economic growth. An empirical analysis using data from 23 OECD countries highlights the essential role of financial development in fostering economic growth (OECD, 2015). The latest financial development is the creation of cryptocurrencies, such as Bitcoin. To the best of our knowledge, there are no data demonstrating or validating the real impact of cryptocurrencies on the economic growth of nations or any contribution in this regard. Therefore, we endeavoured to investigate the role and impact of Bitcoin on the economic growth of selected Asian nations, given their extensive use of such instruments. We, however, focused on the macroeconomic perspective, which we considered a significant contribution to the macroeconomic and economic literature. Our research question aimed to figure out whether Bitcoin has had an impact on economic growth and, if so, whether it manifests as investment or inflation.

Our results differ from certain findings and align with a few others; we share the same opinion regarding the traditional drivers of economic growth, including capital, education, and the crucial role of technology in ensuring sustained long-term growth. However, our results suggest that population growth will increase the labour participation rate, subsequently raising the unemployment rate and having a negative impact on economies. Regarding our primary focus, which represents the object of this research (Bitcoin), we found that this factor does indeed have a negative impact on the economies in our sample. In our humble opinion, we align with the perspective that asserts that the use of Bitcoin, along with its extensive transaction volume, leads to a higher-than-expected increase in the inflation rate, adversely affecting the monetary policies adopted by the countries in our sample. Therefore, we believe that the decision taken by certain countries, such as China, to ban the use of Bitcoin or regulate and supervise it is crucial and necessary to mitigate the direct or external effects caused by this instrument.

An increasingly prominent alternative that has garnered attention from various economic participants, including the International Monetary Fund (IMF), is the Central Bank Digital Currency (CBDC). The 2022 report titled ‘Towards central bank digital currencies in Asia and the Pacific: Results of a regional survey’ suggests that central banks worldwide should emulate Asian economies in adopting CBDCs (Jahan et al., 2022). This strategic approach not only safeguards monetary systems and policies but also holds the potential to enhance payment systems, foster financial inclusion, combat financial fraud and expedite the shift to a cashless society. These benefits and associated ramifications align with the operational dynamics of cryptocurrencies as exemplified by Bitcoin (Urquhart, 2022). Notably, several countries have already instituted CBDCs, such as China’s e-CNY, India’s e-rupee and Singapore.

In Singapore, the Monetary Authority of Singapore launched Project Orchid to assess the viability of a retail CBDC. As part of this innovative initiative, the Development Bank of Singapore (DBS) collaborated with Open Government Products to inaugurate Singapore’s first programmable money live pilot for government vouchers. Looking ahead, in 2023, DBS intends to embark on a pilot program focused on programmable rewards, as pointed out in the Future of Finance Forum (DBS Bank, 2023). Reflecting on India’s e-rupee, (DBS Bank, 2023) proposes the introduction of a digital rupee, allowing consumers to choose between a digital bank deposit or alternative options. He argues that there is no use case for private digital currencies that fiat digital currencies cannot fulfil (DBS Bank, 2023). China’s official launch of e-CNY in 2020 represented a pioneering step for a major economy. With the increasing adoption of CBDCs in China, the simplicity and speed of global business transactions within the country could undergo a revolutionary transformation, as outlined in the Future of Finance Forum (DBS Bank, 2023).

However, the 2022 report from the International Monetary Fund (IMF) underscores that the surge in interest in CBDCs is linked to the growth of the global crypto ecosystem and the increasing adoption of crypto assets in Asia. The recent decline in crypto asset prices and issues with stable coins may intensify regulatory scrutiny, thereby impacting decisions related to CBDCs, including considerations for retail CBDCs (Jahan et al., 2022).

As a result, this study recommends that all economic stakeholders, including families, businesses, and governments, embrace technological innovation across all sectors, with a particular emphasis on financial innovation. Additionally, we suggest establishing clear regulations regarding the use of cryptocurrency, as well as ensuring protection against any fraud that may harm individuals and the economy.

It is imperative to mention that the present study has certain limitations, like any other empirical endeavour. The most important limit is the scarcity of data sources, especially the challenge of accessing Bitcoin data, which is very difficult to collect from only two sources. Therefore, it is hoped that future research in this study could encompass a broader range of countries.

Finally, the current study initiates a lively debate in the literature by investigating economic growth and the factors influencing it. We can safely assert that our results provide valuable insights into the impact of financial instruments, exemplified by the case of Bitcoin, not only on the monetary policies of the sampled countries but also on their sustainable economic growth. For this reason, we believe that our study could serve as the starting point for further scientific investigations in this domain, laying the foundation for future research.

Footnotes

Acknowledgements

The earlier version has benefited from useful comments by an anonymous reviewer of this journal.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.