Abstract

This article builds a Structural Vector Autoregressive model and employs non-recursive identification restrictions to examine the effectiveness of the Monetary policy transmission mechanism in India during the Flexible Inflation Targeting regime (2016–2023). The results indicate that policy rate shocks have a significant negative impact on domestic output and prices during this regime. The findings further, reveal evidence of an exchange rate puzzle during the Flexible Inflation Targeting regime. Our results give credence to the RBI’s move towards a Flexible indicator targeting approach as all the macroeconomic variables of interest, that is, Domestic output and inflation produce plausible estimates in response to a monetary policy shock.

Introduction

The global financial crisis posed considerable challenges for central banks worldwide and subjected their monetary policy mandates to a critical re-evaluation. In the wake of the taper tantrum episode of 2013, the credibility of India’s monetary policy regime based on the Multiple Indicator (MI) Approach came under scrutiny 1 as persistently high inflation and moderate growth began to co-exist. Indian economy which remained insulated from the unprecedented financial instability induced by the crises accordingly, revised its Monetary policy framework by constituting an Expert committee on Monetary policy reforms in September 2013. Concomitantly, a Monetary Policy Framework Agreement was executed between the Government of India and the Reserve Bank of India (RBI) in 2015 under which the inflation target based on Consumer Price Index-Combined (CPI-C) was set at 4% with a range of (+/-) 2%. The credibility of India’s monetary policy stance henceforth rested upon a rule-based monetary policy framework under which the RBI articulates and makes public a target inflation rate and then, attempts to steer actual inflation towards the target through the use of policy instruments, such as policy rate and other monetary policy tools. As interest rates and inflation rates tend to move in opposite directions, the RBI is expected to raise or lower interest rates to move towards the projected inflation target so as to achieve stable prices and thereby ensure economic stability. This new framework thus imparts greater autonomy to the RBI in the conduit of its objective of price stability.

However, over the last two years, central banks across the world have been raising interest rates simultaneously to cool inflation and this has raised significant concerns about the conduct of monetary policy. Even though interest rate hikes work to lower inflation, policymakers would not know until later if the central bank’s forward-looking move was successful or not as monetary policy has a lagged impact on output and inflation. Alongside these global developments, recurrent incidences of large and overlapping supply-side shocks amassing the Indian economy have brought with them the risks of generalization of inflation impulses, possible loss of monetary policy credibility and de-anchoring of inflation expectations. 2 Amidst these uncertainties. India’s inflation outlook remains uncertain. To maintain credibility, RBI’s monetary policy stance has remained disinflationary over the last two years and the central bank is continuously steering inflation towards the target rate of 4%. Amidst these global developments, the key question that emerges is—Has the RBI been able to curb prices through its Flexible Inflation-targeting approach?

To date, no research has been undertaken to investigate the efficacy of RBI’s monetary policy stance during the FIT regime in terms of inflation containment. We thus make a novel attempt to examine the impact of monetary policy on India’s domestic output and inflation during the aforesaid regime and in the process ascertain whether changes in RBI’s policy rate stance during this regime have been successful in curtailing prices. Our research contributes to the extant literature in two major ways. First, we develop a Structural Vector Autoregressive (SVAR) model with non- recursive identification restrictions 3 in line with Kim and Roubini (2000) 4 and examine the effect of an unexpected monetary policy shock on real economic variables during the Flexible Inflation targeting regime in India. Moreover, unlike previous empirics that treat foreign variables as exogenous, we impose block exogeneity constraints to our baseline SVAR model considering India being a small open economy. Second, an assessment of monetary policy transmission dynamics during the FIT is expected to help policymakers in deciphering the credibility of RBI’s monetary policy stance and revisit it accordingly. To anticipate the results in the article, our SVAR model based on a theoretically postulated identification scheme appears to be successful in identifying monetary policy shocks and solving the price puzzles as price fall following a contractionary monetary policy. Also, domestic output declines in response to a monetary contraction. Our findings thus affirm the credibility of RBI’s monetary policy stance during the Flexible Inflation-targeting regime in India.

The article is structured as follows. The section ‘Review of Literature’, reviews the extant empirical literature on monetary policy transmission. The section ‘Data and Variable Descriptions’ discusses the data and the variables chosen for the empirical analysis. ‘Research Methodology’ section summarizes the structural VAR modelling method and details the identification restrictions imposed for examining the response of domestic output, inflation and exchange rates to an unexpected monetary policy shock. The section ‘Empirical Findings’, presents the empirical findings under the Flexible Indicator Targeting Regime. The section ‘Robustness of Empirical Results’ provides for sensitivity analysis and the robustness of the results. Finally, the section ‘Concluding Remarks’ concludes with the findings, policy implications and summary of the study

Review of Literature

Seminal work investigating the impact of a monetary policy shock on key macroeconomic variables is based on Vector autoregressive (VAR) 5 framework (Bernanke & Blinder, 1992; Christiano et al., 1999; Leeper et al., 1996; Morsink & Bayoumi, 2001; Peersman & Smets, 2005; Sims, 1990). However, other exemplary work (Cushman & Zha, 1997; Kim & Roubini, 2000), based on these models highlight that VAR-based Choleski decomposition techniques provide implausible estimates on the effect of monetary policy for small open economies. In order to improve upon these atheoretical VAR models and mitigate the aforestated empirical anomalies, Blanchard and Watson (1986) and Bernanke and Sims (1986) developed SVAR models with both recursive 6 and non-recursive 7 identification structures. These SVAR models have been extensively employed to examine the effect of a monetary policy shock in developed economies, that is, Leeper et al. (1996), Cushman and Zha (1997), Kim and Roubini (2000) and Dungey and Pagan (2000) among others. Studies based on the SVAR model which find plausible results of a monetary policy tightening include those of, Tang (2006), Aleem (2010), Davoodi et al. (2013), Mengesha and Holmes (2013) and Perera and Wickramanayake (2013) among others. Similar findings based on SVAR models have been observed by Smets and Wouters (2002) and Mojon and Peersman (2003) for the Euro Area and Dale and Haldane (1995) for the UK.

The effect of a monetary policy shock on key macroeconomic variables has been investigated at length for the Indian economy. Most studies have found plausible effects 8 of monetary policy shocks during the MI targeting regime in India (Al Mashat, 2003; Aleem, 2010; Bhoi et al., 2017; Khundrakpam & Jain, 2012). On the contrary, there are others who have found no effect of monetary policy shocks on inflation and output during the same period (Banerjee et al., 2018; Bhattacharya et al., 2010; Mishra et al., 2016). Studies examining this effect have mainly relied on VAR frameworks (Aleem, 2010; Bhoi et al., 2017; Sengupta, 2014) that use Cholesky decomposition techniques (e.g., Eichenbaum & Evans, 1995; Grilli & Roubini, 1995; Sims, 1992) under which the monetary policy does not react to instantaneous changes in the exchange rate. This recursive identification scheme, however, appears unappealing 9 for small open economies like India as such economies react quickly to exchange rate shocks (domestic currency depreciation) and quickly respond by tightening their monetary policy to curtail inflationary pressures. Results drawn from such recursive identification schemes are hence likely to be biased and often criticized as they lack strong theoretical insights and exhibit empirical anomalies like liquidity puzzle 10 , price puzzle 11 , exchange rate puzzle 12 and forward discount puzzle 13 .

Critically analysing the effect of monetary policy shocks on the macroeconomic variables, we find the use of SVAR models to examine this effect for India to be rather limited. It is thus a daunting task to set up a truly representative model for empirical analysis as there prevails ambiguity on the choice of appropriate methodology, model specification and the inclusion of variables. In lieu of the drawbacks associated with VAR-based approach discussed earlier, we build a non-recursive SVAR model and develop an explicit monetary policy reaction function that solely accounts for endogenous change in the policy rate.

Data and Variable Descriptions

Our study employs monthly data spanning 2016–2017: M10 to 2022– 2023: M12. The choice of sample period is essentially chosen to examine the effect of monetary policy shocks during the Flexible Inflation Targeting regime in India. There are six variables—World Oil price index (LWOPI), US Federal funds rate (FFR). Index of Industrial Production (LIIP), CPI-C, Weighted Average Call money rate (CMR) and the Real Effective Exchange rates (LREER).

The LWOPI captures the prices of both energy and non-energy commodities. The FFR is taken as a proxy for foreign interest rates. The monetary policy variable is represented by the CMR as this is the operating target of the RBI. This short-term interest rate captures the monetary policy stance during the Flexible Inflation targeting regime in India. The study also conducts robustness checks by employing alternative indicators of monetary policy stance, that is, the Treasury Bill rate (TB) and the 10-year Government Bond rate (TYB). In addition, the LREER are employed to represent the exchange rate dynamics.

Finally, the macroeconomic variable which captures the impact of monetary policy impulses on the real economy is represented by the LIIP)and CPI-C. The LIIP serves as a proxy for domestic output as real GDP data is not available on a monthly basis for the period under consideration. The CPI-C captures the impact of domestic prices during the FIT as post the adoption of the Flexible inflation targeting regime in October 2016, RBI had been communicating its indicative inflation projections based on CPI-C. We however employ the Whole sale Price Index (WPI) in a different specification to assess the credibility of the nominal anchor CPI-C visa vis WPI which was used by the RBI during the MI Targeting regime in India. The study uses an inflation rate rather than WPI/CPI-C as India targets an inflation rate. The Domestic inflation rate is calculated from the WPI/CPI-C, using the inflation rate formula.

The X-12 14 procedure is used to adjust the seasonality in all the variables, except the policy rate. These variables are further changed into natural logs except domestic inflation and policy rates (Both Foreign and Domestic-Federal Funds rate (FFR), CMR, TB and the TYB which are kept in percentage points. The data sources and their compilation are discussed in the Appendix A.

Research Methodology

In view of the evidence obtained from the literature stated and discussed earlier, we take this study forward to understand the effect of an unanticipated monetary policy shock on macroeconomic variables during the Flexible Inflation targeting regime in India. We develop an explicit monetary policy reaction function within an SVAR model 15 , which takes into consideration the structural features of a developing open economy instead of relying on reduced-form equations and Choleski decomposition techniques. In accordance with Kim and Roubini (2000), we henceforth, employ a non-recursive 16 SVAR approach to examine the effect of unanticipated monetary policy shock in India.

SVAR Framework

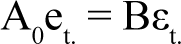

An SVAR model is a simplified representation of multivariate endogenous variables which are assumed to be contemporaneously and dynamically interdependent. Our SVAR has the following form:

where Yt represents (n×1) vector of endogenous variables; A0 is an invertible (n×n) matrix of coefficients representing contemporaneous relationship among the endogenous variables; A(L) is the kth order matrix polynomial in the lag operator L, A(L) = A1(L) −A2L2− AkLk representing the coefficients of the lagged variables and ut is a (n×1) vector of structural error terms. These model residuals have a linear relation with the structural shocks (εt.) such that ut = B where B is a (n×n) matrix. Thus (εt.) is a (n×1) represents the vector of the structural shocks which are assumed to be normally distributed with zero mean and normalized diagonal variance–covariance matrix Ω = I. Equation (1) therefore takes the form:

Pre multiplying the above structural Equation (2) with A0−1, a reduced form VAR is specified

Where C(L) = A0–1 A(L); et. represents a vector of reduced form residuals, that is, A0−1 Bεt.

In compact form, a SVAR system relates to the following relations:

Equation (4) is known as the AB model 17 . In order to obtain the structural parameters, the reduced form Equation (3) is to be estimated by using the relation in Equation (4).

SVAR Model Specification

The SVAR model employed to examine the effect of an unanticipated monetary policy shock on key macroeconomic variables includes six variables as represented by the following vector Yt.

Where LWOPI is the World oil price Index and FFR is the US Federal fund’s rate, LIIP is the Index of Industrial Production, WPI is the Wholesale Price Index, LMD is Broad Money, CMR is the Weighted Average call money rate and LREER is Real Effective Exchange Rates.

The choice of the LWOPI and US Federal fund’s rate is guided by the prior literature (Cushman & Zha, 1997; Kim & Roubini, 2000) on SVAR modelling for small open economies. These two variables are incorporated to isolate and control for exogenous changes in the monetary policy. The choice of the LWOPI is justified as it serves as a proxy for negative and inflationary supply shocks. If the RBI tightens its monetary policy because of an inflation-induced supply shock, the resultant slowdown and price rise is not only due to a contractionary monetary policy stance but also an outcome of exogenous supply shocks. Nevertheless, the US Federal Funds rate is included to control for that portion of domestic monetary policy that emancipates from foreign monetary policy shocks. The remaining four variables are well-documented variables in monetary policy transmission literature which respectively capture the monetary policy stance, domestic output, inflation, and the exchange rates. All variables except the Federal funds rate and CMRs are expressed in logarithms.

Identification of Monetary Policy Shocks

The equations below detail our identification structure

18

:

To identify the Structural VAR, our study imposes non-recursive identification restrictions on both matrices A0 and B (AB model) in accordance with the method introduced by Amisano and Giannini (1997), where matrix A0, represents the contemporaneous relationship between the variables and the B is assumed to be a diagonal matrix.

The overidentified SVAR model is represented in matrix form (5) as follows:

The restrictions imposed on the contemporaneous structural coefficients in A0 are primarily based on Kim and Roubini (2000) but modified in several aspects

19

. Each row in the specification is a representation of the following structural equations:

Where the LIIP, CPI-C and CMR are not present either contemporaneously or with a lag, as the LWOPI remains unresponsive to these variables. However, we do include the lagged federal funds rate variable as a hike in Federal interest rate causes the US dollar to gain strength, making it difficult for consumers to buy crude. This has a negative impact on crude oil which leads to a decline in their prices. In addition, the inclusion of lagged exchange rate variables in the world oil price equation is justified as a major chunk of Indian foreign reserves is spent on imports of crude oil. Any volatility in the exchange rate of the Indian rupee visa vis the US dollar is likely to influence crude oil imports which can impact their prices

20

.

where, the domestic variables are not present either contemporaneously or with a lag, as the FFR remains unresponsive to the Indian macroeconomic variables. However, we do include the lagged LWOPI in the above equation

21

Where aij2, for i = 1, … 6, and j = 1, … 6 is the coefficient of contemporaneous estimate, Ai(L) is the ith row of matrix A(L) and indicates the lagged variables; c1, …,c6 are the intercepts,

The first two equations represent the exogenous shocks originating from India’s increasing integration with the global economy. The World Oil Price Index (WOPI) is not impacted by movements in any of the domestic variables contemporaneously; however, it does get impacted by the lagged values of exchange rates. The Federal Funds rate (FFR) is assumed to react positively and contemporaneously to the LWOPI. This restriction implies that the US Federal is expected to tighten its monetary policy in response oil-price-related inflationary shock. It is expected that

The next two equations represent the structural shocks associated with domestic output (LIIP) and inflation (CPI), which together constitute the goods market equilibrium of the Indian economy. Based on theory and past empirical work (Cushman & Zha, 1997; Kim & Roubini, 2000), our study assumes that the policy rates, US Federal funds rate and the exchange rates do not affect domestic output contemporaneously. They are assumed to affect the domestic output only with a lag. The only contemporaneous variable to affect the Domestic output is the LWOPI.

23

It is expected

The next equation is the monetary policy function of the RBI, which sets the policy rate after considering the current values of exchange rates and all the lagged variables in Yt. Like Sims and Zha (1995) and Kim and Roubini (2000), this restriction is based on the premise that information on domestic output and inflation rates are available to the policymakers only with a lag

24

and so monetary policy remains unresponsive to output and price shocks contemporaneously. Exchange rates are included to control and identify true and exogenous

25

contractionary monetary policy changes that are an outcome of domestic currency depreciation only. The monetary policy function (CMR) equation thus, is assumed to be positively and contemporaneously impacted by the exchange rates and hence and

To sum up, the structural shocks constitute various blocks. The first two equations represent the exogenous shocks originating from the World economy. The next two equations depict the goods market equilibrium for the domestic economy. The consecutive equation represents the monetary policy function of the RBI. The last equation represents the structural shocks associated with the exchange rates.

Our empirical strategy proceeds as follows: First, the study conducts the unit root tests and reports the results. Subsequently, an appropriate lag order for the SVAR is selected based on the optimal lag length as provided by different information criteria. Next, we impose the non-recursive identification restrictions on the appropriate coefficients of the system. Finally, the study generates the Impulse response functions which capture the dynamic response of each variable to shocks in different equations of the SVAR system, that is, the impact of a policy rate shock at a specific period(t) on other macroeconomic variables within the system over subsequent period(t+s). Likewise, our study also computes Variance Decompositions which report the contribution of total variance attributable to each structural shock to the system.

Empirical Findings

Unit Root Tests

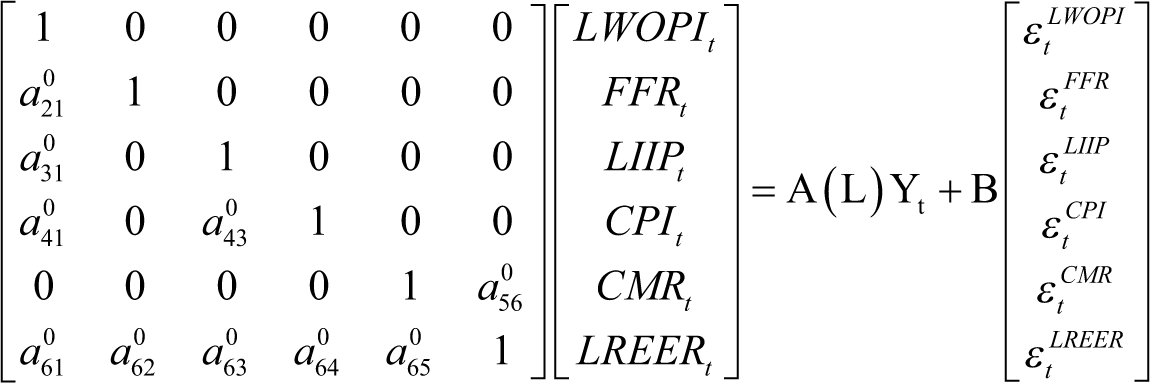

Table 1 provides the results from the Augmented Dickey-Fuller (ADF) and Phillips Perron (PP) unit root test for the variables employed under the Flexible Targeting Regime in India. The ADF test results indicate that all the variables are integrated of order one except the LIIP, which is stationary at the levels. The PP unit root test also shows similar results. Hence, we proceed to conduct the empirical analysis for the others in the first differences.

Unit Root Test.

The subscript *indicates significance level at 5%. The null of ADF and PP test is that the variable has a unit root.

Choice of Lag Lengths

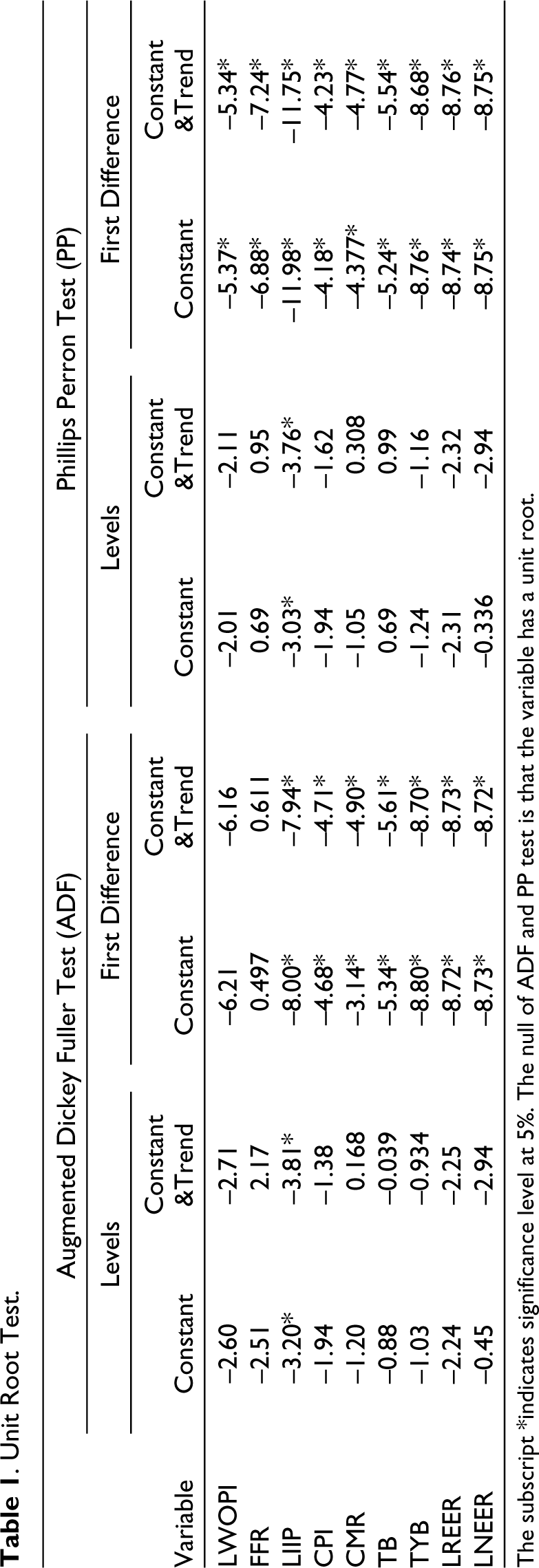

Table 2 provides the optimal lag length under various lag length criteria for the SVAR Model under the Flexible Inflation targeting. The Schwarz Information criterion (SC) and Hannan Quinn Criterion (HQ) suggest a lag length of 1, LR Test statistic and Akaike Information criterion (AIC) indicate a lag length of 5 whereas the Final Prediction criterion (FPE), suggest a lag length of 3 to be the optimal for the model. In view of the drawbacks associated with a small sample size (60 observations), our model is estimated based on a lag length of 3 instead of 1 or 5 indicated by various lag selection criteria. If a lag length of 5 is chosen, impulse response varies explosively over the chosen horizon while a lag length of 1, is not able to explain the variable dynamics. Hence, we choose to take 3 as the optimal lag length which reports no serial correlation. Our SVAR model at lag length 3 satisfies the stability condition, which indicates that impulses generated from the model, are valid and stable.

Lag Order Selection Criterion.

* Indicates lag order selected by the criterion:

LR: Sequential Modified LR Test statistic

FPE: Final prediction error, AIC: Akaike information criterion,

SC: Schwarz information criterion, HQ: Hannan-Quinn information criterion

Impulse Response Analysis

In this section, we conduct the Impulse response functions analysis from our SVAR Model to examine the dynamic responses of macro-economic variables (domestic output and CPI-C inflation) and the exchange rates to one standard deviation positive shock to the policy rate. Before reporting the empirical findings from our SVAR model, it is pertinent to discuss the expected response of the macro variables to an unanticipated monetary policy shock. As widely recognized, the theory of monetary policy transmission postulates that monetary policy contraction leads to a rise in the short-term interest rate. Concomitantly, prices and output are expected to decline. However, if the monetary policy stance is not truly exogenous 26 , one may observe an increase in output and price level following a tight monetary policy. Also, a monetary policy contraction that increases the policy rate will lead to an impact appreciation of the exchange rates.

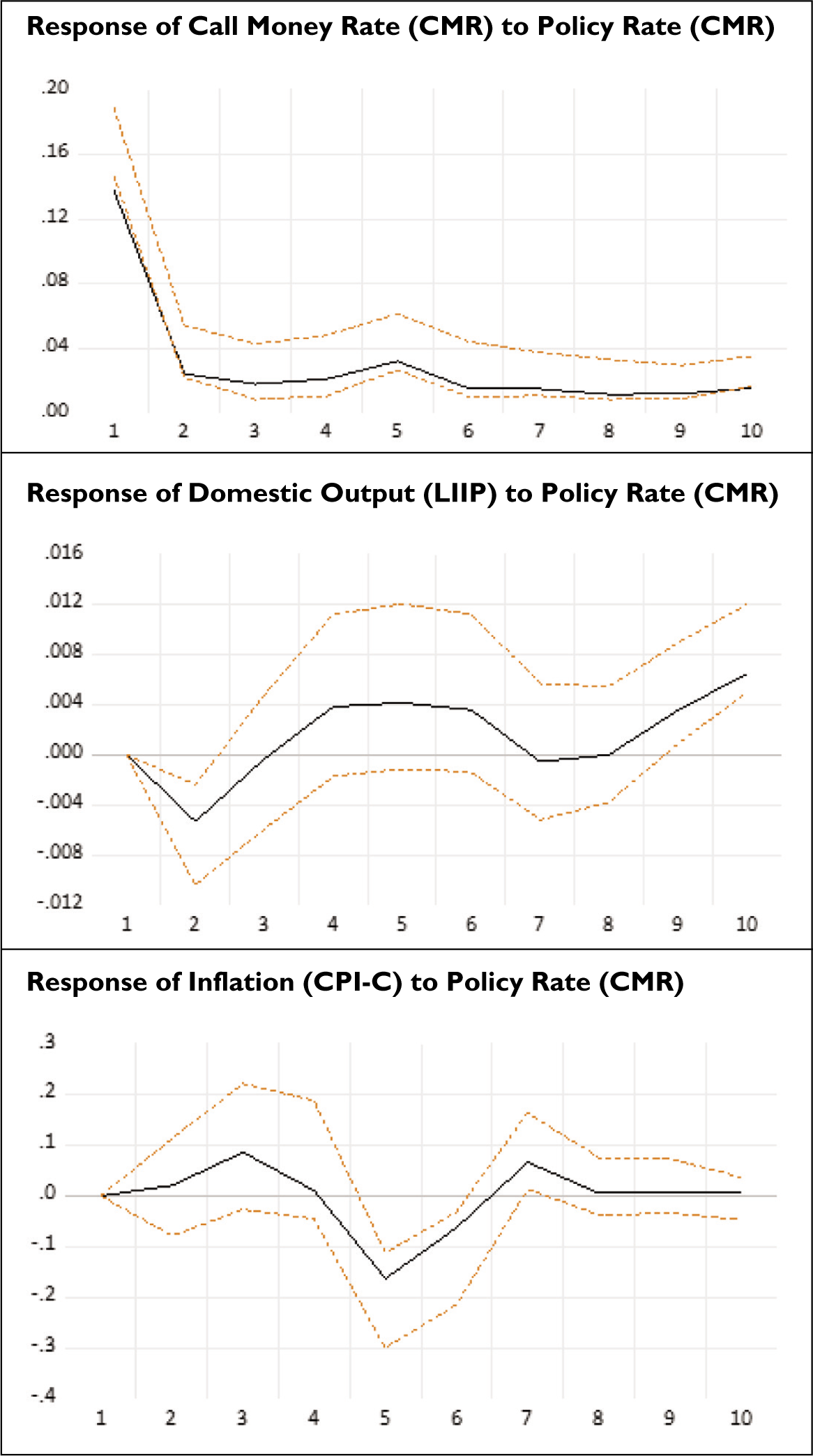

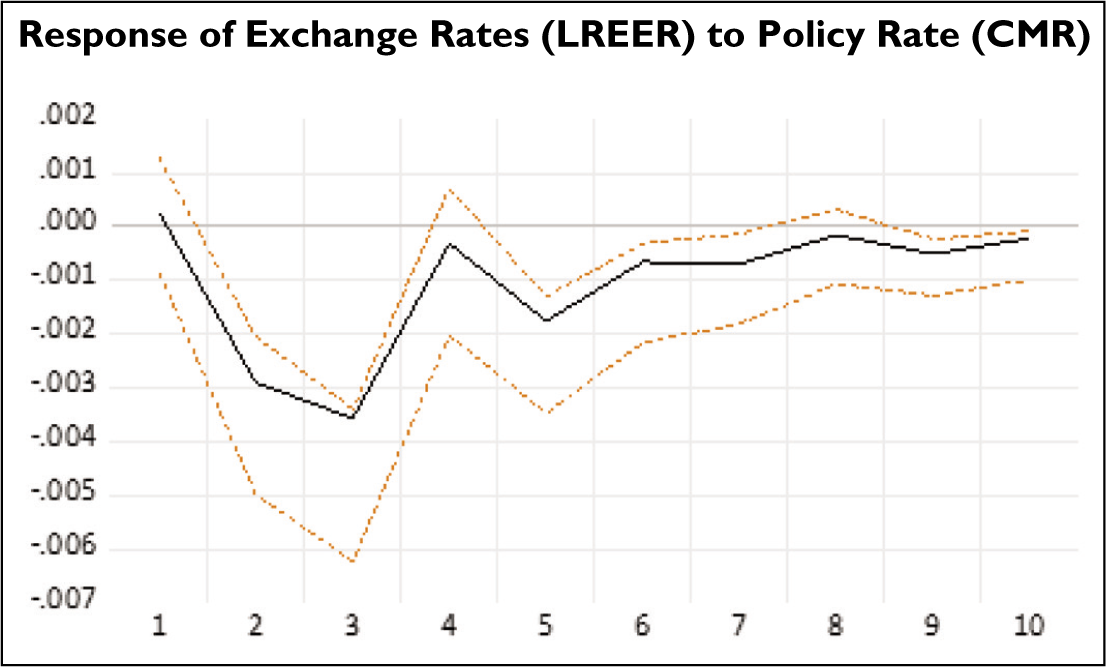

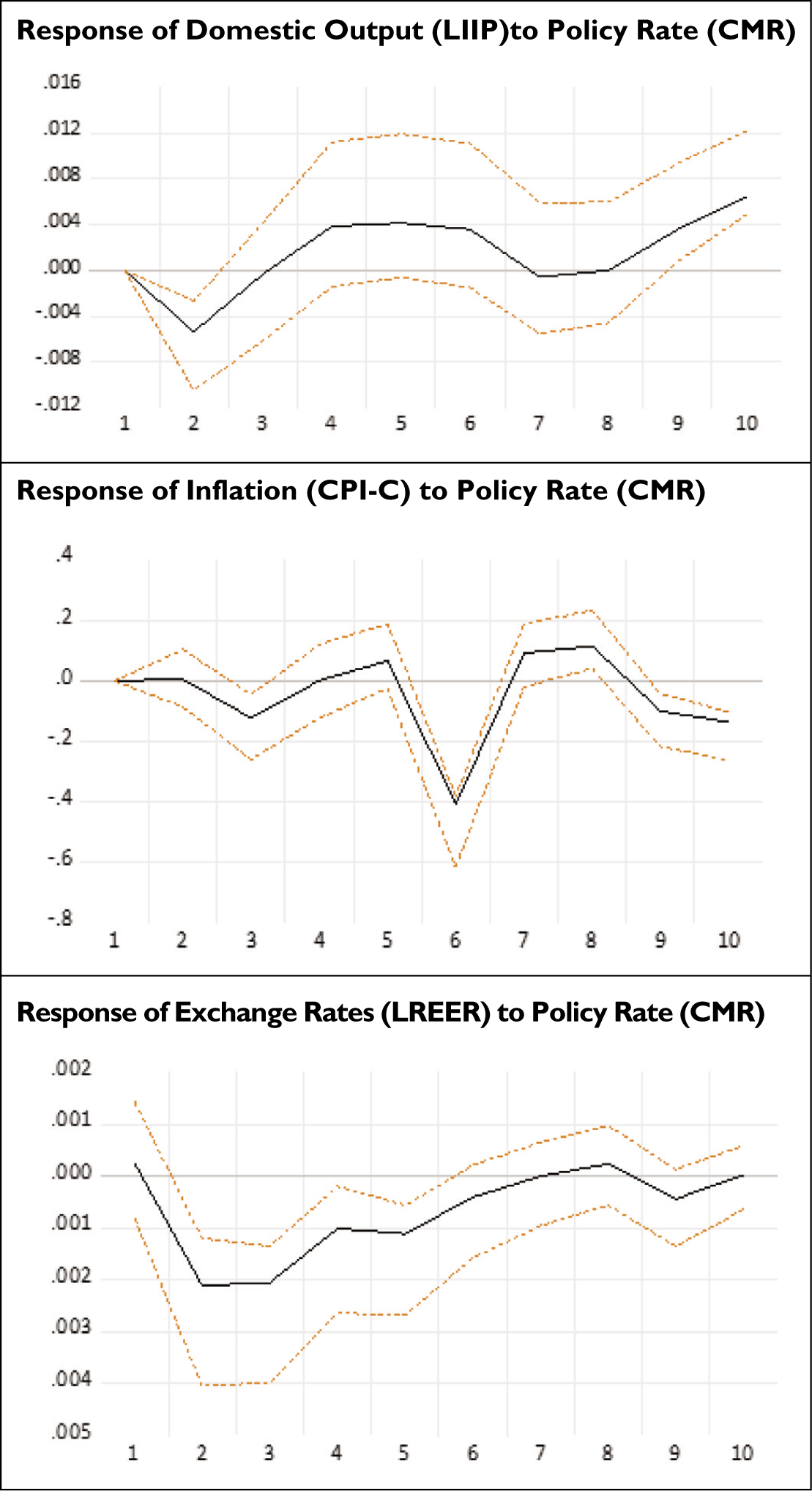

The Impulse responses obtained are presented in Figure 1 where the solid lines in the represent the estimated response while the two dashed lines show the confidence bands. These confidence bands are obtained from Hall’s bootstrapping method, which involves 68% confidence interval and 999 bootstrap replications. The following can be observed. In response to a monetary contraction, the policy rate rises instantaneously and the effect emerges statistically significant on impact and over the chosen horizon. Next, domestic output shows a significant and sharp decline in response to a positive policy rate shock in the second month. Nonetheless, prices show a sharp decline in response to a positive policy rate shock in the fifth month in concordance with the theoretical postulates of the effect of an unanticipated monetary policy shock. In addition, increases in policy rates cause the exchange rates to appreciate instantaneously, which, however, appears to be insignificant. We, however, do observe a significant exchange rate depreciation after the first month contrary to the directions predicted by theory, revealing evidence of an Exchange rate puzzle 27 . Hence, the inclusion of variables characterizing the world economy and imposition of theory-driven identification restrictions have not been able to address the exchange rate puzzles 28 during the Flexible Inflation targeting regime in India.

SVAR Model-impulse Response of Domestic Variables to Policy Rate Shock.

In spite of this empirical anomaly, the results so obtained are suggestive of the fact monetary policy transmission works well during the Flexible Inflation Targeting regime with Weighted Average Call money rate 29 as the operating target of monetary policy and Consumer Price Inflation-Combined as the nominal anchor for targeting inflation. This is evident as we find that positive innovations in the policy rate led to a significant decline in both domestic output and prices (CPI-C). Furthermore, in a different specification with WPI-based inflation as the price variable, we however find that a monetary policy contraction which leads to an increase in the policy rate, does not cause any significant decline in WPI-based prices (Appendix C). This finding implies that the RBI’s monetary stance has been successful in containing the nominal anchor for inflation (CPI-C) during the Flexible inflation targeting regime in India.

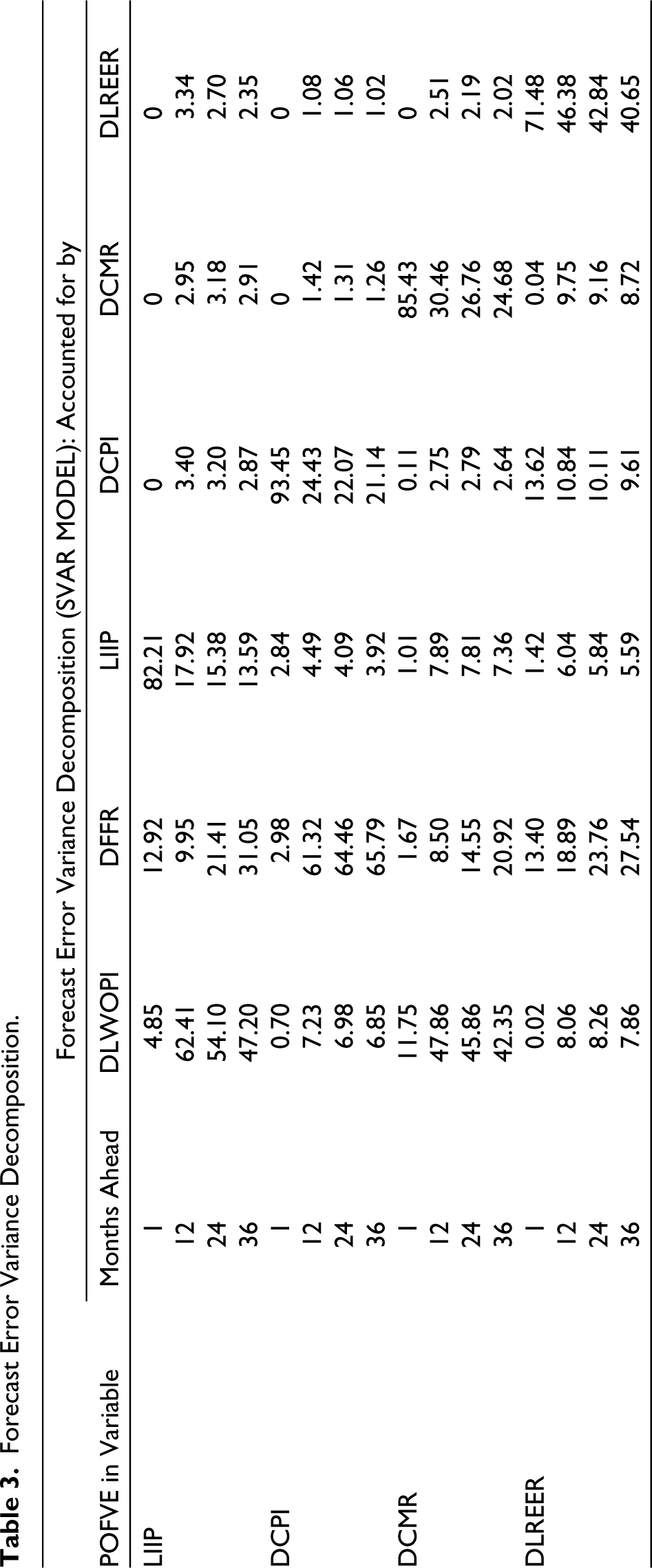

Forecast Error Variance Decomposition

In this section, we report the forecast error variance decomposition at horizons of 1–36 thirty-months to isolate the sources of fluctuations in domestic output and inflation in the SVAR Model. Forecast Error decompositions compute the share of the variances of the macroeconomic variables in the system attributable to shocks to the monetary policy rate. This analysis helps to decipher whether positive shocks to the policy rate that impact the other variables in the system are truly an outcome of contractionary monetary policy changes or whether they emancipate as a result of shocks to other exogenous variables. We further attempt to figure out from the variance decompositions as to how much of the fluctuations in the real economic variables, that is, domestic output and prices and exchange rates are being explained by the policy rates and the proportion of variation these variables account for in the policy rates. Table 3 summarizes the variance decomposition of domestic output, inflation (CPI-C), policy rate and the exchange rates to a positive innovation in the policy rate.

Forecast Error Variance Decomposition.

In Table 3, the monetary policy shocks account for a small portion of the fluctuation in domestic output (2.91%) and inflation (1.26 %) over the medium to long run. This result is like the findings of Bernanke and Mihov (1996) and Sims and Zha (1995a) for the US economy, who find monetary policy to have a negligible impact on domestic output. However, a positive shock to the domestic output and prices accounts for 7.36 % and 2.34 % of the variation in the policy rate after the same period. Hence the effect of monetary policy on domestic output and inflation is clearly identified. However, the same does not hold for exchange rates as the policy rate shocks explain about 2.02 % of the fluctuations in the exchange rates after 36 months but exchange rates account for about 8.72% of the fluctuations in the policy rate after the same period. Our results further find external variables, that is, World oil price index (DLWOPI) and the US federal funds rate (DFFR) to have a sizable impact (42.35% and 20.92% respectively)) on monetary policy rate (CMR) signifying their importance in formulating the monetary policy stance in India.

Robustness of Empirical Results

As the impulse responses so obtained from the construed SVAR model may be sensitive to the choice of alternate variables and the identification restrictions imposed, the baseline model is sensitized in different ways to affirm the stability of the results. Three basic aspects of the SVAR model are examined to check on the robustness of the results: Imposition of Alternate Identification restrictions, Restrictions on foreign variables in line with Kim and Roubini (2000), and some alternative measures for policy variables.

Restrictions on Foreign Variables

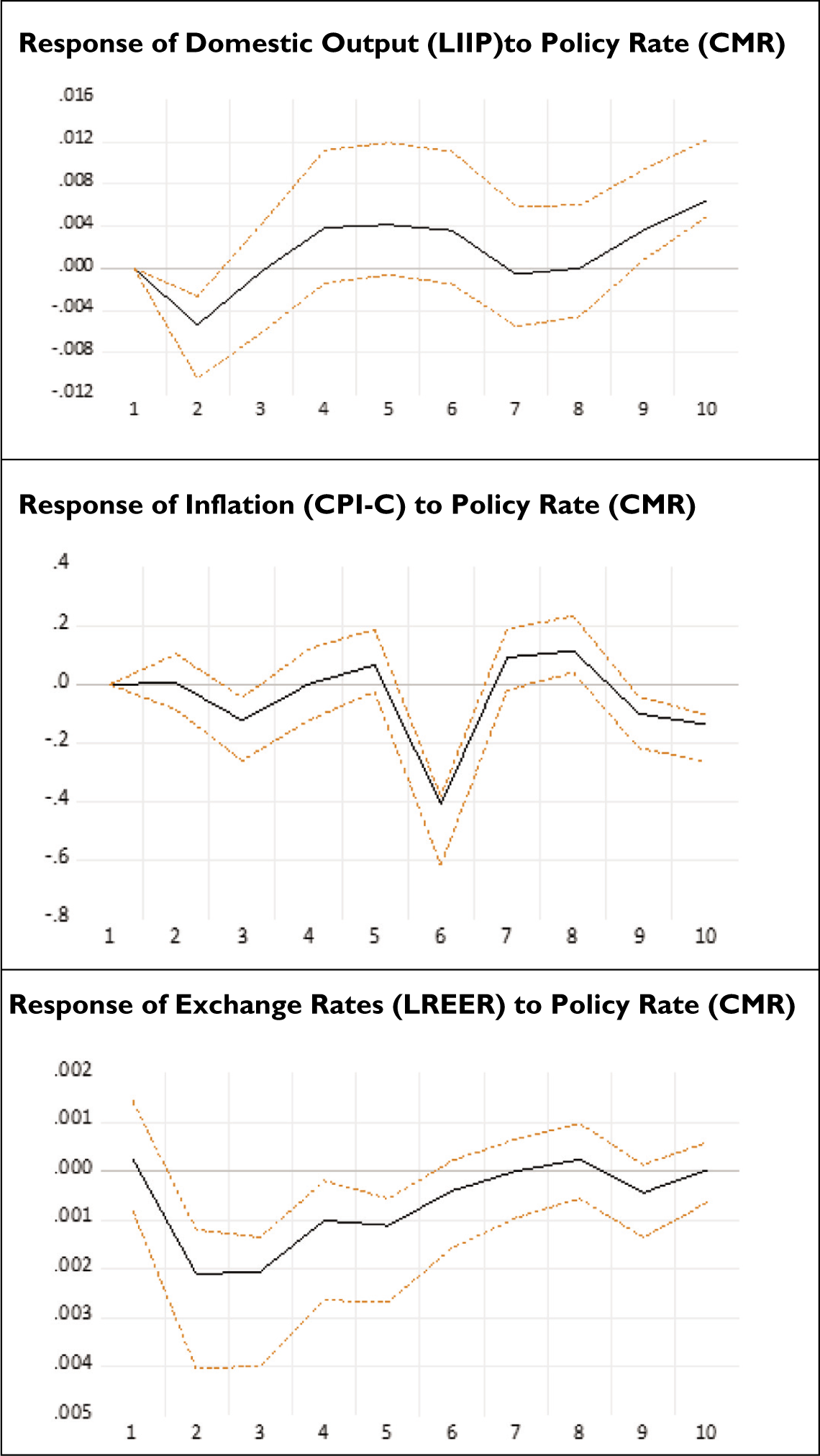

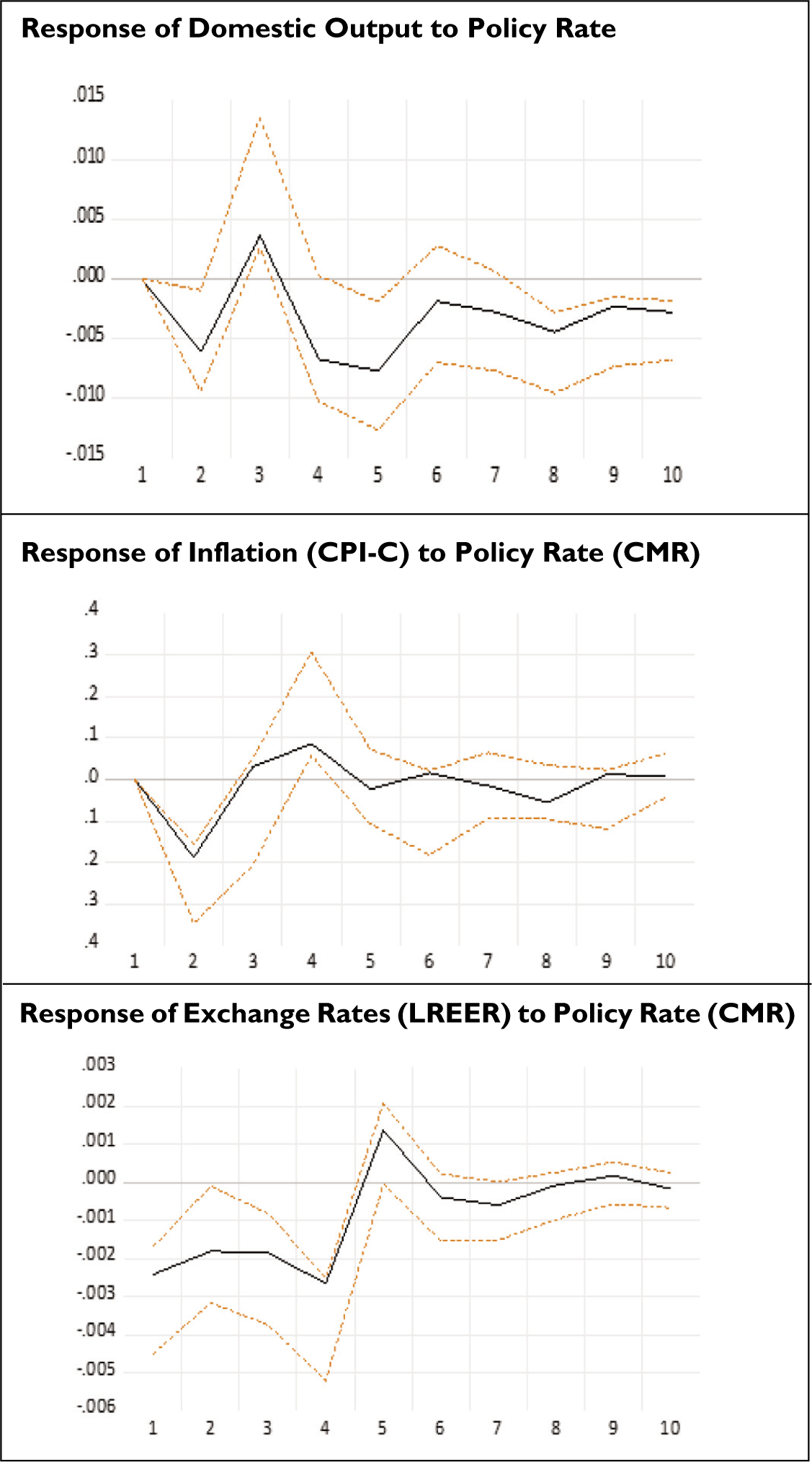

The Baseline specification imposes block exogeneity constraints on foreign variables in line with Cushman and Zha (1997). However, domestic shocks may impact the foreign variables either contemporaneously or with a lag. Hence, we allow the foreign variables to remain exogenous in response to contemporaneous changes in domestic variables and be impacted with a lag to the changes in domestic variables. This implies that foreign variables have a contemporaneous and lagged impact on the domestic variables while the domestic variables have only a lagged impact on the foreign variables. The responses of domestic output and inflation to a positive policy rate shock for the SVAR Model are presented in Figure 2.

Impulse Response Functions of Domestic Output, Inflation and Exchange Rates to Policy Rate Shock Without the Block Exogeneity Constraints.

The responses of domestic output, inflation, and exchange rates without the block exogeneity constraints on foreign variables for the SVAR model in Figure 2 affirm that shocks to policy rate leads to a significant decline in domestic output and CPI prices as portrayed by the baseline specification. Similar to the baseline specification, we obtain significant evidence of an exchange rate depreciation in response to a monetary contraction revealing evidence of an exchange rate puzzle.

Alternate Identification Restrictions

The Baseline specification is based on a SVAR model that imposes non-recursive identification restrictions to examine the effect of a monetary policy shock. Similar to other empirical studies (Bhoi et al., 2017) for the Indian economy we employ a VAR model with a recursive Choleski structure and ascertain whether the results remain robust.

In Figure 3 we obtain compelling evidence to corroborate the findings of our baseline specification that monetary policy shocks have a negative impact on domestic output and inflation. We further find evidence of a significant exchange rate puzzle similar to our baseline VAR model which highlights that alternate identification restrictions based on a VAR model have not been able to mitigate the exchange rate puzzle for the Indian economy during the FIT regime.

Impulse Response Functions of Domestic Output, Inflation and Exchange Rates to Alternate Identification Restrictions.

Alternate Policy Rates

The responses of domestic output, inflation and exchange rates to a positive policy rate shock (Call money rate) in the baseline SVAR model are compared to those obtained with other interest rate shocks, that is, 10-year Government Bonds rate (TYB). Positive innovations to the 10-year government bond rate 30 (TYB) shocks in Figure 4 lead to a significant decline in domestic output and prices. Our study further finds evidence of an exchange rate puzzle with positive shocks to the 10-year Government Bonds rate which is prevalent on impact, unlike the baseline model where the evidence is obtained at the third month. Overall, the results obtained are in conformity with the baseline SVAR model

Impulse Response Functions of Domestic Output, Inflation and Exchange Rates to 10-year Government Bond Rate Shock.

Concluding Remarks

In this article, we develop an open economy structural VAR model with non-recursive identification restrictions and identify monetary policy shocks based on a theoretically postulated monetary policy function keeping in mind the structural features of the Indian economy. Most of the dynamic responses so obtained to an identified monetary policy shock are consistent with a priori theoretical expectations about the effect of an unanticipated monetary policy shock on real economic variables. Our identification scheme successfully mitigates the price puzzle associated with monetary policy shocks for small open economies. We however obtain evidence of an exchange rate puzzle 31 during the Flexible Inflation targeting regime.

The findings obtained have important policy implications for the Indian economy. First, as suggested by the Expert Committee Report (2014), there is an urgent need to remove impediments in the pass-through of monetary policy rates to the real economy in India. In order to achieve this, it is imperative to align the Weighted call money rate (operating target) as close as possible with the policy rate (Repo rate). Second, India being an open economy, it is necessary to strengthen its economic fundamentals so that the effect of exchange rates on lowering domestic price levels appears discernible. Hence, policymakers in emerging economies like India should be prepared to manage the cross-border spillover effects of a monetary policy contraction by strengthening their macroprudential regulations and building up their forex reserves. Lastly, based on the short sample 32 under consideration, these evidence provide valuable lessons to the policymakers on the conduct of monetary policy in the years to come.

To conclude, our results provide credence to the RBI’s move towards a flexible inflation-targeting regime as the key macroeconomic variables of interest (domestic output and inflation) produce plausible responses. The RBI should thus remain steadfastly committed to its goal of aligning inflation to the target of 4%. 33

Footnotes

Acknowledgements

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Data Description and Sources.

| Variable | Description | Source |

| 1. Policy Variable • Weighted Average Call Money Rate (CMR) |

It can be defined as ‘the volume weighted rate of overnight transactions undertaken in the Call money market, i.e., uncollateralized segment of the money market with banks and primary dealers as participants. |

Reserve Bank of India (RBI) |

| 2 Alternative. Monetary Policy Variable • 10-year Government Bond rate (TYB) |

These are rates levied on long-term debt instruments issued by the Central Government and acknowledge the Government’s debt obligation for 10 years. |

Reserve Bank of India (RBI) |

| 4.Exchange Rate Variable • Real Effective Exchange rates • (REER) (Base: 2004–2005)*, 36-currency, trade-based weights |

The Real effective exchange rate (REER) is the weighted average of a nations’ currency in comparison to a basket of other global currencies. |

Reserve Bank of India (RBI) |

| 5. Real Economic Variables • Domestic Output (Index of Industrial Production (IIP) (Base year: 2011–2012) • Inflation (Whole Price Index (WPI)/Consumer Price Index-Combined (CPI-C) WPI:(Base year: 2011–2012)* CPI:(Base year: 2011–2012)* |

The Index of Industrial Production (IIP) depicts the static growth rates for different industry groups of the economy. The WPI measures the price of a representative basket of wholesale goods Consumer Price Indices (CPI) measure changes in the general level of prices of goods and services that both rural and urban households acquire for the purpose of consumption over time. |

Central Statistical Organization (CSO), Ministry of Statistics and Programme Implementation. WPI (Office of Economic Advisor) CPI Ministry of Statistics and Programme Implementation. |

| 6.Foreign Variables • World Oil Price Index (WOPI) • Federal Funds Rate (FFR) |

These are the global prices of crude oil It is the interest rate at which depository institutions trade federal funds on an overnight basis with each other |

Federal Reserve Bank of St. Louis; FRED, Federal Reserve Bank of St. Louis; |