Abstract

This study seeks to explore how enterprise resource planning (ERP) adoption in a manufacturing SME strengthens management accounting and controls, and how ERP-driven changes are sustained to ensure sustainable survival. A single holistic case study design was adopted to explore the ERP adoption process under an extended Burns and Scapens framework and dynamic capabilities as theoretical lenses at ABLT (a manufacturing SME in Pakistan). Fourteen semi-structured interviews, observations and documents were analysed using Gioia’s methodology to surface first-order codes, seven second-order themes and four aggregate dimensions. The findings reveal a multi-stage process. ERP adoption was triggered by the convergence of internal manual frustrations and external customer-driven pressure for traceable information. During implementation, managers negotiated financial, production and technical logics and embedded real-time accounting routines while drawing on existing standard operating procedures to reduce resistance. Once stabilized, these routines enabled team learning that built sensing, seizing and transforming capabilities. Dynamic capabilities, in turn, allowed the firm to reconfigure rapidly when COVID-19 disrupted supply lines, thereby protecting cash flow and accelerating post-crisis growth. A conceptual model shows how institutional alignment and capability building interact recursively rather than sequentially. The study contributes by integrating the extended Burns and Scapens framework with dynamic capabilities theory to understand ERP-driven management accounting and controls in the context of SMEs. For practitioners, the study highlights the significance of aligning customer expectations, internal policies and team learning to turn ERP from a technical project into a platform for ongoing resilience and growth.

Keywords

Introduction

Small and medium-sized enterprises (SMEs) are integral for fuelling economic development and fostering industrial growth and employment. These firms increasingly look to enterprise resource planning (ERP) systems to streamline information flows, improve cost control and support the rapid decision-making process (Alsughayer, 2025; Recchia et al., 2025; Gupta et al., 2017). However, adopting ERP is far from straightforward for SMEs. Limited cash reserves, scarce in-house expertise and the necessity to keep day-to-day operations running leave many SMEs uncertain whether the promised benefits will outweigh the risks (Barbieri et al., 2024; Razzaq & Wali, 2025; Sivaganthan et al., 2025). Previous studies (Alsughayer, 2025; Nguyen et al., 2021; Zotorvie et al., 2025) have asserted that ERP adoption facilitates the management accounting and controls and improves the SMEs’ reporting quality. However, these studies have scantily addressed how ERP becomes part of everyday accounting practices or why some changes endure while others disappear, given the increasing impact of technological advancements (e.g., Ammar et al., 2025; Recchia et al., 2025).

The present study responds to this need in two ways. First, it integrates the extended Burns and Scapens (B&S) framework (Bertz & Quinn, 2022; ter Bogt & Scapens, 2019), which traces how new routines become institutionalized, with the dynamic capabilities theory, which elucidates how firms renew their resources to keep pace with change (Roffia & Dabić, 2024; Teece, 2023). Using both perspectives together allows us to comprehend the complete arc of ERP adoption from the first trigger to sustained use, which earlier research rarely addressed (e.g., Alsughayer, 2025). Second, the research offers an in-depth case from a manufacturing SME in Sialkot, Pakistan. This setting matters because SMEs in this region operate in an export cluster; nonetheless, they face acute resource constraints and customer pressure for traceability and compliance. By situating the analysis in this context, the study provides novel insights into how institutional forces and dynamic capability building interact in an emerging economy like Pakistan, addressing calls for more geographically diverse ERP-related research (e.g., Castillo-Vergara et al., 2025; Zotorvie et al., 2025).

Based on these considerations, the study aims to address the following research questions.

RQ1: How does ERP adoption reshape the management accounting systems in a manufacturing SME from the perspective of the B&S framework?

RQ2: How do dynamic capabilities aid in sustaining ERP-driven accounting transformations?

By addressing these research questions, this study uncovers the process of implementing an ERP system in a Pakistani manufacturing SME and reveals how the system reshapes accounting controls and remains viable over time. This study explains a process view of ERP adoption that blends institutional and capability-based explanations and opens a window onto a setting seldom examined in prior work. In doing so, the research informs both theory and practice by depicting what aids or hinders SMEs when they modernize their accounting systems under resource constraints and institutional pressures.

Theoretical Framework and Literature Review

ERP Adoption in SMEs and Management Accounting and Control Systems

SMEs are relatively disadvantaged regarding the deployment and utilization of technologies in company operations, but recent scholarship has displayed the shift in deploying technological advancements in such firms (Mosbah, 2024; Hossain et al., 2024). In these technology adoption tendencies, ERP has witnessed an upward trajectory in the context of SMEs (Alsughayer, 2025; Gessa et al., 2023). ERP systems have become indispensable for improving organizational operations, integrating different business functions and enhancing decision-making. Diverse scholars (Basu & Jha, 2024; Basu, Dutta & Jha, 2023; Gessa et al., 2023; Haddara et al., 2022) have studied the ERP adoption and associated challenges in SMEs. Larger organizations are more methodical and have less probability of resource constraints. Consequently, ERP technology in larger firms is less challenging than in SMEs (Abazi Chaushi & Chaushi, 2024; Gupta et al., 2017).

SMEs are required to enhance their management information quality via effective management accounting and control systems to thrive in a dynamic environment. Such systems provide relevant information for planning and controlling organizational functions (Malmi & Brown, 2008). A well-adopted ERP system in organizations enhances the information quality of management accounting systems by improving the accuracy, timeliness, readability and availability (Alsughayer, 2025). Spraakman et al. (2018) have also argued that ERP systems enhance and strengthen management accounting information by allowing users to delve into details and disaggregate the financial and non-financial data to facilitate data interpretation in detail. Previous studies have identified some paradoxes regarding ERP’s impact on management accounting and controls. Caglio (2003) and Rom and Rohde (2006) argued that ERP minimally impacts management accounting systems. Conversely, Daoud and Triki (2013) argued that ERP systems support embracing new accounting practices, cost accounting and financial management. More recent research studies (Alsughayer, 2025) converge on the view that carefully configured ERP improves reporting quality, decision-making and the alignment of core processes.

Reflecting this shift, scholars are pivoting their focus to technology-driven transformation in SMEs, including the accounting consequences of ERP adoption (e.g., Alsughayer, 2025; Berisha Dranqolli & Miftari, 2025; Santos et al., 2025). Because SMEs differ markedly from large firms in structure, resources and decision styles, further work is needed to show how ERP strengthens management accounting and controls in these settings. The present study addresses that gap by examining ERP implementation in an SME context and tracing its influence on management accounting and controls.

Extended Burns and Scapens Framework

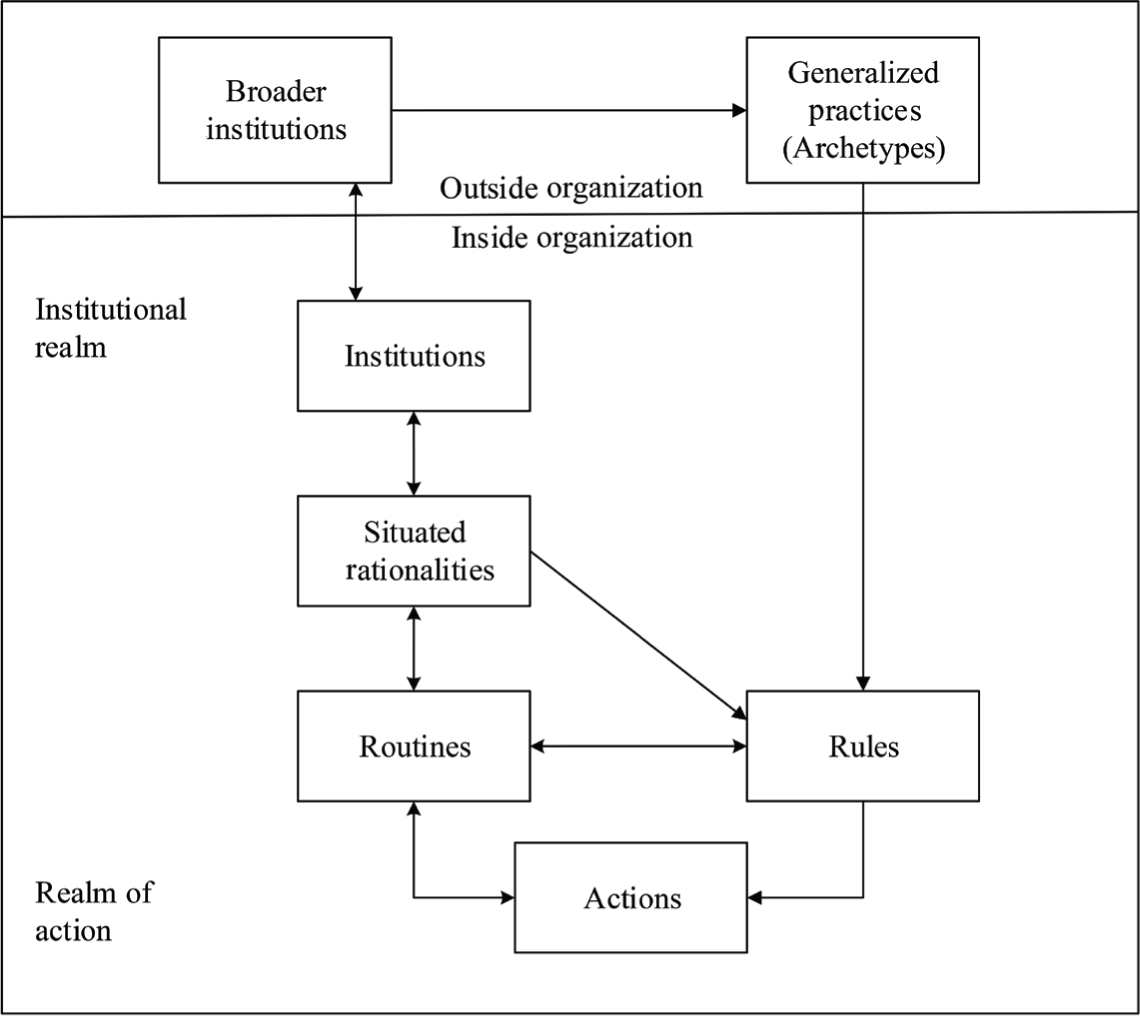

The original Burns and Scapens (2000) framework explains management accounting change by tracing how rules (‘the way things should be done’) and routines (‘the way things are done’) move through four linked processes: encoding, enacting, reproduction and, eventually, institutionalization (Bertz & Quinn, 2022). Change starts when new principles are encoded into rules and routines, usually as modest modifications of what already exists; through repeated enactment, these practices may become taken-for-granted, creating stability unless challenged by new stimuli. Although Burns and Scapens (2000) acknowledge that external institutions can impact this evolutionary flow, their graphic representation focuses on the slow, internal interaction between actions and institutions and gives limited visibility to power, agency or field-level forces (Dillard et al., 2004; van der Steen, 2011). Over the past two decades, scholars have extended particular elements, such as clarifying how routines can be ostensive or performative (Quinn, 2011), distinguishing formal from informal rules (Bertz & Quinn, 2014) and recognizing technologically embedded rules in modern information systems (Oliveira & Quinn, 2015). However, the model’s core linearity remained intact (Bertz & Quinn, 2022).

Ter Bogt and Scapens (2019) updated that model (Figure 1) by weaving in critiques that the original framework underplayed external institutions, individual agency and iterative feedback. Their extended model keeps the foundational loop of rules, routines, actions and institutions yet adds three bridging concepts. First, situated rationality highlights how individuals or groups interpret what is reasonable in a specific context, thereby injecting agency into what was once a primarily structural diagram. Second, they draw a clear line between internal institutions (the organization’s own norms) and broader institutions (field-level logics, regulatory frameworks and professional templates). Double-headed arrows signal that these forces interact recursively, not one-way. Third, the model introduces generalized practices (e.g., industry-wide templates) that act as conduits through which broader institutions influence organizational rules. Power is made explicit: influential actors can impose rules directly by drawing on their situated rationalities, an acknowledgement that leadership choices may disrupt or accelerate the march from encoding to institutionalization. Finally, Figure 1 depicts iterative rather than strictly linear flows, stressing that routines can be regenerated whenever external pressures shift or new coalitions gain influence.

These enhancements are especially pertinent for technology-driven change in SMEs. ERP implementations, for instance, seldom follow a neat, one-off progression; instead, external templates (generalized practices embedded in software), local negotiations over data flows and the agency of owner-managers collide in repeated cycles of adjustment. By making room for situated rationalities and iterative feedback, the extended framework provides a better lens for studying how SMEs embed digital accounting tools under shifting institutional pressures, a gap advocated by recent scholarship (e.g., Ammar et al., 2025). Consequently, the present study leverages this framework by clarifying how ERP-led management accounting and controls can stabilize over time and how customer demands, industry benchmarks and managerial agency can reshape those routines.

Dynamic Capabilities Theory

The dynamic capabilities theory (DCT) is a significant theoretical lens, primarily the extension of the resource-based view theory, considering the dynamism of the external environment. Teece (2023) has asserted that dynamic capabilities are categorized as sensing, seizing and transformation. Sensing refers to identifying opportunities; seizing explains the required steps and actions to take advantage of these opportunities by resource mobilization; and transformation refers to the continued renewal of these resources (Teece, 2016). The association of dynamic capabilities and ERP adoption can be comprehended from the broader context of IT governance. In this regard, research revealed that alignment of information technology can facilitate dynamic capabilities that allow firms to adopt ERP to optimize operational efficiency (e.g., Dan, 2023). Within this spectrum, scholars have studied dynamic capabilities in SMEs in myriad ways. For instance, dynamic capabilities and digital technologies in SMEs (Vo Thai et al., 2024); ERP and MRP adoption in SMEs based on Python (Vitti et al., 2025); and ERP assimilation in SMEs from the dynamic capabilities framework (Zongyuan & Haiyan, 2024). Despite these scholarly reflections, studies that explain ERP adoption and its sustenance from DCT are rare. Recent scholarship (e.g., Castillo-Vergara, 2025) exhibited that SMEs need to leverage their dynamic capabilities to identify technology adoption opportunities and reconfigure their resources. Based on these assertions, it is argued that adopting DCT as a theoretical lens to understand ERP adoption is paramount.

Research Methodology

Research Design: Case Study

To address the research questions of this study, a single holistic case study research design (Yin, 2018) has been employed to explore ERP adoption and its role in management accounting systems in a manufacturing SME. Case study research is advocated to uncover complex and contextualized phenomena because it generates in-depth insights in real-time contexts (Cooper & Morgan, 2008). Based on purposive sampling, which ensures the selection of a case that reflects the subject matter of the study (Bell et al., 2022), data are collected from the manufacturing SME based in Sialkot (a city in Pakistan), which has implemented ERP. This case study focuses on ERP adoption and its role in management accounting and controls, developing dynamic capabilities and sustainable survival.

Context of the Study

AB Labels and Textiles (ABLT) was established as a trading organization in 1992 in labelling and textile-related products due to limited in-house production facilities. For six years, this firm outsourced manufacturing facilities for the production process. However, in 1998, it started manufacturing facilities and installed machinery to produce its textile-related products and labels for other organizations in Sialkot. This was a significant shift from outsourcing to initiating its own manufacturing facility. In 2017, an institutional change occurred in the shape of developing and implementing the ERP system to streamline the operations and strengthen the management accounting and controls. In order to ensure a smooth transition towards ERP adoption, an IT expert was also hired to assist the firm in addressing and aligning technological advancements with the firm’s evolving needs. The transition from manual-based systems towards ERP systems required a shift in organizational routines. Initially, resistance to change was witnessed as employees were accustomed to decentralized decision-making. However, over time, ERP implementation reshaped the accounting practices, formalized the financial reporting process and reinforced compliance.

After implementing ERP, the CEO also sensed the necessity to sustain these ERP-driven changes in his firm. With the active involvement of an IT expert, an accounts manager, a production manager, a managing director and a CEO, they ensured that ERP systems remained aligned with business needs. Employees were hesitant about these transformations, but their habits changed over time. The firm’s ability to sense, respond and reconfigure in management accounting and controls allowed it to develop and maintain its operational continuity after transformations. At the time of the interview, ERP systems were fully embedded in the firm’s management accounting practices and operational structure, exhibiting how organizational routines evolved, institutional changes occurred and resultant capabilities played a critical role in sustaining ERP-driven transformations in this firm.

Data Collection and Analysis

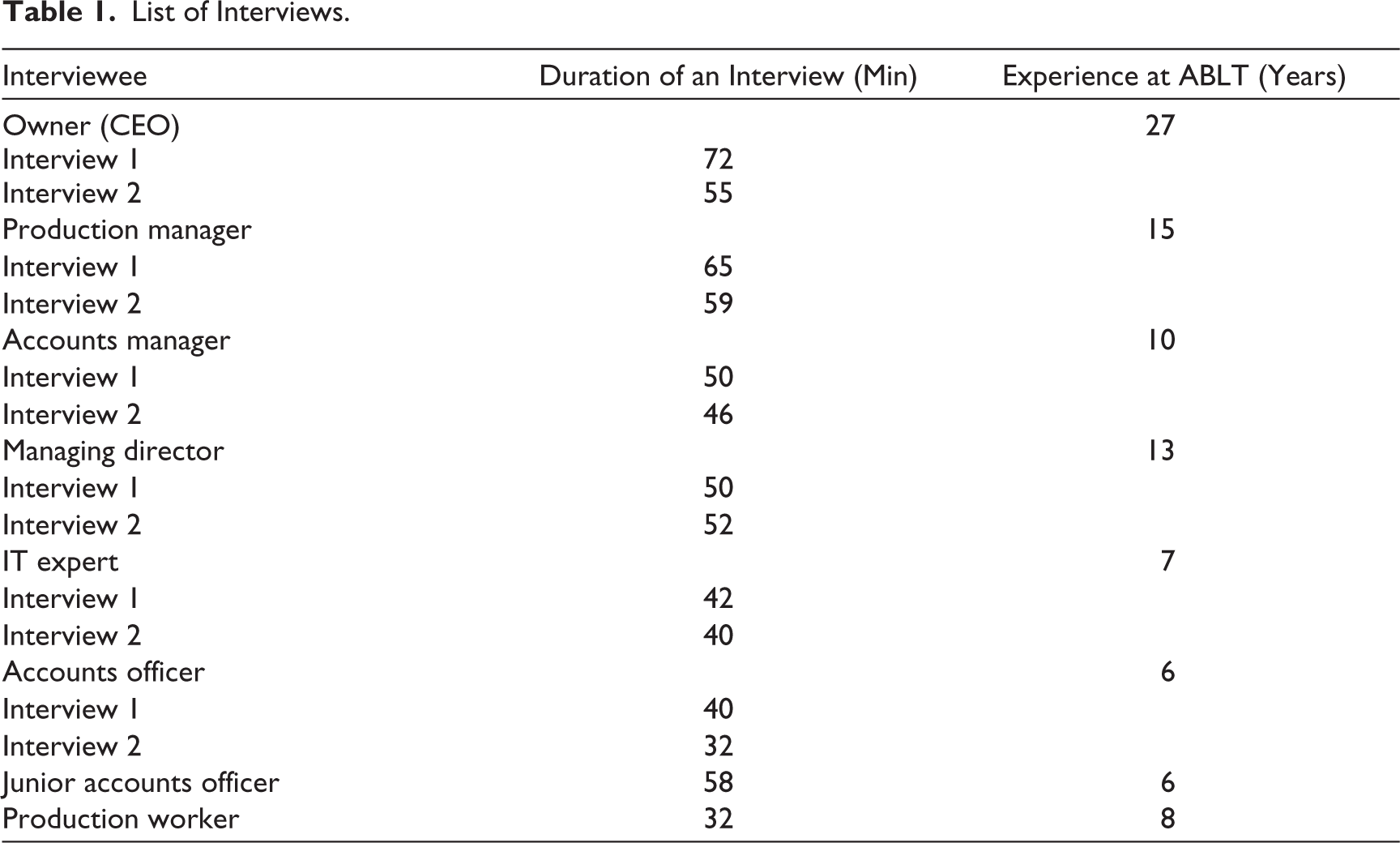

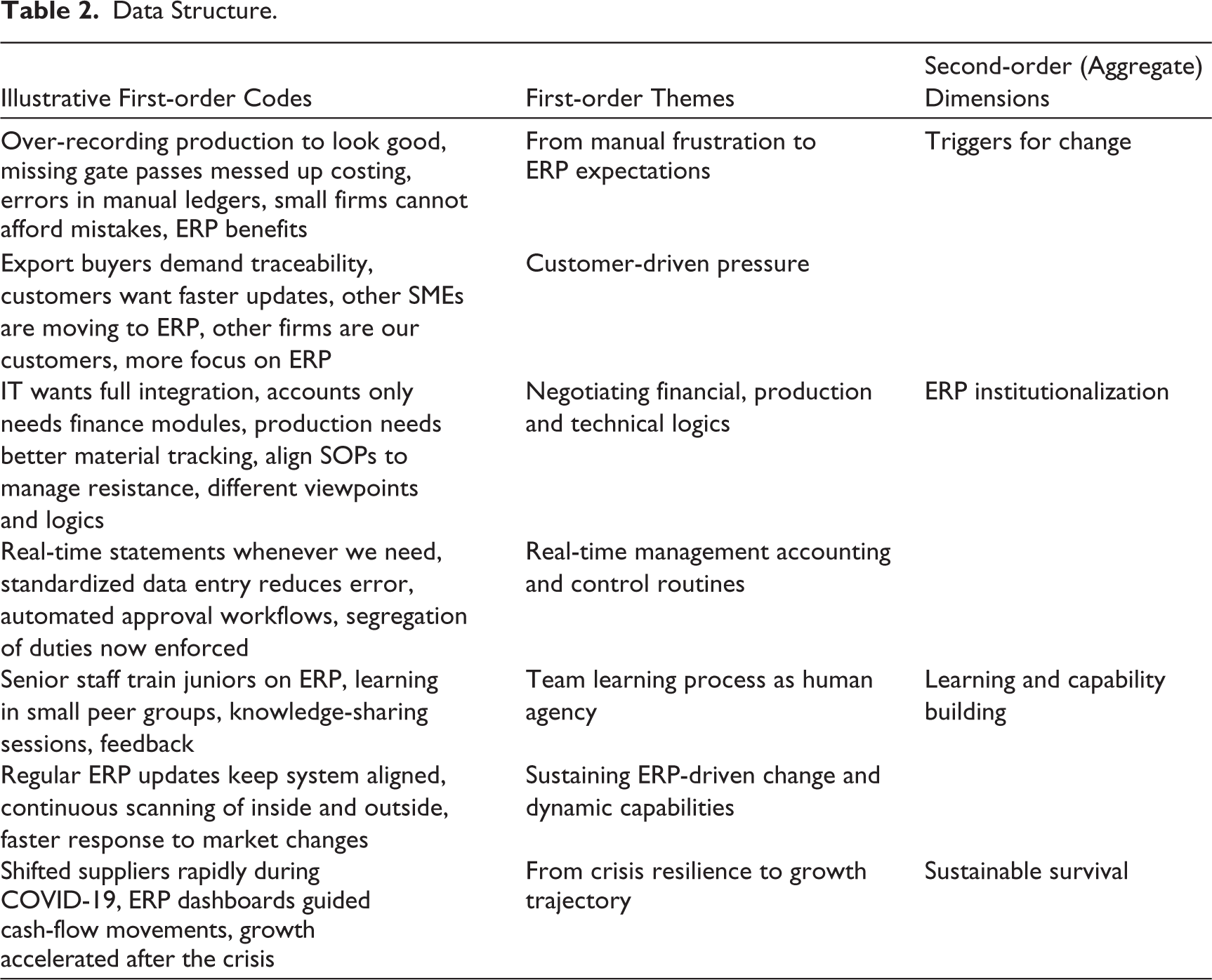

Data were collected from semi-structured interviews with the participants of the case firm. Along with semi-structured interviews, the case firm permitted us to take observations and review some documents relevant to the case context. The organizational actors involved the owner (CEO), accounts manager, accounts officer, IT expert, production manager and managing director (Table 1). A total of 14 interviews were conducted based on the intent of this case study. Before data collection, the objective of the study was clearly articulated to the participants, and prior consent was obtained before the interview. Interview questions were developed based on the interview protocol refinement framework (Castillo-Montoya, 2016). A rigorous qualitative data analysis process was incorporated by following the Gioia methodology guidelines (Gioia et al., 2013). Initially, the entire qualitative data were read and reread to develop familiarity. This qualitative raw data set was codified and treated as the first-order code. Then, conceptually similar codes were clustered into seven first-order themes that surface repeatedly across participants. Finally, by asking ‘what is the phenomenon here?’ in light of the extended B&S framework and DCT, four second-order (aggregate) themes were specified. This three-step progression—codes → first-order themes → second-order dimensions—gives the transparent Gioia data structure (Table 2).

List of Interviews.

Data Structure.

Validity of the Findings

The findings of the study were validated by applying the validation strategy of member checking, which is also referred to as respondent validation. This validation strategy ensures that the research findings accurately mirror the participants’ reflections and perspectives (Creswell & Poth, 2016). Therefore, the findings of this case study were shared with the participants to get their validation. Furthermore, triangulation is another validation strategy that strengthens the findings by triangulating the multiple data sources (Bell et al., 2022). Therefore, interview data were also triangulated from multiple sources, such as observations and some documents.

Findings

Triggers for Change

From Manual Frustration to ERP Expectations

The owner of ABLT was aware of the advantages of management accounting and control systems because he had a formal education in commerce and understood accounting systems better. Earlier, ABLT was involved in manual accounting and controls. However, the owner observed some loopholes in production controls over time. He said, ‘before the ERP system in our firm, sometimes, employees used to over-record production in order to show their performance better’. He further stated, ‘In manual systems, we started facing issues of missing gate passes, which caused a problem in recording material, and due to this, proper material costing was not present’. He also reflected that accounting systems and controls must be strong in SMEs because the probability of the occurrence of problems is higher than in larger firms. ‘I have seen that in small companies like ours, the error chances are high because these companies do not focus on proper controls. Mistakes in small firms cannot be afforded’, he asserted. The accounts manager also stated, ‘in manual recording as this firm practiced, proper accounting controls are not possible’. The managing director also indicated his intentions that the time had come for developing strong accounting and controls, and technology can assist in executing that work. Considering these concerns, the owner called a meeting and decided to adopt and implement a proper ERP system in his firm. These participants’ accounts have revealed that this firm’s upper echelons (e.g., owner, managing director, accounts manager) perceive benefits from ERP adoption due to its ability to strengthen management accounting and controls.

Customer-driven Pressures

The decision to develop the ERP system in ABLT was also reinforced by some broader institutional forces. The customers of this firm were assessed as influential players with a significant impact on the firm’s operations and control systems. ABLT had customers who were also members of many associations (e.g., surgical association, sports association) and had the power to influence. Before 2017, many other SMEs started focusing on transforming their whole financial strategy by developing ERP systems, which was the impact of the industrial shift. However, influential customers also prompted the owner to keep this firm aligned with customers’ preferences. The managing director also seconded this assertion by stating, ‘Customers act as a strong force because our customers are exporters and they also tell their quality requirements which they need to maintain. Due to this, we thought of developing proper ERP systems and quality mechanisms so that earlier production loopholes may be addressed’. This firm’s customers increasingly demanded fast order processing, real-time tracking and enhanced quality. There was the pressure from the customers to bring some technological systems to address these concerns. This pressure was arguably linked to loopholes in the production process and quality and weak material controls before ERP implementation. Therefore, considering these factors, the owner consulted with the production manager, accounts manager and managing director to put effort into ERP adoption.

ERP Institutionalization

Negotiating Financial, Production and Technical Logics

The owner hired an IT expert with experience in ERP implementation in the middle of 2017. He called a meeting with the accounts manager, managing director, IT expert and production manager to discuss the initial implementation process. The implementation of ERP was deeply intertwined with the internal institutions of ABLT. The IT expert voiced, ‘ERP will integrate all the departments and automate the workflow’. The accounts manager argued that they ought to integrate just the modules ABLT requires. He said payroll, taxation, budgeting and costing systems would be the utmost priority, along with strong internal controls to avoid unauthorized access. The production manager underscored, ‘[M]aterial tracking must be efficient as previously, customers demanded fast delivery and in case of delay and quality issues, customers were unhappy’. Arguably, the IT expert voiced the technological rationality, the accounts management was more focused on depicting the financial control rationality and the production manager mirrored the operational rationality. The managing director said, ‘although we faced some disagreements, our working culture is supportive, and anyone can discuss and give a viewpoint …, IT guy wanted full integration whereas accounts manager was more oriented towards finance integration, well I had to listen to all’. In this regard, the owner asserted, ‘before ERP adoption we have developed our internal policies regarding work ethics and now we integrated these policy frameworks in ERP adoption’. The accounts manager said, ‘we had to make sure that standard operating procedures aligned with ERP adoption so that no one could say that this is how we used to things’. The managing director endeavoured to balance these competing arguments between these managers, which was possible due to the supporting working environment and strong internal values (e.g., respecting others’ opinions) of ABLT. The owner also stressed that already established company policies should be reflected in ERP adoption to lessen any potential resistance from employees. In this case, the accounts manager and managing director emphasized robust standard operating procedures must be established to evade resistance.

Real-time Management Accounting and Control Routines

At the end of 2017, ERP was installed in ABLT, and after the ERP adoption, transformations were witnessed in management accounting and control mechanisms. New rules and routines were developed and aligned with ERP systems. These were also institutionalized with structured reinforcement; the accounts manager said, ‘after ERP, we could generate real-time financial statements for analysing the performance at any time’. The accounts officer also reported that standardized data entry was possible after ERP with a minimum likelihood of error. The accounts manager further asserted that ERP adoption streamlined cost management, which also impacted the fair pricing strategies for their customers. After ERP, budgeting took the shape of data-driven budgeting, because due to data generation by ERP, it was possible to develop more robust budgets, as asserted by the accounts manager. The managing director said, ‘[A]utomated approval workflows were introduced for procurement, expense management and resource allocation’. He further asserted that the segregation of duties was enforced in order to enhance the quality of the work. This reflected new transformations in ABLT, and new rules and routines, as elucidated, started evolving in this firm.

Learning and Capability Building

Team Learning Process as Human Agency

ERP adoption in ABLT was not just a technical effort under institutional forces. It also generated the team learning process as a human agency or action. In 2018, efforts were made to institutionalize the adoption of ERP. Despite the initial training and learning workshops for ERP adoption, the owner started focusing on developing more robust knowledge-sharing sessions. He asserted, ‘After ERP, I advised senior staff to also provide training related to ERP to junior staff as well’. One of the junior staff members in the accounting department asserted, ‘I was appointed as a junior account assistant; earlier I just used Microsoft Excel, now accounts manager and other seniors have really assisted me in learning ERP purchases module, and now I am confident that I can use it well’. The accounts manager, production manager, owner and managing director operated as a top-tier team, and learning from each other was observable. Even during the product development phase, the owner and staff collaborated to discuss customers’ design needs, which they sent via WhatsApp. During a visit to a factory, it was observed that employees were present in small groups to execute various tasks, including manufacturing, updating records on paperwork and continuous conversation between group members. One of the production workers indicated that they just need to update the system daily, and for this, they had also received a training session. These reflections were at the end of 2018, signifying that the team learning process started developing after ERP implementation, and the learning culture was enhanced.

Sustaining ERP-driven Change and Dynamic Capabilities

ERP adoption was completed at the end of 2018 and became integral to ABLT. ERP enabled ABLT to integrate financial and operational data, improving real-time decision-making. The reflection was that at the end of 2018 and the start of 2019, ABLT strengthened their management accounting and controls. The owner asserted, ‘At the start of 2019, we as a team were more efficient in making decisions after ERP, and it was a meaningful change, and I want to sustain these changes in the long run’. The managing director also indicated that even after ERP, they did not just focus on learning and training at that time; rather, they started thinking about continuing this process. IT experts asserted that regular updates may be necessary for ERP to work efficiently and remain aligned with ABLT’s evolving needs. The accounts manager also stated that to sustain in the long run, we must continuously analyse inside and outside the ABLT for better future strategic planning. Admittedly, this firm’s sensing, seizing and reconfiguring capabilities were developed due to ERP’s ability to strengthen management accounting and controls. The owner further stated that at the end of 2019, they were in a better position to respond fast to market developments and were better positioned to capitalize on possibilities based on their relationships with customers and suppliers. For example, they had an old machine for generating labels, but the owner came to know an enhanced version of the old machine by discussing it with some customers and suppliers. The owner asserted,

Yes, we upgraded our manufacturing capacity by acquiring a new variant of older machinery. In addition, I informed my clients that, as a result of the improved version, my company could manufacture more products of a high standard. I also spoke with the managing director and the accountant. After consultation, we agreed to purchase.

Sustainable Survival

From Crisis Resilience to Growth Trajectory

At the end of 2019, the eruption of COVID-19 harmed businesses worldwide, but ABLT sustained in that period. As argued earlier, ABLT developed its dynamic capabilities due to ERP-led management accounting and controls. It assisted this firm in sustaining the whole COVID-19 disruption. In the initial days of COVID-19, the production manager convened a meeting with the owner to build an agile and resilient supply chain to survive the market disruption due to the lockdown. The owner said, ‘We made our strategy to quickly shift and identify the alternative options for addressing any potential disruptions’. They quickly enhanced their supplier network so that supply could not be affected. The accounts manager said, ‘Through ERP, we optimized our cashflows and were able to do real-time budgeting based on disruptions in the market at that time’. They ensured their stock levels in order to ensure the cost. This happened very fast when uncertainty prevailed at the time of COVID-19. Due to these measures, ABLT was able to survive during COVID-19. Now, it has achieved sustained survival and is continuously working to ensure it. As described by the managing director, ‘[W]e are now more sustainable, and our company’s growth has accelerated significantly. We strive to reduce unproductive activities in order to reduce costs’. He further added, ‘Our ERP system has enabled us to better judge inside and outside the firm. Based upon reports, we analyse different risks more comprehensively and develop our strategy to be financially stable’. Arguably, ERP led to strengthening the management accounting and controls, which enhanced their dynamic capabilities. Ultimately, they were on a survival trajectory and sustained even during COVID-19.

Proposed Conceptual Framework

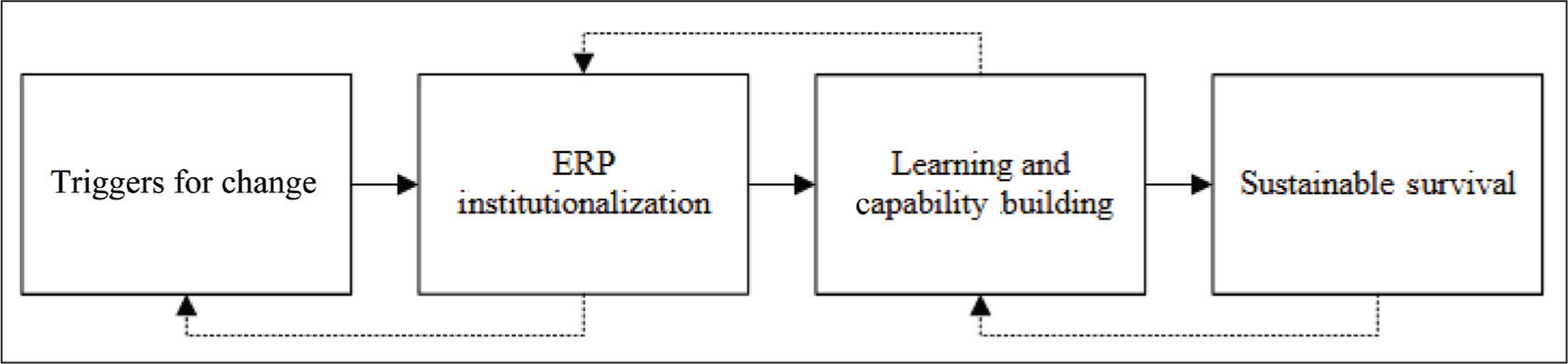

Figure 2 portrays an iterative pathway that mirrors the extended B&S framework (ter Bogt & Scapens, 2019) while linking to dynamic-capability ideas. The process starts with triggers for change. Here, broader institutions, export customers demanding traceability and field-level ‘best practice’ talks about ERP, collide with internal institutions. These dual pressures disturb taken-for-granted routines and supply the situated rationalities that make managers consider ERP a reasonable next step. The second step is ERP institutionalization, which captures the core of the extended model: rules and routines are negotiated in light of both power relations and generalized practices embedded in the software. Accounts staff insist on segregating duties; the production manager wants faster material tracking, and the owner and managing director draw on existing SOPs to mediate. The new digital rules are reproduced through repeated enactment, shifting from ‘project’ to organizational habit. Once routines stabilize, learning and capability building become visible. In the extended B&S view, human agency does not disappear after institutionalization; rather, people continue to interpret and occasionally adjust routines. Peer-to-peer coaching, dashboard experimentation and periodic system updates illustrate this micro-agency at work. These actions also map onto dynamic-capability processes—sensing new information, seizing it through collective learning and transforming workflows when needed. Finally, sustainable survival exhibits what happens when institutional alignment and capability building reinforce each other. During the COVID-19 outbreak, the firm’s digital controls and team learning culture enabled rapid supplier reconfiguration and cash-flow pivots, demonstrating that embedded rules can be a catalyst, not a constraint, for agility. Finally, the dotted arrows reflect the feedback loops in the proposed conceptual framework. Once sustainable survival is achieved, the firm’s success can elevate customer expectations and industry benchmarks, feeding new triggers for change. At the same time, experience gained during crises prompts managers to revisit and fine-tune the rules embedded during ERP institutionalization, ensuring the system stays aligned with evolving conditions. Thus, performance outcomes continually refresh the external pressures that spark change and the internal routines that stabilize it.

Conceptual Framework.

Discussion

This case study research aims to explore how ERP adoption strengthens the management accounting and controls at ABLT (the case firm) and how ERP-driven transformations are sustained due to dynamic capabilities. The findings have indicated that change was triggered by a double prompt. First, managers were frustrated with error-prone manual records and feared the high probability of problems in small firms that lack robust controls. Second, export-oriented customers demanded faster, traceable information, reinforcing the owner’s perception that ERP had become an industry practice among peer firms. This combination of internal weaknesses in manual accounting mechanism and external institutional pressure enlarges our understanding of the extended B&S framework (Bertz & Quinn, 2022; ter Bogt & Scapens, 2019): the case illustrates that routines are questioned not only when old practices fail internally but also when outside actors redefine what counts as legitimate accounting practice. For theory, the study therefore nuances the notion of situated rationality by showing that decision makers weigh inside inefficiencies and outside expectations simultaneously, which is scantly addressed in the prior literature (e.g., Jackson & Allen, 2024). Practically, the finding alerts SME owners that early dialogue with key customers can turn external pressure into a road map for digital investment.

Once the decision to adopt ERP was made, the implementation phase revealed how multiple rationalities (e.g., financial control, production efficiency and technical integration) drew the project in different directions. Quotes from the IT expert, accounts manager and production manager indicate how each endorsed his priorities, while the managing director listened to all and aligned the firm’s existing standard operating procedures with the new system. By formalizing a policy framework in advance, the firm shaped what Malhotra et al. (2025) call a framing mechanism that reduces resistance by embedding changes in familiar routines. This extends the B&S lens by demonstrating that rules can be strategically repurposed during the enacting stage to placate competing rationalities—an insight also relevant to recent debates on addressing resistance to change in organizational settings (Malhotra et al., 2021). For practitioners, the message is clear: codifying work ethics and controls before digital rollout shortens the social learning curve and lowers the hidden costs of conflict.

The findings further demonstrate how new real-time accounting routines emerged. Staff highlighted automated approval workflows, standardized data entry and real-time financial statements as the most evident outcomes. These narratives align with the evidence that ERP enhances information quality and financial discipline (Halimuzzaman & Sharma, 2024). However, the case adds two refinements. First, digital workflows locked segregation-of-duty rules into daily practice, illustrating how technology supports and accelerates the institutionalization loop in an extended B&S model. Second, automated reports allowed the SME to move from simple budgeting to data-driven budgeting and cost management, echoing findings that ERP can foster management accounting and controls development in innovative ways in small firms (e.g., Roffia & Dabić, 2024; Weerasekara & Gooneratne, 2023). Theoretically, the study intrinsically proposes that ERP can act as a routinizing technology—it not only digitizes existing tasks but also crystallizes latent rules into non-negotiable system parameters. Managers contemplating ERP should therefore audit and refine their control rules before implementation; revision becomes harder and costlier once embedded.

A distinctive contribution lies in uncovering the team learning process that began soon after implementation. Senior employees trained junior staff, and informal peer groups exchanged tips on data entry and problem solving. This collective learning turned ERP from a technical artefact into a shared cognitive frame, illustrating that human agency remains vital after technological change appears complete. The finding supports the assertions of Turulja et al. (2024) and further explicates that peer-to-peer learning provides the seizing mechanism in DCT: it converts new information flows into actionable knowledge. SMEs with limited formal training budgets can replicate this low-cost strategy to keep skill levels current as systems evolve.

This case study also clarifies how dynamic capabilities sustain ERP-driven transformations. Post-implementation, managers monitored both internal metrics and external signals, upgraded machinery when customer specifications changed and updated ERP modules to fit new workflows. These actions embody Teece’s (2016) sensing–seizing–transforming cycle and validate calls to link information systems with capability development (Mishra & Kiran, 2025). During the COVID-19 outbreak, the firm re-optimized cash flows and diversified suppliers within days, crediting ERP dashboards for rapid scenario analysis. This supports evidence that integrated data systems improve supply-chain resilience (Sadeghi et al., 2025) and argues by showing how accounting information specifically fuels adaptive moves in crisis. This study therefore advances the scholarship regarding the joint role (e.g., Gupta et al., 2020) of institutional theory in the shape of an extended B&F framework (Ammar et al., 2025) and dynamic capabilities in SME digitalization (Castillo-Vergara et al., 2025; Vial, 2021).

Taken together, this case study has significant theoretical contributions in four ways. First, by delineating the whole pathway from manual frustration to growth resurgence, the study integrates the extended B&S framework with DCT and demonstrates that institutional alignment and capability building are mutually reinforcing rather than sequential. Second, it also reflects on policy-enabled institutionalization, showing that pre-existing control rules can serve as a social support for technology adoption (e.g., ERP), thus enriching the team learning process as an agency dimension in an extended B&S framework. Third, it positions accounting data as a micro-foundation of dynamic capabilities, a connection not widely addressed in the SME context. Finally, a conceptual model is proposed based on the theoretical underpinnings of an extended B&S framework and DCT, which distils these insights into a single process view (Figure 2). From a practical standpoint, this study suggests that SMEs need to focus on their strategic alignment for ERP adoption under the intricacy of institutions outside and inside the organizations. These firms must focus on addressing competing rationalities in the ERP adoption process and the collaborative team learning mechanism. Furthermore, SMEs can develop their crisis preparedness due to ERP adoption, as it generates the dynamic capabilities integral to maintaining sustainable survival.

Conclusion

In conclusion, this case study research has explored the process of ERP adoption in ABLT, a manufacturing SME based in Sialkot, Pakistan, which has transformed and strengthened the management accounting and control environment in this firm. The findings answer the research questions. RQ1 is related to how ERP adoption reshaped the management-accounting system. ERP digitized core ledgers, automated approval workflows and enforced segregation of duties, turning previously informal routines into real-time controls that managers could query at any moment. These features embedded the rules and routines described by the extended B&S framework, giving the firm a more transparent and auditable accounting backbone. RQ2 related to how dynamic capabilities helped sustain those changes. The SME developed sensing capability by monitoring customer demands and industry moves, seizing capability through peer-to-peer learning that converted new data into insight and transforming capability by reconfiguring processes and suppliers, most visibly during the COVID-19 outbreak, thereby validating the arguments proposed by Teece (2016). Three core insights emerge. First, internal frustration with manual errors and external pressure for traceability can combine to accelerate digital adoption. Second, codifying existing policies before implementation reduces resistance and supports the institutionalization process. Third, low-cost peer learning keeps system knowledge current and underpins continuous adaptation. Together, these insights demonstrate that institutional alignment and capability building work best when pursued in tandem, not in sequence.

This study has certain limitations, which provide opportunities for extending this research. This research is focused on a single case study; future researchers can incorporate multiple case study designs. Moreover, this research emphasized ERP adoption, whereas future studies can focus on adopting emerging technologies to explore their impact further. Finally, service-based SMEs are encouraged to be included as a sample in future studies. Even with these limitations, the case demonstrates that small firms can turn an ERP system into a durable platform for control and resilience when they align external expectations, internal rules and learning processes from the outset.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.