Abstract

This study aimed to examine the factors influencing presumptive tax collection in Zimbabwe. An interpretivist paradigm was adopted in this study using a qualitative research approach. Primary data were collected through virtual (online) in-depth interviews with 20 participants drawn from the Zimbabwe Revenue Authority, Civic Societies, Parliament of Zimbabwe, Informal Sector Associations and academics. Qualitative data were analysed using thematic analysis. The results of a qualitative analysis of the factors influencing presumptive tax collection in Zimbabwe show that institutional, legal and regulatory frameworks as well as governance and political factors significantly contribute to presumptive tax collection in Zimbabwe. The findings of this study will help ZIMRA and policymakers formulate policy strategies to promote presumptive tax collection and voluntary tax compliance in Zimbabwe.

Introduction

Empirical evidence indicates that the taxation of the informal economy is a major common obstacle in developing countries (Kundt, 2017; Nording, 2017; Tusubira, 2018) due to the unfettered nature of this economic sphere. The literature maintains that worldwide, tax authorities are grappling with managing the informal economy and strengthening tax systems (Vinnychuk & Ziukov, 2013). According to the literature reviewed, tax regulators in developing countries are focused on existing formal operators who are progressing to socio-economic progress and who are neglecting a potential revenue source (informal economy) (Chen, 2012). Mukherjee and Rao (2019) found that tax authorities are concentrating on taxing the formal economy because it is difficult to identify, locate and register participants in the informal economy.

Heggstad et al. (2011) and others argue that in an economic sense, tax authorities collect more tax revenue from the formal economy than from taxing the multitude of poor people who are struggling for survival. They advocate that, from a much broader nation-building lens, expanding the tax base is vital for concrete psychological fiscal contracts. It is further revealed that governments increase their tax revenue through the taxation of the informal economy, although the revenue yield is very insignificant (Fjeldstad, 2013; Mpapale, 2014). This is because the unstructured and unregulated nature of this economic sphere makes establishing and controlling informal economic activities burdensome.

Furthermore, the informal economy is associated with non-static business activities (mobility) (Heggstad et al., 2011), which makes it difficult to tax according to Mpapale (2014). Boakye (2011) viewed informal economy operators as highly mobile, dispersed everywhere and operating at night, which makes them more difficult for tax authorities to identify. Another challenge noted in the literature is that of capacity. Many tax collection agencies are bedevilled by capacity constraints in terms of competent human resources (Mpapale, 2014).

There are conflicting viewpoints regarding the profitability of the informal economy (Chen, 2012). Some scholars believe that the informal economy generates very low revenue, and most of them earn far less than the datum line, while others are convinced that the upper tier of the informal economy is more profitable than well-established enterprises (Kristoffersen, 2011; Mpapale, 2014). If the first viewpoint is considered, then it would be a mere waste of time and resources to try to tax this varsity nonprofitable economic segment (OECD, 2012; Udoh, 2015).

Furthermore, detecting unreported income and activities will not guarantee compliance in the future (Mpapale, 2014). Economically, it makes no sense to invest a large amount of resources in moderately small tax revenue (OECD, 2024). The extant literature shows that most of the income generated in the informal economy is far below the taxable threshold, which is why this sphere has always been ignored. However, the OECD (2020) suggested that collective tax amounts from the informal economy are substantial and, hence, constitute the taxation of the sector. To ensure the reduction of this sector, there is a need to design a tax system that discourages people from moving into the informal economy (Loayza, 2016, 2018).

Francis (2019) observes that harsh tax enforcement and corruption, coupled with poor infrastructure and other services, are barriers to effectively collecting taxes from the informal economy. Corruption creates an environment for tax evasion and avoidance (Utamire et al., 2013). It is also very difficult to identify and monitor revenue-productive targets from multiple activities within this economic sphere (OECD, 2024).

Various authors have presented different factors that make it difficult for tax authorities to collect taxes from the informal economy, such as the use of cash transactions, lack of proper records, level of illiteracy and political considerations (Seidu et al., 2015; Udoh, 2015). A lack of taxpayer information is considered to be a contributing factor to the taxation of the informal economy. Dube (2014) acknowledges that for any tax system to be effective, there must be information. Without information, identifying potential taxpayers and assessing their tax obligations will be difficult.

In Zimbabwe, the challenge of taxing the informal economy is the lack of information on the informal economy (Utamire et al., 2013). As a result, ZIMRA is chasing a few visible and easy-to-trace operators in the informal economy (Dube, 2014). Studies on the taxation of the informal economy in Zimbabwe have concluded that ZIMRA lacks interagency collaboration linkages with informal economy associations such as the Zimbabwe Chamber of the Informal Economy Associations, the Zimbabwe Informal Commuter Omnibus Organisation and the Informal Commuter Omnibus Association of Zimbabwe (Dube, 2014). He recommends that ZIMRA engage informal economy associations in policy dialogue to build a culture of sustainable tax compliance within the informal economy. However, from the literature, it appears that there is no solid research that provides a qualitative analysis of the factors that influence the presumptive tax; thus, this article is aimed at determining the factors influencing presumptive tax collection from a stakeholder’s viewpoint in Zimbabwe.

Background

Presumptive Tax System

The presumptive tax system, which involves collecting taxes from the informal economy, does not provide a summary of different taxes collected from different informal economic activities (Makochekanwa, 2020). All the taxes collected from various informal activities are put in one pool, namely, “presumptive taxes” (Dube, 2014). This means that there is a lack of essential information for comparison purposes, and this lack of information will lead to the misappropriation of funds because of the absence of taxpayer information. Tax authorities implemented the presumptive tax system due to a lack of ‘costless information for one of the parties’ (Yitzhaki, 2007). To cover a wider range of informal economies, Zimbabwe implemented a presumptive tax system for several categories of the informal economy (Sebele-Mpofu, 2020).

According to section 36C of the Income Tax Act (23:06), the presumptive tax is:

(1) For the benefit of Consolidated Revenue, Zimbabwe should be charged, levied and collected throughout the country in accordance with the Twenty-Sixth Schedule and at the rate from time to time in the charging Act, a tax on the basis of the presumed income (commonly known as a “presumptive tax”) of those persons engaging in any of the trades, occupations or undertakings specified in the Twenty-Sixth Schedule.

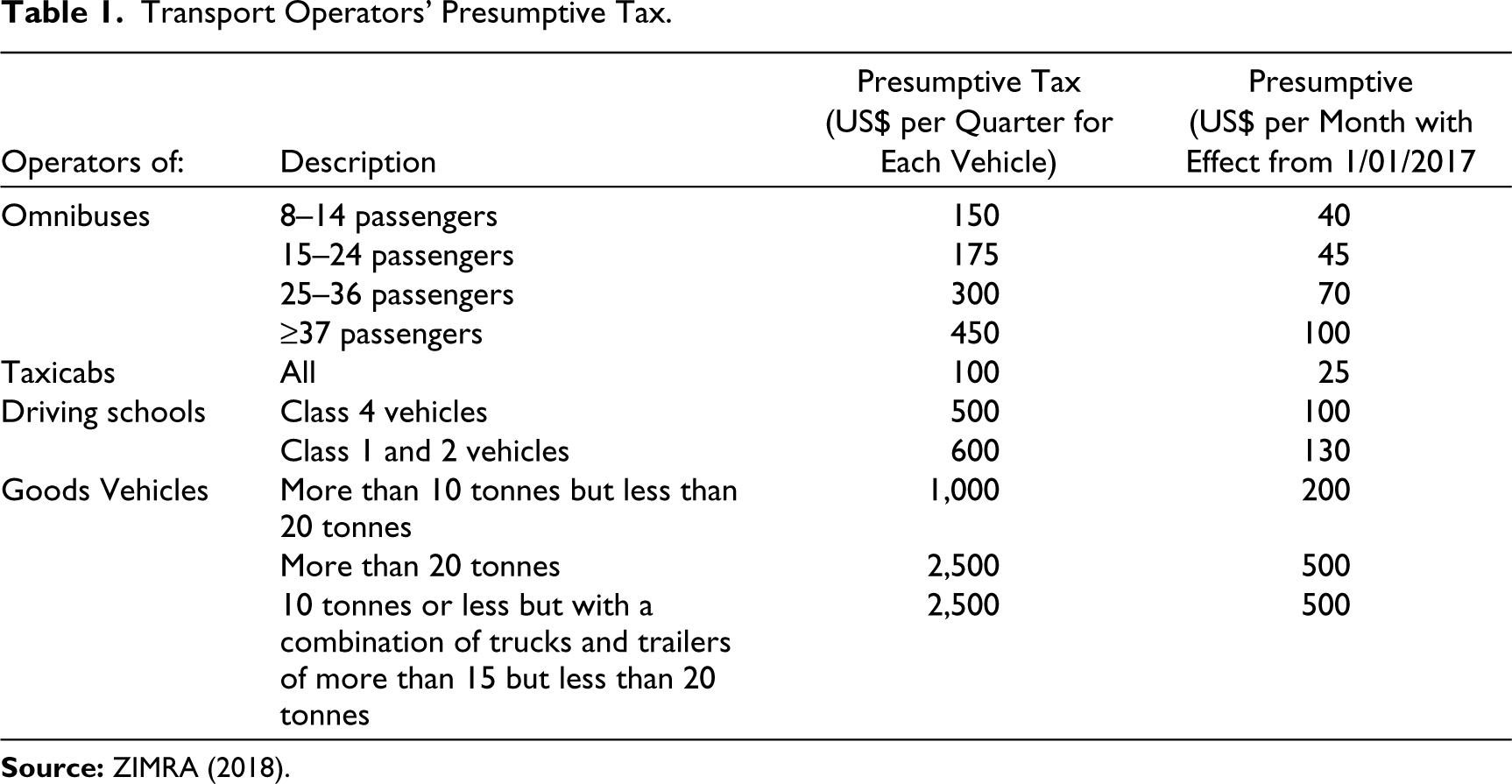

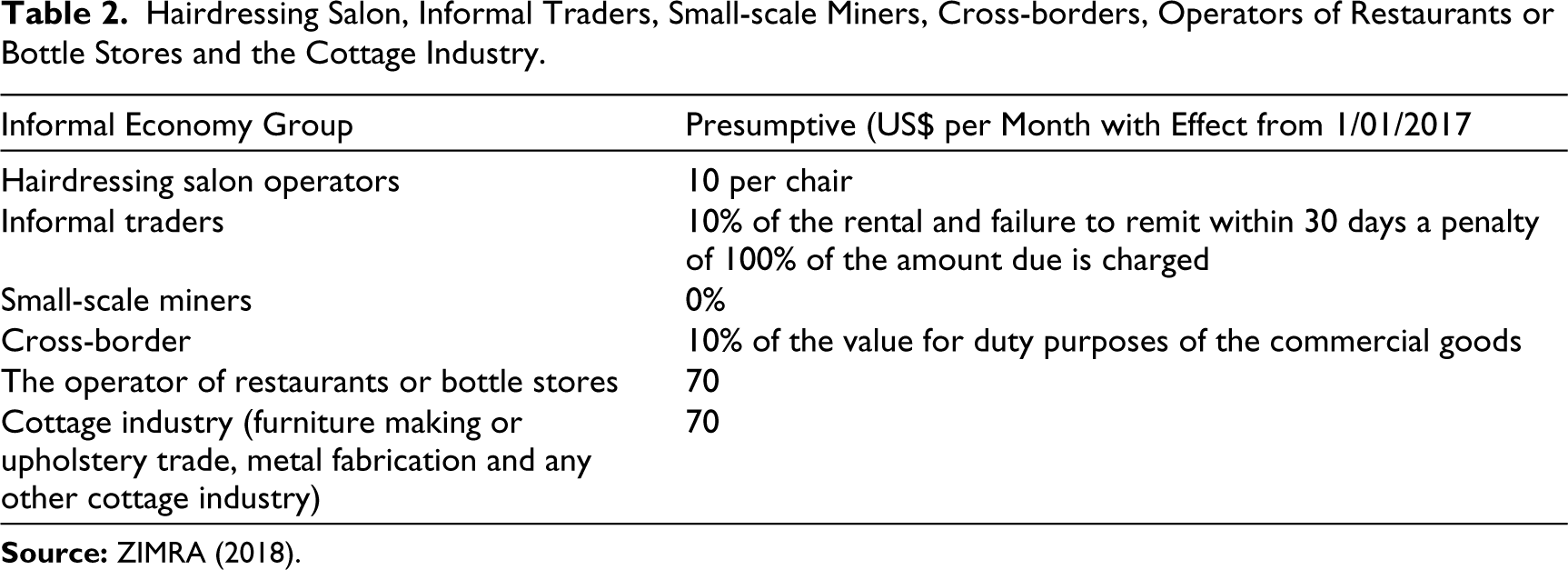

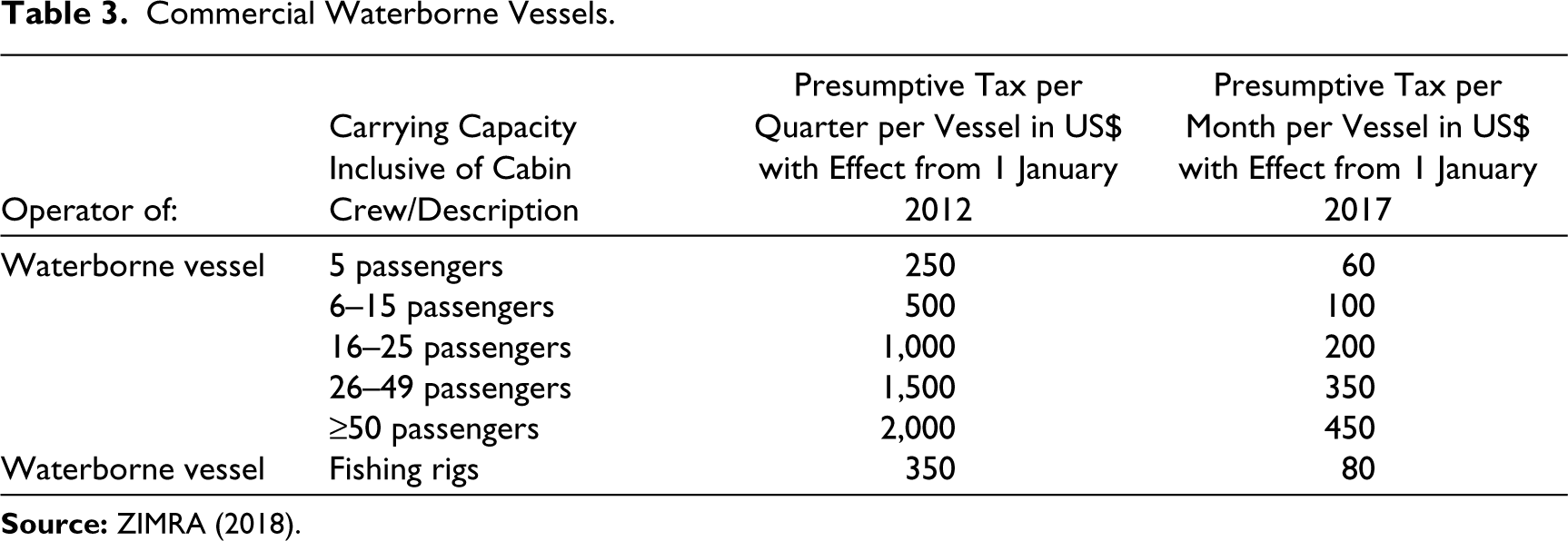

According to section 36C of the Income Tax Act, the presumptive tax system is available to the following operators: informal traders, taxicabs, omnibuses, driving schools, hairdressing salons, restaurants or bottle stores, small-scale cottage industry miners, cross-border traders, restaurant operators, the cottage industry and commercial waterborne vessels (Income Tax Act, 23:06; ZIMCODD, 2014; ZIMRA, 2018). The 26th Schedule (section 36C of the Income Tax Act (23:06)) clearly provided interpretations of the various operators that qualify for the presumptive tax system, the tax liability to be paid and the penalty for nonpayment thereof. Tables 1, 2 and 3 show the original 2005 presumptive tax table and the revised 2017.

Transport Operators’ Presumptive Tax.

Hairdressing Salon, Informal Traders, Small-scale Miners, Cross-borders, Operators of Restaurants or Bottle Stores and the Cottage Industry.

Commercial Waterborne Vessels.

Contemporary literature indicates that ZIMRA has experienced many challenges in taxing the informal economy due to a lack of taxpayer profiles and constitutional legal structures related to disarray and political involvement (AFRODAD, 2011; ZIMCODD, 2014). To date, accurate data on informal economy contributions to tax revenue are scarce (Bachas et al., 2020).

Tax officials worldwide face major challenges in taxing the informal economy (IMF, 1996). Such challenges include complexity (in terms of rules and tax bases), tax uncertainty, scope (too wide or narrow) and lack of data and analysis (Aditya, 2020; Bucci, 2020; OECD, 2024).

It is prudent that revenue authorities should be familiar with these challenges when designing informal tax policies (OECD, 2020). In sum, Fjeldstad (2013) and TRA (2010) inform tax authorities that the challenges associated with the taxation of the informal economy should be examined from a compliance perspective. There are drivers of tax compliance and tax law applicable to both informal and formal economies (Fjeldstad, 2013). In other words, the literature identifies three areas that influence taxpayer behaviour: tax policy, tax administration and another variable that is independent of the tax system (Fjeldstad, 2013; ZIMRA, 2016).

Research Design

While prior studies on taxation in informal economies have applied quantitative methods and very little attention has been given to stakeholders’ perceptions of the determinants of presumptive taxes, a gap in the literature has been identified. This article adopted qualitative research and exploratory research design to understand the factors that affect the collection of presumptive taxes in Zimbabwe. The qualitative research approach attempts to gather nonnumerical data in the form of observations (recorded in a language) or written information (documentary). Qualitative data are analysed by grouping them into different subthemes (thematic analysis) (Braun & Clarke, 2021). In other words, qualitative research is said to be all-inclusive (holistic), unstructured, real (natural) and inductive. This approach provides insight and understanding of the phenomenon and provides room for data triangulation (Hussain, 2015). In this study, the population comprises technocrats at the senior management level in an array of stakeholder bodies, comprising employees or officials drawn from the Zimbabwe Revenue Authority (A), Civic Societies (D), Parliament of Zimbabwe (E), Informal Sector Associations (F) and academics (G) seeking their views of the current informal economy tax framework to establish the factors leading to poor revenue performance from the informal economy. The participants were purposefully chosen based on their knowledge and experience of tax policy as well as informal economy issues. A total of 30 participants were interviewed in this research study. The rationale for selecting 30 participants in this study is that it is in line with the guidelines for qualitative samples (15–30) suggested by Guest et al. (2020). The researchers assumed that interviewing 30 participants would enable the researcher to reach a saturation level—a key ingredient in qualitative research (Mason, 2010). This allowed the researchers to ‘manage complexity of the analytic task’ (Vasileiou et al., 2018, p. 2). The interviews of 20 participants revealed diverse opinions, and all significant issues were identified (Vasileiou et al., 2018). Studies show that beyond this sample size, the researcher believes that the new data to be collected will add little or nothing to the issue under study (Baker & Edwards, 2012).

Data Collection

The study collected data from both primary and secondary sources. As the focus of the study is on understanding the contemporary tax framework in Zimbabwe, it requires the use of secondary data, whereas its interface with respondents representing varying stakeholders’ perceptions, opinions and emotions regarding informal economy taxation in relation to tax digitalization necessitates the use of primary data (Saunders et al., 2018).

Primary data were collected through online interviews to elicit detailed information on the factors influencing presumptive tax collection in Zimbabwe. First, an interview guideline was developed based on documentary analysis of the key variables of the topic. Policy documents, official reports and other publicly available documents were examined to guide the sampling procedure, structure interview questions, and clarify any discrepancies that may be found in the data (Saleheem, 2013). To understand the underlying issues that restrict ZIMRA from effectively collecting presumptive taxes from informal economies, unstructured interviews with relevant stakeholders are integral to the success of this research. The interviews serve as a reliable source of data about (a) the operation of the informal economy, (b) the tax system in the context of a digitalized economy and (c) the payment cycle in a digitalized economy. The data collection process lasted approximately two months and was conducted between December and January 2021. No translators will be used, given the researcher’s proficiency in both English and Shona. All the interviews were handwritten and transcribed.

An in-depth literature review was used as a secondary source of data. A literature review involves the collection of data through the perusal of publicly available documents, such as government circulars, press statements, magazines, media reports, journals and government publications. Document analysis enabled the researcher to understand the contemporary informal economy tax framework, identify the participants and gain knowledge of the phenomenon in the digital era. Document analysis was used in conjunction with interviews as a means of triangulation to provide ‘a confluence of evidence that breeds credibility’ (Bowen, 2009, p. 28).

To reduce potential bias, the researchers combined the findings from interviews and documentary reviews. This study examined the Income Tax Act, digitalization policy documents, the Finance Act, presumptive tax regulations, press statements, treasury handouts and other peer-reviewed journal articles. It is important to note that the analysis of documents is essential for the topic in question.

Data Analysis

Thematic analysis is a process of classifying (data reduction), scrutinizing (data display) and reporting (interpretation) themes within the collected data (Bryman, 2016). The thematic analysis comprises more than one stage, namely, the first stage being the first-level codes followed by the codes of themes and, last, the creation of subthemes (Clarke & Braun, 2017). Thematic data analysis follows numerous stages but not in a standardized procedure: data familiarization, data coding, theme search and discovery and theme review (Cropley, 2019). Saunders et al. (2016) and Hussain (2015) posit that the aim of thematic analysis is to identify themes that occur through the data set. Research studies show that thematic analysis is a ‘foundational method for qualitative data’ (Saunders et al., 2019).

The analysis began with data familiarization by researchers. The transcripts from the interviews were examined in depth to gain an understanding of the content. This was followed by a coding process. The researchers systematically identified interesting patterns in the data. The researchers labelled segments of the data with short, descriptive codes that capture key ideas, concepts or themes. The researchers searched for broader patterns or themes that emerged across the codes. The authors moderated (or reviewed) and refined the identified themes to ensure that each theme was coherent, internally consistent and relevant to the research objectives. The researchers then clearly define each theme and assign a descriptive name that describes its essence. Three distinct themes emerged from the analysis:

Theme A: Institutional factors Theme A: Governance factors and Theme C: Legal and regulatory framework.

Findings

Theme A: Institutional/Administrative Factors

This section focuses on examining whether institutional factors affect presumptive tax revenue collection in Zimbabwe. Three subthemes emerged from this main theme:

institutional capacity financial capacity factors commitment and support.

These subthemes are examined separately below.

Subtheme: Institutional Capacity

Institutional capacity factors were mentioned by participants as determinants of presumptive tax compliance in Zimbabwe. Participant D3 argued:

The revenue collection system in Zimbabwe was affected by many institutional glitches related to institutional discord, politicisation and lack of transparency. The governance of revenue collection requires skilled manpower, government support and strong rule of law. The revenue mobilisation of ZIMRA is often constrained by a lack of agreed upon procedures, corruption and other illicit activities.

The above response is the reason for the failure of ZIMRA to execute and discharge its duties. However, the issue is that the visibility of these challenges makes it difficult to effectively harness tax revenue from the informal economy, as demonstrated in the first part of the statement. The influence of politicians and government support is needed to empower ZIMRA to effectively carry out its mandate. One of these participants, Participant A4, said:

ZIMRA is currently recruiting and training its workers to ensure revenue collection from the informal economy. However, the tax authority remains understaffed due to the limited resources available to employ and train many workers for revenue collection from the informal economy. The informal economy is diverse and is everywhere.

Participant G5 was in unison with Participant A2, who mentioned:

Another visible challenge faced by ZIMRA is the lack of revenue officers for placement in various corners and political regions of Zimbabwe. This is indeed a serious problem for the tax authority to effectively discharge its duties.

Subtheme: Financial Capacity

The evidence gathered from the interviews suggests that ZIMRA officials appreciate the capacity challenges that contribute to the failure of ZIMRA to effectively collect tax revenue from the informal economy. Participants noted that there was an acute shortage of revenue collectors due to budget restrictions. Effectively monitoring, tracking and collecting tax revenue from the informal economy requires knowledgeable and skilled manpower (OECD, 2020). This finding is consistent with that of Mpapale (2014). According to the perspective shared above, Participant G5 said:

First, tax collectors lacked knowledge on how to collect taxes from the thriving economic sector, and second, the tax authority is underrating the revenue potential within the informal economy. Do you know that some operators in the informal economy earn far more than taxed formal employees. …look at the types of cars they are driving…. Most of them they own houses in affluent suburbs. The problem is that Zimra is failing to carry out research to determine which business ventures qualify for taxes. They just underestimate the revenue potentials of this sector, and to them, following them is just a waste of time and resources.

The same point was raised by Participant A2, who elaborated as follows:

ZIMRA is not seeing the value of devoting limited resources in recruiting and training manpower specifically for the informal economy because the desired results are always very low and unrealistic. In short, ZIMRA does not have adequate and capable staff to handle the informal economy.

The statements above indicate that Participants G5 and A2 appreciate the tax revenue potential of the informal economy.

Subtheme: Commitment and Support

The majority of the participants claimed that implementing a presumptive tax system to fully realize its revenue potential requires commitment from those on the ground, especially ZIMRA and local councillors. According to the responses from the participants, there is generally a lack of common understanding of its implementation. The lack of commitment was attributed to a lack of incentives and high administrative costs (Haque, 2013). Participant A4 said:

It is common knowledge that many people are in the informal economy, and the majority of them are not paying anything to the government. ZIMRA decided to concentrate on some segments of the informal economy that seem to be profitable and of fixed abode. Allocating resources to try and tax everyone in the informal economy is a daunting task and thump sucking…. After all, it is unrewarding exercise and life-threatening exercise, especially to the revenue collectors.

This statement indicates that Participant A4 appreciates the existence of a large informal economy in Zimbabwe and government efforts to broaden the tax base. However, resource (both human and financial) constraints represent barriers to the full roll-out of a presumptive tax regime in Zimbabwe. This is also true in the literature provided by Mutsotso (2010), who states that it is impossible to bring all informal activities into the tax net due to administrative challenges. Participant E4 also indicated that the collection of taxes is believed to be fair when the government is deemed effective and fair. He said:

Once the government is perceived to be inefficient and has no capacity to collect taxes from the informal economy, then very few informal economy operators are to comply.

The above excerpt is in line with the view of Hoa (2019) that a high level of informality is an absolute indicator of institutional failure. This implies that perceptions of poor capacity within ZIMRA may increase tax noncompliance behaviour. The following section highlights an analysis and discussion of the results with respect to governance and political factors.

Theme B: Governance Factors

This theme aims to determine how governance influences presumptive tax compliance in Zimbabwe. The subthemes that emerged from the analysis of the major theme are outlined below and subsequently analysed in depth:

cooperation/synergies with other stakeholders policy consistency political legitimacy and interference.

Subtheme: Cooperation—relationships with Other Key Stakeholders

Judging from the submissions made by participants, cooperation or synergies influence the collection of presumptive tax revenue from the informal economy. In this regard, participants A2, F5, F1, D2, F3, E3, E4 and E5 highlight how poor governance and political legitimacy discourage tax compliance. Participant A2, for example, said:

The relationship between the Ministry and ZIMRA is good. However, the Ministry has been accused of being too involved in the authority’s business to the extent of interference. Furthermore, support for programmes has been slow, with the ministry taking long to approve requests.

Participant A4 also said:

The Ministry of Finance has appointed ZINARA to collect presumptive taxes from transport and driving school operators. ZIMRA is now focusing on other categories of the informal economy, and as ZIMRA, we continue offering technical support to ZINARA.

The implication here is that the perceived lack of cooperation between the Ministry of Finance and ZIMRA deters informal economic participation. A lack of cooperation was observed when the Ministry of Finance prescribed arbitrary presumptive tax rates without consulting ZIMRA (tax authority) (Dube, 2014).

Subtheme: Policy Consistency

The importance of policy consistency in tax administration cannot be overemphasized. The existence of conflict and policy irregularities may influence noncompliant behaviour among informal economy operators (Njaya, 2015). Participant F5 tried to confirm incidences of lack of political legitimacy by stating:

This corrupt party (ZANU PF) has reversed the inherited gains in terms of functional industries, and as a result, we are witnessing multiplicity of the informal economy in Zimbabwe…. Populistic policies contributed to resistance by taxpayers because they were told not to pay taxes and do business to survive….

This statement confirms that policy inconsistencies have undoubtedly affected the collection of tax revenue from the informal economy in Zimbabwe. Political leaders have been pushing their political agenda of staying in power and gaining support, as evidenced by their unconstitutional reversal of a well-structured functional system in 2000 and 2007 (Mlambo, 2017; Muchichwa, 2017). They argue that people always use these populist policies to justify the constitutionality of their nonparticipation in the formal sector. Interviewees have also attributed tax noncompliance behaviour to a lack of commitment and seriousness by politicians and government officials in applying tax rules and regulations. Tax rules are generally lax because politicians and other senior government officials benefit from the current state of affairs (Adike, 2018). One of the participants argued:

I think ZIMRA is receiving a directive from some high offices not to tax some of the profitable informal economies. What is on the ground is that politicians are encouraging their constituencies to avoid tax payments (what is commonly termed devil deals) in exchange for votes. (Participant F1).

Subtheme: Political Legitimacy and Interference

External factors such as political interference in affairs have a negative impact on tax revenue collection from the informal economy in Zimbabwe. In a bid to retain their parliamentarian seats in the next election, some politicians advised their supporters not to pay taxes at all. Such an arrangement between the ZANU PF large wings and informal economy operators creates challenges for enforcement. This finding resonates with Ampaabeng (2018), who mentions that politicians influence people in the informal economy not to pay taxes in exchange for election votes, thus making it practically impossible for tax authorities to enforce tax laws. One of the participants, Participant E1, reported that:

…informal economy must be supported by the government, and there government, in turn, must be seen to be transparent in its activities. This is one way you can win this war of trying to tax the informal economy.

Some businesses in the informal economy may decide to circumvent tax laws because they do not recognize the legitimacy of the current government. This finding is consistent with those of Dube (2014) and Makumbe (2009), who found that the question of government legitimacy is a serious issue that influences tax noncompliance within the informal economy. He further argues that the government of Zimbabwe is illegitimate because it has failed the economy and even failed to maintain the inherited infrastructure. Once taxpayers perceive the government to be illegitimate, they avoid paying taxes. The two excerpts below underline this matter:

The legitimacy of the current government is still questionable. Henceforth, anything from an illegitimate government is illegitimate. Given what is happening in Zimbabwe, the tax system is also infiltrated by politicians; as a result, it compromises the revenue drive of ZIMRA. (Participant D2) In the political arena, political leaders do not have people at heart…. I believe that these politicians are not doing what they are elected to do. They are looting taxpayers’ monies, and our state of roads and health sector has dilapidated. (Participant F3)

These assertions indicate that, first, people are still questioning the legitimacy of Mnangagwa’s government, and it is difficult to encourage voluntary compliance. Second, ZIMRA is no longer an autonomous entity since other high offices may override its tax legislation for their political gains. Third, participants felt that government officials and other politicians misappropriated public funds to the detriment of service delivery. This finding indicates that the severity of government interference in the affairs of ZIMRA coupled with deep-seated corruption and tax noncompliance increased. Many operators in the informal economy capitalize on perceived weakness in the tax system and a politically tense environment. Participants also mentioned that senior government officials and politicians should be seen as law defenders, but in Zimbabwe, they are viewed as lawbreakers. In light of such perceptions and practices, the informal economy finds it easy to dodge tax rules, as can be interpreted by Participants E3 and E4:

Pay tax for whose benefits? There is no point in paying taxes when the government is failing to provide public goods and services … our health system is sinking; our road network is in a sorry state…. If they (politicians) are breaking the law (looting without prosecution), then taxpayers are likely to break it even more…. (Participant E3) The government destroyed vendors’ market stalls during COVID-19-induced lockdown…. How do you expect vendors to cooperate with tax laws when the very government is not defending and treating them well? Our political landscape is hostile and not friendly but rather ruthless. (Participant E4)

The statements above show that, first, service delivery is poor even when taxes have been collected. Second, people in ZANU PF networks are not prosecuted when they break tax laws in Zimbabwe. Third, politicians (especially those in large cities) supported the removal of market stalls in a bid to decongest the city (Kulkarni, 2020). This means that the justice system is no longer independent, and generally, there is lawlessness in Zimbabwe, which in turn promotes tax evasion. The results from the interviews suggest that politicians are not encouraging people in their constituencies to pay taxes but rather empowering their voters to defile tax laws. However, Participant G2 recommended:

If the politicians are committed to raising awareness campaigns about tax compliance, those who voted them will be motivated to obey because people trust their local leadership. In Zimbabwe in general, there is a lack of political will….

Clearly, from the above statement, political leaders deliberately refuse to support tax enforcement activities in this section of the economy, especially those that are likely to disadvantage the informal economy to widen their support base. This is substantiated by Ampaabeng (2018), who mentions that the major challenge experienced by tax authorities in developing countries in taxing the informal economy is the lack of political will. The following section provides an analysis and interpretation of the results with respect to the legal and regulatory framework.

Theme C: Legal and Regulatory Framework

The legal and regulatory framework was further cited as one of the determinants of presumptive tax system performance in Zimbabwe by participants, who indicated that it was one of these barriers to effectively taxing the informal economy. Overall, the participants mentioned that the restrictive tax regulatory framework and weak enforcement system influence the participation of the informal economy in Zimbabwe. In establishing these provisions, the following subthemes emerged in this section:

enforcement of rules and regulations quality of services presumptive tax structure.

These subthemes are examined below.

Subtheme: Enforcement of Rules and Regulations

Overall, the participants mentioned that the restrictive tax regulatory framework and weak enforcement system influence the participation of the informal economy in Zimbabwe. Responses from the interviewees on the enforcement of rules and regulations with regard to the informal economy revealed that it is perceived to be inconsistent and selectively applied. Responses from the interviewees on the enforcement of rules and regulations regarding the informal economy revealed that it is perceived to be weak. One interviewee described the current enforcement system as follows:

I don’t know the reason why ZIMRA and the council have decided to engage the Zimbabwe National Army (ZNA) (militias) and the Zimbabwe Republic Police (ZRP) in the revenue collection process. People in the streets are harmless; they don’t have weapons, so why do they engage ZNA and ZRP? Council officials with the state security agents will come and raid the innocent street vendors, arresting some and impounding their goods, especially along Rezende Street. (Participant G2)

This makes the informal economy unwilling to comply with tax laws because of the ‘militarisation of tax revenue collection process’ (Helliker & Murisa, 2020). A senior official from ZISO made the following remark:

The involvement of soldiers and police in revenue collection is a sign of a failed system. Little is known that this commando-driven enforcement will yield no results because operators in the formal economy feel like fugitives…The way vendors will be treated, tortured, terrorised and insulted by the state agents, I feel pity; you know that “warlike” atmosphere. Compliance is out of fear but won’t last…instead ZIMRA and council should demilitarise revenue collection… (Participant E3) …you don’t have to use force to make people comply with tax laws; the key to building sustainable tax compliance behaviour is the provision of basic amenities such as good health services, roads, water and electricity. These benefits greatly contribute to the increase in tax compliance. (Participant F5)

However, Participant A2 justified the acts of involving law enforcement agents by saying:

Due to economic hardship in Zimbabwe, people may not be willing to observe tax laws; therefore, we believe that engaging state agents will help accomplish total tax compliance.

Another participant, A5, revealed:

Approaching the informal economy without the help of police and soldiers is high risk because at times one can be beaten up or humiliated by angry and unaccommodating operators.

The above excerpts show that, first, ZIMRA, as an entity, has failed to collect tax revenue using statutes in place, as evidenced by the engagement of police and soldiers. Second, informal economy operators do not comply due to prevailing economic conditions. Insisting on collecting tax revenue from the informal economy without due concern for their plight would mean that taxpayers will not cooperate at all. The scenario described above in which the informal economy is forced to comply through a ‘state apparatus’ signifies serious trust and governance issues. It can be surmised that the informal economy will continue to circumvent tax regulations because of frustrations, economic crises and the absence of a guarantee of legal protection. The use of police and soldiers indicates the weakness of the tax system as a whole and could spearhead tax noncompliance. The perception that ZIMRA cannot discharge its duties without the help of police and soldiers reduces trust in ZIMRA and tax morale, hence providing fertile ground for its noncompliance behaviour. The same opinion is shared by Lough et al. (2013, p. 16), who state that tax authorities engage police and soldiers when they have limited capacity and when they lose taxpayer trust. They further argue that when taxpayers no longer trust, tax authorities will experience a decrease in tax revenue due to tax noncompliance and resistance.

Participant G3 recalled:

In the colonial era, compliance levels were very high compared with those in independent Zimbabwe. All black people, even those in the remotest areas in Zimbabwe (Rhodesia), paid their tax liabilities on time. I believe that, currently, legal and regulatory frameworks are strong and effective. My question is: Why is it that postcolonial Zimbabwe, with everything (technology and resources), is failing to influence compliance within the informal economy? What is missing in our tax system?

According to this perspective, the colonial tax system was effective, and community leaders assisted tax collectors in collecting taxes from villages or wards (Mkandawire, 2010; Mupfuvi, 2014). Importantly, ZIMRA can draw lessons from Smith’s administration to improve tax compliance and increase tax revenue from the informal economy. These results align with the findings of the extant studies of Makate et al. (2019) and Matamanda et al. (2019), who state that taxpayers are willing to comply with tax laws when they perceive that the tax framework is strong and supportive.

Additionally, Participant A2 confirmed:

‘Due to the absence of physical addresses and fixed premises, it is difficult to monitor and audit informal economy operators. They often hide from ZIMRA.’

Participant E2 substantiated Participant A2’s claims by confirming that the deterrence measures in place for the informal economy are ineffective when he said:

… I believe that detection and sanctions available cannot motivate the informal economy to pay tax unless it is implemented equitably (non-discriminatory)… given what is happening in Zimbabwe, misappropriation of public funds and poor service delivery, no one is afraid of being arrested…they may arrest our members every day, but no one is going to comply…. The current government is corrupt to an extent of stealing cyclone Idai donations…there is generally a lack of accountability…we demand public accountability.

The abovementioned findings reveal that existing deterrence measures have no effect on changing taxpayer compliance behaviour. Participants described the selective application of laws to taxpayers. The perception that there is no accountability in public funds has a significant negative impact on compliance behaviour. However, Participant A2 argued:

‘When taxpayers fail to give us proof of payment of their tax liabilities, we confiscate their wares.’

It is important to note that members of civic societies and ZISO bemoaned the confiscation of wares/goods as a way of penalizing noncompliance. Participant E1 further said:

Penalising the informal economy is not an acceptable solution to build a culture of tax compliance, but the dialogue is important to establish the reasons for nonpayment of taxes. Our members reported that ZIMRA and municipality police demand payment without receiving payment on several occasions. I don’t think the money collected goes to the treasury.

These assertions infer that informal operators and their associations are not afraid of being caught or arrested and that the current deterrence measures cannot in any way create a culture of tax-powering informal economy taxpayers. The fact that informal economy operators are knowledgeable about corrupt practices within the government and misuse of public funds by top government officials means that informal economy operators will also avoid paying taxes. In other words, given the magnitude of misappropriation of public funds and poor service delivery, especially in the health sector, tax noncompliance, on the other hand, becomes a taxpayer’s choice. The findings concerning the application of deterrence measures are consistent with those of Ligomeka (2019), who found that the excessive use of force and punishment might not transform noncompliance behaviour within the informal economy.

Subtheme: Quality of Service Delivery

This study investigated participants’ views on how quality of service influences presumptive tax collection in Zimbabwe. All participants conceded that poor service delivery deterred presumptive voluntary tax compliance among informal players. The paper revealed that the low performance of presumptive taxes is attributed to the quality of the tax service and the structure of the tax system. Participants mentioned that tax service quality is the availability of public goods and services (service delivery), while the tax structure focuses on the tax base, tax rates and compliance measures. One of the participants, Participant D1, mentioned:

Tax service quality has a positive impact on voluntary compliance among informal economy operators. In Zimbabwe, people in the informal economy do not see the value of paying taxes due to poor service delivery in towns and cities.

According to the response of Participant D1 above, informal economy taxpayers can comply with presumptive taxes only when they are satisfied with the way in which public funds are used to provide essential social services. Evidence shows that in Zimbabwe, there are visible signs of abuse and misappropriation of public funds, as evidenced by a lack of clean water, a dilapidated health system and a poor road network.

Participant F3 supported the above opinion by stating:

Informal economy operators are willing to comply voluntarily but are demanding tangible benefits (payoff rule) from taxes paid. When taxpayers see state-of-the-art infrastructure services such as health care facilities, schools, clean water and other social amenities, they are motivated to pay for their tax obligations. Therefore, the government should commit itself to providing tangible services.

Another participant, Participant G2, suggested:

ZIMRA must outline the benefits associated with paying tax. Taxpayers are concerned with the benefits attached to the tax paid. No benefits, no tax paid simple equation.

The same point was raised by participants G4, F1, F5 and D4, who added that many high-density suburbs lacked clean water and electricity for some months because of misappropriation of public funds by those in a position of authority. These declarations show that the government needs to invest in goods and services that are of public interest. However, the tax revenue collected by the government is either diverted or pilfered by government officials at the expense of service delivery. Generally, all taxpayers (in both the formal and informal sectors) in Zimbabwe are discouraged from paying taxes due to deep-rooted levels of corruption and misuse of taxpayer money. Like participants E2, G1, D2 and D5 indicate a lack of political will to fight corruption in Zimbabwe. For example, participant E2 says:

I believe that the current crop of political leaders has fallen in love with criminality and corruption. It is now a new culture embedded in every facet of life in Zimbabwe. Activists in Zimbabwe were denouncing corrupt practices by top government officials and guessing what. They are either jailed or abducted for exposing corrupt deals… look at the state of our roads network; they all are in a sorry state because of these corrupt leaders.

The above statement shows that the informal economy is unwilling to comply with tax laws because of a lack of basic public goods such as roads, drinking water, sanitation and health services. In other words, the availability of these indispensable services influences individuals’ short- to long-term tax compliance decisions. Poor service delivery in Zimbabwe is undisputed evidence of abuse and misappropriation of public funds that will further perpetualize tax noncompliance behaviour within both the informal economy and the formal economy.

Participant D5 had a similar view, signifying the importance of directing tax revenue to social amenities to encourage tax compliance and improve tax morale. Improving service delivery, especially in the health sector, will greatly improve presumptive tax compliance and, consequently, increase tax revenue. These sentiments show that the government is not providing quality goods or services to the public interest, regardless of whether taxpayers pay taxes.

Furthermore, in providing evidence of a public services crisis and corruption in Zimbabwe, Participant E5 said:

…remember US$15 billion that has vanished from treasury without trace…we have heard the NASSA scandal, ZESA scandal, ZINARA scandal and many other tender related scandals in Zimbabwe. These scandals involve high-profile people who are taking advantage of corrupt systems, and this state-captured judiciary is doing nothing about these looters…it appears like Zimbabwe has legalised corruption…Zimbabwe is in crisis….

Participant D5 argued:

The government is not committed to providing essential services to the people. In a country where the health system is collapsed, no medicine, doctors or teachers are on strike. Mr. Munangagwa purchased a US$18 million helicopter for private use using taxpayers’ money.

Considering the above two points, there is a lack of accountability and commitment on the part of the government. The perception that the judiciary system is under siege and that the government is not prioritizing service delivery facilitates tax noncompliance in the informal economy. This was also acknowledged by Utaumire et al. (2013). They report poor service delivery as a catalyst to increase tax noncompliance among taxpayers. This implies that the lack of tangible benefits motivates taxpayers’ noncompliance culture.

Participant D3 also questioned the integrity of judiciary services with regard to the misuse of public funds by saying:

We have received numerous reports about scandals involving high profile individuals, but these perpetrators are not prosecuted at all. Why are these criminals not sent to jail? The failure of judiciary services to challenge perpetrators facilitates tax nonconformity among the informal economy in Zimbabwe.

The evidence in the data gathered suggests that these unwholesome practices, which are common in all public sectors, provide some justification for tax noncompliance in Zimbabwe, explained as follows:

…These ‘tenderpreneurs’ upon bribing those who award them tenders may in turn compromise quality to recover initial payment made to government officials… Some projects have long been abandoned, especially the sewage system in Masvingo and the Harare-Beitbridge Highway. The obvious reason is that officials eat money for projects. Therefore, you expect the informal economy to pay tax for what? (Participant G3)

The above sentiment infers that there is rampant corruption in the tendering and procurement processes in Zimbabwe, and it affects service delivery (ZIMRA, 2016). Failure to follow procurement and tendering procedures results in the government awarding tenders to undeserving contractors who fail to deliver the desired services. Overall, service delivery is a crucial factor that taxpayers consider before they make a choice to pay (European Parliament, 2013; World Bank, 2016). This finding suggests that taxpayers are motivated to pay taxes when there is an improvement in service delivery. Hoffmann and Melly (2015) also give the same results. They further state that corruption remains a major challenge affecting tax revenue mobilization programmes in developing countries.

Subtheme: Presumptive Tax Structure

The tax system structure emerged as a key determinant of existing tax compliance status within the informal economy. Therefore, based on the assessment, the paper revealed that tax rates, penalties, the complexity of the tax system and detection were the key elements for the tax system structure. Similarly, all participants of this article mentioned that presumptive tax noncompliance is influenced by the complexity of the tax system. One of the participants, Participant F1, revealed the following:

The presumptive tax is based on an estimation of tax liability. Owing to the failure to understand the criteria for estimation and computation, taxpayers may decide not to comply or end up on bribing tax officials to avoid paying more. The informal economy operators should be charged based on their income rather than estimates.

The responses collected from the interviews show that the impediment and vagueness of the presumptive tax policy are among the obstacles to tax compliance. Some provisions in the policy are not clear at all, and taxpayers capitalize on the ambiguities. In reinforcing this point, Participant G3 stated:

Some provisions in the policy document have been criticised for open to several meanings. There is need to redefine and rephrase all unclear sections of the presumptive tax policy for simplicity and viability.

The presumptive tax rates prescribed by the MoFED are too high compared to formal economy rates. This means that presumptive tax rates are much too high compared to those of the same activities in the formal economy. This quote confirms this:

I don’t think field research was properly done. If proper research was done, ZIMRA could have prescribed better tax rates. How can the government tax set a high tax rate for the poor? I think our government has lost a sense of humanity; it is taking away again from poor people in operating in the informal economy. (Participant G2).

Participant E2 also added that the current tax system is not pro-poor or fair. He indicates that informal economy business operations controlled by politicians aligned with the ruling party are not worried about high tax rates imposed by the government, especially in the cottage industry. From official documents viewed by the researcher, the MoFED, Professor Muthuli, proposed an upward review of the presumptive tax for 2021, from 10% of the rental to US$30 per month (Ncube, 2019). It is evident from Minister Muthuli’s budget speech that the current presumptive tax framework does not consider the principles of equity, fairness and efficiency to encourage tax compliance behaviour. This seems to contradict the theoretical principle of simplicity, fairness and equity (Abate, 2019; IMF, 1996). In this regard, his understanding of the unfair treatment of the informal economy is worth mentioning:

… our members in the cottage industry (carpentry) were complaining about the selective tax system. They are required to pay US$70 million in foreign or local currency at the FCPR per month, while some people who are more profitable than them are not paying anything. These people have strong connections with high-profile people who give order to ZIMRA to stop collecting from them. In a bid to remain competitive, the informal economy may choose to bribe ZIMRA officials rather than pay the official rate. In such a scenario, the ground is not level at all…. (Participant E2)

The above testimonies were given by Participant E2, who gave the impression that the tax system is selective and oppressive to poor informal economy operators. This seems to contradict the principle of equity and will incentivize further tax evasion (Dube & Casale, 2016). It is common for informal economy operators to resist or avoid paying taxes, and in such a situation, the government is the greatest loser. Political interference in revenue collection weakens the tax system and creates a culture of noncompliance among taxpayers.

Based on the responses of participants in this article, people may defend against noncompliant tax behaviour, citing legal and regulatory barriers as the chief cause. The participants’ comments and observations in this article provide socio-economic intricacies and constraints that justify tax noncompliance within the sector. Solving this puzzle requires a holistic approach because concentrating only on legal and regulatory factors might not help in building a tax culture.

Discussion

This study focused on a qualitative diagnosis of the factors influencing presumptive tax collection in Zimbabwe. The analysis of this study revealed three overarching factors that promote or influence presumptive tax collection in Zimbabwe. The results show that legal and regulatory factors, institutional factors and governance significantly influence presumptive tax collection.

The first is related to institutional factors that influence presumptive tax voluntary compliance. This study establishes that a lack of capacity (both human and financial resources) and commitment and support has significantly contributed to poor presumptive tax collection in Zimbabwe. ZIMRA is understaffed and does not have a budget mobilize tax revenue from the bourgeoning informal economy in Zimbabwe. The study further revealed that the major reason for the poor performance of the presumptive tax system was the lack of resource (both human and financial) constraints, which represent barriers to the full roll-out of a presumptive tax regime in Zimbabwe. The results of this study confirmed the findings of previous research (Hoa, 2019; Mabwe & Mugozhi, 2018).

The second factor that influences the collection of presumptive tax revenue is credit for governance. According to the empirical findings, policy inconsistency and political illegitimacy and interference are often characterized by tax revenue collection inefficiency (Mebratu, 2023). The participants revealed that political interference and policy inconsistency lead to inefficient presumptive tax revenue collection. The results confirm the findings of Nichelatti and Hiilamo (2024), Tagem and Morrissey (2023) and Sanga and Aziakpono (2023) that institutions and tax capacity promote tax revenue collection.

The third and last factor is related to legal and regulatory frameworks. According to participants, the enforcement of rules and regulations, the quality of services and the presumptive tax structure significantly impact presumptive tax collection. Thus, this study identified legal and regulatory agents as critical inhibitors of presumptive tax collection in Zimbabwe. Similarly, Ncube (2020), Wadesango et al. (2019), Mishra and Kumar (2023) and Nieuwenhuizen (2019) reported that players in the informal economy can comply with presumptive tax laws when there is transparency, strong enforcement institutions (mechanisms) and supportive and clear rules and regulations. This means that better legal and regulatory measures can augment presumptive tax revenue collection.

Conclusion

This article concludes that the constant low tax revenue from the presumptive tax system in Zimbabwe is affected by several factors, such as institutional factors, lack of legal and regulatory frameworks, and governance and political factors. This article strongly suggests that the presumptive tax system is the most economic framework applicable in a highly informalized economy. In principle, the informal economy remains a potential revenue base in Zimbabwe. This article has established that taxing this expanse sector of the economy has been a daunting task due to corruption, political interference, the selective use of tax laws and the lack of a proper tax framework.

This article recommends that the government of Zimbabwe demilitarize the tax system and phase out cash in the payment system to ensure the traceability of all financial transactions in real time. Furthermore, the government should invest in public infrastructure, such as roads and hospitals, among others, to gain the citizenry trust.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.