Abstract

The purpose of this qualitative case study was to explore perceptions of a management control system (MCS) in a post-acquisition integration context through sense-making using interpretive case study methodology. The study draws from the theories of the two types of bureaucratic formalization, sense-making in organizations and MCSs. The study material consists of semi-structured interviews with the managers at the corporate, divisional, and business unit levels. At the time of the study, the case company was growing through several acquisitions per year, which created constant challenges with post-acquisition integration and a need for more formal MCS. The article shows how the backgrounds of the acquired business units are related to the perceptions of the MCS. We found that the identity threat and retrospection were properties of sense-making that explained the business unit managers’ attitudes towards the corporate MCS. Particularly prior experiences of production-centred line-manager positions in small entrepreneurial firms seem to foster coercive perceptions of MCS. The results of this study contribute to MCS literature.

Introduction

The purpose of a management control system (MCS) is to assist managerial decision-making and to direct employee behaviour. In management accounting literature, the prevailing viewpoint of senior management is a technical design approach (Chenhall, 2003). Nevertheless, current research is directing attention to how people understand, perceive, and interact with an MCS in practice (Ahrens & Chapman, 2004; Jordan & Messner, 2012; Tessier & Otley, 2012; Väisänen et al., 2021; Wouters & Wilderom, 2008). The research community has also started to investigate more decisively different contexts and situations, and problematize many presumptions behind research and theorizing of MCS to build better theories in management accounting (Malmi & Brown, 2008; Malmi & Granlund, 2009). This study focuses on middle management’s perceptions of a corporate MCS in the context of post-acquisition integration.

The study applies interpretive case study methodology and focuses on one manufacturing company characterized by fast growth achieved through acquisitions and demanding profitable growth targets. Here, the managerial challenges of post-acquisition integration, MCS development, and meeting the targets create a major need for organizational sense-making. In our case study analysis, we draw from the theories of two types of bureaucratic formalization (Adler & Borys, 1996) and sense-making in organizations (Maitlis & Christianson, 2014; Weick, 1995).

The remainder of the article is organized as follows. The next section discusses the theoretical underpinnings of the study and motivates the research question. Then, the methodology is described. The following section presents the analysis of empirical data and key findings. Finally, the last section encompasses the discussion and presents the study’s conclusions.

Theoretical Framework

Perceptions of Management Control

MCS is an organization-specific collection of controls that provide the financial and non-financial information useful for managerial decision-making and directing employee behaviour to support the goals of the organization (Chenhall, 2003). Typically, an MCS consists of the controls for budgeting, enterprise resource planning (ERP), performance management system (PMS) and rewarding. The control process consists of separate phases of target setting, action, feedback, evaluation, and reward/sanction. Further, cultural and administrative controls form the context for the planning of goals and actions, and control and feedback of performance as part of MCS package (Malmi & Brown, 2008).

Researchers have offered several frameworks to represent variations in MCS use or perceptions of such systems. They include Hopwood’s (1972, 1973) early concepts of styles of using controls and Simons’ (1995) concept of positive and negative controls. Recently, attention in research has shifted from the managerial use of controls to the perception of controls within the organization. Theoretical frames largely inspired by organizational theory (Adler & Borys, 1996) can guide empirical investigations into MCSs (Ahrens & Chapman, 2004; Tessier & Otley, 2012). Tessier and Otley (2012) proposed that managerial intentions should be analytically separated from the employee perceptions of the controls and developed a new MCS framework by combining the levers-of-control framework (Simons, 1995) with the employee viewpoint (Adler & Borys, 1996).

Adler and Borys (1996) investigated workflow formalization and proposed a typology of enabling and coercive use of formal controls. The study suggested that employees’ attitudes are more positive when controls enable them to master their tasks and more negative when formalization only serves management’s top-down attempts to coerce employees to increase effort and compliance. According to them, the general features of enabling use are repair, internal transparency, global transparency, and flexibility. This means that controls enable efficiency and innovation if employees understand local work processes and how they connect to the whole organization and have discretion over the use of controls they also understand. Further, they argue that coercive use of controls relies on a de-skilling approach to management where all knowledge is retained by a top management team that commands and monitors to ensure its express instructions are followed.

Adler and Borys (1996) also suggest that perceptions of formal bureaucracy depend not only on the designed features but also on the organizational context and the process of designing and implementing the practices of bureaucracy. Lack of competition or demanding customers, asymmetries of power in the organization or in the distribution of other resources are forces that may encourage a coercive logic. They also called for further studies to analyse other facets of bureaucracy, such as management control.

Ahrens and Chapman (2004) draw on an exploratory case study of a restaurant chain to apply the concepts of enabling and coercive uses of an MCS in management accounting research. The study focused on whether using an MCS improves both efficiency and flexibility and, if so, how. Ahrens and Chapman found several good practices to support a more enabling MCS, such as allowing local ad hoc systems and sharing knowledge of best practice. The study provides examples such as problem-solving flowcharts, divisional control workshops, and ensuring restaurant managers understand why corporate procedures and controls are important for the organization.

Several case studies have since examined the enabling features of MCSs or specific controls. The studies have differed in their organizational contexts and groups of employees focused upon. One stream studies the development process of an MCS. Wouters and Wilderom (2008) sought to identify the characteristics of a PMS development process that resulted in control practices that logistics department employees in a beverage manufacturer perceived as enabling. The study found an approach building on existing skills, local practices, and incremental learning from experiments with specific performance measures enhanced the enabling aspect of the PMS. Further, the transparency of the PMS itself and the professionalism of controllers were important factors in developing a PMS that employees considered useful. Väisänen et al. (2021) examined the means of fostering the enabling perceptions of a new MCS during the post-acquisition integration of a Finnish company by a Canadian company. In this international management context, they found a key role in trust-building activities and active communication of intentions between the managers of headquarters and subsidiaries. Further, controls that aid routine management support enabling perceptions.

Two studies have focus on forecasting, goals and performance evaluation. Henttu-Aho (2016) followed the implementation of rolling forecasting in a paper company and looked at the process features affecting controllers’ perceptions of the new control mechanism. Palermo (2018) identified three different ways of dealing with the information of actual performance and future scenarios. He put forward the concept of disciplined flexibility, in which performance assessment does not become too rigid and reactive when the performance evaluation is based on continuously complementary scenario work and on making plausible narratives about future outcomes.

This study examines perceptions of an MCS on different managerial levels: top, divisional, and business unit management. More particularly, we focus on the differences in how individual middle managers perceive the corporate MCS and seek explanations for the differences. Our analysis from the individual managers’ perspective draws on sense-making theory (Maitlis & Christianson, 2014).

Sense-making in Organizations

Organization studies have used sense-making to focus attention on the cognitive activity of framing situations to make them meaningful (Maitlis & Christianson, 2014). Sense-making is a collaborative process of creating shared awareness and understanding from different people’s perspectives and interests (Weick, 1995) wherein people construct, interpret and recognize different meaningful features of the world (Gephart et al., 2010; Maitlis & Christianson, 2014). People work to understand issues or events that are novel, ambiguous, confusing, or that defy expectations (Maitlis & Christianson, 2014). Weick (1988, 1993, 1995), in particular, introduced sense-making at the organizational level. Weick (1995) ascribed seven properties to sense-making (a) identity; (b) retrospection; (c) enactment; (d) social activity; (e) ongoing; (f) extracting cues and (g) prioritizing plausibility over accuracy.

Here, identity means people think about who they are in a certain context, shaping what they enact and how they interpret events. Sense-making is thus grounded in identity construction (Maitlis & Christianson, 2014). The concept of retrospection provides the opportunity for sense-making; its timing affects what people notice. People enact the environments they encounter through dialogues and narratives. Speaking helps people to understand what they think, to organize experiences, and, furthermore, to control and predict different events, thus reducing complexity.

‘The basic idea of sense-making is that reality is an ongoing accomplishment that emerges from efforts to create order and make retrospective sense of what occurs’ (Weick, 1993, p. 635). Sense-making theory holds that the seven aspects interact as individuals interpret events, meaning they become intertwined. Sense-making becomes observable through narratives (Balogun & Johnson, 2005; Currie & Brown, 2003; Maitlis & Christianson, 2014; Thurlow & Helms Mills, 2009; Weick, 1993, 1995).

According to Maitlis (2005), sense-making occurs in organizations when people confront events, issues and actions that are somehow surprising and confusing (see also, Gioia & Thomas, 1996; Weick, 1995) and even chaos and crisis (Maitlis & Christensen, 2014). For example, Gioia and Chittipeddi (1991) and Rouleau (2005) studied the sense-making phenomenon in the context of strategic change, which as a large-scale new situation, provides a situation for surprises, confusion, chaos and confrontations.

Weick (1995, p. 23) stated that ‘sense-making is triggered by a failure to confirm one’s self.’ Identity threat is thus a powerful prompt for sense-making. If human needs like self-enhancement, self-consistency or self-efficacy are threatened, people tend to be triggered towards the sources of the threat to restore their identity (Maitlis & Christensen, 2014).

Weick et al. (2005, p. 409) asserted that sense-making involves the ongoing retrospective development of plausible images that rationalize people’s actions. Sense-making is retrospective because the attention necessary for sense-making requires the experience to pass before attention can be directed to it (Weick, 1995, p. 24). We found this approach particularly useful in analysing the perceptions of an MCS after several repetitive acquisitions and rapid growth. The process included the characteristics of strategic change (Rouleau, 2005), leading to surprises, confusion, chaos and crisis (Gioia & Thomas, 1996; Maitlis & Christensen, 2014) during post-acquisition integration. Moreover, we are interested in the sense-making triggered by the threat to identity brought about by the process of acquisitions, the integration of acquired firms, and especially the implementation and usage of a common MCS.

In accounting research, sense-making is a relatively less studied area. Boland and Pondy (1983) found that accounting is used to make sense of the frames of reference that characterize an organization. Boland (1984) studied managers’ sense-making of accounting data. The findings indicate that accounting systems play an important role in ordering sense-making activities in an organization. Jönsson (1987) stated that in complex environments, actors try to ‘establish islands of meaningfulness and to create links between such islands.’ The study found that accounting served as a bridge while establishing a common interpretive scheme. Boland (1993) pointed out that accountants and managers make interpretive readings of an organizational situation as a basis for accounting as they try to make sense of different situations. Accounting texts provide meaning for an organization but also for the people themselves and their worlds. Tillmann and Goddard (2008) studied strategic management accounting and found that the potential for accounting to contribute to strategic management rested on sense-making activities. Moreover, Jordan and Messner (2012) found that managers make sense of incomplete performance measures and highlighted the potential for managers to use an MCS to support sense-giving in organizations. Sajasalo et al. (2016) linked sense-making to strategy implementation, accounting and fantasizing.

However, all the above studies address how accounting is used in sense-making, while this study focuses on how sense-making affects perceptions of an MCS. Our research question is as follows: How do the properties of sense-making affect the perceptions of MCS in the context of post-acquisition integration?

Methodology

Our case selection strategy was to find an extreme case, an organization integrating numerous business units within different business contexts (cf. Stake, 1995). The case company—assigned the pseudonym Comet—was a subcontractor in the engineering industry that supplied services for automotive, mechanical engineering, transmission, and defence industries. The firm’s turnover in 2008 was almost EUR 200 million, and it had over 1,000 employees. The company emerged from a business unit in a large industrial company following a management buyout. A company growing rapidly through multiple acquisitions annually suited our interests perfectly as the firm’s strategy created a need for organizational integration and sense-making, a corporate MCS, and formal bureaucracy.

Comet’s main strategic target was to become a subcontractor able to supply ever more demanding systems to global companies. Company acquisitions play a major role in that strategy. Over the first seven years, the company completed 15 acquisitions of small or medium-sized machine shops, which were organized into business units (BUs). At the time of the fieldwork, the organization comprised three divisions and 13 business units. The private equity owner had set the managers at all organizational levels profitable growth targets. Meeting the strategic targets required the flexibility to adapt to changes in customer demand and increasing cooperation between the business units.

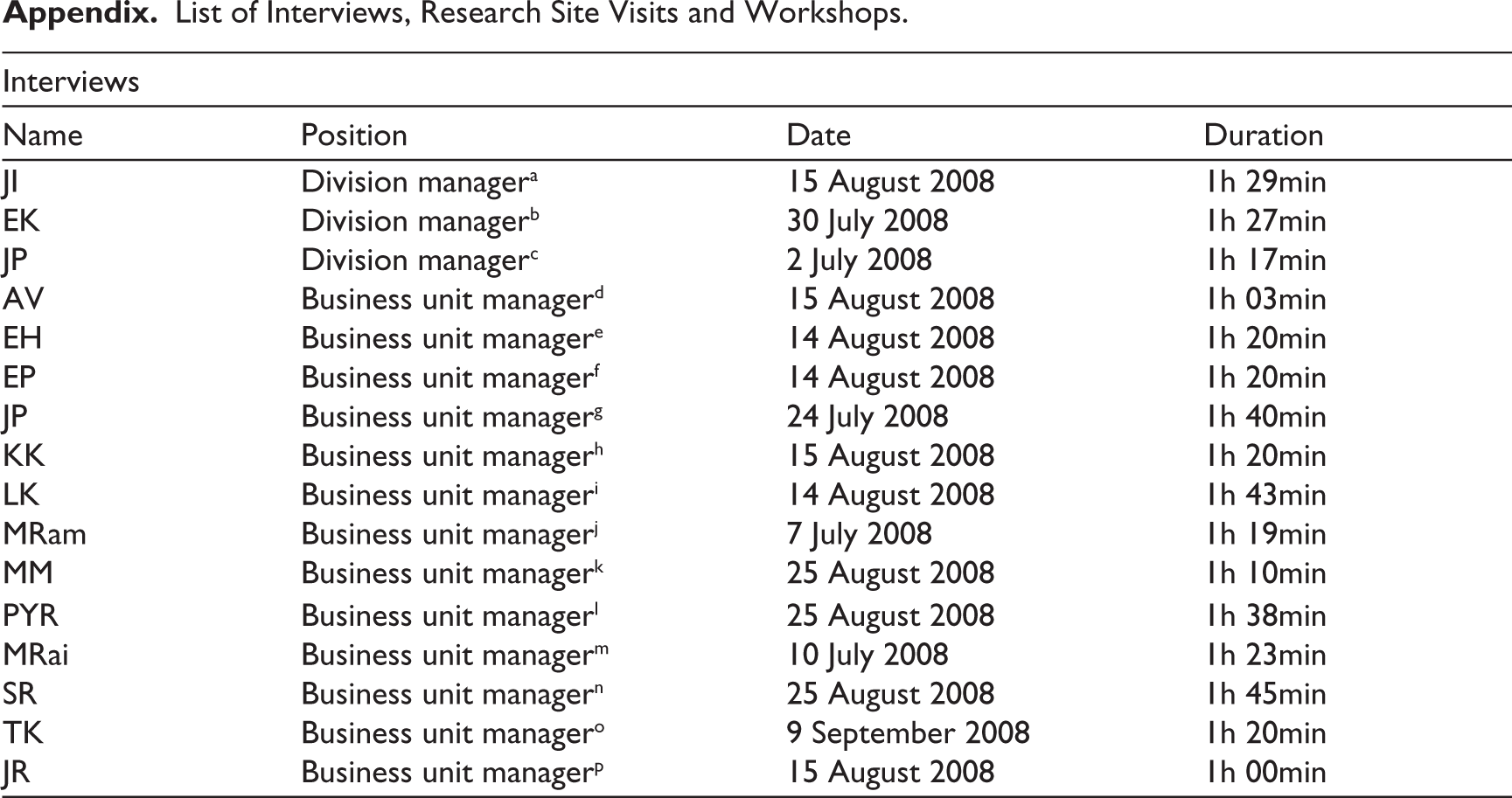

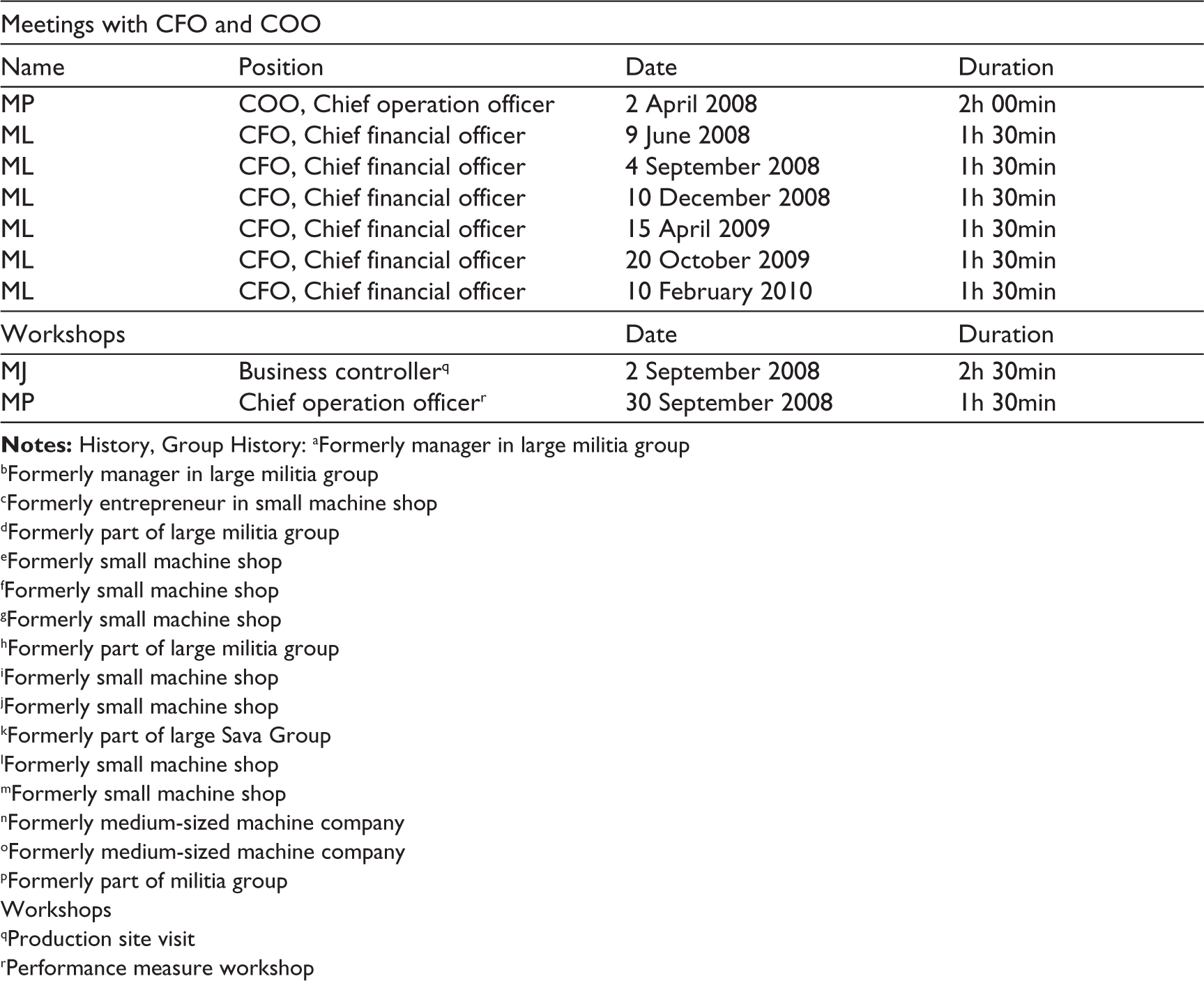

We used semi-structured interviews to gather apposite information in different contexts in terms of organizational level, management function, and management situation of the acquired business units. The interview protocol incorporated the background of the BU and the interviewee, the business model, management practices, the structural elements, the uses, and the local meaning of the MCS for each interviewee. We interviewed 13 business unit managers, three division managers, and three top managers (see the Appendix). All interviews, bar two, were recorded and transcribed. The interviews typically lasted one and a half hours. In addition, we had several informal discussions and meetings with Comet’s CFO, COO, and CEO over the two years of fieldwork.

This interpretive case study aims to get close to everyday management accounting practice in a special context to understand and theorize it (Ahrens & Dent, 1998; Kakkuri-Knuuttila et al., 2008; Vaivio, 2008). Our theorizing is focused on the specific meanings of the MCS for people working in different management positions within a changing organizational context (Ahrens & Chapman, 2006; Czarniawska-Joerges, 1992). The interpretive research approach views the practices of management accounting as highly context-specific interpretations and enactments in evolving situations (Ahrens & Chapman, 2006; Hopwood & Miller, 1994). Therefore, enquiries into local meanings and uses of management accounting are regarded as the essence of qualitative field research (Ahrens & Chapman, 2006; Ahrens & Dent, 1998; Hopwood, 1983).

Findings

The main formal management control at Comet was standardized budgetary control. All business unit managers had responsibility for profits. An ERP system was introduced to coordinate the information flow between the business units and the headquarters. Monthly reporting involved standardized financial and operational figures with a brief management report for the top management. Top management collated those data and prepared group reports for the board.

The standardized set of performance measures included four financial and seven operational measures. The financial measures in the system were as follows: (a) turnover, (b) sales margin, (c) gross margin and (d) EBIT. The operational measures in the system were as follows: (a) productivity, (b) delivery rate, (c) current assets, (d) material usage rate, (e) three-month sales forecast, (f) sick days and (g) production lag in euros. The PMS was built to serve the needs of senior management in managing the group at the strategic level. However, the unit managers were also expected to use the measures at a local, operational level.

Perceptions of Coercive Control

Our respondents perceived the formal MCS to be exerting pressure originating with top management and the private equity financier to squeeze ever better results from the business units. The mechanism utilized was annual targets that were considered difficult or unrealistic. The control style relied on closely monitoring monthly financial performance, budget-constrained evaluations, and incentivizing middle managers.

EBIT, for example, we have such a problem in this firm that the EBIT target is 10%, and you can never reach that. Definitely, if you have a lot of material transmission in your business, and if you target 10% and the customer can calculate even a little bit. (Division manager JI)

Let’s say that the net sales increase target is put up to 15%–20%; that is clear, but when you look at the costs side … you have to swallow it, even if you try hard to explain, the target is hard, maybe too hard, but there are those Private Equity men and upper management, who prepared it, you have to live with it. (BU manager EH)

In budgeting, if we achieved 27.4%, the budget was 37%. The sister unit achieved 24.1, while the budget was 31.2. This can’t be achieved.… In terms of operating margin, we achieved 6.4%, while the target was 19.3%. I have presented to (upper management) that, ok, we have performed poorly, but it is wrong to judge us against the budget; please compare performance against the previous year. (BU manager LK)

Divisional and BU managers perceived budget and non-financial reporting as a coercive surveillance tool that offered no help with managing their units. Business unit managers felt they were merely disciplined by requiring them to fill in the PMS forms and send them to the head office and division managers every month. Managers knew very well how to avoid the attention and negative feedback from top management that exceptions from the targets would attract.

Business unit managers try to set target levels to avoid negative attention. (Division manager JI)

If the numbers in the performance measurement system were negative, it would not be very quiet here. (BU manager MM)

Some BU managers felt that performance reporting was very time-consuming and did not know how the top management team used the information provided. The meaning of the performance measures, used as the basis for rewarding the BU managers and their staff, was more accepted. The profit, value-add, and reliability of delivery measures were felt to be coercive but also meaningful. The same figures were used to support the management of their BU and give feedback to their staff.

First, we can pick the reliability of delivery; it is the most visible measure, which I introduce weekly in the factory, it is best understood, and it is connected with the reward system … then we have this value-added, which is also included in the incentive system … the incentive system has a clear effect … it focuses issues around the action, and always when the figures are reviewed, they are interesting. It has an effect.’ (BU manager SR)

The perception that Comet’s MCS was a coercive tool was based on unrealistic financial targets combined with a tight control style, burdensome reporting requirements, and a poor understanding of the overall meaning of the corporate MCS. The attitude of the BU managers and staff to the same figures improved when they were used to support local management and calculate financial incentives.

Perceptions of Enabling Control

There was some understanding of corporate policies, procedures, and control systems at all levels of management. The managerial interpretation of the MCS was that it provided a common guide, order, and an informational basis for managerial decisions. The controls most often mentioned as important in post-acquisition integration were the ERP, budgeting, and the PMS.

Yes, the ERP has improved the daily operative action, and it creates a clear common platform […] It is really important that employees record the hours properly, in the right order, and the material is recorded correctly on inventories … everything starts from the fact that everyone uses it and use it correctly (COO MP)

We started to watch the monthly figures. And when we have such a PMS, we will not mess around as much as previously. (Division manager JI)

Thank God we got the model when the ERP came … professional approach.’ (BU manager KK)

Corporate guidelines regarding ERP, budgeting procedures and the PMS were often welcomed as they created order and improved efficiency by reducing ‘messing around.’ As a result, administration took less time and management attention was freed for business issues.

I feel that this kind of formal model is good. (BU manager KK)

A positive appraisal of an MCS would probably describe it as helping to motivate people, direct attention, navigate the business, create transparency, and relay hard facts. However, those viewing formalized bureaucracy as enabling were largely in the upper echelons of management and only in some business units. Those BU managers often had prior experience with large organizations and experience with a formal MCS.

In our model, there are a bunch of very independent business units under the divisional manager. They report to the divisional management, which then reports to me, and that route up and down works very well, in my opinion. (COO MP)

Here we are very independent.… It is not very bureaucratic, and you get decisions very quickly.… I can operate fully independently and freely. We discuss a lot with (Divisional manager) … about bigger issues … he visits here weekly … and he knows that we report more often orally and informally than monthly reports. (BU manager LK)

For the corporate-level and divisional managers, the MCS was an essential asset to aid in monitoring the performance of the operations. Before the ERP system was implemented, the only control information was a monthly profit report combined with seven performance measures. Corporate information systems, in contrast, offered timely information as a basis for monitoring and management by exception.

Those (performance measures) will signal when the alarm bells should ring. (COO)

With Digifinance, I look at these almost every day, at least every second day. With Lean, I look merely at sales and orders … when customers send forecasts and volumes … these are such issues that are checked. (Divisional manager EK)

I follow the income statement more. There I see the development of variable costs, net sales and so on. But most often, I look at sales margin and EBIT.… I use, e.g., material usage and value-added, which are bases for the reward system.… I like numbers, and control takes place through them.’ (BU manager JP)

The MCS was considered an important tool to direct employee behaviour, particularly in the upper echelons of management. Some BU managers, however, perceived agreement on targets was a necessary basis for management.

At the moment, we have a clear direction: We will go ahead as has been agreed in the performance measurement system. (Division manager JP)

It (PMS) tells you that the open orders may not be under 5.0 m. euros. (BU manager KK)

The different perceptions of the MCS can be seen to be clearly, but not exclusively, located within certain parts of the organization. In addition to corporate and division management, the MCS was perceived as enabling in those parts of the company that were previously parts of some other larger organization.

Differences in the Perceptions of the MCS

Next, we focus on comparing the perceptions of the MCS among the 13 BUs. We found that those BU managers used to working in large organizations often perceived themselves to be independent-minded. Further, those BU managers considered the transparency of the MCS, the PMS, and/or the ERP system at Comet to be an improvement on that of the systems of their previous employers. In light of these findings, the background of the BU or manager would seem an important factor in explaining how an MCS is perceived during integration.

In Militia [previous employer], they did not present these figures monthly; here, they are reviewed more carefully, and things are presented more transparently. Comet has lower organization; you have, of course, responsibility, but you also have freedom … we report profit figures really openly all the time and where we are going; many have been surprised that we tell the employees the profit every month. (BU manager KK)

I previously worked (in a large technology firm) as a unit manager, let’s say that in Comet, we have very good MCS, this Digifinance, very real-time, very quick; you can see … I am very satisfied. (BU manager EH)

Others have quite similar measures, and many smaller firms run with fewer measures. (BU manager MM)

The coercive perceptions were typical in the business units that had previously been small, entrepreneurially driven companies. Those organizations had not used a formal MCS before Comet acquired them. The fact that the business units are geographically separate, operating as relatively autonomous business entities, each with its distinct organizational history with unique culture and working practices, may enforce the meaning of background in explaining differences in perceptions between the units.

Because people engage in sense-making retrospectively, they will consider a new situation in relation to prior experiences. Those managers who worked in entrepreneurially driven small businesses that were not incorporated into larger distant groups and which did not use formal MCSs, like the PMS and budgeting in our case, reported that the acquisition by Comet created a new, surprising and sometimes confusing situation. Those managers were also unused to being pressured to meet targets set by group management and having to cooperate with other business units to streamline the group-wide value chain.

Unit managers are production-oriented people … e.g., NN was earlier a foreman in Militia … then a production manager, and then a unit manager in our house. Suddenly he got the budget responsibility. But the starting point is the production orientation. In some other units, it is even stronger. (Gives an example) MM was a departmental foreman at XX company and came to us (post-acquisition) in 2003. (Division Manager JI)

This situation was new for managers used to working in safe conditions with a familiar entrepreneurial owner in the next room. Their previous firm probably had clearly defined customers, products, production-oriented hands-on management, and no numbers to worry about other than production volumes and order reference numbers.

The situation is even more understandable in light of the identity threat (Maitlis & Christensen, 2014). The managers in question had based their whole work identity on being local production men, knowing their production facilities, machines, stockrooms, and all the blue-collar staff by name. Their work identity was based on being the trusted man of the entrepreneurial owner who also knew the product and the customers’ needs.

I think that I get along well with the people in this yard, and I can go to discuss things with anybody. (BU manager JP)

We started here with a very small one and slowly grew, so we did not have any systems. Financial issues were kind of ‘grid paper bookkeeping’ … we had no clear financial control.… No, we have these monthly reports, they may be good, but the monthly period is too short … quarterly report would be better … it takes time for paperwork, one-third or even half (of my time). (BU manager MR)

I mean, let’s say this (our unit) managerial meeting. I haven’t seen this s presented in any form anywhere. (BU manager LK)

The operation was remarkably simpler. In practice, we went to the desk of the owner-manager and reported what the problem was. (BU manager PYR)

Business unit managers felt the enterprise founders they worked for trusted them, but now had to complete report templates and send them to headquarters and accordingly were monitored. From this perspective, it is highly understandable that those managers make sense of the chaos, restore their identity, and attach meanings related to surveillance, imposing pressure, or pointless reporting.

I really don’t understand why it (monthly report) is prepared. I don’t believe … it is nicely disseminated to us, but there is nothing you don’t know before you get it.… It comes from (HQ). I didn’t understand when it came the first time. Then I started to wonder what its meaning was. And I don’t know. None of us gets anything from it. (BU manager MR)

We didn’t have to, earlier, to dig into these financial matters … NN (entrepreneur) started this machining, and there is something left from this period … when we got acquired 4–5 years ago, quite some rumble started. More should be monitored and investigated these issues (measures), and then we had this small firm mentality that if there is some cash, we are profitable. Here I have got the (duty) of number monitoring … maybe this is the other extreme, that figures are followed even too carefully. (BU manager MR)

Every BU manager’s perception of controls has importance because their action is based on how they understand the managerial meaning of the new controls. The change was not so dramatic for BU managers with prior experience in formal control systems like budgeting and PMS and experience working in a larger group. They were used to being formally controlled and measured and using the MCS to manage their business. They had also experienced the distance, formality, distrust, and positive power of numbers earlier. For them, this was business as usual, which was reflected in their enabling-type perceptions of the MCS and also more successful compliance in terms of implementation and more intensive use of the MCS. Managers who earlier worked in large Militia groups perceived the Comet control style was even less formal, bureaucratic autonomous and flexible.

Financial control has not changed much since we were removed under Comet … these kinds of measures were already in Militia … they are familiar measures. (BU manager AV)

Militia was a rigid organization. In Comet, the situation is flexible, and decision-making is fast and easy. ( Division Manager EK)

Discussion

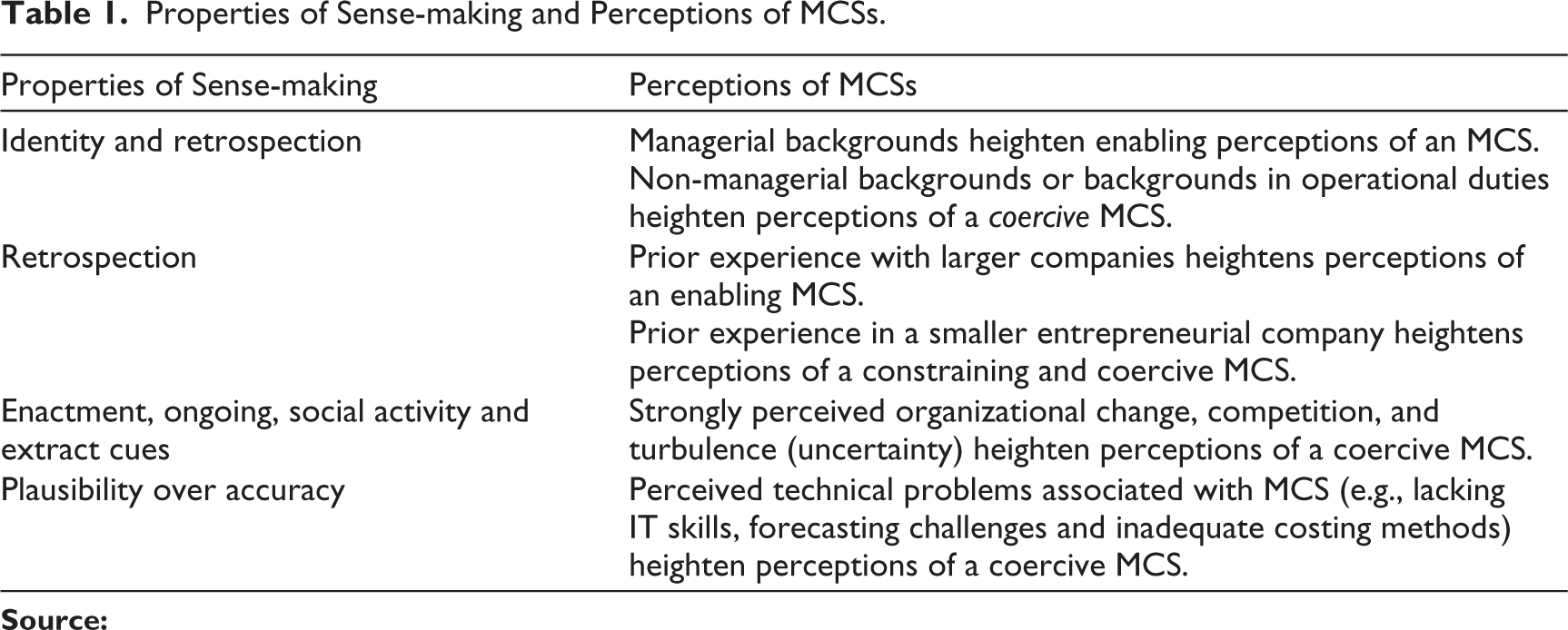

This study examined how BU managers immersed in post-acquisition integration perceived a formalizing MCS. Further, we explored the connection between perceptions of the MCS by drawing on sense-making theory. The most obvious finding to emerge from this study is that the perception of the corporate MCS varied among BU managers (see Table 1).

The evidence from this study suggests that some properties of sense-making may encourage perceptions that an MCS is a coercive tool. First, BU managers with a background and identity tied to production workflow management in a small company tend to perceive MCS that way. Second, that perception tends to be exacerbated by a high degree of perceived organizational change, competition, or turbulence. Third, perceived technical problems associated with the MCS—such as forecasting challenges, inadequate costing methods, or indeed lacking IT skills—go hand in hand with perceptions of an MCS as coercive. According to our findings, the design and use of MCS, which is perceived to be coercive, does not acknowledge local practices and existing skills (Wouters & Wilderom, 2008). Difficulties in forecasting and in envisioning different future states appears to be related to performance evaluation based on future performance expected by the top management (Palermo, 2018).

The BU managers emphasizing the coercive meaning of controls had worked in small workshops where the owner was present, and there was little need for formal controls. For them, the acquisition led to several changes. For many, this was a considerable shift from production to profit responsibilities and general management of a business unit in a fast-growing company. The new role brought new requirements relating to IT skills, financial targets, and the responsibilities of formal bureaucracy. This finding indicates the presence of an identity threat and the importance of retrospection, where meanings are attached to new events based on previous experience (Gephart et al., 2010; Maitlis & Christensen, 2014; Weick, 1993).

The findings from this study make several contributions to the current literature. First, this study supports the growing understanding of the importance of employee perceptions on the functioning of an MCS and the behavioural outcomes intended by the top management (Ahrens & Chapman, 2004; Tessier & Otley, 2012; Wouters & Wilderom, 2008). Second, we add to this discussion by focusing on the BU managers in the context of a company that grows rapidly through several new acquisitions per year. In the context of one offshore acquisition, Väisänen et al. (2021) found trust building between people was crucial for cementing enabling perceptions of the new control practices of the acquiring company. This study, however, analysed perceptions of MCS more on the level of individual managers and suggested that the differences in perceptions rely on the properties of sense-making. We argue that disciplined flexibility in post-integration context calls for attention to be focused on those managers who have no previous experience of large organizations. They should be allowed a learning process aimed at locally plausible planning practices that are based on the company’s MCS and bring about efficiency and flexibility (Ahrens & Chapman, 2004; Palermo, 2018; Väisänen et al., 2021). Third, this study draws on sense-making theory in organizations and thus contributes to the literature on sense-making in accounting. Previous research usually discusses the meaning and importance of management accounting systems for sense-making in organizations (Boland, 1993; Tillmann & Goddard, 2008). However, this study focuses on how managers make sense of an MCS. Accordingly, our findings on the linkages between the properties of sense-making and managerial perceptions of an MCS add to the more current discussion of the incompleteness of management accounting systems (Jordan & Messner, 2012).

Properties of Sense-making and Perceptions of MCSs.

Conclusion

Understanding how managers and employees perceive MCSs is essential to assist managers in decision-making and to direct employee behaviour (Tessier & Otley, 2012). Previous research has sought to explain what features within an MCS advance enabling perceptions to combine efficiency with flexibility (Ahrens & Chapman, 2004). The current research identifies a few contextual properties of sense-making that may strengthen enabling or coercive perceptions of an MCS. Overall, this study strengthens the idea that perceptions of MCSs are relevant when designing an MCS for both efficiency and flexibility.

Further work is needed to fully understand the implications of different management situations on how MCS is perceived and acted upon these perceptions. Further research is also needed to closely examine links between the properties of sense-making and the perceptions of MCSs.

Footnotes

Declaration of Conflicting Interests

The authors declare no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

List of Interviews, Research Site Visits and Workshops.

| Interviews | |||

| Name | Position | Date | Duration |

| JI | Division managera | 15 August 2008 | 1h 29min |

| EK | Division managerb | 30 July 2008 | 1h 27min |

| JP | Division managerc | 2 July 2008 | 1h 17min |

| AV | Business unit managerd | 15 August 2008 | 1h 03min |

| EH | Business unit managere | 14 August 2008 | 1h 20min |

| EP | Business unit managerf | 14 August 2008 | 1h 20min |

| JP | Business unit managerg | 24 July 2008 | 1h 40min |

| KK | Business unit managerh | 15 August 2008 | 1h 20min |

| LK | Business unit manageri | 14 August 2008 | 1h 43min |

| MRam | Business unit managerj | 7 July 2008 | 1h 19min |

| MM | Business unit managerk | 25 August 2008 | 1h 10min |

| PYR | Business unit managerl | 25 August 2008 | 1h 38min |

| MRai | Business unit managerm | 10 July 2008 | 1h 23min |

| SR | Business unit managern | 25 August 2008 | 1h 45min |

| TK | Business unit managero | 9 September 2008 | 1h 20min |

| JR | Business unit managerp | 15 August 2008 | 1h 00min |

| Meetings with CFO and COO | |||

| Name | Position | Date | Duration |

| MP | COO, Chief operation officer | 2 April 2008 | 2h 00min |

| ML | CFO, Chief financial officer | 9 June 2008 | 1h 30min |

| ML | CFO, Chief financial officer | 4 September 2008 | 1h 30min |

| ML | CFO, Chief financial officer | 10 December 2008 | 1h 30min |

| ML | CFO, Chief financial officer | 15 April 2009 | 1h 30min |

| ML | CFO, Chief financial officer | 20 October 2009 | 1h 30min |

| ML | CFO, Chief financial officer | 10 February 2010 | 1h 30min |

| Workshops | Date | Duration | |

| MJ | Business controllerq | 2 September 2008 | 2h 30min |

| MP | Chief operation officerr | 30 September 2008 | 1h 30min |

aFormerly manager in large militia group

bFormerly manager in large militia group

cFormerly entrepreneur in small machine shop

dFormerly part of large militia group

eFormerly small machine shop

fFormerly small machine shop

gFormerly small machine shop

hFormerly part of large militia group

iFormerly small machine shop

jFormerly small machine shop

kFormerly part of large Sava Group

lFormerly small machine shop

mFormerly small machine shop

nFormerly medium-sized machine company

oFormerly medium-sized machine company

pFormerly part of militia group Workshops

qProduction site visit

rPerformance measure workshop