Abstract

Credit risk is one of the most important risks faced by lenders and can affect not only their financial health but also economic growth and financial stability. It is therefore crucial to assess the potential losses from credit risk as conservatively as possible and to manage it effectively. A systematic review of the academic literature was conducted to answer these questions. The results of the review showed that models that examine the relationship between sustainability and credit risk most commonly use the environmental factor as an indicator of sustainability (72% of the studies analysed). The Altman Z-score was the most used credit risk estimator in the reviewed studies. The second most popular estimate was bond and credit default swap spreads. In summary, the studies reviewed show that lending to more sustainable companies improves: The quality of the loan portfolio and reduces credit risk, leading to better credit ratings, and lower borrowing costs for the lenders themselves; lenders’ reputation, which makes it possible to attract a larger number of depositors and investors. However, the lender should consider not only the sustainability of the borrower but also the sustainability of the loan collateral, which is seen as a credit risk mitigant.

Introduction

Financial sector firms operate in a very dynamic environment, influenced by factors such as digitization, innovation, changing consumer needs, increasing competition and evolving regulatory requirements. To ensure financial stability and sustainable growth in the financial sector, it is crucial that financial intermediaries manage the risks they face appropriately and efficiently. Credit risk is one of the main risks faced by the financial sector (Alzeaideen, 2019; Anagnostopoulos et al., 2018; Isnurhadi et al., 2023; Khan et al., 2021; Phan Thi Hang, 2023; Umar et al., 2021; Singh et al., 2023). This is because, in many cases, lending is the main business of banks and, consequently, interest on loans is the main source of their income (Phan Thi Hang, 2023; Singh et al., 2023). Income diversification of financial sector firms (Phan Thi Hang, 2023; Taylor, 2022; Taylor et al., 2022), credit risk hedging (Moellmann et al., 2020) or an effective credit risk management model (Anagnostopoulos et al., 2018; Singh et al., 2023) could be a key tool to manage and mitigate credit risk, ensure sustainable lending and minimize the losses that borrower defaults could cause.

In order to manage credit risk appropriately and effectively, it is important to consider all factors that may give rise to credit risk exposure. The risk management process, therefore, needs to be dynamic and continuously reviewed as new sources of risk emerge. Incorporating environmental, social, and governance (ESG) factors into credit risk assessment is one of the latest challenges in credit risk management. This is because it is still a relatively new topic, and there is still a lack of objective data to assess the sustainability of borrowers. There are also problems with methodology or consensus among international organizations on common definitions related to sustainability and ESG.

As a result of these challenges, some financial institutions are still not responding to calls from international organizations to contribute to sustainability and integrate ESG factors into their business. This could expose them to fines or higher regulatory capital requirements. As a concrete example of the integration of sustainability into credit risk management, the ECB sent a threatening letter to 20 banks at the end of 2023, warning them of fines (e.g., 5% of their average daily turnover) and higher capital requirements if they did not take climate change risks into account in their activities.

Increasing pressure from international organizations, as well as from investors and shareholders, to take ESG factors into account in lending activities means that ESG is emerging as a new direction in credit risk management. It is also leading to the emergence of related research that examines whether ESG factors have an impact on credit risk and, if so, how they can be incorporated into credit risk management. As there is a knowledge gap in systematizing the results of fragmented studies on sustainability in the context of credit risk, the main objective of this article is to systematize the results of studies and present the best ways (indicators) to incorporate sustainability into credit risk models.

The first section describes the methodology of the systematic literature review. The second section provides an overview of the key indicators used in the models to reflect sustainability and credit risk. The third section describes how lending to more sustainable entities affects the credit risk of the lender. The fourth section provides a synthesis of existing research on where future research could focus.

Methods

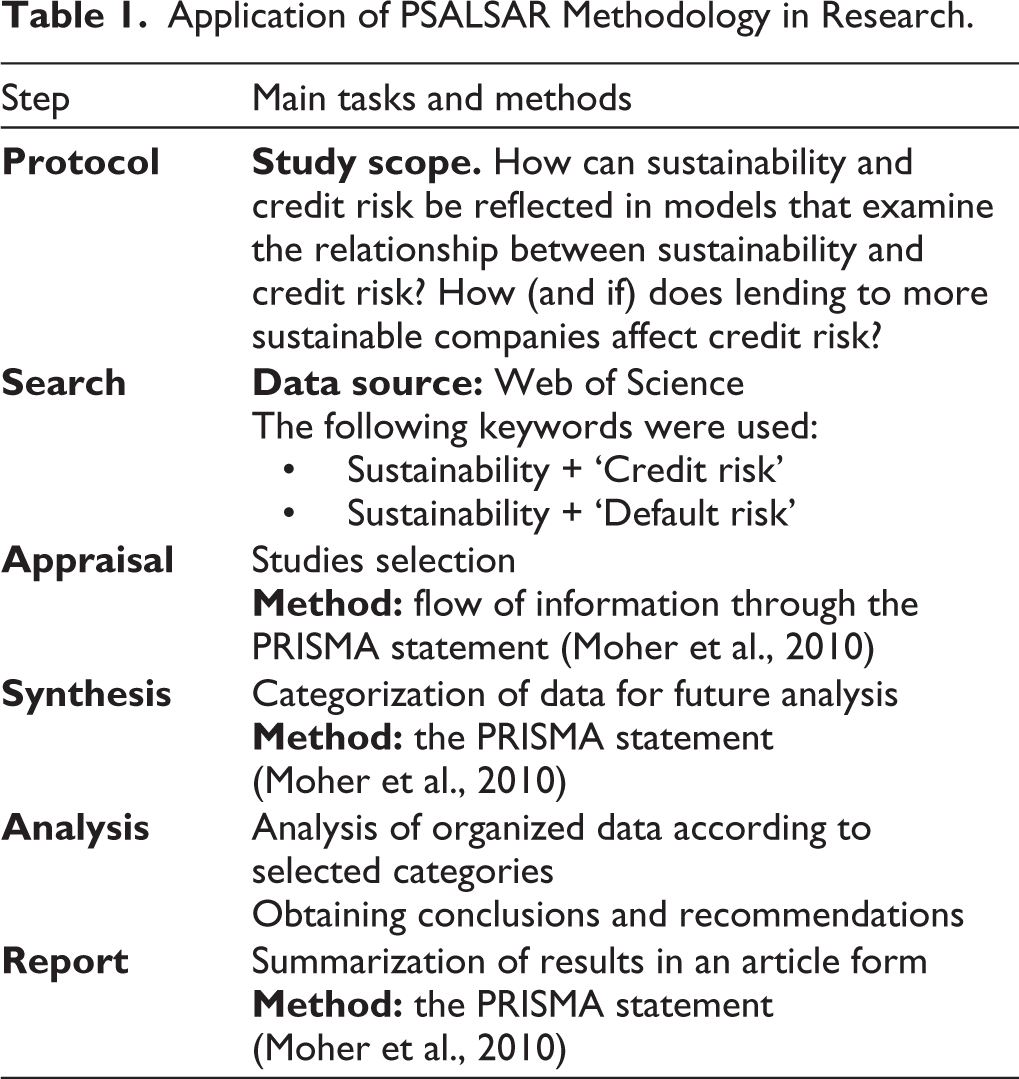

This article conducts a systematic review of the scientific literature based on the PSALSAR methodology developed by Mengist et al. (2020) (Table 1). Based on scientific articles in the Web of Science database, this methodology has been used 17 times since 2020 to perform a systematic literature review. The increasing popularity of this methodology can also be observed. For example, the PSALSAR framework has been applied 13 times since 2023.

Application of PSALSAR Methodology in Research.

Using this methodology, Mengist et al. (2020) conducted a systematic literature review on ecosystem services in mountain regions, and Siksnelyte-Butkiene et al. (2021) reviewed energy poverty indicators etc. However, neither study looked at sustainability in the context of risk and, more importantly, did not analyse sustainability in the context of credit risk. The closest study to the topic of this article looked at corporate social responsibility (CSR) in the context of sustainability and suggested how CSR could be assessed for companies in the energy sector (Kasradze et al., 2023). Another study examined the challenges of the transition to low-carbon energy (Saraji & Streimikiene, 2023).

Researchers using the PSALSAR methodology aim to produce the most coherent, comprehensive, complete and objective literature review possible. This methodology includes the SALSA framework and the PRISMA framework. In other words, to the SALSA framework, Mengist et al. (2020) have added the two steps of the PRISMA framework: research protocols and reporting of results. In total, the PSALSAR methodology has six research steps.

Protocol: The main task in this step is to define the scope of the research.

Search: The main task in this step is to develop and implement a search strategy.

Appraisal: The main task in this step is to establish criteria for the inclusion and exclusion of scientific papers (20,383)

Synthesis: The main task in this step is to extract and categorize the data.

Analysis: The main task in this step is to report the results and finally to draw conclusions.

Report: The main task in this step is to state the procedure followed and to publicize the result.

Research protocol step. This step raises questions that need to be answered in order to achieve the objective of this research. The best tool to determine the scope of the research is PICOC (Siksnelyte-Butkiene et al., 2021), which is also used in this study.

How can sustainability and credit risk be reflected in models that examine the relationship between sustainability and credit risk?

How (and if) does lending to more sustainable companies affect credit risk?

Search step. Web of Science (WoS) is considered to be one of the most authoritative databases of scientific sources, so this research uses articles from this database. The search for academic sources is carried out using the keyword combination ‘sustainability’ + ‘credit risk’. As default risk is often used as a synonym for credit risk, a further keyword search is carried out in the search phase using the keyword combination ‘sustainability’ + ‘default risk’.

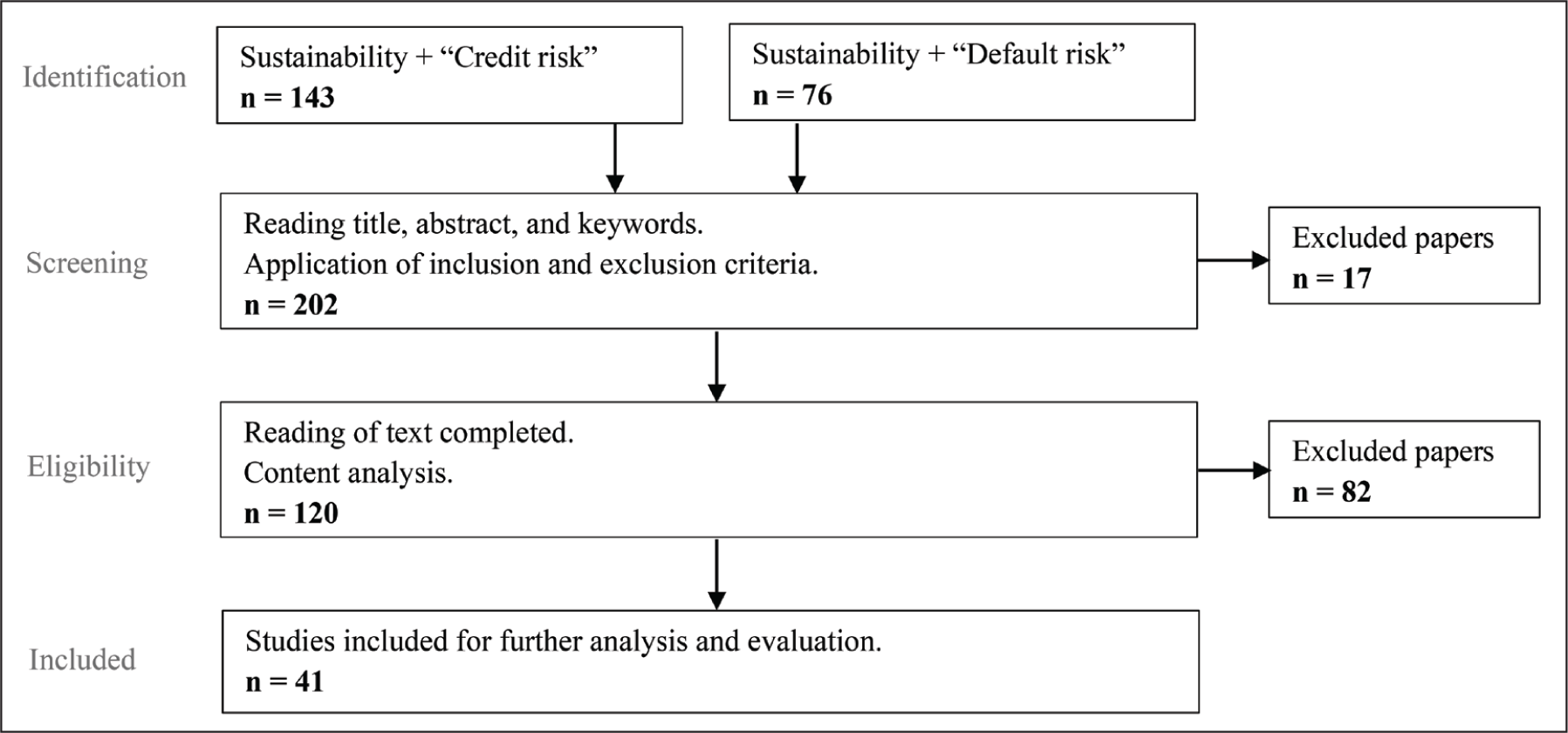

Appraisal step. Once the WoS database has been searched, further source selection is carried out using the PRISMA guidelines: identification of papers for screening, eligibility and included papers. (Figure 1)

After searching the database using keywords, articles that meet the following criteria are included in the next stage of the research: they are in English, and the keywords can be found in the title, abstract or keywords of the article. In addition, repetitive scientific sources are excluded from the sample, as are proceedings, retracted publications and book chapters.

In the identification phase, the keyword combination ‘sustainability’ + ‘credit risk’ finds 143 sources, of which 10 are proceeding papers and 1 is a retracted publication. There are also two sources in Spanish and one in Russian. The keyword phrase ‘sustainability’ + ‘credit risk’ yields 76 sources, of which 5 are proceeding papers, and 1 is a book chapter. There is also one source in French.

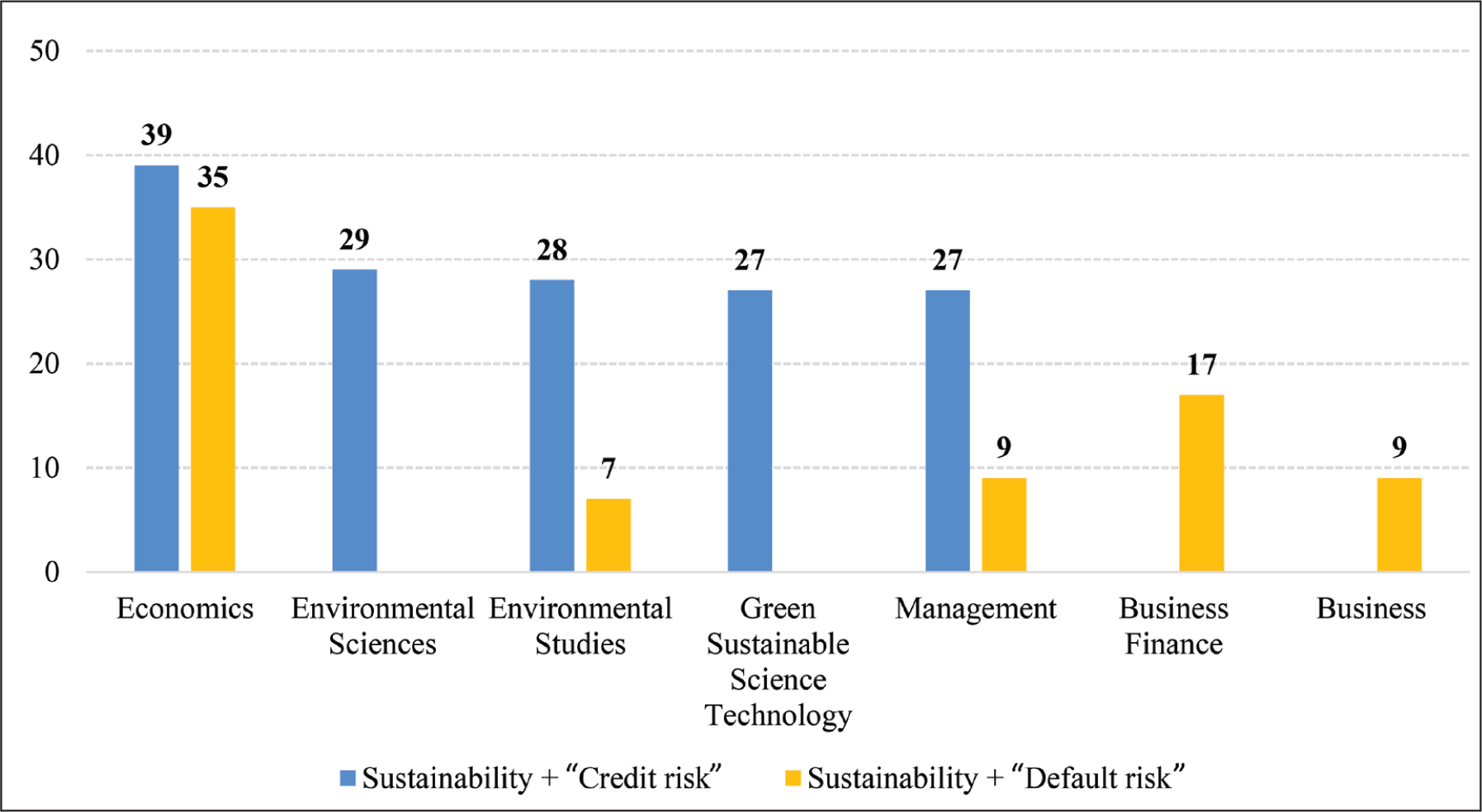

Most of the sources found in the database are economics-oriented (Figure 2). However, the keyword combination ‘sustainability’ + ‘default risk’ also touches on more finance-oriented topics: business and corporate finance. The sources cover the period from 2004 to 2024.

In determining keywords, the study drew on practices used in previous systematic reviews. Anakpo et al. (2023) and Siksnelyte-Butkiene et al. (2021) emphasized the importance of using more synonyms for keywords (but they must be precise) in order to identify as many related studies as possible. With this in mind, the widely used term default risk was chosen as a synonym for credit risk (this term was also used in the studies by Zhao and Chen (2022) and Aslan et al. (2021)).

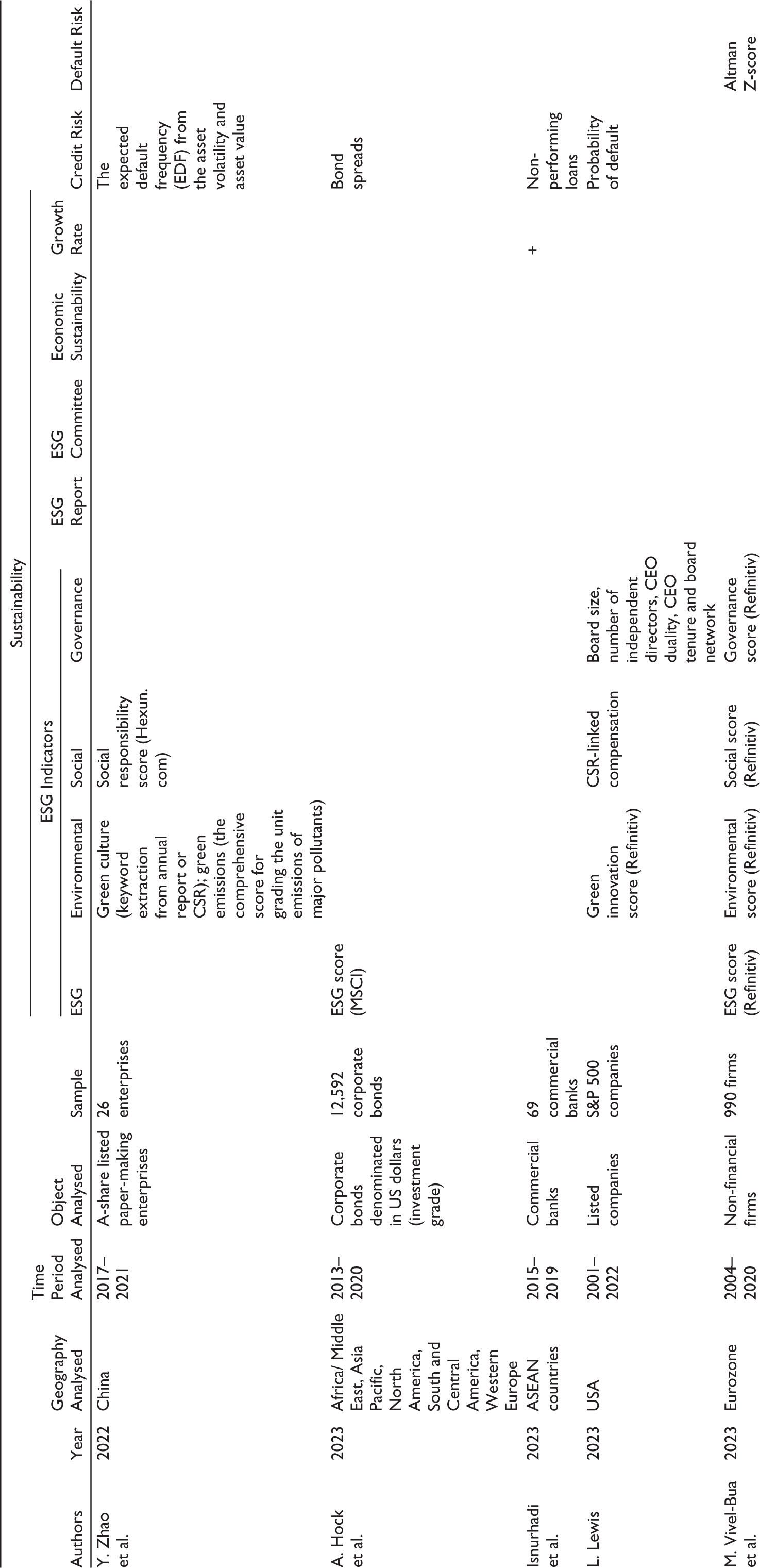

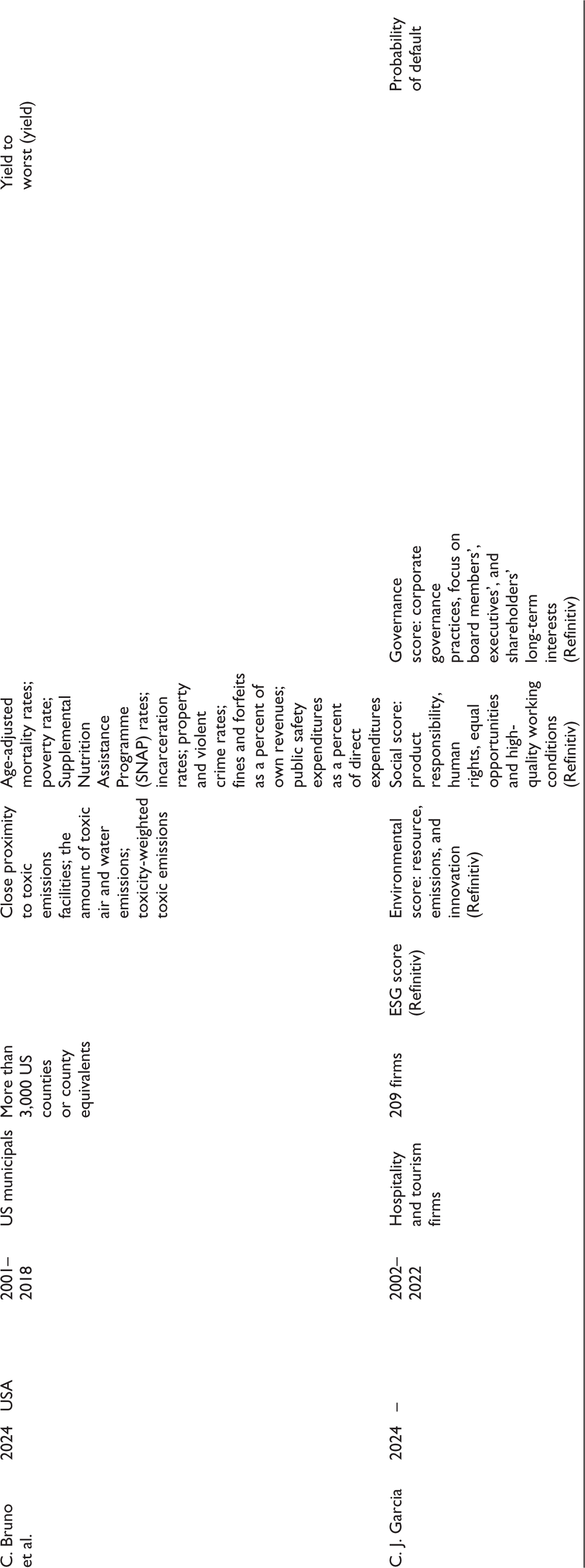

Synthesis step. In this step, the data from the collected academic articles are grouped into a number of categories. In order to determine which indicators are used to reflect sustainability and credit risk in the models, the data from the selected articles are grouped into the following categories: geography researched, time period analysed, object analysed, sample, sustainability, credit risk and default risk indicators used in the models, and conclusion of the study.

To determine how lending to more sustainable companies affects the credit risk of the lender, the selected articles are grouped as follows: the impact of sustainability and ESG factors on the creditworthiness and financial condition of borrowers; the impact of lending to more sustainable companies on the credit risk and financial condition of the lender; the impact of the lender on the economy and financial stability; and the impact of external factors on the financial condition of the lender.

Analysis step. In this step, the academic sources are analysed in order to answer the research questions.

Report step. This step presents the main findings of the systematic literature review. The 27-item checklist of the PRISMA statement is applied (Siksnelyte-Butkiene et al., 2021).

Review of Prior Systematic Literature on Credit Risk and Sustainability

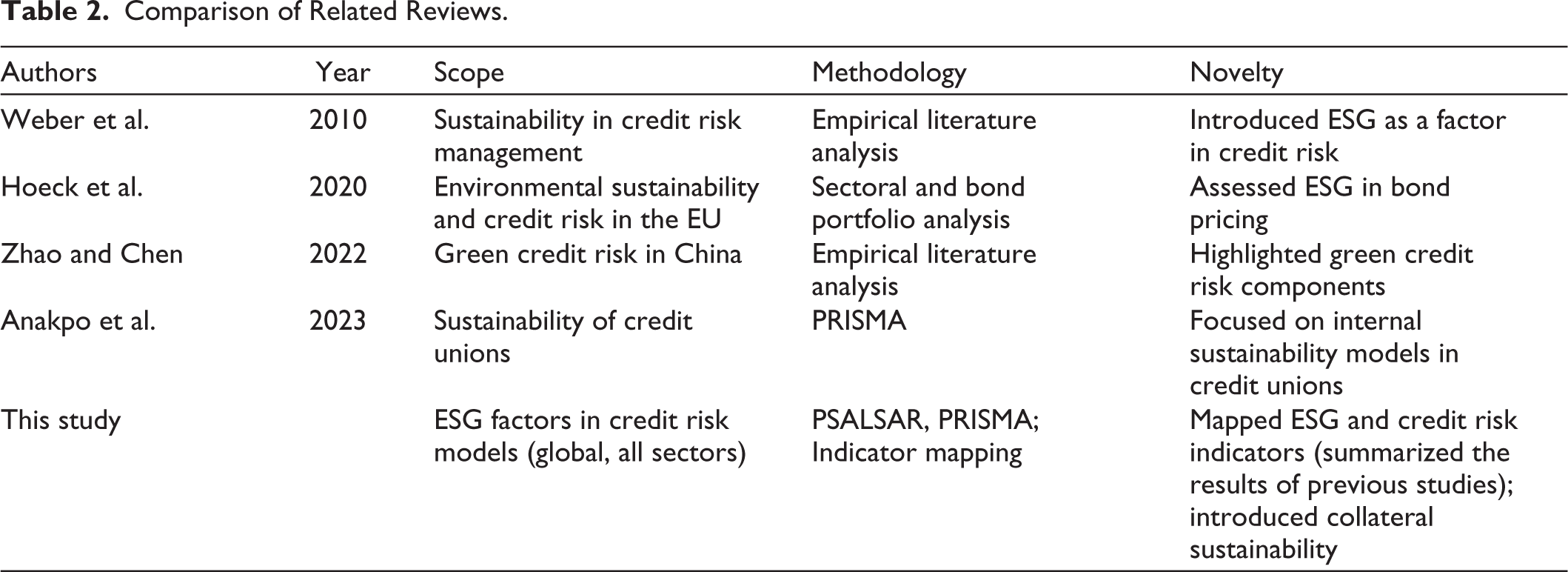

Several studies have conducted, or partially conducted, a systematic review of the scientific literature on the topic under analysis. One of the pioneers who argued for the importance of sustainability in credit risk assessment was Weber et al. (2010). Later, Anakpo et al. (2023) conducted a systematic literature review, but the focus was mainly on the sustainability of credit unions. The researchers also did not consider the importance of sustainability in credit risk assessment. Other researchers (Hoeck et al., 2020, 2023; Zhao & Chen, 2022) focused more on the relationship between environmental factors and credit risk, but did not conduct a comprehensive and structured review of ESG indicators and credit risk metrics (Table 2).

Comparison of Related Reviews.

Unlike previous studies, this study, using the PSALSAR methodology, synthesizes the findings and insights of previous studies and shows how sustainability is incorporated into credit risk models. It also identifies an unexplored area: the sustainability of credit collateral. This means that when assessing credit risk, it is necessary to consider not only the traditional metrics related to the borrower’s financial condition and the sustainability of its operations, but also the sustainability of the collateral. A list of sustainability and credit risk metrics is also provided, which will be valuable to researchers and practitioners seeking to assess and incorporate sustainability into credit risk models.

Novelty of This Study

Previous studies have focused on examining the impact of ESG on stock markets or on the overall financial performance of companies. This study (conducted through a systematic review of the academic literature) focuses on the integration of ESG indicators into credit risk models, particularly from the lender’s perspective.

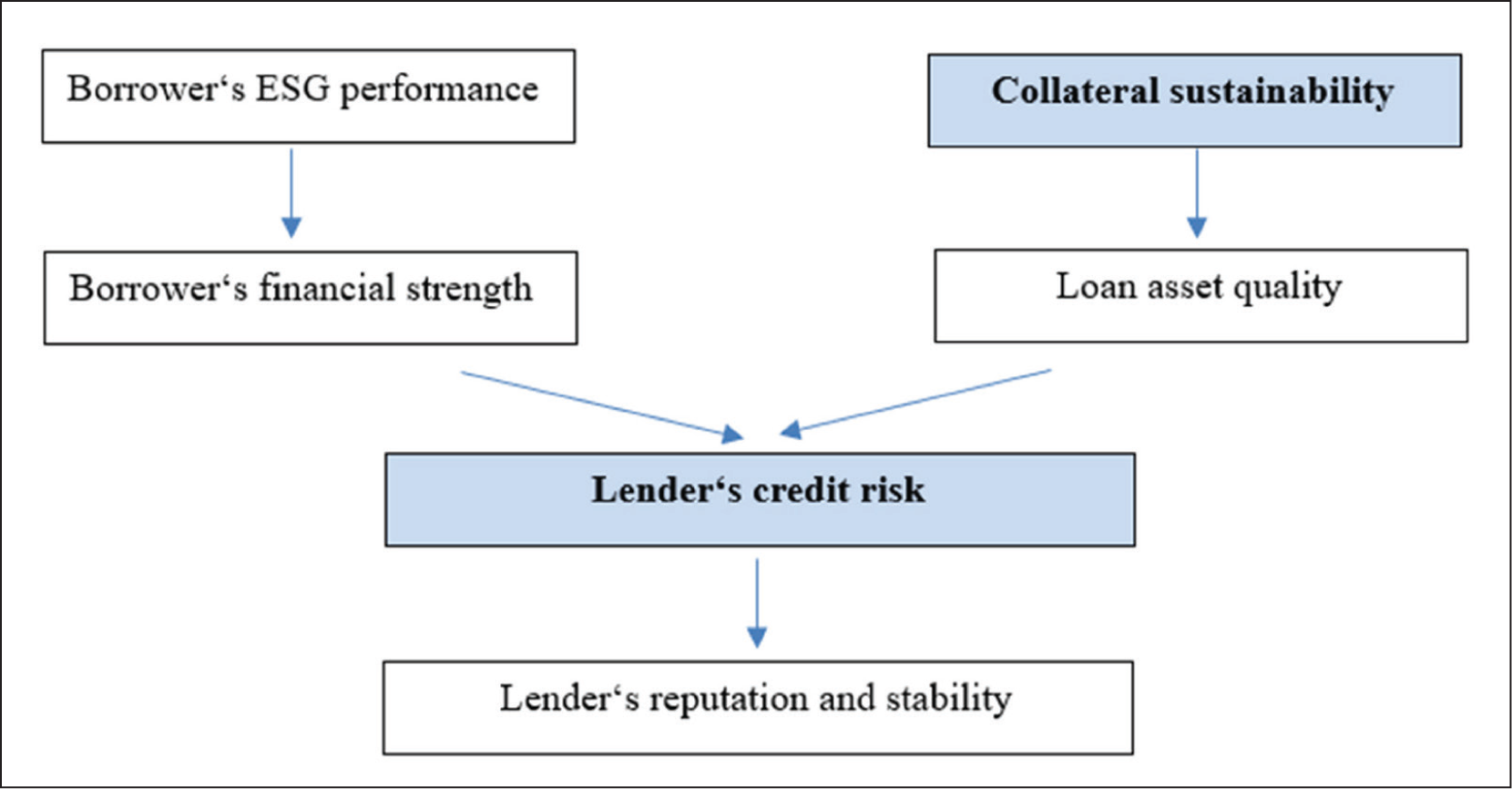

It should also be noted that the sustainability of loan collateral has not been examined. The purpose of collateral is to reduce the lender’s credit risk. However, if it is not valued conservatively enough (i.e., potential ESG risks are not considered), the lender may be taking on more credit risk than it would like (Figure 3).

Therefore, in assessing the lender’s credit risk through the prism of sustainability, two components could be distinguished, one of which would reflect the sustainability of the borrower’s operations and relate to the borrower’s financial position. The other would be related to the sustainability of the loan collateral and would reflect the quality of the pledged assets. All this, together with an additional assessment of regulatory requirements and compliance, would determine the lender’s credit risk. Accordingly, a more sustainable lending policy would have a positive impact on the lender’s reputation and financial stability (as the credit risk would be assessed more conservatively and the lender’s funding costs would be lower due to better credit ratings, attracting more investors). This suggests that considering ESG risks is not just a matter of regulatory compliance, but also a strategic opportunity for lenders to be more financially stable and competitive (especially now that the world is moving towards sustainability).

Another novelty is that none of the scientific articles (selected by keywords) applied the PSALSAR methodology (the closest was Anakpo et al. (2023), but they did not apply the PSALSAR methodology and analysed how sustainability is assessed in credit risk models: that is, they did not analyse credit risk specifically) in order to systematically review the sustainability and credit risk metrics used in the studies. A structured analysis methodology was used to distinguish between these metrics, adding transparency, reliability and completeness to the results obtained.

Key Indicators That Reflect Sustainability and Credit Risk

ESG is like a new strategic direction for business, which is certainly beneficial and potentially profitable, but it is also a new direction in risk management (Brogi et al., 2022). Incorporating ESG factors into credit risk assessment models is therefore one of the latest challenges for the financial sector, but it is also an opportunity to redirect credit to more sustainable borrowers and thus contribute to sustainable economic growth. This view is shared by other researchers who recommend that sustainability and ESG factors should be included in credit scoring models for borrowers (Alzeaideen, 2019; Anagnostopoulos et al., 2018; Badulescu et al., 2017; Cardillo & Chiappini, 2022; Moellmann et al., 2020; Palmieri et al., 2023; Singh et al., 2023).

The fact that the inclusion of sustainability and ESG factors in credit risk management models is one of the latest challenges for the financial sector is confirmed by the results of a study which showed that financial intermediaries operating in Greece take sustainability risk into account in their management of credit risk and non-performing loans, but only assess sustainability risks in a piecemeal manner. The fact that sustainability is taken into account only in individual steps and is not reflected in the strategy and key objectives of the banks was confirmed by the results of a study carried out by Badulescu et al. (2017), which analysed the Romanian case. All of this calls for new research that seeks to identify how sustainability can be integrated into all stages of credit risk management.

Most research on the link between sustainability and credit risk focuses on companies. However, the public sector also borrows to ensure the sustainable development of infrastructure (Bruno & Henisz, 2024; Padovani et al., 2018). Padovani et al. (2018) argue that local governments play a key role in the sustainable development of their communities. Therefore, they need regular funding to ensure their sustainable performance. Continued and increasing financing of local government operations, especially in the case of negative events such as credit rating downgrades, can lead to local government defaults and increased credit risk for lenders. To avoid this, improve creditworthiness and reduce financing costs, Padovani et al. (2018) identified the following as solutions for Italian local governments: increasing transparency of information and financial data, reducing criminal activity and increasing the frequency of external audits. Bruno and Henisz (2024) analysed the US case and found that improvements in ESG factors at the municipal level have a negative impact on the credit risk of municipalities.

The fact that sustainability (e.g., better ESG indicators) reduces credit risk has been confirmed by other studies. Most of the studies analysed looked at non-financial companies. In the case of China, for example, the companies analysed were particularly sustainability-oriented. De et al. (2019) have developed a model that can improve the sustainable development of electricity trading companies. Zhao and Chen (2022b) found that the interest coverage ratio, current ratio, asset–liability ratio and green emissions are the main factors influencing green credit risk in the paper industry. Other scholars have argued that green credit also has a credit risk component (Ozili, 2023; Zhao & Chen, 2022a; Zheng, 2015).

Some of the studies excluded financial companies from the data (Fernandez-Mendez & Pathan, 2022; Hoeck et al., 2020; Vivel-Bua et al., 2023). The reason for this is that, according to Hoeck et al. (2020), financial companies are directly exposed to low environmental risk. They are indirectly exposed to these risks through their loan portfolios. This should be treated differently. Another reason for excluding financial companies was that credit risk assessment models differ between non-financial and financial companies.

Other researchers point out that the relationship between sustainability and credit risk may not be the same in different sectors. For example, one study found that the same improvement in ESG scores can have different effects on credit risk for different sectors. The researchers also stress that the resulting scores should be further adjusted to take into account whether the company being rated is included in a stock market index. The need to pay attention to the sector to which the rated company belongs is confirmed by the results of Palmieri et al. (2023). The study found that the default risk of companies in the energy sector is most strongly influenced by ESG indicators. The researchers also found that the impact varies over time.

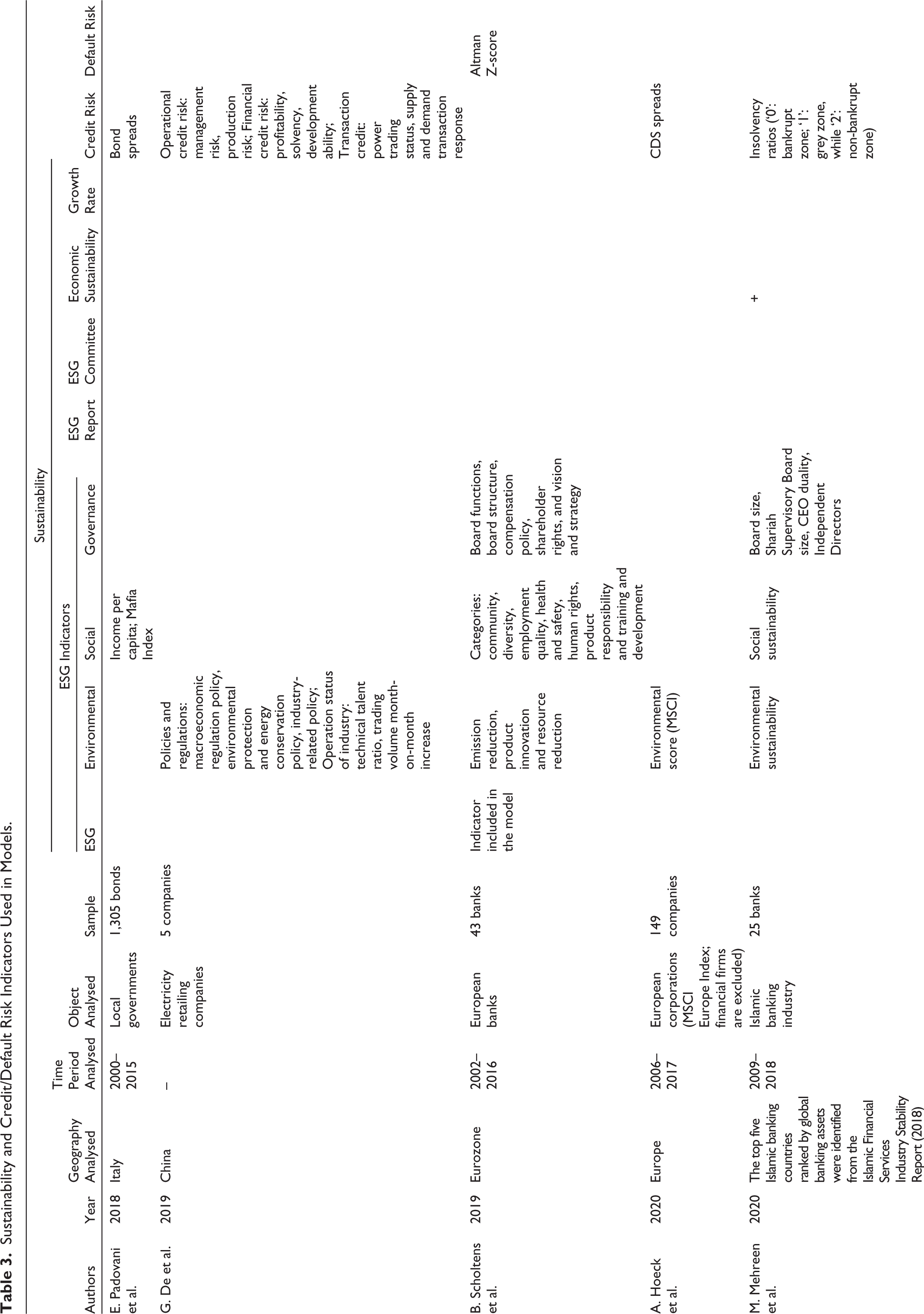

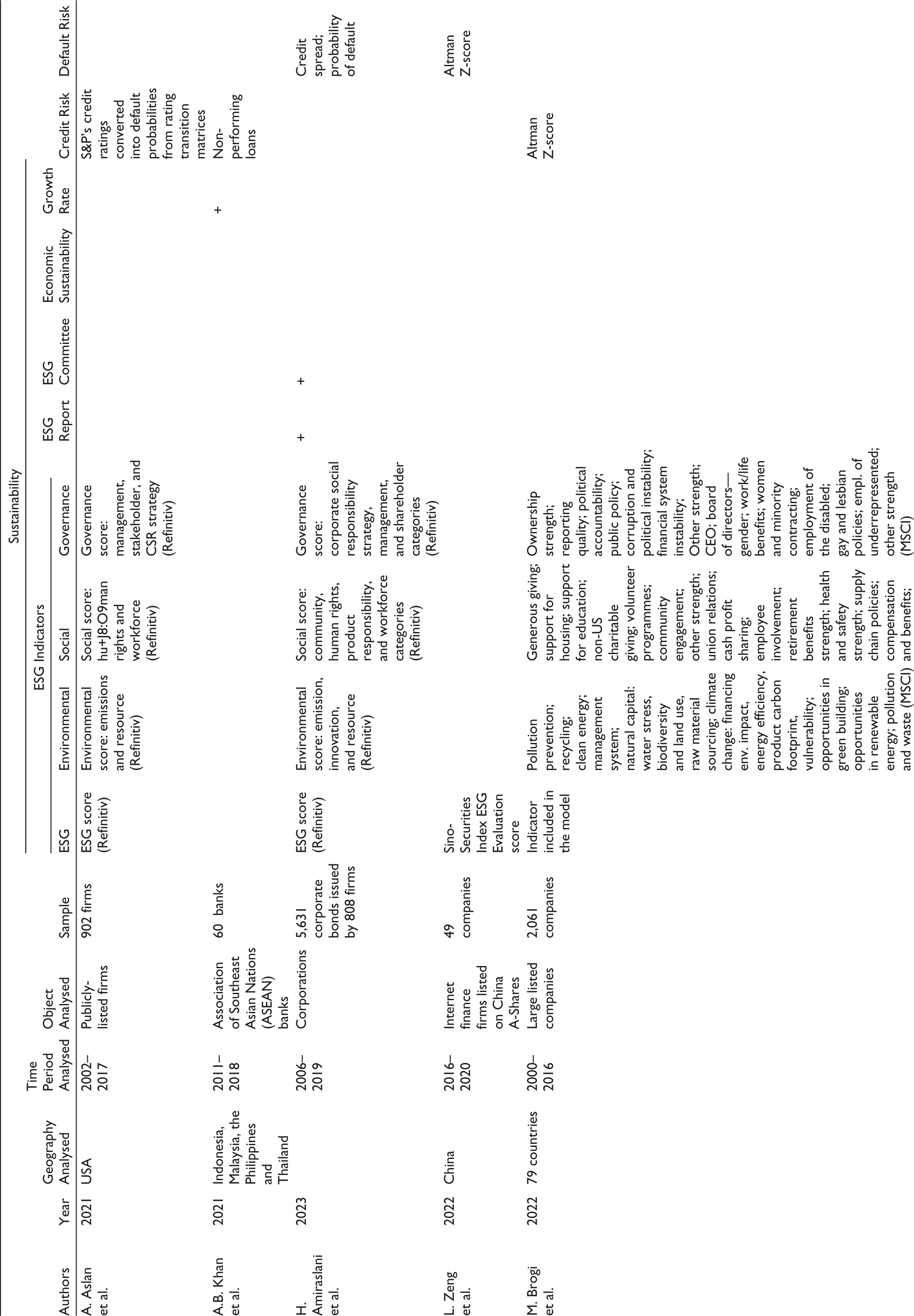

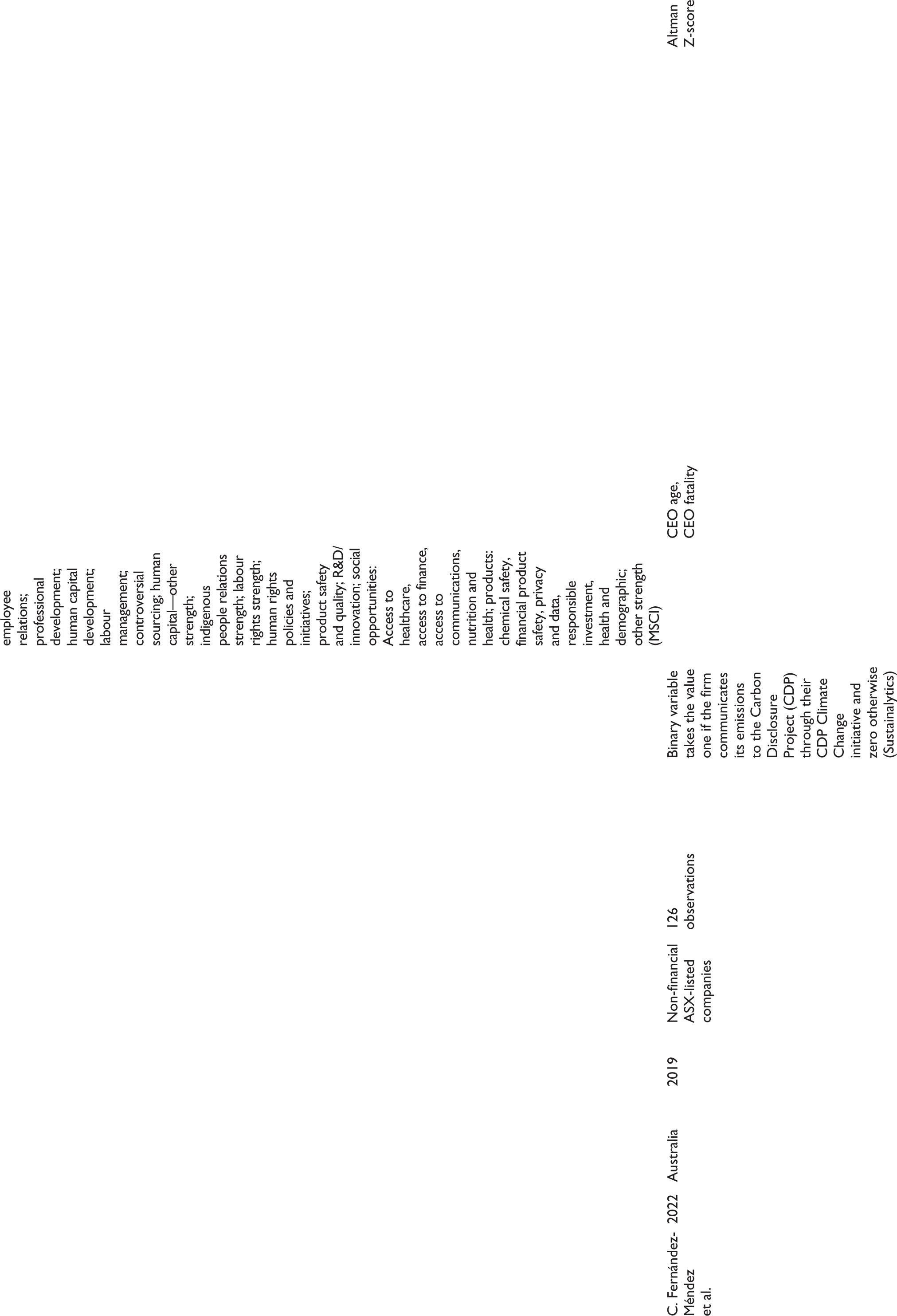

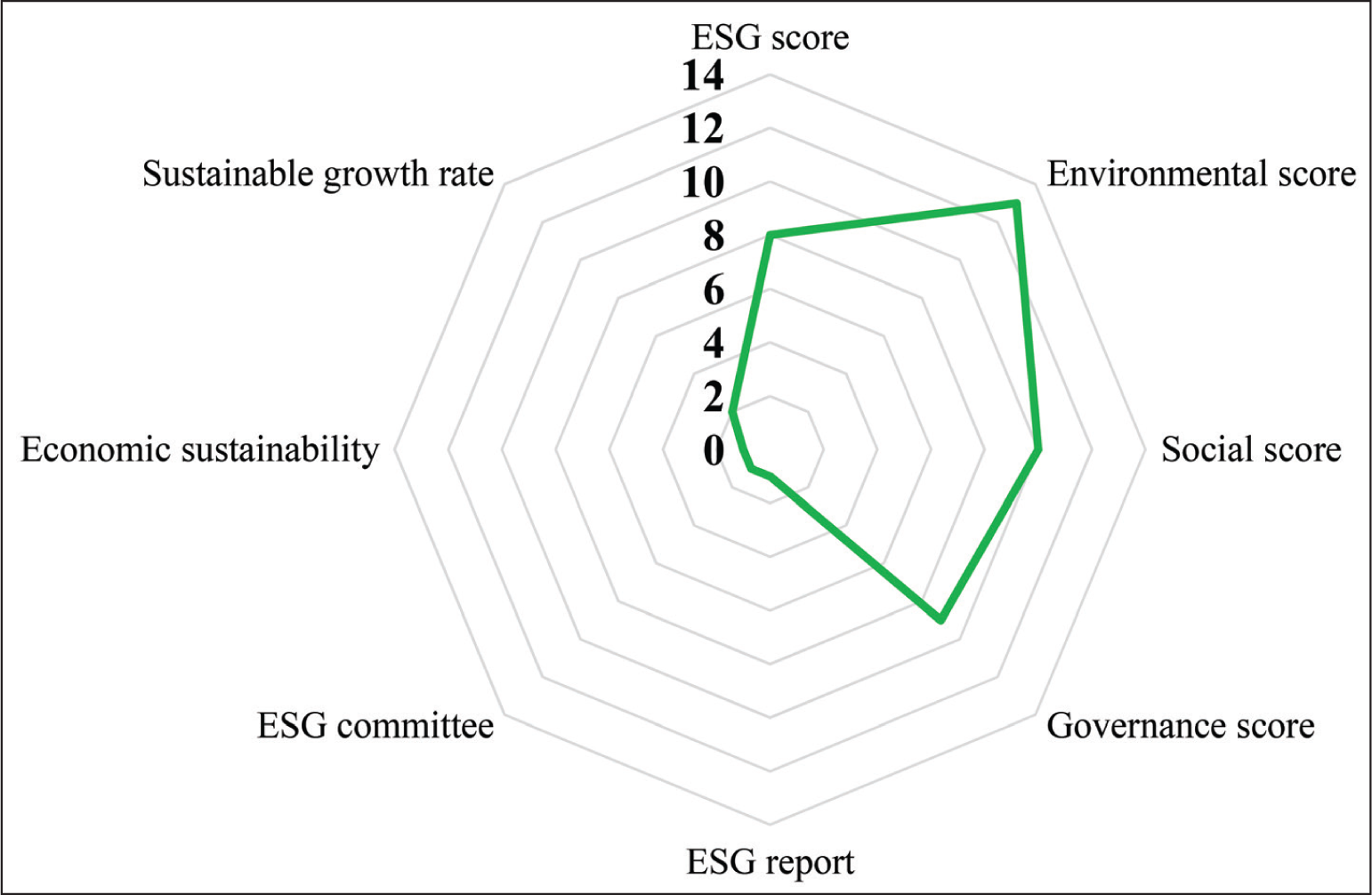

The indicators used in the models to reflect sustainability and credit risk are summarized in Table 3. When investigating the relationship between sustainability and credit risk, the researchers most frequently used environmental factors in their models (72% of the studies analysed) (Figure 4). Social factors are the second most popular (used in 61% of the studies analysed). Researchers also frequently use Refinitiv Eikon and MSCI ratings in their modelling. The analysis of the Islamic banking model included not only ESG factors but also economic sustainability (Mehreen et al., 2020), and Zhao and Chen (2022b) additionally analysed CSR reports to obtain the emissions of chemical oxygen demand, ammonia nitrogen (AN), sulphur dioxide (SO) and nitrogen oxides (NO). Isnurhadi et al. (2023) analysed the sustainable growth rate of the banking sector and therefore considered three different growth rates: Higgins’s SGR, Ross’s SGR and Van Horne’s SGR.

Sustainability and Credit/Default Risk Indicators Used in Models.

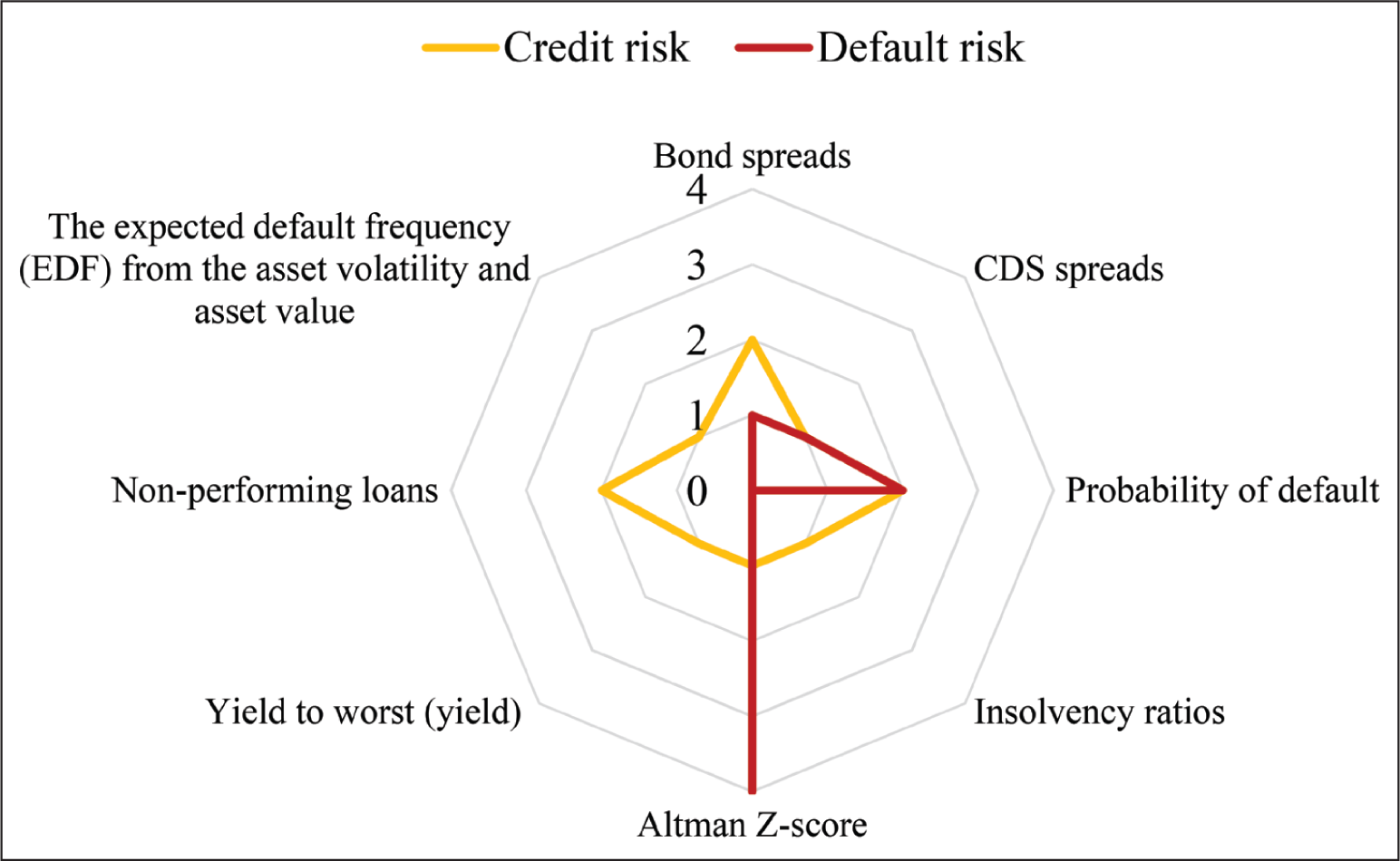

The Altman Z-score is the most commonly used credit risk estimator in the reviewed studies (used in 28% of the analysed studies) (Figure 5). The majority of studies using the Altman Z-score were found using the keyword ‘sustainability + default risk’. The second most polarized estimate was bond and CDS spreads (used together in 28% of the analysed studies). The probability of default is also one of the most popular credit risk estimates. Aslan et al. (2021) obtained this measure by converting S&P credit ratings into probabilities of default.

The Impact of Lending to More Sustainable Companies on the Credit Risk of Lenders

Failure to take sustainability into account when assessing the creditworthiness of a borrower can contribute to an increase in credit risk for the lender. Lending to more polluting entities or investing in more polluting projects may worsen the quality of the loan portfolio or the overall quality of the assets held and the financial position through cash flows, as the creditworthiness of such companies would not be assessed conservatively. This means that not all potential risks to the borrower would be taken into account. For example, if environmental risks were to materialize, there would be a greater likelihood that such a borrower would be more exposed to negative consequences and possibly unable to meet its obligations. This could increase the likelihood of liquidity risk for the lender. Thus, the environmental risk of the borrower could become the financial risk of the lender (Anagnostopoulos et al., 2018).

But even a decision to engage in more sustainable activities can have negative consequences for a company’s creditworthiness. For example, demands from the borrower’s shareholders, customers or policymakers to switch to more sustainable activities may temporarily worsen the borrower’s financial position and lead to an increased likelihood of default, as this often entails significant restructuring costs (e.g., curtailment of activities, reduction of high-emitting energy sources), which may have a negative impact on the borrower’s financial position (Cormack et al., 2020; Palmieri et al., 2023).

Lenders seek to mitigate credit risk in some cases by providing loans with collateral. Therefore, to manage credit risk effectively enough, lenders should also assess the sustainability of the collateral at this stage, as the value of the collateral could also be affected in the event of unexpected adverse events (Anagnostopoulos et al., 2018). This means that the value of collateral may decline and no longer be a source of credit risk mitigation. This brings in market risk, which determines the price at which the collateral could be sold in the market if necessary.

The risks are closely related, and as mentioned above, failure to consider sustainability in the credit risk assessment process can increase the likelihood of a lender’s liquidity risk. Lending to or investing in unsustainable and less socially responsible entities could also lead to reputational damage, which could also lead to the lender’s bankruptcy. For example, if a lender were to lend to an entity involved in terrorist financing, this could adversely affect the lender’s market capitalization, lead to a decline in depositors and trigger a variety of other reputational consequences that could worsen its financial health.

Operational risk also has a significant impact on the qualitative assessment of the sustainability of a potential borrower. For example, too little supervision of the staff assessing the creditworthiness of a potential borrower to make the most objective decisions (Alzeaideen, 2019; Mehreen et al., 2020), or an error in the model used to assess the borrower’s credit risk. All of these can contribute to an increase in the lender’s credit risk.

Compliance risk can also increase a creditor’s credit risk, especially if the creditor does not familiarize itself with the updated requirements or does not comply with the prudential requirements for its credit risk management. For example, the lender would not hold sufficient regulatory capital or would not take into account the requirements to incorporate ESG factors into credit risk assessment models. For example, at the end of 2023, the ECB warned of possible fines and higher capital requirements for banks that do not take climate change risks into account in their activities.

Not only do policymakers’ calls for operational processes to consider ESG risks underscore the importance of more sustainable practices, but research has also shown that more sustainable practices reduce credit risk (Aslan et al., 2021; Cardillo & Chiappini, 2022; Hoeck et al., 2020; Palmieri et al., 2023; Pizzi et al., 2020; Ricco & Bianchi, 2022; Su et al., 2022; Weber et al., 2010). Thus, one way to manage credit risk more effectively would be to assess borrowers more conservatively in terms of their exposure to ESG risks.

Most of the research reviewed emphasizes that more sustainable performance leads to better credit ratings, which in turn leads to lower borrowing costs. For example, Padovani et al. (2018) studied at what factors that influence local government borrowing conditions. In other words, what factors have an impact on a municipality’s sustainable development? The researchers found that local governments in Italy that are highly financially dependent on the state, receive relatively little income from their direct activities and operate in high-crime areas have higher bond-related costs than governments that do not have these characteristics. Researchers argue that they can reduce their financing costs by providing transparent financial information to potential lenders, reducing criminal activity and increasing external audits.

Cardillo and Chiappini (2022) analysed companies in different countries between 2000 and 2016. According to the researchers, companies with better ESG performance also have better credit ratings. Hoeck et al. (2020) study examining the impact of environmental sustainability on the credit risk of European non-financial companies from 2006 to 2017 found that more sustainable companies have a lower credit risk premium if they have better creditworthiness. Mehreen et al. (2020) argued that, according to the stakeholder theory, companies that integrate sustainability into their operations are less likely to go bankrupt due to better financial performance. The fact that better ESG performance improves the creditworthiness of debtors and thus reduces the likelihood of default has been confirmed by other studies (Aslan et al., 2021; Bruno & Henisz, 2024; Palmieri et al., 2023; Ricco & Bianchi, 2022; Weber et al., 2010). Vivel-Bua et al. (2023) found that the size of the borrower is also an important criterion. The researchers found that small and medium-sized companies have a positive impact on their default risk due to their better ESG performance, while for large companies, the relationship is the opposite.

To summarize the studies reviewed, lenders can reduce credit risk by lending to more sustainable companies, not only by lending directly to more sustainable companies with better credit ratings, but also by having a responsible lending policy towards sustainability (Su et al., 2022), which further enhances the lender’s reputation. For example, a lender can mitigate credit risk not only by considering the risks posed by ESG factors when assessing a borrower’s creditworthiness but also by implementing a sustainable lending policy itself. For example, by not financing unsustainable sectors or by lending to less sustainable companies at higher interest rates.

Zheng (2015) argues that the low-carbon economy creates more market opportunities and higher margins for lenders. For example, commercial banks in China have introduced green credits to finance greener projects as part of their efforts to contribute to a sustainable economy. Although green credits lead to sustainability, they still have a credit risk component, as risks are never eliminated, only mitigated (Zhao & Chen, 2022a; Zheng, 2015). According to researchers, the Chinese authorities have a strong interest in issuing as much green credit as possible. State-owned banks are mainly used for this purpose, even though this increases their credit risk. The researchers found the opposite for non-state banks. Green credits were found to increase the profitability of non-state-owned banks and reduce their credit risk. The conclusion is that when the government does not interfere in banks’ lending policies and when lending is based on market, green loans reduce banks’ credit risk.

Zhao and Chen (2022b) conducted a study analysing the paper sector in China and found that the interest coverage ratio, current ratio, asset–liability ratio and green emissions are the main factors influencing green credit risk. ElBannan and Loeffler (2024) found that there is a significant negative relationship between green bond issuance and the future carbon intensity of non-financial corporations. This means that green bonds can help companies finance carbon reductions, but researchers have also highlighted that this does not result in measurable environmental benefits. Ozili (2023) has developed a sustainable (green) loan-loss provisioning system that aligns banks’ loan-loss provisioning with the Sustainable Development Goals. According to the researchers, more environmentally friendly companies need less provisioning, and less sustainable companies need more provisioning. This means that banks that lend to more sustainable companies will need less provisioning and therefore have more money to invest in their operations. Umar et al. (2021) highlighted the concept of the green financial intermediation channel and analysed the impact of carbon-neutral lending on the credit risk of eurozone banks from 2011 to 2020. The results showed that there is a negative relationship between carbon-neutral lending and the risk of borrower default. This means that banks are exposed to a lower risk of borrower default through carbon-neutral lending, as more sustainable borrowers have more stable income and cash flows. The results of the study remained the same regardless of bank size.

The fact that the size of banks does have an impact on their risk exposure was found by Khan et al. (2021). The researchers argued that large banks have more scope to diversify their risks. For example, they have a wider variety of borrowers, so their loan portfolio can be diversified across sectors, countries and currencies. According to Taylor et al. (2022), income diversification reduces risks and ensures a more sustainable and stronger financial position of banks. This is particularly important in times of crisis when the probability of borrower default increases, and interest income stagnates (especially when this is one of the banks’ main sources of income). Large banks also tend to have more effective risk management systems. In one study, researchers found that there is a positive relationship between bank size and diversification, which leads to lower credit risk because, for example, the loan portfolio is more diversified. Thus, while large banks have lower firm-specific risks, which may depend on the supply and demand for their products, they face higher systemic risks, which depend on the ability of other entities to meet their obligations (Isnurhadi et al., 2023; Khan et al., 2021).

Some scholars have analysed the relationship between sustainability and credit risk not in terms of how lending to more sustainable companies or incorporating ESG factors into borrowers’ credit scoring models can affect lenders’ credit risk, but rather in terms of how sustainable economic growth and financial system stability affect lenders’ credit risk.

Khan et al. (2021) analysed the impact of financial innovation and sustainable economic growth on the credit risk of Association of Southeast Asian Nations (ASEAN) banks from 2011 to 2018. The researchers found that both variables had a significant impact on credit risk. According to the researchers, financial innovation helps banks’ services to meet the needs of today’s consumers, which leads to economic progress. Therefore, when formulating financial policies, policymakers should keep in mind that financial innovation has a positive impact on the economy. At the same time, accelerating economic growth, accompanied by strong economic growth, encourages banks to take more risks, as such an economic environment makes banks more optimistic about improving market conditions in the future. In this case, however, they become increasingly vulnerable to credit risk. This is particularly the case when policymakers raise interest rates to fight inflation, as this worsens the financial position of borrowers and increases the probability of default.

Donat and Asa (2011) analysed the case of Uganda and identified weak government policies, different ideologies, political influence and lack of capital as the main factors hindering sustainable banking in Uganda. The fact that the government has a significant impact on bank performance was confirmed by Ahiase et al. (2024). The researchers found that factors such as debt-to-GDP ratio, unemployment, regulatory quality, government effectiveness and inflation have a significant impact on the number of non-performing loans. To reduce the likelihood of borrowers defaulting and banks’ credit risk, the government should maintain a sustainable level of debt, promote employment growth and control inflation. Ensuring regulatory quality and government efficiency is key to financial stability.

Taken together, the results of the reviewed studies suggest that lenders can improve the quality of their loan portfolios by lending to more sustainable entities and adopting more sustainable lending policies (e.g., by financing only sustainable entities and projects or by facilitating lending to more sustainable entities), as these borrowers are less likely to default due to more stable income and cash flows. More sustainable entities are also more resilient to the risks posed by ESG factors. However, the lender should consider not only the sustainability of the borrower but also the sustainability of the collateral for the loan, which is considered a credit risk mitigant as it may also be exposed to ESG risks. All of this means also means that a lender can avoid penalties for complying with regulatory requirements to consider the risks posed by ESG factors in its operations and can also result in lower provisions and capital requirements.

By lending to more sustainable companies or investing in more sustainable projects, the lender not only reduces its credit risk but also improves its reputation by addressing the risks posed by ESG factors in its operations, for example, by adopting a more sustainable lending policy. For example, a better reputation is also likely to reduce the lender’s exposure to negative consequences should risks materialize. Lower credit risk and a better reputation also lead to better credit ratings for the lender itself, which can reduce its borrowing costs and attract more depositors and shareholders.

Overall, identifying, assessing, measuring, monitoring, mitigating and controlling the risks posed by ESG factors (not just in the context of assessing the creditworthiness of borrowers) leads to a more sustainable and stable business. Sustainable and stable lenders who ensure that the financing needs of businesses (both corporate and sovereign) are met contribute to economic growth and financial stability (Ali & Puah, 2019; Anagnostopoulos et al., 2018; Anakpo et al., 2023; Donat & Asa, 2011; Man & Pan, 2014; Padovani et al., 2018). Sustainable economic growth often leads to a better financial position of borrowers, that is, a lower risk of default, which further reduces lenders’ credit risk. Jakubik and Moinescu (2015) have examined what the optimal level of credit growth should be in an emerging banking system and found that quarterly credit growth of 3% to the private sector would be the optimal rate to maintain financial stability and sustainable economic growth in Romania.

It is also important to note that lenders, through their lending policies, not only influence economic growth or financial stability but also contribute to climate change, which they can influence directly (e.g., by adopting more environmentally friendly solutions in their operations) and indirectly (e.g., by granting more favourable lending conditions to more environmentally friendly entities).

Results

The growing demand from policymakers and investors for lenders to tighten their lending policies to less sustainable companies in order to contribute to sustainable economic growth makes it imperative that credit risk management takes into account the risks posed by ESG factors. This is one of the latest challenges for the financial sector, leading to a trend of increasing interest among researchers in this topic and the need for new researchers to answer the question of how sustainability can be integrated into the overall credit risk management process, rather than into individual processes as is often the case today.

The aim of this systematic literature review was to answer two questions. The first question was to find out what indicators are used in models that examine the relationship between sustainability and credit risk in order to incorporate sustainability and credit risk. The results of the review showed that models that examine the relationship between sustainability and credit risk most commonly use the environmental factor as an indicator of sustainability (72% of the studies analysed). The social factor was used by 61% and the governance factor was considered by 44% of the studies. 50% also included an overall ESG score. Although some researchers used their own selected indicators reflecting ESG factors, a large number of researchers simply used Refinitiv Eikon and MSCI ratings. The Altman Z-score was the most commonly used credit risk estimator in the reviewed studies (used in 28% of the analysed studies). The majority of studies using the Altman Z-score were found using the keyword ‘sustainability + default risk’. The second most popular estimate was bond and CDS spreads (used together in 28% of the analysed studies). The second most popular indicator was bond and CDS spreads. The probability of default was also one of the most popular credit risk estimates.

The second question was how lending to more sustainable companies affects the credit risk of the lender. A systematic review of the academic literature suggests that lenders generally reduce their credit risk by lending to more sustainable companies and by adopting more sustainable lending policies. This is based on the fact that more sustainable companies have more stable operations and cash flows, leading to a lower probability of default and better creditworthiness. Moreover, the lender should consider not only the sustainability of the borrower but also the sustainability of the loan collateral, which is seen as a credit risk mitigant.

However, the lending policies of sustainability-oriented lenders can also have a negative impact on credit risk. This is the case when government interference in the activities of lenders becomes excessive and distorts the supply of finance. One example is the case of China, where green loans increase the credit risk of state-owned banks.

Incorporating the identification, assessment, measurement, control and mitigation of ESG risks into credit risk management (both directly and indirectly) contributes to better quality loan portfolios, more stable and sustainable operations and performance of lenders, with a positive impact on economic growth by providing finance to those who want to borrow. During periods of sustained economic growth, borrowers are often in a better financial position, which further reduces the credit risk for lenders.

The results of the systematic review of the scientific literature are useful for representatives of the academic community, policy makers and people working with credit risk. From the perspective of future research, the results of this study (identification of sustainability and credit risk metrics) serve as a summary reference point for the development of further sustainability-related credit risk assessment models. Future research should also investigate whether the evaluation of collateral through the lens of sustainability contributes significantly to credit risk mitigation.

The results of the study conducted for policymakers are useful because they demonstrate the link between sustainability and credit risk, and the metrics and gaps identified (e.g., sustainability assessment of collateral) allow for further development of recommendations, requirements and policies related to ESG disclosure and integration into risk assessment. This is particularly important in an era of increasing sustainability regulation.

For those who deal with credit risk, the results of this study may allow for a more conservative assessment of credit risk (if the sustainability of collateral is also considered) and improve the quality of loan portfolios. A more sustainable lending policy can also increase the financial stability of the lender, improve its reputation, attract more investors and reduce the cost of funding.

Finally, from a societal perspective, it can be argued that more sustainable lending contributes to financial stability in the financial sector, more sustainable growth and progress towards global sustainability goals. Lenders, therefore, have a very important role to play in achieving these goals.

A review of existing empirical studies suggests that future research could seek to investigate the impact of collateral adjusted for potential ESG risks on the lender’s credit risk (this remains an unexplored topic despite its growing importance in the context of climate change and the transition to more sustainable activities, e.g., floods, fires or other natural disasters may damage collateral; as we move towards sustainability, less sustainable collateral may lose value). Further analysis of credit risk could explore the impact of ESG factors on credit provisions.

Future research could also seek to compare traditional statistical models with machine learning methods (e.g., neural networks), as the importance and impact of such innovative research will only grow in the future as the diversity and quality of ESG-related data increase.

Discussion

Numerous studies have analysed the relationship between sustainability and credit risk, but only a few of them have had a significant impact on further research. For example, Weber et al. (2010) argued that sustainability should be considered in credit risk management because it helps reduce credit risk. This insight helped to move ESG from being seen as an external factor to being seen as having an impact on a company’s finances.

Empirical evidence that better environmental performance reduces credit risk is provided by Hoeck et al. (2020). The researchers analysed the impact of better environmental scores on bond spreads. Similarly, Aslan et al. (2021) extended this discussion by using ESG scores and S&P ratings to show that higher ESG performance is correlated with a lower probability of default. These studies measured the impact of sustainability on credit risk.

Another phase can also be distinguished, in which the impact of sustainability credit risk has been assessed not only through the prism of corporations, but also in the public sector. For example, Padovani et al. (2018) and Bruno and Henisz (2024) pointed out that governance and social responsibility factors also affect credit risk in municipalities.

Also, most of the studies reviewed have looked at the impact of sustainable performance (good ESG indicators) on credit risk. However, few researchers have looked at the reverse effect. For example, how an environmental credit rating affects a company’s ESG performance (Cao et al., 2024), or how a green credit policy affects a company’s ESG performance (Han et al., 2023). Similarly, a minority of researchers have examined the impact of sustainable economic growth and financial innovation on the banking sector (Ahiase et al., 2024; Khan et al., 2021).

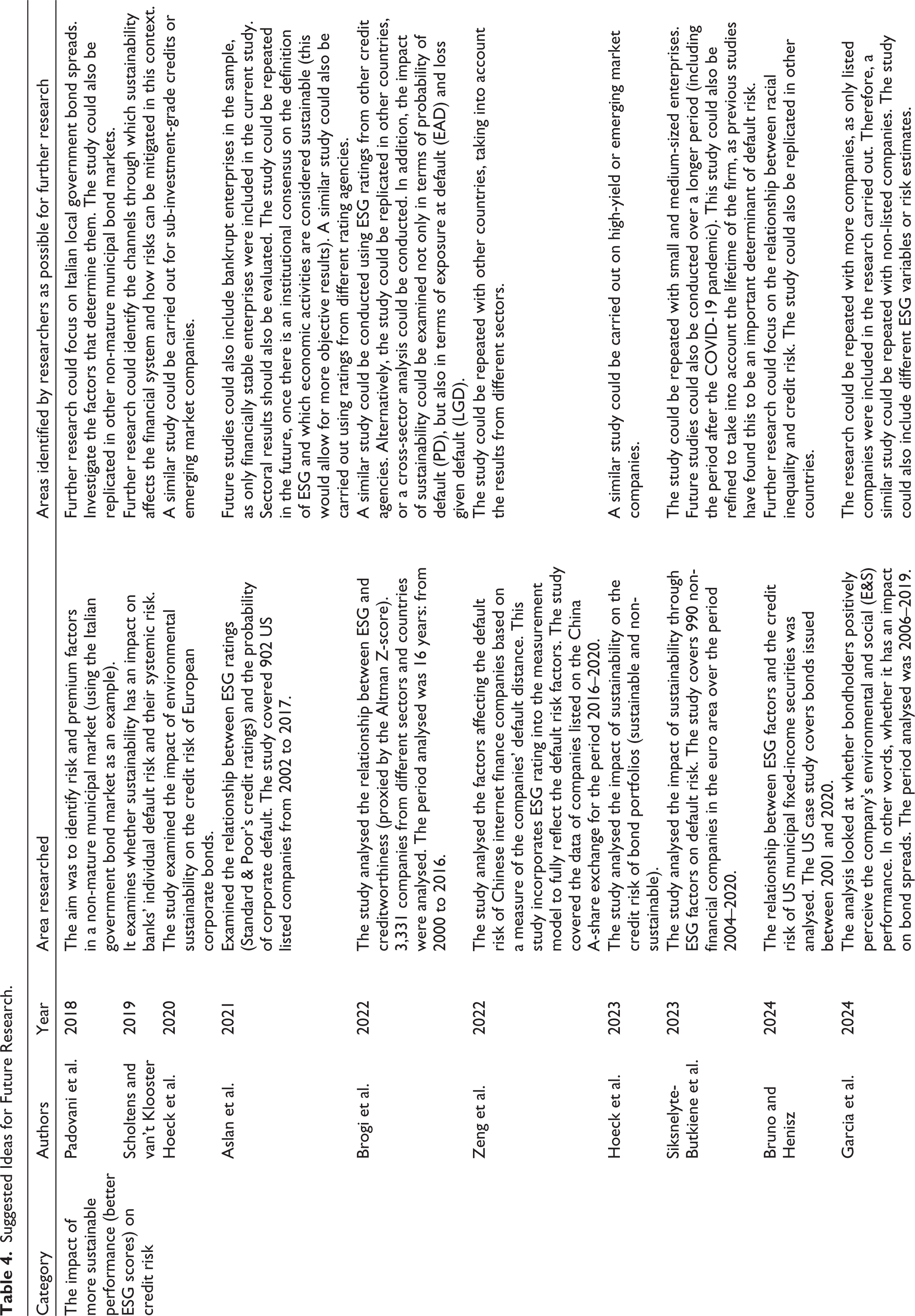

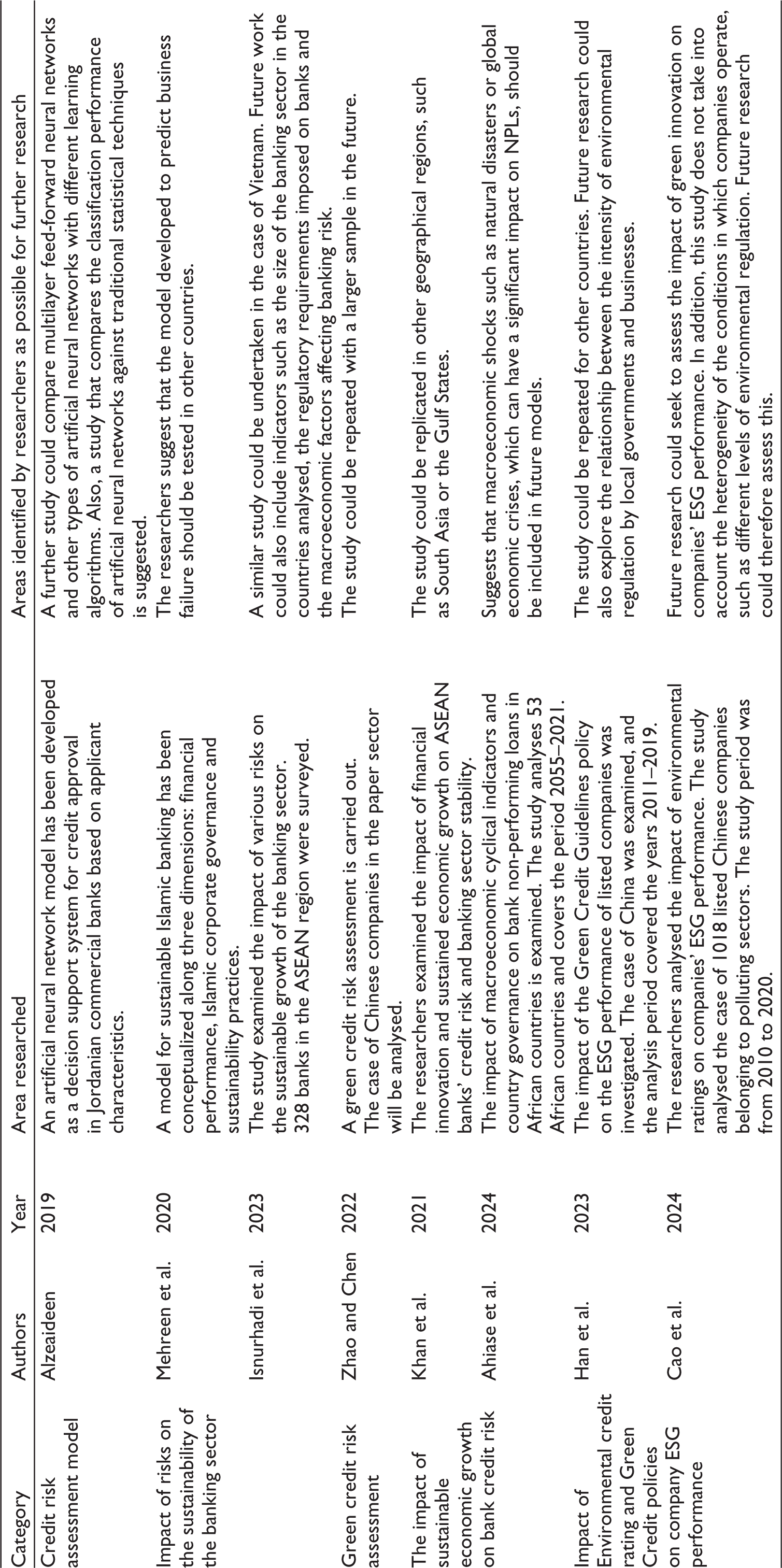

Studies on the impact of better sustainability performance (better ESG scores) on credit risk have looked not only at the case of companies but also at the case of local governments (Bruno & Henisz, 2024; Padovani et al., 2018). The studies have tended to focus on a single country or region, and researchers have argued that studies should be replicated in other countries or regions to obtain more comprehensive and objective results to assess the impact of sustainability performance on credit risk (Table 4). For example, Hoeck et al. (2020) and Hoeck et al. (2023) analysed the impact of better ESG indicators on debt spreads in the case of developed markets. According to the researchers, similar studies could be replicated in the analysis of emerging market debt, as these markets are of interest to investors because emerging market companies or companies with sub-investment grade credit ratings can offer higher returns. In addition, researchers (Aslan et al., 2021; Brogi et al., 2022; Zeng et al., 2022) have raised the need to replicate similar studies with companies in different sectors, as sustainability may have different effects on the credit risk of companies operating in different sectors. Vivel-Bua et al. (2023) suggest that studies should also take into account the fact that the impact may depend on the size of the company.

Suggested Ideas for Future Research.

Researchers (Aslan et al., 2021; Brogi et al., 2022) point out that similar studies could be replicated not only in other countries, with companies from different economic sectors or company sizes, but also with ESG indicators from different rating agencies (and not only the overall ESG indicator, but also the indicators of individual ESG factors). Similar studies could also be conducted on other credit risk factors, e.g., the impact of sustainability could be examined not only in terms of probability of default, but also in terms of exposure at default and loss given default. The researchers suggest using not only traditional statistical methods but also artificial neural networks in their studies and comparing these different techniques (Alzeaideen, 2019).

The researchers identified a lack of data as the main problem they encountered in their studies. The data gaps encountered by the researchers were ESG indicators, older or more recent data. Vivel-Bua et al. (2023) suggest that future studies should also focus on the COVID-19 period and indicators of unlisted companies. Vivel-Bua et al. (2023) also argue that in the future, when there is institutional consensus on the definition of ESG and on which economic activities are considered sustainable, the results of the studies will be of higher quality and more objective. As a result, all these studies could be repeated in the future to assess changes in results caused by different perceptions of what is sustainable.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.