Abstract

Caring for the environment has become everyone’s responsibility because of our significant negative impact. Considering this, companies are spending a substantial amount on corporate social responsibility (CSR) activities not only as part of corporate citizenship but also to enhance corporate image. Using a fixed-effect model on 2,260 companies’ annual data from 2012 to 2017, we analyze whether female board members influence CSR performance. The results indicate that the proportion of female board directors (PFBD) in Chinese firms is relatively small compared with the male. In other words, the boards members are predominantly male.

The fixed effects model indicates that both the number and proportion of female directors are significant in influencing CSR performance. Surprisingly, we note that the average age of female board directors has a significant and negative impact on CSR performance. The results also indicate that the education level of the female director does play a significant role in CSR performance. This demonstrates that firms need to recruit educated board directors and with a right mix of age.

Introduction

In the past, Chinese firms have been criticized by the Western media for their lack of effective corporate board governance (Dahya et al., 2003). In response, there have been a number of regulations and recommendations by the Chinese Securities Regulatory Commission (CSRC). These include the Code of Corporate Governance for Listed Companies in China (2001), the need for the Institutional Independent Directors and the raft requirements regarding the Information Disclosure of Listed Companies (2007).

In September 2006, the Shenzhen Stock Exchange issued a social responsibility guideline for all listed companies, and since then, major companies began to formulate CSR-reporting outlines (Yang, 2012). Consequently, a report by KPMG in 2011 showed that 60% of China’s largest firms reported on CSR in the same year. Nevertheless, it has been noted in the past that CSR performance (CSRP) is directly influenced by the top management or the board (Boulouta, 2013). Given the importance of CSR to corporations, for instance, influencing consumer attitude (Bhardwaj et al., 2018; Chunyan et al., 2019; Ferrell et al., 2019), it is paramount to have a deep insight into the board composition and how such composition influences CSR performance. Therefore, the objective of this study is to examine the relationship between the board characteristics and CSRP.

Considering China is seen as the ‘world’s factory,’ by contributing not only 28% worldwide manufacturing productivity in 2018 (United Nations Statistics Division [UNSD], 2018) but also 30% of China’s total output, this study is not only relevant to Chinese context but also globally in how CSR can be enhanced. Past empirical evidence have addressed the impact of gender diversity on financial performance, but there are limited works on CSRP. To better understand this relation, recent studies have explored the link between female directors and the adoption of CSR practices (Bear et al., 2010; Seto-Pamies, 2013; Zhang et al., 2013). Closely related to this article are the work of Prado-Lorenzo and Garcia-Sanchez (2010) and Liao et al. (2014) where the particular emphasis was on the relation between gender diversity and emission level disclosures.

The results indicate that the number of companies with more than five female board directors is 324, accounting for 14.34% of the total board directors. In terms of their age, the average age for female directors is 42.76 years and the average education level is 2.16, equivalent to a college diploma. The correlation coefficient of the proportion of female executives to CSRP is 0.054, which is significant at the 5% significance level. Using the fixed effects model, the results indicate that it is not just the number of female directors but the proportion that is likely to influence CSRP. This demonstrates the need for a sustained campaign to have a balanced board across many countries in the world. Similarly, using the fixed effects model, the results indicate that the education level of a female director does play a significant influence (5%) on social responsibility. This demonstrates that firms need to recruit board directors who are educated. The idea is that the more educated an individual is, the more likely they are to be aware of the need to take care of the environment and to devise appropriate environmental and social policies.

This paper makes a number of contributions to the board diversity literature and environmental concern. First, we analyse the proportion of female directors in the board and assess how the proportion of female directors influences CSRP. Second, we evaluate whether board age and education influence CSRP.

We focus on Chinese firms because, according to the UNSD, China accounted for 28% of the global manufacturing output in 2018 (UNSD, 2018). This is 10% more than the United States. That is why China is seen as the ‘world’s factory’.

Section 2 is the literature review, followed by the methodology in Section 3. Section 4 is on the analysis of the finding and Section 5 is the conclusion.

Literature Review

Underpinning CSR Theories

The upper echelons and feminist care ethics theories form the foundation of the current study. Hambrick and Mason (1984) proposed the upper echelons theory, which holds that the executive characteristics will affect enterprise’s strategic decision-making and decision-making effect. The executive characteristics that influence the strategic decisions of enterprises include the director’s cognitive ability, value orientation and perceptual thinking (Hambrick, 2007). The theory aligns with Child (1975), who noted that younger managers take more risks. Therefore, using age, Hambrick and Mason (1984) indicated that older managers’ flexibility decreases over time and, hence, they exhibit resistance to changes, such as improvements in CSRP. As a result, they are less likely to take risks that can affect their overall responsibility for a shareholder return.

In terms of gender, the feminist care ethics theory, which originated in the 1970s, holds that women have a more caring attitude than men. However, Gilligan (1993) pointed out that men often see themselves as independent entities and view morality as a category of personal power, while the respected ethics of men pay more attention to the norms and the fairness of power. In contrast, most women think that morality means being responsible for others, hence, more caring.

The Association Between the Number of Female Board Members and CSRP

A diversified composition allows the board to integrate different cognitive and professional skills. Some research has shown that homogeneous groups tend to solve problems the same way and, therefore, repeat assessment errors, which is less likely in heterogeneous groups (Burgess & Tharenou, 2002). Several studies have focused on the association between the number of female board members and the CSRP. Post et al. (2011) selected 78 power and chemical companies in the Fortune 1,000 as research objects. They used regression analysis to study the relationship between female directors’ participation and the companies’ KLD environmental scores. Their analysis showed that companies with three or more female directors participating in the KLD have significantly higher environmental advantage scores than other companies. This implies that the more female board members an organization has, the more environmental and social activities the organization will engage in. In line with this, Zhang et al. (2013) and Glass et al. (2016), using 516 USA companies and all the Fortune 500 CEOs, respectively, noted a significant and positive correlation between the number of female directors and the CSRP. This implies that more women can encourage more participatory communication among board members, assuming gender differences in leadership styles. Some existing research demonstrates that women have a more participatory, democratic and communal leadership style than men (Zhang, 2012).

The Association between the Proportion of Female Board Members and CSR Performance

Luthar et al. (1997) believe that women value morality more than men. Empathic concern is the core of feminist care ethics. The theory holds that female board directors achieve an impact on CSR through empathic concern. In line with this argument, Ibrahim and Angelidis (1994) noted that women pay more attention to perceived health and environmental risks and will take action to reduce the risk. Women are more aware of environmental deprivation, more actively participate in environmental protection actions and doubt the scientific means of solving environmental problems.

Following the empathic view of women, some studies have focused on the relationship between the PFBD and CSRP. Fernandez-Feijoo et al. (2012) took Fortune 250 and 100 companies as research samples, and they studied and analysed the relationship between the proportion of female board members and the quality of social responsibility information disclosed by companies. Fernandez-Feijoo et al. (2012) found through regression analysis that firms with a high percentage of female directors have a more transparent operations and management as well as a stronger willingness to disclose high-quality CSR information. The study notes the inclusion of three women on the board has positive effects on the disclosure of the CSR strategies. Setó-Pamies (2015) conducted an empirical study using data from 2011 to assess the implications of gender diversity on CSR. Global 100 provides reliable, extensive and transparent data for companies in 22 countries in all sectors of the economy. Thus, the data used were reliable and representative of the global corporate environment. Of the companies in Global 100 in 2011, the researcher selected 94 firms that met the research criteria of workers’ diversity, innovation, transparency and safety. The multiple regression analysis and correlation results indicate that gender diversity has significant positive impacts on CSR. Specifically, Setó-Pamies (2015) observed that female talent has a strategic role that promotes social responsibility and sustainable practices. The firms with a higher percentage of women on the board recorded better CSR results than those with fewer women.

A study by Landry et al. (2016) sought to determine whether a female director makes a difference in CSR using a sample of 341 companies ranked in the Fortune 500. The dataset was collected for seven years, 2006–2012, and considered multiple corporate recognition lists, such as Most Ethical, Most Admired, and Best Corporate Citizens companies. The researchers used two weights—by-firm weighted average and an overall weighted average—to assess women’s representation in the sampled corporations. Of the sampled companies, 64.2% had multiple female directors, while the rest had only one or fewer average female directors.

Bear et al. (2010) noted that women increased the board’s sensitivity to CSR and promoted the participative decision process, which has positive impacts on CSR practices. In addition, the study demonstrated that the company reputation increases with an increase in the percentage of women on the board.

Ben-Amar et al. (2017) investigated the impact of female representation on the corporate board’s response to the stakeholders’ demands to improve public reporting on issues related to climate change. The researchers sampled 541 Canadian firms listed on the Toronto Stock Exchange (TSX) for a period ranging from 2008 and 2014. The gender diversity in the study was measured by the percentage of female directors on the corporate board. The result of the sampled firms indicates that participation of the female directors in the company has positive effects on the voluntary disclosure of climate change information. Thus, gender diversity, the percentage of women on the board, improves the board’s effectiveness in adopting initiatives by stakeholders. According to Ben-Amar et al. (2017), the firms must reach a critical mass of 30% women on the board to realise the potential benefits of gender diversity in developing climate change initiatives and its influence on greenhouse gas disclosure. Indeed, Joecks et al. (2013), when they studied 151 German companies, noted that boards with three or more women directors are associated with higher financial performance. Therefore, having three or more women on a board removes the focus from gender to talent (Konrad et al., 2008), resulting in lower out-group bias for female members (Torchia et al., 2011). The critical mass theory postulates that unless a certain threshold or critical mass is reached, gender barriers are not broken down, and the benefits of gender diversity do not influence the content and process of board discussions to a greater extent. In other words, below this number, the vast majority of people may ignore the existence of the minority, which means women cannot exert enough influence to change the group’s decision-making in a meaningful way, Therefore,

The Relationship between the Characteristics of Female Board Directors and CSR Performance

Recent evidence has indicated that there has been an unprecedented increase in female representation on corporate boards in the past decade. For example, Lee et al. (2015) noted that female board members increased from 9.3% in 2009 to 15.3% in 2015. The most recent study indicates that from 2016 to 2017, there was generally an increase of female board members, from 15.8% to 17.3% (Eastman, 2017). Other studies have argued that female board members tend to bring different perspectives to boards due to their unique values, experiences and knowledge (Post & Byron, 2015). In line with this, the upper echelons theory holds that the personal characteristics of female board directors and the gender composition of the directors affect CSRP and corporate governance (Hambrick, 2007). The personal characteristics of female board directors, such as education level, age, tenure and position, are closely related to their management philosophy and behaviour. Terjesen et al. (2009) argued that female board directors generally receive a better education and, in general, have a higher level of ethics. This implies that the female board directors use their knowledge to make the right decisions to improve CSRP. Other studies such as Luthar and Karri (2005) pointed out that as age and work experience increase, women’s moral sensibility increase, and the management tends to be more conservative. Diversity in age aligns with differences in work values and behaviour, personality, traits, skills and attitudes. Studies have shown that these differences across the age groups can be according to various generations. For example the Greatest Generation (1922–1945) are known not only to be self-disciplined and royal but also to value traditions and culture (Twenge et al., 2010). Boomers (1946–1964), believe working hard lead to success and value extrinsic measures of career success, develop a distrust of authority and place a high value on independence. Those born between 1965 and 1983, called Gen Xers, are said to be influenced by the financial, family and societal insecurities. Gen Xers are said to lack solid traditions and are very mobile, and they learn very quickly. Lastly, Generation Y, also called the Millennials (born 1984–2002), are said to be very curious and have more social awareness.

Therefore,

When female board directors hold different positions, their behaviour will be different. The higher the position, the more questions managers need to consider. Other researchers have noted that when women serve as chairman/general managers, they usually pay more attention to CSRP (Stawiski et al., 2010). In addition, board members, including females who hold or held different directorship, are more likely to demonstrate experience, which is vital to financial, social and environmental performance. Other studies have also shown that experience female board members are hardworking and have superior communication skills (Robinson & Dechant, 1997). Therefore, with experience earned from previous organizations or gained internally, female directors are likely to have developed their directorship skills, including communication, that is vital in negotiating the need to be mindful of society and the environment.

Hence,

Zhai and Gao (2015) studied female board directors and Chinese firms CSRP. In addition to the number of female board directors (NFBD) and the percentage of females participating in senior management, they also selected women’s education level and age as moderating variables. Contrary to the findings of Fernandez-Feijoo et al. (2012), Zhai and Gao (2015) found that there is an insignificant U-shaped relationship between female board directors and CSRP, rather than a positive correlation. In addition, the results of Zhai and Gao (2015) show that the higher the average age and the higher the degree of education of female board directors, the better the CSRP. Also, Harjoto et al. (2015) documented a positive association between educational diversity and CSRP. Therefore, we hypothesis that

Data and Methodological Application

Sample and Data Collection

This research selected the A-share companies listed on the Shenzhen and Shanghai stock markets of China, and which were listed on the Chinese stock markets before 2012 as a sample. We screened the initial samples using the following criteria. (s) Eliminate the listed companies in the financial industry. (b) Eliminate companies with incomplete data. (c) Eliminate the listed companies with incomplete information about women board directors. State-owned enterprises (SOEs) have been required to publish their CSR since 2012.

We used the annual data of the 2,260 companies from 2012 to 2017 to conduct the empirical study. The CSRP data were collected from the Corporate Social Responsibility Rating Report published by Hexun.com. The database scores the companies as an index of how they are performing regarding social responsibility. Hexun.com is China’s first social responsibility evaluation system and has been widely used since its creation (Luo & Wang, 2015, Zhao et al., 2011). The other data (number of female board executives, the proportion of female board executives, average educational level, total assets, company size [CS], leverage [LEV], return on assets and years of the listing [YL]) were collected from the China Stock Market & Accounting Research (CSMAR).

Variables for Analysis

We used a number of variables: (a) The NFBD, that, is the absolute number of female board directors in the company. (b) The PFBD, that is, the proportion of female board directors in the company’s executive team. (c) The average age of female board directors (AAFBD). (d) The average educational level of female board directors (AELFBD), denoted by 1–5, in which 5 denotes doctor’s degree and higher, 4 denotes master’s degree, 3 denotes bachelor’s degree, 2 denotes college diploma, and 1 denotes below college diploma. Then, this research averaged the educational level of all-female board directors in the company to calculate the female board directors’ average education level.

Following Post et al. (2011) and Zhang et al. (2013), we controlled profitability and CS in the regression model.

Other variables are (a) CS, using the natural logarithm of the total assets; (b) profitability measured by ROE; (c) YL, that is,, the number of years from the initial public offering (IPO) of the company; and (d) LEV, measured by the asset-liability ratio.

In terms of the dependent variable (CSRP), we used the RKS rating. RKS determines corporate ratings in relation to three principal areas: macrocosm, content and technique. The first relates to the overall strategy that governance and information disclosure channels deployed in an entity’s social reporting activities. The third dimension, technique, covers the depth, coverage and consistency of reporting. Finally, in terms of ‘contents’, the rating looks at community participation, economic performance, consumption, and labour and human rights. Evidence suggests the prominence of RKS in China in guiding investors’ awareness of the quality and content of listed firms’ overall social reporting activities (Lau et al., 2016; Luo et al., 2016).

In this study, before using the panel data regression, we conducted various diagnostic tests to assess the applicability of either fixed effects or random effects. Using the Hausman Test, the results indicated that the fixed effects model is more appropriate than the random effects.

We plug the variables into the fixed effects estimation model expressed as:

Where CSRPit is the CSR rating of firm i in year t, a0 denotes the constant term of the model and ai (i=1, 2, …, 8) denotes the regression coefficient of the model, while εit denotes the stochastic disturbance term. All variables are on level as used in the previous studies (Uyar et al.,2020; Wang et al.,2018).

We follow Oxelheim et al.’s (2013) suggestion to utilize fixed-effects models and include multiple controls to address potential endogeneity. However, we recognize that our results should be seen as evidence of association rather than causation.

Findings

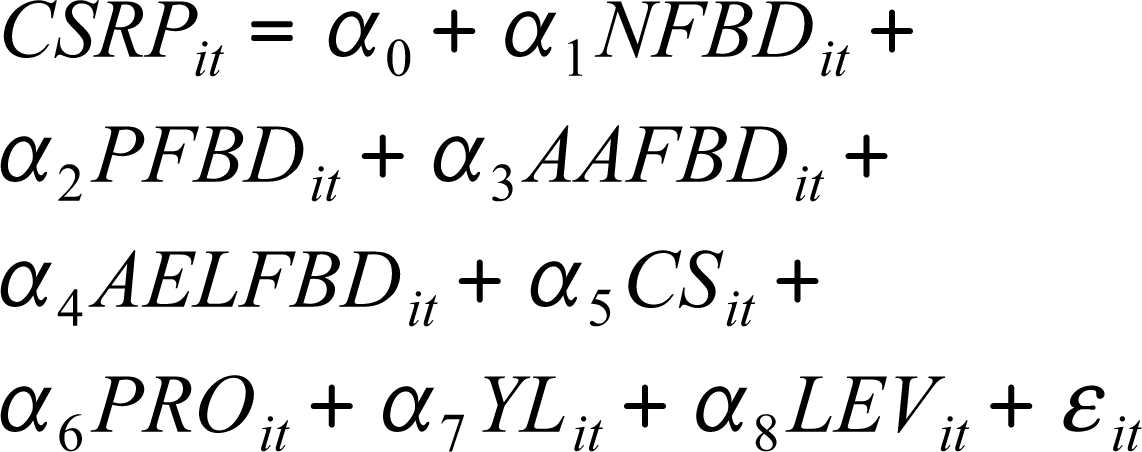

Table 1 shows the descriptive statistics of the NFBD and the PFBD in the sample companies from 2012 to 2017.

Descriptive Statistics of the Number of Female Board Directors and Proportion of Female Board Directors.

According to Table 1, the sample company’s mean value of the NFBD is 2.99. This shows that the average NFBD in Chinese A-share listed companies is 2.99. The standard deviation of the NFBD is 2.24, while the minimum is 0 and the maximum is 20 due to the high standard deviation and the significant difference. This indicates a large difference in the NFBD in Chinese A-share listed companies. From 2012 to 2017, the mean value of the NFBD increased from 2.11 to 3.37. This shows that the NFBD in Chinese A-share listed companies increases year on year.

The mean value of the PFBD is 16.32%, and the standard deviation is 10.44%. The minimum and maximum values are 0 and 64.71%, respectively. According to the mean value, it can be considered that the PFBD in Chinese A-share listed companies is relatively small and that the directors are mainly male. However, the proportion of females is rising as the mean value of the PFBD increased year-on-years from 2012 to 2017.

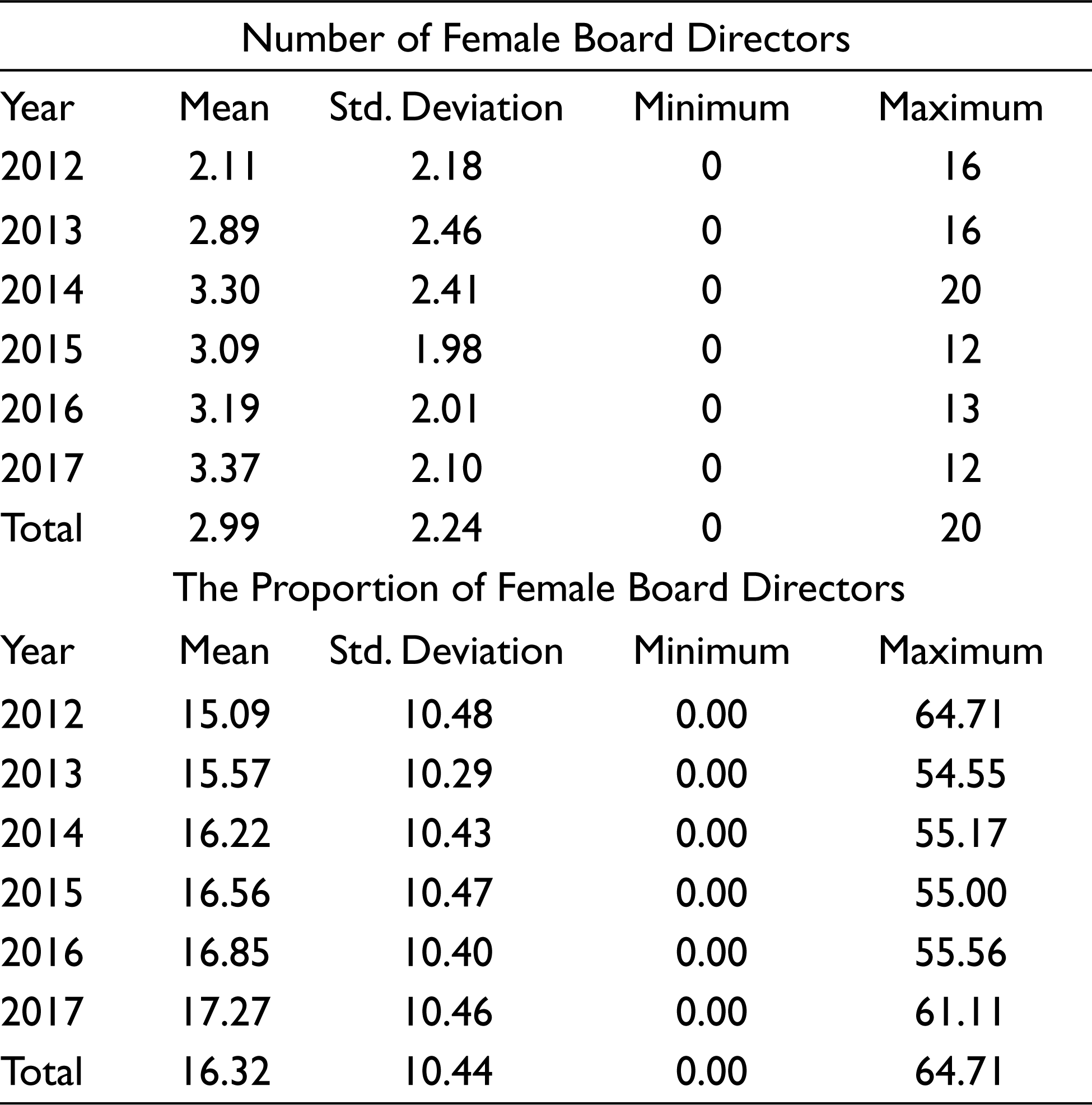

Table 2 shows the distribution of the NFBD in all sample companies in 2017.

Distribution of the Number of Female Board Directors in All Sample Companies in 2017.

According to Table 2, there are 1,294 companies with fewer than or equal to three female board directors in 2017, accounting for 52.76%. The number of companies with four or five female board directors is 642, accounting for 28.41%. The number of companies with more than five female board directors is 324, accounting for 14.34%. It can thus be seen that the female board directors of Chinese A-share listed companies are fewer than or equal to three and that the NFBD is generally relatively low.

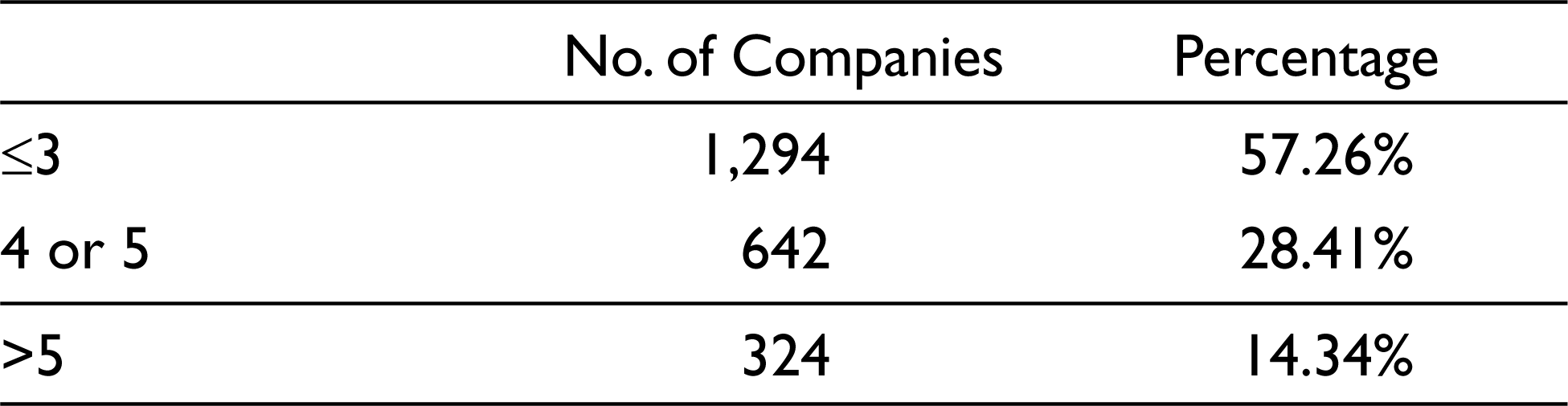

Average Age of Female Board Directors

The AAFBD is the total age of female board directors divided by the total NFBD. According to Table 3, the average age in the sample companies is 42.76 years old. The standard deviation is 17.18. Thus, the AAFBD in the sample companies increased from 2012 to 2017, reflecting the growing age of female board directors in Chinese A-share listed companies.

Mean Value and Standard Deviation of the Average Age of Female Board Directors.

The AELFBD is the total education level of female board directors divided by the total NFBD. According to Table 3, the average education level in the sample companies is 2.16. The standard deviation is 1.27. An average education level of 2 means that the qualification is a college diploma, while an average education level of 3 means that the highest qualification is a bachelor’s degree. The average education level is 2.16, indicating that the AELFBD in Chinese listed companies is between college diplomas and bachelor degree.

Impact of Female Board Directors’ Characteristics on Corporate Social Responsibility Performance in Chinese Listed Companies

Descriptive Statistics of Variables

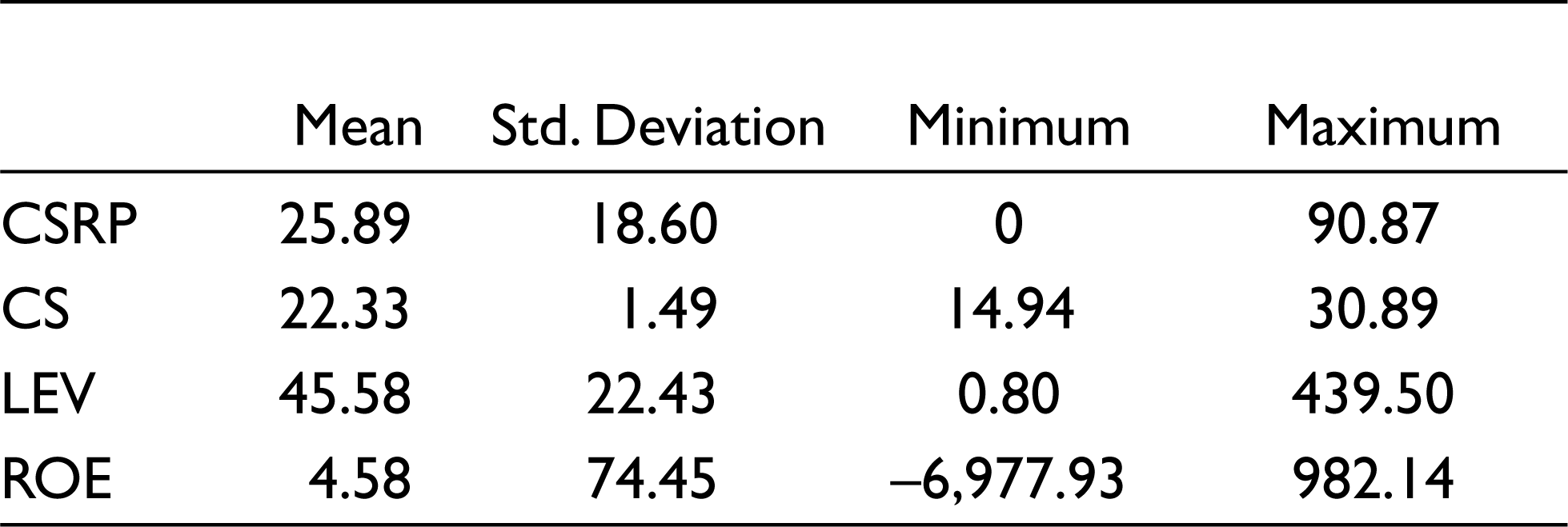

Table 4 shows that the mean value of the CSRP score is 25.89, the standard deviation is 18.60, the minimum value is -18.19, and the maximum value is 90.87. According to the data, the mean value of the CSRP of Chinese A-share listed companies is only 25.89% of 100 points. This indicates that the overall CSRP of Chinese A-share listed companies is relatively low. The difference between the minimum and maximum values is significant, meaning that the CSRP of different companies is quite different.

Descriptive Statistics of Other Variables.

The mean value of CS is 22.33, and the standard deviation is 1.49. The minimum and maximum values are 014.94 and 30.89, respectively. The mean values of LEV and ROE are 45.58% and 4.58%, respectively. The mean value of LEV of 45.58% indicates that the average LEV of Chinese A-share listed companies is relatively high because liabilities account for nearly half of the total assets. On the other hand, the mean value of ROE is 4.58%, which is relatively low, indicating that the profitability of Chinese A-share listed companies is relatively low.

Correlation Analysis

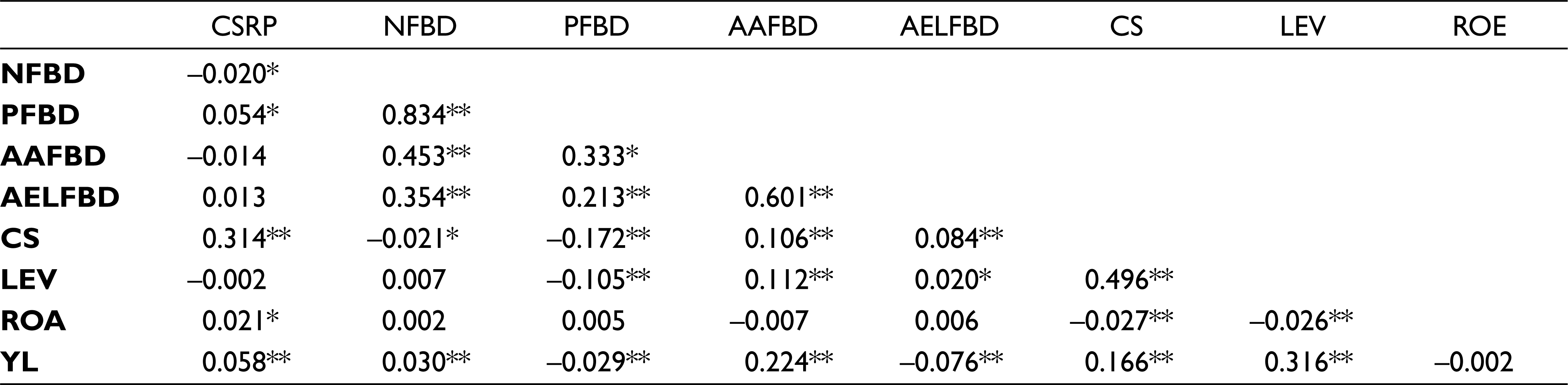

Table 5 shows that the correlation coefficient of the NFBD to CSRP is –0.020, significant at the 5% significance level. This indicates that the number of female board members in Chinese listed companies is significantly and negatively correlated with CSRP at the significance level of 5%, but the correlation is not strong because the absolute value of the correlation coefficient is relatively low. Also, the correlation coefficient of the proportion of female executives to CSRP is 0.054, which is significant at the 5% significance level. This indicates that the PFBD in Chinese listed companies is significantly and positively correlated with CSRP at the significance level of 5%.

Pearson Correlation Coefficient.

*. Correlation is significant at the 0.05 level (2-tailed).

**. Correlation is significant at the 0.01 level (2-tailed).

Further, the correlation coefficient of the AAFBD to CSRP is -0.014, which is not significant at the 5% significance level. This indicates that the AAFBD in Chinese listed companies is not related to CSRP at the significance level of 5%. The results also indicate that the association between the AELFBD and the CSRP is 0.013, which is not significant at the significance level of 5%. This indicates that the AELFBD in Chinese listed companies is positively correlated to CSRP at the significance level of 5%.

In line with Sayedeh et al. (2015) and David et al. (2015), Table 5 shows that CS, ROE and YL are significantly positively related to CSRP at the 5% significance level. This is because profitable firms are likely to have sufficient resources to devote to social or environmental activities. Also, there is a positive relationship between CS and CSRP. In other words, large firms are likely to devote resources to CSR activities. This could be attributed to huge public scrutiny on large firms. However, the results indicate that firms that are highly leveraged are likely to performance lower on CSR because of resource constraint.

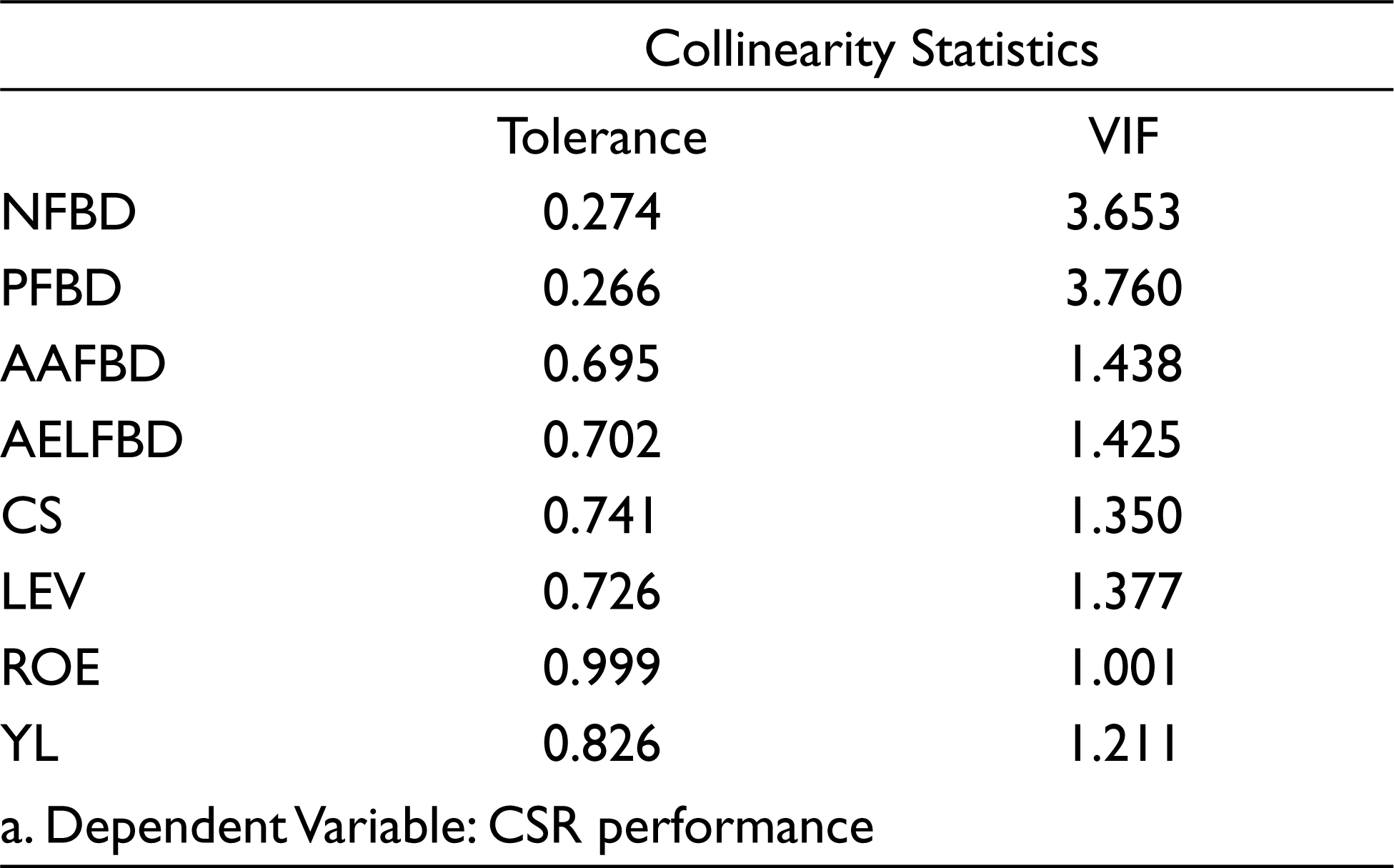

Among the explanatory variables, as expected, the correlation coefficient between the NFBD and the PFBD is relatively high at 0.845. The absolute value of the correlation coefficient between other variables is relatively low. The relatively high correlation between the number of females and the PFBD may lead to multicollinearity in the regression model of this research. The variable;s variance inflation factor (VIF) can be calculated to determine whether there is multicollinearity between the variables. The VIF is the ratio of the variance of the multicollinearity between explanatory variables to the variance of the absence of multicollinearity. When the VFI is between 0 and 10, it can be considered that there is no strong evidence of multicollinearity. When the VIF is greater than or equal to 10 and less than 100, it can be considered that the regression model has strong multicollinearity. When the VIF is greater than or equal to 100, it can be considered that the regression model has severe multicollinearity. The VIF of the explanatory variables and control variables of the regression model are shown in Table 6.

Variance Inflation Factors.

According to Table 6, the VFIs of all explanatory variables and control variables are less than 10. This shows that there is no serious multicollinearity issue.

Regression Analysis

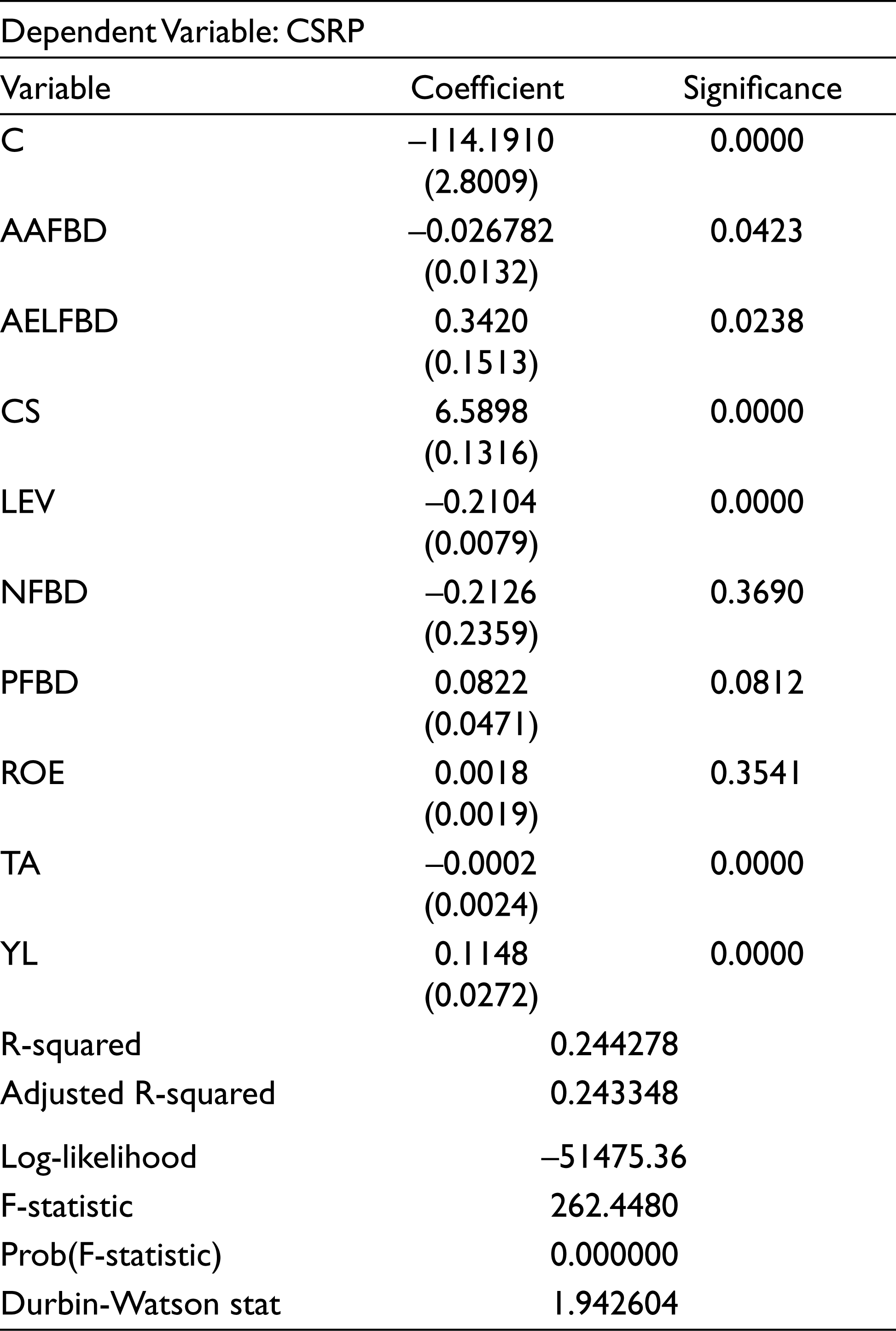

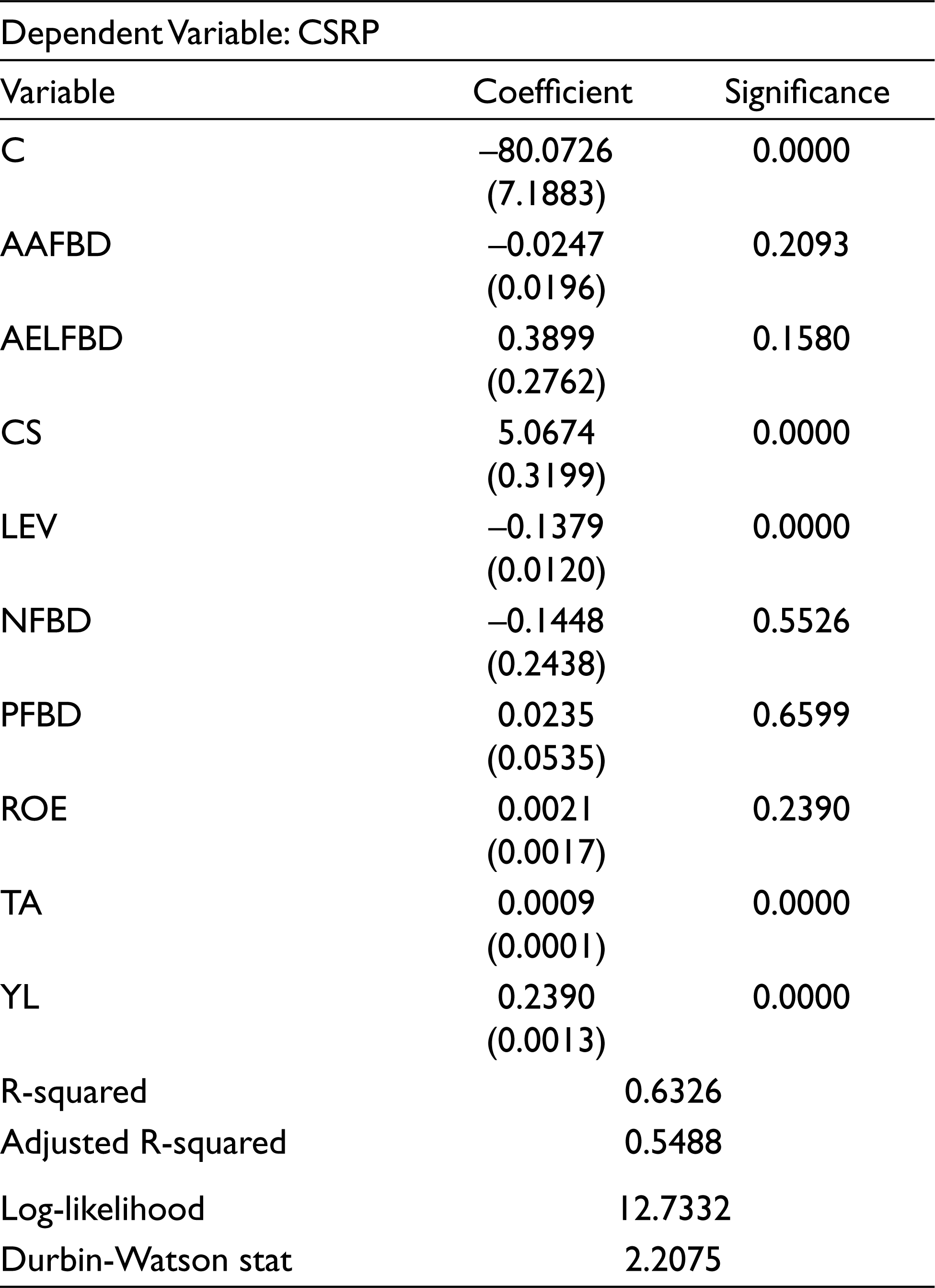

To assess the impact of female board directors on CSRP, we use the fixed-effect model as a robust estimate. This is considering a huge number of firms from different industries that are likely to exhibit different characteristics. The Durbin-Watson (DW) is 1.94, which is close to 2. This indicates that there is less evidence of autocorrelation.

Similar to Zhang et al. (2013), Zhai and Gao (2015), Setó-Pamies (2015), Landry et al. (2016) and Yannick et al. (2018), the results indicate that it is not just the number of female directors but the proportion that is likely to influence CSRP, and hence fail to reject hypothesis 1. This demonstrates the need for a sustained campaign to have a balanced board across many countries worldwide. The findings support Post et al. (2011), Zhang et al. (2013) and Cook and Ingersoll (2016), who indicated that female board directors have a positive impact on CSRP. According to the feminist care ethics theory, females are of a more caring nature than males. Gilligan (1993) stated that men usually view themselves as independent entities and regard morality as a type of personal power.

The feminist care ethics provides the foundation for female board directors’ influence on CSRP from the perspective of ethics and psychology. Specifically, female board directors can impact CSRP due to women’s nature of empathy. When there are more female board directors in the company, the executive team’s overall CSR and degree of care will rise.

Fernandez-Feijoo et al. (2012) argued that companies with a large proportion of female directors have more transparent management and operations and a stronger willingness to disclose high-quality information about CSR. Unfortunately, the NFBD in most Chinese listed companies is fewer than or equal to three. However, Post et al. (2011) pointed out that companies with three or more female board directors taking part in CSR show significantly higher environmental merit scores than other companies.

Similarly, the results indicate that the education level of the female director does play a significant influence (5%) on social responsibility, and hence fail to reject hypothesis 3. This demonstrates that firms need to recruit educated board directors. The idea is that the more educated an individual, the more likely they are to be aware of the environmental impact from the firm’s operations and the need to devise appropriate environmental and social policies. Terjesen et al. (2009) argued that female board directors generally receive a better education and, in general, have a higher level of ethics. At the same time, the female board directors use the knowledge they have gained to make the right decisions to improve CSRP. Therefore, with the rise of the education level, female board directors will have a stronger idea of giving back to society and public welfare.

Moreover, receiving education itself is enjoying social welfare. When it is accomplished, female board directors will be conscious of helping those in need. This will be conducive to the improvement of the overall CSRP.

The result from Table 7 shows a negative significant (5%) between the AAFBD and CSRP. This is in line with Hafsi and Turgut (2013), who noted a negative association between age and CSRP. This goes hand in hand to explain why it is very important to include Millennials in the board as they are known to be socially aware. However, the findings also demonstrate that older and larger (in size, total assets and YL) companies are likely to perform better CSRP than new and young firms. This is because the larger companies are likely to devote sufficient resources to their CSR strategies.

Fixed Effect Estimation Results.

In terms of LEV, the FE model indicates a significant negative coefficient. This demonstrates that less leveraged companies are likely to perform better. The more leveraged the firm is, the more it is expected to be financially distressed. Hence, there will be little if any investment in CSR. Further, although not very significant, there is a positive coefficient between financial performance (ROE) and CSRP. Profitable firms are more likely to devote resources to social responsibility than those struggling financially.

Discussion

Previous empirical evidence has indicated that boards of directors play a pivotal role in ensuring that organisations meet different stakeholders; needs, including environmental concerns (Kassinis & Vafeas, 2002; Walls et al., 2012). Studies have found that board size is positively related to CSR practices and environmental performance (Frías-Aceituno et al., 2012; Osemeke, 2011). Examining the impact of the female directors has extended the knowledge on diversity and size of the board and on its impact on environmental performance. The current study indicates that it is not just the number of female directors but the proportion that is likely to influence CSRP. In other words, both the number and proportion of female directors are significant in influencing CSRP. This implies that female directors are committed and innovative on environmental issues. Luo et al. (2016) noted that women present different skills and interests on corporate boards. Other studies such as Hayes (2001) and Galbreath (2011) indicated a positive but not significant association between female directors and environmental performance. Therefore, female directors’ positive and significant influence suggests that female directors demonstrate empathy and are likely to reject unethical business practices that will damage the environment. The results support the upper echelons theory perspective that a greater representation of female directors on the board exhibit better environmental performance through effective sustainability-related strategies.

Examining the significance of education level for the directors, the results indicate that education is significant at 5% in influencing CSRP. This implies that directors with a high educational level have a better capacity to benefit from opportunities and learn more about new trends (Geletkanycz & Black, 2001). In other words, educated directors display better decision-making compared with less educated directors (Finkelstein et al., 2009). The results also imply that educated directors are more likely to adjust their strategies to deregulation and other changes.

Based on upper echelons theory, Hambrick and Mason (1984) used age as a characteristic of top board directors and they found that older managers’ flexibility declines over time and, thus, they show resistance to such changes as improvement and are likely to take risks which may affect their overall responsibility of shareholders’ return. Hence we reject hypothesis 2. This implies that young executives are more concerned for the environment. Nevertheless, it is important to ensure that the board is diversified. This will stimulate proficiency and innovation, which improve firms’ competitive advantage (Li et al., 2011). Diversity in terms of age is very important in the sense that each decade is unique and special, and has experienced different social, economic and political environments, which consequently increases board effectiveness. Indeed Li et al. (2011) argued that age diversity arouses proficiency and innovation within the board, enhancing the firm’s competitiveness.

Robustness Test

To check the endogeneity issue, defined as an association between the explanatory variables and the error term, we used the generalized method of moment (GMM) estimator proposed by Arellano and Bond (1991). Wintoki et al. (2012) state that the use of lagged values of endogenous variables enables us to account for dynamic panel bias, especially in a dynamic panel context related to the relationship between corporate governance and firm performance. Therefore, following prior studies (Elmagrhi et al., 2018; Nguyen et al., 2015; Orazalin, 2020; Wintoki et al., 2012), we use a GMM estimation tool to account for potential endogeneity problems. Table 8 shows the results of estimating the panel GMM. The signs of the coefficients are similar to that of Table 7, which shows that the results do not suffer from endogeneity issues. This confirms the fundamental results, such as how the presence of female directors influences the CSRP. Both Table 7 and Table 8 demonstrate that the proportion of female directors is positively related to CSR commitment, in line with Bear et al. (2010) and Post et al. (2011). This implies that female board members are emotive, sensitive to the environment and considerate to the needs of other stakeholders.

GMM Estimation of CSR Performance Orientation with Female Directors.

Conclusion and Recommendation

The results demonstrate that the number of females and the proportion of the board of directors is positively associated with CSRP. However, we find the proportion of female board of directors is more than just the number. The findings also indicate that the AAFBD in Chinese listed companies has a significant and negative impact on CSR performance. In addition, the results suggest that it is not just the NFBD but the proportion that is significant in influencing CSR performance. The education level also has a significant impact on CSR performance. Apart from gender balance, the results also indicate that highly leveraged firms are likely to perform poorly in CSR. As expected, the results suggest that older, larger and more profitable companies perform better in CSR. This is because these firms are likely to devote enormous resources and strategies towards their social obligations.

In terms of policy implications, the research suggests that companies should raise the education level of female board directors to improve the overall quality of decision-making. For female board directors, the higher their education level, the more significant the effect on CSRP. Therefore, Chinese listed companies can provide learning or training opportunities for female board directors to improve their overall quality. In addition, the results demonstrate the value of having the right mix of the board. In other words, it is very important to ensure that there is a good proportion (critical mass) of female directors on the board and the right mix in terms of age, that is, there should be senior (in terms of age) and young directors. As a limitation, the current research only focused on Chinese firms.

Footnotes

Ethical Approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.