Abstract

This study examines whether a simple model based on expected goals (xG) can generate accurate forecasts and identify profitable signals in football betting markets. The model uses recent xG to estimate win–draw–loss probabilities via a Skellam distribution, with isotonic regression applied for calibration, and evaluates the performance over eleven Bundesliga seasons (2014/15 through 2024/25). While bookmaker odds tend to exhibit superior statistical calibration, the xG-based model captures certain signals not fully reflected in market prices. In simulated betting, the model yields a return on investment of approximately 10% using average market odds, increasing to nearly 15% under the best available prices. Profits stem predominantly from home win bets, while backing away wins is consistently loss-making. The results show some robustness to modelling choices, though profitability varies considerably by season and bet type. The study highlights the potential of simple models as practical tools for identifying predictive value in structured football data.

Introduction

Forecasting football match outcomes has drawn sustained academic and practitioner interest, particularly as granular performance metrics such as expected goals (xG) have enabled more systematic modelling of team strength and match dynamics. Initially developed within online analytics communities, xG is now deeply embedded in modern football practice. English Premier League clubs, for instance, use xG-based frameworks to inform player recruitment and tactical decisions, supported by evidence of substantial value generation through data-informed strategies (Tippett, 2019, 2024). These models evaluate shot quality and efficiency rather than raw outcomes such as scored goals, allowing probabilistic assessments that are more robust to randomness and variance in match results. They also provide an empirical basis for estimating outcome probabilities that can be compared and potentially combined with those implied by bookmaker odds. Methodologies used to evaluate football markets mirror techniques in financial and economic forecasting, where market data act as proxies for latent probabilities (Kain and Logan, 2014). Even when their forecasts are not perfectly calibrated, such models may capture distinct patterns or structural tendencies that are underweighted or overlooked by the market.

Despite their appeal, predictive models in football face the sport’s inherent complexity. Outcomes are shaped by low-frequency, high-impact events and influenced by a wide range of factors. Betting markets, while often information-efficient, embed structural features and behavioural biases that complicate the interpretation of odds. These challenges necessitate models that are both statistically coherent and robust to real-world constraints.

This paper contributes to the literature by systematically evaluating the predictive and economic value of a simple, robust model for the German Bundesliga. Using eleven seasons of data, it applies this xG-based framework to convert recent match performance into outcome probabilities, finetuned through isotonic regression. These forecasts are compared with bookmaker-implied probabilities in terms of calibration and predictive accuracy and used to identify value bets in simulated betting strategies. A dedicated robustness check also examines how much of the economic performance is attributable to the isotonic calibration layer. While xG-based forecasts are slightly less well calibrated than market odds, they capture certain signals that translate into consistent, albeit modest, profitability: average market odds yield a return on investment (ROI) of about 10%, increasing to nearly 15% under best-available prices. Selective strategies optimised for ROI or Sharpe ratio can exceed 10%, though based on a relatively small number of bets. Notably, home win bets generate the bulk of profits, while away bets remain persistently unprofitable. These findings remain largely robust across seasons, parameter variations and staking approaches.

Conceptually, this study is related to the xG-based performance framework of Brechot and Flepp (2020), who analyse how random variation in finishing and goalkeeping distorts observed results and construct xG-based efficiency ratios and league tables for ex-post assessment of team performance. In contrast, the present paper examines whether a similarly parsimonious xG-driven model can deliver economically valuable ex-ante forecasts and reveal mispricings in football betting markets.

The paper is organised as follows. In Section “Previous research”, a structured overview of prior research on football forecasting is provided, covering statistical models, market-based approaches, hybrid methods and supporting literature. In Section “Data and modelling framework”, the data are introduced and the modelling framework is outlined, based on expected goals and the derivation of probabilistic forecasts. Furthermore, a post-calibration finetuning of the model forecasts through isotonic regression is discussed. Potential value betting strategies are described in Section “Devising a betting strategy”. Besides the identification of opportunities and baseline benchmarks, several money management strategies are introduced. Section “Results” presents the main results, beginning with an evaluation of the model’s calibration and predictive accuracy and then evaluating the profitability of betting strategies after threshold optimisation, including performance by bet type. In Section “Robustness and sensitivity analysis”, the robustness and sensitivity of results to key modelling choices are explored, focusing on elements such as the historical xG calibration window, odds selection, staking method and the use or omission of isotonic calibration. Section “Conclusion and outlook” concludes and outlines avenues for future research.

Previous research

Football outcome prediction has been studied through three principal lenses: statistical modelling, market-based inference and hybrid or machine learning approaches. Each reflects a different philosophy of how match dynamics and uncertainty can be understood, with implications for model calibration, practical implementation and relevance to betting contexts.

Statistical modelling approaches

Statistical models have long underpinned football forecasting, with Poisson-based methods providing the foundation. Maher (1982) modelled goals as independent Poisson processes linked to team strengths; Dixon and Coles (1997) introduced temporal weighting and corrections for low-scoring outcomes and inefficiencies.

The Skellam distribution, capturing the difference between two Poisson variables, naturally models win-draw-loss results. Karlis and Ntzoufras (2009) used Bayesian estimation in this setting, while Xenopoulos (2016) confirmed its empirical validity. However, the assumption of goal independence is often disputed. Bivariate Poisson models address this by introducing scoring correlation, improving the modelling of draws, as shown by Karlis and Ntzoufras (2003) and Groll et al. (2018). More flexible dynamic or latent-state approaches – e.g. the score-driven multivariate models of Koopman and Lit (2015) and the copula-structured hidden Markov model of Ötting et al. (2023) – enhance fit but reduce interpretability and increase calibration effort. Michels et al. (2025) cater for a more general dependence structure and show that richer correlation patterns can substantially improve fit.

Recent xG models estimate scoring potential from shot-level data – e.g. location, angle, assist type – offering more stable proxies for team strength than realised goals. Brechot and Flepp (2020) use such an xG framework to disentangle luck from skill in realised results, constructing xG-based league tables and offensive/defensive efficiency ratios that show how short runs of matches can diverge from underlying performance. Fu (2024) and Mead et al. (2023) highlight how feature choice and data source impact predictive accuracy. Dynamic rating systems such as Elo and pi-ratings, which update based on results, goal margins and opponent strength, remain widely used and have outperformed official rankings in predictive tasks (Hvattum and Arntzen, 2010; Lasek et al., 2013). A recent comprehensive treatment of these models and their implementation in football contexts is provided by Egidi et al. (2025).

Together, these statistical approaches form the backbone of football forecasting, with ongoing work focused on refining match dynamics, enriching input features and improving evaluation.

Market-based models and efficiency

Betting markets serve as a benchmark for probabilistic forecasts, aggregating public sentiment, expert judgement and contextual factors. While generally effective at incorporating information, they show structural and behavioural patterns that can lead to persistent mispricing – creating scope for model-based strategies.

A key research strand evaluates market efficiency ex post. Forrest et al. (2005), Goddard and Asimakopoulos (2004) and Vlastakis et al. (2009) show that while bookmaker odds are well calibrated, they are not fully efficient. Mispricings stem from overrounds, limited competition, pricing conventions and behavioural biases. Using a combination of Monte Carlo simulations and multi-season European football odds, Winkelmann et al. (2024) caution that many reported anomalies are consistent with sampling variation and find little evidence of persistent, exploitable inefficiencies. Work on value betting explores profitability. Franck et al. (2010) find better pricing accuracy on exchanges than with bookmakers. Feng et al. (2016) infer scoring intensities from odds using a Skellam framework and improve calibration by adjusting for draw overpricing. Kaunitz et al. (2017) use simple filters to identify profitable strategies, while Constantinou et al. (2013) apply Bayesian networks that outperform odds. Egidi et al. (2025: Chapter 7) provide a recent, systematic comparison between state-of-the-art statistical models and bookmaker odds, likewise concluding that margins and small, unstable mispricings leave limited scope for persistent outperformance.

Implied probability calibration is central. Strumbelj (2014) proposes margin-adjusted methods to reconstruct fair odds and enable comparison with model forecasts. Behavioural biases are well documented. Franke (2020) and Brown and Yang (2021) examine phenomena such as the favourite-longshot bias and other pricing distortions. Drawing on in-play Bundesliga odds and volumes, Ötting et al. (2025) find that bettors behave as if equalisers create strong momentum, even though estimated win probabilities change little, underscoring the psychological component of pricing. Brown and Yang (2019) show that forecast accuracy improves with crowd diversity and market depth.

In-play and high-frequency studies offer a dynamic view. Croxson and Reade (2014) show that exchange odds adjust almost instantaneously to goals and display little subsequent drift, while Winkelmann and Deutscher (2025) find no systematic adjustment of odds or stakes in the seconds leading up to goals in the Bundesliga, suggesting that markets neither strongly anticipate nor underreact to such events. Michels et al. (2023) and Ötting et al. (2024) document strong shifts in trading volume and stake distribution around short-term performance swings, revealing limits to real-time efficiency.

Overall, markets appear broadly – but not fully – efficient. Odds embed rich information but remain subject to frictions and behavioural distortions.

Hybrid and machine learning approaches

Machine learning (ML) has become prominent in football prediction, offering tools to model nonlinear patterns and feature interactions. These approaches often extend classical models, especially when leveraging domain-specific inputs like expected goals, team ratings or recent form. Methods include tree-based ensembles, support vector machines (SVM), neural networks and probabilistic graphical models.

Bayesian networks capture uncertainty and structural dependencies in outcomes. Joseph et al. (2006) demonstrated early promise, with later work integrating form and rating dynamics. Comparative studies benchmark ML models against Poisson or Elo-type baselines. Singh et al. (2025) and Fischer and Heuer (2025) evaluate families like SVMs, random forests and neural networks, often concluding that feature quality matters more than model class.

Some work assesses profitability as well as accuracy. Stübinger and Knoll (2018) and Hubacek et al. (2019) simulate betting strategies using ML forecasts, highlighting the importance of calibrated inputs and market-derived features. Tree-based methods generally perform well, but rely heavily on effective feature engineering. Baboota and Kaur (2019), Kozak and Glowania (2021) and Edalatpanah and Hess (2024) report strong results across top European leagues, particularly for high-confidence predictions. Berrar et al. (2024) likewise emphasise that thoughtful feature design often outweighs algorithmic complexity.

Recent work integrates spatiotemporal and player-level data. Hewitt and Karakus (2023) enhance xG models with player roles and context, while Bialkowski et al. (2014) use unsupervised learning to extract team formations – signalling a shift toward tactical modelling beyond team aggregates. Explainability is gaining focus. Cavus and Biecek (2022) apply SHAP and LIME to xG-based models, improving interpretability and supporting transparent decision-making.

Together, machine learning methods offer promising applications to football forecasting, though their success depends critically on feature design, calibration and interpretability.

Other approaches and supporting literature

Beyond core modelling, related work addresses evaluation metrics, betting strategy, behavioural factors and data resources – all shaping how football forecasting systems are developed and applied.

A key focus is betting strategy and bankroll management. The Kelly criterion (Kelly, 1956) remains foundational for sizing bets under uncertainty. Uhrin et al. (2021) show that fractional Kelly offers favourable risk-adjusted returns with noisy models. Buchdahl (2003) provides a widely cited guide on fixed-odds betting, covering expected value and margin correction. Kopriva (2015) contrasts utility theory with observed behaviour, revealing consistent deviations from optimal staking. Effective capital allocation is thus as important as accurate prediction.

On model evaluation, Wunderlich and Memmert (2020) provide a taxonomy of forecasting approaches, from expert-driven to ML hybrids. Wheatcroft (2022) recommends log-loss and Brier scores over ranked probability scores in football, stressing calibration and sharpness. Behavioural and heuristic forecasting is another active strand. Tippett (2017) argues that simple, data-driven methods can rival expert judgement. His later works (Tippett, 2019, 2024) further support the consistency of analytical approaches over intuition, echoing broader behavioural economics insights.

Finally, new data resources enhance transparency and reproducibility. Dubitzky et al. (2019) introduce an open-access database spanning over 200,000 matches across 52 leagues. Bassek et al. (2025) expand this with Bundesliga-specific spatiotemporal data, enabling more granular tactical analysis.

Against a backdrop of increasingly complex forecasting methods, this study examines whether a straightforward, interpretable model can nevertheless uncover reliable signals that reflect structural inefficiencies and offer predictive leverage over market odds.

Data and modelling framework

Data

The setup uses match data and xG values for the 1. Bundesliga during the eleven seasons from 2014/15 to 2024/25 (source: https://understat.com). This is complemented by bookmaker and betting exchange data for the same period (source: https://www.football-data.co.uk). The latter consists of closing odds, i.e. the last odds before a match starts. For each time point, the average quotes are obtained – with the panel typically consisting of about 15 providers each. This ensures a sufficiently representative picture of market-implied probabilities as well as liquidity for any bets to be placed at these odds. Section “Robustness and sensitivity analysis” examines how the results change when the ‘best’ available odds are used instead of the averages.

Table 1 provides a descriptive overview of the overall dataset. With 18 teams in the league, there are 306 matches per season, yielding a total of 3,366 over the course of the analysis. On average, teams score between one and two goals per match, with considerable variation. Up to eight goals per team are observed in individual matches. The expected goals largely mimic this picture, although with less variation and extremes (an xG value of 0.0 indicates that a team has not attempted a single shot in the entire match). Across all matches, the average expected goals for home teams (1.66) exceeds that of away teams (1.32), indicating a typical home advantage of approximately 0.34 xG. This asymmetry is reflected in both actual and expected goal statistics and is implicitly captured in the model through venue-specific xG aggregation (see Section “Generating predictions from historical xG”).

Statistics for goals, xG, match outcomes and odds.

This table summarises the statistics for all Bundesliga matches from the 2014/15 through 2024/25 seasons. Panels A and B report descriptive statistics on actual and expected goals for home and away teams, respectively. Panel C shows the relative frequency of each match outcome. Panel D presents odds and market-implied probabilities across the three result types.

Home wins are more common than away wins, while draws occur in about one-fourth of the cases. Odds imply payout multiples as low as 1.03 for favourites (3% gross return) as well as enormous upsides (more than 4,000% for an away-team win). Notably, the means of the market-implied probabilities (corrected for the ‘overround’; see Section “Identification of value bets”) in Panel D are very close to those of the actual realisations (Panel C).

Since goals are the ultimate metric for match outcomes, Figure 1 visualises the joint distribution of home and away goals. Most matches cluster around low-scoring outcomes such as 1–1, 2–1 and 2–0. Notably, the mass of the distribution lies below the diagonal, reflecting the asymmetric nature of match results in favour of the home teams.

Joint distribution of home and away goals. The heatmap shows the joint distribution (in percentages) of home and away goals in Bundesliga matches from the 2014/15 through 2024/25 seasons (restricted to results where both teams scored 0 to 6 goals). Darker cells indicate more frequent outcomes. The dotted diagonal indicates draws; outcomes below this line coincide with wins of the home team.

Modelling framework based on expected goals

From xG to probabilistic forecasts

Expected goals provide a granular, quantitative measure of scoring potential, constructed from the sum of shot-level probabilities within a match. Each shot’s xG is estimated based on features such as location, angle and assist type, often using specific models trained on large datasets (Mead et al., 2023). Aggregating these values yields team-level xG, a match-level proxy for offensive output that is less sensitive to variance than realised goals.

Consider two opposing teams, denoted A (home) and B (away), with pre-match expected goals

Generating predictions from historical xG

In order to produce probabilistic forecasts of match outcomes, pre-match estimates of expected goals are required for both teams involved. The values for

A practical limitation of the method is its reduced coverage at the start of each season and immediately after extended breaks, such as the winter pause. This results from a deliberate modelling choice: team-level expected goals are estimated only from matches within the current competitive phase. Rolling averages are not carried over across seasonal boundaries or long interruptions, ensuring that forecasts reflect recent form rather than outdated information. As a consequence, the setup ultimately reduces forecast coverage to 2,118 out of 3,366 matches.

As shown in Figure 2, the empirical goal difference distribution aligns well with the Skellam-based xG model as per (2), particularly around central outcomes such as draws and one-goal margins. Moderate underestimation in the tails suggests the model may understate extreme outcomes but remains a strong candidate for win-draw-loss modelling.

Distribution of goal differences – empirical vs. model. The histogram compares the empirical distribution of goal differences in Bundesliga matches with a Skellam distribution that, for each match, uses pre-match expected goals

While this study adopts a home vs. away classification to capture venue-specific scoring tendencies, an alternative framing would be to distinguish matches based on favourite vs. longshot status, using pre-match market-implied probabilities. This segmentation aligns closely with how betting markets assess relative team strength. For instance, when Bayern Munich visit VfL Bochum, they are strong favourites despite being the away team – yet the current model classifies them using away xG alone. However, since xG performance already reflects underlying team strength and venue remains a structural driver, the incremental benefit of such a reclassification is not obvious. The home vs. away distinction on the other hand offers a transparent and empirically grounded baseline for the analysis.

Model assumptions and simplifications

The modelling framework relies on several simplifying assumptions:

Zero-inflation. The Poisson model tends to underestimate the frequency of goalless matches. Although this issue is well documented, its impact is limited here because the model uses goal differences – reducing the influence of matches where both teams score zero equally. A more flexible alternative would be a zero-inflated Poisson model (Lambert, 1992), though this would increase calibration complexity. Overdispersion. Real-world goal data often exhibit greater variance than the Poisson distribution allows (where the mean equals the variance). A negative binomial distribution (Cameron and Trivedi, 1998: pp. 70–77) could accommodate this through an added dispersion parameter, but again at the cost of interpretability and greater estimation uncertainty. Goal dependence. The model assumes that home and away team goals are independent random variables. In reality, scoring may be interdependent within a match – for instance, an early goal can shift tactics and increase the likelihood of further goals (or tighten defence). Such within-game dynamics violate the independence assumption. A bivariate Poisson model or a latent shared-component structure (e.g. Opponent independence. Each team’s expected goals are estimated independently of their opponent. More elaborate models might weight past performance by opponent quality, potentially including time decay. However, such refinements would reduce model transparency and again increase the risk of model over-complexity. Feature omission. The model excludes contextual features such as injuries, weather or tactical formations. While these could improve forecasts, they also introduce subjectivity, data sparsity and difficulties in reproducibility. Notably, home advantage is implicitly accounted for, as the xG inputs are based on match-specific home/away performance. Aggregation level. Teams are treated as single entities without decomposing performance to the player level. An alternative would be to allow for more responsive modelling under line-up changes. For example, Hewitt and Karakus (2023) propose a position-adjusted xG model that captures team strength from the bottom up. The necessity and usefulness of such granular player-level modelling for win, draw and loss forecasting, however, is not obvious.

While these simplifications might limit (in-sample) calibration accuracy, they allow for a robust and easy-to-follow framework and, at the same time, the generation of independent ‘signals’ that might be useful for actual betting strategies. The relevance and importance of some of the assumptions is further analysed as part of the sensitivity analyses in Section “Robustness and sensitivity analysis”.

Model finetuning through isotonic regressions

The Skellam-based model produces structured forecasts of match outcomes, but the raw probabilities are often not fully aligned with empirical outcome frequencies. To address this, isotonic regression is applied as a post-processing calibration step. It estimates a non-decreasing function

Calibration is applied separately to each outcome type – home win, draw, away win – using a rolling window of two seasons (so that all results and reliability plots are strictly out-of-sample with respect to their calibration window; see Section “Results”). Within each window, isotonic regression is trained on model probabilities and binary outcome indicators.

2

Each fitted function is stored as a piecewise-linear mapping defined by threshold–value pairs

Figure 3 illustrates the isotonic regression on the example of a given in-sample two-season calibration window. Panel (a) shows the empirical frequency of home wins against the baseline (Skellam) model probabilities, with the fitted isotonic regression overlaid as a monotonic step function. Panel (b) visualises the corresponding mapping function used to transform the baseline model probabilities into their calibrated equivalents. For this process, the model probabilities are binned into fixed-width intervals over the

Finetuning model probabilities via isotonic regression. In order to illustrate the finetuning step, the figure shows calibration and reliability plots for home win probabilities within a single in-sample calibration window (2018/19 through 2019/20 seasons). Panel (a) displays the isotonic regression fit applied to baseline Skellam-based xG model probabilities, together with empirical outcome frequencies. Panel (b) compares reliability curves for the baseline and finetuned (isotonic-adjusted) probabilities. Each point represents the empirical frequency of home wins within a bin of predicted probabilities (with a minimum of 10 observations). The dashed diagonal line indicates perfect calibration.

The method builds on the original formulation of isotonic regression by Robertson et al. (1988) and its application to probability calibration in classification settings by Zadrozny and Elkan (2002). Its effectiveness for multiclass settings has been confirmed empirically by Niculescu-Mizil and Caruana (2005). Compared to parametric methods such as Platt scaling (Platt, 1999), isotonic regression is more flexible but requires more data to avoid overfitting. Earlier work by Zadrozny and Elkan (2001) also provides a comparative evaluation of calibration techniques and highlights the trade-offs between interpretability, flexibility and data efficiency.

In this setup, the isotonic step does not replace the Skellam model, but acts as a one-dimensional, monotone calibration layer applied to its output probabilities. Structural information enters through the xG-based Skellam specification; isotonic regression only adjusts systematic probability bias without changing the ordering of fixtures or introducing additional predictors. It thus serves as a data-driven adjustment to an already structured model rather than as a standalone flexible forecasting device.

Devising a betting strategy

Identification of value bets

In order to apply the prediction model in a betting context – whether against bookmakers or on a betting exchange (e.g. Betfair) – the key objective is the identification of value bets. These are wagers where the model assigns a higher probability to an outcome than is implied by the market.

Let

A bet on outcome

A complementary practical step consists in imposing thresholds to filter out low-quality betting opportunities and mitigate risks stemming from model miscalibration or market frictions. The specific threshold choices are determined via in-sample calibration and discussed in Section “Threshold ‘optimisation’”.

Baseline strategies as benchmark

To benchmark the model-based betting strategy, two simple baselines are implemented and evaluated out-of-sample. These serve as reference points for assessing whether the model delivers meaningful improvements over uninformed or market-driven heuristics.

Historical frequency-based strategy

This benchmark generates a prediction for each match by drawing randomly from the historical league-wide outcome frequencies. These proportions are computed over a rolling window of past matches consistent with the model’s xG lookback horizon (

Market favourite strategy

This approach places a bet on the outcome – home win, draw or away win – with the lowest average closing odds, i.e. on the market’s implied favourite. The strategy hence reflects consensus opinion of the most likely outcome and tests whether the model can outperform publicly available expectations.

Money management strategy

Once qualifying bets have been identified, a staking strategy must be specified to translate these into actionable positions. The simplest option is flat betting, whereby each wager receives a constant stake. However, more refined approaches dynamically adjust stake sizes according to perceived edge and risk. One such method is the fractional Kelly criterion (Kelly, 1956), which recommends bet sizing in proportion to the estimated advantage while reducing the volatility associated with full Kelly staking (Uhrin et al., 2021). For a given outcome

This study considers flat betting as a base case and fractional Kelly staking as an alternative (see Section “Money management strategy: fractional Kelly”); other approaches – such as drawdown-aware rules, staking caps or portfolio-style allocations – may offer further adaptability to market frictions and individual risk preferences.

Results

Calibration and predictive accuracy

Before deploying forecasts in a betting context, their calibration and predictive accuracy must be assessed to ensure statistical reliability and practical relevance. The first step is to compare the model probabilities – as well as those implied by market odds – to actual (out-of-sample) realisations of the matches in scope.

The reliability diagrams in Figure 4 group the matches into ‘bins’ by their probabilities and contrast those with the empirical occurrences, and are based on forecasts for the out-of-sample seasons 2016/17 through 2024/25, using the two-season rolling isotonic calibration described in Section “Data and modelling framework”. As an illustration, for all matches in which the model forecasts a home win with 60% probability, what proportion of those matches has actually been won by the home team? This technique uncovers some subtle miscalibrations of the model. Home win probabilities tend to be slightly underconfident at lower levels (e.g. 10-30% bins). Market-implied probabilities exhibit a marginally higher reliability. Predictions for all outcomes are largely well calibrated across most bins.

Predicted probabilities and actual frequencies – reliability. The figure shows reliability plots for the predicted probabilities of home win, draw and away win. Panel (a) illustrates the reliability – i.e. the comparison of predicted vs. actual frequencies – of the finetuned model probabilities, obtained by applying isotonic regression to the Skellam-based forecasts. Panel (b) displays the performance of market-implied predictions. Each point reflects the empirical frequency of the outcome within a probability bin containing at least 10 observations. Perfect calibration corresponds to the 45-degree diagonal reference line; deviations indicate misalignment between predicted probabilities and empirical frequencies. Both model and market forecasts are evaluated out-of-sample over the 2016/17 through 2024/25 Bundesliga seasons, with model probabilities calibrated via a two-season rolling isotonic regression (see Section “Data and modelling framework”).

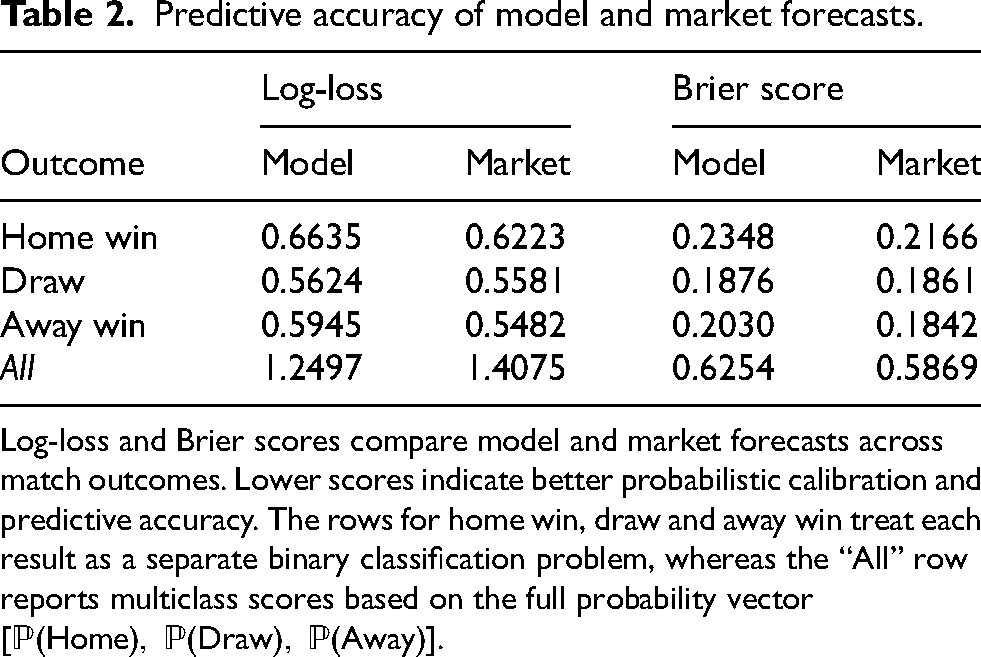

Table 2 presents a numerical comparative assessment of model-derived and market-implied forecasts across different match outcomes using log-loss and Brier scores. Bootstrapped 95% confidence intervals (not reported to preserve table clarity) lie within approximately

Predictive accuracy of model and market forecasts.

Log-loss and Brier scores compare model and market forecasts across match outcomes. Lower scores indicate better probabilistic calibration and predictive accuracy. The rows for home win, draw and away win treat each result as a separate binary classification problem, whereas the “All” row reports multiclass scores based on the full probability vector

Model-based betting

Threshold ‘optimisation’

Although a forecast indicating positive expected value (

Basic thresholds are introduced to determine empirically where potentially attractive bets can be found. They act as a form of practical ‘calibration’, narrowing the betting universe. Concretely, dynamic thresholds in a rolling-window setup are used. Based on information from an in-sample period – set again to two seasons here – the following filters are applied: a minimum expected value

The betting opportunities are then scanned with the help of a grid search,

3

and, individually for home, draw and away bets, the thresholds are tuned by varying

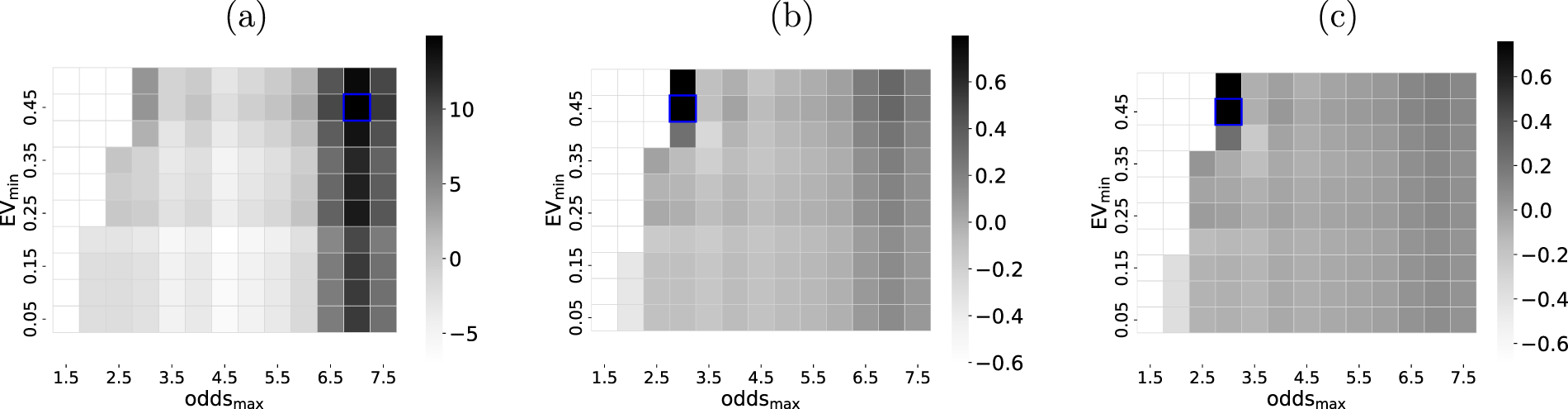

Figure 5 illustrates the threshold optimisation process. For the example used, it is evident that the maximisation of the P&L aims for higher odds and thus greater potential payouts. For both ROI and Sharpe ratio, higher risk bets are constrained, however, as not commensurate with the optimisation goal.

Illustration of grid search for parameter optimisation. On the example of home win bets within a single calibration window (2018/19 through 2019/20 seasons), the grid search for ‘optimal’ in-sample parameters across

Out-of-sample performance

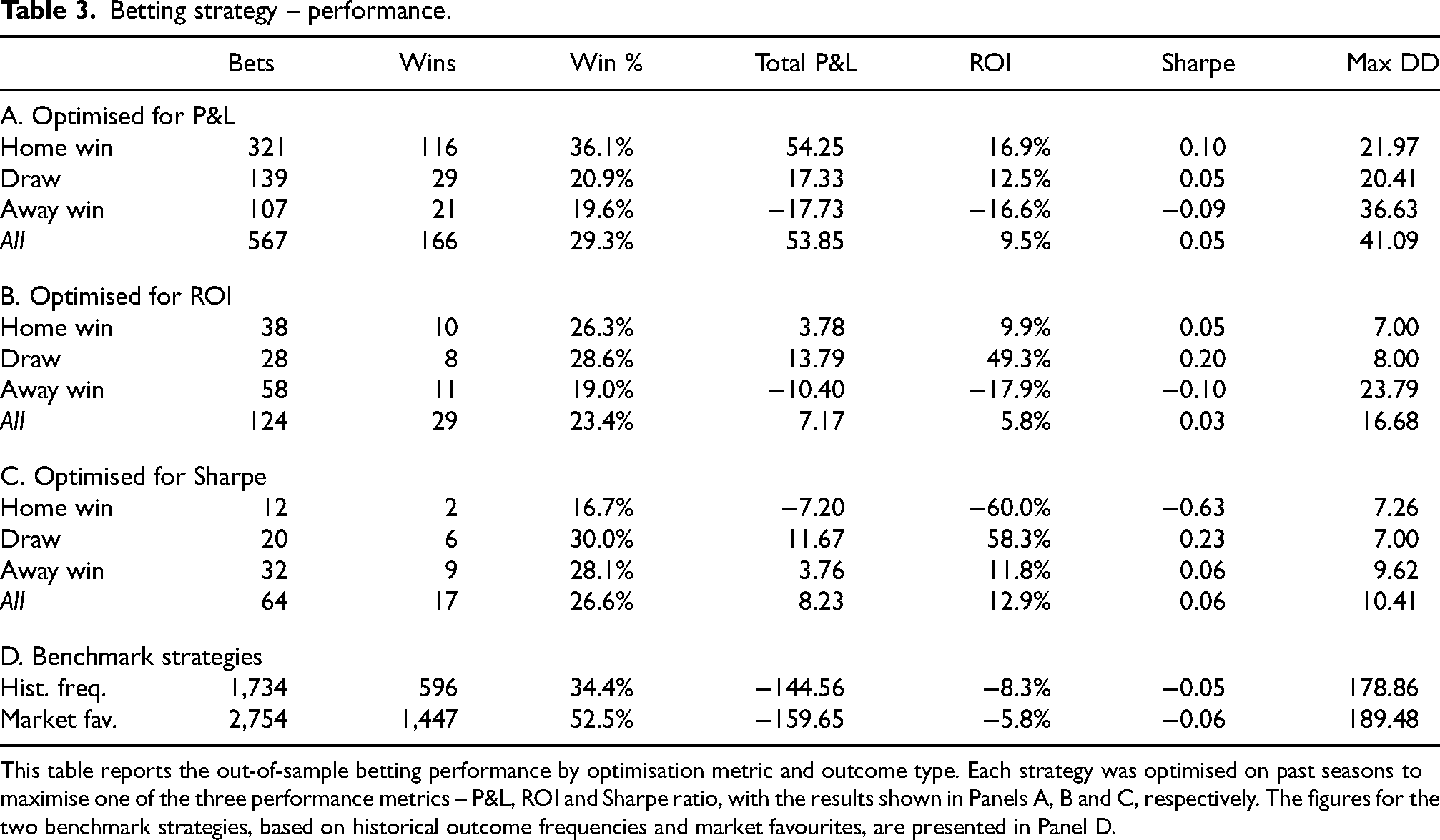

The results from the rolling-window procedure and seasonal bet placements are summarised in Table 3. Performance metrics are reported only for season–outcome combinations with at least five qualifying bets (see also Section “Threshold ‘optimisation”’), to avoid overinterpreting very small samples. Depending on whether the in-sample optimisation targets the highest P&L, ROI or Sharpe ratio, the resulting out-of-sample performance differs noticeably.

Betting strategy – performance.

This table reports the out-of-sample betting performance by optimisation metric and outcome type. Each strategy was optimised on past seasons to maximise one of the three performance metrics – P&L, ROI and Sharpe ratio, with the results shown in Panels A, B and C, respectively. The figures for the two benchmark strategies, based on historical outcome frequencies and market favourites, are presented in Panel D.

When aiming for the highest P&L in the calibration phases (Panel A), the majority of the bets that are placed back home wins. About one-third of them are won and generate ca. 17% ROI. The inherent P&L volatility, however, renders the Sharpe ratio rather unattractive. Draw and away bets are placed less frequently and are successful in only around 20% of the cases. Backing away wins in particular is detrimental to the overall strategy and exhibits a standalone ROI of approximately -17%. In all three types of bets, the maximum drawdown (DD) suggests a rather high degree of instability across time, leading to periods of noticeable decreases in cumulative P&L. Overall, across all outcomes, a positive ROI remains – which would have been markedly higher if away bets were not to be placed.

The in-sample optimisation with respect to the highest ROI (Panel B) leads to substantially fewer placed bets. The overall ROI amounts to about 6% in this setup, still in conjunction with a very low Sharpe ratio. In line with this, even fewer bets are placed when targeting the highest Sharpe ratio during the in-sample grid search (Panel C). The very limited number of positions renders the resulting statistics not very insightful. The scarcity of the bets is driven by the very restrictive in-sample optimisation that, in many cases, tends to demand a large

The two baseline strategies that place bets based on historical occurrence rates and market favourites, respectively, consistently lose money (Panel D), with ROI of -8% (historical frequency) and -6% (market favourite). Notably, despite a high win rate, the low odds on favourites result in a negative ROI owing to poor payout. This is in line with expectations, given that betting markets do not offer sustainable gains for uninformed bettors. As such, the simple model developed and tested here outperforms naive strategies.

Figure 6 visualises the cumulative P&L, additionally broken down by outcome type, on the example of an optimised in-sample grid search for the highest P&L. As seen in Table 3, the pattern is again clear: home win bets drive most gains, draw bets play a minor role, and away bets underperform.

Cumulative P&L of betting strategy. The plot illustrates the cumulative P&L broken down by outcome type – home win, draw, away win – and aggregated across all bets (“All”). The results are based on optimising the in-sample parameter search for the highest P&L, i.e. aligned with Panel A in Table 3.

While the strategy evaluation abstracts from execution frictions, several real-world constraints should be noted. First, odds may not be available at meaningful volume, particularly for less liquid outcomes. Second, transaction costs such as spreads, commissions or slippage could erode profitability — especially at small edges or high turnover. Third, some bookmakers impose limits or account restrictions that may hinder systematic execution. These factors suggest that the reported returns represent an upper bound and should be interpreted as indicative of latent signal quality rather than readily realisable profits.

Robustness and sensitivity analysis

Season-by-season performance

Figure 7 illustrates the out-of-sample performance across individual Bundesliga seasons, on the example of the in-sample grid search optimised for the highest P&L. These results offer a more granular view of the overall performance patterns documented in Section “Results”, where pooled metrics indicate a certain profitability in terms of cumulative P&L.

Season-by-season performance of betting strategy. This figure shows the P&L by season and outcome type – home win, draw, away win – and aggregated across all bets (“All”). The figures are based on optimising the in-sample parameter search for the highest P&L. Each bar shows the number of placed bets as additional information.

The generally high variability of the P&L over time is evident. Some seasons exhibit broad profitability (e.g. 2019/20), others underperform across the board. These fluctuations are consistent with the earlier findings in Section “Results”. The number of bets placed also fluctuates notably, despite the in-sample grid search spanning a period of two years. The picture is very similar for ROI and Sharpe ratio, and likewise when the in-sample optimisation explicitly targets those metrics (not shown here).

The pattern suggests that value opportunities in the market are inherently irregular or that the identification algorithm lacks sufficient specificity. Given a combination of sparse opportunity and high variance, systematically betting – at least under the current specification – is unlikely to be consistently profitable in the long run.

Parameter sensitivity

xG values: ‘calibration’ window

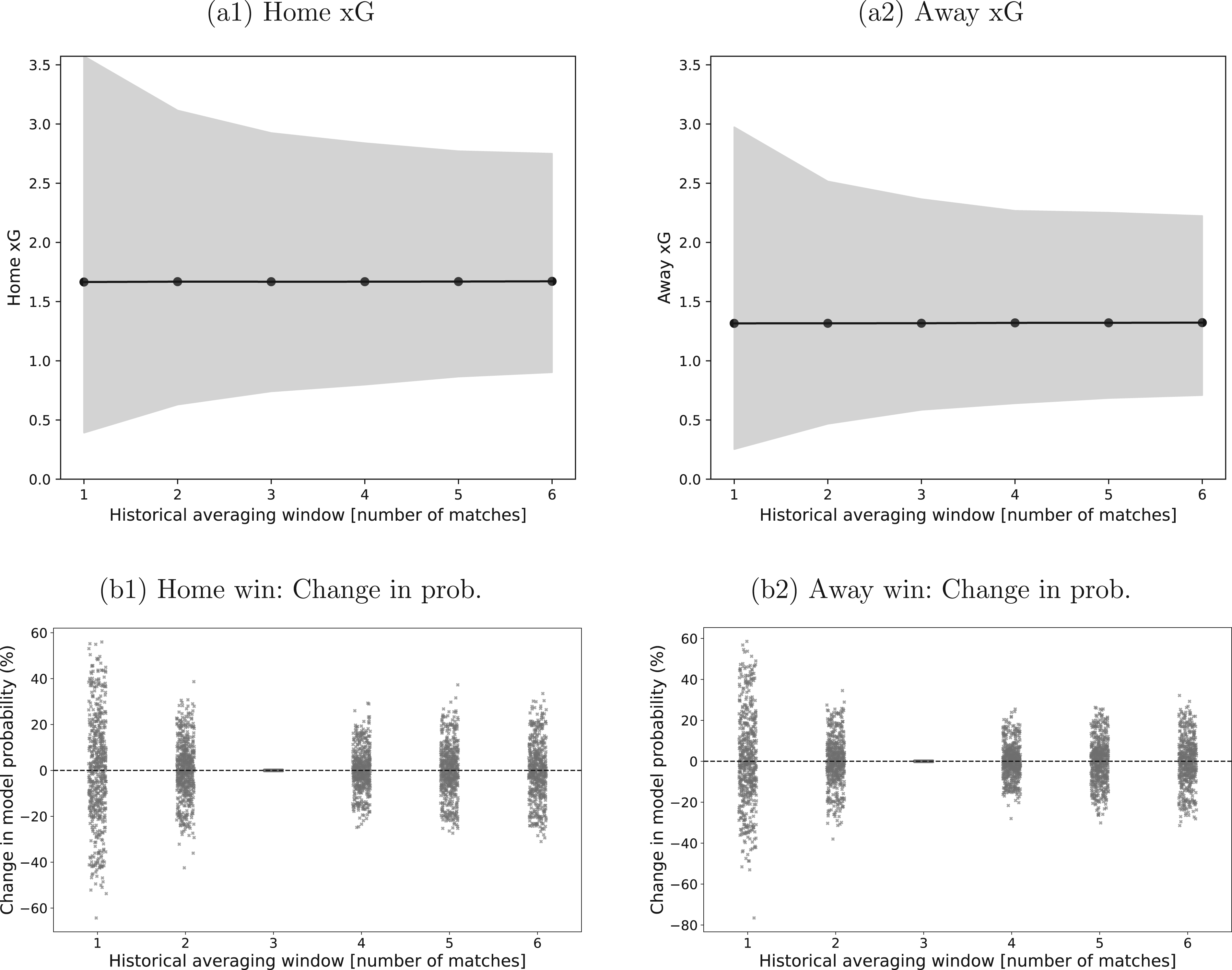

The estimation of the xG values is a crucial part of the modelling framework. The use of the average of the most recent

Sensitivity of xG estimates and model probabilities to the historical estimation window. Panel (a1) shows the average xG for home teams across all matches as a function of the length of the historical averaging window

When translating the xG averages into actual match probabilities, Figure 8 also provides the distribution of the differences over the base case. The majority of those are in the region of

The sensitivity of the ultimate profitability of the strategies to the xG determination (not shown here in detail) is moderate. For

Odds: securing best ones in the market

The main results in Section “Out-of-sample performance” rely on the assumption that average market odds can be secured for all bets. This guarantees a certain liquidity and realistic execution setup. In an ideal case, bets could be placed at the best odds instead. The results of this modification – in comparison to the base case – are shown in Table 4.

Betting strategy – performance using average vs. best odds.

This table reports the out-of-sample betting performance under flat stakes, comparing the use of average odds (Section I) and best available odds (Section II). Strategies were optimised for P&L.

Notably, the better odds are used for the actual bets but not for determining the betting decision itself; the latter are still based on the same grid search as before, to ensure that the trading ‘signal’ itself is robust enough. The P&L for backing away wins is still negative, but the total P&L is now substantially higher (

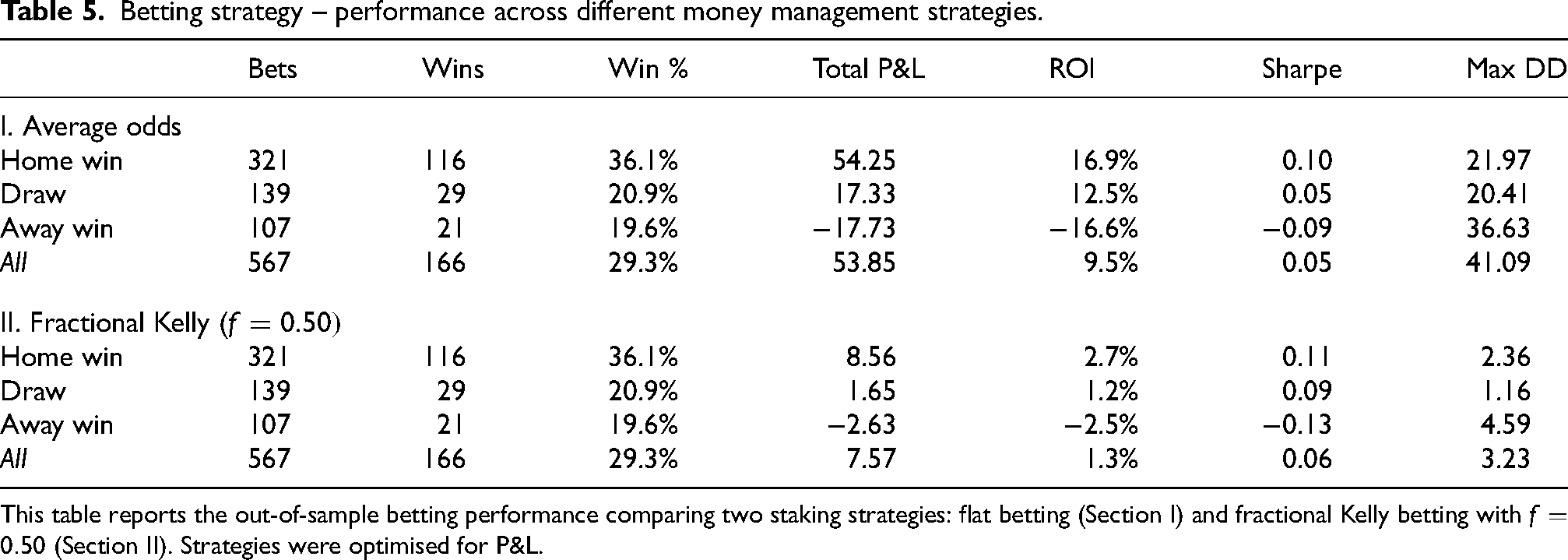

Money management strategy: fractional Kelly

Table 5 highlights the effect of fractional Kelly staking with

Betting strategy – performance across different money management strategies.

This table reports the out-of-sample betting performance comparing two staking strategies: flat betting (Section I) and fractional Kelly betting with

The fractional Kelly method produces more moderate total profits and ROI, reflecting its more conservative stake sizing. Sharpe ratios remain low and close to those observed under flat betting, while maximum drawdowns exhibit a pronounced reduction, indicating improved capital preservation.

More adaptive approaches could further refine capital allocation. For example, dynamic Kelly schemes adjust

Impact of isotonic calibration

Finally, in order to gauge whether the positive ROI are driven primarily by the isotonic calibration layer or by the underlying xG-Skellam signal, the betting performance was recomputed with the isotonic regression step removed. With isotonic calibration, the main flat-stake strategy based on average odds achieves a total profit of about 54, corresponding to an ROI of roughly 10%. Without isotonic calibration, applying the same selection mechanism directly to the raw Skellam probabilities still produces a positive but much smaller profit of around 6, with an ROI close to 1%. The incremental gain from isotonic regression is therefore material, but the underlying xG-Skellam model already exhibits some predictive value on its own.

The cross-section of bets indicates that the main role of isotonic calibration is to trim poorly calibrated away-win positions. Without the additional step, away bets generate a strongly negative ROI of about

Conclusion and outlook

This paper evaluates whether simple, xG-based models can generate accurate and economically valuable football forecasts. Using a Skellam distribution to convert recent xG values – augmented by isotonic regression to improve forecast calibration – into match probabilities, the model is assessed across eleven Bundesliga seasons by comparing predictive accuracy and calibration to those of bookmaker-implied probabilities.

While market odds remain better calibrated, the xG-based model captures certain structural signals that translate into modest but consistent profitability in simulated betting, with the strongest performance observed for home win outcomes. Away bets tend to dilute returns. The isotonic calibration layer improves both reliability and profitability mainly by trimming poorly calibrated away-win positions, while robustness checks show that the underlying xG-Skellam probabilities already contain a modest positive signal on their own. Performance shows some robustness but varies across seasons and bet types. Alternative staking methods, such as fractional Kelly, help reduce drawdown risk but trade off against total return.

A natural next step would be to explore ensemble-style forecasts that combine model- and market-based probabilities. Since the model uncovers latent inefficiencies while markets offer strong calibration, blending the two could improve reliability and economic performance without sacrificing interpretability. Although this study abstracts from frictions such as slippage or betting limits, future work could simulate such effects to better approximate real-world execution. Similarly, while richer feature sets or dynamic inputs might improve accuracy, any such additions should be judged by whether they enhance usability without undermining the core strengths of simplicity, robustness and low model risk. In contrast to recent studies that employ complex machine learning architectures or context-aware expected points models (Bassek et al., 2025; Cavus and Biecek, 2022), this study deliberately prioritises structural parsimony and interpretability.

In summary, the analysis shows that simple, data-driven models – if well-constructed and properly filtered – can extract meaningful signals and, in some settings, deliver economically viable returns from football betting markets. As economist Tim Harford observed: “The power of a good model lies not in its complexity, but in its ability to illuminate.”

Footnotes

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and publication of this article.

Data availability

Historical xG data and betting quotes are freely available from Understat and Football-Data, respectively.