Abstract

The impact of the COVID-19 pandemic on migrant remittances has generated a great deal of confusion and debate. This article aims to test three conflicting global and local narratives about the relationship between the pandemic and remittance flows in the South Africa–Zimbabwe remittance corridor. We refer to these as remittance pessimism, remittance resilience and remittance rerouting narratives. The article presents the pre-pandemic background context of migration from Zimbabwe to South Africa, the evidence for a shift from informal to formal remitting during the pandemic, and the implications of the remittance rerouting narrative for other corridors. We find that many Zimbabwean migrants in South Africa experienced severe economic impacts including unemployment, income loss and lack of access to COVID-19 relief measures. We conclude that there was a significant increase in formal, primarily digital, remittances during the pandemic and a decline in informal remittance conveyance. We highlight the need for more research in other remittance corridors to identify similarities and differences between them in terms of COVID-19 impacts and the shift from informal to formal remittances enabled by digital platforms.

Introduction

The impact of the COVID-19 pandemic on global remittance flows has been the subject of some confusion and dispute. During the first year of COVID-19, for example, the IMF and World Bank and various migration experts confidently predicted that the pandemic would lead to a significant decline in remittances, a result of migrant layoffs and unemployment, return migration, and disrupted remittance channels (Bondarenko, 2020; Ratha, 2021; Sayeh & Cham, 2020; World Bank, 2020). The remittance shock narrative all but vanished during the second year of the pandemic, as macro-level data indicated that remittances had not, in fact, suffered the predicted global collapse. The World Bank revised its gloomy forecast, reporting that remittances to Latin America and Asia had actually increased in 2020 (World Bank, 2021a, 2021b). Although remittances to Africa had declined, much of it was attributed to a 28% decrease in remittances to Nigeria. Other African countries had ‘defied the odds’ and saw a marked increase in remittances during 2020 (Kpodar et al., 2023).

Various hypotheses have been advanced for remittance resilience and why the early projections of the remittance shock narrative were so mistaken. One explanation focuses on migrant altruism and the desire to help families in countries of origin. Kpodar et al. (2023), for example, suggest that migrants responded to COVID-19 by trying to cushion the economic impact of the pandemic in their home countries. According to the World Bank (2021a, 2021b), migrants sent more money home and sacrificed their own needs by reducing consumption and drawing on savings, as well as accessing employment support programmes, which provided them with the extra funds to increase remittances.

A third remittance narrative seeks to resolve the paradox of remittance resilience despite the pandemic shock to migrant employment and incomes. Rather than an absolute increase in the value of remittances, this narrative suggests that there was a major rerouting of remittances from informal to formal (and therefore recorded) channels. As Dinarte-Diaz et al. (2022) note, ‘mobility restrictions made it much harder for migrants and their families to carry cash across borders, as well as within host countries’. Dinarte et al. (2021) argue further that the pandemic accelerated a pre-pandemic trend of growing use of digital platforms by increasing the range of options and reducing transaction costs. Thus, the increase in recorded remittances in 2020 may simply reflect increased use by migrants of formal channels such as banks, MTOs (money transfer operators) and digital remittance service providers (RSPs).

General explanations for pandemic changes in remittance flows fail to explain why there was so much inter-country spatial variation in remitting outcomes. If some countries received massive increases in remittances and others did not, does this mean that migrants from the former took less of an unemployment and income hit than migrants from the latter? Again, does it mean that migrants from the former were somehow more altruistic or had greater access to formal remittance channels than migrants from the latter? Or, following Dinarte-Diaz et al. (2022), were the major behavioural changes brought about by the pandemic both a reduced capacity to remit and a counterbalancing shift from informal to formal remitting channels? These questions can only be properly answered through detailed case study research in migration and remittance corridors.

This article aims to test the applicability of the remittance shock, resilience, and rerouting narratives in the South Africa–Zimbabwe migration corridor during COVID-19. Drawing on data from two surveys of Zimbabwean migrant households in South Africa before and during the pandemic, the article seeks to answer the following three questions: first, did the pandemic negatively affect the employment and income of Zimbabwean households in South Africa? Second, what impact has the pandemic had on the ability of households to sustain pre-pandemic levels and frequency of remitting? And, finally, did restrictions on mobility prompt a shift from informal to formal remitting channels? The next section of the article discusses the survey methodology and other data sources. We then present the pre-pandemic background context of migration from Zimbabwe to South Africa and remittance flows between the two countries. The following section analyses the survey results, including the impact of the pandemic on migrant employment and incomes. We then present the evidence for a shift from formal to informal remitting during the pandemic and how this affected the relative importance of formal and informal remittance channels. Finally, the article revisits the general debate about remittance flows during COVID-19 and calls for more research in this and other corridors.

Methodology

The data for this article comes from the following three sources: (a) the 2022 Zimbabwe Census which provides the most up-to-date picture of the Zimbabwean migrant stock in South Africa; (b) South African Reserve Bank (SARB) data on formal remittances from South Africa to Zimbabwe; and (c) two household surveys of Zimbabwean migrant households in South Africa. The first survey was conducted in Cape Town and Johannesburg in 2016 and the second was conducted in the two cities during the third wave of the pandemic in July and August 2021. A total of 500 Zimbabwean migrant households were sampled in each case, 250 in each city. These cities were selected because they are the major South African destinations for Zimbabwean migrants. The two surveys were conducted in the same six neighbourhoods which ensures a degree of comparability between the two samples. The selected sites were Dunoon, Masiphumelele, and Nyanga in Cape Town, and Johannesburg Central, Alexandra Park, and Orange Farm in Johannesburg. In each site, six migrant households were initially randomly located and assigned numbers between 1 and 6. Using a dice, the first household to be interviewed was selected. That household was interviewed and identified one other household to approach. The process was repeated until the target number was reached before moving on to the next site where the same procedure was repeated. Household heads were interviewed but, in their absence, a partner or any household member above the age of 18 with knowledge of household food economics was chosen for interview.

Pre-COVID Migration and Remittances

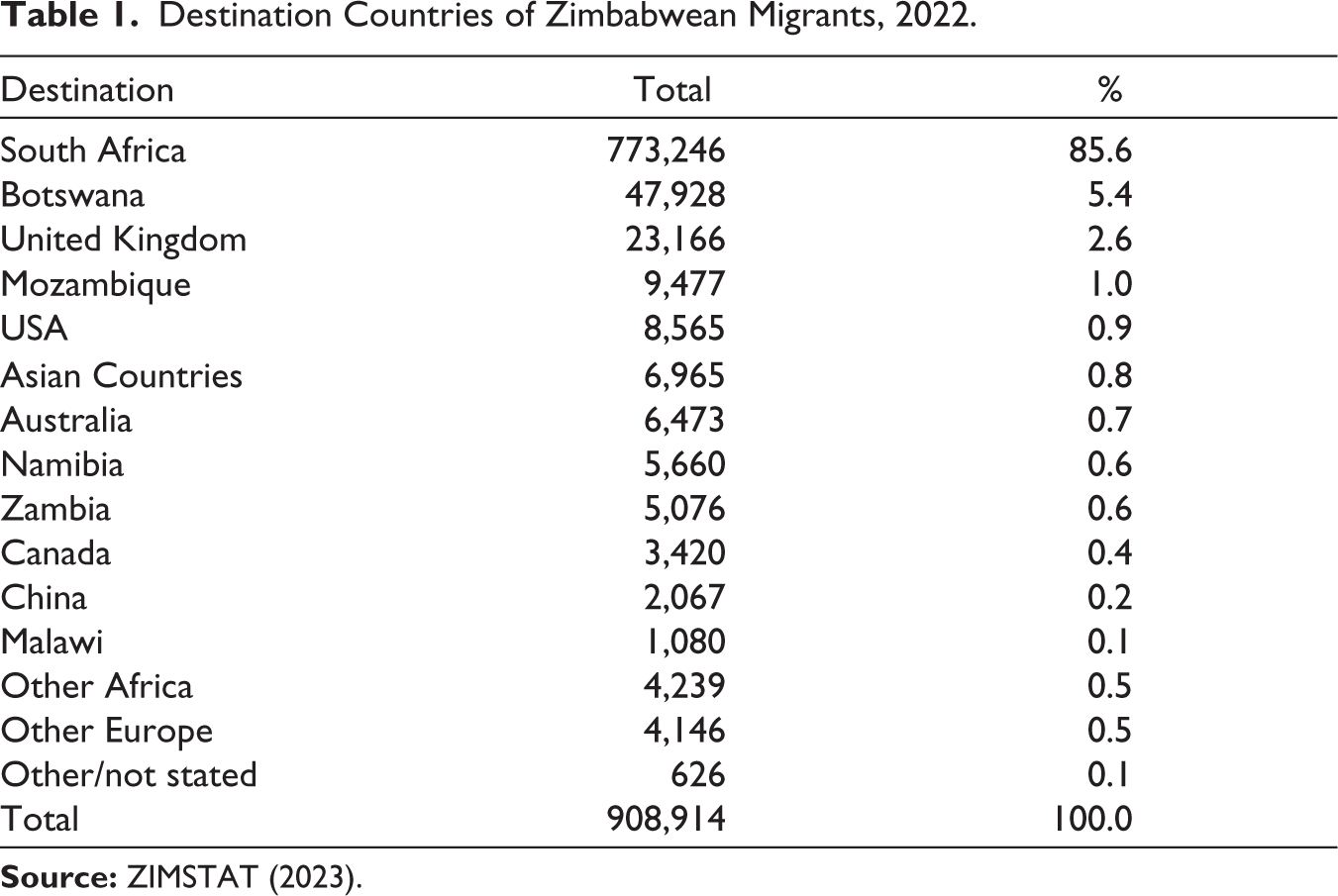

The prolonged economic and political crisis in Zimbabwe has led to a major exodus from the country in the last two decades (Chikanda & Crush, 2018; Crush et al., 2015; Crush & Tevera, 2010). Data from the 2022 Zimbabwe Census indicates that 520,240 Zimbabwean households (or 14% of the total) have at least one member living outside the country (ZIMSTAT, 2023). The total number of migrant individuals recorded is 908,914 of whom the vast majority—773,246 or 86%—live in South Africa (Table 1). Before the COVID-19 pandemic, many Zimbabwean migrants in South Africa relied on insecure employment in low-wage sectors such as commercial agriculture, domestic work, day labour and artisanal mining (Baison, 2021; Bolt, 2015; Jinnah, 2022; Pretorius & Blaauw, 2015). As a result, a significant number of migrants in urban areas of South Africa sought a livelihood in the informal sector.

Destination Countries of Zimbabwean Migrants, 2022.

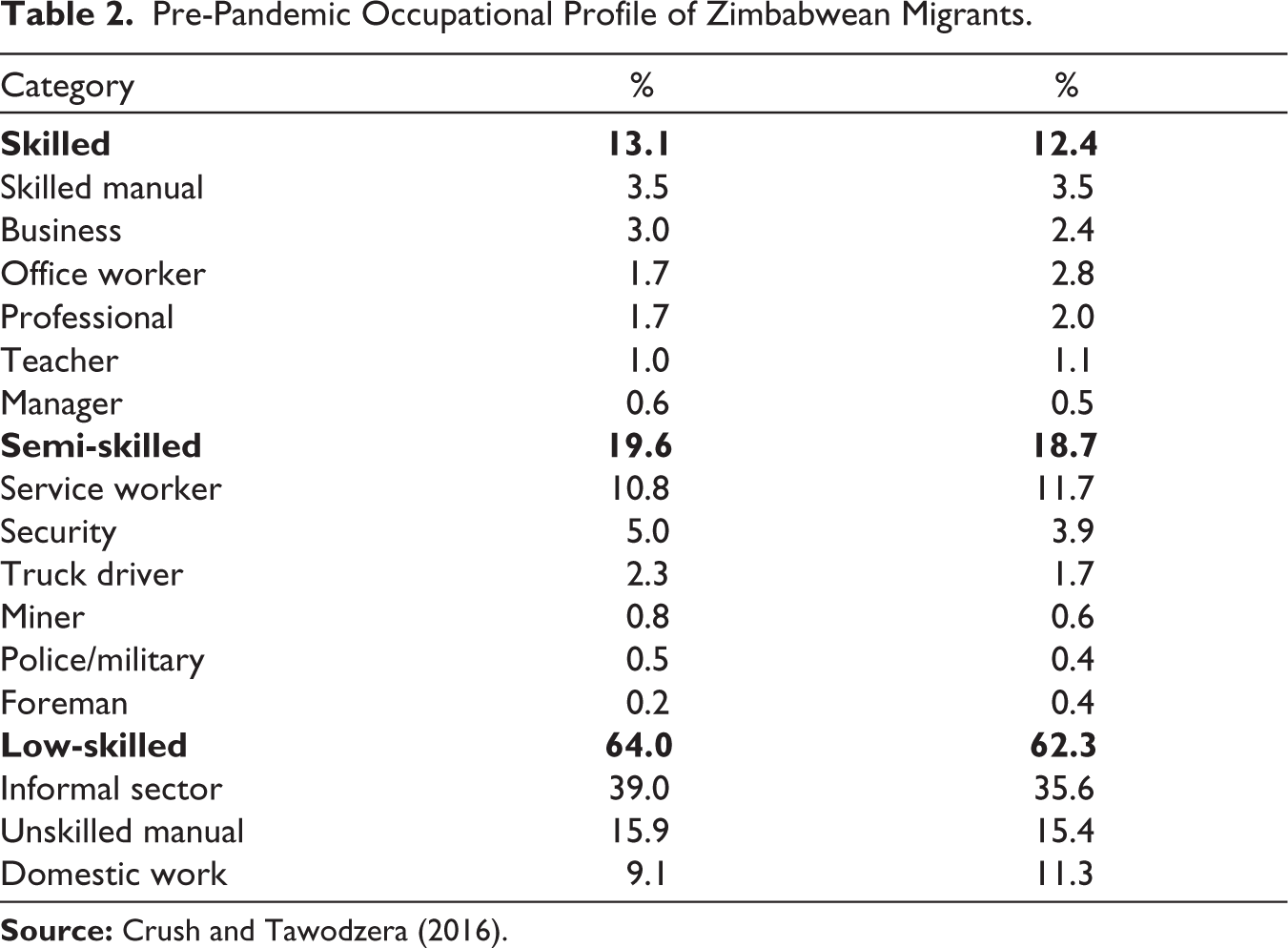

A pre-COVID survey of Zimbabwean migrant households in Cape Town and Johannesburg by the authors demonstrated the limited access of migrants to formal sector employment (Crush & Tawodzera, 2016). Only 13% of the heads surveyed (and 12% of other household members) were regularly employed in skilled formal sector jobs (Table 2). Another 20% of heads and 19% of members were working in a range of semi-skilled jobs, of which work in the services industry was most important. Almost two-thirds of both groups were employed or self-employed in informal trade (39% and 36%), manual work including day labour (16% and 15%) and domestic work in private households (9% and 11%). Other surveys in these two cities found that Zimbabwean migrants have the highest share of jobs in the urban informal sector (23% of all participants in Cape Town and 28–30% in Johannesburg) (IOM, 2021; Peberdy, 2016; Tawodzera et al., 2015).

Pre-Pandemic Occupational Profile of Zimbabwean Migrants.

There is a large literature on the remitting characteristics, motivations and behaviours of Zimbabwean migrants in South Africa before COVID-19 (Chikanda & Dodson, 2013; Hungwe, 2017; Makina, 2013a; Moyo & Nicolau, 2016; Tevera et al., 2010). Most migrants remit to Zimbabwe, but the amounts and frequency vary depending on job status, income, education and age. Remitting also initially increases and then declines with increasing length of time since first migration (Makina & Masenge, 2015). Zimbabwean households sending migrants are heavily dependent on remittances from abroad (Bracking & Sachikonye, 2010; Maphosa, 2007; Mazwi, 2022; Muzapu & Havadi, 2021; Ncube & Gomez, 2015; Nyikahadzoi et al., 2019; Nzima et al., 2017). Remittances are spent predominantly on livelihood needs such as housing, food purchase, medical treatment, transportation, clothing, and children’s education.

Before the pandemic, the remittance corridor between South Africa and Zimbabwe was characterised by a high degree of informality (Chisasa, 2014; Mlambo, 2021). FinMark (2021) estimates that almost 70% of remittances flowed through informal channels in 2019. Government exchange controls, the difficulty for migrants of opening bank accounts in South Africa, and high bank charges combined to discourage the use of formal remittance channels (Nicoli et al., 2018; Nzima, 2017). From 2013, global MTOs such as Western Union were permitted to enter the South African remittances market, but only if they partnered with a major South African bank (Luhabe-Morrison, 2018). Advocates of digital platforms for remittances emphasised the local challenges of scaling up fintech usage (Nicoli et al., 2018; Smith & Van Zyl, 2021; Technoserve, 2016). Mlambo (2021), for example, notes that ‘the Southern African market is failing to benefit from benefits presented by mobile technology. This inability of the Southern African market to reap the benefits of mobile technology is caused by the poor telecommunications infrastructure, poor financial awareness and absence of business-friendly legislation’.

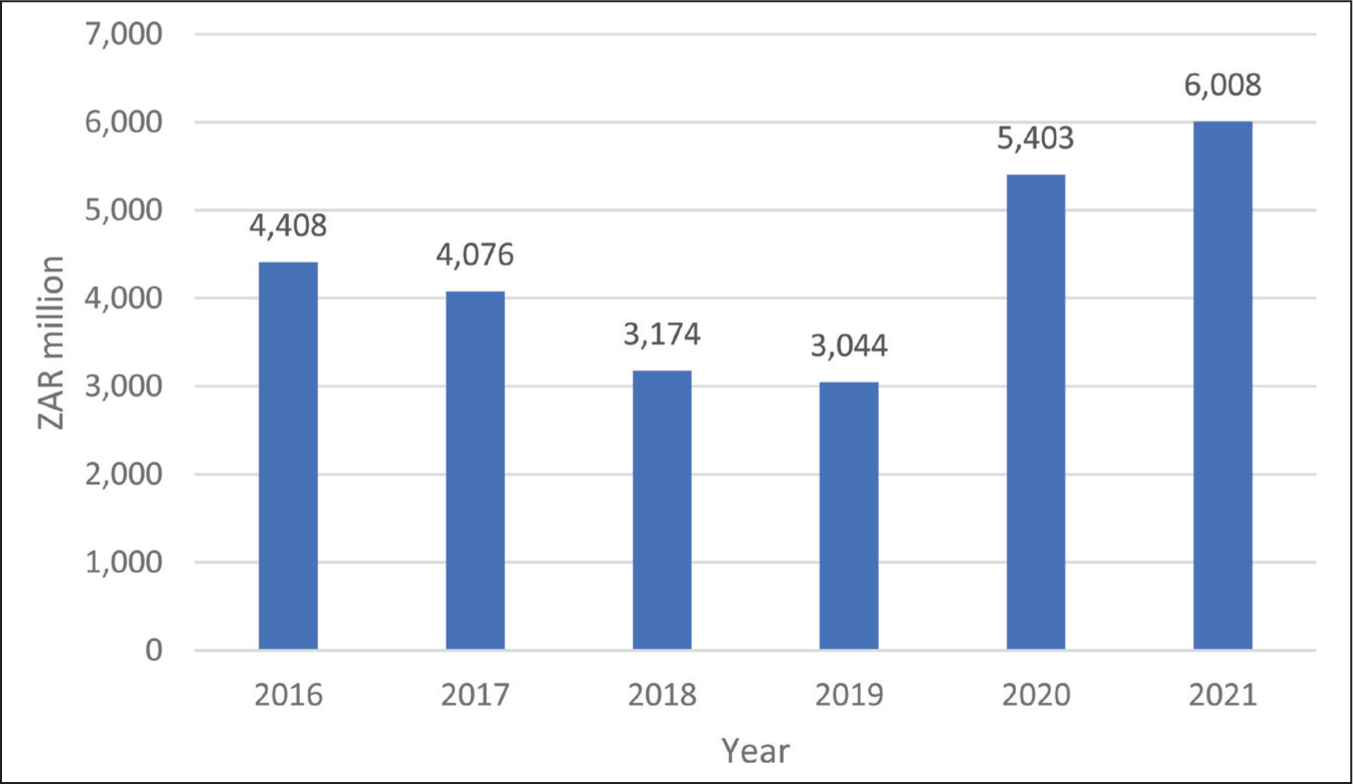

In this environment, informal channels proved very attractive to migrants and led to a boom in the informal remittance industry (Makina, 2013b; Nzima, 2017; Onyango, 2021). In addition to personal cash transfer by migrants and their friends and relatives visiting Zimbabwe, migrants relied on taxi and bus drivers and conductors as couriers and private transporters (known as omalayisha) who would deliver remittances directly to recipient households in Zimbabwe (Nyamunda, 2014; Nyoni, 2012, 2021; Thebe, 2015; Thebe & Mutyatyu, 2017). Makina’s (2013a) survey of Zimbabweans in Johannesburg found that 98% relied on informal channels. Another survey of migrant-sending households in Zimbabwe reported higher use of banks and the post office, but 60% of households still received remittances through informal channels (Tevera et al., 2010). Our survey of Zimbabwean households in Cape Town and Johannesburg found that two-thirds of the remitters used informal channels (Crush & Tawodzera, 2016). Using a different methodology, FinMark (2018) calculated that 60% of total remittances were informal and, therefore, unrecorded, in 2018. Figure 1 from SARB data shows that formal remittances fell in the years immediately before the pandemic in 2020. Total remittances declined from ZAR4,408 million in 2016 to ZAR3,044 million in 2019, most likely because migrants were making increased use of informal remitting channels. This trend abruptly reversed in 2020 and 2021 when recorded remittances increased to unprecedented levels.

Pandemic Livelihood Disruption

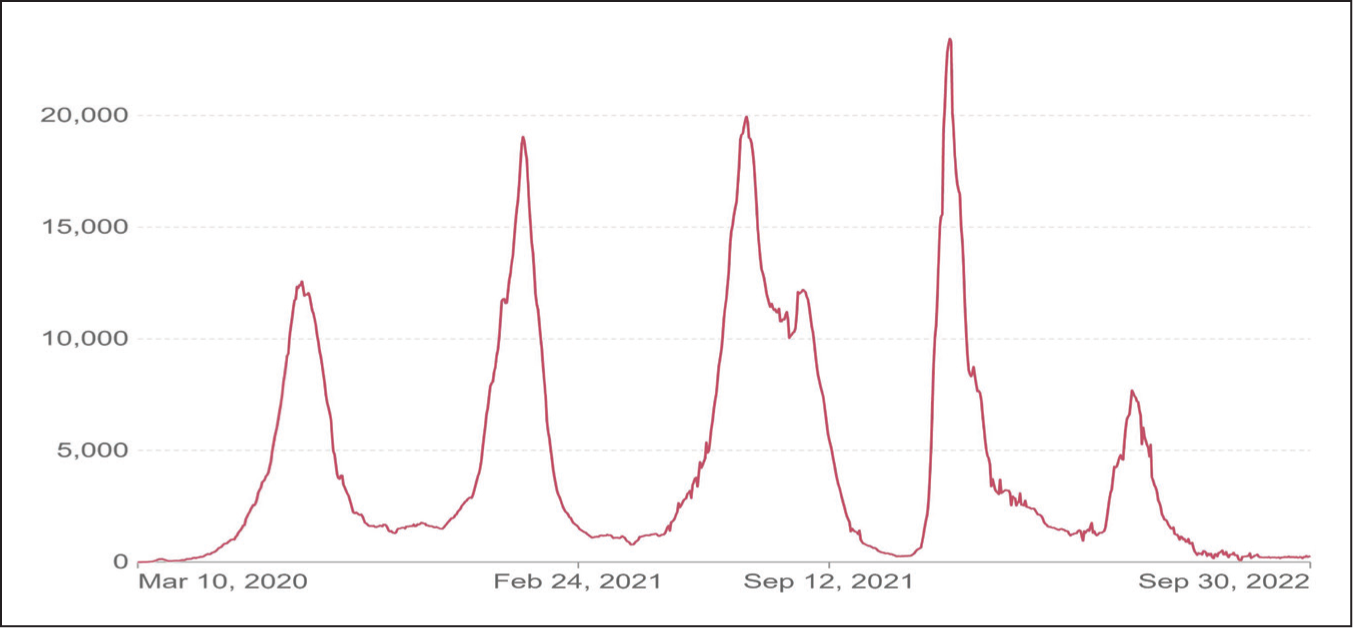

The first recorded case of COVID-19 in South Africa was on March 5th, 2020. At the peak of the first wave in July 2020, over 15,000 people per day were testing positive (Figure 2). By September 30th, four million cases and over 100,000 deaths had been recorded. Excess deaths during the first four waves are estimated at almost 300,000, which would bring total COVID-related mortality in South Africa to over 400,000 (Bradshaw et al., 2022).

The South African government declared a state of disaster on March 15th and imposed a sweeping national lockdown on March 26th, including a stay-at-home order for all except essential workers which was vigorously enforced by the police and the army (Faull et al., 2021; Lamb, 2023; Mkhwanazi et al., 2020; Seekings & Nattrass, 2020). Breach of lockdown regulations was deemed a criminal offence punishable by a fine or up to six months imprisonment. Under the lockdown, people could only leave their homes to buy food, access social grants, seek medical attention or attend funerals in small groups. All public amenities, sporting and cultural events, schools and universities, churches and mosques, and businesses (except those selling food) were ordered to close. The sale of alcohol and cigarettes was outlawed on the grounds that their use encouraged the spread of the virus.

International travel to South Africa was halted and movement between provinces and in and out of cities was also banned. The land border between South Africa and Zimbabwe was closed to all but essential travel and the South African government constructed a largely symbolic 40km fence on either side of the mainland border post between the two countries at Beitbridge. Nearly 300,000 people were arrested by mid-2020, more than in any other country globally. Harsh pandemic restrictions were gradually relaxed after 100 days but re-imposed in December 2020 during the second wave of the pandemic, and again from May to July 2021 during the third wave.

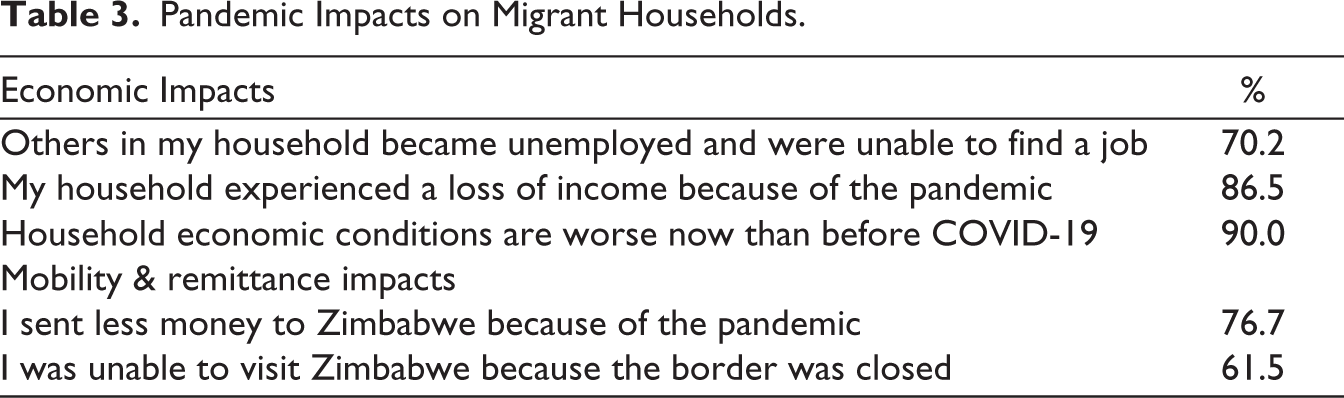

The lockdown had three major consequences for Zimbabwean livelihoods in South Africa. First, many migrant households lost their source of income as businesses laid off or furloughed their workforce. In total, around 5 million workers lost their jobs in South Africa between February and April 2020 (Rogan & Skinner, 2020; Skinner et al., 2021). Zimbabweans working in the hospitality industry, domestic work and as day labourers were particularly badly affected (Blaauw et al., 2021; Mbeve et al., 2020). Pandemic restrictions on informal sector activity deprived many migrants of an alternative source of income (Battersby, 2020; Wegerif, 2020). Our survey found that 72% of respondent household heads had experienced unemployment as a direct consequence of the pandemic restrictions (Table 3). An additional 70% of the households had experienced unemployment of another member. As many as 86% of the households experienced a fall in income during the pandemic. Around 90% indicated that their household economic conditions were worse (65%) or much worse (25%) than before the pandemic.

Pandemic Impacts on Migrant Households.

Second, as Tesfai and de Gruchy (2021) note, South Africa’s mitigation response was characterised by ‘a lack of migration-aware and mobility-competent policies’. The nationalistic response to COVID-19 meant that only South Africans automatically qualified for the ZAR50 billion (USD26 billion) in government pandemic relief and the range of economic and social protection measures introduced by government (Bhorat et al., 2021; Moses & Woolard, 2023; Noyoo, 2023). Their lack of access to government relief programs meant that many migrants and refugees experienced additional economic hardship during lockdown (Angu et al., 2022; Mushomi et al., 2022; Mutambara et al., 2022; Nhengu, 2022; Odunitan-Wayas et al., 2021; Ola, 2021).

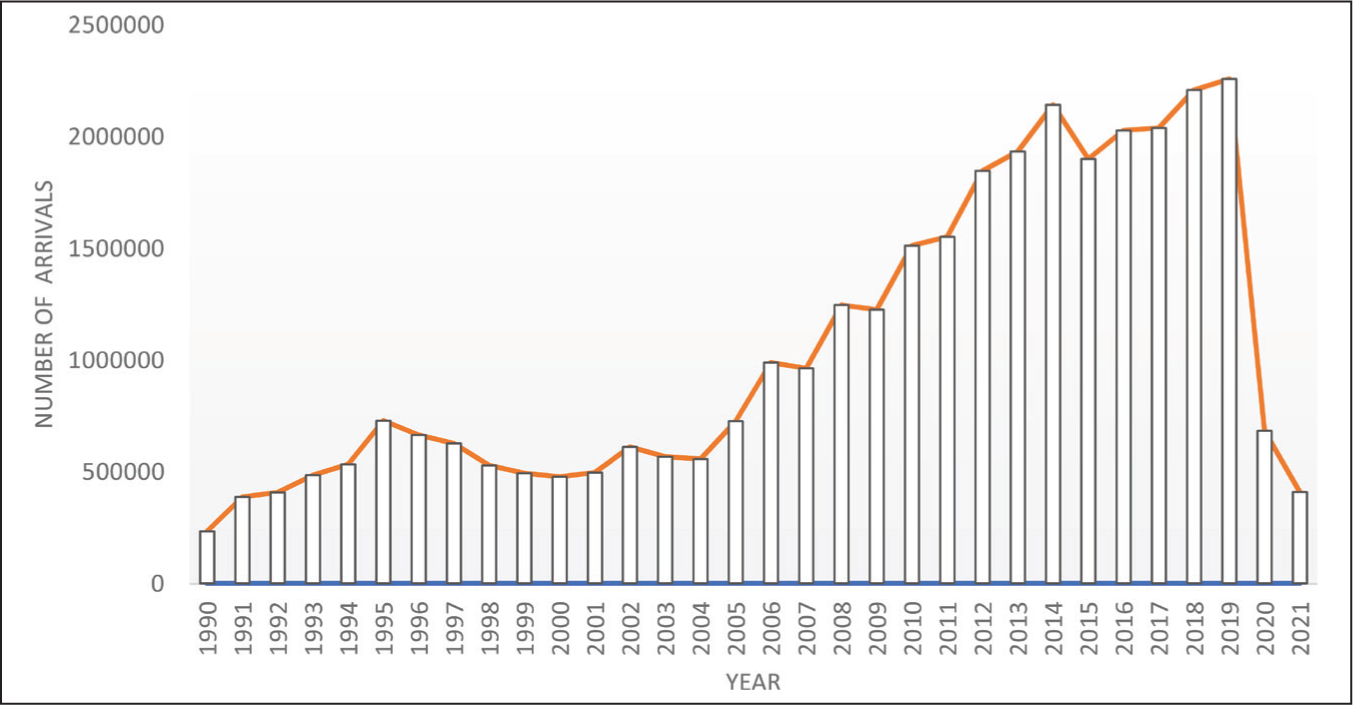

Third, the pandemic lockdown closure of air and land borders between Zimbabwe and South Africa imposed major restrictions on the mobility of Zimbabweans in South Africa. Those who had returned home prior to COVID-19 were trapped in Zimbabwe while those in South Africa were unable to travel to visit (Mukumbang et al., 2020). A major consequence of border closures was a dramatic fall in cross-border traffic between Zimbabwe and South Africa in 2020 and 2021 (Figure 3). In our survey. just over 60% of survey respondents who wanted to visit Zimbabwe had been unable to do so in the 18 months since the borders were closed.

Informal and Formal Remittance Channels

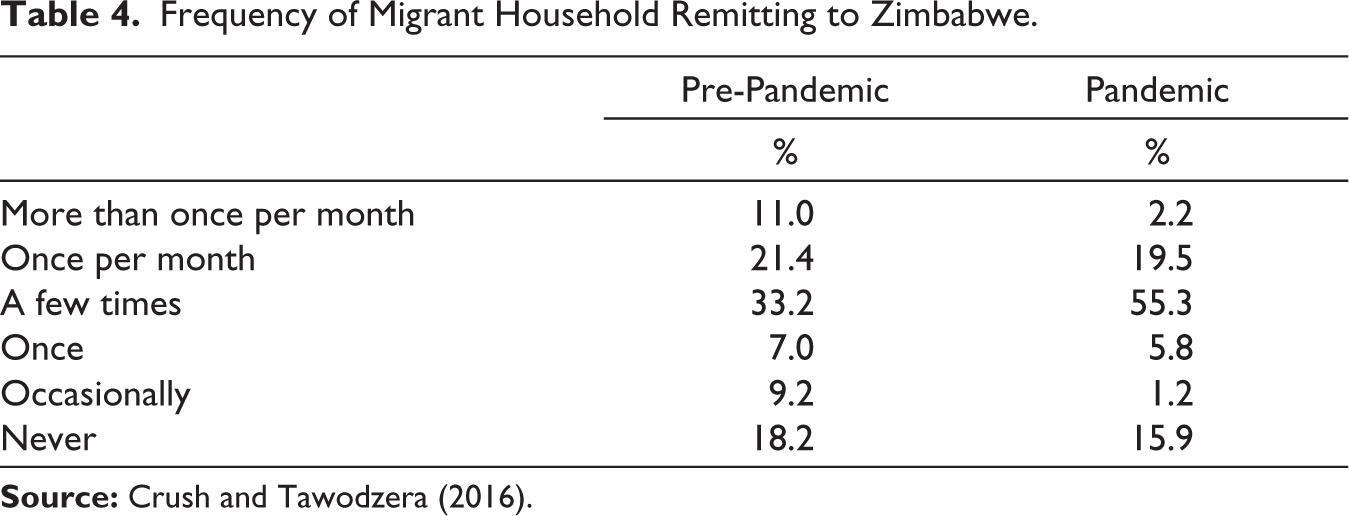

Mbiba and Mupfumira (2022, p. 8) argue that Zimbabwe registered ‘phenomenal increases in remittances’ during COVID-19. They point out that transfers from Europe move through formal channels and suggest that Zimbabwean migrants in the UK ‘dug deep’ to assist relatives in Zimbabwe and ‘sent more money during COVID-19 than in previous years. This happened because of the urgency and gravity of health care and education needs arising during COVID-19 in a fragile socio-economy like Zimbabwe. In addition, the majority Zimbabwean diaspora in the UK retained their jobs and worked extra hours or borrowed to send emergency cash to family in Zimbabwe’ (Mbiba & Mupfumira, 2022, p. 8). By contrast, Masunda and Maharaj (2023) suggest that the pandemic negatively affected the ability of Zimbabwean households in South Africa to remit despite the increased pressures to do so from family in Zimbabwe. Our own survey results suggest that even when Zimbabweans in South Africa ‘dug deep’ they were unable to sustain their pre-pandemic levels of remitting. The number of migrants who remitted nothing at all was only 16% (down slightly from the pre-pandemic figure of 18%). However, more than three quarters (77%) reported that they had remitted less money during because of the pandemic. There was also an accompanying decline in the frequency of remitting (Table 4). Regular remitting (at least once per month) declined from 31% to 22% of households, while infrequent remitting (a few times, once and occasionally) increased from 49% to 61%.

Frequency of Migrant Household Remitting to Zimbabwe.

The survey finding of lower levels and greater infrequency of remitting suggests that, in the aggregate, the total value of remittances should have fallen between 2019 and 2020. However, as Figure 1 showed, there was a massive increase in recorded remittances in 2020 and 2021. The question, therefore, is whether there is an explanation for the paradox of increased remittances recorded by the SARB and the survey results which are indicative of a reduced capacity to remit during the pandemic. One potential explanation is that the major increase in formal remittances was fuelled by a pandemic-related shift from informal to formal remitting channels (Dinarte et al., 2021).

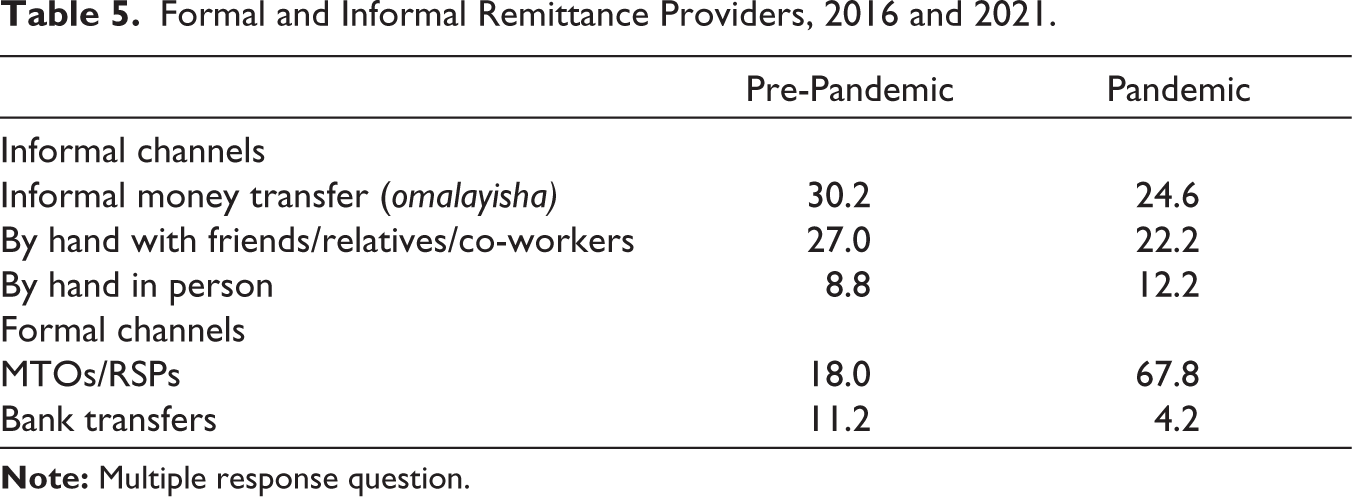

Table 5 compares the patronage of formal and informal remittance channels before and during the pandemic. Prior to the pandemic, 11% of households used bank transfers and 18% of households had switched to MTOs and RSPs. The patronage of bank services for remitting fell from 11% to 4% during the pandemic which is unsurprising given the continued high transactions costs charged by banks and lockdown restrictions. Migrants under lockdown were therefore reliant on other mechanisms for sending remittances. There was a large increase in the patronage of digital RSPs and MTOs from 18% of households in 2016 to 68% in mid-2021. The major beneficiaries of the switch were the new breed of digital RSPs including Mukuru, Mama Money and hellopaisa, and, to a lesser extent, MTOs like Western Union, MoneyGram and Ria, With Mukuru, migrants could use WhatsApp or the Mukuru App to send e-transfers to Zimbabwe, where recipients collected cash from Mukuru orange booths or payout partners such as banks and supermarkets. Remittances could also be transferred directly to Ecocash mobile money wallets. Other digital RSPs (such as Malaicha, Mukuru Groceries, Senditoo, Ahoyi Africa, Shumba Africa and Tinokunda) also provided online ordering of groceries for delivery to recipients in Zimbabwe (Sithole et al., 2022).

Formal and Informal Remittance Providers, 2016 and 2021.

Most informal remittances are transferred to Zimbabwe either by hand or by using the services of omalayisha transporters. The pandemic’s extended closure of land borders between the two countries therefore presented a major challenge to both modes of transferring remittances. Surprisingly, the proportion of households who had used omalayisha only declined by 6%, while conveying remittances by hand (either in person or with someone else) hardly changed at all. In part, this may be because the survey was conducted in 2021 and that movement across borders was easier than in 2020. However, both Moyo (2022) and Mutendi and Chekero (2023) argue that the South Africa–Zimbabwe border remained relatively porous throughout 2020 and that there was a significant increase in two-way irregular border crossing. This would help explain the ability of migrants to take the money themselves or to rely on friends and relatives. Buses and taxis as well as light omayalitsha vehicles were barred from crossing at official land border posts. Permission was restricted to commercially-registered trucks carrying essential supplies such as food imports. Moyo (2022) notes that many omalayisha transporters got around the ban by buying or renting commercial vehicles and posing as essential service providers.

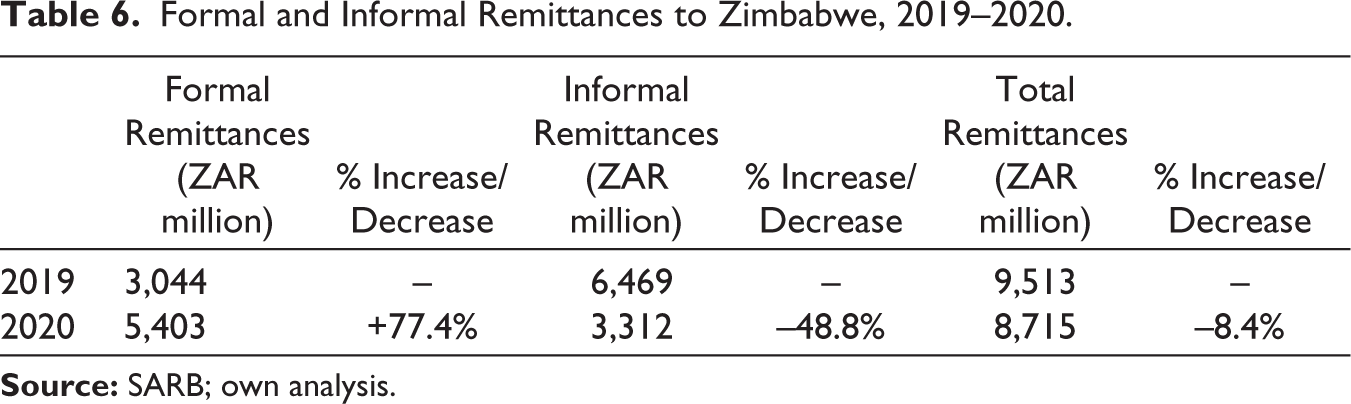

To estimate the magnitude of the shift from informal to formal remitting in 2020, we rely on the FinMark (2021, p. 7) pre-pandemic estimate that 68% of remittances from South Africa to Zimbabwe were informal and 32% were formal. Using this ratio, we estimate that in addition to ZAR3,044 million in formal remittances in 2019, there were an additional ZAR6,469 million in informal remittances for a toral transfer of ZAR9,513 (Table 6). Based on our pandemic survey results on patronage of formal and informal channels, we assume that the pandemic led to a reversal in the pre-pandemic ratio of formal to informal remittances in 2020. We estimate that in addition to the documented 77% increase in formal remittances in 2020, there was a nearly 50% decline in informal remittances from ZAR6,649 million to ZAR3,312 million in 2020. Overall, there was an 8% decline in the total volume of remittances which is more consistent with our survey result of reduced remitting in 2020.

Formal and Informal Remittances to Zimbabwe, 2019–2020.

Conclusion

This article set out to test conflicting global narratives about the impact of COVID-19 on remittance flows with reference to the South Africa–Zimbabwe migration corridor. Underlying these narratives are different, but largely untested, assumptions about the remitting behaviour of migrants during the pandemic. In constructing the first narrative in 2020 it was reasonable to assume that the capacity of migrants to remit was being severely compromised by COVID-19 infection and death, business closures, job layoffs, unemployment and income loss. The IMF and World Bank, as well as numerous economists and migration experts, confidently predicted that there would be a significant decline in remittances during the pandemic. This narrative was upended in 2021 by the IMF and World Bank’s own balance of payments and remittance data. which revealed a very minor slowdown in 2020 and massive differences between individual countries. Some African countries, such as Nigeria, recorded a major decline while others, like Zimbabwe, saw a significant increase.

In a scramble to make sense of the data showing there had not been a precipitous decline in remittances in 2020, the IMF and World Bank did a U-turn. In this second narrative about migrant behaviour, migrants carefully husbanded scarce resources and drew on their savings in a spirit of altruism to maintain and even increase their pre-pandemic level of remitting. In search of a resolution of the pandemic paradox of stable or increased migrant remittances and decreased migrant capacity to remit, a third narrative emerged. This emphasised the distinction between formal (recorded) remittances which are captured in official remittance data, and informal (unrecorded) remittances which are not. If there was a massive decline in informal remitting and an increase in the use of formal transfers, this would explain why formal remittances appeared to be relatively resilient.

Traces of all three narratives can be found in local versions of the impact of COVID-19 on remittances between South Africa and Zimbabwe. There were initial predictions that remittances would slump. These were quickly followed by assertions that they had in fact soared. In this paper, we set out to see if the third narrative might reconcile the differences between the first two by assessing if the increase in formal remittances during the first year of the pandemic might have been driven by a shift from informal to formal remitting, enabled by the rise and accessibility of digital remittance platforms.

Our survey data indicates that many Zimbabwean migrants in South Africa experienced severe pandemic-related economic impacts including unemployment and income loss and, as a result, were not able to sustain their pre-pandemic level of remitting. It also indicates that despite the restrictions on internal and cross-border mobility, informal remitting channels were still able to operate to a degree. The most significant finding, consistent with the third narrative, was the major shift in levels of patronage of digital RSPs and MTOs in 2020. We extrapolate this finding to estimate the flow of informal remittances between the two countries in 2019 and 2020. We conclude that there was a pandemic-related decline in total remittances and that remittances flowing through formal channels increased while informal remittances substantially declined. The formal increase was therefore not a product of increased remitting by altruistic migrants but the result of a shift of resources from informal to formal channels enabled by the rise and accessibility of digital RSPs in particular.

In many parts of the Global South, informal channels have traditionally been more important than formal remittance channels. However, the COVID-19 pandemic greatly accelerated a pre-existing trend towards greater use of digital platforms for transferring remittances. Whether COVID-19 has been a permanent boon to the digitalisation of remitting or whether migrants will revert to informal channels post-pandemic remains to be seen. The findings of this case study of the Zimbabwe–South Africa corridor now need to be tested in other remittance corridors, since there are very likely to be inter-corridor differences in COVID-19 impacts and the changing balance between informal and formal (especially digital) remittances.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors acknowledge and thank the following for their financial support: the Social Sciences and Humanities Research Council of Canada (SSHRC); the Canadian Institutes for Health Research (CIHR) and the New Frontiers in Research Fund (NFRF).