Abstract

Policymakers and tax authorities in developing countries face challenges in comprehending the determinants of tax-compliance behavior. This study employs empirical investigation to explore the factors that influence taxpayers’ voluntary and enforced tax compliance behaviors. Data were collected through a survey questionnaire distributed to 400 taxpayers using simple random sampling and analyzed using an ordered logit model. The results validate the assumptions of the slippery slope framework, showing that trust significantly impacts voluntary tax compliance and that a strong tax authority’s power contributes to more enforced tax compliance in Ethiopia. Additionally, the interaction between trust and power has a more significant effect on enforced tax compliance. This study also emphasizes the importance of improving trust in increasing tax compliance. Moreover, factors such as equity, fairness, tax knowledge, effective tax usage, and taxpayer morale contribute to tax compliance. By identifying factors that contribute to tax compliance, the findings of this research provide valuable insights for tax authorities in Ethiopia and other developing countries in devising strategies to combat tax evasion. This includes implementing a fair tax regime, enhancing the perceived value of public services financed by tax payments, increasing tax knowledge activities to help people understand the importance of paying taxes, and fortifying frameworks to minimize extravagant spending for maintaining public trust and ensuring effective and efficient use of taxpayers’ money.

Introduction

A fiscal platform is built to generate the funds required to pursue shared objectives, including social security, economic expansion, income redistribution, and internal and national security (Khasawneh et al., 2008). Tax revenue is essential for maintaining sustainability worldwide and serves as the primary source of funding for local and federal governments, especially in developing nations (Desta, 2018). To this end, many countries have introduced tax motivation packages such as self-assessment systems (SASs) to increase tax income by streamlining the tax assessment process and promoting voluntary compliance (Ayalew & Jerene, 2016).

However, noncompliance appears to be one of the primary problems in developing economies in terms of obtaining tax income (Kassa, 2021). Tax noncompliance is a taxpayer’s intentional or unintentional failure to meet his or her tax obligations (Kirchler et al., 2007). It has socioeconomic repercussions, impeding economic development and affecting the capacity of governments to enhance people’s living standards and provide budgetary resources for public spending (Bani-Khalid et al., 2022).

This unlawful practice (noncompliance) hurts both economic growth and the functioning of society and politics. In the economic domain, noncompliance entails government entities’ billions of dollars in missing tax revenues (Dularif & Rustiarini, 2022). Crivelli et al. (2016) estimate that tax evasion causes the world economy to lose approximately US$650 billion each year. According to previous research (Agusti & Rahman, 2023), although SMEs’ role in Indonesia’s economic development is highly significant (60.51%), their contribution to total tax revenue is only 0.36%. Abu Bakar et al. (2022) also reported that only 2.27 million of 14.9 million Malaysian employees paid taxes. Tax evasion is a pandemic for governments because it cannot be handled as soon as possible (Kassa, 2021). Although tax evasion is a continual and growing global challenge, sub-Saharan Africans are particularly highly influenced, and taxpayers’ failure to comply is increasing (Ayalew & Jerene, 2016; Desta, 2018).

As in many other developing countries, noncompliance poses a significant problem for Ethiopia’s income tax administration and effective tax collection (Lashetew, 2019). The Ethiopian government carried out modifications and settled on taxation administration regulations in 2016, intending to enhance tax collection, expand the scope of taxation, and create an improved tax structure, mainly to increase tax revenue to combat noncompliance. The share of income taxes in overall government revenue is persistently low and comparatively diminishing. According to World Bank (2020) development indicator reports, Ethiopia’s income tax revenue as a proportion of GDP in 2018, 2019, and 2020 was 7.525%, 6.6%, and 6.2%, respectively. The statistics mentioned above reveal a comparatively low degree of tax compliance; therefore, Ethiopia’s tax compliance/noncompliance is an important topic.

This is because identifying why taxpayers comply or do not comply with the law may assist the taxing body in creating tax rules and strategies to increase income and minimize administrative costs. This finding demonstrates the significance of the findings of the present study.

Several theories and conceptual frameworks have been employed to comprehend the variables that influence tax compliance. Economic-based theory, or “deterrence theory,” was one of the earliest models used to clarify tax noncompliance behavior and was proposed by Allingham and Sandmo (1972). Theory argues that taxpayers are dishonest and work to optimize anticipated benefits by weighing the advantages of effective tax evasion against the risk of being discovered and the potential consequences (tax audits, tax fines, and increased tax; Al-Ttaffi et al., 2021). It is called economic-based because actions tied to the costs and benefits of doing the activities are economical substances that impact tax compliance, including tax rates, public views regarding government expenditure, and penalties (Loo, 2011). Empirical studies on the usefulness of economic variables for reducing tax evasion continue to provide conflicting findings (Cahyonowati et al., 2023; Górecki & Letki, 2021). Therefore, additional research is needed to determine whether economic factors have high explanatory power for practical noncompliant tax behavior in Ethiopia.

However, several countries that apply a deterrence-based (economic) approach to reducing tax evasion fail to enhance tax compliance, and behavioral variables could provide another perspective (Cahyonowati et al., 2023; Kirchler et al., 2007). As a result, in addition to “economic” factors, “psychological” factors such as a willingness to comply, taxpayers’ attitudes toward the authorities, the tax system, the government, legitimacy, and awareness of tax regulations. In addition, individual and societal norms, the morals of economic actors, and views on equal treatment have been shown to influence tax compliance (Bani-Khalid et al., 2022; Gangl et al., 2015; Kirchler et al., 2007).

By incorporating psychological factors and economic assumptions of tax compliance, Kirchler et al. (2007) and Kirchler et al. (2008) suggested a conceptual model called the “slippery slope framework (SSF).” The “slippery slope” framework patterns the modest interaction of power and trust that can solve the social dilemma of tax noncompliance (Gangl et al., 2015). Trust in authority refers to the perception among taxpayers that government officials consistently decide on public welfare. In contrast, the term “power of authorities” relates to taxpayers’ perceptions of tax officials’ capacity to identify unlawful tax disobedience via thorough audits to uncover evasion, as well as to authorities’ authority to sanction evaders (Kastlunger et al., 2013; Mas’ud et al., 2014). The framework assumes that the trust in and power of authorities increase voluntary and enforced tax compliance, respectively (Wahl et al., 2010).

Nevertheless, several earlier studies failed to support links between power and the underlying motive for tax compliance (Faizal et al., 2017). Rather than focusing on voluntary compliance, K. Chong and Arunachalam (2018) noted that enforced tax compliance is influenced by both government and tax administrators’ trust. Because there is no agreement among the results of prior research, a more detailed explanation of the framework is needed. As a result, the empirical analysis of the “slippery slope framework’s” premise is pertinent to the present study.

Furthermore, Kirchler et al. (2007) demonstrated that compliance practices vary across nations and individuals. Thus, individuals’ tax evasion sentiments may respond differently to the slippery slope framework of the tax compliance assumption. For example, Batrancea et al. (2022) suggested that students are more inclined to engage in tax evasion. However, the effect may be offset by boosting authorities’ power, while trust within authority has a more significant impact on tax compliance than enforcement. Even so, no empirical study on the slippery slope framework of the tax compliance assumption for business rental taxpayers’ tax compliance behavior is available. This study aims to fill this knowledge gap by extending the practical implications and relevance of the slippery slope framework tax compliance assumptions to new domains of individual income tax compliance behavior.

Finally, this study seeks to contribute to the tax compliance debate by highlighting the slippery slope as a predictor of tax compliance in a developing nation’s setting by utilizing the economic, psychological, and social forces that drive taxpayers to participate in tax noncompliance or compliance decisions.

Accordingly, this study aimed to investigate the compliance practices of business rental income taxpayers in Ethiopia’s Gamo zone and to answer the following research questions:

What is the relationship between economic factors and taxpayer compliance behavior?

What is the relationship between sociopsychological factors and taxpayer compliance behavior?

How do power and trust affect tax compliance behavior in the Ethiopian context?

Literature Review and Hypothesis Development

Theoretical Background

Tax compliance is an issue in which scholars worldwide are interested. The literature on tax compliance is rather substantial in finding a wide range of factors that impact tax compliance behavior (Kostritsa & Sittler, 2017). There are several definitions of tax compliance. According to Alm (1991), this is the correct reporting of income and spending per the existing tax legislation. As a result, tax compliance is established when taxpayers promptly submit the payment received and the costs paid so that the income tax settlement amount is correct. Tax evasion manifests in two ways: underdeclaration of revenue (e.g., sales suppression) and overdeclaration of costs (e.g., fraudulent invoices or inclusion of ineligible personal expenses) (Inasius, 2019; Rodrigues et al., 2019).

In the subject of taxation or tax evasion research, there are two primary themes wherein regulators maintain taxpayer compliance. The first focused on economic philosophy (deterrence theory), which assumes that taxpayers are reasonable and try to enhance their anticipated value by steering their tactical actions accordingly. Taxpayers will prefer to dodge if the likelihood of discovery or audit is not too great and the consequences are not too harsh (Rodrigues et al., 2019). The taxpayer is viewed as a self-serving calculator of monetary benefits and losses. According to Kirchler et al. (2007), taxpayers start behaving just as they are playing games, with sources of uncertainty causing them to experience the following issues: (a) inspecting the legislation while being certain about the amount of income prepared to sacrifice; (b) violating the law and gaining, if viable, a gain; or (c) violating the law and enduring severe failure due to the threat of punishment (da Silva et al., 2019).

Hence, economic deterrence models assume that people rationally embrace the primary goal of taxpayer control through coercive means, particularly those that focus on identifying and punishing lawbreakers. When these techniques are used successfully, enforcing taxpayer compliance is achieved using the government’s coercive power, or so-called enforced compliance (da Silva et al., 2019; Kirchler et al., 2007). Although deterrence or economics of crime methodological tactics have some use in managing noncompliance by focusing primarily on penalties and fear of being detected, they have a significant flaw. These recommendations for harsher punishment are frequently impractical or unprofitable and may not be able to fully explain the existing levels of compliance in emerging nations (Nkundabanyanga et al., 2017). The constant efforts made by these authorities to find and punish tax evaders were the foundation of the “crime paradigm”, which in turn created a “cops and robbers” environment (Kirchler et al., 2007). Furthermore, recent studies have confirmed that noneconomic, social, and psychological factors could influence taxpayer compliance (Musimenta et al., 2017).

The second approach is the psychological approach, which views taxpayers as trustworthy individuals inclined to follow rules if they believe that the authorities act justly and responsibly. This is comparable to voluntary tax compliance (Kogler et al., 2013; Kostritsa & Sittler, 2017). According to Feld and Frey (2007), there is a real contractual connection between governments and citizens, wherein one side owes other public services in exchange for a portion of their resources. This is the “service paradigm,” wherein authorities encourage cooperation and build trust with the public, thereby obtaining voluntary compliance from taxpayers. The “service paradigm,” therefore, strengthens voluntary compliance. According to the behavioral view, people may not always act rationally and selfishly and care about their interests. The behavior of taxpayers is nevertheless influenced by a wide range of sociological and psychological elements, particularly those based on morality, social norms, reciprocity, tax ethics, patriotism, tax knowledge, perceptions of equity and fairness, and referral groups (Inasius, 2018; Kirchler et al., 2008; Nkundabanyanga et al., 2017).

Slippery Slope Framework

Previous deterrent tax compliance frameworks such as those of Allingham and Sandmo (1972) fail to explain why taxpayers pay income tax without regulatory action. As a result, psychological tax contract theory was developed to explain why taxpayers still pay taxes without deterrence (Feld & Frey, 2007). The study of taxpayer behavior has evolved from traditional neoclassical models limited to economic factors to more dynamic and multidisciplinary models that consider psychological and social aspects. Recent models, such as the slippery slope framework (SSF), have adopted an interdisciplinary approach to better understand tax compliance. According to Kirchler (2007) and Kirchler et al. (2008), the level of tax compliance is determined by the interaction between the power of tax authorities and trust in tax authorities, considering relevant economic factors.

The relationship between the “client and the service provider” is established through complementarities, as the tax authorities and taxpayers cooperate and have faith in one another. Taxing authorities rely on citizens to pay taxes truthfully. People who owe taxes do so voluntarily because they believe that tax authorities treat them respectfully and courteously (Kirchler et al., 2008). According to the slippery slope paradigm, tax officials use two variables, power and trust, to win taxpayer cooperation. Power focuses on the ability of tax administration to influence taxpayer behavior and promote tax compliance by employing deterrent strategies such as audits and penalties.

Additionally, trust underscores the importance of maintaining a respectful and thoughtful relationship between taxpayers and officials (Faizal et al., 2017). According to the slippery slope framework, there will be low levels of compliance because of the low levels of confidence and weak power in the taxpayer. Due to audit-based enforcement, the increased risk of detection and fines, and the greater power of tax authorities with low levels of trust, tax compliance continues to increase. When confidence in tax authorities is at its highest, with little power, trust encourages voluntary tax compliance (Kirchler et al., 2008).

As a result, when the trust and power of tax authorities remain high, the degree of compliance is also high (Faizal et al., 2017). Wahl et al. (2010), Kastlunger et al. (2013), Mas’ud et al. (2014), Kogler et al. (2013), K. R. Chong et al. (2019), and Youde and Lim (2019) verify that the likelihood of voluntary tax compliance is greater when authorities can be trusted. By combining the framework’s postulates with conceptual analysis, it was projected that power could significantly affect how strictly tax compliance is enforced.

Trust and power impact the magnitude of compliance with taxes and are also connected in the sense that changing one parameter could impact the other (Kirchler et al., 2007; Kirchler et al., 2008). A combination of power and trust indicators may be more effective than each measure in encouraging tax compliance. This might be because once authority and credibility are coupled, it is viewed as genuine legitimacy that inspires compliance (Hofmann et al., 2014). The results of Kogler et al. (2013) and Wahl et al. (2010) imply that power and trust are not standalone predictors of tax compliance; rather, the relationship between the two is relevant.

The application of strong power, combined with an insufficient level of trust on the authorities’ side, could be considered coercive and seen as untrustworthy, thus making it doubtful that tax compliance can be achieved because of the consequences of enforcement. Taxpayers in such countries may perceive governments as autocratic and dictatorial, imposing inappropriate measurements, intimidating taxpayers, or instilling fear (Hofmann et al., 2014). A high level of credibility among authorities and a lack of authority may result in well-intentioned tax compliance. Nevertheless, authorities are unable to ensure tax compliance by fellow citizens and, hence, cannot combat free riders. Dishonest taxpayers who are not prosecuted may erode a synergistic atmosphere, and honest taxpayers may begin to distrust authorities (Wahl et al., 2010). Substantial power combined with considerable trustworthiness is probably viewed as legitimate, resulting in the highest level of tax compliance by using power to punish tax criminals while acknowledging those who pay taxes deserving positive reinforcement (Hofmann et al., 2014; Kogler et al., 2013; Wahl et al., 2010). Consequently, the combined influence of power and trust is of great theoretical and practical importance.

Despite these intriguing results, which verify the specific and interactive impacts of trust in authority and the power of authority in affecting tax compliance, research from the perspective of the Ethiopian tax environment is sparse. Therefore, we propose the following hypothesis:

H1: Increased taxpayer trust in the government leads to enhanced tax compliance.

H2: A high perception of tax authorities’power increases enforced tax compliance.

H3: The interaction between authority power and trust in authorities substantially affects tax compliance.

Psychological Factors and Tax Compliance

Positive rewards may improve taxpayers’ likelihood of voluntarily cooperating without direct force. It follows that a taxpayer’s conduct is influenced by his or her contentment or dissatisfaction with the conditions of commerce with the government (Ali et al., 2014). For example, tax morale is affected by the perceived use of collected funds and increases as taxpayers perceive government efficiency. In contrast, if people believe that the government is overspending excessively, they may feel misled and want to avoid paying taxes (Kirchler et al., 2008). As a result, tax compliance is likely to increase if the government wisely spends national money, for example, on essential services such as public transit and education.

In comparison, if people believe that the government is overspending on anything they think is needless, they will feel misled and will want to avoid paying taxes. Ayalew and Jerene (2016) revealed a positive and substantial association between taxpayer perceptions of government expenditure and tax compliance. At the same time, Inasius (2018) findings show a negligible link between perceptions of government expenditure and tax compliance. This discussion resulted in the following hypothesis:

H4: There is a significant connection between taxpayers’ tax usage sentiment and taxpayer compliance.

However, inadequate knowledge was negatively associated with trust. Youde and Lim (2019) found that taxpayer knowledge is positively related to taxpayer tax compliance. In contrast, Taing and Chang (2020) found no statistically significant relationship between tax awareness and compliance intention. Thus, we propose the following hypotheses:

H5: Tax knowledge has a positive effect on tax compliance.

H6: There is a significant relationship between tax fairness and tax compliance.

Similarly, Taing and Chang (2020) demonstrated that tax morale significantly influences taxpayer compliance behavioral intentions. On the other hand, internal self-tax morale does not accurately predict evasive decisions; hence, the study concludes that individual self-reported tax morale cannot anticipate genuine evasion preferences (Guerra & Harrington, 2018). Thus, we propose the following hypothesis:

H7: Tax morale has a significant impact on taxpayer tax compliance.

Previous research by Inasius (2018) established the significance of referent groups and showed that referral groups substantially influence tax compliance or noncompliance. Neighbors, self-employed persons, and relatives can occasionally affect tax evasion or noncompliance behaviors, yet investigations do not specify the magnitude of these impacts (Allingham & Sandmo, 1972). If a taxpayer is linked to compliance with tax payments, the likelihood of evading taxes decreases. However, if a taxpayer refers to a noncompliant payer, they may also misbehave themselves as tax-paying citizens (Ayalew & Jerene, 2016). Consequently, the effect of referent groups appears to be crucial in making tax compliance decisions, leading to the following hypothesis:

H8: There is a significant association between referent group influence and tax compliance.

Youde and Lim (2019) suggested that tax education provides taxpayers with additional information so that they will have a greater understanding and, as a result, abide by tax requirements. In contrast, education and obedience may have adverse effects. It has also been argued that general education, which is unrelated to the taxation system, significantly influences tax compliance behavior more than taxpayers’ tax awareness. Richardson (2008) revealed a negative link between education and compliance. Consequently, education levels are becoming increasingly crucial in enhancing tax compliance across jurisdictions, and the following hypothesis is formulated:

H9: A significant association exists between education and tax compliance.

Materials and Methods

Data and Collection Techniques

This study follows a quantitative approach involving collecting primary data through closed-ended questions using a survey method to obtain information from rental income taxpayers. Given the target population’s limited access to or familiarity with digital technologies, this study opted to use a paper-based survey questionnaire. The questionnaire consisted of items rated on a five-point Likert scale ranging from 1 (strongly disagree) to 5 (strongly agree). Each item in the questionnaire has a different value: 1 = strongly disagree, 2 = disagree, 3 = neutral, 4 = agree, and 5 = strongly agree.

The researchers personally distributed the questionnaire to the business rental income taxpayers. The process involved researchers approaching the responders, introducing themselves, and request to filling out the questionnaires. To encourage participation, the participants were immediately informed of the study’s objectives. This included researchers providing a cover letter outlining the purposes of the study. Second, no personal information was collected to ensure that the requested information was kept confidential. These instructions were included in the questionnaire. As the respondents accepted the invitation, the researcher explained the aim of the survey and provided instructions on how to complete it, ensuring that the respondents fully understood the task before allowing them to proceed. However, during the pilot survey, some participants were hesitant to complete and return the survey in a single sitting position. To reduce the number of incomplete responses, the researchers allowed the respondents to complete the questionnaire at their convenience and then returned it to us. This was done to provide the responders with the preferred option. To promote a higher response rate and to make the survey process more enjoyable and less difficult for participants, the researchers decided to allowed participants to complete the survey at their own ease and convenience. The researchers hoped to lower the possible barriers to cooperation and improve the overall quality of the data collected by offering this option.

The application of this technique can also serve to mitigate the influence of acquiescence bias, which manifests when individuals answer questions irrespective of their actual sentiments. By providing a more impersonal and conducive environment for participants to respond, the study elicited more truthful responses. Furthermore, to diminish the likelihood of social desirability bias, participants were informed that participation was voluntary and that their feedback would be kept anonymous, only being utilized for the purposes of this particular study. Four personnel were trained to address any potential issues that may arise during the distribution process, such as allaying any fears or queries the respondents may have, ensuring that the data collected were accurate and complete, and ensuring that all necessary information was obtained from those who had not yet responded. By implementing these strategies, researchers have successfully attained a higher response rate.

Prior to the commencement of the main study, the original questionnaire was forwarded to three academicians and two tax experts employed by tax authorities for revision. This was followed by a pilot study involving 20 respondents completing the questionnaire. Misunderstandings, ambiguities, typing errors, and other issues were detected and rectified with the phrasing of certain sentences in the survey. Although the questionnaire was originally composed of English, its final version was translated into English by an expert proficient in both languages, as well as in relevant academic areas from the departments of Amharic and literature, and subsequently translated back into English by a different expert to verify its accuracy. The data collection for this study commenced at the beginning of January and was finalized by the start of June 2022. Of the 400 distributed questionnaires, 395 were returned, of which seven were incomplete or did not meet the conditions, and five had missing data. The final sample included 388 individuals, 71% of whom were male and 29% were female. All participants who completed the questionnaire answered all questions. There were 388 usable questionnaires, for a usable response rate of 97%.

Sampling Technique and Sample Size

The study’s target population is business rental income taxpayers enrolled with the Ethiopia Revenue and Customs Authority (Gamo Zone Branch). A taxpayer’s chargeable rental income for a tax year is the total income obtained from renting a building or property for the year minus the respective expenses. The owner of a building may occasionally enable a lessee to sublease the building. As a result, a subtaxable lessor’s rental income is the difference between the total rental revenue collected by the sublessor during the year and the total rental income given to the building’s lessor (Ethiopia Federal Income Tax Proclamation, 2016).

This study’s sample of taxpayers was chosen using simple random sampling approaches. This strategy is applied because the target population has an equal chance of being included or eliminated from the total sample. The use of such sampling methods is supported by the fact that they aid in selecting real representatives and can represent a wide range of dispersion in data collection. The woredas were chosen based on their population size. There are 1,047 business rental income taxpayers in the Gamo zone. The sample size was determined using the Yamane (1967) formula.

According to Yamane (1967): n = N/[1 + (Ne2)]

where n = the sample size

N = population

e = is the error limit (0.05 based on the 95% confidence level)

However, for prudence, 110 samples were added. Hence, the sample size for this study was

Measurement Validity and Reliability

Appropriate statistical approaches were used to confirm the validity and reliability of the measurements. The first was a validation test to determine the uniformity of each component on the study’s Likert-scale questionnaires, which might corroborate the identified characteristics. The Kaiser–Meyer–Olkin test was employed to assess sample adequacy to demonstrate the dataset’s validity. The Kaiser–Meyer–Olkin sample test yields a score of 0.618, which is greater than the conventional value of 0.6 (Kaiser, 1974). Subsequently, principal component analysis was utilized to assess the questionnaire’s diverging authenticity and to investigate the significance of all 32 underlying questions for tax compliance predictors. Consequently, among the 32 elements, nine factors (components) with eigenvalues greater than one were identified.

According to the findings, nine retrieved components explained 58% of the total variation. These parameters consistently reflected the nine explanatory variables in the study’s established tax compliance framework. Cronbach’s alpha was used after the validity test to evaluate the reliability of each Likert scale question that could represent the nine identified parameters. Finally, the component scores obtained from the principal component analysis were subjected to ordered logistic regression to test the hypotheses.

Variable Description

The literature was used to identify both the dependent and independent variables. The dependent variable, the subject of this study, is voluntary and enforced tax compliance.

The slippery slope framework proposes that the relationship between tax authorities and taxpayers can vary from adversarial to cooperative (Kirchler et al., 2008). Compliance with taxes is dependent on whether citizens are compelled to comply or willingly cooperate, which is influenced by the authorities’ power and the taxpayers’ trust (Kastlunger et al., 2013). A cooperative climate is defined by the notion that tax authorities serve the community and strive to bridge the social distance between them. In this climate, taxes paid by the community are perceived as a form of economic value that contributes to the state being out of obligation. Consequently, timely and accurate payment of taxes without any government promotion is referred to as voluntary tax compliance (Kirchler et al., 2008).

In contrast, an adversarial climate emerges when a substantial social distance between tax authorities and taxpayers stems from divergent perceptions. In such a situation, the authorities’ power is exercised through relentless tax examinations, audits, and charges, aiming to detect and penalize noncompliant taxpayers. This compliance form is commonly known as enforced compliance (Kirchler et al., 2008).

Because tax compliance is sensitive, many taxpayers may disclose their compliance intention dishonestly. We employed an oblique inquiry as a latent variable to assess taxpayers’ compliance attitudes to eliminate this distortion. Participants were questioned about their perceptions of other people’s compliance behavior, which was subsequently used to determine their own tax compliance intentions. The survey questions were adapted from previous studies, and measures for factors such as trust in government, the power of tax authorities and voluntary and enforced tax compliance were adopted from Wahl et al. (2010), Kastlunger et al. (2013), and Gangl et al. (2015).

Voluntary tax compliance was assessed with the following four items: “Usually, I pay my taxes willingly”, “When I pay taxes, I do so because the tax authority will probably reciprocate my cooperation,” and “I accept the responsibility of paying my share of taxes,”“Paying tax is a responsibility that all citizens should willingly accept.” Enforced compliance was assessed with answers to four items (“The tax office is more interested in catching you for doing the wrong thing than helping you do the right thing,”“When I pay taxes, I do so because a great many tax audits are carried out,”“When I pay taxes, I do so because I feel forced to pay my taxes,” Once the tax office has you branded as noncompliant taxpayer, they will never change their mind.”

The independent factors include trust in tax authority, tax authority power, tax knowledge, tax morale, the perception of fairness and equity, tax utilization (spending), referent groups, and education. The dependent and independent variables were measured using a 5-point Likert scale, with responses ranging from 1 to 5, with one indicating strongly disagree and five indicating strongly agree. The measures for variables such as tax morale and tax fairness were adopted from (Youde & Lim, 2019); tax knowledge was adopted from (Taing & Chang, 2020); and government spending and referent groups were adopted from (Desta, 2018).

Data Analysis and Model Specifications

The collected data were processed using STATA. The data were analyzed by utilizing descriptive and inferential statistics to study variables impacting the compliance behaviors of taxpayers.

The principal component factor extraction outcome suggested that nine factors with an eigenvalue higher than one were retained. The eigenvalues measure the variances of the principal components (which are the questions that explain the variable). The component score can be obtained by the weighted sum of standardized variables (mean zero variance of one). The factor scores obtained from the factor loadings were incorporated into the regression. Based on this score, taxpayers’ compliance levels are divided into low, medium, and high degrees. Since the latent variables are hierarchically ordered—low compliance, medium compliance, and high compliance—the ordered logit model was suitable for evaluating the tax compliance perspective in this study. The application of the ordered logit model was first verified; therefore, the “parallel line” assumption was satisfied. A set of Wald’s tests on all predictors, wherein minor test statistics suggested that the model met the “parallel line” premise, supported the model’s overall fit.

Defining y* as a latent variable spanning from −∞ to ∞, the structural model is Y*= XiB + ei. where Y* is a tax compliance metric representing the tendency toward agreement. Xi indicates all the independent factors that are considered to influence tax compliance measures, while ei is an error term. The continuous latent variable Y* has several threshold (cut) points depending on the number of ordinal categories the dependent variable possesses. There is a J − 1 number of thresholds (cut points) for the J-number categories. The dependent variable of this research was assessed by five ordinal categories (π1 = strongly disagree, π2 = disagree, π3 = neutral, π4 = agree, π5 = strongly agree), and there were four cut-off points.

Y* can be indicated as follows:

The final ordered logistic regression model using cumulative probabilities is written in the following manner:

Results and Discussion

Before executing the ordered logistic regression, the study conducted variance inflation factor (VIF) testing to assess the possibility of multicollinearity. The highest VIF was 1.47, indicating that multicollinearity was not a problem in this model (Table 1). The data were checked for normality using the Smirnov and Shapiro–Wilk tests; if the distributions as a whole deviated from a corresponding normal distribution, they were considered normally distributed. According to the likelihood ratio χ2 test, this model was statistically significant at the .0001 level.

Model Fit’s and Diagnostic Test.

Source. Authors estimation (2022).

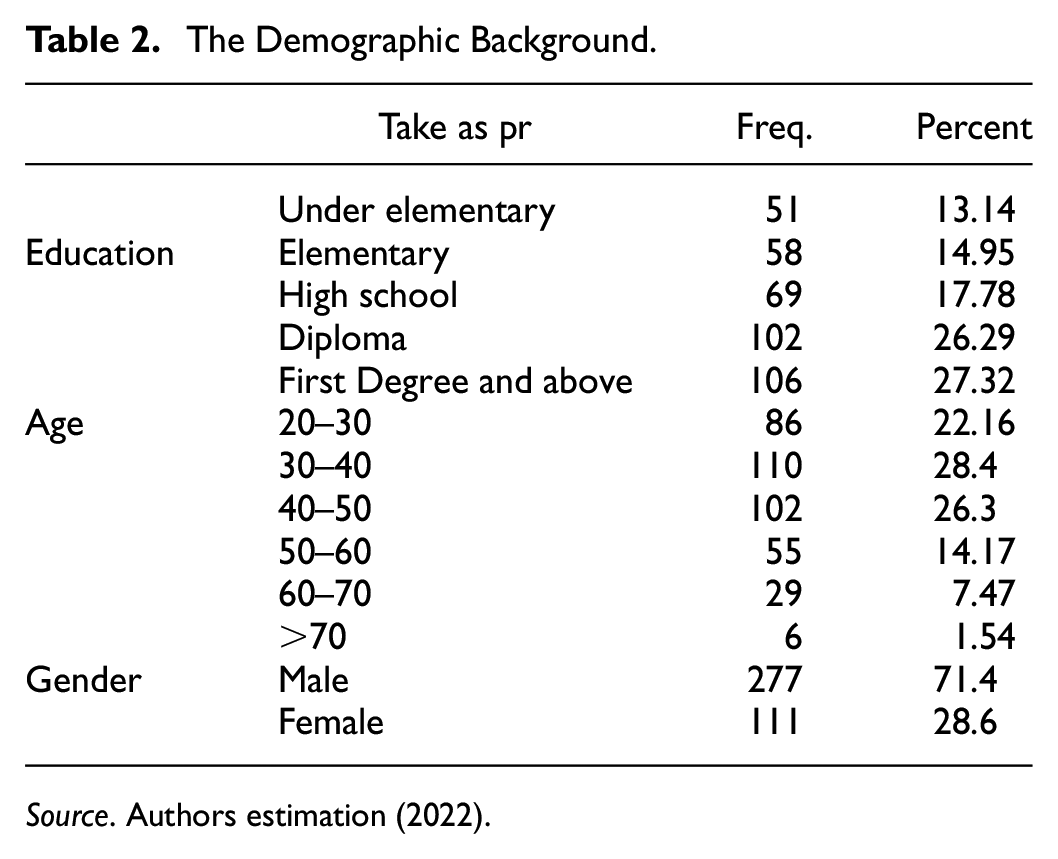

As Table 2 demonstrates, approximately 29% of the respondents in the population were female, while men comprised the majority (71%). Owing to their sociological, cultural, economic, and psychological characteristics, men seem to be more engaged in the business community than women. The average age of the taxpayers in the sample was approximately 40 years. Most of the respondents were in the 30 to 50 years age range. Overall, most of the respondents in this sample had acquired considerable formal education, meaning that most taxpayers in this sample had received some knowledge (Table 2).

The Demographic Background.

Source. Authors estimation (2022).

Tables 3 and 4 present the results of the ordered logit regression with marginal effects. The findings suggest that the seven factors were statistically significant at various degrees of confidence. These factors include tax knowledge, trust in the tax authority, the power of the tax authority, tax morale, tax usage (spending), attitudes toward fairness and equity, and the interaction effect of trust and power. These findings also demonstrate positive or negative connections between these factors and the three levels of tax compliance among business-rental taxpayers.

Ordered Logistic Regression Result for Voluntary Tax Compliance With Marginal Effects.

Source. Authors estimation (2022).

Note. Standard errors in parentheses.

p < .01. **p < .05. *p<0.1.

Ordered Logistic Regression Result for Enforced Tax Compliance With Marginal Effects.

Source. Authors estimation (2022).

Note. Standard errors in parentheses.

p < .01. **p < .05. *p<0.1.

The empirical estimates indicate that trust in authority has a negative relationship with low-income taxes and medium tax compliance but a positive relationship with high tax compliance. If the trust index increases by one unit, the probability of high tax compliance increases by 32%. This positive result could be attributed to a tendency to increase engagement with taxpayers, contentment with the provision of public services, or the degree of enforcement of rules, which establish more faith in the government. Hence, strengthening taxpayer confidence in tax authorities is an essential and viable approach for preventing tax evasion and increasing tax compliance. This conclusion conforms with the “service paradigm” and the results of K. Chong and Arunachalam (2018) and (Lisi, 2019).

For voluntary compliance, perceived power and the interaction of trust and power are substantially adversely connected to greater voluntary tax compliance but positively related to lower and medium voluntary tax compliance. If the power and interaction of trust and the power index increase by one unit, the probability of high tax compliance decreases by 5% and 9%, respectively. This finding suggests that voluntary compliance is optimal when the authority is trusted and less powerful, showing that when a person trusts the tax authority, the enforcement strength of the administration will decrease (Wahl et al., 2010). Moreover, the more users thought they were compelled to pay their dues, the more they tried to evade. When taxpayers feel monitored and punished, they may pay their taxes; however, they may reap the benefits of the situation while sensing an opportunity to escape the law (Kastlunger et al., 2013).

For enforced tax compliance, univariate trust does not significantly affect enforced compliance; when the power of authority increases by one unit, the probability of high enforced tax compliance increases by 6%. These results suggest that in the presence of tremendous authority, people comply with tax duties as a reaction to this situation; in other words, they pay taxes not willingly but forcefully. The findings also demonstrate a tendency for trust and power to interact, indicating that enforced tax compliance is strongest when authorities are credible and authoritative. This indicates that when a trustworthy setting exists from the perspective of the increased power of authorities, taxpayers influence their behaviors, prompting people to obey the law forcefully. Moreover, suppose that tax offices prescribe tax affairs (including collecting taxes, tax filing appraisals, tax rebates, and fines) effectively and efficiently. In this case, taxpayers strive to adhere to countermeasures and tax codes, resulting in less obfuscation (K. Chong & Arunachalam, 2018).

The findings prove the constraint of the classical economic conceptual framework (deterrence hypothesis) by presuming that in a collaborative environment and with trust in authorities, taxpayers will recognize the voluntary basis instead of aiming to maximize usefulness. Hence, taxpayers are driven by motives other than the need for economic gain (da Silva et al., 2019). These findings are consistent with those of previous studies (e.g., da Silva et al., 2019; Kastlunger et al., 2013; Mas’ud et al., 2019; Wahl et al., 2010). Consequently, H1 (strong taxpayer trust in the government contributes to more voluntary tax compliance), H2 (tax authorities’ power results in increased enforcement of tax compliance), and H3 (power and trust interactively affect tax compliance) are supported and verified.

These findings complement the literature by empirically validating the premises of the slippery slope framework, particularly the likelihood that a decrease in power and trust considerably affects the level of tax compliance. Specifically, the “magnitudes” of the association between the two dimensions of tax authority (trust and power) and taxpayer compliance behavior demonstrate that a “slippery slope” scenario occurs primarily with regard to trust. This signifies that a one-unit improvement in the scale of trust in tax authorities would minimize the odds of low and medium compliance by 7% and 24%, respectively. This approach would improve the possibility of a high-compliance perspective by 32%. Conversely, a one-unit increase in the power of authority index is correlated with a decrement of the chance of low and medium compliance by 0.6% and 5.4%, respectively; it would enhance high compliance attitudes by approximately 6% (see Tables 3 and 4). Hence, this study concludes that only improving trust can substantially increase tax compliance.

Furthermore, the results demonstrate that both the “service paradigm” and the “crime paradigm” offer instruments that induce increased tax compliance, allowing the government to control them more efficiently.

Addressing the association between tax usage (spending) and taxpayer compliance, the observed manner of government spending also reveals that it significantly influences tax compliance behavior. If tax usage (spending) increases by one unit, the probabilities of high voluntary and enforced tax compliance increase by 10% and 13%, respectively. A positive coefficient implies that when community members are pleased with public infrastructure, the administration effectively allocates collected taxes, and perhaps the degree of voluntary tax compliance improves. This is because people, especially those who pay large sums of taxes, are susceptible to public expenditure trends. If taxpayers believe that the state spends too much on things they deem superfluous or not compulsory, they could feel deceived and seek to cheat taxes (Alasfour et al., 2016; Inasius, 2018). Therefore, authorities should responsibly expend taxpayers’ funds, ensuring honesty and responsibility for public funds. This is because how administrative spending is conducted creates varied degrees of compliance that impact public trust. Otherwise, taxpayers might rationalize their tax fraud behaviors by claiming that the government spends tax funds and allocates them imprudently, an assertion that could lower compliance in the long term. This conclusion is in accordance with the findings of Ayalew and Jerene (2016) and Shiferaw and Tesfaye (2020). In comparison, this finding contradicts the findings of Inasius (2018), who stated that government spending may not boost tax compliance. Thus, Hypothesis 4 is accepted.

The estimated results suggest that increasing tax knowledge is favorably linked to high compliance behaviors but negatively correlated with low and medium voluntary tax compliance behaviors. In terms of marginal impacts, a one-unit improvement in tax knowledge decreases the probability of low and medium compliance by 3% and 9%, respectively, but increases the propensity for high voluntary compliance by 12%. This explains why knowledge about tax concerns becomes more available, thus increasing tax compliance behavior attitudes. More significantly, improving the understanding of tax concerns might minimize errors in filing and declaring (Youde & Lim, 2019), and the possibility of compliance at a greater tax level is envisaged. Therefore, boosting taxpayer awareness via simple tax legislation, mentoring, and expanding taxpayer assistance enhances trust in authorities (Kirchler et al., 2008). This result parallels the findings of Assfaw and Sebhat (2019) and Shiferaw and Tesfaye (2020), who indicate that good tax knowledge promotes voluntary tax compliance. However, this finding contradicts those of Adu and Amponsah (2020) and Inasius (2018), who stated that tax knowledge does not influence tax compliance. Therefore, Hypothesis 5 is validated by the favorable connection between tax knowledge and compliance.

H6 is accepted, as the findings in Tables 3 and 4 demonstrate a significant negative relationship between tax fairness and low tax compliance and a positive relationship between tax fairness and high compliance. This finding indicates that taxpayers who regard the tax regime as unjust are more likely to undermine their enthusiasm and tax cooperation. This conclusion aligns with equity theory: taxpayers become less (better) compliant when they are sufferers (recipients) of tax unfairness (Allingham & Sandmo, 1972). Tax fairness means that individuals with a comparable capacity to pay taxes have had to pay similar amounts; taxpayers with a higher potential have to pay higher amounts, and those with a lower potential have to pay lower amounts. In many nations, the most vital element is whether residents are treated according to their ability to pay (Alasfour et al., 2016). If a community believes that the nation’s tax system is fair and that people are paid based on their capacity, the level of compliance will increase. Similar findings were reported by Inasius (2018).

The results suggest that tax morale significantly influences voluntary tax compliance at the 1% level of significance. If the tax morale index increases by one unit, the probability of high tax compliance increases by 26%. In contrast, the possibility of low and medium compliance decreased by 6% and 19%, respectively. This signifies that when taxpayers’ attitudes toward taxes are constructively improved, their likelihood of being at a higher tax compliance level will increase. However, the link between tax morale and enforced tax compliance is not substantial. This shows that tax morale is more effective at increasing voluntary tax compliance than at increasing enforced tax compliance (Lisi, 2019). Taxpayers’ compliance is not considerably impacted by their amoral conduct but by other variables, such as power and trust. Tax authorities should continue to carry out enforcement processes, irrespective of whether taxpayers are morally compelled. Citizens with strong tax morale may willingly cooperate instead of forcibly comply, whereas low tax morale could result in nonvoluntary compliance. Hence, the tax office could improve taxpayers’ tax morale on various accounts by decreasing moral and adverse selection hazards, with the assistance of wider information sharing regarding budget transparency, responsible decision-making procedures, spending, and financial transaction details. Similar findings have been reported by K. Chong and Arunachalam (2018) and Alasfour et al. (2016). Therefore, Hypothesis 7 is accepted.

Hypothesis 8 postulates a strong association between referent groups and tax compliance. However, the findings of the logistic regression analysis revealed no significant associations between the referent groups and tax compliance. Thus, H8 was not supported. Finally, concerning the demographic parameters, the estimates demonstrate a negative association between education and tax compliance, although they are statistically insignificant. This finding confirms that although people with higher educational levels are more likely to have contributed positively to the comprehension of taxation, knowledgeable taxpayers could be conscious of noncompliance potentials and administration mishaps in delivering public infrastructure (Adu & Amponsah, 2020; Alasfour et al., 2016; Inasius, 2019). This is because citizens may also scrutinize how the state functions and uses its tax funds.

Moreover, the prevalent notion is that awareness of taxes grows with the duration of education, apart from educational content. However, many individuals with less formal schooling have a greater understanding of taxation than do those with higher academic attainment. Such a criterion does not yield a fully satisfying response to the question of whether there is a link between education and attitudes toward taxes (Alasfour et al., 2016). Therefore, H9 was not accepted.

Conclusion and Policy Implications

As tax contributions allow the government to fund social programs by providing better essential services, suitable measures for boosting tax collection and compliance should be addressed (Wahl et al., 2010). The attitudes and behaviors of taxpayers should be understood to promote tax compliance. By considering the slippery slope framework and other cognitive components, this study empirically provides seven significant, influential tax compliance behavior factors: tax knowledge, perspective of tax usage, sense of equity and fairness, tax morale, trust in tax authority, power of tax authority, and the interaction term of trust and power. These findings, therefore, provide significance for both academia and policy implementation by corroborating the use of the slippery slope framework and psychological elements to understand voluntary and enforced tax compliance behavior in developing nations.

The empirical findings generally confirm the slippery slope framework assumptions that trust leads to greater voluntary tax compliance and that a strong sense of power from tax authorities contributes to more enforced tax compliance, even in the Ethiopian context. Notably, the positive association between trust in tax authorities and voluntary tax compliance validates the theoretical assumptions of the service paradigm and the empirical findings on tax compliance (Inasius, 2018; Kogler et al., 2013; Taing & Chang, 2020; Wahl et al., 2010). Furthermore, a strong impression of the authorities’ power significantly influences enforced tax compliance, which verifies the crime paradigm.

The results indicate that properly distributing tax revenue promotes tax compliance by boosting general confidence in the government and tax morale in the context of good governance in developing nations. The research suggests that equity and fairness have a crucial influence on taxpayers’ tax compliance, reinforcing equity theory. Increasing tax knowledge is significantly related to high compliance but is adversely linked with low and medium compliance, supporting theoretical assumptions and earlier empirical findings (Inasius, 2018; Youde & Lim, 2019). Moreover, the outcomes of this research appear to indicate that enhancing taxpayer morale could increase taxpayer compliance. Therefore, tax authorities should develop enhanced policy instruments to promote taxpayer attitudes pertaining to the requirement to pay taxes and the repercussions of noncompliance to positively mold their views. This may be done by employing appropriate communication programs such as conferences, panel discussions, and press awareness to educate people on their civic obligations to the country through tax payments.

The results also suggest that referral groups and taxpayer education do not substantially influence tax compliance, showing that these parameters are not strong predictors of tax compliance in a developing country. In practice, the empirical results of this research may be relevant to tax authorities in Ethiopia and other regimes seeking to understand taxpayers’ tax compliance levels and devise strategies to combat tax evasion. First, tax authorities should emphasize the creation of trust to encourage voluntary compliance. This means that a policy may generate a positive synergistic climate between taxpayers and administrations through respectful and trustworthy connections. This may be achieved using policies that encourage a feeling of justice based on practical and less expensive trust-building initiatives. Tax authorities should seek to promote open and equitable tax administration. Enforced tax compliance is highest when authorities are trustworthy and powerful. Therefore, committed taxpayers must be encouraged and acknowledged by the government, while tax evaders should be pursued with full rigor of the law. Finally, taxpayers are susceptible to the course of government expenditure; therefore, tax authorities and the government should also put more effort into the redistribution of the collection of taxes with proper care. This might be achieved by spending tax money fairly, economically, productively, and lawfully. This might provide insights into better policy tools and administration tactics to boost taxpayer compliance.

Addressing tax concerns, especially in developing countries, poses significant challenges owing to insufficient comprehension and administrative inadequacies in implementing tax regulations. Consequently, this research is fundamental, as numerous developing countries confront a similar dilemma: how to “produce” as much income tax revenue as possible. Typically, the results indicate that psychological factors and the slippery slope framework play crucial roles in predicting poor and moderate compliance. Furthermore, this study provides insights for other lower- and middle-income developing countries that focus on safeguarding tax revenue and deterring tax evasion. Despite the valuable contributions of this study, its findings are not without limitations. First, it neglects various independent factors, such as financial constraints and political stability, which might significantly influence tax compliance. Second, the sample comprises only business rental income taxpayers and excludes household rental income taxpayers. Future studies could incorporate additional variables and respondent categories to obtain more comprehensive and valuable findings.

Footnotes

Acknowledgements

The authors acknowledge the financial support from Arba Minch University.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Directorate of Research, Arba Minch University, Ethiopia.

Data Availability Statement

The complete data set of the responses that support this study’s findings are available from the corresponding author upon reasonable request.