Abstract

Purpose:

The study’s objective focuses on investigating the involvement of Personal Intelligent Assistants (PIAs) in the Knowledge Management Process (KMP) in Investment Banking Companies leading to Industrial Revolution 5.0 leading to effective Organizational Knowledge Management.

Design/Methodology:

A Self-administered Survey Questionnaire was circulated to 695 employees of Investment Banking Companies operating in Bangalore, Mumbai, Delhi, Hyderabad, Chennai, and Pune using the Cluster Sampling method. The Covariance-based Structural Equation Modelling (CB-SEM) and Gradient Boosting Regression technique of Machine Learning were used to validate the hypothesis through JASP V.18 Software. Knowledge Creation, Knowledge Sharing, Knowledge Retrieval, Knowledge Application, and Organizational Knowledge Management are the crucial constructs considered in the study.

Findings:

The results revealed that Knowledge Application is the most influencing factor in effective organizational Knowledge management among the Investment Banks followed by Knowledge Sharing. It also emphasizes that they have a weak Knowledge retrieval process and minimal efforts taken to create knowledge within these banks.

Implications:

The PIAs can facilitate effective Data Analysis and research in managing vast data eliminating the repeated tasks in portfolio reconciliation and offering personalized recommendations to manage portfolios. It enables in compliance, risk management, client relationship management, real-time monitoring and leveraged decision-making through predictive analysis.

Keywords

Introduction

Investment banking is a specialized segment (Gelsi, 2024) primarily focused on providing financial services to corporations, governments, and high-net-worth individuals (Parisi et al., 2023). Investment banks act as intermediaries between companies requiring capital and investors willing to provide it. These banks usually offer services in either full-service or through the Investment Banking Division (IBD) (Lee and Shin, 2018). Knowledge management is capturing, organizing, storing, and sharing an organization’s knowledge assets to facilitate learning, decision-making, and innovation (Li et al., 2021). It involves creating a systematic approach to managing both explicit knowledge (codified information, documents, and databases) and tacit knowledge (personal expertise, experience, and insights) within an organization (Cai, 2018).

These banks are in a highly competitive industry that faces challenges (Königstorfer and Thalmann, 2020) in knowledge management due to high turnover and talent retention, information fragmentation, confidentiality and security, a dynamic emerging market, leveraged unstructured data, cultural barriers in knowledge sharing, and a magnified level of technology integration (Fasnacht, 2018). Investment banking employees often change employment for better avenues resulting in a severe loss of knowledge and experience. Knowledge management faces the difficulty of retaining talented employees and learning from them before they leave the firm is a critical drawback encountered by most of these banks (Wilson, 2019). Implementing efficient systems for knowledge transfer and succession planning became imperative to guarantee continuity and avert the loss of essential skills (Tchamyou, 2019).

These banks are seeing a shift in their knowledge management procedures, emphasizing using technology to enhance teamwork, guarantee compliance, and enhance efficiency. Data fragmentation may result from the existence of distinct knowledge bases and systems in each department (Soto-Acosta et al., 2018). Leveraging collective knowledge and experience may become more difficult due to the organization’s barriers to collaboration and knowledge exchange. Making significant inferences and learning valuable information from this unstructured data can be challenging. Employee knowledge sharing may be discouraged by the competitive and secretive culture that has historically characterized investment banking (Akram et al., 2020).

RQ1: Is it possible for investment banks to transfer the tacit knowledge of their employees into their knowledge management system?

Artificial intelligence (AI) plays a critical role in investment banking knowledge management by increasing data analysis, search capabilities, tailored suggestions, collaboration, and decision-making (Owen et al., 2018). These banks operate effectively by harnessing and exploiting their knowledge assets to create improved investment strategies, risk management, and client services through advanced technology. These are implemented through Personal Intelligent Assistants (PIAs), Specialized Intelligence, Codification of Knowledge, Know-How and Know-What (Amankwah-Amoah et al., 2021).

RQ2: How can Artificial Intelligence be applied to knowledge management among Investment Banks?

Personal Intelligent Assistants (PIA) are software applications or digital platforms that use Artificial Intelligence (AI) and Natural Language Processing (NLP) to provide personalized and interactive support (Contractor et al., 2020) to users in the form of virtual assistants who offer services as personal assistants and are programmed to perform a variety of chores, deliver information, and provide services via voice commands or text-based interactions (Abedifar et al., 2018). They utilize machine learning algorithms to comprehend user searches, learn from user interactions, and continuously adapt their responses. These assistants are operated through multiple devices like smartphones, smart speakers, and other devices, providing users with convenient and personalized support in various aspects of their lives (Kaur et al., 2020).

Investment banking employees can benefit from applying knowledge by using personal intelligent assistants to help them with various activities and decision-making processes. The main contributions are client relationship management, market insights, financial modeling and analysis, investment decision support, risk assessment and management, compliance guidance, and transaction execution. However, it invites certain challenges in the adoption of new technologies and may encounter resistance from investment experts (Ashta and Herrmann, 2021). These banks often have to deal with challenges in implementing PIAs like adhering to data security and privacy concerns, maintaining data quality and integrating with other information systems, ethical considerations and auditing these systems. A seamless transfer and coexistence with other platforms and tools utilized within the company depend on interoperability. It is imperative to guarantee that PIS can expand to accommodate the growing volumes of data and generate outputs with superior performance. These banks are expected to domicile and local countries’ regulatory compliance to avoid crucial legal issues (Seetharaman, 2020).

RQ3: Can personal Intelligent Assistants improve knowledge management in investment banks?

These assistants are pumped with overloaded information, expanding the cognitive bandwidth, filtering, sorting, and enabling information to navigate through the internal premises of the business (Alt et al., 2018). As a result, the researchers investigated the research gap in testing the theoretical framework empirically (Bolisani and Bratianu, 2018) of Artificial Intelligence in the Knowledge Management Process (KMP) among the Investment Banking Companies leading to Industrial Revolution 5.0 (Radhakrishna et al. 2021) in terms of probable application of Personal Intelligent Assistants in effective knowledge management in the Investment Banks (Machkour and Abriane, 2020).

Therefore, the study’s innovation lies in its empirical testing of the conceptual framework developed (Jarrahi et al., 2023) regarding the use of Artificial Intelligence (AI) through the use of Personal Intelligent Assistants (PIAs) in the Knowledge Management Process (KMP) of investment banks. The suggested research model is examined using a combination of covariance-based structural equation modelling and machine learning. Furthermore, absence of integrated approach and prior research indicates that no empirical testing of the suggested hypothesis has been done to date, which adds to the body of knowledge in the field of investment banking.

Theoretical background and hypothesis development

Knowledge Management plays a crucial role in the dynamics of every business organization facilitating the capturing, storing, and sharing of employees’ knowledge and experience improving the workforce’s efficiency, and protecting intellectual capital (Antunes and Pinheiro, 2020). It assists in organizing information into easily accessible formats for both internal and external consumers by organizing documentation, frequently asked questions, and other information (Schniederjans et al., 2020). There are various forms of information being captured in knowledge management namely, people, process, technology, documentation, advice, training, expertise, onboarding, knowledge transfer, continuous improvement, best practices, FAQs, and corporate calendars.

Organizations often are dependent on innovation as a critical process to adapt to their constantly changing business environment. Innovation is the fundamental catalyst leading toward the result when combined with information and ideas facilitating in creation of business value. The emerging technological advancements in the banking industry have revolutionized both traditional banking operations and client experiences (Ode and Ayavoo, 2020). Mobile banking has ensured to reach out to the remotest geographical localities by offering customers access, to perform banking operations directly from their smartphones where payments can be made in the form of digital wallets or Unified Payment Interface (UPI). Technologies like Near Field Communication (NFC) and QR Scan codes facilitate safe and easy transactions during point-of-sale (POS) terminals, online retail shopping, and peer-to-peer transactions. Blockchain Technology operates on decentralized distributed ledgers in handling financial transactions more transparently and safely reducing operational risks with improved settlements in real-time (Nowacki and Bachnik, 2016).

Artificial Intelligence and Machine Learning are disrupting the banking industry in preventing fraud and money-laundering activities. The banks provide customized financial services by third-party developers through Application Programming Interfaces (APIs) when collaborating with fintech firms, technology firms, and other financial institutions. Biometric authentication methods enhance banking security systems (Muhlroth and Grottke, 2022). Robotic Process Automation (RPA) has simplified repetitive and time-consuming activities in banking operations, improving operational efficiency, and productivity, and reducing errors. Cloud computing-based banking solutions have scaled up the banking infrastructural architecture by reducing costs and increasing the agility, and flexibility to deploy customized services to their customers.

Every Knowledge Management model in the organizations is built on the fundamental factors of Information capture, Storage, Customization, and Usage (Mcadam and Mccreedy, 1999). The models were grouped into knowledge categories, intellectual capital models, and socially constructed models. Organizational learning, Knowledge and memory were considered as the three key interconnected concepts to diagnose the present state of the changing organizational landscape (Martins et al., 2019). Organizations may organize and use their collective knowledge and expertise more efficiently using KM models, which are frameworks (Carayannis et al., 2021). Employing a knowledge management strategy and approach will help organizations stay ahead of the competition. Karl Wiig KM model proposed the integration of individuals and organizations with four stages namely, building, holding, pooling, and applying knowledge (Walczak, 2005). Nonaka and Takeuchi Model was based on knowledge creation through socialization, externalization, combination, and internalization (Ferreira et al., 2020). Zack KM model emphasized the conversion of information into usable knowledge through stages of acquisition, refinement, storage, and retrieval. Bukowitz and Williams Model illustrates recommended management framework outlined on the themes of Get, Use, Learn, and contribute stages in the organization (Abubakar et al., 2019). Choo Sense-making model was based on three major components sense-making, knowledge creation, and decision-making skills. Complex Adaptive Systems models are designed using Intelligent Complex Adaptive Systems performing significant tasks with interaction (Di Vaio et al., 2021).

Knowledge Management is the culmination of the creation, evolution, exchange, and application of new ideas that are converted into marketable goods or services in the organization. It can be observed that considering current business dynamics, knowledge management supports and proves to be a source of innovation. Knowledge management is of various types; (a) Explicit Knowledge—It is formal and documented knowledge that is easily accessible, documented, and applied. (b) Tacit Knowledge—It is personal knowledge that includes knowledge of employees and managers in an organization. (c) Market Knowledge—It is the knowledge in terms of customer expectations, needs, and business processes to execute. (d) Technological Knowledge—It pertains to applying technology in manufacturing, improving employee’s experience in transforming education into working experience.

The current study is based on the knowledge-based theory. Knowledge-Based View (KBV) (Grant, 1996) stipulates that organizations that effectively utilize knowledge-based resources, tend to be successful, competitive, and sustainable in the long run. Knowledge-based theory is a management theory that emphasizes the critical role of knowledge in creating and sustaining a competitive advantage for organizations (Fernández-Villaverde et al., 2021). It builds on the premise that knowledge is a strategic resource that can provide unique capabilities and insights, enabling organizations to outperform their competitors (Chernobai et al., 2021).

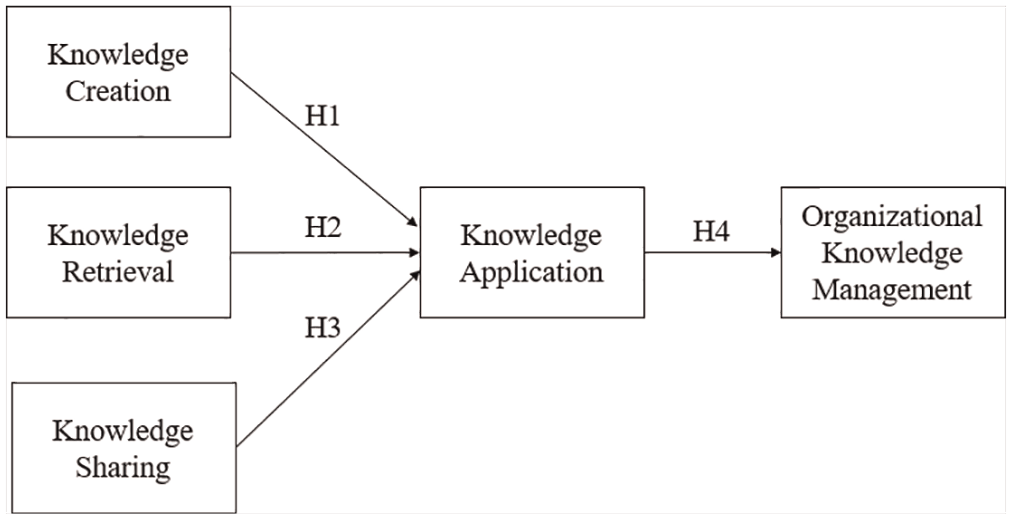

Figure 1 illustrates the conceptual framework designed with knowledge creation, knowledge retrieval, and knowledge sharing leading to knowledge application in effective knowledge management among the Investment banks. Investment banks need to effectively leverage their collective knowledge to make informed investment decisions, identify market trends, mitigate risks, and provide value-added services to their clients (Lee and Chen, 2022).

Proposed research framework.

The process of developing new knowledge or insights through diverse activities, experiences, and interactions is referred to as knowledge generation. It entails changing current information, facts, and knowledge into new ideas, conceptions, and understanding (Margiono, 2020). It is an important part of knowledge management and is required for organizational learning and innovation. Sensemaking is the process of making sense of information and experiences to produce new knowledge (Begenau, 2020).

Knowledge creation entails in analyzing and synthesizing information to identify gaps, inconsistencies, or alternative perspectives. Collaboration and dialogue among individuals or groups with diverse perspectives (Abualoush et al., 2018; Owen et al., 2018). Engaging in discussions, sharing ideas, and challenging one another’s assumptions can stimulate new thinking and generate fresh insights (Lee et al., 2020). It comprises analyzing and synthesizing data to uncover gaps, discrepancies, or alternate points of view (Nizam et al., 2019). Collaboration and communication between individuals or organizations with different points of view can promote knowledge generation. Discussions, sharing ideas, and challenging one another’s preconceptions can all help to inspire new thinking and develop discoveries (Vives, 2019). Creating a culture that values learning from mistakes fosters knowledge development and continual improvement (Oyewumi et al., 2018).

H1: Knowledge creation positively influences knowledge application towards Knowledge management in Investment banks.

Knowledge Retrieval is the process of accessing and retrieving appropriate information, data, or knowledge from numerous sources to meet a specific requirement or answer a question (Sarker et al., 2018). It entails locating and accessing the appropriate resources and extracting the needed information in a timely and effective manner (Moro-Visconti et al., 2020). Identification of needs, proper source selection, search tactics, access information, evaluation, and knowledge storage are the important parts of retrieval (Gallemore et al., 2019).

H2: Knowledge retrieval positively influences knowledge application towards Knowledge management in Investment banks.

Knowledge Sharing is conveying and spreading knowledge, skills, insights, and information across individuals, teams, and organizations (Leo et al., 2019). It entails the exchange of tacit knowledge (personal experiences, abilities) as well as explicit knowledge (codified material, papers) to improve learning, collaboration, and creativity (Lee, 2020). Training programs and mentoring activities can help to encourage knowledge sharing. Recognizing and recognizing individuals and teams for their efforts in knowledge sharing can help to emphasize the value of information sharing (Nawaz, 2019). Effective knowledge-sharing fosters cooperation accelerates learning, and allows firms to capitalize on their employees’ pooled expertise and experience.

H3: Knowledge sharing positively impacts knowledge application towards knowledge management in investment banks.

Knowledge application is compiling knowledge and insights (Aydiner et al., 2019) into practice in real-world situations. It entails applying knowledge acquired, communicated, and understood to solve issues, make educated decisions, innovate, and achieve desired results (Nurdin and Yusuf, 2020). It bridges the gap between theory and practice by translating information into actionable steps and outcomes (Tarullo, 2019). It entails applying insights and information to uncover possibilities, generate new ideas, and produce innovative solutions or products. Converting abstract or theoretical knowledge into actual plans, processes, methodologies, or activities is what this entails. Monitoring and assessing knowledge application aids in determining its impact and efficacy (Gopal and Schnabl, 2022).

H4: Knowledge application positively influences knowledge management in Investment banks.

Organizational knowledge management (Wang et al., 2020) is the systematic capture, organization, storage, and sharing of knowledge inside an organization to improve performance, facilitate learning, and drive innovation (Buckley et al., 2018). It entails developing a supportive culture, putting processes and tools in place, and encouraging cooperation to utilize and maximize the organization’s aggregate knowledge. It seeks to foster a knowledge-driven culture in which knowledge is viewed as a strategic asset that must be actively managed to drive corporate success (Gomber et al., 2018). Organizations may increase their skills, stimulate innovation, improve decision-making, and achieve a competitive advantage in their respective industries by successfully capturing, organizing, sharing, and utilizing knowledge (Berger et al., 2000).

Algorithmic trading analyses large voluminous financial data detecting market trends, and price movements in real-time at greater speed to examine the patterns to execute the trade automatically. Robust risk management systems assess and mitigate potential risks. Chatbots and virtual assistants powered by AI offer personalized services to customers when integrated with Natural Language Processing for better customer engagement. Machine Learning is capable of predicting asset prices, developing investment strategies, and trade optimization in real time considering historical data. AI-driven platforms recommend optimized portfolios depending on the risk, return, market conditions, and investment goals of the investors (Yablonsky, 2021).

Materials and methods

Instrument development process

The study is explorative and focused on exploring the applicability of Personal Intelligent Assistants in organizational knowledge management among the Investment Banks. The conceptualized research model comprises five latent constructs, namely Knowledge creation with four items, Knowledge retrieval with three items, Knowledge Sharing with four items, Knowledge application with three items, and knowledge management with four items measuring the concerned constructs (See Appendix for item measurement).

The conceptualized framework was examined for reliability which was examined through Content validity and face validity (Mardani et al., 2018). The developed conceptual model was tested empirically (Kaushal et al., 2021) using Confirmatory Factor Analysis (CFA) and Structural Equation Modelling (SEM) integrated with Machine Learning. Each construct was theoretically and operationally conceptualized for further statistical analysis as illustrated in Table 1.

Operational and conceptual definition.

Source: Authors’ compilation.

Examining each question on a test and consulting experts to determine whether it targets traits that the instrument is intended to cover constitutes content validity (Yulianto et al., 2021). In this phase, the test is evaluated for its objectives and the construct’s theoretical qualities (Binti Daud et al., 2021). The content validity and face validity of the constructs were investigated by a panel of Subject Matter Experts (SMEs) from the technological domain and Investment banking domain. They were consulted to refine the item measurement scale to suit the current requirements of the study before proceeding with data collection (Choi et al., 2019). The experts chosen were approached due to their experience and expertise in the concerned fields, deemed necessary to understand the conceptual and operational definitions of the constructs and their indicators (Dunn, 2020). They often evaluate the items measuring both quantitatively and qualitatively. Qualitative evaluation comprises examining the content wording, inclusive or exclusive of items measuring the constructs. The quantitative evaluation consists of experts assessing the dimensions using a numerical scale (Likert Scale) ranging from one to three (Fernández-Gómez et al., 2020), considering the relevance, usefulness, and importance of items when combined with both Investment Banking and Technology.

Content validity of the instrument was developed as recommended by (Almanasreh et al., 2019) and measured by a panel of Subject Matter Experts (SMEs) to evaluate each item measuring the construct. Five domain experts comprising two from Investment Banking, two from Information Technology, and one from the academic background were approached to assess whether the component measured by the item is “Essential.” Content Validity Ratio (CVR) (Swerts et al., 2021) was computed for item measuring construct using the below formula.

Where, ne = number of SME panellists indicating “essential,”N = a total number of SME panellists.

Content Validity Ratio ranges between +1 to −1, values below “0” indicate lower validity, and closer to “1” indicates higher validity (Shakibazadeh et al., 2021). However, to rule out the coincidence agreement among the panellists, the critical value was compared against the number of panellists. Table 2 illustrates the summary of CVR, Critical value, and the opinion of experts for each item measuring the construct.

Summary of content validity ratio.

Source: Author’s compilation.

The CVI is the average CVR score of all the items considered for expert opinion (Baghestani et al., 2017). Comparing the CVI against the critical value for a panel of 5 experts (0.99) which falls within the accepted cut-off value (Saiful and Yusoff, 2019) as described in Table 3, it can be inferred that CVI is very close to 1 confirming the content validity.

Content validity index cut-off.

Source: Author’s compilation.

The face validity of the constructs and their items were examined through a pilot study to validate the created scales on the theoretical Framework (Ishanuddin et al., 2021), with a sample size of the Investment Banking employees (n = 50 > 30, (Albers and Lakens, 2018)), which produced a scale reliability (Cronbach’s α = 0.85 > 0.70, (Samat, 2020)) confirming the reliability of the instrument.

Sampling and data collection

Investment banking is increasingly becoming a prominent segment in the banking industry of India due to its supporting the global economy, increasing professional skillsets, expanding industries, and abundant young talented workforce. The current research is fundamentally on Quantitative method (Busetto et al., 2020) involving primary data collected through a Self-administered Survey Questionnaire (Blázquez-Sánchez et al., 2020) circulated to the employees working across the various Investment Banks using Multi-Stage Clustered Sampling method. The geographical location of India was clustered into North and South. Further, these banks were clustered into Investment Banking Divisions and Full-Service Investment Banks operated in Bangalore, Mumbai, Delhi, Hyderabad, Chennai, and Pune. Since their foray into India, the majority of international banks providing services through their Investment Banking Division (IBD) have established in these locations of the financial service industry (Tiberius et al., 2022). A sample size of 695 was arrived randomly from IBD segment of these banks. Out of a total 750 circulated questionnaires across the chosen six metropolitan cities, only 695 were completed in full.

The top 10 investment banks that were randomly selected are made up of a variety of operational divisions that provided equitable participation in the study, including Reconciliation, Trade, Performance Measurement, Graphic Design, Client Reporting, Compliance, and Market Data Service. In this study, the respondents were the employees who worked in each of these divisions.

All participants in the research were given information about the study’s goal and gave their voluntary consent, all by the ethical guidelines established by the Association of Investment Bankers of India (AIBI). The Human Resource team’s permission was sought before contacting the respondents, who were guaranteed their confidentiality. The researchers individually gathered and analyzed the data with utmost care.

The first part of the questionnaire involves the demographic profile of the respondents and the second part consists of the items measuring the constructs on a five-point Likert scale ranging between 1 (Strongly Disagree) to 5 (Strongly Agree). Each employee working across the Investment banks is considered as the sampling unit.

Data analysis

Tacit knowledge is personal in nature which includes the experience, expertise, skills, abilities, values, and novel ideas generated in the form of knowledge from employees and managers in the organization. This type of knowledge is difficult to articulate and transfer to others due to the lack of formalized documentation in the organization’s knowledge base, especially in the Investment banking industry considering the complex nature of operations.

The research objective was to test the feasibility of the application of existing Knowledge-based theory among investment banks and to confirm the ability of Personal Intelligent Assistants to transform their tacit knowledge into an effective knowledge management system. Considering this novel approach of theory testing through artificial intelligence in the less explored domain of the investment banking industry, CB-SEM with reflective measurement was considered appropriate in testing and confirming the proposed research model. Similarly, the measurement error in predictive (knowledge application) and outcome (organizational knowledge management) variables provides more accuracy estimation in the model. It is an apt statistical method to estimate and test correlations between independent (Sharing, storing, creation, application) and dependent (Organizational knowledge management) and account for measurement error in both predictive and outcome variables providing more accurate estimation in the model tested effectively based on indices (Dash and Paul, 2021).

Covariance Based (CB-SEM) Structural Equation Modelling was performed using JASP V.18 to validate the hypothesis. CB-SEM estimates and tests correlations between independent and dependent variables as well as the latent structures that exist between them using a statistical model. The model is calculated with the assumption that the constructs are shared factors, estimating the model based on the presumption that the constructs are common factors. It can analyze latent structures and observed variables simultaneously, as well as their relationships and effects on the associated results variables (Thakkar, 2020). To provide a more accurate estimate of the model parameters and effects as well as better control for both the measurable and the latent factors, it may account for measurement error in both the predictive and outcome. This aids researchers in determining the most accurate and frugal approximation models in theory. CB-SEM was used to analyze the research model that was conceptualized. In addition to being acceptable given the study’s smaller sample size, it is recognized as one of the most sought-after methods that makes it simpler to test and validate existing ideas depending on the research objective. This approach of SEM is most appropriate for testing theories, developing simple models with minimal variables in context to reflective models that facilitate in evaluating the model fit (Cheah et al., 2020).

The data was further analyzed using Machine Learning (Gradient Boosting Regression method) to explore the model fit that could be used in training the PIAs in facilitating the transfer of knowledge to optimize the organizational knowledge management among the investment banks. Machine Learning (ML) is a branch of Artificial Intelligence and Computer Science that is focused on using data and algorithms to enable AI to imitate humans in learning and is reshaping the industries of various sectors (Isabona et al., 2022). Boosting is a supervised machine learning strategy that combines the predictions of multiple weak models (base model) to generate a powerful ensemble model to create a robust predictive model and improve its accuracy (Beheshti et al., 2022).

Results

Descriptive statistics

The demographic profile of the respondents comprised 85% from the Investment Banking Division, and the rest from Full-Service Investment Banking. The gender of the respondents shows that 75% are male and the rest are female. Eighty percent work in the back office, 10% in the middle office, and the rest from the front office. CB-SEM was applied to analyze the data through two phases (Measurement Model and Structural Model) to examine the hypothesized research framework by applying the Maximum Likelihood Estimation (MLE) method of extraction (Kim et al., 2022).

Measurement model assessment

Internal Reliability (Cronbach’s α) and Composite Reliability (CR) were inspected and found above the recommended threshold of 0.7, (Hair et al., 2019) confirming the internal consistency of the indicators. Item’s factor loadings and Average Variance Extracted (AVE) were examined to evaluate the Convergent Validity. The factor loadings of each indicator measuring the construct reflected more than 0.6 (Velten et al., 2021) AVE greater than 0.7 (Sahoo, 2019). Table 4 demonstrates the parameters satisfying the measurement model.

Measurement model summary.

Source: Authors’ compilation.

Discriminant Validity of the model, a metric used as evidence measuring the constructs that theoretically should not be highly related to each other are, in fact, not found to be highly correlated to each other. It was assessed using Fornell and Larker Criterion (Radomir and Moisescu, 2020) as illustrated in Table 5. Therefore, reliability and validity were obtained.

Discriminant validity (Fornell-Larker criterion).

Source: Authors’ compilation.

The bolded values within the table are the square root of variance shared between the constructs and their measures (AVE).

Common method bias

The researchers statistically tested for the absence of Common Method Bias in the data through Harman’s single factor test through unrotated Factor Analysis where the first factor contributed only 48% (< 50%). Variance Inflation Factors (VIFs) which were below the recommended threshold of less than 5, (Javed et al., 2020).

Structural model assessment

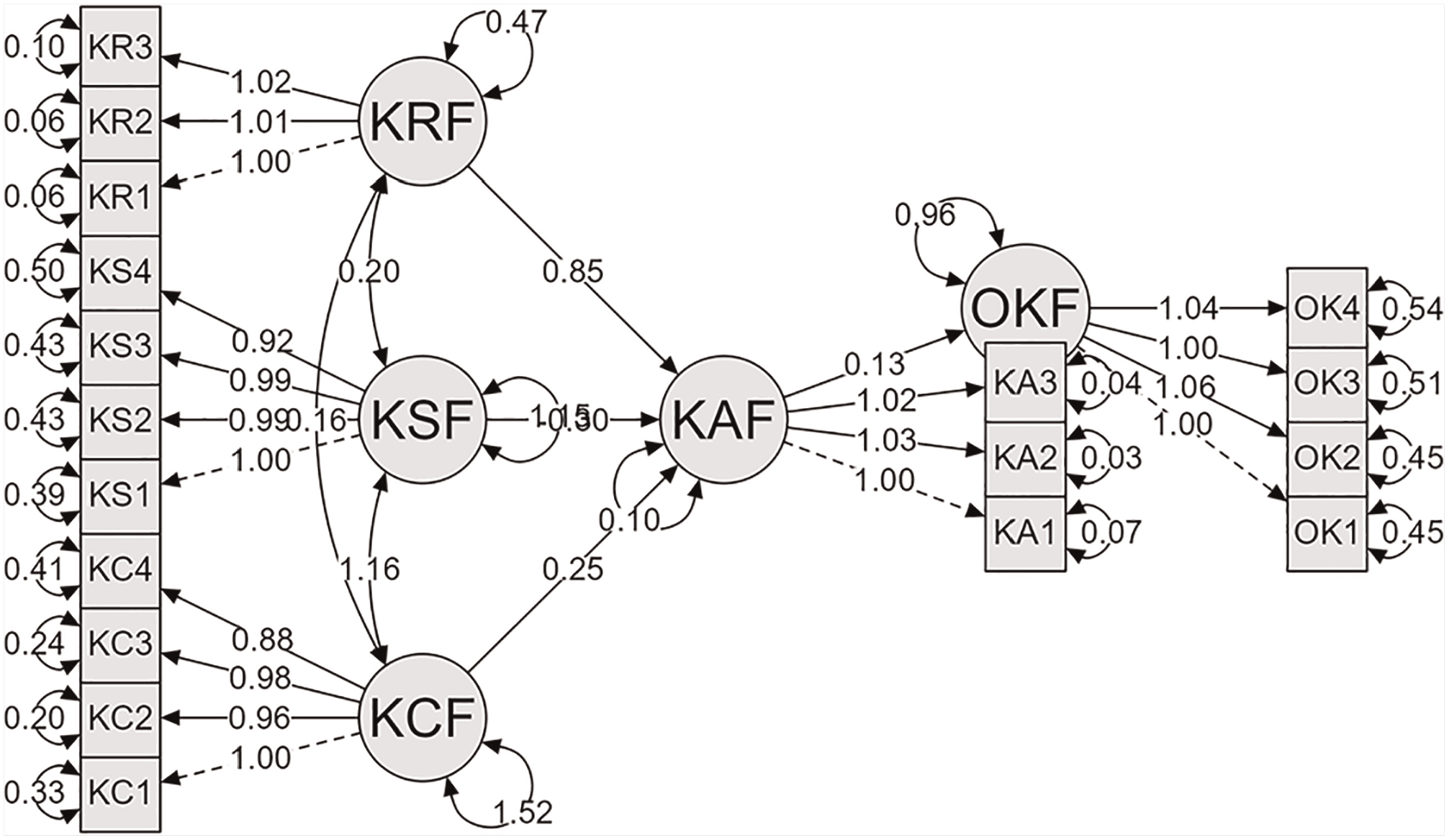

The assessment of the structural model was examined through Fit Indices and Path coefficients. χ2 = 1.892 < 3, CFI = 0.960 > 0.9, TLI = 0.951 > 0.9, NFI = 0.971 > 0.9, PNFI = 0.987 > 0.9, GFI = 0.969 > 0.9, RMSEA = 0.042 < 0.8, SRMR = 0.041 < 0.08 displaying the adequate fit of the hypothesized model based on the recommended fit indices value (Cho et al., 2020). Figure 2 shows the path diagram of the Structural Equation Model of the study.

Path diagram of SEM.

Table 6 shows the summary of the path diagram from which it can be observed that there is a positive and statistically significant influence of knowledge creation on knowledge application (β = 0.250, p < 0.001) supporting H1. Knowledge sharing has a positive and statistical influence on knowledge application (β = 0.300, p < 0.001) supporting H2. Knowledge retrieval has a positive and statistical influence on knowledge application (β = 0.851, p < 0.001) supporting H3. Knowledge application has a positive and statistical influence on Organizational Knowledge Management (β = 0.132, p < 0.05) supporting H4.

Structural model summary.

Source: Author’s compilation.

The standard error (SE) of measurement calculates the distribution around a person’s “true” score on many assessments taken with the same tool. The SE between the path Knowledge creation reflects 0.033, Knowledge sharing reflects 0.039, and Knowledge retrieval 0.028 towards Knowledge Application respectively. Knowledge Application reflects a S.E of 0.060 toward Organizational Knowledge Management. A few unidentified variables, such as lack of technology awareness, bank employees’ resistance to technology adoption, and fear of losing their employment, affect the prediction.

Gradient boosting regression

The gradient Boosting Regression method was deployed to analyze data further in examining the predictive ability of the proposed research model in knowledge sharing, knowledge retrieval, and knowledge creation influencing the knowledge application among the investment banks through PIAs. Effective knowledge application leads to organizational knowledge management. This approach (Dhali et al., 2020) is widely used and designed to produce a strong learner who is accurate on the training data and generalizes effectively on new data.

The performance of the algorithm was evaluated based on the critical metrics for evaluating the predictive model consisting of Mean Absolute Error (MAE = 0.0365 < 1.52) measuring the absolute difference, Mean Square Error (MSE = 0.0015 < 0.22) measuring the mean square error, Root Mean square Error (RMSE = 0.215 < 0.50) measuring the standard deviation of the prediction errors between actual and predicted values. The Coefficient of Determination (R2 > 0.75) measures how well the observed outputs are reproduced by the model. Hence, it can be demonstrated that the gradient boosting regression method can predict the mode more accurately as the quantitative performance metrics as illustrated in Table 7 are within the acceptable range (Feng et al., 2020).

Summary of model performance using machine learning.

Source: Authors’ compilation.

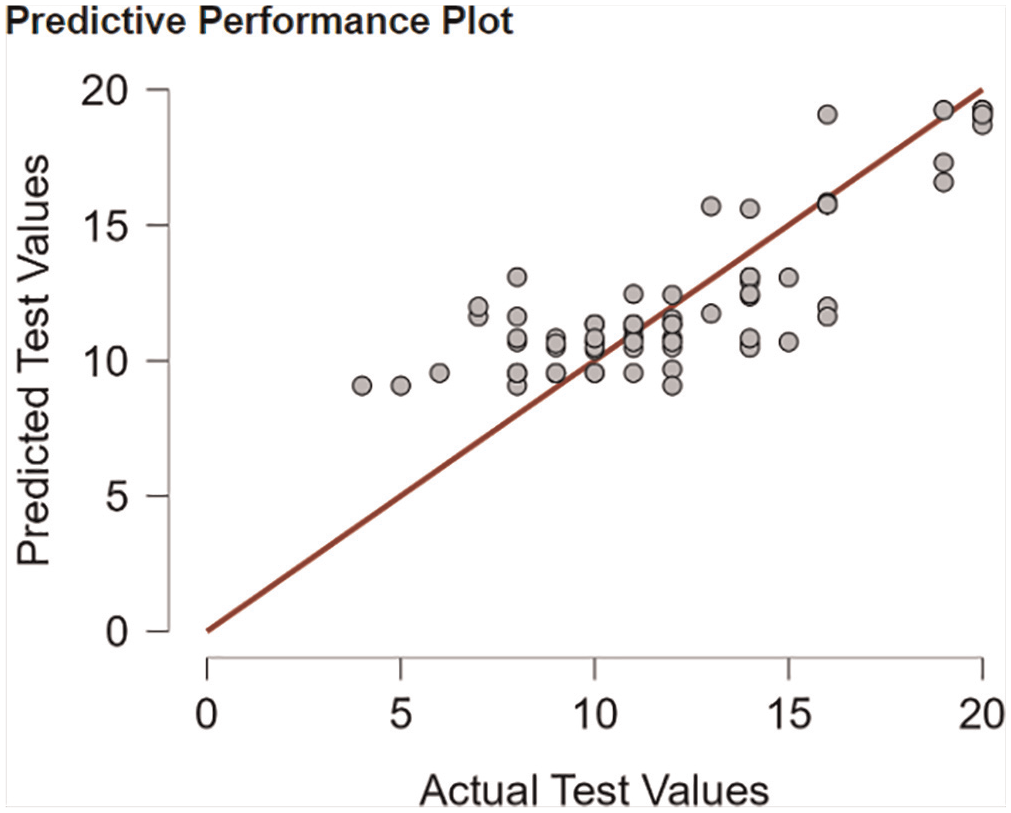

Figure 3 illustrates the predictive performance of the model between the actual and predicted test values in the model.

Graphical illustration of predictive performance.

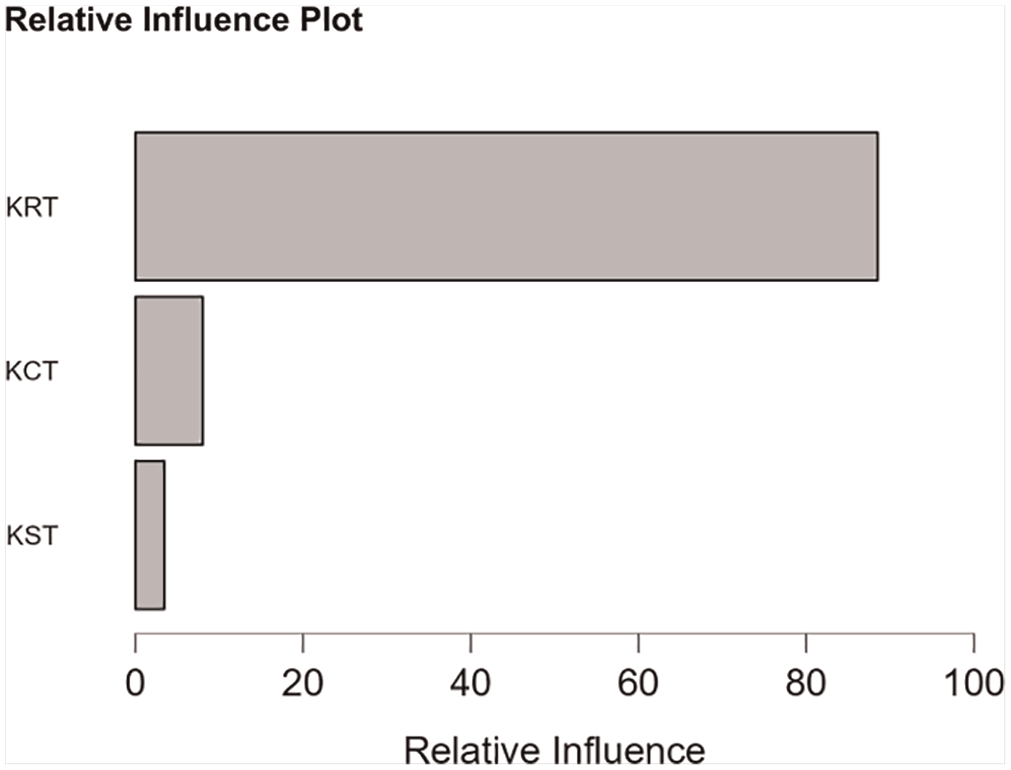

Figure 4 shows the relative influence of each construct, KRT, KST, and KCT in the prediction of a latent variable (KAT) that ultimately influences the (OKM). The variable KRT has a relative influence of 88.5%, KCT influences 8.045%, and KST influences 3.443%.

Graphical illustration of construct influence on dependent variable.

It can be observed that among the mentioned constructs, KRT has the maximum and highest influencing variable, the second being KCT, and the least being KST in determining the KAT in the model. This aligns with the results obtained from SEM where the path coefficient of KRT → KAT is the most influencing construct (β = 0.851, t = 30.32, p < 0.001).

Discussion and conclusion

It can be observed that the variance of Organizational Knowledge Management is highly explained and influenced by Knowledge retrieval (0.851) which plays a key role in the investment banking business in the context of confidentiality of the client information, risk management, and financial services. Therefore, the R2 of the model confirms that the relationship between knowledge retrieval towards knowledge application is predicted by 85.1%. The results obtained from the Structural model are well supported by the gradient boosting regression technique of machine learning where KRT with 88.5% influences significantly in the robust KAT in the predicted model that increases the effectiveness of organizational knowledge management among the investment banks. Hence, it can be confirmed that the model predicted is accurate (Otchere et al., 2022) in demonstrating the successful implementation of PIAs in investment banks.

Similarly, Knowledge creation (0.250) enabled predicts 25% toward knowledge application, and knowledge sharing (0.300) reflects that predicting 3% toward knowledge application. The knowledge application (0.147) can predict Organizational Knowledge Management by 14.7% which is less than the other paths in the model. The use of PIAs in knowledge management by investment banks is still in its infancy stage and may encounter resistance during adoption. Additionally, it demands that employees receive comprehensive training with an emphasis on developing an efficient knowledge management system at the organizational level due to its sensitive and confidential business. The unexplained prediction is the reference to the error terms that tend to remain within the business environment irrespective of internal or external factors of knowledge creation, knowledge sharing, and knowledge retrieval influencing the prediction ability of knowledge application in the context of organizational knowledge management.

The Content Validity Ratio of item, KC 4 (Developing new declarative knowledge) received the lowest score by the panel of experts compared to the other items measuring the construct, “Knowledge Creation.” Declarative knowledge in the context of investment banking is defined as facts, guidelines, and claims that describe the characteristics, concepts, and rules of the sector. Even though standard operating procedures are in place, problem-solving ability is applied based on the situation because of the dynamic nature of the company’s operations (Arsawan et al., 2022). For example, the portfolio manager must decide quickly whether to use the funds in the portfolio upon a client’s contribution to execute trades in buying or selling upon the client’s redemption.

Theoretical implications

Investment banks are prone to information being shared leading to insider trading and hence they must ensure to take every step to prevent the crucial information being shared out of their business (Lee et al., 2021). Most banks have already taken steps towards preventing unauthorized transfer of information by placing controls on their Internet of Things, Corporate governance, Anti-Money Laundering, and many more (Fakhar Manesh et al., 2021). However, they see a huge gap between the knowledge transferred during attrition as the experienced and knowledgeable person passes on the legacy to the new members of the team. These banks must focus on creating documentation in terms of manuals and standard operating procedures within the operational levels across their teams.

Practical implications

PIAs can enhance various stages of this paradigm because of their ability to assist individuals in managing and utilizing knowledge within the banks. Integration into investment banks’ knowledge management systems requires frequent evaluations, feedback loops, and PIA upgrades (Yu, 2020). This section discusses the potential benefits for investment banks from the practical implementation of these assistants based on different knowledge management models:

Nonaka and Takeuchi model: It enables connecting employees with similar interests across operational areas offering a forum to share tactic knowledge using Natural Language Processing (Friedrich et al., 2020). It aids experienced portfolio analysts in assessing market trends during their investment decisions into corporate actions like Mergers and Acquisitions, takeovers, and underwriting, offering tools to collaborate on brainstorming ideas and prompting users to stimulate relevant queries in the process. They facilitate the portfolio managers and portfolio analysts in creating knowledge repositories allowing the users to access and explore relevant information based on their experience. These offer personalized recommendations of content in the form of training material or simulations in real-time guidance and feedback.

Karl Wiig Model: To extract valuable information from a variety of documents, it recommends storing knowledge in individualized repositories and suggests appropriate storage sites (Shahzad et al., 2020). They also propose knowledge transfer in succession planning as a clever mediator for real-time translation between people or groups. To increase productivity, this encourages the recommendation of back-office operations such as portfolio reconciliation about stock and cash positions between custodians, stock brokers, and fund managers. These operations can be automated by integrating with intelligent systems to reflect financial transactions, perform reconciliation, compute portfolio performance measurement by comparing against market indices, project Net Asset Value, and generate client reporting.

Zack Model: This model when integrated with PIAs illustrates the procedures to the banks that outline as a bridge in building the knowledge gap (Crupi et al., 2020) between the sources of knowledge and the concerned user to acquire specialized domain expertise or excel as a subject matter expert that is often applied in front-office operations during onboarding of clients within the banks.

Bukowitz and Williams Model: Under this paradigm, PIAs help banks automatically gather implicit knowledge from employees as they interact in meetings and conferences at common areas, all without the need for human participation (Papa et al., 2020). Cross-training between various operational segments like trade, market data service, client reporting, and induction process towards recruits are automatically documented for future use. This promotes the development of taxonomies with sophisticated search features when the employees need to verify certain process flows. It also provides specialized insights into the challenging issues in risk management of handling client cash contributions, and portfolios not performing well when compared with market indices. This also encourages feedback collection to suggest user reflections based on learning analytics data.

Choo’s Sense-making Model: These assistants can identify problems such as failed trades and system failures during peak productivity periods (Agarwal and Sambamurthy, 2020). They can then quickly notify the relevant help desk teams, gather information about the reason for the failure, and add to the existing knowledge bases to handle similar problems in the future. To facilitate information sharing within the banks, they create knowledge crafts with cooperative tools. Interactive dashboards that integrate data from multiple sources to visualize insights and enhance decision-making can be reflected in it.

Complex Adaptive Systems Model: During the knowledge management process, they examine user behavior patterns (Dwivedi et al., 2020)especially while undergoing the training process, and focus on proposing more related concepts for improved comprehension. They encourage relationships between repositories and personnel from other disciplines. This approach highlights the importance of ongoing learning and adaptability as crucial steps in the knowledge management process.

It is imperative to note that these PIAs cannot replace humans in problem-solving ability and expertise in the investment banking sector and instead must be considered as a tool to complement knowledge management systems to enhance their performance with improved decision-making capabilities. The common challenges encountered by these banks involve data security, resistance to adapting to technology changes, and privacy due to their complex nature of handling confidential and sensitive client information. The integration of these PIAs requires huge investments in infrastructure, technology, and upskilling employees to manage and optimize these systems effectively. The Investment banks may encounter conflicts of interest while using these PIAs when controlled by entities, stringent government regulations governing the financial markets, and clarifying accountability and liability for the decisions made by these assistants to ensure the protection of the investors and other stakeholders. The resistance from employees to adapt to the technology is fear of losing jobs. Ensuring that PIAs are used responsibly and ethically in the context of investment banking necessitates a holistic approach involving cooperation between investment banks, regulators, AI developers, and other stakeholders.

Managerial implications

Effective knowledge management has a significance that can drive improved performance with enhanced managerial decision-making in data-driven decisions in the areas of Customer Relationship Management (Kaur et al., 2020) through tailor-made financial solutions, managing corporate governance, and other compliance policies. It also enables in talent retention and development to retain the best of their employees with more focused succession planning. These benefits encourage in better portfolio performance against a market index, enhanced risk management strategies, customer satisfaction, and long-term sustainability (Luo et al., 2021).

However, Investment banks can greatly improve their knowledge management procedures by utilizing Personal Information Assistants (PIAs). Natural language processing, machine learning, and predictive analytics are examples of advanced capabilities that PIAs can leverage through the seamless integration of AI technology into knowledge management frameworks among these banks (Ali et al., 2020). The bankers can receive real-time insights by using AI algorithms to examine massive volumes of market data through automated market data analysis that helps forecast trends.

The adoption of Machine Learning encourages predicting market trends, stock movements, and risk through predictive tools to make better decisions in optimizing portfolios and enhance risk management strategies (Hock-Doepgen et al., 2021). Combining AI and ML makes it feasible to develop and improve algorithmic trading strategies that boost trading effectiveness and have the power to adjust erratic market conditions to fit predefined standards.

NLP can establish a robust documentation analysis with features of extracting and exporting information from various sources with updated regulatory standards of both domicile and local nations in investments (Azeem et al., 2021). Investment bankers can receive personalized insights based on client preferences, risk tolerance, and investment objectives through AI-driven CRM platforms giving scope for customer involvement.

AI and ML models have the potential to improve fraud detection systems preventing money laundering and retaining regulatory compliance through audit bots monitoring transaction patterns. Sentiment analysis enabled by AI among these banks can forecast market sentiment based on data gathered from Bloomberg, e-news, print media, and social media (Abbas, 2020). This helps investment bankers make collaborative decisions through shared insights while providing financial advisory services.

Limitations and future scope

PIAs are revolutionizing various domains within investment banking by augmenting human capabilities through increased productivity, accuracy, and decision-making processes, but they have several limitations. Firstly, the present study was confined only to the Investment Banking Division across the investment operations in India. The banks offering full-service weren’t considered, as most Indian-operated investment banks are limited to back-office operations due to market volatility and a lack of institutional investors. Second, it emphasized the empirical testing of the model for the proposed framework developed from a previous literature review.

The future scope of research in this domain is grouped into below specific avenues:

Impact of PIAs across different domains within investment banking: The possible application of this technology could be explored in customer relationship management, market research, trade and performance, portfolio management, compliance and regulatory reporting, decision support and forecasting. The operations of middle-office and front-office across Investment banking hubs in India are other avenues to consider.

Integration of other technological innovations in knowledge management processes: AI and ML—Integration of AI and ML to analyze complex data sets, automation of repetitive tasks, and retrieve actionable insights. Blockchain technology—This technology enables in sensitive information especially pertaining to client onboarding, trade settlements, client reporting. Big Data Analytics—The types of data (unstructured, structured, and semi-structured) could be used to analyze the hidden patterns and trends pertaining to market data and customer transactions. Cloud computing—It offers better control on coherent access to knowledge management resources through multiple devices to collaborate across their operating unit at various geographical locations. Usage of emerging technologies like Artificial Narrow Intelligence (ANI), Artificial General Intelligence (AGI) can be explored in detail.

Technology related models: Technology Acceptance Model (TAM), Theory of Planned Behavior (TPB), theory of innovation dissemination, task-technology fit, technology readiness, transtheoretical model, Theory of Reasoned Action (TRA), theory of interpersonal behavior, model for innovation-decision process, Unified Theory of Acceptance and Usage (UTAUT) could be empirically tested in the domain.

Conclusion

Investment banks must promote knowledge-sharing, cooperation, and continual learning to establish a knowledge-sharing culture. They must ensure to invest in user-friendly knowledge management platforms, data analytics tools, and artificial intelligence technologies to help with knowledge capture, retrieval, and analysis. These banks can achieve competitive advantage by leveraging their intellectual capital and knowledge assets creating an information-driven culture, adopting effective management techniques, focusing on continuous learning, and indulging in a collaborative learning atmosphere that treats knowledge sharing and innovation as integral parts of Organizational Knowledge Management They must implement knowledge-based platforms emphasizing the significance of knowledge creation, application, and sharing in the key areas of banking namely, financial analysis, risk management, investment strategies, client relationship management (Abbasi et al., 2021). This facilitates identifying market trends, reducing risks, and delivering value-added services to their clients, making more effective investment decisions through integrated knowledge.

Creating incentives and recognition programs for information sharing can also encourage staff to actively participate in knowledge management projects through a complete knowledge management strategy that focuses on people, processes, and technology (Hughes and Hodgkinson, 2021). Therefore, it can be concluded that the study reveals that Artificial Intelligence can be applied in the Investment Banks through Personal Intelligent Assistants in effective Organizational Knowledge Management.

Footnotes

Appendix—Item scale—Km process

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data availability statement

Data will be shared on request.