Abstract

Elasticity offers contractual parties the linguistic space to manage the unknown. While this has historically operated as a powerful tool in negotiation, elasticity has also behaved as a double-edged sword. That is, elastic language facilitates the present, but does not account for the future. In this article, we consider that by understanding the role of vagueness in contracts, and in effect, making the implicit explicit, it may be more rewarding strategically for contractual parties in the long term. Specific to the context of reinsurance, we notice that elasticity may be regarded as a mirror to negotiation dynamics, traceable by the linguistic complexity of contractual clauses. Therefore, a determination of elasticity, through a diagnostic tool, can offer insights to enable for more intentional drafting and certainty at the contract performance stage.

Introduction

Insurance is a risk management tool, allowing the transfer of risk to a third party. Risk can include any adverse event in the future, whose occurrence is not certain but probable, and one wants to protect herself from the devastating effects of that unwanted event. This transfer of risk from one party to another is the essence of any insurance policy. The precise conditions under which such transfer happens differ depending on many circumstances. Traditionally, conditions are captured in policy wording expressed in natural language, which often contains lengthy and difficult-to-understand terms and clauses. Even though technological advancements are driving innovation in the industry, the core product—the insurance policy—remains relatively unchanged. Arguably, the move from analog to digital is what could transform the industry and unlock new opportunities for consumers and insurance companies alike.

Digitizing the contract in the initial stage means making it human and machine readable by design. Such computable contracts are often expressed in the form of logic programming and may or may not encompass the nuanced expression found in natural language. Therefore, the move from analog to computable contracts could create more transparent and accessible products, allowing insurance companies to tap into new markets and lower costs throughout the value chain.

This transition is relatively intuitive for personal lines insurance products that are fairly standardized and relatively short documents aiming to protect individuals. By contrast, commercial insurance and reinsurance contracts are very sophisticated agreements, providing meticulous specification on the conditions for payout. Commercial insurance and reinsurance are business-to-business sectors where all parties are skilled negotiators. For instance, corporations seeking coverage for their properties hope to purchase insurance policies covering as many risk scenarios for the lowest price possible. Inevitably, the precise conditions of each insurance contract are very nuanced. Moreover, the negotiations between commercial insurance buyers and commercial insurers, as well as insurance companies and reinsurers, are often facilitated by specialized brokers. Intermediaries at every stage of negotiation often use variations in legal definitions to get their client the best deal in terms of coverage and price. Risks are often insured by several different insurers, and then, typically, each insurer will get reinsurance from one or more carriers. Lastly, reinsurers may cede some of their aggregate risks to other capital providers (known as “retrocession”). Each subsequent transaction is a separate legal arrangement, and as the reinsurance agreement is a separate contract from the original insurance contract, the original insured is not a party to the reinsurance. These factors then lead to significant clause wording variation, despite the same risk, product, and/or jurisdiction within the risk value chain (Swiss Re Group 2022).

Consequently, the intricacies of reinsurance contracts are far more difficult to capture for both humans and machines alike. The assumption is that formal languages, unlike natural language, are unable to “enrich” propositions expressed, since formal logic has no dimension capable of expressing context. Though logic is evidently a core component to legal structure, logic lacks the elasticity that is currently only available in the natural language realm. While logic is present, natural language text persists to clarify meaning. This suggests that logic should be considered as an entry-point and the groundwork laid, but that the drafting process does not stop there. What is required then is to unpack the complexity of the contextual and circumstantial use of ambiguity and vagueness in reinsurance wording. A deeper reflection on linguistic triggers and how it can be represented computationally is, therefore, the next logical step.

Linguistic background

As law has language at its core, contract interpretation is, in effect, a linguistic exercise. This has led to a heavy reliance on translation when reconciling human with machine-readability. Core linguistics suggests that natural language is composed of three underlying components: syntax, semantics, and pragmatics. Curiously, the enduring focus on syntax and semantics in computational models has led to a neglect of pragmatics, an arguably essential pillar in meaning-making. Consequently, this impedes understanding and contextualizing of legal concepts.

Pragmatics is the field of linguistics that reflects on intention, using tools of implicature and inference. Consider the phrase: “There is an elephant in the tree.” Semantics is helpful, to the extent that it could raise what may be a prototype example of an elephant. As prototypical elephants are not found in trees, this suggests that there may be other possible meanings. Could this be an idiom (i.e., “elephant in the room”)—or perhaps the elephant in question is a paper elephant? Additionally, pragmatics raises the issue of reference. Consider: “Jane is speaking with Joanne. She is a renowned legal scholar.” 1 The referent of “she” is not clear. Without context, semantics alone is insufficient to ascertain meaning.

Computational systems that use propositional logic reflect the limitations of semantics: propositional logic can enable the validation of some statements but cannot in itself establish the truth of all statements. 2 So, why must we consider pragmatics in computational law, and specifically, computable contracts?

Contrary to the rhetoric on clarity and precision, ambiguity is revered as an inherent property of legal drafting. This is because legal documents are not independent artifacts and instead belong to a broader ecosystem. The aforementioned issues of pragmatics in natural language are integrated into the fabric of law and legal text and powered by literary tools of metaphor and analogy that outline context. This has specific implications for contracts.

Vagueness rebranded

Elasticity offers contractual parties the linguistic space to manage the unknown. While this has historically operated as a powerful tool in negotiation, elasticity has also behaved as a double-edged sword. That is, elastic language facilitates the present, but does not account for the future. In this article, we consider that by understanding the role of vagueness in contracts, and in effect, making the implicit explicit, it may be more rewarding strategically for contractual parties in the long term. Moreover, a determination of elasticity, through a diagnostic tool, can offer insights to enable for more intentional drafting and certainty at the contract performance stage.

Specific to the context of reinsurance, we notice that elasticity may be regarded as a mirror to negotiation dynamics, traceable by the linguistic complexity of contractual clauses. Traditionally, reinsurance contracts contain incomplete and linguistically vague terms. These terms are frequently encased in complex sentences that do not always provide precise direction to their semantic meaning. Moreover, the verbiage of reinsurance clauses can occasionally be regarded as short-sighted, prioritizing current over prospective party relationships.

In order to test these claims, we focus on a subset of “Access to Records” clauses used in the American reinsurance market. Rejecting natural language processing (NLP) as a starting point, we apply human expertise to create a Semantic Fingerprint. We consider that an elasticity score could allow parties to adjust contractual language to increase precision but not nested complexities. That is, structured and precise specification could encourage further formalization efforts for the reinsurance industry. In effect, by developing an abstract framework and assigning a qualitative score to all components, we seek to unpack the extent to which vagueness may be a misnomer for implicit knowledge. More importantly, we consider that in leveraging elasticity, the robustness of reinsurance contracts may be strengthened.

Elasticity as a model for framing trust in reinsurance contracts

In understanding elasticity as a frame for reinsurance, we must first return to the uniqueness of insurance contracts. Zev Eigen investigated the relationship between individuals and organizations in the context of form-contracts (Eigen 2008: 381). Form-contracts are understood as agreements typically drafted by organizations (drafters) and offered to individuals (signers) with little to no opportunity to negotiate their terms. Insurance policies then fall within the broader notion of form-contracts. In his empirical study, Eigen explores individuals’ interpretations of these form-contracts and their perceived enforceability. To complete his analysis, he develops a measure known as “malleable consent” (Eigen 2008: 389). He describes this construct as consent given, without duress or fraud, that is, nonetheless, not necessarily enforceable against the signer. That is, there is a spectrum of expectation around perceived obligations, shifting between “must” to “could.” Eigen suggests that the limits of malleable consent help reveal individuals’ trust in the contractual agreement (Eigen 2008: 390).

Importantly, he determines that the extent of perceived enforceability of form-contracts is indicative of two key elements: (1) the signers’ regard for the agreement as either transactional or relational and (2) the signers’ dependency on the agreement, otherwise, the power differential between the organization and the individual (Eigen 2008: 390). In the former, individuals consider that the obligations stipulated in form-contracts are enforceable when there is an expressed trust between them and the organization. That is, there is a perceived relational exchange between the signer and the drafter. In the latter, the greater the power differential between organization and the individual, the higher will be the likelihood of contract enforceability. In other words, not only is trust substantive to contractual performance, but, more importantly, trust between parties is further compounded by power.

Applying then lessons from form-contracts to insurance, it may be important to acknowledge how trust behaves as a litmus test of the strategic relationship between contractual parties. How might this connect with reinsurance? Unlike insurance, reinsurance contracts are negotiated. Therefore, details of the contract reveal the contractual parties’ expectations, conceptualizations and realizations of their relationship (Chou, Halevy, and Keith Murnighan 2011). Again, Eigen provides helpful insight through his reflections on contracts “in action.” (Eigen 2012) Contracts hold the impression of legal constraints (Eigen 2012: 16), making specificity in language a critical matter in the formation of a contract. In another empirical study, Eigen identifies two key propositions on behavior around contracts. He sees contracts as products of how drafters and signers interpret the law (Eigen 2012: 17). This suggests that how contracts are written frame the behavior of parties and that drafting necessarily influences performance. Contracts that are negotiated tend to be less specific and have more room for interpretation. Performance is less likely to be exact. Yet, performance is not compromised despite the “incompleteness” of the contract. Instead, the contract's incompleteness signals trust, and potentially an ongoing relationship, between contracting parties. 3

Highly specified contractual language, in contrast, is authoritative in character. That is, precise specification reduces the interpretative space and, thereby, acts as a proxy for trust. Prior literature suggests that complete contracts, though having the intention to “align interests and diminish coordination problems,” (Eigen 2012: 17) in fact, implicitly convey the perspective that a party is uncertain about the risks involved. Eileen Chou et al. find that contributing to the lack of trust, in addition to increased specificity of language, is of course, the number of clauses contained. This suggests that, in addition to specificity, the structure of provisions within clauses is also implicit signals around contractual party behavior. 4

Fundamentally, what underpins the discussion is the relational exchange that exists between contractual parties. A contractual relationship that is devoid of trust generally exhibits inflexibility and increased verbosity. Returning to elasticity, the ability to diagnose this characteristic in contractual language is, therefore, crucial in light of computable contracts. Elasticity becomes the first marker of the implicit relationship between parties. Embedded in the language, then, is the DNA of contractual party trust and their inherent negotiation power. Provided this context, the question becomes: how can we leverage understanding of elasticity to provide better models for formalization 5 in reinsurance?

Elasticity as a diagnostic tool

In an earlier version of our paper (Ma and Galka 2022), we introduced four linguistic stretchers that fingerprint the strategic behaviors of their speakers (in this case, the drafters). Of particular interest are the epistemic stretchers. To recall, these forms of stretchers reveal a speakers’ “commitment to their claim” (Zhang 2015: 79). Epistemic stretchers reveal positionality and carry out a “subjective function of language” (Zhang 2015: 105). They act as linguistic clues that implicitly signal the preferences of contractual parties. Notably, these stretchers are capable of revealing intention and strategic uses of vagueness. Therefore, in this paper, we dive further into this realm and consider precisely how certain words behave as markers of intentionality. We continue to advance these notions by formulating a semantic fingerprint within semantic layers.

Prior to discussing our technique and framework put forward, we revisit the use of NLP and why it currently cannot account for the nuances of the reinsurance industry. More importantly, we consider that formalization in reinsurance must operate as an initial step and become the foundation for subsequent tech advancements.

Where NLP falters

General issues with NLP

NLP belongs to the broader family of statistical techniques used to analyze large troves of data. NLP, in particular, examines text-based data. Statistical methods, including machine and deep learning, are appropriate when detecting patterns in big data sets (Hao 2020). However, even the most sophisticated forms of NLP fail to understand the words they are processing. Rather, NLP merely attempts to extract from text syntactically and semantically similar structures. In effect, they are master imitators. NLP cannot interpret the reason behind the pattern. It can merely identify that a pattern exists. In other words, NLP can only provide the map; but it cannot articulate the context and histories of the map.

We previously discussed the linguistic pillars of syntax, semantics, and pragmatics. As NLP models are perceivably stochastic parrots (Bender et al. 2021), these techniques only offer the appearance of understanding. Imagine two people shipwrecked on different islands communicating via letter and a rope. A curious octopus starts to examine the squibbles going back and forth. After a while, it can skillfully predict what squibble might follow. It might even compose its own squibbles. However, at no point can the octopus actually understand the meaning of this message, even if the number of letters is vast and the topics are diverse. The octopus can only learn the linguistic form but would, nevertheless, be unable to make any sense of the text (Bender and Koller 2020). This thought experiment, designed by Emily Bender, showcases the limits of what even the most-cutting edge AI technologies can do. 6

In spite of their incredible sophistication, current AI-driven technologies are conceivably intelligent in the way a calculator might be said to be intelligent: they are both machines designed to convert input into output in ways that humans choose to interpret as meaningful. 7 When dealing with especially complex, subtle, and nuanced legal language, such as reinsurance clauses, the elaborate use of statistical patterns cannot itself lay the initial groundwork. Only by first translating the legal reinsurance language into a formal structure with clear patterns, can we then teach machines to perform such tasks.

Why human intelligence is necessary and NLP alone cannot be starting point for reinsurance

While the reinsurance market prides itself in linguistic diversity, no single organization has developed a comprehensive library of all types of clauses. However, two main administrators, London Market Association (LMA) in the United Kingdom and Brokers & Reinsurance Markets Association (BRMA) in the United States, have been regarded as standard-setting institutions. LMA drafts most of the clauses in the market, but their database is available solely on a paid subscription basis. The BRMA database, though freely available, features clauses volunteered by their members. This has enabled significant irregularities in the currency and comprehensiveness of the clauses available to the public.

Moreover, new types of reinsurance clauses are crafted every year without any mechanism to evaluate or verify the clarity of the wording. Consequently, the quality of the clause is often challenged only when disputes arise. Historically, parties would only be issued a brief summary of the main terms of the reinsurance agreement, known as the “placing slip,” or simply the “slip.” The complete reinsurance contract was issued as a second stage of the negotiation process—often with delays of over a year—to replace the slip (PRICL Project Group 2019). While the practice of “terms to be agreed later” is no longer common, the reinsurance industry is still largely relationship-driven; the element of trust is built into the final legal arrangement. In such an environment, where data is scarce and the relationship between the form and meaning of terms is not always clear, we must first focus on establishing a comprehensive reinsurance knowledge base.

Returning to our curious octopus, it would be simply unwise to expect the octopus to define the types of communication between the two shipwrecked parties. In a similar manner, using NLP to assign and compute an elasticity score, without sufficient understanding of the underlying nuance and intentions behind the clause, would be unsound. By contrast, a model founded on human expertise is required. In the model we defined, we parse the components of the clauses into digestible parameters. These parameters are then weighed against epistemic stretchers. In effect, we ask: are the rules governing each of these components known? This establishes a blueprint, or otherwise, a structured knowledge model. 8 For our NLP octopus, it can serve as a guide to help decipher completely new squibbles in the future. While the model would still be unable to understand the context behind the information received, it, nonetheless, may be able to follow the structure of the input and assign a value to it.

Elasticity as a metric: Between trust and precision

We had previously discussed the market dynamics and its influence on the quality of reinsurance clauses. In conversation with reinsurance practitioners, the key observation described during negotiations is the extent of trust between contractual parties. That is, even the most elastic language might not be challenged for years if there is a strong working relationship between the parties. Any identifiable vagueness could typically be resolved in an amicable manner. In most circumstances, the vagueness is, in fact, not unknown. It is simply implicit knowledge.

We suggest that, even under such auspicious settings, the industry can still benefit from explicit articulation of their intentions. This allows for more robust and durable contracts. The elasticity analysis at the design stage can provide parties with an insight which supports informed decision making. This empowers parties to clearly distinguish between intentional versus unintentional vagueness in a clause. That is, there may be increased awareness of elastic language used either strategically, or in the furtherance of the parties’ relationship, as opposed to elastic language as a consequence of preserving the status quo.

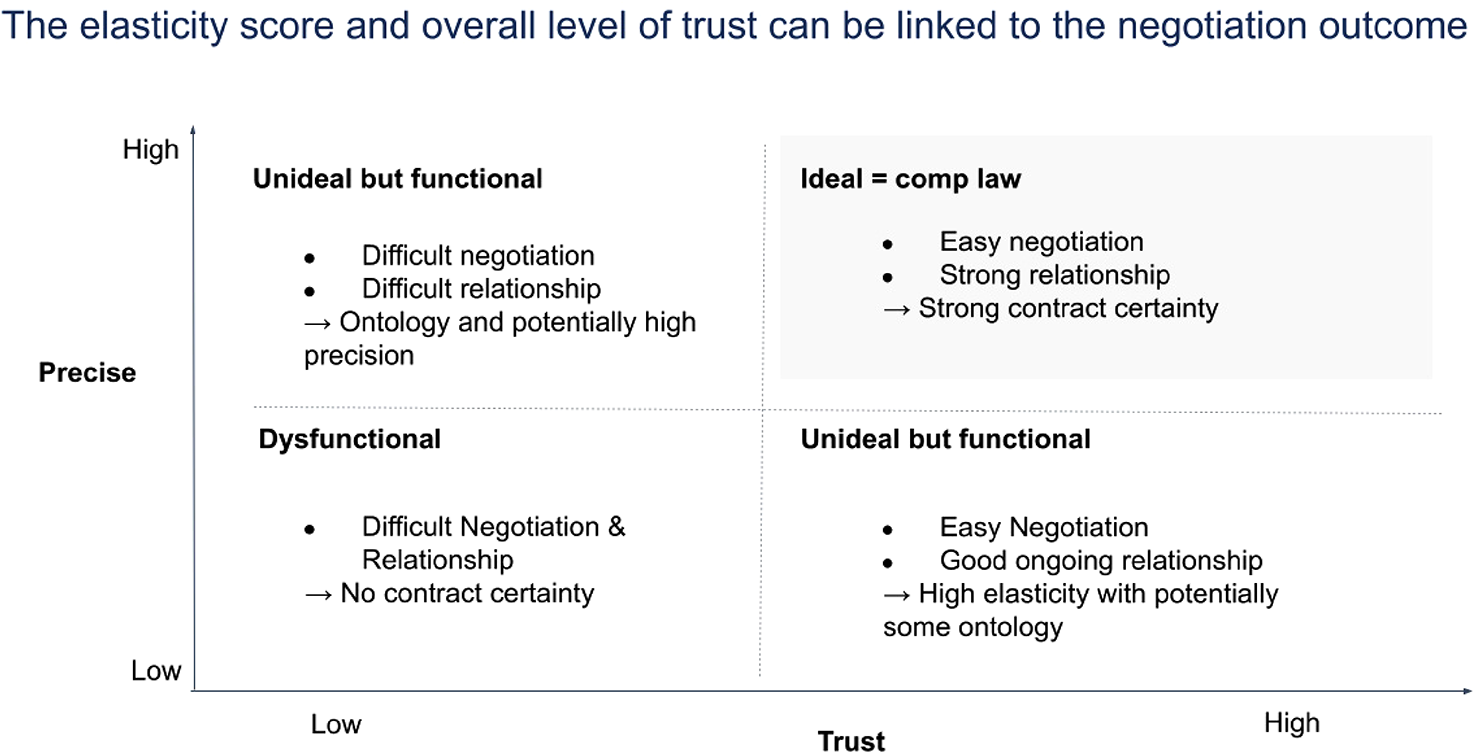

Similarly, in The Language of the Law, David Mellinkoff describes the treatment of precision amongst the legal community. Despite legal language being a “viscous sea of verbiage,” (Mellinkoff 1963) lawyers frequently argue that legal language is necessary because it is precise. Interestingly, what Mellinkoff notes is that the notion of precision is not equivalent to “exact.” Instead, precise refers to “exactly the same way.” This means that the legal language embodies an element of ritualism and is not necessarily intended to be specific. This has important implications for reinsurance wording. Mellinkoff's distinction suggests that prior constructions of reinsurance clauses have argued for precision without acknowledging what precision means. Alternatively, elasticity is capable of testing whether the language of the clause is “exact” or “exactly the same way.” With the former, we enable increased clarity of meaning that can endure past the specific contractual parties involved in the negotiation, and maintain the longevity of the overall relationship between the reinsurer and the company. In effect, parties can still opt for elastic language but, at minimum, there is an explicit understanding of how the vagueness of the language can account for the risks the parties are willing to bear.

Below we represent the relationship between trust and precision through the lens of elasticity. We define “precision” here to mean “exactness” in the specification of components within the clause. Our assertion is that, presently, an increase in the precision of the clause has a correlative decrease in the extent of trust between contractual parties. We argue that this may be a result of misrepresenting precision as “exactly the same way,” as opposed to interpreting precision as “exact.” Accordingly, the current state of reinsurance wording is “unideal but functional.” On the other hand, we suggest that increased specification (or, increased exactness) would foster stronger relationships between contractual parties. This is because the reason behind the elasticity present is taken into account.

Equally, we distinguish ourselves from Chou et al.'s understanding of and argument around complete contracts. To recall, Chou et al. observed that completeness, defined as those with highly specified language and lengthy clauses, signals a lack of trust between parties. We believe this is, again, owed to a perception of specification as definitive and intention to convolute. Alternatively, we suggest that increased specification of clause components better clarifies the contractual relationship; it places at the forefront implicit information explicitly. This method enables a source of a reference, a lineage of how rules governing the terms of a contract were established and have evolved with time.

Observations from data analysis: “Access to Records” as use case

To recall from the methodology of our prior paper, we began our empirical analysis by unpacking the discussion described by the Project Group on Principles of Reinsurance Contract Law (PRICL) (Ma and Galka 2022: 16). PRICL also contained a sample of reinsurance wording. While PRICL provides an extensive background on the use and history of reinsurance clauses, we felt it was necessary to engage with common reinsurance wording used in practice. In particular, we limited our initial data sample to “Access to Records” clauses. These clauses, while not necessarily highly litigated, are incredibly ubiquitous and have substantive significance. Consequently, we chose to focus on open-source “Access to Records” clauses published by BRMA. As discussed, BRMA is the largest US reinsurance association with the aims of elevating contract quality and improving the efficiency of reinsurance contracting. The clauses are made available to the public upon two conditions: (i) if it is substantially different from any other BRMA clause and (ii) at the time of its publication, is reported by at least two BRMA members of their appearance in reinsurance contracts. Their library of clause data on “Access to Records” was last updated in 2016, providing a relatively current sample set. 9

The relevance of “Access to Records’’ clauses to reinsurance agreements is paramount. It regulates the terms and conditions of the reinsurer's right to access detailed insurer data in connection to the contractual relationship (e.g. for the reinsurer to verify premiums). The set of 30 PRICL and BRMA “Access to Records” clauses were evaluated under and tested against stringent expert scrutiny. Our observations of both model and market clauses revealed several fascinating patterns. These were mapped and formed the foundation of our own elasticity framework. We describe in further detail this framework below.

Modeling elasticity: Developing the semantic fingerprint and elasticity score

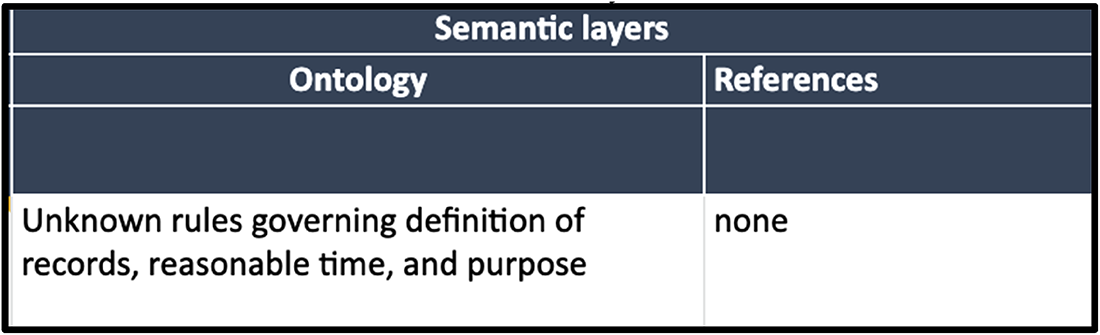

As discussed, reinsurance clauses contain linguistic fingerprints that help reveal the latent relationship between contractual parties. We found that while legal language may appear opaque, when deconstructed into constituent parts, a structure emerges from the complexity. In our proposed model, we decompose “Access to Records” clauses into their respective components and the layers that underlie these components. We arrived then at our general framework: (i) Semantic Phrases = {Who, What, When, Scope, Purpose}; and (ii) Semantic Layers = {Ontology + References}. The Semantic Phrases coupled with Semantic Layers form the basis of the Semantic Fingerprint of a given clause.

Consider for example the following “Access to Records” clause from BRMA:

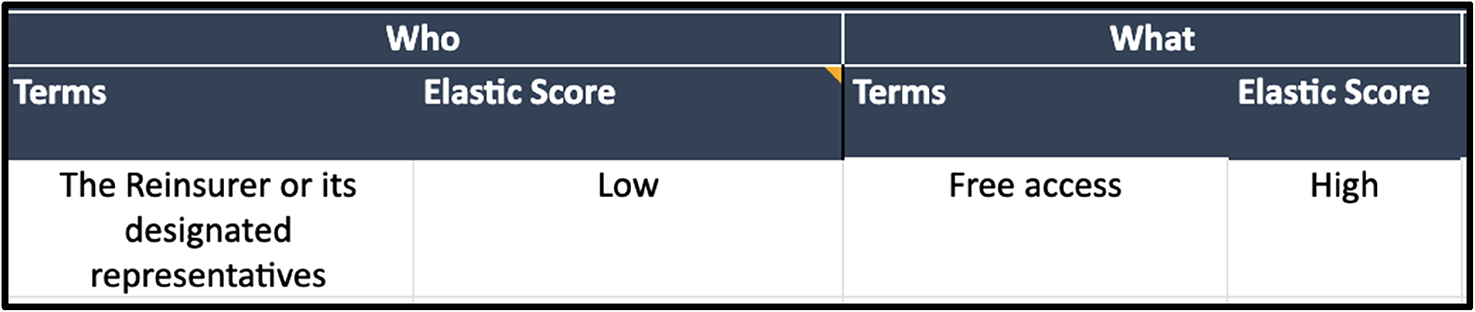

Applying our framework, we first parsed the clause into Semantic Phrases. In its simplest form, the clause was distilled into its core linguistic typology: subject, verb, and object. From there, we focused on the subject and object, and their relevant qualifiers. These qualifiers are helpful in identifying the information contractual parties would like explicitly known.

Delving further, we asked in our model whether each of the specific components had more information surrounding their definitions. For example, what qualifies as a “designated representative”? Or, what are the limits of “free” in relation to “access”?

The answers to these questions are then categorized in one of two ways: (1) Ontology or (2) Reference. Ontology is understood as the explicit “rules” that govern each of the Semantic Phrases. For example, “records” is limited to either the types of documents and materials (i.e. books, papers), or a specific form (i.e. digital, analog). Reference is understood as information that may be connected to how the Semantic Phrase is defined. For example, “records” is defined “to be consistent with the internal policies of the Company.” It could be inferred that the rules qualifying the types of records a reinsurer may access is specific to a definition referenced elsewhere. While we relied on the reinsurance expertise from collaborators of our paper, we anticipate that a more rigorous methodology is required to tackle future applications of our model.

Below is an example of the Semantic Layers relevant to BRMA 1A:

From the framework, we may be able to gather an elasticity score. As elasticity attempts to hone in on the reason behind vagueness, the elasticity score is determined by the extent of specificity in a given Semantic Phrase and Layer. In the example above, we note that none of the qualifiers in the Semantic Phrases have further explicit definition (e.g. no parameters given to “free”).

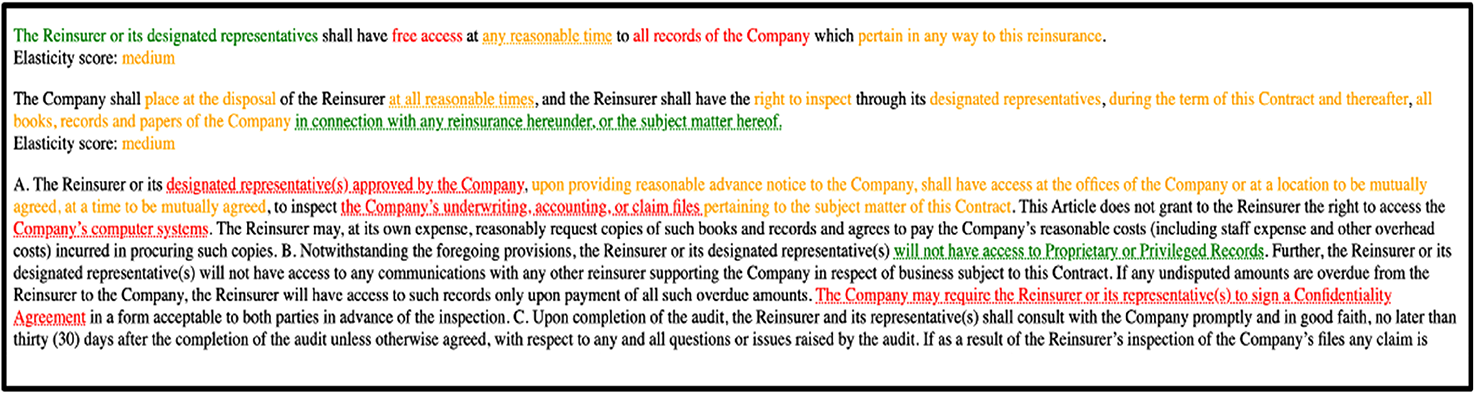

This immediately signals that elasticity is present. Evidently, the presence of elasticity is not in itself necessarily cause for concern, nor definitive of the score. Rather, the elasticity score is derived by a secondary analysis as to whether the presence of elasticity correlates with intentional (strategic) vagueness, or merely that implicit knowledge has not been communicated explicitly. In the example below, we distinguish between “low” and “high” elasticity on the premise of strategic risk, provided that “free” is the substantive qualifier on which the clause hinges.

We also seek to clarify that some forms of elasticity are not generally elastic. For instance, to the contract lawyer, “reasonable” is not necessarily vague. There are typically existing principles that govern what may be considered within the bounds of “reasonableness.” Or, the phrase “in any way to this reinsurance,” to the Reinsurer is rather clear. That is, the records in question must be associated with the terms of the reinsurance contract.

However, diagnosing elasticity is not merely intended to assess clarity and/or readability. Measuring elasticity attempts to reveal the underlying goals behind vagueness and encourage a shift towards “precision as exact.” Currently, contracts are drafted with the lens that the relationship between the specific parties sufficiently governs the overarching relationship between the Reinsurer and the Company. Reinsurance contracts are then limited in their robustness, adaptability, and accessibility. Alternatively, by layering implicit information explicitly, we may be able to develop contracts that account for future changes in contractual relationships.

Diagnosing elasticity: The “Stretch Factor” prototype

For the purpose of this paper, we sought to demonstrate how we envision the tool to diagnose elasticity. With the technical support of our Computable Contracts Developer, William O’Hanley, we built a prototype of our diagnostic tool, “Stretch Factor,” grounded in our elasticity framework. Below is a sample screen capture of the tool: 10

Notably, we translated our low, medium, and high elasticity scores to a corresponding traffic light rating system: green, orange, and red. The above BRMA 1A “Access to Records” clause may be identifiable as the first clause in the codified tool. Therefore, not only would the diagnostic tool act as a mechanism for identifying areas of intentional and strategic vagueness, but also would aim to highlight areas where context may be formalized to facilitate computable contracts implementation. Furthermore, we argue that, in articulating the reason behind elasticity and contractual wording in the longer term, would not only be more precise, but also capable of acting as a lens into party behavior.

We hope to use the Stretch Factor as a jumping point for next steps in how we may be able to apply our framework. We consider that scaling up may be an option, applying our elasticity framework to more clauses. This will allow us to assess whether (1) our framework for elasticity is sufficiently transferable across multiple reinsurance clauses and (2) how might the model adapt to more complex contractual wording. In order to determine the former, we consider first applying the framework to “Confidentiality” clauses. These clauses frequently relate with “Access to Records” clauses. Moreover, they belong to the library of clauses that are rather consistent across reinsurance contracts. These qualities provide a strong test case for our initial experiments on the viability of our model. We will then be able to establish an early metric on elasticity as a quantifiable score for contract drafting.

In the short term, we consider the use of state-of-the-art neural models, such as OpenAI's GPT-4, as a testing ground on the impact of using elasticity as the underlying structure. Results and observations from testing on large language models (LLMs) will provide us information on not only the generalizability of our framework, but also its significance relative to risk. Moreover, we may be able to gather deeper insights into contractual drafting processes. For example, in what circumstances could we imagine drafting a low elasticity clause? Is there a tendency to prefer medium elasticity as the default drafting standard? More specifically, is there a difference in the uses of elasticity when used in the clauses and subjects which are well-established versus new, emerging risks which are simply not tested yet, for example, Cyber Exclusions? We anticipate that the exponential advancements in LLMs will enable a suite of analytical tools with functionalities predicated on risk management and strategic assessment. In effect, we see a form of automated redlining or guided commentary that will flag and/or provide a recommendation on the use of elastic language, built against underwriting guidelines.

Furthermore, this may be a path to providing stronger foundations and expert intervention to computable reinsurance contracts. In our research, we have begun to identify that elasticity is also dependent on subject matter expertise. That is, the extent of stretchiness relies on the specific use of words in context. We allude to this in the above discussion on “terms of art.” As a practical next step, we are seeking to gather specialized technical knowledge and historical experience from underwriters and contract experts. This will allow us to determine whether this is indeed a symptom of elasticity or whether there is indeed a clear definition understood by relevant drafters.

We imagine that aggregating their expertise will allow us to work towards a quantitatively informed model. We take inspiration from the notion of an elasticity coefficient in the field of economics, and aspire to develop an elasticity coefficient for reinsurance contracting. In economics, elasticity refers to the price elasticity, otherwise a measure of whether a change in price would have an impact on the quantity demanded of a good. In a similar light, we are interested, in the longer term, in providing a measure on how the use of certain contractual wording would have an impact on contractual outcomes. The complexity, however, is the ability to quantify both contractual outcomes and uses of policy wording. This will necessarily require the use of proxy variables, which, if not done with care, could invoke more harm than benefit.

Nevertheless, in tandem with exploring contractual party dynamics, an elasticity coefficient would provide a more contextualized understanding of the internal workings around drafting. We consider the analogy of a “consult” in the area of medicine. Frequently, doctors hope to corroborate their medical diagnoses with other doctors prior to informing their patients. With the advent of computational and data-driven technologies, doctors are now able to conduct “consults” as medical information on diagnoses is aggregated as data. This increases both the efficiency and effectiveness of medical diagnoses. Rather than receiving the expert advice of one or two colleagues, doctors are now capable of accessing broad medical expertise at their fingertips. We see a similar potential for our model, providing expert knowledge on contractual wording to underwriters, and reinsurance generally.

As we venture further into the realm of scalability, determining our model's behavior to more intricate, potentially lengthy, clauses are a logical next step. The early tests on clauses beyond “Access to Records” reveal the potential to scale our framework in (re)insurance contracts from the clause to document level. We envision that the Semantic Framework will be further extended as to include more nuanced aspects in key clauses that define the coverage of the underlying risk transfer. This requires, to an extent, clear understanding of the “breaking points” (i.e. limits) of the model, as well as the structure of the contract at the document level. We consider that in order to evaluate the viability of elasticity as a marker for contractual behavior, we must also be able to unpack the relationship between clauses.

In reinsurance, it is not uncommon that coverage related clauses are often dispersed either across various sections of the contract or worse, across different documents. For example, are there hierarchies amongst clauses? Also, what is the intention behind elaborate clauses with multiple nested provisions? The answer to these questions would suggest that elasticity is relative depending on the hierarchical structure of contractual terms. A clause may be highly elastic, but if its general effect on the contractual outcomes is low, it may not raise any flags.

We see our research as capable of capturing insights from legacy contracts as well as enabling the current and future drafting processes for computable contracts. We also encourage future collaborations in the direction of relational contracting, assessing whether findings from reinsurance may be more broadly applicable in complex, multistakeholder agreements. Ultimately, our hope is that we may be able to introduce a complementary perspective that will contribute to the ongoing and fruitful endeavors in the broader space of computational law and computable contracts.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.