Abstract

The participants of the public–private partnership projects have different parts in developing the concessions, hence different perspectives and goals. Besides, the public–private partnership concession agreement has many parameters and components, and a change in one component will have a considerable impact on other components. Thus, determining the optimal value for different concession parameters by providing a series of feasible contribution options was investigated in this paper using two different multi-objective optimization models: genetic algorithm and Thompson sampling. Two case studies (the US I-495 and the I-4 Ultimate) were used to construct and validate the results of the model. The model results showed that the socio-economic sustainability performance increases as the private equity increases and the public equity decreases. The results also showed that the socio-economic sustainability performance increases as the concession price (user-fee) decreases. Having these contribution options could facilitate the decision-making process for both the public and private parties. The genetic algorithm model obtained faster optimization results when compared to the Thompson sampling model; however, the Thompson sampling obtained better results. Moreover, the use of the model could improve the socio-economic sustainability performance of the public–private partnership projects.

Keywords

Introduction

The need for mega infrastructure has increased over the last few decades due to the dramatically increasing population living in big cities. Simultaneously, it may be hard for available infrastructure funds to meet the public needs with the growing demand (Azagew and Worku, 2020; Rodríguez-Pose and Griffiths, 2021). Building new infrastructures and maintaining existing others face insufficient public funds globally (Yun et al., 2009). Hence, the adoption of public–private partnership (PPP) agreements may be necessary to overcome these challenges. PPPs can overcome the limitations that the public party might have to deliver services to the public. Not only that, but also redirect available public funds into more exceptional achievements to the nation. The PPP implementations have been increasing over the last few years, which indicate the importance of such contracts and approaches to the development of societies (PPIAF, 2016).

A PPP may be seen as a constructed agreement involving some parties, a public party, and private parties to construct, renovate, maintain, manage, or operate a project that serves the public and private needs (Pereira et al., 2021; Pukhova et al., 2021). Some refer to it as a method for project funding, which can help overcome the public party's economic limitations via direct capital investment from the private parties in service establishment (Alinaitwe and Ayesiga, 2013). PPP was mainly observed to tackle the public budget burden in delivering the needed social services and infrastructures (Li et al., 2005). Besides, these agreements aim to share risks and investments between the collaborated parties, significantly benefiting each party's achievements. Nevertheless, PPP has also offered the chance for private sectors to contribute to long-term agreements through the public sectors to sell their services and make profits for the long run, especially with the stable demand for public services.

On the other hand, designing a concession for PPP agreements is a complicated process due to the number of variables that need to be considered, affecting all participants in the concession agreement. The concession has many parameters and components, and a change in one component will considerably impact the other components. The determination of fair values of concession components needs to be based on mutual benefits between the concession participants. The concession participants have different parts in developing the concession, hence different perspectives and goals. Therefore, the concession design needs to be constructed to balance the involved parties' interests to ensure smooth and sustainable development. One of the most significant aspects in successfully implementing PPP schemes is the adequate identification and balance between the involved parties' interests (Boyer and Newcomer, 2015; Gordon et al., 2013; Gupta et al., 2013; Hwang et al., 2013; Wang, 2015; Wibowo and Alfen, 2015). Thus, the present study aimed to determine the optimal values of different concession parameters (concession period, concession price (user-fee), government subsidy, and capital structure (in the forms of public and private equities)) when they are dependent on each other by providing a series of feasible combination options. Then, a socio-economic sustainability performance indicator was calculated for each combination option. It is anticipated that having these combination options could facilitate the decision-making process for both the public and private parties, as recently opined in Radzicki (2020). Another aim is to compare between genetic algorithm (GA) and Thompson sampling (TS) models.

Literature review

Many previous studies highlighted the importance of optimizing different concessionary components (Carbonara et al., 2014; Chen et al., 2012; Chou et al., 2012; Jasiukevičius and Vasiliauskaitė, 2012; Ke et al., 2008; Kurniawan et al., 2015; Ng et al., 2007a, 2007b; Niu and Zhang, 2013; Sarmento and Renneboog, 2016; Sharma et al., 2010; Wang, 2015; Wang and Liu, 2015; Xu et al., 2012; Yun et al., 2009). These attempts have been conducted to optimize one aspect or another in the PPP implementation development. However, most of the studies focused only on one or two variables to optimize, while PPP projects have many variables, which differ from one another (Huang et al., 2021; Li and Strahan, 2021). Besides, optimizing one variable alone may reduce the optimal values for the other variables due to the interdependencies among the concession components. This section outlines the general research gaps based on the available literature to justify further the current study's aim of evaluating the effects and interplay of several interdependent socio-economic variables, which is important in giving a holistic perspective regarding effective long-term PPP.

Optimizing the concession period and price

The main aim of selecting the concession period and price is to ensure a suitable revenue for private sectors to recover their capital investment (Shen et al., 2002). In most PPP cases, a 20- to 40-year concession period guarantees an adequate cash flow for the development costs repayment. This period is dependent on some economic and project factors, including the project type, concession price (user-fee), and the potential generated revenue, and therefore, it can be seen as a complicated decision-making process (Ullah et al., 2016). In most cases, private sectors may require long concession periods to reap enough revenue by collecting more user payments. In contrast, the public sector may require shorter durations to protect the public's interest (Tariq and Zhang, 2021).

Practically speaking, the public party may determine the concession period before assigning the project to private parties (Zhang, 2009). The public parties may be focusing on maximizing social welfare, while the private parties may be focusing on maximizing their profits. Therefore, the decision for the concession period may be a complicated process (Liu et al., 2020; Silaghi and Sarkar, 2021). For example, by minimizing the concession period, public parties may have to issue large subsidies or large concession prices, hence increasing their initial capital expenses or decreasing the level of social welfare. Therefore, balancing the levels of the concession period, price, and subsidies may be a critical decision process. From the private sector's perspective, collecting more profits could be accomplished with either a high concession price and a low demand volume or a low concession price and a high demand volume. Therefore, a conflict of interest between the involved parties may be observed. Hence, all parties should work together to balance their interests in the concession agreement.

Concession price (user-fee), on the other hand, should be selected carefully by taking the public interest into consideration (Singh, 2021). The concession price is typically selected based on the society's average per capita income to meet the public needs while ensuring an adequate users flow to increase the cash flow for generating the project's revenue. It can be clear that the concession period and the concession price have an inverse relationship.

Many researchers have investigated modeling the concession period via different approaches, including the net present value (NPV) calculations (Shen et al., 2002; Wu et al., 2011), game theories (Peng et al., 2014: 201; Shen and Wu, 2005; Yang et al., 2007), besides simulation modeling (Carbonara et al., 2014; Ng et al., 2007a, 2007b; Ngee et al., 1997; Scandizzo and Ventura, 2010; Yu and Lam, 2013; Zhang, 2009). However, the process of choosing the ideal concession period and price is complex, and it depends on several concession factors and components that may differ from one project to another. The concession price should be adequately large to cover the private party's investment in short concession periods, and at the same time, it should be small enough to preserve the public's welfare and ensure adequate user flow (Matsumoto et al., 2021). Alternatively, the concession period value should be adequately long to ensure the payback of the private's investments plus an adequate profit is accomplished with a low concession price, and at the same time, it should be short enough to ensure that the public's interests and social welfare are protected. Determining the appropriate values of the concession period and price will affect other related factors and concessionary items in the PPP contract. For instance, reaching an optimal value for the concession period will reduce the optimal value of the other concession factors. Therefore, a tool that considers several PPP concession factors simultaneously is needed due to the conflicting interests between the concession components.

Optimizing the capital structure

The capital structure can be seen in the project's financing combination between debt and equity, indicating the total capital cost and the project's value. Optimizing the capital structure can have significant benefits, minimizing the capital cost and maximizing the project's value. Public and private parties can obtain an agreed-upon equity level in the PPP project's capital structure. Public equity differs from the public subsidy as it is a public investment in the project. The public party acts as an investor (equity holder) instead of a facilitator issuing subsidies. A public party's participation in the concession's capital structure as an equity holder should be large enough to attract more private competitors and simultaneously raise the project's debt capacity. Nevertheless, it should be small enough to mitigate the likely risks associated with the given project and preserve sustainable social welfare. Public and private sectors may agree on an adequate equity level that satisfies each involved party (e.g. equity holders, the public sector, and the lenders). Determining the level of equity is critical in defining the project's capital structure. Nevertheless, it is a challenging task due to the different views and requirements of the involved parties.

In general, financial models are used to create deterministic values for the appropriate level of equity for private parties (Bakatjan et al., 2003; Dias and Ioannou, 1995). However, a recent study suggested that using these financial models to create such deterministic values may lack uncertainties associated with the project (Quitoras et al., 2021). Hence, deciding the adequate level of equity should not be based on these predetermined values as it may lead to unexpected loses and risks. Therefore, the adequate capital structure determinations should be based on feasible options for the participants to choose the adequate values. Many quantitative financial studies have been conducted in the field to examine the appropriate capital structure values. For example, some researchers investigated adequate capital structures using the capital asset price method (Dias and Ioannou, 1995), the linear programming method (Bakatjan et al., 2003), and the Monte Carlo simulation method (Zhang, 2005). Other researchers studied economic and financial feasibility (Chang and Chen, 2001; Ho and Liu, 2002; Ranasinghe, 1996; Tiong and Alum, 1997). It is noteworthy to mention that the Modigliani–Miller theory has been used for several decades for assessing the framework of capital cost and capital structure. However, one of its limitations is the assumption that all financial institutions and flows are insoluble, which has given rise to modified ones such as the Brusov–Filatova–Orekhova theory in the late 2000s (Brusov et al., 2021).

The ideal sharing ratio can be enhanced when all the involved parties balance their interests respectfully to their contribution to the actual contract. The public parties seek to smoothly implement the project sustainably while preserving public funds as much as possible; private parties’ interests must be met to ensure the continuous progress of PPP projects. However, optimizing the capital structure alone can negatively affect the other concession components, such as the concession period and price, due to the conflicting interests between the concession components.

Optimizing the public subsidy

Most of the projects operated under the PPP agreements make low profits due to the considerable current and future risks associated with such projects' long lifespan. In this case, governments or public sectors should provide adequate financial subsidies for such poor profitability projects to make the project economically feasible for private sectors. These subsidies are essential due to such low profitability projects' promising benefits to society's sustainable development. In other words, from the private sector's perspective, the needed infrastructure projects for social development may not see the light if the projects have no potential return on investment. Therefore, financial support from the public parties, such as subsidies and guarantees, is essential to attract private parties due to the PPP long lifespan and the risks associated with its uncertainties (Chen et al., 2012; Khmel and Zhao, 2016; Kokkaew and Wipulanusat, 2014; Shaoul et al., 2012).

The fundamental goal of public parties is maximizing social welfare and adequately delivering the required infrastructures. It can be clear that public subsidies have an inverse relationship with the concession period and the concession price (Jin et al., 2020). The more value of subsidies issued by the public parties to the concession, the less period and price the concession will require to pay back its investments. Therefore, government subsidies may act as an effective tool to decrease the concession period and price. Alternatively, public parties can reduce their initial financial contribution to the project by elongating the concession period or increasing the concession price.

It can be clear that the public parties' subsidies are also used to attract more private parties and enhance their competitiveness. However, preserving public funds and budget is as critical as attracting the participation of private sectors. Therefore, a tool that can balance all the involved parties' interests is vital in PPPs' scope.

In general, subsidies can be seen as a risk-sharing mechanism to balance both parties' interests (Wibowo et al., 2012). However, determining the adequate amount of subsidy is the challenging part. The subsidy should be large enough to cover the potential losses that private sectors may face and act as a leverage tool for the public parties to increase such participation and competition. At the same time, it should be small enough to preserve the public budget and social welfare. Determining the right amount of financial subsidy will affect other related factors in the PPP contract. For instance, reaching an optimal amount of government subsidy will reduce the optimal value of other factors. Therefore, a tool that considers several PPP concession factors is needed due to the conflicting interests between the concession factors.

Optimizing the socio-economic sustainability performance

PPP projects are usually mega projects in their nature and are constructed over a very long lifespan; hence, the concept of sustainability performance should be considered when awarding such projects. Usually, the most focused dimension when dealing with PPP projects is the economic dimension, where all shareholders emphasize the project's financial sustainability. This is for them to ensure that their initial capital investment is paid back with the expected profits. PPP can deliver infrastructures to achieve sustainable development growth from the sustainable socio-economic perspective when governments do not have enough funds. This may be very helpful, especially for developing countries, to develop sustainable growth by utilizing private investments and capital. Besides, PPP can also be seen as new business prospects for the private parties to invest and profit. Hence, private sectors may have the ability to improve their sustainable economic development by undertaking PPP projects (Owusu-Manu et al., 2020). On the other hand, social welfare should be protected when developing concession agreements. This can be accomplished by lowering the concession price (user-fee), shortening the concession period, or reducing the government subsidy.

However, there is a clear need for quantitative methods to address PPP projects' socio-economic sustainability performance. These quantitative methods need to take all the PPP participants' contributions and expected outcomes into account to examine and improve the socio-economic performance outcomes because the participant's contributions to the PPP projects substantially impact the concession and the socio-economic sustainability performance (Hussain et al., 2022, Nkurunziza, 2021). Every participant in the PPP agreement has different goals and expectations. Hence, taking these expectations into account and applying them to the long-term agreement may result in better socio-economic sustainability performance for the PPP projects.

Methodology

Model construction

The model construction is based on the discounted cash flow (DCF) method. With the DCF, the investment assessment from both the public and private parties is based on potential costs and revenues. The future projection of cash flows is converted to today's value to assess both parties' investments. Therefore, the following formulas are utilized to construct the model.

Total investment

The PPP project's total investment may be described as the summation of the debt fund and the equity fund.

The following formulas can calculate the ratios of public and private investment:

Cash outflow

The total cash outflow during the project can be separated into costs due to the construction and cost during the operational year. The total construction cash outflow (TCCO) is the summation of the estimated cost for construction (CC), an increase in cost due to inflation (EC), and the capital interest (IC):

In this work, the CC all through the construction year will be assumed to be the same; therefore,

rc = capitalized interest rate on debt, rf = inflation rate at y year.

The TCCO can be further simplified into the private sector's construction cost and the public sector's construction cost. This can be determined by calculating their equities during the construction phase:

Taxation. The taxation can be considered as the combination of the tax on sales and the income tax and can be calculated by the following equation:

Cash inflow

The total cash inflow (TCI) can be generated from the project's revenue. For example, the TCI for a toll-based PPP project is generated from public usage's toll revenue. The TCI during an operational year depends on the demand for public usage and the concession price. Hence, the total revenue generated in an operational year can be calculated by the following formula:

Debt service coverage ratio

Debt service coverage ratio (DSCR) is a financial indicator used by loan lenders to measure the investment's ability to recover the debt. In this work, DSCR is calculated by computing the average of the DSCR during the loan repayment period, and the following formula can compute it:

Formulation of the objectives function

This work presents a multi-objective function to maximize private and public interests. The objectives function is defined as follows:

1. Maximization of the investment of the private sector using the NPV. NPV has proven to be a financial indicator of the PPP project's profitability regarding private equity. NPV can be calculated using the following formula:

2. Maximization of public interest. While private investors focus on making profits, the public party's priority is protecting public interests, including the social cost of public service usage and the amount of funds invested during the operational year. Therefore, to maximize the public interest, public funds are minimized:

3. Minimization of the concession period. The concession period should be short enough to ensure that the public's interests are met and social welfare is protected. A minimum concession period with a higher NPV can also attract private investors to venture into PPP.

4. Minimization of the concession price. The concession price should be minimized to ensure meeting the public needs and, at the same time, ensure an adequate user-flow to increase the cash flow for generating the project's revenue.

In summary, the objective functions are as follows:

Maximization of NPV, Minimization of public expenditure, Minimization of the concession period, Minimization of concession price,

Therefore, we can define the socio-economic sustainability indicator by balancing the objectives' functions. The soco-economic sustainability indicator is a value obtained using a weighted summation of the objectives' functions. Weighting is introduced to prioritize any objective function. In this paper, we define the socio-economic sustainability indicator as follows:

The summation of the weights is equal to 1:

Assumptions

The assessments of PPP concessions involve projecting the future, following several assumptions and projections. The validation of the model is dependent on the correctness of the assumptions. The following assumptions are made in the model formulation:

The total investment is merely from the loan and the equity. The loan is assumed to be obtained from a source with a capitalized interest during the construction and a current interest rate during the operational year. The equity fund is invested at the time, t = 0. The concession price is considered the average toll charge for all users, increasing throughout the contract period due to inflation. There is no depreciation on the project all through the contract period. An annual inflation rate of 1% is assumed throughout the contract period.

The multi-objective optimization model

Due to the several objectives and conflicting interests between the private and public sectors involved in the PPP contracts, the ideal way to simultaneously address and optimize these objectives is through a multi-objective optimization (MOO) model. MOO techniques have been widely used in the optimization research area nowadays due to their applicability to real-world problems.

Conducting such optimizations to several variables may acquire an optimum solution set, described as the Pareto optimal solutions, rather than a single optimal solution (Deb, 2003). Developing the set of solutions will not give an optimal solution to each of the objectives; instead, there will be some trade-offs between the objectives' optimal values. The goal here is to find the optimal solutions considering the trade-offs between the objective values. Therefore, decision-makers will have the ability to select a suitable set of solutions depending on the ideal level of trade-offs between the objectives based on the importance of each concessionary item.

The traditional solution to a multi-optimization problem involves transforming the multi-objective functions into single objective functions by weighting the objective functions; this pays significant attention to minimizing cost using the global search failing to balance other decision variables.

The multi-objective GA and TS are introduced to solve the multi-objective programming problem in this work. The goal of both algorithms is to compute the parent optimal set, which is the non-dominated optimal solution. Both approaches have been used widely in the literature and have proven to be effective for providing solutions to complex systems that deal with trade-offs. These algorithms aim to compute the parent optimal set, which is the non-dominated optimal solution.

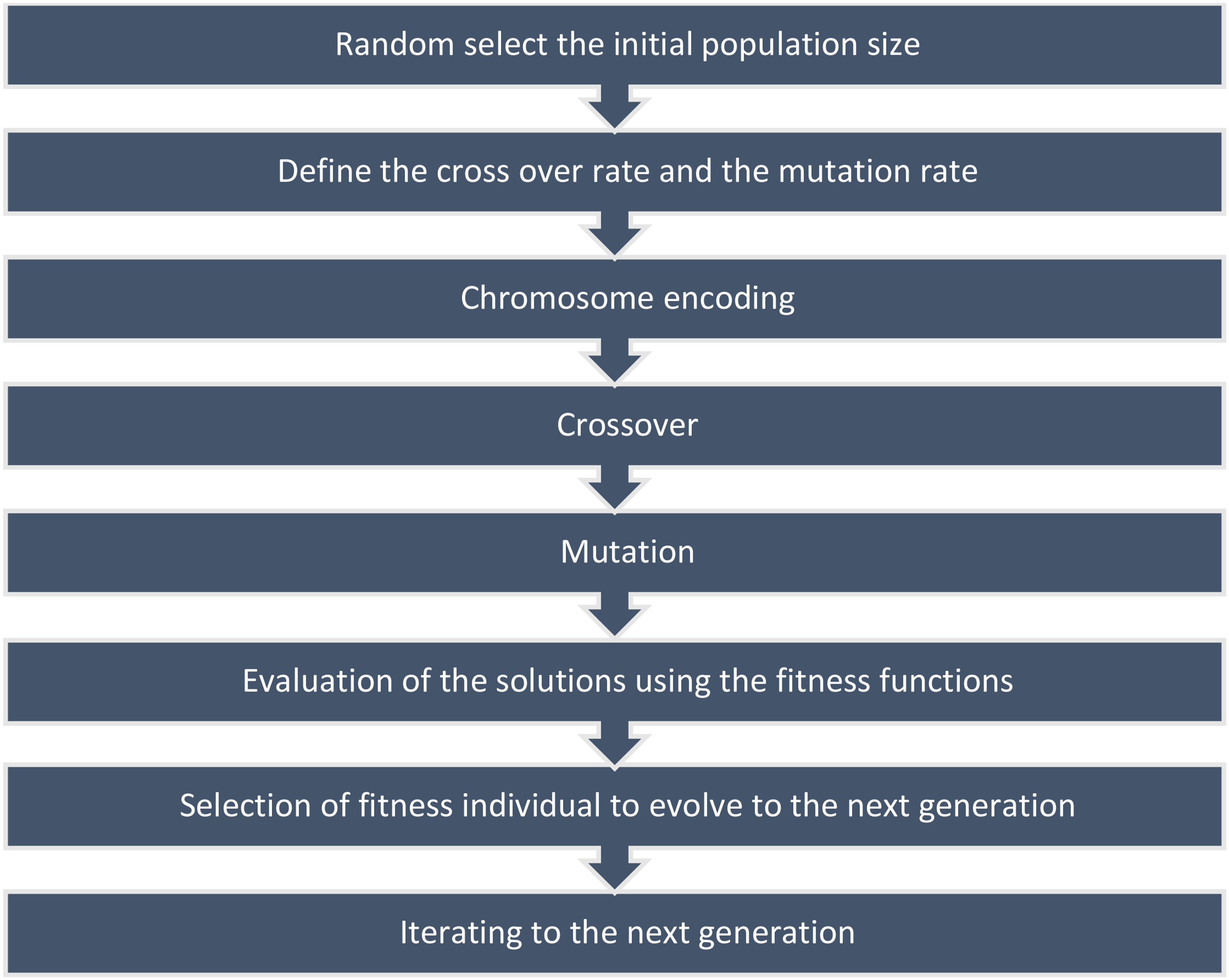

The multi-objective GA works similarly to the conventional GA, including the chromosome's formation, the cross-over operations, mutations, and the selection process. However, the significant difference is in the selection process, which involves selecting Pareto dominance by selecting the fittest individual after considering all the objective functions. The structure of the GA multi-objective functions can be seen in Figure 1.

Genetic algorithm multi-objective optimization structure.

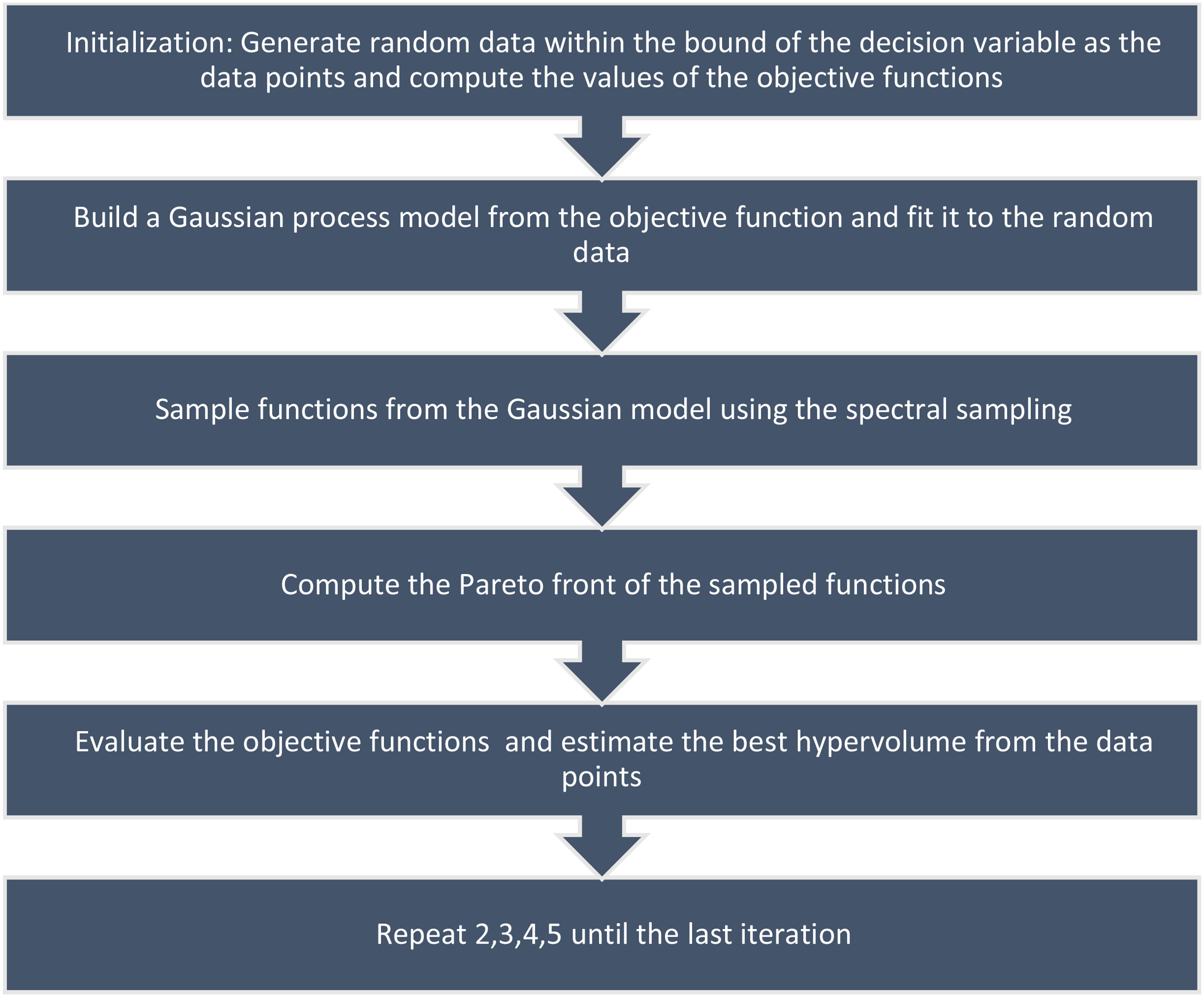

On the other hand, TS MOO uses a stochastic approach by exploiting new solutions using randomness and selects the best solution using the probability of selection. The concept of TS is sampling random numbers using the posterior distribution probability of the reward of the solutions. The TS structure can be described in Figure 2.

Thompson sampling multi-objective optimization structure.

The case studies

Case study 1: The US I-495 express lanes

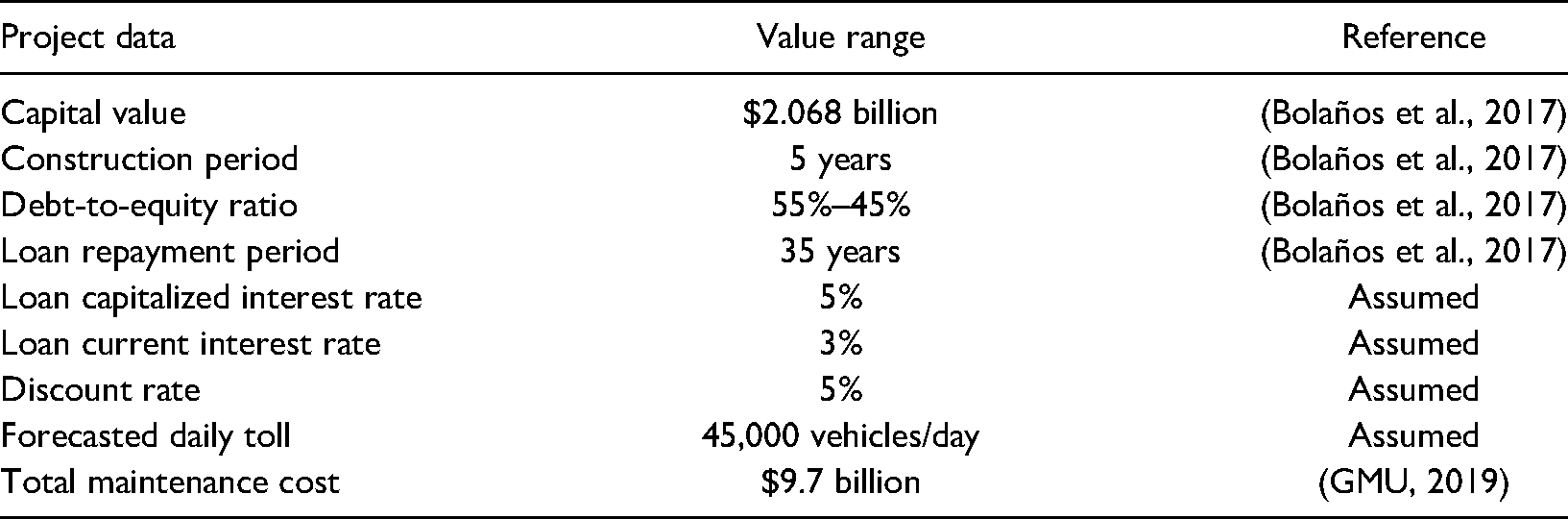

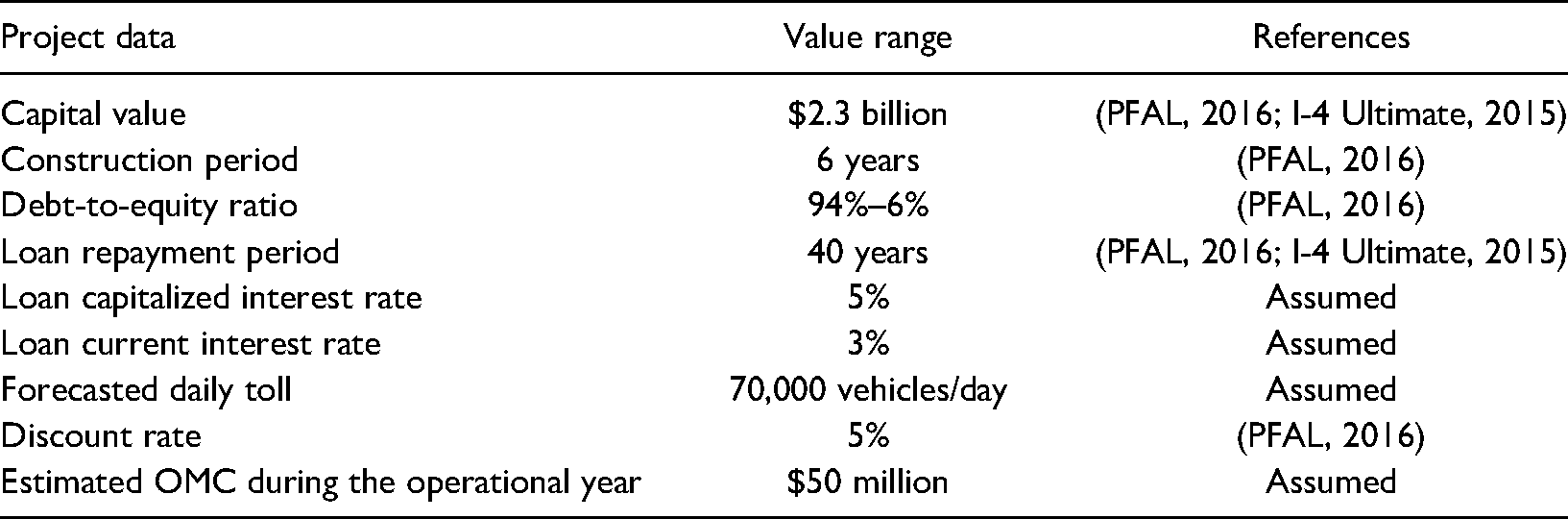

The US I-495 express lanes are carried out by the Virginia Department of Transportation. This project involves constructing two additional lanes in each direction of the congested I-495 highway road. The project company is obligated to design, construct, operate, and maintain express lanes. The data for the case study is shown in Table 1. The PPP contract's concession period for the capital beltway express lanes is 80 years; therefore, 75 to 85 years will be considered in this work. The I-495 express lanes consider a dynamic toll pricing, which depends on the traffic volume. According to the project operator (Transurban), in 2013, the generated price per vehicle ranged between $0.25 and $9.75 (Gilroy, 2013). For simplicity, this case study's concession price is assumed to be in the range of $1 to $10/vehicle to travel the entire length of the project. The traffic volume of the capital beltway is estimated to be 225,000 vehicles per day. However, the toll charges are collected for the extra lanes on users that wish to avoid traffic congestion. Transurban reported in 2013 that the traffic volume for the busiest day on the extra lanes was 47,500 vehicles (Gilroy, 2013). Hence, considering the annual growth rate from 2013 to 2020, the demand for the extra lanes in this study is assumed to be 45,000 vehicles/day with a future annual growth rate of 1%. According to a recent report that was prepared for the Center for Transportation PPP Policy at the George Mason University, the total maintenance cost for the I-495 express lanes is set to be $9.7 billion, which can be seen in $7.2 billion O&M and $2.4 billion major maintenance (GMU, 2019). Therefore, this case study's annual maintenance cost is defined to be

Project data for the I-495 express lanes project.

Case study 2: The I-4 Ultimate

According to the I-4 Ultimate, the I-4 ultimate express lane is a PPP project, which is about 21 miles road that connects Kirkman road to State road 434 (I-4 Ultimate, 2015). The project's total estimated cost is $2.3 billion, including replacing 74 bridges, widening 13 bridges, and building 53 new ones. Furthermore, the project will reconstruct 15 major interchanges and provide four new express lanes to the center of I-4. The express lanes will be running in 2021, and they will be owned by the Florida Department of Transportation (FDOT). FDOT did not have enough cash to fund the project; hence, by having this P3 agreement, the state will construct the road to meet the public needs. In other words, the project would take about 27 years to complete without P3, while with P3, it will take less than seven years to complete. The tolls then will be used to fund more than half of the project during the 40 years contract (I-4 Ultimate, 2015). The tolls will be based on a dynamic toll pricing that varies based on demand and will be collected electronically, and the FDOT will determine the cost of the tolls. For simplicity, the concession price for this case study is set to be in the range of $5 to $7.5 for the passenger journey all through the road, which can be a realistic range based on similar projects around the I-4 ultimate. For example, to travel seven miles on the 95 express lanes in Miami pay, passengers tend to pay from $0.5 to $10.50 (I-4 Ultimate, 2015). The daily demand around the I-4 Ultimatum is estimated to be around 200,000 vehicles (I-4 Ultimate, 2015). However, for a more conservative forecast, the daily demand for this study will be 70,000 vehicles/day. The data for the case study is shown in Table 2.

Project data for the I-4 Ultimate project.

Results

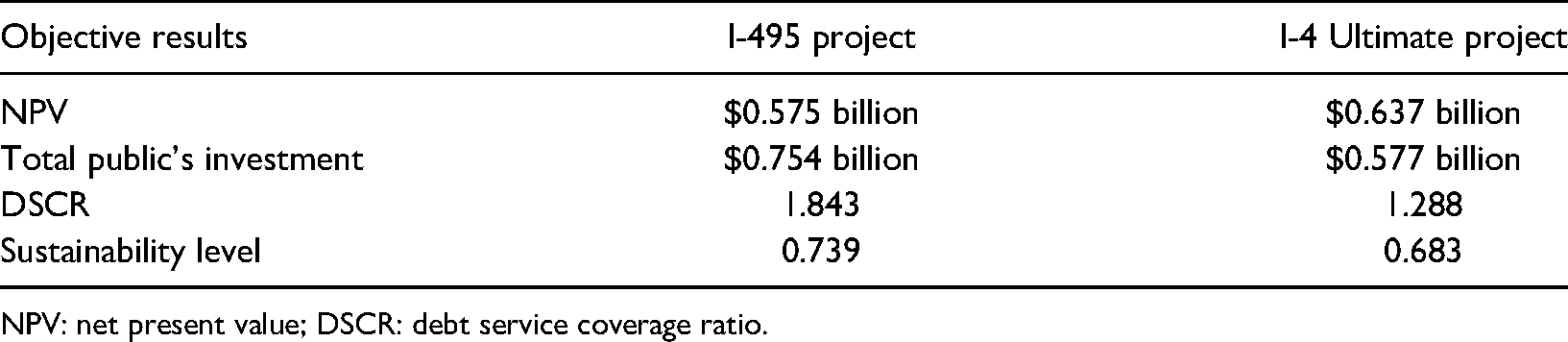

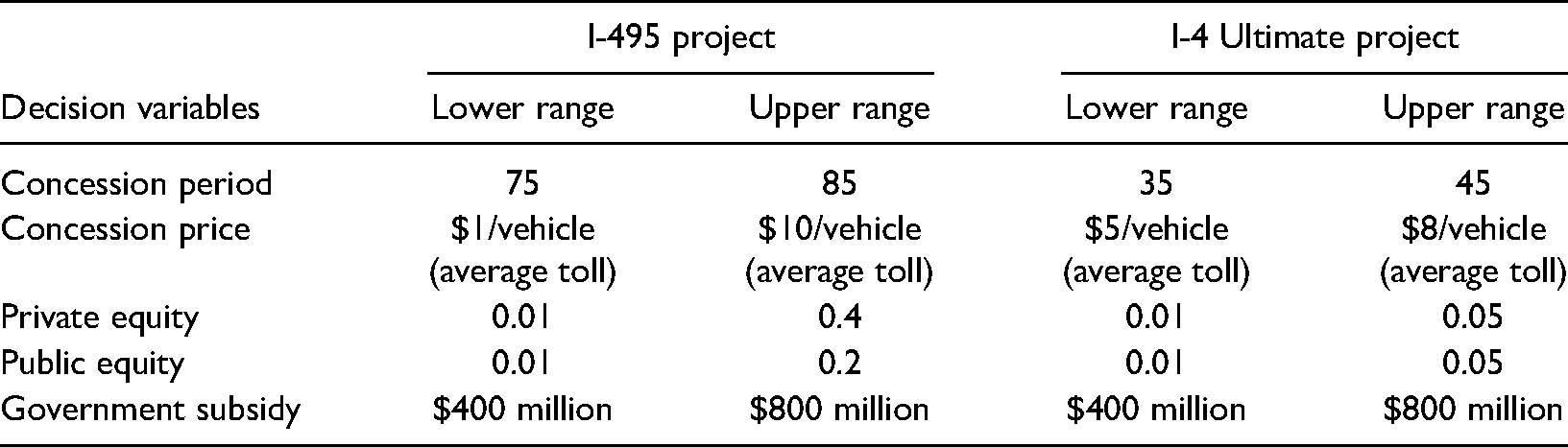

Optimization is carried out within the lower and the upper bound of the decision variables and satisfies the equity constraints. The decision variables are the concession period, concession price, private equity, public equity, and subsidy. The optimization was carried out so that the five objective functions were balanced. The non-optimized solution was computed using the agreement from the two case studies from Table 3 to describe the optimization procedure's effectiveness. The non-optimized results obtained are listed in Table 4. The decision variables were specified within a predefined lower and upper bound (Table 5). Consequently, optimization tuning was carried out to determine the non-inferior combination of parameters compared with the non-optimized results listed in Table 4.

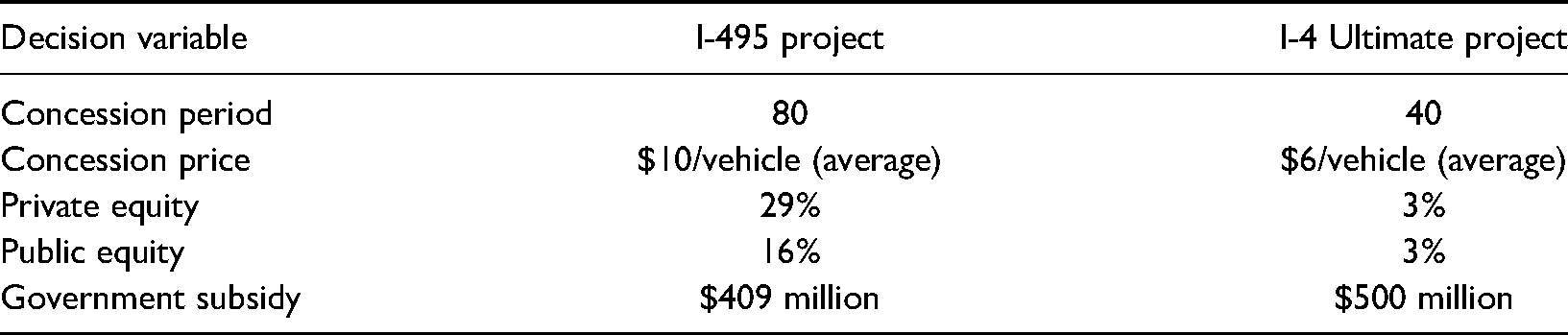

Decision variables from the agreement terms.

Non-optimized results.

NPV: net present value; DSCR: debt service coverage ratio.

Decision variables for the two case studies.

Optimization results using the multi-objective GA

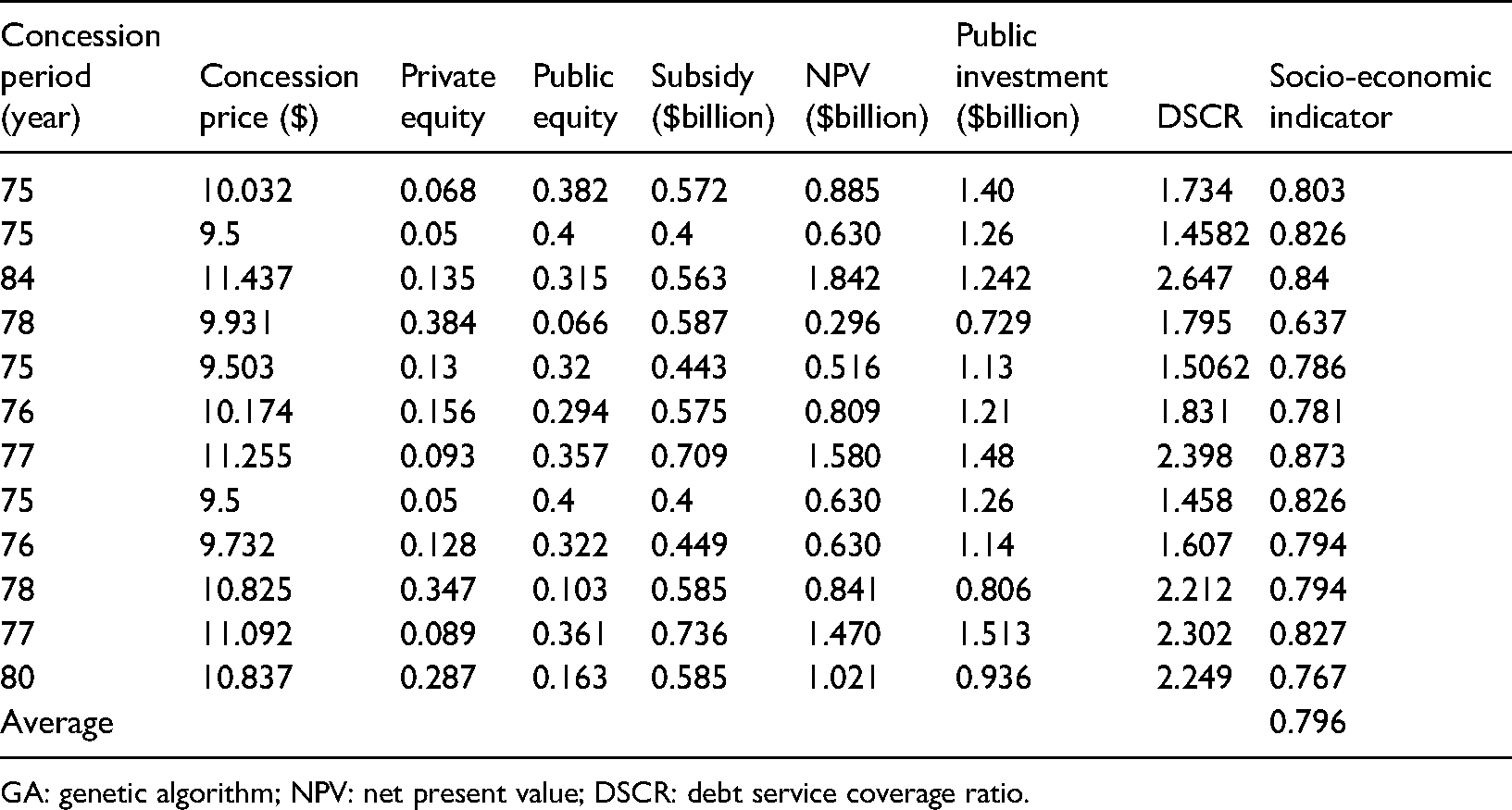

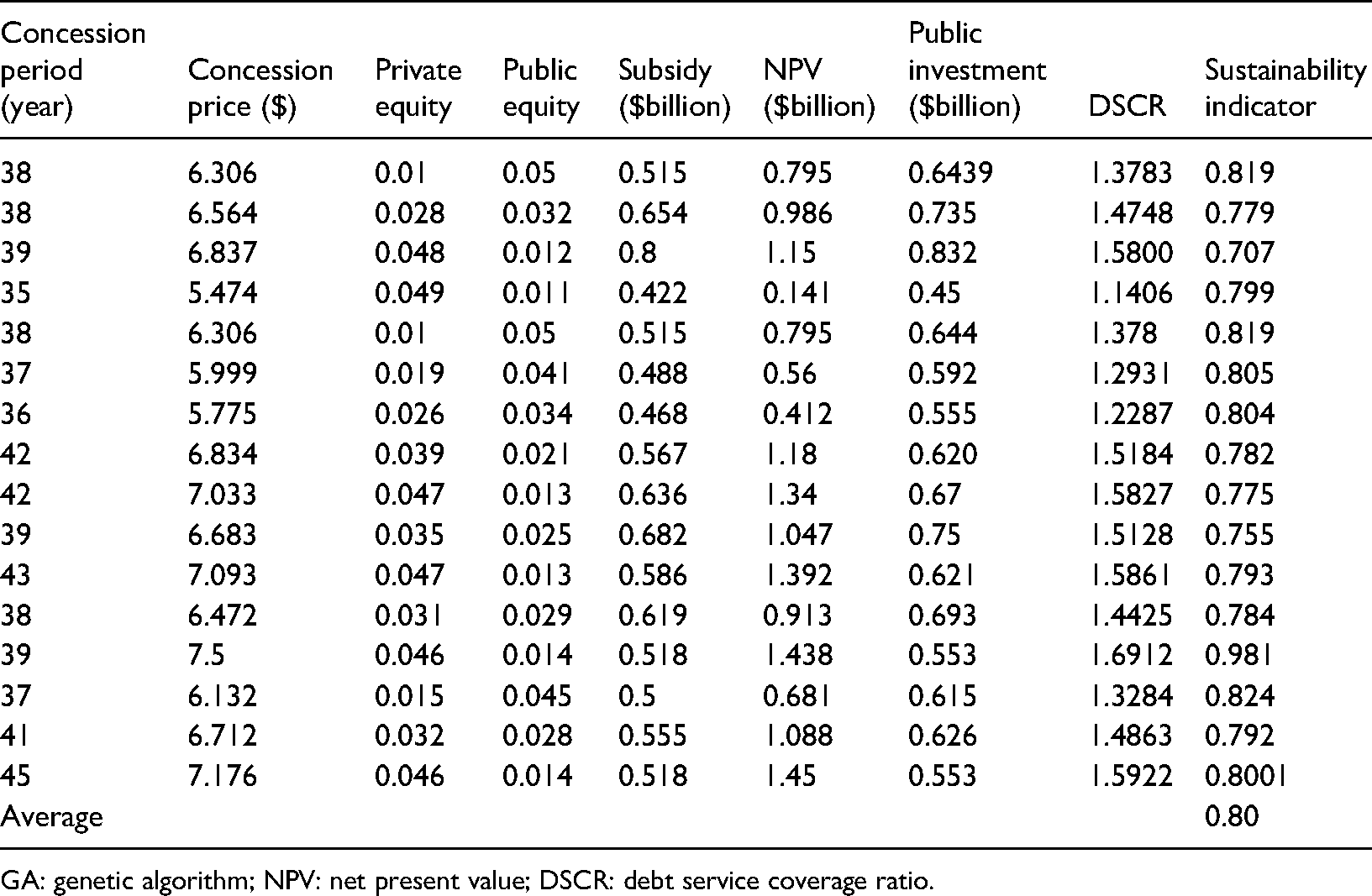

The GA MOO follows the conventional GA, which encodes decision variables into genes to form a chromosome. A bit of string representation was used for the chromosome design in this work. The genetic search was carried out with the GA parameters in Table 6, resulting in 20 Pareto fronts being generated, representing the best combinations of decision variables that resulted in optimum values. The Pareto front was obtained from the GA output at the last generation. The best 10 Pareto fronts that effectively balanced the objective functions were extracted from the front to represent non-inferior solutions. Tables 7 and 8 present the optimization results for the two case studies. The parent front's average socio-economic sustainability level was computed and compared with the non-optimized results, indicating a higher sustainability level than the non-optimal results.

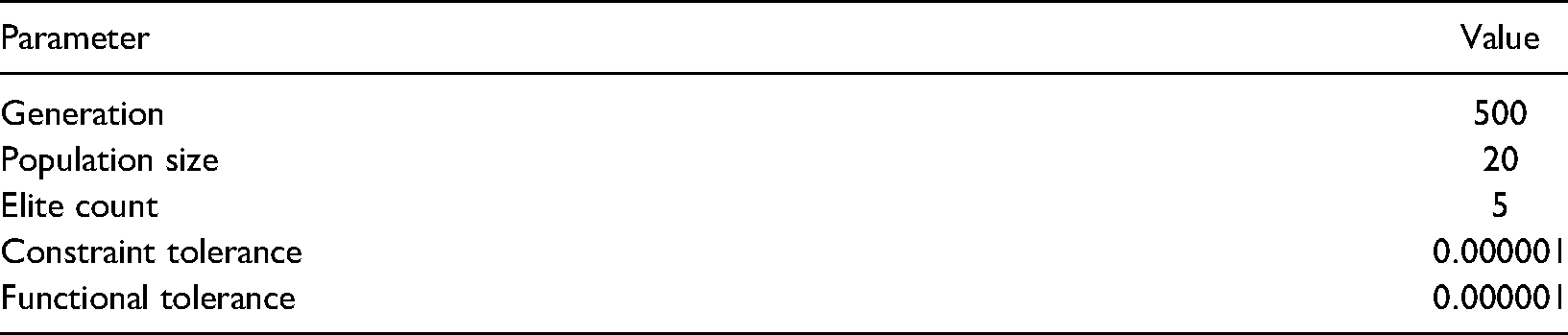

Genetic algoirthm (GA) parameters.

GA optimization results for the US I-495 project.

GA: genetic algorithm; NPV: net present value; DSCR: debt service coverage ratio.

GA optimization results for the I-4 Ultimate project.

GA: genetic algorithm; NPV: net present value; DSCR: debt service coverage ratio.

Optimization results using the TS

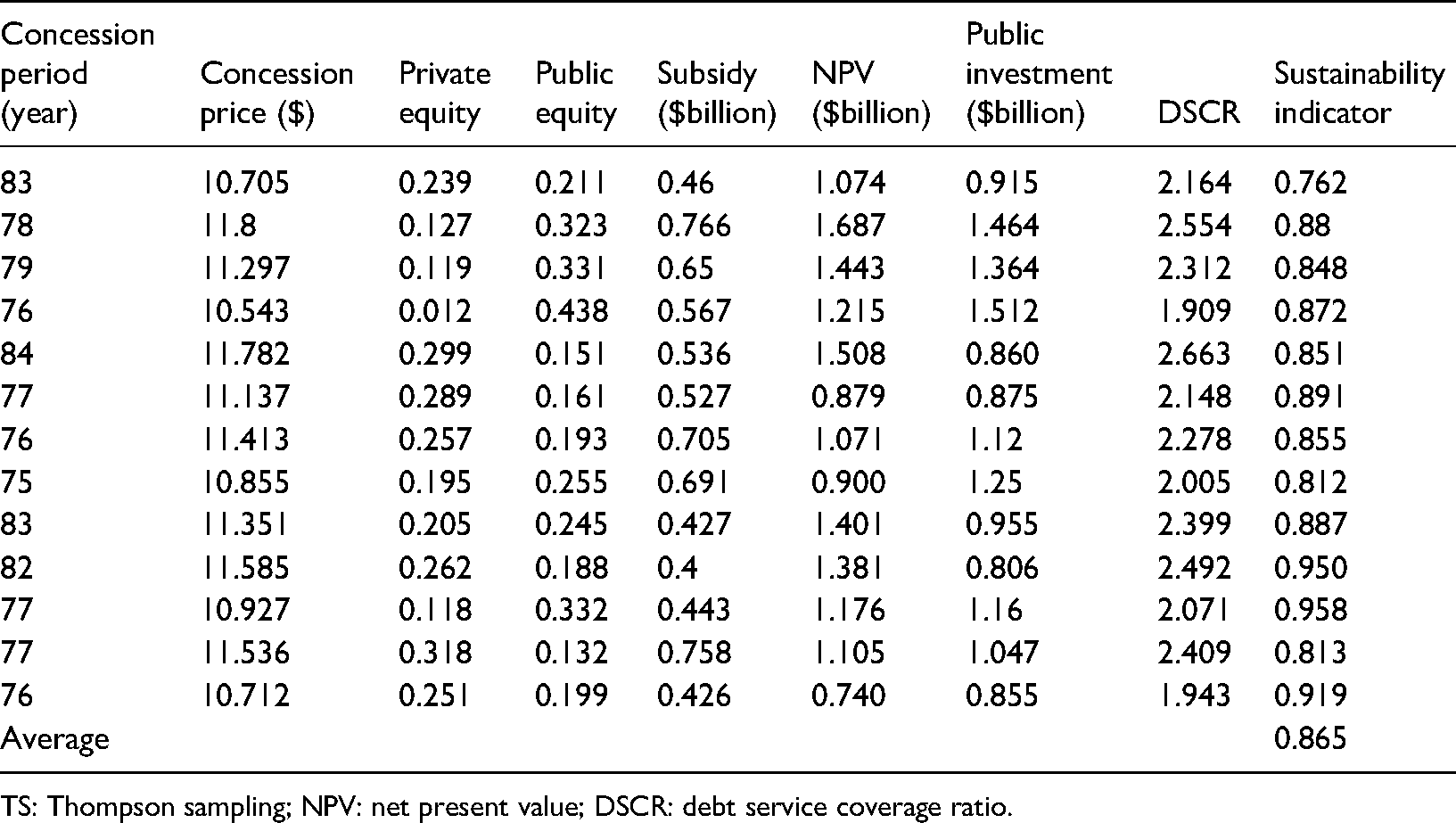

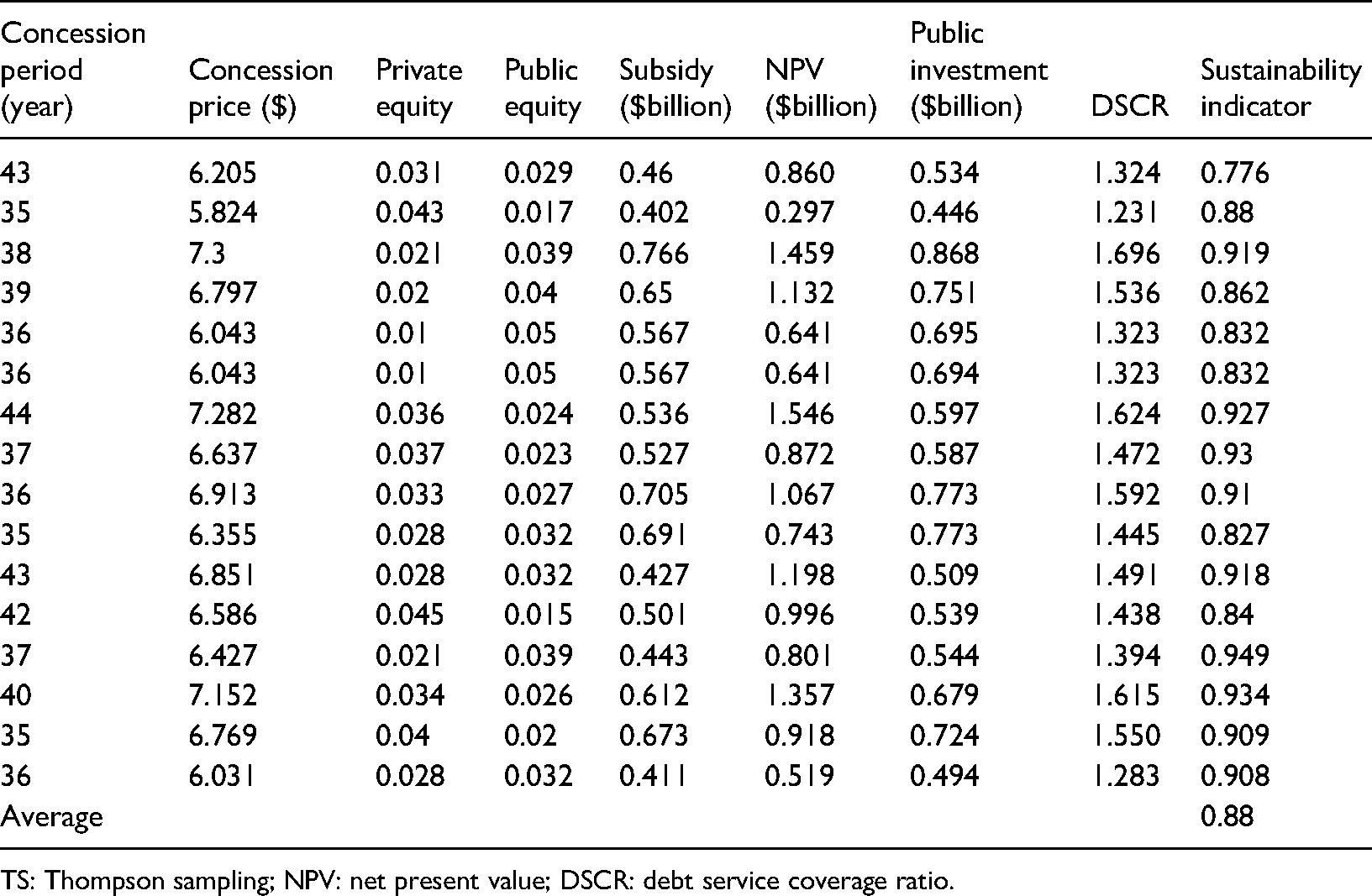

The TS was carried on the data; the first set creates random data sampling for inputs. The TS returned the parent font for the decision variables and the corresponding values for the objective functions. The optimization results for the TS for the two case studies are shown in Tables 9 and 10. The solutions of the parent front are not inferior to the agreement terms. The average sustainability level shows that the TS algorithm provides better optimal results when compared with the GA MOO.

TS algorithm optimization results for the I-495 project.

TS: Thompson sampling; NPV: net present value; DSCR: debt service coverage ratio.

TS algorithm optimization results for the I-4 Ultimate project.

TS: Thompson sampling; NPV: net present value; DSCR: debt service coverage ratio.

Discussion

Comparison between the GA optimization results and TS results

In the GA, the selection of the Pareto fronts is made using an elitist GA, in which GA favors some individuals than others due to better results from the evaluated result from the GA. On the other hand, with the TS optimization algorithm, the best Pareto search is obtained by choosing some set of data points that gave the largest hypervolume indicator (the performance measure that is assigned a single value to the solutions obtained from the data points; (Trovo et al., 2020). The advantage of a GA over the TS algorithm is that it enhances faster optimization results; however, the TS algorithm obtained better results than the GA, which coincides with the findings of Karamcheti et al. (2018).

The common ground between GA MOO and TS efficient optimization is that both algorithms begin by randomly initializing some set of data points (Touloupas and Sotiriadis, 2021). However, the GA produces offsprings from parents through the cross-over operation and mutation, while in the TS algorithm, new data points are generated using sample functions from the Gaussian processes. The TS algorithm formulates m distinct functions from m independent Gaussian processes using spectral sampling (Amrallah et al., 2021).

The TS algorithm obtained better optimization results than the GA; this can be confirmed by the average value of the parent fronts obtained from the results of the two algorithms. The TS algorithm determined the Pareto search from some sampled functions computed using the Gaussian process model for each objective function. The algorithm iterates to determine the best Pareto front by evaluating each objective function at every point to obtain the largest hypervolume until the maximum iteration is reached (Bradford et al., 2018). In view of its potential applications in minimizing logistics bottlenecks, Dumitrascu et al. (2018) proposed an advanced TS algorithm, which agrees with the current study's findings that the TS can be an effective tool to assess socio-economic status variables in viable PPP. In addition, our study is one of the first to compare both algorithm types within a PPP setting.

Sensitivity analysis

The current study used sensitivity analysis techniques to evaluate how the model depends on the input parameters following previously described literature. The model was developed using MatLab functions. The model inputs are concession price, concession period, private equity, public equity, and government subsidy. The sensitivity analysis combined random and predefined data obtained from the optimized results. Fifty random samples within the bound of the decision variables were generated using a uniform distribution and were combined with the predefined data. The values generated for the case study were fitted into the objective function.

The mesh plot's sensitivity analysis results in this study indicate how the model depends on any two input parameters. The mesh plot is a three-dimensional (3D) plot in which any two inputs can be combined to evaluate the level of dependence on the socio-economic level. Other parameters were set to fix, while the two parameters were iterated between the lower and upper bound to develop the sensitivity analysis within any two parameters and the socio-economic level. Interestingly, this analytical tool has been used recently to assess variables for leakages in buried concrete sewage pipes (Zamanian et al., 2021), electromagnetic cardiac therapy (Levrero-Florencio et al., 2020), inkjet printhead troubleshooting (Nguyen et al., 2021), renewable energy appliances (Dezan et al., 2020), among others. The findings of our study pose important considerations for further exploration in the future regarding how a set of variables can interact at various complex levels to climax in a productive and cost-effective PPP in the long term.

Statistical analysis

Statistical analysis was carried using correlation to indicate the model's significant parameters to improve the sensitivity analysis. The correlation measure used linear (Pearson) and rank (Spearman) methods to determine the most significant variable with the model's greatest influence. The statistical results for the two case studies are shown in Tables 11 and 12. It can be observed that the concession price and government subsidy have a significant influence on the socio-economic sustainability level for the first case study (USA I-495). In contrast, the concession price and period have the biggest parameter influence on the sustainability level for the second case study (US I-4 Ultimatum).

Parameter influence for the USA I-495.

Parameter influence for the I-4 Ultimatum.

The partial correlation was also computed to determine how any two parameters controlled the socio-economic sustainability level. The concession period, concession price, private and public equity, and concession period subsidies are the matching parameters. Tables 13 and 14 show how the parameters controlled the socio-economic sustainability level. It can be observed that the equity level of both the private and public sectors has a significant influence controlling the socio-economic sustainability level.

Parameter influence of two parameters to control sustainability for the USA I-495.

Parameter influence of two parameters to control sustainability for the I-4 Ultimatum.

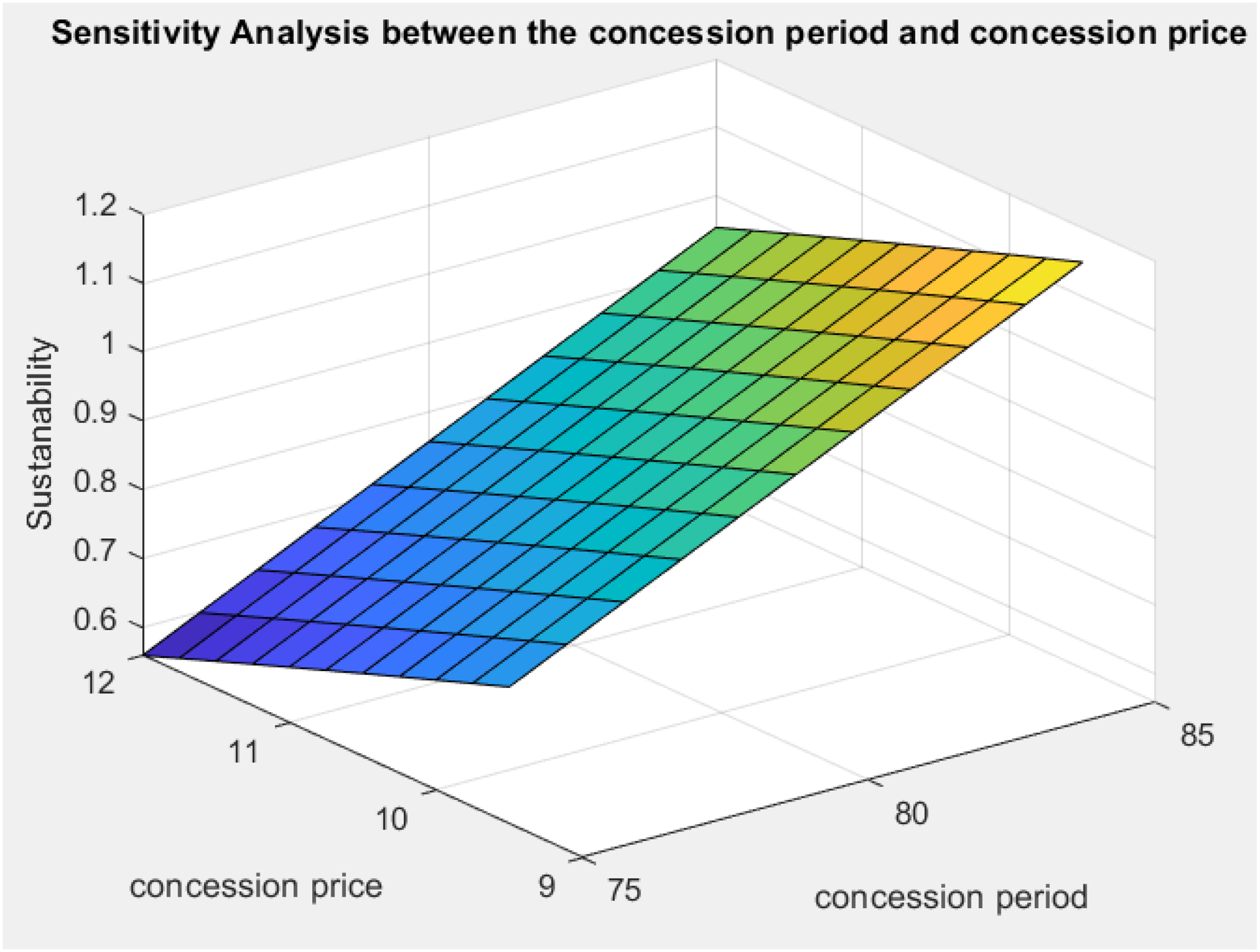

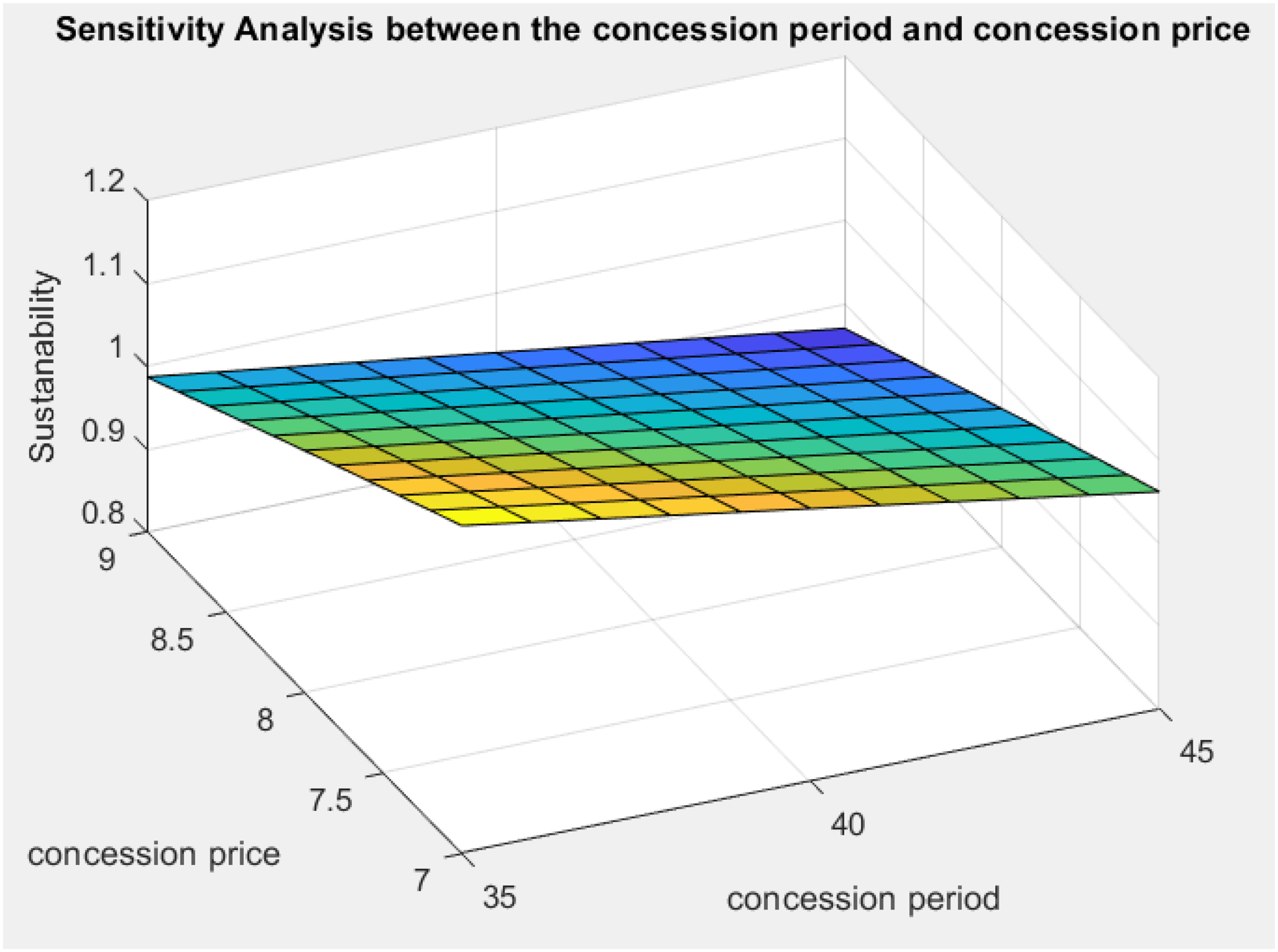

Effect of change of concession period versus change in price

The sensitivity analysis between the concession period and concession price was presented in a 3D plot. Figures 3 and 4 show the case studies' surf plot by comparing the concession period and the concession price. The concession period was matched with the concession price to determine how the socio-economic sustainability level changes concerning the concession period and price. The sensitivity analysis results indicate that the concession price must be low while the concession period can be manipulated for a better socio-economic sustainability level. The results show that the project's socio-economic sustainability performance is inverse to the concession price.

Effect of change in concession price and concession period on sustainability level for the US I-495.

Effect of change in concession price and concession period on sustainability level on the I-4 Ultimatum.

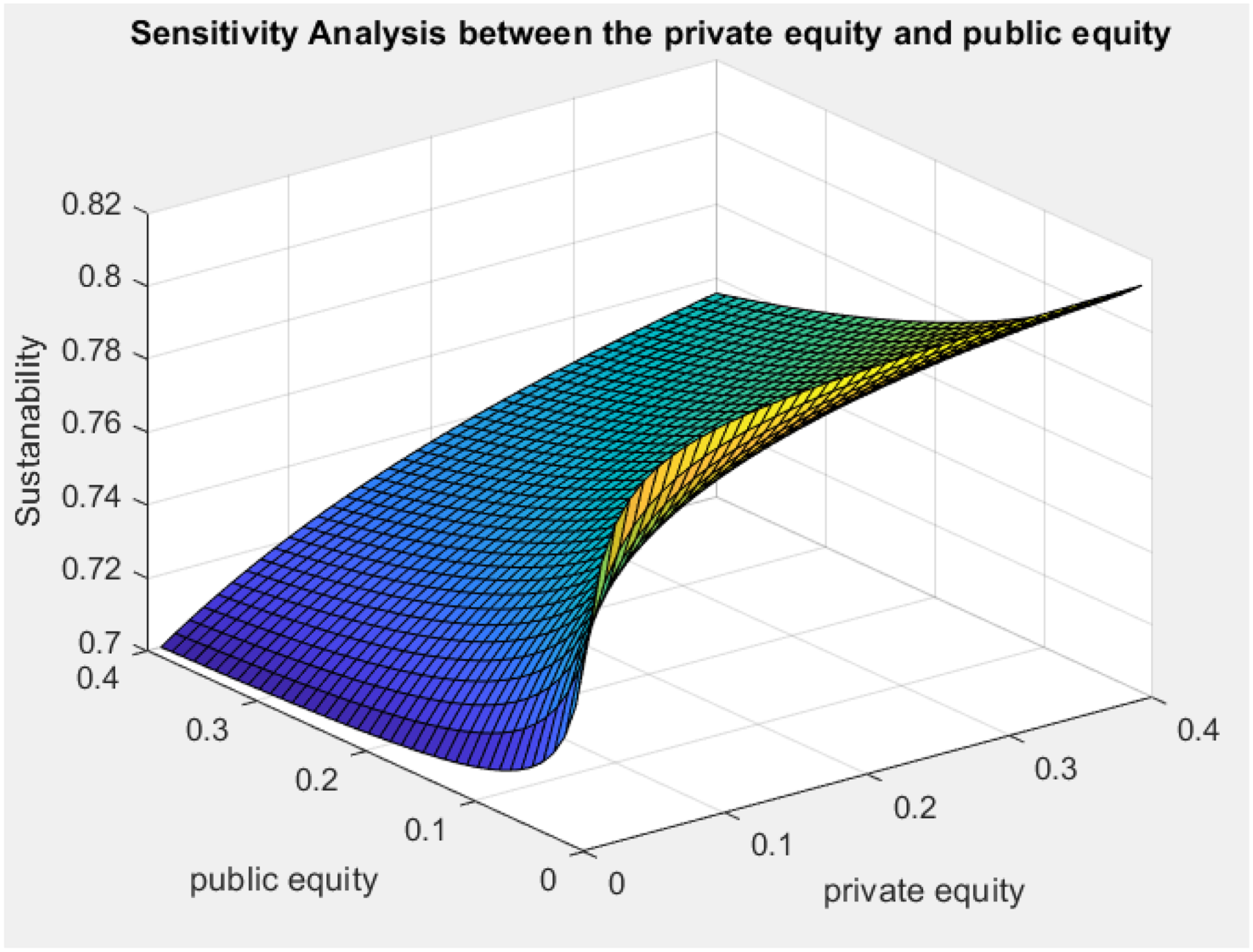

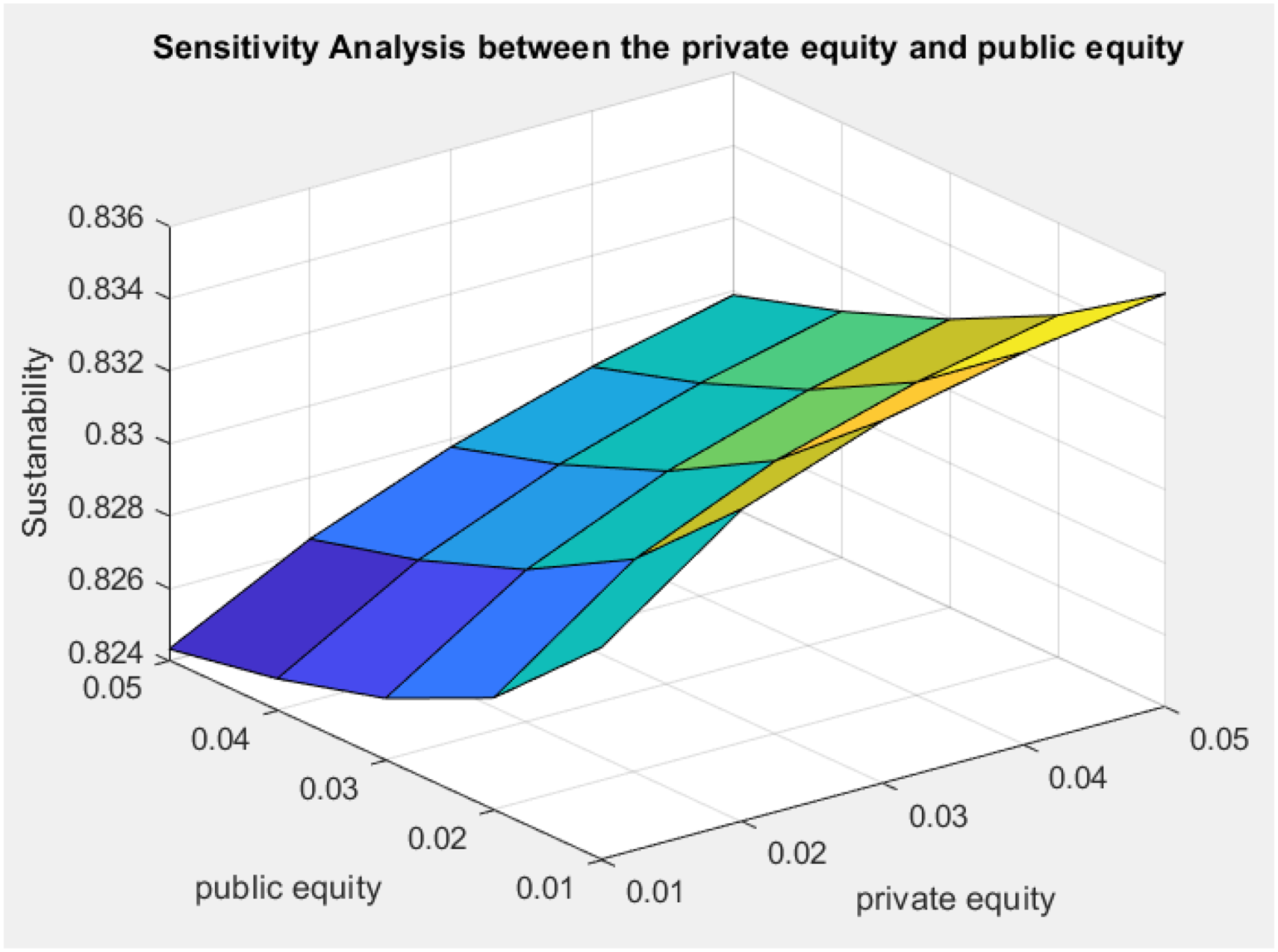

Effect of change in private equity level and public equity level

The sensitivity analysis between private and public equity was carried out (Figures 5 and 6). It shows that a higher socio-economic sustainability level is obtained when the private equity is high and the public equity is low. Therefore, the equity level must be maintained such that the private equity level is considerably higher than the public equity level. The project's socio-economic sustainability performance directly relates to private and inverse public equity.

Effect of private and public equity change on sustainability level (the I-495).

Effect of private and public equity change on sustainability level (the I-4 Ultimate).

Limitations and future studies

This paper has some limitations that need to be taken into consideration. For example, the model's validation depends on the accuracy of the model assumptions. Although the model has considered and investigated different concessions' components, other critical concepts in the PPP agreements have not been fully implemented in developing the model. Future research can expand the multi-objective model by including other critical indicators such as the impact of uncertainties, risk-allocation, interdependencies among the concession variables, project refinancing at the end of the construction period, and value for money. From the sustainability perspective, the model has investigated some of the PPPs' economic and social dimensions; however, other economic and social dimensions and the environmental dimension were not fully considered. Hence, including the effects of these dimensions can play an essential role in future research. Also, PPP projects are usually mega projects and are evaluated on a project-by-project basis. Therefore, this model may facilitate the decision-making process, but may not be used to design the concession.

Conclusion

PPP is a long-term commitment involving several parties, including public, private, and lenders. When designing the concession, all parties' interests must be satisfied to have a robust relationship between the involved parties. Their interests must be balanced optimally according to their contribution to the project, avoiding costly renegotiations or project failures. Besides, optimizing interests between the involved parties may require some trade-offs. Therefore, the goal of the model presented in this paper was to help determine the optimal contribution ratios from each party by providing a series of feasible contribution options for several concession factors (concession period and price, government subsidy, and capital structure). Then, a socio-economic sustainability performance was determined for each combination. This paper presented an MOO model constructed based on the DCF method. The multi-objective GA and TS were introduced to solve the multi-objective programming problem in this work. Case study 1 (the US I-495) was then utilized to construct and demonstrate the model. After that, case study 2 (the I-4 Ultimate) was used to validate the model results. The model helped to optimize the values for the different concession variables when they were dependent on each other. After that, the model presented different concession options containing different values for each of the concession components to help facilitate the decision-making process based on quantitative analysis. The GA model obtained faster optimization results than the TS model; however, the TS obtained better results. The model results showed that the socio-economic sustainability indicator increases as the private equity increases and the public equity decreases. The results also showed that the socio-economic sustainability indicator increases as the concession price decreases. Having these contribution options could facilitate the decision-making process for both the public and private parties. Besides, the use of the model could also improve the socio-economic sustainability performance of the PPP projects. The model presented in this paper can act as a valuable tool for both the public and private sectors in the bargaining process. It can also help reach mutual benefits between the involved parties based on quantitative analysis.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Data availability

All data, models, or codes that support the findings of this study are available from the corresponding author upon reasonable request