Abstract

In 2007 the EC introduced pre-commercial procurement (PCP) to endow the EU public sector with a legal instrument for procuring innovative solutions, unavailable in the market. To induce firms to participate in a PCP, the EC suggests contracting authorities to leave the intellectual property rights (IPR) of the new solution with the firms. Based on the perspective of a possible commercial success, the IPR should work as a major incentive for companies to engage in a PCP. As important as the EC seems to consider the IPR, for a successful PCP, so far no guidelines have been provided on how to estimate their economic value. This paper proposes a methodology for such evaluation, discussing its advantages and limitations. A main message of the paper is that IPR economic value should be based on the expected profits coming from commercialisation of the would-be innovative solution. Moreover, the value should change across the different development phases of the PCP. The findings could be useful for a broad audience of PCP potential participants, contracting authorities intending to promote a PCP and third parties interested in buying the IPR.

Introduction

In this paper we consider the role of patents in pre-commercial procurement (PCP) of innovation (European Commission Communication, 2007), a legal instrument introduced to provide the EU public sector with a purchasing procedure for procuring innovative solutions, otherwise unavailable in the market (Edquist and Zabala-Iturriagagoitia, 2015; Brogaard, 2018; Iossa et al., 2018). In particular, we shall discuss the economic value of intellectual property rights (IPR) in such a specific environment as the PCP, which is procuring research and development (R&D) services only.

Patents are a main institutional incentive system, provided by states for inducing firms to invest in R&D, disclose and introduce innovative solutions in the society, which might be beneficial for the whole community (Scotchmer, 2004; Hall and Rosenberg, 2010). As a form of economic incentive, patents are based on a very basic principle: the patent owner is guaranteed a period of temporary monopoly over the patented invention. More explicitly, during that period the inventor could make whatever use he/she wants of the invention and/or prevent others from using it. Alternatively, the inventor could allow other subjects to use the solution, typically in return for financial compensation. Such compensation could be given through a reward scheme as simple as a lump sum, or a stream of payments paid by the user to the inventor over a period of time, or possibly even more complex payment schemes.

Clearly patenting is not the only way to protect an innovation; indeed, secrecy is also a widely adopted method, however with an important difference. While patenting puts the new solution in the public domain, diffusing its underlying knowledge and function, secrecy does not, rather keeping the innovation in the private sphere. Therefore, patent monopoly could also be seen as the price paid by the society for public disclosure of the invention.

In recent years a debate has taken place on some issues related to the current situation of the patent system, as an effective institutional incentive device for promoting innovation. Among others, Jaffe and Lerner (2004) and Bessen and Meurer (2008) have pointed out that excess patenting, as well as beaurocracy and legal litigation, are hindering the patent system as a driver for innovation. In particular, excessive patenting introduces uncertainty over whether or not a would-be patent overlaps with already existing patents, and fear of being legally suited for this may sometimes discourage the introduction of solutions potentially beneficial for the society. Patent pools (Lerner and Tirole, 2004) represent a partial remedy for this problem, by joining a group of related patents whose use is allowed possibly at FRAND (fair, reasonable and non-discriminating) prices (Layne-Farrar et al., 2007).

For this reason rather surprisingly, and somewhat paradoxically, excess patenting could discourage, rather than encourage, innovation along lines analogous to the tragedy of the anticommons (Heller, 1998; Heller and Eisenberg, 1998). In the tragedy of the commons (Hardin, 1968), R&D investment is discouraged by the absence of well-defined property rights – that is, lack of protection – in commonly available goods. In the polar opposite tragedy of the anticommons, it is overprotection that may hinder innovation, because of an excessive number of patents.

An even more fundamental critique of the patent system has been made by Boldrin and Levine (2008), who are ‘against intellectual monopoly’ altogether, for its being a system discouraging rather than fostering innovation.

The EC 2007 PCP communication, and related documents, suggest that a contracting authority (CA) should leave with the firm the IPR protecting the solution, rather than appropriate them. The intuition is simple: IPR should work as an economic incentive for a firm to participate in a PCP. If the IPR have high economic value, then the firm would have a stronger incentive to accept the CA invitation, investing time and effort to find a solution. Alternatively, if the IPR have low economic value, a PCP might be less attractive for companies.

Therefore, based on the EC indication and above considerations, IPR should play a fundamental role in inducing creative firms to participate in a PCP, when invited by CA. However, whether or not the IPR will eventually be left with the supplier, taken by CA or sold by the supplier to a third party, the EC does not provide guidelines on how to estimate the economic value of the IPR in a PCP. This seems to be an important missing element for the analysis and sound application of PCP. Indeed, whoever is going to be the patent holder, it is crucial to have a good estimate of the IPR’s economic value. In fact, while the company will want to know how valuable is its participation in a PCP, CA will want to evaluate how economically attractive is the IPR incentive for the company. Moreover, as well as for a third party willing to buy the IPR, CA may want to know the IPR market price in case CA is interested in keeping it or purchasing it from the company.

This is what we aim to contribute to in this paper, targeting a broad audience of PCP potential participating firms, PCP contracting authorities and interested third party buyers. More specifically, we shall discuss how the economic evaluation of the IPR may be founded on the firm’s expected profit generated by commercialising the innovative solution. Indeed, this is what the monopolistic protection over the invention could guarantee to the firm. Given this, we then argue that the economic value of an IPR – that is, the price at which the IPR could be exchanged in the market – is represented precisely by the expected profit associated with the new solution. Therefore, the IPR market value incorporates several economic elements: prospective commercial revenues as well as rewards paid by CA, costs but also probabilities to succeed across the various phases of the PCP procedure.

For this reason, the value of IPR should be computed at different phases of the procurement process, since as a firm keeps being selected for subsequent stages, the risk of project failure changes, in particular decreases. Hence a main, rather intuitive, finding of the paper is that the economic value of the IPR typically increases along the procurement procedure. However, somewhat more surprisingly, in the paper we discuss how the IPR evaluation may also decrease, rather than always increase, over subsequent phases of the PCP procedure. The sequential nature of PCP is not new in innovation procurement public programmes, based on demand from the public sector (Bhattacharya, 2018). However the changing economic value of IPR along the PCP phases is an important element to consider, to our knowledge not yet fully investigated, since it could drive the company decision on whether, and at which phase, to sell the patent under the most favourable conditions.

The paper is structured as follows. In the following section we present a methodology to estimate the economic value of IPR in a PCP. Next, we discuss a few challenges that the implementation of such methodology could face, while the final section offers some conclusions.

A methodology to estimate the economic value of IPR in a PCP

The basic model

In what follows we shall consider the typical structure of a PCP with three phases, as suggested by the EC 2007 Communication. Yet, the framework we are going to discuss could easily be generalised to any number

Alternatively both CA and the market could be interested, or only one of them.

Despite being off the PCP procedure, indeed falling within the 2014 EC Directive on Public Procurement, the economic value of an IPR protection depends meaningfully on what may happen in phase

Below we develop a methodology to estimate the IPR value, and then discuss some critical points for its implementation.

Our subject of analysis is a generic company, which has been invited by CA to compete in a PCP. Start assuming that CA will leave initially the IPR, for protecting the proposal, to the company. Moreover suppose

In what follows, for simplicity, we shall assume these probabilities to be given and constant over time. However, in reality, not only may they differ across firms, but are also likely to depend on how much in each phase a single firm and the opponents invest in R&D. Indeed, it is clear that if one firm invests in the PCP much more than the opponents, it would plausibly have higher chances of being selected than with a much lower investment. That is, the value of success probabilities could be the endogenous outcome, rather than being given exogenously, of the competitors’ strategic decision on how many R&D resources to employ in the PCP. For this reason, the value of

Moreover, assume

Finally, if

where R is the expected revenue obtained by the firm when selling the solution to both the CA and the market, C are the related expected production and delivery costs,

Finally

Notice that (1) does not consider the case when a company is invited to a PCP, excluded at some phase and yet capable to win a post PCP procurement competition, with either CA and the market or only the market. Though possible, we believe this to be an event with very low plausibility and for this reason neglected.

Then, from (1), the expected profit of a firm invited to a PCP is

Expression (2) is what drives a firm decision on whether or not to accept the CA invitation for participating in the PCP. Indeed, if upon having received CA invitation the firm realises that

Since there are up to four phases until commercialisation, it is not surprising that expression (2) is composed of four terms, one for each such phase. Finally, notice that it could be

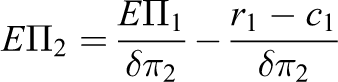

The economic value of IPR

Based on the previous paragraph, in this section we discuss a possible way to define the market price of the IPR. Indeed, what is the price s

1 at which the company would be willing to sell the IPR in the first phase? It seems natural to say that

The above considerations are based on the assumption that both the seller and the buyer would share the same view on

We ask now what would be the economic value of the IPR, should the company be at phase 2 of the PCP. By following a similar reasoning, conditional to having reached phase 2 the firm profit becomes

with the expected profit given by

Putting (2) and (3) together the following recursive equation provides a relationship between

Hence, if

Therefore, the IPR market value at phase 2 would typically be

Indeed when

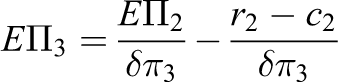

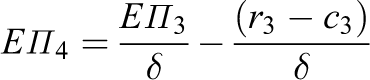

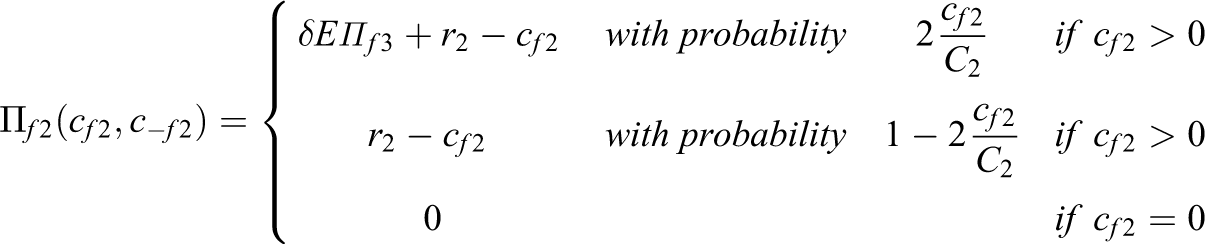

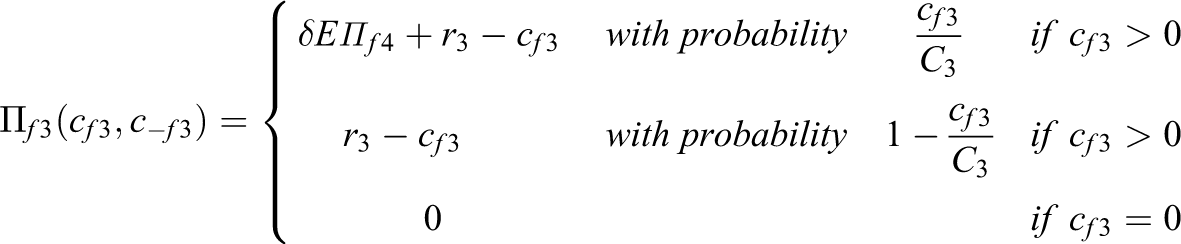

Likewise, by analogous reasoning in phase 3 the firm’s expected profit would be

hence

and similar considerations hold when comparing

so that

The above findings are summarised by the following proposition, where we assume that

Therefore, under the conditions of the above analysis, the economic value of the IPR varies across different phases, and would always be increasing whenever the reward paid by CA to the participating firms does not cover their costs. As a consequence, the sale price of IPR should change with the phase of PCP development, and whether or not they are sold at commercialisation phase.

Methodology implementation

The above methodology may provide guidelines on how to estimate the economic value of the IPR in a PCP. However, as already hinted at, there could be problems with its implementation, as some of the quantities may not be easy to estimate or have been introduced in an oversimplified way. In the next section we discuss some such critical issues.

R&D investment and success probability as a strategic choice

The first point concerns the possible relation between the firm’s R&D investment, in a given phase of the PCP, and the firm’s probability to be selected for the next phase. In the previous section they were introduced independently of each other, as exogenous quantities, not explained in terms of a strategic choice by the firm itself. However we suggested that, perhaps, a more realistic way to look at success probabilities is to see them as related to the amount of resources invested by the firm in a particular PCP development phase, with respect to the investment made by the other competitors.

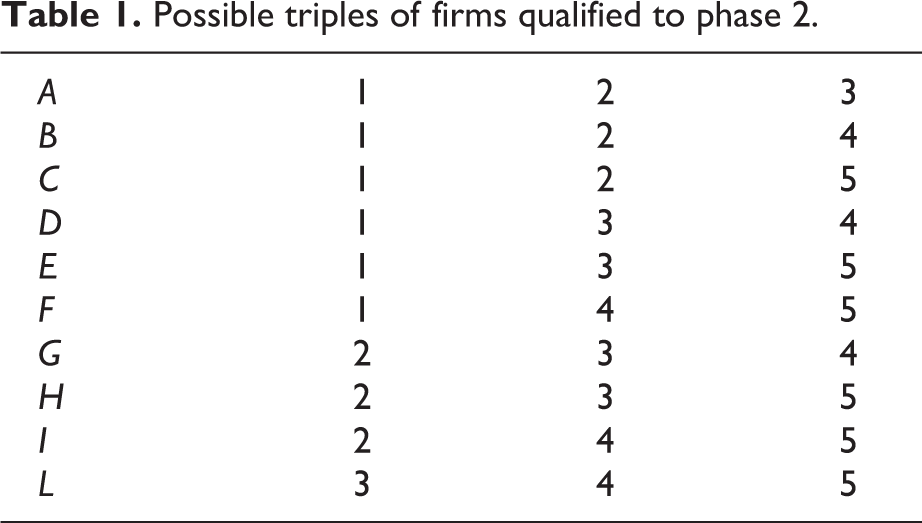

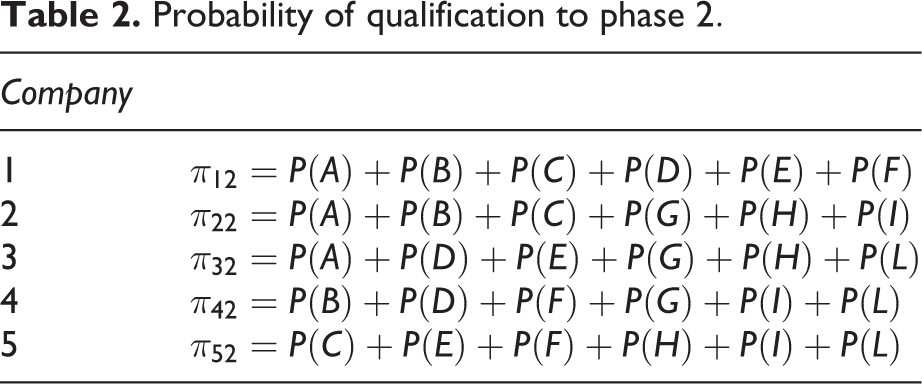

As an example, consider the following simple situation. According to the EC 2007 communication, suppose CA invites five

that is defined as in a Tullock type-of-contest (Konrad, 2009; Vojonovic, 2015) where the success probability is proportional to the own R&D investment, with respect to the total R&D investment made by all participants.

Since

From Table 1 we can construct Table 2, containing the probability of qualification for each firm.

Therefore,

However

and so

which explains the presence of the multiplicative 3 in

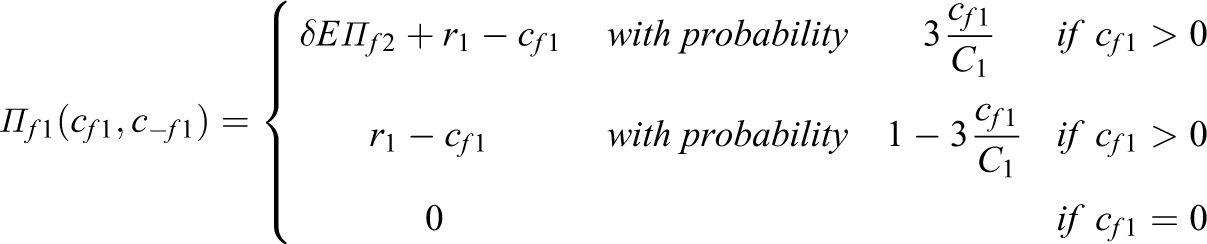

Expression (6) could be justified on the ground that qualification to phase 2 is akin to winning a lottery, where 3cf1 is the amount of money spent by firm f to buy tickets while C 1 is the total amount spent by participants to buy tickets. It must also be pointed out that formulation (6) considers all firms symmetric, that is, with the same ability – a point which will be discussed later. Finally, notice that a more articulated model should also take into account the possibility that company f could qualify for the second phase with either 0 or 1 competitor. Yet, without major loss of generality, to keep the argument simple we only considered the EC suggestion, with three firms qualified for phase 2. Similar considerations would hold for the following phases.

In this case, if

and its expected profit is given by

Assuming that company f chooses its investment

Consequenly, when investments are defined as in (8a) and (8b) the probability of firm f to qualify for the second phase is

as if the triple selected by CA or phase 2 was chosen with uniform probability from the

In this case, expected profit would be equal to

A few comments are in order.

First, notice that expressions (8a) and (8b) depend on prospective profits

Therefore, once r 1 is received, a company maximising expected profit would choose how much to invest considering only future profits. Therefore, if firms are paid exclusively for participation, as a compensation for the R&D costs, with expected profit maximisation r 1 would not operate as an incentive to increase R&D investments in phase 1.

Given the above considerations, if r 1 does not increase the firm’s investment it will play no role in increasing the probability of a successful discovery, which in turn is positively related to the level of R&D investments of the firms.

Indeed with a profit maximising company, for r

1 to act as an incentive for increasing a company’s R&D expenditures, it should be paid (at least part of it) conditionally on the company being qualified to phase 2. Indeed, in this case it is easy to see that (8a) would become

To summarise, the criterion by which CA would pay r 1 to an expected profit maximising company, that is, whether just for participation or conditional to qualification to subsequent phases, will affect its R&D investments and then its profits.

The investment is positively related to the discount rate

As stated above, the chosen level of investment is the same, symmetric, for each company because we assumed symmetry in the success probability function. A more general formulation of

where

Finally, if the company would not pursue expected profit maximisation, but rather invest in R&D as much as possible in the first phase, up to the breakeven level of the expected profit, then the chosen level of investment solves the equation

Still with symmetric investments, the solution is given by

which is larger than (8a) and increasing in r

1.That is, expected profit maximisation would reduce the company investment in the first phase, with respect to when investment is made up to the expected profit breakeven level. In particular, in (12) firms would invest

Assume, with no loss of generality, that firms qualify for phase 2. Then, analogously for a generic firm, with

and its expected profit defined as

Maximising (13), and still considering symmetry of investments and of the discount factor, provides as solutions

where

Hence

Finally, assuming that only

where

and maximising (16), again with symmetric investments, we obtain

so that

Therefore, in the third phase it would be best for the company to invest about

Numerical example

To gain further insights on what the model prescribes, it could be interesting to present a simple numerical example. Suppose the interest rate is

The example shows that testing the goodness of the model, in predicting firms’ behaviour, amounts to first estimate

Expected rate of return

Why should a company employ resources in a PCP? If the prevailing interest rate in the market is

As well as for expected profits and costs, the PCP rate of return will vary across its different phases.

Let us start by considering the first phase; if

As compared to the interest rate currently prevailing in the economy, around

Likewise, for firms qualified in the second phase, the rate of return

while in the third phase

an impressively high rate of return.

Therefore, according to our analysis, most probably participating in a PCP would seem to be rather convenient for an expected profit maximising company. Therefore, if the analysis is a good description of what takes place in a PCP procedure, then CA should have no major problems in attracting firms to participate in a PCP. Notice that expected return rates would be sufficiently high even if

Expected revenue

It is clear from the previous analysis that as long as

First, for both the companies and CA, it may not be easy to obtain a reliable estimate of future revenues and costs, once at a commercialisation phase. As the PCP proceeds along its phases, potential demand may change, similar solutions may enter the market, etc., all of which could contribute to update the estimate of prospective profits. As a result, an R&D investment level that was considered optimal in one phase may turn out to be suboptimal in retrospect because estimated profits are now different. Likewise, if in phase 1 a company plans to invest a certain amount of resources in the second phase, upon reaching phase 2 it may change decision because estimates on future profits have changed.

Based on the above considerations, as already said, the company and CA may entertain different views on prospective profits and then on the value of IPR. This might cause controversy in case CA wants to retain (at least part of) the IPR, as well as when other third parties would be willing to buy the IPR.

Conclusions

In the paper we considered the pre-commerical procurement for innovation, introduced by the EC in 2007. In it, a main economic incentive suggested by the EC to attract companies in the PCP and invest in R&D is to leave the IPR of the innovative solution with the firm. As important as it appears to be, so far a methodology for approaching the economic evaluation of the IPR seems to be missing. In this paper, we proposed such methodology and argued how the market value of IPR must be founded on prospective revenues and costs, related to potential commercialisation of the would-be innovative solution, as well as to the probabilities of being selected through the PCP phases, the R&D costs and rewards of the CA to the firms.

We also discussed that if the likelihood of finding the needed solution to the CA problem depends on how much firms would invest in R&D, then the objective function of the relevant companies, expected profit maximisation versus breakeven or others, could meaningfully affect the amount of investments and so the probability of finding a successful innovative solution in the PCP.

If the proposed methodology may have the merit of providing guidelines on how to proceed to estimate the economic value of IPR, it also has some limitations. First, as already stated, even if different subjects agree on the methodology, they may produce different estimates on some of the crucial quantities, such as success probabilities and expected future revenues and costs. This is due to the intrinsic difficulty in finding reliable estimates for R&D processes concerning new solutions whose development, by their own nature, has not yet been experienced. It would therefore be important to have a sufficiently rich data set of past projects available, for example, that of the US Department of Defence (DoD) related to the Small Business Innovation Research (SBIR) (Bhattacharya, 2018). For this reason it will be highly desirable if PCP cases would be collected, and information organised in publicly available data sets.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.