Abstract

This paper analyzes how financial controls, as established through the payment structure, are used and whether they influence federal contractor performance. These payment structures include variants on three primary types of contract: firm fixed-price, cost-reimbursement, and time-and-materials. Each of these payment structures creates different performance incentives for contractors, provides government contract managers with varying levels of information on contractor activities, and alters the dispersion of risk between the partners. The Federal Acquisition Regulation (FAR) prefers fixed-price contracts whenever possible, as they theoretically place the risk on the contractor, who is required to finish the work for the allocated price. Based on an analysis of nearly 25,000 federal definitive contracts that concluded between 2005 and 2014, findings indicate federal contracting officials tend to use payment structures in expected ways: to limit exposure to risk, leverage market forces, and reduce transaction costs when possible. Findings also show that there are important performance differences between contracts that use different financial structures, even when accounting for information asymmetries, asset specificity, and the complexity of the contracted work. Cost-reimbursement contracts are highly correlated with early contract termination.

Introduction

Government agencies increasingly rely on contracts for the delivery of services. Much of the existing research has focused on describing types and frequency of contracting activity (Ferris and Graddy, 1986), determining what should and should not be contracted out through the application of transaction cost economics (Brown and Potoski, 2003b; Brown, Potoski, and Van Slyke, 2006), and improving oversight through the application of agency theory to broad contracting challenges (Johnston, Romzek, and Wood, 2004; Kelman, 1990; Romzek and Johnston, 2002). However, there has been little attention paid to the specific mechanisms that public administrators use to hold contractors accountable. At the federal level, various types of managerial controls exist to maintain contractor accountability, including competitive selection, the financial structure of the contract, periodic performance reporting, transparency initiatives, and threats or mandates for re-competition (Federal Acquisition Regulation, 2014). Despite this array of potential accountability mechanisms, little work has been done to determine the effectiveness of the different options that public managers have available.

This paper analyzes how financial controls, as established through the financial payment structure, influence federal contractor performance. At the federal level, these payment structures include variants on three primary types of contract: firm fixed-price, cost-reimbursement, and time-and-materials. Each of these payment structures creates different performance incentives for contractors, provides government contract managers with varying levels of information on contractor activities, and alters the dispersion of risk between the partners. In addition, each of the structures is generally used in specific contexts, which are defined in the Federal Acquisition Regulation (FAR). As a result, it can be expected that payment structures which differ in context, incentive, and information exchanged might influence contract outcomes. Findings indicate that the structure of a contract affects contractor performance in ways that may run counter to the preferences listed in the FAR. In particular, cost-reimbursement contracts are much more likely to terminate early than other types of contract. This indicates that detailed information exchanges may not be sufficient to overcome the risks associated with the complex work that is most frequently contracted out using these financial structures.

Literature review

Increasingly, public administration scholars are studying contracting. Within the field, there are three primary types of contracting research. First, descriptive studies identify how frequently contracting occurs (Ferris and Graddy, 1986), what types of contract are used (Kim and Brown, 2012; Prager, 2008), what kinds of goods and services are being procured (Savas and Savas, 2000), and cost comparisons of public versus private provision (Savas, 1977). These studies, while interesting, do not explain why contracting is occurring outside political or economic explanations associated with efficiency gains.

Second, transaction cost economics have been applied throughout the contract process to attempt to explain the make-or-buy decision, an analysis of whether to contract out or produce the good/service internally ( Brown and Potoski, 2003b; Preker, Harding, and Travis, 2000; Tadelis, 2002; Walker and Weber, 1987); how to recognize asset specificity 1 and manage markets, primarily those associated with particularly complex products (Anderson and Dekker, 2005; Choi and Triantis, 2013; Hefetz and Warner, 2011; Johnston and Girth, 2012); and identify ways to address information asymmetries and uncertainty, although this has primarily focused on the initial decision to make or buy (Agranoff and McGuire, 2003; Brown, Potoski, and Van Slyke, 2013; Getha-Taylor, 2012; Girth, 2014). These studies tend to downplay external influences (such as politics) on the make-or-buy decision, and tend to focus on a small number of cases, which makes broad generalizability of findings difficult.

Third, there are agency theory studies, which assess how the principal (the government) can control the agent (the contractor) through the reduction of information asymmetry (Lambright, 2009; Ross, 1973; Steel and Long, 1998; Verhoest, 2005). These studies worry less about how the contract came into being, focusing on the immediate management challenges of contractor oversight. As a result, much of the context of the contract analyzed can be ignored, including its initial purpose, the cost of oversight, and the capacity of the contracting officials.

The importance of the financial design of public contracts has been largely neglected in existing scholarship. While transaction cost and agency theory studies both relate to the financial structure of a contract, only two studies address the financial structure as more than a control variable. Kim and Brown (2012) assess how frequently the Departments of Defense (DOD), Homeland Security (DHS), and Health and Human Services (HHS) use fixed-price and cost-reimbursement contracts and whether these contracts are used as specified in the FAR. They find that more than 70% of contracts in each department use the fixed-price payment structure. This adheres to the FAR’s preference for fixed-price contracts. Cost-reimbursement contracts are more likely to be used for complex products, such as computer system management or program management. Since these tend to be longer-term, more expensive, and riskier types of contract, Kim and Brown conclude that, despite using fixed-price contracts for a majority of outsourcing, federal agencies still take on high levels of risk for certain types of contractual work (Kim and Brown, 2012). They also link higher numbers of contract modifications with complex contracts, indicating perhaps less willingness to re-bid complex work on the open market due to high costs (Kim and Brown, 2012).

Building on Kim and Brown’s study, Girth and Lopez (2018) assess whether contracts that employ financial incentives differ from other types of contracts. Although rarely used, 2 contracts with financial incentives have the potential to provide public managers additional levers to influence contractor performance. Girth and Lopez focus on determining whether incentive contracts differ from other contracts in terms of duration, cost, and technical performance—aspects of contracts that incentive structures are designed to influence. Duration and cost are analyzed as measures of contract complexity. To examine how differing levels of contract complexity affects the use of incentive contracts, they analyze contracts for housekeeping services (simple), construction (mixed), and space-related services (complex). Their findings indicate that federal contract managers are slightly more likely to use financial incentives on contracts for more complex work. However, their findings on performance (which they measure in terms of contract modifications) are mixed and do not provide clear evidence about how financial incentives may be used to influence performance.

Although quite interesting, both of these existing studies are fairly preliminary and lack the detail necessary for a careful examination of the effect of a contract’s financial structure. Neither study specifies which types of contract they assess. At the federal level, there are many different kinds of contract (definitive contracts, indefinite delivery vehicles, purchase orders, BPA calls, etc.), and comparisons between the types can be challenging. Second, both studies examine limited data samples. For example, Kim and Brown only examine three departments, while Girth and Lopez only look at contracts for three types of work. In a government where millions of contract actions are reported each year, variation between agencies and across product types is likely, meaning that a limited data sample reduces the generalizability of findings. As a result, we still know little about how financial structures are used and whether they are used as intended in the FAR.

More importantly, both studies have difficulty addressing the relationship between financial structure and performance. Kim and Brown do not look at the impact of payment structure on outcome variables. Instead, they assess contract length and contract value. And, while it is interesting that certain agencies tend to modify and spend more than initially planned, this may tell us little about the performance of the contractor. Girth and Lopez extend the use of modifications as a measure of performance in their study, and also produce inconclusive results. It is likely that these difficulties linking contract financial design to performance are as result of the use of modifications as the performance indicator. High numbers of modifications and overspending may reflect changed priorities, altered scope, difficult contract requirements, or complex work, instead of indicating anything about contractor performance. It is also possible that modifications may be evidence of good performance (extensions, added resources, etc.).

Historically, studies of contractor performance have either used cost measures (Savas, 1977, 1981; Shetterly, 2000) or surveys of contract officers (Amirkhanyan, 2009, 2011; Brown and Potoski, 2003a; Heinrich and Choi, 2007) to gather data. Cost, while an important aspect of a contract, is an input and does not reflect any of the outputs or outcomes that are traditionally associated with performance (Holzer and Yang, 2004; Moynihan, 2008). Surveys have been demonstrated to generate biased responses, particularly if they are administered long after an event or if the respondent has a personal motive to inflate their responses (Singleton Jr, Straits, and Straits, 1993)—conditions which are clearly present in the case of public-sector contracts and contracting officials. A measure that allows comparability across many types of goods and services, reduces the possibility of bias, and includes aspects of outputs and outcomes would be an improvement upon the existing scholarship.

As a result of both the few studies and the methodological concerns, we know little about whether these financial structures affect the success or failure of a contract, and many questions about contract financial structures remain unanswered. In this study, I present a new measure of performance based on how the contract ends—closeout, termination, etc.—that facilitates comparison, captures elements of post-contract outputs and outcomes, and reduces the likelihood that data is biased in unexpected ways. Before describing this measure and the analytical approach in detail, it is first necessary to introduce some background on the different financial structures that federal contracts can employ.

Federal contract payment structures

During the pre-solicitation phase of the contracting process, public officials choose the financial (or payment) structure of the contract. The federal government uses three overarching financial structures for definitive contracts that alter the risk that the contractor assumes, change the incentive structure of the contract, and provide different accountability mechanisms and oversight procedures (FAR, 16.101, 2014). The guidance in the FAR shows a preference for fixed-price contracts, which shift risk to the contractor (FAR, 16.2, 2014). More than 65% of federal contracts are fixed-price (Kim and Brown, 2012). In each case, it is up to the contract manager to determine which financial structure best fits the contract, although the FAR does provide guidelines for when each might be appropriate (Federal Acquisition Regulation, 2014). In all cases, public managers are required to identify approximately how much will be obligated on the contract. Contracting officials generally establish a minimum amount of spending that will be made and estimate a spending ceiling. This approximate value of the contract can be altered through change orders, funding actions, and the exercise of options. As a result, financial actions taken throughout the course of the contract, when compared to this total value, can provide additional insight into contractor performance, particularly if the overarching financial structure is considered.

Fixed-price contracts

Fixed-price contracts provide a firm price ceiling for the contract. Fixed-price contracts place the maximum possible risk on the contractor, who is obligated to complete work for the established price (FAR, 16.202-1, 2014). As a result, this structure provides profit motive incentives for efficiency; if the contractor wishes to make a profit, the work will need to be completed for less than the fixed price. As a result, fixed-price contracts reduce administrative oversight costs since the contractor should be motivated to perform efficiently. Fixed-price contracts are most appropriate when there is price competition, when price comparisons are available to make reasonable performance and cost estimates, and when performance uncertainties can be identified and associated risk shifted to the contractor (FAR, 16.202-2, 2014). Generally, fixed-price contracts are preferred in federal contracting as they are seen as efficient vehicles which distribute risk between contractual partners.

Despite potential efficiency benefits, fixed-price contracts may limit oversight capabilities of public managers due to the reduced reporting requirements and limited provision of progress information (Müller and Turner, 2005). Indeed, fixed-price contracts may even flip the balance of power, making the contractor act more like the principal in the relationship, as they possess greater knowledge of the activity, pricing, and day-to-day performance of the contract (Shenson, 1990). However, fixed-price contracts tend to be preferred at the federal level over other types of contract due to the ability to shift risk to the contractor, to clearly define the overall cost for the effort, to reduce chances of opportunism, and to limit oversight and accountability costs (Curry, 2010; FAR, 16.2, 2014).

Cost-reimbursement contracts

Cost-reimbursement contracts allow for payments to the contractor for expenses incurred during work on the contract. These contracts are used if work or product requirements are hard to define or if performance costs are particularly hard to estimate. Cost-reimbursement contracts establish an estimated total cost of the contract, including a ceiling over which contractors cannot make charges without approval from the government (FAR, 16.301, 2014). Contractors run no risk of loss under these contracts, making them more appealing in instances where a contractor’s project-specific investments costs are high or when markets are thin. If the government agency fails to reimburse for costs, contractors have no obligation to continue to perform on the project.

These contracts place more financial risk on the government than the contractor, as performance criteria and expectations may be less clear. In addition, contractors may have the incentive to work slowly to incur higher costs, thus delaying meaningful progress.

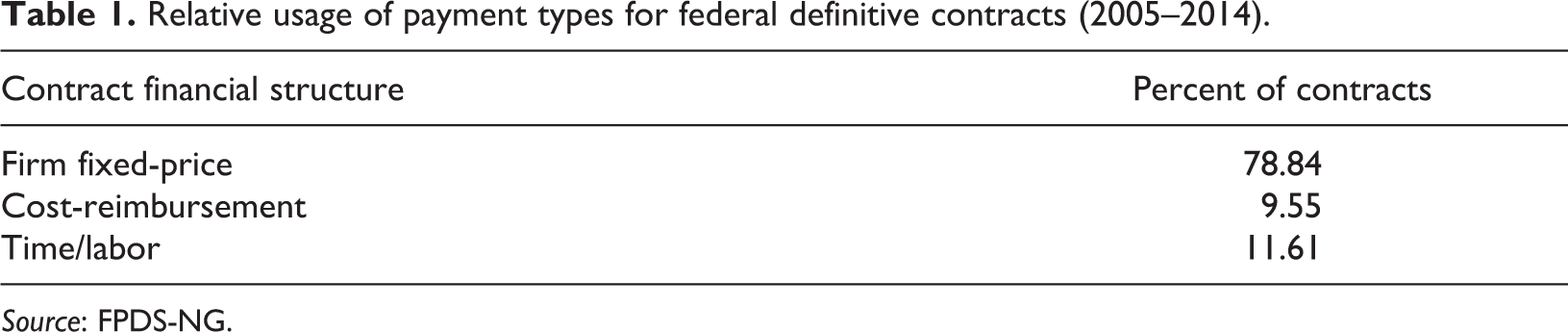

The FAR views cost-reimbursement structures as undesirable unless unavoidable. Since many federal contracts are for exploratory projects, R&D, or other kinds of technical development, these structures are used more frequently than might be preferred, accounting for slightly less than 15% of definitive contracts (see Table 1). It is worth noting that cost-reimbursement structures give increased visibility into the actions of contractors (as they have to report how costs are incurred), possibly increasing accountability and reducing information asymmetry. In addition, the diversity of sub-types allows government contracting officials some discretion in determining the best method to incentivize performance when requirements are poorly defined or performance measurement is difficult.

Relative usage of payment types for federal definitive contracts (2005–2014).

Source: FPDS-NG.

Time-and-materials and labor-hours contracts

These financial structures do not necessarily establish an overall price for the contract, but rather reimburse the contractor for the labor hours and materials used in the completion of the desired work (FAR, 16.601, 2014). Such contracts are used only when the government cannot accurately assess the length of the contract or the costs of the materials and labor required to complete the work. Due to the uncertain nature of the work and the inability of the government to anticipate costs and duration, contractors may have some incentive to inflate costs. As a result, the use of these types of contract is discouraged unless unavoidable (FAR, 16.601(d), 2014). To ensure that this does not happen, time-and-materials and labor-hours contracts require intensive government oversight. In addition, spending ceilings, fixed hourly rates, materials handling costs, limitations on general and overhead spending, and detailed guidelines for the transfer of funds between contractors and subcontractors are clearly established in the contract.

Some have labeled time/labor contracts as versions of fixed-price contracts (Shenson, 1990). However, the FAR is very specific that these are not fixed-price contracts (FAR, 16.600, 2014). Instead, they are more like cost-reimbursement contracts where the duration is uncertain and costs are particularly difficult to estimate beforehand. Profit incentives are very limited with these types of contract, as there are few mechanisms available to control costs or incentivize efficiency. Instead, contractors are simply reimbursed for effort expended. As a result, opportunism is a potentially large problem. Additional constraints, such as profit limitations, are put into place if such contracts are not able to be competitively sourced due to unique requirements (FAR, 16.601(c)(2)(ii), 2014).

Federal officials encounter contracts with diverse requirements. The structures described above are designed to limit government risk, encourage bids, and reduce contractor opportunism depending on the context of contractual requirements. As a result, the payment structure of each contract may be indicative of the circumstances surrounding it. Contracting officials have the discretion to decide which of these structures to use on each contract. They make this decision based on the complexity of the contract, the strength of the market, and associated managerial costs (Kim and Brown, 2012). In particular, the overarching structure chosen provides insight into how the contracting official perceived the clarity of requirements—a measure of task complexity. Thus, these potential problems (risk, market-making, and opportunism) relate closely to transaction costs.

Hypotheses

This research focuses on understanding how financial structures are used and the extent to which they affect federal contractor performance. Each financial structure offers particular benefits and drawbacks for public managers. Fixed-price contracts are most appropriate where there is competition, as this allows contracting officials to set an appropriate price ceiling for the contract. Generally, fixed-price contracts are best when the good or service provided is relatively simple, as performance risks can be identified ahead of time. This forces both the agency and the contractor to think through management challenges before the contract is in place, but such planning can be impossible if the requirements are too complex. As a result, fixed-price contracts are most likely to be used when there is a competitive marketplace and when contract requirements are well defined (i.e., when the good or service procured is well understood). H1: Competitively sourced contracts are more likely to use fixed-price structures.

Many of the goods and services that government procures through contracts do not meet these criteria. Markets may not be competitive, forcing the government to use single vendors (Girth et al., 2012). Under these conditions, asset specificity rises for the contractor as there may be no way to repurpose the investments necessary to work on the contract. As a result, few contractors may be willing to bid on the contract, and the government may need to incentivize interest in some way. One way to do this is by guaranteeing reimbursements for investments of time, labor, and other purchased resources through the financial structure of the contract. Although this approach does not encourage efficiency, as vendors are incentivized to charge for as much reimbursement as possible, it does encourage firms to bid on contracts that may be perceived as riskier. Much economic research demonstrates that fewer vendors bid on contracts as asset specificity rises (Joskow, 1988; Lajili et al., 1997; Mithas, Jones, and Mitchell, 2008). As a result, sole source contracts may be evidence of asset specificity, while contracts receiving many bids are evidence of a competitive marketplace where sellers’ investments can be repurposed for other buyers. H2: Sole source contracts will be more likely to use cost-reimbursement and time/labor financial structures. H3: Contracts that receive five or more bids will be less likely to use cost-reimbursement and time/labor financial structures.

In other cases, certain aspects of a contract may increase the uncertainty associated with bidding for or managing the contract. In general, contracts for more technical goods and services, contracts with longer durations, and contracts that involve higher total expenditures of funds are considered to have higher levels of uncertainty (Kim and Brown, 2012). Often the requirements of a contract are difficult to clearly define in advance, as the project is exploratory or for a relatively rare (or even unique) good or service (Bajari and Tadelis, 2001). Uncertainty is pervasive on such contracts for both the government and the contractor. Public contracting officials may have a hard time clearly explaining what is desired and may have more difficulty evaluating performance (Williamson, 1979). Vendors may not have a clear idea what the government desires from the project and may be more likely to shirk if quality problems are easy to hide (Romzek and Dubnick, 1987). On very technical projects, holding contractors accountable can be particularly difficult as public officials experience extreme information asymmetries (Anton and Yao, 1987; Bahli and Rivard, 2003; Gallini and Wright, 1990). For highly uncertain contracts, financial structures might be used to facilitate greater information exchange between the government and the contractor in an effort to reduce the information asymmetry and facilitate more informed performance evaluation over the duration of the contract. Regular information exchange can help build familiarity between the contractor and the agency, as well as make more transparent the processes used to both perform and evaluate the work on the contract (Faems et al., 2008). This can reduce both process and behavioral uncertainty. H4: Contracts for goods and services with uncertain requirements are more likely to use cost-reimbursement and time/labor structures than contracts for other goods or services. H5: Contracts for goods and services with more clearly defined requirements will be less likely to use cost-reimbursement and time/labor structures than contracts for other goods or services. H6: Longer contracts are more likely to use to use cost-reimbursement and time/labor structures than shorter contracts. H7: Contracts that involve a high amount of spending are more likely to use cost-reimbursement and time/labor structures than other contracts.

Despite challenges associated with transaction costs, contracting offers value to government because it enables public agencies to take advantage of market forces to improve the efficiency of service provision (Kelman, 1990; Osborne and Gaebler, 1992; Savas and Schubert, 1987). As contractors strive to make a profit, they must provide goods and services efficiently to retain market advantages over their competitors. Any reduction in efficiency could result in competitors providing the service at a lower price or of a better quality. Thus, as long as markets are competitive and requirements are clear, firms can be held accountable for high levels of performance through their own profit motive (Brown, Potoski, and Van Slyke, 2006; Williamson, 1979). The contracts most likely to perform well are those where there are competitive markets and with well-understood requirements. Under such conditions, firms have the financial incentive to perform highly and government contracting officials can readily understand the service being provided. Fixed-price contracts are appropriate to use in these conditions, and as a result are likely to be used on contracts that perform well. H8: Fixed-price contracts will be less likely to terminate early than other types of contract.

Data and methods

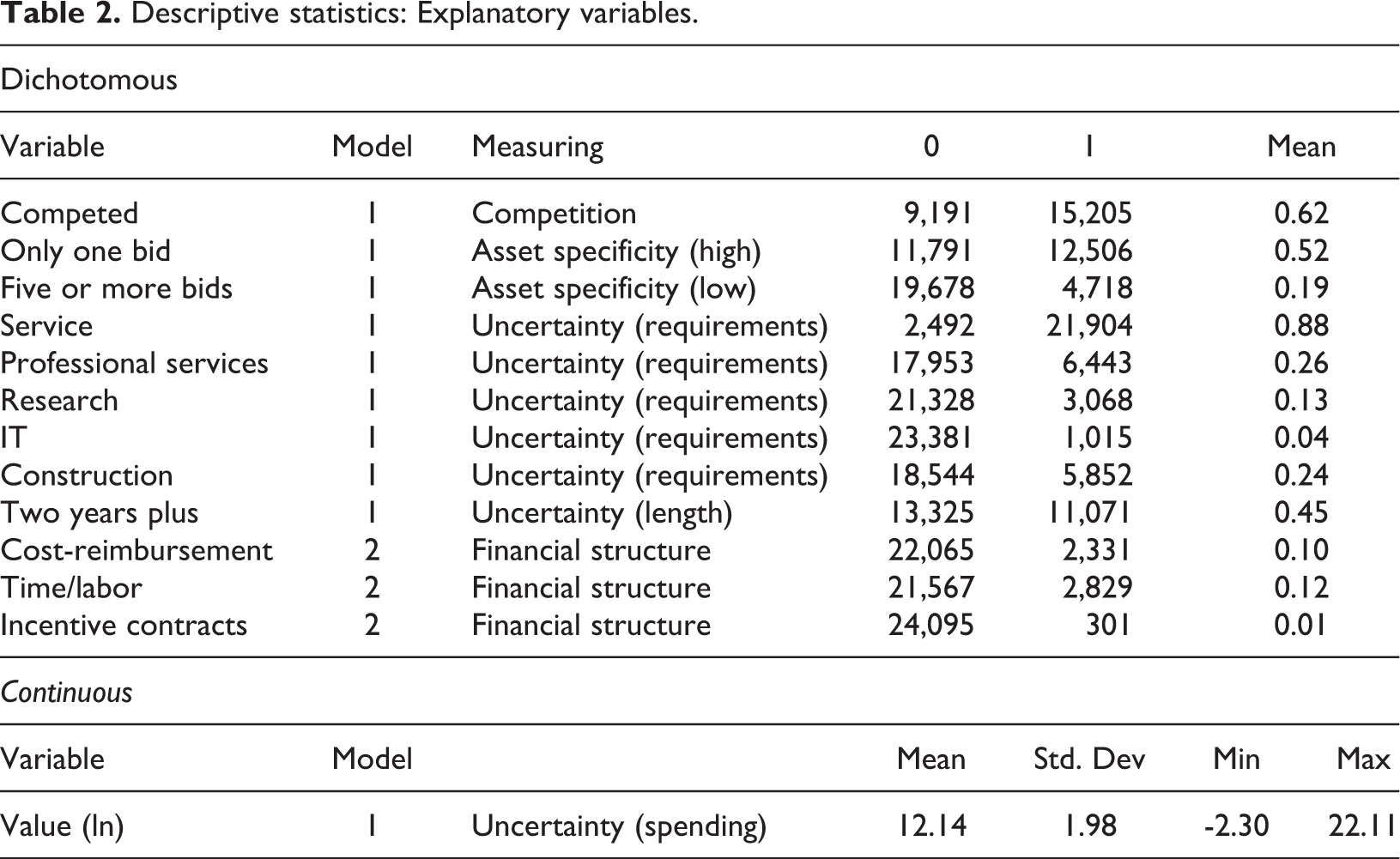

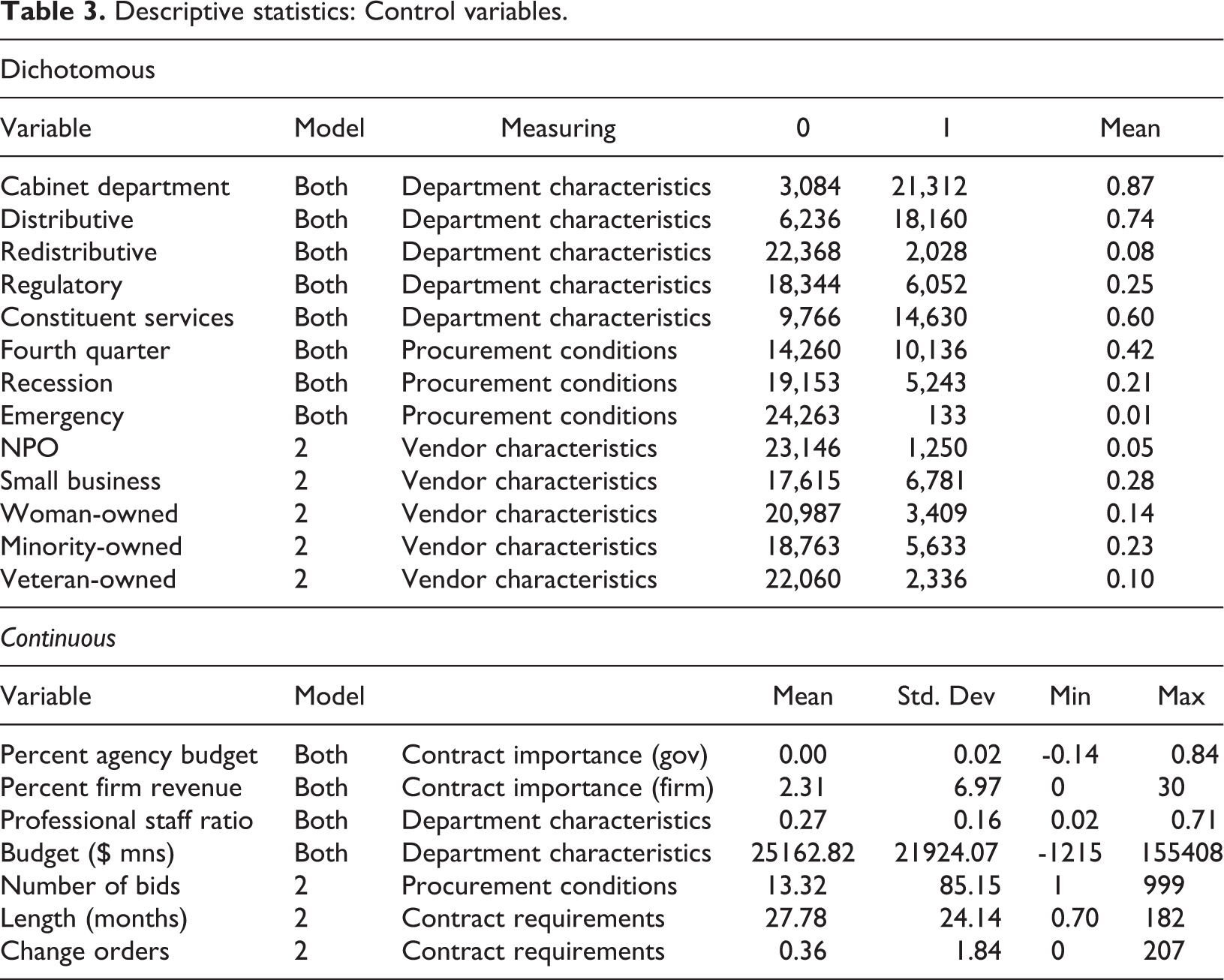

The unit of analysis for this research is the individual contract. The sample consists of the 24,396 federal definitive contracts which ended between FY2005 and FY2014. Definitive contracts are standalone agreements between the government and contractor for a particular good or service. To ensure completeness of records, the contracts in this dataset began no earlier than 1998. The average contract lasted for more than 27 months and involved the expenditure of nearly US$1.9 million. Ninety percent of the contracts in the dataset lasted for more than six months and involved expenditures over US$50,000. As a result, the dataset is comprised of contracts for fairly complex goods and services. Descriptive statistics for the explanatory variables used in this analysis can be found in Tables 2 and 3. 3

Descriptive statistics: Explanatory variables.

Descriptive statistics: Control variables.

To assess how financial structures are used and affect performance, the analysis uses two multinomial logistic (MNL) regression models. Each is described in detail below, including broad specifications. Both models use an unordered, categorical variable of interest, which is appropriate for MNL methods. Hausman tests indicate that the assumption of independence of irrelevant alternatives (IIA) is not violated in either model.

Model 1: What affects the selection of financial structures?

The first model assesses how federal contracting officials use different financial structures to respond to transaction costs and market conditions. The previous hypotheses hold that when markets are competitive and contracts involve low levels of asset specificity and uncertainty, contracting officials are more likely to use fixed-price pricing structures that shift the risk of performance to the contractor. When contracts are more complex and transaction costs are higher, contracting officials are more likely to use the other financial structures to incentivize bids and increase the exchange of information to facilitate contract management. To test this, the analysis models the effect of market characteristics, transaction costs, and control variables on the selection of contract financial structures. The model is specified conceptually below:

Model 1: Pr | Contract financial structures = competitive sourcing + transaction costs + department characteristics + contract importance + procurement conditions + e

In this model, the variable of interest is the financial structure used on the contract, operationalized as a “0” for fixed-price contracts, a “1” for cost-reimbursement contracts, and a “2” for time/labor contracts. The primary explanatory variables are competition and transaction costs (uncertainty and asset specificity). Competitive sourcing is a dichotomous indicator of whether the contract used competitive procedures or not. Competitive mechanisms include full and open competition, competition after exclusion of sources, and competition under simplified acquisition procedures.

This analysis focuses on two types of transaction cost: uncertainty and asset specificity. Consistent with literature in economics which finds that buyers are less likely to bid on riskier contracts ( Joskow, 1988; Lajili et al., 1997; Mithas, Jones, and Mitchell, 2008), asset specificity is operationalized as two dichotomous indicators based on the number of bids received. Contracts receiving just one bid, or sole source contracts, are indicators of high asset specificity, as market interest in the contract was low. Contracts receiving five or more bids are indicators of low asset specificity, as many bidders were interested in the project. Since previous researchers have found that government contracts are likely to receive approximately three bids, five bids suggests high competitiveness (Girth et al., 2012).

Uncertainty is related to the length of the contract, the complexity of the work performed on the contract, and the resources expended (Kim and Brown, 2012). Length is operationalized as a dichotomous indicator for contracts that last more than two years. A dichotomous indicator is used instead of the continuous measure of length for two reasons. First, previous findings have indicated that longer contracts are more likely to use cost-reimbursement and time/labor financial structures (Kim and Brown, 2012), so the indicator highlights these contracts. Second, an indicator variable makes interpretation of relative risks much easier, allowing for substantive discussion of findings. Total expenditure on the contract is operationalized as the natural logarithm of the total amount of funding obligated to the contract over its duration. To capture the complexity of contract requirements, the analysis includes a dichotomous indicator for all services, which are generally more complex to deliver than goods. 4 Also included are dichotomous indicators for professional services contracts, research contracts, and information technology contracts, each of which is acknowledged to be particularly complex types of work (Anderson and Dekker, 2005; Girth and Lopez, 2018). Contracts for these particular types of product can involve weaker markets, challenging requirements, and difficult evaluation criteria. To provide a foil for complex services, there is an indicator for construction contracts that have a strong market and clearer performance measures (Kagioglou, Cooper, and Aouad, 2001).

In this model, I use a number of control variables to account for contextual factors that might influence contract decision making. First, there are variables designed to control for differences between the contracting departments and agencies. This includes dichotomous indicators for cabinet departments, distributive agencies, redistributive agencies, regulatory agencies, and constituent services agencies. Due to the different types of work that these departments do, we might expect them to procure different types of things and to use slightly different procedures. In addition, I include the professional staff ratio of the agencies, which is calculated as the percentage of professional employees to total employees in the year of the contract’s initiation using data from OPM’s FedScope. Organizations require more professional staff to deal with more complex policy areas (Chun and Rainey, 2006). I also include the agency’s budget to capture size differences between federal organizations. Together, this group of variables controls for the impact of department-specific variation in contracting behavior, work requirements, and policy-area complexity.

Second, I include variables that account for the relative importance of the contract for the agency and the contractor: percent agency budget and percent firm revenue. To calculate these values, I divided the total value of the contract into the agency’s annual discretionary budget (from the Government Publishing Office) and the firm’s annual earnings (as reported in FPDS-NG). Contracts which account for a higher percentage of total spending are likely to be of greater importance to the agency, as well as to receive greater attention from political actors (Brown, Potoski, and Van Slyke, 2013).

Finally, I include variables that account for the practical context of each contract, particularly the political, economic, and managerial constraints placed on the public manager. These include dichotomous indicators for recession years, contracts signed in the fourth quarter, and emergency contracts. The Great Recession occurred during the period of this study. In response, federal government spending rose in a Keynesian attempt to counteract macro-economic forces stifling American economic growth (Gosling and Eisner, 2013), so both the downturn and the uptick in federal spending could affect my analysis. The federal budget cycle runs from 1 October to 30 September each year. Public finance literature suggests that in the final quarter of each year, there is pressure on public managers to spend their remaining budget to ensure similar funding levels in future years, and contracting is thought to be a common method used to do this (Lewis and Hildreth, 2011; Rubin, 2013). Finally, some contracts are written in response to emergency conditions. These contracts are not just for emergency response activities, but for other types of emergency, including repairs and other contingency contracts. Such contracts are not subject to all FAR requirements (FAR 1.602-603, 2014). In emergency conditions, requirements generation and contract planning may be less thorough, relying on contracting officials to make quick decisions using their expertise to preserve public values (Cooper, 2003). These three variables control for macro-level contextual factors that could influence federal contract managers.

Model 2: Does financial structure affect contractor performance?

The second model analyzes whether the financial structure of a contract influences contractor performance. The variable of interest for this model is the status of the contract at its conclusion. Federal contracts can end in closeout, termination for convenience, termination for default, and termination for cause. Termination for cause and termination for default are similar, indicating extremely poor performance. The distinction between the two relates to the type of good or service procured. Early termination for poor performance is catalogued as “for cause” when non-commercial goods are procured and as “for default” when commercial goods are procured. Terminations for convenience indicate that the contractor was performing poorly or that the government decided to change direction. Normal closeout reflects a wide range of performance, all of which are, at worst, acceptable. To address variations within the closeouts, the financial transactions on the contract are used to indicate performance. Previous studies have found that managers of poorly performing closeouts will reclaim funds for the government—that is, contracting officials opt to de-obligate much of the contract’s funding to preserve public value (Svabek, 2011; Wicecarver, 2012). Low-performing closeouts are those where more than half of the total obligations were taken back by the government. High-performing contracts, by comparison, are identified as those that did not have any money de-obligated. Essentially, the way that the contracting official handles the funding provides some insight into the performance across closeouts.

This variable of interest allows the comparison of contracts across a variety of types, purposes, agencies, and durations. Measures of a contract’s financial activity and end result rely on the contract manager’s decisions. Since the manager makes financial decisions and ends the contract based on the best information immediately available at the moment of the modification, he or she is best suited to judge the contractor’s performance. Modifications also have the benefit of carrying legal weight; these are not simply perceptual measures, but rather official determinations about what is necessary for contract management. Much of the previous research on government contracting has struggled to find ways to compare across large numbers of contracts. This measure allows greater comparability as it focuses directly on the manager’s documented assessment of vendor performance. There is no question that contracts terminated early for convenience, default, or cause represent poorly performing federal contractors. As a result, it is possible to make better claims about truly bad performance than about what leads to good or exceptional performance.

The primary explanatory variable of interest in this study is the financial structure of each contract, operationalized as dichotomous indicators for cost-reimbursement and time/labor contracts. Fixed-price contracts are the reference category for the variables of interest in this analysis. This approach facilitates the comparison of the less common contract structures with fixed-price contracts.

Model 2: Pr | Contractor performance = financial structure + contract requirements+ procurement conditions + department characteristics + vendor characteristics + e

The second statistical model incorporates all of the control variables used in the first model, and also controls for vendor characteristics, contract requirements, and procurement conditions during the period of performance. Characteristics of the contractor are also potentially important for contractor performance (Brown, Potoski, and Van Slyke, 2006; Smith and Fernandez, 2010). Recent work indicates that nonprofit organizations may have goals that are more closely aligned with public organizations, resulting in cultural similarities that could improve performance (Brown, Potoski, and Van Slyke, 2006; Van Slyke, 2007). At the same time, small-, minority-, veteran-, and woman-owned businesses are given preference in the source selection process, potentially influencing performance (Snider, Kidalov, and Rendon, 2013). To account for these different types of contractor, I employ the dichotomous variables for non-profit organizations, SBA-designated small businesses, woman-owned firms, minority-owned firms, and veteran-owned firms. To capture experience, I include a dichotomous indicator of whether the contractor has previous contracts with the same department or agency during the period of the study. Previous work suggests an existing relationship that may ease some of the tensions of contract management for both the vendor and the government, but can also create knowledge-based asset specificity that benefits existing contractors (Williamson, 1981).

Additionally, I include three variables to account for the complexity of contract once it is being managed: a count of the number of bids received, the number of change orders made to the contract, and the contract’s duration (in months). The number of bids received is a commonly used measure of market competitiveness (Brown, Potoski, and Van Slyke, 2013; Girth et al., 2012; Savas, 1977). Contracts that receive more bids are leveraging more competitive marketplaces. FPDS-NG includes information on the total number of bids received for each contract. To add granularity to the analysis, I include dichotomous indicators for contracts that receive only one bid (i.e., where markets are particularly weak), and for contracts that receive five or more bids (i.e., where markets are likely strong). Change orders are modifications that alter a contract’s requirements, scope of work, or other managerial elements. Change orders are common, but more change orders generally indicate that the contractor is in need of redirection (Kerzner, 2013). As such, more change orders may indicate a more difficult contract. Contract duration is an indicator of the complexity of the contract (Anderson and Dekker, 2005; Girth and Lopez, 2018), as well as of the duration of the relationship between the parties (Bertelli and Smith, 2010).

Results

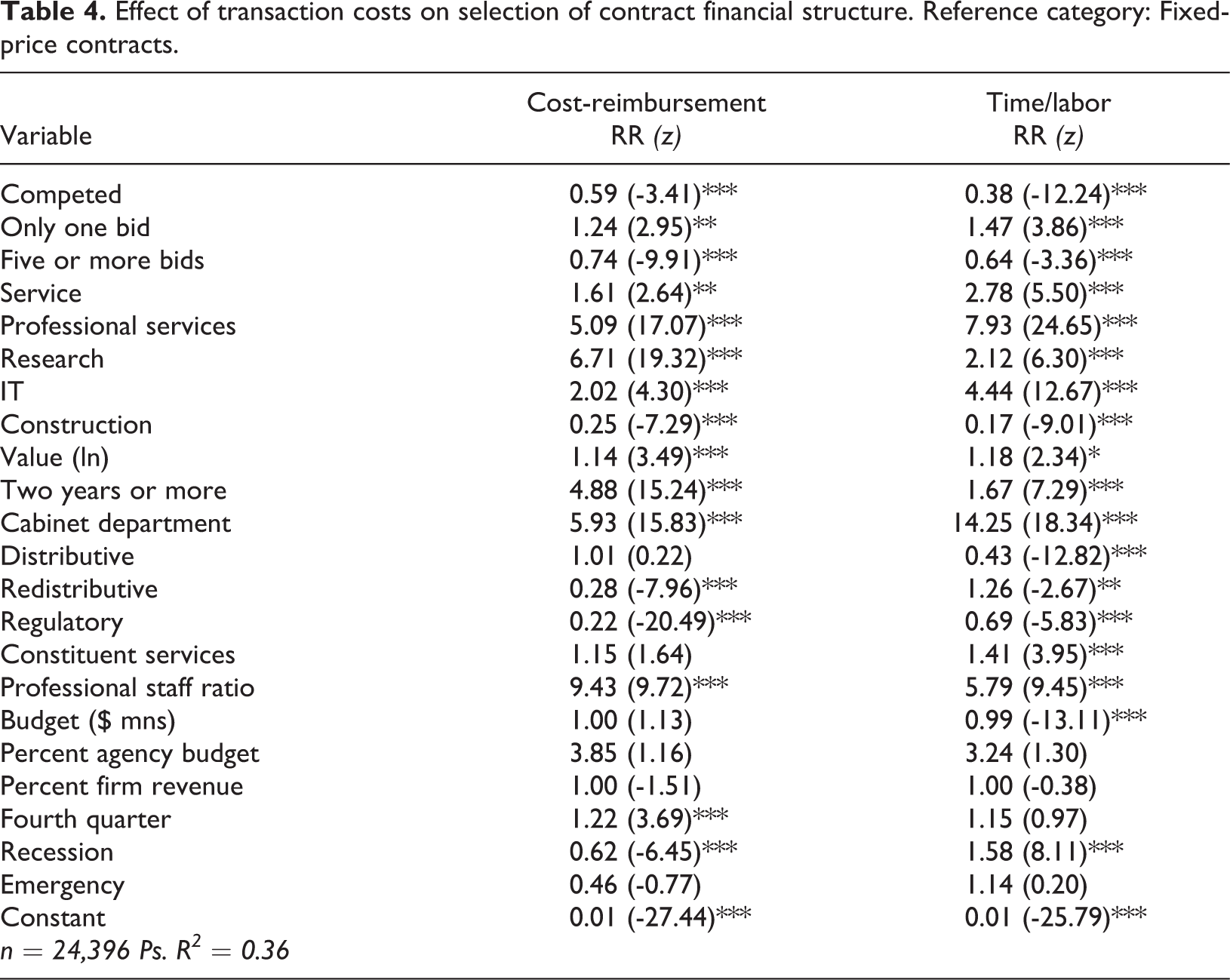

Complete results for the two models are presented in Tables 4 and 5. 5 Table 4 has results pertinent to hypotheses 1–7, dealing with the effect of transaction costs on the decision to use risker financial structures. Table 5 has results pertinent for H8, addressing the relationship between financial structures and contractor performance.

Effect of transaction costs on selection of contract financial structure. Reference category: Fixed-price contracts.

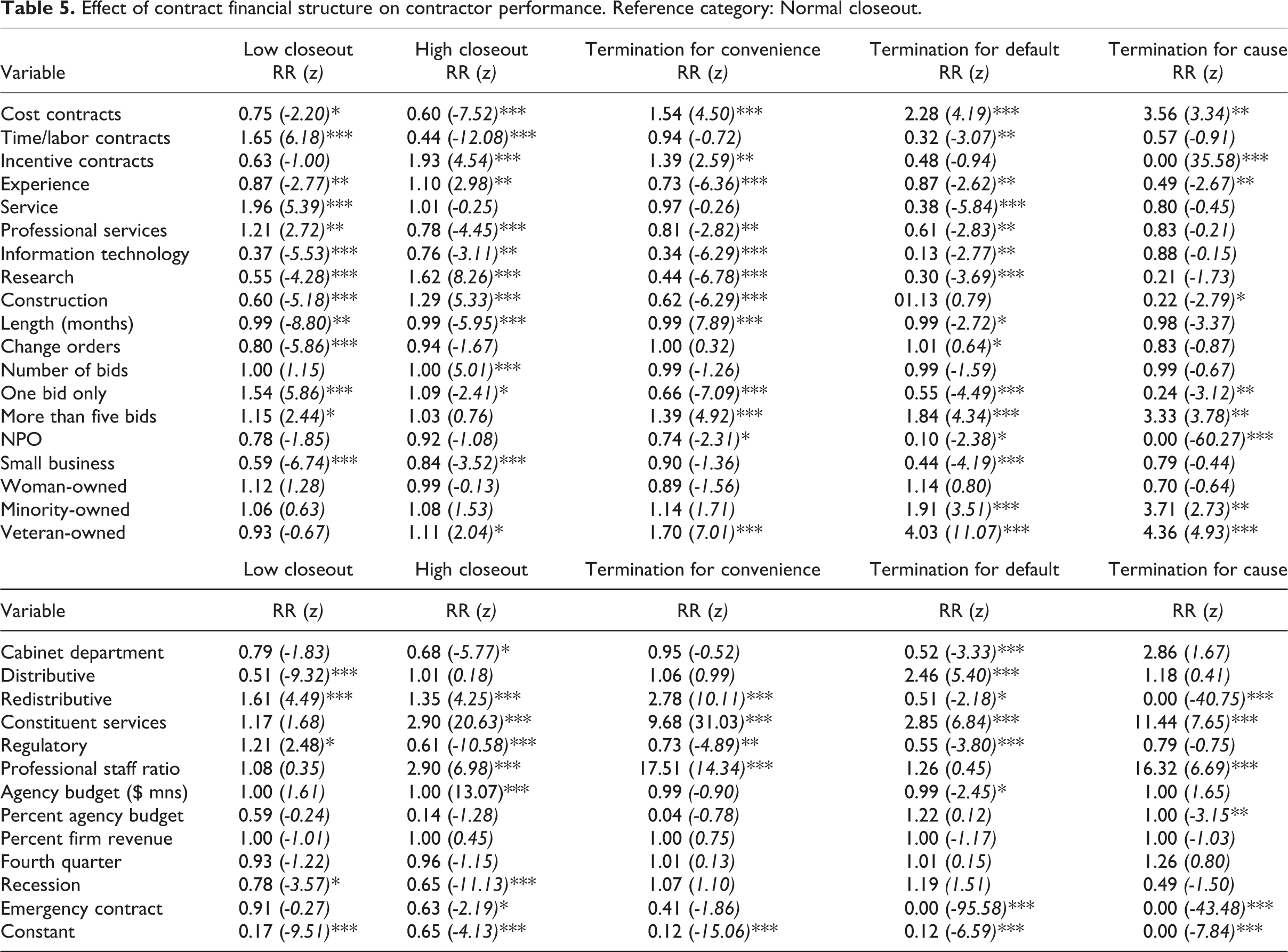

Effect of contract financial structure on contractor performance. Reference category: Normal closeout.

Contracts that use competitive sourcing procedures are 40% less likely to use cost-reimbursement financial structures and nearly one-third as likely to use time/labor structures. This indicates that contracting officials prefer to use fixed-price payment structures when they competitively source contracts. In this way, contract managers hope to shift risk for performance to the contractor when possible, benefiting from the presence of competition and the profit motive. This may also indicate that requirements generation and price-ceiling estimation are easier in competitive markets, as market research is possible. Hypothesis 1 is supported.

Contracts that receive only one bid are nearly 25% more likely to use cost-reimbursement structures and 50% more likely to use time/labor payments. This indicates that when markets are weaker, managers are more likely to select financial structures that ensure information sharing to reduce the chances of shirking and facilitate performance evaluation. Contracts that receive five or more bids are approximately 25% less likely to use cost-reimbursement or time/labor financial structures, indicating that managers are more willing to let market forces guide performance when markets are competitive. Taken together, these findings indicate that when there are few bidders, contracting officials employ financial structures that are more likely to attract contractors by guaranteeing cost reimbursement at bare minimum. This supports the idea that the number of bids received can be used to estimate asset specificity. Hypotheses 2 and 3 are supported.

Across the board, contracts for more complex services are more likely to use cost-reimbursement and time/labor payment structures. Contracts for services are 60% more likely to use cost-reimbursement and nearly three times as likely to use time/labor. Professional services contracts are more than five times as likely to adopt cost-reimbursement payments and eight times as likely to employ time/labor structures. Research contracts are nearly seven times as likely to reimburse costs and more than twice as likely to pay based on time/labor expended. IT contracts are twice as likely to use cost-reimbursement payments and more than four times as likely to make payments based on hours worked or labor expended. This is strong and substantive evidence that contracting officials react to uncertainty by employing financial structures that increase the exchange of information to ease oversight. On the other hand, construction contracts, where markets are strong and management procedures are well-established, are one-quarter to one-fifth as likely to employ either cost-reimbursement or time/labor financial structures. This provides both significant and substantive evidence that when contract requirements are well-defined and process uncertainty is low, contracting officials rely on market forces to hold contractors accountable. Hypotheses 4 and 5 are supported.

Other measures of contract uncertainty include the length of the contract and the amount spent on the contract. Contracts lasting more than two years are nearly five times as likely to use cost-reimbursement payments and nearly 70% more likely to use time/labor remuneration. As the value of contracts increases, they are also slightly more likely to use non-fixed-price payment structures. As a result, there is support for hypotheses 6 and 7.

Taken together, these findings provide substantive (not just statistically significant) evidence that contract managers use different financial structures in response to market conditions and transaction costs. This is consistent with theoretical work that indicates that this is how these mechanisms should be used ( Brown, Potoski, and Van Slyke, 2006; Williamson, 1979). In addition, it augments descriptive work that indicates that contracts with high transaction costs might use financial steps to reduce risk and encourage information sharing (Brown and Potoski, 2003b; Johnston and Girth, 2012; Kim and Brown, 2012). These findings demonstrate that contract managers are assessing market conditions and transaction costs prior to designing contracts, and that the decisions that they are making are consistent with the recommendations in public administration and economics.

The second model, displayed in Table 5, assesses the relationship between financial structure and contractor performance. Results indicate that cost-reimbursement contracts are more than one-and-a-half times as likely to terminate for convenience, more than twice as likely to terminate for default, and more than three times as likely to terminate for cause. Cost-reimbursement contracts are also 40% less likely to result in a high-performing closeout. These are both substantively and statistically significant findings, indicating a clear and meaningful relationship between cost-reimbursement contracts and performance problems. The first model indicated that cost-reimbursement financial structures are used on complex contracts where markets are weak and transaction costs are high. Such contracts are longer, involve higher levels of expenditure, and are more difficult to oversee. The financial structure used to reduce these concerns does not seem to improve performance. Instead, cost-reimbursement contracts are much more likely to terminate early, regardless of reason. This is evidence that contracting officials considering cost-reimbursement contracts might want to carefully review the decision to make or buy, as there is no evidence that such contracts perform well. Fixed-price contracts are much less likely to terminate early than cost-reimbursement contracts. Thus, there is some evidence supporting hypothesis 8.

However, time/labor hours contracts are one-third as likely to end in termination for default and do not significantly differ from fixed-price contracts with regard to terminations for convenience and default. This suggests that information exchange may be important for some types of risky contract. In these data, time/labor contracts are most commonly used for personal services, administrative and management support, technical assistance, and technical services. These broad categories include contracts for expert witnesses, subject matter experts, project managers, and program analysts. For services of this nature, contractors may perform a specific complex task that is related to a particular program or project. In these cases, although the work itself requires great expertise, the contract may blend into the government workforce as part of a larger team working on the initiative (Voelz, 2010). In many cases, the contract is with a single individual or very small organization. Time/labor contracts seem to allow public officials the ability to manage these kinds of relationship better. This provides evidence against hypothesis 8, showing that information sharing can be more effective than market forces in certain contexts.

Of the control variables, contract duration is statistically significant in four of the five outcomes, but not substantively important (relative risks approach one, meaning that there is no greater or lesser risk of termination associated with longer contracts). Experience seems to matter, as more experienced contractors are between 15% and 50% less likely to terminate early across all three categories. Incentive contracts are also interesting, as they appear to be more likely to terminate for convenience, perhaps giving credence to contractor fears that governments may be unwilling to pay their incentive fees or subject to unpredictable budgetary environments (Girth, 2017; Smith and Lipsky, 1993). Contracts that receive more than five bids are likely to terminate early, which makes sense given the ready supply of substitute firms available to take the place of the poorly performing contractor. Consistent with this finding, sole source contracts are much less likely to terminate early. Contractor ownership demographics have little substantive effect on performance, except in the case of nonprofits and veteran-owned firms. NPOs seem to be much less likely (30–90%) to terminate early, perhaps providing some credence to the stewardship arguments that other scholars have advanced about the benefits of goal-alignment between government and social sector organizations. Veteran-owned firms seem to be consistently more likely to terminate early. More research into veterans’ preference procurement programs is necessary to better interpret this finding.

Discussion

This analysis finds that transaction costs influence both the selection of contract financial structures and contractor performance. Specifically, contracts that have high levels of asset specificity and uncertainty are more likely to employ financial structures that facilitate the exchange of information and enable improved oversight. When transaction costs are high, managers select payment structures that either a) incentivize contractors to bid on risky work, or b) increase the information exchanged between the partners to improve performance assessment. Financial structures are used to overcome asset specificity problems by guaranteeing that the costs will be covered, limiting the risk associated with contract-specific investments. Cost-reimbursement and time/labor contracts are comparatively low-risk for contractors, as they know that their investments will be covered. For public managers, these structures require the regular exchange of information on how resources are being spent, making performance assessment easier. For complex contracts where work processes are perhaps unknown and the behavior of contractors might be suspect, regular information exchanges about financial management can reduce uncertainty. Findings indicate that federal contract managers employ cost-reimbursement and time/labor structures in ways that reduce transaction costs and manage risk associated with complex contracts.

It is worth noting the substantive meaning of the findings in this analysis. Cost-reimbursement contracts are associated with very high chances of early termination when compared to fixed-price contracts, ranging from one-and-a-half times to nearly four times as likely, depending on the type of termination. This means that engaging in such contracts is incredibly risky for public agencies, and provides evidence that the financial structure of the contract does not seem to address problems associated with weaker markets through information exchange. Despite efforts to lower transaction costs through financial structure, contracts that employ cost-reimbursement structures are much more likely to terminate early than other kinds of contracts.

However, time/labor contracts are much less likely to terminate early. Since the contract mechanisms are so similar—reimbursing contractors for incurred costs—this suggests that something specific to the cost-reimbursement financial structure might actually influence the likelihood of termination. In these data, the major differences between these two financial structures are the sourcing mechanism and the experience of the contractor used. Seventy-three percent of cost-reimbursement contracts were competitively sourced, while just 30% of time/labor contracts used competitive mechanisms. Sixty-eight percent of contractors working on time/labor contracts had previous experience with the agency, but only 27% of cost-reimbursement contracts went to experienced contractors. This indicates that time/labor contracts, although used for complex services, tend to rely on experienced contractors via sole sourcing. When sole sourced, time/labor contracts can include profit limitations, a fixed-price-like ceiling mechanism that leverages profit motive to spur performance (FAR, 16.601(c)(2)(ii), 2014). Cost-reimbursement contracts tend to attempt to use competitive mechanisms, but receive few bids; more than 42% of contracts received only a single bid. In addition, cost-reimbursement contracts tend to use less experienced contractors. Despite attempting to leverage market forces, cost-reimbursement contracts fail to do so. Time/labor contracts leverage financial incentives, information exchange, and inter-organizational relationships to reduce transaction costs as much as possible. Cost-reimbursement contracts are not able to leverage the financial structure or the experience of contractors to improve performance, and as a result are likely to terminate early.

Taken in sum, this discussion indicates that the financial structure of a contract is important for its performance. Although the structure selected is based on the presence of transaction costs, the findings indicate that subtle differences between the structures have meaningful effects on how contracts end. As a result, both the make-or-buy decision and contract design are particularly important. Existing literature suggests that such an examination should include an assessment of the values relevant to the contract (efficiency, effectiveness, innovation, etc.), the organizational structures that affect the contract, market characteristics, and the contract’s design (Brown, Potoski, and Van Slyke, 2006). The present findings indicate that if contracting officials cannot find ways to avoid cost-reimbursement methods, a careful look at the appropriateness of the contract is necessary. It might be less risky to make the good or service internally, instead of hiring a contractor. Market mechanisms, such as profit motive and competitiveness, are able to reduce the likelihood of termination more than processes that reduce information asymmetries.

Conclusion

This analysis finds that contract financial structures can be used to hold contractors accountable. Depending on the type of contract, both internal and external accountability mechanisms can be useful for public managers. When markets are strong and transaction costs are low, contracting officials can rely on competitive forces and profit motivation to hold contractors accountable. Fixed-price structures, which shift the burden of performance to the contractor, blend internal and external accountability mechanisms. External organizations, including market competitors and the government agency, hold that contractor accountable for their performance. At the same time, internal pressures to complete the work according to professional standards while preserving a wide profit margin motivate performance. This is consistent with findings in public administration that indicate that using a combination of accountability mechanisms is most likely to preserve public value (Gilmour and Jensen, 1998; Mulgan, 2000; Rhodes, 1997).

When markets are not as strong or when transaction costs are high, managers are forced to hold contractors accountable in other ways. When asset specificity is high, managers may need to encourage vendors to bid on contracts through financial guarantees. Cost-reimbursement contracts and time/labor contracts both offer more security to vendors, as any effort or investment made will be covered financially. When contract requirements are unclear or information asymmetries are large, these financial structures provide managers regular reports on contractor activities and expenditures. Under such structures, profit motivation actually encourages shirking and inefficiency, as more charging to the contract results in greater earnings. To make up for this negative incentive, public contracting officials require detailed information about performance. The findings indicate that information exchange has mixed effects. When regular communication is paired with financial incentives that encourage attentiveness in time/labor contracts, early termination is extremely unlikely. However, when information is exchanged without financial incentives, as occurs in cost-reimbursement contracts, performance suffers. Thus, contractor accountability is best when market forces can be leveraged, or when they can be paired with information exchanges that reduce uncertainty. Information exchange on its own does little to hold contractors accountable.

Kim and Brown called on public administration scholars to investigate how contract design affects contractor performance (Kim and Brown, 2012). This paper indicates that financial structures can influence performance in both predicted and unexpected ways. Public managers can use payments to hold contractors accountable, exchange information, and leverage market forces to influence performance. Market mechanisms seem to be more effective methods of ensuring performance than information exchange, but their simultaneous application may be the best way to preserve accountability while getting the best execution from vendors.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.