Abstract

The social relation between the platform and its users is defined by engagement with digital infrastructures and the rendition of this engagement into data. User-data, however, are surrounded by regulatory and legal ambiguities as they are not accounted for as intangible assets and their ownership and control are not transparent. I investigate how platforms rectify these ambiguities to realize user-data value as codified capital through an intensive case study of two major platforms. I use qualitative content analysis (QCA) to analyze annual and earnings reports, terms of service (ToS) agreements, and internal documents from 2017 through 2023 with qualitative data analysis (QDA) software. The findings reveal the exploitation of user-data ambiguities by platforms on two fronts: the necessary relationship between user-data inputs and platform outputs, with a growing emphasis on artificial intelligence, and the ownership and control of user-data. I argue that these ambiguities are exploited by platforms in a process of mystification of user-data to investors and other political economic actors at one end and users at the other. Mystified assets are then transformed into codified capital through financialization in the platform, contributing to studies of corporate financialization and fictitious capital. The findings place the ownership and control of user-data and their relationship to platform outputs as essential to advancing data accumulation and platform financialization.

Keywords

Introduction

Data are amassed from a wide and expanding array of sources: machine data from logistical operations, transportation, and other mechanics; data depicting a time and location of a transaction; consumer data composed of an immense sprawl of biographical and demographic data, purchasing habits, trends, and preferences; social data that is self-disclosed and made of photos, videos, posts, likes, clicks, and relational networks. Personal information in the form of user-data amassed through a new model of firm called the platform are relentlessly pursued at rampant volumes through old and novel methods.

User-data are unique in that they are not recognized or codified as capital and their status as property along with their ownership and control are ambiguous, particularly in a dynamic and uncertain regulatory environment. User-data are assumed to have inherent economic value realized by firms given the voraciousness with which they are cultivated from user interactions within, and often outside of, platform infrastructures; there is a presupposed direct line between data and capital. Given these a priori assumptions about data, how do platforms reconcile the regulatory and legal ambiguities of user-data as assets and of their ownership and control to realize economic value from them?

Transitions in digital political economy have led to a data-centered model of firm operations referred to as the platform business model. Platform firms 1 differ from antecedent models in a range of characteristics, including functioning as intermediary infrastructures, relying on constant user engagement, achieving a quasi-monopolistic scale of users through “network effects,” and a core dependency on data rendered from those who interact with their systems (users) (Rahman and Thelen, 2019; Srnicek, 2017; Van Dijck et al., 2018). User-data—personal information rendered into data through interactions with and through platform infrastructure—are a necessary foundation of the platform model. User-data have a growing presence in global political economy: “…we should now expect organizations to be data-driven; that is, the drive to accumulate data now propels new ways of doing business and governance” (Sadowski, 2019: 1).

I use an intensive case study of Amazon and Meta from 2017 through 2023 focusing on the outward-facing communications of firm reporting and terms of service agreements or user contracts to investigate how firms reconcile the ambiguities of user-data. I demonstrate throughout that platforms exploit user-data regulatory and legal ambiguities, blurring the connection between user-data and platform outputs and infrastructure through processes of mystification in order to realize value from mystified assets by converting them into codified capital while avoiding contentions of data property, ownership, and control. I argue that platforms reconcile regulatory and legal ambiguities of user-data by mystifying their ownership and control and their essential relationship to platform outputs to users on one end and to market and other political economic actors on the other. Platforms then market user-data outputs and infrastructures with emphasis on artificial intelligence to investors as a mechanism of value realization through market capitalization. In doing so the thread connecting the user and their data to the AI products and services that are marketed to entice investors is blurred. A purpose of mystifying the essential relationship between user-data and platform products, services, and infrastructures is to realize value from user-data without their legal or regulated (codified) recognition as assets, and without reconning property and ownership claims of user-data amidst a dynamic regulatory environment. This study contributes to investigations of the treatment of data by platforms and “big tech” and the evolving terrain of corporate financialization.

The article proceeds with conceptualizations of user-data as “mystified assets” and the processes of “mystification,” and a theoretical framework of platform financialization and codified capital. I then provide an outline of the methodology applied in the study followed by analysis of the findings. I end the article with a discussion of the mystification of the indispensability of user-data in platform outputs and contentions of user-data as property, and the transformation of user-data as mystified assets to codified capital through user-data securitization and platform financialization.

Regulatory and legal ambiguities of data

The ambiguities of user-data stem in part from their lack of recognition in accounting and financial reporting standards. In both the Generally Accepted Accounting Principles (GAAP) used in the United States and the International Financial Reporting Standards (IFRS) used in some 110 countries, data are not listed on balance sheets. Accounting scholars express frustration at the lack of recognition of data as firm assets in accounting methods and financial reporting (Klinge et al., 2022; Nani, 2023). More than a subtle oversight in reporting standards, user-data are not legally codified as assets or capital. In The Code of Capital (2019), Katharina Pistor argues that the codification of financial instruments and assets are selective and advantages groups that hold these instruments and assets over those who do not; “law is the cloth from which capital is cut” (209; Bilić et al., 2021: 70). Pistor's work is not exclusive to the platform, but the platform is unique in the absence of legal codification of data. GAAP and IFRS guidelines exemplify the Code of Capital in what are included and excluded as assets. The second source of user-data ambiguity within the platform is the absence of legal coding of property. There is general confusion and legal ambiguity over the separation between property, ownership, control, and access regarding data. Property and ownership are central to assets and codified capital. Absent clearly defined and regulated definitions of user-data as property and their ownership and control in a dynamic and turbulent regulatory environment, platforms are best served avoiding confrontation with this ambiguous area altogether while dictating the terms of user-data.

I follow a framework of assetization and datafication wherein data are thought to be assetized as an intangible asset class (Birch and Muniesa, 2020; Chiapello, 2024), and “in which data is created, collected, and circulated as capital” (Sadowski, 2019: 3). Birch et al. (2021) define assetization as “a mode of techno-economic ordering that helps to explain how the measurement, governance, and valuation practices used by political-economic actors transform personal data into future revenue streams” (2). Birch et al. used Security and Exchange Commission (SEC) records, earnings calls, and annual reports to examine the assetization of user-data in “Big-Tech” firms. They found few references to user-data within firm sources and that firms do not value data as goodwill or as recorded intangible assets (12). Rather, firms rhetorically convert data into metrics of users and user engagement within their platforms. This was most obvious in acquisitions where firms explicitly valued users and user engagement in innovations. These findings are significant because they point to firms framing user metrics rather than their data as the asset and source of value. Firms can sidestep the issue of data ownership by coding the right to access users as the fundamental contract as opposed to the ownership of data. Legal coding ambiguities do not allow firms to include data on balance sheets, but also permit firms to treat and present data in other ways. The authors refer to the presentation of data as user metrics as techcraft, “the performative transformation of personal data into user metrics that are measurable and legible to Big Tech and other political-economic actors” (2).

Continuing from the observation that user-data are not codified as assets and firms thereby perceptually transfer them into other metrics presentable to market and political economic actors, I theorize a process of exploiting the ambiguities outlined here to create “mystified assets.” Mystified assets are those central to a firm and from which they benefit absent regulatory or legal codification as assets. Note that a firm's ability to benefit from an asset's regulatory and legal ambiguities need not be exclusive to potential advantage from their clarification. Rather than clarifying the ambiguities of user-data as assets and their ownership and control, firms can exploit these ambiguities to further obscure the rendition and application of user-data and their role in platform operations, infrastructure, products, and services. I refer to the process of exploiting regulatory and legal ambiguities as “mystification.” Mystification describes the processes and mechanisms through which firms exploit or exacerbate regulatory and legal ambiguities of assets.

User-data remain a central feature of the platform while the details of their application and questions of their ownership and control are mystified to users, and their connections to platform infrastructure, products, and services are mystified to market and political economic actors. Exploiting ambiguities in financial and legal coding by platforms rather than clarifying them allows platforms to sidestep questions of whether user-data are—or normatively, should be—property, who owns them, who controls them, and how they are applied. Platforms then transform user-data as mystified assets into codified capital.

Mystified assets to codified capital

In examining the transformation of mystified assets to codified capital I follow two currents in financialization: corporate financialization and Marxian political economy perspectives. 2 Ben Fine (2013) describes financialization as the expansion of interest-bearing fictitious capital. This expansion occurs both within realms already occupied by finance capital as well as to new ventures. More than just intensive and extensive expansion of financial instruments or finance capital, Fine insists that financialization consists of “the subordination of such finance to [interest-bearing capital] in the form of assets that straddle the roles of money as credit and as capital,” as well as the globally uneven distribution of financialization (56). Crucially, the concept of fictitious capital is essential in the Marxian perspective of financialization.

Fictitious capital, “which ontologically cannot be separated from its legal form,” is particularly dependent on codification (Bilić et al., 2021: 70). The concept of fictitious capital stems from Marx's critique of classical political economy but remains a topic of scholarly discussion and debate. Michael Hudson (2010) places the concept of fictitious capital among classical political economists to explain the seeming “magic of compound interest” from spent capital and claims to future incomes: Instead of consisting of the tangible means of production on the asset side of the balance sheet, financial securities and bank loans are claims on output, appearing on the liabilities side. So instead of creating value, bank credit absorbs value produced outside of the rentier FIRE [finance, insurance, and real estate] sector (421, 424).

Palludeto and Rossi identify three necessary criteria for fictitious capital: dependence on future income, the presence of secondary markets, and real nonexistence. The authors point to capitalization of potential future incomes as the formation of fictitious capital, where “interest-bearing capital represents the commodification of money as capital, and the fictitious capital represents the commodification of future income flows as capital” (551). Secondary markets are essential to the formation of fictitious capital as this is where circulation takes place. Secondary markets create an alternate value of an asset through the commodification of a claim to ownership. The third criteria, real nonexistence, describes the title to ownership reified to contain its own value independent of the capital that it represents. I apply each of these criteria to the transformation of mystified (uncoded) assets to coded capital through financialization to realize value from user-data.

Klinge et al. (2022) use corporate financialization literature to demonstrate that Big Tech is leading corporate financialization. The authors apply three metrics to measure corporate financialization in Big Tech firms, including the platform cases Meta and Amazon: growing financial assets and debts, shifting asset structures with emphasis on intangible assets, and increased dividends and share repurchasing schemes to the benefit of the shareholder. The authors find four trends: higher than average profits with financial asset accumulation, asset structures reflecting increased mergers and acquisitions, increased debt leverage, and benefiting firm management through share price. The findings presented here largely support the conclusions by Klinge et al. but offer a mechanism of platform financialization unique to the ambiguities of user-data.

I combine theories of corporate financialization and fictitious capital with codified capital to assert that the unique status of user-data as uncodified and therefore ambiguous leads to a particular mechanism of financialization wherein user-data as mystified assets are transformed into codified capital through their securitization. This process relies on platforms mystifying the indispensability of user-data in artifacts and infrastructures to avoid contentions of user-data as property and their ownership and control. These marketable artifacts and infrastructures are dependent on user-data and increasingly feature artificial intelligence.

Method

I applied an intensive case study of Meta and Amazon in a seven-year period from 2017 through 2023 using close readings and content analysis. These two cases are top “big tech” firms and fit within conceptualizations of the platform (Bilić et al., 2021; Srnicek, 2017). these cases offer varying operational structures and dominant revenue sources. Amazon raises revenue through its marketplace, through subscription services, and through Amazon Web Services cloud computing. 3 Meta receives substantially all of its revenues from third party advertising to users (Meta Annual Report, 2021: 63).

I describe three data types: annual reports, earnings calls and shareholder meetings, and terms of service (ToS) agreements or “user contracts,” in addition to basic financial data and leaked internal and court documents. Data were obtained through the firms, from the SEC EDGAR system, Wharton Research Data Services (WRDS), ToS agreements from firms and through the Internet Archive “Wayback Machine,” and leaked documents from secondary gray literature and Harvard's “fbarchive.” I use qualitative content analysis (QCA) to investigate the textual data from the three data categories and supplement the study using financial data and leaked internal documents. QCA allows for systematically describing and inferring meaning from textual and other qualitative materials through category and coding schemes (Schreier, 2012).

The QCA began with conceptual analysis to determine the use and frequency of occurrences of concepts before moving to a relational analysis to interrogate relationships between concepts and concept occurrences in the data. Concepts and themes from the literature informed how to abstract the data categories and were used as a foundation in analyzing the text. This deductive feature was combined with an inductive approach of close readings and “rearticulation” of data in close connection to conceptual frameworks and theoretical underpinnings (Krippendorff, 2004: 17).

The structured content analysis approach was applied to annual reports, earnings calls, and ToS data for both cases, while financial statements, such as 8-Ks, and leaked internal documents underwent unstructured analysis to search for anomalous data. A total of 521 documents were reviewed, 268 in the three document categories revealing 22,652 quotations from three primary theme and three concept codes. I used Atlas.ti qualitative data analysis (QDA) software to apply a non-hierarchical coding structure to the data.

Three primary theme concepts from the literature were applied to the data: “user,” “data,” and “value,” with variations of these themes used in search terms 4 (Table 1). These concepts reflect how user-data, their use in platform outputs and operations, and their ownership and control are presented to both users and market actors. These three primary theme concepts were applied in various combinations and new concepts were used after initial analysis. For example, initial analyses found that artificial intelligence (AI) was a frequently used relevant concept in the data and a consultation of theory and the literature links the concept to the “value” theme. The resulting adjusted concepts used were “user engagement,” “user data,” and “AI,” with a multitude of related search terms. The following sections detail the study findings and followed by a discussion of the analyses.

QCA coding scheme.

Data and AI mystification

The two case firms exhibit similar trends in the data despite their differences in operations and revenue methods. Content analysis of ToS agreements, earnings calls, and annual reports revealed a rhetorical discordance between user-data and their AI outputs conforming to the theory of mystification by the platforms. “Data” was mentioned in earning calls and annual reports, but rarely in reference to user-data. Similarly, “user” was rarely in reference to user engagement or user-data. Terms associated with the “value” theme also rarely related to user-data. “Monetization” was a term used with some frequency within Meta data, but primarily regarding monetization of platform systems. Investors frequently raised the topic of WhatsApp monetization and the firm commonly responded with an ongoing platform strategy of accumulating a large mass of users (network effects) before applying a monetization strategy (Meta Earnings Calls, 2017–2023). The strategy revealed in later earnings calls was to draw users through WhatsApp into the broader platform system and more monetizable areas. Here we have an implicit reference to user engagement as a marketable metric of user-data (Birch et al., 2021).

Across both cases, “user engagement” occurred significantly more frequently in earnings reports (1164) than annual reports (474). The concept did not appear in ToS agreements. “User engagement” was less frequent in Amazon than in Meta occurring 19 times in earnings reports and nine times in annual reports. In Meta, “user engagement” occurred 1145 times in earnings reports and 465 times in annual reports while not occurring in ToS agreements. User engagement as a way of making user-data “measurable and legible” is evident in the case of Meta (Birch et al., 2021: 4), while Amazon had fewer mentions of user engagement in any of the data categories but maintained the same category division as Meta. Amazon does not publicly release active user metrics and no such metrics were found in the data. A close reading of Amazon document groups confirms a reliance on user-data with increasing efforts for user-data accumulation, like enabling Alexa to record “whispered speech” (Amazon Earnings Call Q3 2018). User metrification is a part of the “techcraft” of mystifying data and their role in developing products and services, and particularly artificial intelligence technologies (Birch et al.).

Meanwhile, “user-data” occurred frequently in ToS agreements (692) and less frequently in annual reports (386) and earnings reports (310). Conversely, “AI” terms were heavily featured in earnings reports (1909), less frequently in more public-facing annual reports (720), and rarely occurred in ToS agreements (10) (Figure 1).

Sankey of concept frequency in both cases.

“User data” maintains its cascading division between ToS agreements, annual reports, and earnings reports. “AI” terms occurred the most frequently of the concepts and featured heavily in Amazon data, occurring 606 times in earnings reports and 423 times in annual reports while not appearing in ToS agreements. “User-data” featured more prominently in Meta data overall maintaining a division between ToS agreements (525) and the other groups with a less pronounced descent between annual reports (356) and earnings reports (305). The trend of stark division between “AI” in investor targeted earnings reports and user targeted ToS agreements is present in both cases with Meta earnings reports leading with 1303 occurrences, followed by 297 in annual reports and only 10 occurrences in ToS agreements (Figures 2–4). These findings indicate a perceptual division between AI related outputs and the user-data on which they rely; user-data inputs are referenced without acknowledging their application in platform outputs to users while platform outputs are referenced without acknowledging their necessary relationship to user-data inputs to market and political economic actors in firm reporting.

Amazon concept frequency (left), Meta concept frequency (right), comparison of cases (bottom).

The perceptual divide trend noted above continues with “Data” having a low co-occurrence with “value,” coinciding in one percent of cases. Most of the co-occurrences between the two concepts in annual and earnings reports contextually refer to perfunctory fair value and financial data statements, while some refer to data value regarding value of added data centers in both cases (Meta “Notice of Annual Meeting and Proxy Statement” 2023, 82; Amazon Q2 2022 Earnings Call Transcript). These findings reflect the ambiguities of user-data as platform assets exacerbated by firms in their reporting. A potential reflection of user-data in firm assets is in tangible property rather than intangible assets. Birch et al. (2021) did not find an increase in intangible assets in “big tech” firms analyzed despite the common assumption that data must be reflected somewhere in intangible assets under the emerging data-driven capitalism. The increase in tangible assets in Amazon and Meta documented by Birch et al. ending in 2018 and 2019 respectively, is corroborated here (Figures 5–7). Data centers as tangible assets and the immense resources required to operate them may be a better indicator of user-data assetization in the firm than intangible assets, though there is no explicit acknowledgment of this tangible connection to user-data and firm outputs and infrastructure in the data analyzed.

Stacked area plot of firm assets. Stacked in order of tangibility beginning with intangible assets (cash and equivalents (CHE)) at the bottom and tangible assets (total property, plant, and equipment (PPENT)) at the top. Data from Compustat, WRDS. Based on Birch, Cochrane and Ward 2021, p. 8. Amazon (left), Meta (right), combined cases (bottom).

Co-occurrences further reflect the dissonance between users and assetizable value both within and between document groups. The highest co-occurrence of original concepts in the cases is between “user” and “data” with approximately 22%. Some mentions of “user” and “data” in the same sentence are not referencing information from users but rather information presented to users (Amazon Proxy Statement 2023, 82; Meta Annual Report 2021, 14). Despite the high frequency of both “user engagement” and “AI” in Meta earnings calls, there is low co-occurrence of the two concepts in any of the document categories across cases. Moreover, there are low co-occurrences of “AI” with any concept across all of the document groups for both cases (Figure 8).

Co-occurrences between concepts across all cases.

Low co-occurrence holds true when isolating “AI” and “user-engagement” in Meta earnings reports, the document group with the highest mentions of both concepts, with a co-occurrence of only 7%. Many of the co-occurrences found between “AI” and “user engagement” or “user-data” in both cases reflect applying AI-related technologies to users, their data, and the content they view, rather than the application of user-data and metrics in AI development (Meta Q4 2019, 22). In other words, in the few instances where AI and data terms appear together, the platforms are discussing how to apply AI to users and their data, not how users and their data are applied to AI.

The study shows disparate language used within both cases when external points of contact within the firm are abstracted into annual reports, earnings calls, and terms of service agreements. Amazon sees a starker division of concepts between document groups than Meta. Firms have some autonomy in reporting just as they do in selective opacity. For example, Amazon's AWS facial recognition cloud service, Rekognition, was not mentioned in any annual or earnings reports during the study period outside of proxy reports where a group of “shareholder activists” consistently contested its development and use by law enforcement and other entities (proxy statements 2017–2023). 5 This autonomy is reflected in mystifying connections between user-data and platform outputs between user contracts and investor marketing and reports. Artificial intelligence is an increasingly prominent concept used in investor-facing rhetoric in both study cases. The use of the “AI” concept in reporting, particularly the more investor directed earnings reporting, without its connection to user-data, and the inverse in user contracts, consistently through the study period can reasonably be asserted as a process of mystification by the firms. This perceptual disconnect in reporting as a process of mystification exploiting existing regulatory and legal ambiguities of user-data is expanded on in the following sections, beginning with an analysis of the findings on perceptually separating user-data from their necessary relationship to platform outputs followed by the mystification of the ambiguities of user-data control, ownership, and property.

User-data outputs: Services, infrastructure, and AI

There are numerous similarities between the two case firms despite their differences in business operations and organization. Both cases are seeking to expand critical infrastructures that third parties rely on through building new digital platform real estate. Meta has invested heavily in the Metaverse, a virtual reality interface proposed by the firm to be “the holy grail of online social experiences” leading to: … a massive increase in the creator economy and amount of digital goods and commerce. If you're in the metaverse every day, then you'll need digital clothes, digital tools, and different experiences. Our goal is to help the metaverse reach a billion people and hundreds of billions of dollars of digital commerce this decade. Strategically, helping to shape the next platform should also reduce our dependence on delivering our services through competitors (Meta Q3 2021 Earnings Call, 4).

Amazon calls their approach to building critical infrastructure to maximize their reach and importance in other systems “primitives,” individual foundational components designed to work together and be built upon (AR 2023, iii). AWS benefits Amazon through subscribers and users of other firms and platforms. Disney Plus, for example, is an AWS customer with over 150 million subscribers. Amazon is expanding its platform infrastructure in areas such as Amazon Pharmacy, Amazon One palm recognition service, and Sidewalk, “a low-bandwidth, long-range community network that connects devices across long distances where Wi-Fi and Bluetooth signals often cannot reach” (Amazon Q1 2023, 4). Amazon claims Sidewalk coverage reaches 90% of the US population and is courting internet of things (IoT) developers to adapt new product lines to the proprietary infrastructure. The most notable expansion for Amazon is generative AI. “Sometimes, people ask us ‘what's your next pillar? You have Marketplace, Prime, and AWS, what's next?’ … what's the next set of primitives you’re building that enables breakthrough customer experiences? If you asked me today, I’d lead with Generative AI” (AR 2023, vi). Establishing foundational and critical infrastructure is to create the very digital ground on which development takes place. Each of these critical infrastructures is dependent on user-data for their development and functionality. There is a dual relationship between infrastructure and user-data. Platform infrastructures are necessary to facilitate engagement and accumulate user-data, while simultaneously user-data are necessary to the maintenance and development of platform infrastructure. User-data are largely absent from reporting and marketing, but their connections to platform outputs are also excluded by platforms.

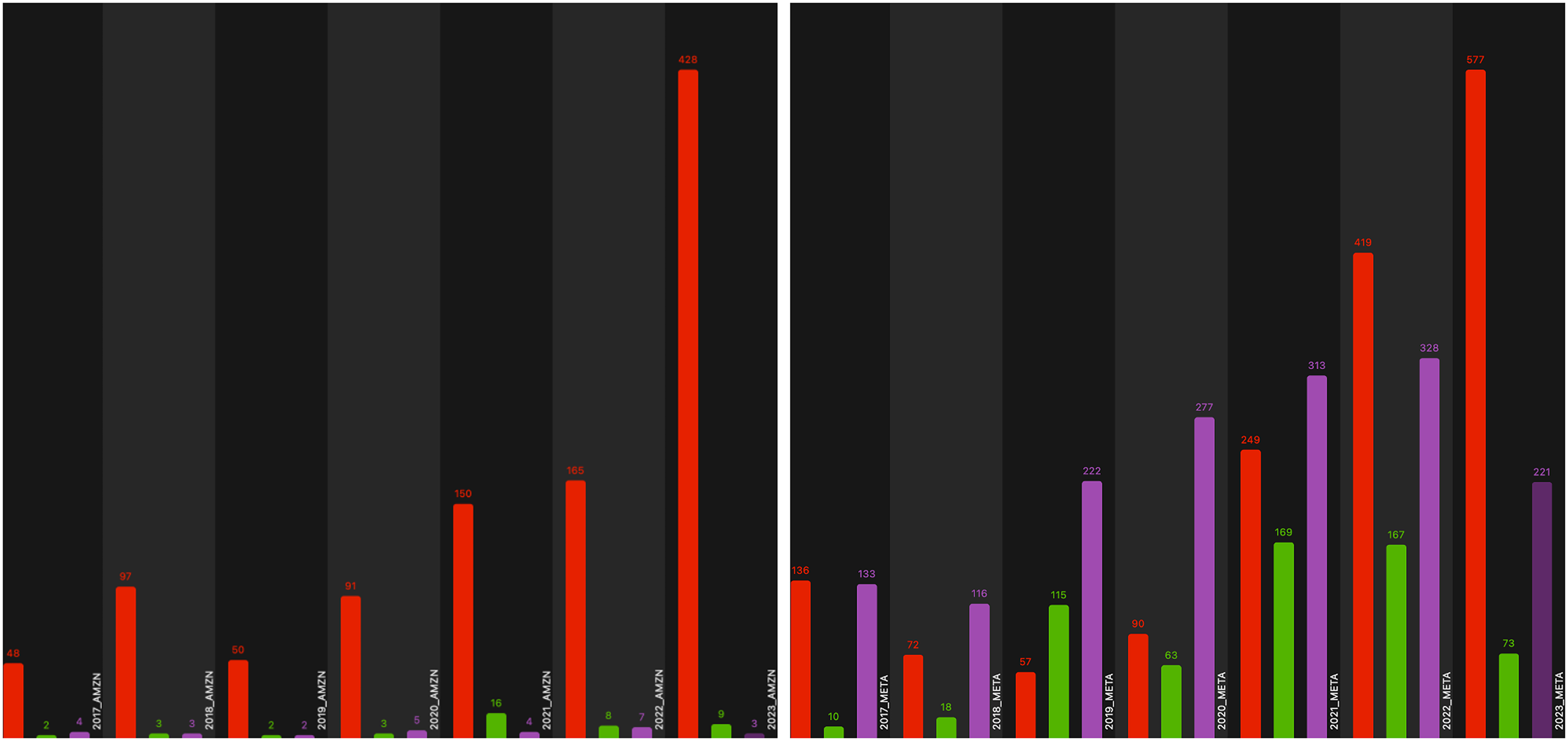

These findings of mystification are reflected in trends in the findings between the two cases in occurrences of the “AI” and “user-data” concepts. “User-data” appears dominantly in ToS agreements and the least frequently in earnings reports for both cases. “AI” was rarely mentioned in ToS agreements in either case while appearing frequently in annual reports and occurring most often in earnings reports in both cases. Another similarity between cases is the increase of “AI” occurrences over time. Figures 9 and 10 show that 2021 through 2023 saw the largest increase of references to AI related technologies in firm data with 2023 holding a substantial increase for both cases. Amazon and Meta both saw large increases in “AI” occurrences from 2020 to 2023, roughly 470% and 640%, respectively. Interestingly, Meta had a substantial decrease in occurrences of the “user engagement” concept alongside the stark increase of “AI” occurrences in 2023. Generative AI and other AI related outputs are strong indicators of mystification where their dependence on user-data is omitted from firm reporting and the application of user-data to develop and market these outputs are absent from terms of service agreements. AI outputs also appear to be displacing user metrics as a preferred method of presentation.

Bar graph indicating concept frequency for Amazon (left) and Meta (right) over time by year, 2017–2023. “User-data” displayed in green, “user engagement” in purple, “AI” in red.

Amazon and Meta share trends in concept use between categories. Meta utilizes the “user engagement” concept more frequently than Amazon, but findings reveal both firms have an increased use in the “AI” concept, particularly beginning in 2021.

Like platform infrastructures, products and services that fall under the artificial intelligence hypernym developed by platforms are directly linked to users and their information. User-data are used to develop, train, and test AI products and services, and the finished technologies are often used to render further user-data. This is the case for user demographic and personal information, purchase history and habits, geolocation, images on Instagram, voice and other audio input on Amazon's Echo, and all content used in the development of increasingly sought after “generative AI” technologies. 6 AI products and services are developed and applied back on users and to third-party customers, including other platforms. Referring to AWS customers, “people want to bring generative AI models to the data, not the other way around” (Amazon Q2 Earnings Call, 2023).

It is clear that user-data are vital to platform outputs be they services, products, or infrastructure, as well as the increasingly marketed AI outputs. Why mystify the connection rather than move to codify user-data as recognized assets or clarify their ambiguities to market and political economic actors? User-data are absent from firm reporting as assets or outputs due to their regulatory and legal ambiguities, but so are acknowledgment of their necessary relation to the platform outputs which rely on them in firm reporting and investor marketing. The mystification of this relationship through firm reporting exploits the ambiguities of user-data as assets allowing platforms to indirectly market them as mystified assets focusing on their outputs. Mystification serves a second purpose, to circumvent complications of property, ownership, and control of users and their data.

Property, ownership, and control

Data produced from users is most frequently referenced in ToS agreements. Such agreements are user contracts designed to dictate rules of engagement with platform infrastructure, the boundaries of information collection inside and outside of the platform, and control of data. User contracts establish control over user-data while remaining vague about what that entails; user contracts offer opaque frameworks for control absent conceptualizations of data property and ownership, and how the data are used. Explicit references to AI related product and service development and their use in enticing investors were not found, despite “how we use your data” sections in user contracts with disclosures of “to show you ads that are more relevant to you” and “to operate, provide, develop, and improve the products and services that we offer our customers” 7 (Instagram Terms of Use, 2022; Amazon.com Privacy Notice, 2023). Platforms exploit the ambiguities of user-data as property by mystifying the concepts of ownership and control through user contracts.

An incident of terminological slippage in user contracts reveals a rare reference to user-data as assets wherein Amazon explicitly states that if the company were acquired, “customer information will of course be one of the transferred assets” (Changes to the Privacy Notice, 2023, emphasis added). User-data are framed in another contract as owned by the user but licensed to the platform: When you share, post, or upload content that is covered by intellectual property rights (like photos or videos) on or in connection with our Service, you hereby grant to us a non-exclusive, royalty-free, transferable, sub-licensable, worldwide license to host, use, distribute, modify, run, copy, publicly perform or display, translate, and create derivative works of your content (consistent with your privacy and application settings) (Instagram Terms of Use, 2022).

Platforms mystifying data as property and ownership claims to their benefit as opposed to asserting property rights and ownership over user-data intersects with Katharina Pistor's propositions on the codification of capital (2019). Pistor argues that the codification of financial instruments and assets are selective and advantages groups that hold these instruments and assets over those who do not. Pistor's work is relevant to the financial and investment aspects of firms generally. What is unique about the platform cases is the absence of legal codification. GAAP and IFRS guidelines exemplify the Code of Capital in what is included and excluded as assets. It is unclear the extent to which the codification of user-data would be beneficial to platforms. 8 However, it is clear that platforms are able to maneuver the absence of data codification to their benefit. Platforms control and effectively own user-data, exercising property rights (transferability, unlimited use, universal and unending licenses, and so on) without the express codification or acknowledgment of user-data as such. Platforms create elaborate contracts granting near unlimited control of user-data while suggesting users retain ownership of their data. Platforms codify their own rules for data extraction in concert and contention with evolving regulatory landscapes. Platforms also tout their commitment to never sell user-data because data reciprocity, access, and service and infrastructure creation are not rivalrous transference of ownership. That platforms mystify the role of user-data in the products, services, and infrastructures that they exchange and securitize is possible through the absence of the codification of user-data as property and assets.

Far from refuting Pistor's argument, I argue that this demonstrates its importance. Platforms are able to exploit the gap in codification while circumventing issues of property, ownership, and control by mystifying the essential relationship between user-data and platform outputs: products, services, and infrastructure. User-data are foundational and essential to these outputs, but platforms mystify or perceptually minimize their connection. These outputs are skewed heavily towards those branded as artificial intelligence, currently an attractive label to investors and other political economic actors. Platforms could benefit from the codification of data as a recognized asset. Nevertheless, platforms are able to benefit from the current ambiguities of user-data by mystifying their connection to outputs and avoiding contentions of property. User-data can then be transformed from mystified assets into codified capital through financialization.

Platform financialization

The direct monetary conversion of user-data, such as through their sale or treatment as a traditional commodity, is not necessary to realize value: “There are a group of customers who use our devices and then we monetize that in different ways to commitment to Amazon and the video and everything else.” (Earnings Call Q4, 2018). Capturing as many users, their engagement, and their data as possible are a primary concern of platforms. Shareholders often asked about the monetization of platform segments in the cases observed, and the firms responded with the goal of creating network effects through attracting some critical threshold of users: “And then once we get to many hundreds of millions of people or billions of people using it, then we'll focus on ramping up the monetization, which has been a formula that's worked for us. That's the general approach” (Meta Earnings Call Q4, 2022: 9). Investors are concerned about the monetization of platform segments that do not generate revenue, but user-data from those segments and elsewhere are financialized; they are informally securitized and marketed to investors through their mystification.

Data securitization

User-data comprise unique assets that they are not directly accounted for as an intangible asset class. Like goodwill, user-data are unidentifiable as intangible assets. Unlike goodwill, user-data are not quantifiable in platform acquisitions. User-data are mystified assets given their mimicry of traditional assets but with a lack of financial and accounting regulatory norms that follow traditional assets and their securitization, ambiguities that are exacerbated in platform reporting. This is evident in addressing user-data directly and particularly their possession and control in user contracts contrasted with annual and earnings reports. User-data, therefore, are not standard assets and do not follow standard processes of securitization where they are bundled and passed through special purpose vehicles (SPVs) to directly back securities. 9 Nevertheless, user-data are informally securitized through a process of mystification into securities in the platform.

Shoshana Zuboff (2019) describes securitization through a “behavioral futures market” wherein platforms and third-party advertisers contract a payment for a future deliverable of human behavior in click-through rates or other metrics of interaction with advertised content (2019: 8, 86). Zuboff offers one mechanism of derivative securitization available to advertising-based platforms, such as Meta. However, not all platforms operate solely or dependently on advertising to users and derivative user securities. Behavioral futures contracts are determined through metrics of click-through rates and other measurements of user interaction with advertisements, a metricized obfuscation of user-data that is activated in some platforms to appeal to investors and increase the value of firm common stock directly. 10 As noted, not all platforms apply “user engagement” metrics in their reporting, though “AI” is increasing in the cases examined as a concept used in firm reporting to appeal to investors. User-data are informally securitized into share value and market capitalization through market-to-market stock valuation by mystifying their indispensability to the platform generally and in creating and maintaining outputs marketed to investors. User-data equity securitization is likely the most ubiquitous form of data securitization in the platform and the central focus of financialization in this study.

User-data also plays an informal role in debt securities in the form of bonds, which Amazon and Meta have issued for tens of billions of dollars in recent years (Amazon Form 424B3, May 2018; Meta Form 424B3, November 2022). Platform bonds are not typically backed by specific assets but their overall ability to pay, in which assets are considered. User-data are not factored as an asset directly but are essential to platform operations, revenues, and services and products, whether in advertising, subscriptions, or AI outputs. In other words, debt securities market a debt contract between the firm and financial institution as a tradable commodity. In this way it is not user-data or firm assets that platforms directly securitize. However, the loan that is securitized is backed by collateralized assets, either by specific assets or in the firm's overall operations and value should it fail to pay. Debt equities issued by the platforms securitize a debt agreement with a financial institution either backed by specific assets or, more typically, debentures backed by all platform assets, to which user-data are essential. The firm's total assets—in this case dependent on and built from user-data—are fundamental in determining the details of the loan and back the loan that is securitized, sold, and traded in secondary markets.

A firm issuing securities and collecting user-data, no matter how voraciously, does not necessarily mean that data are being securitized by the firm. However, the evidence outlined in this study suggests the informal securitization of user-data by the platform. The case of Meta is clear in marketing metrics of user-engagement and average number of active users in a set period to entice investors. As previously noted, user-engagement is a proxy for user-data. The Amazon case is less clear as it does not directly market user-engagement to investors and does not release metrics of active user engagement with their platforms. Nevertheless, AI appears to fulfill the same obfuscatory function as user engagement and much of Amazon's achievements marketable to investors goes beyond retail revenues. 11 The outputs marketed to investors by the case firms are dependent on user-data inputs. The following sections discuss the conversion of user-data as mystified assets into codified capital through corporate financialization and Marxian fictitious capital perspectives on financialization.

Corporate financialization

Klinge et al. (2022) describe three aspects of corporate financialization surrounding so-called big tech firms, including the two platforms examined in this study: expanding financial assets and debts, augmenting asset structures, and maximizing shareholder value. The authors establish these trends in Amazon and Meta; both firms have engaged in immense stock buyback programs and command rent incomes through control of intangible assets, despite the relative increase in tangible assets shown in Figures 5–7. Two additional mechanisms for corporate financialization found in the platform cases are incorporating financial services as part of platform operations, and the securitization of what many lament as unreported firm resources.

First, platforms like Amazon and Meta trade equity stock as well as immense debt securities through corporate bonds, but they are also more deeply entangled with the financial sector. Amazon's AWS hosts numerous major banks, online bond markets, and has its own business lending and credit services enabled by its partnership with finance (8K April, 2023; Earnings Call Q1, 2020). Amazon has also entered cash advance and lending services through the introduction of its own platforms (Amazon Press Center, 2022). In November 2023, Amazon and Citibank agreed to an unsecured five-year revolving credit line of $15.0 billion, and a short-term credit line of $5 billion. The agreement replaced a similar agreement with JP Morgan Chase. The new credit line has an interest rate of 0.45% and a commitment fee of 0.03% on any undrawn portion (Amazon 8-K November, 2023). Meta, meanwhile, allows cryptocurrency (securities) payments through Meta Pay after shuttering attempts to create its own cryptocurrency called Libra. Meta discontinued its trading platform Novi around the same time it filed five trademark applications involving digital assets, gaining the attention of some lawmakers (U.S. House, 2024). Both firms leverage their network effects to offer their own payment methods and platforms.

Second, Klinge et al. point to the frustrations lamented by scholars and practicing accountants about the uncodified disposition of data in firm financial reporting and acknowledge that “data do not by themselves constitute a revenue-generating asset but become an indispensable input for the production of knowledge” (2022, 4). The transformation of these mystified assets into codified capital through securitization is itself a mechanism of financialization unique to the peculiar status of user-data. Not the exclusive means of value realization from user-data, mystifying the indispensable and internal connections between user-data and platform outputs in order to indirectly market user-data to investors while circumventing obstacles of property and codification is a means of financialization. This particular mechanism is specific to the aforementioned obstacles of property and codification, but the endeavor of mystification demonstrates a drive for finance capital beyond profit.

The authors point out that methods of financialization are not homogenous in firms, and that financialization does not replace but augments practices of accumulation in firms: “we do not consider corporate financialization an alternative accumulation or governance strategy in and of itself but view it as a means to augment existing operations and strategies by embracing a range of financial practices made possible by the broader development of financialized capitalism” (05). Expanding to offer financial instruments are also an augmentation of platform operations rather than an emerging central focus. These mechanisms of platform financialization contribute to corporate financialization literature. However, the securitization of uncodified user-data and primacy of market capitalization suggests that intensive and extensive expansion of financial operations in general are subordinated to fictitious capital as suggested by Fine (2013).

Fictitious capital

The role of fictitious capital in the platform is examined through three criteria established by Palludeto and Rossi (2022) beginning with the dependence on future income. The structure of the platform is dependent on the continuous flow of users and user-data, while user contracts secure future flows of data from engagement on and off of the platform. The firm then extracts rents in the form of data and monetary subscriptions from users, and monetary payments and “reciprocal data” from third parties ( Six4Three, LLC v. Facebook, Inc. : 19, 25). User-data is the basis of future income flows in the platform whether from monetary payments for advertising to users, subscriptions (a contract for future payments), or future data flows guaranteed through user contracts. Additionally, platforms appeal to investors with future incomes from real monetization and more efficient data extraction, and abstruse assumptions of unrealized future applications and value of both data and AI generally.

Second, the reification of fictitious capital as autonomous and naturally occurring phenomena takes shape in secondary markets. The secondary market differs from a primary market in that only claims to ownership are exchanged in the former. Platform-related secondary markets are largely unremarkable from other firms in that stocks and bonds are traded as claims to ownership of equity and debt. The departure from other firms is that the capital and future incomes in question are centered and dependent on user-data. A secondary market of user-data is not necessary for a secondary market based on user-data, though secondary markets of users also exist. 12

Finally, the real nonexistence criterion is where fictitious capital is fully reified as a financial artifact independent from the future incomes it is supposed to represent. Palludeto and Rossi use the example of fixed capital, a machine that is both associated with future incomes and sold on a secondary market. The machine does not represent fictitious capital since it does not meet the requirement of real nonexistence. It is in claims to ownership of the machine traded separately with their own exchange values that completes the reification of this fictitious capital as an outwardly autonomous commodity seemingly removed from the social relations of capital (2022: 553). Real nonexistence is paramount to the platform. Securities derived in the platform are fetishized like in any other firm; platform securities take on their own exchange values and appear to move independently of any future incomes. Additionally, real nonexistence describes the seeming autonomy of platform securities because while there are claims of ownership to future incomes, monetary or data, and ostensibly claims to ownership to capital assets in the firm, claims to ownership of user-data—the essence of platforms—are rigidly avoided.

Dependence on future income, the presence of secondary markets, and real nonexistence are all present in platform financialization through data securitization. This definition of fictitious capital is applicable to securities markets generally and is not unique to platforms. What is unique in fictitious capital through platform financialization are the core dependance on user-data, the processes of mystification of the necessary relation between user-data and platform outputs and of property, ownership, and control of user-data, and the transformation of user-data as mystified assets into codified capital through their informal securitization. Securitization of the user is not without precedent, the conversion of social relations into fictitious capital occurs through “the securitisation of workers’ debts and mortgages” (Palludeto and Rossi, 2022: 550). User-data securitization is an expansion of this sort of financialization by converting more of everyday life into tradable claims. The concrete value of user-data is not quantified and standardized; what is taken as a certainty is the eventual use and value of data, leading to the ubiquitous capture of data for potential future value. Absent the acknowledgement of user-data as actually controlled and effectively owned by the platform, fully reified and seemingly autonomous claims to future user-data and derived monetary incomes are the primary financialized expression of the platform.

Michael Hudson (2010) suggests that fictitious capital is not a divergence from ‘real capitalism’ but has been a permanent feature of capitalism since its emergence. Hudson details the symbiotic relationship between finance, insurance, and real estate (FIRE) sectors, “junk accounting” in leveraged businesses, and the pursuit of monopoly rentierism in expanding fictitious capital (425). The processes of user securitization and fictitious capital formation through mystifying user-data detailed here are nascent and evolving, prompting further examination of platform relations with the FIRE sectors, as well as developments in the control and ownership of user-data as property and the mystification thereof.

Conclusion

Regulatory and legal ambiguities surround user-data in platforms. User-data are not a standard asset class in firm reporting and their standing as property along with their ownership and control are not clear. Such ambiguities provide platforms latitude in their presentation and application of user-data. Platforms exploit these regulatory and legal ambiguities through a process of mystification on two fronts. The necessary relation between user-data inputs and platform infrastructure, products, and services outputs along with the standing of user-data as property and their ownership and control are mystified to market and political economic actors on one end and users on the other through firm reporting and user contracts. The process of mystification demonstrated here allows platforms to rectify regulatory and legal ambiguities by transforming mystified assets to codified capital through their financialization.

The findings of the study contribute to corporate financialization literature and Marxian theories of fictitious capital in platforms by demonstrating the financialization of user-data as mystified assets into informal securities. Rather than directly marketing user-data or acknowledging their indispensability to platform outputs, platforms perceptually separate user-data from the outputs, particularly AI related outputs, marketed to investors and political economic actors. User-data are not traded as traditional commodities or recorded as standard assets, but as mystified assets are informally securitized and marketed to investors through their dependent outputs. These securities do not follow the formal processes of bundling, passing through a financial vehicle, and converting into marketable securities. The platform as a whole and particularly investor marketable outputs are dependent on user-data. The mystification tendency can be explained by securitizing users as a means of realizing value from inputs that are not directly sold, marketed, or accounted for, but are nevertheless understood to be of value and are fundamental to the essence of the platform.

Platforms mystify the essential relationship between user-data and platform products, services, and infrastructures rather than acknowledging or attempting to clarify their ambiguities or confronting property and ownership claims of user-data, seizing on the difficulties of regulatory and institutional bodies to quickly adapt to the high dynamism of technological development. Pistor's Code of Capital describes the power of legal codifiers to decide what is and is not capital to the benefit or detriment of select actors. This study highlights where firms can exploit gaps in codification just as they can the application of legal code and regulation. In Amazon and Meta, the platforms exploit a regulatory gap by avoiding addressing data as property and formalized claims to ownership. This is not to say that platforms would not benefit from the codified recognition of data as accountable assets that are owned, quantifiably valuated, and necessarily classified as property with clear boundaries of ownership and control. However platforms could benefit from codified and assetized data property, they do benefit from the absence of codification and avoidance of property issues, particularly in an unpredictable and dynamic regulatory environment.

Along with issues of data privacy and security in critical data and policy approaches, the determination of data as property and their ownership, and perhaps more importantly, their control, are fundamental normative and policy issues. However, it may not be as simple as crafting data governance that codifies, regulates, and enforces data as property of the user with clear ownership titles. In other words, I do not anticipate changing GAAP and IFRS guidelines to include data or enforcing the codification of data as property, whether owned by the firm or the user, to be normatively transformative. Explorations of comprehensive policy to address ethical, privacy, and security concerns of data and AI will need to address the dual issues of the absence of codification of user-data as property with concerns over ownership and control, as well as the codification of user-data property laws and regulations that could just as easily exploit users as data yeoman left to sell the rights to their digital approximations. The control of user-data and their rendition at the outset, as well as the logics motivating these pursuits, are more consequential conditions for user-data value realization than their codification as property and ownership. It remains essential to interrogate the substance and appearances of emerging technologies, the building blocks on which they rely, and the social relations altered and forged through them as our data and the infrastructures built to extract them may outlast the very firms responsible for their creation. The growing social, economic, and political power of personal information wielded through platforms as user-data is reshaping relations across these domains. Demystifying user-data in the platform is essential to understand the advancing imperative for data collection, and subsequently to confront it through normative or positive approaches.

Footnotes

Acknowledgments

I am grateful to Tim Luke, Giselle Datz, Besnik Pula, and Chad Levinson for their guidance while developing this project. Many thanks to the reviewers for their insightful help improving the paper. I am particularly grateful to Kean Birch for his invaluable critique and suggestions for improvement. Portions of this article received helpful feedback at the International Studies Association annual convention in Montréal, Canada in 2023.

Data availability statement

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.