Abstract

Attempts to use Big Data to transform car insurance pricing in France have failed. Why? Three possible explanations are discussed: organisational and cognitive inertia, normative preventions, and deliberate strategy. This article finds that moral or political reluctance has played only a secondary role in the failure of telematics devices. More important has been the deployment of an experimental strategy that has resulted in the conclusion that in the short and medium term at least, the use of big data to rate car insurance is not profitable. There are too many organisational and cognitive barriers to the smooth adoption of innovation. All insurers note they all arrived at this conclusion. An implicit consensus therefore remains to retain the old business model.

Insurance has been based on the principle of risk pooling since the end of the 18th century (Daston, 1986). Although this principle is in part normatively motivated (Ewald, 1986), it is largely motivated by technical considerations. 1 The purpose of insurance is to protect against risk, but when an insurer is deciding to accept or refuse a potential client, they are not in a position to know whether this particular client will actually face the risk against which they wish to be covered. The insurer can, however, know whether, on average and within a given population, one individual in 100 or in 10,000 will see the risk materialise. This form of prediction became possible in the second half of the 18th century, with the development of probability calculations and the first databases. The pooling of risks helps insurers to make more informed decisions: What risk do they face providing this service to a given individual? At what price?

One might be tempted to assume that the emergence of so-called “Big Data” would disrupt this economic model. Certainly, a large number of recent publications have made this assumption. Some actors in the field, such as supervisors (ACPR, 2018; EIOPA, 2019) or consultants (Balasubramanian et al., 2021; Deloitte, 2016), have advanced this prediction in primarily technical terms. Others have been more critical in their predictions (O’Neil, 2016; Zuboff, 2019): for them, the growth of Big Data opens the door to a dark future of mass surveillance, regulated behaviours, and individually targeted prices.

From varying perspectives, these publications concur that Big Data promises to upend the very concept of risk pooling as a guiding principle in the field. In a traditional insurance relationship, the insured knows more than the insurer about the risk they carry (Akerlof, 1970): whether they drive too fast, brake too suddenly, or forget their turn signals. By contrast, the insurer simply knows that, on average, individuals who share certain characteristics (age, occupation, gender, etc.) are more or less likely to engage in risky driving. By collecting a large amount of information on the driving habits of their policyholders, insurers seek to reverse this asymmetry. Big Data promises insurers a more fine-grained representation of each policyholder, and with it a more individually tailored risk assessment. Rather than assigning individuals to rate categories, to which a tariff is applied, it is a question of making everyone pay for their own risk.

The big data revolution is projected to have the most significant impact on two types of practices: health and driving. For the latter, driving habits are recorded by a “telematic device,” either via a phone application or a box installed in the vehicle. The data thus recorded could be used in addition (or instead of) the data traditionally used by insurers (policyholder age, profession, individual accident history, etc.). This combination, or substitution, raises several types of challenges. The first is technical. In the traditional pricing system, data used to calculate insurance rates are easy to collect from vehicle owners themselves, through a questionnaire. By contrast, telematic rating systems collect data in real time. These data are far more abundant, posing an epistemic challenge (Kitchin, 2014). Whereas insurers have traditionally relied on stable and parsimonious sociographic data (age, place of residence, profession, etc.), telematics is meant to generate data that are more voluminous, produced in real time, heterogeneous in nature, fine-grained and extensional (new fields can be easily added), potentially calling for new processing methods. Traditional data processing methods, such as actuarial methods, are designed to produce information from rare, static and clean data, built from strict hypotheses. Because Big Data, by contrast, requires methods capable of dealing with its abundance, heterogeneity, intertemporal evolution, messiness and uncertainty, its introduction into the field of car insurance would seem to augur epistemic rupture. The last challenge is normative: because its economic model is that of mutualisation, insurance operates on a principle of solidarity among policyholders (Ewald, 1986). Everyone pays for the few affected by the occurrence of a loss. Theoretically, Big Data allows insurance to operate differently, demanding that each person pays for their own risk. From this perspective, keeping the promises of Big Data would constitute a normative revolution (Meyers and Van Hoyweghen, 2018).

As this brief overview makes clear, a revolution is underway in the insurance sector – theoretically, at any rate. However, as McFall et al. (2020) point out, the publications describing this revolution have provided little empirical evidence to support their claims. Certainly, some companies are making use of these new tools. But these insurtech start-ups (Lemonade, Theranos) have been more effective at changing the discourse around insurance than at devouring the market share of old-school insurers (McFall et al., 2020). Similarly, in the United States, it is true that insurers are using credit scores to price home (Prince and Schwarcz, 2020) and car insurance (Kiviat, 2019). In Europe, though, there is little to no empirical evidence that any revolution is taking place. In the health sector, for example, Jeanningros and McFall (2020) have shown that in France, the implementation of behavioural insurance is largely incomplete. Similarly, in the field of motor insurance, efforts in Belgium to test telematics devices have been a massive failure (Meyers and Van Hoyweghen, 2020). And because data is lacking, Barry and Charpentier (2020) note that the models discussed by academic actuaries to price automobile contracts remain highly traditional. It would seem that the implementation of telematics devices has only added to the list of Big Data failures (Reggio and Astesiano, 2020): while Big Data analytics promise to radically disrupt certain markets, their implementation often leads to more modest results (Kusi-Sarpong et al., 2021).

The empirical cases we study in this article also show that the ‘Big Data revolution’ in insurance describes a hypothetical future, rather than a reality. We have investigated four attempts in France to develop an offer for car insurance using telematics devices. The principle is similar in all cases: a device records data relating to how the vehicle is driven (speed, sudden or gradual braking, tightness of corners, etc.). Customers are charged based on the data recorded by the device. These offers, most of which were developed between 2015 and 2020, have all been discontinued. The revolution, it would seem, did not take place. Why?

Organisational inertia, moral prevention or deliberate strategy?

In the description traditionally proposed (Mayer-Schönberger and Cukier, 2013), big data is a paradigmatic embodiment of radical innovation; that is, an innovation that significantly impacts a market or an organisation by making certain products, services or production processes obsolete (Fagerberg, 2006). Big Data radically transforms marketing practices (Erevelles et al., 2016), business models (Sorescu, 2017), and production processes (Rawat et al., 2014). However, radical innovations often fail to take hold. Many classic studies of innovation have shown that technically superior devices do not necessarily catch on (David, 1985). To understand the fate of innovation, it is necessary to reconstruct the process of its development, appropriation and use (Pavitt, 2006). The many pitfalls likely to occur over this process may limit its adoption. If Big Data can be described as a radical innovation, three mechanisms are likely to hinder their disruptive power.

M1. Organisational and cognitive inertia

Identifying the distinction between incremental and radical innovation shows the unequal capacity of organisations to deal with profound change. Established companies struggle to master new fields of knowledge and to adapt their organisational practices to new technologies; core competencies can easily become core rigidities (Leonard-Barton, 1995).

In the case of Big Data and the insurance sector, concrete instantiations of this general proposition may be observed in two specific mechanisms. First are the set of organisational routines challenged by disruptive technologies (M1.1). Organisations are built on stabilised, shared and legitimate practices (Nelson and Winter, 1982). A radical innovation, in challenging these practices, comes up against their inertia. The people who are supposed to implement it refuse to endorse it or transform it, sapping much of its subversive potential. Because the business model of insurance companies is old, organisational routines are very powerful – in contract design, marketing approaches, rate calculation methods, etc. These organisational routines are likely to limit the scope of any innovations associated with Big Data.

The second source of inertia is cognitive. Organisations such as insurance companies are battlegrounds for professional groups working with more or less esoteric knowledge (Abbott, 1988). When a group arrives with new knowledge, it may encounter opposition from groups that previously played a decisive role. For this reason, companies that have long used a given business model may find it difficult to seize new knowledge to develop new markets (Levinthal, 1998). In the insurance sector, technical know-how has been embedded for decades in the actuarial techniques mastered by a single, highly structured professional group. These techniques are based on probabilistic models whose underlying epistemology is very different from the one underpinning Big Data techniques (Kitchin, 2014). The mathematical and computational tools required for machine learning are very different from those generally used by actuaries. In this way, Big Data threatens the stature of actuaries, who are therefore likely to hamper innovation.

M2. Moral and political preventions

The principle of mutualisation is justified in technical terms by the impossibility of measuring risk individually. But it is also motivated by normative principles. Mutualisation makes it possible to establish solidarity among the clients or members of an insurance company (Ewald, 1986). Moral and political justifications for insurers’ activities have long played a decisive role in the dynamics of the sector (Zelizer, 1979). Calling the principle of mutualisation into question involves more than technical considerations: normative principles come into play, as well. These principles are likely to delay or hamper the disruption promised by Big Data in at least two ways.

The first is on the producer side (M2.1). This is what Kiviat (2019) shows when she studies U.S. insurers’ use of credit scores to price car insurance. Industry regulators only accept the use of credit scores if the predictions they make are consistent with their definition of responsible driving. In France, where the principle of mutualisation is still dominant, challenging it may arouse significant resistance, particularly within mutual companies.

Moral and political reservations are also likely to arise among consumers (M2.2). The use of telematics devices implies monitoring and recording customers’ behaviour. It has been shown that consumers are less likely to consent to share their data when it is accessible to companies (Hartman et al., 2020). While access to driving data has been less hotly debated than health data (Cheung, 2020), the revolution promised by Big Data may also be hindered by customer reluctance.

M3. A deliberate strategy

The presence of strong inertia does not mean that organisations are unaware of the nature and the potential of radical innovations (Pavitt, 2006). They may therefore implement strategies to determine whether or not adopting such innovations are appropriate for them. Insurance companies have not necessarily been passively contemplating the advent of Big Data; many have been proactive. The failure of telematics is not necessarily the symptom of an inability to adopt an innovation: it may be the result of a deliberate calculation and strategy.

This deliberate strategy often takes the form of experimentation (M3.1): companies encountering potential new markets may not immediately invest massively or systematically in them. Markets can be used deliberately as a space for experimentation (Muniesa and Callon, 2007). As Hopp et al. (2018) point out, the implementation of radical innovations depends first and foremost on the establishment of organisational capabilities. Insurers test to find out what these organisational capabilities are, and experimentation may be necessary in order to accrue knowledge relating to topics such as which data are likely to improve pricing, what devices should be put in place to collect them, or how the sales forces will appropriate new products. Such questions have no obvious answers. Experimentation offers a way to gather this new knowledge.

In this kind of experimentation, results are not the only significant variables. The question of what competitors are doing (M3.2) is also important. As they experiment, insurers observe direct competitors testing the market, as well. In this respect, the insurance market functions as a producer market in White's (1981) sense: it is a market in which producers observe each other, and their behaviour depends on what they observe about the behaviour of others. Experiments with telematics are part of a process that DiMaggio and Powell (1983) would describe as mimetic isomorphism: the market functions as an arena where producers observe each other and imitate their competitors.

Data and methods

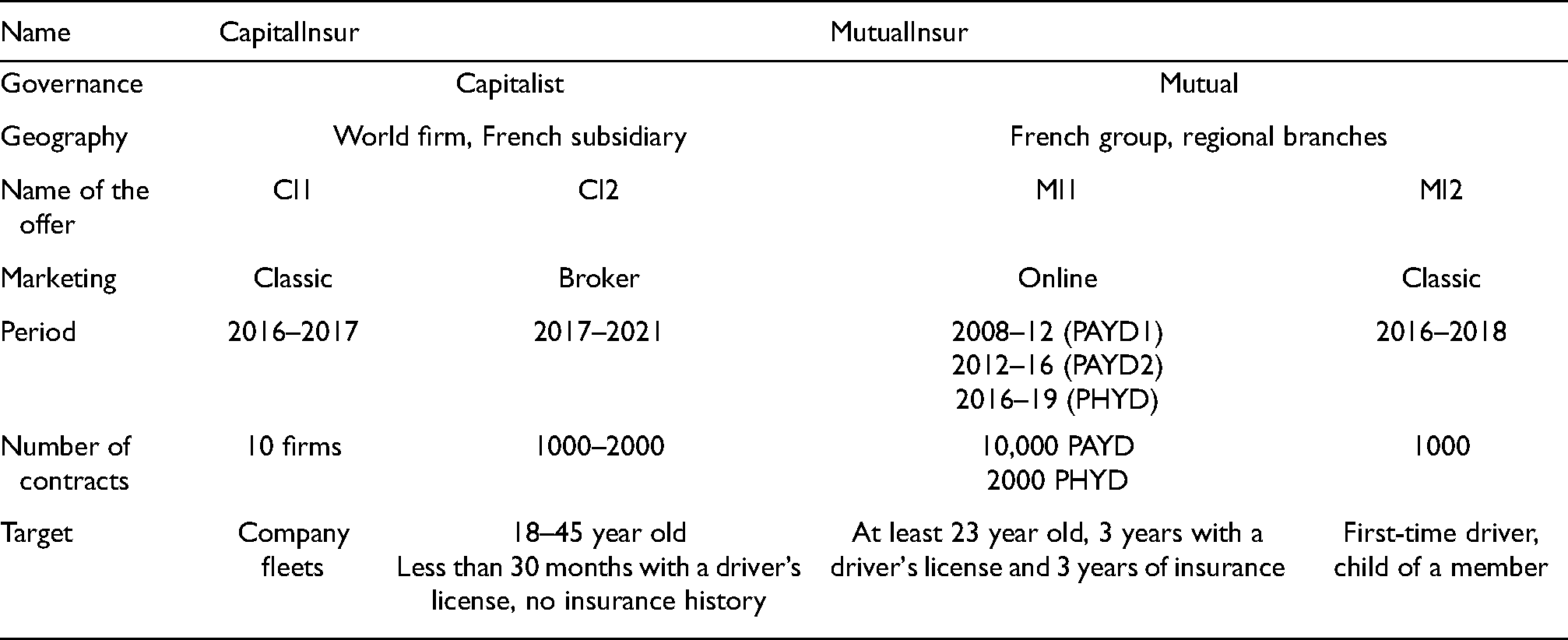

This article is based on an analysis of the trajectory of four telematics-based car insurance offers in France between 2010 and 2019. They were developed by two insurance companies (whose names will be kept anonymous, at the request of the interviewees), CapitalInsur and MutualInsur, that have been part of the French insurance landscape for at least three decades. In 2019, these companies were among the ten largest in the French insurance market, based on sales figures. The French auto insurance market in France is dominated by ten companies, which account for between 85% and 90% of sales. Both companies are part of this group; neither is specialised in auto insurance, and neither occupies a dominant position within it. Both are established companies.

They may be distinguished from each other by multiple features. First, their type of financing: one is capitalist (CapitalInsur), the other is a mutual (MutualInsur), a distinction with both an economic and a normative dimension. CapitalInsur follows a classic capitalist logic: its goal is to generate profit, which will ultimately be redistributed to shareholders. The mutualist company operates according to a principle of solidarity among its member-policyholders. The governance structures of the two companies also differ. The capitalist company's classic governance structure contrasts with the double hierarchy (technical and political) of the mutual. Finally, CapitalInsur and MutualInsur differ in their organisational and market position. CapitalInsur is the French branch of a large international insurer whose headquarters are not in France. It is an important subsidiary of the group, with a form of strategic autonomy. MutualInsur is a French mutual group, with 85% of its sales generated in France. Its business activity is organised into regional branches, each of which has a degree of autonomy under the coordination of the group's central body.

We studied four telematics offers, two of which were proposed by CapitalInsur and two by MutualInsur. In both companies, some offers were marketed through traditional channels. At MutualInsur, an offer (MI1) was made to young drivers who were children of member-policyholders. At CapitalInsur, an offer was proposed to a dozen companies to insure their fleet of cars (CI1). Both companies also proposed other offers through alternative channels; online at MutualInsur, via MutualOnline; and to young drivers who had never been insured at CapitalInsur, via the company's network of partnerships with independent brokers. With the exception of MutualOnline, which proposed offers as early as the end of the 2000s, these offers were launched between 2015 and 2019. All were based on a similar principle: customers whose driving was deemed to be virtuous received a discount on their premium.

The telematics supply chain.

The implementation timeframe of CapitalInsur's and MutualInsur's telematics offers places them in the average range of such offers in France (Deloitte, 2016), which were very sparse before 2015, around the time when a number of major auto insurers expressed the desire to invest in telematics. A few did, but their offerings were exploratory, and they soon scaled back their ambitions. Both CapitalInsur and MutualInsur had abandoned them by the spring of 2021, with the exception of one offer (CI2), which was radically redefined. Regardless of the nature of the companies or the forms of marketing adopted, attempts to develop a telematics offer ended in failure, which is what we wish to explain here. The failure we are investigating is not spectacular; that is, no company made a massive attempt to systematically offer a service that was then scuttled. The type of failure we seek to explain is subtler, and cyclical, one in which experimentation is followed by outright withdrawal.

The article draws on two main types of material. The first are interviews, conducted mainly in the spring of 2021, and mainly with employees of the two companies whose offers we studied: three at CapitalInsur (the managers of the CI1 and CI2 offers, and a marketing policy manager) and seven at MutualInsur (the two regional managers of the MI2 offer, the manager of the MI1 offer, the manager of the car insurance department of MutualInsur, the manager of car pricing, and two managers of telematics offers proposed by MutualInsur abroad). These interviews were supplemented by interviews with insurance professionals outside these two companies: three with academic actuaries and two with professionals working either in a company competing with MutualInsur and CapitalInsur, or in an actuarial firm. This material was supplemented by two types of written source. First, the numerous reports produced by consultancy firms attempting to map out the future of the auto insurance market. Second, a systematic press review, of two specialised press publications (La Lettre de l'assurance and L'Argus de l'assurance), two economic dailies (L'Agefi and Les Echos), and two national daily newspapers (Le Monde and Le Figaro). All articles published between 2015 and September 2021 that included the terms ‘telematics’ and ‘insurance’ in the body of the text were included in our study, for a total of 84 articles.

Results

Experimental approaches

Insurance companies’ attitudes toward the arrival of Big Data in their sector, as Pavitt describes (2006), were proactive and focused on developing experimental strategies to contend with the innovation. The approaches they implemented were all explicitly experimental; in no case did they seek to create a systematic offer available to all potential clients. The person in charge of the CI2 offer at CapitalInsur explicitly described the process in experimental terms: We experimented with this with a desire to learn and therefore to test the waters. With our private partner we intentionally chose to make it limited in order to gain experience. We didn't go full throttle, so to speak. [Manager in charge of CI2]

The experimental slant also clarifies the objective, which is not to make money, but to learn. The offers implemented were not primarily aimed at verifying profitability, but at gathering information on service provider reliability, client reactions, sales staff motivation, the nature of the data, device precision, data-processing quality, etc. The manager of one of MutualInsur's regional offers (MI2) explained: We knew from the start that we would lose money on our experiment. We knew that. But on the other hand, we wanted to test whether there was any potential. [Manager 2 in charge of MI2]

Every step in the production chain of the telematics offer must be tested. Upstream, various means of collecting and processing data must be investigated. At MutualInsur, for example, data collection was initially carried out using an application on customers' mobile phones. The system had its drawbacks: the application had to be activated, and quickly drained the phone's battery when it was. After a few months, it was decided that subscribers would be asked to install a box in their vehicle to record the data, instead. Once collected, the data itself had to be scrutinised: was it reliable, or not? Below, the manager of MutualInsur's MI2 offer explains how customers expressed how consistent they felt their scores were with their own perceptions, leading managers to decide to test the system themselves: We sometimes had clients who said "well, I don't understand, because my score is not very good. Whereas …" We had a few specific cases, so we also tested it with colleagues' children, which made communication easy. They were our beta testers. Testing it ourselves, we found it was mainly we who felt that our scores did not always correlate with the reality on the ground. [Manager 1 in charge of MI2]

The second question to be explored was of whether the data, once produced, actually helped improve pricing. For those predicting the Big Data revolution in the insurance sector, the answer is yes. Insurers wished to put this hypothesis to test. To do so, they first needed to know the specific nature of the information being integrated into their pricing tools. In most cases, the raw data recorded by devices (acceleration and deceleration speeds, abrupt braking or cornering, etc.) was not used directly. Instead, this data was processed to create an overall score, which was then used by insurers to try to improve rate calculations. These indicators were integrated into the generalised linear models used by actuaries, following a classic methodology; in other words, the experiments carried out within insurance companies aimed to improve existing actuarial models, following stabilised methods. This meant that experimentation occurred within a framework that possessed a degree of cognitive inertia (M1.2). The experimental nature of the approach, in other words, did not imply that all cognitive frameworks were to be called into question.

Experimentation also took place at an organisational level, both externally and internally. Externally, insurers had to form partnerships to collect telematic data, and sometimes to process it, since they did not possess the technical expertise needed to develop the boxes or applications that collected the data. They therefore had to seek out service providers and test their reliability, as well: would they really be willing to share the data they collected? CapitalInsur's CI2 offer, for example, involved a cascade of service providers: the broker selling CapitalInsur's policies, the subsidiary of a major equipment manufacturer, and the independent company to which it subcontracted some of its work. CapitalInsur's access to the raw data ultimately proved so complex that the manager chose to end the collaboration: Everyone knows that data is the raw material … So it has value and the owner absolutely wants to monetise it or at least keep it. We, moreover, were at the end of the chain with a delegated broker, another service provider, and then the subsidiary of [the equipment manufacturer], which meant that we were pretty much the last in line, we were driving a bit blind. In fact, we had difficulty getting access. We got it at the very end, after three years, by going to great lengths […]. Because also, afterwards, these are things that have to be stipulated contractually from the start, like everything else, so that the rules are applied. And if they are not applied, there are exit mechanisms, so that we leave as good friends and find someone else who is more transparent. [Manager in charge of CI2]

Internally, and according to the logic of organisational inertia described above (M1.1), experiments cannot be conducted just anywhere: some organisational spaces welcome them more than others, in some cases because their information systems are more flexible than others. The marketing manager of the French subsidiary of CapitalInsur explained to us that this was the reason for conducting the experiment aimed at young drivers through partnerships with affiliated brokers: [Through classic marketing channels], it is more complicated, in terms of computer systems, to set up this kind of test on a small scale. […] Through [broker] partnerships, we are able to run this kind of small-scale test We have all our networks to run. Meaning that it is not possible for 800 agencies to run a pilot scheme. Only doing it in a few agencies, implies IT fixes that we are not necessarily able to make [Marketing Manager, CapitalInsur].

The same is true of MutualInsur. The ‘classic’ company was less agile in testing a telematic offer (MI2) in two regions, than the online branch of the mutual: MutualOnline was a young company at the time and it had integrated this type of insurance natively. So their computer system was completely adapted to accommodate the logistical management of the score calculation boxes. All this was quite well integrated into their information system. Whereas we, well, we had information systems which were rather old, especially the system that is really the source of the contract data. It is therefore very complicated to maintain, especially for a pilot program where we cannot make heavy investments. So that's why we encountered logistical problems, problems with calculating scores, problems that are really linked to the technological aspect, on the data platform on the box, which MutualOnline didn't have. [Manager 2 in charge of MI2]

Organisational inertia seemed likely to hinder the adoption of the innovation, but those involved were aware of it. In order to test the innovation, they either deliberately choose to deploy it in a context where obstacles were smaller (at CapitalInsur), or to take these obstacles into account when interpreting results (at MutualInsur). Companies were not passive, in other words (M3): they identified and anticipated the challenges they were likely to face, and attempted to deal with them proactively.

Continuing down the production chain, we see that the innovation also had to be tested commercially. CapitalInsur and MutualInsur thus had to identify populations to whom they could propose their telematic policy offers. They targeted small populations: young drivers (in three of the four offers we studied), and corporate fleets. Young drivers were selected because they have trouble finding insurers willing to take them on: some simply exclude them from policy offers, while others charge rates as high as the regulations allow. Company fleets were targeted for reasons of convenience and scale: with just a dozen corporate contracts, CapitalInsur hoped to collect data on several hundred vehicles. One facet of the experimentation sought to explore the reactions of the targeted populations: young drivers, in particular, are perceived as more willing to share data and less hostile to new technologies. A hostile reaction from a population seen as more receptive might lead insurers to conclude that extending telematics offers to other populations would be even trickier.

The content of telematics offers, which may take many different forms, was also tested. Some policies charged the driver in proportion to kilometres driven (‘Pay As You Drive’). While such an offer might be considered simplistic in view of the promises of Big Data, it draws on a trivial observation that tidily sums up the main findings of in-vehicle devices: the more you drive, the more accidents you have. Those who drive less, therefore, see their premium reduced. By contrast, the ‘Pay How You Drive’ offer comes closer to following through on the promises of telematics, but faces a steep challenge: identifying an aggregate score (or detailed data) that can be used to assess the riskiness of someone's driving in order to calculate the amount of their premium. Indeed ‘Pay How You Drive’ formula was not possible in the early days of telematics: the first MI1 offers proposed by MutualInsur in the early 2010s were all ‘Pay As You Drive.’ Gradually, by the second half of the 2010s, insurance companies began attempting ‘Pay How You Drive’ offers, which were the ones being tested by CapitalInsur and MutualInsur between 2016 and 2021.

The implementation of telematics insurance systems follows a logic of experimentation that is present at all the stages of the production chain. At various points in this chain, cognitive or organisational inertia may hamper the disruptive power of big data. However, since telematics offers were abandoned even in organisations with little inertia, inertia cannot be the primary explanation for the abandonment. Instead, telematics was abandoned after test findings proved inconclusive.

Inconclusive results

A restricted population: Moral reluctance or legal disincentives?

Relationships with customers are central to service relationships (Gadrey, 2000). In the case of telematics-based insurance, these relationships are not easy to build. The small size of the populations interested in these offers is symptomatic of this challenge, although not, as might be expected, due to customer reluctance to make personal data available to insurers. Based on interviews conducted with managers, it did not appear that potential customers were opposed to sharing their data with insurers, at least not when it came to offers aimed at young drivers. Previous work has already established that insurance customers do not tend to balk at sharing their data with insurers (Deloitte, 2016). None of the sales managers interviewed described any such reluctance among young drivers; in the case of corporate fleets, by contrast, they identified it as one of the main reasons for the experiment's failure. This was due to the fact that employees whose vehicles were equipped with a telematics device saw them as a way for their bosses to monitor their journeys. The problem, in other words, was not to be found in the relationship with the insurer, but rather within the employer–employee relationship. The spontaneous mention of driver reluctance in the case of company fleets, alongside the fact that driver reluctance was never mentioned in the case of young drivers (even when the question was explicitly raised in interviews) indicates that in the latter case, customer reluctance was not a driving force behind the low numbers of interested customers.

There are two main explanations for the small size of the population. First, the target populations were themselves quite small, due to the experimental nature of the offers, as we have just pointed out. The second is the legal framework, and here, a comparison between France and Italy is enlightening: telematics systems have been more successful in Italy than anywhere else in Europe. Their success comes from the fact that premiums tend to be very high in Italy (particularly in the south of the country): in its 2010 annual report, the Italian supervisory authority estimated that the average annual cost of car insurance in Italy is €407, compared with €172 in France. In Italy, telematics contracts offer an opportunity to lower one's premium significantly. French insurers have taken this into account in proposing telematics offers to young drivers, as the cost of insurance is significantly higher for them than for the rest of the population. However, this additional cost is closely regulated: the Code des assurances (Art. A121–1 and A121-2) stipulates that premiums charged to young drivers cannot exceed twice the normal rate for more than three years; they also must decrease rapidly if there are no accidents. While a telematics policy offer does lower costs for young drivers in France, the gain remains modest. The legal framework in France reduces the incentive to take out a telematics policy, in part explaining the lack of interest in the CapitalInsur and MutualInsur offers.

Managing client relationships

The lack of interest in telematics offers makes it more difficult to build client relationships. When clients are interested, the relationship is difficult for the insurer to manage. Are telematics policies only available to current clients? The sales staff responsible for proposing telematics offers are sometimes reluctant to do so. At MutualInsur, this reluctance was intensified by a lack of financial incentive: We have salespeople who, from the start, found this new offer really top-notch and signed up straightaway. They systematically suggested it. We have others who thought that it was extra work, on top of everything else they had to do. And that, ultimately, they could continue to insure young drivers without it. Meaning that we have sales representatives who proposed it, and others who did not. And that's the game, that's how it is. They did not receive a specific commission for selling this policy. [Manager 2 in charge of MI2]

Telematics systems are also technically cumbersome, both for customers and for sales teams. Where the data is recorded by a smartphone application, the driver has to remember to launch the application when driving. Drivers may forget to do so, or may strategically choose not to record certain journeys. Some systems, therefore, such as the ones used in some MutualInsur offers, are designed so that the smartphone launches the application as soon as it detects motion in a vehicle. The resultant drain on the phone's battery was one reason for MutualInsur's decision to switch to an in-vehicle device. However, the device was not made available by insurance agencies; instead, customers had to order it from a service provider and install it themselves. Some customers were able to do this on their own, while others had to go to a garage. Either way, many customers who signed on to the offer were slow to install the device. Those who chose to change policies faced the same challenge in reverse: what to do with the device? The contract stipulated that it be returned to the service provider, but customers often preferred to take it back to their branch office – where devices, as a result, piled up. The whole process was logistically cumbersome, a disincentive for both customers and sales staff.

It was therefore quite challenging to build relationships with customers around telematics offers, a difficulty not compensated for by any gain in economic efficiency, despite theoretical predictions.

Scores and sorting

In theory, telematics scores may be used in two contrasting ways. The first is for sorting: telematics can be used to distinguish between risk profiles and to retain only the good ones. There are two drawbacks to this. The first is over-selection: the offers are both intended for a set population and remain optional: young drivers were able to choose between a traditional policy or a telematics contract. This increases the likelihood that telematics subscribers will be good drivers who anticipate that they will be able to benefit from the advantages reserved for customers with the best scores. In the case of MutualInsur's telematics offers, 80% of the policyholders who chose them benefited from the promised discount. If only ‘good drivers’ agree to a telematics policy, then trying to use telematics to eliminate ‘bad’ risks is doomed to failure. Moreover, the knowledge accumulated about this population is unlikely to map onto the rest of the population if the offer is expanded.

The second drawback was specific to MutualInsur, and relates to the desire to find a way to exclude ‘bad drivers.’ As one manager of the MI2 offers makes clear, this desire was lacking at MutualInsur, due in large part to its status as a mutual: To make this type of offer profitable, with the slightest deviance you have to be able to say to yourself: "Well, I'm ready to cancel, Mr Customer". And today in France, and in any case at [MutualInsur], that is something we are not able to do. Saying to ourselves: "I have detected that the client is driving very badly. Every Friday, every Saturday night, from 4 to 5 in the morning. And he is a real danger” is no reason to terminate [a policy]. It's very, very complicated, and even more so with an insurer like us, a mutual insurance company with elected representatives, with proximity. We did it with young people, because young drivers are the most at risk. And clearly, the ones who cost us a lot of money. But behind a young person, there is always a household, there is always a family, there are potentially parents who have been insured with us for 20 or 30 years. So we cannot cancel a young person just because he drives badly every weekend. [Manager 1 in charge of MI2]

It is possible to understand this reluctance in utilitarian terms: by refusing a young driver, an insurer would risk losing the rest of their family. While this interpretation does not contradict the one proposed by the manager, it should be noted that he justified his reluctance in moral, rather than utilitarian terms – and did so spontaneously. MutualInsur's reluctance to exclude ‘bad’ risks is one of the few cases where we can specifically identify forms of normative reluctance (M2.2). This relative scarcity of normative reluctance could be linked to the state of the legislative framework when these offers were put in place. Most were defined in 2015 and 2016, when the European framework (GDPR) was being finalised. The provision of personal data was governed at the national level before the definition of this framework (in France by the CNIL), but the adoption of the GDPR in 2016 and its passage into French law in 2018 has raised the profile of these issues among actors in the industry (Ewick and Silbey, 1998), particularly the actuaries and sales professionals who were in charge of creating these experimental offers. Lawyers, who were better informed about normative issues, remained marginal in their creation.

In any case, both in MutualInsur and CapitalInsur, the use of scores did not actually make it possible to distinguish between good and bad risks. Nor could scores be used in another practice that was supposed to be a cornerstone of their economic efficiency: personalised rates.

Scores as a tool for individualisation

Whereas, as we saw in the previous section, telematics can be used to sort and select, their use in individual pricing follows a different logic, that of hyper-flexibility: telematics, theoretically, makes it possible for each person to pay for their own risk. Telematics tools promise a cognitive revolution: because the data they provide is rich and precise, the behavioural variables they produce make it possible to measure the risk attributable to an individual's driving. The challenge, then, consists of using this more granular understanding to target pricing more effectively and offer individualised rates. This objective has only been poorly achieved. The link that insurers have managed to build between risk measurement and claims experience is very tenuous, as this CapitalInsur manager explains: You said that there was a gamble and that you had not found the correlation between driving and accidents.

Yes, exactly.

In other words, your scores were not correlated with the loss?

No. Afterwards, I'm not privy to the secrets of insurers, but the specialists I've met with on the subject are unanimous in saying that no one has yet found the answer. [Manager in charge of CI2]

If gains in explaining claims are small, it is first because existing models, developed over many decades, are excellent: [The question is] how do I use telematics data to refine my pricing model? But in any case…. There are some who have tried to beat the insurers' pricing models. They are already very well done, they can be enriched, but you can't beat them with telematics just like that. [Manager in charge of CI2]

It is all the more difficult to improve existing models because the data collected by telematic devices has so far proven to be rather poor. The scores integrated into pricing models most often summarise information collected by telematic devices, and are calculated by external service providers according to opaque procedures. The poverty of the data is compounded by the small size of the populations from which this data is collected. Cognitive inertia (M1.2) undoubtedly hinders the adoption of new offerings: it is difficult for them to outperform older ones.

Despite these difficulties, insurers have tried to use telematics data to develop pricing policies. Once again, the theoretical simplicity of indexing individual rates to the risks measured by telematics is far more complex in practice. Put simply, offers to drivers follow a rebate or cash-back logic: the customer subscribes to a policy; hypothetically, if their scores are good, part of the premium is refunded. Reality, however, is far less clear-cut. There are, of course, the simplest situations: drivers with good scores and no claims and drivers with bad scores and many claims. Neither one is of great interest to the insurer. In the first case the insurer earns little money; while it pays out little to nothing in reimbursements, it also earns little in premiums. In the second, the insurer usually loses money: gains made by increasing premiums are generally not enough to cover claims. By contrast, both situations are clear from the client's point of view: rates (linked to scores) correlate with the frequency or magnitude of claims. Two other possible situations make much less sense to clients: in the first, the customer drives badly but has no accidents; their poor score justifies higher rates in the eyes of the insurer – and since there are no claims, the insurer makes money. For the client, however, this situation is hardly understandable. The second situation involves good scores but large or frequent claims. While advantageous for the client, it poses a problem for the insurer: its costs increase, but it cannot increase rates, and may even be required offer a rebate.

The apparent simplicity of models where better scores mean higher discounts fades into a more complex one where it is far more difficult for the insurer to identify a ‘good’ client. Of course, identifying good customers is not always a purely technical consideration: moral or normative criteria may also come into play (McFall, 2011; Meyers and Van Hoyweghen, 2018). However, technical considerations are also present in the identification of what is a good customer, and in the case of telematics offerings, insurers are still groping for the right approach. They need more experience and greater knowledge, and while the experiments they conduct are not expected to be profitable in the short run, they hold little promise without the prospect of medium-term profits. Insurers lack the time needed to refine their telematics offers in a way that strikes the right balance while also preserving customer satisfaction.

Telematics systems are proving to be ineffective in the short term. This lack of profitability must be understood from within the general economy of auto insurance offers. As we have seen, in contrast to other countries, such as Italy, car insurance rates in France are extremely low. Pricing models are efficient, and competition among insurers is high, resulting in a combined ratio (which relates the cost of claims to premiums) above 100% in 2017. This has been the case for the past 12 years (Bardaji, 2017). In the portfolio of products offered by an insurer in France, car insurance is a loss leader, attracting customers who then subscribe to other, more profitable products.

This means that insurers have very little room to push prices down: to do so, they would have to be able to substantially reduce their claims by eliminating the 'bad' risks from their portfolios – which, as we have seen, would be extremely difficult. But prices are also very inflexible upwards: competition is such that they cannot deviate significantly from the baseline price of the ten companies that share the market in France. To be profitable, telematics systems must not only be technically efficient, they must also be implemented within a market with sufficient room for manoeuvre where rates and pricing are concerned, which is not the case in France.

A second constraint also affects the profitability of telematics offers: because of pricing in France, the profitability of an insurance company's auto insurance business depends on a few very large claims, in particular ones involving serious bodily injury. If, in a given year, a handful of policyholders file a claim of this type, then the company's auto insurance business will book losses. When the number of policies is large and the timeframe is long, it is possible to set rates that balance these losses over a number of years, thus achieving some form of profitability. When, as in the case of telematics, the number of policies is very low and the timeframe is short, the profitability of the offer depends on claims whose probability of occurrence cannot be predicted. Under these conditions, whether or not a telematics offer will be profitable is ultimately just a roll of the dice.

A mimetic validation

As we have seen, there are multiple drawbacks to telematics offers that make them unattractive to insurers, who have tested them and walked away. It is the agility of these companies, not their inertia, that leads them to abandon this innovation, which many believed would challenge a centuries-old economic model.

This strategy of experimentation is not isolated: in step with one another, multiple French insurers are implementing it, and giving it up. Prior to 2015–2016, very few telematics offers existed (Deloitte, 2016); five years later, about half of the ten companies who dominate the car insurance market had risked offering telematics products – and are now setting much more modest targets for them

2

. This is no accident, and can be explained by one of the forces driving these companies’ experimentation: market surveillance. At the beginning of the 2010s, every insurer operating in the car insurance market knew that telematics devices existed, and had been installed by car manufacturers since the beginning of the 2000s. All of them could imagine the potential uses of these data. No one knew, however, when these new pricing techniques would become the new norm. If (or when) the market was to change, they simply wanted to be ready, to have data on telematics that would allow them to offer their own rates, and to have spotted pitfalls in the new value chains. Without this information, they feared, they would be left to insure 'bad' risks only. This is what a telematics offer manager at MutualInsur explains: If the whole market was going to change, we thought that those who had the telematics data would be better able to segment the risks. So, if we were not able to segment them, we would only be able to sell products, traditional auto insurance, to people who had not found a good price with the telematics insurers. Meaning we would end up with all the bad risks that the others didn't want. [Manager in charge of telematic offers abroad, MutualInsur]

As soon as some insurers began experimenting, it was in the interest of anyone wishing to remain in touch with the market to make a move. Even if the specific results of any given company's experiments were not made public, their success or failure could be tracked. It soon became apparent that all the systems put in place came up against prohibitive difficulties (at least temporarily). Under these conditions, the reasoning of the various actors follows a kind of specularity: all observe that all observe that all observe, etc.… that no one has any interest in making a move. Therefore, no one moves. Theoretically, it might be interesting for an insurer to break this ‘tacit collusion’ (Green et al., 2014): by being the first to offer telematics to risky young drivers, it might gain first mover advantage. But the opposite logic prevails: the risks of movement are seen as outweighing potential benefits.

This cycle of monitoring, however, is not over. And if market surveillance were to indicate the existence of potentially destabilising initiatives, the companies that carried out telematics experiments possess the data and the knowledge of the value chain they need to react quickly. For the time being, all market players agree it is urgent to do nothing.

Conclusion

Of the three main mechanisms we identified to explain the (possibly temporary) failure of telematics systems in the auto insurance sector, moral or political prejudices are the least significant. In particular, young drivers are not reluctant to share their data with insurers, and telematics offers have not failed because customers refuse to share their data. On the supply side, and particularly on the part of some managers working in mutual insurance companies, there may be some reluctance, but it remains theoretical, as mutual companies have not had to choose whether or not to abandon the principles of solidarity they claim to uphold. Telematics programmes were abandoned before the choice presented any opposition by capitalists or mutuals, in other words, did not have time to play out.

Taken together, two mechanisms explain the abandonment of telematics offerings: inertia – both organisational and cognitive – and deliberate strategy. The clearest finding of our research is that the use of telematics was a deliberate experiment, and that the experiment was not successful. Insurance companies have not been passive about innovation. Instead, they sought to measure its viability and identify potential obstacles to implementation. Among these obstacles, there are many elements of inertia, both organisational and cognitive: data collection generates trivial but potentially prohibitive difficulties; the cognitive frameworks of actuaries are not destabilised by often rudimentary data; the habits of salespeople are not easily challenged. These elements of inertia play out unevenly from one organisation to another. Seen from this perspective, the tensions between capitalist and mutual models or contrasts between the French and other national models are not the most significant. Whatever their mode of financing or their type of governance, flexibility (or lack thereof) seems to be the most significant factor.

Whatever these differences may be, they do not call into question the basic observation that telematics offers are not profitable, either in the short term or the medium term. This is due first to the fact that the development of a viable offer would require an amount of time and a demographic expansion that insurers are not prepared to invest. Second, it is due to the fact that auto insurance in France is a loss leader whose profitability depends on a few very serious claims whose occurrence is impossible to predict. Finally, because experimentation was undertaken so that insurers had the information they needed to react in a timely manner if the market were to develop, the fact that the market has not developed has rendered this experimentation moot. If no one moves, no one has any interest in moving. When it comes to auto insurance pricing, the Big Data revolution has yet to take place.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.