Abstract

This article examines lobbying firms as intermediaries between organized interests and legislators in the United States. It states a partisan theory of legislative subsidy in which lobbying firms are institutions with relatively stable partisan identities. Firms generate greater revenues when their clients believe that firms’ partisan ties are valued highly by members of Congress. It hypothesizes that firms that have partisan ties to the majority party receive greater revenues than do firms that do not have such ties, as well as that partisan ties with the House majority party lead to greater financial returns than do partisan ties to the Senate majority party. These hypotheses are tested using data available under the Lobbying Disclosure Act from 2008 to 2016. Panel regression analysis indicates that firms receive financial benefits when they have partisan ties with the majority party in the House but not necessarily with the Senate majority party, while controlling for firm-level covariates (number of clients, diversity, and organizational characteristics). A difference-in-differences analysis establishes that Democratically aligned lobbying firms experienced financial losses when the Republican Party reclaimed the House in 2011, but there were no significant differences between Republican and Democratic firms when the Republicans reclaimed the Senate in 2015.

Introduction

How interest groups attempt to influence Congress has been a significant topic of inquiry since the early days of the political science profession (Herring, 1929). The majority of research in this area has investigated either lobbyists as individuals or the interest group clients that they represent (Baumgartner et al., 2009). Despite this history, the field has only recently turned its focus to the business side of lobbying (Drutman, 2015; LaPira and Thomas, 2017). Research has begun to examine not only the substance of what lobbyists do – such as how they choose their issue positions – but also how they sustain an economic enterprise.

Developing scholarship on the business of lobbying calls attention to “the presence of the lobbying industry as an intermediary” in the political process (Bertrand et al., 2014: 3886). However, this progressing literature still gives only minimal attention to lobbying firms – the business organizations that are responsible for hiring and managing thousands of contract lobbyists. Some studies use data on lobbying firms (Bertrand et al., 2014; Blains i Vidal et al., 2012), but this work seeks to explain the behavior of lobbyists as individuals rather than the firms that employ them.

This article argues that lobbying firms themselves are institutions with relatively stable partisan identities that make them relevant intermediaries between organized interests and legislators. Firms may have partisan ties that affect their revenue generation by helping to resolve uncertainty on the part of potential clients about how the firm is likely to perform its work. To understand this intermediation, this article tests a model of lobbying firm revenue. It evaluates the extent to which partisan ties between lobbying firms and the partisan leadership of Congress explains the ability of firms to raise lobbying revenues from their clients. In extending beyond previous studies that analyzed lobbying revenue as an individual-level phenomenon, the model incorporates firm partisan identities, as well as firm clientele size, diversity, and other organizational characteristics. This analysis lays a foundation for appreciating how lobbying firms are political enterprises within the party system.

This article has three key findings. First, lobbying firms have identifiable and relatively stable partisan identities. Second, lobbying firm ties with the partisan leadership of the US House of Representatives are significantly associated with higher revenues for firms, approximately US$5000 to US$6000 per lobbyist per quarter. Third, change in the party controlling the House of Representatives is associated with revenue losses for firms tied to the party losing control, roughly US$40,000 per lobbyist for one year. Evidence regarding firms’ ties with the partisan leadership of the Senate is mixed, with the presence of significant effects depending on model specification.

A partisan theory of legislative subsidy

To appreciate why lobbying firms may benefit financially from their connections with political parties, we consider why legislators pay attention to lobbyists at all. Hall and Deardorff (2006) explained that legislators face perpetual shortages of time and staff resources to work on issues they care about. If lobbyists bring policy information, political intelligence, and legislative labor to issues that legislators are concerned with, then legislators may be able to devote more time to those issues than they otherwise would. Meeting with lobbyists expands a legislator’s time budget for working on an issue, thus subsidizing attention to that issue.

If legislators are to accept the information, intelligence, and labor provided by lobbyists, then they need to trust lobbyists. For this reason, legislators are most likely to meet with lobbyists who are among their closest allies (Hojnacki and Kimball, 1998). During a period of high partisan polarization – such as the contemporary era – allies are likely to be members of the same party (Poole and Rosenthal, 2000). Organizational identity is a key way that advocacy organizations become known with respect to their political loyalties (Heaney, 2004; Heaney and Leifeld, 2018). Thus, we argue that the partisan organizational identities of lobbying firms are important to them being understood as partisan allies to legislators.

Given the procedural advantages that accompany majority status in Congress, outside interests are willing to pay more to have access to the majority than to have access to the minority (Cox and Magar, 1999). If lobbyists gain access to legislators by being allies – which usually requires being co-partisans – then sharing partisan identification with the party in control of a chamber should translate not only into more access but also into greater payments from clients for the access that is granted.

Based on these arguments, we state:

Hypothesis 1: Lobbying firms that have partisan ties to the majority party receive greater lobbying revenues than do lobbying firms that do not have such ties, other things equal.

The willingness of legislators to accept subsidies provided by lobbyists likely depends not only on partisan alignment but also on the degree to which they are already supported by staff. A legislator with an extensive staff may place less reliance on lobbyists than would a legislator with fewer staff resources. Given notable differences between members of the House and Senate in access to staff resources – with the Senate allocating more resources per member than the House – lobbying clients may be willing to pay differently for lobbying the chambers (LaPira and Thomas, 2017: 13). Thus, we state:

Hypothesis 2: Lobbying firms receive greater financial returns when they have partisan ties with the partisan majority of the House than when they have partisan ties with the partisan majority of the Senate, other things equal.

In addition to the partisan theory of legislative subsidy, there may be other reasons to expect differential returns from lobbying the two chambers. Baker (2008: 144–151) interviewed 12 lobbyists about their perceptions of differences in lobbying the House and Senate. His respondents perceived Senators as being harder to lobby than House members because they viewed Senators as more cross-pressured by diverse constituencies, more concerned with broad national interests, and less attentive to the technical details of legislation. Thus, there may be reasons in addition to staffing disparities for differential lobbying returns between the chambers.

Organizational characteristics and lobbying firm revenue

Lobbying firms have organizational-level characteristics beyond their partisan identities that may affect their revenue stream. First, number of clients is important because larger firms are better known, more prestigious, and thus more capable of demanding higher payments for their services than are firms with fewer clients (Schiff et al., 2015). Second, client diversity with respect to issues and industries is important because of the long-standing expectation in economics that diversification spreads risk across investment portfolios (Markowitz, 1959). Third, firm organizational characteristics – such as whether a firm is a law firm, has international offices, the number of its domestic offices, and its age – may account for variations in prestige and economies of scale for client recruitment that may correspond with how firms earn revenue. For example, a lobbying firm that is also a law firm may assign its associates both legal and lobbying tasks, thus potentially reducing its lobbying revenue per lobbyist (but increasing its legal revenue).

Research design

We draw on lobbying reports that are available as a result of the Lobbying Disclosure Act (LDA) of 1995. We focus on reports filed from 2008 to 2016, after the passage of the Honest Leadership and Open Government Act of 2007, which changed the LDA reporting frequency from semi-annually to quarterly and modified rules for lobbyist registration. We combine publicly available lobbying data with original research on the lobbying firms appearing in the records.

We modeled our dependent variable, Revenue per Lobbyist, in real dollars, which reflects the aggregate income each lobbying firm earned from all clients in a period. We adjusted for inflation using the Consumer Price Index for All Urban Consumers: All Items (FRED, 2017).

Our focal independent variables are Firm Partisan Alignment with House Leadership and Firm Partisan Alignment with Senate Leadership. It is possible for a firm to be aligned with both the House and Senate, one or the other, or neither chamber. We did not consider bipartisan firms or those without clear partisan identifications to be aligned with either chamber.

We determined the partisan ties of a firm using campaign contributions of its lobbyists. If a firm’s lobbyists gave a high percentage of their contributions to one party, then we considered the firm to be aligned with that party. In recognizing that the boundary between “partisan” and “bipartisan” firms may be fuzzy, we calculated partisanship using three different giving thresholds: 85%, 90%, and 95%. Further, we calculated two versions of each of these measures. For the first version, each firm’s alignment was calculated once and fixed in time (based on lobbyists’ campaign contributions dating to 1990), treating it as a relatively stable characteristic. The second version allowed the firm’s identity to vary each year as a function of changes in its lobbying roster and campaign giving, treating it as a more fluid factor. Fleiss’s κ, a reliability measure for categorial variables, was 0.86 for the time-fixed measure and 0.84 for the time-varying measure, indicating “substantial” to “nearly perfect” agreement (Landis and Koch, 1977). The time-fixed and time-varying measures of partisan ties exhibit highly correlated partisan classifications (ranging from 0.62 to 0.63, p ⩽ 0.05), yielding strong evidence of relatively stable firm partisan identities.

We examined the validity of our measures by using data from firms’ web pages on the founders of lobbying firms. Firms were classified as Democratic if they had only Democratic founders, Republican if they had only Republican founders, and bipartisan if they had at least one founder from each party. We correlated these founder-based measures with the contribution-based measures discussed above. We found positive, statistically significant correlations between firms having only Democratic founders and those making homogeneously Democratic contributions, or between having only Republican founders and those making homogeneously Republican contributions (with correlations ranging from 0.31 to 0.55, p ⩽ 0.05), supporting the conclusion that our measures are relatively stable and valid indicators of firm identity. Indeed, the influence of the founders is not ephemeral; it persists over time.

We calculated the Number of Clients and Client Diversity using LDA data. Data on Law Firms, International Offices, Number of Domestic Offices and Firm Age were drawn from lobbying firm websites. These web-based variables contain substantial missing data because not all lobbying firms have websites. Smaller, newer, and disbanded firms were especially at risk of not having a site.

Statistical analysis

We analyzed quarterly data reported by an unbalanced panel of 1603 lobbying firms from the first quarter of 2008 through the third quarter of 2016. Registrants were taken from lobbying reports where the registrant and the client differed – indicating that the registrant was a contract lobbyist or firm hired by a client. To count as a firm, a registrant had to list two or more lobbyists as active in the same quarter at least once and have at least two quarters with nonzero dollars.

Descriptive statistics

Figure 1 shows the distribution of partisan giving, from which we calculated partisan ties, based on firms with nonzero campaign giving (84% of firms). It exhibits a bimodal pattern, with partisan firms clustered at the extremes of the distribution. The time-fixed and time-varying distributions are similar. One notable difference between them is that the percentage of Democratically tied firms is greater when using the time-varying measure than when using time-fixed measure. This pattern indicates that fewer firms reliably give 95% or more of their contributions to Democrats than there are erstwhile Democratic firms that meet this threshold periodically. Either way, the distribution reveals a drop-off in partisan ties after the 95% threshold. These findings indicate that roughly 42 to 60% of firms have a “partisan” bent and 40 to 58% have a “bipartisan” orientation, depending on the selected cutoffs.

Distribution of partisan giving by lobbying firms.

Figure 2 reports the average revenues over time for bipartisan, Democratic, Republican, and unclassified firms. We used the 90% partisan-giving threshold and the time-fixed measure of partisanship for this graph. Bipartisan firms consistently earned greater average revenues than did their partisan-leaning competitors. Republican and Democratic firms were roughly at parity over time. However, a marginal advantage traded back and forth corresponding with congressional control. Democratic firms earned higher average revenues when Democrats held congressional majorities from 2008 to 2010. Republican firms earned more when Republicans reclaimed congressional control from 2011 through 2016. Unclassified firms earned consistently lower average revenues than did partisan and bipartisan firms.

Revenue trends lobbying firms, 2008–2016.

We report variable definitions and descriptive statistics in Table 1.

Variable definitions and ddescriptive statistics.

Note: aDiversity = [Σ[(ni/N)2]]-1, where ni is the total dollars reported with that industry or issue for the firm in a given quarter and N is all dollars reported by the firm in a quarter (Simpson, 1949).

Panel linear regression models

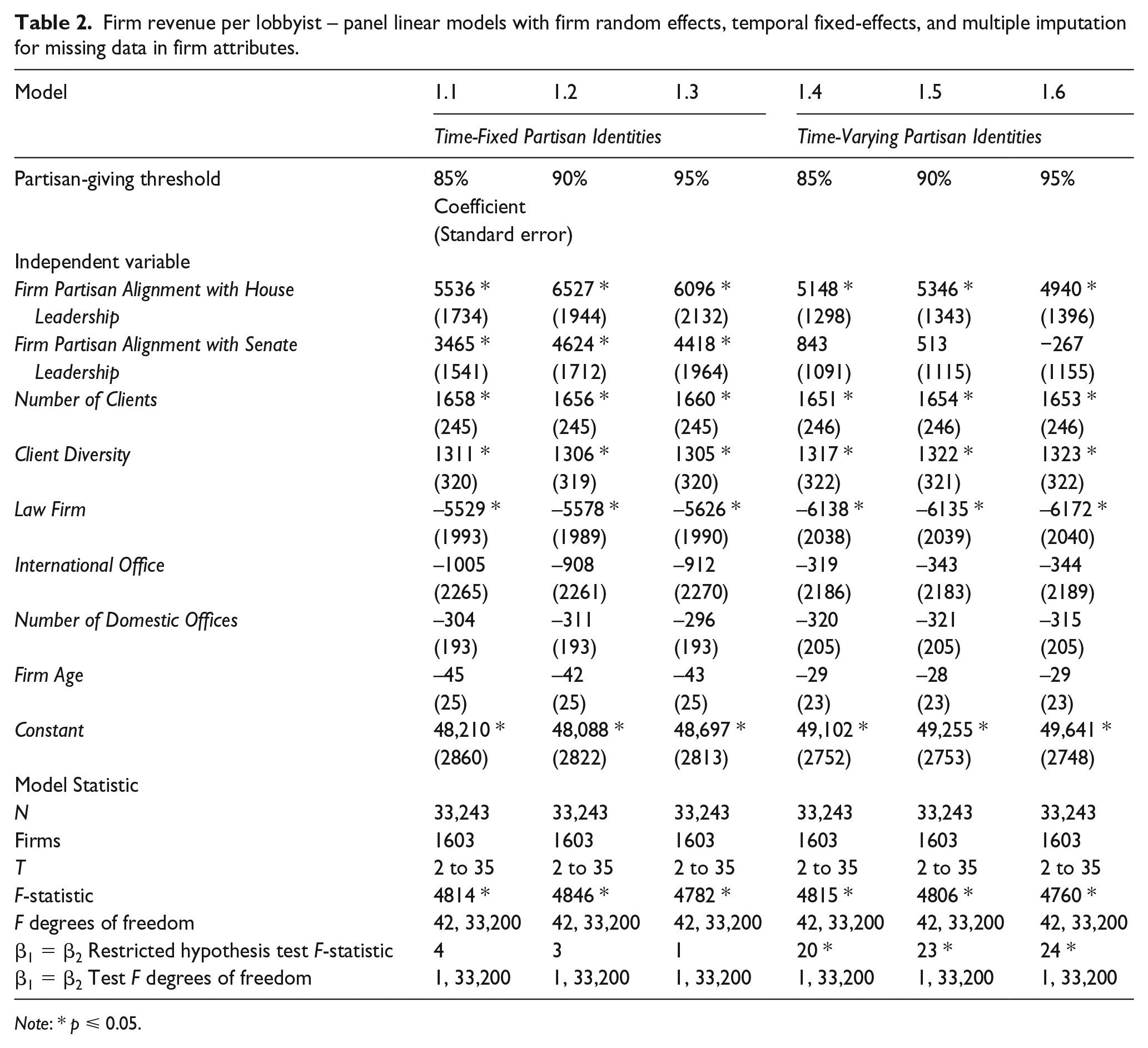

We estimated two sets of panel linear models. The first set was estimated on Revenue per Lobbyist as the dependent variable. Six versions were estimated to allow for time-fixed and time-varying measures of Firm Aligned with House Leadership and Firm Aligned with Senate Leadership, as well as 85%, 90%, and 95% cutoffs for each.

We included control variables for Number of Clients and Client Diversity, neither of which contained missing data. Our remaining, time-invariant control variables (Law Firm, International Office, Number of Domestic Offices, and Firm Age) contained missing data. We applied multiple imputation to address this issue (King et al., 2001). Imputation procedures and diagnostics are reported in Online Appendix A. Panel linear models 1.1 through 1.6 were estimated using random effects for firms and fixed effects for years (see Table 2). We employed HC3 Arellano standard errors (clustered by firm) that are robust to heteroskedasticity and serial autocorrelation (Arellano, 1987).

Firm revenue per lobbyist – panel linear models with firm random effects, temporal fixed-effects, and multiple imputation for missing data in firm attributes.

Note: * p ⩽ 0.05.

The results in Table 2 support Hypothesis 1 with respect to the House of Representatives. The coefficient on Partisan Alignment with House Leadership is significant in all six models. The results indicate that firm partisan ties are worth approximately US$5000 to US$6000 per lobbyist per quarter, other factors held constant. Hypothesis 1 is only supported with respect to the Senate when firm partisan alignment is based on a time-fixed measure (in models 1.1, 1.2, and 1.3). Hypothesis 2 is tested using a restricted hypothesis test that is supported only when firm partisan alignment is based on a time-varying measure (in models 1.4, 1.5, and 1.6). Online Appendix B shows that these results are substantively the same as those obtained when using a fixed-effects specification. Online Appendix C indicates that support for Hypothesis 1 would be somewhat higher were we to consider the effects of multicollinearity on suppressing the significance of Senate effects. The control variables, Number of Clients and Client Diversity, are significant with positive coefficients, while our Law Firm control variable is significant with negative coefficients.

The second set of models was estimated on Change in Revenue per Lobbyist as the dependent variable. These first-differences specifications use Change in each of the independent variables. The advantage of estimating these models is that they remove residual unobserved heterogeneity (Greene, 2012: 356). They also remove time-invariant, firm-level independent variables from the models (i.e., Law Firm, International Office, Number of Domestic Offices), since these variables have ΔX = 0 in all cases, as well as Firm Age, since ΔX = 1, yielding a constant. Consequently, variables containing missing data drop from the equations, eliminating the need for imputation. We followed the same procedures for estimating standard errors as in the first set of models.

The results of the first-differences analysis are in Table 3. Hypothesis 1 is supported with respect to the House in five of the six models, with the coefficient falling just short of the conventional threshold of significance (p ≈ 0.07) in Model 2.5. Substantively, these results indicate that a change in firm alignment with the House is worth approximately US$1800 to US$5000 per lobbyist per quarter. We find no support for Hypothesis 1 with regard to the Senate in the second set of models. Hypothesis 2 is supported with respect to differences between the House and Senate in two of six models. For the control variables, Change in Number of Clients is significant in five of six models, while Change in Client Diversity is not significant in any model. Robustness analysis in Online Appendix D shows that these results are not an artifact of multicollinearity. Online Appendix E shows that our results are substantively similar if we use the partisan identities of firms’ founders as our focal independent variable.

Change in revenue per lobbyist – panel linear models on first differences (i.e., ΔY on ΔX).

Note: * p ⩽ 0.05.

Difference-in-differences designs for party takeover “treatments”

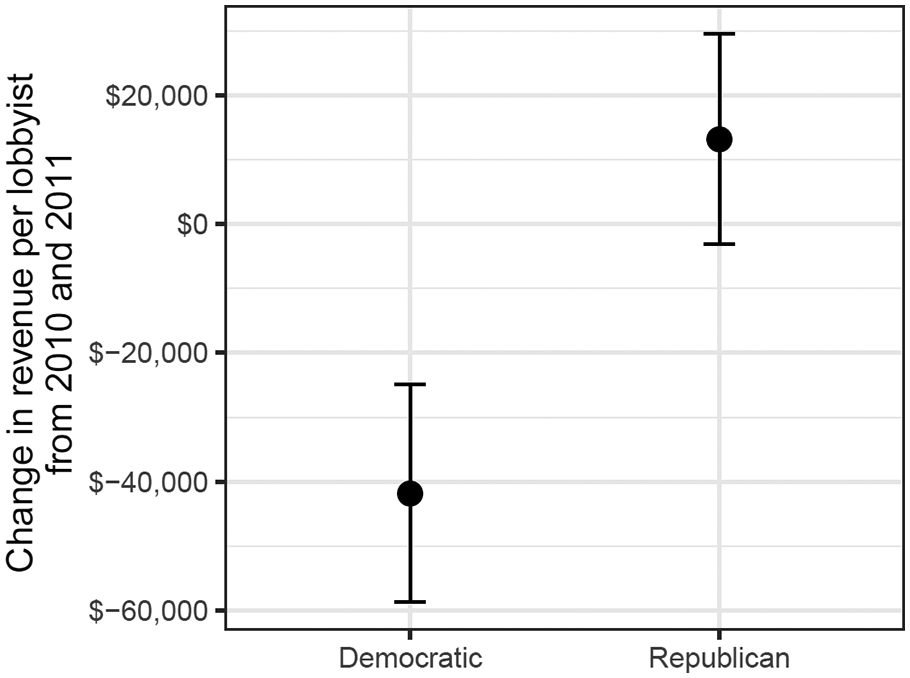

In order to address questions of causation, we subjected the data to a harder test. If partisan efforts – or some other unobserved endogenous process – caused partisan firms’ revenues to increase, then it is not likely that they occurred immediately after a new majority took over. Starting new House-majority-party-aligned firms immediately after a takeover occurs would be costly. We think it is more plausible that any year-over-year changes in party-aligned firms’ revenues can be attributed to the immediately perceived value in an in-party-aligned firm. In Online Appendix F, we considered and ruled out the possibility that lobbyists switching to firms with different party loyalties in the aftermath of changing partisan control of a chamber is a significant factor.

We addressed causation by exploiting exogenous changes in House and Senate party leadership as temporal interventions. We used a kernel-weighted difference-in-differences estimator (Hazlett, 2019) to test temporal causality for changes in both institutions, which occurred as a result of separate electoral cycles. We exploited exogenous shocks created by changing control of the House in 2011 (from Democratic to Republican) and Senate in 2015 (from Democratic to Republican). Blanes i Vidal et al. (2012) and de Figueiredo and Richter (2014) recommended the difference-in-differences approach when dealing with panel datasets on lobbying because it effectively addresses persistence issues – the continuation of previous trends despite a changing state of the world, as may be induced when firms keep the same clients that they had the year before – that commonly affect this type of data (Buraimo et al., 2016).

We estimated the causal effect of a lobbying firm being tied to the party gaining control over a chamber of Congress. A firm was “treated” when its aligned party gained control of a chamber. These firms were compared to newly ousted-party firms. We uncovered a positive treatment effect on Revenue per Lobbyist when the Tea Party movement helped Republicans regain of the House majority in 2011. Figure 3 plots the values for the 2010–2011 takeover treatment effects. Lobbyists at Republican-aligned firms are estimated to have gained just over US$10,000 for the year. Ousted-Democratic lobbying firms are estimated to have lost more than US$40,000 in annual revenues, despite still holding the Senate majority. We observed no significant effects after the Republican Party’s takeover of the Senate in 2015, as we report in Figure 4. Additional information on the difference-in-differences estimation is in Online Appendix G.

Revenue per lobbyist difference-in-differences for 2010 to 2011.

Revenue per lobbyist difference-in-differences for 2014 to 2015.

Conclusion

Lobbying firms have relatively stable partisan identities that matter in their ability to attract revenue from interest group clients. Our measures of firm partisan identities are reliable, their validity is supported by their correlation with the partisan identities of firms’ founders, and scarcely few lobbyists leave a partisan firm from one party to work for a partisan firm of the opposite party. Partisan ties help to define lobbying firms as institutions.

Partisan ties between lobbying firms and the partisan leadership of the House of Representatives help to boost lobbying firm revenues, with 12 of 13 tests supporting this conclusion, including a difference-in-differences analysis. However, evidence of financial benefits from partisan ties with the partisan leadership of the Senate is more limited, with only 3 of 13 tests favoring this view (though this support would be somewhat higher if we considered the effects of multicollinearity in models 1.4, 1.5, and 1.6). There is some indication that ties to the House are more revenue-enhancing than ties to the Senate, with 5 of 12 tests backing this expectation. Since the outcomes of the 2018 midterm congressional elections led to another switch in partisan control of the House (from Republican to Democrat), these events will present another opportunity to test these hypotheses once the 2019 lobbying data become available.

Our analysis favors the view that partisan ties with the House are a more reliable source of revenue than are ties with the Senate. This difference may be attributed to how differences in congressional staffing by chamber affect the perceived value of lobbying by firms. Nonetheless, there may be viable alternative explanations rooted in the longer electoral cycle, supermajoritian rules, and higher member prominence in the Senate. Moosbrugger’s (2012) theory of institutional vulnerability may provide a fruitful starting point for parsing these explanations in future research.

Our findings extend beyond Bertrand et al. (2014: 3915) by demonstrating that partisan identities (and other organizational characteristics) of firms matter, as opposed to only the partisan identities of individual lobbyists. Our finding that ties to the House leadership have greater reliability for revenues than do ties to the Senate leadership contrasts with Blanes i Vidal et al. (2012), which found a greater value of being connected to the leadership of the Senate than to the leadership of the House (see Cox and Magar, 1999 for a related finding). Future research could explore interactions among lobbying firms, legislative subsidies, chamber leadership, campaign contributions, and fundraising to further extend our understanding of partisan lobbying firms as political institutions.

Supplemental Material

Online_Appendix – Supplemental material for The partisan ties of lobbying firms

Supplemental material, Online_Appendix for The partisan ties of lobbying firms by Alexander C. Furnas, Michael T. Heaney and Timothy M. LaPira in Research & Politics

Footnotes

Acknowledgements

An earlier version of this article received the Best Paper Award from the APSA Organized Section on Political Organizations and Parties for its presentation at the Annual Meeting of the American Political Science Association, San Francisco, California, 31 August –3 September 2017. Additionally, an earlier version of this article received an Honorable Mention for the Best Paper Award from the ECPR Standing Group on Interest Groups for its presentation at the European Consortium for Political Research General Conference in Hamburg, Germany, 22–25August, 2018. For helpful suggestions, the authors are grateful to Scott Ainsworth, Marie Hojnacki, Tom Holyoke, Daniela Kabeth, Cole Kauffman, Beth Leech, and Rick Price. For research assistance, the authors thank Amy Cesal, Amelia Chan, Dulce Guerrero, Connor Herrington, Brittany Honos, Ji Soo Kang, Imran Mohamedesha, Nurlan Orujlu, Nabah Rizvi, and Heather Smith.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research benefited from financial support from the Summer Research Opportunity Program and the Rackham School of Graduate Studies at the University of Michigan, as well as from the Hewlett Foundation Madison Initiative.

Supplemental materials

Carnegie Corporation of New York Grant

This publication was made possible (in part) by a grant from the Carnegie Corporation of New York. The statements made and views expressed are solely the responsibility of the author.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.