Abstract

Purpose:

Physician and medical practices have undergone significant consolidation over the last decade. This has been in response to federal and financial changes to health care delivery within the United States. As per the 2021 AUA annual census, the percentage of employed practicing urologists (not in solo or partnership practice) increased from 51.3% to 64.4% between 2015 and 2020 (AUA Census 2021). Our objective was to further examine the changing trends among provider groups within Urology between 2014 and 2021.

Methods:

Publicly available information from within Medicare Physician Compare, published by the US Centres for Medicare and Medicaid Services (CMS) was used. Practice size data were pulled from 1 month each year between 2014 and 2021 and filtered by physicians listing ‘Urology’ as their primary specialty. Practices were divided into categories based on size. Statistical calculations were conducted using R (version 4.0.2).

Results:

Solo or partnership practice declined by 15.9% compared to larger practice groups which increased by an average of 5.1%. Providers within the Northeast US illustrated the largest migration to larger practices with 101%, 162% and 232% growth among practices with 25–99, 100–499 and over 500 providers, respectively.

Conclusion:

Urologists have been moving increasingly towards larger group practice since 2014. An emphasis on value-based healthcare, integration of electronic records and an increase in administrative workload are only some of the influencing factors likely responsible for this trend. Further studies are needed to examine the effect practice consolidation has on patient outcomes and cost of care.

Introduction

Urologic practices have changed drastically over the past decade, primarily in response to the many financial and federal adjustments that have occurred within the United States. Health policies, such as the Patient Protection and Affordable Care Act (PPACA) in 2010, have redirected practices of all specialties and sizes towards focusing on reducing costs while providing comprehensive quality care for all patients, often through practice consolidation.1,2 As seen within a multitude of other medical specialties, market consolidation has yet to be fully explored or described within the field of Urology.

As a result of market consolidation, the business of a medical practice has undergone foundational changes, most notably to physician reimbursement and cost incentive-based payments. 3 This adjustment in reimbursement has forced providers to navigate a shifting landscape within healthcare services. Community-based groups, often private practices, have seen increasing pressures towards merging and consolidating within larger practices or health systems to maintain clinical and financial sustainability. While these changes in health care dynamics influence providers, they ultimately impact patient care through changes in physician referral patterns, physician choice, availability, and even physician value within a larger health system. 4

While the American Urologic Association (AUA) provider census has reported a 13% increase in employed Urologic practice compared to self or partnership practice from 2015 to 2021, specific changes in practice size have not been analysed with Urology.5–8 Considering the known demands for urologic services among an ageing US population, in addition to the shift within physician ownership and practice, we sought to analyse the degree of and scale of these trends in Urologic practice size within the United States.

Methods and materials

Since 2014, the US Centres for Medicare and Medicaid Services (CMS) has published the Medicare Physician Compare dataset providing information on physicians participating in Medicare. Data within Physician Compare are updated twice a month as new physicians enter practice and existing physicians make changes to their practice. Accordingly, CMS provides quarterly archives to Physician Compare, providing a snapshot of the most current information. We used the archived data from September 2014, October 2015 to 2020, and June 2021 to analyse how practice size may have changed over time.

The resulting dataset contains all physicians performing at least one procedure billed through Medicare during the calendar year. Subsequent results were filtered so that all physicians listing ‘Urology’ as their primary specialty were captured. Next, the practice size of each individual urologist was determined. Practice sizes within Physician Compare are defined as the total number of professionals belonging within a medical group (Urologists and non-Urologists). Urologists practicing under multiple unique organisations were listed with the smallest group practice they were affiliated with. Also, Urologists lacking a group affiliation were recorded as working in a solo practice with a size of 1.

After obtaining group size information for each Urologist, practice sizes were categorised into six distinct categories: 1 or 2, 3–9, 10–24, 25–99, 100–499, and ⩾ 500 professionals. We then calculated both the number and proportional breakdown of Urologists within each practice size for each year during the study period. To provide further information on trends, changes in number and proportional breakdown of 2014 and 2021 were compared while stratifying by geographical region within the United States, Northeast, Midwest, West, and South.

Finally, we analysed data at the practice level by obtaining a set of unique urology practices. Unique practices were identified by their group practice identification number. Both number and proportion breakdowns for 2014 and 2021 were analysed to measure the addition/subtraction of urology practices. Institutional review designated this project exempt from further IRB review (STUDY20211336). All statistical calculations were conducted using R (version 4.0.2).

Results

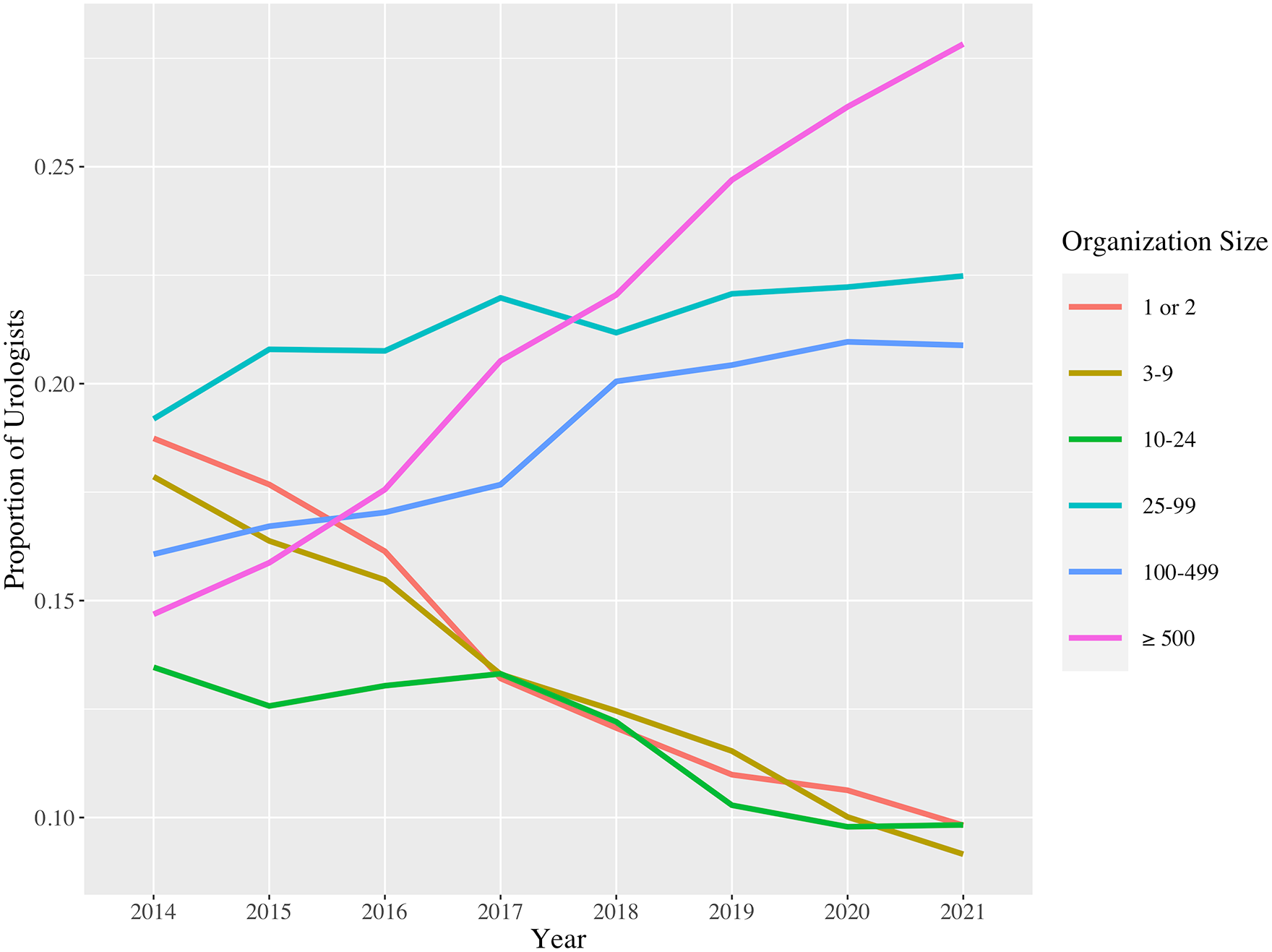

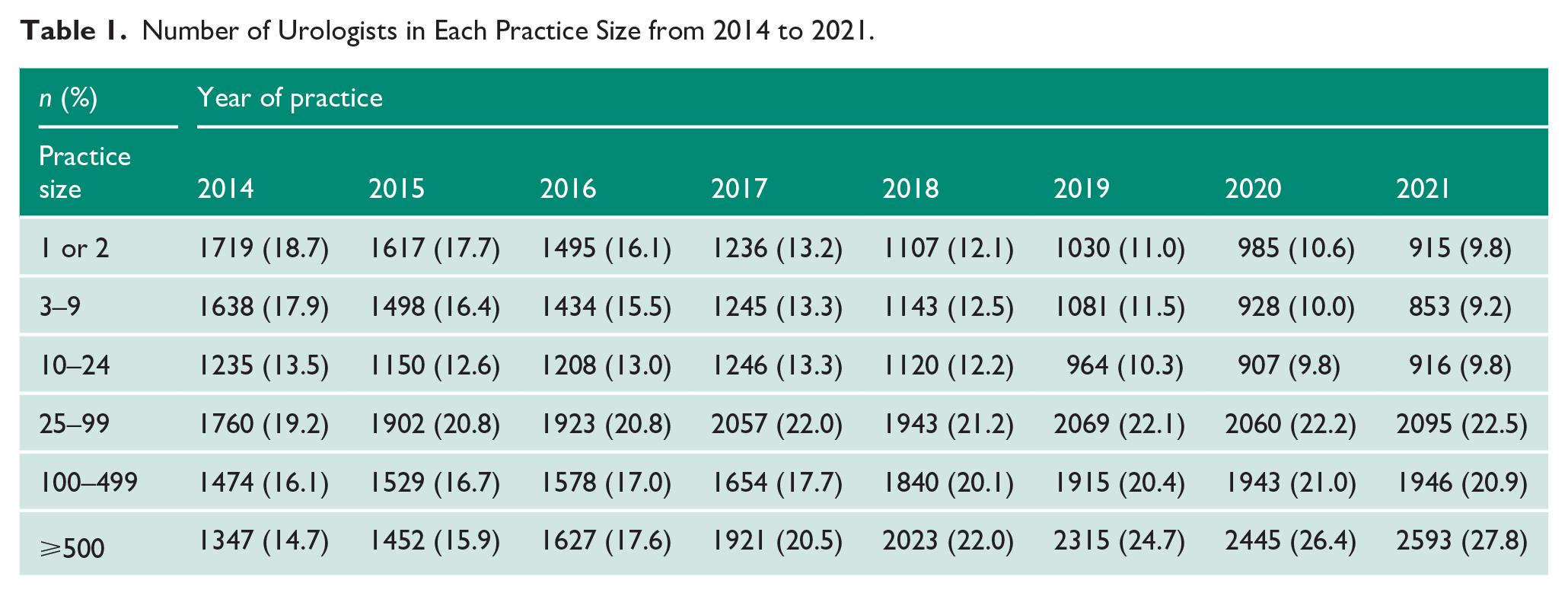

From 2014 to 2021, there was a decrease in the proportion of Urologists practicing in groups sizes of 1 or 2 (18.7–9.8%), 3–9 (17.9–9.2%), and 10–24 providers (13.5–9.8%). In contrast, there was an increase in the proportion of Urologists practicing in groups of 25–99 (19.2–22.5%), 100–499 (16.1–20.9%), and 500 or greater providers (14.7–27.8%) (Figure 1, Table 1).

Proportion of urologists employed within various healthcare organisation sizes between 2014 and 2021.

Number of Urologists in Each Practice Size from 2014 to 2021.

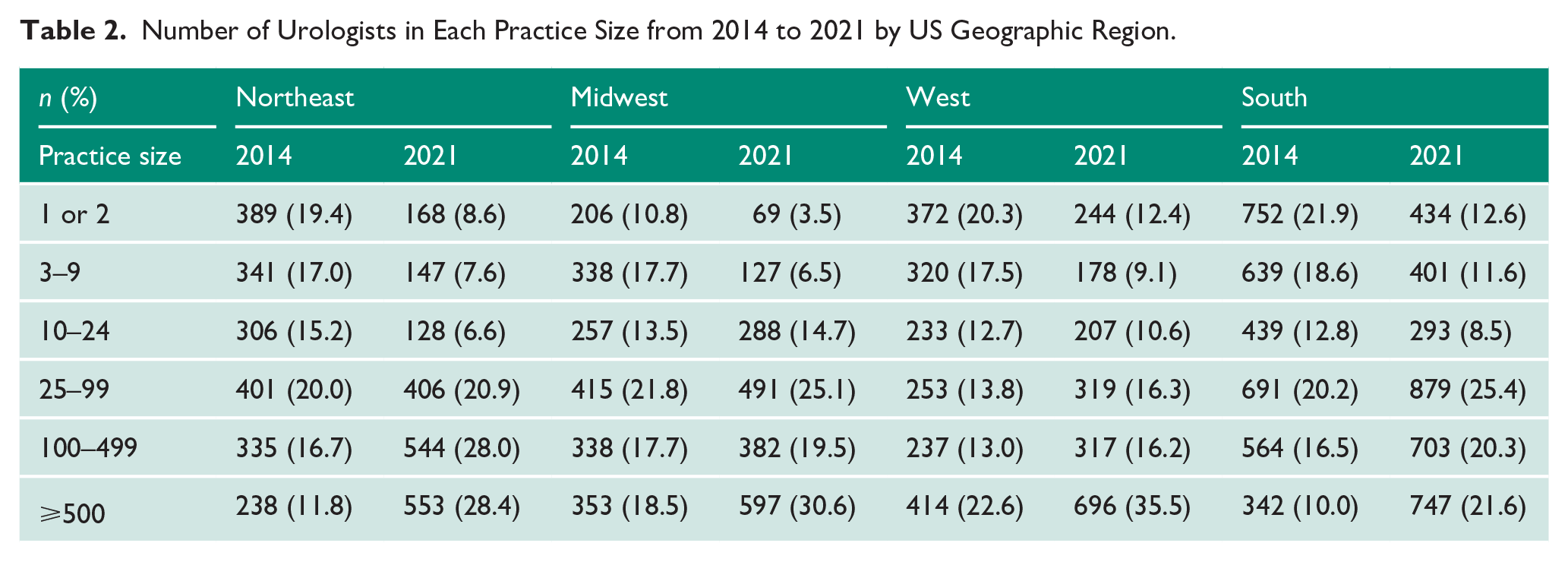

When stratifying by region across the United States, we observed a similar trend. Urologic practices with 1 or 2, 3–9, and 10–24 providers all decreased from 2014 to 2021 across the Northeast, Midwest, West, and South regions (Table 2). This change was the most pronounced within the Midwest region, with decreases within practice sizes of 1 or 2 (−67%) and 3–9 (−62%). Lesser declines occurred in the Northwest (1 or 2, −57%; 3–9, −57%), West (1 or 2, −34%; 3–9, −44%), and South (1 or 2, −32%; 3–9, −37%). Conversely, practices between 25–99, 100–499, and > 500 all increased between 2014 and 2021 across each US region. This growth was most significant within the Northeast region, where practices increased within practice sizes of 25–99 (101%), 100–499 (162%), and > 500 (232%). The only region to illustrate an increase in practice size within the 10–24 provider size was the Midwest at a 12% increase. This increase could possibly be signalling a consolidation of multiple small practices.

Number of Urologists in Each Practice Size from 2014 to 2021 by US Geographic Region.

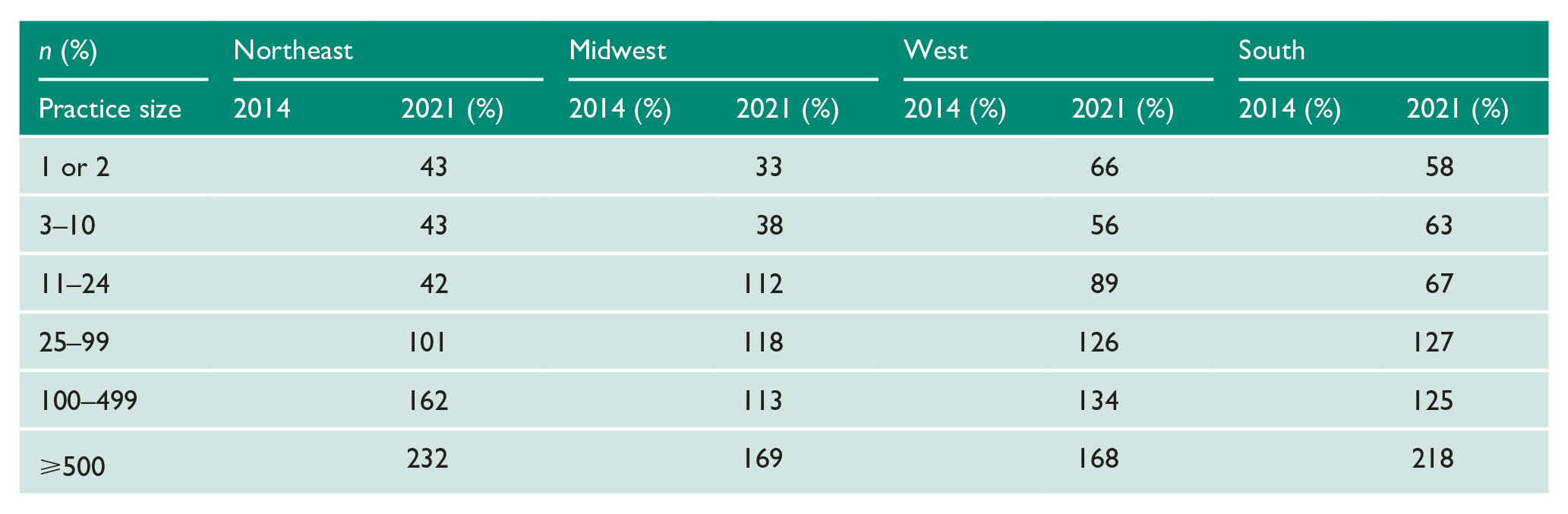

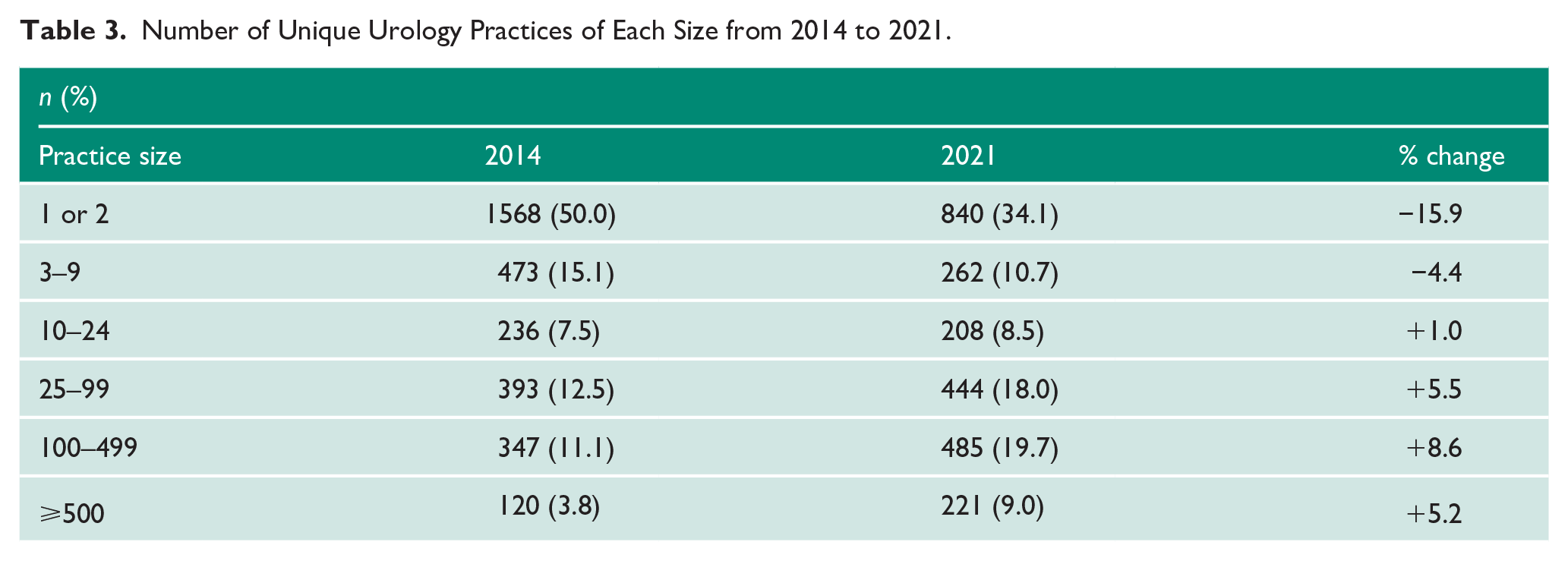

The number and proportion of unique Urologic practices have decreased at the practice level among practices sized 1 or 2 (−5.9%) and 3–9 providers (−4.4%). However, there has been an increase in the proportion of practices size 10–24 (1%), 25–99 (5.5%), 100–499 (8.6%) and > 500 (5.2%) (Table 3).

Number of Unique Urology Practices of Each Size from 2014 to 2021.

Discussion

Our analysis demonstrates a gradual consolidation of Urology practices across the United States from 2014 to 2021. This trend is demonstrated both by an increasing proportion of Urologists practicing at institutions with large practice sizes and a growth in the number of unique large practices. While variations exist within each US census region, these overall trends remain consistent across the United States and are in line with previous research documenting increased consolidation within other medical specialties.6,7,9

The observed consolidation may be explained by many factors given the changing healthcare environment over the past decade. Adjustments in reimbursement models have re-centered practice operations towards quality and cost reduction. Large medical practices are likely best equipped to meet these demands through access to favourable capital investment and technology. In addition, large practices likely benefit from access to favourable commercial reimbursement rates and market control over a specific medical specialty or technology. These costs prompted out of necessity within a medical practice become advantages through scale and lead to efficiency, also known as economies of scale. One example of the economies of scale available within a large practice is the ability to integrate an electronic medical record (EMR) while simultaneously diffusing the significant expense of an EMR across a larger number of practitioners.10,11 Consistent utilisation of resources within a large provider network often leads to improved efficiency and ultimate cost reduction per provider; all essential measures play an important role in reimbursement within the new era of health care payors.

Within the realm of Urology, there has been a gradual trend towards increasing sub-specialisation for a myriad of reasons. This trend has coincided with the transition towards larger group practices demonstrated in other subspecialized fields within the United States.6,7 Large group practices provide a forum for interdisciplinary discussion and allow practitioners to share patients to focus on the areas of expertise within their own practice. Subspecialized providers can increase procedure-specific surgical volume and, as a result, increase practice efficiency. In turn, this improves the standard of care by decreasing the morbidity and mortality for patients. 12 Academic centres or large medical groups afford this to providers and patients. An additional benefit to both patients and providers within large multi-disciplinary groups involves access to complementary medical services, such as access to radiation oncologists, medical oncologists, pathologists, primary care providers, imaging, and laboratory services all within a single similar network. In addition to reliable and cost-effective care, this internal referral pattern within large practices allows for revenue to be contained within the practice group.

Given that Urology is a surgical subspecialty, access to a provider is not consistent across rural or underserved regions. As medical practices consolidate, underserved populations and regions may face increasingly difficult access to care and the ability to recruit and retain providers to meet demand. 5 One detriment to the consolidation and vertical integration of medical practices has been the impact on health care costs for patients. While vertical integration and corporatization can lead to efficiency and increased shareholder value, it has also been shown to be loosely associated with higher medical costs and hospital spending by patients and by private preferred provider organisations (PPOs).13,14 Further analysis is needed to determine whether practice consolidation is truly beneficial for patient health outcomes and community health measures.

The trend towards larger practices over the study period may have important implications for Urologists. Historically, increased medical and financial autonomy has driven small, private practice growth. Physicians managing their own scheduling can often mould their practice model and appointments to afford more time to each patient, strengthening the physician–patient relationship, and therefore often reporting higher patient satisfaction. While conflicting literature has reported higher degrees of physician burnout within small practices, more recent cross-sectional analysis has noted that 53% of clinic-owned practices have self-described ‘zero-burnout’ compared to only 19% of hospital-owned or larger practices.15,16 This difference has been attributed to the flexible, dynamic and clinician-focused management. This is seemingly more prevalent within a small, solo, medical practice compared to a larger practice with several non-clinical external constraints and demands. Large medical practices typically incorporate non-clinical staff to help address many of these day-to-day operations within the practice. By delegating these tasks, larger practice models with dedicated non-clinical staff can effectively function as teammates with clinicians towards distributing patient demand effectively, efficiently, and safely. This model of vertically integrated team-based care is fundamentally easier to achieve within larger practice settings supported with more resources and division of practice labour.

With regard to smaller physician practices, self-employed physicians have characteristically reported higher average annual incomes than employees of a hospital or hospital-owned practice. 17 The high risk and reward nature of starting a private medical practice can be financially fruitful and require substantial capital investment and subsequent administrative responsibility essential to maintaining and running a successful practice. At an average cost of US$70,000–US$100,000, start-up expenses can be one of the greatest challenges. These expenses (i.e. durable goods, equipment costs, insurance, staff, and overhead) are essential to all practices regardless of size; however, they can be more readily dispersed across multiple providers within larger practice groups or among groups owned and managed by private equity. Young and new providers may see the benefits of dedicated and consistent management, accommodating practice patterns, and low overhead cost as increasingly favourable and further drive practice changes into the future.

While the transition towards larger Urologic practices is widely recognised, what remains unclear is the structure and characteristics of the groups actively performing the consolidation. Several models of provider employment have become omnipresent within healthcare, namely the trend towards hospital employment versus multi/single-specialty practice managed through private equity. While our dataset is unable to illicit practice management details, further work and understanding regarding the management dynamics would be invaluable with regard to understanding the resulting influence on patient access, cost, insurance rates and coverage and outcomes. Future directions will be aimed towards better exploring and eliciting these differences.

Our study contains several limitations. First, the CMS physician compares dataset only includes those providers accepting Medicare patients and, therefore, can miss any Urologic providers that do not accept any Medicare patients. This dataset also does not separate Urologists who have completed fellowship or specialist training to allow for further practice pattern identification. In addition, some practices may list their practice under multiple smaller practices for business and tax purposes. This ultimately may cause an underrepresentation of the number of large practices within the data. Our study is likely confounded as it includes 2019–2021 of which the COVID-19 pandemic had immeasurable impact and influence on health care delivery and practice patterns. Finally, we are limited by the data collection timeframe and cannot compare changes in practice size outside of 2014–2021.

In conclusion, we noted that Urologists have been moving towards larger group practice models between 2014 and 2021. This is most likely due to the changes in medical infrastructure, market forces, and delivery of health care within the United States. An emphasis on value-based healthcare, integration of electronic records, and an increase in administrative workload are only some of the influencing factors likely responsible for this trend. Further studies are needed to examine the effect practice consolidation has on the patient outcomes and the cost of care.

Footnotes

Conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical approval

University Hospitals Cleveland Medical Centre and Case Western Reserve University do not require ethical approval for reporting data from this study following internal review – STUDY20211336.

Informed consent

Informed consent was not necessary for this project.

Guarantor

M.C.

Contributorship

T.C., M.C., and A.D. researched literature and conceived the study. B.P., M.C., and A.A. were involved in protocol development, gaining ethical approval, data gathering and data analysis. T.C. and B.P. wrote the first draft of the manuscript. All authors reviewed and edited the manuscript and approved the final version of the manuscript.