Abstract

Intergenerational poverty and scarce financial resources can create and sustain detrimental behaviors and outcomes among adolescents. Efforts to increase financial literacy and job-related skills, however, can offer youth from low-income households knowledge, skills, and opportunities otherwise unavailable to them. Targeted interventions that combine financial literacy and job-readiness components may help adolescents disrupt the cycle of intergenerational poverty by increasing economic awareness, adaptive financial behaviors, and work-related skills. Drawing on career construction and asset theory, the present study examined changes in financial knowledge and labor skills among youth from low-income households (N = 111) over the course of their participation in the Road to Success curriculum as well as how changes varied across demographic characteristics of participants. Data analysis included descriptive statistics, t-test analyses, and MANCOVA. Results indicated several improvements from Wave 1 to Wave 2 as students developed job-readiness and financial literacy knowledge. Potential educational and policy implications are discussed.

An estimated 18% of US adolescents live in families with incomes below the federal poverty line (Department of Health and Human Services, 2018). Researchers have consistently demonstrated the importance of economic stability and how it can be transmitted across generations from parents to youth (Hubler et al., 2016). Children born into families living in poverty are 6 times as likely to live in poverty in adulthood as compared to children born into wealthier families (Odgers and Adler, 2018; Ratcliffe and McKernan, 2010). In addition to having fewer material resources, youth in lower income families may have reduced knowledge of modern financial services (Clark et al., 2018; Garg and Singh, 2018) and limits in the development of job-skills (Moore and Morton, 2017). Contemporary youth report low levels of financial literacy, (i.e. the ability to process economic information and make informed financial decisions; Gal, 2014; Supon, 2012) and are often perceived as lacking job readiness (e.g. employability skills such as critical thinking, and preparation for workplace communication, Moore and Morton, 2017). In addition, research has found that female students, migrants, and students with low-income parents have lower levels of financial knowledge (Oberrauch and Kaiser, 2020).

Research on financial literacy programs among low-income youth typically include knowledge on planning strategically around issues such as student loans or credit card debt, which may improve their ability to manage already scarce wealth (Lusardi et al., 2010). Although there has been some research that suggests that financial literacy interventions fail to improve the quality of financial decision making (Ambuehl et al., 2014), encouraging youth to develop skills that increase their chances of obtaining and maintaining employment (i.e. job-readiness skills) along with financial literacy knowledge, may also offer benefits (Hartog et al., 2016). Research by Kaiser and Menkhoff (2017) found evidence that financial education might be less effective for low-income families, yet, efforts to increase both financial literacy and job-readiness may offer low-income youth economic and social capital that would otherwise be unavailable to them, providing important benefits for their future financial behaviors and outcomes (Berry et al., 2015). Therefore, the present study examined the effectiveness of a combined financial literacy and job-readiness intervention, in promoting financial and work-readiness knowledge and behaviors among youth from low-income households in the Midwest US.

Addressing intergenerational poverty

A prevalent characteristic among families with low incomes is intergenerational poverty (Lee and Seon, 2019), a cycle wherein poverty is transmitted from one generation to another, with poor parents having poor children, who are then more likely to develop into poor adults. For vulnerable youth, low levels of financial literacy make it difficult to escape from the cycle of intergenerational poverty, as family income is positively associated with financial literacy in young people, and youth financial literacy is positively correlated to the amount of wealth they can accumulate during adulthood (Loibl, 2017; Lusardi and Tufano, 2015). In addition, research has demonstrated the importance of financial literacy in achieving economic stability for low-income families, in particular youth, whose financial situation is characterized increasingly by high levels of debt (Lusardi and Mitchell, 2014), often causing anxiety and stress, while also influencing job-related decisions (Clark et al., 2018). Although intergenerational poverty has been linked to the emergence and sustenance of wage stagnation (Pew Research Center, 2017), low-income families can achieve economic stability by securing employment that allows them to build assets through savings, small businesses, and housing (Federal Deposit Insurance Corporation (FDIC), 2009).

Learning job-readiness skills, accessing a living wage, and developing financial knowledge can be challenging for youth, as intergenerational poverty is linked to inadequate education and health care, poor mental health, fewer assets, and fewer economic and labor opportunities (Cedeño et al., 2020; Drentea and Reynolds, 2015; Gugushvili, 2016). Scarce financial resources can create and sustain detrimental behaviors and outcomes in children, adolescents, and their families, for instance, by means of transmission of economic-related stress from parents to children (Santiago et al., 2012; Yeung et al., 2002). Because unemployment is a strong predictor of poverty, job readiness programs are important for youth who live in poverty, as securing permanent employment would offer income in the form of wages and benefits (Paul et al., 2018). In contrast, poor job-readiness skills among young adults may hinder important critical skills and job-related experiences, which can lead to decreased employability skills (Turan, 2021) and low wages in adulthood (Lim and Mitchell, 2017).

The cycle of intergenerational poverty in which many low-income families are embedded is difficult to escape in part due to low wages that make it difficult for families to pay off debt or afford necessary goods and services (Marimpi and Koning, 2018; Ponnet, 2014). It is particularly difficult for racially minorized families (i.e. racial and ethnic groups who are rendered minority status based on others’ perceptions of their identities or systems that favor privileged identities; Benitez, 2010; Stewart, 2013) to escape intergenerational poverty, as they are far more likely to be poor than their white counterparts (Working Poor Families Project, 2018). The depletion or reduction of funds of social programs such as Temporary Assistance for Needy Families (TANF), has often produced negative unintended consequences for adolescents and families (Allen et al., 2013; Cilesiz and Drotos, 2016). Adding to these challenges is the fact that low-income households are less likely to have checking or savings accounts, and often have less exposure to or knowledge about other financial services (Federal Deposit Insurance Corporation (FDIC), 2009). Valero et al. (2019) have suggested that low-income racially minoritized youth may have little instruction in job-readiness (i.e. training programs designed to provide individuals with the skills needed to look for, obtain, and maintain a job; Strauser et al., 1998), thus limiting their potential to further develop these skills. Moreover, previous research has found that financial literacy has important consequences for financial behavior (Garg and Singh, 2018).

Compounding these issues, impoverished families may be more exposed to predatory aspects of the financial system that can trap them in costly debt (Lusardi and Tufano, 2015). For example, predatory loans often target low-income and racially minoritized communities with ‘payday’ loan interest rates reaching an average APR up to 400% (Policy Link, 2017) and low-income families may not have other loan options available (Seamster and Charron-Chénier, 2017). Partially because of limited education on financial issues, low-income youth tend to fall victim later as adults to high-interest rate loans and increasing debt (Seamster and Charron-Chénier, 2017; Sherraden and Ansong, 2016), which they often must incur because their wages are not enough to cover basic household needs or because of unforeseen events (e.g. a medical emergency; Pew Research Center, 2018). Adding to an already precarious budget, financial products such as credit cards, student loans, mortgages, and retirement accounts have proven to be difficult to access for low income youth (Daly and Kelly, 2015). Although there is some evidence about the benefits of higher levels of financial literacy and job-readiness for changing financial and work-related behaviors (Danes et al., 2013; Moore and Morton, 2017), curricula vary widely and findings in this research area remain mixed (Kaiser and Menkhoff, 2017).

Financial literacy is associated with more responsible long-term financial planning such as investing and saving for retirement—as well as short term management such as avoiding overdrafts of checking accounts and maintaining an emergency fund (Fox et al., 2005; Henager-Greene and Cude, 2016). Nevertheless, there are theoretical and practical gaps in the literature regarding the effects of combined financial literacy and job-readiness interventions (Moore and Morton, 2017). In addition, although research has considered financial literacy among low-income families (Hartog et al., 2016) there is still a gap in understanding how low-income racially minoritized communities, and particularly adolescents from these communities, benefit from interventions that incorporate a dual approach addressing both financial literacy and job-readiness. Given that adolescence is a period when many individuals first enter the workforce and begin to earn a wage, this developmental period may offer a critical “teachable moment” for concrete application and reinforcement of learned skills (Kaiser and Menkhoff, 2017).

Targeted interventions that combine financial literacy and job-readiness components may help adolescents from low-income households disrupt the cycle of intergenerational poverty by increasing economic awareness, adaptive financial behaviors (Clark et al., 2018; McCormick, 2009), and work-related skills such as cooperation and creativity (Moore and Morton, 2017). Specifically, increased financial literacy may help youth strategically address issues such as student loans or credit card debt that may hinder their ability to manage already scarce wealth (Lusardi et al., 2020), while job-readiness skills may impact employment opportunities and earnings (Hartog et al., 2016). That is to say, efforts to increase both financial literacy and job-related skills may offer youth from low-income households career construction skills and financial knowledge that would otherwise be unavailable to them, providing important learning opportunities for their future financial behaviors and employment possibilities (Johnson and Sherraden, 2007; Krause et al., 2016).

Overview of the present study

To some extent, economic stability is dependent on both the knowledge to properly administer and manage economic capital accrued through work and access to opportunities to earn a wage that satisfies household budgets. Therefore, the present study focuses on the improvement of financial literacy as well as job-readiness skills, and utilizes an asset-based theory (Sherraden, 1990) as a framework for conceptualizing how financial and job-related knowledge may benefit vulnerable youth, a population that typically does not have wide access to accurate financial information (Clark et al., 2018) and often struggles to access lucrative employment (Pew Research Center, 2018). Specifically, the present study sought to evaluate changes in youth's financial literacy and job-readiness over the course of their participation in a school-based program.

The present study utilized a non-experimental design to examine changes in job-readiness and financial literacy variables for students completing the Road to Success curriculum. Because of funding and school partner requirements that excluded the possibility of including a control group, the curriculum was provided to any students at partner schools that qualified to participate in the program. Two waves of quantitative surveys were administered: one before students received the curriculum (Wave 1), and one after receiving the curriculum (Wave 2). Our primary research questions were: 1) Would youth from low-income households involved in a job-readiness and financial literacy program experience increases in financial literacy variables such as financial knowledge, saving behaviors, having checking and savings accounts, and communicating with family about finances following completion of the program? And, 2) Would youth from low-income households involved in a job-readiness and financial literacy program experience increases in job-readiness variables such as job-related knowledge, job-obtainment self-efficacy, and current employment? Given consistent evidence of gender disparities in financial behavior and youth employment experiences (Fernandes et al., 2014; O’Reilly et al., 2019), and, historically, meta-analytic evidence that financial education programs are often variable in their effectiveness depending on the income and socio-economic status of their participants (Fernandes et al., 2014), we also conducted secondary exploratory analyses to examine whether changes in job-readiness or financial literacy variables from pre- to post-intervention differed by youth's gender or socioeconomic status.

Description of the curriculum

The Road to Success curriculum consists of ten lessons: six focused on workforce readiness, three on financial literacy, and one review session that integrated concepts from all nine previous lessons. The curriculum includes current statistics and research findings, engaging student-centered discussions and activities, and practical projects that result in a product (e.g. competitive résumés) that the participant can use to be successful in their transition into adulthood. The participants received the curriculum once per week over a 10-week period and each session lasted 50 min. The job-readiness lessons were compiled using the Empower Your Future: Career Readiness Curriculum Guide (Commonwealth Corporation, 2016) and training materials from CYGNET Associates. The main learning objectives were:

Identify signature character strengths and how to cultivate lesser strengths Identify transferrable skills to create an elevator speech Learn problem-solving skills and apply them to workplace scenarios Increase knowledge of the job search and application process Learn the components of a résumé (design, layout, format, content, key words, action verbs, references, etc.) Create a résumé and reference list Identify the etiquette and procedures for an interview including the preparation and follow-up Participate in a mock interview and provide constructive feedback to other participants Identify dominant Money Habitude(s) and discuss how they impact relationships Describe and create a S.MAR.T. goal Increase knowledge of potential obstacles for financial goal setting including unexpected expenses and spending leaks Demonstrate knowledge of options to track and balance income and expenses Create a monthly spending plan based off current and local pricing including median salary, housing options, grocery expenses, etc. Discuss the connection between conflicts in relationships and money

The financial literacy lessons were compiled using the High School Financial Planning Program curriculum (National Endowment for Financial Education, 2014) and the Money Habitudes curriculum from The Dibble Institute (Pool and Solomon, 2014). The main lesson topics are listed below. A final review session consisted of multiple scenarios that participants had to resolve referencing concepts, strategies, or skills learned from the Road to Success curriculum. The primary learning objectives for the financial literacy sessions were:

In addition to the curriculum, an important foundational assumption of the program was that participants would be more receptive to curricular concepts and tasks if they were also able to develop meaningful relationships with the program facilitators. Therefore, in addition to training on the curriculum, staff were also trained on strategies for developing rapport with low-income youth, determining the appropriate degree of self-disclosure of their own lived experiences, and remaining non-judgmental and supportive. Throughout the Road to Success program, facilitators intentionally integrated aspects of all course content, including how youths’ broader life-goals surrounding relationships, career, and finances were related and impacted each other. Additional details about the specific resources (e.g. activities, audio/visual materials) and lesson-plans utilized in the Road to Success curriculum are available upon request

Methods

Participants

Adolescents who participated in the Road to Success curriculum during Spring 2018 (N = 112) provided data at both a baseline, prior to the intervention (Wave 1) and approximately 5 months later following completion of the curriculum (Wave 2). Participants were recruited by posting flyers, visiting schools, and collecting student interest forms at five partner high schools in a midsize Midwestern city. The sample was predominately female (Gender, Female = 73.7%, Male = 25.3%, Trans = 0.9%) and approximately half the sample identified their ethnicity/race as African American (Ethnicity, African American = 48.4%, European American = 16.8%, Asian American = 15.8%, Latinx = 6.3%, Native American or Alaskan Native = 5.3%, Other = 7.4%). The average age of youth in the study was 15.82 (SD = .86). Nearly three-fourths of the sample (72.6%) reported that their family received some form of governmental assistance such as Temporary Assistance for Needy Families, Free/Reduced Lunch, or Cash Assistance. Approximately 46.2% of youth reported that their biological or adopted parents were married, 20.5% reported their biological or adopted parents were divorced/separated, and 16.1% of youth were in single parent families.

Measures

Demographics

Significant evidence suggests that youth's access to economic opportunities and financial and social experiences may be shaped by factors such as their race/ethnicity, gender, parental marital status, and age (Fomby et al., 2010; Mandara and Murray, 2000). For analyses, categorical variables (e.g. race/ethnicity, gender, parental marital status) were recoded into dichotomies (African American = 1, all other racial/ethnic groups = 0; women = 1, men = 0, and one transgender participant was dropped from analyses given statistical analysis requirements; youth with married parents = 1, all other family structures = 0).

Financial literacy and job-readiness content knowledge

At baseline (Wave 1) and the follow-up assessment (Wave 2), adolescents reported on 10 content knowledge questions created by the developers of the Road to Success curriculum to assess the “big ideas” regarding the financial literacy and job-readiness knowledge (e.g. I should always turn off (or silence) my cell phone and beeper before heading into an interview; 0 = false, 1 = true). Scores were computed by assigning 1 point for every correct answer, and 0 for every incorrect answer and calculating a sum score.

Job-obtainment self-efficacy

At each wave, adolescents reported on their job-obtainment self-efficacy with 16 items from the job search self-efficacy scale (Saks et al., 2016). Participants were asked to rate their confidence in different activities such as, “Plan and organize a weekly job search schedule” and “Be successful in your job search”; (1 = not confident at all to 5 = totally confident). Although this scale initially had two factors (job behaviors and outcomes), we combined these two subscales as they were highly correlated (r = .87Wave1 and .82Wave2). These scales were averaged for each individual, with higher scores indicating more job-obtainment self-efficacy. This combined scale demonstrated strong reliability at each wave (α = .97).

Saving behaviors

At each wave, adolescents reported on their saving behaviors with nine items (Varcoe et al., 2005; for example, “When I get money, I save some of it no matter what”; 1 = strongly disagree to 4 = strongly agree). These items were averaged with higher scores indicating more saving behaviors. This scale demonstrated adequate reliability at each wave (α = .76 and .79).

Job-readiness and financial behaviors

Adolescents were asked at each wave whether they (0 = no, 1 = yes) had a résumé, checking account, or savings account, were currently employed, or used a budget. These job-readiness and financial behaviors were used as individual dichotomous outcomes of interest throughout analyses.

Family communication about finances

Adolescents reported on their communication with family members about finances with four items (Varcoe et al., 2005; for example, “I talk to my family about my own use of money”; 1 = never to 4 = a lot). Items were averaged with higher scores indicating more communication with family members about finances. This scale demonstrated adequate reliability at each wave (α = .78, .86).

Procedure

Prior to data collection, all study procedures were approved by the institution of record's Institutional Review Board. Parent permission, child assent, and/or informed consent were obtained for participation in the research component of a grant-funded program that provided healthy relationship education to underserved (e.g. foster care exposure, from low socioeconomic households) youth in an urban, Midwestern county. The program recruited participants through partner sites that included local high schools and alternative schools. Sites hosted one to four groups, with a total of 14 groups of students participating. Data collection took place during regularly scheduled group meeting times at each partner site; demographic data were collected in August and September of 2018, with Wave 1 data collected in January and February of 2019, and Wave 2 data collected in April of 2019. Researchers communicated the voluntary nature of the study and obtained verbal assent to participate. Then, assistants handed out iPads to each participant to complete Qualtrics-based surveys. Once participants completed the surveys, a staff member gave them a $10 gift card as an incentive. Participant identification numbers linked the surveys across data-points.

Analyses

First, correlation matrices were computed of Wave 1 variables in order to evaluate associations among demographic variables, and baseline financial and job-readiness knowledge and behaviors. Second, to evaluate changes in variables of interest after completion of the Road to Success curriculum, we conducted a series of paired sample t-tests (for continuous variables; content knowledge, job-obtainment self-efficacy, and savings behaviors) and McNemar tests (for dichotomous variables; use of a résumé, budget, checking and savings accounts, employment status) comparing Wave 1 and Wave 2 reports. Finally, we conducted exploratory analyses to investigate if changes in continuous outcomes differed by youth's gender or socioeconomic status. A MANCOVA was conducted using residual change scores to represent change from Wave 1 to Wave 2.

Results

Preliminary analyses

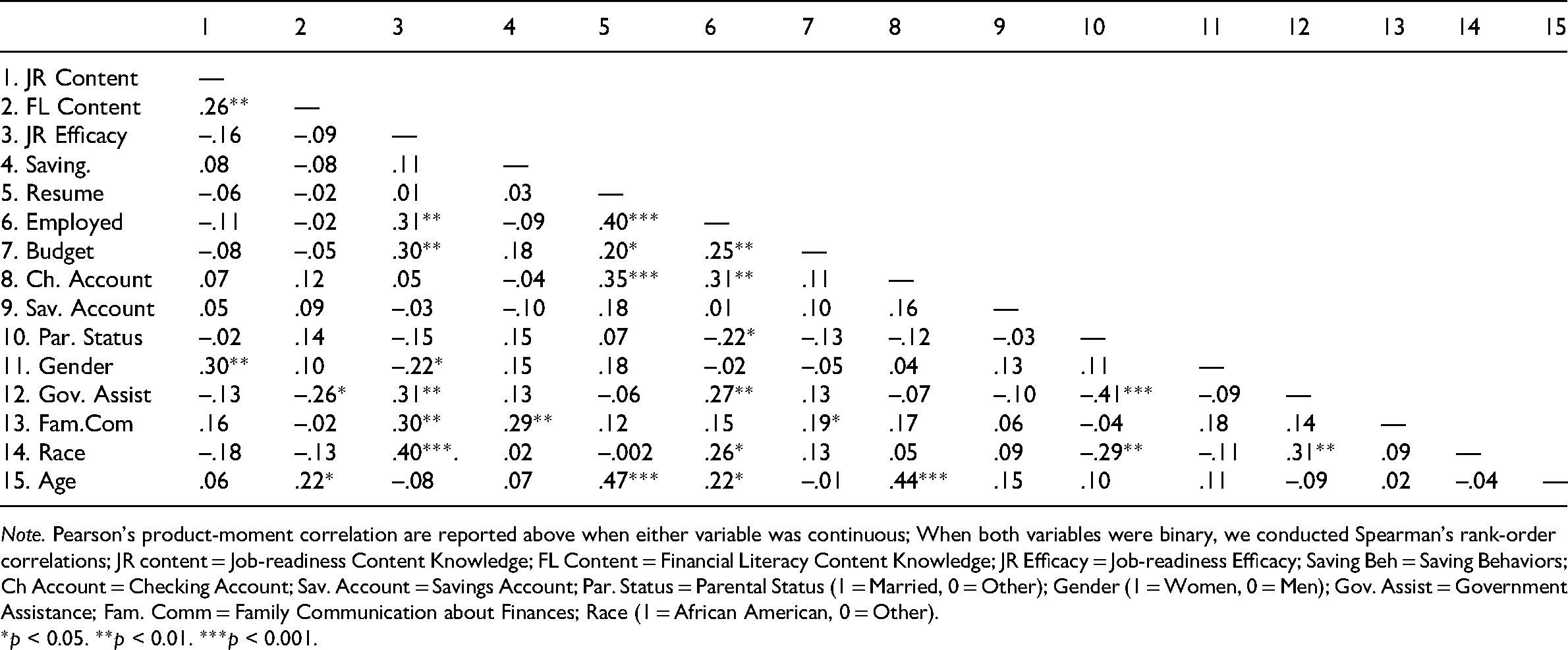

Correlation coefficients among all variables measured during Wave 1 (prior to participation in the Road to Success program) are reported in Table 1. Aligning with previous research (e.g. Taft et al., 2013), age was associated with several variables related to financial literacy. Specifically, there were statistically significant positive correlations between student's age and higher scores on Wave 1 personal finance content questions (r = .22, p = 0.043), having a résumé (r = .47, p <.001), being employed, (r = .22, p = 0.040), and having a checking account (r = .44, p < .001) prior to their participation in the Road to Success curriculum. Students who identified their race/ethnicity as African American were more likely to have a higher sense of job-obtainment self-efficacy (r = .40, p < .001), were less likely to be living in a household with a pair of biological married parents (r = ‒.29, p = 0.004), though were more likely to report being employed at baseline (r = .26, p = 0.012) and more likely to be receiving government assistance (r = .31, p = 0.002) as compared to youth not identifying as African American.

Correlations for pretest variables.

Note. Pearson's product-moment correlation are reported above when either variable was continuous; When both variables were binary, we conducted Spearman's rank-order correlations; JR content = Job-readiness Content Knowledge; FL Content = Financial Literacy Content Knowledge; JR Efficacy = Job-readiness Efficacy; Saving Beh = Saving Behaviors; Ch Account = Checking Account; Sav. Account = Savings Account; Par. Status = Parental Status (1 = Married, 0 = Other); Gender (1 = Women, 0 = Men); Gov. Assist = Government Assistance; Fam. Comm = Family Communication about Finances; Race (1 = African American, 0 = Other).

*p < 0.05. **p < 0.01. ***p < 0.001.

Changes in knowledge and behaviors

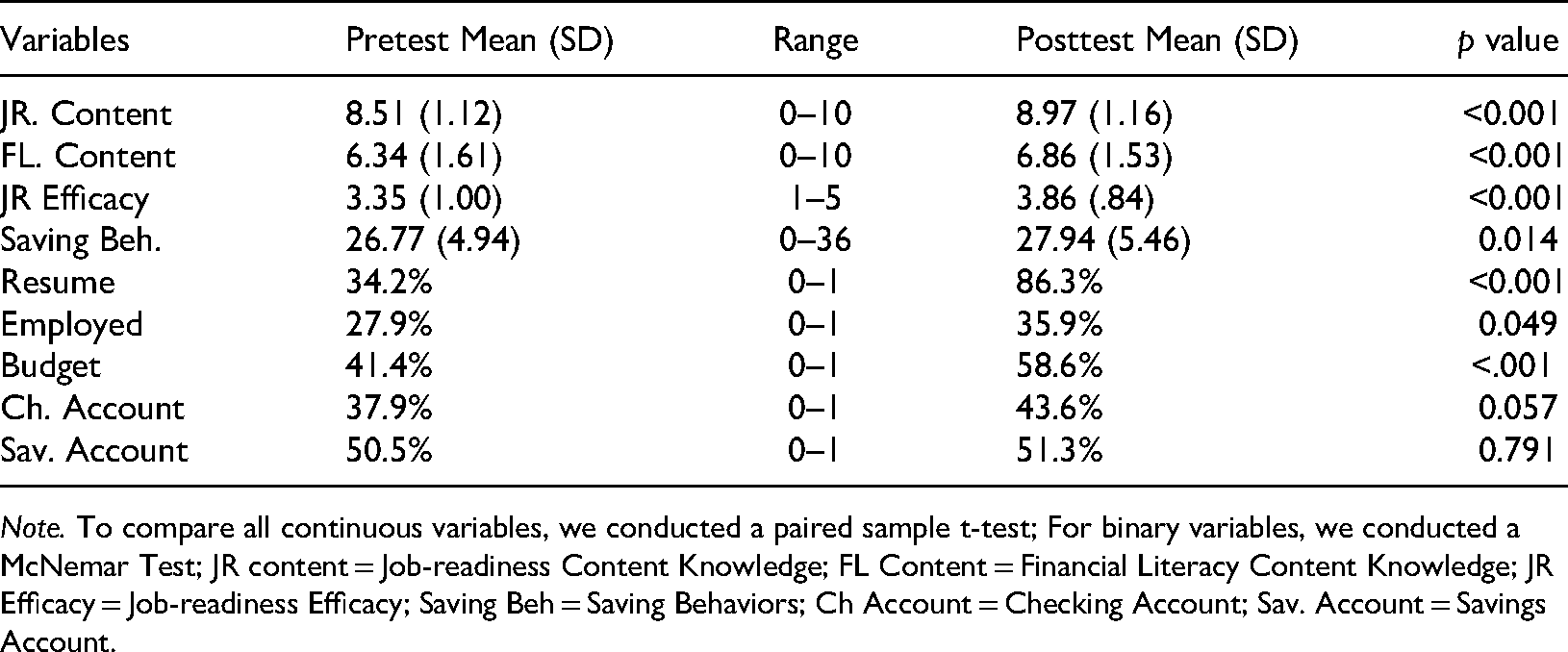

As shown in Table 2, analyses indicated that participation in Road to Success was associated with several improvements over time (see Table 2). Specifically, students improved in knowledge of both job-readiness [t (110) = 4.21, p < .001] and personal finances [t (110) = ‒3.90, p < .001]. Students were also more likely to report higher levels of job-obtainment self-efficacy [t (110) = 6.48, p < .001] and engagement in savings behaviors [t (110) = 2.50, p = 0.014] following the completion of the program. McNemar tests, which systematically examine if proportions of dichotomous frequencies over time are equal, were conducted on Job-Readiness and Financial Behaviors following the completion of Road to Success. Results indicated that compared to baseline, students in the program demonstrated an increase in the use of a résumé (p < .001) and budget (p < .001), and also exhibited an increased likelihood of being employed (p = 0.049). Youth did not report using a checking (p = 0.057) and savings accounts (p = 0.791) more following program completion.

Change in variables over time.

Note. To compare all continuous variables, we conducted a paired sample t-test; For binary variables, we conducted a McNemar Test; JR content = Job-readiness Content Knowledge; FL Content = Financial Literacy Content Knowledge; JR Efficacy = Job-readiness Efficacy; Saving Beh = Saving Behaviors; Ch Account = Checking Account; Sav. Account = Savings Account.

Correlation coefficients between residualized change scores and predictor variables.

Note. ≜ = residual parameter (i.e. change) from pre to posttest; Pearson's product-moment correlation are reported above when either variable was continuous; When both variables were binary, we conducted Spearman's rank-order correlations JR content = Job-readiness Content Knowledge; FL Content = Financial Literacy Content Knowledge; JR Efficacy = Job-readiness Efficacy; Saving Beh = Saving Behaviors; Par. Status = Parental Status (1 = Married, 0 = Other); Gender (1 = Female, 0 = Male); Gov. Assist = Government Assistance; Fam. Comm = Family Communication about Finances; Race (1 = African American, 0 = Other). For resume, employment, and budget, if youth reported using these strategies at pre and posttest, they received a 0; A minimal number of youth reported using these strategies at pretest and not at posttest, these youth received a 0.

*p < 0.05. **p < 0.01. ***p < 0.001.

Exploration of factors associated with changes in knowledge and behaviors

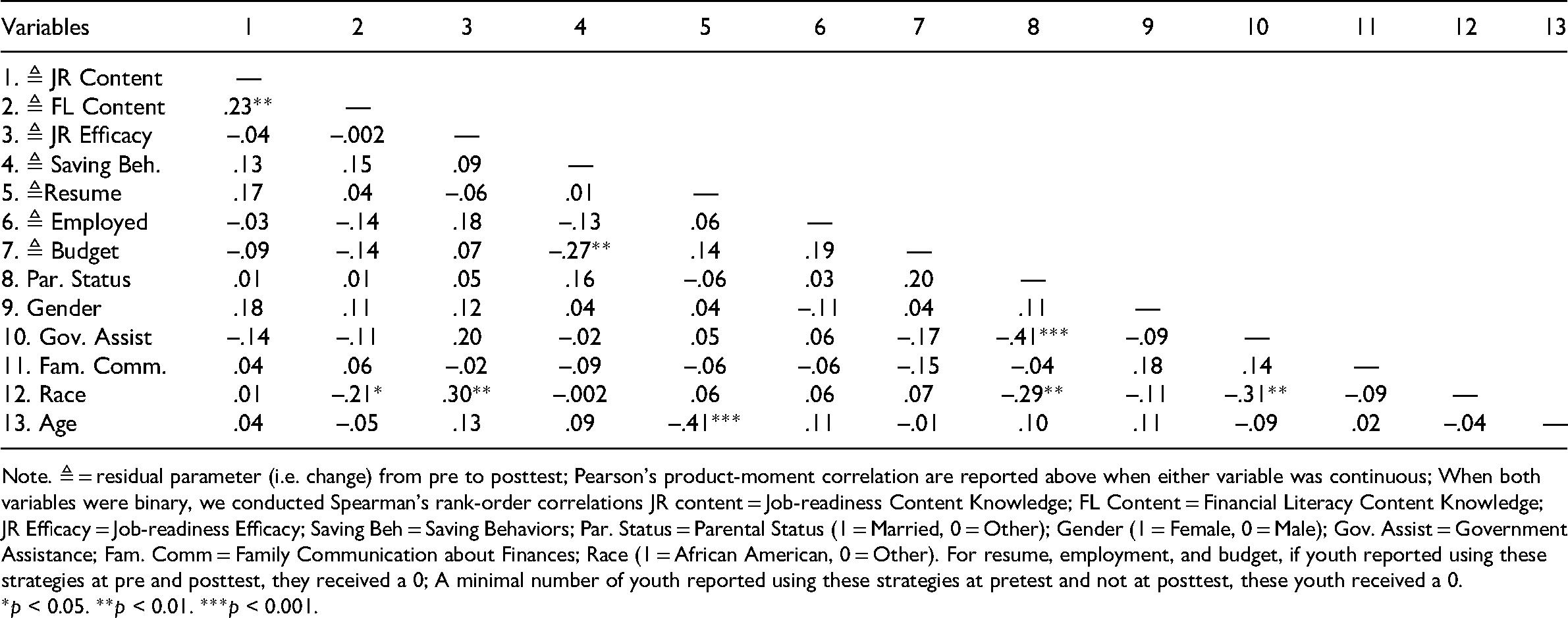

We then computed residual change scores for knowledge about job-readiness and financial literacy and behaviors targeted by Road to Success (see Table 3). In the current study, residual change scores were calculated to provide estimates of change in the variables of interest Residualized change scores were calculated by regressing a variable (e.g. financial literacy at Wave 2) on itself at a prior occasion (financial literacy at Wave 1), with the residuals representing any variance that is not explainable by Wave 1 levels of that variable—that is, variability due to change (Castro-Schilo and Grimm, 2018). There were no statistically significant differences in changes from Wave 1 to Wave 2 by gender (F (4, 88) = 1.19, p = 0.321; Wilk's Λ = 0.95, ηp2 = .05) or socioeconomic status (F (4, 88) = 1.94, p = 0.112; Wilk's Λ = 0.92, ηp2 = .08). These non-significant results suggest that Road to Success did not differ across gender and socioeconomic status.

Discussion

The present study empirically examined changes that occurred for youth completing Road to Success—a job-readiness and financial literacy educational program aimed at improving work-related and financial outcomes for youth from low-income households. Results of the present study indicated that after completing a comprehensive program targeting both job-readiness and financial literacy, youth exhibited an increase in relevant knowledge, job-obtainment self-efficacy, and self-reported financial and work-related behaviors. These results provide promising evidence for the positive influence of teaching both personal finance and job-readiness skills to lower income adolescents via targeted intervention programs, and aligns with prior research on the effectiveness of job-readiness (Hartog et al., 2016) and personal finance programs (Lusardi et al., 2010) among low-income families.

The overall pattern of results aligns with the conceptualization that early training in financial literacy can influence a life-long habit of savings, improve financial security, and stimulate a more future-oriented economic outlook (Amagir et al., 2018; Johnson and Sherraden, 2007). Furthermore, the reinforcing components of the job-readiness and financial literacy curricula may represent an increase in youths’ “capital”, equipping them with resources that provide a sense of agency and the ability to accumulate and manage assets to better navigate their world (Bourdieu, 1986). Indeed, economic stability may require both access to opportunities to earn a wage that satisfies household budgets as well as the knowledge to properly administer and manage economic capital accrued through work. For instance, by using a strengths-based approach, facilitators worked with participants on developing a résumé that demonstrated how their school, volunteer, and work experiences would make them a qualified job candidate for positions aligned with their interests. Adolescents also participated in mock interviews with program facilitators, school personnel, and local community volunteers. Engaging in these kinds of mastery experiences via experiential learning and role-playing can be an effective way to bolster self-efficacy (Bandura, 1997; Parikh-Foxx et al., 2020). Lessons always provided opportunities for some form of active participant engagement. For example, in the last lesson, adolescents were given several hypothetical scenarios composed by several factors (e.g. a specified occupation, monthly income, and expenses; unanticipated financial emergency, etc.) and asked to develop a spending plan that identified and avoided “spending leaks.” These active learning strategies engaged youth in a learning process that required thoughtful reflection and action applied to real-world scenarios (McConnell et al., 2017). After completing Road to Success, youth were more likely to report higher levels of job-obtainment self-efficacy. This is notable given that those with greater general self-efficacy may be more likely to engage in and persevere in activities required for searching for a job (Ozyilmaz et al., 2018).

Interestingly, in the present study, students who identified as African American were more likely to report higher job-obtainment self-efficacy and were more likely to report being employed before starting the curriculum, despite higher rates of receiving government assistance and lower rates of living in a household with a pair of biological married parents. It is possible that our sample, which consisted largely of African American women, may come from households where additional financial assistance is needed. There is justification for the development of financial literacy interventions targeted specifically to women, mostly because they tend to have fewer personal savings/investments and confront challenges related to access to financial services (Coleman and Robb, 2018; Hira and Loibl, 2008). Incorporating existing vocational role-models, while also expanding exposure to adults in a variety of careers may be an important area for future applied programming and research (Gottfredson and Lapan, 1997; Valero et al., 2019), given that low-income racially minoritized families face a higher risk of poverty and economic exclusion (Cedeño et al., 2020).

Additionally, after program participation, youth were also more likely to engage in a variety of behaviors that are related to positive long-term economic outcomes—such as greater likelihood of having a résumé and being employed. To support this outcome, aspects of the curriculum included lessons about the job search and application process, the different components of résumé building, and etiquette and procedures of job interviews. Notably, after the curriculum, youth were not more likely to have a checking account, which suggests that additional motivation may be needed to help youth track and balance income, a necessary step for addressing potential obstacles for financial goal setting. Recently, skills such as budget management and opening savings/checking account have been recognized as relevant for youths’ financial future, in particular for low-income racially minoritized families (Al-Bahrani et al., 2019; Daly and Kelly, 2015). Although no changes were found in the use of a checking and savings accounts among participants, these types of economic activities require having some money and a parent co-signer for those who are eighteen or younger, and therefore it was expected that these were the least likely to change.

The present results provide initial evidence for the utility of programming that integrates both job-readiness and financial knowledge (Hartog et al., 2016; Lusardi et al., 2010). Findings also point toward how such interventions increase the likelihood of youth to engage in a variety of behaviors that are related to positive long-term economic outcomes, such as having a strong résumé and being employed. Moreover, our results suggested pathways through which youth understood and implemented content knowledge (e.g. conceptualizing and prioritizing expenses, addressing potential obstacles for financial goal setting, résumé building, etc.; Garg and Singh, 2018), suggesting that youth are receptive to a well-thought-out and intentionally designed curriculum, which positively affects their employment and financial knowledge skillset, which in turn influences their future economic stability.

Within the context of developing countries, we recommend a similarly integrated approach with youth in low-income communities, including financial literacy and job readiness components (e.g. financial platforms, online job search, networking, and hiring platforms; Wheeler et al., 2019). Regarding under-developed countries, where youth and their parents often do not have access to ample financial services, it is especially important to develop interventions that not only invest in financial literacy, but also job readiness, as employment could provide income that may prove useful as a savings tool (see The Aflatoun Program; Amagir et al., 2018). Finally, similar research in under-developed countries has demonstrated the importance of including a social component to such interventions (Berry et al., 2015), including sessions focused on personal exploration, personal rights, and work conditions (e.g. to be aware of social or economic exploitation, requirements to perform work i.e. likely to be hazardous or to interfere with education).

Implications for policy and intervention

Although results of the present study are promising, adolescents from low-income households may require a multi-faceted approach to address the overarching goal of increasing their potential to escape the negative consequences of intergenerational poverty. Beyond individual economic behaviors, youth's lives are powerfully impacted by larger structural forces, such as institutional practices and, for many, a lack of economic opportunity in the underserved communities in which they live (Daly and Kelly, 2015; Seamster and Charron-Chénier, 2017). Youth in these environments may require direct access to social and economic opportunities for their new knowledge, confidence, and skills to flourish.

To address the need for access to knowledge, educators and youth-oriented organizations are well-positioned to develop interventions that deliver both job readiness and financial literacy skills and knowledge to youth from low-income households. In addition to the curricular components, programs should consider training staff on strategies for developing meaningful relationships with youth (Zeldin et al., 2014). Developing these relationships requires intentional efforts to build mutual trust (Christens and Peterson, 2012; Henderson et al., 2020; Zeldin et al., 2014). Ongoing supportive and guiding relationships have been linked to the development of key cognitive processes, such as information processing and self-regulation among youth from low-income households (Parra et al., 2002). Program staff may be well-positioned to reinforce curricular concepts by supporting youth in setting and pursuing employment goals while enrolled in financial literacy and job readiness curricula.

In addition to intentional relationship-building and skill-development efforts, adolescents from low-income households may benefit from additional investments in their “capital.” This investment may include broadening the social safety net, including cash payments under some circumstances and other transfers such as family allowances (National Academies of Sciences, Engineering, and Medicine (NASEM), 2019). Stability and predictability of income is an important contextual factor within antipoverty policy (Hill et al., 2017; National Academies of Sciences, Engineering, and Medicine (NASEM), 2019). Cash payments have been found to improve the lives of families (Hardy, 2017), can stabilize family budgets that may be depleted to an emergency (e.g. sudden illness), and may offer synergistic effects alongside curriculum targeting increases in knowledge, confidence, and behaviors related to getting a job and managing finances.

Intergenerational poverty is a multifaceted issue that may require both individual interventions as well as solutions that address structural inequities. Facilitating the financial success of adolescents from low-income households requires addressing the systemic and institutional challenges these youth face as well as building their economic capital via interventions that combine personal finance and job-readiness components (Fernandes et al., 2014). Recognizing the importance of taking active steps to lessen structural constraints impacting youth from low-income households may help attenuate adverse conditions in impoverished communities. The findings from this study show preliminary promise for government and community-led initiatives to also consider benefits of combined personal finance and work-readiness curricula like Road to Success.

Strengths and limitations

The present investigation has strengths in that it examined an underserved sample across two waves of data and involved both job-readiness and financial literacy content. However, limitations require consideration. First, although the diversity of our sample was a strength of the study, the results may require replication in other populations to generalize the findings beyond adolescents who come from predominantly low-income households. It is also important to note that our design for this project did not include a control group, precluding causal inferences. Second, our results should be considered within the constraints of the possibility of volunteer bias (Brownell et al., 2013). Third, readers may be cautious concerning findings on gender effects; the sample was primarily girls and low statistical power suggests that replicating these analyses in larger samples may be necessary. Finally, research may consider both experimental and extended longitudinal designs to test causal relations, focusing on which specific aspects of (or lessons within) curricula contribute to meaningful changes in knowledge or behavior, and examining the persistence of the effects the present study observed. This first-step evaluation, however, demonstrates that Road to Success, and similar programs that combine job readiness and financial literacy training for youth from low-income households may hold promise for utilization in more intensive (and costly) randomized-control trial designs.

Conclusion

The present study establishes an initial step in understanding how targeted interventions may function to address factors contributing to intergenerational poverty such as low usage of financial services and lack of professional skills and efficacy in the job market. Specifically, low-income youth who participated in the Road to Success program demonstrated positive increases in financial literacy, knowledge about job-searching, job-obtainment self-efficacy, and use of a résumé following completion of the curriculum. The present research suggests that such programs may benefit from being paired with community-level initiatives and policy changes to build the capital of impoverished families and encourage the positive changes youth form low-income households are trying to implement for themselves.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

Funding for this research was provided by the U.S. Department of Health and Human Services, Administration for Children and Families (Grant #90FM0076). Any opinions, findings, and conclusions or recommendations expressed in this poster are those of the authors and do not necessarily reflect the views of the U.S. Department of Health and Human Services, Administration for Children and Families.