Abstract

The global financial services industry stands at an inflection point where serving the world’s 1.4 billion unbanked adults has transformed from a development challenge into a commercial imperative. This case study analyzes 13 financial institutions that have achieved profitable inclusion, chosen for their strategic diversity and proven ability to generate revenue while serving populations traditionally deemed unviable. Through a systematic analysis of their strategic frameworks, from Capitec’s biometric revolution in South Africa to HesabPay’s blockchain innovation in Afghanistan, our case proposes a five-pillar architecture enabling sustainable profitability at scale. We define scale as the capacity to serve a large customer base, handle a high transaction volume, and achieve extensive geographic reach. These institutions demonstrate that by removing documentation barriers, building mobile-first distribution, integrating with local ecosystems, offering simplified products, and adopting a community-centric approach, they create competitive advantages that redefine banking success. The evidence strongly suggests that financial inclusion represents one of the sector’s largest untapped growth opportunities.

Keywords

Introduction

Maria lives in a South African township where her address is “third shack past the blue container.” For years, no bank would serve her because she could not produce a utility bill or lease agreement. Rashida operates in rural Bangladesh, where the nearest bank branch requires a full day’s journey through monsoon-flooded roads. Joseph farms in Papua New Guinea’s highlands, hundreds of kilometers from the nearest city, connected to the world only by a basic mobile phone. These three individuals represent 1.4 billion adults worldwide who remain locked out of the formal financial system (Demirgüç-Kunt et al., 2022).

These very different stories point to a common shift in emerging markets: financial services are being redesigned to reach excluded populations while remaining profitable. Until recently, the banking industry considered these customers unprofitable due to high transaction costs, regulatory complexity, and perceived risks (Baradaran, 2013; Birkenmaier and Janssen, 2021; Consumer Financial Protection Bureau, 2022; Mujeri, 2015; Welburn et al., 2024).

Traditional business models were built around urban professionals with formal addresses and complete documentation, leaving everyone else behind (Birkenmaier and Janssen, 2021). We argue that this assumption no longer holds. A new generation of financial institutions has discovered that serving the unbanked is not only socially valuable but also one of the most lucrative opportunities in global finance (Algorand Foundation, 2022; Bharathi et al., 2025). The key insight driving this revolution is counterintuitive. When banks eliminate traditional barriers and meet customers where they are, the resulting scale (in terms of customer volume, transaction volume, and geographic reach) generates extraordinary profits through high-volume, low-margin models.

Consider Capitec Bank’s transformation of South African banking. Starting in 2001 with the audacious goal of banking the previously unbankable, this digital-first institution now serves 22 million customers, making it the country’s largest retail bank by customer count (Capitec, 2024; Makhaya and Nhundu, 2016). In 2023 alone, Capitec generated $570 million in earnings while maintaining an industry-leading 37% cost-to-income ratio (Capitec, 2023). Their success did not stem from charity, but from eliminating address verification requirements through biometric identification, simplifying their entire product suite to a single account structure, and processing over 6 billion transactions annually (Capitec, 2025). This is volume economics operating at a scale previously unseen in retail banking.

The success stories span continents and contexts. As of March 31, 2025, Bandhan Bank had a strong customer base of 3.16 crore (31.6 million), with 34% of its 6,309 banking outlets located in rural areas, reflecting its continued focus on rural and unbanked populations (Bandhan Bank, 2025). Their field officers conduct weekly banking meetings under village trees, bringing full-service banking directly to customers’ doorsteps (Nayak, 2017). In Kenya, by 2022, Kenya Commercial Bank (KCB) Bank processed 99% of its transactions outside traditional branches and disbursed loans worth approximately USD 1.3 billion through its mobile platform integrated with M-Pesa (Giorgioni, 2023). In Afghanistan, HesabPay operates in all 34 provinces and serves around 400,000 users through blockchain-based digital wallets that deliver humanitarian aid while ensuring compliance with international anti-money laundering (AML) and counter-terrorism financing (CTF) regulations (Bharathi et al., 2025).

These institutions succeed because they have fundamentally reimagined banking. Instead of forcing customers to adapt to banking systems, they adapted their systems to customer realities. Legacy banking models presuppose formal addresses, stable employment, and pre-existing financial relationships, criteria that exclude vast segments of the population. Successful inclusion-focused banks recognize that these prerequisites exclude their largest potential market.

The technological revolution enabling this transformation cannot be overstated. Artificial intelligence (AI), biometric verification, mobile connectivity, and digital identity systems have fundamentally altered the economics of serving dispersed, low-income populations. Bank Jago in Indonesia achieves 99% identity verification accuracy through AI-powered systems (Advanced AI, 2020). CIMB Bank in the Philippines reduced customer onboarding from 15 minutes to under 10 minutes, enabling them to acquire 2 million customers in their first year (Jumio, 2020). Kasikornbank in Thailand deployed over 1,300 biometric kiosks processing 2–3 million identity verifications annually, available 24/7 in locations where traditional branches would be economically unviable (Asian Banking and Finance, 2020; The Digital Banker, 2023).

However, technology alone cannot account for these outcomes. We argue that the most effective financial inclusion strategies combine sophisticated digital capabilities with a deep understanding of local communities, regulatory environments, and customer behaviors. The institutions in our case recognize that serving the unbanked requires not just different products but fundamentally different operating models that prioritize accessibility, transparency, and trust-building over traditional metrics like profit per customer.

The evidence presented here substantiates a compelling business case for profitable inclusion. These institutions consistently demonstrate that financial inclusion and profitability are not just compatible, they are also synergistic. Bandhan’s consistent profits serving primarily rural customers, KCB’s 16% market share in Kenya’s competitive banking sector (Kwama, 2025), and Capitec’s 25% return on equity all prove that accessing previously untapped markets creates significant opportunities rather than charitable obligations (Standard and Poor’s Rating Services, 2015).

The strategic implications extend far beyond individual success stories. As these innovative banks demonstrate sustainable profitability while serving previously excluded populations, they are attracting significant attention from investors, regulators, and development organizations worldwide (Bandhan Bank, 2025; Bharathi et al., 2025; Kantabutra and Aphiraks, 2016; Makhaya and Nhundu, 2016). Their success challenges fundamental assumptions about market segmentation, risk assessment, and the relationship between social impact and commercial viability.

This transformation is not merely incremental. It is a fundamental reimagining of banking itself. By eliminating traditional barriers, leveraging mobile-first technologies, building extensive agent networks, and developing community-centric service models, these institutions have proven that the world’s underserved populations represent not a burden to be managed but an opportunity to be captured.

The question is no longer one of feasibility, but of urgency, how quickly incumbents can adapt before more agile competitors dominate. Our case is straightforward: through detailed analysis of thirteen institutions across Africa, Asia, and the Pacific, we demonstrate that financial inclusion at scale is not just achievable, it is profitable when executed with the right strategic framework, technological infrastructure, and community-centric approach.

Case overview

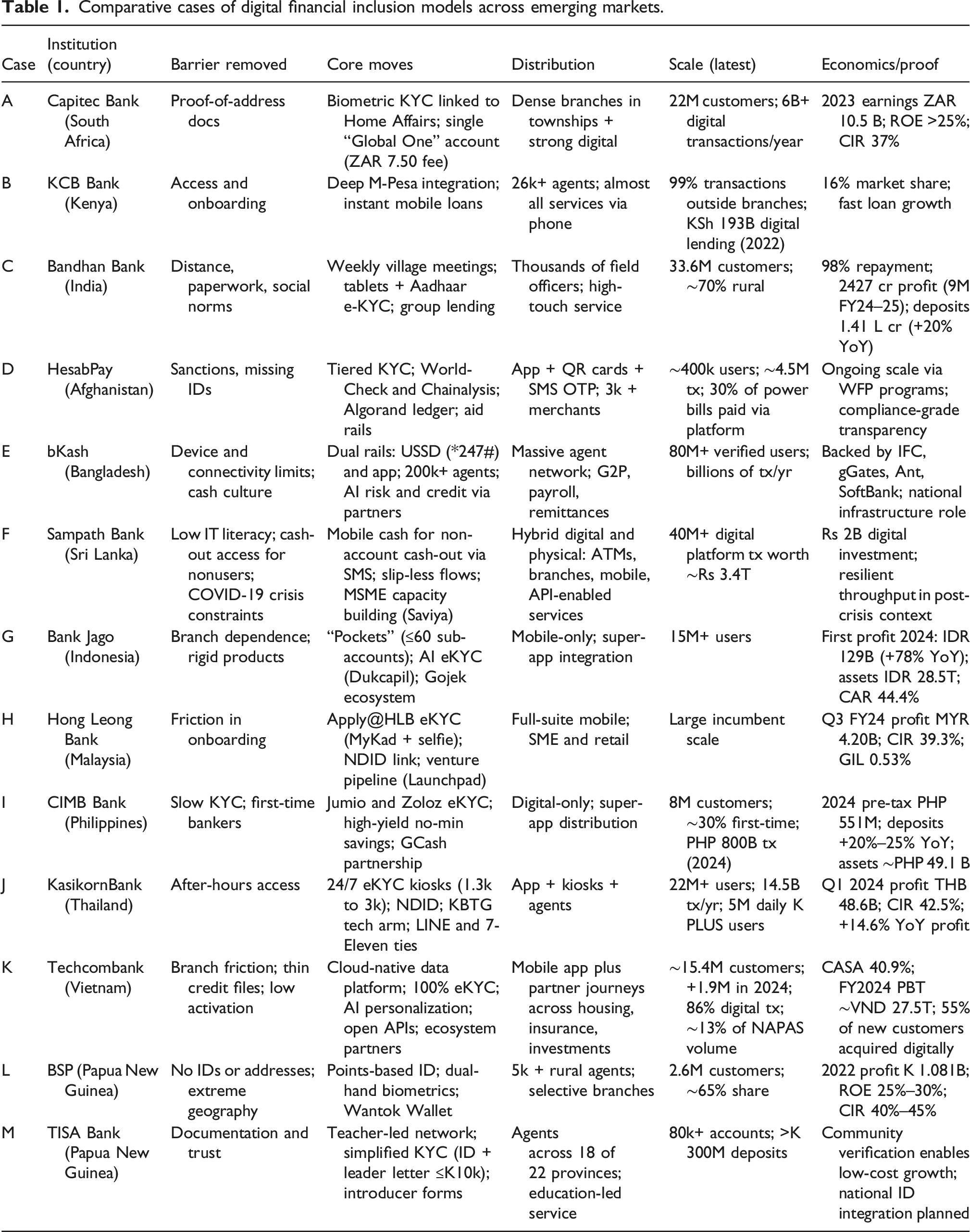

The 13 institutions were chosen for strategic diversity, not similarity. Each tackles a different inclusion challenge across underserved markets. From Capitec’s township model to Bank South Pacific (BSP)’s island logistics, they trace multiple routes to profitable inclusion, from mature markets like South Africa and Thailand, where inclusion means convenience and lower cost, to frontier settings like Afghanistan and Papua New Guinea, where it means basic participation. Geographically they span Africa to Asia and very different regulatory environments, including Malaysia’s advanced digital frameworks, PNG’s sparse infrastructure, Vietnam’s sandbox, and Sri Lanka’s post-COVID-19-crisis pragmatism. This demonstrates that adaptable strategic principles can be successfully applied across diverse regulatory and geographic contexts. Collectively they cover the full business-model spectrum: digital-only challengers (e.g., Bank Jago and CIMB Philippines), incumbents reinventing themselves (e.g., Hong Leong, KasikornBank, and Techcombank), microfinance upscalers (e.g., Bandhan), COVID-19-crisis-responsive hybrids (e.g., Sampath), fintech-and-aid platforms in extreme conditions (e.g., HesabPay), ecosystem plays (e.g., bKash), and community-rooted banks (e.g., Teacher Saving and Loan Society/TISA). Together they serve more than 250 million customers and process trillions in transactions, indicating that profitable inclusion is repeatable across contexts. The additions of Sampath Bank and Techcombank complete the map by pairing crisis-driven pragmatism with data-driven, ecosystem-led scale.

Case A: Capitec bank (South Africa)

South Africa’s banking system long excluded millions in informal settlements who could not provide traditional proof of address (Chitimira and Ncube, 2020). Capitec Bank, launched in 2001, saw an opportunity in this exclusion. Their breakthrough was eliminating the requirement entirely by integrating biometric identification with the Department of Home Affairs. Customers provided a national ID and fingerprints at onboarding, creating a unique biometric signature that both removed documentation barriers and reduced fraud risk (Makhaya and Nhundu, 2016).

Capitec also reimagined products with radical standardization and simplicity. They collapsed multiple account types into a single Global One Account, which functions as both savings and checking with a transparent monthly fee of just ZAR 7.50, or roughly $0.40. No minimum balances, no hidden charges, just banking anyone could understand (Makhaya and Nhundu, 2016; Umar, 2022). This approach, while simple for the customer, was a strategic move to standardize operations and minimize complexity. It allowed the bank to achieve profitability through high-volume, low-margin transactions rather than fee extraction. Such a model is viable only when unit costs are kept low and operational complexity is minimized. Capitec’s success, in part, rests on a business model built for efficiency and automation, which enabled it to serve millions of customers profitably (Capitec, 2025).

The outcomes were commercially significant and strategically transformative. By 2024, Capitec had more than 20 million customers, making it South Africa’s largest retail bank by customer count (Capitec, 2024). Despite serving primarily low-income households, the bank generated ZAR 10.5 billion ($570m) in headline earnings in 2023/24, with a cost-to-income ratio of 37% and return on equity of 26% (Capitec, 2024, 2025). With annual transaction volumes surpassing 6 billion, it proved that simplicity, trust, and scale can transform exclusion into sustainable growth (Capitec, 2025).

Case B: KCB Bank (Kenya)

Kenya’s financial revolution began with M-Pesa in 2007, building digital infrastructure that redefined how Kenyans interacted with money (Islam et al., 2025). KCB Bank recognized early that competing with M-Pesa would be futile; instead, they partnered with Safaricom to create KCB M-Pesa, allowing instant account opening and microloans through mobile phones without branch visits (Giorgioni, 2023; Onyango and Maina, 2024). KCB added a crucial layer of formal banking services to M-Pesa’s existing platform, including formal savings accounts, overdrafts, and larger loans that a pure mobile money service could not provide. M-Pesa’s strategic incentive was to expand its ecosystem and provide greater financial depth to its users, thereby increasing its own transaction volume and entrenching its platform as a financial hub. This was not about digitizing old services but reimagining banking for a mobile-first economy (Safaricom, 2023).

The strategic insight was deceptively simple: embedding services within existing behaviors accelerates adoption. By embedding within M-Pesa’s ecosystem, KCB gained immediate access to millions already using digital finance (Safaricom, 2023). They expanded their reach through KCB Mtaani, equipping local shops with point-of-sale terminals to act as banking agents. By 2023, over 26,000 agents formed one of Africa’s largest alternative banking networks (KCB Group ESG & Sustainability, 2023; Kibet, 2016). The results were transformative. By 2023, 99% of KCB’s transactions occurred outside branches, predominantly via mobile and agents. Digital credit flows surged, with KSh 193 billion disbursed in 2022, that is, 22.5% growth year-on-year (KCB Group ESG & Sustainability, 2023). This scale enabled KCB to capture 16% of Kenya’s banking market while serving rural populations that traditional banking models could not reach (Kwama, 2025). KCB’s trajectory demonstrates how ecosystem partnerships and data-driven credit models can extend financial access at a national scale.

Case C: Bandhan Bank (India)

In rural eastern India, where the nearest bank branch could be a day’s journey away, Bandhan Bank transformed access by taking banking to customers rather than expecting them to travel to branches (Mishra et al., 2015; R. Tiwari and Anjum, 2015). Evolving from a microfinance NGO into a commercial bank, Bandhan redefined financial inclusion through community engagement. Recognizing that rural women faced barriers beyond distance, such as cultural restrictions and intimidating branch environments, Bandhan deployed thousands of field officers who conducted weekly meetings in villages (Jagtap, 2017; Mandal, 2024).

Equipped with tablets and biometric tools, these officers turned villages into mobile banking points. Customers could deposit, withdraw, and apply for loans without visiting a branch. Leveraging India’s Aadhaar biometric ID system solved documentation hurdles by replacing utility bills and proof-of-address requirements with Aadhaar-enabled verification (Rao and Nair, 2019; P. R. Tiwari et al., 2022). By 2023, 91% of savings accounts were opened digitally through Aadhaar-enabled eKYC and video KYC, streamlining onboarding while ensuring compliance. By March 2024, Bandhan’s customer base had grown to 33.6 million, with nearly 70% in rural and semi-urban areas underserved by traditional banks (Bandhan Bank, 2024, 2025). Despite serving primarily low-income clients, repayment rates held at 98% even during COVID-19 disruptions. This strong asset quality supported consistent profitability, with ₹2,427 crore earned in the first 9 months of FY24–25. This success is rooted in the bank’s ability to reinforce technology with human relationships, as the high repayment rates are likely due to the trust and social collateral built through its group lending model and the close relationships its field officers cultivate with local communities (Bandhan Bank, 2024, 2025).

Case D: HesabPay (Afghanistan)

HesabPay operates in one of the world’s most challenging financial environments, delivering digital wallet and payment services across all 34 provinces of Afghanistan despite sanctions, political instability, and limited banking infrastructure (Bharathi et al., 2025). Founded in 2016 by an Afghan entrepreneur, it was the country’s first online payment application, designed to facilitate trade, daily transactions, and technology adoption among the unbanked majority. 1 This mobile-first fintech illustrates how blockchain and adaptive compliance can expand financial access in conflict-affected regions.

A tiered KYC framework balances inclusion with risk management, allowing even displaced users with limited documentation to open accounts. The lowest tier of KYC allows a user with no official identification to open an account with a simple selfie and a declaration of their identity, sufficient for small-value transfers. Higher tiers are unlocked as users build a transactional history on the platform. The platform uses the Algorand blockchain to provide immutable records, near-instant, low-cost settlement for millions of transactions, and support auditing in liquidity-constrained environments. It also incorporates integrated compliance tools, such as Refinitiv’s World-Check for sanctions screening and Chainalysis for blockchain monitoring, to ensure transparent oversight. The costs for these crucial tools are borne by the platform itself, demonstrating a commitment to creating a sustainable and transparent infrastructure in a high-risk environment.

HesabPay’s role has expanded to humanitarian infrastructure in partnership with the World Food Programme (WFP). It delivers digital cash assistance to over 182,000 beneficiaries via cashless transfers that preserve dignity, reduce security risks, and stimulate local economies. This humanitarian mission is central to HesabPay’s business model and a significant driver of its scale and adoption. The platform’s profitability is both a byproduct of its aid distribution role and a separate business line. Users can open accounts in 15 minutes at local branches, redeem assistance as digital Afghani through QR code cards or at merchants, and pay over 30% of electricity bills nationwide using the platform. This multi-channel approach, which includes an app for smartphones and USSD codes for feature phones, ensures inclusion across all technology levels. Currently, HesabPay serves roughly 400,000 users, processes 4.5 million transactions, and connects with more than 3,000 merchants.

Case E: bKash (Bangladesh)

bKash has evolved from offering basic money transfers in 2011 to becoming Bangladesh’s dominant financial ecosystem, serving over 80 million verified users (Islam et al., 2025; Nandhakumar, 2023). Operating under Bangladesh Bank’s oversight, it redefined inclusion by leveraging mobile technology to reach populations long excluded from formal banking (Mahmud, 2024; Pesek, 2020). While the mobile network infrastructure was an existing foundation, bKash strategically built its own comprehensive financial infrastructure from scratch (Yesmin et al., 2019).

Its dual-platform model reflects a sophisticated grasp of Bangladesh’s diverse infrastructure. The USSD-based service (*247#) enables full transactions through feature phones without internet, ensuring access for rural customers (Islam et al., 2025; Mahmud, 2024). In parallel, the smartphone app delivers advanced features for digitally connected users. The 200,000+ agent network proved central, bridging digital and physical systems while acting as financial educators and trust builders for first-time users (Nandhakumar, 2023; Yesmin et al., 2019). This large, high-touch agent network serves as a key competitive advantage that creates a significant barrier to entry for agile, digital-only competitors. The network’s role as a trusted point of contact and educator is difficult for new market entrants to replicate, making it an indispensable part of bKash’s business model.

Strategic partnerships accelerated growth. IFC investment in 2013 and Gates Foundation funding in 2014 provided credibility. The 2018 Ant Financial alliance introduced AI-driven credit scoring, while SoftBank’s $250 million injection in 2021 made bKash Bangladesh’s first unicorn (Xiao, 2018). The platform’s impact extends beyond transactions to social transformation. Women’s financial inclusion rose sharply, with 43% now holding accounts. During COVID-19, digital salary mandates validated its strategic role, rapidly expanding access among women in formal employment (Finighan, 2025).

Case F: Sampath bank (Sri Lanka)

Sri Lanka’s financial inclusion faced two major constraints: relatively low IT literacy (35%–36%) and uneven financial literacy (57.9%) amidst the lingering economic crisis after 2022 (Aruna et al., 2023; Central Bank of Sri Lanka & International Finance Corporation, 2019; Maragaoda, 2020). Sampath Bank recognized that a purely digital push would leave millions behind. Instead, it pioneered hybrid digital-physical solutions that met customers where they were, both technologically and geographically. The breakthrough was Mobile Cash, which allowed account holders to send up to Rs. 200,000 per day to non-account holders. Recipients received an SMS and could withdraw cash instantly from any ATM or branch, 24/7. By leveraging basic mobile phones and existing infrastructure, Sampath removed digital literacy as a barrier while extending banking access far beyond traditional channels.

Their “Credit-Plus” philosophy further distinguished the bank. Through the Sampath Saviya program, MSME loans were paired with training in business management, marketing, and financial literacy, delivered with the National Enterprise Development Authority. This blended model addressed limitations in existing financial practices and reduced information asymmetry that had long made MSMEs too risky for conventional lending. Sampath was already advancing technology-enabled services, but COVID-19 accelerated their rollout as customers turned to digital channels. The economic crisis created wider challenges but did not slow the bank’s progress. At the same time, the central bank introduced stricter requirements including qualified leadership, regular audits, stronger cybersecurity, and improved reporting. These policies raised governance standards across all financial institutions and reinforced sector-wide resilience (Aruna et al., 2023; Dewasiri et al., 2024; Maragaoda, 2020).

Sampath itself has been at the forefront of technology-enabled services for more than a decade, introducing Sampath Vishwa in 2008, Saviya in 2013, and WePay in 2021/2022. By 2024, it had invested Rs. 2 billion in digital infrastructure, processing more than 40 million transactions worth Rs. 3.4 trillion through Vishwa and WePay (Sampath Bank, 2024). With a standardized API platform transforming corporate banking and AI-powered lending through Sampath Select, the bank showed how innovation can thrive within constraints. Sampath’s model demonstrates that in digitally immature markets, relevance matters more than sophistication, whereby hybrid solutions bridging the digital and physical worlds can achieve meaningful, sustainable inclusion (Dewasiri et al., 2024).

Case G: Bank Jago (Indonesia)

Bank Jago represents Indonesia’s bold digital-first banking experiment, operating entirely without physical branches while serving over 15 million users through innovative mobile-only services (RetailBanker International, 2021). Founded within the Gojek ecosystem, Bank Jago exemplifies how fintech integration can accelerate inclusion in Southeast Asia’s largest economy. The core innovation lies in the “Pockets” system, allowing customers to create up to 60 sub-accounts within a single master account (Guild, 2025). 2 Each pocket serves different purposes: salary deposits, savings goals, bill payments, or shared family accounts. This architecture mirrors how Indonesians manage money, moving from artificial simplicity to flexible systems accommodating real financial behavior.

Bank Jago’s eKYC solution, powered by ADVANCE.AI, achieves 99% verification accuracy through sophisticated AI algorithms combining optical character recognition, liveness detection, and facial recognition (Advanced AI, 2020). The system verifies customers against Indonesia’s Dukcapil database in real-time, reducing onboarding to under 5 minutes while maintaining strict Bank Indonesia compliance. Gojek ecosystem integration creates powerful network effects. GoPay users seamlessly transition to full banking services, while Bank Jago customers access the broader Gojek merchant network. This symbiotic relationship accelerates customer acquisition while reducing marketing costs.

Financial performance demonstrates digital-first viability. Bank Jago reported first profit of IDR 129 billion in 2024, representing 78% year-over-year growth. Total assets reached IDR 28.54 trillion, with deposits growing to IDR 18.8 trillion and loans expanding to IDR 17.7 trillion (Bank Jago, 2024). Bank Jago’s success illuminates critical insights: ecosystem integration provides distribution advantages, flexible product architecture drives adoption more effectively than rigid structures, and AI-powered verification achieves both inclusion and compliance when properly integrated with national identity infrastructure.

Case H: Hong Leong bank (Malaysia)

As the first Malaysian bank to offer fully digital account opening via eKYC in October 2020, Hong Leong bridged conventional banking excellence with innovative digital inclusion (Yin, 2020). The Apply@HLB platform transformed customer onboarding by enabling accounts to be opened entirely through mobile devices using only MyKad scanning and selfie verification (Digital News Asia, 2020). This required close collaboration with Bank Negara Malaysia to create regulatory frameworks that balanced inclusion goals with anti-money laundering safeguards. Hong Leong’s eKYC employs advanced biometric technology that matches live selfies with MyKad records, achieving high accuracy and reducing fraud risk (Digital News Asia, 2020; Yin, 2020). Integration with Malaysia’s National Digital ID platform enhances cross-bank verification, reinforcing security and efficiency within the digital ecosystem. The bank’s ambitions extend beyond digitizing existing services: the HLB Connect platform offers comprehensive digital banking, while the HLB Launchpad invests in fintech startups, ensuring innovation feeds directly back into operations.

Financial results confirm the effectiveness of this strategy. According to Hong Leong Bank’s FY2024 Annual Report, the bank recorded a net profit after tax of RM4.196 billion and total assets of RM297.8 billion, maintaining a net interest margin of 2.05%, a cost-to-income ratio of 39.3%, and an industry-leading gross impaired loan ratio of 0.53% (Hong Leong Bank, 2024). The 2025 alliance with WeBank Technology Services introduces advanced AI for analytics and fraud prevention, enabling Hong Leong to compete with digital challengers while preserving the trust and stability of an established brand (PR Newswire, 2025). Together, these moves illustrate how regulatory collaboration creates first-mover advantages, while long-term digital transformation demands balancing innovation with operational excellence.

Case I: CIMB Bank (Philippines)

Operating without physical branches, CIMB leveraged AI-powered technology and strategic partnerships to reach 8 million customers by 2024, with 30% being first-time bankers never holding formal accounts (Chong, 2025; CIMB Bank, 2024a). The entry strategy recognized that the Philippines’ large unbanked population represented opportunity and challenge (Banco Sentral ng Pilipinas, 2021). With significant overseas worker remittances, growing e-commerce adoption, and increasing smartphone penetration, markets were ready for digital innovation. However, regulatory requirements, documentation challenges, and limited financial literacy required sophisticated solutions balancing inclusion with compliance.

CIMB’s partnership with Jumio for AI-powered eKYC proved transformational. The system verifies identities by matching live selfies with government-issued IDs, reducing onboarding from 15 minutes to under 5 minutes with automated verification (Hamilton, 2020). This dramatic improvement enabled rapid scaling while maintaining Bangko Sentral ng Pilipinas compliance. Collaboration with Zoloz enhanced eKYC capabilities further, bringing advanced liveness detection and anti-spoofing technologies preventing fraud while ensuring legitimate customer access. The technology stack processes multiple Philippine government identification forms, accommodating customers regardless of documents possessed (Businesswire, 2020).

Strategic GCash integration created powerful network effects accelerating customer acquisition. This partnership enabled CIMB to reach GCash’s massive user base while providing banking depth pure payment platforms cannot offer. Financial performance demonstrates digital-first inclusion viability. CIMB Philippines achieved estimated pre-tax profit of PHP 551 million in 2024, dramatically improving from 2023 break-even. Total assets reached approximately PHP 49.13 billion, with deposits growing 20%–25% year-over-year (CIMB Bank, 2024b). CIMB’s rapid customer acquisition validates digital-first approaches in emerging markets with large unbanked populations (Chong, 2025; CIMB Bank, 2024a, 2024b).

Case J: KasikornBank (Thailand)

Through innovation subsidiary Kasikorn Business-Technology Group (KBTG), the KasikornBank pioneered facial recognition eKYC systems and multi-channel digital banking serving over 22 million users through K PLUS platform (Banking Frontiers, 2023; KBTG, 2024). The approach focuses on convenience and accessibility rather than serving completely unbanked populations. Thailand’s relatively developed banking infrastructure means KasikornBank’s innovation targets customers seeking better service experiences and 24/7 access rather than first-time banking relationships (Kasikornbank, 2025). KasikornBank has introduced 24/7 e-KYC services through Boonterm kiosks, now available at more than 1,300 locations with plans to expand to 3,000. These kiosks are integrated with Thailand’s National Digital ID (NDID) platform, enabling cross-bank identity verification and supporting more secure and efficient digital ecosystems. The growing adoption of the service reflects strong demand for convenient, self-service identity verification options (Kasikornbank, 2024).

KBTG’s role as internal innovation engine demonstrates how traditional banks maintain technological competitiveness against fintech challengers (KBTG, 2024). Kasikornbank’s KBTG subsidiary advances AI, blockchain, and fintech partnerships while staying integrated with core operations. In Q1 2024, the bank posted a net profit of THB 48.6 billion, total assets of THB 4.33 trillion, a cost-to-income ratio of 42.5%, and 14.6% profit growth. The success of K PLUS demonstrates the scalability of digital banking in smartphone-driven markets (Kasikornbank, 2024).

Case K: Techcombank (Vietnam)

Operating in a market with 80%+ smartphone penetration and government support for cashless transformation through the State Bank of Vietnam’s innovation-friendly regulatory sandbox, Techcombank pursued an ecosystem-centric strategy that embeds banking services into customers’ daily lives through open APIs and strategic partnerships (Cao and Nguyen, 2023). Their integration with Techcom Securities, TCLife insurance, and Masterise Homes creates a holistic digital lifestyle where the bank becomes indispensable rather than transactional (Minh et al., 2025). The strategy focuses on “customer activation” rather than mere acquisition, using AI-powered hyper-personalization to drive engagement exceeding 50 logins per active user monthly. This unified data platform enables precise customer segmentation and behavioral insights that create positive feedback loops whereby more engagement generates better data, leading to superior personalization that further increases engagement (Kien, 2025; Nguyen et al., 2025).

Alternative data credit scoring enables access for populations lacking formal credit histories, while remote account opening eliminates branch dependency entirely. Strategic partnerships with Vingroup and other ecosystem players create seamless customer journeys from real estate purchases to investment management, transforming the bank from service provider to lifestyle enabler (Lainez and Gardner, 2023; Yen, 2025). By 2024, 86% of Techcombank’s transactions were digital, accounting for 13% of Vietnam’s market volume via NAPAS. An industry-leading CASA ratio of 40.9% and 1.9 million new customers highlight how ecosystem-driven digital strategies deliver both low-cost funding and strong customer growth, positioning Techcombank as a lifestyle platform in a digitally ready market (Techcombank, 2024).

Case L: Bank South Pacific (Papua New Guinea)

Papua New Guinea illustrates one of the toughest financial inclusion frontiers: 87.5% of its people live in rural areas spread across 600+ islands, with limited transport, weak digital connectivity, and over 800 languages. In this fragmented environment, Bank South Pacific (BSP) demonstrated that banking could be both inclusive and profitable, becoming the country’s dominant financial institution (Asian Development Bank, 2015; Santosdiaz, 2024). The main obstacle was identification. With 80% of the population lacking formal IDs and no consistent addressing system, standard KYC was unworkable. BSP first introduced a points-based identification framework, assigning values to different documents, but the true breakthrough came with biometrics. Using Fulcrum technology, BSP recorded fingerprints from both hands to create unique profiles linked to accounts. These biometric signatures replaced conventional documents, enabling secure banking access for people previously excluded (Eves and Titus, 2017; International Finance Corporation, 2019).

Reaching customers across Papua New Guinea’s remote islands posed a significant challenge. Building traditional branches was costly, while relying solely on digital banking was impractical given infrastructure constraints. BSP adopted a hybrid model: limited branch expansion supported by mobile services and an extensive rural agent network. By 2024, the bank had over 5,000 agents who processed more than 38 million transactions worth PGK 11 billion, extending banking access into communities that had never previously been served. The results show that complexity does not rule out profitability. BSP served 2.6 million customers, achieved record profits of K1.081 billion, and secured a dominant 65% market share. BSP’s model demonstrates that with innovation and distribution creativity, banks can thrive even in the world’s hardest-to-reach markets (BSP, 2024).

Case M: Teachers Savings and Loan Society (TISA) Bank (Papua New Guinea)

TISA Bank’s transformation from the Teachers Savings and Loan Society into a licensed commercial bank highlights how community-rooted institutions can scale while retaining their social mission. Operating across 18 of Papua New Guinea’s 22 provinces, TISA leverages its deep ties to the education system, where more than 80,000 teachers act as trusted ambassadors (PNG Business News, 2024; Timothy, 2024). In remote and fragmented communities, teachers hold high social standing, enabling them to naturally serve as financial advisors and service advocates. This network gives TISA a distribution and credibility advantage that larger commercial banks struggle to replicate.

Comparative cases of digital financial inclusion models across emerging markets.

Financial inclusion: A transformation, not a digitization

The institutions in this study have not simply digitized traditional banking models; they have fundamentally re-imagined them to serve populations that have long been excluded. This transformation is driven by several shared strategic approaches that consistently overcome the most common barriers to financial access in emerging markets.

Breaking down documentation barriers

A primary obstacle for millions worldwide is the lack of formal documentation, such as utility bills or fixed addresses. Successful banks have turned this barrier into a competitive advantage by pioneering innovative identity verification solutions. In South Africa, Capitec Bank eliminated the need for address verification by integrating its biometric system with a government utility, the Department of Home Affairs. This approach streamlined onboarding while maintaining security (Makhaya and Nhundu, 2016).

Similarly, Bandhan Bank in India leveraged the government-provided Aadhaar biometric ID system, enabling digital verification that removed address proof requirements that rural populations could not provide (Mishra et al., 2015; R. Tiwari and Anjum, 2015). Even in the challenging environment of Afghanistan, HesabPay demonstrated an adaptive tiered KYC framework that allows users with limited documentation to access basic services with a simple selfie and ID scan (Bharathi et al., 2025). These strategies show that a successful path to inclusion often requires a flexible approach to identity that works within the realities of customers’ lives.

Building a hybrid digital and physical foundation

Technology alone is not a sufficient solution for financial inclusion, as it often assumes a level of digital and financial literacy that may not exist. The most effective models bridge digital innovation with physical accessibility. In Kenya, KCB Bank recognized that competing with the mobile money platform M-Pesa was “futile.” Instead, it integrated with the platform, leveraging its vast network and user base to offer formal banking services, such as accounts and loans, that M-Pesa did not provide (Giorgioni, 2023; Onyango and Maina, 2024). This approach worked by building on existing user behavior rather than forcing new habits (KCB Group ESG & Sustainability, 2023). Similarly, Bangladesh’s bKash built a comprehensive financial ecosystem from the ground up, with a dual platform that serves both smartphone users and those with basic feature phones via USSD codes (Islam et al., 2025; Mahmud, 2024). The success of both KCB and bKash was critically dependent on their extensive agent networks, which turned local businesses into a form of physical infrastructure for last-mile reach, extending access to remote areas where traditional branches are unviable.

Cultivating community trust and financial education

Sustainable inclusion is ultimately about building trust and embeddedness within local communities. Bandhan Bank’s high-touch doorstep model, which deploys field officers to conduct weekly meetings in villages, is a prime example of this (Jagtap, 2017; Mandal, 2024). This human-centric approach has not only brought banking to customers but has also established a relationship of trust that has contributed to exceptional repayment rates, even during economic disruptions. This is a reminder that trusted relationships can create superior financial discipline compared to purely transactional banking (Bandhan Bank, 2024).

In Sri Lanka, Sampath Bank’s “Credit-Plus” philosophy combined MSME loans with financial literacy and business management training, addressing the root causes of exclusion by empowering clients to use financial services productively (Sampath Bank, 2024). HesabPay’s partnership with the World Food Programme further demonstrates this, as it made the platform an essential part of the community’s daily life by handling humanitarian aid distribution and utility payments (Bharathi et al., 2025; Lalzoy, 2021). These examples prove that financial services become sustainable when they are integrated into a community’s essential functions, not just offered as an isolated service.

The transformation impact

These institutions demonstrate that financial inclusion and profitability are synergistic rather than competing objectives. Their exceptional financial performance while serving primarily excluded populations proves that accessing underserved markets creates significant business opportunities rather than charitable obligations (Bandhan Bank, 2025; Capitec, 2025; Kwama, 2025; Techcombank, 2024). The success formula emerges clearly: innovative identity verification removes documentation barriers, mobile-first approaches leverage familiar platforms, extensive agent networks solve distribution challenges, and community-centric models build essential trust. Most importantly, these institutions reimagined financial services entirely around previously excluded populations’ needs rather than digitizing existing banking. Whether through Sampath’s crisis-responsive pragmatism or Techcombank’s ecosystem dominance, sustainable inclusion demands fundamental transformation rather than incremental adaptation. The implications extend beyond individual institutional success. These models demonstrate that emerging market banks can achieve superior performance by serving excluded populations, suggesting that traditional banking’s focus on affluent segments may be strategically misguided. When structural barriers are dismantled through innovative approaches, previously “unprofitable” populations become the foundation for exceptional growth and returns.

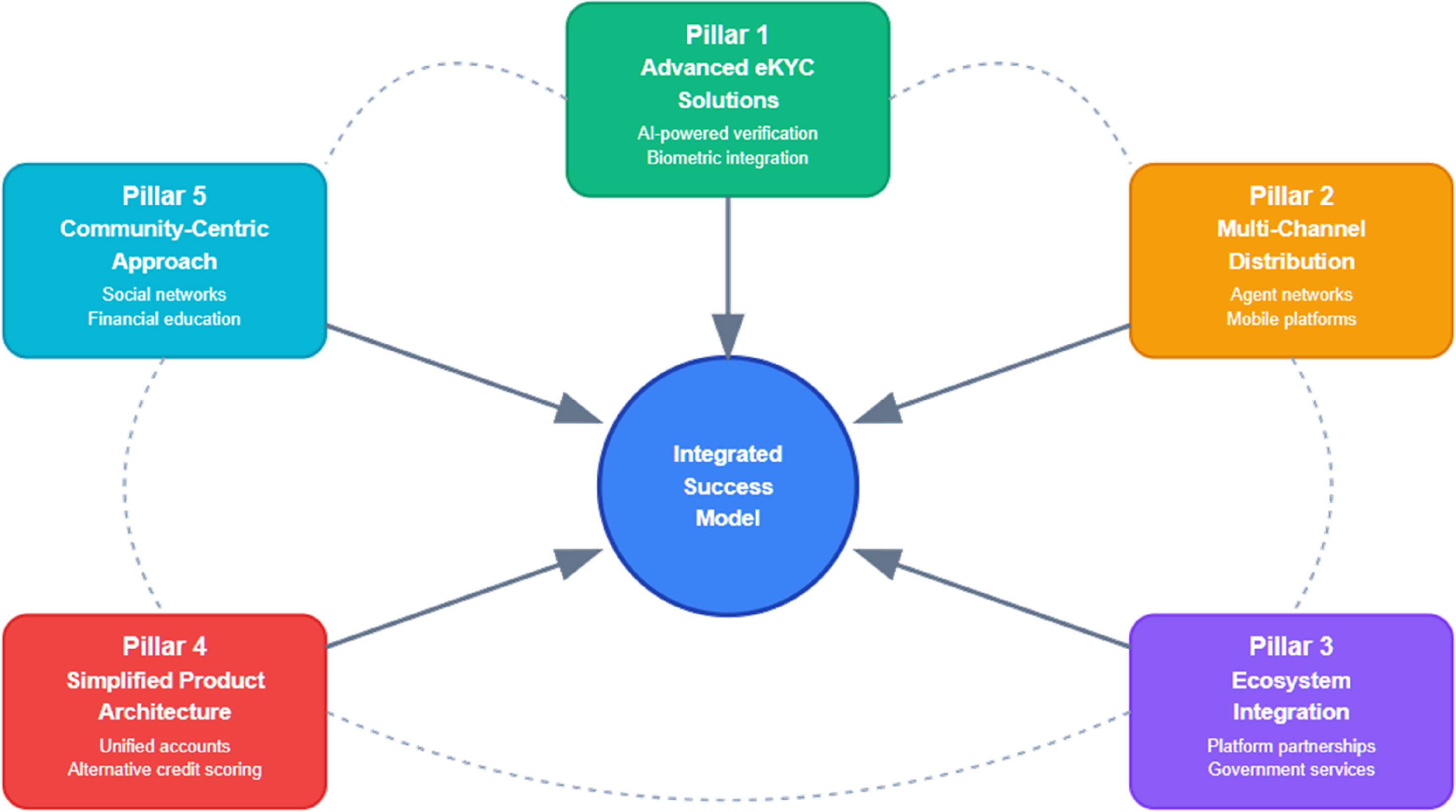

Strategic framework: Five pillars of success

Across emerging and developed economies alike, financial institutions face the persistent challenge of extending services to excluded populations while maintaining commercial viability. Evidence from multiple markets suggests that success is not derived from isolated innovations but from an integrated system of practices. This system rests on five interconnected pillars: advanced eKYC, multi-channel distribution, ecosystem integration, simplified product architecture, and community-centric engagement. Together, these pillars form a strategic framework that enables banks to convert exclusion into inclusion, and inclusion into profitability (see Figure 1). Five pillars of digital financial inclusion success.

Pillar 1: Advanced eKYC solutions

The first pillar, advanced eKYC solutions, redefines customer identification from a barrier into a gateway. These solutions often depend on a crucial precondition: the availability of an existing national digital ID system, which is a key enabler for success in many emerging markets. Institutions like Capitec in South Africa, Bandhan in India, and Bank Jago in Indonesia all capitalized on government-provided KYC utilities to streamline onboarding. This approach leverages AI-driven tools such as optical character recognition, liveness detection, and facial recognition to verify identities with greater accuracy and speed than manual processes. This reduces fraud risk while allowing legitimate customers to onboard quickly. For contexts where a national digital ID is not available, such as in Papua New Guinea, banks must create their own systems, such as BSP’s points-based framework and biometric signatures, to overcome the lack of formal documents.

Pillar 2: Multi-channel distribution

Yet verification alone cannot ensure inclusion. The second pillar, multi-channel distribution, addresses the core challenge of reach. In fragmented geographies and low-infrastructure environments, traditional branch networks are neither affordable nor scalable. Instead, agent banking transforms local shops, teachers, and small businesses into access points, creating grassroots infrastructure that doubles as employment generation (KCB Group ESG & Sustainability, 2023; Nandhakumar, 2023). In Papua New Guinea, for example, BSP demonstrates how agent models can succeed where branches cannot, providing millions with first-time access to banking (BSP, 2024). Parallel to agents, mobile-first platforms allow services through both smartphones and basic feature phones, ensuring continuity across diverse digital landscapes (Islam et al., 2025; Mahmud, 2024). Hybrid infrastructure such as kiosks equipped with facial recognition offers another bridge, reducing costs while extending services to semi-urban and peri-urban populations that fall between branch coverage and digital reach (Kasikornbank, 2024).

Pillar 3: Ecosystem integration

The third pillar, ecosystem integration, recognizes that banking does not exist in isolation but within broader social and economic systems. Successful institutions build on existing user habits rather than forcing new behaviors. The success of these integrations is primarily due to embedding banking services directly into platforms already familiar to users, which reduces acquisition costs and accelerates adoption (KCB Group ESG & Sustainability, 2023). Beyond convenience, ecosystem integration generates network effects, where banking becomes embedded into daily life through APIs that connect payments, remittances, retail, and transport (Kien, 2025; Minh et al., 2025). Government partnerships strengthen this logic by tying banking to policy objectives such as cash transfer distribution or aid delivery, ensuring scale while meeting national development goals (Finighan, 2025; Lalzoy, 2021). By anchoring themselves in existing platforms and state systems, banks shift from being optional service providers to indispensable infrastructure.

Pillar 4: Simplified product architecture

While infrastructure and integration address accessibility, the fourth pillar, simplified product architecture, ensures usability. This is not always about giving customers more choices; often, it is a strategic decision to standardize products for operational efficiency and lower costs. Capitec’s single “Global One” account is an example of radical standardization that minimized complexity and enabled volume economics. Other institutions, like Bank Jago with its “Pockets” system, take a different approach, offering an intuitive architecture with “multi-pocket” features that align with how users naturally manage their money. Both strategies achieve the goal of usability but through different means. Furthermore, alternative credit scoring, a component of this pillar, leverages transactional and behavioral data in place of formal credit histories. It is important to note that this is not always feasible in low-data environments, which can limit its applicability in some markets.

Pillar 5: Community-centric approach

Finally, the fifth pillar, community-centric approaches, underscores that trust and cultural embeddedness are indispensable for lasting inclusion. Technology may enable reach, but adoption hinges on social legitimacy. Leveraging local networks and trusted figures transforms financial agents from mere transaction facilitators into advisors embedded within the social fabric (Bandhan Bank, 2024; Timothy, 2024). Community-based verification substitutes for absent documentation, with village authorities or community leaders providing attestations that both enable access and strengthen accountability (International Finance Corporation, 2019). Crucially, financial inclusion extends beyond opening accounts; it requires ensuring that services improve lives. Embedded financial education programs, often delivered alongside microcredit or savings initiatives, reduce default risks while empowering clients to use services productively (Mandal, 2024; Sampath Bank, 2024). This combination of education and community accountability creates virtuous cycles where institutions and customers succeed together, even amid economic volatility.

The integrated success model

Taken together, these five pillars highlight that profitable inclusion is not a byproduct of isolated innovations but of systemic design. Advanced eKYC provides the gateway, multi-channel distribution ensures reach, ecosystem integration embeds banking in daily life, simplified products guarantee usability, and community engagement builds the trust that sustains long-term relationships. When executed in concert, these strategies transform financial institutions from gatekeepers into enablers, proving that inclusion and profitability can reinforce rather than contradict one another.

Discussion questions

(1) If financial inclusion is now a commercial imperative, what ethical boundaries should financial institutions navigate when designing profit-driven models for low-income and vulnerable populations? (2) How can traditional banks reimagine their legacy systems, cultures, and cost structures to compete with agile, mobile-first players that are proving profitable at scale in underserved markets? (3) In contexts such as Sri Lanka, where both IT literacy and financial literacy remain uneven, how did Sampath Bank’s IT innovations improve customer service without excluding large segments of the population? To what extent did hybrid digital-physical models prove more effective than purely digital strategies in addressing these constraints? (4) Sampath Bank had already invested in digital infrastructure before COVID-19, yet the pandemic accelerated the pace of adoption. How did this crisis-driven acceleration, combined with central bank regulatory reforms, shape the bank’s competitive positioning as a market leader? Could Sampath’s approach be seen as a case of leveraging constraints as innovation catalysts? (5) How can financial institutions ensure that rapid digitalization does not inadvertently deepen inequality by leaving behind populations without digital literacy, internet access, or compatible devices? (6) bKash relied heavily on its agent network as both distribution channels and trust-builders. As Bangladesh transitions toward a more digital-first economy, should bKash continue investing in its agent network, or pivot toward full digitalization? (7) The pillars are presented as a collective success model. Do all institutions need to execute all five pillars to succeed, or can they focus on a subset of them? What factors, such as regulatory environments or market maturity, might determine which pillars are most critical in a given context?

Concluding remark

The institutions profiled here have rewritten the rules of banking by proving that constraints often become catalysts for innovation. They created competitive moats by leveraging their innovative approaches to geographic isolation, regulatory complexity, and customer education needs. Their success signals a fundamental shift in financial services where agility surpasses legacy infrastructure, customer-centricity triumphs over product complexity, and inclusive growth outpaces exclusive profitability. For incumbents, the challenge is whether to adopt transformative strategies or risk being outpaced by more agile competitors. The window for strategic repositioning is narrowing rapidly as digital-native institutions establish dominant positions in emerging markets. The most successful banks of the next decade will be those that recognize inclusion not as corporate responsibility but as their core competitive strategy, understanding that in a globally connected economy, institutions that broaden access are also positioning themselves for sustained growth.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Notes

Author biographies

![]() .

.

![]() .

.

![]() .

.

![]() .

.

![]() .

.