Abstract

Prior research linking anxiety and depression to risky decision-making has yielded inconsistent findings. This may reflect differing definitions of risk, characterized as outcome variance or potential negative consequences. This cross-sectional experimental study investigated affective distress and aimed to determine whether choices were driven by aversion to riskier (higher variance) outcomes, sensitivity to negative outcomes, or a combination of the two. A sample of adults (N = 526, aged 18-60) completed a risky decision-making task involving choices between probabilistic gambles with positive and/or negative outcomes. An affective distress component was obtained from self-report measures of anxiety and depression using principal component analysis. When losses were possible, choice behavior reflected risk aversion and heightened sensitivity to differences in expected value; however, this was attenuated with increasing levels of affective distress, resulting in less reliable selection of mathematically advantageous options. In gain-only lotteries, choices were consistent with risk seeking and reduced sensitivity to differences in expected value, regardless of affective distress. These findings suggest that decision-making and risk attitudes are substantially influenced by the presence or absence of potential loss. Affective distress alters choice behavior specifically when loss is present, suggesting that loss may play a more prominent role than variance in risky decision-making for anxiety and depression.

Affective disorders such as anxiety and depression are among the most prevalent mental health conditions globally (World Health Organization, 2022), impacting approximately 298 million and 193 million people, respectively (Santomauro et al., 2021). Anxiety is primarily characterized by excessive worry and heightened sensitivity to threat, and depression is defined by persistent low mood and reduced sensitivity to reward. Both anxiety and depression involve common features including general distress, and comorbidity between them is high (Clark & Watson, 1991). Heightened intolerance of uncertainty, wherein unknown future events elicit aversive emotional responses, has been identified as a transdiagnostic feature, impacting individuals with subclinical and clinical presentations of anxiety and/or depression (Carleton, 2016; McEvoy & Mahoney, 2012). Furthermore, altered decision-making processes, namely over-valuation of bad outcomes and under-valuation of good outcomes, have been observed in individuals with affective disorders (Paulus & Yu, 2012). However, current understanding of value-based decision components underlying these trends remains somewhat contentious due to conflicting perspectives and variability in the definition of risk (Aven, 2012; Mata et al., 2018; Schonberg et al., 2011). Some argue that differences in decision patterns are driven by an aversion to risk, in terms of uncertain (i.e., probabilistic and/or indeterminate) outcomes (Charpentier et al., 2017; Hartley & Phelps, 2012), whereas others suggest that aversion to potential loss plays a more prominent role (Xu et al., 2020). The present study used a novel adaptation of an established risky decision task (Levy et al., 2010; Ruderman et al., 2016; Tymula et al., 2013) to clarify differential contributions of risk and loss to value-based decision-making across the spectrum of affective distress symptoms in the general population.

Conceptualization of risk plays an essential role in what we understand about affective distress and decision-making. Risk, or first-order uncertainty, is typically defined as any scenario in which potential outcomes and their probabilities are known, but the eventual outcome is indeterminate (Bach & Dolan, 2012). This is distinct from second-order uncertainty, which involves uncertainty about the decision environment in addition to outcomes, such as ambiguity, where some element of potential outcomes (e.g., value and/or probability) is unknown or obscured. According to economic definitions, the objective degree of risk is quantified by the variance of potential outcomes relative to the expected value (EV; the sum of the probability-weighted potential outcomes; Markowitz, 1952). Larger variance reflects greater disparity between potential outcomes and therefore higher risk. In contrast, psychological approaches define risk in terms of negative consequences, such as harm or loss (Schonberg et al., 2011). Accordingly, the degree of risk is measured by the magnitude and probability of undesirable outcomes (Botelho et al., 2023). While both models involve uncertainty regarding eventual outcomes, they differ in their methods of quantifying risk, leading to distinct interpretations of which element makes it aversive (Hertwig et al., 2018). For the purposes of the present study, we adopt the economic definition of risk as variance, and account for the psychological definition through examination of discomfort with loss. Clarifying these distinctions is critical because theoretical differences map directly onto competing explanations of why individuals with affective distress may deviate from optimal choice.

The process of decision-making is informed by assessing and comparing the values of available options (Rangel et al., 2008). A rational decision-maker would be expected to choose the option with the most favorable EV, reflecting attempts to maximize positive outcomes and minimize negative outcomes (Bishop & Gagne, 2018); however, it is well established that human behavior often deviates from such expectations as choices are guided by subjective rather than objective valuation (Camerer, 1989). The ‘risk-as-feelings’ hypothesis offers a potential explanation, highlighting that emotional responses, rather than cognitive assessments of risk, often drive decisions involving uncertainty (Loewenstein et al., 2001). Under this theory, uncertainty creates an internalized negative state that influences decision-making rather than relying on the objective EV of options. Anxiety and depression are characterized by increased negative affect, which may exacerbate the ‘risk-as-feelings’ effect when faced with potential negative outcomes (Phelps et al., 2014). Anxiety and mood disorders have been associated with elevated appraisals of the likelihood and severity of negative future events (Butler & Mathews, 1983), with depressed individuals additionally anticipating fewer positive outcomes (Miranda & Mennin, 2007). Affective states have been shown to distort the valuation of probabilistic outcomes through heightened sensitivity to low-probability negative outcomes, diminished responsiveness to reward magnitude, and altered weighting of gains versus losses (Bishop & Gagne, 2018; Gu et al., 2017; Paulus & Yu, 2012).

Attitudes toward risk are commonly evaluated using value-based decision-making tasks that manipulate the properties of potential outcomes of options, such as their magnitude, probability, or valence (positive or negative; Botelho et al., 2023). For example, consider a pair of gambles with one option offering a 20% chance of winning $20 and an 80% chance of receiving nothing, and the other offering a 60% chance of winning $10 and a 40% chance of losing $5. Neither option is mathematically advantageous, as they both have an EV of $4; however, the mechanisms driving choice can be inferred from the option selected. Discomfort with variance would likely result in selection of the second gamble, while preference to avoid the possibility of loss would lead to selection of the first gamble. There are numerous studies examining the relationship of anxiety and depression with risky decision-making, but a primary limitation of these studies is their focus on gain outcomes, which does not allow for examining gain/loss asymmetry (valence; e.g., Chung et al., 2017; FeldmanHall et al., 2016; Hagiwara et al., 2022). Anxiety is typically associated with a preference for certain or low-variance options, even when that preference results in lower reward (Hartley & Phelps, 2012). Such findings have emerged across diverse samples including induced (Raghunathan & Pham, 1999) and subclinical anxiety populations (Schmidt et al., 2018).

There is evidence to suggest that individuals with anxiety exhibit increased discomfort with variance when loss is possible. According to the reflection effect (Kahneman & Tversky, 1979), people tend to be risk averse for gains, avoiding probabilistic gains in favor of guaranteed reward, and risk seeking for losses, preferring probabilistic losses which present the possibility of avoiding unfavorable outcomes. Contrary to these expectations, Galván and Peris (2014) found that individuals with anxiety selected significantly fewer risky choices under loss relative to the control group, preferring certain options, consistent with risk aversion in a context that would predict risk seeking. This may indicate that those with anxiety find not knowing whether a negative outcome will occur more aversive than the loss itself. However, the comparison between probabilistic and guaranteed outcomes conflates tolerance for outcome variance and preference for certainty because selecting the guaranteed option eliminates variance altogether. Accordingly, sensitivity to variance can be better evaluated in the absence of guaranteed options. In a study presenting choices between pairs of probabilistic gambles, each offering a 50% chance of resulting in a gain or loss, variance was manipulated by adjusting the magnitudes of potential outcomes (Giorgetta et al., 2012). Anxious individuals selected the ‘safer’ lower variance gambles more frequently than healthy controls. Although this behavior may be driven by heightened discomfort with variance when loss is possible, it cannot be distinguished from desire to minimize loss because higher variance options also involved larger potential losses. In addition, both paradigms attempted to isolate variance preferences by presenting choices between options of equal EV; however, this approach precludes evaluation of rational value-based choice as when value is held constant, it is not possible to determine whether choices are driven by altered sensitivity to variance or potential loss.

In an influential study, Charpentier et al. (2017) aimed to quantify the relative contributions of risk aversion and loss aversion in clinical anxiety using a prospect theory modeling approach (Kahneman & Tversky, 1979; Tversky & Kahneman, 1992). Participants made binary choices involving gain lotteries (certain gain versus a 50% chance of winning a larger gain or nothing) and mixed lotteries (certain $0 versus a 50% chance of winning or losing some monetary amount). Beyond evaluating choice proportions, Charpentier and colleagues (2017) conducted computational modeling to estimate risk and loss parameters. Relative to healthy controls, individuals with anxiety exhibited increased risk aversion, but not loss aversion. However, it is important to note that these parameters represent subjective adjustments to value informing choice selection rather than discomfort with variance or loss. Under prospect theory, risk aversion is operationalized as diminishing sensitivity to value, which describes how differences between larger outcomes are perceived as smaller than equivalent differences between smaller outcomes (Kahneman & Tversky, 1979; Tversky & Kahneman, 1992). Furthermore, loss aversion specifically represents how the magnitude of losses are weighted relative to equivalent gains. Additionally, the fundamentally different formats of lotteries potentially compromised comparability. Specifically, mixed gambles were more akin to accept/reject approaches given the certain alternative was $0 whereas gain lotteries presented a clear certain versus probabilistic choice. These analytic approaches and methodological features limit the strength of the conclusion that risk aversion, rather than an exaggerated weighting of losses, underlies anxiety-related decision biases. Consequently, it remains unclear whether the presence of loss increases discomfort with variance relative to gain contexts or whether anxious individuals exhibit a generalized discomfort with variance regardless of valence.

As real-world decision-making rarely includes a guaranteed option, paradigms involving choices between risky alternatives varying in both EV and variance offer more ecologically valid inference (Holt & Laury, 2002; Wright et al., 2012, 2013). Wright and colleagues (2012, 2013) demonstrated that the pattern of choice preferences across gains and losses reversed when participants could avoid risk by selecting a guaranteed option compared with when they were required to choose between two risky options, underscoring the importance of task structure in interpreting attitudes toward risk. Complementary evidence shows that potential losses increase attention to EV differences, enhancing discrimination between advantageous and disadvantageous options rather than reflecting increased risk seeking or loss-averse behavior (Yechiam & Hochman, 2013). This heightened attentiveness to potential loss information may be especially pronounced in individuals with affective distress symptoms given that heightened sensitivity to punishment is characteristic of both anxiety and depression (Katz et al., 2020).

The Present Study

The present study aims to investigate decision-making under first-order uncertainty by examining the contribution of distinct aversive features identified in economic and psychological theories of risk, and how these interact with affective distress symptomatology. To achieve this, we implemented a binary choice paradigm including pairs of probabilistic lotteries with gain only, loss only, or mixed monetary outcomes. If behavior is driven by a general discomfort with variance, we would expect to observe avoidance of riskier (higher variance) options regardless of whether potential outcomes are gains or losses, even when the EV of the safer (lower variance) option is less favorable (

Method

Participants

Data were collected from 627 participants recruited via Amazon’s Mechanical Turk (MTurk) in September 2018. Subjects between 18 and 60 years old residing in the United States were eligible to participate. Following exclusions (see Data Screening), the final sample consisted of 526 participants (254 male, 271 female, 1 non-binary) aged 19 to 60 (M = 35.78, SD = 10.40). Participants completed one of three conditions (see Experimental Conditions): reward-only lotteries (gain-only), reward-only and punishment-only lotteries in separate blocks (gain/loss separate [G/L-separate]) and mixed reward and punishment lotteries (G/L-mixed), which were comprised of 190, 185 and 151 participants, respectively. All participants provided informed consent. This study was approved by the Human Research Ethics Committee of the University of Melbourne (ID 1852118).

There is currently no single standardized analytical procedure for calculating the statistical power of binomial generalized linear mixed models involving complex random-effects structures and multiple interaction terms (Kumle et al., 2021; Mathieu et al., 2012). Accordingly, we conducted a sensitivity analysis for an ANCOVA, with lottery type as a between-subjects factor, and affective distress and

Measures

Psychopathology Questionnaires

Several reliable and well-validated questionnaires were administered to assess psychopathology. Cronbach’s alpha was calculated from the items of each subscale and/or scale, to assess the internal consistency of the present sample.

Generalized Anxiety Disorder Questionnaire (GAD-7; Spitzer et al., 2006)

The GAD-7 is a 7-item scale designed to measure the core symptoms of Generalized Anxiety Disorder per the DSM-5 (American Psychiatric Association, 2013). Participants reported the extent to which they experienced each symptom over a retrospective period of 2 weeks using a Likert scale ranging from 0 (not at all) to 3 (nearly every day). Previous literature has indicated a cut-off score of 10 is able to identify probable cases of generalized anxiety disorder with 89% sensitivity and 82% specificity (Spitzer et al., 2006). Internal consistency in the present study was excellent (

Patient Health Questionnaire Depression Module (PHQ-9; Kroenke et al., 2001)

The PHQ-9 is a 9-item scale designed to measure the nine depression criteria as per the DSM-5 (American Psychiatric Association, 2013; Kroenke et al., 2001). Participants reported how much they had been bothered by each problem over the past two weeks using a Likert scale ranging from 0 (not at all) to 3 (nearly every day). A cut-off score of 10 has been shown to identify individuals likely to meet diagnostic criteria for major depressive disorder at a sensitivity and specificity of 88% (Kroenke et al., 2001). Internal consistency in the present study was excellent (

Depression, Anxiety and Stress Scale (DASS-21; Lovibond & Lovibond, 1995)

The DASS is a 21-item scale designed to measure negative affect (depression), physiological arousal (anxiety), and general anxiety/tension (stress). Participants reported how much each statement applied to them over the past week using a Likert scale ranging from 0 (did not apply at all) to 3 (applied very much or most of the time). Internal consistency in the present study was excellent for Depression (

Repetitive Negative Thought Questionnaire (RNTQ; Stout et al., 2022)

The RNTQ is a 22-item scale designed to measure trans-diagnostic and disorder-specific repetitive negative thought. Participants indicated how typical each statement regarding thoughts or behaviors was to them on a Likert scale ranging from 1 (not at all typical) to 6 (extremely typical). Elevated RNTQ scores have been observed in individuals with probable anxiety and/or depressive disorders (Stout et al., 2022). The RNTQ includes four subscales: Worry, Interference, Brooding and Pessimistic Fixation. Internal consistency in the present study was excellent for all subscales (α ≥ .88).

Intolerance of Uncertainty Scale – Short Form (IUS-SF; Carleton et al., 2007)

The IUS-SF is a 12-item scale designed to measure one’s aversion to the uncertainty of a negative event occurring. Participants rated how much they agreed with each statement on a Likert scale from 1 (not at all characteristic of me) to 5 (entirely characteristic of me). Internal consistency in the present study was excellent for the total score (

Experimental Procedures

Decision Under Ambiguity and Risk Task

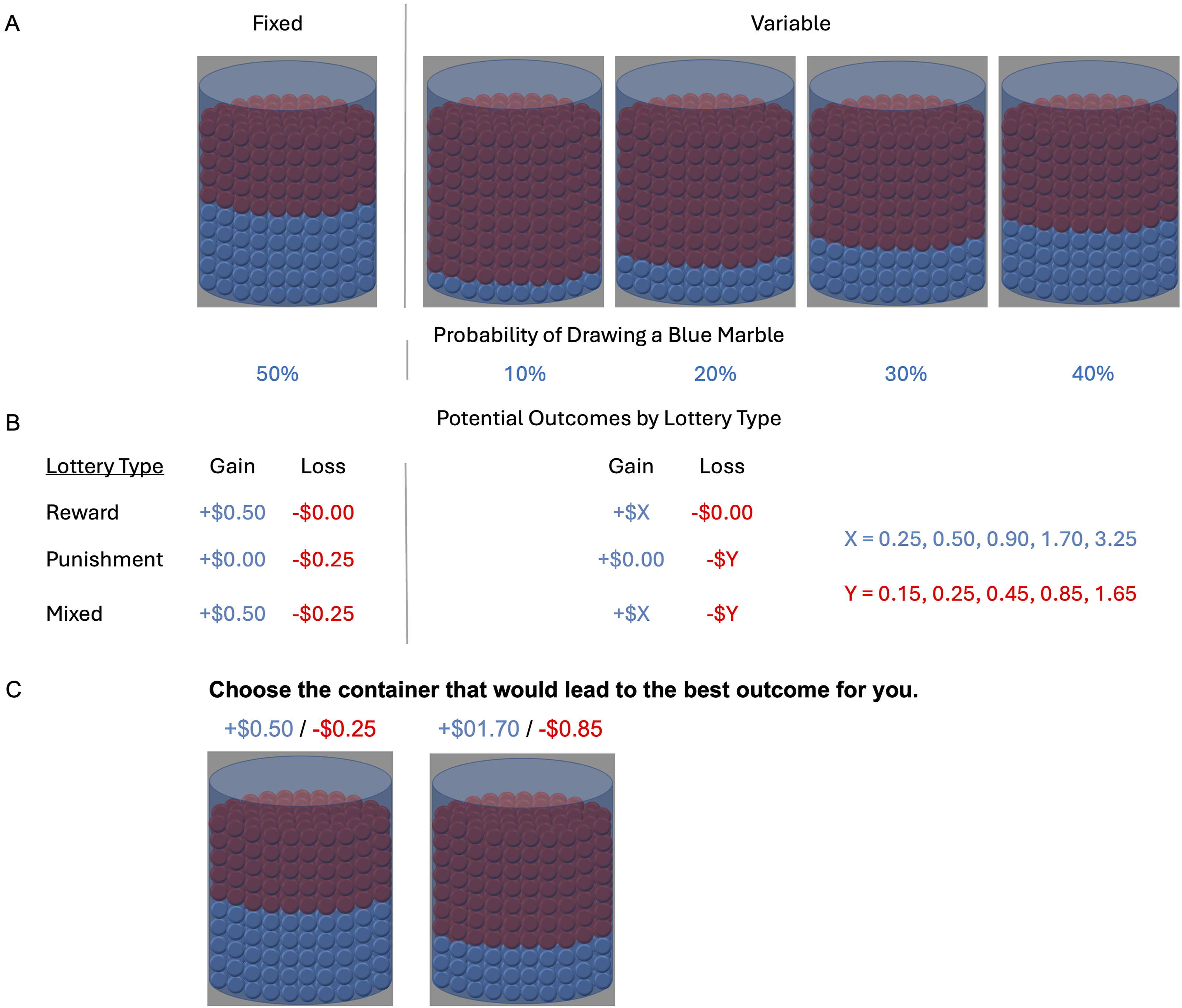

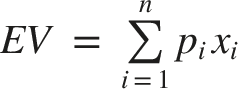

The DART was developed to expand on the principles of a similar task (Levy et al., 2010). In contrast to the previously used version, wherein participants were only presented with one option at a time, to be compared to an option that was not visually presented (i.e., a fixed reference), the DART required participants to choose between two lotteries displayed side-by-side on each trial (which reduced memory load as compared to the original version). The choice options were displayed in the form of ‘urns’, filled with a mix of red and blue marbles representing the probability of winning or losing monetary amounts displayed above each urn (Figure 1). More specifically, each visible row of marbles corresponded to approximately 10% of the contents of the urn. Gamble pairs consisted of a fixed urn that remained unchanged within a block and a variable urn that presented variations in both probability and magnitude of potential outcomes as a function of the lottery type. Participants were advised that a marble would be drawn from their selected urn. Blue marbles corresponded to positive outcomes while red marbles corresponded to negative outcomes. Schematic of risky trials from the decision under ambiguity and risk task.

Experimental Conditions

Participants were randomly assigned to one of three conditions reflecting lottery types distinguished by the valence of potential outcomes. In the gain-only condition, participants were presented with reward-only lotteries that could result in monetary gain but not loss. The G/L-separate condition consisted of both reward-only lotteries (G/L-reward; identical to those presented in the gain-only condition) and punishment-only lotteries (G/L-punishment), where money could be lost but not gained. The G/L-mixed condition contained mixed lotteries whereby drawing a blue marble resulted in monetary gain but drawing a red marble resulted in monetary loss.

The fixed urn was always a risky lottery (i.e.,both the outcome amount and probability of potential outcomes were known). On half the total trials, the variable urn was also risky, with the probability of winning being equally balanced between 10%, 20%, 30%, and 40%. In the other half of the trials, the variable urn was an ambiguous lottery in which the potential outcomes were known but their probabilities were partially occluded. Note that this manipulation resulted in two fundamentally different forms of uncertainty. In each condition, half of the blocks presented consisted of risky trials (first-order uncertainty) while the other half consisted of ambiguous trials (second-order uncertainty). The current study is solely focused on risk, with ambiguity to be the subject of a separate publication.

We aimed to present a total of 80 risky trials in each condition. Due to a technical error, the block of reward-only trials in the gain-only condition was presented twice, allowing participants to review their prior responses, and resulting in data from only 40 trials being retained. The G/L-separate condition consisted of one block of 40 risky reward-only trials and one block of 40 risky punishment-only trials. In the G/L-mixed condition, one block of 80 risky mixed trials was presented. We counterbalanced the side on which the fixed and variable options were presented. Presentation of the gamble pairs and selection of an urn was not limited by time. Within each condition, blocks were presented in a randomized order. The presentation of trials within each block was also randomized.

DART Parameters

In addition to the probabilities of the choice options, we also manipulated the potential winnings. For reward-only lotteries (presented in gain-only and G/L-separate condition) the fixed gamble constituted a 50% chance of winning +$0.50 while the variable option constituted a chance of winning the following amounts: +$0.25, +$0.50, +$0.90, +$1.70, +$3.25. For punishment-only lotteries (presented in the G/L-separate condition) the fixed gamble comprised a 50% chance of losing -$0.25, while the variable gamble could result in losing the following amounts: -$0.15, -$0.25, -$0.45, -$0.85, -$1.65. In the G/L-mixed condition, the fixed option involved a 50% chance of winning +$0.50 and a 50% chance of losing -$0.25 while the variable gamble constituted a chance of winning or losing the following outcomes: +$0.25/-$0.15, +$0.50/-$0.25, +$0.90/-$0.45, +$1.70/-$0.85, +$3.25/-$1.65. Potential loss outcomes were half the magnitude of potential gain outcomes to account for the tendency for losses to be weighted as twice as much as equivalent gains (Tversky & Kahneman, 1992). This method has been employed in similar economic decision-making tasks (e.g., Ernst et al., 2014). Potential outcomes and their associated probabilities for all risky urns across lottery types are provided in Supplemental Table S1.

Monetary Incentive

In addition to the guaranteed payment of $2.50, participants could receive a bonus ranging from $0 to $3.25 (up to an additional 130% of the guaranteed reimbursement), depending on their choices and simulated outcomes. Participants were informed that bonuses would be calculated by simulating the outcome of a gamble they had selected in a trial chosen at random. A random number was computed and compared to the probability of winning. Selecting a trial for implementation and using actual monetary payment ensured that participants treated every trial as if it were real, because they did not know which trial would be selected (cf. Camerer & Mobbs, 2017). Simulated outcomes were determined by generating a random number which was then compared to the probability of winning associated with the selected gamble. For participants allocated to the G/L-separate condition, one trial from each of the lottery types (reward-only and punishment-only) was simulated. The difference between the outcomes of the gambles was calculated and added as a bonus if it was greater than 0. For participants allocated to the G/L-mixed or gain-only conditions, one trial was simulated, and the value of the outcome was added to their payment if it was greater than 0.

Procedure

Participants were directed to Qualtrics from MTurk via a hyperlink. First, they were asked to answer demographic questions and self-report psychopathology questionnaires. They then viewed instructions for the experimental task and were given four practice trials with feedback. Participants were then randomly assigned to one of the three conditions described above (gain-only, G/L-separate, G/L-mixed) and completed the task. The median study duration was approximately 20 min (M = 25.62, SD = 16.49). Participants were paid electronically via MTurk following the experiment.

Data Analysis

Data Screening

Several data cleaning procedures were applied following data collection. Questionnaire data from 21 participants were discarded due to incomplete or missing responses on the experimental task. Based on the assumption that each item of the questionnaires would take at least 1s to answer, and that the minimum amount of time the behavioral task could be completed in was 300 s (5 min), responses from six participants who completed the study in 400 s or less were excluded. Further, an inconsistency score was calculated from DASS responses using a method analogous to the procedure employed by Conners et al. (1999). In an independent dataset from n = 39,775 participants (OpenPsychometrics, 2019), responses for four item pairs were found to be highly correlated (r > .6), indicating that the response to one question in the pair should be very similar to the response on the other question in the pair. The inconsistency index consisted of the sum of the absolute difference in responses within the item pairs. A simulation of 10,000 random responses from 5,000 participants each indicated that 95% of responses resulted in inconsistency scores of 5 or less (i.e., a score greater than 5 occurred only 5% of the time in random data). Accordingly, we excluded data from 30 participants with scores exceeding this value. To examine whether participants were attentive during the risky choice task, we separately analyzed the choices in the subset of trials in which both the fixed and the variable gambles offered identical outcomes, but the probability of the variable option was less advantageous (i.e. the fixed gamble was the clear logical choice). Overall, there were six of these trials in the gain-only condition and 12 such trials in the other two conditions. The proportion of fixed gamble choices in the aforementioned trials represented a ‘logic score’. Data from 44 participants with a logic score at or below chance were excluded, consistent with decision quality analyses performed by Ruderman et al. (2016). Differences in the number of exclusions by condition were not significant.

Psychopathology Scales

As we anticipated high intercorrelations among the psychopathology variables, we conducted a principal component analysis (PCA) to reduce the data (Suhr, 2005). This method was selected over averaging items or exploratory factor analysis as PCA ensures the contribution of each subscale toward the composite score reflects the actual variance. PCA indicated a single component (see Results), which was standardized and used in analyses to explore the influence of psychopathology on decision-making (described below). Additionally, to determine whether individuals in our sample were likely to meet diagnostic criteria for anxiety and depression, clinical groups were created using established cut-off scores.

DART Performance

For the DART, we first calculated the expected value (EV) for each gamble. The EV was calculated drawing on Cumulative Prospect Theory (CPT; Tversky & Kahneman, 1992) and expected utility theory (Von Neumann & Morgenstern, 1944):

Note that EV,

Choice Behavior

We modelled selection of the riskier option via generalized linear mixed-effects models with a binomial distribution and logit link function, which transforms probabilities to the log-odds scale for estimation.

We began with a Null model, which included only a random effect that allowed intercepts to vary for participants. The null model presented the possibility that no variable systematically predicted choice and served as a comparison point for models including fixed effects.

To compare trials with and without gain or loss outcomes, the G/L-separate condition was split into its component lottery types, henceforth referred to as G/L-reward and G/L-punishment. Lottery types differed in the valence/s of potential outcomes, resulting in systematic variation in ΔEV. Accordingly, to improve interpretability and correct for this variation, cluster-based mean centering was implemented (Sommet & Morselli, 2017). This method separates within-cluster effects from between-cluster variation so that sensitivity to ΔEV is evaluated within each specific lottery type, preventing confounding effects due to differences in the distribution of ΔEV between lottery types.

A Base model was constructed that included task variables (ΔEV, lottery type) and their interaction as fixed effects, with participant (id) and ΔEV as random effects, allowing participants to have random intercepts and for slopes to vary by ΔEV:

Individual differences in psychopathology were examined by adding the psychopathology PCA component and its interactions with task variables as fixed effects to the Base model equation to construct the Psychopathology model:

Model fit of the Null, Base and Psychopathology models were compared via evaluation of Akaike information criterion (AIC), which penalizes model complexity (Burnham & Anderson, 2004). The percentage of variance explained by fixed and random effects were also examined via theoretical pseudo

As lottery types were not ordinal, there was no logical reference point. Accordingly, we applied sum coding, which constrains the coefficients to sum to zero. Under this coding scheme, the intercept represents the grand-mean log-odds of selecting the riskier option across all lottery types when the continuous variables are held constant at their centered means (i.e.,0). The fixed effects model estimates (β) therefore indicate changes in log-odds relative to this grand mean. For continuous predictors, coefficients represent linear trends (slopes), specifying the change in log-odds associated with a one-unit increase in the predictor, holding remaining predictors constant. Because coefficients under sum coding do not directly yield condition-specific predictions, to aid interpretability, we report estimated marginal means, which are identical to the sum of the model intercept and model coefficient of the predictor/s of interest. Predicted probabilities were obtained by transforming the fitted log-odds from the model using the inverse-logit function.

Index of Risk Attitude

We derived a model-based estimate of the indifference point (IP), an index of the ΔEV at which selection of riskier and safer gambles are equally probable. While ΔEV indicates which gamble is mathematically favorable according to their objective EVs, the IP signifies subjective equivalence based on choice behavior. Risk attitude can be inferred by comparing subjective and objective equivalence. For instance, subjective and objective evaluation are aligned at IP = 0, as neither option is favored mathematically or behaviorally, reflecting a risk-neutral attitude. A more negative IP indicates a stronger mathematical advantage of the riskier option is required for the predicted probability to exceed 50%, consistent with risk aversion. Conversely, a more positive IP denotes risk seeking, as selection of the riskier option exceeds chance at a point where it is not objectively advantageous, revealing greater willingness to tolerate variance even in the absence of more favorable outcomes.

Statistical Analyses

Data pre-processing and analyses of choice behavior were implemented within the statistical package R (v4.3.3; R Core Team, 2024), using RStudio (v2023.06.0; Posit team, 2023). Mixed effects modelling was conducted via the lme4 package (Bates et al., 2015) and estimated marginal means were obtained with the emmeans package (Lenth, 2023). Statistical analyses of PCA, t-tests, ANOVA, ANCOVA, post-hoc comparisons and Pearson’s correlations were performed with the statistical program JASP (v 0.18.3; JASP Team, 2024). For transparency and to support interpretation of the results, data and annotated analysis scripts are available at osf.io/cvshu.

Analyses of overall task effects were conducted followed by investigation of individual differences in psychopathology. Statistics are reported for the best fitting model. Where there were significant effects, we conducted post-hoc analyses. We implemented pairwise comparisons and linear trend analysis for categorical and continuous variables, respectively. Where there were interactions, we used combinations of pairwise and linear contrasts, as appropriate. All statistical inferences were conducted on the log-odds scale. The Benjamini-Hochberg method was used for controlling the false discovery rate (FDR) and was chosen to balance the risk of Type I and Type II errors. For post-hoc pairwise comparisons, we applied Bonferroni correction due to its conservative nature.

Results

Demographics

All sociodemographic data are described in Supplemental Table S2. Approximately 75% of the sample identified as Caucasian. Most of the sample (52.47%) had completed a college/university degree or higher education. Less than 25% of the sample had never been enrolled in a college course. More than 80% of the sample was employed and approximately 70% of participants earned between $25,001 and $100,000. Roughly 45% of participants were married and an additional 45% were single or had never been married. No significant differences by DART condition were found (p’s

Psychopathology Scales

We administered the GAD-7, PHQ-9, DASS, RNTQ and IUS. There were no differences in any of the questionnaire scales or subscales by DART condition (gain-only, G/L-separate, G/L-mixed), controlling for multiple comparisons. Descriptive statistics of questionnaires are provided in Supplemental Materials (Table S3). All psychopathology questionnaires were moderately-to-highly intercorrelated (see Supplemental Table S4). PCA with promax rotation indicated a single component that accounted for 69.31% of the variance. Inclusion of a second component accounted for an additional 9.52% of the variance, which did not meaningfully contribute to the total proportion of variance explained. As such, the single component solution was selected for analysis (see scree plot, Supplemental Figure S1). Scale loadings on the first component are provided in Supplemental Table S5. Given the high loading for all questionnaires, and that the contribution of depression and anxiety measures were equivalent, the component was labelled Affective Distress (AD).

Clinical cut-off scores on the GAD-7, PHQ-9 and DASS were used to categorize individuals to assess the percentage of our sample likely to meet diagnostic criteria. Approximately 30% of the sample was likely to have an anxiety disorder and approximately 40% of the sample was likely to have a depressive disorder, with significantly higher AD scores observed in the groups likely to meet diagnostic criteria (see Supplemental Table S6).

Choice Behavior

Omnibus Test of Effects for the Base and Psychopathology Mixed-Effect Generalized Linear Models

Note. Relative Expected Value

*** p < .001.

DART Effects

First, we examined the main effect of lottery type, which captures differences in the selection of the riskier (higher variance) option across the lottery types (gain-only, G/L-reward, G/L-punishment, and G/L-mixed) when holding ΔEV and AD constant at their means. The predicted probability of selecting the riskier gamble was lowest in G/L-punishment lotteries, followed by G/L-mixed, and highest in gain-only and G/L-reward lotteries (see Figure 2A). Pairwise comparisons indicated significant differences in gamble selection between all lottery types (all p’s < .001), except between gain-only and G/L-reward lotteries (p = .214). That is, lottery types involving potential losses were associated with significantly lower selection of the riskier option than lottery types involving potential gains. Main effects of lottery type and relative expected value on the predicted probability of selecting the riskier gamble.

The main effect of ΔEV reflects systematic variation in choice behavior as a function of ΔEV, averaged across lottery types and holding AD constant. Because ΔEV was calculated by subtracting the EV of the riskier option from the EV of the safer option, negative values correspond to trials where the riskier option was optimal, whereas positive values indicate that the safer option was optimal. A significant linear trend was identified such that as ΔEV increased by one unit, the log-odds of selecting the riskier gamble decreased (β = -6.37, z = -34.47, p < .001). This negative linear trend represents sensitivity to ΔEV with predicted choice generally aligning with selection of the gamble with the higher EV, as illustrated in Figure 2B. That is, the predicted probability of choosing the riskier option was higher when the riskier option was mathematically advantageous, but lower when the safer (lower variance) option was advantageous. The largest changes in predicted choice occurred where gambles within a pair were close in EV (i.e., near 0). The predicted probability of selecting the riskier option fell below the 50% threshold despite having a slightly higher EV than the safer option (IP = -0.12, 95% confidence interval [CI] [-0.17, -0.06]), indicating very slight overall risk aversion.

Psychopathology Model Estimates for the Lottery Type × Relative Expected Value Interaction Effect

Note. Relative Expected Value (

*** p < .001.

Sensitivity to relative expected value varies according to the valence of potential outcomes.

Effects of Psychopathology and Interactions with the DART

The main effect of AD indicates how selection of a riskier (higher variance) gamble varies as a function of AD when averaging across lottery types and holding ΔEV constant. A one unit increase in AD was associated with an increase in the log-odds of selecting the riskier gamble ( Predicted probability of selecting the riskier gamble as a function of affective distress and its interactions with lottery type and relative expected value.

The interaction effect between AD and lottery type assesses whether the relationship between AD and selection of the riskier gamble varied as a function of lottery type when holding ΔEV constant. Significant positive linear trends were identified in G/L-punishment (

The interaction effect between ΔEV and AD examines whether sensitivity to ΔEV varies as a function of AD when averaging across lottery types. As AD increased, the linear trend of ΔEV weakened, becoming less negative, relative to the main effect of ΔEV (

Finally, the three-way interaction between lottery type, ΔEV and AD evaluates whether the impact of AD on sensitivity to ΔEV differs across lottery types. As AD increased, the magnitude of the ΔEV linear trend decreased in G/L-punishment ( Moderating effect of affective distress on sensitivity to relative expected value as a function of lottery type

Discussion

The present study investigated drivers of value-based decision-making under first-order uncertainty and examined whether affective distress symptoms influenced how variance and loss contributed to decision-making. We contrasted two theoretically motivated accounts and hypothesized that behavior driven by economic conceptualizations of risk would involve avoidance of riskier (higher variance) gambles, independent of the valence of potential outcomes (

Asymmetry in behavior between gambles with and without loss is an established finding in economic decision-making tasks. We found that the probability of selecting the riskier gamble was lowest in lotteries with potential loss, while in lotteries with gain outcomes participants were more willing to select the riskier gamble. In lotteries without potential loss, this occurred even when the safer option was the rational choice, indicative of a greater tolerance of variance (i.e., risk seeking behavior). Although prospect theory predicts risk aversion for gains and risk seeking for losses (Kahneman & Tversky, 1979; Tversky & Kahneman, 1992), reversed choice preferences have been observed when risk (variance) cannot be avoided through selection of a guaranteed option (Wright et al., 2012). In the present study, the point at which gambles involving potential loss reached subjective equivalence appeared to function as a threshold, whereby there was a strong shift aligned with selection of the optimal gamble. As such, this pattern suggests that loss enhanced sensitivity to differences in value, rather than reflecting uniform discomfort with variance. This interpretation aligns with Yechiam and Hochman (2013), who argued that potential loss results in increased sensitivity to option values, leading to more reliable selection of optimal choices. Our findings further align with von Gaudecker et al. (2011) who varied the probabilities on a set of lotteries, thereby systematically manipulating EV and variance, and found that the riskier option had to be more favorable to be selected in the presence of potential loss, while higher tolerance of variance was demonstrated when only gains were possible. Collectively, these findings suggest that choice behavior may be contingent on task structure, including the presence or absence of certainty or loss, which may be of particular importance in attempting to understand individual differences in psychopathology. By demonstrating these patterns in a large, normative sample before exploring affective distress variables, we establish a baseline understanding of decision behavior in our paradigm, which allows us to more precisely characterize how affective symptoms alter these processes.

Although the influence of affective distress was relatively small, individual differences in psychopathology accounted for additional variability in participants’ choices beyond the influence of task features. In general, when the objective EVs of options were equal, such that a risk-neutral individual would be expected to be indifferent between them, we found that increasing symptoms were associated with a greater probability of selecting the riskier gamble (although the predicted probability remained below chance across levels of affective distress). Examination across lottery types revealed this pattern was only significant in the presence of loss and was particularly evident in the absence of potential gain. Furthermore, while there was no relationship between affective distress and risky choice selection in gain lotteries, the predicted probability remained above chance, further demonstrating the risk-seeking attitude revealed in the task effects. While participants were generally sensitive to differences in EV in lotteries with loss, relative to individuals with lower levels of affective distress, those with elevated affective distress demonstrated diminished sensitivity to EV. This resulted in less reliable selection of the advantageous gamble. Higher affective distress was associated with reduced selection of the riskier gamble when it was objectively optimal. When evaluated in isolation, this may appear to be consistent with elevated discomfort with variance; however, selection of riskier gamble was simultaneously more likely when the safer option was advantageous. This pattern may indicate that affective distress disrupts the calibration of risk assessment in relation to potential losses, leading to decision-making that is less guided by objective evaluation of outcomes.

Individuals with higher affective distress may have struggled to integrate key decision variables (e.g., EV and variance) in the presence of loss, opting for higher probabilities of avoiding loss or obtaining a lower magnitude loss (e.g., preferring a 90% chance of losing 15c over the option with a 50% chance of losing 25c), even when such choices were less optimal. Interpretation of our findings is bolstered by the appraisal-tendency framework (Lerner & Keltner, 2000) and the risk-as-feelings hypothesis (Loewenstein et al., 2001). Both theories underscore the role of emotions in risk and decision-making, with the appraisal-tendency-framework focusing on the effects of specific emotions and the risk-as-feelings hypothesis emphasizing the conflict between emotions and cognitive evaluation. In other words, the presence of loss may have decreased rational appraisal in favor of affective appraisal, resulting in suboptimal choices. Our findings align with established distinctions in the decision-making literature between integral affect (emotion directly relevant to a decision) and incidental affect (background emotional states unrelated to the decision at hand). While integral affect can serve as an adaptive heuristic for guiding decisions (Slovic et al., 2007), the affective distress measured in our study represents incidental affect (i.e., how an individual is feeling unrelated to the task at hand) that appears to interfere with optimal decision-making. This interference aligns with well-documented evidence that incidental emotions can bias judgment processes (Lerner et al., 2015; Schwarz & Clore, 1983). Our findings demonstrate how persistent affective distress symptoms interact with loss contexts to produce specific patterns of suboptimal choice behavior. For individuals with higher levels of affective distress, rather than simply increasing risk aversion as might be expected, incidental negative emotions appear to disrupt EV estimation processes specifically when loss is possible. This suggests that the everyday decision-making challenges faced by individuals with elevated anxiety and depression may be most pronounced in contexts involving potential negative outcomes, where emotional states may cloud rational evaluation of options. In the real world, this means people with elevated affective distress might be more prone to taking harmful risks or avoiding necessary risks, impacting their well-being, relationships, and economic stability. Underlying affect may have a potentially more persistent influence on decision-making than decision-related components and may be particularly insidious when threat, harm, or loss is possible.

Our results also speak to ongoing debates about the mechanisms underlying altered risky decision-making in anxiety and related forms of psychopathology. Charpentier and colleagues (2017) modelled choices within a prospect theory framework and found that anxiety broadly enhanced risk aversion (diminishing sensitivity to value), independent of loss aversion (weighting of losses relative to equivalent gains). The present study quantified risk as degree of variance, and examined discomfort with potential loss, finding that altered risk attitudes in affective distress are specifically modulated by the presence of potential loss, particularly in the absence of potential gains. The conflicting findings are likely to be a result of differences in methodological and analytic approaches. The selective influence of affective distress on choices in the context of loss reflects a pattern that cannot be captured by a single diminishing sensitivity parameter because such aggregation may obscure distortions in decisions about losses that do not generalize to decisions about gains. These findings further demonstrate that modelling loss-aversion, which requires mixed gambles where potential gain and loss outcomes can be directly compared, may not be sufficient to evaluate how attitudes toward loss interact with risky decision-making and individual differences in affective distress.

Our dimensionality reduction of psychopathology measures resulted in one component, Affective Distress, that did not differentiate between anxiety and depression. This single component is congruent with the suggestion that common psychiatric disorders are characterized by an underlying General Psychopathology dimension, also referred to as the p factor, which is associated with symptom severity and functional impairment (Caspi et al., 2014). Additionally, the use of an online, non-clinical sample resulted in access to a large sample for notable statistical power that was well suited for identification of individual differences in symptomology and behavior (Gillan & Daw, 2016; Kraemer et al., 2004). More distinct patterns of behavior may have been found if comorbidity of disorders was accounted for; however, given the suggestion that concurrence of anxiety and depression is more common than pure cases of each disorder (Preisig et al., 2001), our findings may have greater ecological validity than those using case-control comparisons. Recent evidence suggests that elevated risk aversion may be specifically altered in individuals with anxiety (Sporrer et al., 2024). In a sample of patients with major depressive disorder induced worry increased risk aversion (as defined in prospect theory) only in those with comorbid generalized anxiety symptoms, with similar baseline levels of risk and loss aversion across patient and control groups. Future research should examine whether comparable findings are observed outside of the prospect theory framework, in paradigms where uncertainty cannot be avoided by rejecting probabilistic options and that also include conditions with and without the possibility of gains.

Our findings should be interpreted in light of study limitations. Our gambles featured equivalent gamble outcomes across lottery types (i.e., the potential gain and loss outcomes for mixed gambles were identical to the potential gain and loss outcomes in reward and punishment gambles, respectively), but this resulted in an imbalanced range of EV and VAR values. Future research should implement standardized EV and VAR values across lottery types even though this may result in gamble outcomes that are not matched across lottery types. This approach may aid in directly comparing the contribution of risk as conceptualized by economic and psychological theories. Due to a programming error, participants allocated to the gain-only condition received half the number of trials as participants in the other conditions. They also were able to review their previous answers when making subsequent decisions. This may have led to inconsistencies in findings between the reward-only gambles. Alternatively, exposure to G/L-punishment lotteries may have influenced subsequent choice behavior in G/L-reward lotteries contributing to inconsistencies with gain-only lotteries (Schneider et al., 2016). Although evidence suggests that exposure to gains and losses can influence behavior when participants receive feedback following a choice (e.g., Giorgetta et al., 2012; Shapiro et al., 2020), our task did not present feedback. We additionally note that participants were also presented with blocks of ambiguous trials to be the subject of a separate manuscript. The current study was not sufficiently powered to conclusively examine potential order effects; however, previous studies employing the task from which the DART was derived have neither found evidence of order effects between alternate presentations of gain and loss blocks (e.g., Pushkarskaya et al., 2017), nor reported order effects in relation to risky and ambiguous trials (e.g., Jia et al., 2020; Ruderman et al., 2016). Nonetheless, we acknowledge that it is possible that behavior was impacted by exposure to different combinations of valence and types of uncertainty. Finally, our investigation was limited to economic choices, but it would be beneficial to expand examination of choice behavior to non-monetary domains such as social risk (see Moutoussis et al., 2021). Future research could more directly investigate the extent to which prior experience with different decision-making contexts influences risk preferences, such as when social influence is present (Mislavsky & Gaertig, 2022).

This study advances the understanding of how affective distress influences decision-making under first-order uncertainty. Using a data-driven dimensionality reduction approach, we uncovered variation in affective distress symptoms in the general population that were relevant for economic choice behavior. In the presence of loss, although participants generally demonstrated sensitivity to differences in value to select mathematically advantageous choices, this tendency was comparatively diminished in individuals with higher levels of affective distress. In contrast, affective distress did not influence choice selection in the absence of potential loss. Our findings underscore the role of incidental emotions in shaping decision-making, aligning with psychological theories like the appraisal-tendency framework and the risk-as-feelings hypothesis, which highlight how emotions can override rational cognitive processes in risk assessment.

Supplemental Material

Supplemental Material - Disentangling Components of Suboptimal Risky Decision-Making in Affective Distress

Supplemental Material for Disentangling Components of Suboptimal Risky Decision-Making in Affective Distress by Kiran Sutcliffe, Sarah M. Tashjian, Nicholas T. Van Dam in Journal of Experimental Psychopathology.

Footnotes

Acknowledgments

We acknowledge Aboriginal and Torres Strait Islander people of the unceded land on which we work, learn and live. We pay respect to Elders past, present and future, and acknowledge the importance of Indigenous knowledge in the Academy.

Ethical Considerations

This study was approved by the Human Research Ethics Committee of the University of Melbourne (ID 1852118).

Consent to Participate

All participants provided informed consent electronically as indicated by selecting the statement “I consent to participate in this study” displayed via Qualtrics.

Author Contributions

Kiran Sutcliffe: Formal analysis; Methodology, Visualization, Writing – original draft; Writing – review & editing

Sarah M. Tashjian: Supervision; Writing – review & editing

Nicholas T. Van Dam: Conceptualization; Investigation, Methodology; Supervision; Writing – review & editing.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: KS is supported by an Australian Government Research Training Program (RTP) Scholarship. NTVD is supported by the Contemplative Studies Centre at the University of Melbourne, established via a philanthropic gift from the Three Springs Foundation, Pty, Ltd. SMT is supported by an Australian National Health and Medical Research Council (NHMRC) Investigator Grant (2033400) and a Brain and Behavior Research Foundation Young Investigator Award (30788).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.