Abstract

This article considers the national priority recently accorded to institutional eldercare in the People's Republic of China, with particular emphasis on the re-purposing of existing buildings to found new facilities. This new approach is noteworthy in the very parts of the country that for decades now have been profoundly committed to new construction, and in a country that has retained for so long deep commitments to at-home, family-centred eldercare as a feature of filial piety. Rapid demographic aging and heavy migration of younger adults for employment and education are among the forces that have eroded the practical foundations for this older, valued mode of eldercare. But the present article moves beyond other important social policy questions associated with institutionalized eldercare, to consider the re-purposing of buildings for this purpose. We argue that this might also point to a form of ‘capital switching’ at work in the face of over-accumulation in fixed capital and other elements of the built environment. After an initial period of building new facilities at the suburban interface with the countryside, the turn to abandoned factories, hotels, and kindergartens brings seniors closer to the inner-city neighbourhoods where the clients lived most of their lives. But ‘bundling’ these commodities with eldercare services to be delivered and paid for short, repeated turnover periods also taps into the value once invested in these abandoned or underutilized facilities. The pervasiveness of profit motivations alongside social policy concerns across nominal state, private-sector, and not-for-profit divides further suggests to us that this pattern in the circulation of capital deserves more attention in eldercare in particular, and current conditions in the real estate markets of urban China suggest that the pattern may be present for researchers to consider more generally.

Introduction

Social-scientific and policy literatures typically discuss eldercare primarily as a social policy problem that foregrounds conditions for the elderly and their families. This orientation is vitally important, but its limits come at a cost. For instance, it tends to occlude the working conditions of particularly vulnerable waged workers, and some of the hardest unpaid work in households (Chen and Powell, 2012). Situating eldercare in a wider ‘care economy’ has the virtue of retaining focus on the needs of the frail elderly, while also bringing to the fore the special burden of emotional labour that workers in eldercare bear, alongside workers in education, health, and social policy. But a second limitation of taking eldercare as a social policy problem or a problem of care alone is the occlusion of its wider socio-economic roles. Here, placing eldercare in the vaster domain of ‘social reproduction’ practices has obvious value that ‘care economy’ literature does not emphasize. Both literatures seek to make sense of work, often but not always unpaid and/or not-for-profit, that takes place in part or in whole outside the normal production facilities of the economy – feeding, clothing, and cleaning the population, educating them and caring for their health. But ‘social reproduction’ points more clearly to the wider significance of this work, beyond the immediate needs of its recipients. Yet even with social reproduction approaches, relatively few studies have linked eldercare to the explicitly geographic literature on fixed capital in the built environment. For this reason, we emphasize a third point, the under-examined role of institutionalized eldercare in re-purposing under-utilized buildings, a role that has emerged during the prolonged stagnation that has followed China's recent era of rapid urban construction.

We use the terms, ‘eldercare’ or ‘seniors care’, to analyze what some call long-term care. This care work ‘encompasses (but is not limited to) care provided in nursing homes, retirement homes, residential care facilities, and assisted living facilities’ (Strauss and Xu, 2022: 110). We examine the increasingly prominent and initially puzzling material interest in eldercare that is evident among urban construction, renovation, and real estate interests in the People's Republic of China. We draw heavily on the debate about David Harvey's (2003: 108–115, 1982/1999: 235–238, 1985) ‘capital switching’ into and out of the built environment. This theoretical formulation has already influenced debates about China's political economy, but (to our knowledge) not yet debates about eldercare in the aftermath of China's most recent construction boom. To understand the (otherwise improbable) attraction of eldercare as an investment for major landholders, we also adapt insights from the concept of ‘bundled commodities’ (Adams and Yellen, 1976).

Eldercare presents urban geographers and theorists of social reproduction with special analytical problems; the special conditions of local land markets in urban China deepen that complexity. As we will argue, unlike other parts of the so-called ‘care economy’, eldercare is not directly an investment in present or future labour. Eldercare therefore stands in a special relationship with ‘socially reproductive’ labour, for it is not directly ensuring the ongoing condition of the current workforce, nor does it prepare succeeding generations to enter the workforce. Its contribution to social reproduction is at best more indirect: as a unique stage in a cycle of reciprocal intergenerational care obligations, within and beyond extended families; and as an element in reproducing the social relations of society at large. As we will see, the competing frameworks of ‘care economy’ and ‘social reproduction’ thus provide key insights into eldercare, without speaking directly to its place in shaping the built environment.

In China's built environment, now burdened by many stranded assets in the form of under-utilized large properties, eldercare's wider significance derives as much, we argue, from the multiple temporal rhythms of its returns on investment, as these relate to the diverse turnover times of different circuits of capital. By this, we mean the daily cycles of for-profit eldercare service provision – and the similarly short and frequent payments for that service.

To summarize our explanation of this state of affairs, eldercare in metropolitan China, a heavily commodified, institutionalized, and waged service, typically provided through some combination of for-profit incentives and state involvement, can be usefully understood as a bundle of commodities. The conditions for production of the component commodities – facilities and their maintenance services, but also medical and personal services – are interwoven as they present themselves to the clientele, but they are qualitatively distinct in the interests and processes involved in their provision. In particular, they differ by the number of turnover times they require to recoup the initial outlay of interested parties. Eldercare consists partly of a set of specialized personal care services, delivered and paid for in regular, relatively short intervals. Much ‘social reproductive’ or ‘care’ work has this repetitive character – food preparation, domestic cleaning, tutoring children, etc.; so, too, do some of the other most labour-intensive parts of capitalist production. However, eldercare also involves specialized (aging-friendly) housing and lesser durable products, such as wheelchairs or adjustable beds. These yield their benefits over many repetitions of personal service provision. They are enjoyed by the clients (or put another way, used by the shorter-term service providers) over a longer period. But significantly, clients or their families commonly pay for the housing component of eldercare in regular short-term payments, much as with a lease, alongside payments for eldercare's personal services.

We arrive at the larger significance of this situation through three major research questions: What aspects of the capital switching literature help analysts most in reckoning with problems in eldercare development, and what specifically do they contribute? What elements in that literature cast most light on eldercare generally and on the Chinese experience in particular? Finally, what refinements in capital switching debates would serve Chinese eldercare analysis best?

The paper has four sections. The first introduces the recent state of paid eldercare in rich Chinese cities, primarily the major coastal cities at the heart of the long urban-industrial boom. The second section focuses on the reform era's real estate and construction patterns. The third section engages David Harvey's ‘capital switching’ framework directly for what it might contribute to the intersection of eldercare and urban construction policy. Finally, we introduce bundled commodity analysis, as outlined briefly above. This section outlines a way of thinking about capital switching in relation to repurposing disused properties for eldercare, and its macro-economic significance. We arrive at our conclusions, by situating eldercare in relation to Harvey's three circuits of capital. That placement of eldercare turns on a comparison of what the feminist political economy of social reproduction and the overlapping concept of the care economy draws out in the social characteristics of eldercare.

Institutional eldercare in rich, post-boom Chinese cities

The stupendous expansion of China's urban built environment in recent decades has elicited worldwide comment and analysis. Shaped by the specific entanglements of local state institutions and capital accumulation in China, ‘new town’ and ‘characteristic town’ construction has struck urban geographers as a special instance of David Harvey's ‘capital switching’, especially as a macro-economic remedy in periods of crisis (Harvey, 1985; Shen and Wu, 2017; Zhang et al., 2021; Zou, 2021).

We have located little if any research that has linked China's ‘capital switching’ debates to the peculiar problem of establishing eldercare facilities. Yet while on its own, re-purposing buildings for eldercare would hardly resolve the challenges that China confronts in its disused buildings, the connection still strikes us as suggestive, with wider potential implications. China currently encourages major urban centres to create new eldercare centres by re-purposing disused industrial fixed capital (e.g. abandoned factories) or buildings originally built for other social-reproduction activities (e.g. abandoned kindergartens), particularly in inner-city neighbourhoods (Guo, 2016; Ministry of Civil Affairs, 2016).

Acquiring or building eldercare facilities has also increasingly attracted new institutional actors, including insurance, real estate, construction, and landholder interests. State direction and Party guidance, as well as (officially) non-profit institutions, complement the entry of for-profit interests into eldercare. For reasons we explain below, we suggest that the rhythm of returns on health and personal services at the heart of eldercare (themselves often offered by for-profit interests) are arguably central to eldercare's appeal to these diverse interests in construction and renovation.

First, however, we will sketch some key features of China's eldercare problem, read strictly as social policy. Relative to dominant practices in North America and much of Europe, China relied more heavily and far longer on family-based at-home eldercare (with or without paid help). Providing eldercare in that way is still a powerful ethical norm in China, but it is increasingly at odds with the material and medical situations in many families. Until recently, institutionalized care has been a service of last resort for those without relatives or means. As those norms came under pressure, central government campaigns initially worked to reinforce them (National People's Congress Net, 2019).

But demographic aging and increased dispersion of family members due to urbanization, internal and overseas migration have forced the central government and the Chinese population to turn to more institutionalized eldercare, first and especially in major urban centres. First, some of the major drivers of a ‘Second Demographic Transition’ (Zaidi and Morgan, 2017), initially proposed to explain declining fertility rates in Western advanced industrialized countries, now also apply to China. Second, China's demographic trends now run well below natural replacement levels, for reasons that also reflect distinctive Chinese policy legacies (including the period of the One-Child Policy) and socio-economic conditions (Xu, 2022). In combination, these trends that have radically depressed fertility rates now place mounting burdens for eldercare on Chinese family members of working age. 1

China's political leadership has identified institutionalized eldercare as a top policy priority, with major imperatives for action at lower levels of administration (State Council, 2021). As part of this policy turn, a noteworthy discussion has emerged about acquiring the needed facilities, including re-purposing parts of the existing built environment.

In recent years, China has been facing a profound transformation in eldercare after decades of rapid urbanization and demographic aging. ‘Actively responding’ to this challenge has recently been named a national strategic priority (State Council, 2021). According to the Seventh National Census conducted in 2020, population aged above 60 and above 65 accounted for 18.7% and 13.50% of the total population respectively. The share of population over 60 increased by 5.44% in comparison to the Sixth National Census in 2010. Average annual population growth rate was 0.53%, a decrease of 0.04% compared to the previous decade. The Census forecast continued low population growth rate and increase of demographic aging in the next decade (People's Republic of China Government net, 2021). According to more recent official statistics, those over 60 and 65 accounted for 21.1% and 15.4% respectively in 2023, an increase of 2.4% and 1.9% respectively in three years since the Seventh National Census (Ministry of Civil Affairs and National Committee on Aging, 2023). Average family size within the same hukou decreased from 3.1 persons in 2010 to 2.62 persons in 2020; 63.8% of the population lived in urban areas; inter-provincial migrants increased by 88.52% in comparison to 2010 (People's Republic of China Government net, 2021). Large cities face especially serious demographic aging: those with Shanghai hukou and over 60 accounted for 37.6% of the total population with Shanghai hukou at the end of 2024 (Zheng, 2025); those with Beijing hukou and over 60 accounted for 30.2% of the total population with Beijing hukou based on 2023 official statistics (Wang, 2024).

Urbanization, migration, declining family size, and heavy work pressures have all undermined the material base for the strong Chinese tradition of unpaid family-based eldercare. As more Chinese live longer, and as medical technology improves, more seniors also need or want ongoing care that families cannot offer.

Government first responded to these pressures on historic eldercare practices with general publicity campaigns that reinforced neo-traditional norms of filial piety and thus family-based care. (We personally observed that more general filial piety campaigns remain notable in public spaces in Shanghai and surrounding municipalities in Spring 2025.) This policy choice addressed the normative dissonance presented by these emerging practical problems with home-based eldercare, and significant capacity gaps in institutionalized care (Chou, 2011; Yan, 2021).

More recently, however, central and local governments have prioritized institutionalized eldercare as necessary and urgently needed (General Office of Shanghai Municipal Government, 2021; National Health Commission, 2019; State Council, 2021). In 2011, China's State Council initiated a policy favouring institutionalized eldercare development (2011). Institutional seniors care has since become an official priority, as mentioned above, especially in the country's four wealthiest regions: Beijing-Tianjin-Hebei, the Yangzi (or Changjiang) River Delta, the Pearl River Delta, and Sichuan-Chongqing (Forward-the Economist, 2021a). The institutional seniors care industry (finance, real estate, health production, equipment production and provision, and personnel training) has concentrated first on Shanghai (Forward-the Economist, 2021b).

China's institutional seniors care to date has taken three distinct ownership forms: publicly owned and operated (relatively rare); publicly built and minjian (‘non-profit’) operated; and privately owned and operated. Only minjian registrants can bid on contracts for publicly built facilities. However, private, for-profit companies can and do take up ‘minjian’ registration: the public/private divide is a poor guide to the presence or absence of the profit motive. Most institutional seniors care facilities therefore incorporate state-based and profit-making elements (Xu, 2022). Contracting out service provision in government-owned eldercare facilities cuts costs for government, and simultaneously stimulates a seniors care market. But the aspect of state involvement also deserves attention: without government-owned infrastructure, operating subsidies, and tax breaks, policymakers fear that private unprofitability would stunt that emerging market (Ma, 2020; 60 Plus Eldercare Service Platform, 2020).

The for-profit element – along with the government priority given to it – has direct implications for eldercare labour conditions. First, competitive pressures force firms to minimize labour costs. Second, and as a partial consequence of the first, middle-aged women internal migrants typically hold paid eldercare jobs. Despite eldercare's importance, their labour is devalued, both absolutely and relative to the labour of trained health professionals. Client-oriented government policy also makes this work invisible.

If we then consider the implications of for-profit care for its recipients, government support for the payments still rests on family-based means testing. Those who can afford to pay do so; those below the poverty line receive subsidies; and those unable to labour and who lack income or relatives (wubaohu) to provide care, receive free but basic services (Strauss and Xu, 2018, 2020; Xu, 2022).

Institutional seniors care is new in China, and has grown to its current state in stages. For instance, like other industrial and residential concerns during China's long construction boom, eldercare interests initially built large facilities in big-city suburbs: neighbouring farmland was relatively abundant, available, and cheap. But such distant sites often proved unpopular and underutilized, isolating seniors from family and former neighbours; officials also ultimately restricted urban sprawl as a general measure to save remaining farmland. Meanwhile, the crowded city centres obviously had little land for new construction. High vacancy rates hit the less desirable suburban facilities, alongside serious bed shortages in the limited facilities located in established districts.

At this point, local attention turned to re-purposing existing buildings in city centres. This shift has helped building holders profit from disused assets, while meeting seniors’ demands for facilities in familiar and more accessible surroundings. Such assets are as diverse as their current owners, and they are surprisingly common: abandoned factories, motels/hotels, downsized government and non-profit office buildings, clubhouses abandoned in anti-corruption campaigns, and kindergartens abandoned amidst demographic aging (Ministry of Civil Affairs, 2016; State Council, 2011; Tan, 2020; WeZooms, 2019).

To facilitate this re-purposing trend, the Ministry of Civil Affairs, together with ten other central government entities, issued an official Notice in 2016 encouraging the re-purposing of urban structures for eldercare. Those who re-purposed these buildings now enjoyed subsidies for construction and operation, as well as tax reductions and preferential utility policies (Guo, 2016; Ministry of Civil Affairs, 2016; Tan, 2020).

The published rationale that Civil Affairs offered for this form of support for eldercare is telling: ‘to promote the expansion and upgrading of residents’ consumption, promote the adjustment and upgrading of the industrial structure, accelerate the cultivation of new driving forces for development, and enhance economic resilience’ (Ministry of Civil Affairs, 2016; emphasis added). In other words, they intend eldercare in city centres to attract more seniors and to help the wider economy. Zhejiang Provincial government and Shanghai municipal government were the first in providing policy support for repurposing idle buildings for institutional eldercare (Shanghai Municipal Development & Reform Commission, 2024; Zhejiang Provincial Development & Reform Commission, 2024). Both policy documents include re-purposing idle commercial or office buildings, industrial or warehousing facilities, schools, low-level health clinics, apartments, idle buildings, training centres and wellness centres owned by government, state-owned enterprises and non-profit entities, and so on (Shanghai Municipal Development & Reform Commission, 2024; Zhejiang Provincial Development & Reform Commission, 2024). Although gauging the scale of re-purposing would reward more systematic study, documented examples are common (e.g. WeZooms, 2019).

Recent domestic investors in China's paid eldercare are diverse, most notably including real estate, insurance, pharmaceutical and IT interests. Insurance and pharmaceutical companies arguably have natural affinities to eldercare. But other investors might seem more surprising: they include the Capital Steel Plant (Shougang) and the conglomerate China Resources Holdings (Huarun), both State-Owned Enterprises or SOEs (Hua, 2020; Jia, 2014).

If we seek to explain SOE investment in eldercare, Maoist legacies likely play a clear role. SOEs still have developmental missions in both economic and social policy, a feature that dates from that period (Naughton, 2017). They are expected to support government social policy when instructed. However, SOEs today also have for-profit incentives built into their mandates. Under current conditions, such social policy obligations are easier for the SOEs to absorb, if they include for-profit elements. A final, crucial element of SOE involvement in eldercare concerns their considerable real estate holdings, many of which are legacy properties abandoned or underutilized in the aftermath of SOE reform beginning in the early 1990s; and later, during de-industrialization of Shanghai and the surrounding regions of Jiangsu province. Through eldercare, SOEs can mobilize profit from under-utilized or abandoned parts of the built environment that they hold.

Foreign investors have also entered Chinese eldercare, especially since 2014, when Chinese policy first encouraged them (Xinhua News Agency, 2014). To date, their primary interests have not lain on the real-estate side, but in asset-light, service-heavy care. They often serve wealthy Chinese seniors, or those with specialized needs, such as dementia (memory) care, and assistance with mobility, toileting, eating, etc. (DBS Asian Insights, 2017). But if such services are commonly their business models, they still need facilities in which to deliver them. Given different but complementary interests, such foreign firms often partner with local landholders, such as the SOEs described above.

To summarize, insurance and pharmaceutical companies have begun investing in institutional paid eldercare, much as observers might expect. Major for-profit industrial interests, SOEs, and foreign firms are also involved, bringing either substantial real-estate holdings or experience in specialized services. But a final category of new entrants in eldercare is big real estate (e.g. Vanke, Greentown, Poly, Sino-Ocean and Evergrande (now defaulted)) (Forward-the Economist, 2021a). To understand the latter's newfound eldercare interests, we need to discuss some wider trends in their fields.

Real estate and construction in coastal and urban China

Amidst massive geographic transfer of investment world-wide in both light and heavy industry, China's urban landscape has experienced successive phases of explosive and transformative growth over about 25 years, especially on the eastern and southern coasts. These booms ran from the 1990s to 2007–2008 (or at most, 2014–2015), and massively expanded both fixed capital and the consumption fund 1 in the built environment.

As we have already noted in describing early eldercare expansion, the first major growth wave in China's reform era stimulated rapid suburbanization of both residential and industrial facilities; this also entailed an increased separation of the latter two facility types from each other in space (e.g. Zhang et al., 2021). This vast suburbanization included ‘new town’ construction – the rapid, coordinated creation of whole city districts (Shen and Wu, 2017; Wu et al., 2007). In this period, the central government's material incentives to municipal officials and cadres under the position-responsibility system encouraged intense competition between municipalities for investment (Liu and Lin, 2015). So, too, did new tax-sharing arrangements formalized in the Budgetary Law of 1994. The new tax regime greatly enhanced local revenue generation through municipal authority over land-use sales to local construction and real-estate interests, a revenue stream that compensated for the central government appropriating previously important municipal revenues at the time (Saich, 2015). The change profoundly altered municipal motivations and behaviour. Local governments throughout China seized on their new land leverage to generate new revenue and simultaneously economic investment (Hsing, 2010; Lin, 2007; Wu et al., 2007). Because ultimate ownership of land remained overwhelmingly with government, the expropriations necessary for rapid growth were further encouraged. Key mega-events (e.g. the Beijing Olympics and Shanghai's World Expo) stimulated infrastructure construction still more. Land-leveraged urbanization powerfully stimulated local government debt-financing (Tsui, 2011; Zhang et al., 2022).

China's recent urban revolution has thus been anything but a passive or natural market outcome. Instead, an urbanizing ‘growth machine’ drew on local officials’ intense pursuit of economic growth, which in turn was tied tightly to revenue requirements and personal interests of officials (Lin and Yi, 2011; Sun and Huang, 2015), not merely profit for commercial and residential long-term leaseholders (Hsing, 2010; Wu and Piper, 2013; Zhou, 2017).

These complex spatial reorganizations have gradually shifted the largest coastal cities from centres of production to centres of consumption, as well as of financial and managerial oversight. Urban place-promotion and image-building now target foreign investment, professionals, and tourists, far more than masses of manufacturing workers to work and live in these cities (Wu et al., 2016).

But these booms were driven by more than elite decisions and state policy implementation. Real estate also became prominent in personal and institutional financial strategies, from extremely wealthy investors to middle-class ones, to peasants receiving in-kind compensation in urban real estate for the loss of farmland. Where Maoist thought had viewed housing as a de-commodified social necessity that urban work units (danwei) supplied as a right of employment, the central government now promoted real estate as a market-based growth engine. By 1998, with the creation of a housing market, developers began to compete fiercely for commercial land (Li, 2010; Wu, 2015; Wu et al., 2007). After the 1997 Asian financial crisis (and all the more for a period after 2007–2008 and 2014), individual investors also sidelined local stock markets, favouring real estate as the core basis for their wealth and retirement savings (Wu et al., 2007; Zhu, 2019). As many Chinese households lost state- or danwei-based pension guarantees, secondary real estate became crucial investments for a wide swath of income brackets, including expropriated peasants (Dong, 2020). For their part, institutional investors also increasingly emphasized debt-financed real estate and construction.

All this ultimately drove new construction well beyond apparent user demands, perhaps especially in third- and fourth-tier cities, but also in the major centres (Renmin Wang, 2016; Rogoff and Yang, 2022). Real estate activity slowed after 2013 (Hetzner, 2022). More generally, economic growth slowed after this point to about 5% per annum, another sign of an emerging ‘new normal’. The real estate glut continues, made worse by slowing population growth (Feng, 2024; Hawkins, 2024; Hoskins, 2025). Vacant units grew as a share of the total building stock. The default of real estate giant Evergrande and its delisting from the Hong Kong Stock Exchange on 25 August 2025 suggest some of the resulting fragility (Hoskins, 2025). In 2015, the central government issued a policy of selling off real estate holdings (No name, 2022; Renmin Wang, 2016). Reacting to the rapid urban sprawl on the coasts, central government policies also now aim at preserving the remaining agricultural land in growth regions, which had been some of the best in the country. All this shifted attention to upgrading the already-urban built environment in policy areas where new or different facilities were still needed (Chien, 2015; Wu et al., 2007: 140–54; Zhong et al., 2021).

As Wang (2021: 17) points out, since 2015, due to declining economic growth, intensified competition, and increased regulatory control over land prices and financing channels, many real estate companies, whether SOEs or otherwise, have begun to search for alternative strategies and aimed at diversification, departing from the previous model that depended heavily on for-sale real estate production.

The relative decline of real estate growth rates encouraged real-estate interests to explore other investments, examples of Chinese ‘capital switching’ not directly mediated by the state. Re-purposing real estate holdings for institutional eldercare is another expression of the interest in capital switching in a new strategic environment (Niu and Hu, 2017). This is the story we will emphasize further, below. But first we turn to the potential of ‘capital switching’ itself as a conceptual framework for understanding these times, and the stakes of re-purposing unused urban buildings for eldercare.

Harvey's ‘capital switching’ and re-purposing China's built environment

In his 1985 Urbanization of Capital, David Harvey reframed the city itself as a capitalist process, with particular emphasis on its evolving built environment. He also announced ‘capital switching’ and ‘switching crises’ as major theoretical contributions to the study of urbanization. The switching in question concerns capital flows between three capital circuits (see below) that both financial market signals and the state mediate (Harvey, 1985: 7).

Barriers to switching commonly develop, and can give rise to ‘switching crises’. Something more than sectoral or local crises, but something less than a general one, switching crises may develop between sectors of the economy or between geographic sectors (Harvey, 1985: 12–13).

Early roots of Harvey's insights include work by Walter Isard in 1942. Isard tracked investment moving during business downturns from industrial production to the built environment. Henri Lefebvre, notably in Urban Revolution, contributed to Harvey's thought more directly, including these particulars (Isard, 1942; Lefebvre, 2003/2003, 159–160; see Haila, 1991: 346). Both these earlier thinkers had observed that capital investment switches from industrial production over to the built environment (or should do), where and when over-accumulation develops and competitive re-investment opportunities dwindle in industrial production. Central to their exposition is the observation that industrial production returns profits on all or most of initial investments with every turnover cycle, and that the growth imperative of capitalist investment implies exponential growth in the absolute mass of those profits. Because of the constant pressure to reinvest a substantial portion of those profits at a competitive rate, such over-accumulation expresses itself with considerable urgency, especially in the face of diminishing returns. Central to their argument was that switching much of this mounting capital flow to fixed-capital investments would spread the imminent tsunami of returns on investment over much longer periods, temporarily abating the problem of finding profitable re-investments for the accumulating profits. Fixed-capital investments by definition depreciate and also provide returns on investment incrementally over many turnover periods.

Harvey systematized and extended this model of crisis and crisis management. First, following Lefebvre, he drew attention to the built environment as a combined subset of fixed capital (purchased for further for-profit production) and consumption fund (purchased for final consumption). Both categories, whether or not they are expressed in buildings and other urban infrastructure, are characterized in Marxist analysis by providing benefits to their owners over multiple turnover periods. This added complexity to the switching opportunities that Isard and Lefebvre observed: these two sub-categories may overlap, or re-purposing can switch one to the other without major physical changes (Harvey, 1985: 7). (For example, a disused Chinese factory (fixed capital) can be re-purposed as condominiums (consumption fund), or an 18th-century English cottage (consumption fund) can be re-purposed in whole or in part as a capitalist weaving workshop (fixed capital) (2013: 127–128; compare Harvey, 1982: 218, n. 5).)

Second, although Harvey describes switching crises as either geographic or ‘sectoral’ (1985: 13), he otherwise prefers the language of capital circuits to the language of sectors. (Lefebvre had alternated freely between ‘circuits’ and ‘sectors’ (e.g. 1970/2003: 159–160).) This avoids some terminological confusion, but also enriches the implications of switching.

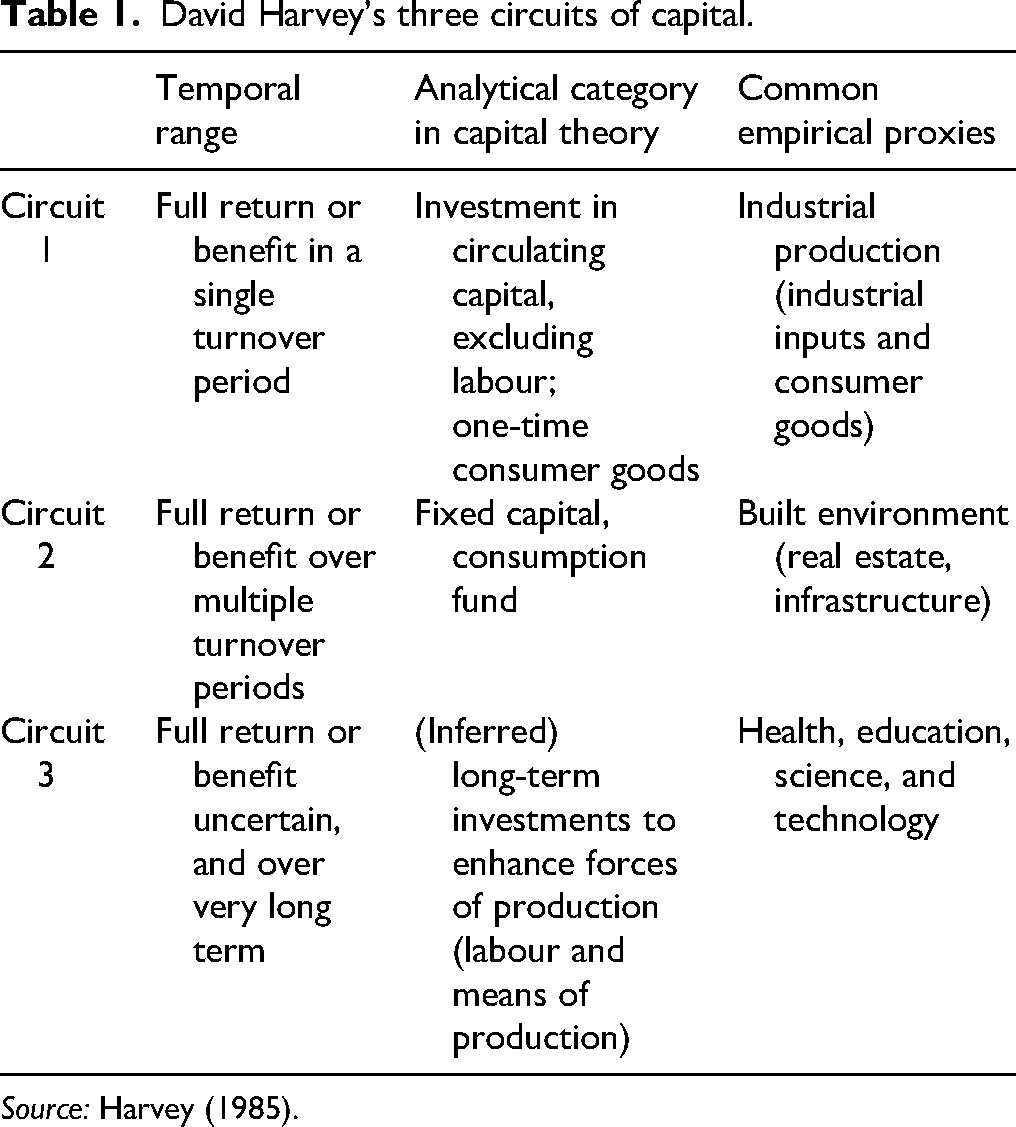

If switching happens between ‘circuits’, not ‘sectors’, how are the distinct circuits defined? (See Table 1) In 1985, Harvey firmly distinguishes the first two circuits by temporal scale (see Kutz, 2016: 1075). 2 The primary circuit covers a range of processes completed in a single ‘time period’ or turnover time. The secondary circuit is also defined temporally, but this time by depletion over multiple time-periods. Like the primary circuit, however, (Harvey, 1985: 5, Figure 2), the secondary circuit embraces both cycles of production (in its case, as fixed capital) and cycles of consumption (in its case, as consumption fund). (See especially the careful wording in Harvey, 1985: 6). These temporal definitions deserve emphasis, because so much reporting and testing of Harvey's consequent propositions revert essentially to sectoral definitions (Aalbers, 2011: 36; Beauregard, 1994: 716; King, 1989a: 446; see Christophers, 2014, and comments below).

Here our concern is to draw attention to the abstraction at work in the definitions of Harvey's circuits based on temporality, relative to a sectoral definition. That abstraction does pose an immediate problem for strictly empirical and positivist verification. For instance, hardly any real ‘industrial’ production process (often confused with Harvey's primary circuit) would fully expend all its inputs in a single turnover period (the definition of the primary circuit), since fixed capital (secondary circuit) plays a crucial role in most industry. However, the abstraction also undermines the significance of results that rest on an empiricism at odds with the ‘critical realism’ and ‘depth ontology’ on which Harvey's work rests (Marsh et al., 2018: 193–194; Pilon, 2021: 106).

We follow Christophers (2011, 2014) in emphasizing Harvey's Marxist method. Carefully sequenced and interwoven ‘real abstractions’ are central to Marxist analysis of concrete and complex situations (Harvey, 2010; Ollman, 2003: 59–112): one cannot set abstraction lightly aside in deciding whether Harvey's argument holds. Harvey's abstract circuits do seemingly cut across those for which Marx is best known: for instance, while the opening chapters of Marx's Capital, volume 1, are general read to be the most abstract, 2 Harvey draws on all three volumes in constructing the primary circuit (1985: 3). But reading Harvey's primary circuit as industrial production alone (for example) is arguably a case of misplaced concreteness.

In testing Harvey's arguments, those who read the primary circuit as industrial production (see above) tend also to read the secondary circuit primarily as the built environment. As Harvey makes clear in 1985 (6), the latter is certainly a subset of the former. And the secondary circuit (including but not limited to the built environment) intuitively seems more concrete and more complex than the primary circuit, consisting as it does of realized, relatively durable material objects.

However, Harvey notably abstracts the secondary circuit's definition from the built environment alone. Other fixed-capital or consumption-fund items are no less part of the secondary circuit, though they are ‘enclosed’ by processes of production (fixed capital) and consumption (consumption fund). Examples include a factory machine or a household appliance (1985: 6).

These abstractions in conceiving of circuits link the problems of capital switching to broader patterns in Marx's account of capital accumulation, such as the general technological dynamism of capital contributing to the quest for relative surplus value (Harvey, 2010: 211), or to the class antagonisms that arise from de-skilling by mechanization, and the resulting reinforcement of managerial control over the work process (Braverman, 1974).

We emphasize this temporal orientation to defining circuits, because Harvey (1985) added a tertiary circuit that he did not initially define in the same way, and elements of that circuit do resemble some features of eldercare. Relating eldercare to Harvey's framework depends on understanding it in relation to the interplay of all three circuits.

That said, the initial account of the tertiary sector poses a problem. We read that the tertiary circuit consists of investments in both science and technology (enhancing society's means of production), and health and educational services (enhancing society's labour power). Because Harvey proceeds in this way, simply listing subfields of social activity, we must infer an overall defining principle. For instance, direct returns to a capitalist investor seem less certain in the tertiary circuit than in the other two, even though both areas serve to enhance forces of production (that is, the labour force itself and technological inputs to production). Further, this circuit arguably depends disproportionately on state and other ‘non-economic’ actors, due to exceptionally long time horizons as well as the exceptionally uncertain returns.

We will return to the latent definitional boundaries of the tertiary circuit, below. Some of the above associations prove to be doubtful, given Harvey's overall framework. (For instance, Harvey names the state as a mediating force for all capital switching, alongside capital markets, regardless of the circuits involved (Harvey, 1985: 7).) Here, we observe simply that some of the inferred traits of the tertiary circuit may apply to eldercare, but that a direct and easy tie between them is premature.

Now that an initial account of Harvey's three circuits is in place, we can return to primary-to-secondary capital switching as a prescription for over-accumulation (the switching originally observed from industry to the built environment in Isard and Lefebvre). Harvey's temporal definition of these circuits is useful in explaining the effectiveness of this switching pattern. To repeat, a mass of surplus value (roughly, profit) grows rapidly on a compounding basis over multiple turnover times if it is repeatedly re-invested in the primary circuit. But re-investment opportunities at competitive rates of return will diminish there over time, and at an accelerating rate. Capital, if not reinvested at a competitive rate, necessarily risks a catastrophic loss of value. Diverting primary-circuit returns into investments in fixed capital (or the consumption fund) provides temporary respite: returns now trickle back into active circulation over many cycles, rather than surging back repeatedly and all at once, while still productively re-investing the capital (Harvey, 1985: 7, 10–11).

As mentioned above, this primary-to-secondary switching in Harvey's framework has provoked considerable discussion and testing in multiple contexts (e.g., Aalbers, 2011; Beauregard, 1994; Christophers, 2011; Haila, 1988, 1991; King, 1989a, 1989b, 1989c; Yin et al., 2018). In particular, after 2008, and still more after 2016, China has undertaken massive state-directed capital switching into the secondary circuit, most visibly in the built environment (Zhang et al., 2021).

But Harvey's framework opens up several switching possibilities, not just this one (e.g. Aalbers, 2011: 36–37). Problems also appear to be taking centre stage in contemporary China that are not examples of the primary-to-secondary pattern. For instance, scholars draw on Harvey's switching framework to analyze a possible crisis of over-investment in China′s built environment (as part of the secondary circuit) (e.g. Harvey, 2005: 141; Yin et al., 2018; see below). Such a crisis implies an excess of the very solutions that primary-to-secondary switching affords. Indeed, this danger is the very opposite of the first one observed: destructive under-accumulation due to investment in the built environment well beyond current needs.

In the same period, other countries also face the threat of destabilization near the end of a speculative construction boom. But the exceptional scale and proportion of China's boom – including construction policies intended to fend off impacts from world financial crises – have drawn considerable comment, including from Harvey (Zhang et al., 2021). What might be distinctive about that Chinese experience, particularly with respect to the distinctive drivers of secondary circuit investments?

First, as Yin et al. (2018) and others have observed, state direction in China plays an exceptionally important role in capital switching. Key features of state operations also differ from their Western equivalents. For instance, as outlined above, distinctive state-based logics have motivated local cadres to accelerate construction on a vast scale (and thereby, to accelerate the accumulation of secondary-circuit assets). Some have argued that local administrative incentives in China combine with distinctive legal and revenue institutions to form an ‘administrative territorial economy’ (Cartier, 2013; Liu and Lin, 2015).

For instance, one incentive for local officials to encourage secondary circuit investment surrounds privileged access to ‘administratively allocated land’ (AAL). These extensive land parcels arose from central planning during the Mao period. Central state agencies, as well as SOEs, had exceptional institutional privileges and responsibilities then; they therefore gained major land holdings for free or at nominal prices (Zhou, 2017; Zhu, 2019).

Since 1949, virtually all land in China has also been publicly owned. With marketization and privatization of land rights in 1987, however, much of it became available for private productive or residential use. The state retained ultimate title and an active right to revoke other titles, a right comparable to American eminent domain, but arguably far more potent. However, AALs held by SOEs and other remaining danwei were theoretically non-transferable. To surmount this barrier in the intense local competition for investment capital and tax revenues, many local governments, with support from local construction interests, made AALs subject to special informal ‘land-development rights’. Their purpose was to ‘unlock land supply for redevelopment while accommodating the existing institution of the danwei's land use right’. Specifically, ‘the land development right is what a sitting danwei can claim, based on its land use right, to redevelop the site occupied by itself and, if necessary, neighbouring sites occupied by other danwei land users or residents’ (Zhu, 2019: 102).

Recently, mandatory guidance from higher levels of government has tightened these leasing rules. But for a time, these innovations allowed SOEs and other danwei to transfer or lease their land rights, if they built on the land first. Much construction ensued, with an eye to quick transfer. A portion of these properties did sell, but many remained in SOE hands, disused or vacant (Zhu, 2019: 117).

At this point in the process, we re-connect to the eldercare policy domain. Some SOEs subsequently invested in eldercare projects, offering lands of this sort, just as other real estate markets tightened up, partly in the rush mentioned above to protect remaining farmland (Chinese Financial Information Network, 2019). Integrated into fee-for-service eldercare, re-purposed facilities could finally generate revenue for the SOE holding AAL rights, facilitating eldercare without being sold.

Such state-based dynamics have not been the only drivers of secondary-circuit over-investment in China. Others include declining conditions for profit in the primary circuit. Risks of obsolescence and speculative busts also threaten invested capital more, the longer fixed-capital investments (or consumption fund purchases) endure. Sometimes these dangers intervene on a scale that threatens overall capitalist accumulation. Just such dangers appear to be mounting in China.

In some situations, like the earlier AAL crisis, uncompleted construction projects or otherwise unsaleable holdings mean that such risks to expected profits from fixed capital construction affect primarily the original builders and investors. In other situations, direct users or speculators have bought the real estate, in which case, they now bear the risk. For the original investors, a turnover cycle has completed after such a sale; someone else linked to a different industry holds the value embedded in the built environment over multiple turnovers. But the wider macro-economic problem – sudden devalorization – remains.

Harvey's capital switching framework clarifies the stakes of over-investment in the secondary circuit, not only in the primary circuit. But what of the tertiary circuit? Returns on science, technology, health, and medical care are commonly viewed as long-term and uncertain. In that sense, the tertiary circuit extends the temporal features, together with the virtues and dangers, of the secondary circuit (see Harvey, 1985: 10–11). Since investing in fixed capital and the consumption fund (secondary circuit) implies competitive technological innovations (tertiary circuit), capital dynamics affecting the two circuits are also likely to intertwine. All this suggests that capital switching into the tertiary circuit would only intensify the problems arising from over-investment in the secondary circuit: both would tighten the vise on primary circuit accumulation.

We can now turn to the place of capital switching in eldercare. Where does the latter belong in relation to Harvey's three circuits? We have already mentioned, above, that eldercare appears to resemble some sectors that Harvey clearly includes in the third circuit. If we think of those sectors, eldercare might seem to be comparable to health and education. As work process, for instance, all three could be readily placed in the ‘care economy’, with all the associated implications for emotional labour, and so on (Yeates, 2012). Is the tertiary circuit therefore the way to situate eldercare in the capital switching debate?

If we consider the overlapping category of ‘social reproduction’ as a way of thinking about what belongs in the tertiary circuit, the link to eldercare is less clear. Healthcare and education clearly contribute to the capacities of the labour force, mirroring the contribution of the science-and-technology side of the tertiary circuit in enhancing means of production. Not so for eldercare, however, at least not directly: no one expects most of the elderly who need this care to return to work.

We pursue this point in more detail below. But to summarize, if one thinks of the definitional limits of the tertiary circuit in terms of functions analogous to the tertiary-circuit sectors that Harvey does mention, it is not clear that eldercare belongs, even though alternative analytical frameworks (such as the ‘care economy’) suggest the opposite. If, instead, one thinks of the tertiary circuit in terms of a length and uncertainty of returns on investment that exceed those of the secondary circuit, we see that capital gains little overall from a turn to the tertiary circuit, if capital is already over-invested in the secondary one. In China's current circumstances, including eldercare in the tertiary circuit, if the latter circuit is defined in such ‘temporal’ terms, would suggest that the official prioritization of eldercare is being driven primarily by social imperatives, and that it risks deepening the emerging problem of over-accumulation in long-term and uncertain investments.

The problem is that government policy documents do not reliably argue the point in this way. Instead, Chinese government policy documents regularly invoke positive wider implications of eldercare, alongside its social policy dimensions. Beijing has elevated seniors care to a national priority, in order to address demographic aging and the growing impracticality of family-based eldercare solutions. But it also officially considers eldercare to be an important element in realizing macro-economic priorities: stimulating consumption; creating jobs; and releasing labour power from unpaid eldercare to paid labour (Chinese Financial Information Network, 2019). Can we add to these macro-economic benefits a rational basis for the alleviation of an emerging over-investment in the secondary circuit? To explain our tentative answer in the affirmative, we turn now to the concepts of ‘bundled commodities’ and ‘social reproduction’.

Interpreting eldercare as ‘bundled commodities’ in relation to social reproduction

We have just considered whether institutional eldercare might be tertiary-circuit investment, based on what it shares with health and education. Another possibility, however, is that eldercare operates as a combination of secondary and primary circuit investments, with primary investments ‘in the lead’. This could be what makes it significant for capital-switching in an era of over-accumulation in the secondary circuit.

To consider this possibility, we return to the comparison of eldercare with the sectors that Harvey includes in the tertiary sector. But instead of considering health and education as parts of the ‘care economy’, we deploy the alternative framework of ‘social reproductive’ functions. Harvey's treatment of social reproduction in 1985 appears to be a narrow one, emphasizing the economic functionality of reproducing labour power. By contrast, many feminist political economy scholars today identify three components of social reproduction: reproduction of humans at the level of biology, of labor-power, and of wider social relations (Laslett and Brenner, 1989).

As a work process, eldercare shares key features with the health and education activities that Harvey links to the tertiary circuit: eldercare is (like them) readily identifiable as ‘care’ work, and household-based, non-profit, and unpaid or underpaid labours are likewise important aspects of it. Even if waged, these are also labours that stand removed from waged, for-profit factory- or office-based labour. Though Harvey does not name it, including eldercare in the tertiary circuit, alongside health and education, might seem obvious.

If we think of social reproduction simply in relationship to reproducing the working class, paid eldercare does have effects on labour power in capitalist society, though the effects are mostly indirect: as Chinese policy documents observe (see above), it creates paid work for caregivers (albeit often under adverse and degrading conditions), and also frees up unpaid caregivers for other roles, including roles in the waged economy. However, it remains the case that few expect eldercare recipients to return to the paid workforce, as they might expect children and many adults of working age after health or education services end.

If this distinction from health and education proves to be important, eldercare's place in the tertiary circuit seems less certain. Investors who shift capital to eldercare may not be shifting it to the tertiary circuit. And if we return to a definition based on long-term and uncertain returns, following through on Harvey's approach to the primary and secondary circuit, this could link the tertiary circuit's long-term and distanced relations to accumulation to the indirect and general contributions of eldercare to capitalist society.

But in another sense, it may be more pertinent to focus attention on the daily services at the centre of for-profit eldercare, which are typically paid for in regular, short-term instalments. Perhaps, in this view, eldercare is significant for the wider economy, because as a for-profit, waged service, much of the total outlay operates in the primary circuit.

Of course, this is a partial return to the primary circuit: as residential care, institutional eldercare necessarily draws on the built environment, and thus the secondary circuit as well. But this occurs in a specific arrangement, by which the relevant buildings and other infrastructure are bundled with a series of personal services that are provided daily, and by which the bundle as a whole is paid for on a schedule that more nearly reflects the latter than the former. 3 We have also seen that the buildings and the services are delivered by different interests. Finally, for-profit interests are usually present (to varying degrees) on the side of both the facilities and the services. The idea that eldercare unites useful commodities from two discrete circuits leads into a final conceptual discussion, with specific reference to what eldercare represents to the holder of disused property. But it also bears on what eldercare represents to a whole economy, if that economy is confronting over-investment in the secondary circuit.

‘Bundled commodities’ 4 are produced separate from one another, but they are brought together in a bundle for combined marketing and sale (Adams and Yellen, 1976). One implication of this is the possibility of limited but valued differentiations of a single set of related products: a single marketing strategy can fully exploit a range of consumer incomes and tastes. This first aspect of bundled commodities speaks directly to marketing realities in unequal neoliberal societies worldwide. In this respect, it certainly speaks to Chinese eldercare, as it does to much eldercare elsewhere. In China, eldercare residents can opt for a range of services based on taste, need, and income, while still being co-resident in the same facility. Examples include variations in meal quality, room or canteen service, differentiated medical services (memory care, etc.), and differentiated personal services for mobility, feeding, bathing, toileting, or dressing.

This variation extends to the residential portion of eldercare. The construction interest Vanke, for example, has developed a multi-line eldercare business since 2016. Each line delivers eldercare facilities differently – community/shequ seniors centres, institutional seniors care, and continuous care retirement centres (Sohu, 2018). The production of the buildings is less differentiated than the other, notional commodities bundled with them, and it is the latter commodities that alter the basis for a client's access to the buildings. The differentiated access targets clients with different needs and means.

This business plan has become central to Vanke's future in an over-supplied real estate market (Sohu, 2018). Vanke is not alone in this (Wang, 2021: 17–18). By adding services to the bundle, alongside real estate they now hold rather than sell, real estate companies diversify their profit-making. Eldercare is considered to be a ‘sunrise’ industry by both government and business, where all other construction seems headed towards dusk (Chinese Financial Information Network, 2019).

In this sense, the wider feminist conception of social reproduction appears to be operating in this dimension of the eldercare ‘bundle’: the latter reproduces the social stratifications that mark other aspects of contemporary China. But the concept of bundled commodities offers something more significant to the central discussion here. The concept reveals eldercare as a combination of commodities produced separately from different circuits of capital, and then bundled together for sale on terms more in keeping with the primary circuit than with the secondary or tertiary. 5 The result enhances the willingness of distinct capitals that produce or hold different component commodities to invest in eldercare. While the elements that come from the secondary circuit (disused properties, etc.) are essential to residential care, the daily and intermittent for-profit services at the core of that care (consistent with the temporality of the primary circuit) are essential to the secondary circuit elements retaining any value at all. The regular returns for the bundle as a whole, based on the logic of services, are what allow investment in the re-purposed properties to release profit back to the wider economy.

Conclusion

This article has investigated convergent demands for institutional eldercare in Chinese society and for re-purposing a large portfolio of disused properties in coastal cities. These properties are largely consequence of institutionalized incentives to over-invest in the built environment. The paper has also considered less widely explored dimensions of capital-switching theory, systematized by David Harvey in 1985 and deployed in both Chinese and Western settings.

Despite difficulties in demonstrating the principle if statistically generated sectors are taken as indicators of Harvey's circuits, these applications clearly suggest reasons to think that construction and real estate can serve as a sink for capital, in the face of over-accumulation in the primary circuit. However, Harvey's framework shows that this primary-to-secondary switching is not the only possibility. It also suggests why over-investment in the secondary circuit could create difficulties of its own, choking off returns in the short-term and thus threatening accumulation. Analysts of such problems in China have drawn on Harvey to make both points. Harvey's insistence that one analyze circuits in terms of temporal differences, as these play out in production and consumption, is crucial to explaining why capital switching works and why particular switching crises arise.

Beyond the growing imperative to expand institutional eldercare to accommodate demographic and social change in China, eldercare has proven to be an attractive investment target for a wide variety of interests that face over-investment in the urban built environment. Why this is so requires conceptual work. We have suggested tentatively that bundled commodity theory could supplement capital-switching analysis in the Marxist tradition. Eldercare itself merits careful analysis in this process, and its differing relationships to the ‘social reproduction’ and the ‘care economy’ frameworks helped here to establish principles for relating eldercare to Harvey's framework. Other industries that make use of re-purposed buildings may merit investigation for similar macro-economic functions (Zhou, 2017).

Integrating these comparisons with Harvey's own emphasis on the temporal distinctions between different capital circuits, perhaps eldercare serves the problem of over-investment in the secondary circuit, insofar as it links returns from parts of the built environment to the daily personal and medical services repeatedly provided on a regular payment plan. In short, eldercare is of macro-economic significance, because it consists of bundled commodities, in part in the primary circuit, and in part in the secondary circuit. As a consequence, disused portions of the built environment become available again as a portion of the total outlay for eldercare provision, and the value embedded in those buildings become available again (or for the first time) for capital accumulation, through the regular, shorter-term payments that resemble patterns in the primary circuit. As early signs show real estate investment trusts beginning to play a role in the re-purposing of buildings in China, including for eldercare facilities, their imperative to minimize re-investment at the expense of returns to investors may add strength to this argument (National Development and Reform Commission, 2024).

David Harvey's three circuits of capital.

Source: Harvey (1985).

Footnotes

Ethics approval

The Board of Record [University of Victoria] has reviewed and approved the empirical study on which this article is based in accordance with the requirements of the Tri-Council policy statements: Ethical Conduct for Research Involving Humans (TCPS2, 2014). Board Record Approval Reference: BC16-028.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Social Sciences and Humanities Research Council of Canada (Grant No. 435-2016-0872).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.