Abstract

This article provides a technical assessment of the February 2022 Treasury Department report titled “Competition in the Markets for Beer, Wine, and Spirits” as it relates to the overall beer industry. Furthermore, this article investigates the various governmental departments and regulations that govern the production, distribution, and selling of beer within the U.S. Departments and regulations at both the federal and state level are discussed and the impacts that each have on the (lack-of) competition within the beer industry are outlined. The article also offers a call-to-action for policymakers and academics, respectively, to ensure the future of the beer industry is fairer and more competitive than it has been in the past.

Introduction

Executive Order 14036 “Promoting competition in the American economy” was signed on July 9, 2021, by President Joseph R. Biden Jr. The stated goal of this executive order “is to reduce the trend of corporate consolidation, increase competition, and deliver concrete benefits to America’s consumers, workers, and small businesses” (Exec. Order No. 14036, 2021). The administration suggests that the potential benefits include: more choices, better service, and lower prices for consumers through a more competitive market, along with fairer opportunities for small businesses and entrepreneurs to compete (Exec. Order No. 14036, 2021). In particular, sections 5(j) and 5(k) of the order focused on protecting the beer, wine, and spirits industries while improving accessibility for smaller, independent, and new operators. As part of the directive, the president ordered the treasury department to submit a report on the current structure and competitive conditions within the beverage alcohol industry, including an assessment of potential barriers to entry and threats to competition (Exec. Order No. 14036, 2021). In February of 2022, the treasury department submitted its 64-page report titled “Competition in the Markets for Beer, Wine, and Spirits” (Treasury Department, 2022). The treasury report indicates two significant trends that have been prevalent within the beverage alcohol industry recently, (a) significant growth in the number of small, local, and craft alcoholic beverage producers and (b) consolidation, specifically within distribution and/or retail for beer, wine, and spirits, as well as within production for beer. Along with these trends, the report outlines other areas of concern, including current laws around labeling, classification of beverages, bottle size restrictions, complex application requirements for a permit to produce alcohol, taxation of different alcoholic beverages, and lacking direct-to-consumer sales opportunities (Treasury Department, 2022). Although the report and the overall focus from the administration highlight areas of concern for beer, wine, and spirits, this article will focus solely on the beer industry, given the country’s history of brewing and consumption of beer.

It should be noted that these areas of concern are not new to the beer industry and have been discussed in previous research as well as by industry organizations. The authors also outlined the importance of product differentiation and innovation for breweries and wineries to ensure a competitive marketplace. Consolidation in the beer industry as evidenced by the global market share of the top 10 producers was recently addressed. AB-Inbev, the global leader in the beer category, held 26.8% of the beer market and the top 10 producers accounted for 67.0% of the market (Jernigan & Ross, 2020). Within the United States, AB-Inbev (42.4%) and Molson Coors (22.4%) combined account for 65% of the national beer market as measured by revenue, even though they are only 2 of the over 8,000 breweries operating in the country as of 2020 (Wood, 2021). Considering the findings of the treasury report, recent research on the state of the beer industry, and commentary from industry organizations, this article aims to highlight the major areas of concern and provide potential solutions and suggestions for future research projects to ensure a competitive beer industry. The following sections provide background information on the U.S. beer industry, federal departments/regulations, state regulations, and the negative influences of the various regulations. Finally, a future research agenda will be provided.

Background of the Beer Industry in the United States

At the end of 2021, there were over 9,200 breweries operating in the United States (Brewers Association, n.d.), generating over US$30 billion in revenue and employing over 79,000 individuals (Wood, 2021). Despite the sheer number of beer producers in the country, the brewing industry was recently found to be the ninth most concentrated manufacturing industry (Pease, 2021). However, as Pease (2021) points out, these data do not show the entire picture as most of that concentration is held by just two firms (i.e., AB-Inbev and Molson Coors) and one major beer importer (i.e., Constellation Brands) does not appear in the brewery sector in U.S. Census data as they are not a U.S. manufacturer. In 2020, the top four firms (i.e., AB-Inbev, Molson Coors, Constellation Brands, and Mark Anthony Brands) held 75.5% of the U.S. beer market share (Pease, 2021). In contrast, craft-brewed beer was estimated to account for 16.6% of the combined US$30.3 billion dollars of industry revenue in 2021 (Wood, 2021).

Regarding production levels, Pease (2021) indicates that 1% of all breweries make up 88% of U.S. beer production, while 77% of breweries make up <1% of total production. Even as craft producers have been able to steal away market share from the larger producers, much of their sales growth has relied heavily on their ability to sell directly to consumers via taprooms (i.e., own-premise sales). Taproom sales allow brewers to sell their beer at retail prices directly to consumers, equating to more than a 300% profit margin over the traditional wholesale process (Probrewer, 2016). Furthermore, within the traditional three-tiered system (outlined in detail in the next section), small brewers often suffer due to consolidation at the wholesale level.

According to the National Beer Wholesalers Association, as of 2020, there were 3,000 beer distributors in the United States (National Beer Wholesalers Association, 2020). However, Pease (2021) notes that, in 2017, the top 50 beer wholesalers accounted for 46.8% of the market share. Furthermore, only two effective beer wholesalers serve most territories in the United States. As such, when it comes to beer distribution across the country, most markets—both brewers and retailers are stuck dealing with a duopoly (Pease, 2021). More specifically, the supposed independent wholesalers are typically associated with AB-Inbev or Molson Coors because they sell a large amount of either, and other brewers effectively must rely on one or the other to get their beers to market (Treasury Department, 2022). Relatedly, some states allow for a two-tiered system to exist wherein a brewer is allowed to own a wholesaler or to distribute their own beer without restrictions. In these instances, the wholesaler is colloquially referred to as a “wholly-owned distributor” (Pease, 2021; Treasury Department, 2022). Along with wholly owned distributors, there has also been a heavy amount of consolidation at the wholesaling level (Diment, 2021). For example, one investment company currently owns multiple wholesalers across the state of California, accounting for roughly half of the beer market in the state in terms of sales, along with owning additional facilities in six other states (Pease, 2021; Treasury Department, 2022).

Although the beer industry overall suffered significant losses due to COVID-19, these losses were not felt uniformly across the industry. In 2020, many small-craft breweries suffered more significant losses due to the inability to serve guests directly in their taprooms (i.e., own-premise), as well as the loss of on-premise sales at restaurants and bars. Relatedly, smaller brewers who did not have strong off-premise distribution suffered from the inability to reach consumers in the same ways that larger brewers could (Lombardo, 2021; Wood, 2021). In total, 600 small breweries were permanently closed due to COVID-19 (John Dunham & Associates, 2021). Overall, the high level of concentration and the increasing consolidation that exists at the brewing and wholesaling levels have been major concerns for many in the beer industry for more than a decade, as many of the issues highlighted by the Treasury Department (2022) were also outlined by Ascher (2012). However, the impacts of the COVID-19 pandemic further stressed these issues and the struggles that many smaller craft brewers face when trying to get their products to consumers. The following section provides further background on federal departments, regulations (i.e., taxation, labeling, marketing, three-tier system, mergers and acquisitions, etc.), the negative effects on craft brewers, and the overall competitive nature of the industry. This is followed by a section outlining various state regulations (i.e., open, control, franchise, and post and hold states) and the impacts of those regulations on competition within the industry.

Federal Departments/Regulations and the Impacts Thereof

Federal Departments/Regulations

Beer, along with wine and spirits, is a heavily regulated product at the federal, state, and often local levels; every aspect from production, distribution, and sales is regulated. At the federal level, there are four different agencies with jurisdiction over beverage alcohol markets, including (a) the Treasury’s Alcohol and Tobacco Tax and Trade Bureau (TTB), (b) the Department of Justice (DOJ), (c) the Federal Trade Commission (FTC), and (d) the Food and Drug Administration (FDA) (Treasury Department, 2022). The Treasury Department’s TTB collects federal excise taxes on alcohol, tobacco, firearms, and ammunition and enforces federal alcohol and tobacco permitting, labeling, and marketing requirements to protect consumers. Much of the work done by the Treasury regarding alcohol is connected to regulating market competition. It is tied to the administration of the FAA Act’s exclusive outlet, tied house, consignment sale, and commercial bribery provisions, which were put in place to restrict vertical integration and exclusionary practices within the alcohol industry (Treasury Department, 2022). Similarly, the tax laws administered by the Treasury and the FAA Act’s provisions on labeling and advertising also affect competition.

Within the DOJ, the Antitrust Division enforces the Sherman Antitrust Act and the Clayton Act. The Sherman Act bans all contracts, combinations, and conspiracies that unreasonably restrain interstate and foreign trade, along with making it illegal to monopolize any part of interstate commerce. The Clayton Act prohibits mergers and acquisitions wherein the effect is aimed at substantially decreasing competition or to tend to create a monopoly (Treasury Department, 2022). Relatedly, the FTC enforces the Clayton Act and the FTC Act, which gives the Commission the authority to block unfair methods of competition, including those that violate the Sherman Act, and any unfair or deceptive practices (Treasury Department, 2022). The FDA implements regulations related to food. As such, beer is subject to the Food, Drug, and Cosmetic Act’s adulteration and misbranding provisions and certain labeling requirements on menus within restaurants and similar places of business (Treasury Department, 2022). The following section outlines the impacts and failures of federal regulations as they pertain to the specific agencies discussed above.

Impacts (Failures) of Federal Regulations

TTB Regulations

In 2020, the TTB collected roughly US$3.4 billion in federal excise taxes on beer (TTB, 2020); however, not all breweries were taxed at the same rate due to the Craft Beverage Modernization Act (CBMA) that was passed in 2017. In most cases, these taxes—no matter the rate—were passed along to consumers in the form of price increases (Nelson & Moran, 2019). Before the CBMA was instituted, brewers were taxed US$7.00 per barrel on up to 60,000 barrels so long as they brewed under 2 million barrels a year—giving smaller brewers a competitive tax advantage—beginning in 2018, the tax rate was cut to US$3.50 per barrel for the first 60,000 barrels. However, this US$3.50 rate is available to all brewers on the first 60,000 barrels of beer, regardless of their production level; as such, most of the tax cuts are enjoyed by large domestic and foreign brewers (Looney, 2018). Further tax cuts were included in the legislation that specifically affected larger brewers. In total, AB-Inbev and Molson Coors each received approximately US$12 million in tax breaks (Looney, 2018). Relatedly, foreign brewers can now benefit from these lower rates by representing their products as “craft,” without a governing body to oversee production in foreign countries, U.S. Customs would simply have to trust the importer (Looney, 2018; Treasury Department, 2022). Beyond taxes paid by brewers, there are additional issues related to tax-related reporting requirements. Currently, the TTB tax returns and operational reports require brewers to submit information that is not used for tax administration purposes. Similarly, there is currently no regulation or form requiring brewers to submit information necessary to confirm they are paying the correct tax rates under the CBMA (Treasury Department, 2022).

The TTB also deals directly with the FAA Act and the six categories of unfair competition and unlawful practices outlined. Each of these practices and how they are or are not enforced have direct influences on competition in the beer industry. The exclusive outlet provision bans brewers or wholesalers from “forcing” through agreement or otherwise a retailer to purchase alcohol from that producer or wholesaler to the exclusion of alcohol sold by others. Brewers and wholesalers are banned from “inducing” a retailer to purchase their alcohol to the exclusion of others through certain specified means, such as partial ownership, offering credit, and repaying loans under the tied-house provision. The commercial bribery provision bans brewers and wholesalers from using money or other items of value to induce a retailer or wholesaler to buy its products to the exclusion of others. Each of these three practices requires proof that the practice resulted in “the exclusion in whole or in part” of products offered by others, and as of 1995, no court has assessed or interpreted the legislation (Treasury Department, 2022). The only area to be tested since 1995 is that of slotting fees or what is often called “pay to play” schemes, wherein a retailer is paid for prominently stocking and displaying products. Slotting fees are considered a threat via the tied-house provision. Relatedly, category management—wherein a wholesaler is involved in decisions for how to stock and display products for a retailer and tying arrangements—wherein a wholesaler requires a retailer to buy its less desired brands as a condition for buying its more desirable brands, are both also considered to be violations of the tied-house provision. However, even as complaints have been raised associated with both category management and tying arrangements, the TTB has not brought any action in either area (importantly, FTC and DOJ have also not brought action regarding tying arrangements). The fourth area prohibits consignment sales or the selling of alcoholic products to a retailer who is not required to pay for the product until it is sold. Interestingly, TTB has investigated some small wineries regarding consignment sales in 2017 and 2018; however, it has been suggested that consignment sales should be considered for small producers as it provides an aid to the producer while lessening the risk for a retailer to carry an unknown product (Treasury Department, 2022).

In general, these four provisions, when carried out against smaller producers, can be detrimental. On the contrary, when carried out against larger producers, the penalties effectively amount to a slap on the wrist. However, it is not just these provisions that can often be burdensome for small brewers, as the TTB also oversees alcoholic beverage labeling and permitting for brewers before they are able to sell their beer. Regarding labeling and permitting, the two biggest issues currently impacting the industry are the length of time it takes to get (a) labels and (2b permits approved. In 2021, TTB received 195,706 applications for label approval, and even as TTB has been able to cut approval time down from 27 days in 2016 to 6 days in 2021, there are still issues when minor changes are made that often lead to a complete resubmission (Treasury Department, 2022). Though not currently a concern to competition, there are also multiple proposals that the TTB has put forth that could unnecessarily burden small brewers, mainly regarding labeling (i.e., ingredient labeling, allergen labeling, serving facts labeling).

DOJ Regulations

As noted previously, consolidation within the beer industry has been a major concern for many parties, and the DOJ has had to get involved with numerous mergers and acquisitions in recent years, starting with the 2008 merger of SABMiller and Molson Coors (Miller et al., 2021). More recently, AB-Inbev sought to acquire Grupo Modelo, a Mexican-based brewing company that ranked third highest in beer sold within the United States (Ascher, 2012). Although the deal inevitably went through, AB-Inbev was required to divest Grupo Modelo’s entire U.S.-based business and a brewery in Mexico to Constellation Brands, Inc. (Treasury Department, 2022). The specifications of the deal were supposed to keep the wholesale distribution operations outside of AB-Inbev’s network (Ascher, 2012) and allow Constellation to compete on production and pricing (Treasury Department, 2022). According to Constellation’s most recent 10-K report for the fiscal year that ended February 28, 2022, they have experienced tremendous growth and success in the beer market (Constellation Brands, Inc., 2022). However, given the effective distribution duopoly in most states which is outlined in greater detail in the next section, Constellation-owned beers are typically distributed by AB-Inbev wholesalers, which still provides AB-Inbev a relative competitive advantage in the marketplace. Two years after the Grupo Modelo acquisition, the “ultimate” merger was proposed as AB-Inbev attempted to acquire SABMiller. In this instance, the DOJ required AB-Inbev to divest SABMiller’s entire U.S. business to Molson Coors. Along with this, the DOJ prohibited AB-Inbev from engaging in certain anticompetitive practices specifically geared toward the distribution of products (Miller et al., 2021; Treasury Department, 2022).

Regarding each of the mergers and acquisitions outlined above, there is a consistent argument made by the companies suggesting that the transactions will create substantial cost savings for the companies, which will, in turn, benefit consumers (American Antitrust Institute, 2012). However, as pointed out by numerous sources, prices of beer directly following mergers have increased and are not in line with might be expected per the Consumer Price Index (American Antitrust Institute, 2012; Ascher, 2012; Miller et al., 2021.; Miller & Weinberg, 2017). These price increases have not only hurt consumers by forcing them to pay artificially inflated prices but they have also come at the detriment of smaller-local brewers by shrinking already consolidated distribution channels and creating further price competition (Ascher, 2012; Treasury Department, 2022). Furthermore, there have been numerous acquisitions since 2011 wherein one of the major producers has purchased smaller craft breweries. These acquisitions are of major concern to other small-craft brewers who fear that the larger players will be able to further control distribution channels and price points and might drop the prices of their craft portfolio, forcing other smaller operators to follow suit (Ascher, 2012; Treasury Department, 2022). These concerns are not unfounded either, as AB-Inbev and MillerCoors engage in follow-the-leader type pricing schemes (Miller et al., 2021). In most local markets, these schemes are led by AB-Inbev who announces price increases (or decreases—very rarely) ahead of time. MillerCoors follows suit, thus, forcing other competitors to decide which direction to go (Miller et al., 2021; Treasury Department, 2022). Though competitors could choose to keep prices or even lower them, as Ascher (2012) noted, discounting in the beer industry is not a good long-term strategy as it can often cheapen the brand’s image. Often, craft brewers have not hit the economies of scale that larger producers have; therefore, discounting is simply not an option.

FTC Regulations

Concerning the FTC, although the commission pays close attention to the potential harms that could occur if a large company, particularly within the distribution sector, engaged in anticompetitive behavior, they have not brought any cases in this area in multiple decades (Treasury Department, 2022). This is particularly concerning when considering the level of consolidation that has occurred at the distribution and wholesaling levels. The following section provides greater detail on distribution within the states. Still, a major concern that the FTC should consider is that larger distributors have bought out many medium distributors, and numerous small distributors have simply stopped operating. This has not only caused problems within the distribution level but it has also negatively affected small-craft brewers looking to get their products to market (Ascher, 2012; Pease, 2021).

FDA Regulations

Currently, there are no major concerns regarding the FDA, though if certain proposals by the TTB go through regarding labeling, this could change.

State Regulations and the Impacts Thereof

State Regulations

Since the end of Prohibition in 1933, the states have been responsible for regulating the production, distribution, importation, and sales of alcoholic beverages (Norris et al., 2022; Treasury Department, 2022). Most states have adopted some version of the three-tiered system for alcohol distribution, where producers are required to sell to wholesalers, who then sell to retailers, then retailers sell to consumers, and where no business operating in one tier may hold a significant ownership stake in another tier (Norris et al., 2022; Pease, 2021; Tamayo, 2009; Treasury Department, 2022). However, in some states, producers have been allowed to sell directly to consumers via taprooms or tasting rooms (i.e., own-premise sales). Other states also allow some producers to self-distribute directly to retailers within the state, and even fewer allow for direct-to-consumer shipping across state lines (McCormick, 2015; Pease, 2021; Treasury Department, 2022). However, in states that do allow brewers to sell directly to retailers, state laws often impose major constraints, which include capping the volume a brewer can sell to retailers, restricting a brewer from distributing beers of other brewers, or limiting self-distribution rights to in-state breweries only (Pease, 2021). Regarding direct-to-consumer shipping of beer across state lines, only 11 states and the District of Columbia currently allow breweries to ship beer directly to consumers (Pease, 2021).

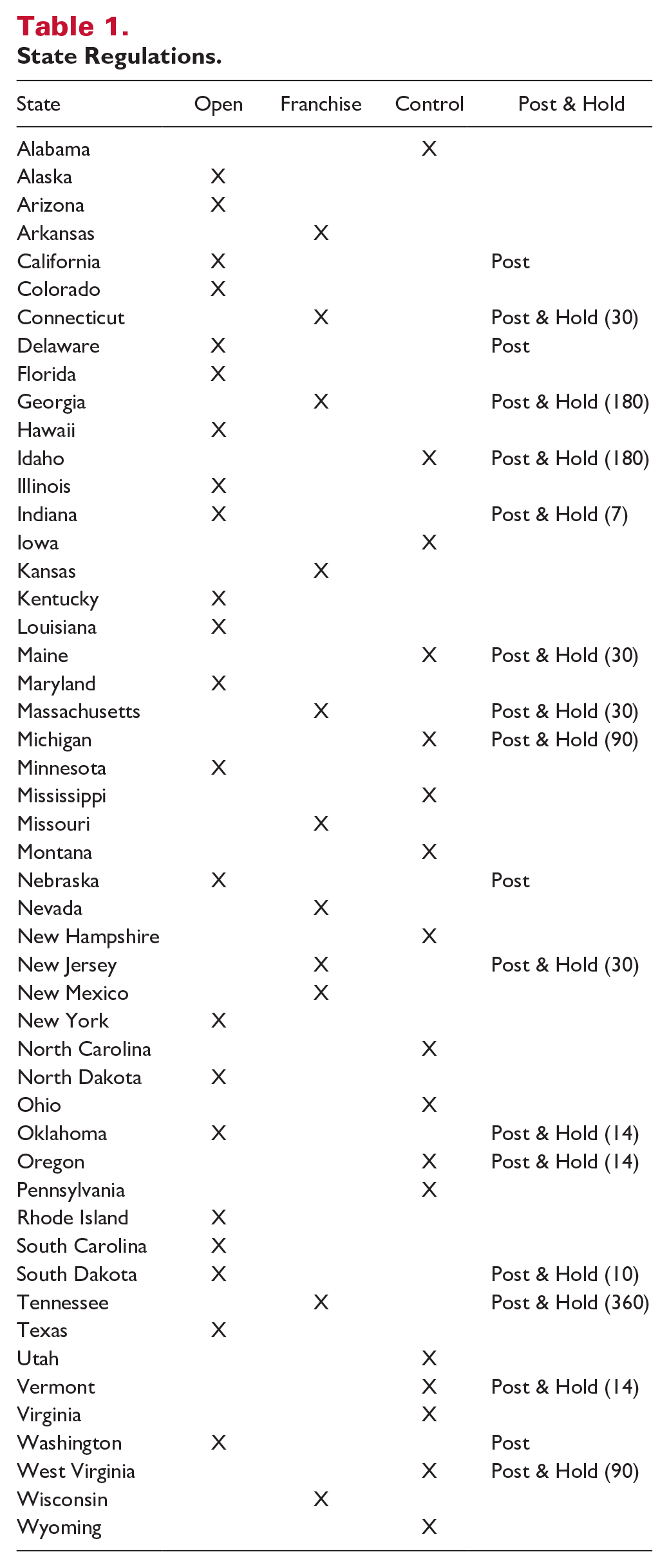

At the distribution level, there are extensive and varying state regulations, with states engaging in three primary regulatory schemes: open, franchise, and control (Treasury Department, 2022). States operating open regulatory systems (i.e., open states) allow producers to terminate their relationships with existing distributors and switch to another distributor, with distributors buying and selling alcohol and providing marketing and promotional services. In franchise states, a producer must show cause in a legal proceeding before terminating its relationship with a distributor. This is also the case if a producer wishes not to renew a contract with a distributor. Likewise, most state laws allow a distributor to sell or assign a brewery brand’s rights without the brewery’s consent (Pease, 2021; Treasury Department, 2022). In control states, the state effectively runs a distribution monopoly and may also operate the off-premise sale of alcohol. Within these states, producers sell directly to the state and use distributors for the purpose of marketing services (Norris et al., 2022; Treasury Department, 2022).

Furthermore, many states also prohibit intrabrand competition by requiring brewers to grant exclusive distribution rights to a single distributor in a specific territory. At the retailing level, few states allow retailers to distribute beer among their stores; similarly, few states allow retailers to sell alcoholic beverages to other retailers (Pease, 2021). In addition to the regulations listed above, 18 states impose some form of post-and-hold restrictions on beer distributors. These laws require distributors to post their prices with state authorities and then hold those prices for a period. Some even include so-called meet-but-not-beat provisions (Treasury Department, 2022). The following section will outline some of the negative impacts of these state regulations as they pertain to brewers—specifically small/craft brewers, consumers, retailers, and distributors. Table 1 provides an outline of states falling into these various categories.

State Regulations.

Impacts (Failures) of State Regulations

The three-tiered system of alcohol distribution, which was conceived postprohibition, has not effectively been adapted or modified in all states to keep up with the changes in the brewing industry, or the greater alcoholic beverage industry for that matter. The original goals of the three-tiered system included: the prevention of vertical integration, reducing consumption through artificially higher prices, limiting alcohol sales to minors, collecting taxes more efficiently, and preventing organized crime from gaining control of alcohol distribution (Treasury Department, 2022). Although these goals are understandable and even commendable, the system often negatively affects the business of small brewers, limits product offerings of retailers, and consequently limits purchase options of consumers. According to Pease (2021), the specific mandates within states that follow some version of the three-tiered system severely restrict or even ban the ability of small brewers to react to a consolidating and narrow distributor tier by getting their own products to market. Similarly, the Treasury Department (2022) noted complaints of brewers indicating that large distributors with large portfolios either refuse to distribute their products or force them to sign exclusive contracts and then fail to promote their products. This trend has worsened as consolidation continues at the distributor tier (Pease, 2021; Treasury Department, 2022).

Another major issue relating to the three-tier system of beer sales is the inability of small-craft brewers to ship their beer direct to consumers within their state or across state lines. Currently, 47 states allow any winery to apply for a permit to ship directly to consumers within the state, and 13 states allow out-of-state wineries to ship direct to consumers (Treasury Department, 2022). However, only 11 states and D.C. currently allow for out-of-state shipment of beer to consumers. Several wholesale and distribution companies have recently made major investments in third-party home-delivery companies. In contrast, these same companies have opposed efforts by producers, retailers, and consumers to lessen restrictions on cross-state sales and shipping (Pease, 2021).

Furthermore, state franchise laws which are maintained in 48 of 50 states (i.e., Alaska and Hawaii do not have franchise laws, nor does D.C., California does but does not stick to the “good cause” requirement), further impede the ability of smaller brewers to compete on an even playing field (Ascher, 2012; Pease, 2021; Treasury Department, 2022). These laws effectively lock a brewer into a contract with a distributor and should a brewer wish to end or decline to renew a contract, they are burdened with proving “good cause” or “for cause” to terminate the contract while also allowing the distributor an opportunity to “fix” the situation (Pease, 2021; Treasury Department, 2022). These laws also create additional barriers to entry for smaller distributors, creating hurdles for retailers wishing to carry small-craft products and leading to higher prices for consumers (Ascher, 2012; Treasury Department, 2022). Issues for retailers are made even worse in states that also require exclusive distributor rights within a specific geographic territory, wherein a brewer cannot have multiple wholesalers selling its product. Thus, retailers can only procure a product by dealing with one specific wholesaler (Pease, 2021).

Additional state laws that provide wholesalers and distributors greater control over the beer industry and undercut the potential for craft brewers to compete with larger producers include post-and-hold laws. As noted above, post-and-hold laws effectively mandate that distributors “post” their prices with state authorities and “hold” them for a set period. These prices are not controlled by the states, and states do not review them; however, multiple states have further revisions that effectively provide the distributor with the lowest prices to set minimums for competitors (Treasury Department, 2022). Although these pricing schemes were initially implemented to limit alcohol consumption, they negatively affect small brewers, distributors, and retailers. Relatedly, as noted by the Treasury in their report, states could achieve these same goals by increasing taxes which would further benefit the public treasury (Treasury Department, 2022). Other major issues regarding post-and-hold laws have come to light as retailers across the country have argued that these laws and other laws within the three-tiered system may violate the Sherman Act, the Clayton Act, and the Commerce Clause (Ascher, 2012; Treasury Department, 2022).

Conclusion

As stated above, the goal of Executive Order No. 14036 (2021) “is to reduce the trend of corporate consolidation, increase competition, and deliver concrete benefits to America’s consumers, workers, and small businesses.” As such, the Treasury Department delivered a thorough review of the current state of play and general lack of competition within the U.S. beer industry. This article sought to highlight the major areas of concern and provide potential solutions and suggestions for future research projects to ensure a competitive beer industry. Major issues and concerns that were discussed include current laws around taxation, issues within the three-tier system and how it is regulated, labeling concerns, and concerns regarding mergers and acquisitions. Each of the issues outlined above underscores the need for multiple agencies (i.e., Federal and State agencies) within the United States to re-assess laws as they are currently written and enforced. Furthermore, a deeper look into past mergers and acquisitions at the brewer and distributor levels should be considered as there is currently in effect an oligopoly as it pertains to market share. Likewise, researchers in hospitality, tourism, retail, economics, and law should further assess the issues discussed above to provide potential solutions to policymakers, operators, and consumers/voters. It is important to note that the beer industry is not the only industry affected by the issues outlined above. As such, researchers should further consider the implications within the wine and distilled spirits industries, especially as not all alcoholic beverages are treated the same regarding federal and state law. The following two sections provide calls to action for policymakers and academia.

Call to Action for Policymakers

Given that there are issues within at least three of the four federal departments discussed above, suggestions for those departments will be provided before discussing things that should be considered at the state level. Major concerns related to the TTB include closing the loopholes in the CBMA, simplifying tax forms, considering an income tax credit for smaller brewers, reconsidering penalties for FAA Act violations—specifically targeting larger brewers who engage in anticompetitive behavior, and reconsidering/simplifying labeling issues. The DOJ and FTC should continue to scrutinize the impacts of acquisitions, mergers, and overall consolidation in the alcoholic beverages market. They should also re-assess the previously approved mergers and acquisitions at the producer and distributor levels and consider the negative effects that have occurred at various levels of the supply chain and within the three-tier system of distribution. One area of interest would be investigating the “hidden ties” between brewers and distributors, wherein a brewer purchases another brewer and even if they are forced to divest, they might still have sole distribution rights within certain states. These hidden ties are widespread in the beer industry and though may not be readily apparent they provide large brewers and distributors an unfair competitive advantage. Along with this, all three agencies should work with state policymakers to investigate how mergers and consolidations have already and may in the future lead to anticompetitive markets. All three departments should continue to advise and work together to bring larger, more complicated antitrust cases against large operators. In addition, all three departments should consider looking into other areas of the supply chain to investigate how larger companies use their standing and buying power to buy up stocks of ingredients and packaging materials such as hops and aluminum cans.

At the state level, there is a need for many states to re-assess how the three-tier system is enforced and consider allowing smaller brewers to self-distribute, and not forcing smaller brewers to show “good cause” when terminating a distribution agreement as this only benefits the distributor. Other issues many states should reconsider include franchise laws, post-and-hold regulations, and direct-to-consumer sales. Many of the laws as they currently stand in multiple states are written and enforced in a manner that reduces the competitive power of small-craft brewers and smaller distributors while simultaneously negatively impacting retailers and consumers. The Treasury Department (2022) report provides additional suggestions and details that federal and state policymakers should consider that could create a more competitive U.S. beer industry.

Call to Action for Academia

The issues outlined in this article also provide ample opportunity for researchers in various fields to dig deeper and collaborate to better inform one another, industry, policymakers, and consumers/voters. First and foremost, there is a need for hospitality, tourism, and retail researchers to look further into legislative issues that negatively impact various stakeholders, especially when these issues influence multiple multi-billion-dollar industries. Beer is a product that is bought and sold in various manners (i.e., on-premise, off-premise, own-premise) and a product that has created its own form of tourism (Kraftchick et al., 2014) and under-ground trading marketplace (Whalen et al., 2019). These federal and state laws have myriad effects on local economies, and it is imperative for researchers in these fields to assess the potential positive and negative influences they may have. Along with this, hospitality, tourism, and retail researchers should consider looking outside of their field of study and collaborate with economists and legal researchers who may better understand the market impacts and lexicon, respectively. These collaborations could lead to more significant influences as researchers in the management fields can often better articulate the findings and potential implications to industry operators and subsequently assess the perceptions and potential behavioral changes of consumers given the implications of potential policy changes. Likewise, economic and legal researchers should seek out researchers in the hospitality, tourism, and retail fields to better inform the industry professionals who are being affected by federal and state policies. Researchers in the management fields tend to maintain relationships with industry professionals that might allow for a deeper understanding of the impacts that various economic and legal factors have on day-to-day operations.

Specific areas of concern that researchers may consider include the anticompetitive pricing schemes such as post-and-hold schemes that large producers utilize in the market to set prices. Various state-level distribution issues, including franchise laws, mandated exclusivity, retailer constraints, and the potential positive (negative) effects of direct-to-consumer sales, particularly across state lines. Though brewer/distributor mergers and acquisitions have been assessed in the realm of economics (Miller et al., 2021; Miller & Weinberg, 2017), there has been only one study in recent years within hospitality and tourism focused on mergers, and it was focused on consumer perceptions (Legendre & Bowen, 2020). As such, additional research should be conducted looking at the industry implications of mergers and the perceptions of various stakeholders (i.e., consumers, retailers, wholesalers, etc.). There is also a need for research to investigate the perceptions and behaviors of retailers (i.e., on-premise and off-premise) regarding distribution practices and pricing schemes. Relatedly researchers may consider looking into consumer knowledge, perceptions, and behaviors regarding who “owns” the products they are buying, how the distribution channels work, who sets prices, etc. Furthermore, there is an immediate need to assess how these laws and issues outlined above impact the competitive nature of the wine and distilled spirits industries. These studies should also be followed by additional research into other areas of hospitality, tourism, and retail that are negatively influenced by anticompetitive practices (i.e., the oligopoly of Coke and Pepsi, pricing schemes of airlines and hotels, etc.).

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, or publication of this article.