Abstract

An investment bubble occurs when there is a surge in asset prices that is not warranted by asset fundamentals because of irrationally exuberant market behavior. When prices rise to a level where no additional investors are willing to buy at the elevated price, then a massive sell-off typically occurs. Digital health investments represent approximately 10% of venture capital-backed startup investments, and diabetes digital health startups represent 4% of digital health investments. Attributes of a bubble indicate evidence for and against the current time period being in an investment bubble for digital health startups. After analyzing these attributes as well as the overall economy and the demand for healthcare products, we conclude that digital health startups and particularly digital health startups for diabetes are not in a bubble.

Introduction

Diabetes is the poster-child disease for investors in digital health. Although the rates of diabetes continue to rise, the number of clinicians specializing in diabetes care is diminishing, creating an access to care gap amenable to digital health devices and systems, including decision support. At the same time, people with diabetes have the potential to access increasingly sophisticated technologies to support self-management, which in turn is generating ever increasing amounts of information for both individuals and populations. From an investment perspective, business communities see great potential in these health data being harnessed for profitability. However, in reality and despite the opportunities for significant returns for financial investors, digital health has yet to become a mainstream part of the modern diabetes ecosystem. 1 From an investment perspective, the anticipated financial returns are yet to materialize, and therefore, the question arises: is digital health investment in a bubble?

What Is a Bubble?

An investment bubble is an economic cycle characterized by a rapid increase in asset prices followed by a downturn. 2 It occurs when there is a surge in asset prices that is not warranted by their fundamentals because of irrationally exuberant market behavior. When prices rise to a level where no additional investors are willing to buy at the elevated price, then a massive sell-off occurs.

This type of situation can be a major problem for startup companies that are backed by venture capital funding and who need regular access to fresh capital to fund continuing growth. If valuations fall sufficiently far or fast, then investors are likely to withhold the fresh capital these companies need to develop new technologies and new markets, regardless of their fundamentals. At this point, the bubble is said to be bursting.

Current Status of Investments in Digital Health

Digital health startup companies have recently experienced a surge in venture capital investment but have not enjoyed an equally robust “exit market,” wherein venture investors are able to sell their shares and realize returns. An unprecedented amount of capital has recently been invested into digital health startups with more than $30 billion in venture funding since 2011. In 2018, investments in this sector amounted to nearly $8.1 billion dollars. 3 This amount was nearly 40% more than the amount invested in these types of companies in 2017 ($5.7 billion), which had been the previous record-setting year. 3 This rapid increase in venture investment and the as-yet absence of commensurate returns have attracted attention as to whether digital health startups are overvalued. Using the assumption that venture investors expect an approximate 4× return over ten years, the value of the existing digital health startups would be expected to grow to $120 billion in the next four to six years. 4 This is a modest figure relative to the $3.65 trillion spent on health care in America in 2018. 5 In addition, the digital health market has been predicted to grow with a compound annual growth rate of 21.1% from 2018 to 2023. 6 Taken together, these observations suggest that it is possible that the aggregate value of the existing venture-backed digital health startups could increase substantially and achieve a 4× target return. On the other hand, recent increases in the pace of venture investment in digital health and high startup valuations 7 raise the question of whether digital health companies might now be overvalued and headed for a bubble.

How Bubbly Is Digital Health Venture Investing?

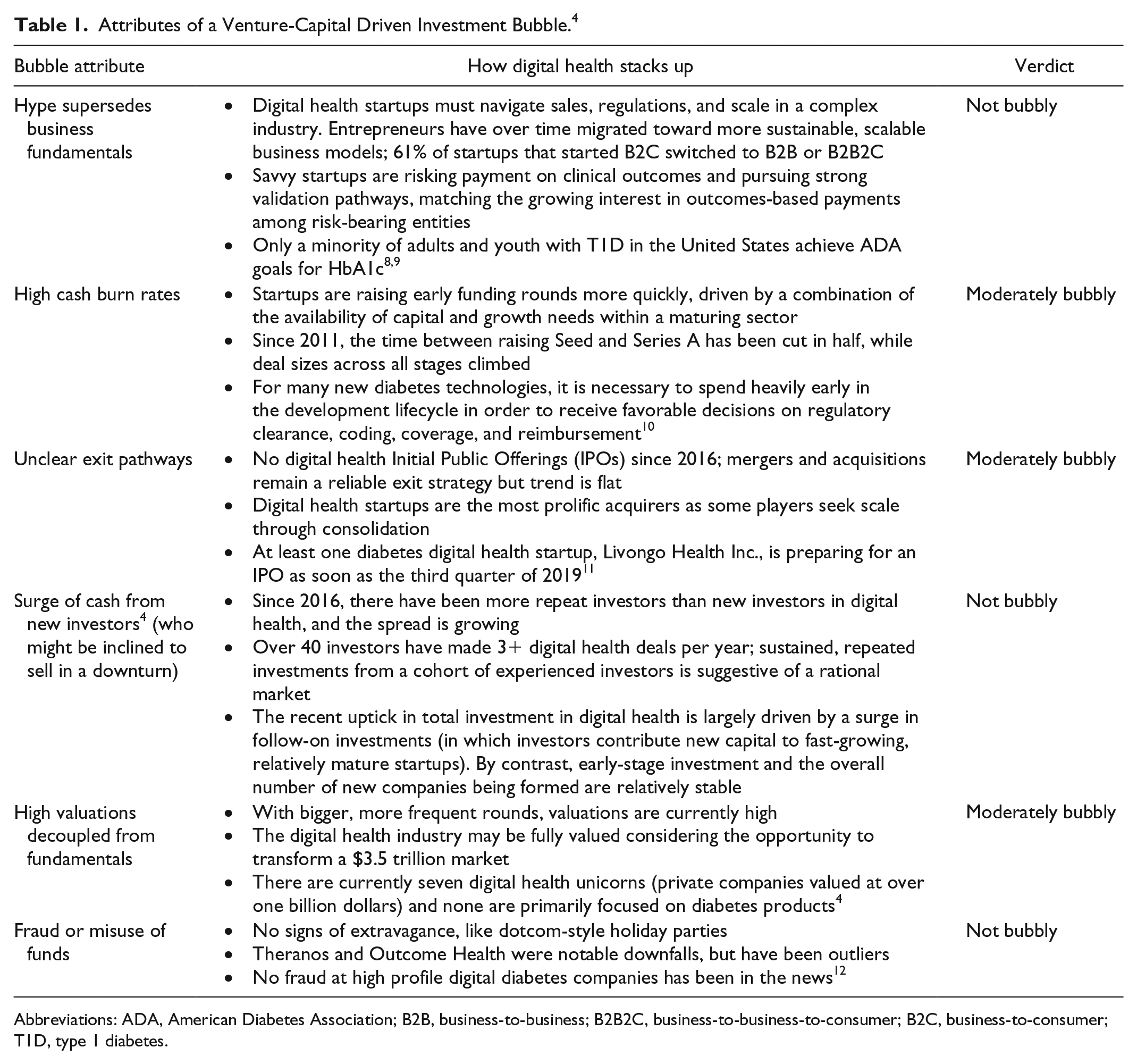

An investment “bubble” is often preceded by signs of “irrational exuberance,” terms which we can formalize through an evaluative framework. 3 Table 1 presents our proposed framework of six attributes of the startup world, which can be assessed to form a conclusion as to whether digital health startups (and digital diabetes startups in particular) are currently close to a bubble. These attributes have been observed in previous investment bubbles. 4

Attributes of a Venture-Capital Driven Investment Bubble. 4

Abbreviations: ADA, American Diabetes Association; B2B, business-to-business; B2B2C, business-to-business-to-consumer; B2C, business-to-consumer; T1D, type 1 diabetes.

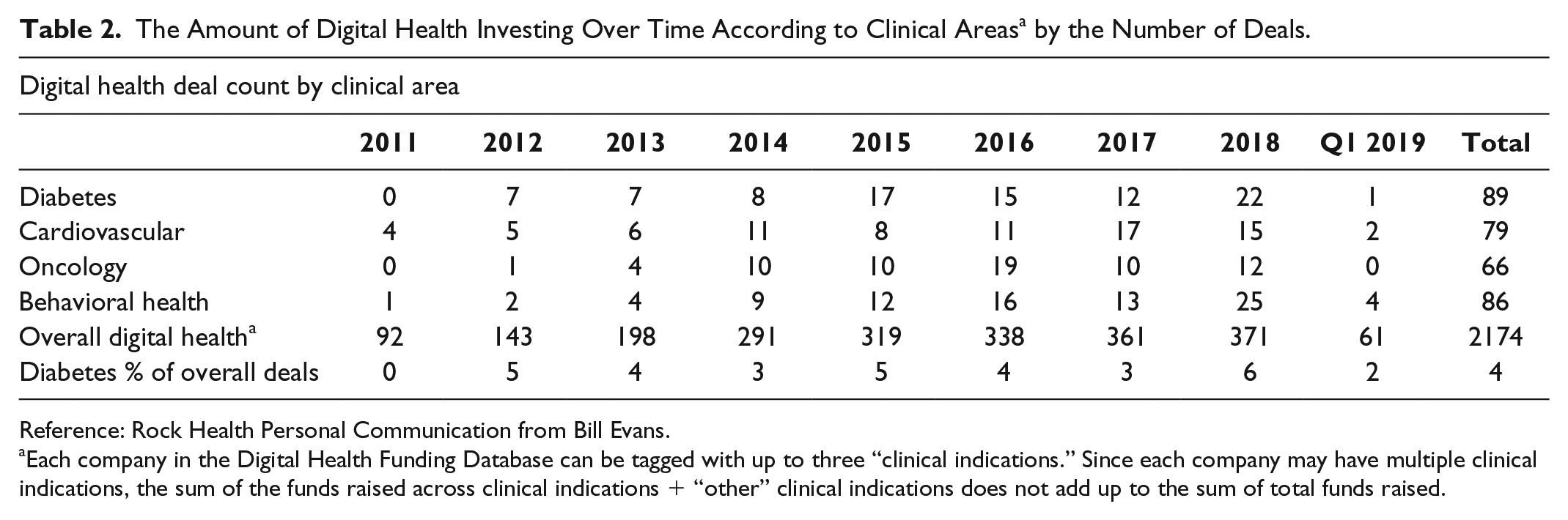

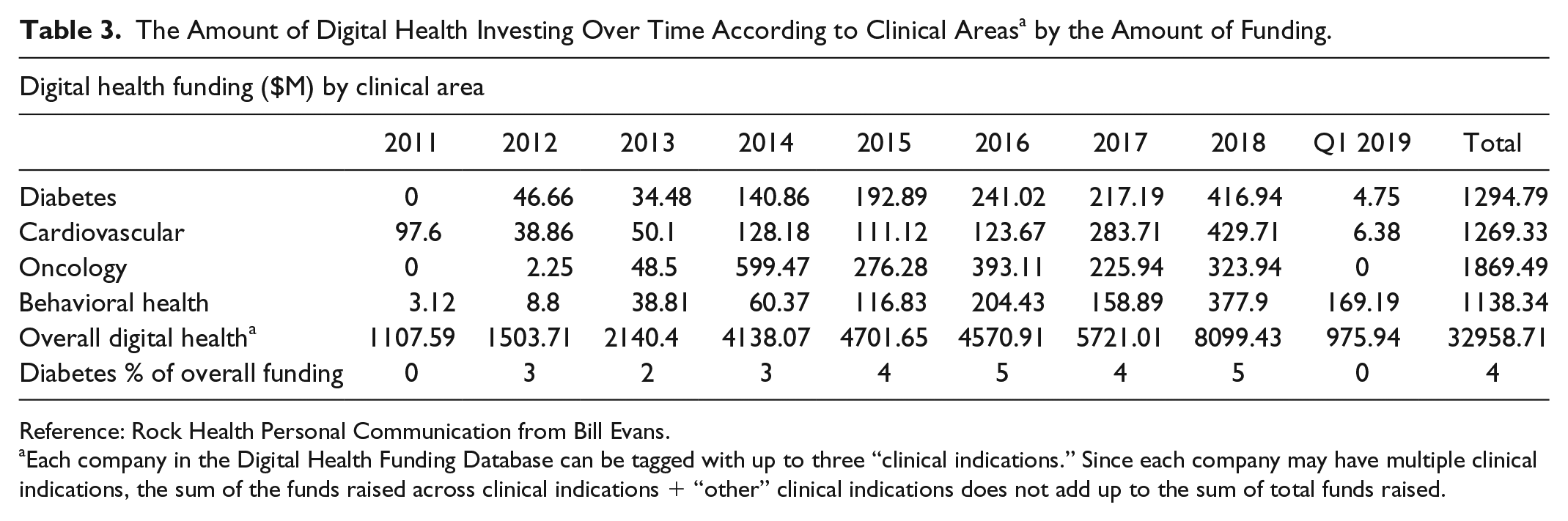

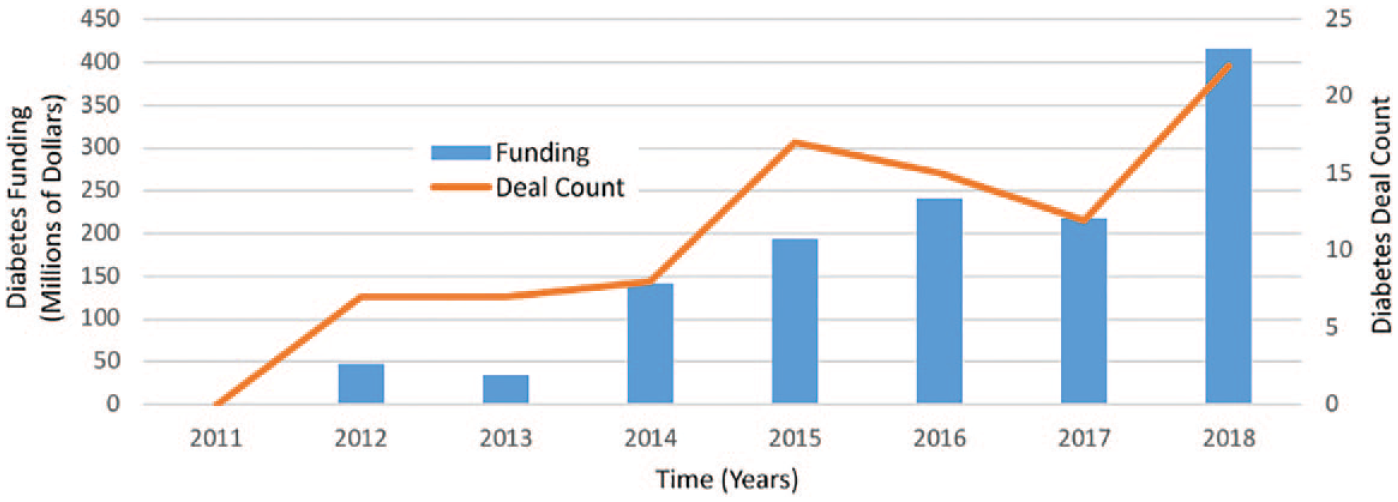

From 2011 through the first quarter of 2019, almost $1.3 billion has been invested by venture capital firms into startup companies focused on digital health where diabetes was one of their top three disease targets. For all diseases, these investments comprised 2,174 deals for an average investment of $15.2 million per digital health startup company (see Tables 2 and 3), and for diabetes, these investments comprised 89 deals for a total investment of $1,294.8 million and an average investment of $14.5 million per digital health startup company (see Figure 1). Many established companies (including pharmaceutical and technology companies) are already developing digital health products to (1) encourage heathy behavior, (2) serve as standalone digital therapeutic treatments, or (3) increase adherence to treatments.

The Amount of Digital Health Investing Over Time According to Clinical Areas a by the Number of Deals.

Reference: Rock Health Personal Communication from Bill Evans.

Each company in the Digital Health Funding Database can be tagged with up to three “clinical indications.” Since each company may have multiple clinical indications, the sum of the funds raised across clinical indications + “other” clinical indications does not add up to the sum of total funds raised.

The Amount of Digital Health Investing Over Time According to Clinical Areas a by the Amount of Funding.

Reference: Rock Health Personal Communication from Bill Evans.

Each company in the Digital Health Funding Database can be tagged with up to three “clinical indications.” Since each company may have multiple clinical indications, the sum of the funds raised across clinical indications + “other” clinical indications does not add up to the sum of total funds raised.

Recent activity as measured by amount of funding and number of deals for diabetes digital health startup companies.

Factors Suggesting a Potential Investment Bubble in Digital Health Startup Companies

The cost pressures facing the United States (US) healthcare system represent a headwind for digital health startups. Healthcare spending currently exceeds 20% of the US Gross Domestic Product (GDP), which is more than any other country’s share of their GDP. 13 Any new digital health products that do not save money or produce greater benefits for the same amount of money spent will not be well received. 14 With fewer than eight full years as an investment category and only three to five years of significant investment (as a proportion of the broader venture capital investment market), digital health as an investment category is still relatively nascent. The products and services under development by digital health startups today are yet to fully mature, and therefore, it remains to be seen whether digital health startups will fully succeed in saving money, improving outcomes, and avoiding additional cost to an already-overburdened healthcare system. In addition, the increasing size and frequency of investments in the absence of notable “exits” are also markers of a developing investment bubble. 2 The median funding deal size in digital health increased across all funding stages from 2011 to 2018. In that period, the average time between raising seed and Series A rounds has fallen from over 30 months to 15 months. If during this period of rising investment activity investors are unable to sell the shares purchased and realize a return, then they may hold back from deploying capital to digital health companies in the future.

Why Digital Health Startup Companies Appear Not to Be in an Investment Bubble

However, we believe that a bubble in digital health startup companies appears to be unlikely at this time. Digital health tools have demonstrated their potential to save money by delivering low cost scalable treatments based on best practices and guidelines both synchronously and asynchronously. 15 The increased use of remote diabetes management programs and lower mean blood glucose levels have been associated with reduced medical spending. 16 These tools can not only replace costly human interactions but they also have the potential to direct appropriate therapy earlier and more accurately than current in-person interactions with healthcare professionals. The US can reduce waste in healthcare spending by up to $1 trillion if waste (primarily from delivery of better care, less administrative complexity, more efficient supply, and elimination of fraud and waste) can be eliminated. 17 In that case, there will be more money to invest in new technology for healthcare. There is currently a trend toward value-based healthcare strategies to deliver better outcomes using new technologies, like digital health, while simultaneously managing costs and outcomes.” 18 Diabetes is a disease where digital health can greatly contribute to cost savings. Ironically, switching to a new payment model will require investment, and many digital health companies are built with value-driven payments in mind, thereby positioning themselves to provide assistance with this transition and leading to commensurate growth in their value in a changing healthcare economy. Finally, the low price elasticity of demand for healthcare limits the effects of changing prices and payment methods on overall consumption. 19 From this perspective, shifts in consumption patterns are more likely than changes in overall spending in the near future, providing a stable financial base for innovation to grow and flourish during a period of system-wide transition.

Conclusion

Digital health is increasingly becoming part of mainstream healthcare, and as such, the future of digital health startups will be tied to the economic prospects of the healthcare sector. Diabetes is a disease where digital health technology is particularly useful because the management of diabetes is in part a function of monitoring and managing quantifiable biological and behavioral phenomena—numbers—that affect a patient (such as blood glucose values, total calories, carbohydrates, exercise durations, and exercise time). Digital health technology and services are suitable for collating, interpreting, and in some cases, directly acting upon these data to improve glycemic control with real-time interventions. Although we are watchful for signs of irrationally exuberant investor behavior and we advocate near-term moderation in startup valuations, the evidence for an investment bubble is lacking. Moreover, digital health innovation is steadily increasing in importance as a driver for cost savings in healthcare broadly. Furthermore, the digital health industry shows stability in terms of 1) the fundamentals of emerging digital health business models, 2) strong interest by repeat investors, and 3) an absence of significant waste and fraud. We therefore believe that digital health startups, and particularly digital health startups for diabetes, are not in a bubble.

Footnotes

Acknowledgements

The authors would like to acknowledge Annamarie Sucher for her expert editorial assistance.

Abbreviations

ADA, American Diabetes Association; B2B, business-to-business; B2B2C, business-to-business-to-consumer; B2C, business-to-consumer; GDP, Gross Domestic Product; IPOs, Initial Public Offerings; T1D, type 1 diabetes; US, United States

Declaration of Conflicting Interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: David Klonoff is a consultant for Abbott, Ascensia, EOFlow, Lifecare, Merck, Novo, Roche Diagnostics, and Voluntis. Bill Evans, Megan Zweig, and Sean Day are employees of Rock Health. David Kerr is a medical advisor to Glooko, Vicentra, and Hi.Health. He has also received remuneration for participation in advisory boards for NovoNordisk and Sanofi, Ascensia and has received research support from Lilly and Abbott Diabetes Care.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.