Abstract

Insulin prices in the United States have risen dramatically in recent years, yet pharmacies cannot provide a stable price for a given insulin due to factors that are not widely understood. This commentary discusses the complex and obscure factors that drive today’s insulin prices with a discussion of the other players, besides the insulin manufacturer, who benefit from higher prices. An open discussion is critical regarding this drug and others that are essential to the lives of millions of people with diabetes. We’ll also explore whether the market introduction of biosimilar insulin will impact insulin prices.

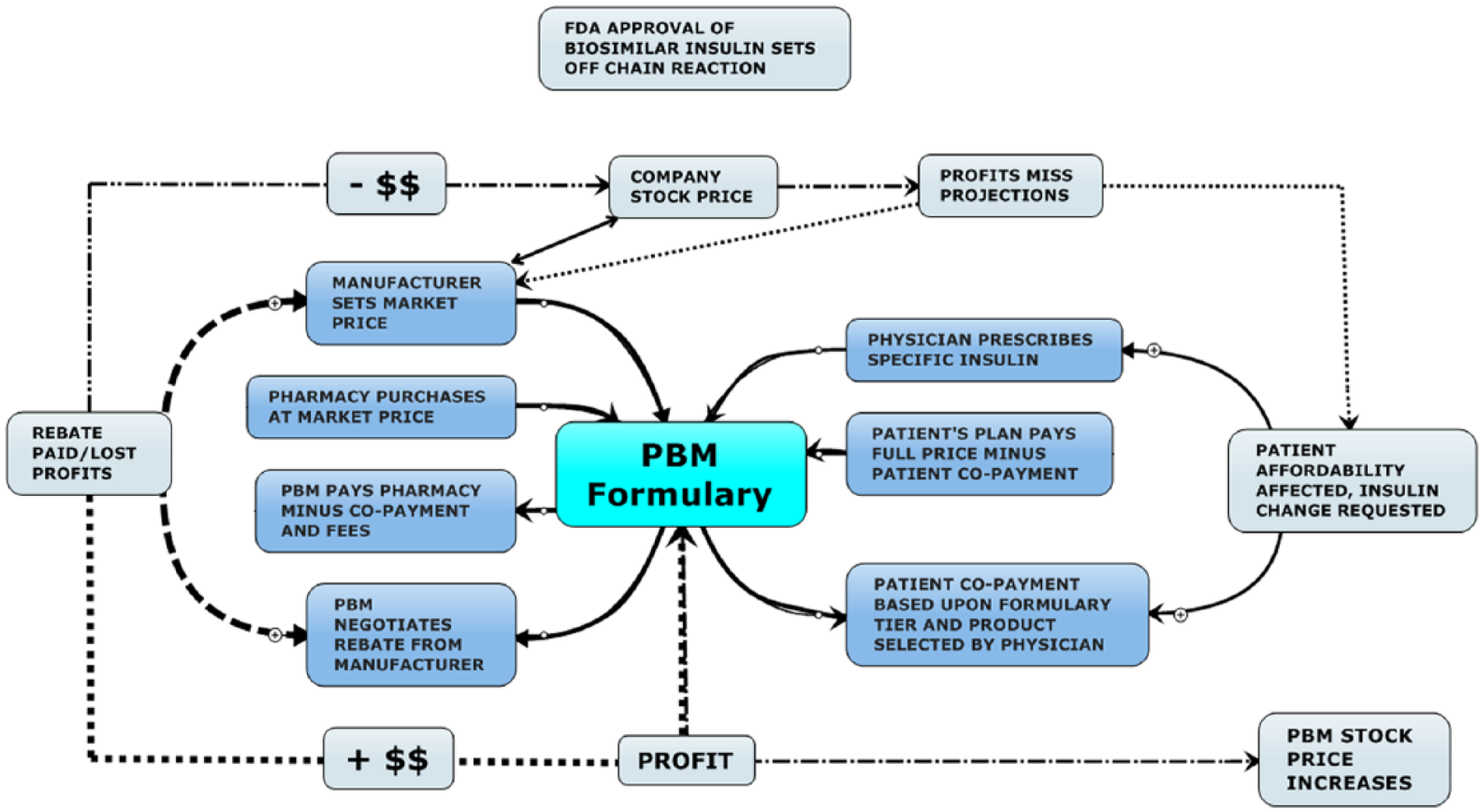

Who Controls the Final Consumer Price of a Drug?

The price a patient pays at the pharmacy counter for a given drug (eg, insulin) is usually not the full price the pharmaceutical company requests. Drug prices are negotiated by middlemen; in the United States these are pharmacy benefit managers (PBMs) (Figure 1). These confidential price negotiations often create financial choices at the pharmacy when the patient’s insurance does not provide affordable access to every drug that their physician recommends. Instead, they have access to 1 or several “preferred” drugs in each classification of drugs according to what drugs an insurance company’s PBM selects. The underlying assumption is that the patient (consumer) will get a good price for a high-quality drug without a lot of strings attached.

Diagram showing the complex interplay between the players in the United States and their potential formulary impact on drug prices, drug selection, and therapy options.

Why Is the Price for Insulin So High, and Is There Hope?

This discussion of the complex world of drug pricing in the United States will focus on insulin prices that have increased tremendously in recent years. For example, between 2001 and 2015 insulin lispro increased from US$35 to US$234 per vial and human insulin soared from US$20 to US$131 per vial. 1 The usual price complaint is about the greediness of the insulin manufacturer, but are they the only ones that benefit from higher prices and how much do they get from a higher price? The consumer expectation is that with a market introduction of biosimilar insulin the price of insulin might go down somewhat. 2 However, one concern with biosimilar insulin is that manufacturing processes may not maintain the same quality and clinical effectiveness of the original products the consumer has been using. 3

Are PBMs Acting in the Best Interest of Patients with Diabetes?

PBMs utilize pharmacy and therapeutics (PT) committees to review therapeutic classes of drugs and determine if significant differences exist in outcomes, tolerability, dosage forms, and so on. If the PT committee determines that no particular FDA-approved drug in a therapeutic class (such as human insulin or insulin analog) is clinically superior to another, then the therapeutic class becomes open for price competition requests from the Finance Committee. The negotiated price reductions are separately paid by the manufacturer directly to the PBM. PBMs in the United States are for-profit companies responsible only for their bottom line and may or may not pass a portion of the negotiated rebate savings back into the health care system. This method of price negotiation works pretty well for the PBMs and their shareholders, but not so well for manufacturers nor consumers and the health plan they are enrolled in.

How Are Prices of Insulin “Controlled” in Other Countries?

Other areas of the world, like Europe and Canada, have more affordable drug pricing overall, but this has not proven true in the United States unless the drug is available from competing generic manufacturers. Biosimilar insulin (and other biologic therapeutics) cannot be classified as generic equivalents because of regulatory aspects raised by the FDA and regulatory agencies outside the United States, primarily the EMA. Instead, they are classed as “similar” for therapeutic use and possibly “interchangeable.” This means the true price competition between manufacturers is unlikely to occur and significant insulin price savings will not be realized. Countries outside the United States may negotiate better manufacturer prices for their citizens through national formularies but in the United States the for-profit PBMs negotiate on their investor’s behalf first.

Outcome of Price Negotiations of PBMs—Role of Rebates

PBMs rely on generic drug pricing to save everyone money but in the case of branded products within the same therapeutic category they leverage the number of covered lives they have in a plan to negotiate rebates from manufacturers. Each manufacturer approached has to take into consideration their cost of production and distribution along with manufacturing capacity to determine how much rebate they can afford to pay the PBM. The manufacturer’s quick question is “how much do we have to pay to play?”

In this context it is important to understand that in the United States insurance companies are regulated under specific federal and state laws and are monitored by Insurance Commissions but have little/no interest in amortizing the cost to pay for drugs outside a hospital system as part of their base premium. To offer a robust package of health care services that includes difficult to predict out-patient drug coverage they must own or subscribe to a PBM. PBMs have little regulatory oversight and operate under private business contract law, serving as middlemen negotiators who separately contract with the insurance company as a service provider to pay retail pharmacies for drugs and services. The PBM then secures a different contract with pharmacy providers for drugs and services that also indemnifies the insurance company from any liability to pay the pharmacy bill should funds run short. The PBM serves as a “bank” (and is registered as such under a banking identification number [BIN]) that collects money from the company or insurance plan to pay the pharmacy AFTER a prescription is filled. The PBM bills the company or plan for the drug who then writes a check/transfers funds plus a service fee to the PBM, to pay the pharmacy. The PBM then pays the pharmacy, minus a “processing fee” and patient copay, for the drug. The PBM plays the float time on checks/fund transfers for more interest, charges a service fee to both the client and the pharmacy, and retains an undisclosed portion of the manufacturer rebates.

Does This Complex System Provide a “Fair” Price?

For the US consumer this price lowering tactic should reduce overall health care cost, but this has not proven to be true with insulin being a case in point. PBMs are not required to share any specific amount of their rebates with insurance companies, employers, or Affordable Care Act (ACA) groups (subscribers) who subscribe to their services. As diagramed in Figure 1 the FDA regulates consumer access but not price; the manufacturer controls availability access and price depending on what the market will tolerate; the prescriber directs consumers to a drug category but not price or a specific brand; the pharmacy maintains consumer access with some impact on the final consumer price; the PBM controls both consumer access and consumer out-of-pocket price through their formulary plan.

The consumer works his or her way through this jungle without control of anything. In some cases the PBM may offer a “discount” of 5-10% to subscribers who use their complete formulary and mail order options but may have negotiated undisclosed rebates from manufacturers that reduce their final drug purchase costs by 30-50%. 4 This unrestricted windfall is added to the PBM’s bottom line along with the fees charged the subscribers for handling claims along with the fees for issuing payment and audit charge backs (that may go unreported to subscribers) levied on pharmacy providers. The employer or ACA group pays the full list price to the PBM minus the individual patient’s copayment while the PBM pockets most of the rebate windfall.

This hidden cost is significant and has led to the insurer Anthem suing the PBM giant Express Scripts for US$15 billion to recoup drug price overcharges from Express Scripts. In its lawsuit, Anthem said it had sought the advice of a consulting firm and other sources, and determined that it was paying “massively excessive prices” to Express Scripts, generating “an obscene profit windfall” for the PBM. 5

Meanwhile, the local pharmacy purchases the insulin at the manufacturer’s suggested price then must wait for 2 to 12 weeks to receive payment for the insulin that was dispensed. The total payment received will be minus the consumer paid copayment, PBM processing fees and incidental charges which lowers the pharmacy profit margin unless the pharmacy corporation happens to own the PBM. In that case the processing fees are retained to boost the PBM-pharmacy profits along with portions of undisclosed manufacturer rebates paid for formulary placement.

The manufacturers have also learned to play this game pretty well. By raising suggested list prices the manufacturer can offer greater “paper” discounts for large volume purchases and meet PBM rebate demands. For example; raise the manufacturer suggested list price by 10%, give a 3% discount for large wholesale purchase netting a 7% gain, offer a 4% rebate to a PBM for a 6% net gain that also increases their drug market share by 20% will add millions to their bottom line. (Note: percentages are for illustration only, actual percentages are trade secrets.)

Undisclosed Rebates

In many business models, undisclosed “rebates” negotiated and paid in this fashion along with fees for payment and audit charge-backs levied on merchants (pharmacies) that go unreported (except to IRS) could be considered kickbacks (payment for preferential status) 6 and extortion (requiring payment to protect ongoing business from elimination). 7 That is not the case in the mostly unregulated world of PBMs in the United States. Perhaps the Federal Trade Commission, or even a special congressional panel, could look into ways to improve drug pricing transparency to help ensure that both private and public funds are being used wisely.

If My Copayment Stays the Same (and I Don’t Have a High Deductible Plan), Why Should I Care? Be Aware of the Medicare Part D Guideline!

PBMs sell the notion of lowering prices, but manufacturers may be forced to raise prices substantially to help pay for the rebates and avoid losses that will affect their share prices. This cycle of rebate/price hike may repeat as often as quarterly partly due to Medicare Part D guidelines for formulary management. One unfortunate aspect of the Medicare Part D program is that these guidelines allow a PBM to make product changes to their medication formulary every 90 days. For example, each time another biosimilar insulin receives market approval by the FDA, a PBM can renegotiate rebates from a manufacturer and replace their formulary preferred insulin as long as they follow the 90-day formulary change rule. Copayment may remain the same but the insulin product may change unless the patient is willing to pay the difference in price. In some cases this could be a $500 difference, depending on drug manufacturer list price and plan restriction or deductible! A PBM may declare that a biosimilar insulin is therapeutically equivalent to a brand name insulin (such as insulin glargine) and offer to cover only the cost of the biosimilar insulin but not the brand name insulin. They then offer the biosimilar insulin as their preferred product in the therapeutic class, with a copay range of $10-50. The patient is free to request the brand name product but must pay a higher copay, the copay plus price difference (defined by PBM) or they may be forced to pay the full usual and customary pharmacy retail price. The PBM declares that they don’t restrict access to any drug, they just specify what they will “pay” for and the patients out-of-pocket responsibility.

Since the FDA Doesn’t Consider Biosimilar Insulin Products to Be Interchangeable, This Won’t Happen to Me, Right?

Even in their latest draft guidance, the FDA has yet to determine how a manufacturer can demonstrate that a biosimilar is interchangeable with the original reference (branded) product. A demonstration of biosimilarity generally means the FDA has determined that there are no clinically meaningful differences between the proposed product and the reference product in terms of safety, purity, and potency. 8 Though this is a significant hurdle to clear for market approval, the trials designed to determine biosimilarity are performed in healthy volunteers lasting weeks to months. Actual clinical differences between biosimilar products from prolonged use in real patients with diabetes are difficult to determine using today’s methods. To be considered interchangeable, the biosimilar product must provide the same clinical result and, the safety or efficacy of alternating or switching between the biosimilar and original product is not a greater risk than using the original product without switching in any given patient. Given this complexity the FDA wants to be sure to get the science right, but, during this period of guidance development, several US states have enacted legislation in an attempt to manage the interchange of biosimilar products. Unfortunately, many of these same states also have legislation requiring the pharmacy to dispense the lowest cost product available unless the consumer is willing to pay for a higher cost product. 9 Differences between different state laws and conflicts between different sections of the same state’s laws generates confusion at the pharmacy counter. Once a biosimilar insulin is FDA approved for treatment of type 1 and/or type 2 diabetes, the PBM is free to create a preferred therapeutic product category regardless of an interchangeability designation. As things currently stand a consumer could theoretically be dispensed a specific brand of insulin in 1 state then refill it at a pharmacy in another state and receive a PBM preferred biosimilar insulin instead. In some metropolitan areas in the United States the other pharmacy may be as close as across the street!

Although insulin is a biologic product, the FDA has historically regulated insulin products predominately under drug manufacturing guidelines, not biologic manufacturing guidelines. This could contribute to misunderstandings about how a state’s interchange rules apply to biosimilar insulin products. Technically no automatic substitution is allowed as long as no interchangeability has been demonstrated but, in the case of insulin, that line may be blurred. As mentioned, there are states in the United States that have long established legislation to ease market access for manufacturers offering lower drug prices for FDA-approved products. With the first biosimilar insulin arriving on the market, Basaglar (insulin glargine) by Eli Lilly, it might happen that in a pharmacy on 1 side of the street you can get a long-acting insulin analog at a lower price, assuming that in the state in which the pharmacy resides substitution is allowed, but not on the other side.

So, What Drives Substitution?

Therapeutic class substitution options are primarily determined by the amount of the rebate that is confidentially negotiated between the PBM and manufacturer. By creating an artificial unaffordable price difference between similar products through a preferred product payment system, the PBM is able to circumvent FDA equivalence and substitution guidelines via consumer request to reduce their out-of-pocket expense.

Since the rebate only goes to the PBM, the employer or ACA group plan will be billed the original manufacturer listed price at the time the pharmacy processes the prescription. By utilizing separate secret business contracts between the PBM and manufacturer and between the PBM and pharmacy provider, the PBM is able to keep their true costs hidden. This creates a false sense of individual savings since the employer or ACA plan will still pay nearly full price. With the employer and ACA groups being billed (and paying) current list prices, no significant system savings are realized. For patients who require insulin therapy for daily survival the PBM business practices may also introduce undesired variables in therapy (hypoglycemia, hyperglycemia, allergies, circulating antibodies) caused by financially forced substitution of insulin manufacturer if the biosimilar insulin is not interchangeable.

Summary

Price, quality, and convenience are usually the primary drivers of purchase consideration, but health care consumers lack transparency of cost and information about quality. Their PBM chooses the preferred formulary insulin for them based on the best price for the PBM with ongoing product quality presumed to be ensured.

We invite all insulin manufacturers to openly discuss issues that impact their ability to ensure consistent product quality at a fair price to serve global society given the challenges present in the new world of insulin competition. Given the cost of long-term clinical comparison trials, perhaps analytical comparison of insulin products for content variation could be used to justify higher prices for independently verified higher quality.

PBMs circumvent FDA product substitution guidance by utilizing therapeutic substitution categories for direct (and substantial) financial gain. As the FDA continues to ponder biosimilar interchangeability, the PBMs are positioned to become the true guardians of biosimilar substitution to increase their profits. With little business regulatory oversight or forced contract pricing transparency, who will guard them?

Footnotes

Acknowledgements

We thank John Walsh for his thorough reading of the manuscript and his very helpful comments.

Abbreviations

ACA, Affordable Care Act; BIN, banking identification number; EMA, European Medicines Agency; FDA, Food and Drug Administration; PBM, pharmacy benefit managers; PT, pharmacy and therapeutics.

Declaration of Conflicting Interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: AWC declares no conflict of interest. LH is a member of a number of national and an international Advisory Boards for companies that develop novel insulins and routes of insulin administration.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.