Abstract

In the era of digital transformation, the structure and application of economic sanctions have evolved, expanding from traditional trade embargoes to sophisticated digital and financial sanctions. The recent conflict in Ukraine triggered a spectrum of responses from the Western powers, targeting Russia’s digital sectors. The sanctions include restrictions on quantum computing, IT services, manufacturing, aerospace technology, and other measures that may impede the country’s digital transformation. This study aims to understand if these emerging digital-technology related measures can be perceived as a novel form of economic sanctions and to explore the potential economic implications for Russia. Two primary research questions are addressed in this paper: First, we ask whether sanctions targeting digital technology and development can be seen as an advanced form of economic sanctions, and what would be the subsequent economic losses incurred by Russia. We also explore possible Russian responds or adapt to these economic pressures. As digital transformation continues to revolutionise economies globally, this research posits that digital-technology sanctions hold substantial economic ramifications for targeted countries. By analysing the features and outcomes of the recent sanctions against Russia, the study provides insights into the evolving landscape of sanctions mechanisms and diplomacy in the digital age.

Keywords

Introduction

The term ‘economic sanctions’ refers to diplomatic tactics that withdraw or threaten to withdraw economic relations with a target country to modify or revoke the country’s diplomatic decisions (Hufbauer et al., 2009, p. 3). The target country calculates the expected economic losses from the proposed sanctions, and if it modifies or revokes its foreign policy decisions to minimise the possible losses, we may consider the economic sanctions effective. Hence, economic sanctions must be designed to inflict considerable economic losses on the target country. In the earlier era of globalisation, when trade relations between nations were rapidly expanding, policymakers believed that the loss of trade could significantly impact a nation’s foreign policy decision-making. Consequently, most economic sanctions included trade embargoes. Today, financial sanctions are being implemented more frequently, given that the leverage of financial transactions surpasses that of commodity trading. Furthermore, financial sanctions are relatively free from ethical criticisms, as they cause losses only to a specific group or individuals and thus have a limited impact on the vulnerable population of the target country.

The current era of digital transformation has had a significant impact on economic activities across various sectors, with digital transactions becoming increasingly commonplace. Hence the need to reconsider the types of economic sanctions that can effectively cause substantial losses to target countries has become more pressing. For example, Benatar (2011) suggests that cyber sanctions represent a new category of coercive measures that international institutions could utilise to influence a country’s foreign policy behaviour. Cyber sanctions refer to measures imposed by governments or international organisations to penalise and deter malicious cyber activities conducted by individuals, groups, or state-sponsored actors. These sanctions are typically targeted at entities involved in cybercrimes, such as hacking, intellectual property theft, cyber espionage, and other disruptive cyber operations. The concept of cyber sanctions involves a combination of traditional and modern elements of economic sanctions. In its traditional sense, it fits within the contemporary definition of sanctions as a coercive measure. In addition, it is executed in the realm of cyberspace, utilising highly efficient and advanced computer network attack methods. However, the existing concept of cyber sanctions is limited since it specifically focuses on possible countermeasures against cyberattacks and thus fails to address the broader impact and consequences of sanctions imposed intentionally or un-intestinally on digital development.

This paper examines whether the digital transformation, much similar to past globalisation trends, creates a new landscape for a new form of economic sanctions that specifically target digital-related sectors and developments of a target country. We suggest that changes in economic structure can in fact create different effects due to digital sanctions. We focus on the possibility of defining sanctions against Russia’s technology sectors imposed by the Western power as digital sanctions. On February 24, 2022, Russia launched an attack on Ukraine. The United States and its allies reacted by enforcing wide-ranging sanctions. 1 Around a dozen areas of the Russian economy to apply economic pressure, in retaliation to Russia’s aggressive actions in Ukraine. These areas also include digital transformation-related technologies such as quantum computing, IT services, manufacturing, and aerospace technology. Export controls have been put in place, limiting the export of microchips to Russia. Such measures are expected to cause serious harm to Russia’s tech industries. The European Union (EU) also responded with ‘unprecedented sanctions’ against Russia, adding to sanctions already in place since 2014 (EU Commission, 2023). The newly imposed EU sanctions include bans on advanced semiconductors and software, and IT-related consulting and engineering services. Major Russian banks have been banned from using the SWIFT service, crucial for international currency transfers. Ukraine also requested that Internet Corporation for Assigned Names and Numbers (ICANN) and IP Europeans Network Coordination Centre (RIPE NCC) limit Russia’s use of domain names to counter Russia’s cyberattacks on Ukrainian internet space. However, both the ICANN and RIPE NCC have declined to enact the requested measures, suggesting that such sanctions may potentially threaten internet neutrality and cause regional fragmentation within the global internet. Nevertheless, a number of private enterprises mostly based in Western countries have independently taken actions to isolate Russia’s digital sphere. For example, both Cogent Communications and Lumen Technologies, two major internet service providers (ISPs), have terminated their operations within the country, while companies like Microsoft and SAP have stopped their product sales.

These evolving circumstances raise two central questions: firstly, can measures imposed on digital technologies and development be considered as a new form of economic sanctions? If so, what might be the economic losses Russia may incur from digital technology sanctions in its digital transformation? Secondly, what could be the likely outcomes for Russia due to the predicted and/or actual economic losses? By tackling these questions, this paper explores the economic impact of the digital-related sanctions issued by the Western powers and potential effects on Russia’s digital economy. It further examines possible Russian responses to these sanctions. We first delve into a theoretical discussion on whether sanctions that intentionally or unintendedly disrupt digital economy and transformation of a target country can function as a form of economic sanctions, similar to traditional measures that induce economic losses to a target country. We propose that as digital transformation expands, sanctions against digital technology sectors can lead to significant economic impacts. The following sections provide an in-depth analysis of the unique features of digital technology and platform sanctions implemented towards Russia as a retaliation against its 2022 attacks. We conclude with an exploration of the study’s findings and limitations, alongside proposing potential directions for future research in the conclusion.

Digital-related measures as a new type of economic sanctions

This section investigates the classification of digital-related measures as a form of economic sanction. Firstly, it examines the mechanisms and operational aspects of economic sanctions, along with the measures employed as economic sanctions. Secondly, it demonstrates that as the structure of the digital economy intensifies, digital-related measures can effectively function as a type of economic sanction. Finally, the section describes the intended and unintended effects of digital-related measures when utilised as economic sanctions.

First, we ask: how do economic sanctions operate, and what measures are utilised as economic sanctions? A measure can be considered an economic sanction if it is expected to generate economic losses or if the potential economic losses from the measure are perceived as a threat by the target country (Park, 2016, p. 22). If the measure does not induce enough economic losses or if the target country fails to perceive the potential losses it could incur, then categorising such a measure as an economic sanction becomes challenging. The effectiveness of an economic sanction is evaluated based on the degree to which the measure influences the target country’s diplomatic decision-making. If the expected or incurred economic losses resulting from the measure are significant enough to prompt the modification of diplomatic decisions, it can be considered an effective economic sanction; otherwise, it would be deemed ineffective (22–23). Therefore, for a measure to qualify as a type of economic sanction, it must either cause or be expected to cause economic losses to the target country. According to this framework, withdrawal of trade relations or suspension of financial transactions, which directly leads to anticipatable economic losses, has been perceived as a type of economic sanctions (Hufbauer et al., 2009, p. 44–47; Bergeijk, 2009; Mulder, 2022). Additionally, sanctions related to shipping or aviation operations are also treated as a type of economic sanction due to the anticipated economic losses they may cause (Biersteker et al., 2016, p. 162).

Then, how can we conceptualise digital-related measures within the framework of a target’s economic ramifications? Currently, there is only limited research that specifically addresses sanctions on digital technology as a distinct category of economic sanctions (Danilin, 2022; Hufbauer & Jung, 2020; Mirrlees, 2022; Nepthew, 2019). Nonetheless, digital-related measures have been implemented in diverse capacities, serving both diplomatic and economic objectives. In 2019, the United States levied sanctions on Huawei, a prominent Chinese telecommunications conglomerate, on the grounds of national security implications (US Federal Register 2019, May 21). These sanctions curtailed Huawei’s access to U.S. technological resources, encompassing semiconductors and software, precipitating a notable disruption in its global operations and procurement of essential components. Earlier in 2010, Google’s partial retreat from the Chinese market – motivated by concerns over censorship and cyberattacks aimed at human rights advocates – serves as another exemplar of digital-related measures (Stanford Daily, 2010, April 9). Subsequent to this decision, Google rerouted its Chinese search engine to operate from Hong Kong with comparatively liberal internet space than that of China. These measures could be considered as examples of digital-related sanctions.

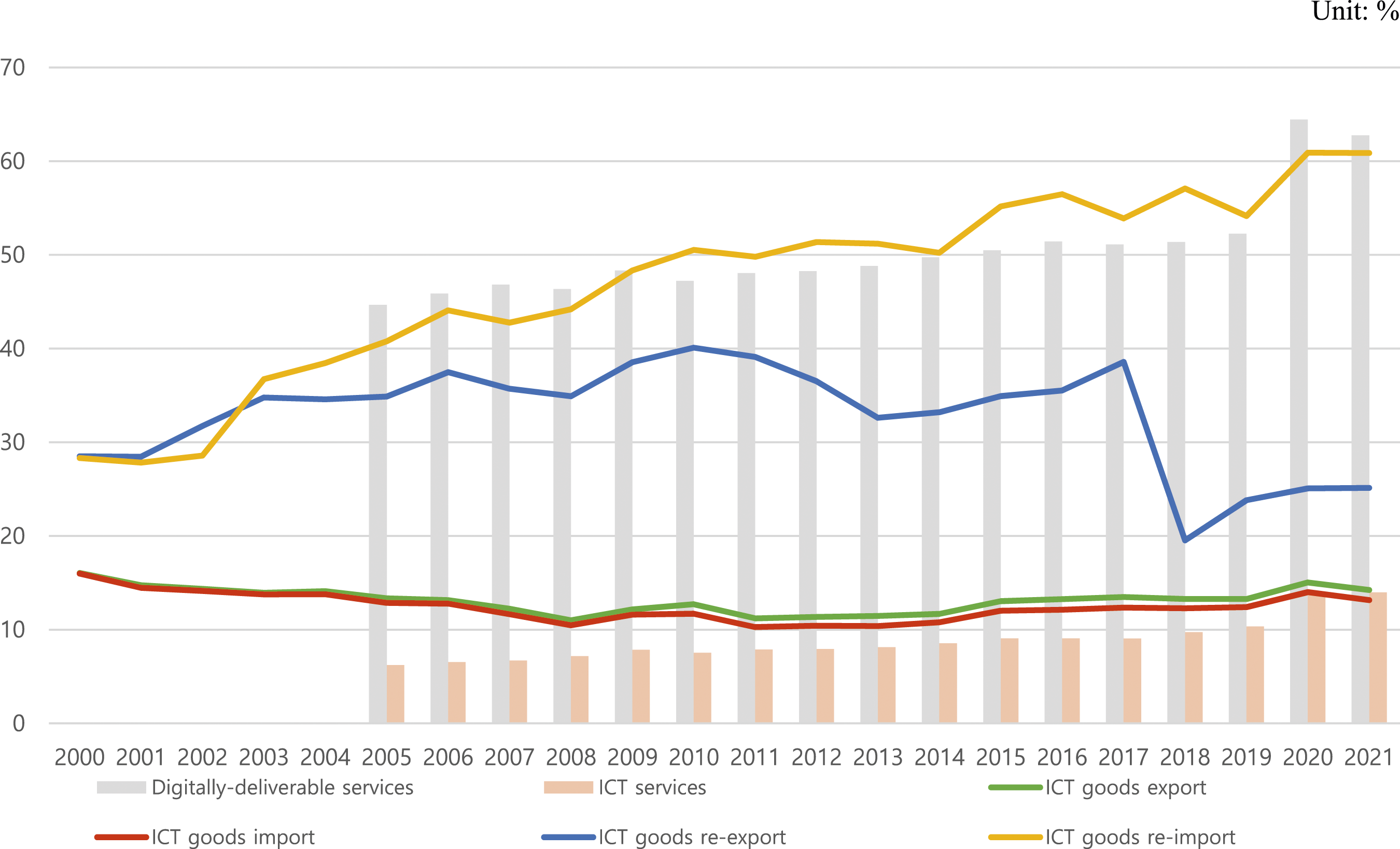

We must also consider to what extent these digital-related measures can impact the economic losses of states undergoing digital transformation. To answer this question, we need to estimate the size of the digital economy. Reviewing UNCTAD’s survey on measuring e-commerce and the digital economy would help us understand the scope of the digital economy and, consequently, the potential economic impacts on the targets of digital-related measures. The UNCTAD’s working definition of the digital economy, following Bukht and Heeks (2017) is ‘that part of economic output derived solely or primarily from digital technologies with a business model based on digital goods or services’. This definition has been further developed by the OECD and the G20. According to the summary of UNCTAD reports, the core and narrow scopes of the digital economy relate to information communication technology (ICT) infrastructure, the ICT-producing sector, digital and platform-based services, while the broad scope encompasses the use of digital technologies in various economic activities, including e-commerce (UNCTAD 2022, November 9). Based on these definitions, UNCTAD has generated nine relevant data categories. However, there are discrepancies in the information gap among these categories due to differences in the production of country-specific statistical data. If we examine the size of the digital economy in individual countries, we may utilise all available data if it is offered by a state. However, in this context, we are examining the overall global scale of the digital economy. For this purpose, we rely on three indicators: the share of ICT goods ((re)import, (re)export), international trade in digitally-deliverable services, and international trade in ICT services, which provide a measure of the world’s total volume of trade in digital goods and services (Figure 1). The share of digital economy in the global economy. Source: UNCTAD. https://unctadstat.unctad.org/EN/BulkDownload.html.

As of 2021, the share of international trade in digitally deliverable services among individual economies and various groups of economies is around 60%, and the share of ICT services is around 40%. In terms of trade volume, the import and export of ICT goods account for 15% of the total import and export volume, with re-imports constituting approximately 60% of the total. Second, when examining the changes in the size of the digital economy, a noticeable upward trend can be observed, particularly in the categories of digitally deliverable services and ICT services. Additionally, the share of trade volume has been relatively stable, and the proportion of re-imports continues to show a consistent upward trend. Therefore, it can be estimated that the digital economy holds a significant share in the global economy, with a relatively significant proportion in terms of service mobility. Clearly, digital-related measures can be interpreted as a form of economic sanctions due to their potential to cause significant economic losses. Especially in the current era, where the Fourth Industrial Revolution is rapidly increasing the importance of the digital economy and driving changes in the industrial structure, similar to the previous era of globalisation and increased global trade, it is highly likely that digital sanctions will be introduced as a form of economic sanctions in international negotiations. Therefore, it is relatively evident within the current context of the expanding digital economy that digital measures can serve as a form of economic sanctions, given their potential to induce economic losses. This highlights the notion that digital-related measures can be considered as a type of economic sanction within the growing digital economy.

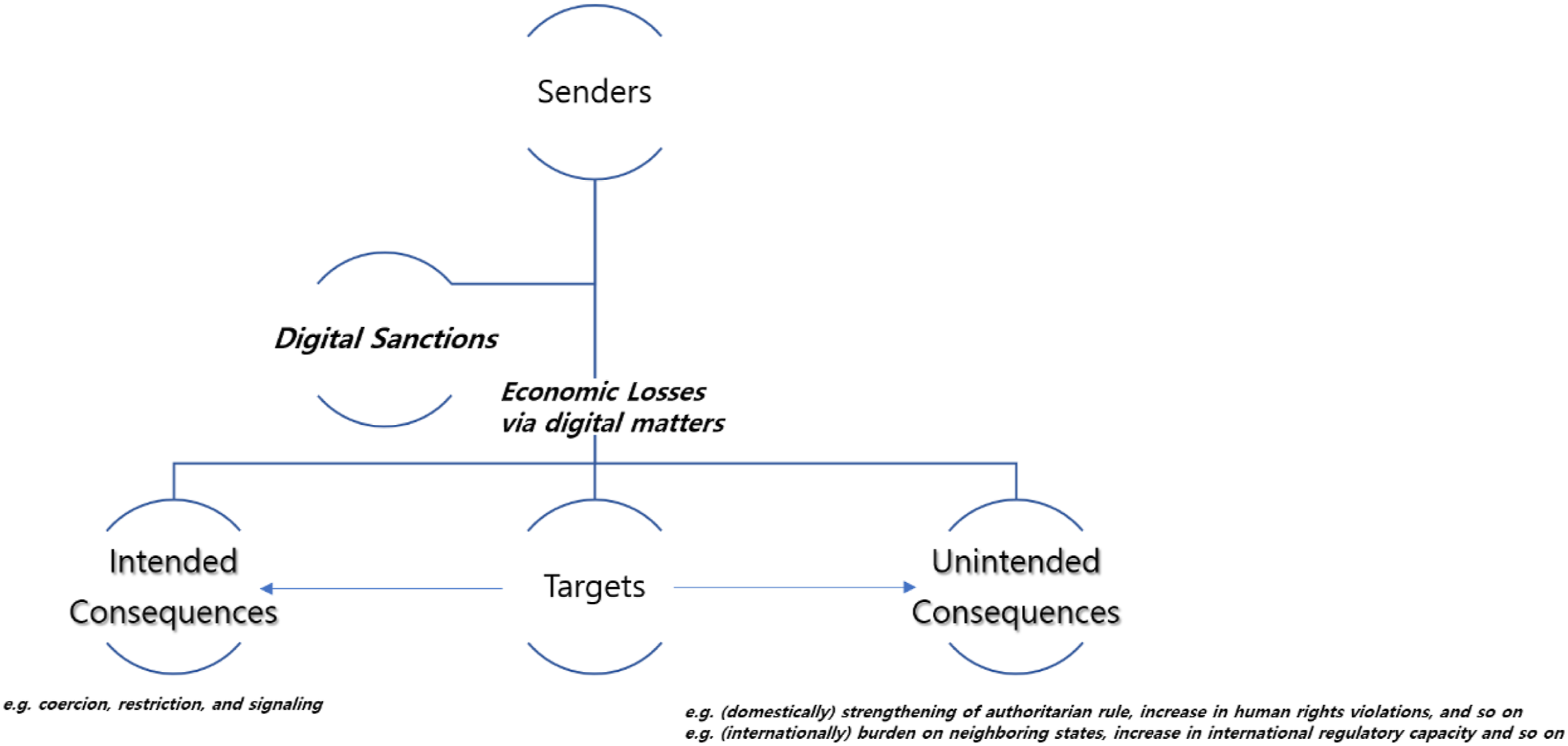

Then, what might be the intended and unintended effects of using digital-related measures as a type of economic sanctions? The primary aim of implementing sanction measures is to bring about a shift in the decision-making process of the targeted country by inflicting economic losses, regardless of the specific nature of the measures employed. Thus, within the context of the expanding global digital economy, it is expected that the digital measures implemented by the initiating parties will lead to economic losses for the targeted entities and can be strategically utilised to achieve deliberate objectives. In this context, it can be argued that digital sanctions and traditional economic sanctions share the same intended effects. Drawing from previous discussions on traditional economic sanctions, intentional effects can be distinguished and classified into three categories. It is reasonable to posit that a similar categorisation can be applied to digital sanctions. These categories include coercion and restriction, which represent the anticipated direct effects traditionally associated with sanctions, as well as the signalling effect, which is an indirect effect of sanctions that has recently gained attention (Biersteker et al., 2020). For example, when implementing digital-related measures as economic sanctions for the purpose of nuclear non-proliferation, the intended consequences align with those of traditional economic sanctions (Biersteker et al., 2020, see cases of Iran and North Korea). The objective is to apply pressure on the targeted country, coercing them to relinquish completed nuclear programs, impose restrictions on further nuclear development, and signalling a deterrent message to neighbouring nations regarding nuclear-related concerns.

Economic sanctions often lead to unintended consequences with predominantly negative outcomes. These repercussions not only affect the target country, leading to strengthened political factions, entrenched authoritarianism, heightened corruption, and human rights violations but they can also ripple out to neighbouring countries. Such consequences further influence international regulatory dynamics in the broader sphere of international relations (Biersteker et al., 2020). Research from the post-Cold War period indicates that approximately 93% of United Nations-sanctioned episodes have led to unintended consequences. The specific nature of these repercussions can vary, influenced by the particular sanctions imposed and the prevailing circumstances. Similar to traditional economic sanctions, digital sanctions are anticipated to have unintended effects. However, these digital sanctions can produce even more pronounced adverse outcomes, given their capacity to concurrently cause economic disruptions through limitations imposed on access and availability of information. Digital sanctions, for instance, engender not only economic repercussions within the targeted state by impeding the flow of digital information and services, but also harbour the potential to exert influence over information dynamics. This phenomenon holds particular significance in the context of autocratic regimes and authoritarian leadership, wherein external digital sanctions can serve as a means for a dictator to solidify their grip on power and maintain their position in office. For a holistic understanding of both intended and unintended ramifications, it is essential to view digital-related measures within the broader framework of economic sanctions (Figure 2). Digital sanctions as a new type of economic sanctions. Source: Authors.

In sum, this section has demonstrated that indeed measures targeting digital economy and development can be construed as a distinct category of economic sanctions. With the global emergence of digital economy, the relevance and applicability of these measures have become increasingly salient within the comprehensive paradigm of economic sanctions. This section has highlighted the potential intentional and unintentional ramifications of digital sanctions, drawing parallels with conventional economic sanctions. Given that digital economy is rapidly expanding globally, there is a compelling imperative to contextualise digital measures within the framework of economic sanctions. The next section will provide an in-depth examination of digital sanctions imposed by the Western powers – namely the United States and the European Union – on Russia as a retaliation against its aggression in Ukraine and their intended and unintended outcomes. In so doing, it will underscore the importance of analysing digital measures within the established framework of economic sanctions.

Digital transformation and digital sanctions against Russia since 2022

Digital transformation and strategy in Russia before the 2022 Ukrainian war

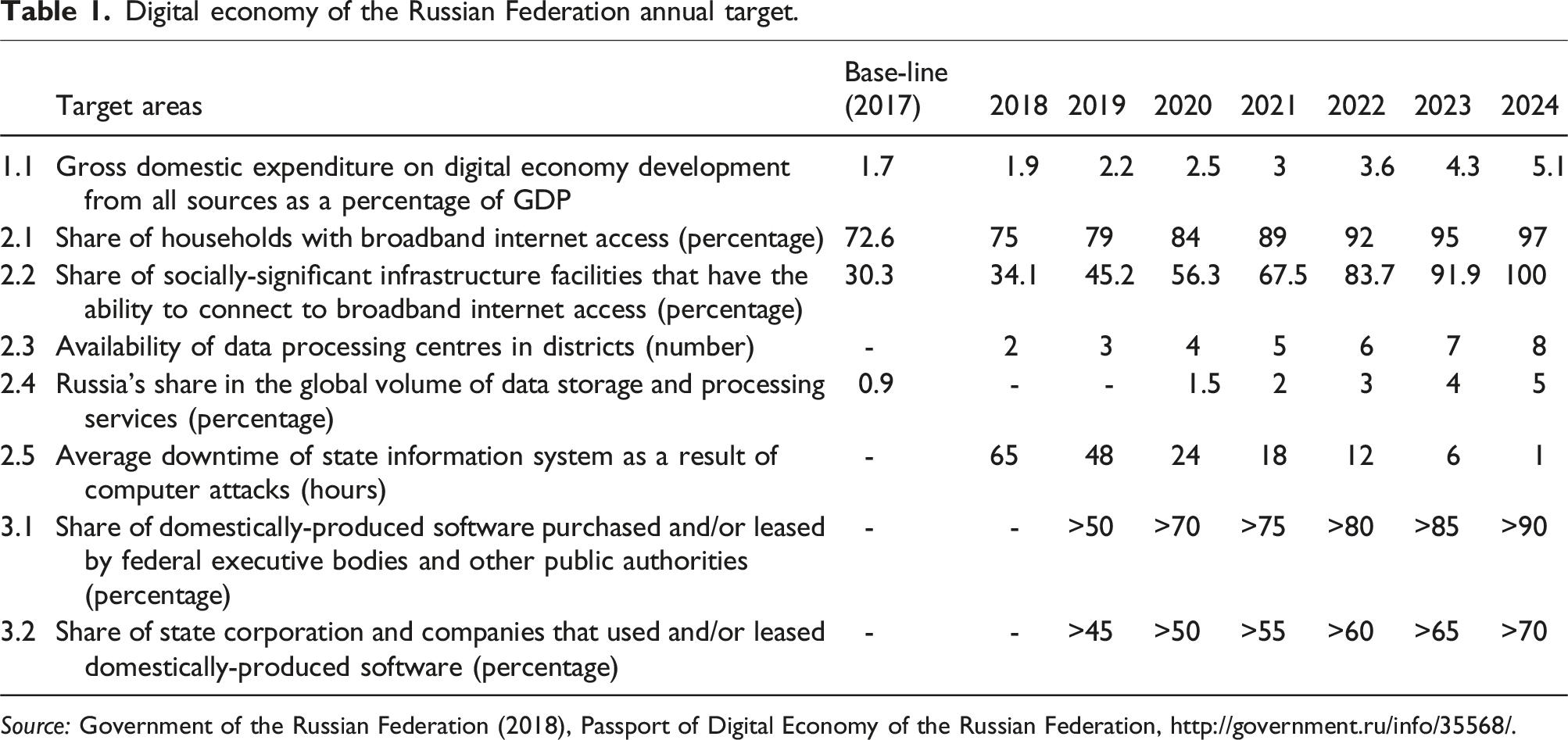

Digitalisation of Russia’s economy has become a top priority for the country’s leadership. Recognising the significance of digital transformation, the government perceives it as a crucial component of a broader agenda aimed at modernising Russia economy and steering away from its traditional reliance on raw materials and energy exports. The current national digital economy strategy aims to transform the country’s economy through digitalisation, while also fostering the growth of the digital industry sector. In December 2016, President Putin delivered a pivotal address to the Federal Assembly, emphasising the need to formulate a comprehensive digital economy program. This call to action for Russia’s digital transformation was reiterated by the President during his speech at the St Petersburg Economic Forum in June 2017. The momentum generated by these statements led to extensive discussions on the digitalisation strategy across various platforms within the country. Within a month of President Putin’s address, prominent Russian business associations and scientific communities convened meetings, seminars, and conferences dedicated to national digital economy development. In July 2017, the Presidential Council for Strategic Development and Priority Projects presented a draft of Russia’s national digital economy development strategy. This strategy was subsequently ratified in December 2018, becoming the official ‘Digital Economy of the Russian Federation’ (Tsiforovaya Ekonomika Rossiiskoi Federatsii) program. The program outlines the following set of goals: 1) Triple domestic spending in the digital economy as a share of GDP compared to the levels recorded in 2017. 2) Establish a robust and secure information and telecommunication infrastructure capable of facilitating high-speed data transmission, processing, and storage. This infrastructure should be made accessible to all organisations and households with the territory of the Russian Federation. 3) Enhance the utilisation of Russian-made software by government agencies and public organisations.

Digital economy of the Russian Federation annual target.

Source: Government of the Russian Federation (2018), Passport of Digital Economy of the Russian Federation, http://government.ru/info/35568/.

The duration of the program was between 2018 and 2024 with the budget of approximately 1,640 billion RUB (approximately 28 billion USD in 2017 value).

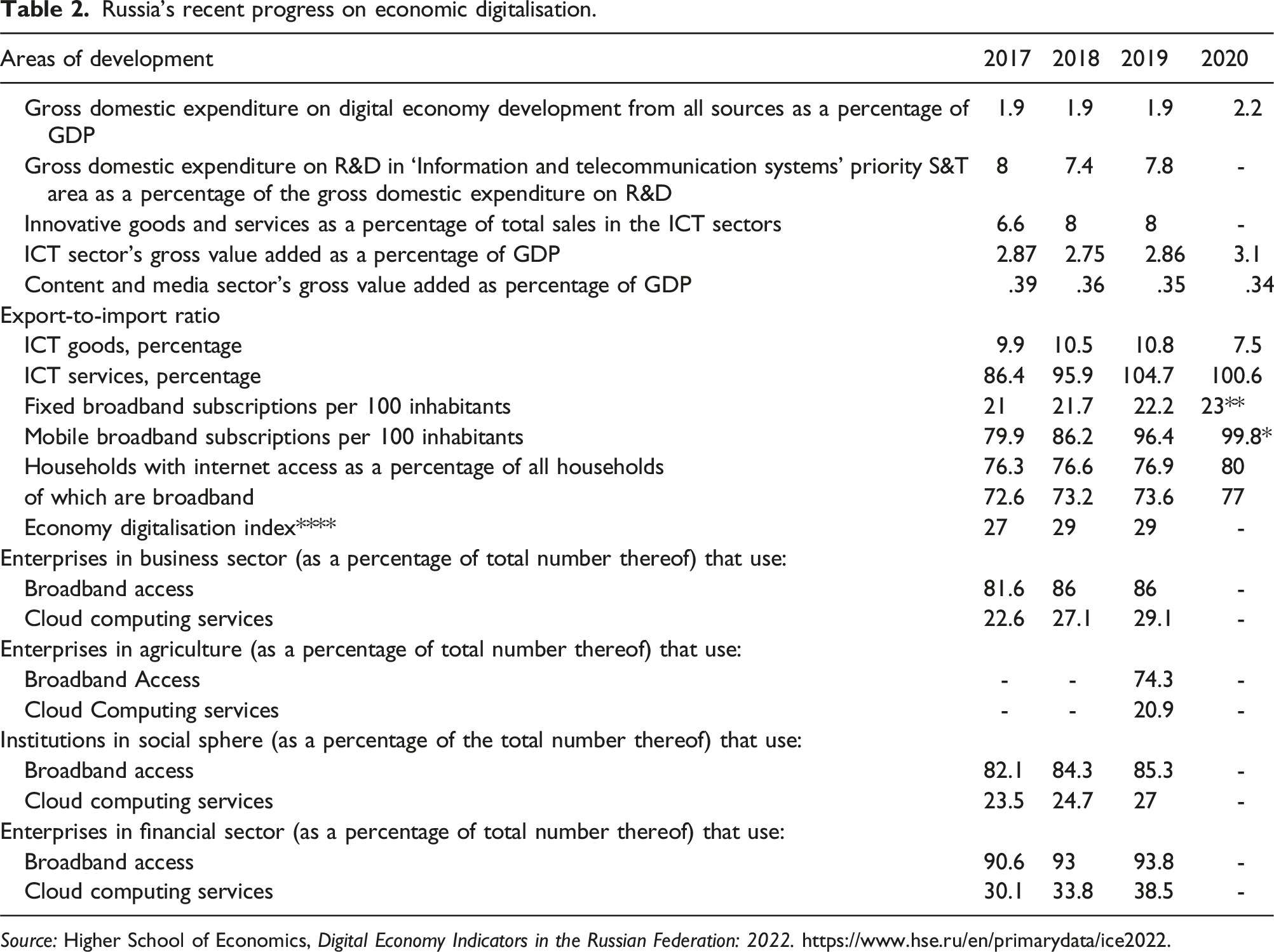

Russia’s recent progress on economic digitalisation.

Source: Higher School of Economics, Digital Economy Indicators in the Russian Federation: 2022. https://www.hse.ru/en/primarydata/ice2022.

Based on the recorded progress from 2017 to 2020, Russia’s national program on Digital Economy development has achieved mixed results. For gross domestic expenditure on digital economy development from all sources as a percentage of GDP, the program has witnessed marginal progress, moving from 1.9% in 2017 to 2.2% in 2020. This falls short of the set target of 2.5% by 2020. The percentage of gross domestic expenditure on R&D in the information and telecommunication systems priority S&T area has slightly decreased, moving from 8% in 2017 to 7.8% in 2019. The proportion of innovative goods and services in the ICT sectors has seen a modest increase from 6.6% in 2017 to 8.0% in 2019. The ICT sector’s gross value added as a percentage of GDP has shown a small rise from 2.87% in 2017 to 3.1% in 2020. However, the content and media sector’s gross value added as a percentage of GDP has slightly decreased from .39% in 2017 to .34% in 2020. Despite the shortfalls in some areas, significant strides in internet penetration and access indicate positive trends in digital inclusion, which is a key aspect of digital economy development. Broadband access has improved significantly, both in fixed and mobile broadband subscriptions per 100 inhabitants, showing progress from 21 to 23 and 79.9 to 99.8, respectively. Furthermore, the percentage of households with internet access has increased from 76.3% to 80% during this period.

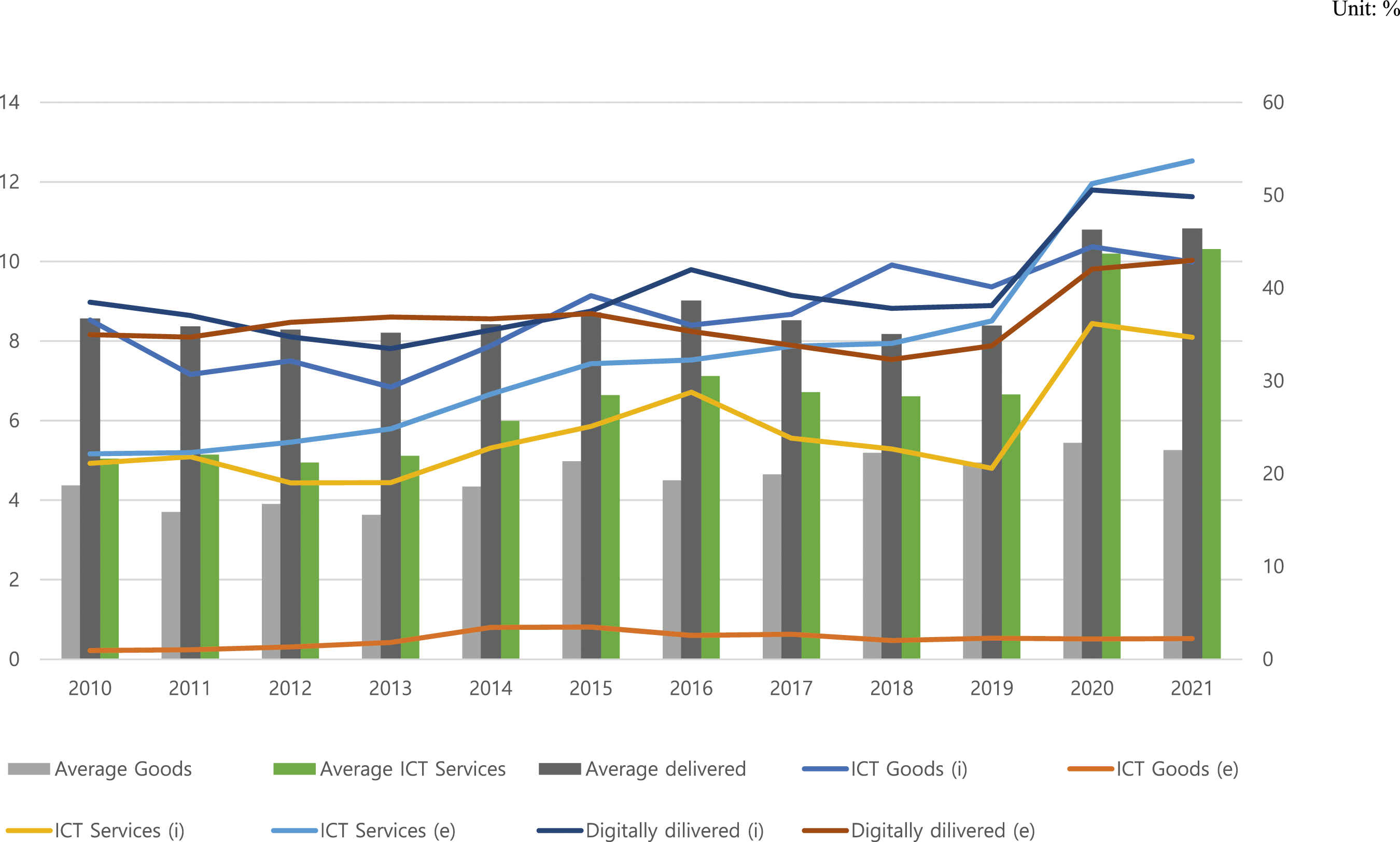

Moreover, when approaching Russia’s digital economy growth from a broader perspective through the UNCTAD data, we discover that Russian economy has demonstrated rapid expansion in terms of international trade in the sector over the recent years. The data provided by UNCTAD reveals that in 2015, digital production accounted for 19% of Russia’s total production sector. Cross-border digital activities, such as e-commerce, have also flourished, with Russian consumers increasingly procuring goods and services from international digital platforms. This showcases Russia’s significant integration into the global digital economy. In terms of digitally deliverable services, Russia’s trade data indicates a consistent average of 30–40% in its exports and imports. Particularly in 2020 and 2021, approximately 50% of the imports were classified as digitally deliverable services. As for the ICT services, there has been a steady increase in their share in trade, from around 3% in 2005 to over 10% in recent years. Specifically in exports, a sharp growth has been observed in the last three years, exceeding 12% as of 2021. With respect to ICT goods, their proportion in Russian trade stood at around 10% of imports in 2021. Compared to the 7% share in 2005, this figure signifies a consistent growth. Although the share of ICT goods in exports remains relatively low, a four-fold increase from .2% in 2005 to .8% in 2015 was recorded. This data signifies a substantial expansion and gaining importance of digital economy in Russia’s economic structure (Figure 3). The share of digital economy in Russia. Note: Digital delivered from 0% to 60% (right), others from 0% to 14% (left). Source: https://unctadstat.unctad.org/wds/ReportFolders/reportFolders.aspx.

The UNCTAD data suggests a remarkable expansion of Russia’s digital economy, marking its critical role in the country’s overall economy. A contributing factor to this growth is Russia’s successful integration into the global digital economy, underscored by a surge in cross-border digital activities such as e-commerce. The robust participation of Russia in global digital commerce and the sharp rise of imports classified as digitally deliverable services in 2020 and 2021 affirm the Digital Economy of Russia program’s effectiveness in promoting digital sector growth. The lower proportion of ICT goods in exports and the slower than anticipated growth in GDP expenditure on digital economy development indicate an increasing reliance on the global digital economy for Russia’s digital transformation. This reliance emphasises Russia’s need to integrate and align its digital strategies with the dynamic global digital economy. It also means that any sanctions obstructing Russia’s access to essential digital goods and services may cause substantial harm to Russia’s overall economy. Implications could range from hampering the growth and profitability of Russian businesses engaged in e-commerce and digitally deliverable services, slowing the nation’s digital infrastructure development, or increasing operational costs for Russian IT and telecommunication companies. Such measures may reduce the quality or increase the costs of digital services for the country’s population. Hence, sanctions of this nature could inflict significant damage to Russia’s overall economy, considering the crucial role the digital economy plays in Russia’s economic development and digital transformation.

Digital-related sanctions on Russia since the 2022 Russian-Ukrainian war

In response to Russia’s war against Ukraine which began in February 2022, the United States and its allies including the UK, Japan, Taiwan, and Singapore imposed sanctions on Russia. The European Union also adopted economic and financial sanctions, individual sanctions, and visa restriction measures in retaliation against Russia’s aggression in Ukraine. The sanctions packages include export ban on telecommunication equipment and technology that are essential for enhancing telecommunication infrastructure. The purpose of the ban is to disrupt Russia’s ability to procure Western technology and equipment in support of its military capabilities (EU Council 2022). Exporting digital computers such as laptops are allowed to private individuals not included in the sanctions list and for civilian uses only. More importantly, the sanctions also restrict exports of semiconductor devices and their parts as well as equipment and materials required for the manufacture, analysis, and testing of semiconductors. As such, these sanctions not only prevent semiconductors from entering Russia but they also significantly hamper Russia’s ability to gain technological autonomy, which is an important objective of its national digitalisation strategy. They curtail the country’s efforts to develop its own semiconductor manufacturing capabilities, stifling domestic advancements in this critical field.

In terms of digital services, the US government discussed possibility of imposing a similar restriction on virtual currency transactions and cryptocurrency mining as early as in March 2022, to monitor possible sanctions evasion using cryptocurrency (US Congressional Research Service, 2022, March 26). The “Digital Asset Sanctions Compliance Enhancement Act of 2022” introduced by the 117th Congress in 2022 suggested that “the Secretary of the Treasury may require that no digital asset trading platform or digital asset transaction facilitator that does business in the United States transact with, or fulfil transactions of, digital asset addresses that are known to be, or could reasonably be known to be, affiliated with persons headquartered or domiciled in the Russian Federation.” (US Congress, 2022, April 6). In addition, the US sanctions currently restrict US companies and individuals from internet-based communication services to persons in the Donetsk, Luhansk and any other regions in Ukraine as determined by the Secretary of Treasury and the Secretary of State. These services include instant messaging, chat and email, social networking, sharing of photos and movies, web browsing, and blogging (US OFAC, 2022, September 9). The EU sanctions adopted in October 2022, against Russia imposed a comprehensive ban on providing crypto-asset wallets, accounts, or custodial services to Russian individuals or residents, with no exceptions based on the transaction amount (EU Council 2022, October 6). This marks a departure from the previous sanctions that allowed the provision of the service up to 10 thousand EURO. Furthermore, the restrictions extend to cover a broader range of services that can no longer be offered to the Russian government or legal entities based in Russia. These include IT consultancy, legal advice, as well as architecture and engineering services. In addition, the US, EU, Canada, and the UK introduced measures to disconnect major Russian banks and financial institutions, including the central bank, from the SWIFT network used for facilitating cross-border payments. This removal was intended to economically isolate Russia from dollar-based, global economy.

The Western allies have also implemented sanctions targeting multiple Russian technology firms and institutes. These sanctions primarily focus on prominent public research and development institutes engaged in the advancement of telecommunications for both military and civilian purposes. These entities are believed to be involved in activities that raise concerns for national security or have connections to military applications. In addition to the aforementioned institutes, the US has also sanctioned companies that are engaged in the wholesale distribution of electronic equipment and components. Similarly, the EU has expanded its sanctions to encompass Russian IT companies that supply critical technology and software to the Russian intelligence community. Companies that possess licenses granted by the Federal Security Service of the Russian Federation (FSB) to handle information classified as a ‘state secret’ at the Russian security level and therefore hold specialised ‘weapons and military equipment’ licenses issued by the Russian Ministry of Industry and Trade are also listed in the EU sanction list (EU Council, 2023, June 23).

Intended and unintended consequences of the sanctions on Russia’s digital transformation

Intended consequence 1: Semiconductor shortages and its impact on daily lives

Both the EU and the US authorities have reported that the sanctions have effectively disrupted not only the Russian state’s efforts to achieve technological autonomy and have interrupted the Russian population’s closely digitally-integrated daily lives (Adam & Keijer, 2023). One of the areas most affected by the digital sanctions is procurement of key digital technologies, especially semiconductors and microchips. Semiconductors are foundational to digital transformation, driving computing power and connectivity across diverse technologies. Essential for data processing, storage, and advanced analytics, the power IoT devices, mobile devices, and data centres, enabling real-time automation, mobility, and efficient digital service delivery. Additionally, they underpin emerging technologies like AR, VR, 5G, and autonomous vehicles. Russia strategically sought to develop its own domestic semiconductor manufacturing capability, because of its essential importance in digital transformation.

In 2014, Russia annexed Crimea, provoking the West into imposing sanctions, much more lenient compared to those currently being imposed. Since then, acquiring technological autonomy by strengthening domestic technological capabilities has been a key agenda of the Russian authorities. For example, in May, 2022, a few months since the Russian invasion of Ukraine, the former president and the current deputy chair of the National Security Council, Dmitry Medvedev, proposed a shift in rhetoric concerning the replacement of foreign products with Russian ones, particularly within industry and critical technologies. He suggested that the term ‘technological sovereignty’ or ‘technological autonomy’ would be more appropriate than the previously used term ‘import substitution’ considering Russia’s particular situation (Lisitsyna, 2022, May 26). Speaking to a local newspaper, Argumenty i Fakty, Medvedev further emphasised the importance of developing home-grown products and components. He underscored that a key political priority for Russia is achieving self-reliance, reducing the need for imported parts, software, or services (Ivanov & Rukobratskii, 2022, June 28).

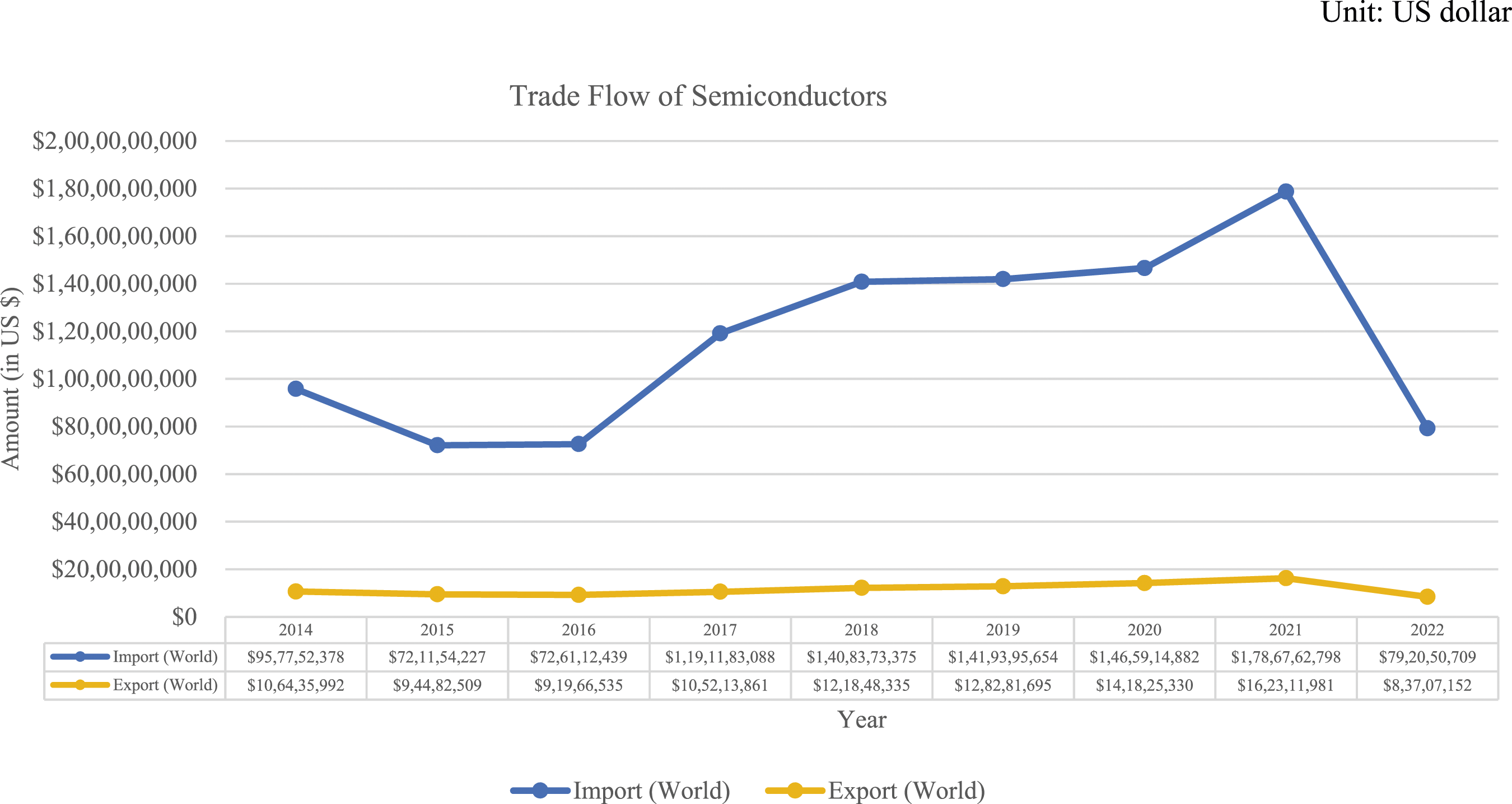

However, Russia’s ambitions for technological autonomy remain largely unrealised. Between 2014 and 2019, the import of semiconductors devices and integrated circuits to Russia increased by 60% and 25%, respectively. In addition, there has been a substantial surge in Russian imports of other electronic equipment, encompassing telecommunications and data storage systems, along with advanced machinery like gas turbines and aircraft parts since 2014. According to Washington, there has been a staggering decline of nearly 90% in global exports of semiconductors to Russia by the summer of 2022 (Alper & Freifeld, 2022, June 29). The UN COMTRADE data further supports this decline, revealing a substantial decrease in the import of semiconductors (HS codes 8541 and 8542) by Russia from countries worldwide in 2022. The trade value of semiconductors, measured in US dollars, witnessed a decline of approximately 55% compared to the previous year (see Figure 4). Similarly, the value of semiconductor exports from Russia also experienced a comparable decrease from approximately 162 million US dollars to approximately 84 million US dollars. Import and export of semiconductors to and from Russia. Source: UN Comtrade Database https://comtradeplus.un.org/.

During the months immediately following the implementation of new sanctions, news reports suggested that the decline in the semiconductors supply in Russia caused significant disruptions in the country’s manufacturing and finance sectors. For example, the Russian auto industry has been adversely affected, experiencing the most severe decline in recent history. According to Federal State Statistics Service of Russia (Rosstat), Russian automobile production plunged 47% to 264,000 vehicles in the first four months of 2022 (Sazonov, 2022, June 6). Notably, AvtoVAZ, the country’s biggest car manufacturer, had to suspend operations for two months due to component shortages and resumed with only a simplified version of its Granta model in June, 2022. Nearly all foreign assembly plants in Russia have temporarily shut down, with only the Chinese Haval facility in Tula still operating, while Russian plants have not been functioning at full capacity. Reflecting this downturn, the Russian Ministry of Industry and Trade projected a 55% drop in passenger car sales for 2022 to about 750,000 units, potentially marking the lowest sales since the financial crisis of 1998 and 1999 (Morzharetto, 2022, July 14). These severe declines, analysts suggest, are caused by disruptions in essential components from abroad including semiconductors and microchips. Meanwhile, in the financial sector, daily banking operations were interrupted by the disruptions in the microchip supply. In response to a chip shortage, Sberbank, one of Russia’s largest banks, is harvesting chips from non-activated cards. This issue arises from logistic challenges with European suppliers of microchips, and an increased demand for the domestic Mir cards after the exit of Visa and MasterCard from the Russian market since March 2022. This surge in demand resulted in a record issuance of 12 million bank cards in the first quarter of the year, totalling 341 million (Kolobova & Il’ina, 2022, July 5). To mitigate the chip shortage and its increased cost, Sberbank devised a solution to extract chips from non-activated cards and insert them into new ones, an approach expected to save the bank 1 billion roubles in 2022 (Poliakova, 2022, July 7). Russian authorities have contemplated allowing Chinese manufacturers into the market, while the Central Bank stated it would only support local producers offering reasonable prices admitting foreign competitors only if necessary.

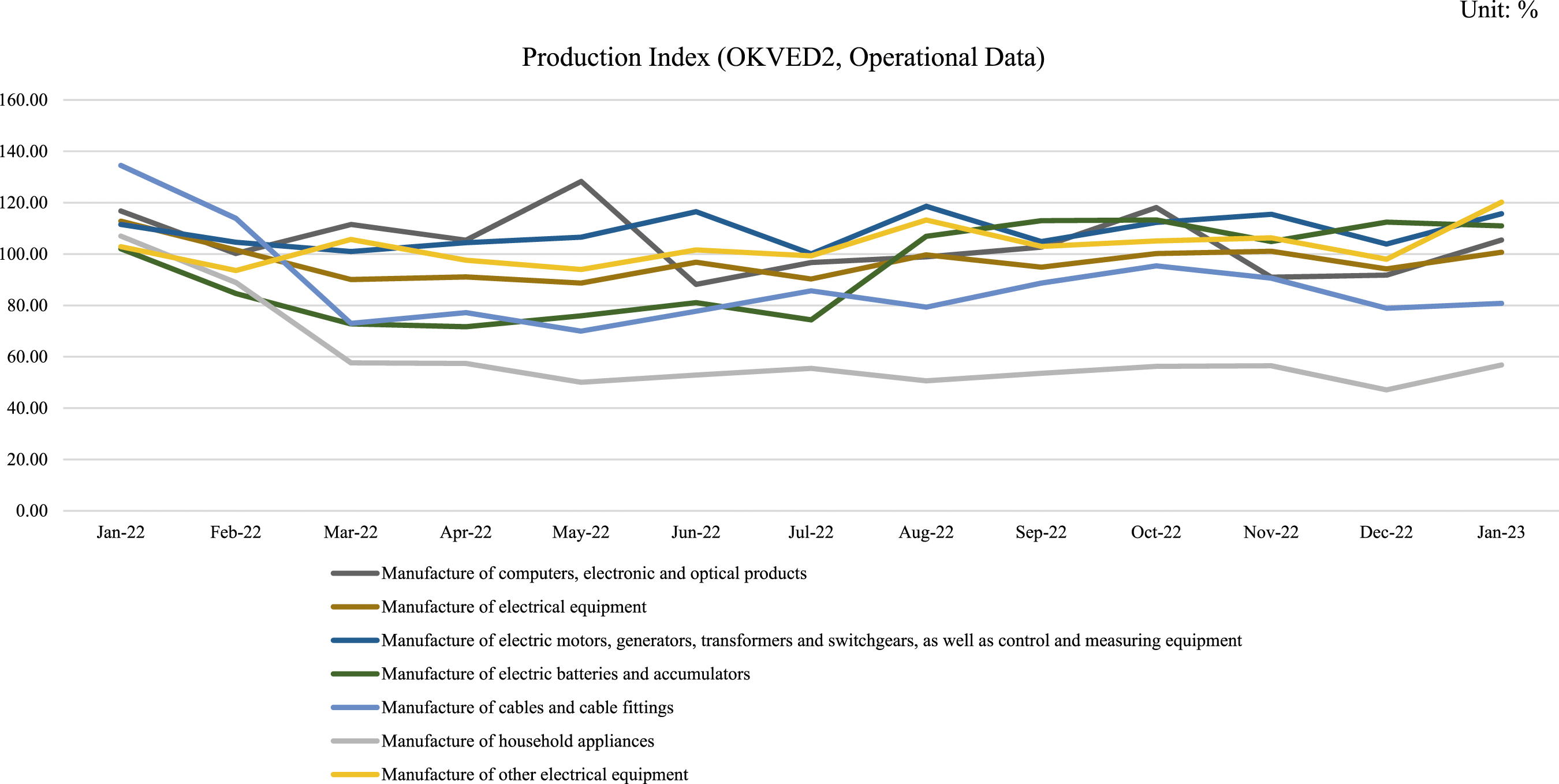

Shortage of key components that had been supplied from abroad is also affecting domestic manufacturing of digital and electronic goods. According to Rosstat data, sanctions have also had an impact on the manufacturing of digital goods as supported by Figure 5, which plots the change in the monthly production index relative to the previous month. From January 2022 to May 2023, many sectors within electronic and digital goods manufacturing saw periods of decline. For instance, the production index for computers, electronic, and optical products fell markedly to 88.2% in June 2022. Similarly, the index for the manufacturing of electric accumulators and battery accumulators decreased from 84.6% to 76% between February and May 2022. Household appliances experienced the steepest decline during this same period, with the index plummeting from 88.9% to 50.1%. Despite these downturns, most indices, with the exception of household appliances, rebounded to over 100% by early 2023, indicating recovery. The sector of electric motors, generators, transformers, distribution devices, and control-measuring apparatus displayed relative stability, with minor dips but no severe drops throughout the period under study. Production index in electronic goods manufacturing sector (compared to previous month). Source: Russian Federal State Statistics Service https://rosstat.gov.ru/.

The digital sanctions imposed by Western allies have significantly disrupted Russia’s digital economy and transformation efforts. With a reliance on foreign imports for advanced digital and technological goods, these sanctions have interfered with Russia’s pursuit of technological autonomy through home-grown digital technology development and production capacity. Notably, shortages of key electronic components, such as semiconductors and microchips, have caused disruptions to Russia’s economy and daily life. These shortages are especially impactful for items that Russia and its allies lack the technological capability to produce. In response to these challenges, Russia has turned to Chinese technology to mitigate the supply shortages caused by sanctions. For example, following the departure of leading Western cybersecurity providers from the market, Russian companies have increasingly adopted Chinese solutions, particularly for firewalls. Although current restrictions prevent Chinese companies from working with the public sector and critical information infrastructure, industry experts predict this to be a temporary barrier (Isakova & Kornev, 2023, April 6). 60% of the surveyed Russian companies plan to replace Western cybersecurity solutions with Chinese alternatives, up from just 5% in 2022. However, concerns are mounting over Russia’s potential over-reliance on Chinese technology, as senior Russian officials and the country’s Security Council fear the growing influence of Chinese firms, like Huawei and China Mobile Ltd, could compromise national information security, particularly regarding microchips and radio-electronic devices (Nardelli, 2023, April 19). Despite these worries, Russia, hindered by sanctions and cut off from foreign markets, is keen on acquiring Chinese technological components and expanding domestic production capacity, with discussions ongoing between Russian and Chinese officials.

Intended consequence 2: Disruptions in technological development and brain-drain

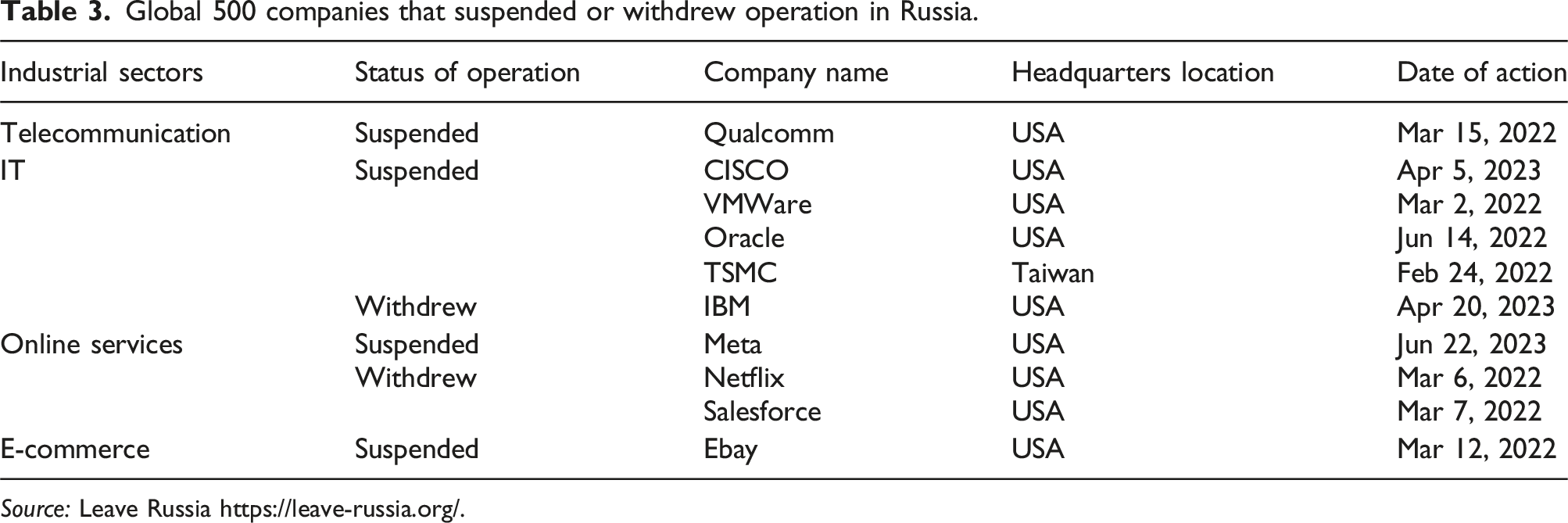

Global 500 companies that suspended or withdrew operation in Russia.

Source: Leave Russia https://leave-russia.org/.

The sanctions and the consequential exit of international IT and digital companies in the spring of 2022 sparked a significant exodus of Russian IT specialists. Sergey Plugotarenko, the head of the Russian Association for Electronic Communications (RAEC), estimated that around 50–70 thousand professionals left during this initial wave in March 2022 (Shishulin, 2022, December 27). Russoft projected that by mid-year, the outflow would have reached approximately 40 thousand IT specialists. A subsequent announcement of partial mobilisation sparked a second, larger wave of departures, reportedly two to three times the magnitude of the first. However, government officials contended that a significant portion of the emigrants, up to 85%, have since returned. The precise extent of this IT brain drain is unclear. In the first three quarters of 2022, the Federal Security Service (FSB) border service documented 17.4 million trips abroad by Russian citizens, marking a 13.8% increase from the previous year. Concurrently, Rosstat reported that by September, 419 thousand people had departed Russia since the beginning of the year, twice the amount during the same period in 2021. Although these figures don’t specify the share of departures due to the war, discernible patterns are emerging. Georgia’s President, Salome Zurabishvili, reported that around 700 thousand Russians entered Georgia following the mobilisation announcement, with about 100 thousand remaining and the rest moving onward (Martov, 2022, December 5). Marat Akhmetzhanov, Kazakhstan’s Minister of Internal Affairs, also reported that about 200 thousand Russians crossed the Kazakh border within two weeks of the mobilisation. Many of these individuals have chosen to remain, as indicated by nearly 200 thousand foreigners, primarily assumed to be Russians, applying for an individual identification number (IIN) – a requirement for employment, business operation, or extended stay in Kazakhstan – from September 21 to October 26, 2022.

The digital sanctions and subsequent brain drain have resulted in immediate and substantial disruptions to Russia’s digital economy and innovation. The cessation of operations by over 1,000 foreign firms, including major IT, e-commerce, and telecommunication entities, has created a service void, impacting various sectors and reducing digital infrastructure availability. Concurrently, a significant exodus of IT specialists has depleted Russia’s talent pool, disrupting overall sector competitiveness. Long-term effects could include decreased foreign investment and business partnerships, discouraged domestic entrepreneurship, and a lingering skills shortage within the digital sector. Despite the government’s claims of returning specialists, it remains uncertain whether this trend will continue, especially given potentially better opportunities overseas. The situation presents a significant challenge for Russia’s future digital development and innovation landscape.

Unintended consequence: Russia’s online sovereignty and internet fragmentation

Digital sanctions may also result in outcomes unanticipated by the West. While they may momentarily curb Russia’s pursuit of technological self-reliance, they could paradoxically stimulate Russia to innovate and evolve, propelling advancements in its domestic digital technology. Scholars have noted that Western economic sanctions since 2014 have indirectly spurred growth in Russian technological sectors. Specifically, Russian-based academics highlight how these sanctions positively impacted the development of Russia’s IT landscape. Ryazanova (2020) contends that by restricting global tech giants from the Russian market, these sanctions fostered a more welcoming environment for local companies, which now faced reduced competition. Kukushkina (2023) notes that the gradual imposition of these sanctions allowed Russian policymakers to adapt and counteract their effects in the promotion of domestic digital economy. Analysing Russia’s high-tech exports between 2014 and 2018, Khachaturyan et al. (2021) concur, indicating that while sanctions bring challenges, the benefits for Russia’s digital businesses have, by 2020, outweighed the negatives. This suggests that these sanctions inadvertently strengthened Russian digital industries. Other scholars (Belozyorov & Sokolovka, 2020; Komissarova et al., 2023; Solodilova et al., 2022) further posit that by focussing on the digital economy, Russia has bypassed the economic sanctions imposed by the West and ensure continued growth.

Disintegration of Russia’s domestic digital market from the global digital market could ultimately fragment Russian cyberspace from the global internet, potentially shielding its citizens from external information sources, considering the Russian state’s ambition to gain stronger control over its domestic cyberspace. The concept of “technological sovereignty” mentioned in the earlier sections, extends beyond digital hardware such as internet infrastructure. It also encompasses online content and information security perceived as a matter of national security. Scholars argue that Russia’s version of “technological sovereignty” or “internet sovereignty” often justifies the enhancement of online surveillance and state control and warn that it may contribute to solidifying the government’s authoritarian grip. For Russia, the cyberspace is similar to the physical national territory that needs to be protected from foreign interference. Litvinenko (2021) emphasises that Russia conflates cybersecurity with information security, prioritising state control over data flows. Core components of Russia’s digital sovereignty perspective include data control through filtering and localisation, and infrastructure control via protectionism and centralised monitoring. A study of the changes in Russia’s digital economy laws since 2014, especially those measures fostering technological sovereignty, indicates that the laws were partly driven by Western sanctions (Ryazanova, 2020). These policies aimed to both counteract the sanctions' effects and reduce Russia’s reliance on foreign – mostly Western – technologies due to the perceived risks of such dependence. Reinforcing this point, shortly after Russia’s assault on Ukraine and the subsequent implementation Western sanctions, the Russian government enacted a new cybersecurity law which prohibited Russian entities from using information security software produced by ‘unfriendly countries’. (Presidential Decree from May 1, 2022, No. 250).

The Russian state has implemented strict cybersecurity laws to consolidate state control over the Russian cyberspace in the recent years. In 2016, a significant shift occurred in Russia’s cyberspace regulations with the introduction of the ‘Yarovaya Law’. Under the stipulations of the law, these entities were mandated to furnish state agencies, notably the Federal Security Service (FSB), with the capability to access not just metadata, but also the content of user communications, including text messages, voice calls, and various other electronic exchanges. This was perceived by many as an attempt by the Russian state to enhance its surveillance mechanisms and gain sweeping access to personal data for intelligence and potentially suppressive purposes. The following year saw the enactment of the Law on Security of Information Infrastructure. The main thrust of this legislation was to fortify the nation’s digital infrastructure against cyber threats, ensuring its resilience and stability. The law stipulated that entities operating within the realm of Russia’s critical internet infrastructure must transition to predominantly using Russian-made software and hardware by the year 2025. The ‘sovereign internet’ laws were then introduced in 2019. At the heart of these laws was the establishment of the National Domain Name System (NSDI), a move aimed at creating an independent domain resolution system, potentially insulating Russia from the global Domain Name System (DNS) should there be a need. This step was symbolic of Russia’s pursuit of greater internet autonomy and resilience against potential international interventions or outages. The new regulations require ISPs in Russia to implement Deep Packet Inspection (DPI) technology, allowing state authorities to block online content and potentially isolate Russian internet traffic from the global network.

The Russian perception of internet sovereignty also seeks to exert dominion over the nation’s digital space, thereby contesting global notions of internet governance. Nocetti (2015) posits that geopolitics in the cyberspace realm are intricately connected to this concept, with Russia aiming to challenge the predominant Western narrative on internet governance. From Moscow’s viewpoint, internet freedom and the U.S.'s free flow of information’ doctrine are just means by which the US propagates its ideals and influence (Maréchal, 2017). Shared concerns have led both China and Russia to champion ‘internet sovereignty’ as an alternative to the perceived technological dominance of the U.S. (Budnitsky & Jia, 2018; McKune & Ahmed, 2018). The strong government control over the internet also finds resonance in the former Soviet space, especially in Central Asia (Shin, 2018; Uffelmann, 2011).

Digital sanctions on Russia thus risk deepening its drive for digital autonomy, potentially isolating Russian citizens from the global internet community. Russia’s pursuit of ‘technological sovereignty’, bolstered by legislative measures, showcases its intent to consolidate control over digital content and challenge global open internet governance norms. These actions, amplified by sanctions, could fragment the global internet and undermine principles of open access and information exchange.

Conclusion

The rapid digitalisation of global economies and the proliferation of cross-border digital transactions highlight a significant shift in global and national economic landscape. Within this context, this study explores the ramifications of digital sanctions, specifically whether they can be categorised as and conceptualised within the broader framework of traditional economic sanctions. The main premise is that recognising digital sanctions as a new type of economic sanctions can lead to more effective calibration, achieving desired foreign policy goals while mitigating unforeseen consequences. To shed light on this, the research delves into the sanctions imposed on Russia from February 2022 in the wake of its aggression towards Ukraine.

Data reveals a significant expansion of Russia’s digital economy in the recent years, closely aligned with the nation’s integration into the global digital ecosystem. However, the sanctions imposed since 2022 may present challenges to continuous growth of Russia’s digital sector, and with it, overall economy. Western sanctions have not only restricted Russia’s access to pivotal technological tools such semiconductors but also disrupted influx of digitally delivered financial and technical services such as cryptocurrency and IT consultancy. The implications of these sanctions manifest in two primary ways. Firstly, the sanctions have not only hindered Russia’s digital growth and its pursuit of technological autonomy but also had ripple effects through other industries, disrupting automobile manufacturing to banking services. The sanctions drove Russia towards alternatives, notably Chinese tech solutions, especially in the cybersecurity sector. Secondly, these sanctions have caused a ‘brain drain of IT-sector workers, crucial for digital transformation. As opportunities in Russia wane, tech professionals might look overseas, eroding the nation’s intellectual capital and impeding its innovative potential. However, the digital sanctions may also inadvertently bolster Russia’s pursuit of ‘technological sovereignty’, isolating its cyberspace and thereby limiting citizens' exposure to external information. The strict cybersecurity laws and measures, including the ‘Yarovaya Law’, signal Russia’s intent to enhance state surveillance and control. These actions, magnified by sanctions, risk solidifying the Russian state’s authoritarian grip over its population and challenging the global standards of open internet governance.

Russia’s case underscores that the rapidly changing digital landscape necessitates a re-evaluation of traditional economic sanctions, emphasising the need to recognise digital sanctions as a distinct form of economic sanctions. While digital sanctions can effectively disrupt the targeted country’s technological and economic growth, they can also result in unintended consequences. In Russia’s instance, while the digital economy faces hindrances, the sanctions simultaneously accelerate Russia’s drive for ‘technological sovereignty’, potentially reinforcing state surveillance and amplifying authoritarian control. This highlights the importance of meticulously conceptualising and calibrating digital sanctions to ensure they achieve foreign policy objectives without inadvertently strengthening authoritarian regimes. Though the research offers a holistic examination, it acknowledges the inherent challenges, particularly the informational limitations related to Russia. It is paramount in academic inquiries to articulate and define concepts with precision, more so for nascent areas of study. This research, by placing digital sanctions within the larger ambit of economic sanctions, draws attention to their layered impact on Russia. Estimating the direct economic repercussions remains intricate. Consequently, our narrative furnishes a panoramic insight into the influence of sanctions on Russia’s digital trajectory, cautioning that the full spectrum of outcomes may become apparent only over a protracted period.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This Work was supported by National University Development in 2020.