Abstract

India and Kazakhstan share deep-rooted historical relations since millennia. The spread of Buddhism to Central Asia from India and Islam to India through Babur – the founder of the Mughal dynasty – vividly reflects at least 2500 years old cultural and civilizational ties with both the regions, yet India has been perceived in Kazakhstan as a latecomer and disinterested power. While many attribute New Delhi’s lack of political willpower and economic muscle as reasons for its consistent failure in the energy sector of Kazakhstan since 1990s, this article after thorough examination holds New Delhi’s diffident policy accountable for this. Although, at the beginning of the 21st century, the UPA government led by Dr. Manmohan Singh had tried to come out of that slumber through the initiation of ‘Connect Central Asia Policy’ yet a lack of concerted effort has derailed the renewed process. However, with Modi in New Delhi as the Prime Minister of India has shown keen interests and passionate desire to tie up with the region through commercial and strategic opportunities especially with Kazakhstan in energy sector yet both the countries need a massive overhaul in their relationship to transform the short-sighted association into a broad-based strategic engagement focussing on energy cooperation. This article uncovers the irritants, misplaced imaginations and wrong assumptions that deny India a foothold in the energy hub of Kazakhstan. It therefore argues for a paradigm shift in India’s Central Asia policy which New Delhi so far has been ignoring and strongly urges India to take Russia on board while dealing with Kazakhstan.

Introduction

India-Kazakhstan relationship dates back at least 2500 years. A vivid reflection of ancient Indian texts refers to the region beyond the Hindukush as Uttara-Kuru (Stobdan, 2020: viii). As evident in various Hindu scriptures and Buddhist texts, the relationship between India and Central Asia including Kazakhstan remained uninterrupted since the days of Sakas. Mention of a trade route named Uttarapatha in ancient Indian texts depicts India’s fable Silk Route linkages with the region. A study of Mahabharata and Pali literatures also provides a glimpse of the security significance of the region for India. During the medieval era too Central Asia largely shaped India’s political history starting from Genghis Khan to Babur. Even during the classical Great Game between Tsarist Russia and the Colonial British regime the geopolitical importance of the Central Asian region remained unflinching. During Soviet times also, India has remained far engaged with the region than its neighbours yet to our strategic dismay New Delhi earned the distinction of a later comer, disinterested power and importantly a low performer. Despite deep-rooted historical relations, cultural goodwill and thorough friendship between India and Kazakhstan, New Delhi has failed to transform the short-sighted association into a broad-based strategic engagement largely focussing on economic and energy cooperation. Although, the maiden visit of Indian Prime Minister Mr. Modi to all the five Central Asian republics in July 2015 in a single tour certainly has helped in clearing the air of confusion yet a paradigm shift is what needed to add substance to what is being viewed as a symbolic visit. In this context, this article emphasizes a change of going alone approach that has precisely limited New Delhi’s presence in the region in the past and advocates for developing the Russian factor in India’s Central Asia policy not just to smoothen its entry but also to deepen its engagement in the region vis-à-vis China. This article takes the help of the Paradigm shift methodology as advocated by Thomas Kuhn to see how the Russian factor would help India to ensure its much-needed energy footprints in Kazakhstan vis-à-vis other powers in place of its old cultural and historical paradigms. With this premise, this article advocates that India must take Russia on board while engaging with Kazakhstan or to say any other Central Asian countries in contrast to what historically been projected as strategic ineptness and wrong assumptions on part of New Delhi which was laid on cultural goodwill rather than strategic engagement.

Geopolitics of Kazakhstan: An overview

Kazakhstan with an area of approximately 2.8 million sq km is ‘the 9th largest country in the world (CIA, 2021)’. Geographically consisting of almost 86% of India’s landmass, ‘Kazakhstan is also the largest landlocked country in the world (Sajjanhar, 2013)’. Situating at the intersections of Europe and Asia, Kazakhstan represents a marriage of the East and West with the significant impression of eastern values in its vibrant culture and social life while its architecture, economic dynamism signifies western orientations. Its geopolitical salience is further buttressed with its geographical positioning between Russia and China sharing long and tumultuous borders. Apart from this, what makes Kazakhstan the striking destination for international attention and global investment is its huge bases of energy reserves including oil, gas, coal, uranium and minerals such as chromium zinc and lead. Given the geopolitical and geo-economics importance of Kazakhstan for Russia, it is explicit that Kremlin would never want Nur-Sultan to go out of its geostrategic orbit. That is precisely why this article argues that despite having a multi-vector foreign policy, Kazakhstan, in reality, is intricately integrated with Russian foreign policy discourse. It can be well assessed from the U.S’s design to deracinate Russia from its traditional hinterland by playing Kazakhstan against Kremlin but utterly failed in its intent, particularly after the assertive foreign policy of Vladimir Putin divorcing from the Eurocentrism of Yeltsin. Moscow further cemented its security zones manoeuvred mechanism to regulate the Central Asian affairs and particularly to regulate Kazakhstan and to give it future direction. While Russia has taken complete control of Eurasian security, Kazakhstan in foreseeable future doesn’t likely to go against Moscow in any case. ‘The recently concluded energy trade with China is a case in point. Although the China-Kazakhstan pipeline is constructed to export Kazakhstan’s energy resources to China, in reality, the main supplier of hydrocarbons to China is Russia itself (Stobdan, 2020)’. The failure behind the Southern stream which was supposed to connect the Caspian energy with European countries was allegedly Russia. But the point of temptation is why Russia would oppose any Chinese deepening engagements in Central Asia when the Kremlin itself is a beneficiary of it and on top of all they are ideologically closer. The answer is simple: National Interest knows no ideology. It is beyond doubt that whatever initiatives China taking is intriguing with a very sinister purpose to establish hegemony in Asia to transform the global balance of power in its favour. Central Asia being an important constituent every action Beijing has been taking supposedly to counter the U.S, in reality, would also offset Moscow in the long term. Given the strategic acumen of Putin, the recent strategic manoeuvring of China in debt trapping its small neighbours to form a regional alliance and aggressive intent of territorial aggrandizement in the neighbourhood would make Russia possessive about China and its plans. Even history is evident how both the neighbours went almost to war in 1969. Despitemutual disagreements, the only factor that binds them together is the U.S. But if China sustains its robust economic development experts like Mearsheimer believes that the Russians will ally with the US (Mearsheimer, 2020). The U.S move of shifting its focus from Europe to Asia-Pacific is reason enough for Moscow to understand the new softness of Washington towards it. Further, Russia has plenty to worry about China, particularly in Central Asia. The Belt and Road of China with a strategic agenda in long term would block the Russian influence in the region; the dominance of China in SCO reduced Russia to just a mere member of the Eurasian organization; Chinese reluctance to join the Eurasian Economic Union of Russia and importantly Chinese deep inroads into Central Asian energy sectors and its control over pipelines would hinder the Russian core objectives certainly pitting Moscow against Beijing sooner than later. For, Russia, therefore, India seems to be an ideal and credible alternative given their historical friendship and superb bonding guided by mutual recognition of political and national interests to collaborate in Central Asia.

Since Russia considers India to be honest, dependable and an inevitable partner, Kazakhstan would stick to the same contours with the Russian patronage. Indeed Kazakhstan also has expressed keenness to have India in its energy market. But the indecisiveness of New Delhi in the past has to be blamed for the failure in bagging the contract attributed to its shack policies and red tap approaches. Importantly, India’s policy so far in Central Asia has been going alone discounting the Russian factor is a strategic miscalculation that India needs to rectify in days to come to taste success vis-à-vis China in the energy heartland. The country’s huge reserves of energy resources and friendly investment environment with decisive national leadership are reason enough for India to develop its keenness in Kazakh hydrocarbon resources and enriched uranium.

Why Kazakhstan is important for India?

For India, Kazakhstan is a country of strategic significance not just for oil and energy but also for its critical geopolitical positioning in the heart of Asia and strategic location between China and Russia and a key partner in the North-South Corridor project and the enriched Uranium resources. Its economic potentials and the enormous energy reserves add to her weight in international politics and lure the regional powers including India. In a nutshell, Kazakhstan for three pertinent reasons is important for New Delhi. These are 1. Geostrategic location, 2. Energy Resources and 3. Economic Potentials. While the geopolitical significance of Kazakhstan has been discussed vividly the energy resources and economic potentials will be discussed in the following paragraphs.

Also, India is aware of the huge energy reserves and production potentials of Kazakhstan which could become the potential guarantor of the much-needed energy security of India for a long period. Also, the enriched Uranium of Kazakhstan can be used for India’s nuclear reactors with no strings attached after the completion of Indo-US Civil Nuclear Cooperation in 2008. Its coal fields are also of high quality and with the North-South Corridor about to be ready; it is only a matter of time before the Kazakh coal would be used in Indian factories. That is the reason why New Delhi holds Nur-Sultan in high esteem and lays great emphasis on cementing its relationship with that country. Apart from the diplomatic ties, political activities in recent times between both countries have improved significantly. The bilateral relationship between the two countries also has marked momentous improvement in different areas including space, culture, science and technology, defence small and medium scale industries, infrastructural facilities, and notable cooperation in the energy sector. Kazakhstan remains a major energy and economic partner of India among all the Central Asian countries and that is precisely because of the energy geopolitics of Kazakhstan in the Central Asian heartland.

Energy Resources of Kazakhstan

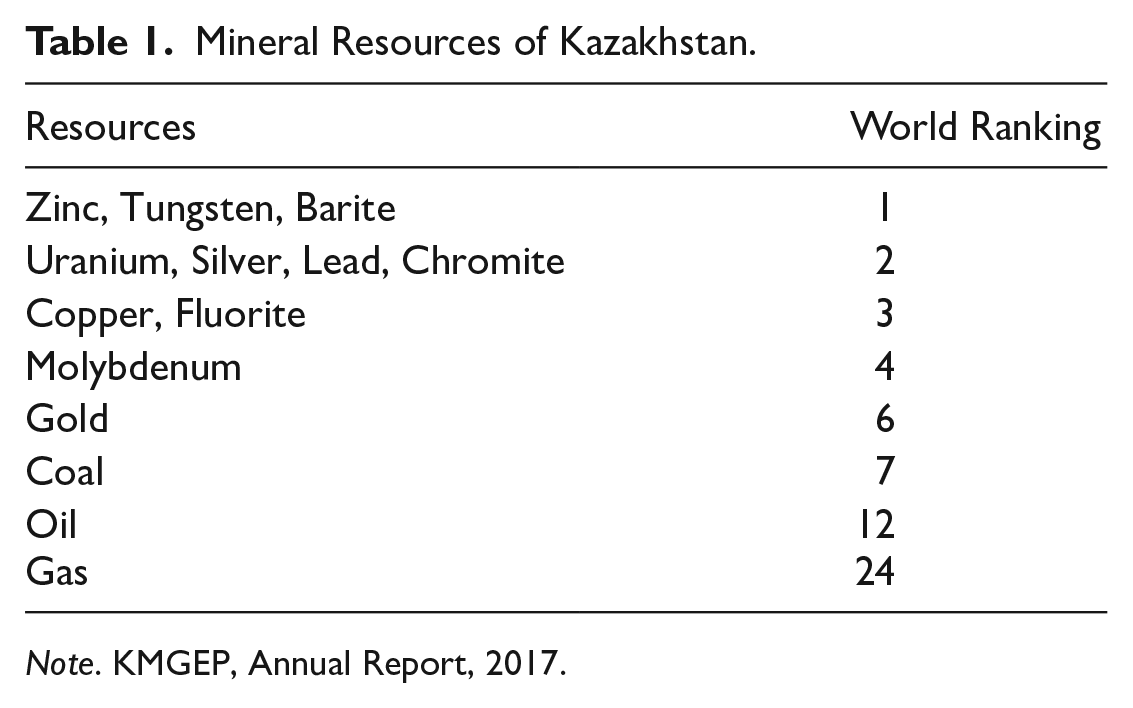

Kazakhstan is blessed with huge deposits of minerals and hydrocarbon resources. It is home to 99 types of minerals out of 105 elements in the periodic table. It has already explored 70 of these minerals and is involved in the production of at least 60. As far as Uranium, Coal, oil and gas are concerned Kazakhstan ranks 2, 7, 12 and 24, respectively, as given in Table 1 in detail. It is believed that it can lay claim to 493 known deposits containing 1225 types of mineral raw materials (KMGEP, 2017). In addition to the minerals, ‘Kazakhstan is also known to have about 1.8% of the world oil and gas reserves which are discussed below in detail (Ibid)’.

Mineral Resources of Kazakhstan.

Note. KMGEP, Annual Report, 2017.

Oil

Kazakhstan is predominantly the oil-producing country of the region with ‘at least 3% of the total world oil reserves and placed among the top 15 countries in terms of oil reserves (Stobdan, 2020: 260)’. The country as per the records of KazMunaiGaz has at least ‘172 oil fields out of which more than 80 are under development. Almost 62% of the country is occupied with oil and gas fields while 90% of the oil reserves are concentrated only in the 15 largest oil fields such as Tengiz, Kashagan, Karachaganak, Uzen, Zhetybai, Zhanazhol, Kalamkas, Kenkiyak, Karazhanbas, Kumkol, North Buzachi, Alibekmola, Central and Eastern Prorva, Kenbai, Korolevskoye (KazMunaiGaz, 2017)’. Out of 14 provinces of Kazakhstan 6 provinces are known to have oil fields. These are Aktobe, Atyrau, Karaganda, Kyzylorda, Mangystau and West Kazakhstan provinces. Among them, Western Kazakhstan is known to be fertile with oil having almost 70% of hydrocarbon reserves.

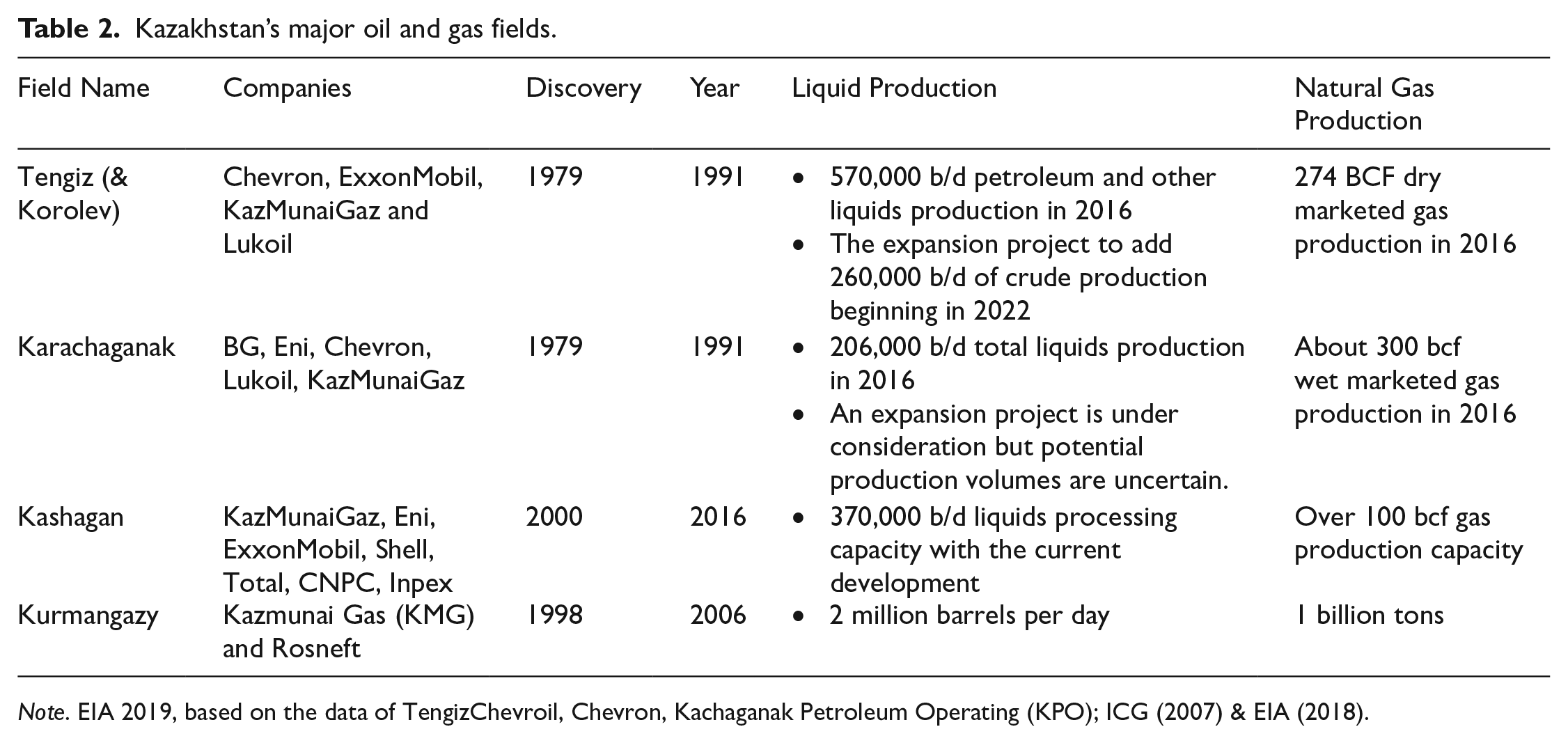

An oil producer since 1991, ‘the country has the reputation of having the second-largest reserves and second-largest oil production among the former Soviet states except for Russia (EIA, 2018)’. According to the Oil and Gas Journal, ‘tt is estimated to have between 30 and 40 billion barrels of crude oil reserves (OGJ, 2017)’ while EIA (2019) estimates the oil reserves of the country both onshore and offshore to be around 35 billion barrels as stated inTable 3. Its oil potential is ‘about half of Russia and 11% of Saudi Arabia and ranks 12th in the world, between Nigeria and the U.S in terms of oil (EIA, 2018)’. In 2016, ‘Kazakhstan’s estimated total petroleum and other liquids production was about 1.698 million barrels per day (EIA, 2018)’. However, from January to May in 2018, Kazakhstan has increased production of oil and gas condensate by 6.4% to 37.7 million tons (The Embassy of the Kingdom of Netherlands, 2018). This unprecedented boost of oil production in the early years of 2018 is ‘attributed to the increasing production level in the three major oil fields amounted to 22.7 million tons including 5 million tons at Kashagan field, 12.5 million tons at Tengiz field and 5.2 million tons at Karachaganak field (Ibid)’. Additionally, ‘the Tengizchevroil consortium decided to proceed with expansion plans that will increase liquid production in Tengiz by about 260,000 billion barrels per day by the beginning of 2022 (EIA, 2018)’. According to the estimates of the U.S Energy Information Administration, ‘Kazakhstan’s hydrocarbon reserves are contained in 153 occurrences, including 80 petroleum, 24 gas-petroleum, 21 petroleum-gas condensate, 5 gas condensate and 19 gas fields (EIA, 2018)’. Also, it has a share of 17 billion tonnes or 124.3 bbl in its part of the Caspian sea basin. In 2017, the Ministry of Energy of Kazakhstan in its report stated that the oil production was at 81 million tonnes and expected to grow to 88 million tons by 2020 (Stobdan, 2020: 260). Most of Kazakhstan’s oil growth in petroleum, however, comes from the four large oil fields. The details about them are given in Table 2.

Kazakhstan’s major oil and gas fields.

Note. EIA 2019, based on the data of TengizChevroil, Chevron, Kachaganak Petroleum Operating (KPO); ICG (2007) & EIA (2018).

The tengiz field

This field is discovered in 1979 in Atyrau province. It is the sixth-largest oil reserve in the world (International Crisis Group, 2007: 7). Tengiz is distinct and matchless when it comes to known and rival petroleum and gas deposits of the world. Although ‘the deposit has been explored to a depth of only 5500 m, its potential recoverable reserves are estimated at 6–9 billion barrels of petroleum by consortium member Chevron Texaco (Zhanseitov and Asanov, 1993: 388)’. In 2007, ‘Chevron is the leading partner (50%) in the Tengiz Chevron Oil (TCO) consortium that has developed the field since 1993 and operates at 50/50 production sharing with the government (International Crisis Group, 2007: 7)’.

In 2016, Tengiz contributed about 35% of the country’s oil production (EIA, 2018). Besides, it has decided to partner with the Future Growth Project in a bid to expand its productions. As per the estimates of the Energy Information Administration (EIA), ‘the liquid production capacity of Teniz in 2016 is about 570,000 b/d petroleum and projected to add 260,000 b/d of crude production beginning in 2022 with the expansion of the field (2019)’. As stated in Table 2 this field in 2016 has also produced 274 BCF dry marketed gas (EIA, 2018).

The Kashagan field

The Kashagan oil field was discovered in 2000 in the northern Caspian Sea basin. According to EIA, ‘it is the largest oil field outside the Middle East and is the fifth largest oil field in the world in terms of reserves (EIA, 2018)’. Kashagan spreads over an 80 km × 25 km field and is located near Atyrau off the northern shore of the Caspian. ‘Its recoverable reserves are estimated to be around 7 to 13 billion barrels of crude oil. As of January 2017, the field was producing more than 100,000 billion barrels per day (EIA, 2018)’. According to EIA (2018 & 2019), this field has a production capacity of about 370,000 b/d in oil while the production capacity in gas has been 100 bcf as stated in Table 2.

The karachaganak field

Discovered in 1979, ‘the Karachaganak field is an oil and natural gas and condensate field located in Western Kazakhstan province (International Crisis Group, 2007: 7)’. According to the estimate of Karachaganak Petroleum Operating (KPO), ‘the reserve of the oil field is about 1.2 billion tons and condensate of approximately 8.76 billion barrels (Ibid)’. However, the field is expected to be surprised by growth potentials as several geological structures were not covered under the estimates of the current survey. This field in 2016 has produced around 206,000 b/d of total liquids while the wet marketed gas production has been about 300 bcf in the same year (EIA, 2018). See Table 2 for details.

The Kurmangazy field

The Kurmangazy field – located near the Russian maritime border in the Caspian Sea basin – is among the first four fields developed in the earliest stage of energy exploration (ICG, 2007:7–8). As per the agreements signed in 1998 and the protocol of 2002 between Kazakhstan and Russia, Kazakhstan was given sovereignty over this field whereas two nearby fields were accorded to Russia (Ibid). The Kurgmengazy partners are Kazmunai Gas (KMG) and Rosneft and are supposed to develop under 50: 50 PSAs (Ibid). The reserves of the field are estimated to be around one billion tons. The first well started operating in 2006 (Ibid). Kazakhstan is optimistic about the full utilization of the resources of this field which will boost the country’s oil production of over 2 mb/d to place itself among the top eight non-OPEC countries of the world. Table 2 especially is designed to provide details regarding the oil and gas fields, their year of operation, companies involved in exploration activities, production capacity both in terms of oil and gas.

Kazakhstan until 2006 had operated only three oil refineries namely, ‘Pavlodar, Shymkent (formerly Chymkent), and Atyrau located in the northern, southern and western regions of Kazakhstan, respectively (Dorian, 2006: 546)’. According to the EIA estimates, ‘the refineries have a combined total crude oil refining capacity of 427, 000 b/d (20 million metric tons per year) and capacity utilization of 95% (EIA, 2004)’. In 2006, about 10 million metric tons of Kazakh crude oil was processed annually in all three refineries combined. But, ‘the import was relatively small amounts of product to make up for slightly inadequate domestic refinery output, notably at harvest time (International Crisis Group, 2007: 8)’. Since the crude oil production in 2016 was about 54 million metric tons, ‘net crude oil export was set to be about 41 million metric tons (about 820, 000 bbl/d). Outside OPEC, only Russia, Norway and Mexico export more (EIA, 2016)’.

Kazakhstan is the highest producer of oil among the non-OPEC countries with the potential to raise its oil production level at times of requirement. Although, the domestic energy consumption of Kazakhstan is set to grow shortly, however, the diminutive population and the hefty addition expected in production will certainly translate the productions into exports. According to EIA, ‘Kazakhstan is an exporter of light and sweet crude oil. In 2016, it has exported about 1.3 trillion barrels per day as per the estimate of EIA (2018)’. Until 2009, Kazakhstan’s crude exports were mostly confined to the European Countries. However, since 2009Kazakh oil started going eastward to China. Although a significant portion of oil exports transit through Italy and Netherland, an additional 5% of Kazakh crude oil also goes to China (EIA, 2018).

Natural gas

Kazakhstan with proven natural gas reserves of around 85 tcm, ranks eleventh in the world (OGJ, 2017). Kazakhstan in total has 83 natural gas deposits. Among these only 17 are exclusive gas reserves while other deposits include oil and associated gas reserves (Dorian, 2006: 546). Besides, Kazakhstan has about 31.8 billion tons of additional proven reserves in the Caspian Sea basin. This has propelled the country to the second position in Central Asia after Turkmenistan in terms of gas reserves and production capacity (see Table-3 for details) (Stobadn, 2020: 261). While more than 40% of gas reserves of the country are located in the huge Karachaganak and Tengiz fields, the remaining gas fields are unevenly scattered all through Kazakhstan (EIA, 2018).

Coal

As given in Table 3, Kazakhstan has recoverable coal reserves of about 28,225 million short tons (MMst). The country in terms of coal production, export and reserves is placed among the top ten countries in the world. Simultaneously, it also ranks among the top fifteen coal consuming countries of the world. According to the EIA report, ‘despite being among the top coal producing countries, Kazakhstan is a relatively small contributor to global coal volumes. The top four countries globally account for disproportionate shares of total global coal reserves, production, consumption, and exports (between 65% and 75% combined), while Kazakhstan accounts for between 1% and 4% (EIA, 2018)’.

Kazakhstan’s Energy Resources.

Note. EIA, 2019; OGJ, 2017; KMGEP, 2017; KazMunaiGaz, 2017 and WNA, 2020.

Uranium

Kazakhstan has the largest base of world Uranium. It is indeed the largest Uranium producer in the world (EIA, 2018). Despite closing down of its only nuclear power plant in 1999, ‘Kazakhstan has been an important source of uranium for more than fifty years’. During the years from 2001 to 2013, ‘the production of Uranium in Kazakhstan has risen from 2022 to 22,550 tonnes U per year (Ibid)’. Of its 17 mine excavation projects, ‘five are wholly owned by Kazatomprom and 12 are joint ventures with foreign equity holders, and some of these are producing under nominal capacity (WNA, 2018)’. In the year 2016, Kazakhstan produced an unprecedented amount of Uranium making it the largest producer in the world contributing about 21% to global production. In this endeavour, Kazatomprom along has contributed around 12,986 tU. As per the reports of World Nuclear Association, ‘in January 2017 Kazatomprom said that production would be reduced by about 10%, due to low prices in December 2017 Kazatomprom announced that the reduction would be 20% from 2017 levels, enacted over three years (Ibid)’. after the announcement, the country has reduced the production capacity to 11,000 tonnes of natural uranium. In May 2018, ‘the country’s energy minister announced that the production target for 2018 is set at 21,600 tU (WNA, 2018)’. In fact, in 2019 it has produced about 22,800 tU of Uranium as stated in Table 3. As such, ‘Kazakhstan has 15% of the world’s uranium resources (WNA, 2020)’. Set up in 1997, ‘Kazatomprom is the national atomic company and owned by the Kazakh government. It controls all uranium exploration and mining as well as other nuclear-related activities, including imports and exports of nuclear materials ( KazAtomprom, 2010)’. In 2008, Kazatomprom had announced that, ‘it will supply 30% of world uranium by 2015 and it had produced 39% through joint ventures: 12% of the uranium conversion market, 6% of enrichment and 30% of the fuel fabrication market by then (WNA, 2018)’.

Since it has massive uranium deposits and potential for production, Kazatomprom has inked strategic links with major countries of the world including Russia, China, India and Japan. It also owns major shares in ‘Westinghouse’ international nuclear company. Besides, companies from Canada and France are involved in the mineral-rich country for uranium mining. A country like India is also stepping into the shoes like other actors in the region for gaining access to the uranium resources of Kazakhstan.

Export Routes and Refinery Facilities

Since Kazakhstan is a landlocked country, supply of oil through the pipeline has always been a formidable challenge for the Eurasian country. The state-run KazakhTrans Oil a subsidiary of KazMunaiGas is in charge of operating the pipelines that transport Kazakh crude oil. As noted above due to its geographical compulsions it has either to depend on the Soviet-era infrastructure or the oil and gas transportation routes of the companies exporting the Caspian energy resources (EIA, 2018).

Besides the Caspian Sea routes, Kazakhstan also transports its oil through trains. Especially at the Aktau and Atyrau fields, ‘oil is loaded into tankers and then shipped across the Caspian Sea, where it is loaded onto the Baku-Tbilisi-Ceyhan pipeline or the Northern Route Pipeline (Baku-Novorossysk) for onward transportation (EIA, 2018)’. Apart from the rail networks through which Kazakhstan transports its oil to other neighbouring countries, one such potential route like BCT pipeline exports to Iran via the Caspian Sea port of Neku (Ibid). Although no such swap has been operationalised until now yet both Iran and Kazakhstan are mulling to resume the trade arrangements through mutual negotiations since 2013. If this starts operating, Kazakh oil will have access to the South Asian and African Market. Importantly, after the recent modalities reached upon by Iran and India on Chhabbar port, it will allow India to have access to the Central Asian oil which it can then load onto the tankers to India via the Arabian Sea.

In a nutshell, the Kazakh oil distribution networks for export purposes are spread in three different directions. These are: ‘The Northward (via the Russian pipeline system and rail network), Westward (via the Caspian Pipeline Consortium (CPC), project and barge to Azerbaijan), and Southward (via swaps with Iran) (EIA, 2018)’. The CPC pipeline was Kazakhstan’s main line for exporting the Caspian Sea. There are further plans to increase its carrying capacity. The other manner through which Kazakhstan exports its Caspian oil is by barge to Baku, Azerbaijan, Neka and Iran. It is still looking to increase pipeline and rail shipments to China or shipments to Baku for transportation on the BCT pipeline.

Besides, Kazakhstan has a built-in facility for refining its crude oil before it is loaded for transportation. According to EIA as of January, ‘the country had three major oil refineries with a crude oil capacity of 340,000 barrels per day. Pavlodar, Atyrau and Shymkent are the three major oil refineries in the country (EIA, 2019)’. Besides, Aktau has a very small refinery meant to process raw crude oils produced at the nearby fields (Ibid).

Apart from Oil transportation routes, the country also has developed two divergent gas supply systems as well. According to EIA, ‘One is in the west, which services the nation’s producing natural gas fields, and the other in the south which primarily delivers imported natural gas to the southern consuming regions (EIA, 2018)’. In 2016 alone, Kazakhstan exported natural gas of approximate 22.3 billion dollars in comparison to its 2007 estimate of about 408 tbl/d northward via Russian pipelines and rail; 620 tbl/d westward via the CPC; 70–80 tbl/d southward via oil swap with Iran; and 85 tbl/d eastward via the Atasu-Alashankou pipeline (EIA, 2009; UNESCAP, 2018).

The strategic location of Kazakhstan also makes it an important transit route not just for its energy resources but also for the oil and gas exports from Turkmenistan and Uzbekistan. Similarly, the Russian pipeline: the Central Asia Center (CAC) gas pipeline – controlled by Gazprom runs through Beyneu in Kazakhstan before entering into the Russian pipeline network at Alexandrov Gay. Two branches of this CAC pipeline network carries the Uzbek and Turkmen gas including the gas produced from Tengiz and Karachaganak fields in Kazakhstan. Over the years a number of pipeline routes for transportation of gas from the Caspian region have come up largely attributed to the involvement of major energy consumers of the world. This has led to the opening up of the Kazakh energy market for the world. While its northern and eastern routes are developed to a greater extent, NurSultan is in talks with Iran to transport its oil and gas to the southern direction which would indirectly benefit India to meet its hydrocarbon requirements.

Energy policy of Kazakhstan

Kazakhstan is a country of great importance to Europe, Asia and the region as well. It has emerged as a regional leader and an example of successful economic development for the rest of Eurasia’s New Independent States (NIS). With estimated oil reserves of 39.8 billion barrels, proven natural gas reserves of 105.9 trillion cubic feet (3 trillion cubic meters), (British Petroleum 2007:6, 20, 22). Other natural resources, such as uranium, coal, and metals, and a fast-growing services sector, Kazakhstan’s future looks promising to its people and attractive to foreign investors. Kazakhstan possesses huge hydrocarbon resources inside its territory and in particular on the coast of the Caspian Sea, which is equal to 33% of the whole coastline of this sea. After Russia, Kazakhstan ranks second in oil and gas resources among former Soviet states. This is why energy is the most important factor in Kazakhstan’s external policy.

Mainly, there are two important pieces of legislation regulating foreign investment into Kazakhstan’s energy sector (Griffin, 2008). The first is the ‘Republic of Kazakhstan Law on Petroleum,’ originally passed in June 1995. The other is the ‘Law on the Subsurface,’ passed in January 1996 (Ibid). Both laws, however, have gone under tremendous change since their original introduction more than a decade ago.

The Subsurface Law has the wider scope of the two pieces of legislation. It outlines the rules and regulations for an investor to acquire a ‘subsurface-use right.’ In Kazakhstan, the subsurface use right is equivalent to a license or a concession in other jurisdictions. In oil and gas projects, it is granted upon the execution of a ‘Hydrocarbon Contract’ between the ‘Competent Body’, that is, the Kazakhstan Ministry of Energy and Mineral Resources and the producer, known in Kazakhstan typically as the ‘Contractor’ (Griffin, 2008). The Petroleum Law is in some ways an addendum to the Subsurface Law in that it regulates petroleum and gas projects.

One important feature of Kazakhstan’s energy law is the government’s pre-emptive purchase right to produce hydrocarbons. Previously, the Petroleum Law required the Kazakh Government to pay a ‘world-market price’ for any hydrocarbons that it received from producers. The 2007 Amendments now provide that petroleum acquired by the government under pre-emptive right from the Contractor be compensated ‘at prices not exceeding world-market prices’ (Barry 2009: 46). This is significant because it means that the Kazakh Government now has the choice of negotiating down the price, instead of automatically paying the world market price.

In the early years of independence, the newly born nation had to face several alternatives in the energy policy-making field: the road to full nationalization and transfer of some energy to private sectors. While the latter is a completely Russian model, the former has a Middle Eastern base. However, both scenarios included risks – Kazakhstan could become a ‘banana republic’ – a raw material appendage of Russia or the West. It could also become internationally isolated and squander its energy potential.

Kazakhstan’s declared policy of openness to foreign investment and its assurances of political support for pipeline routes did not have an instant effect. International oil companies wanted firm guarantees for their investments, demanded protection from nationalization and introduced taxation stability clauses into their contracts.

In his 1997 annual State of the Nation Address, the president of the Republic of Kazakhstan Nursultan Nazarbayev emphasized that the opportunities offered by Caspian mineral wealth have potential dangers: Our natural resources are an enormous wealth. Ironically, world experience shows that many countries with natural resources were not able to dispose of them properly and never came out of poverty. The East Asian countries, poor in natural resources, have demonstrated the most dynamic development. These examples highlight that the people, their will, motivation, persistence and wisdom, primarily determine the development outcome (Nazarbayev, 2008).

Ultimately, Kazakhstan opted for a balanced approach, with proper consideration for the interests of all the world powers involved in the region, by opening access to the international oil companies. The Kazakhstani leadership considered this strategy to be consistent with the country’s foreign policy priorities, believing that Kazakhstan would be able to maintain partnerships with key players in the region and utilize oil revenues towards achieving sustainable economic development.

In deciding in favour of foreign direct investment, according to Ariel Cohen, ‘Kazakhstan was becoming one of the few oil-rich countries that are open to foreign companies’ (Cohen, 2008: 118). In a short time, Kazakhstan undertook a series of legislative initiatives and became the most attractive CIS country for foreign investment (Shiells, 2007). Interestingly, the country did not apply the model is used in opening the energy sector to foreign capital to other sectors of the economy. Thus, protectionism and reliance on internal resources dominated the financial sector, the media, and other markets (The Heritage Foundation, 2008).

Despite its declared policy of limiting government interference in the economy, transnational corporations contending for a slice of the ‘Caspian cake’ had to undergo rigid screening. The Kazakh government has given preference to internationally recognized companies interested in developing long-term projects and is ready to take into account the country’s domestic interests. They have to emphasize environmental safety programs, train local staff, and exercise corporate social responsibility. Transnational companies, such as ChevronTexaco, ExxonMobil, Agip/Eni, Royal Dutch Shell, British Group, Total, Fina, Elf, Impex and others have emerged as the winners in this race.

Second-wave investors – Canadian, Middle Eastern, and Russian companies – have been rapidly establishing their presence in the Caspian region. China’s desire to strengthen its role became more obvious in 2005 and 2006, with Russia’s presence on the increase and American influence on the wane. With Chinese and Indian extractive and financial corporations entering the scene, the interests of all major world players are represented in the Caspian region.

The arrival of Multi-National Corporations (MNCs) demanded the construction of a system to export oil and gas. As Kazakhstan is a newly independent republic, it lacks the infrastructure to develop the giant fields and connect them to the international oil markets. The Soviet-era oil and gas infrastructure tied it to Russia for access to ports and external markets, especially in Europe. Russia, in turn, insisted on maintaining control over the energy transportation routes and opposed any project that could provide Central Asian producers with alternative export channels. This underdevelopment of the petroleum transportation system still limits the exploration and production of the largest Caspian fields.

To realize the full potential of its oil fields, Kazakhstan has to assure export routes that would guarantee its ability to fill the demand for ‘black gold’, particularly to the West, China and India. Nazarbayev is also aware of respecting the interests of all the major players in the Caspian region, namely the West, Russia, and China. It may enhance the stability of the energy sector in Kazakhstan. This approach would facilitate a balance of power in the region, keeping major players in check.

To conclude, Kazakhstan’s overall potential is immense. Its territory is four times that of France. It currently surpasses Kuwait in its oil production and expects to export 3 million barrels of oil a day. Kazakhstan also has some of the largest reserves of uranium on the planet and is a major exporter of grain. Kazakhstan’s economic and political reform agenda is largely on track, despite setbacks caused by the spread of global financial instability.

Kazakhstan and India’s energy security concerns

As we know, India with a 1.32 billion population ranks second in the world. But relative to its populace, she is inadequately endued with energy assets. In fact, ‘its share in the world population is 17% whereas the shares in the world coal, oil and gas are only 7%, 0.4% and 0.6%, respectively (NITI Aayog, 2017).’ This means the domestic energy resources of India are insufficient to meet the bourgeoning needs. Thus, India has to depend on imports heavily despite a very low intensity of energy utilization. Although, ‘India is the eighth largest producer of energy in the world with 2.4% of world’s total energy production is also the third-largest energy consumers in the world with 3.7% of global energy consumptions (EIA, 2018).’ With this rate of energy use, its consumption rate is projected to grow at 4.2% per year through 2035 (The Economic Times, 2017). India’s domestic coal reserves of 293.5 billion tons with an annual production of over 739.92 million tons (Ramachandra & Hegde, 2015). According to NITI Aayog, ‘Coal constitutes the largest energy source of India with almost 44% followed by traditional biomass and wastes 24% and petroleum and other liquids with 23% while other renewable fuel sources make up a very small portion of primary energy consumption (NITI Aayog, 2017).’ Since the population of India especially after the dawn of Liberalization, Privatization and Globalization has been moving more and more to the urban centres, the fuel use pattern has shifted from fossil fuels and waste to utilization of electricity meant for cooking, heating and lighting. ‘Power sector in India is one of the fastest-growing areas of energy demand rising from 11% to 15% of total energy consumption between 2000 and 2013 (EIA, 2018)’ and projected to grow at 26% by 2040 (NITI Aayog, 2017). According to the estimates of IEA, ‘about 240 million people in India (almost 19%) lack basic access to electricity as of 2013; although the rate of electrification in India been growing since the NDA government came to power in 2014 under the leadership of Prime Minister Modi (2015).’ The remaining 33% is met by oil and gas with more than 65% of it being imported, mainly from the Middle East (NITI Aayog, 2017).

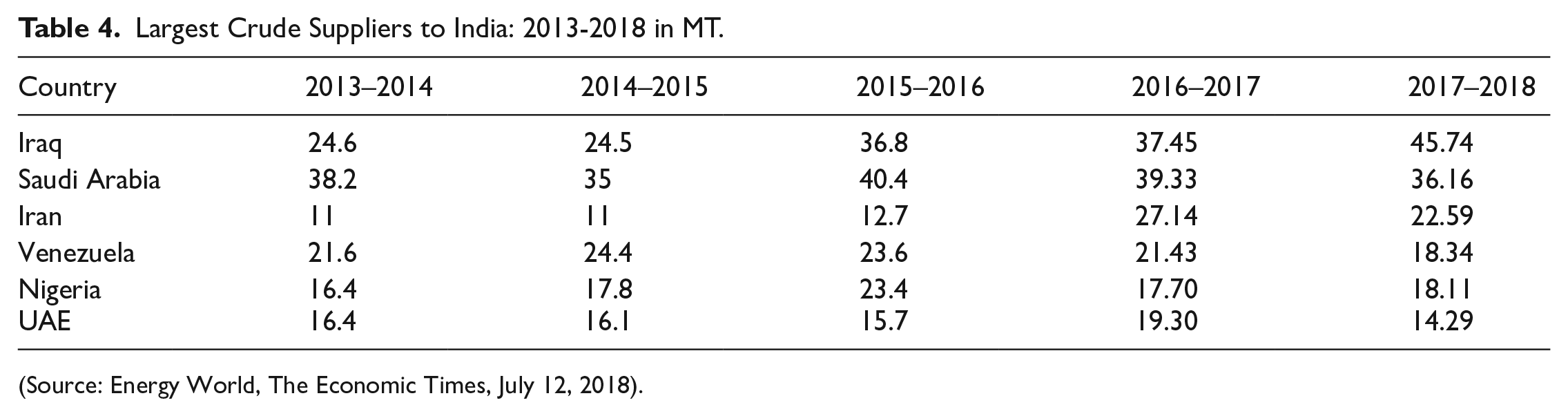

Until 2009-10 Saudi Arabia and Iran have been the main crude oil import partners for India (EIA, 2009) but with the increasing dependence on crude oil, the trajectory of India has changed and as of June 2018 as shown in Table 4 Iraq is the main import partner of India followed by Saudi Arabia and Iran. To be honest, ‘India’s crude oil imports from Iran jumped to a staggering 52% to 2.57 million tonnes (MT) in June 2018 as per the revised data sources of Director General of Commercial Intelligence and Statistics (DGCIS, 2018).’ In the scenario of inadequate domestic production, the government of India expects this import dependence to rise in future. Although, few discoveries in the domestic front have taken place in recent years but they are not supposed to alter the energy mix and profile of India given their smallness in size and low production capability. In this scenario, India’s overdependence on energy imports is going to stay at least in the short term, especially in terms of oil usage. In this light, ‘International Energy Agency estimation predicts that with the current level of reserves and production, India’s oil dependence by 2030 is projected to grow to 91% (IEA, 2004: 106).’ Thus, India is destined to be a net importer of oil until the extinction of total world reserves.

Largest Crude Suppliers to India: 2013-2018 in MT.

(Source: Energy World, The Economic Times, July 12, 2018).

It is to be noted here that, ‘India’s dependence on foreign oil is longer standing than that of China. India either buys its oil through spot purchases (Nigeria), short-term contracts (generally of three months) or long-term contracts (Saudi Arabia, for a year) (Madan, 2006: 11).’ As of 2018, it imports oil from the Middle East accounting for around 70% of India’s overseas oil acquisitions. India’s largest oil suppliers are Iraq (45.74 MT) Saudi Arabia (36.16 MT), Iran (22.59 MT), Venezuela (18.34 MT), Nigeria (18.11 MT), UAE (14.29 MT) and Kuwait (11.9 MT) as shown in Table 4 (The Economic Times, 2018).

Unfortunately, all these countries are shown in Table 4 except Saudi Arabia are trouble-torn, marred by civic unrest, political instability, ethnic violence, terrorism and while Iran has been battling the U.S sanctions has serious questions about the energy security system of India. Additionally, the recent bonhomie between Chin and Iran added to India’s energy worry. Therefore, it is natural on the part of India to look for diversifying its oil sources particularly available in her extended neighbourhood: Kazakhstan.

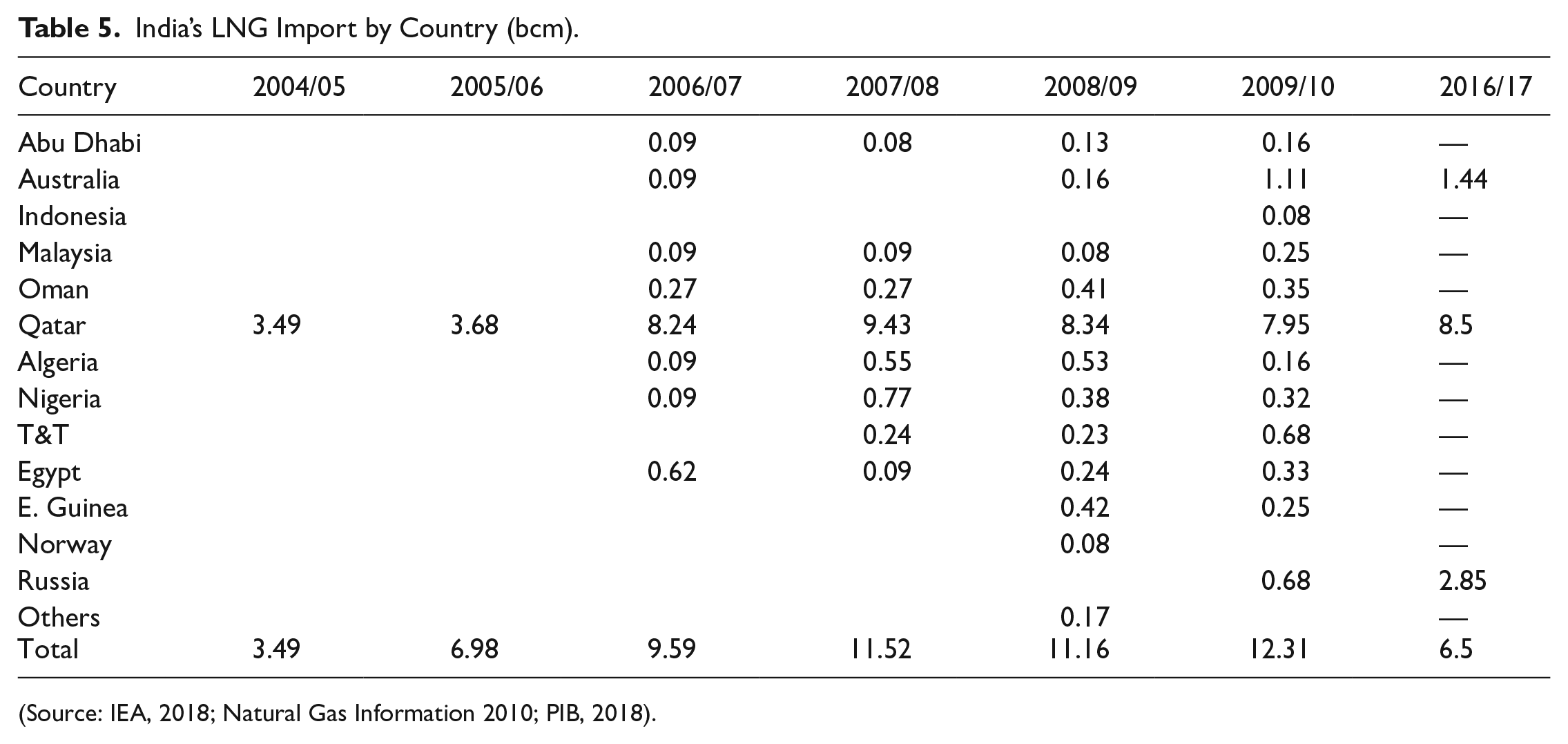

As far as natural gas is concerned, ‘India mainly uses it for power generation (23%), in the manufacture of fertilizers (32%) and the replacement of LPG for cooking oil and other uses in the residential sector (14%) (EIA, 2016).’ Transportation, agriculture and domestic uses account for the rest of the consumption. A majority share of India’s gas usage is from domestic sources especially located offshore near the western coast. With expenditures projected to augment, the domination of domestic natural gas resources is expected to amplify. India of course, like oil, will become increasingly dependent on imported gas. The present scenario as given in Table 5 regarding India’s LNG imports from 2005-2017 shows an increasing trend and over-dependence on the Middle East with Qatar is being the important exporter. In this scenario, an energy destination like Kazakhstan with its huge number of gas-filled unexplored especially in the Caspian Sea region would be an alternative source with an option of easy transportation to India through the Iranian pipeline up to Bandar Abbas.

India’s LNG Import by Country (bcm).

(Source: IEA, 2018; Natural Gas Information 2010; PIB, 2018).

From the above table, it is quite clear that the gas import dependence of India is increasing substantially year by year. And much of this comes from countries like Qatar, Oman, Nigeria and Trinidad and Tobago – far away from India. In this respect, Kazakhstan can prove beneficial for India because of its geographical proximity.

Given its current rate of consumption, ‘BP Energy Outlook estimates that India’s energy consumption is set to grow 4.2% a year by 2035 (BP, 2018).’ As of 2018, ‘India is the second biggest energy consumer in Asia after China and predicted to be the highest fossil fuel consumer by 2035. This means India’s gas demand to expand by 162%, followed by that of oil (121%) and coal (105%). Renewable will rise by 712%, nuclear by 317%, and hydro by 97% by 2035 (ETA, 2018).’ India’s oil import is projected to go up by 165% and would augment about 56% of the rise in imports. Imports of natural gas will also follow the rising pattern with 173% and cola by 105% (BP, 2018). The only options before India in such a scenario seem to of both diversifications of sources and diversification of resources. As India already imports almost three-fourths of its oil from the Gulf countries, Saudi Arabia and Iran, the question that looms large now is where India will get these resources at a cheaper cost with reliable and uninterrupted supplies. The only option that comes to mind is Central Asia and the Caspian Sea energy-rich region especially Kazakhstan and Turkmenistan emerged as the new geological landscapes of energy.

India-Kazakhstan energy trade: Looking back

Since the opening up of Central Asia for the world in 1991, an energy great game has been taking place to control and administer the sources of the resources and their pipeline routes among the major consuming countries. Kazakhstan being a predominant energy producer undoubtedly has invited global attention. Even regional countries like China and India have developed keen interests in energy ties with landlocked countries. In fact, New Delhi since 1995 has been trying tirelessly to gain an entry into the hydrocarbon map of Kazakhstan (Sajjanhar, 2013). Its concerted effort has finally borne fruit as agreements were between the OVL (ONGC Videsh Ltd.) and the KMG (KazMunaiGas) in 2009 (Sachdeva, 2017). This has led India to join an exploration contract signed in 2010 between India’s Ministry of Oil and Gas and the Kazmunaigaz. In 2011, however, the much-anticipated energy cooperation agreements were signed during the visit of Prime Minister Dr. Manmohan Singh to Kazakhstan. The agreement indeed is ‘a package of three agreements – participating share assignment agreement, carry agreement and joint operation agreement – on Satpayev exploration Block was signed between ONGC Videsh Ltd. and National Company Kazmunaigas (KMG) in highly prospective waters of the north-western Caspian Sea (Sajjanhar, 2013).’ This accord has allowed India ‘25% participating interests in the Satpayev block which holds estimated reserves of 1.8 billion barrels in the Kazakh sector of the Caspian Sea (Sachdeva, 2017).’ As per the agreement, ‘the Kazakh state oil company will pay about $80m signature bonus for a 25% stake in Satpayev where oil reserves are estimated to amount to 250 MT (Gorst, 2011).’ However, the drilling was launched only in 2015 during Prime Minister Modi’s visit to Kazakhstan. OVL has taken a stride in investing $400 million in the venture with the oil flow expected by 2020. As part of this, ‘OVL also bought a 2.7-per cent stake in the Azeri-Chirag-Guneshli oil field in Azerbaijan, along with a 2.4-per cent stake in the associated Baku-Tbilisi-Ceyhan pipeline (Sachdeva, 2017).’

ONGC has agreed as per the accord inked to sponsor costs of the entire exploration expenses at Satpayev. This is to ensure reduce the investment risk for Kazmunaigas that ultimately requires investment worth $9 billion. The practice of foreign companies paying the exploration costs in collaboration with the state-owned national companies is common all over the world. In the case of Kazakhstan, the case is a bit different as the country requires more investment not just for the exploration of the energy resources but also to develop the infrastructure for their excavation. That is why perhaps India has had very less accomplishments in comparison to other competitors in acquiring Kazakh oil contracts. The energy companies of the U.S and Europe earned the right to explore the Tengiz and Karachaganak fields in the 1990s which now produces 80 million tonnes of oil per year contributing to the bulk of Kazakh oil production. Similarly, India’s arch-rival China secured the right to explore the upstream resources of Kazakhstan and to transport the oil and energy to its north-western border. China since then has made massive inroads into Kazakh energy sectors and never looked back. In the initial years, it was competing with India to secure oil and gas deals. For example, the 2005 bid between China and India to acquire Kazakhstan’s third-largest oil producer – Petro-Kazakhstan – by placing a bid of $4.18 billion has out bided India (Sachdeva, 2017).

Learning from its failures in biding the deals in Kazakhstan, India has been consistently trying to materialize the Satpayev contract. To actualize the project, in 2009 when the Kazakh President Nursultan Nazarbayev visited India as the Republic Day guest, ‘India’s ONGC Mittal Energy Limited (OMEL) and KazMunaiGaz (KMG) signed a Heads of Agreement for exploration of oil and gas in the Satpayev block in the Caspian Sea (Sachdeva, 2017: 122).’ The Satpayev block with an area covering 1582 square kilometres is a highly prospective region of the North Caspian Sea. Its location close to important oil fields like Karazhanbas, Kalamkas, Kashagan and Donga with considerable oil reserves provides India with a ray of hope in its energy exploration bid in Kazakhstan. Important, the Satpayev block as reported has an ‘estimated reserves of 1.85 billion barrels. The Indian company will have a 25% stake. The remaining 75% stays with KazMunaiGas (Times of India, 2009).’ Once again China outpaced India in snatching the deal from New Delhi attributing to the prolonged delay from the Indian side. The Kazakh president using his sovereign rights has handed over the deal to China assuming India is unserious and lacks interests.

Another setback came in the Indian way in 2013, ‘when it lost a bid to acquire an 8.4% venture in the North Caspian Sea Production Sharing Agreement from ConocoPhillips (Pradhan, 2020).’ The winning of this deal was significant as it would have allowed New Delhi an important stake in the Kashagan oil field. Although OVL attempted to finalize the deal for $5 billion but the Kazakh government handed over the deal to CNPC (China National Petroleum Corporation) using their legal rights. The deal was believed to be agreed as reported for a sum between $5.2 and 5.4 billion (Sachdeva, 2017). In total, India’s loss to China in Kazakhstan alone is estimated to be around $12.5 billion. As compensation, ‘India was given a stake in the Abai oil block in 2014 to which India has summarily rejected. With the declining oil prices, the ONGC did not find the offer particularly attractive (Ibid).’

If properly channelized, both countries can collaborate in the Oil and gas sectors for their mutual benefits. It is well-known that India currently trades in 70% of its energy demands at home. It is import dependence as expected to grow at a faster pace attributing to its steady economic growth. Kazakhstan with 80 million tons of oil per year (1.6 million barrels per day) can help India in her quest for equity oil. With the operation of the Kashagan oil field, Kazakhstan’s oil production is expected to rise to 150 million tons per annum and very soon it will be figured among the top ten exporters of oil in the world. ‘Kazakhstan can take advantage of the rich and vast experience that India has accumulated in downstream processing and refining of crude oil to manufacture petrochemicals and other related products (Sajjanhar, 2013).’

Undoubtedly, the venture of OVL was shattered after it lost the Kashagan deal to China despite Indian interests. As reported, ‘this has caused an avoidable psychological disappointment, shock and heartburn to the section of opinion makers and leaders in India who have been speaking out vociferously in favour of stronger strategic and economic links with Kazakhstan (Pradhan, 2020).’ Notwithstanding, the setbacks India got from its oil and gas bids in Kazakhstan, it would be imperative to carry on and pursue renewed projects and initiatives for intensification and consolidation of the mutual relationship.

As a way forward, India and Kazakhstan in 2009 have entered into ‘Strategic Partnership. This means both the countries have agreed to develop all-inclusive bilateral partnerships in areas of security and strategic importance. According to Robert Cutler, ‘the two sides are negotiating a possible uranium supply agreement as civil nuclear energy cooperation presents attractive prospects for further diversifying bilateral economic and commercial contacts (Cutler, 2011).’ While India and Kazakhstan have agreed for uninterrupted trade in Uranium, New Delhi may depend more on Astana for enlarged uranium purchases.

For its part, Kazakhstan has extended vigorous support to India at the international level by both the International Atomic Energy Agency (IAEA) and Nuclear Suppliers Group (NSG) for waiver of conditions to supply nuclear materials to New Delhi. It should be noted here that, ‘Kazakhstan is the biggest producer of uranium with an annual production of around 20,000 tons (Sajjanhar, 2013).’ It needs a market for its enriched Uranium and India as a proximate neighbour is dependent on Uranium trade to maintain its nuclear reactors. Cooperation between India and Kazakhstan in the nuclear sector would provide a win-win situation for both countries.

According to India’s 12th Five Year Plan, ‘nuclear power will play a major role in meeting the country’s energy needs. The country needs an additional 1, 00,000 MW of power during the 12th Plan (2012-17) (Planning Commission, 2012).’ India is allowed to have diversified sources of access after the inking of the ‘Indo-US Civil Nuclear Energy Cooperation agreement’. Kazakhstan in this direction has emerged as a reliable partner by extending its support for India in IAEA and NSG in 2009 for commerce in nuclear energy meant for civilian purposes. In 2009, ‘MoU was signed between Nuclear Power Corporation of India (NPCIL) and National Atomic Company, Kazatomprom during the visit of Nazarbayev (president of Kazhakstan) (Pradhan, 2019).’ This initial diplomatic negotiation was further strengthened in 2011 when Prime Minister Manmohan Singh visited Kazakhstan. During the visit, both countries have an ‘Atomic Energy Agreement’ for peaceful use. ‘The agreement provides a legal framework for cooperation in fuel supply, reactor safety mechanism, and exchange of scientific and research information, exploration and joint mining of uranium, design, construction and operation of nuclear power plants. According to the agreement, Kazakhstan had supplied 2000 tonnes of uranium to India in 2014 (Pradhan, 2019).’ Importantly, Kazakhstan has expressed keen interest to put up small nuclear reactors with the capacity of 220 MW with the Indian help (The Indian Express, 2017).

Paradigm shift methodology

Paradigm shift coined by Thomas Kuhn in his 1962 masterpiece ‘The Structure of Scientific Revolution’ refers to the change in worldview, concepts and practices to see the work is accomplished. The methodology of paradigm shift can be applied not just to scientific research and industry but to international relations among nations as well. Just like the introduction of new technologies in industry augments production process and alters the manufacturing capabilities of the industry-leading to better goods and services, a paradigm shift in international relation with application/introduction of new factors in a country’s dealing with another country/region brings in major changes in their bilateral relationship. In this milieu, this article advocates for the shifting of paradigm in India’s approach to deal with the countries of the Central Asian region. The prolonged paradigms of soft-power, cultural chord, historical bonding need to be replaced with strategic calculations by bringing in a Russian factor and doing away with the ‘go alone’ approach in its engagement with the region.

In recent years, India has exhibited keen interests in developing energy trade with Kazakhstan. Prime Minister Modi’s landmark visit to Kazakhstan along with other countries of Central Asia brought about a paradigm shift in India’s outlook towards the region. This has facilitated India to forge a relationship with Kazakhstan in the oil, gas and uranium sectors which would, in turn, unlock New Delhi’s entry into NurSultan’s energy sector. Amb. Stobdan in his analysis of the Prime Minister’s visit to Central Asia in 2015 has revealed three important takeaways: ‘first, President Nursultan Nazarbayev’s decision to sign a major contract for a renewed long-term supply of uranium to India; second, ONGC Videsh Ltd (OVL) has finally made its first breakthrough when PM Modi launched the drilling operation for oil exploration in the Satpayev block on July 7, 2015; third, Modi’s follow up visit to Turkmenistan after the Ufa Summit would help TAPI pipeline to see the light of day (Stobdan, 2020: 259).’

The intricate energy pursuit of India in Kazakhstan seems to have taken a positive turn since 2015. If you see, ‘OVL has opened its office in Almaty in the mid-1990s inside the building of Indian Embassy (Ibid).’ It has been a period of consistent struggle and frustration since then as Kazakh authorities have shown cold shoulder to its bidding process repeatedly or the bidding agreement was not honoured later on and the repeat ion continued. OVL was ignored as a small fish in the bigger Central Asian energy market leading to its closure of the Almaty office in 1998. This has been attributed to India’s strategic ineptness and wrong assumptions as New Delhi was non-serious about the energy deals given their transportation unsuitability and overemphasis was laid on cultural goodwill rather than strategic engagement. That era now seems to be over with pragmatic leadership at the helm of affairs in New Delhi. But one more important factor that India so far has been discounting while engaging with Kazakhstan or to say any other Central Asian countries is ignoring the Russian role. If India would identify the misplaced imaginations and wrong assumption that New Delhi has put in place since the 1990s in the disguise of Soft-Power and would rectify them with a keenness to take Russia on board borne results in favour of India given New Delhi’s strategic leverage for both Russia and the greater Central Asian region. he present dispensation in New Delhi for sure would devotedly look into it in its energy quest in Kazakhstan and reinforce its holds over the ongoing energy deals with Kazakhstan as discussed below.

Launch of Oil drilling

Prime Minister’s maiden visit to Kazakhstan in July 2015 witnessed the inauguration of the oil drilling operation in the Satpayev oil field. Besides, ‘OVL is rethinking on its refusal to accept the 25% stake in Abai field abandoned by Statoil of Norway to participate in the ‘Eurasian Project’ of Kazakhstan with whopping 300 oil and gas fields in the Caspian Sea region (Stobdan, 2020).’ With Modi’s briefing about India’s interests in the Kazakh oil and gas fields and positive response from the Kazakh side, New Delhi no longer can afford to ignore the Kazakh energy bastions. But for that India needs to open up to Chinese competition and stop shying for massive investment discounting immediate benefits.

Uranium deals

India and Kazakhstan agree to renew the contract for the supply of Uranium on July 7-8, 2015. ‘It was agreed between the National Atomic Company (NAC) and Nuclear Power Corporation of India Ltd (NPCIL) to supply 5000 metric tons of nuclear fuel to India for the period 2015-19 (MEA, 2015).’ The uranium signed is more promising than the hydrocarbon sector as it has allowed India to get more than twofold the size of uranium it received under the previous phase contract (2009–2014) (Stobdan, 2020: 266). However, when compared to China which imports almost 55% of Kazakh Uranium, the position of India looks minuscule. New Delhi needs to work aggressively on this front and it can count its friendship with Moscow to manoeuvre space to control more Kazakh uranium.

TAPI and Kazakhstan

The much delayed and more controversial TAPI (Turkmenistan-Afghanistan-Pakistan-India) gas pipeline envisioned in 1995 seems to be moving in a positive direction after 25 years of initiation. In December 2016, the groundbreaking ceremony was held in Ashgabat in which it was decided that India will host the next meeting of the Steering Committee in 2018 in New Delhi. This will further, India’s energy cooperation with Kazakhstan and help India to transport gas from the gas fields of Kazakhstan located in the Caspian Sea region as well.

North-South Corridor

INSTC (International North-South Transport Corridor) is a multimode connectivity network project between India, Russia and Iran. This 7200 km long project was proposed in 2001 in St. Petersburg for transporting consignments connecting India with Russia via Iran, Europe and Central Asia. Now the project is backed by 13 more countries including Kazakhstan envisages a sea route from Mumbai o Bandar Abbas in Iran and then to Bandar-e-Anzali in the Caspian Sea to Russia via Central Asia. This project also is connected with another Iranian port called Chabahar would enable India to transport Central Asian energy resources effortlessly and importantly bypass Pakistan and Afghanistan. ‘The first dry run of two routes was conducted successfully in 2014 (Chaudhury, 2017).’ According to the Ministry of External Affairs, Government of India, ‘the result was amazing as the cost of transportation was reduced by $2500 per 15 tons of cargo (MEA, 2017).’ India and Kazakhstan agreed to collaborate closely in the framework of INSTC to improve surface connectivity between them when Prime Minister Modi was in Astana in July 2015. In 2017, other countries were also part of the working group of the Ashgabat Agreement instituted in 2011. Once the road becomes fully operational, India will be in a strong position to transport hydrocarbon resources not just from Russia, Iran and Kazakhstan but also the wider region.

SCO and India

The recent inclusion of India along with Pakistan into the Shanghai Cooperation Organization (SCO) as a full member is an important step towards India’s growing engagement with the region. It should be noted here that since 2005 India had been the observer member of SCO. Russia and Kazakhstan proposed to include India as a full member of the organization but the Chinese reluctance denied India a rightful place in the regional organization and limited New Delhi’s role in the region. The proactive diplomacy of India under the NDA government and the constructive support of Russia and Central Asian countries allowed India to be part of the grouping is reason enough to understand the weightage these countries offer to India. If India can identify its areas of priority and give impetus to strategic engagements, New Delhi would certainly gain a substantial footprint in the hydrocarbon map of Kazakhstan and Central Asia.

Result and discussion

Kazakhstan is the leading trade partner of India among the Central Asian republics. Among the components, trade-in energy and natural resources dominate the bilateral trading basket. With an annual trade turnover of $ 1.3 billion between India and Kazakhstan, the commercial commodities that remain the mainstay of their trade relations are oil, oil products, uranium, titanium, pharmaceuticals and agriculture among others. The major stake of economic cooperation between two countries is driven by energy trade and the visit of the Indian Prime Minister to the country and the region in 2015 further enhanced the opportunity for greater energy trade between the two countries.

In fact, India has entered into several energy agreements with Kazakhstan and worked on previous agreements agreed upon by two countries for oil exploration and drilling. To state, the first agreement between India’s OVL (ONGC Videsh Limited) and KazMunaiGas of Kazakhstan was signed in 2005. On the basis of this agreement in 2011, OVL could acquire a 25% share of the Satpayev oil block with a signing contract of $ 13 million. This has further encouraged OVL to invest $ 400 million in oil exploration in this field. However, China’s intermittent bidding and lucrative financial packages pushed India out of the oil deal as Kazakhstan has awarded that deal to China citing unprecedented delay on part of India. Correspondingly, in the Atyrau region, a very small oil deal was awarded to OVL which India was not interested to invest in due to lack of feasibility study. Nevertheless, in 2015 when the Indian Prime Minister visited Astana his Kazakh counterpart Karim Massimov jointly inaugurated the first exploratory drilling off the Satpayev block. Similarly, in the nuclear energy sector, the Department of Atomic Energy of India and the Kazatomprom, Kazakh national nuclear company have agreed to supply enriched uranium to India for civilian usage. Also, MoU between BHEL (Bharat Heavy Electrical Limited) and Samruk Energo of Kazakhstan was signed on June 7, 2015, to cooperate in production, construction and reconstruction of thermal, hydropower, gas-turbine and other power plants and stations in India. Although, both the countries have made relative progress in the energy sector when compared with China and other energy consumers of Kazakhstan, the progress of India looks dismal and underrated. A reflection of the previous literature has blamed India for its disinterested approach and lack of seriousness while some others have blamed it on the overemphasis of the cultural chord in bilateral relations instead of real politicking. In contrast to what others have stated, this article instead has voted for a Russian card in India’s Central Asia policy and rejected the hitherto adopted go alone approach of India in the region which only brought more failures than anything else.

Further, it asserts that India shouldn’t mistake the growing Russian-Chinese convergence as the end of the road instead should treat it as solely U.S centric. Despite overlapping interests and frozen historical conflicts, Russia is playing into the hands of the Chinese largely because of the unscrupulous sanctions imposed by the west led by the U.S. But the Covid-19 gripped world symbolizes transformations ahead with smoothening in the relationship between Washington and Moscow while a patchy road ahead for Beijing-Washington entangled in the trade war. Further, the Chinese lebensraum in its neighbourhood and illegal claims over the South China Sea in recent times, of course, would caution Russia reminding the Chinese territorial design in 1969 against the Soviet Union. Importantly, Russia for longer wouldn’t like to play a second fiddle role to China in its hinterland. The moment Moscow feels threatened with the initiatives and intentions of China, it will resort to its old tactic of containment. For that Moscow needs New Delhi to offset the sway of China in the area. The Russian move of including India as a full member in SCO should be seen in this framework. Moreover, Russia is going to remain the key factor in Central Asia’s foreign and security policy for decades to come. Therefore, India shouldn’t make any mistake in discounting Russia in its Central Asia policy.

Although countries of Central Asia especially Kazakhstan pursue a multi-vector foreign policy yet, in reality, they all are integrated into the strategic calculations and foreign policy objectives of Russia. Their socio-economic and political dependence on Moscow and the integrated energy transportation system speaks volumes about the Russian dominance over the region. Although China has made enough inroads into the region economically they have come only through Russian consent and collaboration. Since Russia considers China a strategic competitor and India a historical and reliable friend, New Delhi must include Russia in its Central Asian affairs to yield results in its energy quest and strategic initiatives.

Importantly, the Transit pipeline is of utmost importance given India is not directly connected to Central Asia and the Central Asian countries on the other hand are landlocked. India, therefore, has to depend on the third country to build its pipelines either through China, Pakistan, and Afghanistan or through Iran to the Arabian Sea. Given the geopolitical situation in Afghanistan, hostility with Pakistan and relentless opposition from China, the Iranian route looks like the best feasible option. The transportation of hydrocarbon can be carried out to Iran through the Caspian and to India through pipeline options. Another feasible option is to transport oil via the Iran-Turkmenistan-Kazakhstan railway link inaugurated as part of the North-South Transportation Corridor (INSTC) in December 2014. Moreover, an agreement was signed between Kazakhstan and India on July 9, 2015, for affordable and easy transportation of goods via railway giving Kazakhstan access to Indian seaports. Trial runs carried out in 2018 along with the Mumbai-St. Petersburg North-South Transportation Corridor proved to be cost-effective and time-saving. If things go well with India and Iran over the Chabahar port, this route would undoubtedly be the next energy corridor of world politics.

Looking ahead

India despite strong historical relations and strong intentions suffers from multiple constraints when it comes to its Central Asia policy. Although, lack of political willpower, financial capability and geographical constriction have been projected as major hindrances in the way of New Delhi’s engagements with the region. This article adds India’s lack of understanding of the region, wrong assumptions and strategic miscalculations of discounting Russia has limited India’s presence in the region. For India, the way forward must include a strategic rethinking of Central Asia under active collaboration with Russia as the region through independent pursue their policies in consonance under Russian guidance.

Further, India should overarch its Central Asian strategy through Visa relaxations, promoting private investments, learning their languages and nurturing experts on the region through funding projects and organizing conclaves. Notwithstanding, New Delhi must take Moscow in confidence while dealing with the region and improve its record marred with historical indecisiveness when it comes to energy deals.

Limitation of the study and scope for future research

Nevertheless, this study is limited to India’s approach to Central Asia in the energy sector where calculating the Russian factor holds the key for New Delhi. Although, various other factors including lack of economic muscle and geographical constraints add to India’s lack of political willpower for greater engagement in the energy sector in the region yet its initial failures in bidding the oil deals and consequent Chinese takeover of India’s prized deals in Kazakhstan tells stories of India’s wrong assumptions and strategic miscalculations of discounting Russia in the region. However, further research may be conducted to underneath other possible reasons behind India’s failure in the energy front in Kazakhstan while this article strongly believes the Russian factor will add vigour to India’s energy manoeuvre in Kazakhstan.

Conclusion and policy implications

Kazakhstan in many respects is important for India. Therefore, the indecisive policy process leading to random and anaemic ties needs revision. Modi’s visit perhaps has changed the narrative and led to a paradigm shift in India’s policy towards Kazakhstan. The agreement signed and understanding developed between two leaders Modi and Nazabayev would further India’s position in the energy-rich nation giving way for Indian goods to enter the Kazakh market while Kazakh energy will feed the Indian industry. Despite geographical constraints, India can reap benefits if it takes Russia into confidence in its Central Asia policy. Besides, New Delhi must invest heavily in its ties with Iran while balancing its relations with the U.S. Importantly, India must develop people to people contact, relax visa regimes, encourage private enterprises to invest in Kazakhstan, imparting Kazakh language and avoid the cost-benefit analysis among other things would enable India to deepen its engagement with Kazakhstan.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.