Abstract

This article examines how Russia’s economic crisis and ban on agricultural imports from the United States and other Western countries that began in 2014 have impacted its agricultural and food sector. The import ban was a Russian response to geopolitical tension with the West stemming from the country’s conflict with Ukraine, while the main cause of the economic crisis was a plunge in world oil prices. Given that the bulk of Russia’s export earnings come from oil and other energy products, the oil price decline triggered a major depreciation of the ruble against the US dollar and other major currencies. Ruble depreciation and the import ban have affected Russian consumers by reducing Russia’s imports of agricultural and food products, substantially raising food prices, and lowering consumption. However, the country’s basic food availability has not been threatened. By increasing domestic prices, the depreciation and import ban have stimulated agricultural production. The added output has reduced meat imports and raised grain exports. Russian meat imports in 2014–2016 (average annual) were about 40% lower compared to 2011–2013, while grain exports in 2014–2016 were 50% higher than in 2011–2013 (though production-enhancing favorable weather was also a cause).

Introduction

In 2014, Russia was hit by several geopolitical and economic crises. Tension arose early in the year between Russia and Ukraine, which led to Russia seizing the Ukrainian territory of the Crimea. In response, the United States, European Union (EU), and other Western countries enacted economic sanctions against Russia. Russia then retaliated in August 2014 by establishing an import ban on many agricultural and food products from the sanctions-imposing nations. Russia gets the bulk of its export earnings from oil and other energy exports, and the plunge in world oil prices in late 2014 generated major depreciation of the ruble against the US dollar and other major currencies. By 2015, these developments had created both high inflation and major recession for the Russian economy.

The International Monetary Fund (IMF, 2015), Gurvich and Prilepskiy (2015), Mau and Ulyukaev (2015), and Mau (2017) examined how these various crisis-related events have affected Russia’s overall economy, while Golikova and Kuznetsov (2017) investigated the impact specifically on manufacturing. Wegren, Nilssen, and Elvestad (2016) examined how Russian food security policy, which focuses on agricultural import substitution and self-sufficiency, has impacted the agricultural and food sector since Russia created its Doctrine on Food Security in 2010. Although that study touched on some of the current crises’ effects on agriculture during 2014–2015, it did not assess the full impact of Russia’s geopolitical and economic crises on the agricultural and food economy, nor did it provide any longer term outlook for the sector. W. Liefert and Liefert (2015) examined what the effects of the current crises on the agricultural and food economy could be when the crises hit in 2014.

This article examines the effects of Russia’s economic crisis and agricultural import ban on the country’s agricultural and food sector during the three crisis years of 2014–2016. 1 One reason for focusing on that particular sector is that Russia’s retaliatory import ban directly affects it. Another reason is that agricultural and food products are tradable goods, such that major currency depreciation could be expected to have strong effects on these products’ domestic prices, the volumes of the goods domestically produced and consumed, and consumers’ overall economic welfare.

Another reason for focusing on the agricultural sector is that even before the crisis, the Russian government was committed to expanding the agricultural economy, especially the livestock sector. This policy was motivated to a large degree by the desire to reverse the extreme downsizing of agriculture during the economic transition decade of the 1990s. From 1990 to 2000, total agricultural output declined by about two-fifths and the production of livestock goods by half, and Russia became a big meat importer (3.0 million tons in 1997, the year before Russia’s severe economic crisis of the late 1990s, and 25% of total world meat imports; W. Liefert & Liefert, 2012; US Department of Agriculture Foreign Agricultural Service [2017b, USDA PSD]). Import substitution and self-sufficiency are major goals of Russia’s current agricultural policy (as investigated by Wegren et al., 2016). The Russian government, including the Agriculture Minister and President Putin, have argued that the economic crisis (and import ban) provides the country with the opportunity to strengthen agricultural production, import substitution, and self-sufficiency (The Moscow Times, 2015; Russia Insider, 2015; USDA, 2015). At the start of the crisis, the federal government stated that it would support these objectives by increasing state subsidies to the sector. The article will examine the interplay between the crisis and these policy goals.

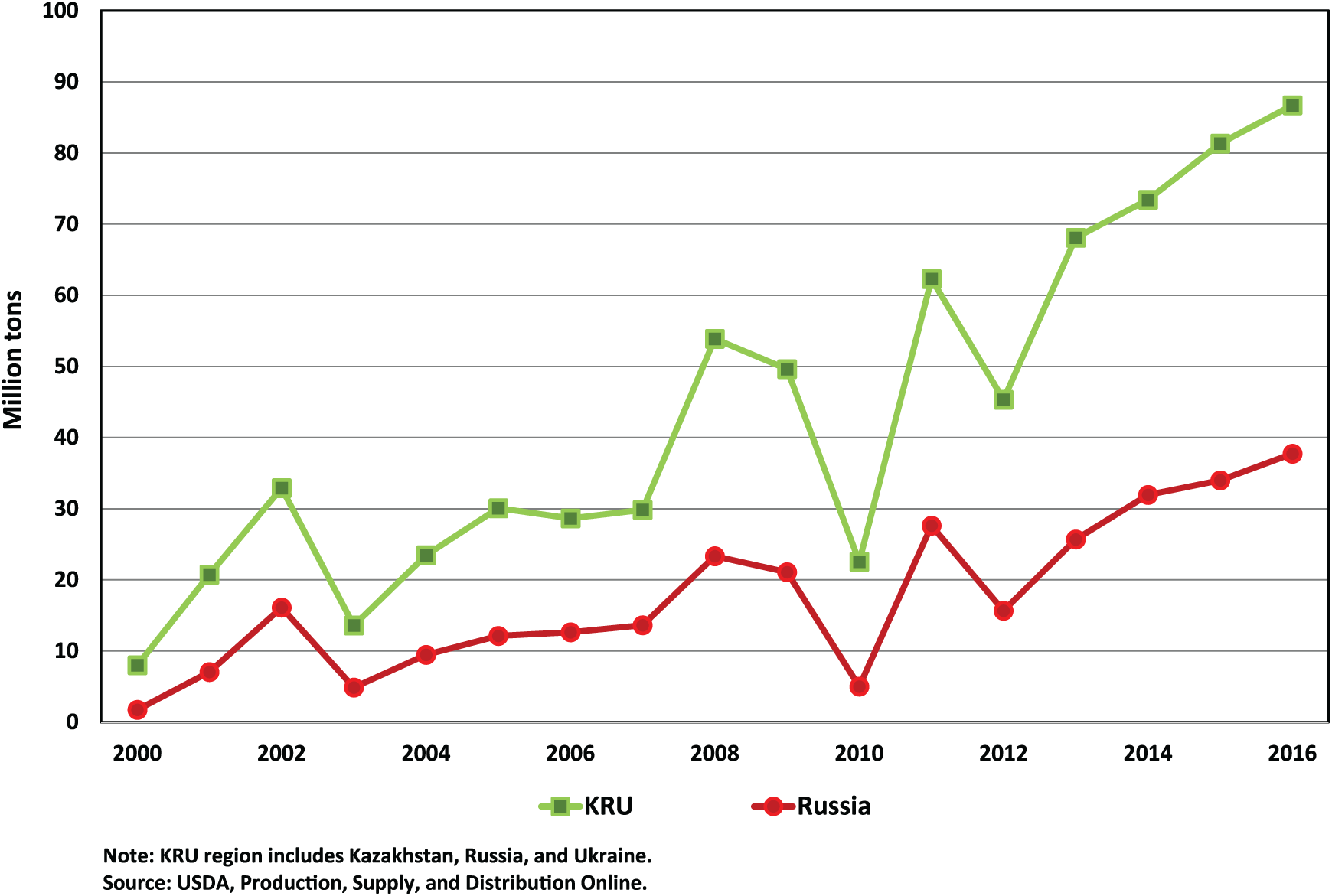

The last reason for focusing on agriculture is that since 2000, Russia has become increasingly important for world agricultural markets. Beginning around 2000, Russia became a major grain exporter, along with Ukraine and Kazakhstan. Russia exported 35 million metric tons (mmt) of grain a year during 2014–2016 (average annual), while Russia, Ukraine, and Kazakhstan collectively exported 80 mmt (average annual, excluding any sales to each other; Figure 1). Over this period, Russia supplied 10% and 15% of world exports of total grain and wheat, respectively (USDA PSD).

Russian and KRU region grain exports.

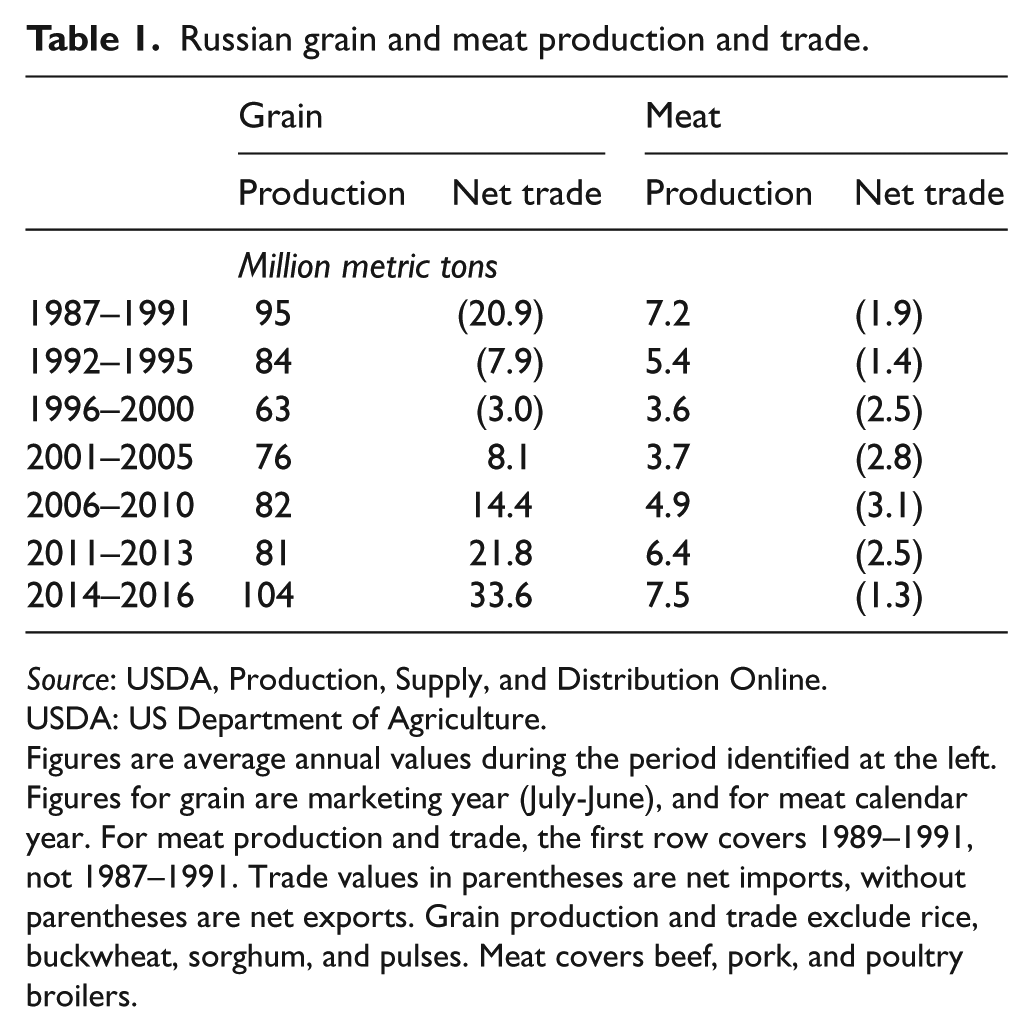

By 2000, Russia was a major importer of meat (as mentioned earlier) and other livestock products, and these imports continued to grow up to 2008 (the year before Russia’s previous serious economic crisis of 2009). Russian meat imports (of beef, pork, and poultry broilers) peaked in 2008 at 3.5 mmt (USDA PSD). By 2011–2013, the push toward import substitution and self-sufficiency had reduced meat imports to 2.5 mmt (average annual; Table 1). The article will examine how the crisis has impacted Russia’s presence in the key world agricultural markets of meat and grain.

Russian grain and meat production and trade.

Source: USDA, Production, Supply, and Distribution Online.

USDA: US Department of Agriculture.

Figures are average annual values during the period identified at the left. Figures for grain are marketing year (July-June), and for meat calendar year. For meat production and trade, the first row covers 1989–1991, not 1987–1991. Trade values in parentheses are net imports, without parentheses are net exports. Grain production and trade exclude rice, buckwheat, sorghum, and pulses. Meat covers beef, pork, and poultry broilers.

Given that meat and other livestock products are targeted in Russia’s agricultural import ban, and that a main goal of Russian agricultural policy is to expand the production of livestock goods, the article pays particular attention to the meat sector. Though focusing mainly on the crisis’ impact on agriculture through 2016, the article also discusses to some degree the possible longer term effects. We use the USDA long-term modeling system for world agriculture to generate projections for the volumes of Russian production and imports of meat to the year 2026 to assess how the Russian meat sector might develop once the country has settled its current crisis. However, the modeling system is also used to create scenarios and projections based on different assumptions for future Russian gross domestic product (GDP) growth and change in the ruble exchange rate, with a low growth scenario reflecting continuation of some of the economy-stunting elements of the current crisis.

Given that the crisis-related macroeconomic developments have so strongly impacted agriculture, the article also investigates to some extent the crisis’ effects on Russia’s macro economy. Some attention is also paid to the crisis’ impact on EU and US agricultural trade with Russia, though that is not a major focus of the article.

Ukraine has also been in geopolitical and economic crisis since 2014, enduring even greater inflation and GDP decline than Russia. The causes and effects of Ukraine’s current crisis, including the impact on agriculture, share some similarity with Russia’s experience. Yet, the political and economic uncertainty created by the Russian-Ukrainian geopolitical conflict has affected Ukraine even more than Russia, and Ukraine’s current economic troubles are more severe. The effect of Ukraine’s crisis on its agricultural and food economy merits its own study, and is not a topic of this article.

The restructuring of Russian commodity agriculture during transition and consequences for world markets

During its last decades, the Soviet Union, as well as Russia itself, was a large grain importer. From 1970 to 1990, the Soviet (and Russian) livestock sector expanded substantially, aided by hefty subsidies to both producers and consumers (W. Liefert & Liefert, 2012). The livestock growth motivated large imports of grain, soybeans, and soybean meal used as animal feed (see Table 1 for grain imports in the late Soviet period).

When Russia began the move from a planned to a market economy in the early 1990s, it could no longer afford the large direct and indirect subsidies to the agricultural sector. Consequently, output contracted heavily, in both the livestock and crop sectors (see again Table 1). Average annual Russian meat production during 1996–2000 was 50% lower than during the late Soviet period of 1989–1991, while Russian meat imports started to rise.

Beginning around 2000, Russia became a major grain exporter (Table 1). The main reason is that grain production began increasing (though output could dip in any given year because of poor weather), such that surpluses were available for export. O. Liefert, Liefert, and Luebehusen (2013) and W. Liefert and Liefert (2017) examine why Russian grain output has risen since 2000, and the consequences for exports. Farm level improvements that increased input productivity and yields apparently played a key role. Rather than importing grain and oilseeds to feed an over-expanded and expensive livestock sector as during the Soviet period, Russia become a large meat importer and big grain exporter. These major shifts in Russian agricultural production and trade appear to have been consistent with the country’s underlying cost/price competitiveness across commodities on the world market (what economists call comparative advantage; see W. Liefert, 2002).

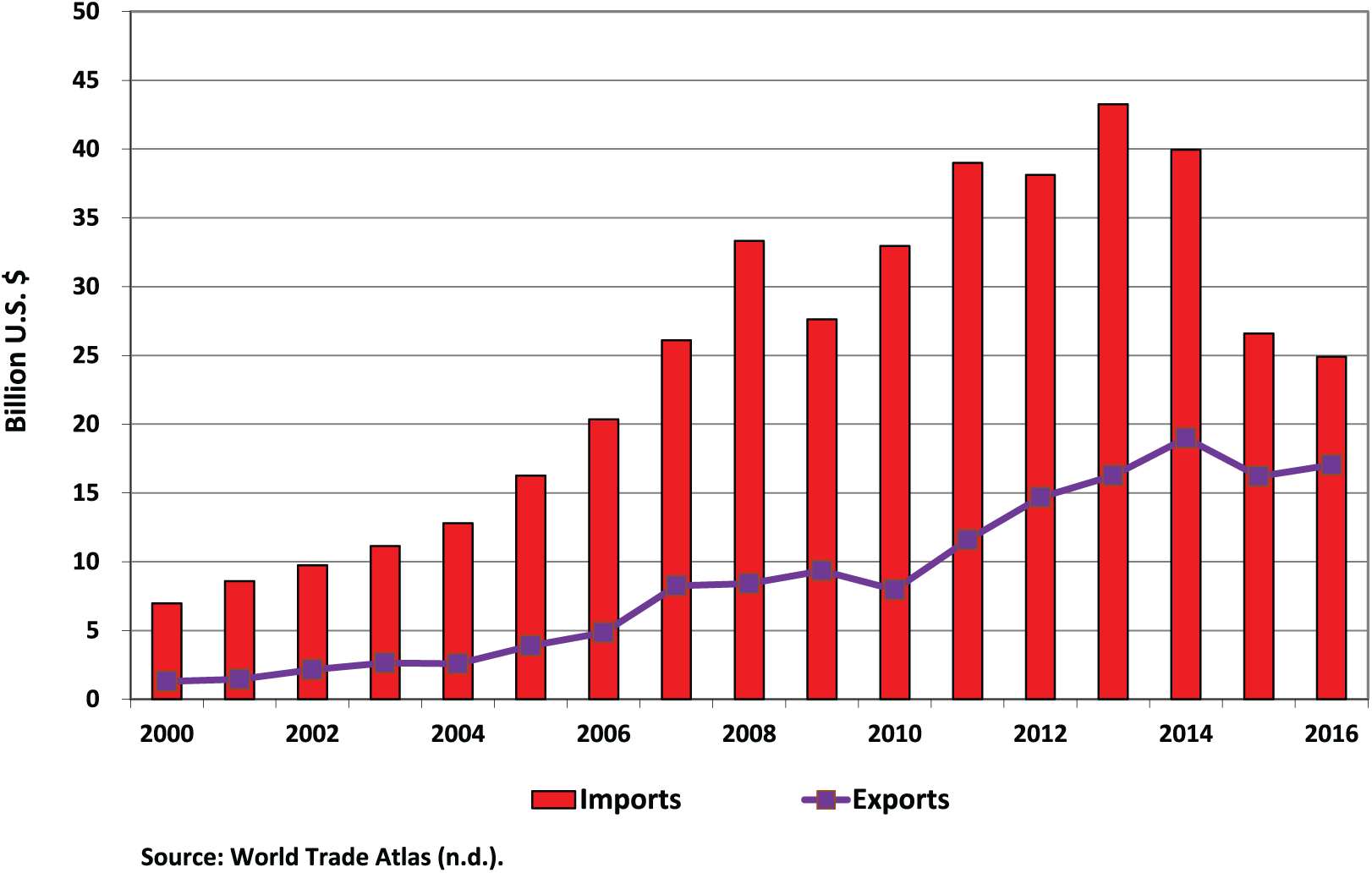

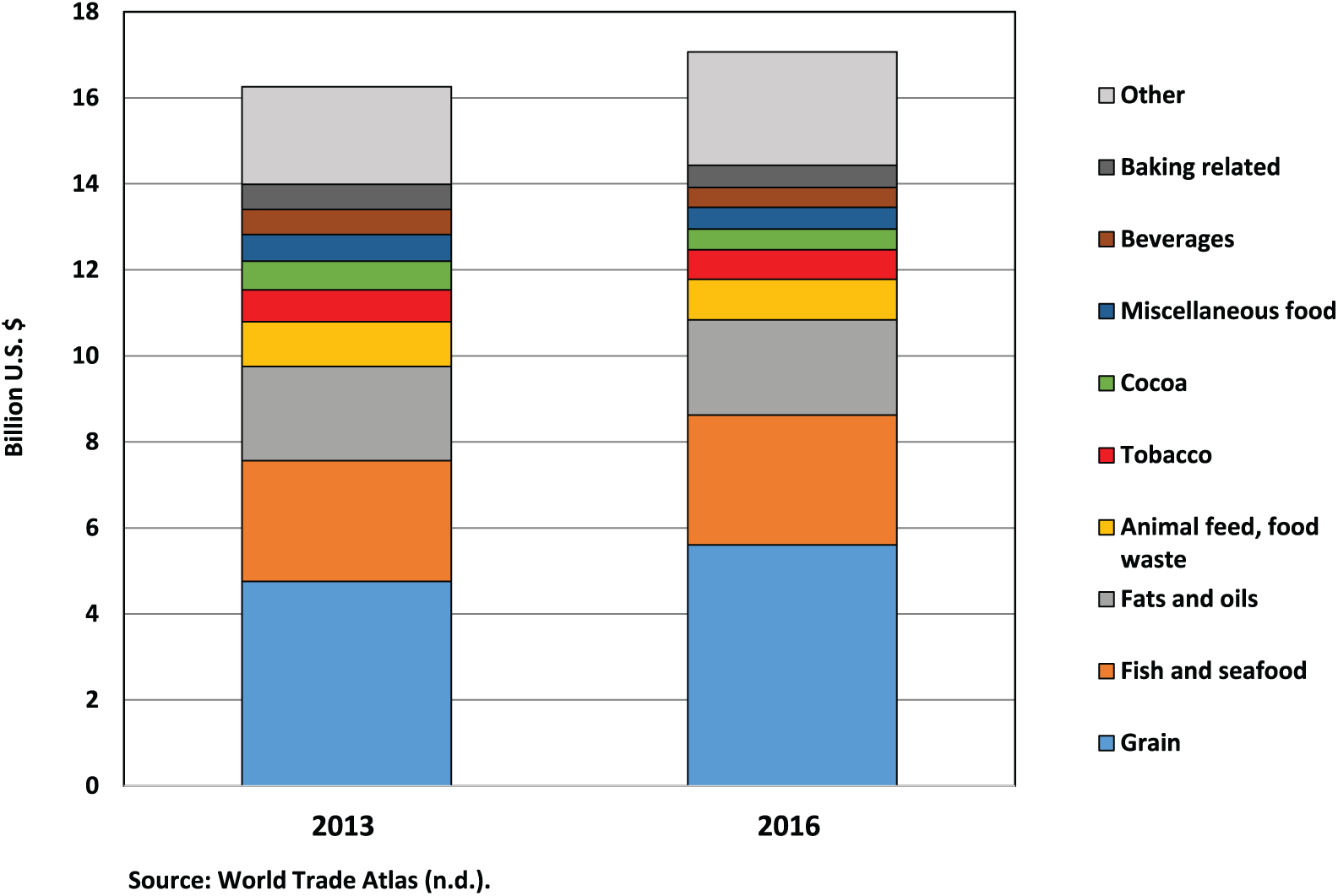

Russia’s large grain exports notwithstanding, the country is a larger agricultural importer than exporter (Figure 2). Russia’s total agricultural imports in 2013 (the year before its crisis began) equaled US$43 billion, while exports were US$16 billion. The main reason for the large negative agricultural trade balance is that high-value products, such as meat, dairy products, fruit, vegetables, and processed foods, comprise a larger fraction of Russia’s imports than exports (see Figures 3 and 4).

Russian agricultural imports and exports.

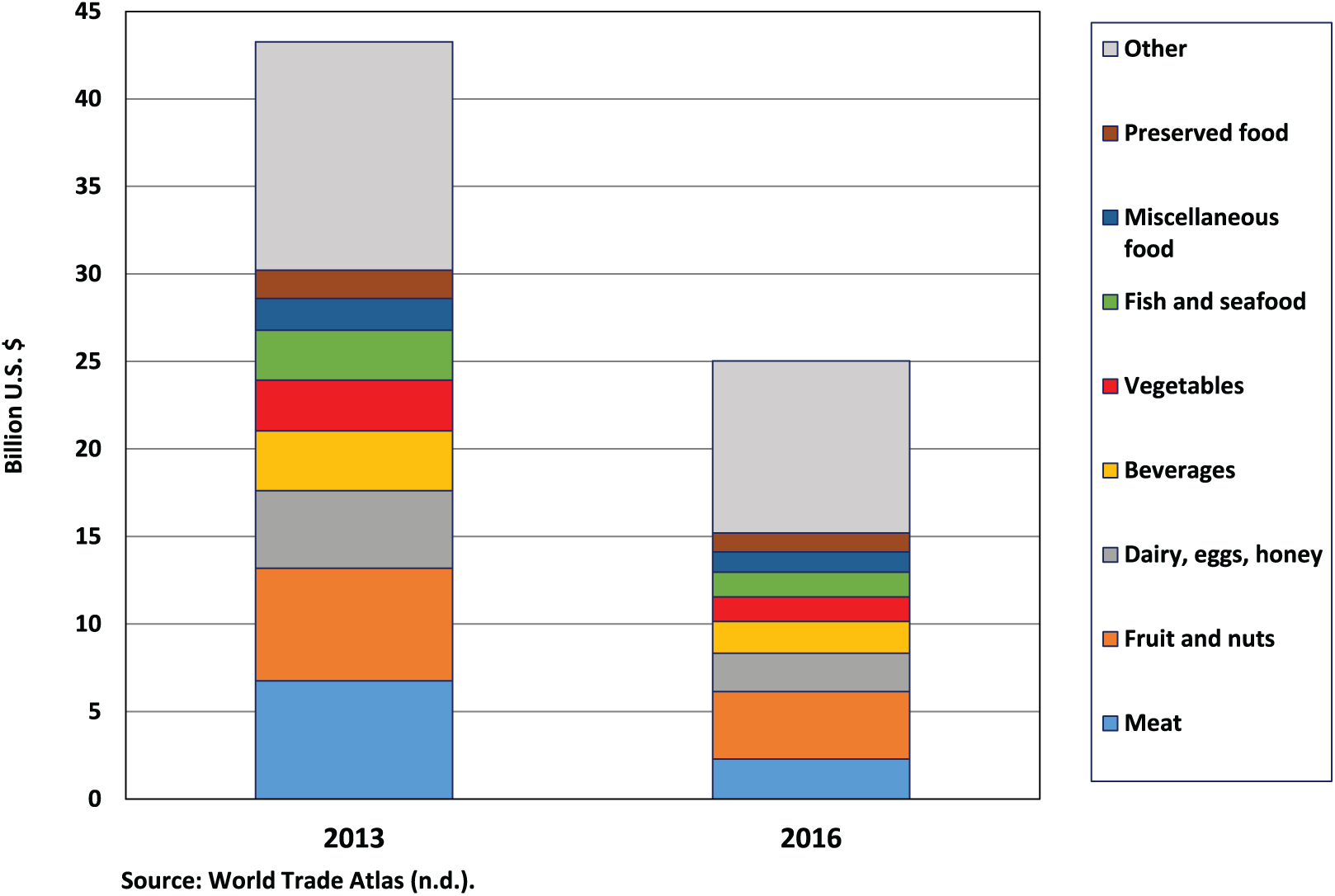

Russian agricultural imports.

Russian agricultural exports.

Russia’s agricultural imports have grown considerably since 2000. Over 2001–2008, high GDP growth of 6.6% a year (on average) increased consumer income, and correspondingly demand for food, including that imported (W. Liefert, Liefert, & Shane, 2009). The world economic crisis of 2009 hit Russia severely, with GDP declining by 8%, such that agricultural imports dropped that year. Yet, import growth resumed when the country began recovering from the crisis in 2010.

A second reason why agricultural imports increased after 2000 is that food price inflation in Russia exceeded that in its main trading partners. From 2000 to 2008, food prices in the countries of the EU (collectively) and the United States rose by 26% and 28%, respectively (Eurostat, n.d. and US Bureau of Labor Statistics, n.d.), while food price inflation in Russia over the period was 168% (Russian Federal Service of State Statistics, n.d.-b). This made foreign imported foods more price competitive within Russia vis-a-vis domestic output, which in turn increased Russian demand for imports (During this time, higher inflation economy-wide in Russia, compared to its trading partners, technically resulted in real, as opposed to nominal, appreciation of the ruble vis-à-vis foreign currencies.)

A third cause of the import growth in value terms, and one not specific to Russia’s macroeconomic developments, is the rise in world agricultural and food prices since 2000, and especially the high growth from 2006 to 2012 (see Food and Agriculture Organization of the United Nations [FAO, 2017] Food Price Index). As mentioned earlier, Russia has been a major importer of high-value products, especially livestock goods. During 2000–2012, world meat prices rose by about 90% (FAO, 2017, Food Price Index). However, the food price inflation means that Russian agricultural imports grew less in volume than value terms.

After peaking in 2008, Russian meat imports began to decline in volume terms (see again Table 1). One reason was rising domestic production of poultry and pork (but not beef) that displaced inflows. Policy developments that helped increase output and erode imports were growing government subsidies, a system of tariff rate quotas (TRQs) for meat imports, and widespread use by the government of sanitary measures, which often included complete import bans, against meat imports (W. Liefert & Liefert, 2012).

The effects of Russia’s current crisis and import ban

Effects on EU and US agriculture

The agricultural import ban that Russia imposed in August 2014 against the United States, EU, Norway, Australia, and Canada covered meat (beef, pork, poultry), milk, cheese, other dairy products, fish and other seafood, fruit, vegetables, nuts, and many processed foods. 2 Although initially created for just one year, the ban was renewed (again officially for one year) in both 2015 and 2016, and in 2017 extended through 2018.

Russia is a major market for EU agricultural goods, importing U$15–U$16 billion of EU agricultural products in 2013, about 10% of total EU agricultural exports, and 35%–40% of Russia’s total agricultural imports. Russia’s import ban has adversely affected many EU agricultural producers, especially of meat, dairy, fruit, and vegetables. In 2013, Russia was the top destination for EU meat (especially pork and pork products), taking 18% of European meat exports, as well as for dairy (such as yogurt, buying 17% of total EU exports of that product), fruit (40% of EU exports), and vegetables (23% of EU exports). However, in 2015–2016 Russian imports of the above products from the EU virtually ceased to exist. From 2013 to 2016, EU exports (out of the region to all other countries) of cheese and fruits and vegetables were down by 20% and 9% in value terms, respectively (Global Trade Atlas, n.d.). 3

In contrast, Russia is a small market for US agricultural goods, such that the import ban has not strongly impacted US producers as a whole. In 2013, sales to Russia comprised less than 1% of total US agricultural exports, US$1.31 billion out of US$162 billion. Poultry was the main US agricultural export to Russia ($312 million of sales), followed by tree nuts (mainly almonds), soybeans, and live animals (US Department of Agriculture, Foreign Agricultural Service [USDA FAS, 2017a]).

However, the ban has probably affected US agriculture indirectly (as well as producers in many other countries), by depressing world prices for the banned products. Although world agricultural and food prices rose substantially from 2006 to 2011, since that year they have been steadily falling. From 2011 to 2016, the world food price index dropped by 30% (FAO, 2017, Food Price Index). The main reason for the price decline is that world agricultural production has grown by more than demand (see Shagam, 2015). The Russian import ban contributed to this imbalance by reducing world import demand for the proscribed products. 4

A mitigating point is that some major agricultural-exporting and non-banned countries such as Brazil and Argentina have to some degree shifted exports to Russia from other foreign markets (in pursuit of now higher Russian prices). For example, Brazilian pork exports to Russia in 2016 were 75% higher in volume terms than in 2013 (an additional 200,000 tons; Global Trade Atlas, n.d.). This allowed the banned countries to export more to the foreign markets to which Brazil and other non-banned countries were now exporting less. The overall effect of these trade adjustments was to dampen the downward effect on world agricultural prices from Russia’s import ban.

Effects on Russia’s macroeconomy

Russia’s economy was already frail in 2014, with forecasters predicting annual GDP growth of less than 1%. The reasons were weak overall demand, for goods covering three of the main categories of aggregate demand−consumption, investment, and exports (World Bank, 2013)−and deeper structural and institutional problems in the economy (Mau, 2016). The Western economic sanctions imposed against the country in 2014 put further pressure on the economy, in two main ways. The first was the virtual extinction of international investment in and lending to Russia, and the second was large-scale capital flight (US$150 billion in 2014, compared to 2013 GDP of US$2.1 trillion; Business Insider, 2015).

An even more serious economic setback was the massive drop in world oil prices that began in late 2014. At the start of that year, a barrel of Brent crude sold at US$110, but by late January 2015 the price had dropped to about US$50 (Bloomberg Markets, Energy, 2017). In 2013, about 70% of Russia’s export earnings came from energy products (mainly oil, oil products, and natural gas), such that the oil price drop severely reduced demand for the ruble. 5 These developments, combined with the capital flight, led to a major fall in value (depreciation) of the ruble vis-à-vis the US dollar and other major currencies. In January 2014, one dollar exchanged for 34 rubles (on average); by mid-December the exchange rate had dropped to 80 rubles per dollar, but then rebounded to around 60 rubles to the dollar by March 2015 (X-RATES, 2017).

To combat the ruble’s decline, the Russian Central Bank in December increased its lending rate from 10.5% to 17%, though in late January 2015 the Bank lowered the rate to 15% (Interfax, n.d.). By attracting funds to the Russian banking/financial system, the higher rate was intended to increase demand for the ruble and thereby stem its depreciation.

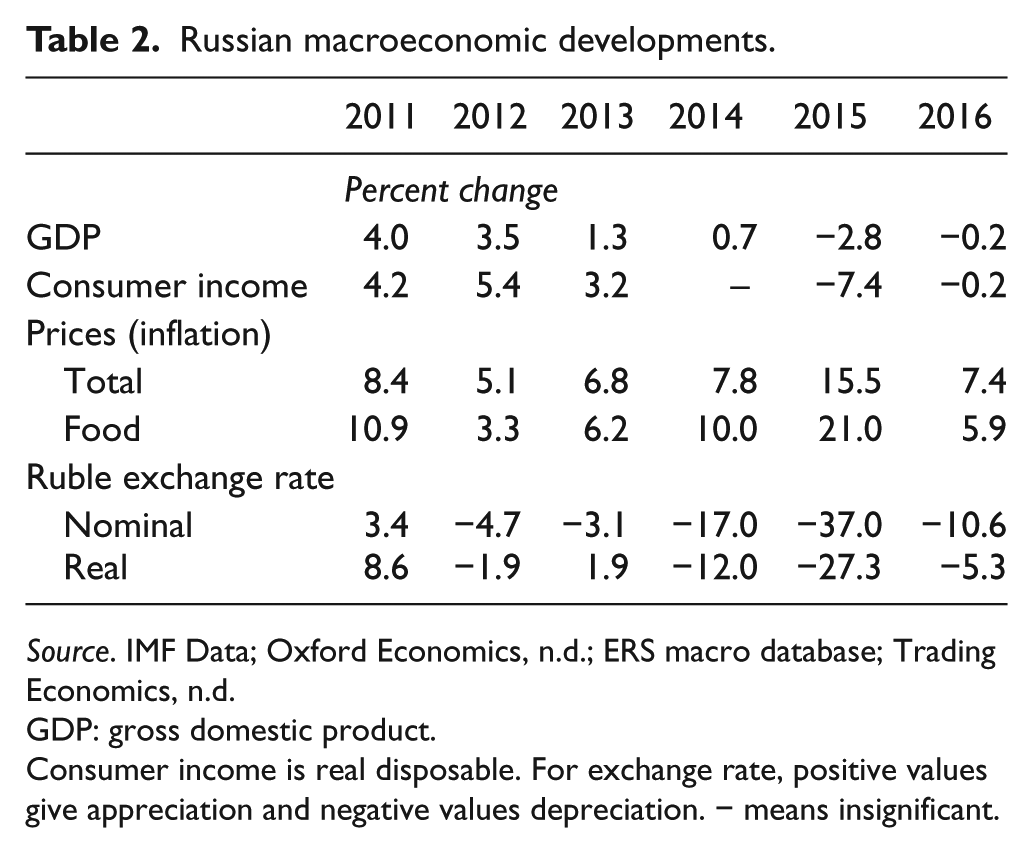

These developments spawned concurrent high inflation and recession for the Russian economy. The severe ruble depreciation generated inflation by raising domestic prices for all imports. The ensuing shift in demand from imports to domestically produced goods also increased prices. In 2013, Russian inflation was 7%; in 2015, it equaled 15%–16%, though it dropped back to 7% in 2016 (Table 2).

Russian macroeconomic developments.

Source. IMF Data; Oxford Economics, n.d.; ERS macro database; Trading Economics, n.d.

GDP: gross domestic product.

Consumer income is real disposable. For exchange rate, positive values give appreciation and negative values depreciation. − means insignificant.

Recession has been an even more serious problem. Capital flight and the drying-up of foreign lending and capital inflows decreased investment. The oil price decline cut the country’s export earnings, with negative effects for wealth, aggregate demand, and GDP. The interest rate increase by the Central Bank to prop up the ruble in December 2014 further dampened investment, demand, and GDP.

Russian GDP growth fell from 1.3% in 2013 to 0.7% in 2014, and GDP declined in 2015 and 2016 by 2.8% and 0.2%, respectively (Table 2). Consumer income dropped along with GDP, declining from 2013 to 2016 by almost 8%. The official unemployment rate, however, has changed little during the crisis years, moving from 5.5% in 2013 to 5.9% in 2015, and then dropping back to 5.5% in 2016 (The Telegraph, by Bloomberg, 2015). One reason is that the Russian federal government, as well as regional and local governments, are among the country’s largest employers, and they have followed the policy of retaining personnel while letting their wages and salaries fall (either in nominal terms, or in real terms because of inflation). The state has also made it clear to the private sector that it should follow the same policy with its workers. The consequences are that the working population has not experienced significant layoffs, but at the expense of falling wages, salaries, and incomes. Another effect is that the Russian economy is currently suffering from much underemployment, in that many officially employed people are underutilized or in effect working only part-time.

Table 2 shows that the most adverse macroeconomic effects of Russia’s crisis hit in 2015, with inflation and the fall in GDP being substantially greater than in 2016. The forecasts for Russian GDP growth for 2017 from the IMF is a rise of 1.4%, with inflation at 4.5% (IMF, 2017). Although such numbers imply some recovery from the crisis, they also suggest that the Russian macroeconomy in 2017 will remain frail.

A key factor in determining the length and severity of Russia’s economic crisis is the world price for oil. A rise in the oil price would increase Russia’s export earnings, and thereby raise the country’s GDP, wealth, and consumer income. Given that about half the revenue of the Russian federal government comes from taxing energy exports, the government could use the additional funds from an oil price rise to increase government spending, including on social welfare and other income support programs. According to the IMF, world oil prices fell in 2015 and 2016 by 47 and 16%, respectively. However, the IMF (2017) predicts that some price recovery will occur in 2017 and 2018 with anticipated price rises of 20% and 3.6%, respectively, which is consistent with projected rising Russian GDP in those years.

Just as the fall in the world oil price in late 2014 caused the ruble to depreciate substantially, the ruble’s exchange rate has fluctuated since then in response to movement in oil prices. The exchange rate recovered somewhat from 80 to the US dollar in December 2014 to around 60 in March 2015, but was back up to 85 rubles in February 2016, and then down to 56 in May 2017 (X-RATES, 2017). According to the information in Table 2, from 2013 to 2016 the ruble depreciated (in nominal terms) against the dollar by 53%. 6

Effects on Russian food consumers

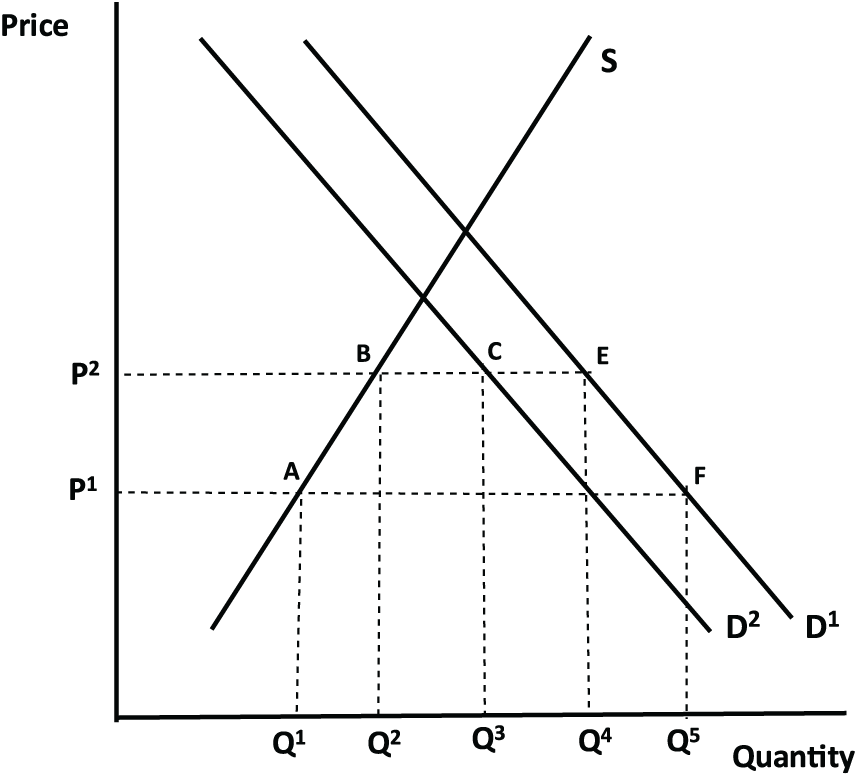

Figure 5 shows how the crisis has affected the market for an imported food product that was subject to the ban, such as meat, covering purchases/consumption, production, and imports. D1 is domestic demand for the good before the crisis and S domestic supply. P1 is the pre-crisis border and domestic prices, such that the pre-crisis volumes of the good domestically purchased and consumed, produced, and imported equal Q5, Q1, and Q5–Q1, respectively.

The crisis’ effects on Russian meat markets.

The economic crisis, including the agricultural import ban, has impacted Russian food consumers by reducing their income and food availability, and raising food prices. We mentioned earlier that the crisis lowered Russian consumer income from 2013 to 2016 by almost 8%. In Figure 5, the income decline shifts the demand curve for the good to the left to D2. The isolated effect (i.e., assuming no other market changes) is that consumption of the good falls from Q5 to Q4. 7

The import ban and ruble depreciation during the crisis have both worked to raise the domestic prices of the affected goods. The ban has done so by reducing import availability, and ruble depreciation made imports more expensive in ruble terms, which in turn drove up prices for domestically produced substitutes. In Figure 5, these effects raise the domestic price to P2, such that the volume of the good domestically purchased and consumed falls further to Q3. The total impact of the crisis on consumption is a decrease of Q5–Q3.

Our approach in analyzing the crisis’ effects on Russian food markets with the use of Figure 5 does not break out and identify the (isolated) market effect of each of the major components of the crisis. For example, both the Western economic sanctions (and ensuing drying up of foreign investment in Russia and capital flight) and the fall in the world oil price have contributed to the drop in Russian GDP, and thereby also consumer income, which shifts the demand curve in Figure 5 to the left. Likewise, both the agricultural import ban and ruble depreciation have increased domestic food prices, reflected in the figure in the price rise from P1 to P2. Correspondingly, our empirical assessment of the crisis’ effects on the consumption, production, and imports of foodstuffs using actual data also does not break out the isolated impacts of the main causes of the crisis, but rather examines the crisis’ apparent total effects. However, as shown by Figure 5, the sub-elements of the crisis have moved food markets in a similar and reinforcing direction.

In Figure 5, given that imports equal the difference between the volumes of the good domestically demanded and produced/supplied, the drop in consumption of Q5–Q3 also cuts into (reduces) imports of the good by an equal amount. We therefore can get an initial empirical gauge of how Russia’s crisis, and especially the import ban, has affected consumption by examining the drop in agricultural imports during the crisis years.

In 2013, Russia imported about 40% of the food it consumed (in value terms). For meat, the import share was about 25%, and for fruit almost 70% (FAO, 2014). Of Russia’s US$43 billion of total agricultural imports in 2013, US$23.5 billion were in the product categories affected by the ban, with the value of the banned products from the embargoed countries equaling US$8.3 billion (FAO, 2014).

Figures 2 and 3 show that Russian agricultural imports in value terms have fallen substantially during the crisis years. Measured in US dollars, total imports in 2016 were down by 42% compared to 2013. However, given that Figures 2 and 3 depict trade in value rather than volume terms (as discussed earlier), they overstate the drop in the magnitude of food availability from declining imports. Just as the rise in world agricultural and food prices from 2000 to 2011 (and especially beginning in 2007) increased the value of Russian agricultural imports by a greater degree than the volume of imports, the decline in prices in recent years reduced import values by a greater percentage than import volumes. As mentioned before, the world price index for food fell from 2011 to 2016 by 30%, while the price index for meat dropped from 2014 to 2016 by 21% (FAO, 2017, Food Price Index). 8

Figure 6 shows that in 2015 and 2016, Russian meat consumption in volume terms was 5 and 4% lower than in 2013, respectively. However, given that Russia imports mainly high-value products, the import ban has not lowered the availability of staple foodstuffs such as wheat and other grains, much less threatened the country’s overall food security. Yet, in addition to reducing food availability to some degree, the crisis and import ban have hurt Russian consumers by raising food prices. Food price inflation increased from 6% in 2013 to 10% and 21% in 2014 and 2015, respectively, though it then dropped down to 6% again in 2016 (Table 2). The inflation (overall as well as specifically for food) is a contributing factor to the rise in Russian poverty during the crisis, with the share of the population living below the national poverty line increasing from 10.8% in 2013 to 13.3% in 2015 (The World Bank, 2017, Poverty and Equity).

Russian meat consumption.

Effects on Russian agricultural production

In Figure 5, the rise in the domestic price for the imported good from ruble depreciation and the import ban from P1 to P2 should increase production from Q1 to Q2. Another crisis-related spur to production was the drop in world prices for oil (and kick-on effect for other energy products). Given that fuel and energy are used to produce livestock products (as well as crops, including the production of energy-intensive fertilizer), the oil price decline decreases agricultural input costs. This has the isolated effect of increasing the output of agricultural goods. However, the crisis-generated currency depreciation raises the domestic prices of energy products and all other tradable inputs used in production, such as the grains and oilseeds used to make animal feed. This has the isolated effect of decreasing the output of agricultural products. These two effects on agricultural inputs costs (the drop in world energy prices and ruble depreciation that raises Russian domestic prices for tradable inputs) have opposite effects on production, though they do not fully cancel each other out (which depends on the specific agricultural good).

Russia’s economic crisis has also affected agricultural production and markets through state subsidies to producers. The severe economic downturn reduced state revenue and put pressure on governmental budgets. Total Russian state spending on the agricultural sector in 2015 (from both the federal and regional governments) was about the same as in 2013 in nominal terms, but 16% lower in real (inflation-adjusted using the GDP deflator) terms (Russian Federal Service of State Statistics, n.d.-a; Oxford Economics, n.d.). Much of state support to agriculture takes the form of producer subsidies for specific inputs, and the spending cuts have the overall effect of raising production costs (if not directly, then by lowering productivity). 9

The drop in the real value of state support to agriculture in 2015 shows that the Russian government was unable to honor its pledge at the beginning of the crisis to increase subsidies to the sector. In 2016, the Russian government announced that federal support to agriculture would fall in nominal terms each year from 2016 to 2019, with the total decline in the 3 years being 18% (USDA, 2017a). Given that Russia will continue to have some inflation during that time, the inflation-adjusted drop in real terms will be even greater (an estimated 28%, using IMF (2017) inflation predictions as value deflators). 10

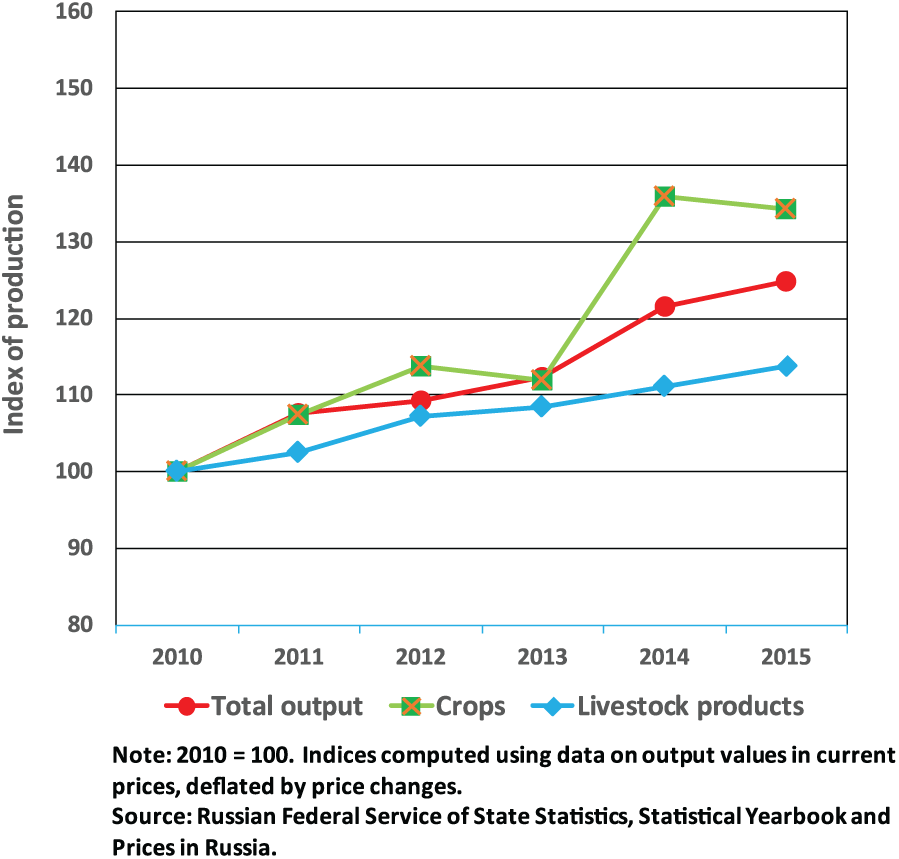

The fall in the real value of state support to agriculture during the crisis also has the isolated effect of reducing output. However, the rise in domestic output prices from ruble depreciation, which in turn stimulates more production as depicted in Figure 5, should dominate all the other (more indirect) ways just discussed by which crisis-related developments could impact agricultural output. 11 Figure 7 supports this argument. In 2014–2015, total Russian agricultural production grew at the higher average annual rate of 5.4%, compared to 3.9% during the previous 3 years.

Russian agricultural production.

However, the conclusion that Russia’s crisis has on net stimulated agricultural production requires some qualification. Although ruble depreciation should have the isolated effect of increasing output in both the livestock and crop sectors, the import ban should have favored the livestock sector more. Yet, over 2014–2015 livestock products grew at the average annual rate of 2.5%, a bit lower than their average annual growth of 2.7% during 2011–2013, and far below the growth rate for the crop sector of 9.6% (average annual) during 2014–2015. 12

Grain output rose from 2011–2013 to 2014–2016 by 28%, to 104 mmt (Table 1). O. Liefert et al. (2013) and W. Liefert and Liefert (2017) examine why the output of Russian crops, and especially grain, has grown substantially in recent years (as also reflected in Figure 1 in the rise in Russian grain exports). Ruble depreciation that increased domestic prices is one likely reason, though another is favorable weather during 2014–2016.

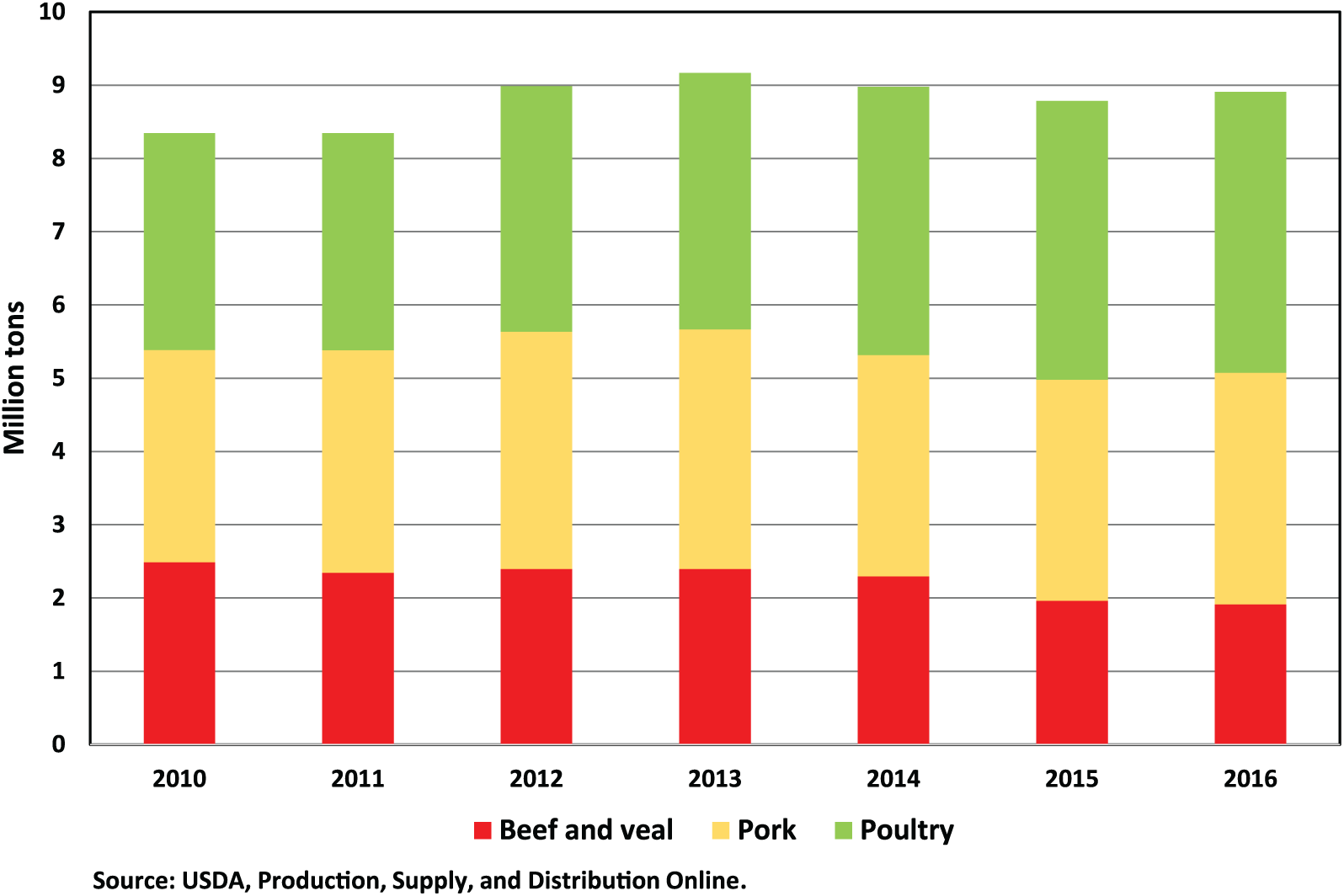

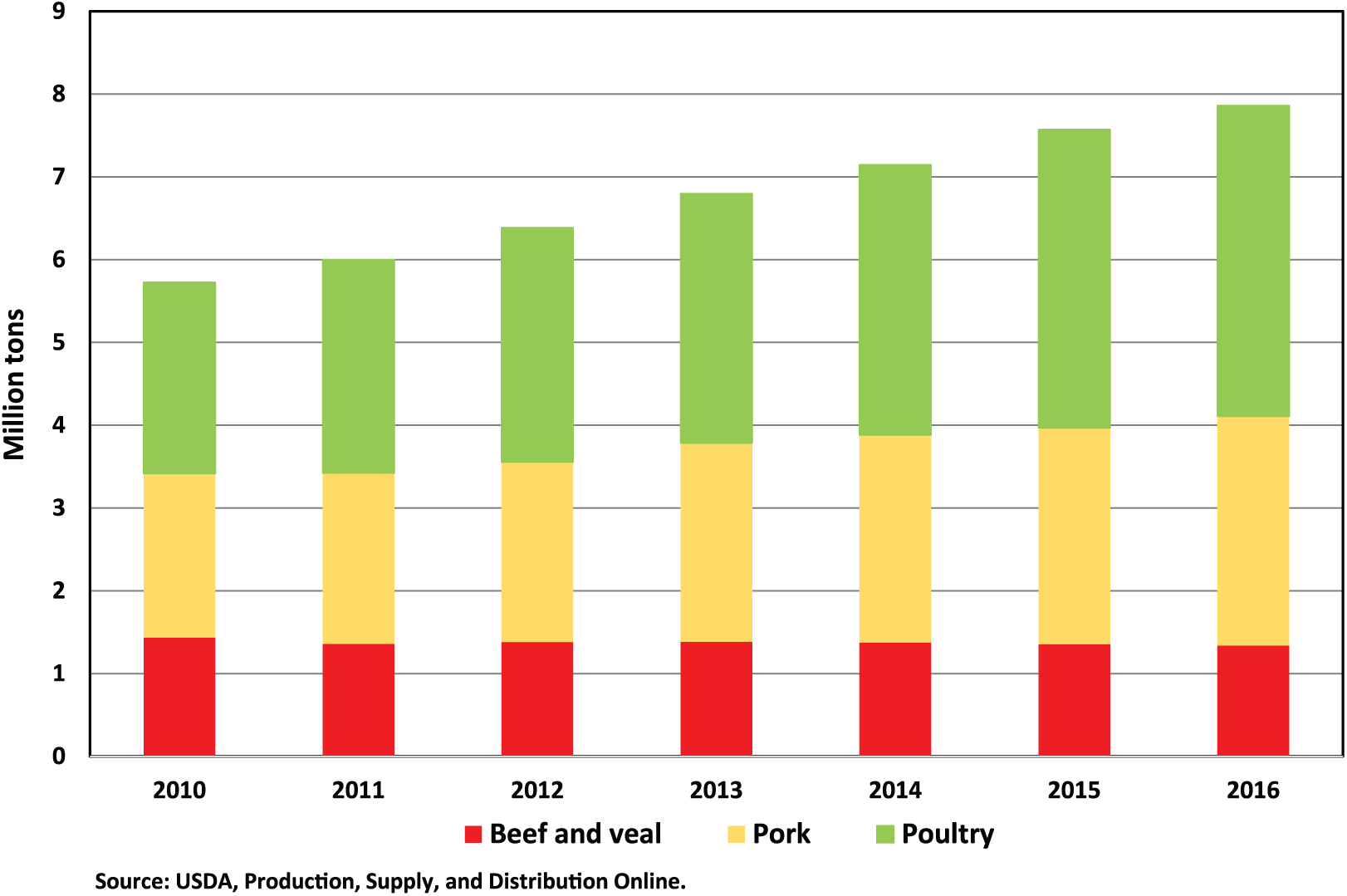

Figure 8 shows that Russian meat production rose during 2014–2016, but again at an average annual rate (5.0%) lower than during the pre-crisis years of 2011–2013 (5.9%), as well as during the earlier 10-year period of 2004–2013 (6.0%). One can therefore conclude that although the production of Russian meat and other livestock products has increased during the crisis years in a way consistent with expectations, the crisis has not moved production growth above its pre-crisis trend. This might reflect the difficulty of substantially raising the trend growth rate of meat and other livestock products in the short run even under favorable market conditions, if doing so requires the major investments and accompanying technological changes that can generate growth only in the longer term.

Russian meat production.

However, in the longer run, the Russian agricultural and food economy is expected to suffer from the crisis-driven decline in investment, resulting from economic sanctions, capital flight, and higher interest rates, as well as the drop-off in Western technology transfer. In 2015, capital investment in Russian agriculture fell by 4% (Russian Federal Service of State Statistics, n.d.-a). Foreign direct investment (FDI) in the entire Russian economy (which is tied to technology transfer) dropped from US$69 billion in 2014 to US$22 and US$7 billion in 2014 and 2015, respectively, though then jumped up to US$33 billion in 2016 (Oxford Economics, n.d.). The Russian government and agricultural establishment have made the technological upgrading of agriculture a priority, a main part of the program being the importation of higher quality seeds, machinery, and live animals (Interfax, n.d.). Reducing the inflow of these valuable inputs, as well as weakening the connection to Western technology, should also have long-term negative consequences for Russian agriculture. Gurvich and Prilepskiy (2015) and Golikova and Kuznetsov (2017) argue that the crisis’ dampening of investment and innovation will cause long-term harm to the Russian economy.

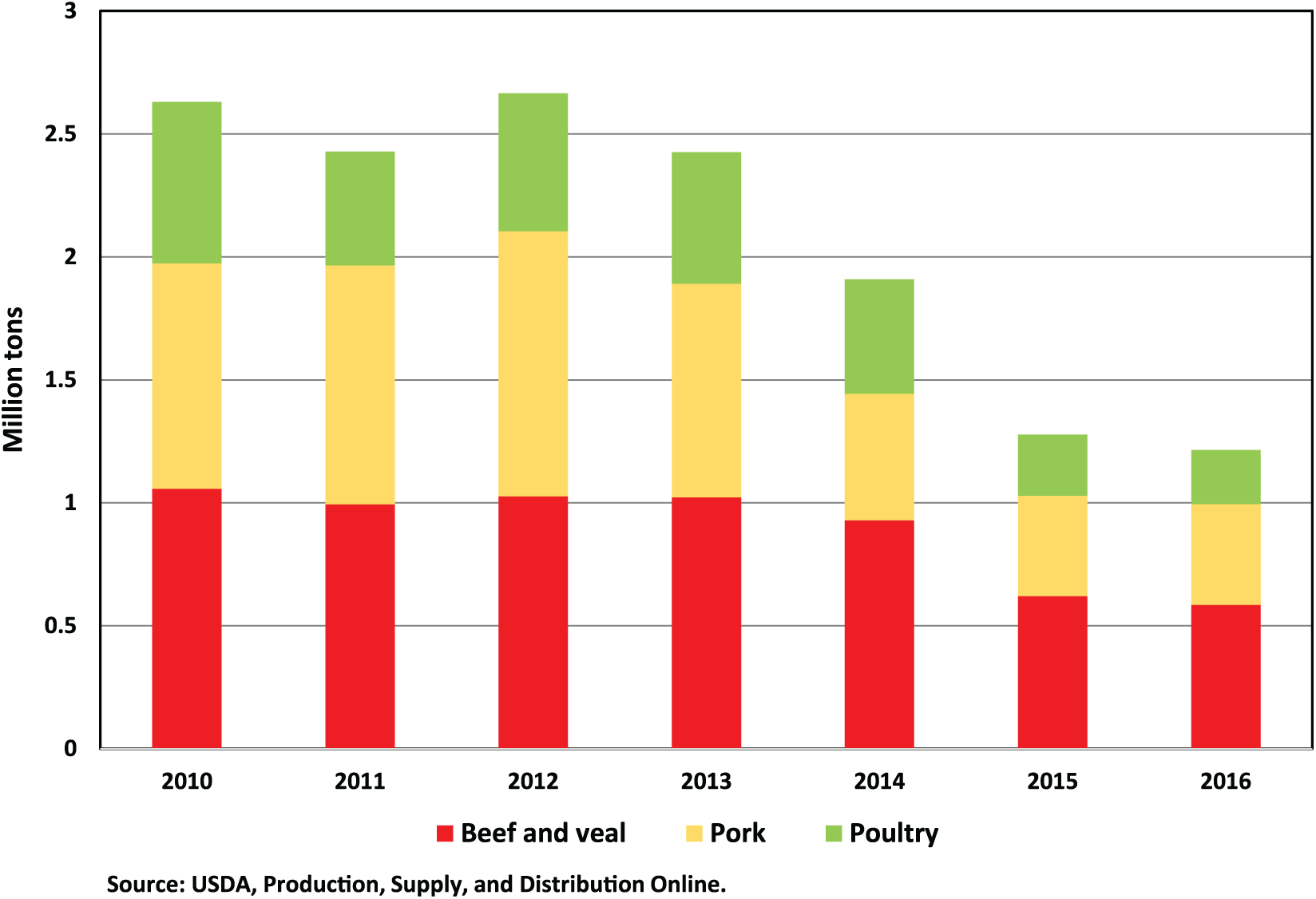

The rise in Russian meat production during the crisis years and drop in domestic consumption have resulted in a major decrease in meat imports (Figure 9), and explain why the decline in imports has exceeded that in consumption. Russian meat imports (net in volume terms) fell from 2.5 mmt during 2011–2013 (average annual) to 1.3 mmt during 2014–2016 (Table 1). The crisis has strengthened the state goals of import substitution and food self-sufficiency, especially in the meat sector. Imports of meat as a share of national consumption dropped from 26% in 2013 to 14% in 2016 (using the information in Figures 6 and 9). Russia’s share in total world meat imports (beef, pork, and poultry broilers) declined from 16% during 2006–2010 to 6% during 2014–2016 (USDA PSD). 13

Russian meat imports.

Ruble depreciation has also stimulated Russian agricultural exports by enhancing their price competitiveness on world markets. Figure 4 shows that from 2013 to 2016, the value of Russian agricultural exports (in US dollars) rose by 5%. However, given that world agricultural and food prices dropped during these years, the figure understates the rise in exports in volume terms. This is especially so for grain, the (net) export of which increased from 22 mmt during 2011–2013 (average annual) to 34 mmt during 2014–2016 (Table 1). Russia is in particular a big wheat exporter, and over these two periods its share in world wheat exports rose from 11% to 15% (USDA PSD).

This growth in grain exports notwithstanding, the crisis and import ban have disrupted the internal flow and export of grain. To counter the rise in domestic prices for bread and animal feed (and thereby assist both food consumers and the livestock sector), the Russian government has taken various steps to restrict grain outflows. These measures have included controls on grain exports, including sanitary measures in issuing export licenses, limits on the rail transport of grain to ports, and in February 2015 a grain export tax. However, the export tax was abolished in September 2016 (Interfax, n.d.).

Projections for Russia’s post-crisis meat production and trade

Given that Russia has been a major meat importer during the past two decades (and especially before the current crisis), and that meat was a main product group included in the import ban, we next examine how the Russian meat sector could progress once the country comes out of its current economic and geopolitical crisis. Specifically, we present the USDA projections in 2026 for Russian meat production and trade, assuming that its current economic crisis and agricultural import ban have ended (USDA, 2017b).

The forecasting model we use for Russian agriculture was developed by the Economic Research Service of the US Dept. of Agriculture, and is part of the agency’s model for world agriculture. The model is dynamic and partial equilibrium in nature and generates annual volumes of production, consumption, and trade for specific commodities. The modeling framework consists of supply and demand equations for products that use synthetic (rather than estimated) own and cross-price elasticities.

The model requires assumptions for key macroeconomic variables, which for our purposes are as follows: (1) that Russian GDP grows each year out to 2026, but never by more than 2%, and at an average rate of 1.6%, and (2) that the Russian ruble appreciates in real terms by 2.5% a year on average. 14 The ruble appreciation in real terms corrects for the substantial ruble depreciation during the crisis years, and occurs specifically because Russian price inflation over the period is not offset by ruble depreciation in nominal terms. We present not only the official USDA projections for Russian meat production and trade to 2026 (called the base projections), but also projections based on different assumptions concerning the macro variables of GDP growth and change in the ruble exchange rate (discussed later).

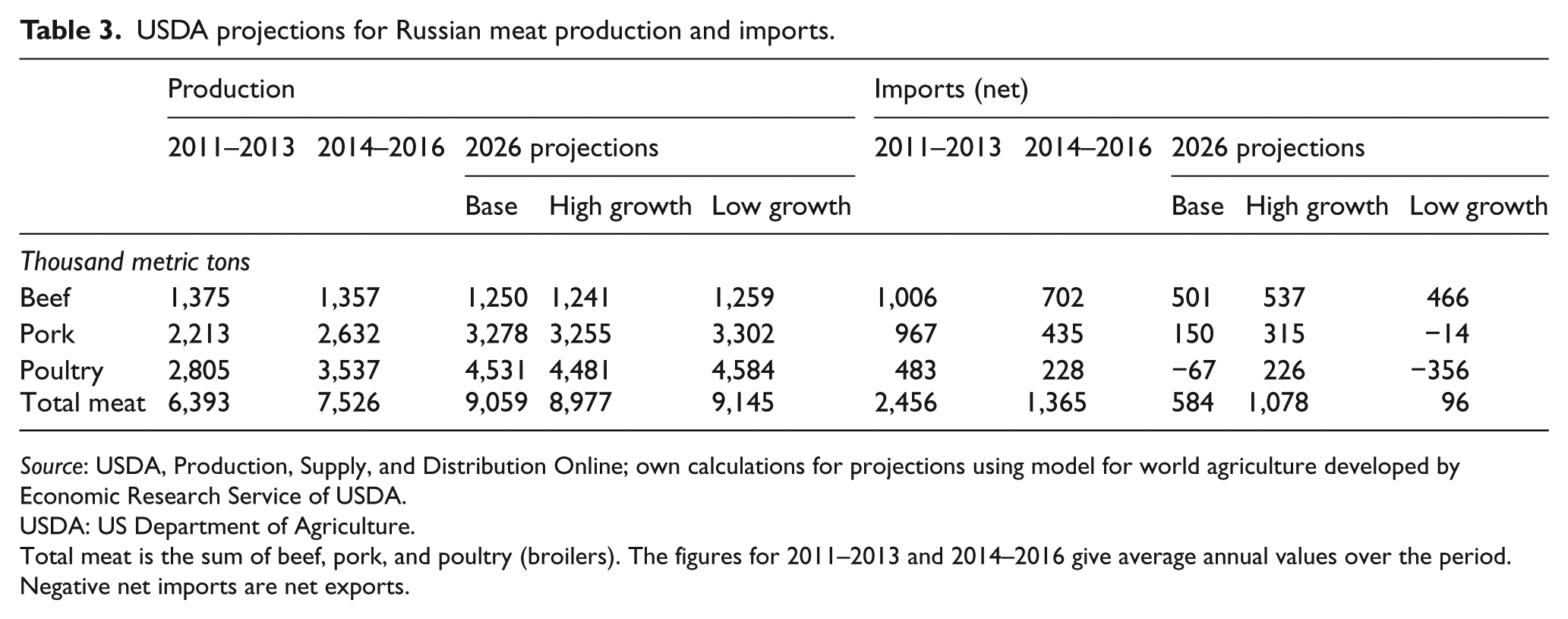

In Table 3, the “base” column under the 2026 projections for production gives the official USDA projections for Russian meat output in 2026. In that year, projected total meat production of 9.1 mmt is 20% higher than average annual meat output during the crisis years of 2014–2016. Although beef output continues to slide, pork and poultry production rise by 25% and 28%, respectively, over these periods. Ruble appreciation in real terms over the projection period has the isolated effect of reducing output. The currency appreciation initially reduces the ruble prices of imported goods vis-à-vis domestic output, and domestic producer prices fall to remain price competitive. However, that negative output effect notwithstanding, meat production increases because of continued long-term improvements and productivity growth in the Russian livestock sector, a key development being the adoption of modern mass production techniques, first for the poultry industry and then pork (see Prikhodko & Davleyev, 2014). 15

USDA projections for Russian meat production and imports.

Source: USDA, Production, Supply, and Distribution Online; own calculations for projections using model for world agriculture developed by Economic Research Service of USDA.

USDA: US Department of Agriculture.

Total meat is the sum of beef, pork, and poultry (broilers). The figures for 2011–2013 and 2014–2016 give average annual values over the period. Negative net imports are net exports.

Russian (net) meat imports are projected to fall from 2014–2016 (average annual value) to 2026 by 57%, to 584,000 metric tons (Table 3, see “base” column under the 2026 projections for imports). Net imports of beef and pork drop to 500,000 and 150,000 tons, respectively, while Russia becomes a net exporter of poultry of 67,000 tons. Resumed GDP growth and real appreciation of the ruble both work to increase meat imports. The rise in consumer income that accompanies economic growth increases demand for meat, some of which is met by more imports, while ruble appreciation makes imports more price competitive vis-à-vis competing domestic output. However, the large production response dominates these effects, such that imports drop. This meat import projection indicates that although Russia’s current crisis generated a large short run fall in meat imports, it simply strengthened a long-term decline.

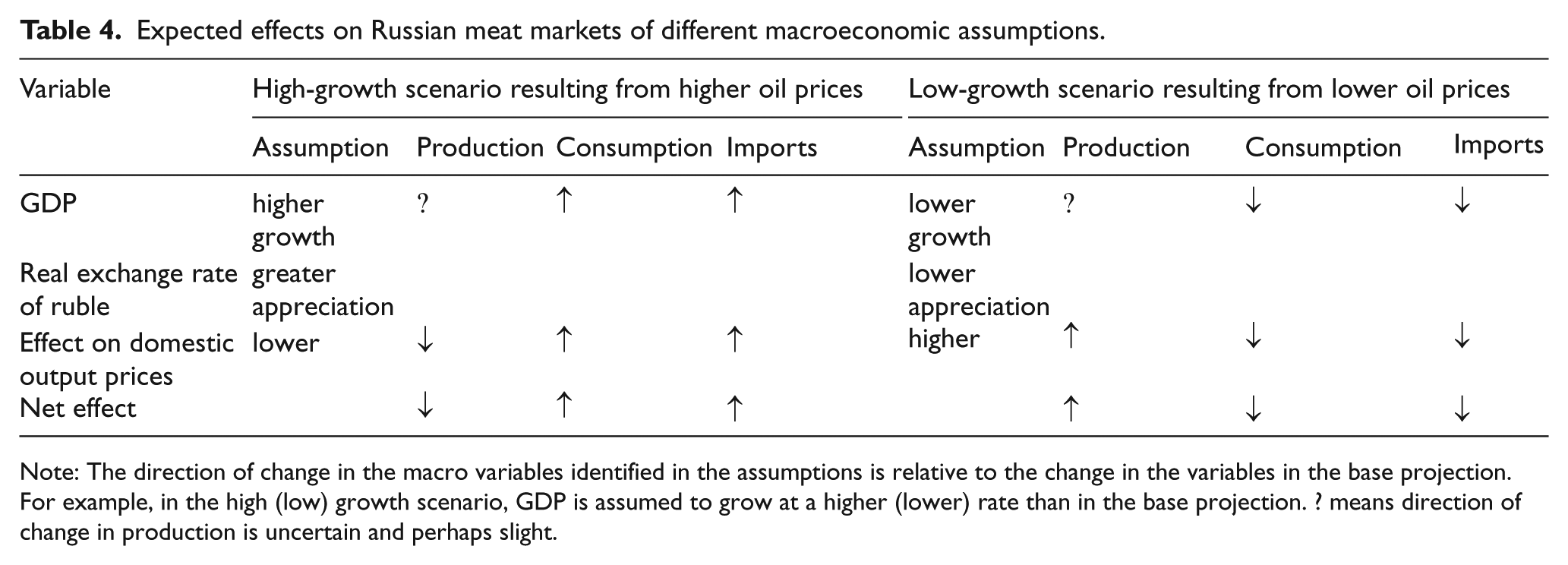

We next present projections based on different macroeconomic assumptions for Russia’s future. In the high growth scenario, we assume that in each year out to 2026: (1) Russian GDP growth is 50% higher than in the base scenario and (2) the real appreciation of the ruble is 50% greater than in the base scenario. The specific assumptions in this scenario are based on the more general assumption that world oil and energy prices are higher compared to the base scenario. Russia is a major energy and oil exporter, such that higher oil prices would increase GDP and national wealth and the ruble would appreciate further. The latter would occur because with higher oil prices, the amount of foreign currency earned from a given volume of oil exports, and then to be exchanged for (converted into) rubles, would be greater. This scenario also assumes that the current geopolitical tension between Russia and the West has completely ended.

We can use Table 4 to examine the expected effects on the projections for Russian meat production and imports in the high- and low-growth scenarios. In the high growth scenario, the information given in the “Assumption” column of higher GDP growth, greater real appreciation of the ruble, and ensuing lower domestic output prices, are vis-à-vis the base scenario. Lower domestic prices compared to the base scenario should reduce production relative to the base scenario, and the production projection for the high growth scenario in Table 3 supports that expectation. Although projected 2026 meat production of 9.0 mmt is 19% higher compared to the average annual volume during 2014–2016, the figure is 1% lower than projected meat output in the base scenario.

Expected effects on Russian meat markets of different macroeconomic assumptions.

Note: The direction of change in the macro variables identified in the assumptions is relative to the change in the variables in the base projection. For example, in the high (low) growth scenario, GDP is assumed to grow at a higher (lower) rate than in the base projection. ? means direction of change in production is uncertain and perhaps slight.

However, the difference in projected meat output between the base and high growth scenarios is small (for all three meats). This is mainly because the negative output effect from lower meat prices that results from greater currency appreciation is offset in part by the positive output effect resulting from lower prices for tradable inputs used in meat production, such as energy and feed. 16

In Table 4, both higher GDP growth and greater real appreciation of the ruble (compared to the base) are expected to increase consumer demand for meat (again relative to the base). In the case of greater ruble appreciation, this happens because the enhanced appreciation lowers domestic meat prices even more. Given that much of Russian meat consumption is supplied by imports, the augmented meat consumption should generate higher imports (compared to the base). The meat import projection in Table 3 of 1.08 mmt is 85% higher compared to the base scenario, though 21% lower than the average annual volume during 2014–2016.

Projected Russian meat imports in 2026 of over a million tons might nonetheless seem high, given the current determination of the Russian government to reduce such imports. The USDA forecasting model is driven by long-run changes in economic fundamentals, such as growth in GDP, consumer income, and farm productivity, and does not make assumptions about long-term policy developments. This is another reason why the high growth scenario generates upper bound projections of meat imports.

In the low growth scenario, we assume that in each year out to 2026: (1) Russian GDP growth is 50% lower than in the base scenario and (2) the real appreciation of the ruble is 50% lower than in the base scenario. In this scenario, world oil and energy prices are assumed to be lower than in the base scenario. This scenario could also reflect other features of the current crisis continuing into the future, such as the geopolitical conflict with the West, which would also work to stunt both future real appreciation of the ruble and GDP growth.

The main expected effect of these new assumptions for meat production is that the higher prices resulting from less ruble appreciation (compared to the base scenario) should generate higher output (also compared to the base; Table 4). In Table 3 in the low growth scenario, projected total meat production in 2026 is now 9.15 mmt—22% higher than the average annual volume in 2014–2016, as well as 1% above the base output projection. Recall again, though, that this positive output effect is mitigated by the negative effect on production from the higher input prices in this scenario compared to the base scenario. This helps explain why the 2026 projected meat output is only slightly higher than the projected volume in the base scenario.

Lower GDP growth and less ruble appreciation in this scenario (compared to the base) are now expected to result in less growth in consumer meat demand and consumption, and thereby lower imports (compared to the base; Table 4). The meat import projections in Table 3 for the low growth scenario are again consistent with this expected import effect. Total meat imports drop from 2014–2016 (average annual) to 2026 by 93% to 96,000 tons, and are only 16% of the volume in the base scenario. Beef imports are not as strongly affected by these new assumptions and remain fairly high at 466,000 tons. However, the trade effect is so great for poultry that Russia becomes a nontrivial net poultry exporter of 356,000 tons, and also a net exporter of pork (14,000 tons).

This modeling exercise is based on the assumption that Russia largely recovers from its current economic crisis, and the high- and low-growth scenarios are driven by differing assumptions for the future values of the key macroeconomic variables of Russia’s GDP growth and the real exchange rate of the ruble. However, the development of Russia’s livestock subsector (and specifically production and exports), and its agriculture in general, will also depend strongly on progress and changes originating within the sector itself. As Gokhberg, Kuzminov, Chulok, and Thurner (2017) and Kuzminov, Gokhberg, Thurner, and Khabirova (2018) show, although many problems and challenges remain in Russian agriculture, productivity-enhancing investment and technological change are occurring, and should continue. For example, these specialists mention that between 2010 and 2015, investment in machinery and equipment grew by 120% in real terms. The anticipated future progress is reflected in our model, specifically in the values chosen for productivity measures within the livestock sector, such as output per animal and feed requirements per ton of meat produced.

Conclusion

Major macroeconomic effects of Russia’s current geopolitical and economic crises are severe depreciation of the ruble against the US dollar and other major currencies, high inflation, and serious recession, including declines in GDP and consumer income. Before the crisis hit in 2014, Russia was a much larger importer of agricultural products than exporter. The crisis, which includes the ban on major agricultural imports (such as meat and other livestock goods) from the United States, EU, and other Western countries, has reduced Russia’s agricultural imports substantially. Total Russian agricultural imports dropped from US$43 billion in 2013 to US$25 billion in 2016.

The crisis has hurt Russian consumers mainly by generating inflation, especially for food. The crisis raised total price inflation from 7% in 2013 to 16% in 2015, and inflation for food from 6% to 21%. However, given that Russia imports mainly high-value products, such as meat, fruit, and vegetables, the import ban has not reduced the availability of staple foodstuffs such as wheat and other grains, nor has it threatened the country’s overall food security.

Just as the crisis (especially the import ban and ruble depreciation) has hurt food consumers, it has helped producers. Total agricultural production in 2015 was 11% higher than in 2013, and livestock product output was greater by 5%. However, the average annual growth rate for total livestock production in 2014–2015, and for meat (beef, pork, and poultry broilers) output in 2014–2016, was lower than the corresponding rate during the pre-crisis years of 2011–2013. This shows the difficulty of raising the long-term growth rate within the livestock sector, which will be hurt by the crises’ longer term effects from the drop in investment (including foreign direct) and technology transfer from the West.

The crisis reinforced a longer term drop in Russian meat imports, which peaked in 2008 at 3.5 million tons, and more generally strengthened the country’s move, supported by state policy, toward agricultural import substitution and self-sufficiency. Projections from USDA’s long-term modeling system for world agriculture indicate that, even if Russia completely comes out of its current crisis, meat imports will continue to fall. Net meat imports in 2026 are projected at 0.58 million tons, a 57% drop from the average annual level during 2014–2016 of 1.37 million tons. Using more optimistic assumptions about Russia’s future macroeconomy (higher world oil prices and domestic GDP growth and a stronger ruble), Russian net meat imports in 2026 are projected at 1.08 million tons, while more pessimistic macro assumptions generate a 2026 net meat import projection of only 96,000 tons. The more pessimistic scenario rests on assumed lower world oil prices and Russian GDP growth and a weaker ruble, and thereby has features of the current economic crisis lingering into the future.

Footnotes

Acknowledgements

The authors thank Cheryl Christensen, Joseph Cooper, Suzanne Thornsbury, Steven Zahniser, and an anonymous referee for helpful comments. The findings and conclusions in this preliminary publication have not been formally disseminated by the US Department of Agriculture and should not be construed to represent any agency determination or policy.

Authors’ Note

The work in this article is original and unpublished, and is not being considered for publication elsewhere. All the authors are employed by the Economic Research Service, the fully funded governmental agency of the US Department of Agriculture, and we have no conflicts of interest to disclose.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This research was supported by the intramural research program of the US Department of Agriculture, Economic Research Service.